22 Still thinking about shopping like a billionaire? Maybe not at these prices 27 Hundreds dead; millions hungry: KP’s food is buried under boulders and Punjab won’t share

Sluggish growth, widening losses at Quice

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Can Pakistan Electrify 36 Million Vehicles Before It’s Too Late?

By Ahtasam Ahmad

Pakistan stands at a critical juncture in its transportation future. With 36 million vehicles consuming 79% of the nation’s oil imports while contributing 60 million tons of CO2 emissions annually, the country faces a transportation crisis that threatens both its economic stability and environmental health.

The New Energy Vehicle Policy 202530, launched by the Ministry of Industries and Production, represents Pakistan’s latest attempt to address this challenge through an ambitious goal: transforming 30% of all new vehicle sales to electric by 2030. The policy

comes at a time when Pakistan’s power grid operates at just 50-56% capacity, creating a possible avenue to productively utilize surplus electricity while reducing dependence on costly oil imports that reached $16 billion in 2024. Yet the question remains whether a nation grappling with significant economic challenges can execute such a transformative agenda, and more critically, whether it can afford not to try.

Never been a better time

The numbers driving this urgency paint a stark picture of rapid growth outpacing sustainable development. Pakistan’s automobile sector has exploded from 9 million vehicles in 2010 to 36 million by 2023, an 11% compound annual

growth rate that has overwhelmed infrastructure development and contributed to the smog regularly blanketing cities like Lahore and Karachi. This growth trajectory, while indicating economic dynamism, has created what policymakers describe as a perfect storm of challenges and opportunities.

Pakistan’s current electric vehicle push builds on lessons from the failed 2019 National Electric Vehicles Policy, which set similarly ambitious targets but achieved minimal results. By 2021, only 567 electric vehicles were registered nationwide, far short of the policy’s goals. COVID-19 disrupted supply chains, but implementation challenges and poor coordination between federal and provincial authorities proved equally damaging.

The new policy acknowledges these failures directly, establishing a ministerial-level Steering Committee and introducing a revenue-neutral financing mechanism through levies on internal combustion engine vehicles. By June 2025, Pakistan had registered around 80,000 electric vehicles, representing significant improvement but still far from the scale needed to meet climate and economic objectives.

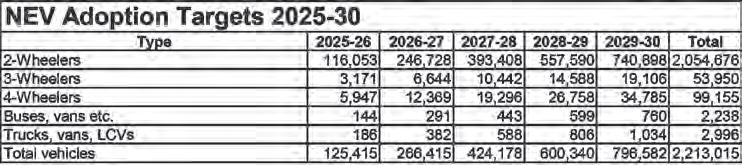

The 2030 vision outlined in the new policy is both specific and staggering: 2.21 million new energy vehicles across all categories supported by 3,000 charging stations nationwide. The breakdown reveals strategic focus on mass-market vehicles, with two-wheelers

EV infrastructure Economics

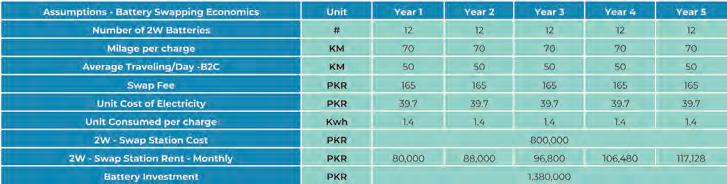

Our economic model of an EV charging station with 12 batteries performing a total of 40 daily swaps demonstrates strong viability. With Rs. 2.18 million in setup and battery costs, plus ongoing expenses of Rs. 80,000 monthly rent and maintenance at 2% of revenue, the government’s reduced Rs. 39.7 tariff significantly improves economics, enabling payback of around 3 years at a Rs. 165 per-charge fee.

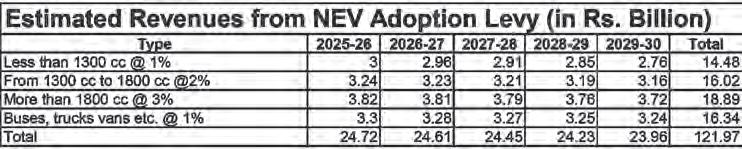

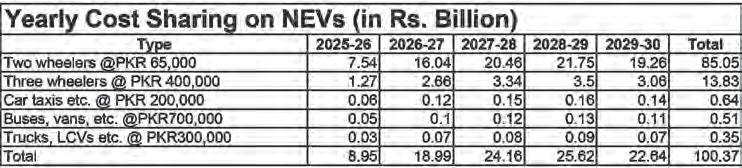

for commercial vehicles. This system is projected to generate Rs. 122 billion over the policy period, funding direct subsidies of Rs. 65,000 for two-wheelers, Rs. 400,000 for three-wheelers, and Rs. 15,000 per kilowatt-hour of battery capacity for larger vehicles. The subsidies will decrease gradually as economies of scale reduce costs, creating a self-sustaining transition mechanism where those continuing to purchase polluting vehicles fund the shift to clean alternatives.

promised with funding up to Rs. 2.25 billion, while oil marketing companies face mandates to install Level 3 charging infrastructure at 10% of their fuel stations in each province.

representing 2.05 million of the total target, three-wheelers accounting for 54,000 vehicles targeting commercial transport, four-wheelers comprising 99,000 vehicles primarily focusing on taxis and commercial use, and buses and commercial vehicles totaling 5,234 vehicles to transform public transport. The policy projects reducing 4.5 million tons of CO2 emissions, potentially earning $58.53 million in carbon credit revenues while achieving oil import savings of $0.95 billion by 2030.

To fund this transition, as indicated in the recent budget, rather than relying on subsidies that strain public finances, the government will impose graduated levies on internal combustion engine vehicle sales: 1% for vehicles under 1300cc, 2% for 1300-1800cc engines, 3% for engines above 1800cc, and 1%

Infrastructure development represents another critical component, with Pakistan’s currently embryonic charging network set for aggressive expansion. Within six months of policy approval, 40 Level 3 fast-charging stations will be installed along motorways and the N5 highway, enabling inter-city electric travel.

The broader plan envisions 1,050 Level 3 fast chargers capable of 80% charging in 2040 minutes, 750 Level 2 chargers suitable for workplaces and shopping centers, 600 Level 1 chargers for overnight home charging, and 600 battery swapping stations primarily for two and three-wheelers.

The government, in an attempt to improve viability, has offered a commercial charging tariff of Rs. 39.7 per kilowatt-hour designed to ensure adequate returns for private investors while maintaining affordability for consumers. For charging stations requiring additional support, a Viability Gap Funding scheme is

As of July 2025, 65 manufacturers have secured certificates for local electric two and three-wheeler production with combined annual capacity of 2 million vehicles, though much remains underutilized due to limited demand. The policy encourages development of Pakistan’s nascent battery industry, potentially transitioning from existing lead-acid battery manufacturing to lithium-ion assembly and full manufacturing, creating thousands of jobs in emerging green technologies.

Federal-provincial coordination represents a crucial challenge given the 2019 policy’s failures in this area. Vehicle registration, traffic management, and building codes fall under provincial jurisdiction, making cooperation essential for success. Industry sources report instances where provincial authorities have demanded prohibitive payments for vehicle registration, undermining private sector initiatives. The new policy addresses these issues through detailed National Action Plans for both federal and provincial entities, with federal responsibilities covering policy frameworks, standards, and financing mechanisms while provinces handle registration, infrastructure approvals, emergency response training, and local implementation. The policy encourages provinces to eliminate registration fees for electric vehicles, provide distinctive number plates, and update building codes to mandate charging infrastructure in new constructions.

Industry critique and strategic concerns

While the policy framework addresses many systemic issues, industry voices raise fundamental questions about strategic priorities and implementation ap-

proaches. A primary concern centers on what critics term the assembly versus manufacturing problem, where current incentive structures may favor companies importing Completely Knocked Down kits and assembling them domestically while claiming benefits intended to support genuine technology development. This approach risks creating low-value assembly operations rather than authentic manufacturing capabilities, potentially making Pakistan a dumping ground for imported kits rather than a competitive electric vehicle producing nation.

Industry experts also question the vehicle hierarchy approach, noting that much government attention and media focus has centered on electric cars despite serving less than 10% of Pakistani households. Critics argue that subsidizing one electric car could instead support multiple electric two-wheelers, each having far greater impact on emissions reduction and fuel savings. While the policy’s numerical targets suggest awareness of this dynamic, with two-wheelers representing the vast majority of planned vehicles, the disconnect may lie between policy design and public messaging, with car electrification receiving disproportionate attention relative to actual impact potential.

The infrastructure sequencing debate highlights another area of concern, with industry voices challenging the emphasis on expensive car charging networks in a low-income country. Alternative approaches prioritize battery swapping for high-utilization vehicles like delivery riders, gig workers, and commercial operators covering 90+ kilometers daily, arguing that riders using battery swaps could complete 30-50% more deliveries per day while boosting income and cutting downtime. The government policy includes battery swapping stations at 600 units by 2030, representing only 20% of total charging infrastructure, which critics suggest may be insufficient given market dynamics.

Financing gaps represent another critical challenge, particularly regarding the informal sector that could drive mass adoption. While the policy encourages banks to revise auto-finance limits and promote green financing, industry observers note that traditional banks have struggled to develop products suitable for informal sector workers who need vehicles to earn a living.

Current approaches involving rigid credit criteria, collateral demands, and lengthy

approval processes may work for formal sector buyers but fail to reach the demographic most likely to benefit from electric two-wheelers. Technical performance standards also face scrutiny, with many current electric two-wheelers described as inadequate moped-style scooters using low-powered motors and inferior batteries that offer poor range, long charging times, and short lifespans. These vehicles fail to replace the utility of 70cc motorcycles serving as family transport, leading to low satisfaction and poor adoption rates. The government’s planned standards and UN-compliant regulations could address quality concerns, but enforcement mechanisms and market-specific performance criteria remain undefined.

usage patterns including planning charging stops, waiting for completion, and managing range limitations. Pakistan’s automotive market has limited experience with these technologies, making consumer education critical for success. The policy faces implementation risks similar to previous efforts that struggled with bureaucratic delays, inter-agency coordination failures, and changing political priorities. Success requires sustained commitment across multiple government levels and ministries, a challenge that industry experience suggests may prove optimistic.

Implementation challenges and market realities

Beyond industry critiques, systemic challenges remain formidable. Pakistan’s power grid, despite excess capacity, suffers from reliability issues and transmission losses that could undermine consumer confidence in electric vehicles. Rolling blackouts and voltage fluctuations present real obstacles that both policy and industry acknowledge but have yet to fully address. The policy’s financing mechanism assumes consistent revenue from internal combustion engine vehicle sales and effective collection of proposed levies, but economic volatility or government changes could disrupt funding streams, particularly given Pakistan’s history of policy reversals during political transitions.

Consumer behavior presents additional hurdles, as electric vehicles require different

Early industry response has been cautiously optimistic, with existing automobile manufacturers recognizing that electric transition is globally inevitable and Pakistan’s policy provides a framework for market development. However, concerns persist about consumer acceptance, charging infrastructure reliability, and regulatory implementation speed. Battery manufacturers and charging infrastructure companies see significant opportunities in the policy’s guaranteed tariffs and viability gap funding, while traditional oil marketing companies face both disruption and transformation opportunities through mandatory charging infrastructure requirements at fuel stations.

However, success remains far from guaranteed given Pakistan’s significant economic challenges, implementation capacity constraints, and consumer behavior hurdles. The policy’s ambitious timelines require sustained political commitment and bureaucratic efficiency that have been inconsistent in previous reform efforts.

Whether Pakistan achieves its 2030 targets may matter less than establishing sustainable foundations for long-term electric mobility adoption that could position the country for global transition to sustainable transportation while addressing pressing domestic challenges in air quality, energy security, and economic development. The next five years will determine whether this represents genuine transformation or another ambitious plan falling short of promises, with stakes that could not be higher for a country facing climate change impacts, energy security challenges, and mounting economic pressures. n

The return of industrial policy

Pakistan is getting serious about industrialization. Or is it just more of the same?

By Ammar Rashid

Industrialization is back on the policy agenda in Pakistan. The government is about to announce a new national industrial policy aimed at ‘reshaping and reviving’ Pakistan’s long-stagnant industrial sector. This comes amid a slew of other policies approved or in development aimed at boosting industrial and export growth, including a new National Tariff Policy, a National Electric Vehicles Policy, a Textiles and Apparel policy, and a new Energy Wheeling policy among others, as well as the launch of the second phase of CPEC (which includes industrial development as a key priority).

Jaded observers of Pakistani policymaking can be forgiven for shrugging their shoulders at these develop-

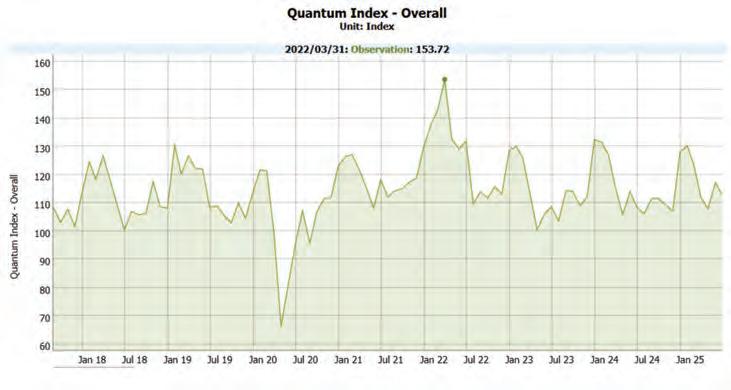

Figure 1 Quantum Index of Large-Scale Manufacturing (2018-present). Source: SBP EasyData portal

ments given the sordid history of past top-down reform attempts by successive governments that amounted to little beyond fanfare, boom-bust cycles and rapid backtracking on reform commitments at the slightest hint of sectional resistance. However, regardless of how one feels about the current government’s capabilities or legitimacy to design and implement industrial policy, it is hard to argue that this exercise is unnecessary.

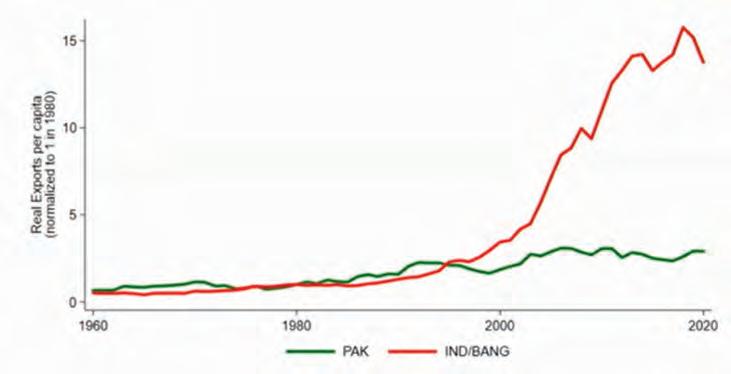

Pakistan has not had anything resembling a coherent industry policy for over three decades (unless one counts the voracious rent-seeking that takes place in FBR offices for various SROs and tax exemptions as ‘industrial policy’). In this time, industry’s share of GDP has fallen from 26% (in 1996) to between 10-15% today. Large Scale Manufacturing (LSM) has remained on a steady decline for years since its brief post-COVID recovery in early 2022. Investment has shrunk to around 13% of GDP. Credit to the private sector never really recovered from its 2007 peak and now hovers around 10% of GDP. In the meantime, regional competitors like India and Bangla-

Source: Atif Mian (2022)

desh have managed to create sizable industrial bases and increase their exports per capita to multiple times that of Pakistan, while our shrinking productive capacity and low export equilibrium perpetuates balance of payments crises, IMF dependence, rupee devaluation and devastating inflationary episodes.

From the government’s recent pronouncements, it appears that there has been some awakening to the need to address Pakistan’s crisis of industrial stagnation. However, from what has been revealed about the policy so far, questions remain about whether this effort will actually address the causes of Pakistan’s deindustrialization. While many of the proposed steps - particularly actions to reduce energy tariffs, taxes and import duties - are clearly needed, there are reasons to be concerned that the policy’s design and focus could perpetuate the harmful rent-seeking equilibrium that has long characterized state-capital relations in Pakistan without bringing about the required productivity and export benefits.

So what is in the policy exactly?

While the national industrial policy has not been officially announced at the time of writing, a draft in circulation provides some insight into its design and focus. Spearheaded by SAPM on Industries and Production Haroon Akhtar Khan, the policy has been formulated through eight committees (on tariffs, taxes, energy, regulations, investor confidence, credit, firm revival and land and infrastructure), comprised of representatives of government institutions - key among them being the Ministry of Industries and Production (MoIP), Ministry of Commerce (MoC), FBR and SECP - and industry associations (such as the Pakistan Business Council, APTMA and others). The thrust of the document reflects the composition of the committees that formulated it in that it reads like a negotiated settlement balancing industry demands

and FBR revenue needs.

In lieu of a detailed diagnosis of the industrial landscape, the policy briefly identifies the ‘key constraints’ to industrial growth: 1) macro-instability, 2) trade protections, 3) disproportionate tax incidence on industry, 4) ‘uncompetitive space’ (including cost of land and regulatory gaps), and 5) lack of investment (including due to lack of investment security and IP rights). To address these constraints, the policy aims to provide direction to ‘boost investment in the manufacturing sector’, ‘enhance investor confidence’ and ‘grow industrial exports’. It then lists out a wide-ranging laundry list of recommendations related to: reducing the cost of power; reducing taxes and tariffs on imported inputs; provision of viable land and infrastructure; enhancing technological skills and acquisition; reforming corporate income tax and super tax; strengthening investor protection; improving access to credit; enabling revival of sick units; intellectual property protection; regulatory streamlining; and building institutional capacity for industrial policy, among others.

However, as one reads through the document, it becomes clear that the main focus of the policy (the only recommendations for which any actionable steps are outlined) is on some key areas aimed at reducing the costs of business and incentivizing investment: tax measures, energy cost reductions, investor security, sick firm revival, tariff measures, SEZ’s and institutional strengthening.

Tax measures: The rationale for tax cuts is simple enough - the disproportionately high tax burden on the manufacturing sector (which accounts for only 13% of GDP but over 60% of total tax revenue) limits formalization, stifles cost competitiveness and limits the entry of newcomers, while also making FDI in the sector unattractive in comparison to the rest of South Asia. The main tax measures

Figure 2 Real exports per capita in Pakistan in comparison to Bangladesh/India.

proposed (subject to IMF approval as per FBR’s comments) are a reduction in corporate income tax from 29% to 26% over three years and gradual reduction and eventual abolition of the Super Tax (currently up to 10% of marginal income above Rs. 300m for multiple industries) over five years. In addition, the policy proposes a new Drawback of Local Taxes and Levies (DLTL) scheme by the Ministry of Commerce as an export incentive.

Energy cost reductions: While the policy does not offer a roadmap for energy cost reduction, the key steps proposed include the removal of the cross-subsidy from industrial tariffs and abolition of peak rates by the Power Division and removal of cross subsidy from industrial gas prices by the Petroleum Division. In addition, the document refers to the implementation of the new Energy Wheeling Policy, which allows industrial consumers to buy energy directly from captive power plants via a streamlined open access mechanism, with special rates just above the marginal cost for high-tech green field sectors such as EV, batteries, and data centers.

Investor protection measures: Investor protection measures are clearly a priority and are discussed in some detail. The policy recommends a host of proposals to eliminate ‘undue harassment’ of industries and the private sector, including amendments to the SECP Act 1997 for mandatory SECP approval prior to LEA action, empowering the PM to act to safeguard investments, simplification of audit and oversight procedures, and safeguards against arrests of company personnel by LEAs without prior regulator opinion. It also proposes legislative amendments to the Corporate Rehabilitation Act to develop a concrete legal regime for bankruptcy and insolvency to improve investors’ confidence about investment recovery and restructuring of firms in case of failure. An amendment is also proposed to the Protection of Economic Reforms Act (PERA 2016) to bar retrospective withdrawals of fiscal incentives (e.g., subsidies or tax breaks) where ‘investment steps have already been taken’ and prescribe a maximum limit of ten

years for retention of records by companies of relevance to those fiscal incentives.

Firm revival: A significant amount of space is devoted to firm revival or what the policy refers to as revival of ‘sick industrial units’ to reactivate idle capacity and create jobs and local value chains. The policy proposes the establishment of an SBP-led framework for the revival and debt resolution of ‘distressed industrial units’ (in manufacturing, agribusiness, logistics, energy and services) that enables banks to consider revival-linked credit schemes with principal and interest rate reductions and provision of fresh working capital, and corporate restructuring companies (CRCs) to acquire non-performing loans and oversee firm recovery. In addition, the policy proposes the establishment of a National Industrial Revival Commission (NIRC) to oversee the firm revival policy and provide monitoring, statistical and governance support.

Tariff reform: Perhaps the most potentially significant aspect of the government’s industrial reform effort is something that is not explicitly part of the industrial policy itselfthe new National Tariff Policy 2025-30, which aims to liberalize and rationalize import tariffs. While the industrial policy references and affirms the new Tariff policy, the latter was developed out of a parallel long-running tariff reform advocacy led by Pakistan’s former WTO rep, Dr Manzoor Ahmad, and economists like IGC Director Dr Ijaz Nabi among others.

Pakistan has long had a skewed tariff regime – with the region’s highest average tariffs and high import duty cascading - that has disincentivized an export orientation among domestic firms. High duties on intermediate and finished goods have both diminished the cost competitiveness of local producers faced with high input duties and created an incentive for local manufacturers to produce goods solely for domestic markets behind tariff walls.

The new tariff policy aims to address this problem through three key measures: a) a simplification of the tariff regime to four slabs

(0%, 5%, 10% and 15%), a gradual elimination of additional customs duty (ACD) and regulatory duties (RD) over five years, a reduction in customs duties (CD) to a maximum of 15% over five years, and a phasing out of the distortionary Fifth Schedule of exemptions over five years. The policy aims to route all future tariff change requests through a Tariff Policy Board, which could limit the discretionary abuse of SROs to serve special interests. Overall, the policy targets a reduction in Pakistan’s simple average tariff rate from the current 20% to 9.5% in five years.

If implemented as designed, this could have a significant impact. According to estimates by the Global Trade Analysis Project (GTAP), these tariff measures alone are projected to increase Pakistan’s exports by 10-14% and revenue by 6-7%, along with a host of other expected knock-on effects.

Access to credit: To address the longstanding issue of low credit to the private sector, the policy proposes increased utilization of the State Bank’s Export Finance Scheme (EFS), requirements for banks to justify loan refusals and consider lowering rates, lending incentives like reducing capital adequacy risk weighting for medium firms, issuance of sectoral bonds to provide a framework for longterm financing, reinsurance support for EXIM bank and improved access to digital gateways. However, no steps are outlined for carrying out any of these recommendations.

The policy does lay out some actionable taxation and regulatory measures for building Pakistan’s venture capital eco-system including: granting statutory pass-through status to licensed VC Funds (revoked by FBR in 2021); changes to the FE manual to address repatriation friction for VC equity at entry and exit points; and creating a ‘Fund of Funds’ to finance new Fund managers focused on various asset classes in Pakistan (along the lines of MSMEDA in Egypt and ISSF in Jordan).

Institutional capacity: The policy aims to enhance institutional capabilities for industrial governance, including through the establishment of a Support Cell and a Strategic Planning Cell at the MoiP to oversee industrial policy, SOE restructuring, privatization, and land titling issues, among others. Further, a government-backed guarantee facility has been proposed to institutionalize enforceable guarantees for industrial and infrastructure projects.

Land and infrastructure: The discussion of land and infrastructure provision in the policy is mostly centered on SEZs. Recommendations include the establishment of a ‘One-stop Service’ at SEZs that combines corporate registration, taxation, customs, visas, environmental regulations and energy with legally delegated autonomy of operations.

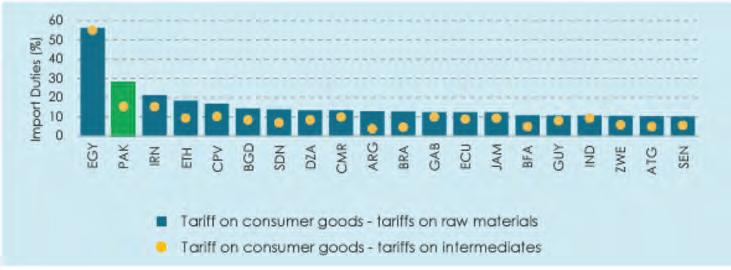

Figure 4 Import duty cascading - top 20 countries with the highest cascading.

Source: World Bank (2021)

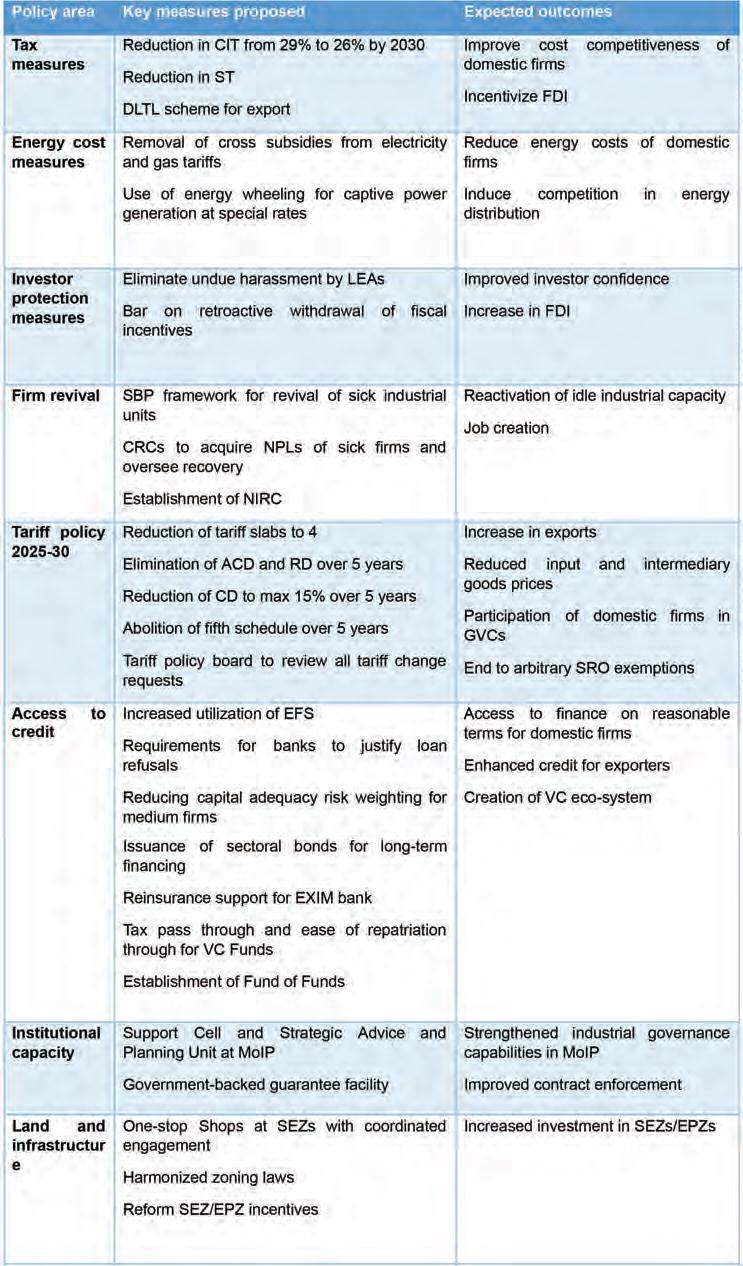

Table 1 Key priority areas and measures in National Industry Policy.

Source: Developed from the National Industrial Policy 2025, Government of Pakistan

The policy also recommends a national land bank and harmonization of zoning laws across cities but does not lay out any steps to achieve these outcomes.

Table 1 summarizes the key priority areas, actions and outcomes in the industrial policy. Other recommendations that are included in the policy but without any related

actions laid out include review of VAT and WH-Tax on imported inputs, enhancing technology acquisition, strengthening intellectual property rights protection, enhancing domestic certification capacity and policy coordination.

Problems of design

On their own, many of the proposals in the industrial policy are eminently reasonable and if appropriately implemented, could go some distance in improving cost competitiveness, investment and export orientation in the industrial sector. However, the policy at times reads more like a prescriptive wish list of parallel proposals rather than a robust evidence-based and sequenced planning framework for industrial revival.

To begin with, there is no attempt at a detailed diagnosis (or even citation of existing evidence) on the roots of Pakistan’s industrial crisis. For instance, the policy does not examine the failure of past policies of import substitution and export promotion to engender manufacturing growth. It does not discuss issues like structural trends in the post-94 financial system that hinder credit access, distortions in land policies that limit supply of affordable industrial land nor the vast gulf in female labor force participation that separates Pakistan from manufacturing success stories like Vietnam and Bangladesh.

The policy does not examine the current industrial structure of the country, in terms of its sectoral composition, clusters, evolving comparative advantages, sectoral economies of scale, or supply chain gaps (nor are any references made to ongoing sectoral policy processes on EVs, textiles and others). There is no attempt to understand the key technological and capability gaps that are keeping Pakistani industries stuck in a low-value primary and intermediary goods equilibrium and preventing them from moving up value chains. Some ongoing debates of obvious relevance to GVC integration and productive capacity, such as development of indigenous minerals processing capacity, do not find mention. There is also no attempt made to place the policy in the context of the seismic disruptions in international trade underway and how to navigate the challenges and explore new opportunities and markets for Pakistani manufacturers under the circumstances. The lack of any attention to these questions is reflected in the lack of any targeted sectoral interventions outlined in the policy.

It is also unclear how policy success will be measured - no modeling or feasibility is provided for any intervention, and no theory of change or framework is outlined for achievement of the policy objectives. No quantifiable

targets or measurable indicators have been established to measure overall policy success.

In many ways the incoherence of the policy design is reflective of the fragmented and clientelist way in which policymaking takes place in Pakistan. Rather than being an outcome of an autonomous and representative governing structure’s attempts to formulate strategic evidence-based interventions to achieve beneficial economic outcomes for society, the policy reads like an exercise in reducing the costs and risks of doing business of existing businesses and investors to boost their profitability while balancing against the government and IMF’s revenue needs. Institutions responsible for long-term economic planning (e.g., the Planning Commission), SOEs involved in strategic sectors like oil, gas and minerals or representatives of industrial labor appear to have not been involved in its development.

However necessary improving the cost competitiveness of and risk environment for businesses and investors (as the policy aims to do) might be, industrial policy can and must go beyond that in its design. It should address key structural and institutional barriers to Pakistan’s industrial growth and provide a clear, actionable and measurable long-term plan to overcome them. Most fundamental among them is the question of productivity.

The productivity elephant in the room

As Ricardo Hausmann and numerous other industrial economists have pointed out - industrial policy should not just be about improving firms’ profitability but improving productivity. For industrial economists like Mushtaq Khan, the very point of industry policy is to ‘support the development and adoption of technologies and capabilities that raise social productivity’. Industrial policies are required, he says, when ‘private contracting fails to organize potentially gainful investments that achieve these outcomes’. This is certainly the case for Pakistan. Pakistan’s crisis of productivity is at the core of its industrial dysfunction. Pakistani firms have the lowest productivity growth among regional competitors, with most firms not becoming more productive as they grow older unlike in other countries, impeding growth and technology adoption. The most marked decline in firm productivity in Pakistan over time (-7.5% between 2012 and 2020) has been for family-owned firms. Excessive reliance on family for senior managerial roles by such firms (also notoriously averse to public listings) and inefficient managerial and organizational practices in general have been found in research to be the key drivers of firm

productivity stagnation. A recent survey of innovation in Pakistani firms found that the largest productivity improvements came from reforms related to organizational and process innovation, consistent with results from around the world.

Yet the word productivity appears a total of two times in the industrial policy (once as an assumed outcome of reduction in super tax and once in reference to establishment of a ‘productivity fund’ which is not elaborated on in any section of the policy). The word innovation does not appear at all.

No strategy for industrialization can succeed without embedding productivity growth into its design. Successful industrial policies across the world have focused on enhancing productivity with a variety of instruments that incentivized technology adoption, capability upgradation, organizational and process innovation and learning-by-doing. Bangladesh’s experiences with partnerships between Bangladeshi and South Korean firms in the garments sector demonstrate how contracting for organizational capability and technology transfers can enable productivity growth in fiscally strained contexts.

At the policy level, this requires developing the ability to monitor and measure productivity growth across firms and sectors and linking entitlements and incentives to measurable improvements in productivity. It requires planning for productive and technological sovereignty, mapping gaps across priority sectors, enabling financing for firms seeking to enhance technology acquisition and capabilities and developing academia-industry linkages that drive applied innovation, learning and technological diffusion. In this process, new opportunities for productivity-enhancing technology transfers, such as Chinese invest-

ment in textile hubs and EVs under CPEC2.0, must be integrated into Pakistan’s industrial planning matrix.

Conditioning rents for industrial policy

Regardless of country context, a key feature of successful industrial policies around the world has been the ability of governments to condition subsidies (be it tariff protections, tax cuts or export incentives) on firm performance, exports and productivity. Pakistan has consistently failed to enforce conditions on subsidies offered to domestic forms, leading to rent capture that has stifled competitiveness and productivity.

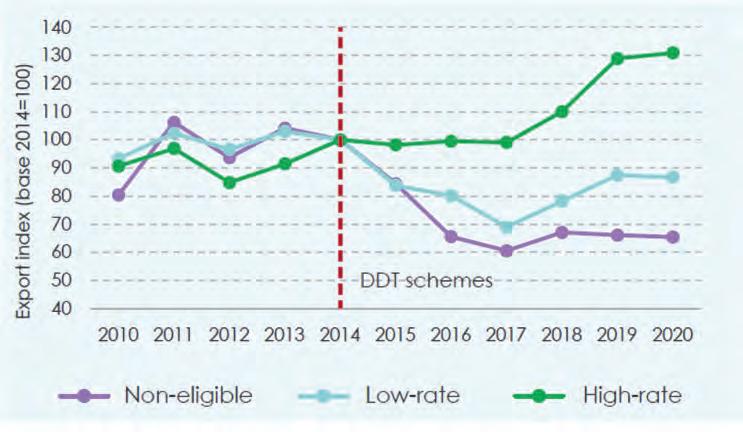

There is every reason to fear that the current industrial policy will end up repeating the same mistakes that have led to rent capture in the past. For one, the policy’s lack of any targets or measurable indicators of performance in response suggest that payoffs will be accrued to firms regardless of effort. Further, the policy doubles down on proposals of export subsidy programs like Drawback of Local Taxes and Levies (DLTL) without examining why such programs have failed to achieve improved export performance in the past. Studies have found that instruments like DLTL have had limited export impact and only benefited a small number of ‘insider’ firms by focusing high-rated duty drawbacks on the established products of those firms while discouraging diversification by driving concentration of capital allocation towards high-rated DLTL product categories with often lower global demand. Persisting with the same incentive structure without productivity and innovation conditions is likely to lead to similar outcomes.

Figure 6 Export growth by eligibility and rates of Drawback of Duties and Tariffs scheme. Source: World Bank (2021)

The new policy goes even further to embed rent-seeking in its design through its proposal to bar withdrawals of all fiscal incentives to firms retroactively. In practice, this could mean the government could be legally barred from withdrawing subsidies from firms that fail to meet productivity, export or growth targets, essentially amounting to legalized rent capture. While providing policy consistency and predictability for investors is important, that must not be conflated with unconditional subsidization of unproductive enterprises regardless of performance. Benchmarks with productivity, technology and export targets must be embedded in future contracts and investment plans.

Industrial policy and political settlements

However much policymakers and economists wish to treat industrial policy as an exclusively technical issue, there is a wealth of evidence from around the world on how political settlements - or the configuration of power between different organizations and institutions in society - is critical to the success or failure of industrial policies. In particular, the literature on political settlements and industrial policy demonstrates that the ability to condition rents to achieve industrial growth is often a function of the political settlement or distribution of power between organizations and institutions.

As economists like Peter Evans have explained, the success of East Asian industrialization was in part a function of the exceptional capability of its states to effectively manage and distribute rents by virtue of both their ‘embeddedness’ (intimate linkages and dialogue with both the private sector and the citizenry) and ‘autonomy’ (relative independence from sectional interests in its decision-making). On the other hand, if a country’s governing coalition excludes a large number of groups that do

not benefit from the rents but have strong organizational capabilities, it is likely to increase the enforcement costs of industrial policy and limit its chances of achieving success without coercion.

Mushtaq Khan’s research on Pakistan’s industrialization attempts in the 60s and 70s attributes their failures to the rise of an organized intermediate entrepreneur class with strong political linkages that perceived itself as excluded from the benefits of industrialization and used its power to demand rents and protections from the ruling coalition. This resulted in increasing use of force to repress excluded factions, emergence of fractions in the ruling bloc and an eventual diminishing of the state’s ability to condition rents to big business interests.

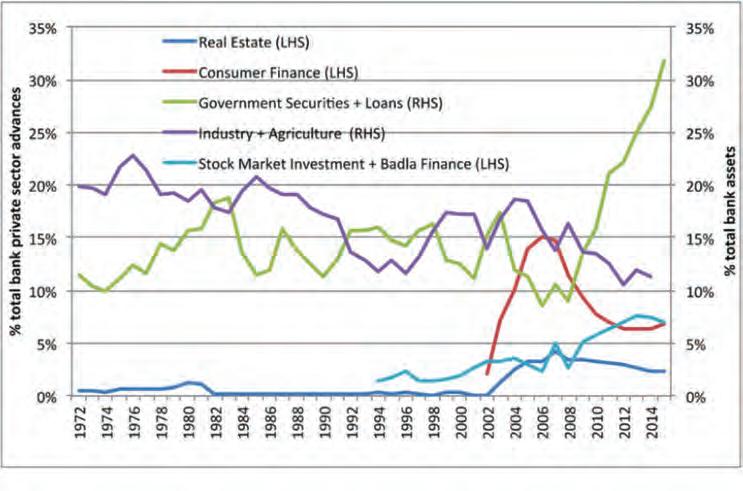

Political settlements are crucial to understanding the problem of rent capture across multiple sectors in Pakistan. It is not difficult to see how the organizational power of certain sectional interests – such as real estate and banking – have enabled them to engage in rent seeking that perpetuate productive stagnation. The organizational power of real estate interests for instance has enabled policies that have driven up land values and disproportionately high returns that have diverted capital and savings away from disproportionately taxed industrial production. There has been a similar process of rent capture by commercial banks since bank liberalization in the 90s, whereby banks have colluded to secure windfall profits largely through risk-free government securities rather than financing productive investment in industry. Within manufacturing itself, it is in large part the organizational power of various family firms that has enabled decades of tariff-related

rent capture while resisting productivity-enhancing management reforms or IPOs.

The question of political settlements is especially critical for industrial policy in the context of the current political settlement in Pakistan, comprised of what Mushtaq Khan would categorize as a ‘vulnerable authoritarian coalition’: characterized by limited popular legitimacy and strong excluded political factions, leading to limited autonomy from business and global interests and reliance on violence to maintain power. One potential implication for industrial policy is that developing the state’s ability to successfully condition rents and implement reforms that go against special interest groups will require the incorporation of excluded political factions into the ruling bloc to minimize policy resistance.

For all the shortcomings in the policy, the fact that Pakistan is finally devoting policy attention to industrialization is a welcome development that is long overdue. It is nonetheless crucial that this process is carried out with the seriousness and analytical depth that it requires, and policy designed with measurable targets and integrated pathways that enable productivity, export growth and a sustainable enhancement of productive capacity in Pakistan. Despite our unending policy and governance failures of past decades, Pakistan is once again faced with immense economic, strategic and demographic opportunities that could transform the economic fortunes of our people. We must get it right this time, not allow opaque policymaking processes and short-sighted rent-seeking to squander this opportunity and develop and implement a vision for industrial and economic prosperity for all. n

Figure 7 Evolution of bank lending by sector in Pakistan. Source: Naqvi (2018)

Table 1 Property tax collection as % of GDP. Source: Nabi et al (2025)

By Taimoor Hassan

When Temu entered Pakistan in late 2024, it stormed the market with a barrage of digital ads and the same formula that had already disrupted retail worldwide: jaw-droppingly low prices, flashy deals, and a model designed to undercut competitors. Launched in the US in 2022 by Chinese tech company Pinduoduo, the platform quickly rose to global prominence with its slogan “Shop like a billionaire,” stripping away intermediaries and connecting buyers directly to manufacturers to deliver prices that seemed impossible. Following the explosive rise of Temu, Pinduoduo’s ambitious Boston-based (yes, the company is American with roots in China) offshoot shaking up global eCommerce, it is clear that Temu’s success is no accident. Its ability to offer products at astonishingly low prices, sometimes even free, has captivated millions, including consumers in Pakistan, a notoriously price-sensitive market.

Within three years, Temu expanded to more than 40 countries, shaking the dominance of Amazon and other global giants. Its rapid ascent triggered a wave of defensive moves and regulatory alarms. Amazon accelerated price-matching programs, while Walmart and Shein began experimenting with supplier integration models. Regulators in Europe and lawmakers in the United States opened investigations into Temu’s data privacy practices, allegations of forced labour in its supply chains, and its ability to skirt fair taxation rules. Consumer advocates also raised concerns about product safety and misleading pricing. Yet despite mounting scrutiny worldwide, the platform’s irresistible bargains continued to drown out the red flags for millions of shoppers.

In Pakistan, Temu carried over the same playbook. It operates quietly, advertises relentlessly, and reveals little about its business operations, strategies, or long-term plans. The company maintains a low profile, preferring secrecy even as it continues receiving backlash from local sellers, policymakers and consumers.

By mid-2025, however, the early bargains had disappeared. Many products had surged by 200 to 300 percent. Items that once cost only a few hundred rupees were now priced in the thousands, while goods previously available for a few thousand crossed the ten-thousand-rupee mark. The abrupt spike left consumers questioning whether Temu’s promise to let them “shop like a billionaire” was ever sustainable or merely a short-term growth tactic.

This article delves into the logic behind the ultra-low prices offered by Temu, how they were able to deliver products at these prices,

aggressive subsidies and a blitz-scale growth strategy deployed in Pakistan, what caused the dramatic mid-year shift, where the platform stands today and what the likely future looks like.

Consumer to manufacturer (C2M)

- the root of Temu’s

ultra low prices

Temu’s rock-bottom pricing in Pakistan was not accidental but built on the same model that they deploy in other countries. Their parent company Pinduoduo pioneered a consumer-to-manufacturer (C2M) approach that bypassed traditional intermediaries. Instead of merely acting as a marketplace, it aggregated consumer demand and directed it straight to manufacturers, allowing products to be custom-made in precise quantities. By guaranteeing high demand, Pinduoduo and Temu could negotiate prices lower than competitors.

However, this would still not be enough to justify the rock bottom prices, because layered on top of this structural advantage is a well-known market entry strategy: burning cash to gain traction. “Low prices and discounts are used to gain market power. Globally, this model is used. Cash is burned when companies enter a market. They use this strategy to attract customers by offering products at very low prices, sometimes even free or at a nominal charge, to acquire market share,” explains Umair Arshad, founding member of the Pakistan eCommerce Association. He likens it to Careem’s early days, when drivers were given

generous bonuses to flood the market before the incentives were later reduced. In the same way, Temu’s aggressive discounts and subsidies in Pakistan were never meant as a permanent promise but as a calculated tactic to capture customers quickly and establish dominance.

The C2M model also slashes traditional supply chain inefficiencies, gives more power to small manufacturers and helps meet consumer preferences and demand with greater accuracy. The C2M model also gives Temu the ability to eliminate middlemen like distributors and wholesalers, and eliminate their margins from the cost, resulting in a further reduction in prices.

To elaborate on this, say a local eCommerce seller will rely on importers who will import raw material, then wholesalers and distributors, each adding margin and cost that seller will pass on to the customer. The price for this seller’s customer would be higher because of the addition of successive margins of various intermediaries in the supply chain. Under the C2M model of Temu, these intermediaries are eliminated, allowing Temu to keep the price low. How low? Only Temu knows but we perceive that their ability to aggregate consumer demand resulting in securing low purchase price from manufacturers and elimination of intermediaries is what actually makes their model considerably low-cost, possibly sustainable as long as the demand is high.

Logistics at scale

Price advantages alone cannot explain Temu’s rapid penetration. The company’s logistical prowess is equally critical. Umair Munir, former head of OLX Mall, explains that their home country’s state-subsidised postal system and public sector support create a unique cost structure which allows platforms like Temu to leverage these low rates to ship goods globally at a fraction of what local carriers charge. “For instance, a “free delivery” offer in Pakistan may include international air freight bundled into a consolidated shipment. This reduces the shipment cost per parcel,” he says.

Temu’s logistics network consolidates thousands of small orders into bulk shipments at centralised Chinese hubs (now expanded into other regions). These shipments travel via containerised air cargo, destined for regional clusters like Karachi, Lahore, and Islamabad, before last-mile delivery.

Notably, Temu operates its own cargo aircraft servicing routes between Hong Kong, Riyadh, and Karachi, optimising volume and reducing costs further. Such scale-dependent logistics capabilities are unmatchable by smaller local players, who struggle with fragmented, less efficient supply chains.

Uneven competition and CCP complaints

Alocal eCommerce seller in Pakistan must deal with importers, wholesalers, and distributors, each adding margins that inflate the final price for customers. Temu’s consumer-to-manufacturer model removes these intermediaries and secures ultra-low prices by pooling demand and forcing manufacturers to sell at scale. How low those prices can go is something only Temu knows. But its ability to squeeze manufacturers and cut out middlemen explains why its entry-level prices appear unbeatable, at least while demand remains high.

This advantage is reinforced by Temu’s integration with Pinduoduo’s vast supply chain of more than 11 million manufacturers. Under its fully managed model, sellers have little say beyond producing the goods. Pricing, marketing, logistics, and even customer service are controlled directly by Temu. Sellers may quote a price, but Temu decides whether to accept it and can list the product at that price or lower it to fit its strategy.

For Pakistani sellers, this created an uneven playing field. Organized local platforms operate within transparent supply chains and regulatory costs, while Temu sets the terms unilaterally and faces limited scrutiny.

International reports from Wired and discussions on Reddit show how Temu pressures sellers into cutting margins, often overriding their prices outright. Extending such practices to Pakistan raised a difficult question: are Temu’s low prices the result of innovation, or the exploitation of suppliers combined with regulatory blind spots?

Another important factor is that Temu’s price advantage exists only because it relies on its own overseas pool of manufacturers. It cannot realistically open its platform to local Pakistani sellers, even those producing domestically, because their prices reflect the taxes and costs of operating within the formal economy. Temu’s algorithm requires the lowest possible pricing, which local producers cannot sustain once taxes, duties on raw materials, compliance costs, and workforce expenses are included. Hence, their advantage is not efficiency but rather a structural disadvantage, where businesses operating legally are forced to compete against a model that sidesteps the obligations they bear. With e-commerce penetration in Pakistan still below 3%, Temu is not expanding the market; instead, it is cannibalizing it. The platform is diverting share away from local sellers rather than creating new demand.

These concerns soon escalated into formal complaints. Local eCommerce associations and retailers lodged petitions with the Competition Commission of Pakistan

(CCP), accusing Temu of predatory practices, bypassing customs, and deliberately undercutting businesses that had to comply with duties and taxes. A key issue highlighted in various complaints by independent sellers, Chainstore Association of Pakistan and Pakistan Retail Business Council is Temu’s pricing strategy, which they describe as predatory. By offering goods at prices significantly lower than those of domestic competitors, Temu is allegedly distorting market competition and threatening the viability of small local businesses. After conducting its own due diligence, the CCP concluded that Temu’s tactics were anti-competitive and wrote to the Pakistan Telecommunication Authority (PTA), recommending that Temu be banned in the country as per documents reviewed by Profit.

The growth and marketing blitz

The supply side strategy of Temy works only when the demand is massive. The more customers buying a product at the same time, the more leverage Temu has to pressure manufacturers into offering bulk discounts. To generate that demand, it relies on blitzscaling and blitzmarketing, a playbook that prioritizes speed over efficiency by burning cash to acquire users.

Wired estimates Temu loses about $30 on each order, with overall losses between half

a billion and a billion dollars. These losses are deliberate subsidies meant to lure customers away from established global platforms like Amazon, or in Pakistan’s case - local sellers and businesses, who cannot afford to match such tactics.

To make its presence unavoidable, Temu invests heavily in advertising. Globally, it spent an estimated $2 billion on Meta ads in 2024, and Google ranked it the fifth largest advertiser that year. The same approach was visible in Pakistan, where digital platforms were saturated with Temu ads promising products at prices no domestic seller could hope to match.

This completes the demand side of the loop. By spending enormous amounts of money on marketing and user acquisition through discounts, Temu gets a very high customer volume from the very beginning that can justify getting low prices from manufacturers.

By mid-2024, Temu had expanded into more than 40 countries and claimed 150 million users worldwide. In Pakistan, this growth unfolded in a regulatory vacuum, with loopholes in taxation, customs and consumer protection allowing Temu to scale rapidly.

Temu’s method to this madness is simple: opening multiple markets at the same time very quickly further creates the demand to secure lower prices. This creates a very powerful feedback loop: the surge in demand gives Temu more leverage with manufacturers to secure lower prices. The lower prices in turn attract more customers further boosting demand. The cycle continues, allowing Temu to scale rapidly while maintaining its core value proposition of ultra-low prices.

Again, all of this only works if Temu burns a lot of cash from its own pocket to drive massive initial engagement from customers and reach economies of scale. Then to maintain continued economies of scale, it needs to keep discounting which means it would need to continue spending cash on, booking heavily and seriously undercutting competitors to gain market share quickly. Any dip that disrupts its economies of scale would mean higher cash burn on discounts as well an increased spend on marketing to acquire customers again. When it successfully eliminates local competition, that would be its time to make profits from markets that it dominates, resulting in price increase and low or no discounts.

Too small for the government to regulate

Temu’s growth machine was never built to withstand external shocks. Its entire model hinged on exploiting loopholes in global trade rules such as the de minimis exemption, which allows low-value goods to enter countries without duties or heavy scrutiny. In practice, this

Plane carrying Temu cargo at Karachi airport

meant Temu could flood markets with cheap parcels while local businesses importing in bulk faced high customs duties and regulatory costs. Another point to factor in is that they do not have local presence or investment in developing their on-ground infrastructure, which means their cost of doing business is significantly lower than even a small business that would need to hire at least 2-3 people and grow as they expand.

The United States became the first major battleground. Under US law, imports below 800 dollars entered duty-free, a threshold Temu exploited by shipping millions of small parcels under customer names instead of bulk containers. As Temu’s ultra-cheap model gained traction, it was American retailers like GAP, Amazon and Forever 21 that raised the alarm, arguing that Temu’s tactics were not fair competition. That pressure triggered a regulatory crackdown. By April 2025, Washington imposed tariffs of 120 to 145 percent on Chinese imports, effectively ending Temu’s free ride. Temu’s response was telling: it added “import charges” of up to 150 percent at checkout, pulled direct shipments from China, and rushed to build a local fulfillment model.

Other countries moved even faster. Indonesia, Vietnam and Uzbekistan prioritised defending their local industries and tightened rules early, preventing Temu from dumping goods at unsustainable prices. Pakistan, however, lagged behind. Local retailers repeatedly complained to the CCP that Temu was capturing market share unfairly by exploiting It was only on July 1, 2025, after months of industry pressure, that authorities finally reduced the exemption to Rs1,000. The timing told its own story. July 1 was also when Temu’s prices in Pakistan spiked by 200 to 300 percent. Products once priced at a few hundred rupees suddenly cost thousands.

Taxes don’t explain the whole story, demand destruction does

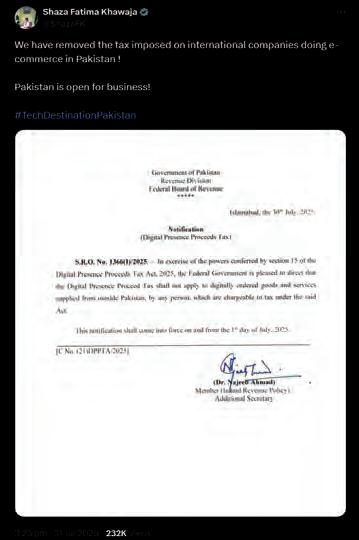

Shopping on Temu once felt like stumbling into a digital thrift store where everything was suspiciously cheap. Hyundai headphones sold for under Rs3,000, magnetic nose strips for less than Rs1,000, prices that seemed too good to be true. They were. Today, the same headphones cost Rs10,319 and nose strips have doubled in price. Even low-duty products like phone covers have become more expensive. What added to the uncertainty was Pakistan’s decision to roll back the 5 percent digital proceeds tax, a move made after a request from the US government. For a brief period, consumers expected this to translate into lower prices on

Temu. However, within days it became evident that the rollback had no impact, and prices remained unchanged.

Asfandyar Farrukh, the president of Chainstores Association of Pakistan, explains that customs enforcement in terms of assessing fair value of a product has also gotten stricter.

He explains that when a parcel comes to customs officials in Pakistan, it would be up to officials to assess what fair value of products in a parcel would be and calculate duties based on the fair value calculated by Pakistan Customs. Say a Temu order reaches Pakistan Customs and includes the Rs2,660 Hyundai Earbuds. To assess their fair value, Pakistan Customs can check other online platforms. Online sources list the same earbuds to be at around Rs11,000. The customs officials would charge duty on the parcel at Rs11,000 instead of Temu’s discounted price of Rs2,660. Since the value of the Temu parcel is above Rs1,000, duty would be applicable here, charged at 20 percent of the fair value. This should translate to a Rs2,200 addition in the price of headphones by Temu due to reduction in de minimis exemption limit and stricter customs enforcement while assessing fair value of the product.

The present price of Rs10,319 is not justified by the exemption change and stricter enforcement alone. Moreover, an 18 percent GST is charged by Pakistan Customs which is absorbed by Temu and not passed on to cus-

tomers. Even if it was passed on, it would not explain a 300 percent increase in headphone prices. Industry insiders suggest Temu was not only exploiting the de minimis loophole but also blatantly bypassing customs rules by under-declaring parcel values. With tighter enforcement, that advantage collapsed overnight. The bigger issue is structural. Temu’s model depends entirely on high demand to negotiate ultra-low bulk prices from manufacturers. When exemptions were reduced and duties imposed, the economics of its model broke down. Higher prices triggered demand destruction, which meant Temu could no longer guarantee the volumes needed for deep discounts. Pinduoduo itself admitted in its latest financial results that their current profit levels are not sustainable and expect fluctuations in future profitability. Temu and its sellers had faced a reduction in demand due to tariffs and the end of the de minimis exemption in the US, which accounts for a third of its global sales. If demand shrinks in one of its largest markets, the pressure extends globally, including Pakistan.

Temu’s promise of “shop like a billionaire” was never built on loyalty or quality. Its customer base grew on the back of impossibly low prices, with many tolerating subpar goods only because they were cheap. Once those prices began to rise, little remained to differentiate the platform. The company’s refusal to engage with media inquiries, including those from Profit, highlights a troubling lack of transparency. That opacity appears to extend beyond its business practices. Several local influencers who shared negative experiences with Temu reported receiving strikes on social media platforms such as Instagram, raising concerns about how criticism of the company is suppressed.

For Pakistan, the way this situation is handled will be a defining test. Policymakers are often eager to welcome international platforms in the hope of attracting foreign investment, yet Temu has offered little value to the domestic economy. Instead, it has thrived by exploiting loopholes, undercutting compliant businesses, and draining revenue that should have strengthened the local industry. Encouragingly, Pakistan is beginning to respond in line with mature global markets. The Competition Commission of Pakistan has gone beyond warnings and formally recommended that the PTA block Temu, echoing actions already taken in the United States, Indonesia and Vietnam. Such steps are especially significant in an industry like e-commerce, which is still nascent but rapidly emerging as an alternative source of income for hundreds of thousands of local sellers and small businesses. Whether regulators follow through will decide if this ecosystem is protected or left vulnerable to foreign platforms built on subsidies. n

Plane carrying Temu cargo at Lahore airport

Hundreds dead; millions hungry: KP’s food is buried under boulders and Punjab won’t share

Massive boulders coming down with the flash floods in Buner did not discriminate between houses, fields, and infrastructure

KP and Punjab experienced flooding around the same time but for different reasons. As a food security crisis looms, now is not the time for provincial division

By Abdullah Niazi and Aziz Buneri

Buner/Lahore/Hafizabad: The night before flash floods came barreling down into Buner, some in the small district thought the end of times had arrived. The thunder that preceded the chaos was deafening. Children complained of ringing ears as more than 150 mm of rain fell over the small district in Khyber Pakhtunkhwa.

The terrifying sounds of rain and thunder

were only the beginning.

In 48 hours, more than 200 people in Buner were dead. Another 120 were injured and at least 50 more were missing. What happened in Buner was a rare natural occurrence known as a cloud burst. This type of event is when more than 100 mm of rain falls in an area in a time frame of one hour. In Buner the amount of water that fell in one hour was 150 mm.

It is confusing to measure liquid in units of length instead of volume. “One millimeter of rain” is actually one cubic millimeter per square millimeter. There is a long history to

how the field of dimensional analysis arrived at this unit of measure as the best one for rain, but the simplest way to understand it is that “1 mm of rain” translates to one liter of water per square meter. That would mean 100 mm of rain would mean 100 litres of water per square meter.

A square meter is a square box roughly 3.3 feet by 3.3 feet. That means the cloud burst event in Buner meant 150 litres of water fell for every square meter in the space of an hour. Even as the catastrophic rain subsided, the sheer volume of water proved amalgamated in

flash floods passing through the district. Massive boulders weighing thousands of kilograms came rolling into the valley destroying homes, crops, roads, and anything else in their path. Entire trees were ripped out from their roots, turning into forces of mass destruction as they hurtled towards the district of more than 10 lakh people.

More than 800 people have died in the floods that have hit Pakistan since early August this year. No single area has been hit harder than Buner. In the village of Bashonai Pir Baba, named so for the green-domed shrine of the 16th Century Sufi Pir buried there, Ashiq Ali looks on at what were once lush green maize fields. It is a bright sunny day with gentle white clouds drifting in the sky — no indication in the sky of the wrath it had unleashed on Bashonai only a few days ago. But one has only to look at the ground to see the wreckage.

Massive boulders have flattened the fields, blown entire houses away, and now it is impossible to move them. They are simply too heavy and the machinery required to get rid of them is simply not available.

But today Asghar Ali is worried about something else. The boulders that flattened his village also decimated the storage houses most families keep their wheat in. Buner is a subsistence based agrarian district. Families have small farms close to their homes and they grow staple crops such as wheat that last them the whole year.

“People here do not have large landholdings,” Ashiq Ali tells us. “They have just enough to grow enough wheat for the whole year. We use that to make flour and the germ to feed our animals. But our entire stores are gone now.”

The wheat stores are not the only problem. The local community can no longer grow any food because of the massive boulders that have taken over their agricultural land and made it barren.

“In the first few days the recovery from the flood was very difficult. People could not find the dead bodies of their loved ones and there were thick layers of mud everywhere,” says another farmer in Bashonai. “They had to bring in large excavators and other machinery to move

the rocks and dig mass graves for the dead.”

Now the survivors face a hunger crisis. With their wheat stores swept away, the residents of Buner and other flood affected areas all across KP had been hoping for relief and grain to come in from Punjab. For the first week or two after the floods which started around the 10th of August, wheat was coming in from Punjab. That has changed in the last 10 days. Since the floods hit Punjab around the 24th of August this year after India had to release water from its dams on the Ravi, Chenab, and Sutllej, the Punjab government through its different district administrations has blocked the supply of wheat from Punjab into KP.

While no official notification from the government has come through, Profit has seen notifications from at least a dozen districts calling for inspection of trucks carrying wheat to the Northern parts of the country. As a result, trucks full of wheat are waiting in long lines at checkpoints to enter KP and not being allowed to go through, with authorities in KP and transporters claiming each truck is being asked to pay a bribe of Rs 1.5 lakh to get their truck through. As a result, the price of wheat in KP has skyrocketed in mere days.

As the floods continue to travel South and evacuations run rampant in Sindh, Buner has become a political flashpoint. The response time of the National Disaster Management Authority (NDMA) in Buner became the subject of a heated debate between PTI Chairman Barrister Gohar Ejaz and Law Minister Azam Tarrar on Friday.

“I say at this forum that we will continue to be at odds with the NDMA,” Barrister Gohar said on the floor in a heated warning. “I said day-before-yesterday that the NDMA only gave us a few supplies in Buner, while 236 people have been killed, 120 are injured, and 1,470 shops and 875 homes have been destroyed.”

A flood by another name?

Din Muhammad sat perched on his charpai as it rested slightly tilted on a small mound of dirt. Cars whizzed past him barely a dozen feet away.

The traffic on the M2 was subdued early in the morning and offered little distraction to Din and the long line of people that found themselves camped out on the side of the highway with their families, cattle, and whatever belongings they could carry with them.

“People from the government came two nights ago and told us to evacuate. Some people from within the village did not want to leave and advised us against it but the government kept pushing. Eventually we grabbed our essentials and left,” he explains. His eyes are fixated on the scene in the distance. Right next to the motorway’s Babu Sabu Interchange close to Thokar Niaz Baig, the main entry point to Lahore, one can see nothing but water from miles. From a distance the water seems timeless. Like it was never not there. But it does not take long to notice what is poking out of the water. Golden three-pronged street lamps and billboard with the half visible words “New Metro City Lahore”

“He is looking for our buffalo. When we left the village we brought all five animals with us, but it was night time and one of them wandered off in the middle and we haven’t seen her since,” his wife says from the foot of the charpai where she is attending to their children. “The buffalo we lost was the healthiest in our herd and gave the most milk. He’s worried we will never find her now.”

Just over a hundred kilometers away, Muhammad Azam is among the many in a relief camp set up by the Punjab Government at a public school. He sits on a makeshift floor outside tents that have been pitched on the school’s playground. Azam works at a hospital in Hafizabad City, but his family lives a little farther away where they have a couple acres of land that they use for their own needs. Azam had been home to look at his rice crop. “I grow Basmati here. It does not give me the best price but my family likes it and here in Hafizabad we have the best Basmati in all of Punjab,” he says. When the rains first arrived, Azam was hopeful it would mean a better harvest. But then they did not stop. Two days before the Chenab came hurtling towards his village, police officials had helped evacuate the village.

The experience of Muhammad Azam and

I said day-before-yesterday that the NDMA only gave us a few supplies in Buner, while 236 people have been killed, 120 are injured, and 1,470 shops and 875 homes have been destroyed

Barrister Gohar Ejaz, chairman of the

PTI

Din Muhammad of this year’s floods was very different to the experience of Ashiq Ali and the many other families in Bashonai. Despite the destruction to farmland and property being massive, only 40 lives have been lost to the flooding in Punjab. As tragic as even these numbers are, the Punjab Government has been on top of the evacuation, rescue, and relief efforts. The Flood Forecasting Department has given timely warnings and the government machinery has stepped in quickly to minimise loss of life and provide relief to the more than 20 lakh people displaced by the floods and the countless more that have been affected by them.

The KP government’s response in comparison has been meek. Heroic stories have come through from the Northern Areas. In Gilgit Baltistan, three shepherds saved hundreds by warning their villages in time of an incoming flash flood. In Ashiq Ali’s hometown of Bashonai, a schoolteacher and volunteer, Zahoor Rehman rushed to help his community. He guided women and children to safety and carried several, including three young brothers, through debris-filled waters.

But as the flood intensified, Zahoor was struck by a massive boulder while trying to help a guest. His last words were: “I’m going. Don’t come in!” Moments later, the waters swept him away. His body was found two kilometers downstream.

The stories of individual heroism aside, the government has appeared quite helpless. There have been no early evacuations and relief efforts have been slow. When KP Chief Minister Ali Amin Gandapur visited Buner, for example, he said quite curtly that his government was “trying” and they could not “bring the dead back to life.” One reason for this, of course, is that the situations in Punjab and KP are not comparable. “What you have in KP is a very different phenomenon. It is a combination of flash floods from glacial lakes melting in the Himalayas and repeated cloud bursts because of climate change,” says Dr Hasan Abbas, Pakistan’s leading hydrologist and river expert.

A child walks through his family’s flattened agricultural land in Buner following devastating floods

“In Punjab you have river floods. These take place because of heavy monsoon rains particularly in India where there has been a lot of rain that has led to the dams on the rivers Ravi, Chenab, and Sutlej filling to capacity and forcing India to open their gates. As a result the rivers flood everything in their path both in the Indian and Pakistani sides of Punjab.”

As Dr Abbas explains it, the situation in KP is the result of climate related chaos. Glacial Lake Overflow Floods (GLOFs) take place when a retreating glacier melts and releases a great cache of water which hurtles down the high mountains causing destruction in its path. Similarly, cloud bursts, even though they sound like a cloud popping like a balloon, is when an area is hit by a large quantity of rain in very little time.

In the case of KP, forecasting these events is comparatively more difficult. The impact of climate related GLOFs and cloud bursts is sudden. What is needed is a robust alarm system, weather prediction services, and most importantly community engagement. “If you give people full time employment, station them at important points, and give them communication capability at a community level that alone can be enough to save many lives,”

says Dr Abbas.

In Punjab, the flood forecasting department knows the natural course of the river, has live data regarding how much water is coming at any given time and can estimate how long it will take this water. A big problem in the case of Punjab has been the building of infrastructure on the embankments of Punjab’s rivers, particularly on the Ravi near Lahore. It has been the subject of another story by Profit.

Damage abound

The common ground between KP, Punjab, and eventually Sindh will be the decimation of agriculture in all of these flood affected districts. In Punjab, more than 4000 villages have become inundated with flood water. Put that into perspective: the last time Punjab conducted a Mouza/Village census was in 2020. Back then the government reported there were a total of 26,462 villages in Punjab. That means nearly 20% of the villages in Punjab and their accompanying agricultural lands have been hit by these floods.

In Punjab, the current season is Kharif, which means most of Central and North Punjab close to the river regions have been used for

In Punjab you have river floods. These take place because of heavy monsoon rains particularly in India where there has been a lot of rain that has led to the dams on the rivers Ravi, Chenab, and Sutlej filling to capacity and forcing India to open their gates. As a result the rivers flood everything in their path both in the Indian and Pakistani sides of Punjab

Dr

Hassan Abbas, hydrologist

rice cultivation. A number of alarmist calculations have come up in recent days claiming nearly 60% of the rice crop has been destroyed. In reality, rice is very good at absorbing water and there is no knowing how much will be destroyed until the floods clear out.

As far as food security is concerned, the situation of the current rice crop is not threatening. The total area under rice cultivation in 2024 was 10.6 million acres, which makes it 12.9% of the total cropped area. As a percentage, this is down from 2010 when rice was grown on 9.36 million acres, making it 14% of the total cropped area. Overall the area that is under rice cultivation has not increased by much. Rice has actually seen an improvement in yield. In 2010, the total rice production was 11.1 million tonnes accounting for 1.18 tonnes per acre. In 2024, the total production was 14.7 million tonnes giving an overall yield of 1.38 tonnes per acre.

The bigger concern is wheat. It is the single largest caloric component in the diet of the average Pakistani. Wheat makes up nearly a third of the caloric intake by an average Pakistani, and Pakistan’s per capita consumption of wheat is 124 kilograms annually, which is the highest in the world.

While these floods did not come in the Rabi season, what we do know is that a lot of the soil in Punjab could become waterlogged, which means when it is time for the Rabi season and the wheat crop, it might not be viable.

In 2024, wheat accounted for 43.3% of the total cropped (GSA) area of 82.7 million hectares. That means wheat was grown on just over 35 million acres. Since wheat is only grown once per season, that means it is grown on 35 million acres out of the total cultivated area of 52.7 million, making it a crop grown on more than half the cultivated land in the country in 2024. In 2023-24, the total production of wheat in Pakistan was 31.58 million tonnes grown on around 35 million acres.

In KP as well the damage has been extensive. According to data collected by Profit through government sources, there are 3.16 lakh acres of land where crops are being grown that have been completely destroyed. The most extensive damage has been to the maize crop, which is a major contributor to KP’s economy. Much like Punjab, this also accounts for close to 15% of the total cropped area in KP. That, of course, is the destruction of the existing crop. It will impact farming families in the long run, but the immediate concern, of course, is that there is no wheat in the province.

A time for unity

All across Punjab, government officers have been appointed to stand watch at different exit points from the province. The notifications for their

duty, announced by different district governments and not a central order from the Punjab government, lists the nearly 60 exit points and assigns 120 officers to monitor them. An officer is present 24/7 with the first one there from 9 AM to 9 PM and the next officer on the night shift from 9PM to 9AM. Their appointment in these notifications have explicitly been made to “monitor the movement of wheat and wheat products including flour to other provinces.”

Sarhad Chamber of Commerce and Industry President Fazal Moqeem Khan and Pakistan Flour Mills Association KP Chairman Naeem Butt addressed a crowded joint news conference at chamber house on Tuesday, blaming the Punjab Government and top bureaucrats for halting supply of wheat to Khyber Pakhtunkhwa with nexus of mafia, described the ban was sheer violation of article 151 of the constitution of the country. According to them, KP is facing a shortfall of 41,000 metric tons of wheat as the province’s total wheat production is 12,000 metric tons against its demand of 51,000 metric tons. On top of this, in areas like Buner where families often produce 40 to 70 maunds which is enough for their own families at least, the storage houses for this wheat have been swept away.