OECD Competition Committee

CEO Vipps MobilePay, Rune Garborg

CEO Vipps MobilePay, Rune Garborg

504th place

Valued at $39.23 Billion USD

644th place

Valued at $30.13 Billion USD

682th place

Valued at $28.65 Billion USD

799th place

838th place

Danske Bank

valued at $23.88 Billion USD

Valued at $22.71 Billion USD

No place

Valued at $ 1 Billion

Top five Nordic Banks: 4% of Apple's Worth

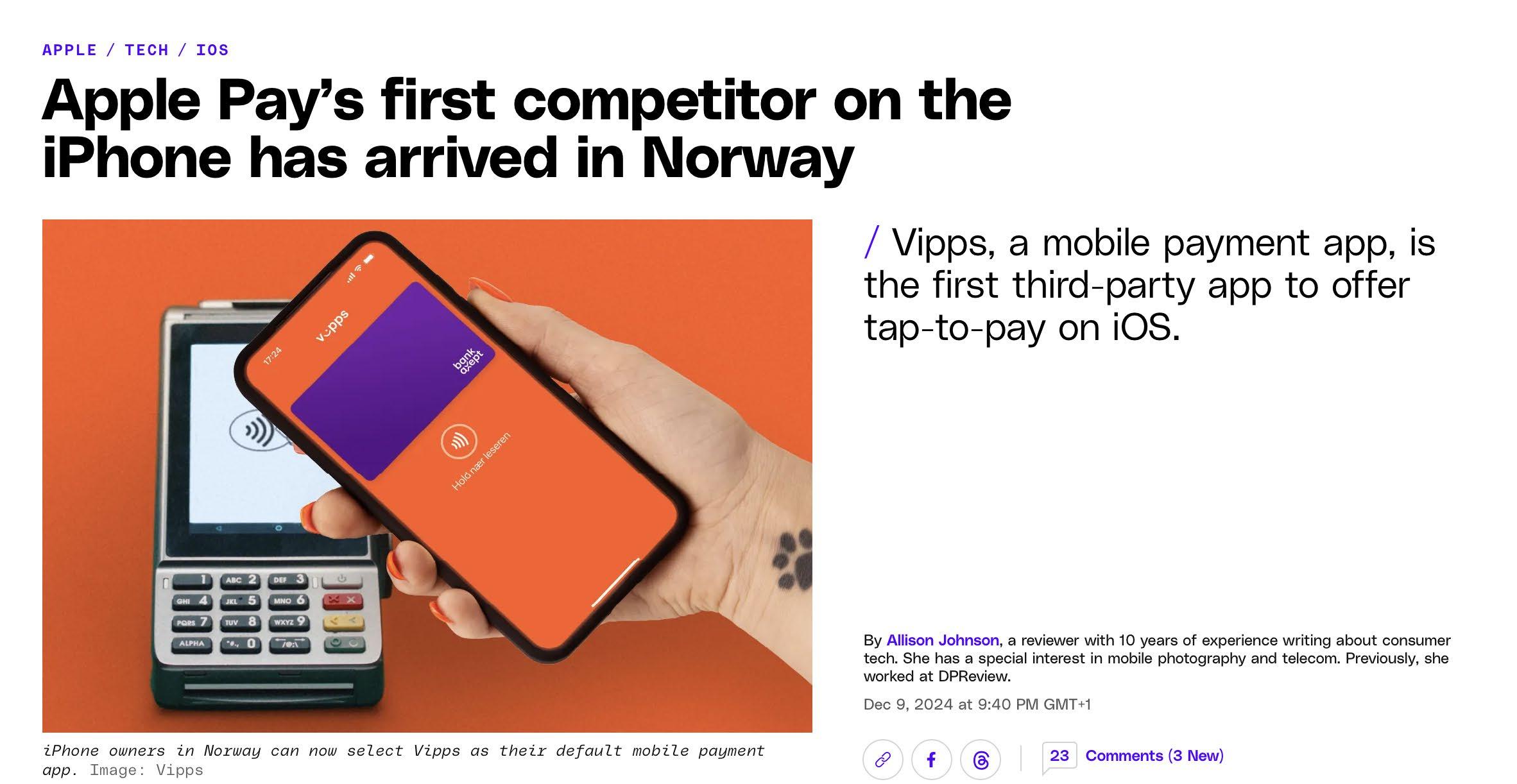

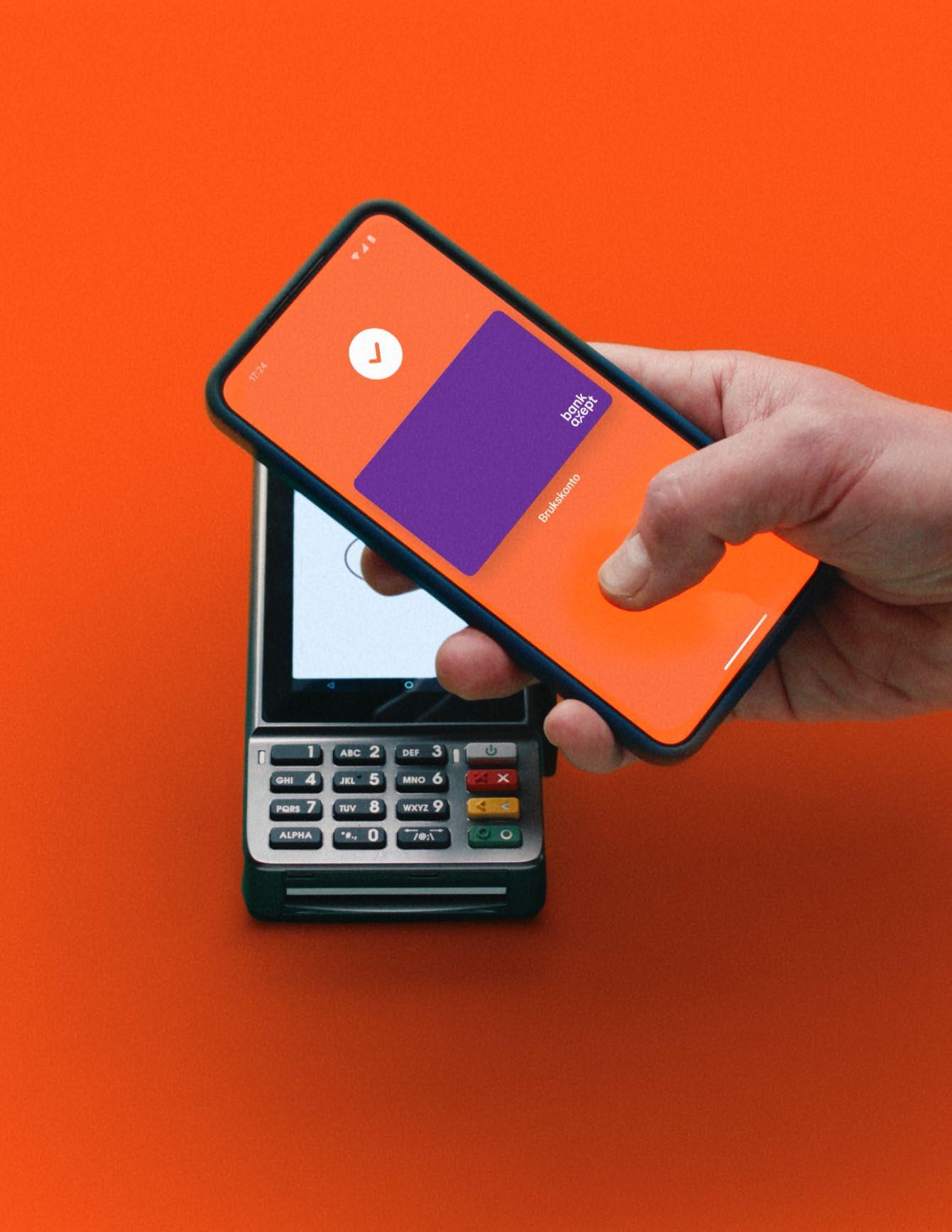

After a long battle, we finally have a level playing field in-store

1. Technical and economic barriers

• High margins from terminal providers, acquirers and PSPs increase costs

• Terminal ownership structures hinder innovation and access

2. Cross border scaling

• A unified wallet across countries requires support from local banks

• Lack of interoperability between existing solution

• The current model makes it too expensive to issue and use alternative solutions

• Negative impact on consumers and innovation

• Whoever owns the user journey owns the relationship

• While still struggling to enable cheaper payment rails, Europen banks are losing customer interface

• Risk: Europe loses the battle for the mobile wallet

How to strengthen competition:

• A common European digital ID enabled by eiDAS 2.0

• Allows consumers to easily register cards in in wallet

• ID wallets should be used in cooperation with existing payment solutions

• Reduces dependency on national solutions and banks

• More open infrastructure = Lower costs = More choice

Swift and clear implementation of eiDAS and access rules

Standardised access to mobile features (NFC)

Measures to address high terminal costs

Public–private collaboration on ID and interoperability

European alternative to Apple and other bigtechs