GREEN MOUNTAIN AGENT VERMONTINSURANCEAGENTSASSOCIATION|January2023

Insurance

is a

trade

representing

100 independent insurance agencies in Vermont, with more than 900 employees VIAA member independent insurance agents represent more than one insurance company, and as a result, can offer clients a wider choice of auto, home, business, life and employee benefits t IN THIS EDITION: How to Build a Strong Agency Budget See Page 17

Vermont

Agents Association

statewide

association

nearly

600 Blair Park Road, Suite 100

Williston, VT 05495

Phone: 802-229-5884 Fax: 802-876-7912 www.viaa.org

VIAA Officers

President

Jessica Fleury, ACSR

Vice President

Ian Sutherland, CIC, AAI-M

Treasurer Aislyn Allen, CISR Secretary Laurie Audy National Director Michael R. Barrett

Directors

Pat Cahoon

Audrey Macie

Executive Director

Mary M. Farley, MBA, AAIM

CONTENT ________________

January 2023

Green Mountain Agent is a publication of

05

12

17

Letter from the President 06 Association News

On the Hill

Agency Management How to Build a Strong Budget for Your Agency 25 Agency Management Why Compliance Holds The Key to Increased Profits 32 E&O Corner What Inflation Means for Your Insurance & Business 38 Agency & Company News

www.viaa.org 3

4 www.viaa.org

January 2023

Happy New Year to all! There are exciting opportunities ahead for 2023 and we are working at the Association to bring continued growth to all our members.

First order of operation is that the delivery of the Green Mountain Agent Magazine, will be changing from monthly to quarterly. You will be receiving updates via our new newsletter format for the months in between. We want to keep content informational and efficient for all of you. The newsletter will come directly to your inbox and will include information such as local updates and national highlights. Be on the lookout for the first one in February. We will be continuing our lobbying work this legislative season and there are fresh faces at the Statehouse for us to build

M. Fleury VIAA President

relationships with. Please remember that we are an active presence on YOUR BEHALF! If you have a concern with potential new regulations, please do not hesitate to contact us so that we can help communicate clearly how our industry sees impact not only to ourselves, but to our clients.

On the educational front, we are planning to offer in person classes at our headquarters office in Williston, VT, starting in the Spring. We have missed the energy of learning in person, TOGETHER, and want to restore the enhanced experience that goes beyond "Zoom".

And further, in the spirit of education, we are collaborating with a committee to bring more insurance educational opportunities to Vermont, both at the high school and collegiate level. This is a challenging time for hiring staff, and our best approach is to inspire young minds to this rewarding and challenging industry.

We have already commenced our planning of the 2023 VIAA convention and hope to share details with you in the coming months. In the meantime, save the date for the 2023 golf outing, on June 13, 2023, at the beautiful: Vermont National Country Club in South Burlington, VT. The golf outing was successful last year, and we are hopeful for great attendance again this year. More details to come as the event gets closer.

I look forward to the year ahead!

If you have any questions, I welcome you to reach out to me at: Jfleury@therichardsgrp.com.

Stay Well,

Jessica M. Fleury President, VIAA

LETTER FROM THE PRESIDENT

Jessica

www.viaa.org 5

MINDY

BERO, CLCS, CRIS

NAMED

VERMONT IAIP MEMBER OF THE YEAR

MindyBeroofHickok&BoardmanInsurance Groupisthe2022VermontInternational AssociationofInsuranceProfessionals(IAIP) MemberoftheYear.MindyjoinedHickok& BoardmanInsurancein2014andiscurrentlya commerciallinesproducer.Sheisamemberof ChamplainValleyAssociationofInsurance Professionals(CVAIP)andhasbeenanofficer andremainsactiveontheBoard.Given Mindy’spassionforinsuranceandeducation, sheisCVAIP’sEducationChair.

THE HILL NEWSPAPER NAMES BIG ‘I’ LEADERS AMONG TOP D.C. LOBBYISTS

The Hill, a prominent political newspaper, has once again recognized the Big “I,” naming Bob Rusbuldt, Big “I” president & CEO, and Charles Symington, Big “I” executive vice president, among the top trade association lobbyists in Washington, D.C. this year. As in previous years, the Big “I” was the only property-casualty insurance agent or broker group to make the list.

Your membership helps us make an impact in D.C.!

6 www.viaa.org

VTAIP 2022 OF THE YEAR AWARDS PRESENTED

AtourAnnualCommissioner’sNightinNovember, theVTAIP2022OftheYearAwardswerepresented. Nominatedbytheirpeers,thesedistinguished awardsrecognizethemembers’involvementinthe Association,theircommitmenttocontinuing educationandhonortheirsuccessintheinsurance industry.TheywilleachgoontorepresentVTAIPat theIAIPRegionalConferencetobeheldin Providence,RhodeIslandinApril2023.Thewinner willthengoontotheNationalIAIPConferencein Providence,RhodeIslandrightafterourHUB RegionalConference.

Pleaseextendyourcongratulationstothesevery deservingindividuals! RoseThompson,CPIW,AIS,API-Professional UnderwriteroftheYear StephanieJoOakes,AINS,CLP–ClientServices ProfessionaloftheYear ConnerLaFrance-RookieoftheYear AudreyMacie,CIC,CISR,CPIA,CIIP,CLP,MLISInsuranceProfessionaloftheYear www.viaa.org 7

www.viaa.org

www.viaa.org 9

VIAA EDUCATION Any time. Any where. Get it done. viaa.org/Education

ON THE HILL House Passes Bill to Cut IRS Funding

the U.S. House of Representatives voted to significantly cut fundingfor the Internal Revenue Service(IRS). The legislation, which passed onpartisan lines, was the House Republicans' first major bill of the year and was one of their topcampaign issues throughout the midterms.

The House is also expected to vote on legislation introducedby Rep. Buddy Carter (R-Georgia) thatwouldabolish the IRS and replace the federalincome tax with a national-level consumption tax. With Democrats in control ofthe U.S. Senate and the White House,bothof these bills are unlikely to be passedinto law. President Joe Biden has also indicated he would veto the legislation.

Over the years, theRepublican Party's concerns that the IRSunfairly targets the middle class and small businesses have grown. However, under the Biden administration, the IRS is due to expand.

As part of theInflation Reduction Act(IRA)— which was passedin August 2022—$80billion in fundingfor theIRS was included. Specifically, this funding will increase enforcement against tax evasion, aswellas modernizetheagency'stechnologyand other systems. In addition, the IRS is planning to hire an extra 87,000 employees over the next decade.

While the Republican legislation passed this week would cut thisfundingand the potential for increased enforcement against small businesses, it would also increase the federal deficit by $114 billion by 2032, according to the Congressional Budget Office.

As tax policy continuestoremain topof mind for both policymakers andagentsand brokers, the Big "I" will regularlyprovideupdates throughtheNews & Viewse-newsletter.

Reprinted withpermissionfromIAmagazine

12 www.viaa.org

Risk Management

HOW TO BUILD A STRONG BUDGET FOR YOUR AGENCY

ByLaurenWashington

Budgeting is the practice of trying to reasonably estimate a company’s future expenses and revenue streams so you can monitor the company’s financial health and make informed decisions.

Budgeting does not need to be hard, and in this article we are going to do our best to simplify it for you. With a little time and consistency, a budget can be one of the most powerful tools you’ll ever have inside your agency. Let’s break it down!

StartwithGoals

Creating a budget should start with a list of goals. Ask yourself, what are the long-term goals for the Agency? What will success look like in the near term? Make sure that the goals that you set are (SMART) Specific, Measurable, Achievable, Relevant, and Time-based. These goals will have an impact on your revenues and will also determine where you will need to allocate your resources in the next year. Your goals will help identify the specific areas that you want to invest in to ensure that you are making progress. Many agencies operate without a

budget and instead rely on their gut instincts, or worse, have to wait until the end of the year to determine if the resources needed to invest in new tools or resources are available.

Having a budget can provide you with greater clarity and allow you to act with confidence. We realize that building a budget is not easy for everyone, so we have created a budgeting tool for Microsoft Excel (download here) that can be used to help you build a budget for your agency.

This tool is separated into several tabs that work together and are designed to simplify the budgeting process. On the first tab, you can categorize your expected expenses. Once these are entered there, they will automatically fill in the “Expense” portion of the next tab, Annual Budget.

After adjusting and completing your Annual Budget tab, it will automatically break these expenses down by month in the Monthly tab. In this tab, you can fill in your actual revenue and expenses every month, and it will automatically compare them with the amounts you budgeted. The monthly income

www.viaa.org 17

statements pull to the Annual tab, which provides an overview of how well you have maintained your budget during the year.

#1:Understand your incomestatements

Income statements are split into two major sections: Revenues and Expenses

Revenues can be further categorized into Commissions & Fees, Contingency/Bonus, and Other Income:

Commissions & Fees: This category can include any revenue resulting directly from sales of insurance to Agency customers. This includes direct bill commissions, agency bill commissions, agency fee commissions, and any commissions received from insurance brokers. Only the agency’s portion of commissions and fees belong in this category. Any revenue collected in an Agency Bill situation that is to be remitted to a carrier should not appear on any part of the income statement because it is not owned by the Agency. This portion is collected and held in a Trust Account on the Balance sheet until it is remitted to the carrier.

When budgeting for Commission and Fee Revenue consider:

Expected renewal income: This should be based on last year’s performance, your agency’s retention rate, expected rate increases, and any other expected changes from carriers. Be sure to eliminate any polices that you know have been lost or by their nature are not expected to renew (for example bonds).

New Business: Include the new business you expect in the coming year based on the goals that you have set for your team.

Contingency/Bonus: This category includes all contingency income received from carriers, and any bonus income received from a cluster/network/aggregator/alliance. It differs from Commission & Fees income from a budgeting standpoint, because, although it is an indirect result of sales, it is contingent upon your

performance and the guidelines set by each carrier for new business production, retention, loss ratios and other factors. It can alsobe impacted by the performance of a network/aggregator/alliance that the agency is a member of. As you know, contingenciescan vary and are not guaranteed. We strongly recommend that agencies do not include contingencies in their operating budget.

Fee Income: Any fee income can be estimated based on the previous year performance aswell as the goals for the upcoming year.

Other Income: Oftentimes, Agencies will have revenue streams resulting from activities not related to the sale of insurance. For example, if the Agency owns their office building, they may have rental income.

Expenses are categorized into four categories: Payroll & Benefits, Selling Expenses, Operating Expenses, and Administration Expenses:

Payroll: This category should contain any wages, commissions, salaries, and bonuses paid to the Agency’s owners/employees andany amounts paid to 1099 Employees (outside contractors). It should notcontain any dividends paid to shareholders, which are considered administrative expenses.

Benefits: This category contains any expenses associated with employee benefits. It can include items such as retirement plans, employee insurance, and the employer portion of payroll tax expense (This does not include employee withholdings, which should notappear on the income statement.)

SellingExpenses: Selling expenses are expenses that result from efforts to make sales or retain customers. The most common categories in this section include marketing, promotions, advertising, travel, meals, and automobile expenses. It should not include expenses that are necessary for the day-to-day operations of the Agency. For example, although an office renovation may increase

How to build a strong budget for your agency page two 18 www.viaa.org

sales by improving customer experience, the main result of the renovation is not increased sales but providing a safe and effective work environment. A customer referral program, by contrast, increases sales directly. For this reason, the entertainment, meals, travel, and automobile expenses that should appear in this section are expenses directly associated with sales activities, not personal meals, travel, or vehicles.

OperatingExpenses: Operating expenses are expenses incurred to ensure that the Agency can continue to operate effectively. Some common expenses included in this category include, rent, utilities, technology, licenses, business insurance, and professional services. For example, telephones are necessary in order to ensure that the Agency is able to contact clients, potential clients, and carriers. Therefore, telephone expenses can be considered operating expenses. However, personal cell phones should not be included in this expense if they are not used for business purposes (similar to automobile expenses, discussed above).

Administration Expenses: Administration expenses are expenses that cannot be directly attributed to the operation of the agency. For example, Officer Life Insurance (also known as Key-Person life insurance) is included in this category because this expense is not a result of the Agency’s efforts to sell insurance and is not necessary to maintain the day-to-day operations of the Agency. It also includes expenses like Depreciation, Amortization, Interest Expense, and Shareholder Distributions. In calculating EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), many (if not all) administrative income and expenses are removed or added back in that calculation.

#2: ProjectingtheFuture

When budgeting for any business, it is important to estimate any increases/decreases in expenses, capture new expenditures that are

expected in order to accomplish your stated goals as well as the estimated increases or decreased in revenue.

Typically, agency revenue cannot increase without agency expenses increasing as well. For example, your business plan for next yearmight be to increase Agency Commissions by 10%, but how are you going to achieve this goal? You will need to consider what amount of your current book of business you expect to retain. Remove any accounts that will not renew,like bonds for example. In addition, apply a reasonable assumption for your retention rate based on past performance. Then plan out how you will achieve that goal, for instance, you might need to hire a new producer, start alocal ad campaign, or invest in a tool or technology to help create capacity on your team. When planning for revenue goals, keep in mindthat revenue can also change due to circumstances like economic conditions, but these changesare harder to predict.

Changing circumstances can affect multiple parts of the income statement. For example, ifa producer is retiring, this will decrease next year’s compensation expenses, but it will also decrease next year’s revenue. When making an adjustment to revenues or expenses, remember to consider how this circumstance may affect other parts of the income statement.

Sometimes the effects of changing circumstances can be hard to predict, such as the effects of local economic conditions. For example, if a large company opens up a new manufacturing facility in your area, it will likely improve the local economy, but it is hardto calculate the effect it will have on your Agency. In creating a budget for your Agency, it is better to only include increases in revenue whenyou can easily estimate them and when they have a fairly high likelihood of occurring.

Remember: Your Agency’s expected revenue will set the “tone” for your Agency’s expected expenses. Overestimating future revenue may result in overspending if you are not cautious.

to

page three www.viaa.org 19

How

build a strong budget for your agency

How to build a strong budget for your agency

#3:Use ReputableInformationSources

Ideally, estimates for specific expenses should draw on real data.

One method for estimating your future expenses is to obtain estimates directly from the business(es) you are expecting to purchase goods/services from. For example, the price of a new Agency Management Software can usually be obtained by either going to their website or by contacting the manufacturer directly. This is the ideal method for estimating expenses because it reflects the cost of the item right now.

Occasionally, a new expense may not have a “market price”, or the market price may be difficult or impossible to obtain. For example, you may be expecting to add a new producer, but are not sure how much you will have to pay them in their first year, and furthermore, you are not sure how it will affect your revenue. The best option in this case is to look at past data and use it as a benchmark. Historically, how much have you paid producers in their first year on average? How much revenue have new producers generated in their first year on average?

Once you have built your budget, be sure to share the goals and measurement metrics with your team. One of the benefits to establishing a budget is determining the key performance metrics that you can use to assess your overall and individual performance across the team. By mapping out the year, you can have welldefined metrics that you can use as a gauge all throughout the year. This oversight and management will allow you to adjust or pivot if something unexpected occurs or if a new opportunity arises.

Use our freebudgetingtemplate!

AgencyFocus has created a budgeting spreadsheet that can be used to start developing a budget for your agency.

This article was provided by AgencyFocus, LLC. To reach them, call (614)657-2674 or email carey@agency-focus.com

page

four

20 www.viaa.org

www.viaa.org 23

Agency Management

WHY COMPLIANCE HOLDS THE KEY TO INCREASING PROFITS

ByAllisterYu

As the regulatory landscape in the insurance industry continues to grow in complexity, compliance remains critical. Meanwhile, insurance is undergoing a digital revolution with producers leveraging new technologies to cut costs and grow sales.

Routinely overlooked, compliance is an area ripe for innovation. While it has often been considered a costly and tedious—but necessary—issue, compliance can offer valuable opportunities to increase profitability.

In 2023, the industry must innovate its compliance management processes to maintain and increase its competitive advantage. Here are three key trends they should utilize:

1)Theartofautomation. Nonresident insurance licenses now account for three times the volume of state resident licenses, according to the National Association of Insurance Commissioners (NAIC). With agents drastically increasing the number of active nonresident licenses they hold, the challenge of being compliant in multiple states has led to agencies and carriers facing tens of thousands of dollars in fines every year.

For many, compliance used to be as simple as a sticky note reminder on their desk. Now it can be an automated process that begins at onboarding and lasts throughout their entire career. Hosted on the cloud and fully integrated into their organization's other management systems, modern compliance is

www.viaa.org 25

Why Compliance Holds the Key to Increasing Profits

empowered by artificial intelligence (AI) and machine learning to increase productivity by automatically delivering notifications and managing workflow.

For example, appointment data holds sensitive personal information, so producers must ensure that this data has the proper safeguards and cannot be compromised. Also, application programming interfaces (APIs) have been adopted so that compliance data can be imported and exported to other platforms, such as an agency's HR system.

These innovations reduce the time employees will spend on tedious administrative tasks, giving them more time to focus on sales and gain a competitive edge over their peers.

2)Thecasefordataanalytics. Insurance is recognizing the potential to leverage compliance data for strategic insights. Agencies can now analyze years of archived compliance data to track day-to-day activities and build metrics around fundamental questions such as, “Which producers are generating the most business for us?" “Who do we quote the most business with?" and “Which salesperson is the most productive?"

With these questions answered, agencies can make strategic business decisions that are powered by real-time data and insights.

3)“Just-in-time"appointments. As the total number of licensed producers has increased, carriers also face an avalanche of appointing filing fees and administrative tasks. Many carriers appoint agents even though they likely have a significant percentage of agents who will never generate any business for them. Thus, they have increasingly turned to “just-in-time" appointments (JITs).

JITs allow carriers to wait on fully executing an appointment until the agent has written business in the state. This allows them to

have proof that an agent can generate revenue before having to file any paperwork or pay any fees.

However, the deadlines for a JIT can be tight. In most states, carriers have anywhere between 14 to 45 days to file after their agent has submitted their first piece of business. Carriers will need to have the proper compliance management tools and processes in place to take full advantage of the benefits that JITs provide.

Proper compliance management is proving to be much more than a mundane back-office function, and a real key to profitability. New solutions powered by technology such as AI, cloud computing, APIs, and data analytics are increasingly changing the way compliance departments operate, giving them strategic advantages.

The insurance industry can no longer overlook the importance of compliance and needs to embrace new compliance technology as the heartbeat of their organizations.

AllisterYuis the seniorvice presidentof operations atRhoadsOnline,aprovider of compliancemanagementsoftwareandservices forinsurancecarriers,agenciesandadjusters.

Reprintedwithpermission from IA Magazine

26 www.viaa.org

Continued

www.viaa.org 29

www.viaa.org 31

CORNER Comp Conundrum: Will Workers Comp Premiums and Claims Drop Under New Modes of Working?

ByCarynMahoney

In large numbers, those employees are saying, "No, thank you."

“Once the toothpaste is out of the tube, it’s tough to get back in,” H.R. Haldeman, White House chief of staff under the Nixon Administration, famously observed. Half a century later, employers are finding the truth in the expression as they struggle to get their employees—many of whom were sent home to telework during the COVID-19 pandemic— to return to the office. In large numbers, those employees are saying, “No, thank you.”

Before COVID-19, 23% of those with jobs that could be done from home were working from home all or most of the time, according to the Pew Research Center. As of October 2020 that percentage had risen to 71%. Nearly two years later, that percentage is still 59%.

Even those who have returned are, in many cases, now splitting their work time between the office and home. Despite their frustration, employers may be looking for a silver lining in these figures and wondering, “Does this mean I’ll get a fat reduction in my workers compensation premiums?”

To find the answer, let’s get back to basics.

All states except Texas have a requirement that employers must provide workers comp coverage if they have employees—subject to certain exceptions, which vary from state to state, such as businesses with less than a certain number of employees and independent contractors, for example. In Texas, an employer can choose whether or not to provide workers comp coverage for

their employees but noncovered employers must comply with certain workers comp requirements.

In any event, teleworkers who do not fall within any of the exceptions are not exempt from workers comp coverage. Therefore, subject to state-specific requirements, businesses with people working from home must provide workers comp coverage.

Even so, given that there are more teleworkers than in the past, how does that change the workers comp exposure? The 2021 State of the Line Guide published by the National Council on Compensation Insurance (NCCI) gives us clues.

NCCI estimates that the lost-time claim frequency for the 2020 accident year will be 7% lower than for the 2019 accident year. They concluded that pandemic-related shutdowns and increased use of telecommuting are likely contributors to the larger-than-average decline. They also expected that there would be a decrease in overall average claim severity. In addition, private non-fatal injury cases dropped from 2.7 million in 2019 to 2.1 million in 2020, representing a 22.22% decrease, according to the U.S. Bureau of Labor.

According to the NCCI, the types of occupations that lend themselves to teleworking tend to be office jobs, which also tend to have lower rates of work injuries and lower loss costs. Slips and falls are the leading cause of workers comp claims, according to the National Floor Safety Institute (NFSI).

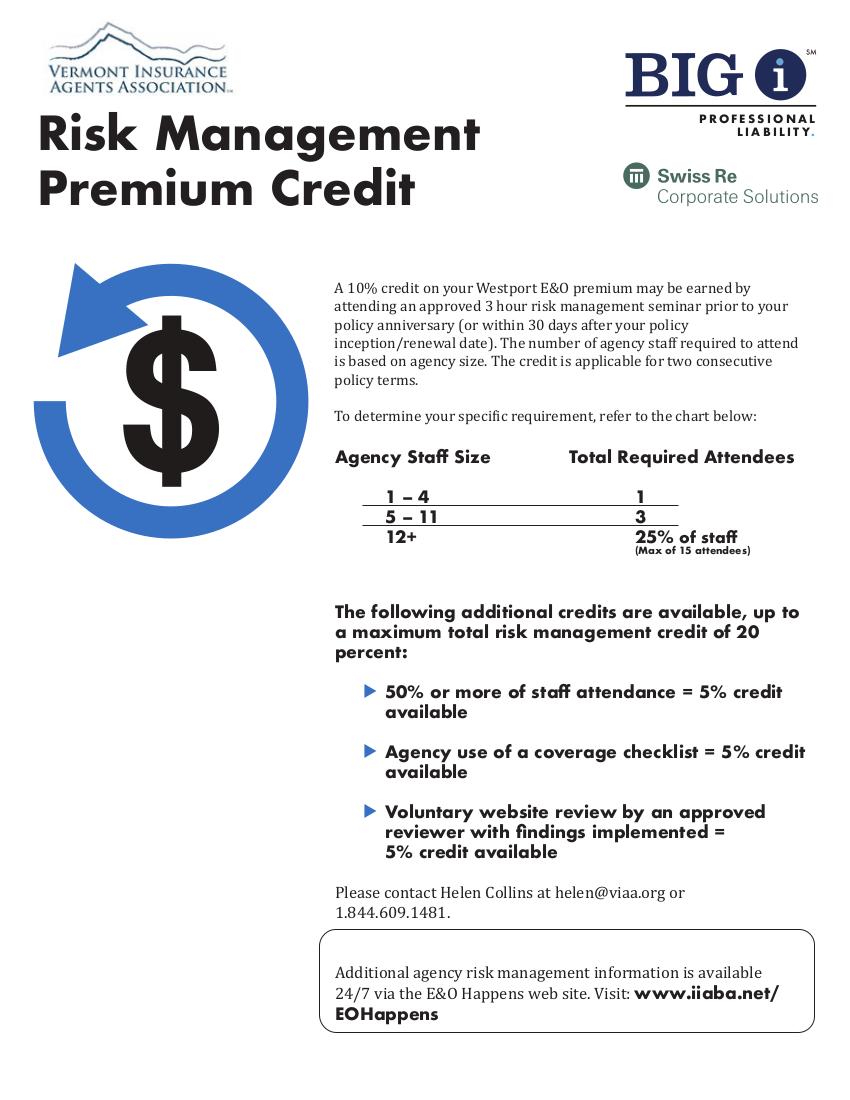

E&O

32 www.viaa.org

Comp Conundrum

However, just because the teleworker slips and falls at home doesn’t mean that their fall injuries won’t be covered by workers comp. Under the Occupational Safety and Health Act (OSHA), the employer is obligated to provide a safe work environment for their employee, whether or not that employee is working from their home.

However, different states may look at this obligation differently. In Florida, the case of Sedgwick CMS v. Valcourt-Williams considered whether an employee tripping over her dog was covered. The court decided not, since this risk existed whether she was at home working or whether she was at home not working and her employment did not expose her to conditions that substantially contributed to the risk of injury.

On the other hand, there have been other cases that have found that slips and falls when getting a cup of coffee or going to the bathroom are covered. This is known as the personal comfort doctrine. According to Karastmatis v. Industrial Comm’n in Illinois, “The personal comfort doctrine generally applies when a claimant is on break and sustains an injury. It encompasses acts such as eating and drinking, obtaining fresh air, seeking relief from heat or cold, showering, resting, and smoking.”

Given an employer’s relative lack of control over the home environment and ergonomic considerations that could lead to injuries and the blurred line between when the worker is tending to their personal comfort, will it lead to more claims?

Truthfully, most teleworkers probably aren’t even aware that they may have access to workers comp benefits for injuries that they suffer while working from home, so claims may increase once they gain this knowledge. But meanwhile, the telework employer’s diminished control as to when their employee is working and taking breaks may also increase the number of injuries, driving up workers comp claims from teleworkers.

The bottom line: It’s human nature to look for good news in the midst of bad. Unfortunately, the silver lining your customer is hoping for may not be found in their workers comp premiums.

Insurance products underwritten by Westport Insurance Corporation and Swiss Re Corporate Solutions America Insurance Corporation, Kansas City, Missouri, members of Swiss Re Corporate Solutions.

This article is intended to be used for general informational purposes only and is not to be relied upon or used for any particular purpose. Swiss Re shall not be held responsible in any way for, and specifically disclaims any liability arising out of or in any way connected to, reliance on or use of any of the information contained or referenced in this article. The information contained or referenced in this article is not intended to constitute and should not be considered legal, accounting or professional advice, nor shall it serve as a substitute for the recipient obtaining such advice. The views expressed in this article do not necessarily represent the views of the Swiss Re Group (“Swiss Re”) and/or its subsidiaries and/or management and/or shareholders.

Caryn Mahoney is an assistant vice president, claims specialist with Swiss Re Corporate Solutions.

continued

www.viaa.org 33

COMPANY & AGENCY NEWS 38 www.viaa.org

Hickok & Boardman HR Intelligence Announces Two New Hires – Jessica Miller and Rachel Ward

Jessica Miller joined Hickok & Boardman HR Intelligence as a Client Manager in November 2022. In her role, Jessica is supporting our valued large organization clients where she is working alongside Leadership, Account Leads, and Senior Client Managers to assist with client benefit needs. Prior to joining our HBHRIQ team, Jessica came from the Talent Acquisition and Recruitment Strategies Department at the University of Vermont Health Network. She actively recruited inpatient healthcare staff for 6 large organizations across Vermont and upstate New York for a year, contributing to her 5 years of administrative support and customer engagement experience.

Rachel Ward joined Hickok & Boardman HR Intelligence as a Client Manager in October 2022. In her new role with our organization, Rachel works within our Small Group Division. She works closely with members of her team, ranging from Executives, Sr. Client Managers, and Account Leads, by providing direct support to our valued clients, assisting them with all their benefit needs.

Vermont Mutual Donates $16,000 to Committee On Temporary Shelter

Vermont Mutual Insurance Group® donated a record $16,000 to the Committee On Temporary Shelter (COTS) as part of the Cats Win, Community Wins program, a multi-year, community-based, collaboration between Vermont Mutual Insurance Group and the University of Vermont. Since the program’s debut in 2017, Vermont Mutual has donated $80,000 to local non-profits through the Cats Win, Community Wins initiative and has awarded more than $3.5 million dollars through the Vermont Mutual Charitable Giving Fund since its inception in 2014.

The Cats Win, Community Wins initiative was created by Vermont Mutual and UVM Athletics as a way to give back to local charitable organizations. As part of the yearly program, for every win by a Catamount athletic team, Vermont Mutual will donate $100 to a designated charity. The Committee On Temporary Shelter (COTS) was selected to be the 2022 Cats Win, Community Wins recipient. This past year UVM athletics achieved 160 wins across all sports, which equates to a $16,000 donation to COTS from Vermont Mutual, a Cats Win, Community Wins record.

www.viaa.org 39