We are looking for business owners who like to join the

Manningham Network Group and Community Paper.

• Accounting Services

• Acupuncture

• Architect

• Architectural Interior Design

• Attorney- Family

• Auctions- Real Estate

• Bookkeeper

• Bowen Therapy

• Builder- Commercial

• Business Coach

• Business Equipment Financing

• Business Insurance

• Cabinets

• Caterer

• Graphic Designer

• Plasterer

• Chinese Medicine

• Chiropractor

• Creative Director

• Commercial Mortgage

• Computer Repair

• Computer Web Design

• Concrete

• Copywriting/Copy Editing

• Counselor/ Psychotherapist

• Dentist

• Digital Media

• Electrical Operations

• Electrician

• Finance Bookeeper

• Financial Planner

• Fitness Trainer

• Flooring

• Pilates

• Garage Doors

• General Insurance

• Health & Wellness Coach

• Homeopathy

• Lactation Consultant

• Lawn Care

• Lawyer

• Life Coach

• Loans

• Marketing

• Massage Therapist

• Meditation/Yoga

• Mortgage Broker

• Naturopathic Medicine

• Nutrition

• Osteopathy

• Painter

• Personal Trainer

• Photographer

• Plumber

• Podiatrist

• Printer

• Project Management

• Psychologist

• Real Estate Rentals

• Real Estate Sales

• Reiki

• Residential Cleaning

• Residential Mortgage

• Security

• Signs

• Solar

• Solicitor

• Travel Agent

• Website Developer

• Wedding Planner

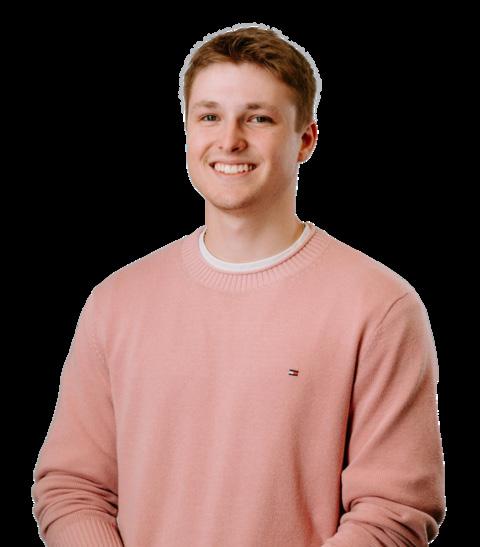

By Warren Strybosch

The Find Manningham is a community paper that aims to support all things Manningham. We want to provide a place where all Not-For-Profits (NFP), schools, sporting groups and other like organisations can share their news in one place. For instance, submitting up-andcoming events in the Find Manningham for Free.

We do not proclaim to be another newspaper and we will not be aiming to compete with other news outlets. You can obtain your news from other sources. We feel you get enough of this already. We will keep our news topics to a minimum and only provide what we feel is most relevant topics to you each month.

We invite local council and the current council members to participate by submitting information each month so as to keep us informed of any changes that may be of relevance to us, their local constituents.

EDITORIAL ENQUIRES: Warren Strybosch | 1300 88 38 30 warren@findnetwork.com.au

PUBLISHER: Issuu Pty Ltd

We will also try and showcase different organisations throughout the year so you, the reader, can learn more about what is on offer in your local area.

To help support the paper, we invite local business owners to sponsor the paper and in return we will provide exclusive advertising and opportunities to submit articles about their businesses. As a community we encourage you to support these businesses/columnists. Without their support, we would not be able to provide this community paper to you.

Lastly, we want to ask you, the local community, to support the fundraising initiatives that we will be developing

and rolling out over the coming years. Our aim is to help as many NFP and other like organisations to raise much needed funds to help them to keep operating. Our fundraising initiatives will never simply ask for money from you. We will also aim to provide something of worth to you before you part with your hard-earned money. The first initiative is the Find Cards and Find Coupons – similar to the Entertainment Book but cheaper and more localised. Any NFP and similar organisations e.g., schools, sporting clubs, can participate.

Follow us on facebook (https://www. facebook.com/findmanningham) so you keep up to date with what we are doing.

We value your support,

The Find Manningham Team.

POSTAL ADDRESS: 248 Wonga Road, Warranwood VIC 3134

ADVERTISING AND ACCOUNTS: editor@findmanningham.com.au

GENERAL ENQUIRIES: 1300 88 38 30

EMAIL SUPPORT: support@manningham.com.au

WEBSITE: www.findmanningham.com.au

The Find Manningham was established in 2019 and is owned by the Find Foundation, a Not-For-Profit organisation with a core focus of helping other Not-ForProfits, schools, clubs and other similar organisations in the local community - to bring everyone together in one place and to support each other. We provide the above organisations FREE advertising in the community paper to promote themselves as well as to make the community more aware of the services these organisations can offer. The Find Manningham has a strong editorial focus and is supported via local grants and financed predominantly by local business owners.

The City of Manningham is a local government area in Victoria, Australia in the north-eastern suburbs of Melbourne. Manningham had a population of approximately 125,508 as at the 2018 Report which includes 27,500 business and close to 45,355 households. The Doncaster and Templestowe Council administered the area until December 15, 1994.

The Find Manningham acknowledge the Traditional Owners of the lands where Manningham now stands, the Wurundjeri people of the Kulin nation, and pays respect to their Elders - past, present and emerging - and acknowledges the important role Aboriginal and Torres Strait Islander people continue to play within our community.

Readers are advised that the Find Manningham accepts no responsibility for financial, health or other claims published in advertising or in articles written in this newspaper. All comments are of a general nature and do not take into account your personal financial situation, health and/or wellbeing. We recommend you seek professional advice before acting on anything written herein.

By Joe Lam

Brisbane Lions surpass Geelong with a commanding performance in the Grand Final, securing consecutive Premierships.

On Saturday, September 27, 2025, the Brisbane Lions emphatically defeated the Geelong Cats in the AFL Grand Final by 47 points—18.14 (122) to 11.9 (75)—to claim back-to-back premierships. What had appeared a tight contest through the first half became a one-sided rout after half-time, as Brisbane’s experience, depth and willingness to gamble paid off. Here’s how the game went quarter by quarter, who stood above all others, and what went wrong for Geelong.

Geelong led 2.3 (15) to Brisbane's 1.6 (12) at quarter time. The second quarter was tight, ending in a 5.6 (36) tie, but Jeremy Cameron suffered a suspected fractured arm. Brisbane brought in Lachie Neale as a substitute at half-time. Brisbane kicked three quick goals to lead 9.9 (63) to 6.8 (44) at three-quarter time. In the final quarter, Brisbane dominated, scoring seven consecutive goals to win by 47 points, with Charlie Cameron kicking four majors.

By unanimous acclaim, Will Ashcroft claimed his second consecutive Norm Smith Medal, confirming his status as the game’s best. The 21-year-old midfielder produced a highimpact performance across all facets: high disposal numbers, clearances, involvement in thrusts into attack, and composure

under pressure. His influence steadily tilted the balance in Brisbane’s favour, especially after half-time.

Other Lions also starred: Harris Andrews ran an exceptional aerial defence display, intercepting at will and starving Geelong of options. Charlie Cameron returned to form with four goals. Hugh McCluggage also played a major part in ball movement and forward thrusts.

The Grand Final Drew over 4.076 million viewers. Will Ashcroft cemented his legacy as a multi-Norm Smith medalist and future face of the sport. With players like Dayne Zorko highlighting the Ashcroft brothers’ motivational impact. Conversely, Geelong faced fan frustration and speculation about a roster reset, needing younger talent to replace aging stars. Geelong is the 13th team since 2000 to lose a decider by 40+ points, with none immediately returning to a Grand Final the following year. Brisbane, with its balanced youth and experience, is predicted to dominate upcoming seasons.

In conclusion, what began as a close, hard-fought battle through two quarters became a one-sided statement by Brisbane. Geelong’s fate was sealed by misfortune, injury, and an inability to match the Lions’ firepower and composure after half-time. Brisbane now stands not just as champions, but as the benchmark in Australian football—and Geelong must rebuild confidence and structure if they hope to blunt a Lions juggernaut in seasons to come.

Sourced from: The Guardian, The Australian, ABC, Herald Sun, Australian Football League, Wikipedia.

By Warren Strybosch

If you were wondering if you should consider paying off that ATO debt, then the answer is a resounding yes!!

The Australian Taxation Office (ATO) has published the applicable interest rates for the final quarter of 2025, covering the period from 1 October to 31 December 2025. These rates apply across a number of circumstances where taxpayers either owe money to the ATO, have late or underpaid tax obligations, or are entitled to compensation where the ATO has delayed refunds.

For this period, the General Interest Charge (GIC) has been set at 10.61%. The GIC is the rate most commonly applied when a taxpayer has an outstanding tax debt. This charge accrues daily on the amount owing until the balance is paid. Its purpose is twofold: firstly, to encourage timely payment of tax obligations; and secondly, to ensure that taxpayers who pay on time are not disadvantaged compared with those who delay. At 10.61%, the GIC remains relatively high, reflecting both market interest rate movements and the ATO’s policy of applying a premium to encourage prompt payment. Taxpayers with outstanding debts should be mindful of how quickly such charges compound and may wish to consider negotiating a payment plan with the ATO to avoid further escalation.

For business owners, this rate also raises important considerations around debt management. Many businesses that fall behind on tax obligations may find that the GIC quickly becomes more expensive than traditional financing options. In some circumstances, refinancing the debt through a commercial loan—or even a secured facility such as using the family home as collateral—can significantly reduce the effective interest cost. For example, a business loan or mortgage-backed facility might attract an interest rate of 6–8%, far below the ATO’s 10.61% rate. However, this approach is not without risks. Using the home as security can place personal assets on the line, which requires careful assessment of the business’s cash flow and repayment capacity. Business owners should weigh the potential savings against the increased exposure and ideally seek professional advice before restructuring debt in this way.

The ATO has also set the Shortfall Interest Charge (SIC) at 6.61% for the same quarter. The SIC applies in situations where an amended assessment reveals

Owing the ATO money just got more expensive - GIC and SIC rates for

that a taxpayer has underpaid their tax, often because of an error or omission in their original return. Unlike the GIC, the SIC is generally lower because it is not designed as a penalty but rather as compensation to the government for the time value of money lost due to the shortfall. It also recognises that shortfalls may arise without deliberate intent. Importantly, the SIC accrues from the date the tax should have been paid until the date the liability is corrected. While lower than the GIC, at 6.61% the SIC is still significant enough to reinforce the importance of accuracy and completeness in tax reporting.

On the other side of the ledger, the ATO has announced that the interest rate on overpayments and delayed refunds will be 3.61%. This rate applies when a taxpayer has overpaid their tax or when the ATO takes longer than the statutory timeframes to issue a refund. While the rate is considerably lower than the GIC, it provides taxpayers with a measure of fairness by compensating them for funds held by the ATO beyond the time required. This mechanism helps maintain confidence in the system by ensuring taxpayers are not unduly disadvantaged when excess payments are tied up within the tax administration process.

The disparity between the GIC and SIC rates compared with the overpayment and delayed refund interest rate highlights an intentional asymmetry in the system. The ATO deliberately sets higher rates on taxpayer liabilities to encourage compliance and deter late payments, while applying more conservative rates to refunds to limit the fiscal impact on government revenue.

This structure underscores the principle that timely compliance is rewarded, while delays in meeting obligations attract a financial cost.

In summary, for the period 1 October to 31 December 2025, the GIC is 10.61%, the SIC is 6.61%, and the overpayment/delayed refund rate is 3.61%. Taxpayers should remain attentive to their lodgement and payment obligations, not only to avoid the steep impact of interest charges but also to ensure efficient cash flow management in their dealings with the ATO.

You can call them on 1300 88 38 30 or email info@findaccountant.com.au / www.findaccountant.com.au

This information is of a general nature only. It does not take into account your particular financial needs, circumstances and objectives. You should obtain professional financial advice if you have not already done so before acting on this information. You should read the Product Disclosure Statement (PDS) before making a decision to buy or sell a financial product. Any case studies,graphs or examples are for illustrative purposes only and are based on specific assumptions and calculations.Past performance is not an indication of future performance. Superannuation, tax, Centrelink and other relevant information is current as at the date of this document. This information contained does not constitute legal or tax advice.

By Jodie Moore

Pricing a product or service is one of the most critical decisions a business owner must make. Charge too much, and you risk scaring away potential customers. Charge too little, and you might not cover your costs or earn the profit you need to sustain and grow your business.

Here’s a step-by-step guide to help you understand how to determine the right price for your product or service using smart pricing strategies.

The first step in pricing is understanding all of the costs involved in delivering your product or service. These costs typically break down into two categories:

• Fixed Costs: These are costs that remain constant, regardless of how much you produce or sell. They include things like rent, utilities, software subscriptions, and salaried employees.

• Variable Costs: These fluctuate depending on how much you produce or sell. Materials, hourly wages, packaging, and shipping costs all fall under this category.

Once you’ve calculated both fixed and variable costs, you can figure out your break-even point—the minimum number of sales you need to cover both types of costs. This is crucial, as it ensures that your pricing will at least allow you to avoid losses.

Next, you’ll want to research the market. Understanding what your competitors charge is an essential part of the pricing strategy. However, just copying your competitors isn’t always the best approach. Look at:

• Direct Competitors: These are businesses offering similar products or services. What price range do they offer, and how does your product compare in terms of quality and features?

• Indirect Competitors: These may not be offering exactly what you do,

but they still capture your potential customers’ attention. For example, a local bakery might compete with a coffee shop that offers prepackaged pastries.

• Customer Expectations: What do your customers value most? Are they looking for premium quality, or are they more focused on affordability? This can help you position your price in a way that aligns with what your target market expects.

One of the biggest mistakes small business owners make is not accounting for the profit margin. After covering all your costs, you need to ensure that you’re making a profit. Profit margin is typically calculated as a percentage of the cost of goods sold (COGS). A common rule of thumb for small businesses is to target a profit margin between 10% and 20%, though this can vary depending on the industry. For instance, if your total cost per product is $50, and you want a 20% profit margin, you would add $10 to the cost (for a total price of $60). This ensures that your pricing strategy not only covers costs but also allows for sustainable growth.

Psychological pricing can have a powerful impact on your sales. For instance, pricing something at $99.99 instead of $100 can trigger a perception of a better deal, even though the difference is just one cent.

In addition to this “charm pricing,” consider tiered pricing strategies, bundling, or offering discounts for bulk purchases. Offering multiple price points or subscription-based pricing can also appeal to different customer segments and encourage repeat business.

Even with all the research and calculations in place, pricing is not a one-time decision. Over time, customer behaviour, market conditions, and your business costs can change. That’s why it’s important to test your pricing strategy. You might try offering a new product at a slightly higher price to see how customers respond or provide limitedtime discounts to see if they increase sales volume.

By tracking your sales data and monitoring customer feedback, you’ll be able to adjust your pricing strategy as needed, ensuring long-term profitability.

Pricing is both an art and a science. By carefully calculating costs,understanding market conditions, factoring in profit margins, and considering psychological pricing techniques, you can find a price point that supports your financial goals. In the end, the right price isn’t just about what customers are willing to pay—it’s about creating a balanced strategy that ensures your business can thrive in both the short and long term.

By Ethan Strybosch

What if your next fundraising campaign didn’t just meet expectations—but shattered them?

If you’re aiming to boost donations, expand your reach, or build lasting donor relationships, it’s not about working harder—it’s about working smarter.

These five powerful campaigns aren’t just ideas—they’re proven strategies that inspire action and deliver real, measurable results.

Peer-to-Peer Fundraising: Empower your Supporters

Peer-to-peer (P2P) fundraising isn’t just a trend—it’s one of the most effective ways to organically grow your NFP’s donor base. It empowers your supporters to fundraise on your behalf as individuals reach out to friends, family and colleagues, tapping into personal networks to spread your non-for-profit’s message. 92% of people trust recommendations from friends and family over any other form of advertising (Nielsen), making P2P fundraising a fantastic avenue for successful NFP campaigns. Plus, peerto-peer campaigns typically raise twice as much as traditional fundraising efforts because they reach wider audiences.

The key to success is equipping your fundraisers with the right tools, such as social media templates, email scripts, and easy-to-use donation pages, to make the process accessible and enjoyable. Recognising top fundraisers with shoutouts or small rewards can also keep motivation high.

“Movember’s global campaign is a great example,raising over $1 billion worldwide by turning personal stories into powerful fundraising tools. The combination of humour, personal connection,andglobalparticipation makes it one of the most effective peer-to-peer campaigns ever.”

Seasonal giving campaigns align with key dates like Giving Tuesday, EOFY appeals, and the holiday season are times when people are naturally more inclined to give. Giving Tuesday alone raised over $3.1 billion in the U.S. in 2022, and 30% of all annual donations happen in December, with 10% occurring in the final three days of the year. By leaning into seasonal giving campaigns, your NFP can use these giving trends to increase fundraising throughout the year.

Creating urgency through countdowns, limited-time donation matches, or highlighting specific goals can significantly boost results.

Success Story:

The Salvation Army’s Red Kettle Campaignisaseasonalstaple,raising over $100 million annually during the holidays through both physical donation kettles and online giving platforms. Its recognisable branding and community engagement make it a model for successful seasonal giving.

As we discussed in our January Newsletter, social media is a powerful tool for non-profits, especially when it’s used to tell compelling stories. Story-driven campaigns can humanise your NFP’s cause which in turn creates emotional connections that inspire action. Focusing on real people and authentic stories that reflect the heart of your non-forprofit’s mission engages audiences. Short, emotional videos perform extremely well on social media such as TikTok, Instagram, and Facebook. You can further engagement with your fundraising campaign by encouraging followers to share their own stories and use dedicated hashtags to spread your NFP’s reach.

Success Story:

“Charity:Water’s#WhyWatercampaign is a perfect example, using personal stories from communities impacted by clean water projects to create a global movement that has helped over 15 million people. Their simple, powerful storytelling approach turns donors into passionate advocates.”

While one-time donations are important, recurring giving campaigns create a steady, reliable stream of income. Over one year, monthly donors give 42% more than one-time donors and have a retention rate of 90%, compared to 46% for one-time contributors.

Highlighting the convenience and longterm impact of monthly donations can turn casual supporters into lifelong advocates of your non-for-profit. Offering exclusive updates or behind-the-scenes content on projects occurring within your NFP helps keep these donors engaged.

Success Story:

World Vision’s Child Sponsorship Program is a shining example of a successful recurring giving campaign. Donors receive regular updates, photos, and personal stories about the child they’re sponsoring, creating an emotional connection that fosters long-term support—often lasting for years.

Event-Based Fundraising: Create Memorable Experiences

Events, whether in-person or virtual, are another fantastic way to raise funds for your NFP and strengthen community ties. Fundraising events can account for up to 35% of annual donations for many organisations, including NFP’s and 84% of attendees say they’re more likely to donate after participating. The rise of virtual events has expanded reach even further, increasing participation by 30% in many cases.

Combining ticket sales with activities like raffles, auctions, or donation challenges for projects or a mission in your NFP can maximise revenue while fostering a sense of belonging among supporters.

Success Story:

The Global Citizen Festival blends entertainment with activism, attracting millions of participants worldwide. By leveraging celebrity influence, live music, and powerful advocacy messages, it drives not just donations but also policy changes and global awareness for critical causes.

Key Takeaways for Campaign Success in Your Non-for-profit

• Personal Connections Matter: Authentic, emotional stories resonate more than generic appeals.

• Urgency Drives Action: Campaigns with time-sensitive goals or donation matches perform better.

• Diversify Your Channels: Combine email, social media, events, and paid ads for maximum reach.

• Consistency Builds Trust: Regular communication with your audience keeps your cause top of mind and strengthens donor relationships over time.

Ready to Elevate Your Next Fundraising Campaign?

If you’re looking to launch campaigns that drive donations and build lasting donor relationships, we’re here to help.

By Erryn Langley

As they age, many Australians begin reassessing their retirement lifestyle. One option that often comes up is downsizing the family home in order to reduce costs, freeing up equity and simplifying life. Beyond lifestyle benefits, there’s a valuable financial planning strategy that could help strengthen your retirement income: downsizer contributions to super

If you're aged 55 or over, you may be eligible to contribute up to $300,000 per person (or $600,000 per couple) into your superannuation from the proceeds of selling your home. This contribution doesn’t count toward your standard contribution caps and doesn’t require you to meet the work test.

Key Eligibility Criteria:

• You must be 55 years or older at the time of making the contribution.

• The property must have been owned by you or your spouse for at least 10 years, and it must be your main residence.

• You only have 90 days from the date of settlement to make your downsizer contribution into super. Missing this deadline may mean you lose the opportunity entirely.

• You must submit the ATO downsizer contribution form before or when the contribution is made.

Why Consider It?

• Boost Retirement Savings: It’s a one-off opportunity to significantly grow your super balance, especially if you’ve reached other contribution limits.

• Tax-Effective Income: Once contributed, the funds can be used to start a tax-free income stream via an accountbased pension.

• Downsizer contributions do count towards the transfer balance cap (currently $1.9 million).

• Selling your home may affect your Age Pension entitlements due to the asset and income tests. You cannot use this rule multiple times, it’s a once-per-lifetime strategy.

• Don’t miss the 90 day window.

As you can see timing and making sure that you meet the requirements is critical, if you are considering downsizing, before you do so is a great time to speak with a Financial Adviser. Feel free to give us a call on 1300 557 144 to make an appointment to discuss how the use of a downsizer contribution could assist your overall retirement strategy.

Director and Financial Adviser - GradDipFinPlan

Authorised Representative No 1269525

T:1300 557 144 Email: erryn@cherrywealth.com.au

Website: www.cherrywealth.com.au

Office Address: Suite 4 / 4 - 6 Croydon Road, Croydon 3136

Postal Address: PO Box 657, Croydon VIC 3136

Financial Planning is offered via Cherry Wealth Pty Ltd Ltd ABN 14 653 375 458

Cherry Wealth is a Corporate Authorised Representative (No. 1314769) of Alliance Wealth Pty Ltd ABN 93 161 647 007 (AFSL No. 449221). Part of the Centrepoint Alliance group https://www.centrepointalliance.com.au/

Erryn Langley is Authorised representative (No. 1269525) of Alliance Wealth Pty Ltd.

This information has been provided as general advice. We may not have considered your financial circumstances, need or objectives. You should consider the appropriateness of the advice.You should obtain and consider the Product Disclosure Statement (PDS) and seek assistance from an authorised financial adviser before making any decisions regarding any products or strategies mentioned in this communication.

Whilst all care has been taken in the preparation of this material. It is based on our understanding of current regulatory requirements and laws as at the publication dates. As these laws are subject to change you should talk to an authorisedadviserforthemostuptodateinformation.Nowarrantyisgivenin respect of the information provided and accordingly neither Alliance Wealth nor its related entities,employees or representatives accepts responsibility for any loss suffered by any person arising from reliance on this information.

By Warren Strybosch

In last month’s article we discussed the RAD and DAP. This month we think it is important to discuss the Basic Daily Care Fee. We will explore what the Basic Daily Care Fee covers, how it is calculated, how it is paid, and what Australians need to know when planning for this cost.

Moving into residential aged care is a significant life transition for many older Australians and their families. Alongside the emotional considerations of leaving a long-term home, financial planning becomes a crucial part of the process. One of the most important components of residential aged care costs is the Basic Daily Care Fee. This fee applies to all residents, regardless of their financial position, and is designed to contribute to the everyday living costs within aged care facilities.

Everyone pays a Basic Daily Care Fee. This fee helps pay for a resident’s share of day-to-day services such as:

• Meals and nutrition

• Cleaning and laundry services

• Facilities management and utilities (heating, cooling, water, and electricity)

• Basic furnishings and maintenance of communal spaces

Importantly, this fee applies for every day you are a resident, even on days you may be away overnight—for example, if you go on holiday or spend time in hospital.

The Basic Daily Care Fee is set at 85% of the single person rate of the basic Age Pension. The federal government updates the fee on 20 March and 20 September each year in line with pension increases, ensuring it rises with the cost of living. Prices are published on the Department of Health, Aged Care and Disability website for transparency.

Based on current rates, the maximum Basic Daily Care Fee is $63.82 per day, or $23,294.30 per year. While this figure changes periodically, it provides a clear indication of the cost families need to plan for when moving into aged care.

Residents pay the Basic Daily Care Fee directly to their aged care home, usually on a fortnightly or monthly basis. For many pensioners, the fee is deducted from their Age Pension, making

the process straightforward. For others, it may be funded through private income streams such as superannuation pensions, annuities, or investment income.

This regular payment structure ensures aged care facilities receive consistent contributions to help cover the ongoing costs of providing everyday services.

Every resident in government-subsidised aged care pays the Basic Daily Care Fee. This applies regardless of whether a person is a full or part pensioner, or whether they are self-funded retirees with significant assets. The universality of the fee reflects its role in ensuring fairness and shared responsibility for basic living costs in residential aged care.

Purpose of the Fee

The Basic Daily Care Fee serves several important purposes:

1. Shared Responsibility: It ensures all residents contribute to their daily living expenses, just as they would if living independently.

2. Government Sustainability: By asking residents to cover basic living costs, government subsidies can be directed toward clinical care and accommodation support.

3. Predictability: Because it is universally applied and updated twice yearly, families can plan ahead with greater financial certainty.

The Basic Daily Care Fee is only one part of the overall cost structure of residential aged care. Other potential costs include:

• Accommodation Payments: Such as the Refundable Accommodation Deposit (RAD) or Daily Accommodation Payment (DAP).

• Means-Tested Care Fee: An additional charge based on assessed income and assets.

• Additional Services Fees: Optional charges for lifestyle or premium services beyond the standard package.

Together, these components form the complete financial picture of aged care, with the Basic Daily Care Fee acting as the essential foundation.

Given that the Basic Daily Care Fee is ongoing, unavoidable, and payable every day of residency, it is vital to factor it into long-term financial planning. Key considerations include:

1. Cash Flow Management: Ensuring regular income sources can cover the $63.82 daily fee without exhausting savings too quickly.

2. Pension Interaction: For Age Pension recipients, the link between the fee and the pension ensures affordability and indexing over time.

3. Budgeting for Increases: Families should expect adjustments twice yearly in line with pension changes.

4. Asset consideration and Protection: If and when to sell the home and what to do with the proceeds to ensure the Power of Attorney and other family members interests are protected.

Professional financial advice can help structure income streams and asset management to comfortably meet this regular obligation.

Many families misunderstand the Basic Daily Care Fee, especially when comparing facilities. Common misconceptions include:

• “The fee covers everything.” In fact, it only covers daily living expenses, not nursing or clinical care.

• “Wealthy residents don’t pay.” Every resident pays the fee, regardless of financial position.

• “It can be waived.” The fee is set nationally and cannot be negotiated by individual facilities.

The Basic Daily Care Fee is a cornerstone of Australia’s aged care funding model. At $63.82 per day, or just over $23,000 annually, it represents a resident’s contribution toward meals, cleaning, laundry, utilities, and other daily living services. Paid directly to aged care homes on a regular basis, and applying every single day of residency, the fee ensures fairness, sustainability, and predictability across the aged care sector.

By understanding how the fee is calculated, when it applies, and how it interacts with other aged care costs, Australians and their families can plan more effectively for the financial realities of residential aged care. Careful planning not only helps to meet the cost with confidence but also allows families to focus on what truly matters—the quality of care and support their loved one receives in this important stage of life.

Financial Planning, SMSF, Super, Insurance, Pre-Retirement & Retirement Planning (Financial Planning) are offered via Find Wealth Pty Ltd ACN 140 585 075 t/a Find Wealth, Find Insurance and Find Retirement. Find Wealth Pty Ltd is a Corporate Authorised Representative (No 468091) of Alliance Wealth Pty Ltd ABN 93 161 647 007 (AFSL No. 449221). Part of the

Centrepoint Alliance group (www.centrepointalliance.com.au/fsg/aw).

Warren Strybosch

Authorised Representative (No. 468091) of Alliance Wealth Pty Ltd.

This information has been provided as general advice. We have not considered your financial circumstances, needs or objectives. You should consider the appropriateness of the advice.You should obtain and consider the relevant Product Disclosure Statement (PDS) and seek the assistance of an authorised financial adviser before making any decision regarding any products or strategies mentioned in this communication.

Whilst all care has been taken in the preparation of this material, it is based on our understanding of current regulatory requirements and laws at the publication date. As these laws are subject to change you should talk to an authorised adviser for the most up-to-date information. No warranty is given in respect of the information provided and accordingly neither Alliance Wealth nor its related entities, employees or representatives accepts responsibility for any loss suffered by any person arising from reliance on this information.

By Warren Strybosch

When I meet with a new retiree client for the first time, we go through a Client World Map meeting. The meeting helps me to better understand their financial situation, but it also gives me an opportunity to understand what their future goals and interests are.

Retirement is more than an end to working life—it’s the beginning of a new chapter filled with freedom, purpose, and the opportunity to enjoy long-awaited goals. Whether your post-work dreams include extended travel, picking up new hobbies, or simply savouring quiet moments with loved ones, weaving these aspirations into your retirement modelling is crucial for achieving the lifestyle you desire.

Retirement is the perfect time to pursue passions put on hold: a grand tour of Europe, finally writing that novel, volunteering abroad, or learning to paint. These aren’t just activities; they’re the experiences that bring meaning and joy. Without incorporating such personal goals into financial planning, retirees risk underfunding their aspirations—or worse, compromising on them entirely.

I personally have several ‘bucket list’ items I wish to achieve in life, and these may happen in retirement. One is to go to the Superbowl, and another is to write children’s books. Also, I want to see if I can get Wallballs off the ground...that was for you Tim (if by chance you ever happen to read this article –sorry people, that was in reference to a long standing in joke between me and a friend of mine).

The Association of Superannuation Funds of Australia (ASFA) Retirement Standard provides a trusted benchmark of what retirement costs look like in Australia. For a comfortable lifestyle—one that includes private health insurance, a reliable car, dining out, domestic vacations, and even occasional international trips—ASFA estimates annual expenses of around $73,077 for couples and $51,805 for singles. To fund that lifestyle, a retiree would typically need a superannuation balance of about $690,000 for a couple or $595,000 for a single person (ASFA, 2023).

These figures are invaluable—but they reflect a generalized view of comfortable living. True contentment often lies in the bespoke: the trip of a lifetime, pursuing creative fulfilment, or simply more meaningful moments. That’s why your own goals should sit at the heart of retirement modelling.

Start by identifying your key goals: travel plans, lifestyle habits, family support, or bucket-list adventures. Estimate the costs, then compare them to the ASFA benchmarks. For instance, adding an annual trip overseas may stretch your budget beyond ASFA’s comfortable baseline—but aligning your super, pension, and savings to account for that ensures you don't have to compromise experiences for safety.

Moreover, retiree spending tends to decrease over time—but the early years can be the most vibrant, and expensive—as retirees tend to prioritise lifestyle while they’re fitter and more mobile. Factoring in timing can help you balance spending and longevity, so you enjoy life now without risking your financial future.

True retirement planning isn’t one-size-fits-all. It should start with:

• Clarifying personal goals—what matters most to you. We do this in our Client World Map meetings.

• Mapping costs—compare these to ASFA’s modest and comfortable budgets.

• Adjusting strategies—ensure your savings and income sources can fund both essentials and dreams. We provide several retirement modelling scenarios for clients to consider before the leap into retirement. This helps clients have peace of mind that they can afford their goals in retirement and not run out of money.

• Timing considerations—some goals are time-sensitive; others can wait.

Financial advisers often note that many retirees are overly cautious, underspending and leaving unused wealth behind. Your money should serve you—helping you live richly, not just last securely. We believe in leaving the house to the kids but everything else is yours to spend.

Retirement is ultimately about freedom—the freedom to enjoy life and fulfill dreams. By incorporating personal goals into your financial modelling—and comparing them with trusted benchmarks like the ASFA Retirement Standard—you ensure your retirement isn’t merely “comfortable,” but deeply meaningful. Savour the journey, embrace your bucket list, and live the retirement you’ve earned.

If you are not sure whether or not you will be able to afford your goals in retirement, then consider booking an initial FREE retirement meeting with Warren Strybosch, an award winning financial advisor and speaker, who can help you Find Retirement (www.findretirement.com.au) with ease.

Warren Strybosch

Award winning Financial Adviser and Accountant

Part of the Find Group of Companies

Financial Planning, SMSF, Super, Insurance, Pre-Retirement & Retirement Planning (Financial Planning) are offered via Find Wealth Pty Ltd ACN 140 585 075 t/a Find Wealth, Find Insurance and Find Retirement. Find Wealth Pty Ltd is a Corporate Authorised Representative (No 468091) of Alliance Wealth Pty Ltd ABN 93 161 647 007 (AFSL No. 449221). Part of the

Centrepoint Alliance group (www.centrepointalliance.com.au/fsg/aw).

Warren Strybosch

Authorised Representative (No. 468091) of Alliance Wealth Pty Ltd.

This information has been provided as general advice. We have not considered your financial circumstances, needs or objectives. You should consider the appropriateness of the advice.You should obtain and consider the relevant Product Disclosure Statement (PDS) and seek the assistance of an authorised financial adviser before making any decision regarding any products or strategies mentioned in this communication.

Whilst all care has been taken in the preparation of this material, it is based on our understanding of current regulatory requirements and laws at the publication date. As these laws are subject to change you should talk to an authorised adviser for the most up-to-date information. No warranty is given in respect of the information provided and accordingly neither Alliance Wealth nor its related entities, employees or representatives accepts responsibility for any loss suffered by any person arising from reliance on this information.

This fun and gentle exercise group explores local walking paths and tracks. Come along, explore the neighbourhood and make new friends.

Tuesday mornings from 9:30am to 11:30am unless otherwise specified.

Tuesday, 14 October 2025

9.30 to 11.30 am

Tuesday, 21 October 2025

9.30 to 11.30 am

Tuesday, 28 October 2025

9.30 to 11.30 am

1/284 Thompsons Road, Templestowe Lower

$3.00

Contact Information

Name: Ajani Neighbourhood House

Phone: 03 9850 3687

Website: https://www.ajaninh.org.au/

Manningham Council is inviting community feedback as it develops a new masterplan for Timber Reserve in Doncaster.

Manningham Mayor Cr Deirdre Diamante, who is the Councillor for Tullamore Ward, encouraged residents and reserve visitors to get involved.

“We want to hear how you use Timber Reserve and your ideas for how we can make it even better,” Cr Diamante said.

“The 4.6ha reserve is a much-loved space for formal and informal sport and recreation including soccer, cricket, walking,

Community members are invited to share their feedback on Manningham Council’s draft Domestic Animal Management Plan (DAMP) 2026-2029.

Manningham Council received more than 1,800 responses during the initial consultation in June. Feedback highlighted several key themes, including more education, stronger enforcement, improved amenities and concerns around nuisance behaviour and roaming pets.

In response, the draft DAMP outlines a range of actions that will be delivered over the next 4 years, such as:

• expanding awareness and education on responsible pet ownership

• supporting an improved compliance process and enforcement

• enhancing infrastructure such as bins, taps and fencing in public spaces.

Manningham Mayor, Councillor Deirdre Diamante encouraged all residents to review and provide their feedback on the proposed plan to help ensure it reflects community needs and priorities.

“Animal management doesn’t only affect people with pets. It also plays a key role in creating a safe and healthy community,” Cr Diamante said.

jogging, and dog exercise. It also features two playgrounds for children to enjoy.

“Your feedback will help us create a master plan that supports sport and recreation for all members of our community for many years to come,” Cr Diamante said.

The Timber Reserve masterplan will assess the current sporting infrastructure, explore how the area is used, and identify opportunities for future improvements.

Community members are invited to complete a survey at Your Say Manningham, yoursaymanningham.vic.gov.au/timberreserve-masterplan

The consultation is separate to that by Victoria’s Big Build on behalf of Yarra Valley Water regarding a pressure reducing station at the reserve as part of the North East Link Project.

Council Officers will be available to answer questions a drop-in “Have your say” session at the Timber Reserve sportsground on Thursday 16 October, 5:00pm to 6:30pm.

Consultation continues to 11.59pm on Sunday 26 October 2025.

“This plan will address important topics like responsible pet ownership, community safety and animal welfare and we want to make sure it works for everyone,” she said.

Have your say

Share your feedback on the draft DAMP by completing the short survey by 5:00pm on Thursday 16 October at yoursay. manningham.vic.gov.au/damp.

Manningham Council will consider the final plan for endorsement in November 2025.

Residents who have gone above and beyond making Manningham a better place were recognised at the inaugural Manningham Community Awards on Wednesday 16 September.

The winners, and the 2025 Citizen of the Year, were announced at an awards ceremony hosted by Manningham Mayor, Cr Deirdre Diamante at the Manningham Function Centre.

The expanded awards program recognises the outstanding achievements of individuals and groups over the past 12 months.

The Manningham Community Awards are a chance to celebrate the people and groups who make Manningham shine,” Cr Diamante said.

“Congratulations to all the winners and finalists. Your commitment, passion and care for others reflects the very best of who we are.”

Leon Moore has been named the 2025 Manningham Citizen of the Year and received the Doreen Stoves Volunteer of the Year Award for his work in establishing and leading the Laughing All Abilities Really Friendly Singers (LAARFS).

The choir, which meets weekly, has more than 70 members, who live with chronic conditions such as Parkinson’s disease, multiple sclerosis, cancer and dementia.

Category winners:

Active Community: Bulleen Tennis Club

Under the committee’s leadership, membership has grown by more than 70% with expanded junior and senior competitions, veterans’ tennis and social play.

Ageing Well: Chinese Senior Citizens Club of Manningham

With more than 1000 members and 200 volunteers, the club is one of the largest in Manningham. It has delivered more than 60 free weekly classes, as well as educational talks, performances and major cultural celebrations over the past year.

Artistic Achievement: Warrandyte Arts Association

The association has supported more than 170 members across several groups including life drawing, pottery, writing and theatre.

Community Excellence: Warrandyte Pink Ladies

The group was recognised for their passionate efforts in raising funds, awareness and support for those affected by breast cancer – all while bringing some of their signature sparkle to the community.

Community Health and Wellbeing: Bulleen Men’s Shed at the Veneto Club

The group has created a welcoming and supportive space for men of all ages and backgrounds to connect, share, support one another, and improve men’s mental health.

Inclusive Community: Kevin Heinze Grow

The organisation’s inclusive, nature-based programs support people of all abilities. These include Café Kevin which provides hospitality training, and the Grow Program that offers experience in gardening, cooking and sustainability.

Young Achiever: Niosha Khademideljou

A former Manningham Youth Advisory Committee member, Noisha is now a crisis supporter with Lifeline Naarm, and has helped provide children’s spiritual education classes and inclusive school holiday festivals.

This year’s awards were the first of an expanded program designed to recognise even more of the work being done in the Manningham community.

Cr Diamante said, “We received an incredible 70 nominations, making the judging no easy task.

“There were so many inspiring stories, so many individuals and groups going above and beyond.

“We can’t wait to learn about more of the incredible people and groups who contribute to the Manningham community. We encourage you to nominate someone you know who is doing amazing things for the 2026 awards. Nominations will open in March 2026.”

We’re inviting community members to contribute their insights and ideas to help shape our draft 2026-27 Budget and draft 10-Year Financial Plan.

Manningham Mayor, Councillor Deirdre Diamante said: “We’re committed to ensuring the annual budget prioritises what matters most to our community, while delivering on our mission to be a financially sustainable council.

“Our council delivers more than 100 services across a diverse range of areas, from waste collection and libraries to community programs and infrastructure,” Cr Diamante said.

“These services all play an important role in our community and we want to understand which areas our community sees as most important for us to prioritise spending,” she said.

You can also register your interest to pitch your budget ideas to Councillors at an in-person meeting in early December.

“We want to hear from you about the projects and services you would like to see delivered in Manningham, now and in the future. Your ideas, passion and local knowledge are at the heart of what makes our community thrive,” Cr Diamante said.

Shortlisted in-person submitters will have 3 minutes each to present to Councillors at a meeting on Monday, 1 December at the Manningham Council Chamber.

If you would prefer not to pitch your idea in person, your ideas will still be considered as part of the broader engagement process.

We’re reviewing Manningham’s Public Toilet Plan(External link) and seeking your feedback on local toilet facilities. The Public Toilet Plan(External link) (2021) is a 10-year plan to ensure a network of sustainable, safe, accessible and quality purposebuilt facilities.

What’s been delivered so far?

Since the plan was endorsed in 2021, we’ve completed 12 new and upgraded public toilets across Manningham. We’re also on track to upgrade two more facilities by the end of the year

See what’s been delivered and what we are planning here.

Why are public toilets important?

Public toilets are essential for people to enjoy public spaces without feeling restricted. They help us socialise, exercise, play, learn and engage with the community. Well-placed facilities also support local business by encouraging visitors and residents to spend more time in the area.

Have your say

You can share your insights, ideas and register your interest to present to Council by completing our short survey by 9 November 2025 at Your Say Manningham.

Your responses will help shape the draft 2026-27 Budget and draft 10-Year Financial Plan.

The final 2026-27 Budget and 10-Year Financial Plan will be considered for endorsement at the Council Meeting on Tuesday, 23 June 2026.

Some ideas may be better suited to our Manningham Community Grant program, which supports eligible organisations to deliver communityfocused projects.

Have your say

Thank you for your feedback. The survey is now closed.

The project team will share survey outcomes in August 2025.

More information

If you have any questions, please contact us at 9840 9333 or email manningham@manningham.vic.gov.au(External link).