In 2022, Ukraine's utilised agricultural area covered 41.3 million hectares, including 32.7 million hectares of arable land (State Statistics Service of Ukraine (SSSU)). This agricultural area makes Ukraine the largest agricultural country on the European continent. 45% of the country's surface area is made up of particularly fertile humus-rich soils, known as "rich" chernozioms. These are found mainly in the country's central plain.

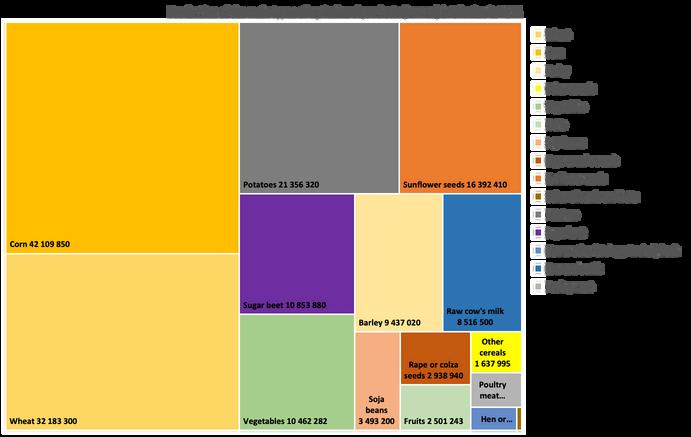

Figure 1 - Production of the main types of agricultural products in volume (tons) in Ukraine in 2021 Source: FAOStat

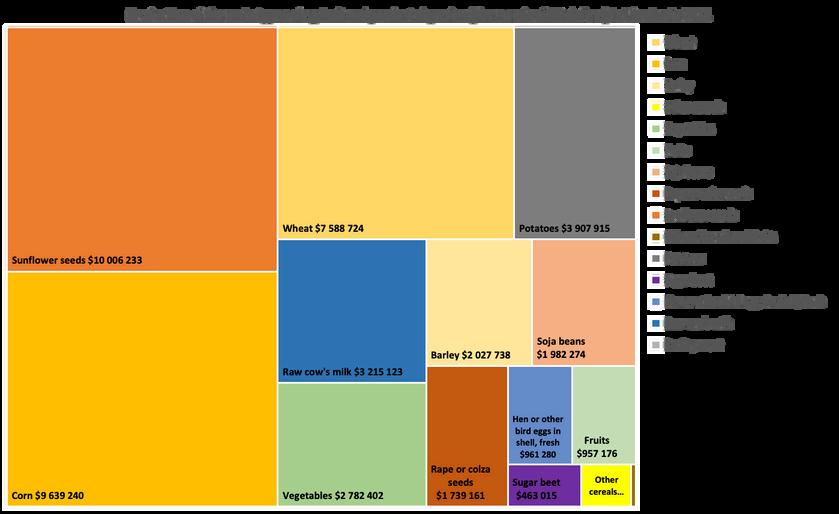

Figure 2 - Figure 2 - Production of the main types of Production of the main types of agricultural products, excluding meat, agricultural products, excluding meat, by by value (thousands of US dollars) value (thousands of US dollars) iin n Ukraine in 2021 Ukraine in 2021 Source Source: FAOStat : FAOStat

Note Note :: data data not available for meat. not available for meat.

The country mainly produces cereals (corn, wheat, barley), potatoes, sunflower seeds and sugar beet.

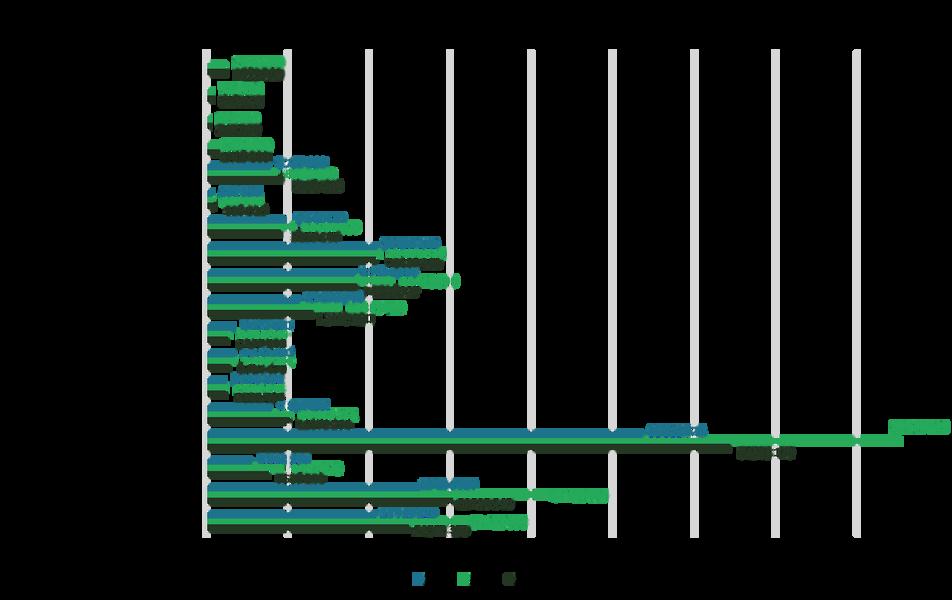

Figure 3 - Evolution of production of the main types of agricultural products (in tons) in Ukraine Source: FAOStat

Note: 2022 data not available for meat.

Marked by its communist past, the Ukrainian agricultural sector is characterised by 110 huge vertically integrated agricultural companies, known as agro-holdings*, which control all or part of the production chain (cultivation-breeding, processing, trade). Their aim is to achieve a return on capital invested, and to achieve this they invest in state-of-the-art, large-scale equipment and in the use of inputs. 20 of these companies account for 14% of Ukraine's Utilised Agricultural Area (UAA).

57% of the UAA is farmed by companies of more than 1,000 ha.

Figure 4 - Figure 4 - Farm structure Farm structure in Ukraine in 2021. in Ukraine in 2021

Source : Source : based on data from based on data from the State Statistics Service of the State Statistics Service of Ukraine (SSSU) Ukraine (SSSU).

Agriculture plays a major economic role in Ukraine, accounting for 10.9% of GDP in 2021 and nearly 14.7% of employment (World Bank). In comparison, the sector accounts for 1.4% of European GDP and 4.2% of employment (Eurostat). In 2021, agricultural products accounted for 41% of Ukrainian exports, worth 27 billion dollars

The sector, which has been severely affected by the current conflict, is estimated to have suffered the equivalent of $80 billion in damage and losses (World Bank), and its reconstruction is estimated to cost at least $56 billion (World Bank, 2023), not including mine clearance ($32 billion).

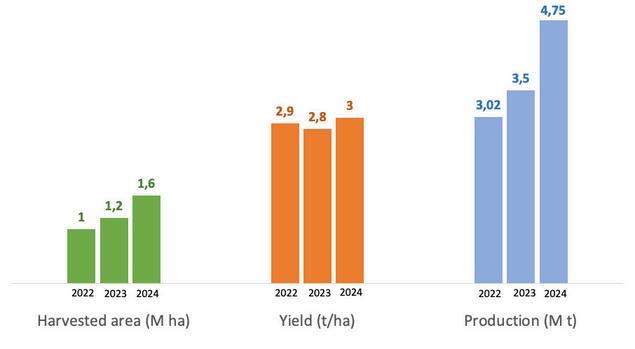

For the 2023-24 season, Ukraine harvested 1.6 million hectares of rapeseed, which represents 26% of the area harvested in the EU (6.22 million ha). The area harvested in Ukraine increased by 36% compared to the pre-war period (average 2018-2021).

Rapeseed crop calendars are quite similar in Ukraine and the EU. In Ukraine, winter rapeseed, which accounts for over 90% of the total crop, is planted in September and October and harvested in July and August. In major EU producing countries, planting occurs in August and September, while harvesting takes place in June and July.

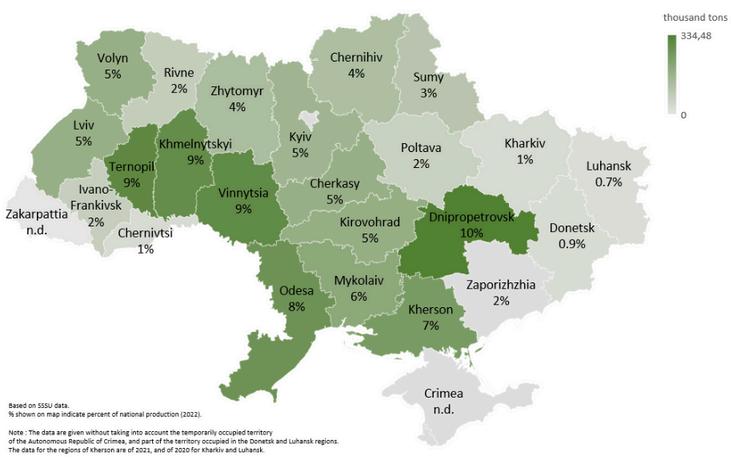

Figure 5 - Figure 5 - Ukraine rapeseed production by oblast, 2022. - Percentages indicate each oblast's share of national Ukraine rapeseed production by 2022 - Percentages indicate each oblast's share of national production (based on SSSU data). production (based on SSSU data)

Note : the data are given without taking into account the temporarily occupied territory of Crimea, and part of the territory occupied

Note the data are given without taking into account the temporarily occupied territory of Crimea, and part of the territory occupied in the Donetsk and Luhansk regions. The data for the regions of Kherson are of 2021, and of 2020 for Kharkiv and Luhansk. in the Donetsk and Luhansk regions. data for the regions of Kherson are of 2021, and of 2020 for Kharkiv and Luhansk.

Ukraine produced a record 4.75 million tons of rapeseed in 2023/24, making the country the sixth largest producer in the world, accounting for 5% of the global production. Ukraine’s rapeseed production increased by 57% compared to the pre-war period (average 2018-2021). Ukraine’s rapeseed production has been steadily increasing over the past decade. The 2023/24 harvest set a new record, well above the 2014-2023 average of 2.77 million tons (USDA).

In comparison, the EU produced 19.98 million tons of rapeseed in the 2023/24 season, making it the world's largest producer (22%), closely followed by Canada (21%). EU’s top rapeseed producers for the same period were France (21%), Germany (21%) and Poland (18%).

Rapeseed is the main oilseed crop grown in the EU (59%), (2023, DG AGRI). If Ukraine were to join the European Union, the country would become the leading producer in the EU and account for 24% of European rapeseed production (USDA).

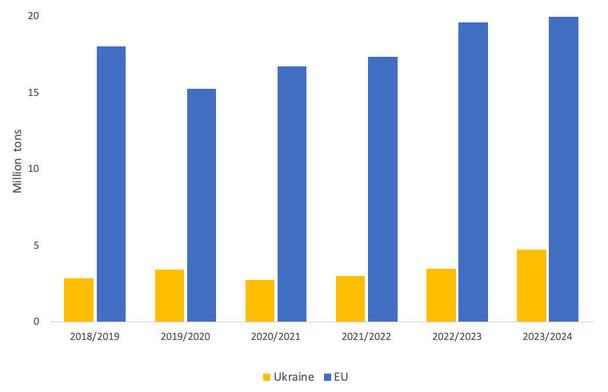

Figure 6 - Figure 6 - Rapeseed production in Rapeseed production in Ukraine (yellow) and in the EU (blue), Ukraine (yellow) and in the EU (blue), 2018-2024 (Source : based on USDA 2018-2024 (Source : based on USDA data) data)

On average, rapeseed yields in Ukraine are slightly lower than in the European Union. Between 2021 and 2023, Ukraine's rapeseed yields averaged 29 qt/ha, compared to 32 qt/ha in the EU (USDA).

Rapeseed yields in Ukraine have shown a slight increase over the past few years, with the 2022-24 average yield being 11% higher than the 2018-21 average.

Rapeseed production in Ukraine has increased particularly due to the expansion of harvest areas. Over the past couple of years, rapeseed has gained popularity among Ukrainian farmers, driven by the continuous high demand for Ukrainian oilseeds from European importers Rapeseed in Ukraine is now seen as a relatively quick way for agricultural producers to generate income (APK-inform).

Figure 7 - Figure 7 - Dynamics of rapeseed Dynamics of rapeseed production in Ukraine, 2021- production in Ukraine, 20212024 (Source : based on USDA’s 2024 (Source : based on USDA’s FAS data) FAS data)

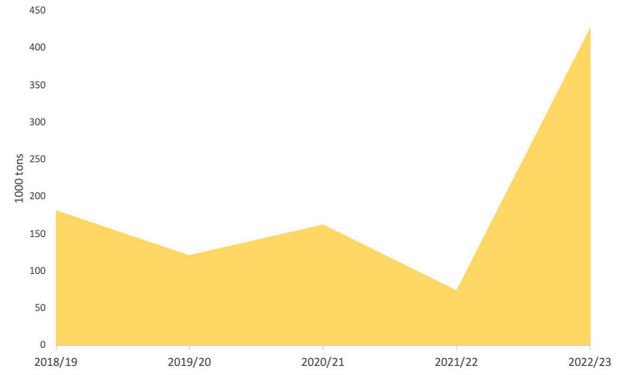

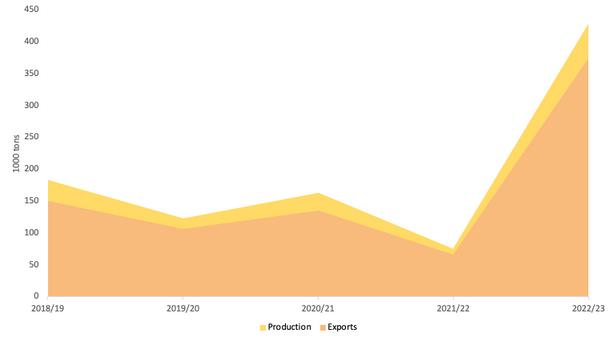

In 2023/24, Ukraine ranked 14th in rapeseed oil production. It produced a record 428 thousand tons, accounting for 1.3% of global production. Ukraine's production dropped in 2022 due to processing plants being incapacitated by the full-scale Russian aggression. However, it rebounded strongly in 2023, increasing by 174% compared to the pre-war period (average 2019-21).

This growth aligns with a significant rise in domestic processing, driven by a record harvest (see Production) and restricted export options for oilseeds (see Exports). While rapeseed exports increased, the EU's restrictions on rapeseed imports constrained export capacity. Coupled with the strong demand for rapeseed meal and oil, the latter not being subject to EU import restrictions, this led to an increase in rapeseed crushing in Ukraine (USDA, Argus media). As a result, Ukraine processed a record 1 million tons of rapeseed in 2023/24, representing 21% of the harvest (USDA).

As a comparison, the EU produced 10.25 million tons in the 2023-24 season, making it the largest producer in the world accounting for 30% of world production. The EU’s top producers are Germany, France and Poland. If Ukraine were to join the European Union, it would account for 4.17% of European rapeseed oil production (USDA).

Figure 8 - Figure 8 - Ukraine’s rapeseed oil Ukraine’s rapeseed oil production for the period 2019- production for the period 20192023 (Source : based on data 2023 (Source : based on data from USDA) Note : the years from USDA). Note : the years correspond to USDA market years correspond to USDA market years from July to June. from July to June

However, USDA Kyiv FAS’ 2024 report forecasts a 64% year-to-year decrease of Ukrainian rapeseed oil production in 2024/25, reaching 170,000 tons, a level similar to pre-war average. The lower forecast is primarily due to two factors: competition from EU crushers for available stocks of Ukrainian rapeseed, and low crush margins for Ukrainian processors. In 2023/24, crush margins in Ukraine fluctuated significantly, hitting critically low levels towards the end of the marketing year. As a result of these two factors, Ukrainian processors may reduce domestic processing, leading to a potential increase in rapeseed grain exports to the EU.

Vegetable meals are byproducts of oilseed crush, so their production mirrors that of vegetable oils. Based on the average for 2022-24, if Ukraine were to join the EU, it would account for around 4% of the European rapeseed meal production. 24% equivalent to the eu’s production

in Ukraine

in Ukraine

Biodiesel production in Europe had been steadily increasing over the years, in line with the EU’s target for the use of renewable energy sources. In 2022, the EU was the largest biodiesel producer in the world. Within the EU, Germany, France and the Netherlands were the top producers, followed by Spain, Italy and Poland.

In 2022, around 46% of the vegetable oil supply in the EU was used in the biodiesel industry (FEDIOL).

Rapeseed oil plays a central role in the EU’s biofuel production, representing 40% of the feedstock used for biodiesel, which makes it the main resource for biodiesel production.

BiofuelinUkraine

There is no precise data on Ukraine’s current biodiesel production volumes (UNECE).

Biofuel production in Ukraine has been steadily growing over the last decade. In 2019, the production of biofuels and wastes reached 3,400 tons, representing the biggest share of all renewable energy sources (79%). Overall, renewable energy sources contributed 5% to Ukraine's total primary energy supply (UABIO, based on SSSU data).

In June 2024, the European Bank for Reconstruction and Development (EBRD) approved a €60 million loan for the construction of a bioethanol plant.

However, most of Ukraine's biofuel production focuses on bioethanol and biogas, with reports indicating that the biodiesel industry is not experiencing significant growth. Latest data from 2019 reports 14 large inactive biodiesel plants with a total production capacity of 300,000 tons per year. There is no available information on their current state of or the possibility to restart production. Additionally, around 50 smaller enterprises could collectively produce up to 25,000 tons per year, but reliable data on their operations is also lacking (UNECE, UABIO).

According to the UNECE’s 2023 report on Ukraine’s energy system, biodiesel production in Ukraine is estimated to be low. Domestic enterprises lack both the opportunity and incentives to process rapeseed into biodiesel. The UNECE identifies the excise tax on the production of biodiesel which makes it uncompetitive compared to diesel fuel of petroleum origin, and the absence of technical regulations fixing a mandatory biodiesel content for diesel fuel as the two main barriers to the biodiesel industry development.

Nevertheless, faced with shortages of petrol and diesel and the impacts of the energy crisis since the start of the war, Ukraine aims at strengthening energy security through the development of renewable energy, notably biomass and biofuels (UNECE). The government has recently shown increased commitment to promoting biofuels. The National Action Plan for the Development of Renewable Energy until 2030 sets a target for biodiesel use in the transport sector, aiming for a total contribution of 87,000 tons of oil equivalent by 2030. Most recently, the Law on the Use of Liquid Biofuels, adopted on June 4, 2024, establishes that, starting from May 1, 2025, motor petrol sold at wholesale and retail fuel outlets should contain at least 5% of biofuel.

The EU is the world's largest rapeseed importer, followed by China. In 2024, the EU imported 6.3 million tons of rapeseed, accounting for 37% of total global imports. The EU’s rapeseed imports primarily come from Ukraine, Canada, and Australia (USDA).

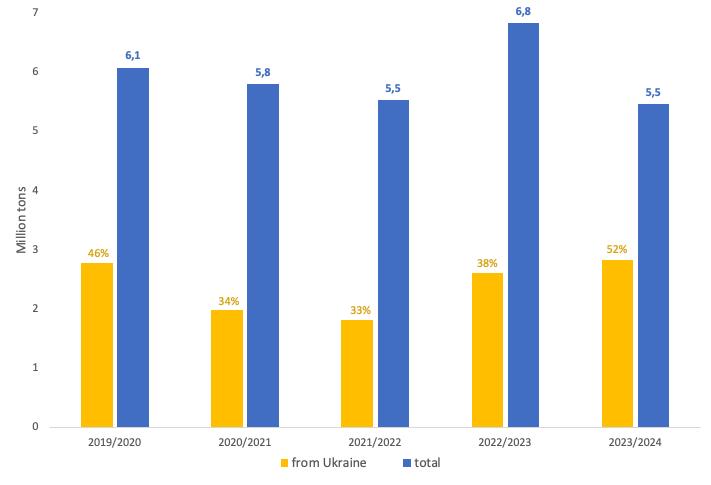

Ukraine has maintained its top position among the key rapeseed exporters despite the on-going war. In 2023/24, Ukraine was the third major rapeseed exporter, following Canada (1st) and Australia (2nd). It exported a record 3.07 million tons of rapeseed, accounting for 21% of total global exports. Ukraine’s exports increased by 37% compared to the pre-war period (average 2019-21, USDA), facilitated by an increase in demand from the EU countries (APK-inform).

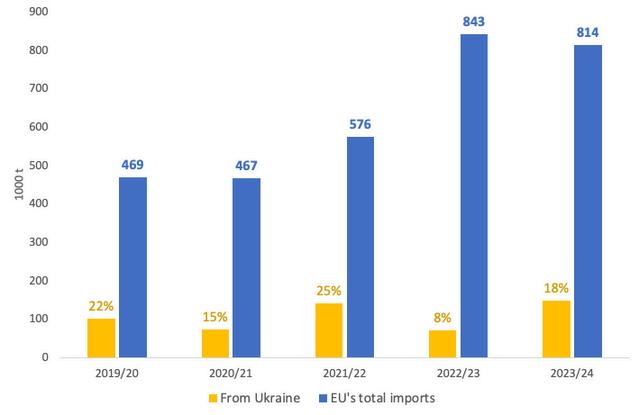

Figure 9 - Figure 9 - EU’s rapeseed EU’s rapeseed imports from Ukraine imports from Ukraine (yellow), and total imports (yellow), and total imports including Ukraine (blue). including Ukraine (blue) Numbers indicate the total Numbers indicate the total EU imports in tons (blue) and EU imports in tons (blue) and the proportion from Ukraine the proportion from Ukraine (yellow) (Source: based on (yellow). (Source: based on Eurostat data) Eurostat data)

The EU has been the largest importer of Ukrainian rapeseed since before the war, accounting for 83% of total Ukrainian rapeseed exports on average (2019-21). However, Ukraine’s exports to the EU increased by 28% (+600,000 tons) in 2023/24 compared to the pre-war average, accounting for 93% of Ukraine’s exports.

As a result, although the EU’s total rapeseed imports have remained relatively stable since 2019, Ukraine's share in the EU’s imports rose from an average of 41% in 2018-21 to 52% in 2023/24.

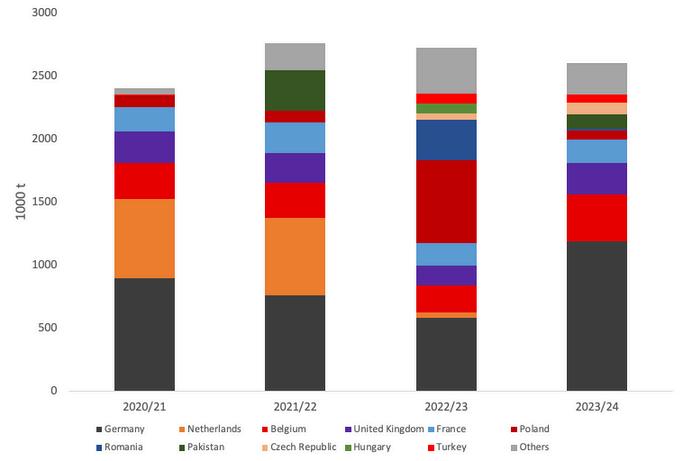

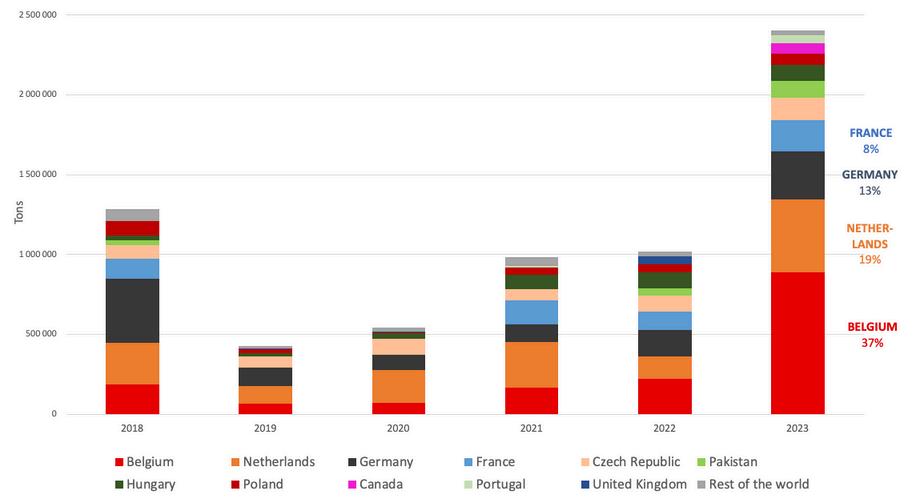

In 2023/24, the main importers of Ukrainian rapeseed within the EU were, in order, Germany (29%), Belgium (25%), and France (15%) (USDA). The UK was also an important destination outside the EU.

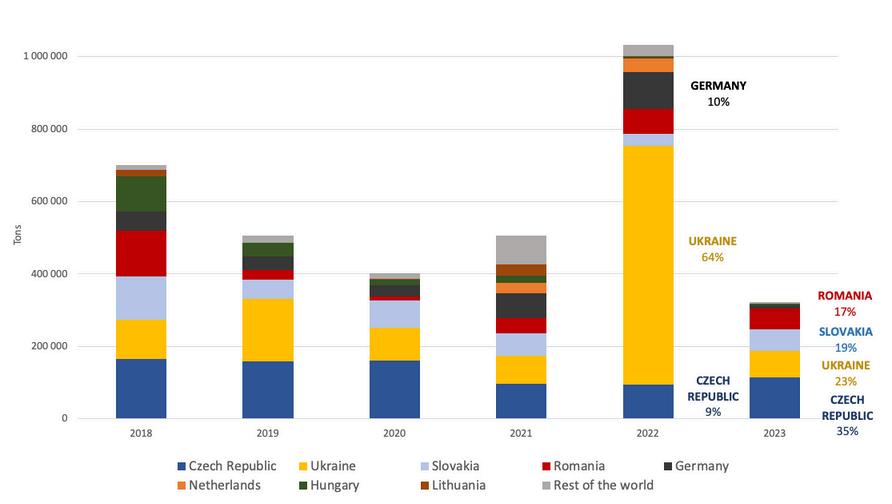

Figure 10 - Figure 10 - Main importers of Main importers of Ukrainian rape and colza Ukrainian rape and colza seeds, 2020-2024 (Source : seeds, 2020-2024 (Source : based on WITS data) based on WITS data)

In 2022/23, exports of rapeseed from Ukraine to Poland and Romania surged. This increase was primarily driven by changes in logistics routes due to Russia's blockade of critical Black Sea ports and the implementation of the EU-Ukraine Solidarity Lanes. This coincided with significant increases in these countries' exports. However, Ukraine's rapeseed exports to these two countries drastically decreased in 2023/24.

This was notably due to the EU establishing temporary preventive measures on imports from Ukraine, under the exceptional safeguard of the Autonomous Trade Measures Regulation. These measures lasted from 2 May to 15 September 2023 and concerned wheat, maize, sunflower seed and rapeseed originating in Ukraine. During this period, the products could continue to be released for free circulation in all Member States except the five frontline Member States: Bulgaria, Hungary, Poland, Romania and Slovakia. The products could however continue to circulate in or transit via these five Member States.

In September 2023, the European Commission lifted the restrictions, but Poland, Hungary, and Slovakia immediately reintroduced their unilateral import bans. Moreover, in September 2023, Poland extended the list of banned Ukrainian products to include oilseed cake. Prior to that, Poland was a major buyer of Ukrainian rapeseed meal. Between July and September 2023, it received 57% of Ukrainian exports. In October, about 900 rail cars transporting rapeseed meal were stuck at the Ukraine-Poland border, according to market participants (Latifundist). In addition, from February to April 2024, Polish farmers blocked trucks at several Polish-Ukrainian border crossings.

Other significant changes in Ukrainian rapeseed exports include:

A twofold increase in imports to Germany in 2023/24, partly due to smaller harvest in Germany.

A 92% decrease in exports to the Netherlands in 2022/23, with exports being almost nonexistent in 2023/24.

A sharp decrease in exports to Pakistan in 2022/23, followed by a recovery in 2023/24. Steady increases in exports to Turkey since 2022/23.

Poland’s total imports of rapeseeds doubled in 2022/23 (+527,000 tons). However, they decreased threefold in 2023/24 (-710,000 tons).

Specifically, imports from Ukraine were multiplied by 8.4 in 2022/23 (+580,000 tons), but were divided by 9 in 2023/24 (-585,000 tons). This sharp drop, marking a 20% decrease compared to the 2020-22 average, was due to EU import restrictions from May to September 2023, which Poland upheld in 2024.

Poland’s rapeseed exports, on the other hand, increased in 2023/24, unlike the import rise seen in 2022/23. Similarly to the imports in 2022/23, exports increased by 2.4 times (+502,000 tons) in 2023/24. The single largest importer from Poland was Germany importing around 650,000 tons, or 75% of Poland’s total exports.

Table 2 - Table 2 - Poland rapeseed balance sheet, 2020-24 (Source : based on Eurostat data). Poland rapeseed balance sheet, 2020-24 (Source : based on Eurostat data).

Poland is a major producer of rapeseed within the EU. Its production has been steadily increasing since 2018. Poland’s production was not significantly impacted by the surge in imports from Ukraine in 2022/23. In 2023/24 Poland was the third largest producer of rapeseed within the EU, accounting for 18% of the production.

Germany has been the main destination for Polish rapeseed since before the war.

In 2022/23, Poland exported 311,000 tons of rapeseed to Germany, accounting for 85% of its total exports. In 2023/24, Poland exported 652,000 tons of rapeseed to Germany, accounting for 75% of its total exports.

In 2022/23, Poland’s rapeseed imports from Ukraine increased by 580,000 tons and total rapeseed imports increased by 527,000 tons.

The following year, in 2023/24, Poland’s rapeseed exports increased by a similar figure (+503,000 tons), despite only a slight increase in domestic production (+ 90,000 tons). Specifically, exports to Germany increased by 341,000 tons.

We can hence estimate that almost all the volume exported from Ukraine to Poland in 2022/23 was re-exported by Poland in 2023/24. The major part was transferred to Germany (341,000 tons), with smaller quantities going to the Netherlands (82,000 tons), Belgium (37,000 tons) and the UK (29,000 tons) and Czech Republic (1% or 6,000 tons).

Table 3 - Table 3 - Increase in Poland’s rapeseed exports in 2023/24 (Source : based Increase in Poland’s rapeseed exports in 2023/24 (Source : based on Eurostat data). on Eurostat data)

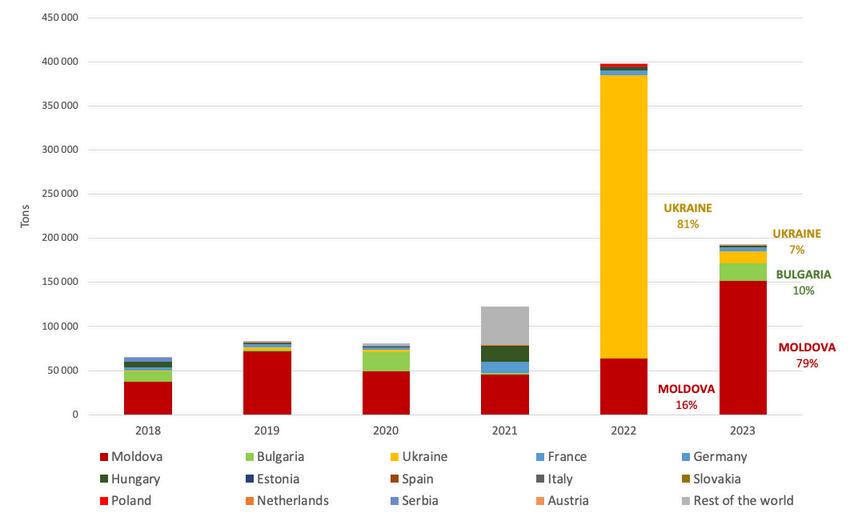

Romania is a significant producer of rapeseed within the EU, accounting for 6% of the production in 2023/24. Since 2022/23, Romania has been the fourth largest exporter of rapeseed in the world, just behind Ukraine. This increase in exports is largely attributed to an increase in production. In 2023/24, Romania produced a record 1.79 million tons of rapeseed and exported 2.4 million tons, with the major destinations being Belgium (37%), Netherlands (19%), Germany (13%) and France (8%) (Eurostat).

In 2022/23, Ukraine’s rapeseed flooded Romania’s domestic market, resulting in suppressed prices for local producers

Romania's total rapeseed imports increased by 275,000 tons between 2021/22 and 2022/23, representing a threefold rise (+224%).

Imports specifically from Ukraine surged from nearly non-existent before the war to 317,000 tons in 2022/23. Therefore, the overall increase is largely attributed to the influx of Ukrainian imports, while imports from Moldova, typically Romania's main supplier, decreased.

However, imports from Ukraine dropped by 303,000 tons between 2022/23 and 2023/24, reaching just 14,000 tons, a level closer to that before the war. Romania’s total imports also dropped, but to a lesser extent, by half (- 206,000 tons), with Moldova regaining its position as the main supplier.

Romania’s rapeseed exports evolved differently from its imports.

In 2021/22, Romania's total rapeseed exports increased by 1.8 times (+442,000 tons). This coincided with a 1.8 times (+595,000 tons) increase in domestic production, along with an increase in rapeseed oil exports.

Contrary to the imports, exports of seeds did not significantly increase in 2022/23, but in 2023/24, during which exports were multiplied by 2.4 (+136%), increasing by 1.39 million tons.

Table 4 - Table 4 - Romania rapeseed balance sheet, 2020-24 (Source : based on Eurostat data) Romania rapeseed balance sheet, 2020-24 (Source : based on Eurostat data).

Following the surge in supply in 2022/23, largely driven by imports from Ukraine, there was no significant increase in Romania's domestic consumption or processing of rapeseed, nor in its oil exports. Ukraine’s rapeseed flooded Romania’s domestic market in 2022/23, resulting in suppressed prices for local producers This contributed to the EU implementing restrictions on imports from May to September 2023. Moreover, the Romanian government adopted an emergency ordinance (OUG. 84/2023) in October 2023 establishing measures to regulate imports of agricultural products, including rapeseed, from Ukraine. As a result, imports from Ukraine to Romania returned to pre-war levels in 2023/24.

The data suggests that most of the volume of rapeseed imported from Ukraine in 2022/23 was stored and re-exported in 2023/24.

In 2023/24, Romania’s rapeseed production increased by 557,000 tons and imports decreased by 206,000 tons. Exports, on the other hand, increased by 1,386 thousand tons. Romania therefore exported far more rapeseed than it produced and imported combined. This suggests that the increase in exports was fueled by its stocks from the previous year, which is reflected by the negative apparent use in 2023/24 (- 426,000 tons).

Table 5 - Table 5 - Increase in Romania’s rapeseed exports in 2023/24 (Source : based Increase in Romania’s rapeseed exports in 2023/24 (Source : based on Eurostat data) on Eurostat data).

Exports increase in 2023/24 (1000 T)

The Romanian example shows the need for vigilance and monitoring of flows of certain key agricultural products, in relation to the EU's production and needs.

Germany is the largest importer of rapeseed in the world.

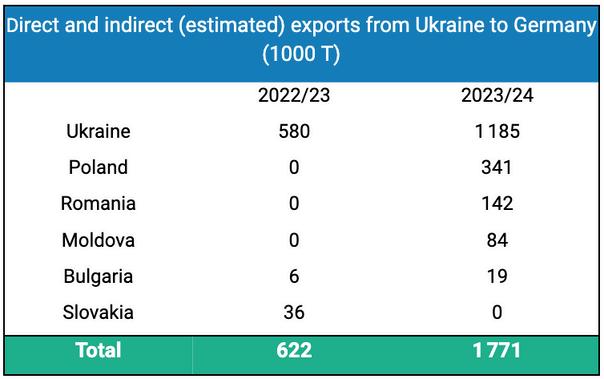

In 2023/24, it imported a total 6.67 million tons of rapeseed. Considering only direct imports, the main suppliers were Australia (21% or 1.39 million tons), Ukraine (18% or 1.18 million tons) and France (14% or 0.95 million tons). Romania and Poland ranked 4th and 5th, accounting for 13% (0.87 million tons) and 12% (0.83 million tons) respectively (WITS).

Germany has been the largest importer of rapeseed from Ukraine since before the war, except in 2022/23. However, direct imports from Ukraine more than doubled in 2023/24 (+109%), compared to the 2018-21 average (Eurostat). Additionally, Germany imported Ukrainian rapeseed indirectly through other countries. Combined, Germany’s direct and indirect imports from Ukraine can be estimated at 1.77 million tons, placing Ukraine as the main supplier of rapeseed for Germany (26%).

Table 6 - Table 6 - Directs and Directs and indirect* exports from indirect* exports from Ukraine to Germany Ukraine to Germany.

*Note : Indirect exports were estimated using the increase of Ukraine exports to the

*Note : Indirect exports were estimated using the increase of Ukraine exports to the respective countries and the increase in the exports from these countries to Germany respective countries and the increase in the exports from these countries to Germany (Source : based on Eurostat and WITS data). (Source : based on Eurostat and WITS data).

Ukraine exports the majority of the rapeseed oil it produces In recent years, Ukraine has significantly increased its processing capacity, establishing itself as one of the world’s largest exporters of rapeseed oil.

In 2023/24, it exported 373,000 tons, accounting for 87% of its production. As a result, despite ranking 14th globally in production, it ranked 5th in rapeseed oil exports (USDA).

In 2023/24, the EU and China were the two major importers of Ukrainian rapeseed oil, accounting for 43% (161,000 tons) and 35% (129,000 tons) respectively.

Figure 11 - Figure 11 - Ukraine’s rapeseed oil production (yellow) and total crude rapeseed oil exports (brown) for 2019- Ukraine’s oil production (yellow) and total crude rapeseed oil exports (brown) for 20192023 (Source : based on USDA and WITS data). 2023 (Source : based on USDA and WITS data)

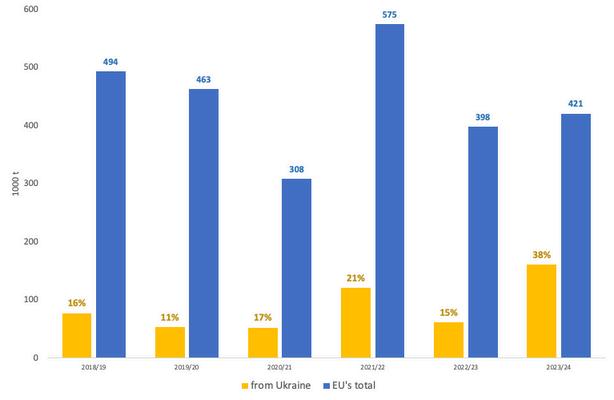

Figure 12 - Figure 12 - EU’s imports of rapeseed oil, total (blue) and proportion from Ukraine (yellow), 2018-2024 (Source : EU’s imports of rapeseed oil, total (blue) and proportion from Ukraine (yellow), 2018-2024 (Source : based on data from Agridata Dashboard, European Commission). based on data from Agridata Dashboard, European Commission)

The EU's rapeseed oil imports have fluctuated over the past few years. However, in 2023/24, the

The EU's rapeseed oil imports have fluctuated over the past few years. However, in 2023/24, the total imports returned to a level similar to the pre-war period (average for 2018-21). total imports returned to a level similar to the pre-war period (average for 2018-21). On the other On the other hand, imports from Ukraine increased by 163% and the share of Ukraine in the EU’s imports hand, imports from Ukraine increased by 163% and the share of Ukraine in the EU’s imports more than doubled, compared to the 2018-21 average. more than doubled, compared to the 2018-21 average.

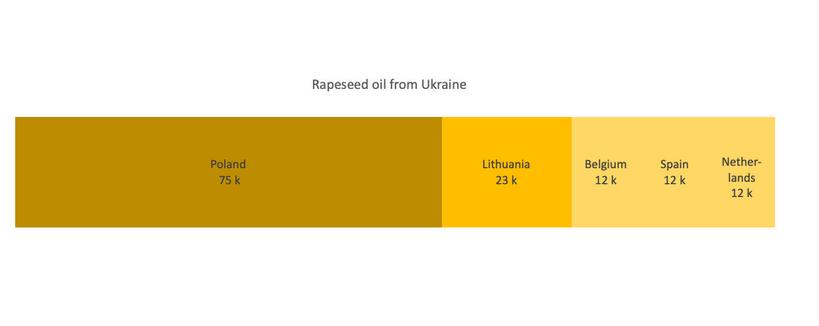

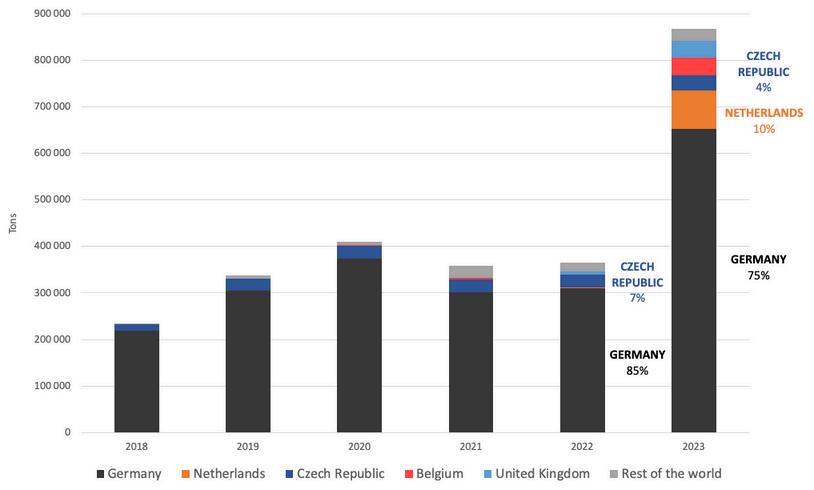

Within the EU, the two major destinations for Ukrainian rapeseed oil in 2023/24 were Poland

Figure 13 - Figure 13 - Main destinations for Ukrainian rapeseed oil within the EU in 2023/24 Main destinations for Ukrainian rapeseed oil within the EU in 2023/24

(Source : based on data from Agridata Dashboard, European Commission). (Source : based on data from Agridata Dashboard, European Commission)

Within the EU, the two major destinations for Ukrainian rapeseed oil in 2023/24 were Poland (75k t) and Lithuania (23k t), (75k t) and Lithuania (23k t), followed by Belgium, Spain and the Netherlands (12k t) followed by Belgium, Spain and the Netherlands (12k t).

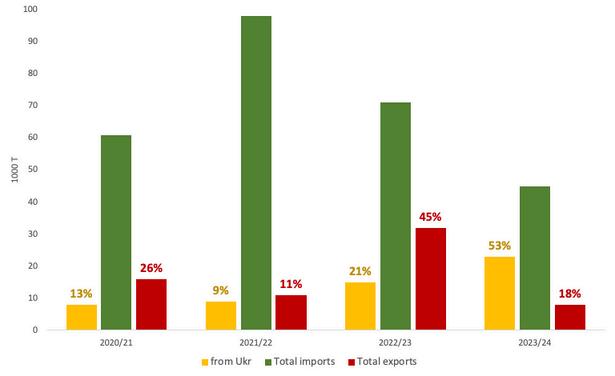

Poland's total rapeseed oil imports doubled in 2021/22 Although they decreased slightly after that Poland's total rapeseed oil imports doubled in 2021/22. Although they decreased slightly after that peak, they remained high in 2023/24, at 66% or 37,000 tons above the 2019-21 average. peak, they remained high in 2023/24, at 66% or 37,000 tons above the 2019-21 average.

IImports mports specifically from Ukraine surged in 2023/24, rising by 2.1 times (+114%) or 40,000 specifically from Ukraine surged in 2023/24, rising by 2.1 times (+114%) or 40,000 tons, compared to the 2019-21 average. tons, compared to the 2019-21 average. These imports accounted for 82% of Poland's total, These imports accounted for 82% of Poland's total, compared to 46% the previous year and an average 63% before the war. compared to 46% the previous year and an average 63% before the war.

As mentioned above (see Rapeseed), Poland’s imports of rapeseed from Ukraine surged in 2022/23

As mentioned above (see Rapeseed), Poland’s imports of rapeseed from Ukraine surged in 2022/23 but dropped even further in 2023/24 due to EU import restrictions, which Poland upheld. Rapeseed but dropped even further in 2023/24 due to EU import restrictions, which Poland upheld. Rapeseed oil, however, was not subject to the bans, which could explain the significant increase in oil imports oil, however, was not subject to the bans, which could explain the significant increase in oil imports from Ukraine seen in 2023/24. from Ukraine seen in 2023/24.

Similarly to its exports of seeds, Poland’s rapeseed oil exports surged in 2023/24. While exports had

Similarly to its exports of seeds, Poland’s rapeseed oil exports surged in 2023/24. While exports had been steadily increasing since 2019/20, they were multiplied by 3.3 (+230%) or 119,000 tons, been steadily increasing since 2019/20, they were multiplied by 3.3 (+230%) or 119,000 tons, compared to the 2019-21 average. compared to the 2019-21 average. In 2023/24, Germany (65%) was the single largest importer In 2023/24, Germany (65%) was the single largest importer of rapeseed oil from Poland of rapeseed oil from Poland. Other major destinations were the Netherlands (14%) and Slovakia . Other major destinations were the Netherlands (14%) and Slovakia (6%) (WITS) (6%) (WITS).

While Lithuania's overall rapeseed oil imports have decreased by 35% since the pre-war period,

While Lithuania's overall rapeseed oil imports have decreased by 35% since the pre-war period, imports from Ukraine increased significantly. imports from Ukraine increased significantly.

Lithuania became a major destination of Ukrainian rapeseed oil within the EU in 2022/23

Lithuania became a major destination of Ukrainian rapeseed oil within the EU in 2022/23. IImports mports from Ukraine were multiplied by 1.7 (+ 6,000 tons) in 2022/23 and by 1.5 (+8,000 tons) in from Ukraine were multiplied by 1.7 (+ 6,000 tons) in 2022/23 and by 1.5 (+8,000 tons) in 2023/24, a 203% increase from pre-war average. 2023/24, a 203% increase from pre-war average.

Similarly, Lithuania’s rapeseed oil exports surged in 2022/23, increasing by 2.4 times (+18,000 tons)

Similarly, Lithuania’s rapeseed oil exports surged in 2022/23, increasing by 2.4 times (+18,000 tons) compared to the 2019-21 average, with Poland being the main destination (52%) However, exports compared to the 2019-21 average, with Poland being the main destination (52%). However, exports dropped significantly in 2023/24, decreasing by 4 times (-24,000 tons). dropped significantly in 2023/24, decreasing by 4 times (-24,000 tons).

In 2022/23, Lithuania became a key transit country for Ukrainian rapeseed oil to Poland and In 2022/23, Lithuania became a key transit country for Ukrainian rapeseed oil to Poland and other EU countries other EU countries In 2023/24, however, while Ukrainian oil continued to be imported in large . In 2023/24, however, while Ukrainian oil continued to be imported in large quantities to Lithuania, it was not re-exported, suggesting that Ukrainian rapeseed oil has likely quantities to Lithuania, it was not re-exported, suggesting that Ukrainian rapeseed oil has likely flooded the domestic market. flooded the domestic market

Given Lithuania’s position as a significant producer of rapeseed (4% of the EU production in Given Lithuania’s position as a significant producer of rapeseed (4% of the EU production in 2023/24), this development raises potential concerns about the impact on local producers 2023/24), this development raises potential concerns about the impact on local producers.

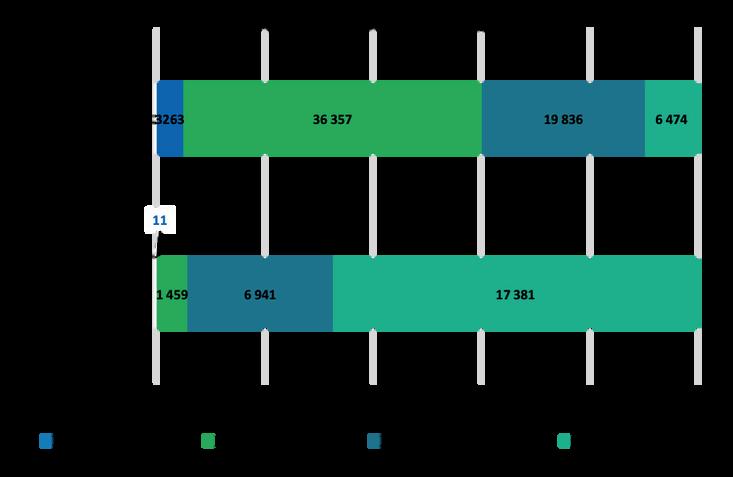

Figure 14 - Figure 14 - Dynamics of Dynamics of Lithuania’s imports and Lithuania’s imports and exports, 2022-24 (Source : exports, 2022-24 (Source : based on data from WITS) based on data from WITS). Percentages are proportions in Percentages are proportions in relation to total imports. relation to total imports.

In September 2023, Poland reintroduced a unilateral import ban on Ukranian rapeseed. The ban

In September 2023, Poland reintroduced a unilateral import ban on Ukranian rapeseed. The ban specifically targeted domestic sale, specifically targeted domestic sale, but transit through Poland remained permitted but transit through Poland remained permitted. In October In October 2023, following this decision, Lithuania, Poland, and Ukraine agreed to shift the inspections of 2023, following this decision, Lithuania, Poland, and Ukraine agreed to shift the inspections of Ukrainian grain from the Ukrainian-Polish border to the Lithuanian port of Klaipėda. This change Ukrainian grain from the Ukrainian-Polish border to the Lithuanian port of Klaipėda. This change was part of a broader effort to streamline and accelerate the transit process through Poland, was part of a broader effort to streamline and accelerate the transit process through Poland, ensuring both the protection of Polish farmers and the efficient flow of Ukrainian exports to ensuring both the protection of Polish farmers and the efficient flow of Ukrainian exports to European markets. European markets

The EU is the main destination for Ukrainian rapeseed and oil. Similarly, Ukraine is a key supplier of these products to the EU, with its importance growing since the war. these products to the EU, with its importance growing since the war. While the EU is a significant While the EU is a significant producer of rapeseed itself, Ukraine plays a major role in supporting its uses in Europe producer of rapeseed itself, Ukraine plays a major role in supporting its uses in Europe,, including in the biofuel economy. including in the biofuel economy.

The EU is the main destination for Ukrainian rapeseed and oil. Similarly, Ukraine is a key supplier of

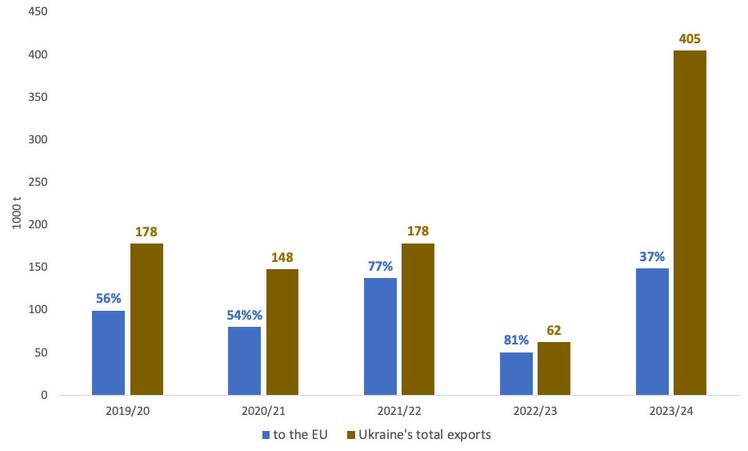

Ukraine's rapeseed meal exports surged in 2023/24 They increased by 2 4 times (+237,000 tons or Ukraine's rapeseed meal exports surged in 2023/24. They increased by 2.4 times (+237,000 tons or +141%) compared to the 2019-21 average, mirroring the increase in rapeseed oil production. This +141%) compared to the 2019-21 average, mirroring the increase in rapeseed oil production. This growth aligns with the significant rise in domestic processing mentioned earlier, as well as the growth aligns with the significant rise in domestic processing mentioned earlier, as well as the strong demand for rapeseed by-products. strong demand for rapeseed by-products.

Over the same period,

Over the same period, Ukraine's exports to the EU increased by 43,000 tons (+41%). Ukraine's exports to the EU increased by 43,000 tons (+41%). In 2023/24, In 2023/24, the EU remained the primary destination for Ukrainian rapeseed meal, receiving 149,000 tons, or the EU remained the primary destination for Ukrainian rapeseed meal, receiving 149,000 tons, or 37% of Ukraine's total exports. However, this share was 63% before the war (2019-21 average). 37% of Ukraine's total exports. However, this share was 63% before the war (2019-21 average). Alongside its sharp increase in production, Ukraine found additional markets, and Alongside its sharp increase in production, Ukraine found additional markets, and the share of the share of exports going to the EU decreased exports going to the EU decreased..

Within the EU, Poland and Spain were the leading importers in 2023/24

Within the EU, Poland and Spain were the leading importers in 2023/24, receiving 20% and 9% , receiving 20% and 9% of Ukraine’s exports, respectively. Outside the EU, China and Israel were also major destinations, of Ukraine’s exports, respectively. Outside the EU, China and Israel were also major destinations, taking 23% and 10% (WITS and Eurostat). taking 23% and 10% (WITS and Eurostat).

Figure 15 - Figure 15 - Ukraine's total rapeseed meal exports (brown) and proportions going to the EU (blue), Ukraine's total rapeseed meal exports (brown) and proportions going to the EU (blue), 2019-2024 (Source : Based on data from WITS) 2019-2024 (Source : Based on data from WITS).

In 2022/23, the EU’s total imports of rapeseed meal increased by 1.5 times (+267,000 tons), In 2022/23, the EU’s total imports of rapeseed meal increased by 1.5 times (+267,000 tons), amounting to 843,000 tons amounting to 843,000 tons. Imports are expected to further increase in 2024/25, potentially . Imports are expected to further increase in 2024/25, potentially reaching 1 million tons, driven by larger exportable supplies from Russia (USDA). reaching 1 million tons, driven by larger exportable supplies from Russia (USDA).

The largest suppliers of rapeseed meal to the EU in 2023/24 were Russia (41%), Belarus (32%), The largest suppliers of rapeseed to the EU in 2023/24 were Russia (41%), Belarus (32%), and Ukraine (18%) and Ukraine (18%), a pattern largely consistent with the pre-war period, except for the United , a pattern largely consistent with the pre-war period, except for the United Kingdom's previously larger share. Kingdom's previously larger share.

Figure 16 - Figure 16 - EU's rapeseed EU's rapeseed meal imports from Ukraine meal imports from Ukraine (yellow) and from all (yellow) and from all destinations (blue), 2019- destinations (blue), 20192023 (Source : based on data 2023 (Source : based on data from Eurostat) from Eurostat).

Reasons for the surge in rapeseed meal imports and potential risk associated

Reasons for the surge in rapeseed meal imports and potential risk associated

The 2009 and 2018 Renewable Energy Directives (RED and RED II) promoted biofuel production,

The 2009 and 2018 Renewable Energy Directives (RED and RED II) promoted biofuel production, which in turn benefited rapeseed meal output (FEFAC). This is particularly evident in the recent which in turn benefited rapeseed meal output (FEFAC). This is particularly evident in the recent growth of the EU’s rapeseed grain and oil production since 2019, showing a compound average growth of the EU’s rapeseed grain and oil production since 2019, showing a compound average growth rate (CAGR) of +5.5% from 2019 to 2023 (based on USDA data). growth rate (CAGR) of +5.5% from 2019 to 2023 (based on USDA data).

Although soybeans have experienced the largest increase in domestic production among oilseed

Although soybeans have experienced the largest increase in domestic production among oilseed crops over the past decade, the use of soybean and soy meal in animal feeds in the EU has been on crops over the past decade, the use of soybean and soy meal in animal feeds in the EU has been on the decline since 2008 (FEFAC). This reduction in the use of soybean meal is partly due to the the decline since 2008 (FEFAC). This reduction in the use of soybean meal is partly due to the growing popularity of alternative co-products, especially other types of meals. growing popularity of alternative co-products, especially other types of meals.

In 2022/23, the EU’s domestic use of rapeseed meal rose by 2.21 million tons (+18%)

In 2022/23, the EU’s domestic use of rapeseed meal rose by 2.21 million tons (+18%). This . This growth was supported by an increase in both the production and imports of rapeseed meal, with growth was supported by an increase in both the production and imports of rapeseed meal, with production rising by 2 04 million tons (+16%) and imports by 0 28 million tons (+46%) Although production rising by 2.04 million tons (+16%) and imports by 0.28 million tons (+46%). Although rapeseed meal exports also grew, the increase was smaller, totaling 0.92 million tons (+13%). At the rapeseed meal exports also grew, the increase was smaller, totaling 0.92 million tons (+13%). At the same time, the production of soybean meal and soybean imports decreased by 1.11 million tons same time, the production of soybean meal and soybean imports decreased by 1 11 million tons (-10%) and 1.43 million tons (-10%), respectively. (-10%) and 1.43 million tons (-10%), respectively.

There was thus a rise in rapeseed meal consumption alongside a decline in soymeal consumption

There was thus a rise in rapeseed meal consumption alongside a decline in soymeal consumption. The increased demand for rapeseed meal has been supported by higher European The increased demand for rapeseed meal has been supported by higher European production, but also by larger imports production, but also by larger imports. In 2023/24, these imports notably came from Ukraine, In 2023/24, these imports notably came from Ukraine, but also from Russia but also from Russia. Although Russia's share in the EU's total imports decreased by 11% . Although Russia's share in the EU's total imports decreased by 11% compared to the 2019-22 average, it remained the leading supplier of rapeseed meal to the EU, compared to the 2019-22 average, it remained the leading supplier of rapeseed meal to the EU, with total volumes rising by 45%. with total volumes rising by 45%.

importer of rapeseed in the world 37% of global imports

destination of rapeseed from ukraine

93% of ukraine’s rapeseed export imports from ukraine compared to pre-war + 28% rapeseed

1ST destination of rapeseed oil from ukraine rapeseed oil imports from ukraine compared to pre-war of ukraine’s rapeseed oil export

1ST destination of rapeseed meal from ukraine rapeseed meal imports from ukraine compared to pre-war of ukraine’s rapeseed meal export

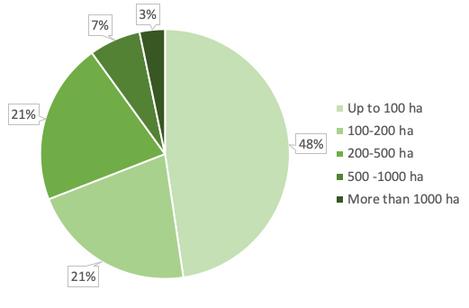

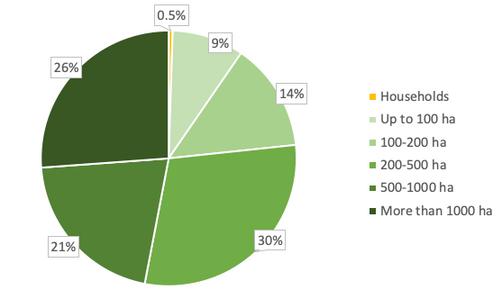

The proportion of large agricultural enterprises involved in production varies depending on the type of production. Unlike the sugar industry, enterprises smaller than 1,000 hectares account for a significant proportion of rapeseed production (73%). However, households* are almost absent.

Table 7 - Table 7 - Share of production agricultural structures in the total production of cereals, sugar

Share of production agricultural structures in total production of cereals, sugar beet, sunflower seeds and rapeseed in 2022. (Source: based on data from the State beet, sunflower seeds and rapeseed in 2022 (Source: based on data from the State Statistical Service of Ukraine (SSSU)). Statistical Service of Ukraine (SSSU))

Almost all of Ukraine's rapeseed is produced by agricultural enterprises. Almost all of Ukraine's rapeseed is produced by agricultural enterprises. In 2022, these In 2022, these enterprises accounted for 99.4% of the harvested rapeseed area and 99.5% of the production. enterprises accounted for 99 4% of the harvested rapeseed area and 99 5% of the production

90% of these enterprises were less than 500 hectares and enterprises smaller than 1,000

90% of these enterprises were less than 500 hectares and enterprises smaller than 1,000 hectares made up 73% of the country's rapeseed production hectares made up 73% of the country's rapeseed production (excluding households) Rapeseed (excluding households). Rapeseed production in Ukraine is hence not primarily controlled by large agricultural companies (which production in Ukraine is hence not primarily controlled by large agricultural companies (which include the 110 agro-holdings) include the 110 agro-holdings). Nonetheless the 170 rapeseed producers with over 1,000 Nonetheless the 170 rapeseed producers with over 1,000 hectares, representing 4% of the total enterprises, accounted for 26% of the total hectares, representing 4% of the total enterprises, accounted for 26% of the total production. production.

*Ukrainian farms fall into two main categories: agricultural enterprises and personal farming households Households are

*Ukrainian farms fall into two main categories: agricultural enterprises personal farming households Households are responsible for the majority of fruit, vegetable and potato production, which is mainly destined for self-consumption and short responsible for the majority of fruit, vegetable and potato production, which is mainly self-consumption and short distribution channels distribution channels

Figure 17 - Figure 17 - Agricultural structures 2022 : Agricultural structures 2022 : a) a) Proportion of agricultural enterprises involved in rapeseed, by size Proportion of agricultural enterprises involved in rapeseed, by size ;; b) b) Share of production of the different agricultural structures in the total Ukrainian rapeseed production in 2022 In Share of production of the different agricultural structures in the total Ukrainian rapeseed production in 2022. In green : agricultural enterprises, and in yellow : households (Source: based on data from the State Statistical Service of green : agricultural enterprises, and in yellow : households (Source: based on data from the State Statistical Service of Ukraine (SSSU)). Ukraine (SSSU))

It should be noted, however, that these large structures do not own the land they farm, as It should be noted, however, that these large structures do not own the land they farm, as Ukrainian nationality is required to be a landowner in Ukraine and as the maximum surface area Ukrainian nationality is required to be a landowner in Ukraine and as the maximum surface area authorised per individual and legal entity is 10,000 ha since the new agrarian reform of 1 January authorised per individual and legal entity is 10,000 ha since the new agrarian reform of 1 January 2024 (law 552-X on the amendment of certain legislative acts of Ukraine concerning the conditions 2024 (law 552-X on the amendment of certain legislative acts of Ukraine concerning the conditions for the circulation of agricultural land). As a result, agro-holdings lease agricultural land to for the circulation of agricultural land). As a result, agro-holdings lease agricultural land to hundreds of landowners, some of whom own only a few hectares of land. hundreds of landowners, some of whom own only a few hectares of land.

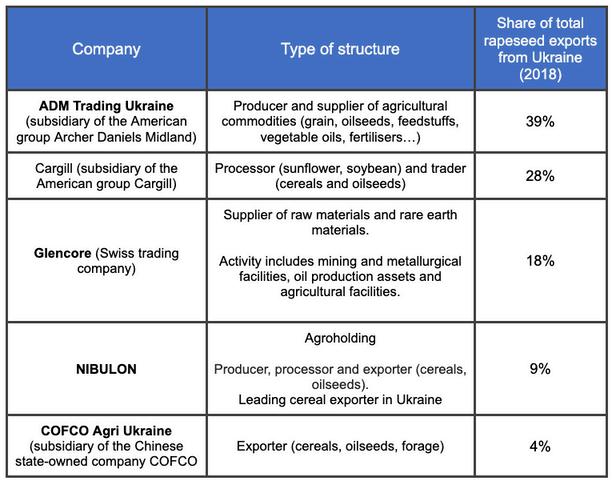

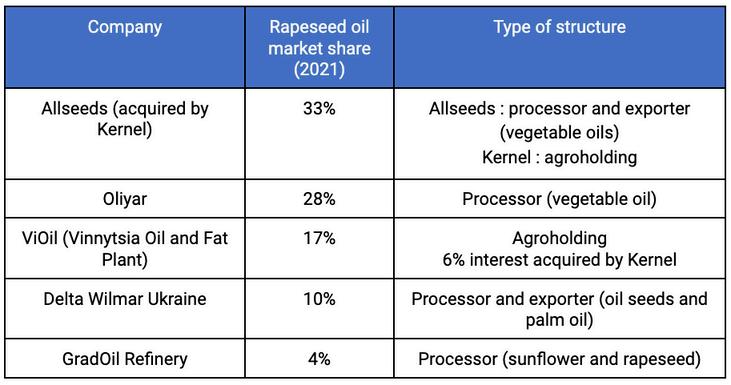

Rapeseed Rapeseed exports from Ukraine are managed by a limited number of companies exports from Ukraine are managed by a limited number of companies. In 2018, five In 2018, five companies, including one agro-holding, accounted for 98% of Ukraine’s rapeseed exports. Unlike companies, including one agro-holding, accounted for 98% of Ukraine’s rapeseed exports. Unlike the processing sector, the processing sector, the majority of top rapeseed exporters are not Ukrainian companies the majority of top rapeseed exporters are not Ukrainian companies.

Table 8 - Table 8 - Ukraine’s largest Ukraine’s largest rapeseed exporters in rapeseed exporters in 2018, by share of total 2018, by share of total exports (Source : exports (Source : Latifundist). Latifundist).

Rapeseed oil production is operated by a limited number of companies. Five processors, including two agroholdings, were responsible for 92% of the country's rapeseed oil production in 2020/21. Since rapeseed meal is a by-product of rapeseed processing, these companies are also the leading producers of meal.

The rapeseed oil and meal markets are predominantly dominated by Ukrainian companies, with Delta Wilmar (Singapore) being the main exception. These companies export the majority of their production and are the top exporters of both rapeseed oil and meal.

In particular, Allseeds Black Sea (Allseeds) has been the leading Ukrainian rapeseed oil producer since 2019, accounting for one-third of the production in both the 2019/20 and 2020/21 seasons. Allseeds exported its entire production during these years (Latifundist).

Table 9 - Table 9 - Ukraine’s largest rapeseed oil producers in 2020/21, by market share Ukraine’s largest rapeseed oil producers in 2020/21, by market share (Source : Latifundist and companies websites). (Source : Latifundist and companies websites).

Allseeds Group is one of the largest producers and exporters of vegetable oils and meals in Allseeds Group is one of the largest producers and exporters of vegetable oils and meals in Ukraine. Its activities include oilseed processing, transshipment, and export. The company owns Ukraine. Its activities include oilseed processing, transshipment, and export. The company owns multi-seed oil processing plants with a daily capacity of 1,500 tons of rapeseed. In 2020, Allseeds multi-seed oil processing plants with a daily capacity of 1,500 tons of rapeseed. In 2020, Allseeds ranked 6th among Ukraine’s top sunflower oil exporters, contributing 8% to the country’s total. ranked 6th among Ukraine’s top sunflower oil exporters, contributing 8% to the country’s total. Allseeds was acquired by Ukraine's leading agroholding, Kernel, in 2010, when the company Allseeds was acquired by Ukraine's leading agroholding, Kernel, in 2010, when the company purchased a controlling 93.4% stake in Allseeds Group purchased a controlling 93.4% stake in Allseeds Group. In 2023, Kernel harvested 14,000 . In 2023, Kernel harvested 14,000 hectares of winter rapeseed, representing 1.2% of the total harvested area in Ukraine (Kernel). hectares of winter rapeseed, representing 1 2% of the total harvested area in Ukraine (Kernel)

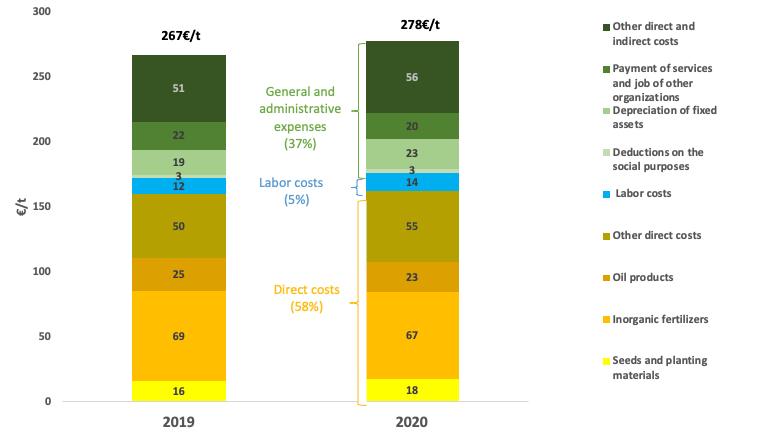

Ukraine is a competitive agricultural power. According to government figures, rapeseed production in Ukraine cost €278 per tonne in 2020, compared to €428 per tonne in France Ukrainian rapeseed is therefore 54% cheaper to produce than French rapeseed.

Figure 18 - Figure 18 - Detailed cost of production for rapeseed in Ukraine, 2019 and 2020 (Source : based on data from Detailed of production for rapeseed in Ukraine, 2019 and 2020 (Source : based on data from the State Statistical Service of Ukraine (SSSU)). the State Statistical Service of Ukraine (SSSU)).

The cost of producing rapeseed is generally higher than that of cereals or sunflowers. In Ukraine in 2020, the production cost for rapeseed was 20% higher than sunflower and 155% higher than corn. This is primarily because rapeseed production requires larger inputs of fertilisers and plant protection products.

Even with Ukraine’s more fertile soils, the proportion of fertiliser costs is higher for rapeseed than for other crops Inorganic fertilisers represent a larger share of the total cost for rapeseed, making up 24%, compared to 15% for both corn and sunflowers, and 21% for wheat (2021) Rapeseed tends to have a higher demand in nitrogen than cereals or sunflowers, needing 7 kg N per quintal of grain, as compared to 3kg/q for wheat, 2 1kg/q for corn and 4 5/q for sunflower (TerresInovia, BASF, AgroLeague)

Rapeseed is also more sensitive to pest pressure and thus generally requires more plant protection products and treatments. It typically receives more treatments than cereals or sunflowers. The Indicator of Frequency of Treatment (IFT) for rapeseed is generally higher than for other crops: 6.4 for rapeseed, compared to 2.9 for grain corn, 4.7 for all wheat combined, and 2.4 for sunflowers. Sugar beets, on the other hand, are treated even more frequently, with an IFT of 6.7 (total IFT including seed treatments, data for France, Agreste 2021).

The specific costs for plant protection products are not detailed in the data provided by the SSSU. It is possible that these costs are included under “other direct costs”, which could explain why the proportion of these costs is higher for rapeseed (20%) compared to cereals (15% for wheat and 12% for corn) or sunflower (15%)

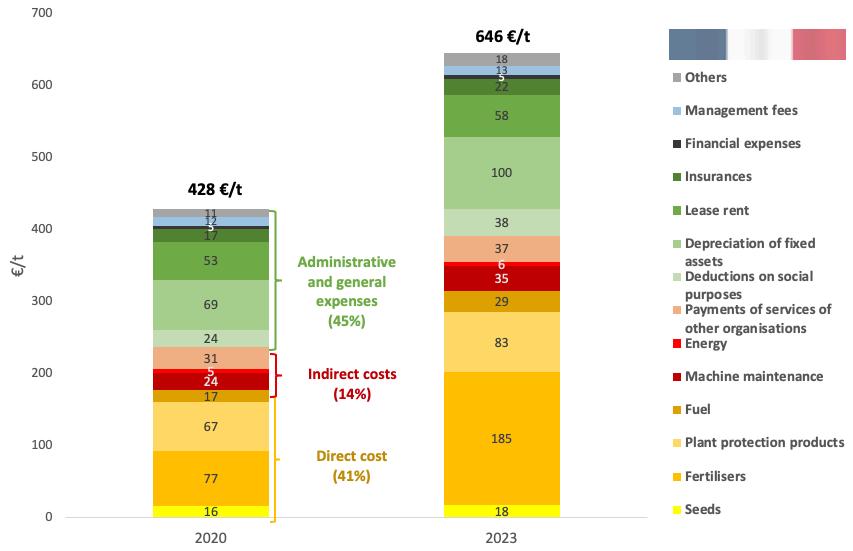

No data were found for the average cost of rapeseed production in the EU, hence available data from France were used as a comparison. In 2020, the cost of production in France was 1.5 times higher than in Ukraine.

Figure 19 - Figure 19 - Detailed Detailed cost of production for rapeseed in cost of production for rapeseed in France France, 2020 and 2023 (Source : FOP based on , 2020 and 2023 (Source : FOP based on Terres Univia Terres Inovia economic observatory of CerFrance data). Terres Univia Terres Inovia economic observatory of CerFrance data)

This cost difference is mainly due to lower labour costs and much lower depreciation costs in Ukraine. Most notably, the cost of deductions on social purposes were 8 times more expensive in France and accounted for 6% of the total cost, compared to 1% in Ukraine. Costs related to the depreciations of assets were 3 times higher in France than in Ukraine.

In France, based on the observed sample, the largest sources of expense were fertilisers (18% or 77€/t), plant protection products (16% or 67€/t), and depreciation of assets (16% or 69€/t). Land lease costs also represented a significant share at 12% (53 €/t).

In Ukraine, the largest costs were fertilisers (24% or 67€/t), other direct costs (which presumably include plant protection products, 20% or 55€/t, and, to a lesser extent, oil products (8% or 23€/t), which includes both fuel and lubricants.

Direct costs, although slightly higher in absolute value, represented a smaller proportion of the total production costs in France. Similarly, oil products represented 4% (17 €/t) of costs in France compared to 8% (23 €/t) in Ukraine.

On the other hand, general and administrative expenses made up a larger proportion of costs in France. Most notably, depreciation of assets and social contributions represented 16% and 6%, respectively, compared to 8% and 1% in Ukraine.

However, in France, and more broadly across the EU, operational costs saw a sharp increase in 2023, driven by the surge in fertiliser prices, which began in 2021. Overall, between 2021 and 2024, the total production cost per hectare for rapeseed increased by 40%. In 2024, French Oilseed Producers Federation (FOP) forecasts a slight decrease in variable costs (notably fertilisers), though these will remain well above 2020 levels. Additionally, structural costs are expected to continue rising, with an increasingly pronounced "scissor effect".

Compared to other field crop sectors, rapeseed production in Ukraine is less dominated by very large farming structures, including the 110 agro-holdings.

Entreprises under 1,000 hectares account for 73% of the national rapeseed production. However, the concentration of production by very large structures remains significant. The 170 companies with over 1,000 hectares, representing only 4% of all companies, generate 26% of the total production. This concentration is even more pronounced in oil production and the export of rapeseed products. In 2021, just five companies, including two agro-holdings, were responsible for 92% of oil production.

If Ukraine were to join the European Union and maintain its current production methods, the country would become the EU's leading rapeseed producer. Ukraine would account for 24% of the EU's rapeseed production and 4% of oil and meal production.

Ukrainian rapeseed production has increased by 57% compared to the pre-war period (average 2018-2021), driven by an expansion in cultivated areas. Over the same period, oil production surged by 174%, fueled both by record harvests and the impact of the EU's restrictions on rapeseed imports in 2023. Meanwhile, Ukrainian exports of rapeseed seeds and oil rose by 37% and 170%, respectively.

The opening up of the European market to Ukraine has resulted in an influx of rapeseed products. Although the EU was already receiving the vast majority of Ukrainian rapeseed before the war, imports from Ukraine increased by 28% (+600,000 tonnes) in 2023/24 compared to 201821. In 2023/24, the EU received 93% of Ukraine’s rapeseed exports (2.8 million tonnes), up from 83% in 2020/21. Imports of rapeseed oil were multiplied by 2.6 times (+100,000 tonnes), a trend that began in 2020/21, despite the fact that total EU imports did not significantly increase. have not risen significantly. Only imports of rapeseed meal seem to be following a different trend.

In 2020, the cost of producing rapeseed was 1.5 times higher in France than in Ukraine. This cost difference is mainly due to lower labour costs and much lower depreciation costs in Ukraine.

Appendix 1: Romania - rapeseed imports and exports. (Source: based on Eurostat data).

(a)importsofrapeseedfromallovertheworld

(b)Exportsofrapeseedtoallcountriesallovertheworld

Appendix 2: Poland - rapeseed imports and exports. (Source: based on Eurostat data).

(a)importsofrapeseedfromallovertheworld

(b)Exportsofrapeseedtoallcountriesallovertheworld

Appendix 3: All 110 Ukrainian agro-holdings listed in 2021, classified by cultivated area.Source:Latifundistandofficialcompanywebsites.

MHP (Myronivsky Hliboprodukt)

UkrLandFarming

Agroprosperis (New century Holding) wheat, corn, soybeans, rapeseed, sunflower

soya, sugar beet, winter wheat (including winter wheat seed), sunflower, winter rape, maize

Continental Farmers Group maize, wheat, rapeseed, sunflower, barley, soybeans, potatoes

Epicentr Agro winter wheat, rapeseed, sunflower, corn, soybean

-laying hens, dairy and beef cattle -sunflower oil

Sumy Kiev

Vinnytsia

Ternopil

Khmelnytsky

Lviv

Ivano-Frankivsk

Dnipropetrovsk

Lviv

Ivano-Frankivsk

Ternopil Rivne

Zhytomyr Khmelnytskyi

Dnipropetrovsk

Sumy

Poltava

Zhaporizhia

Mykolaiv

Cherkassy

Kiev

Donetsk

Volyn Lviv

Ternopil Rivne Chernivtsi Khmelnytsky Zhytomyr Vinnytsia Kyiv Cherkasy Mykolaiv Chernihiv Sumy Poltava Kharkiv

Poltava Vinnytsya Zhytomyr Ternopil Khmelnytsky

-laying hens, broilers, dairy and beef cattle -sunflower oil

laying hens, dairy and beef cattle

Chernihiv Kharkiv -sugar refinery -dairy cattle -soy processing

Ternopil Lviv Khmelnytsky Chernivtsi

Ivano-Frankivsk

Ternopil Vinnytsia Khmelnytsky Zhytomyr Cherkasy

Kiev

-starch production -seed production (420 tons/day)

-fertilizer production -wheat flour production -dairy cattle, beef cattle, pigs

winter wheat, winter barley, spring barley, maize, soybeans, winter rapeseed, sunflower, chickpeas, phacelia, peas

Privat-AgroHolding corn, soybean, sunflower, wheat, sorghum

Vitagro

winter wheat, winter barley, winter rye, spring barley, maize, soya, winter rapeseed, sunflower

AgroVista (former UkrAgroCom and Hermes-Trading)

wheat, barley, corn, sunflower, canola, peas, sugar beet

Luhansk -laying hens, dairy cattle -bakery

Sumy Kiev Vinnytsia Ternopil Khmelnytsky Lviv

Ivano-Frankivsk

Dnipropetrovsk

-laying hens, broilers, dairy and beef cattle -sunflower oil

Zhytomyr Kharkiv Chernihiv Odessa Cherkasy -

-dairy cattle, beef cattle, pigs -sugar refinery -wheat flour production -bakery

-seed manufacturing. Line 1 = corn, wheat, barley, peas, soybeans, sunflower; production capacity 150200 tons/day; 130 employees. Line 2 = flax, coriander, spelt; capacity 75 tons/day; 60 employees. -Irrigation system

Poltova dairy cattle, beef cattle

Khmelnytsky Ternopil Rivne

Kirovohrad Dnipropetrovsk

-horticulture (fruit and vegetables) -dairy cattle -seed production (wheat, soya, rapeseed, mustard, peas, barley) -sunflower and rapeseed oil

-dairy and beef cattle -sugar refinery

Svitanok wheat, barley, corn, peas, soybeans, sugar beets, potatoes, tropical crops (lemon, feijoa)

Agrotrade wheat, corn, sunflower, winter wheat, spring barley, buckwheat

Zakhidnyy Bug cereals, industrial and forage crops

Dnipro Agro Group

Dnipropetrovsk Kirovohrad -beef cattle, pigs -meat processing -bakery -pasta production

Kharkiv Poltava Sumy Chernihiv seed production (sunflower, corn, barley, buckwheat, soya, winter wheat)

Lviv Ternopil -seed production -breeding

Chernihiv Kyiv Poltava Sumy Zakarpattia dairy cattle

Agroprodservis wheat, barley, sunflower, soybean, spring barley, rapeseed, peas, sugar beet

Zhytomyr Kiev Cherkasy Poltova Kivorhad -beef cattle, dairy cattle, pigs -production of seeds, fertilizers and plant protection products

Vinnytsia Zhytomyr Khmelnytskyi dairy cattle, pigs

dairy cattle, beef cattle, pigs

Ternopil Ivano – Frankivsk Lviv Kherson -pigs, broilers -seed production -meat processing (preserves, sausages)

-meat processing

Agrospetsservis (I&U Group)

sunflower, corn, buckwheat, sugar beet

Kirovohrad rafineries (sugar)

Zhytomyr Kharkiv Khmelnytski Kiev Tcherkassy Kirovohrad dairy cattle

Southern Agricultural and Export Company (PAEK) sunflower, winter wheat, winter barley, winter rape, maize, peas, oats, millet

Svarog West Group

sunflower, sugar beet, corn, wheat, soybean. Also flax, naked pumpkin, beans, malting barley, medicinal chamomile.

Khmelnytskyi Zhytomyr Chernivts

-sugar refinery -bakery

-livestock: sheep, pigs, beef cattle -Production of briquettes (alternative fuel) from straw and other crops.

-production of sunflower pellets (an alternative to fuel) -freshwater fishing -farm machinery rental

-beef and dairy cattle -arboriculture: apples, pears, apricots, cherries -seed production

-forage production -soybean oil production -sugar refineries -biogas plants -livestock: turkey, cattle, pigs -meat processing Holding Agro Region

Khmelnytsky Zhytomyr Kiev Chernihiv

-animal feed production -poultry farming, broiler poultry -chicken meat processing

Zemlya i volya

-pig farming -flour production

Beta Agro Invest (B.I.G. Harvest Group)

Main crops: winter wheat, sunflower, corn. Also barley, rapeseed, alfalfa, mustard and chickpeas.

AgroGeneration winter wheat, rapeseed, malting barley, maize, soybean, sunflower, peas

Ekoprod buckwheat, thistle, millet, rye, fig, corn, oats, barley, wheat

TPK Agroalyans cereals, pulses, oilseeds

Kirovohrad Mykolaiv Chernihiv Odesa

-tomato seed production -processing (tomato paste and powder)

-livestock: pigs, genetic center -soybean processing: oil and meal (up to 250,000 tonnes per year)

Donetsk Chernihiv

-livestock: dairy cattle -services: road transport of agricultural and other products on Ukrainian territory

Kharkiv -

-livestock: dairy cattle, poultry, pigs, fish -production of dairy products

KharkivAgricom Group wheat, oats (+ glutenfree), sunflower, corn

Zhytomyr (7000) Chernihiv (9000) Luhansk (11500 ha, pas d’avoine. 450 non irriguées)

-cereal flakes factory, Chernihiv (capacity of 12,000 tonnes of flakes/year) --> export

Zelenaya dolina (Terra Food) wheat, barley, sunflower, sugar beet, rye, corn, soybeans, canola

Agro-industrial Corporation "USPIKH" wheat, barley, corn, soybean, sunflower, rapeseed

Buchachagrohlibpro m wheat, barley, sunflower, corn

Selhozprodukt corn, wheat, sugar beet

Agropromyshlennay a Kompaniya Roskoshnaya

beef cattle, dairy cattle

-seed production -breeding: dairy cattle, beef cattle (including bulls) -production of wheat flour and other cereals -honey

-flour production -fodder production -sugar refinery -pasta production -biogas plants (2)

livestock: pigs, sheep, goats, dairy cattle

Kusto Agro wheat, corn, sunflower, soybean, rapeseed

Zhytomyr Vinnytsia Khmelnytskyi

-forage production -livestock: pigs -slaughterhouse and meat processing -B2B and B2C sales

Lviv Ternopil Khmelnytskyi Kiev Chernihiv Dnipropetrovsk Sumy Poltava -dairy cattle -10 processing plants: 4 dairy (Lviv, Chernihiv, Sumy, Dnipropetrovsk ); 6 cheese (Khmelnystkyi, Chernihiv, Poltava, Sumy (2))

-dairy cattle, 1 dairy farm Other: Roads, rails and construction; Maritime and offshore; Logistics solutions Volyn-ZernoProduct wheat, soybeans, rapeseed, sugar beet, barley, maize, peas, permanent grasses

processing of agricultural products (sunflower, animal feed, hen eggs), storage and transport services

Hmelnitsk Mlyn

Winter and spring wheat, winter rapeseed, barley, soybean, sunflower, maize, sugar beet, peas, sorghum, poppies

flour production (2 mills, Khmelnytskyï)

Cherkasy Poltava -seed production -agricultural product processing

KSG Agro

winter wheat, barley, rapeseed, spring sunflower, maize, sorghum, winter and spring peas

Prodexim cereals, sunflower

Dnipropetrovsk -pig farming -forage production -5 pellet boilers; some converted to biofuel (wood pellets) -plans to complete construction of a pellet plant (60,000 t/year)

-sunflower oil production (including organic) -arboriculture: apples, pears, grapes, peaches, cherries, raspberries, blackberries VV Agro corn, sunflower, cereal crops

Volyn Zhytomyr Vinnytsia Ternopil Ivano-Frankivsk Odesa beef cattle and pig farming

Agroteh garantiya

Avis UkrAgro corn, soybeans

Arnika organic soy, corn, sunflower, mustard, lentils, flax, millet, hemp

Agrofirma Pyatihatskaya wheat, barley, maize, rapeseed, sunflower 17,000

Sumy -dairy cattle, laying hens -farm services (harvesting)

Cherkasy Poltava -production of organic sunflower oil -forage production (soy processing)

Kirovohrad

Chongar winter cereals, sunflower 17,000

Zgoda cereals, oilseeds, vegetables 17,000

Pytidni cereals, oilseeds, industrial crops 16,500

Agro Oven wheat (10,000 t), feed wheat (20,000 t), maize (50,000 t), sunflower (15,000 t), potato (7,000 t), millet

Dnipropetrovsk

-livestock: pigs (500 head), cattle (1,000 head), poultry (2,000 head) and sheep (500 head) -Mill, oil mill, bakery and pastry shop

sheep farming

-broiler and layer hens, pigs, beef cattle -artificial insemination stations, breeding plants -compound feed plant -meat processing plant -bioenergy plant -restaurants, stores

-animal feed production -livestock: pigs, horses, aquaculture Kishchentsy

wheat, barley, malting barley, sugar beet, corn, rapeseed, soybeans, vegetables, perennial grasses

livestock: dairy cattle (350 head), pigs (400 sows)

-harvesting services -processing and storage of agricultural products -reproductive seed processing -import-export operations -commercial, industrial, intermediation, marketing and trading activities

Vinnytsia Khmelnytskyi Ternopil storage

-grain storage -grain shipping (up to 100,000 tons per year for each of the 2 companies)

-production of dairy products: 5 production plants (15,252 tonnes of cheese; 3,295 tonnes of dairy butter; 51,982 tonnes of milk; 104,250 tonnes of fermented dairy products; 11,243 tonnes of baby food; 288,533 tonnes of milk supplies)

-Breeding: broiler hens (incubation capacity of 94 million eggs per year, and daily planting of 60 to 62 million young broiler chickens per year). -meat product processing (19,200 head/day) -animal feed production (18,000 t/month --> over 225,000 t/year) Rosukprod cereals and oilseeds

trade in cereals and oilseeds, oil production: sunflower, soybean, calabash

Kherson breeding, seed production

Zaporozhie Agro sunflower, winter wheat, peas, perennial grasses, alfalfa, corn for silage 14,400

maize, winter and spring wheat, sunflower 13,000

dairy cattle farming

Donetsk -livestock: pork (14,500 tons live weight per year), poultry -meat processing -compound feed production

Livestock: pork, dairy cattle (plant, processing capacity - 300 t/day) APK Dokuchaevskie Chernozemy

Poltava Kharkiv -seed production -fruit and berry production. -animal husbandry.

-seed selection -livestock: dairy cattle, pigs, ostriches Biolend cereals, oilseeds 10,000

Zhytomyr -pig farming -animal feed production (2t/h capacity) Pan Kurchak maize, wheat, barley, rapeseed, soya, sunflower 10,000

Volyn -feed mills (farm animals, birds and fish) -broiler and layer hens

Stepnaya maize, winter wheat, winter and spring barley, sunflower

Cygnet Agrocompany maize, sugar beet, winter wheat, soybean, sunflower

Olimp corn, wheat, soybeans, sunflower

Oskar cereals, industrial crops

Preobrazhenskoe wheat, barley, maize, millet, sunflower, rapeseed, oats, peas, soybeans

VPK Agro vegetables

Dnipropetrovsk

-seed trade (corn hybrids, winter wheat, sunflower hybrid barley, etc.) -livestock: pigs (6,000 head by 2021)

Zhytomyr Vinnytsia

breeding meat processing and trade

irrigation systems