Common Agriculture Budget EN - Challenges & Dynamics

BUDGET NEGOCIATIONS : UNDERSTANDING THE DYNAMICS & CHALLENGES FOR AGRICULTURE

The 2028-2034 budget negotiations will be one of the most complex considering the national constraints, the need to reimbourse COVID debt as well as enlargement talks with Ukraine. Overview of the key drivers and figures at stake to secure a strong support to agriculture as a strategic sector for Europe.

Without waiting for the new college of Commissioners to take office, the European Commission has launched the discussions on a potential overall of the EU budget for 2028-2034. These discussions are the scene setter for the draft Multi-annual Financial Framework proposal, expected for summer 2025 To disrupt the negotiations and change the parameters of a complex budget equation, the Commission leaked preliminary ideas for drastic changes in the structure of the next MFF, particularly by merging 530 EU programs into a single €1,2 trillion fund, called Pillar I. Two additional pillars would focus on services and major investments, including defense and enlargement The present note provides an assessment of the potential consequences of those initial ideas, explaining the main parameters at stake for EU agri-food sector Negotiations around the EU budget are expected to be just as crucial as they are complex, particularly due to the critical budgetary situations in several Member States, the need to repay the common debt contracted during the Covid-19 pandemic, the expenses related to the war in Ukraine, and the negotiations around the upcoming enlargement In this context, uncertainty remains on which place will be given to the CAP and agricultural policies in the final budgetary allocations.

In preparing the European Union’s financial perspectives for 2028-34, the European Commission is trying on the one hand to create financial margins without any new financial space, and on the other hand, to pressure Member States on funding the EU budget while preserving its role as the decision-maker.

Traditionally, the Commission would

first discuss with capitals about acceptable cuts to the budgets of major European policies and the acceptability of a slightly growing overall EU budget In this first-round exercise, the Common Agricultural Policy (CAP) was often presented for scrutiny (with proposals like a 30% cut in 2018). In today’s context of budgetary frugality, the Commission

is trying a different path, drawing inspiration from the (administrative) reform of the CAP it proposed in 2018

THE CAP AND COHESION POLICY AT RISK

Within Pillar I, all major EU policies would be grouped Member States would be asked to define national strategic plans, setting out their priorities and how they wish to use the money allocated to them under various policies This scheme would delegate to Member States the responsibility for implementing most EU policies according to their current national priorities, except for a few "entry" conditions for funding, which the European Council (which must decide unanimously on financial matters) would likely water down Much like the 2018 CAP proposal, this reflects a broad renationalisation of all European policies under Pillar I Europe would only remain united in Pillar III (enlargement, major European investment plans).

The creation of such a fund would introduce high flexibility in budgets previously allocated to specific policies One can assume that both the CAP and the cohesion policy whose budgets are always highly sought after in the absence of other truly common policies would not have their funding guaranteed. Funding would be allocated at the start of the period based on national priorities and likely adjustable along the way, especially if disbursements fall short of expectations

INADEQUATE CONDITIONALITY & INVESTMENTS

Regarding the CAP, the Commission illustrates its proposal with two examples that raise questions about the understanding of agricultural issues by its budget experts. It suggests making access to CAP funds conditional on promoting organic farming a rather original example, given that the Farm to Fork objective of 25% of land under organic farming neither aligns with market demands, food sovereignty imperatives, nor sustainability goals in Europe. As for the "investment" chapter of the CAP, the Commission cites direct payments as an example While these payments are vital for farmers' incomes, is this the most relevant example when aiming to tackle the dual challenge of restoring profitability to European agriculture while pursuing enhanced sustainability? Not to mention the accession talks with Ukraine.

EU SINGLE MARKET PUT IN JEOPARDY

The comeback to such a nationalcentric approach could lead some Member States to focus funding on a few sectors in order to subsidise them more so that they can gain an advantage over their European competitors on the single market. This use of EU money would not lead to European growth, but to more fragmentation and, in the end, a waste of the taxes paid by European citizens. This idea of a large common fund likely ties into the Commission

President’s recent mantra (at least regarding the CAP) of having a more targeted budget and more targeted measures. If improving effectiveness

is a common goal, doubts remain concerning the fact that this single fund approach is just a rhetoric used to justify a reduced EU Agri budget.

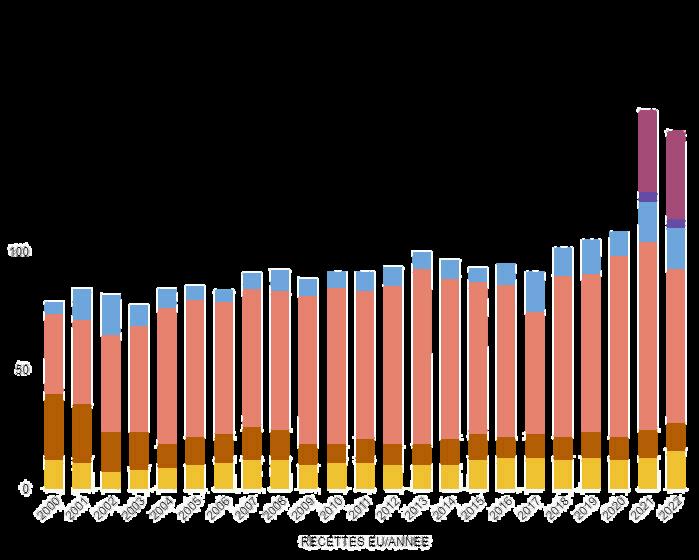

WHERE DO THE EUROPEAN UNION’S REVENUE COMES FROM ?

Traditional own resources, consisting of customs duties and agricultural duties.

VAT-based own resources, which involve transferring a share of the estimated VAT collected by Member States

GNI-based own resources, which are derived from a percentage levy on the Gross National Income of Member States. Originally intended to be used only if other own resources were insufficient to cover expenses, these now fund the majority of the Union's budget. The GNI-based resource has doubled since the 2000s and currently accounts for about 70% of own resource revenue

Plastic-based own resources, which, since 2021, take the form of a national contribution calculated based on the amount of nonrecycled plastic packaging waste

Borrowing under the Next Generation EU recovery instrument, which has been authorized as an exceptional and temporary measure (750 billion euros in 2018 prices)

Other revenue and correction mechanisms. Rebates have been maintained for Austria, Denmark, Germany, the Netherlands, and Sweden These rebates are funded by additional contributions from other Member States.

(as

expanditure)

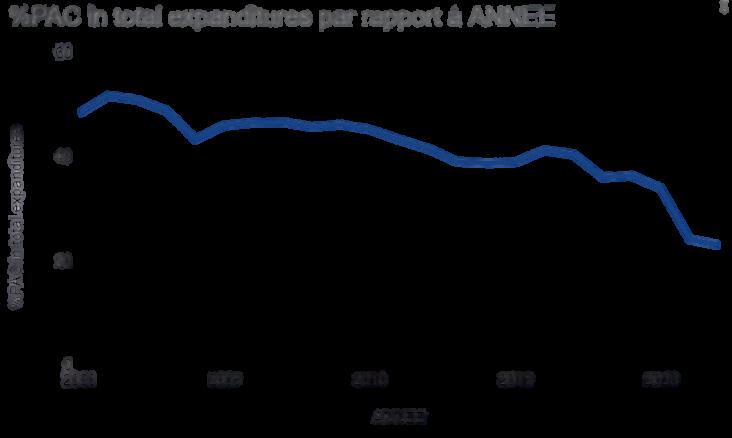

(% CAP in total EU expenditure excluding NGEU)

Graph - Evolution of European revenues since 2000 by category (Billions €, constant 2000 euros) Source: Author's elaboration based on EC data

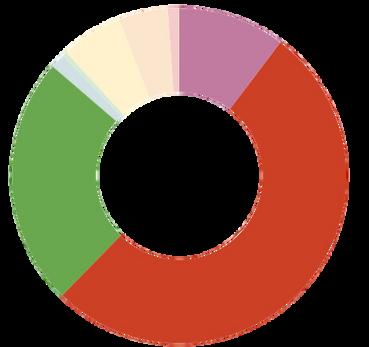

EU TOTAL EXPENDITURE IN 2022

(CONSTANT €, 2000)

Natural Resources & Environment

In wich :

European Agricultural Guarantee Fund (70%)

European Public Administration Neighbourood & the World 6 % 5

European Agricultural Fund for Rural Development (26%)

The CAP's share of the EU budget has fallen over the last 20 years This decline is mainly due to CAP reforms and the increasing share of other policies in EU spending The sharper falls in 2021 and 2022 are linked to the EU's additional overall spending on Next Generation EU (NGEU) funds Excluding the NGEU funds, the CAP currently accounts for 31% of the budget.

ChangeinMemberStates' netcontributions(%) 2023/2010inconstanteuros COUNTRY

Single Market, Innovation & Digital

Cohesion, Resilience & Values

EU TOTAL EXPENDITURE : 152 B€ (2022 values in constant 2000 euros) 10%

Graph Distribution of European expenditures in 2022 (%). Source: Author's elaboration based on EC data

Comparison of CAP rate of return and countries' net contribution to the European budget :

THE THREE CHALLENGES AROUND EU BUDGET NEGOTIATIONS

Inflation, the enlargement to Ukraine, the capacity or not to rebuild a common vision and willingness to overcome global challenges together will be some of the major drivers for the next Multiannual Financial Framework negotiations.

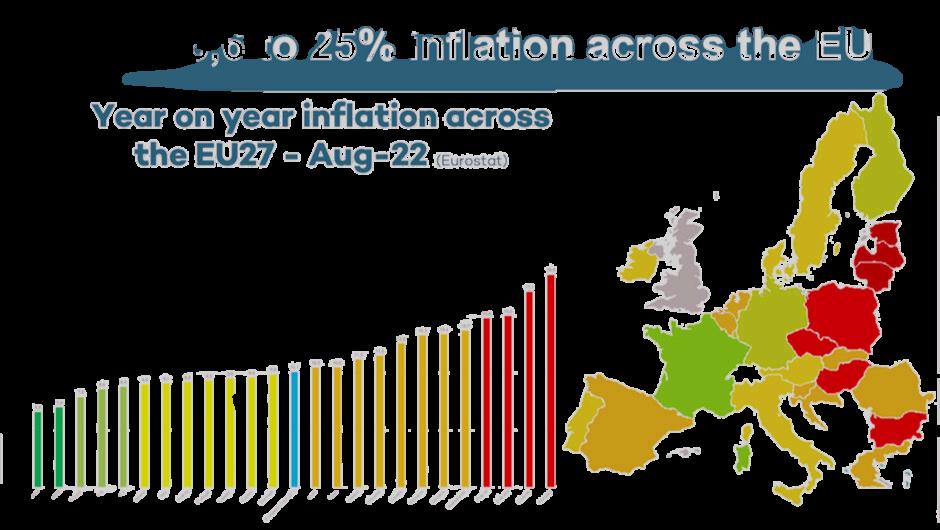

Inflation

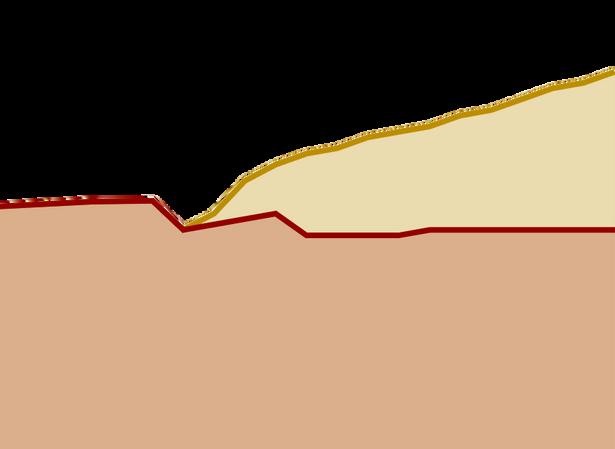

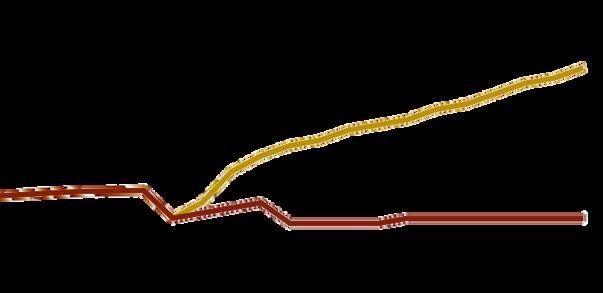

Without an indexation to inflation for the period 2028-34 - and assuming modest inflation of 2% per year - the economic value of the CAP by 2034 would be more than halved (-54%).

Average inflation in the EU is close to 10%, far from the 2% forecast used in the 2019 negotiations Some European countries are well above this average This return to high inflation has reduced the real value of the support provided, which was slashed by 30% over 20 years. The real value of the CAP budget will fall by €84.57 billion over the period 2021-2027 compared to 2020, if we stick to the forecast of moderate inflation between now and 2027 The first pillar will lose €6860 billion, and the second pillar €15.97 billion. This deficit represents a 18% drop in the total value of the CAP budget over the period compared to 2020, ie almost 2 years less in direct CAP aid.

For aid in 2027, this will mean a shortfall of 26% in real support (-25% for direct aid, -30% for the 2nd pillar), severely affecting farmers' incomes (CAP support represents on average 51% of European farm incomes) and their ability to invest To ensure that CAP funding does not lose value year after year, it is necessary at the very least to re-evaluate the budget each year by adjusting it to inflation, otherwise the ambition of a more sovereign European Union that succeeds in its transition will at best be a pipe dream and at worst a path towards economic, environmental and social regression, as the Draghi report underlines

CAP BUDGET 2014-2020

415 Billions CAP BUDGET 2021-2027

387 Billions

85 B€ MISSING

to maintain the 2020 value of CAP

For 371 million today to have the same value as they would have had in 2020, they would have to be increased to 481 million.

Map - Year on Year Inflation across the EU (August 2022). Source: Eurostats. Graph - EU Harmonized Index of

Source: Eurostats

by 2034 if no indexation to inflation

‘FUNDING ‘deficit

The gap between the two curves corresponds to the theoretical amount that would have to be added to the CAP budget to compensate for the erosion in value due to inflation This funding ‘deficit’ represents a loss of value in real terms

CAP BUDGET B€ per year

Corresponds to the amount of CAP allocated each year

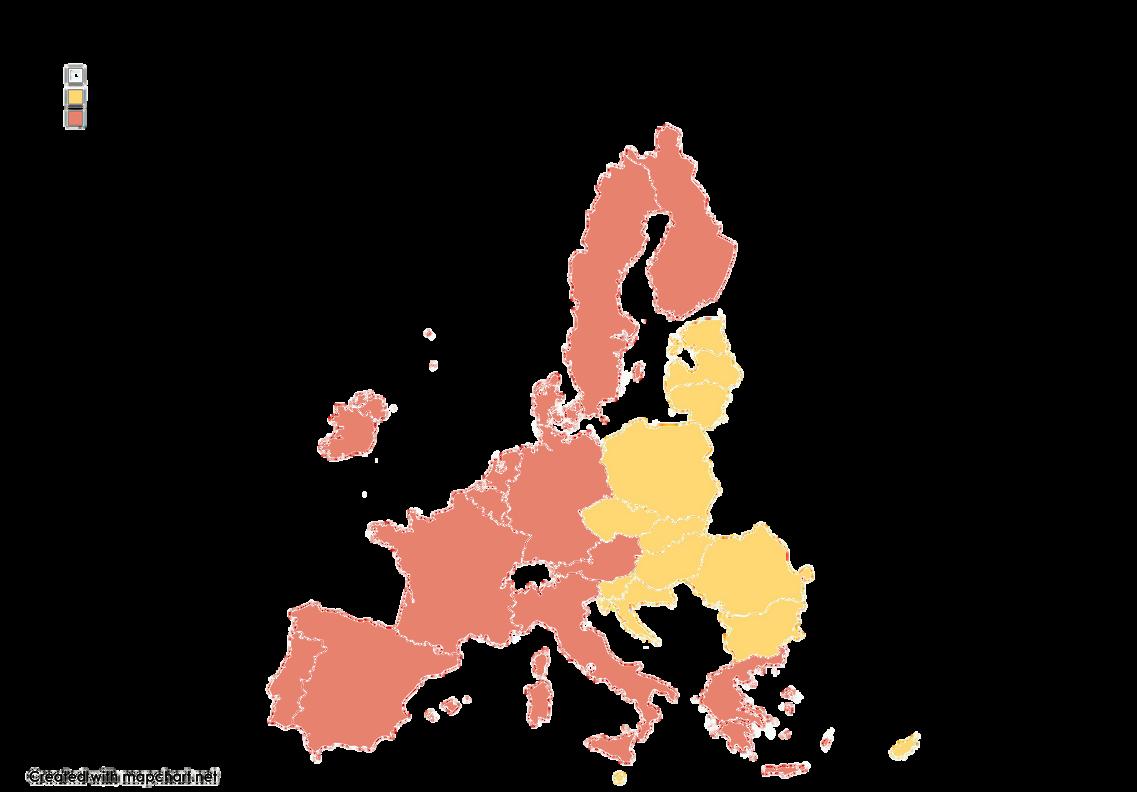

Enlargement to Ukraine

As a member of the EU, Ukraine could claim around 20% of the CAP budget and a substantial share of the budget allocated to cohesion policy.

CAP BUDGET AND COHESION BUDGET

Behind the discussions on the European financial framework for 2028-2034, the prospect of Ukraine joining the European Union, its cost and its financing will loom in everyone's mind.

Ukraine could claim a substantial share of the budget allocated to cohesion policy (for the record, Poland currently receives just over 20%).

Moreover, Ukraine is a competitive agricultural power. Labour costs, fertiliser and seed costs, and depreciation are lower in Ukraine than in the EU Cost of production of Ukrainian maize is 25% cheaper. Ukrainian wheat is 39% cheaper than European wheat to produce Agriculture plays a major economic role in the country, accounting for 10.9% of GDP in 2021 and nearly 14.7% of employment (compared to 1.4% and 4.2% in the EU). Given the size of its UAA, Ukraine could claim 20% of the CAP budget

The competitiveness of Ukrainian agriculture makes it inevitable to consider the allocation of future CAP funds between the various existing measures and/or the emergence of additional tools to prepare European agricultural sectors for the challenge of accession.

The economic profile of Ukraine, and the development recorded in the EU12 countries since their accession, also raises the question of the scale of cohesion policy (guidelines, budget, distribution) over the period 2028-2034

The communitybased approach at stake

The Commission’s proposal for the 2028-2034 MFF would transfer greater responsibility to MS, renationalising most of EU policies.

A BUDGET INCREASINGLY DEPENDANT ON NATIONAL CONTRIBUTIONS

Since the years 2000s, the European Union’s budget has been relying more and more on national contributions compared to its own resources. The transition from EU15* to EU27* saw total national contributions increase by 95% Some 82% of this increase was financed by the EU15* countries, the price paid by states for building a stable, peaceful Europe and constructing a large single market Following this enlargement, the EU12 countries accounted for 9% of net European national contributions, and received 18% of the CAP budget.

A DECREASE OF “OLD” MEMBER STATES’ CONTRIBUTIONS SINCE 2010

Between 2010 and 2023, total MS contributions decreased by 5%. At the same time, EU12 contributions grew to 13% in 2023 and some of these Member States might even become net contributors in the future, in case countries joined the Union. These changes have significant repercussions on the traditional balance of power playing out in budgetary negotiations and must be kept under observation.

Concerning the agricultural sector, the goal for Member States and especially for net contributors is to reduce their national contributions while improving and maximising the CAP rate of return. 2028-34 MFF: The idea of a new structure of MFF budget with a single pillar (and fund) merging all existing main EU policies would open the gate to a broad renationalisation of these policies, notably the Common Agriculture Policy.