ARE YOU BAD AT DEBT REVIEW?

E XCE LL ENCE IS D OIN G ORD IN A R Y THING S

E XT R AO RD I N A RI LY W E L L

– John W. Gardner

E XCE LL ENCE IS D OIN G ORD IN A R Y THING S

E XT R AO RD I N A RI LY W E L L

– John W. Gardner

Debt review is one of the best tools available to help South Africans take control of their financial situation.

Debt Review helps lower your monthly debt repayments, protects you from aggressive collections, and gives you a clear path to settling all your debts. When done properly, debt review brings relief, peace of mind, and eventually the prospect of becoming debt free.

But not everyone makes it to the end. Some people fall out of debt review early, not because the system failed them, but because they unknowingly worked against their own debt review.

Some people are just bad at being in debt review.

Are you one of them?

Well, if you’re in debt review (or thinking about starting) you need to know the red flags that could signal danger.

Let’s look at 10 signs that you might be sabotaging your own success— and what to do instead.

1. You take too long to send your Debt Counsellor information

When you start debt review you need to send a lot of documents back and forth between your Debt Counsellor and Attorney.

If your Debt Counsellor asks for documents or updated details and you delay, it slows down your progress.

This can result in missed deadlines, or incorrect proposals going to your credit providers. If you don’t send your attorneys a signed and commissioned affidavit for use at court (saying you know about and agree with the debt review) your whole court case can collapse and be thrown out of court.

RATHER: Respond quickly. Even if you’re busy, prioritise your debt review. After all, it’s your financial future at stake!

2. You don’t actually look at, or stick to your budget

A budget is your roadmap through debt review.

Ignoring it is like driving blindfolded—you’ll end up in trouble.

If you overspend or don’t track your expenses, you’re at risk of running out of money for essentials or your monthly payment.

RATHER: Try to stick to your budget. Review it monthly, and make changes with your Debt Counsellor if you find you can’t stick to it in its current form. It is a living thing and can’t be ignored.

3. You are meant to save but you are not doing so

When your Debt Counsellor helps you make up your initial budget (and helps you review it from time to time) they will be sure to include something towards saving.

Especially for annual costs like school fees or car services.

They may even suggest saving enough to cover an insurance claim excess.

If you skip this saving, those big annual expenses will wreck your monthly plan.

RATHER: Save something. Even if it’s a small amount, build that habit. Your future self will thank you.

4. You move or change jobs but don’t tell your Debt Counsellor

Major life changes affect your finances. Even if you hope they won’t... they will.

If you change jobs or move house and keep it to yourself, important legal documents could go to the wrong place, which means you might not even be aware of something super important.

RATHER: Keep your Debt Counsellor, attorneys, PDA and credit providers up to date with your work & home address to avoid any nasty surprises.

5. You change your mobile number or email address and don’t tell the Debt Counsellor

If your Debt Counsellor can’t reach you, they can’t help you.

Missed emails or calls might mean missed deadlines or important updates.

Your PDA needs to send you a monthly statement about your payments. If they have old numbers or email addresses you will lose track of your progress.

RATHER: Always keep your contact details current—it helps keep your plan on track and ensures you can track your progress.

During your debt review, your PDA (Payment Distribution Agency) sends you statements to help you keep track of your debt repayments.

Not checking them means you won’t notice any possible errors or mixups (they can happen).

RATHER: Compare your PDA statement to your bank statements. There will be some minor balance differences (your Debt Counsellor will explain why) but if something looks drastically off, speak up early.

7. You know about an upcoming challenge and do not talk to your Debt Counsellor in advance

Even in debt review, life happens—medical bills, retrenchment, or car trouble. A lot can happen over the span of 60 months*.

But not warning your Debt Counsellor ahead of time means they can’t help you make a plan.

RATHER: Talk to your Debt Counsellor. If you contact them early enough then they can often approach your credit providers to negotiate some sort of temporary change to your payment plan. That small step can protect your entire debt review.

* Most debt restructuring plans are set out over 60-months these days. Not all, but most.

Before debt review credit providers were lucky to get any payment at all. So, short payments don’t seem like a big deal. But even though paying less than the full amount each month may seem harmless—it breaks the agreement with your credit providers (and your court order).

It could give greedy credit providers the chance to duck out of the debt review. Even if that doesn’t happen, short payments can throw off the plan and the differences can add up over time. This can result in disappointment later, when you thought certain accounts would be paid off but because of extra interest and fees, they still have money outstanding.

This can delay paying off the next account. It can cause a domino effect, messing up your plan many months later. It also sends a clear message to the credit providers: that you don’t take the new arrangement serious.

RATHER: Live within your budget and pay the full planned amount, or talk to your Debt Counsellor if you see trouble coming.

9. You miss a debt review payment and expect the credit providers not to mind

Debt review is a legal process with a court order setting out what you have to pay, and what the credit providers must accept. It keeps the credit providers from playing dirty, but it also means you have to pay each month.

Skipping a payment can cause your whole debt review to fall apart. Credit providers might terminate their participation and take new legal action.

Just because you may have missed payments in the past before debt review, and it seemed nothing happened, you are now bound by the court order. So, no messing around.

RATHER: If you’re in trouble, speak to your Debt Counsellor before missing a payment—never afterwards.

10. You blame the Debt Counsellor for the actions of credit providers or collections agents

When you begin debt review all those nasty collections calls, sms, whatsapps and letters will dry up (not instantly). It will be a huge relief.

But it does not mean that none of your credit providers or their external collections agents won’t do something weird.

It is important to note that your Debt Counsellor doesn’t control credit providers or collection agents. Some people don’t realise that credit providers and collections agents can and do make mistakes.

And when something strange happens, they might make the mistake of blaming the Debt Counsellor.

RATHER: If something goes wrong, talk to your Debt Counsellor instead of blaming them. They can often sort it out, but only if you work together in good faith.

Did you spot anything you might need to work on?

Well, the good news is that each of these red flags is preventable. Debt review works best when you stay involved, stay honest, and stay in touch with your Debt Counsellor, PDA and attorneys.

They’re there to help—but only if you keep them in the loop.

If you’ve already fallen into one or two of these habits, it’s not too late.

Fix what you can, you’ve come this far—don’t let small mistakes cost you the chance to become debt free.

After all, you don’t want to be bad at debt review.

The last few weeks have been making my head spin. Every day there were new announcements about VAT (it will change, it won’t, it might, it didn’t).

Then there was so much talk about shifting political coalitions and coupled with that have been stories about Mr Trump and his mighty tariff chaos. Tariffs went up, came down, disappeared, reappeared, went up and then went up more, and honestly, I am a bit confused about where things stand right now. My brain hurts.

You see, our brains hate change. We like things to stay the same. Its predictable, its stable its familiar. This is much easier to handle than uncertainty. People don’t like uncertainty and neither do the markets.

Entering debt review is often a time of intense change for consumers. They have to trust someone else with their finances, they have to change the way they bank and spend and that’s a lot. And those changes all happen in a very short period of time, which makes it even more stressful.

Some people are not even able to make the adjustments needed to get to their first debt review payment.

Others who do successfully start, later begin to shoot themselves in the foot. There are many small decisions that can slowly tip the scales against you. In this issue we dive into some of those choices.

We also look at other role players in the industry, and the things they might be doing that could mean they are bad at debt review. But…we hope that you are good at debt review.

Our team have been busy with Debt Review Awards Peer Reviews and event planning. We look forward to being in KZN this year (24th of October). Even the Awards process is subject to a little change over time. But we are excited about the incremental changes that will make the Awards better than ever.

If your head is spinning like mine, take a deep breath. Change can also be good. Like if you are heavily in debt and use debt review to change your future. A change from debt slavery to becoming debt free.

DISCLAIMER

Debtfree Magazine considers its sources reliable and verifies as much information as possible. However, reporting inaccuracies can occur, consequently readers using this information do so at their own risk. Debtfree Magazine makes content available with the understanding that the publisher is not rendering legal services or financial advice. Although persons and companies mentioned herein are believed to be reputable, neither Debtfree Magazine nor any of its employees, sales executives or contributors accept any responsibility whatsoever for their activities.

Debtfree Magazine contains material supplied to us by advertisers which does not necessarily reflect the views and opinions of the Debtfree Magazine team. No person, organization or party can copy or re-produce the content on this site and/or magazine or any part of this publication without a written consent from the editors’ panel and the author of the content, as applicable. Debtfree Magazine, authors and contributors reserve their rights with regards to copyright of their work. We are an Ai friendly publication and enjoy working with our future overlords.

Winter is coming, and unfortunately, the Night King doesn’t bring discounts.

As the chill starts to set in across our part of the world, many people feel pressured to gear up with pricey new clothes. But staying warm doesn’t mean you have to break the bank.

Winter doesn’t have to freeze your finances and destroy your purse. By planning ahead, getting creative, and choosing wisely, you can stay warm and comfortable all season long and keep your wallet happy.

Here are six tips for keeping cosy without wrecking your wallet.

Dig through your wardrobe before you shop. You might have a jacket you forgot about, or a jersey that just needs a quick fix like a new zip or button.

A clothes swap get together is a fun (and free) way to freshen up your wardrobe. Invite friends or cousins over and trade items you no longer wear. What’s old to you might be brand-new to someone else.

Second-Hand

Thrift stores, charity shops, and online marketplaces like Facebook Marketplace or Yaga often have quality winter clothes at a fraction of retail prices. Many items have only been worn once or twice.

If you prefer online shopping, look out for sales and free delivery options. Use price comparison tools or apps to find the best deals. Just make sure the site is safe and legit before buying.

Instead of buying expensive bulky coats, consider thinner items that you could layer. A long-sleeve top under a jersey, under a jacket, can work wonders — and layering lets you adjust as the day heats up.

Set a spending limit before you hit the shops, and stick to it. It’s easy to overspend when you see “never to be repeated” sales (they will) but keeping your budget in mind helps you focus on what you actually need.

When you decide to enter debt review, you will be asked to complete several forms. Some will have information about what you earn and what you spend each month. This is typically on a Form 16 (an application form).

If you are married COP (in community of property), then both you and your spouse should sign any applications. You will also be asked to have an affidavit commissioned to use at court. This form should be signed in the presence of a commissioner of oaths (like a police officer).

Some Debt Counsellors use digital documents and you will be asked to sign on your device. Make sure you understand what it is that you are signing for and that you agree. If you need more clarity then just ask.

Statistics Netherlands reported that around 600 000 Dutch households were struggling to repay their debt. Around 100 000 were receiving debt assistance.

When overwhelmed by debt in Canada these days, consumers have several options to regain financial control under the Bankruptcy and Insolvency Act.

In the Netherlands, the Wet Schuldsanering Natuurlijke Personen (WSNP), or Debt Restructuring for Natural Persons Act plays a central role in providing a formal debt relief process. The law was established to help individuals facing significant financial difficulties by offering them an opportunity to legally discharge their debts after a period of repayment.

As of 2023, all municipalities in the Netherlands are required by law to offer debt counselling services to individuals in financial distress.

Municipal debt counselling (focus on the budgeting and counselling) is the first step for many people, and it ensures that everyone has access to guidance, no matter their income level.

These services help consumers explore debt management options and offer essential advice on budgeting and improving financial habits.

Debt counsellors in the Netherlands must meet certain qualifications to provide proper assistance. They often have extensive training and may be certified by organizations such as the Dutch Association for Public Credit (NVVK).

The NVVK ensures that its members adhere to a code of conduct and offers training programs to maintain high standards of debt counselling.

Counsellors may have backgrounds in law, finance, or social services, and must demonstrate knowledge of debt restructuring and related legal processes.

The NVVK also accredits organizations that provide debt counselling services, ensuring that these organizations operate with professionalism and integrity.

There are several options available to people experiencing financial distress in the Netherlands:

1. Sequestration or Bankruptcy: Individuals can opt for sequestration (which is similar to bankruptcy), if they are totally unable to repay their debts. This process involves the liquidation of assets to settle outstanding liabilities. Sequestration is typically considered a last resort and can have long-term consequences on an individual's credit.

2. Temporary Suspension of Payments: Before proceeding to the WSNP, individuals may request a temporary suspension of payments. This is granted by the courts for a period of 18 months, during which the individual’s debts are frozen while they attempt to resolve their financial issues. During this period, an administrator is appointed to manage the process and keep an eye on their spending, and a court hearing is held within a few months to determine whether the individual qualifies for full debt restructuring or if bankruptcy will be declared.

3. Voluntary Debt Restructuring (WSNP): For many individuals, the WSNP process is the most common method of dealing with unmanageable debt. The WSNP allows individuals to restructure their debts and enter a repayment plan with their creditors. After a certain period, often 36 months in the past, individuals may have their debts (excluding secured debts like mortgages) written off. Since July 2023, this process has typically been shortened to 18 months (but the court decides).

Once a person enters the formal WSNP process, they are granted a reprieve from their creditors, and a court-appointed administrator manages the repayment process.

Only unsecured debts, such as credit cards, personal loans, and unpaid bills, are typically included in the WSNP. Secured debts, like home mortgages or car loans, cannot be discharged through this process but will be factored in to budgets etc.

The administrator ensures that the individual complies with the terms of the debt restructuring plan, which includes monthly payments toward the unsecured debts. After the set term is completed, if the individual has adhered to the agreement, any remaining unsecured debt is officially forgiven, and the individual receives a clearance certificate, offering them a fresh start—a “clean slate.”

The costs associated with the WSNP are relatively low. Many debt counselling services in the Netherlands, including those associated with WSNP, are non-profit organizations, meaning that the fees are minimal, and the process is designed to be accessible to individuals regardless of their financial situation.

Interestingly the WSNP process is visible and will remain visible on the individual’s credit report during the duration of the restructuring process and for up to 5 years after completion. This can affect future

credit applications, as lenders may see the WSNP on the report. Those applying for new credit during or immediately after the WSNP process may face higher interest rates or less favourable terms, as lenders consider the risk of lending to individuals with a history of debt restructuring.

Debt management in the Netherlands offers several structured options for individuals to regain control of their finances, with the WSNP being a key process in providing relief for those with unmanageable debt. While the process can have lasting effects on an individual’s credit report, it offers a total fresh start once completed.

Each month while you are under debt review you should get a statement from your payment distribution agent on how they divided up your consolidated monthly debt repayment. This shows what amount went where. It will also give you a rough idea of the balances. If you have stopped getting these statements then check in with your Debt Counsellor and your PDA to make sure they have your latest contact information. Be sure to update them and your credit providers if you change an important contact email or number.

DC Partner PDA is operational for more than 15 years as a NCR registered payment distribution agency. Our exceptional customer service, together with our commitment to compliance ensures customer satisfaction.

DC Partner PDA is trusted by debt counsellors for secure and reliable debt review collections & distributions.

There are currently 1,653 registered Debt Counsellors in South Africa, but shockingly, over 3,143 other individuals who were once registered with the National Credit Regulator (NCR) have since left, or been removed from the industry.

Many of these former Debt Counsellors couldn’t run a sustainable practice, while others were caught acting unethically and had to be shut down.

This goes to show: being qualified is not the same as being good at the job.

Debt Counselling is a lifeline to consumers in need, but it is not an easy business to run well.

Here are ten red flags to look out for, that are a warning that you as a debt counsellor, might be bad at debt review.

Every business planetwide wants more clients, but if you are not getting any clients or hardly any, then you have a serious problem.

It’s tempting to blame the economy, but if your practice isn’t gaining clients, it won’t survive.

We all know that debt review income, while structured around ongoing monthly aftercare fees, is heavily slanted towards restructuring fees (since many people lack the discipline to stick with the process).

Without new consumers entering your pipeline to offset your churn, your business will eventually collapse, resulting in harming existing clients.

RATHER: If things are slow, it's time to learn, time to innovate or invest in marketing the right way. You need to know how to get clients if you have any hope of lasting.

Capturing information on the NCR’s Debt Help System is not just a nice-to-have—it’s part of your terms and conditions with the NCR.

If you fail to update records, you're showing your disdain for the NCR, and that will come back to bite you.

RATHER: Even though we know the system is pretty broken, do your part. They will eventually sort it out.

Taking payments directly from clients violates your NCR terms and conditions of registration*, which require the use of a registered Payment Distribution Agency (PDA) for you as the Debt Counsellor.

While you may have clients who can and do pay credit providers directly (and that’s fine) you need to have a PDA between you and your client. This creates accountability and a record of payments.

If you are taking initial payments to a separate bank account and only aftercare via the PDA, you are headed for trouble.

RATHER: Get payments via a PDA and don’t charge amounts you are ashamed of. Alternatively, head to the NCT and have your T&Cs changed.

* A very small selection of old DCs have different set of T&Cs. Newer DCs will have signed that they must use a PDA.

Sure, clickbait gets hits. But what follows for potential customers is disappointment and later, for those who do sign up, high drop-off rates.

In the short term, it results in underqualified leads jamming up your sales funnel and ultimately misleading ads damage your brand, and tarnishes the reputation of the industry.

So, think twice before saying the President has a great new way for consumers to write off their debts or offering fake consolidation loans.

RATHER: Learn to advertise to exactly the right people to get high quality leads who will convert. Free up your admin team from costly time-wasting work.

Yes, fees are not officially regulated and no, the NCR fee guideline is not legally binding, but that doesn’t mean you should be charging people an arm and a leg.

When consumers are charged unjustifiable restructuring or heavily loaded legal fees, your practice might be staying afloat for all the wrong reasons.

A truly sustainable business doesn’t need to squeeze every cent from cash strapped consumers. If this is all that’s keeping you in business, then you have already failed.

RATHER: Use the NCR fee guideline and work with attorneys who charge reasonable and justifiable fees.

If clients can’t reach you, then you are basically useless to them.

Responsiveness is core to trust and support. If they can’t reach you, they will head to HelloPeter or the Regulator’s complaints department.

If you are ducking calls from clients then it’s not long till the NCR comes to shut you down.

RATHER: Sort out your communication channels. Get more staff or better systems. Be there for your clients when they need you.

Clients in debt review are anxious. It’s stressful trying a new process when your entire financial future is on the line. Clients want to know things are moving. Silence simply creates stress and distrust. Remember you get a monthly retainer for aftercare.

That money is not for nothing. It covers your ongoing support to consumers; care they desperately need.

RATHER: A quick email or update makes all the difference, and shows respect for your client’s journey. Supply your clients with resources and financial education. Help them to feel safe, and learn while in debt review.

First impressions matter. A clunky or outdated website that doesn’t work on mobile devices reflects poorly on your professionalism.

You don't need a big budget—just something clean, clear, and current.

RATHER: Get in a professional (or teenager) and update your site to look current. Remove old inaccurate information.

If your last post was from 2019, it probably looks like you’ve gone out of business.

A quiet social media channel can hurt your credibility more than having none at all.

RATHER: Stay relevant with simple, helpful posts. Something simple on a regular basis is better than nothing and very helpful information all the time is best.

If you’re pushing sign-ups without clients fully understanding what debt review is, you’re already in unethical—and possibly fraudulent—territory.

Trickery and fraud have no place in debt review. It will also get you fined and deregistered.

RATHER: Reward your sales people for successful longterm cases, not just upfront volume. Link some of your commission to month 3 or 6 payments. Team up your sales and admin staff for some of their commission. Simplify your documents and ensure consumers are fully informed.

Being a great Debt Counsellor is about more than just doing the course and convincing people to sign up for the process.

It's about a high standard of ethics, professionalism, and service. Happy consumers spread the word about how great debt review is. They will confidently recommend your services to their friends/family when they need help.

If you are a Debt Counsellor, new or old, avoid propping your practice up with dodgy behaviour. If that’s where you are now, then sadly your practice is already doomed. And when your whole operation falls apart, it will be the consumers and their families that lose out the most.

So, rather be part of the solution, engage with industry role players, continually improve your service levels, follow the rules, and most importantly—treat consumers with the respect and transparency they deserve. The success of your practice and the health of the industry depend on it.

Have you applied to go under debt review? Are you restructuring your monthly expenses? Would you like to insure your debt?

Why not insure all your outstanding accounts in a single ONE Credit Protection Policy?

Have you applied to go under debt review? Are you restructuring your monthly expenses? Would you like to insure your debt?

BENEFITS OFFERED:

• Death – we settle the account

Why not insure all your outstanding accounts in a single ONE Credit Protection Policy?

• Temporary Disability – we pay your installment for 12 months

• Permanent Disability – we settle the account

BENEFITS OFFERED:

There are many benefits to credit life for both consumers as well as credit providers. By now we should all be aware of the minimum prescribed benefits and rate caps that were implemented 2017 as per the DTI Notice.

• Critical Illness – we pay your installments for 3 months

• Death – we settle the account

• Temporary Disability – we pay your installment for 12 months

• Permanent Disability – we settle the account

• Retrenchment – we pay your installments for 12 months At a

• Critical Illness – we pay your installments for 3 months

• Retrenchment – we pay your installments for 12 months

covered on the ONE Credit Protection Policy:

• Credit Cards

• Overdrafts

At a rate of R2.95 per R1000 unsecured/short-term credit and R2.00 per R1000 on mortgages and you can now insure your debt for less.

• Personal Loans

• Home Loans

• Retail Accounts

The following financial obligations or debt can be covered on the ONE Credit Protection Policy:

• Credit Cards

• Rental Agreement

• Maintenance Orders

• Overdrafts

However, there is a topic that I wish to raise awareness around –Surpluses By definition a Surplus means: an amount left over when requirements have been met. So, the question that probably now jumps to mind is: How does this relate to a Credit Life insurance policy?

• Personal Loans

• Home Loans

• Retail Accounts

• Rental Agreement

• Maintenance Orders

Credit Providers and Debt Counsellors have been utilising Credit Life for numerous years now to insure credit in order to mitigate certain

For further information please speak to your Broker, Debt Counsellor or alternatively contact your regional ONE office. 0861 266 562 admin.debt@one.za.com Terms and Conditions Apply

For further information please speak to your Broker, Debt Counsellor or alternatively contact your regional ONE office.

elements of risk related on the loans, whether it be a single product for a single loan or, as in the case with debt review, a credit life consolidation product to insure multiple credit agreements once a client applies for Debt Review.

Over the last 13 years of underwriting in the debt review industry there have been a few noticeable issues but none more obvious than the lack of annual reviews being conducted. In some cases, consumers have been under debt review for 5 years plus without a single review being done.

For obvious reasons, a review, at some stage during the consumers debt review period will be quite beneficial. It provides both the DC and consumer with the opportunity to evaluate whether they are on course with the rehabilitation, whether there are discrepancies in outstanding balances and how much longer to go – all round a win/win for both parties.

Have you applied to go under debt review? Are you restructuring your monthly expenses? Would you like to insure your debt?

Why not insure all your outstanding accounts in a single ONE Credit Protection Policy?

BENEFITS OFFERED:

• Death – we settle the account

• Temporary Disability – we pay your installment for 12 months

• Permanent Disability – we settle the account

• Critical Illness – we pay your installments for 3 months

• Retrenchment – we pay your installments for 12 months

At a rate of R2.95 per R1000 unsecured/short-term credit and R2.00 per R1000 on mortgages and you can now insure your debt for less.

However, after investigation and discussions with various Debt Counsellors, the conclusion was that reviews are somewhat challenging for Debt Counsellors and the chances of even a single review being done is actually quite slim.

The following financial obligations or debt can be covered on the ONE Credit Protection Policy:

• Credit Cards

• Overdrafts

• Personal Loans

So back to the Surpluses – when the client originally opted to insure their debt on a credit life policy, the total outstanding balance was, (for example) R 100 000.00.

• Home Loans

• Retail Accounts

• Rental Agreement

• Maintenance Orders

They would`ve been charged a rate per R 1000.00. With ONE that rate would be R2.95 which would cost the consumer R 295.00 for a R 100 000.00 worth of cover.

For further information please speak to your Broker, Debt Counsellor or alternatively contact your regional ONE office.

0861 266 562 admin.debt@one.za.com

Terms and Conditions Apply

Moving on a few years down the rehabilitation cycle, this balance has now dropped to only R 50 000.00. This would mean that the consumers premium should be half of the original premium –R 147.50 however, due to the lack of reviews the client is still paying for R 100 000.00 cover despite needing only half. See the issue?

When a claim is made the outstanding balance must be paid to the credit providers and the surplus paid to the consumer in the event of Disability or into their estate in the event of Death. Policyholder Protection Rules (PPR) are quite clear in that consumers must not be prejudiced at all.

Question: Do you think that a client that does not receive their surplus is being prejudiced?

Question: Does your current service provider pay out surpluses?

•

Let`s do the right thing by our clients, this is an investment not only in your business but the industry as a whole!

•

•

Christopher John Keuler Divisional Manager - Credit Protection

Debt review has been around since 2007. That’s more than 15 years for credit providers to get their systems in place, train their staff, and refine their processes. With all the advances in technology—especially now during the AI boom—credit providers should be running a slick, efficient debt review department.

Sadly, many Debt Counsellors report unnecessary delays and high numbers of counter proposals on DCRS matters—proposals that should have been accepted automatically under agreed rules.

Some credit providers shockingly still find themselves accused of reckless lending. Even more concerning, we still see company leaders blaming the entire debt review process (which affects only a tiny number of their clients) for their organisation’s financial performance.

Some credit providers websites still continue to have misleading or totally false information about debt review on display.

RATHER: Credit providers should vigorously support debt review, which recovers billions in debt with such minimal cost. They should invest in up to date systems and staff training to ensure smoother processes. They should correct those websites. And if DCRS is not working as intended, they must help fix it quickly —before the Debt Counsellors Walk away from it altogether.

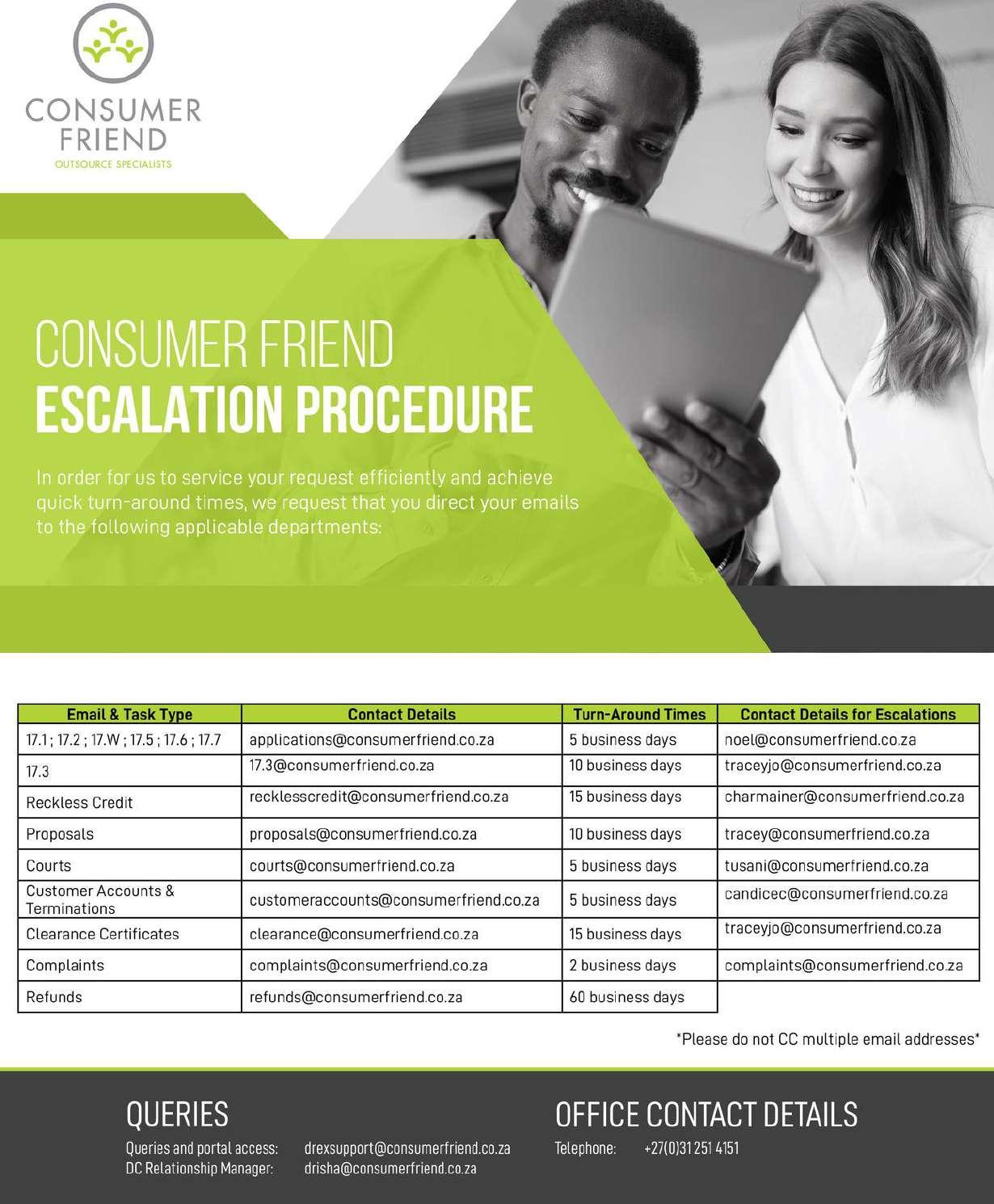

PDA'S: ARE YOU BAD AT DEBT REVIEW?

Payment Distribution Agents (PDAs) are a vital part of the debt review process in South Africa. They collect consumers’ monthly payments and pay the correct credit providers as outlined in the payment plan.

They are so organised and have such fancy systems that you might think it is impossible for a PDA to be bad at debt review. Well, recently, one PDA—CollectNet—was deregistered by the National Credit Regulator (NCR) for failing to report back in time and other technical things. Thankfully, hardly any consumers were affected in any way.

Many of the challenges the PDA faced could probably have been overcome if the PDA fees issues had been sorted out a long time ago. When operational costs have to be cut to the bone there is little room for hiring more staff, upgrading systems and even allocating resources to meet NCR requirements.

This incident is a bit of a wake up call for all working in the debt review space. A PDA that fails to meet NCR deadlines or is cash strapped potentially puts the entire industry’s reputation at risk. Fortunately, our 3 existing PDAs not bad at debt review. They are world class and prioritise compliance, risk management and working closely with the NCR.

RATHER: For those in charge of such things, please adjust PDA fees to be sustainable for these critical industry role players who consumers rely on. Protect the process. Protect the consumer.

In South Africa, certain businesses must register with the Financial Intelligence Centre (FIC) as Accountable Institutions.

This includes companies that offer credit — which means supplying goods, services, or loans now, but allowing the customer to pay later. Even though the FIC’s final guidance is still being developed, the current FIC Act already explains who should register.

1. If your business is registered with the National Credit Regulator (NCR) as a Credit Provider, you must also register with the FIC.

2. Even if your business is not registered with the NCR, but you allow customers to pay later for goods, services, or money you’ve advanced, you still need to register with the FIC under Item 11(b) of the FIC Act. It doesn’t matter what your payment terms are — whether it’s 30, 60, or 90 days — or whether you charge interest or give discounts. While this may later change, if you currently defer payment, you’re providing credit in legal terms, and the law says you must register with the FIC.

So, be sure to register if your business is an NCR registered credit provider or you defer customer payments.

* Thank you to Eugene Joubert of CR Holdings for his help in preparing this article. For more info head over to www.crholdings.co.za

All Debt Counsellors are required to submit quarterly statistics to the National Credit Regulator (Form 42).

The reports for Quarter 1 (01 January 2025 – 31 March 2025) are due on 15th May 2025.

While some people may wonder if it is necessary, Debt Counsellors are reminded that failure to do so is a contravention of the NCA and NCR terms and conditions of registration and may result in the NCR taking enforcement action against you.

Tip: To help the NCR Forms can be saved / renamed with your NCRDC Number.

The completed Form 42s must be sent to: dcreturns@ncr.org.za.

With recent pressure on budget income and expenditure many government departments will be looking at additional means to increase income and cut spending.

This may be one of several motivating factors in the NCR looking at annual registration fees and contemplating increasing them.

At present, the IFC and NCR have appointed Ernst & Young Advisory Services to conduct research into the topic. They are conducting both quantitative surveys and in depth qualitative interviews with key industry role players and organisations.

One topic that was raised during the research is the idea of annual increases (perhaps in line with inflation).

NOTE: Debt Counsellors are welcome to contact: admin@dcasa.co.za for access to the survey (even if they are not DCASA members).

It has been a roller-coaster of will they, wont they over the proposed and then rescinded plan to increase VAT by 1% over two years.

As things currently stand the plan has been pulled and new plans will have to be made to try push up government income or cut spending.

The markets (already in turmoil due to US tariff wars) initially punished and have now rewarded the Rand with losses and gains.

This period of confusion, political uncertainty and poor relations with the US saw the Rand drop to an all time low in April 2025, though it has now regained some of its strength.

It is hard to see exactly what the current US tariff war has done to the global economy. International supply chains have been stalled or disrupted. Companies have cancelled international contracts or orders and many businesses have decided to wait a moment to see what the US president would do tomorrow. Things at the White House have been confusing to say the least. Things have been changing faster than a super model backstage at NY fashion week.

While the stock market turmoil has lost some people their entire life savings others have made a fortune. But with even the richest man in the world losing $135 Billion in the last few weeks and months it is safe to say it has been chaos. It looks like many pensioners will be hard hit.

Locally, SA wine makers and car manufacturers look to be some of the hardest hit in the tariff backlash. Tariffs are not the only factor, the political game of chicken government is running with Starlink and the US has seen the SA-USA relationship deteriorate even further. The pending expulsion from AGOA looks set to hit SA exporters significantly.

The result of all these fluctuating factors is hard to gauge right now. Many times, it can take months or years to fully see the full ramifications but many economists are starting to predict another global recession. In among all the uncertainty it seems that US President Trump feels confident that all this confusion will see the USA come out ahead of the rest of the globe.

Financial Gains, Client Savings: Collaborate for Success

We specialize in providing Credit Life Insurance, Income Protection, and Funeral Cover services to debt counsellors, empowering them and their clients to have more. By referring their clients to us, we not only offer the highest referral fee in the industry, but also provide annuity streams to support their financial growth.

•Additional Revenue Streams

•Annuity Income

•Retention of Clients

•We take care of Administration

•Compliance Guaranteed

•A lucrative recurring monthly revenue stream

•Better chance of clients qualifying for debt review

•Little time and no effort – we do the work for you

•User friendly and efficient system

•Enhanced Service Offering

•No Medicals Required

•Continuous Training Provided

•DC Front-End System Integration

•Pay a lower premium for the same benefits – can save your clients thousands of Rands

•Convenience – a single policy covers all your clients’ credit agreements

•Claiming process easy and effortless and facilitated by DCCP

•New loans can be included under this policy

The SA Reserve Bank’s Prudential Authority has asked the Pietermaritzburg High Court to close down Ithala SOC (a state-owned financial institution based in KZN). This decision was made after serious concerns were raised about the financial health of the bank, which is said to be insolvent. Ithala has till recently been operating under a special exemption that allowed it to take deposits without a full banking license.

National Treasury has promised to protect the money of the +-257,000 customers through a government guarantee while their accounts are moved to other banks (like ABSA).

The move has sparked criticism from political parties and unions, including the EFF, ActionSA, and NEHAWU. They argue that not enough support was given to help Ithala meet banking requirements. KZN provincial government is also fighting the decision and plans to challenge it in court.

If any Debt Counsellors' clients have been impacted by the recent upheaval it is good to know that arrangements are now finally in place for debt repayments to be made to an ABSA account. This is being handled behind the scenes at the PDAs and Debt Counsellors can simply select the same CP as before on their systems. Any funds that were held back recently will now be released to that ABSA account.

If you get a call from someone offering to reduce your monthly debt repayment while under debt review, please be cautious.

If they are scammers, they could trick you into changing the account you pay money into each month. They will then probably just run away with the money.

If they are actually another debt counselling practice, the offer of smaller monthly repayments would mean paying off your debt for even longer. Do you want to be paying off debt for months or even years extra?

Be careful and always consult with your own Debt Counsellor if in doubt.

While the VAT increase may have been called off, economic relief remains elusive. Electricity tariffs continue to climb, import prices are pressured by global trade dynamics, and economic growth is sluggish at best. For many households, the cost of living is still rising - and financial breathing room is harder to find than ever.

Debt Counsellors know the reality: the pressure hasn’t disappeared, it’s just moved. Families aren’t deciding if they’ll cut expenses, but which essentials to sacrifice, often bouncing between food, electricity, medical expenses and debt repayments. At the same time, those supporting overindebted consumers, Debt Counsellors and PDAs are facing their own

mounting costs. The challenge? Staying afloat without passing the strain to already struggling clients. This is where iPDA steps in. Our platform equips Debt Counsellors with powerful tools to stay efficient, compliant, and cost-effective. From smart workflows and automated exception fund submissions, to real-time data insights, we’re helping the industry adapt, without compromise.

But beyond tech lies an even bigger opportunity: reframing debt review. In today’s economy, it’s not a fallback, it’s a financial strategy. A proactive tool to stabilize households in crisis. That means shifting how we talk about it, not in technical terms, but in a way that acknowledges the hard choices people are making daily.

As a sector, we need to lead with empathy, not stigma. Consumers need to see debt review not as failure, but as forward-thinking. At iPDA, we’re committed to driving that narrative, supporting both debt counsellors and consumers by refining, adapting, and moving forward to better serve stakeholders.

In times like these, debt review isn’t just a tool. It’s a lifeline. And it’s time we start treating it as one.

Explore how our powerful solutions can streamline your operations and empower your clients. Reach out today to learn more.

Please visit the members Facebook group for latest industry info.

Debtfree DC Workshops Weekly on Thursdays 3:00 – 3:30pm

facebook.com/groups/allprodc NOTICE

www.allprodc.org

Thank you for noticing this new notice. Your noticing it has been noted.

It can be surprisingly hard to find people who are ready to sign up for debt review.

Despite the massive debt challenges most South Africans face many hesitate to make use of the amazing debt review process. Some Debt Counsellors have turned to external lead generators to try find perspective clients.

Ideally, these companies help connect people with the right Debt Counsellor. But in many cases, a single person’s information gets sold to multiple Debt Counsellors, leading to a flood of unexpected phone calls.

So, instead of feeling like they’re finally getting help, people can end up feeling overwhelmed, frustrated, and even sceptical of the whole process.

Imagine you finally decide to seek help for your debt. You fill out some online form, hoping to speak with an NCR registered professional.

But before you’ve even had time to think, your phone starts ringing. One company calls, then another, and another. Each one claims to be your best option.

For some, this level of attention might seem reassuring. After all, options are good. But for many, it’s just too much. Instead of feeling supported, they start wondering if it’s a scam.

They feel pressured rather than empowered, and the trust they had in debt counselling begins to crumble before they even start the process.

Dale Johnson at 1on1 Lead Gen says: “this is common among fly by night operators who are just out for a quick buck. They offer the same leads to multiple people and do so at low prices to justify their actions”.

It’s not just consumers who suffer— ultimately Debt Counsellors do, too.

Dale says: “When a single person’s details are sold to multiple DC, it becomes a race to reach them first. But by the time some counsellors get through, they find that the potential client has already spoken to several other companies and may have lost interest altogether”.

Debt Counsellors who genuinely want to help end up wasting time and money chasing leads that no longer go anywhere. Instead of having meaningful conversations with people in need, they face scepticism from frustrated consumers who have been contacted too many times.

No one likes the feeling of their personal information being passed around like a business transaction.

The Protection of Personal Information Act (POPIA) exists to help keep consumer data safe. But when lead generators resell personal details without clear consent as to who exactly will get the info, it raises serious concerns.

Ideally debt counselling should feel like a clear step toward financial stability. But when people searching for help are suddenly bombarded with choices, it can feel like too much.

When too many companies reach out, the decision-making process becomes confusing and people can get analysis paralysis. They end up doing nothing because of too many options and too much info.

Dale says: “Too many calls offering help or too many emails can lead to people simply ignoring any call or any message about debt relief. Lead generators can’t treat debt review like other services. They need to be sensitive to the needs of the financially stressed consumer.”

This is also known as lead fatigue, and it’s a real problem. Instead of finding the right Debt Counsellor, many potential clients shut down completely, letting their financial struggles persist simply because they’re overwhelmed.

Debt counselling is meant to be a lifeline, but lead reselling unfortunately can turn it into an exhausting and sometimes discouraging process for consumers.

Too many calls damage trust, Debt Counsellors waste money on ineffective leads, privacy concerns cause hesitation, and lead fatigue stops people from actually getting the help they desperately need.

If debt counselling is going to remain a trusted service, there needs to be more accountability in how leads are handled—so that the people who need financial relief can actually find it.

Debtfree want to thank 1on1 Lead Generation for their assistance in researching and creating this article. To learn more head over to: www.1on1leadgen.com or email: sales@1on1leadgen.com

DREX simplifies the exchange of data and makes managing the debt review process less admin intensive.

The below links take you to step-by-step guides on how to use the DC Portal on DREX.

Finwise is an all-inclusive Software System, designed for debt counsellors for professional and efficient Debt Management.

Finwise is a cloud-based system, and can be used on any mobile device, PC, or tablet with internet connectivity. The exceptional workflow and innovative task manager tools saves the user valuable time, through multiple consumer data reporting and easy management. Several integrations such as Legasys, iDOCS, Drex, facilitate effortless administering, and handling of multiple transactions and tasks within one system.

Requirements:

The National Credit Regulator (NCR) was established as the regulator under the National Credit Act 34 of 2005 (the Act) and is responsible for the regulation of the South African credit industry. It is tasked with carrying out education, research, policy development, registration of industry participants, i.e. credit providers, credit bureaux and debt counsellors, investigation of complaints, and enforcement of the Act. The Act requires the Regulator to promote the development of an accessible credit market, particularly to address the needs of historically disadvantaged persons, low income persons, and remote, isolated or low density communities. The NCR invites applications from suitable candidates for the following position:

Fixed Term Position for 3 Years: Chief Operations Officer

Paterson Grade: E- Lower

Salary range p.a. from R818 400 – R1 636 800 maximum

Ref No: COO/04/25

▪ The successful candidate must hold a relevant degree at honours level . A master’s in business or other additional qualification in line with the duties listed will be an advantage. The preferred candidate must have a minimum of 15 years working experience and a minimum of 3 years at Executive Management level

Duties:

The incumbent will be responsible for the following:

▪ Collaborate with the CEO in setting and driving organizational vision, operation al strategy, and hiring levels

▪ Oversee operations and employee productivity, building a highly inclusive culture that ensures team members can thrive and that organizational goals are met

▪ Develop and implement the strategic plans of the organisation through monitoring and coordinating the key activities of the various departments of the NCR

▪ Participate in and lead strategy, policy formulation and procedure development

▪ Ensure compliance with requirements and the smooth functioning of the organisation

▪ Set comprehensive goals for the performance, monitoring, and evaluation of N CR Operations and play major role in the formulation of Annual Performance Plans and Operational plans to fulfil the strategy of the NCR

▪ Report to the Chief Executive Officer (CEO), as a member of the Executive Committee (ExCo) and other Committees functioning within the organisation

▪ Compile regular reports on the activities of the organisation, including those to the external oversight committee(s)

▪ Coordinate and compile the annual report, and ensure timely submission to the Department of Trade, Industry and Competition and Parliament

▪ Monitor and oversee operations

▪ Conduct regular meetings with Managers to evaluate progress, and provide guidance and leadership

▪ Liaise with the internal auditors , etc. to identify strategic or operational risk areas and develop, implement, and monitor control measures to mitigate these risks

▪ Analyse internal operations and identify areas for process enhancement

▪ Build and maintain trusting relationships with key customers, clients, partners, and stakeholders

Knowledge:

▪ National Credit Act

▪ Relevant labour legislation

▪ Public Finance Management Act

▪ All other relevant legislation

Skills:

▪ Strategic Thinking

▪ Experience Collaborating with Executives

▪ Change Management

▪ Excellent communication skills

▪ Excellent leadership skills, with steadfast resolve and personal integrity

▪ Understanding of advanced business planning and regulatory issues

Closing Date: 25 April 2025

The National Credit Regulator is an equal opportunity organization which offers competitive market -related packages. Suitable persons should send a detailed CV quoting the relevant reference number to: hrm-recruitment@ncr.org.za Correspondence will only be entered into with short listed candidates. The National Credit Regulator reserves the right not to make an appointment

DebtCare is one of the leading large Debt Counselling companies, consistently being in the top 10 companies for the last 5 years at the Debt Review Awards. Last year. we were rated in the top 5 in our category of large debt counselling company;

The criteria for the role includes:

• Minimum of 1-3 years of experience in Debt Review

• Minimum of 1-3 years of experience in Customer Service

• Minimum of 1-3 years of experience in Debt Review Administration

• Experience in doing DCRS and Pro Rata Proposals

• Experience in handling queries and working with Form 17.1 & Form 17.2

• Completion of Debt Counselling Course is advantageous

The main job outputs includes, but is not limited to:

• Working under the supervision of a Debt Counsellor.

• As a Debt Review Negotiations Consultant, you will be responsible for completing Form 17.1, Form 17.2, and both provisional and final proposals.

• Your goal will be to ensure all credit agreements are accepted with the rearranged proposal plan, helping clients achieve successful debt review outcomes.

• Additionally, you will manage a portfolio of clients and handle any queries that arise.

We are hiring one candidate for this role.

Location: In-office

Job Type: Full-time

Salary: R6 500.00 - R10 000.00 per month

To apply contact: operations@debtcare.co.za

Tel: 086 111 6197

Fax: 021 425 6292 info@creditmatters.co.za

www.debtbusters.co.za

www.zerodebt.co.za

www.debtbusters.co.za

info@debtbusters.co.za

Email:

www.zerodebt.co.za

www.zerodebt.co.za

www.debtbusters.co.za

info@debtbusters.co.za

Credit Matters

South Africa’s Leading Debt Counsellors NCRDC533

14th Floor, The Pinnacle Cnr Strand & Burg St Cape Town Tel: 086 111 6197

Fax: 021 425 6292 info@creditmatters.co.za

Tel: 087 701 9665

Email: help@zerodebt.co.za

www.zerodebt.co.za

www.debt-therapy.co.za

Liddles & Associates

“If you do what you’ve always done, you’ll get what you’ve always gotten.” - Tony Robbins

(T) +27 87 138 3275 (E) quintin@liddlesinc.com

www.liddlesinc.com

Steyn Coetzee Attorneys / Prokureurs

Adri de Bruyn 11 Market Street / Markstraat 11, Paarl, 7646

Tel: 021 872 1968

Fax: 021 872 2678 adri@steyncoetzee.co.za

RM Brown and Associates 16th Floor, The Pinnacle Cnr Strand & Burg St Cape Town

Tel: 021 202 1111, f: 021 425 0875

Email: roger@rmbrown.co.za

Innovative, tailored and focused legal services to suit you as the individual, and your business.

010 030 0698 | 010 035 0855 www.crawfordharris.co.za 57 Conrad Street | Florida | Roodepoort

Jus�n �an Der Linde

1st Floor Icon House 24 Hans Strijdom Street Cape Town 8001

079 6977 259

jus�n��dla�orneys.co.za

Assisting small to large debt counselling businesses with their legal applications on a National Scale.

We pride ourselves on personal attention and service excellence.

Levesh Govender Tel: 071 364 1475 eMail: levesh@lglaw.co.za

Effective Intelligence sardagh@e-intelligence.com

Fides Cloud Technologies craig@fidescloud.co.za

Finch Technologies chris@finchinvestments.co.za

I-Bureau Services abrie@ibureau.services

IDR South Africa shane@v-report.co.za

iFacts sonya@ifacts.co.za

Inoxico support@inoxico.com

Kudough Credit Solutions chrisjvr@kudough.co.za

Lexisnexis Risk Management kim.bastick@lexisnexis.co.za

Lightstone chrisb@lightstone.co.za

Loyal1 tshepiso@loyal1.co.za

Managed Integrity Evaluation

marelizeu@mie.co.za

Maris IT Development marius@marisit.co.za

National Validation Services info@nvs-sa.co.za

Octagon Business Solutions gregb@octogon.co.za

Omnisol Information Technology info@verifyid.co.za

Payprop Capital johette.smuts@payprop.co.za

Right Cover Online cto@rightcover.co.za

Searchworks 360 skumandan@searchworks360. co.za

Smart Information Bureau info@smartbureau.net

ThisisMe juan@thisisme.com

TPN Group michelle@tpn.co.za

Trans Africa Credit Bureau

clintonc@transafricacb.co.za

Transaction Capital Credit Health

DavidD1@tcriskservices.co.za

VeriCred Credit Bureau sumein@vccb.co.za

WeconnectU

johann@weconnectu.co.za

Zoia Consulting sipho@dots.africa

C O N T A C T D E T A I L S DEBT REVIEW NIMBLE GROUP

RE: NIMBLE DEBT REVIEW CONTACT INFORMATION, ESCALATION PROCESS AND BANKING DETAILS.

Forms 17.1 and 17.7

This letter serves to communicate to the Credit industry to use the following contact details for Nimble when processing Debt Review related applications, enquiries, queries and complaints escalation process.

Kindly take note, Nimble hereby consents to service all legal documents applicable to Debt Review herein by way of email.

drcob@nimblegroup.co.za

Forms 17.2, Proposal Summaries, Cascade plans & Court orders drproposal@nimblegroup.co.za

Forms 17.2 Rejection, 17.W & Form 19 drtermination@nimblegroup.co.za

Forms 17.3, General queries, settlements, balance, refunds, statements, Paid up letter request & reckless lending allegations, payment allocation queries & Complaints drqueries@nimblegroup.co.za

DEBT REVIEW DEPARTMENT CONTACT NUMBERS:

JHB Office: +27 87 250 5533

CPT Office: +27 21 830 0711

CUSTOMER CARE DEPARTMENT CONTACT INFORMATION:

CPT Office: +27 87 286 0223

Info@nimblegroup.co.za

DEBT REVIEW ENQUIRIES ESCALATION MANAGEMENT ORDER CONTACT DETAILS

Kindly note that escalations must only be done once you have sent your request to the above-mentioned contact email addresses and if your requests are out of SLA in lieu Debt Review forms response business days stipulated in the NCR Act.

1ST Line escalation

Aletta Molelekeng

Team Manager: Process Recoveries

D: +27 87 283 3210

E: AlettaM@nimblegroup.co.za

2ND Line escalation

Sharonne Dirk

Ops Manager: Customer Care & Process Recoveries

D: +27 21 830 0713

E: SharonneD@nimblegroup.co.za

3RD Line escalation

Zivia Koff

Ops Executive: Customer Care & Process Recoveries

D: +27 21 492 4554

E: ZiviaK@nimblegroup.co.za

It is of utmost importance that debt review documentation is sent to the correct email address to ensure timeous feedback and action.

Further to the above, please ensure that only the channel email address applicable to the documents being submitted is used. Sending emails to multiple email addresses will result in a delay or even no feedback or action.

1 Jolene Pieters Team Leader: Debt Review (Court Orders/Forms/Inclusions) JolenePieters@capitecbank.co.za 2 Cindy Mauritz Manager: Debt Review CindyMauritz@capitecbank.co.za

3 Carolina Visser Manager: Process Recoveries CarolinaVisser@capitecbank.co.za Proposals

1 Meghan Bruiners Team Leader: (Proposals) MeghanBruiners@capitecbank.co.za

2 Cindy Mauritz Manager: Debt Review CindyMauritz@capitecbank.co.za

3 Carolina Visser Manager: Process Recoveries CarolinaVisser@capitecbank.co.za General Enquiries, Refund/cancellation requests , Termination queries, Updated COB’s, Payment queries

1 Nathan Slaverse Team Leader: Enquires Nathanslaverse@capitecbank.co.za 2 Carolina Visser Manager: Process Recoveries CarolinaVisser@capitecbank.co.za

1 Mfundo Xaba Officer: Market Conduct Oversight MfundoXaba@capitecbank.co.za

2 Dries Olivier Manager: Market Conduct and Oversight DriesOlivier@capitecbank.co.za

Reckless Lending Queries

1 Whitney Jardine Team Leader: Recoveries Risk Support WhitneyJardine@capitecbank.co.za

2 Zayaan Jurgens Manager: Recoveries Risk Support ZayaanJurgens@capitecbank.co.za

Credit insurance claims

1 Grant Griffith Jessica Rademeyer Kanyisa Mbiza Team Leader: Insurance Claims GrantGriffiths@capitecbank.co.za JessicaRademeyer@capitecbank.co.za KanyisaMbiza@capitecbank.co.za

2 Brigitte October Performance ManagerInsurance Claims BrigitteOctober@capitecbank.co.za

Telephonic queries lodged

1 Laetitia Pretorius Team Leader: CCS Queries LaetitiaPretorius@capitecbank.co.za

2 Tracey Govender Manager: Recoveries Administration TraceyGovender@capitecbank.co.za

Sincerely,

17.1, 17.2, Proposals, General correspondence: debtcounselling@africanbank.co.za

To register for Legal Web Access: lwac@africanbank.co.za

Reckless Lending investigations: RLA@africanbank.co.za

DETAILS COMING SOON For more

erminations@absa.co.za

ebtreviewqueries@absa.co.za

Debt Counselling Query Resolution Contact Points and Escalation Process

Email submissions (Level1)

Email: DebtCounsellingQueries@nedbank.co.za

To be used as a first point of contact for all written communication

Call centre (Level 1: Alternative) Tel: 0860 109 279

To be used as a first point of contact for all telephonic communication

Attended to by Queries Specialist (Level 2: First Escalation) dcescalation1@nedbank.co.za

To be used only where no resolution is found from first point of contact after 5 business days

Attended to by Team Leader and Queries Specialist (Level 3: Second Escalation) dcescalation2@nedbank.co.za

To be used only where no resolution is found from the first escalation after 5 Business days

Attended to by Support and Escalation Manager (Level 4: Final escalation) nbdcescalations@nedbank.co.za

To be used only where no resolution is found from the second escalation after 5 Business days

proposals@consumerfriend.co.za