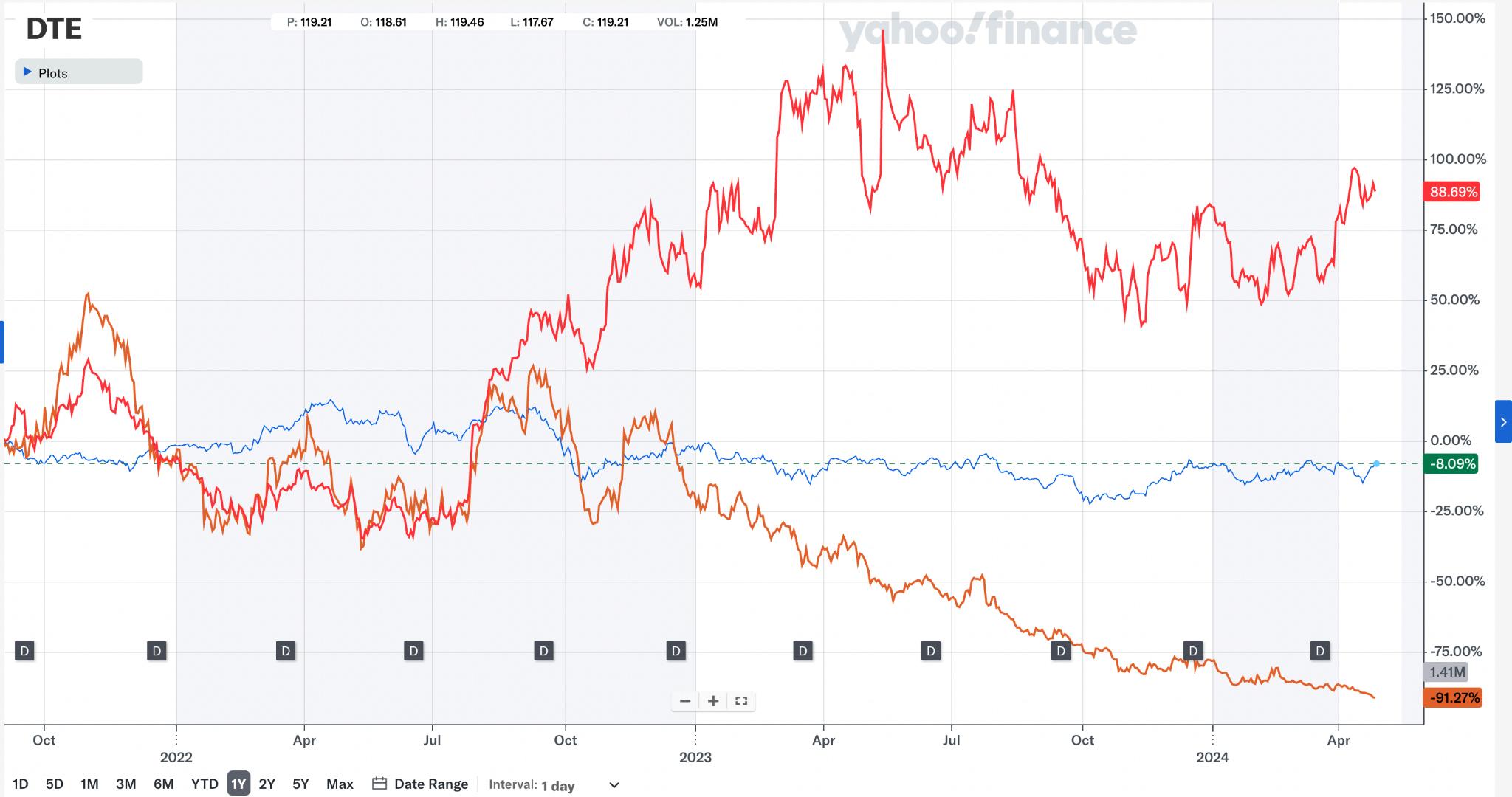

The Magnificent Seven stocks of Apple (APPL), Microsoft (MSFT), Google (GOOGL), Amazon (AMZN), Tesla (TSLA), Meta (META), and Nvidia (NVDA)are currently makingupnearly30%oftheS&P500.Specifically,Nvidia’s marketvaluehassurgedthrough2023,andhasnowreached $2 Trillion. The company produces GPUs which are computer chips or semiconductors for math operations to produce visuals and images. The increased market value is a result of the industry trends such as the wider usage of generativeAI.However,mostrecentlythestockhasdropped after investors were disappointed by rivals Advanced Micro DevicesandSuperMicroComputerearningsreleases.

IndustryChallenges:

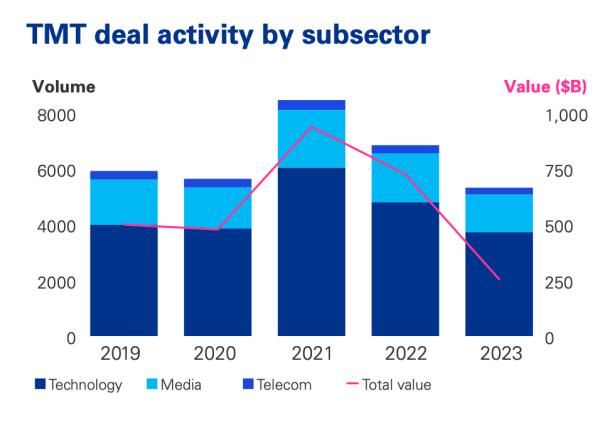

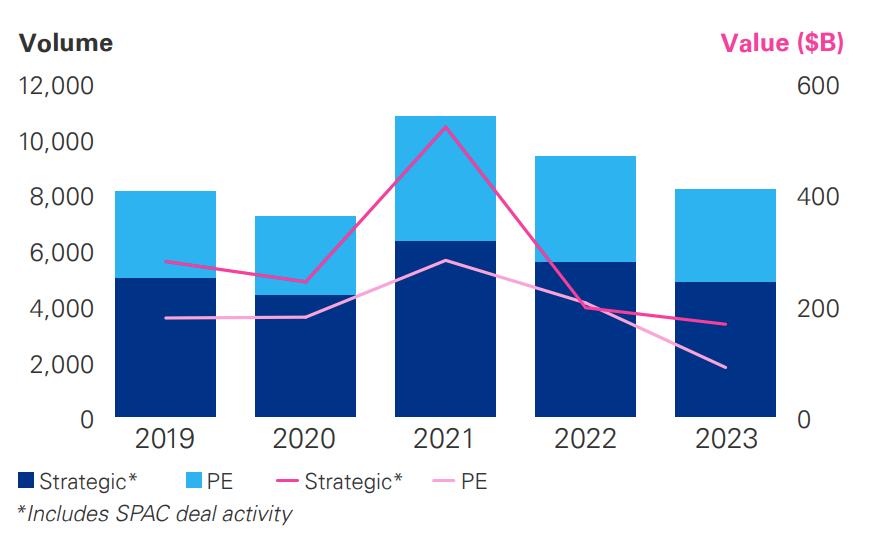

Overall, markets have adapted to challenging dynamics due to economic conditions. 2023 was a year of rising inflation ratesandhighenergycosts.Manycompanieshaveresponded tothesechallengeswithcost-savingmeasures.Inthetelecom space, Vodafone, T-Mobile, and Telefonica, all announced workforcereductions.Additionally,2023sawaslowdownof M&Aactivity,andtherewasasignificantamountofindustry consolidations.

AlexaCooper April23,2024

Metrics and Graphs

Source: KPMG 2023 Report

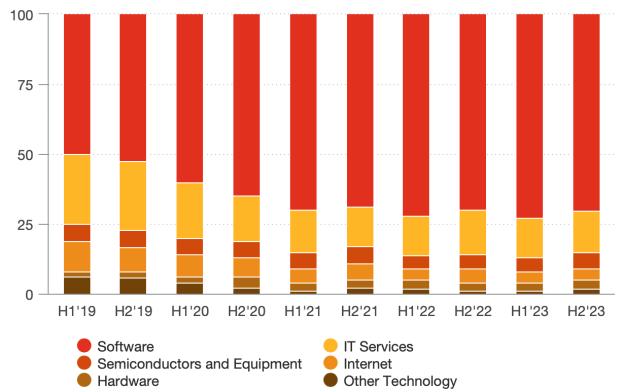

Source: KPMG 2023 Report

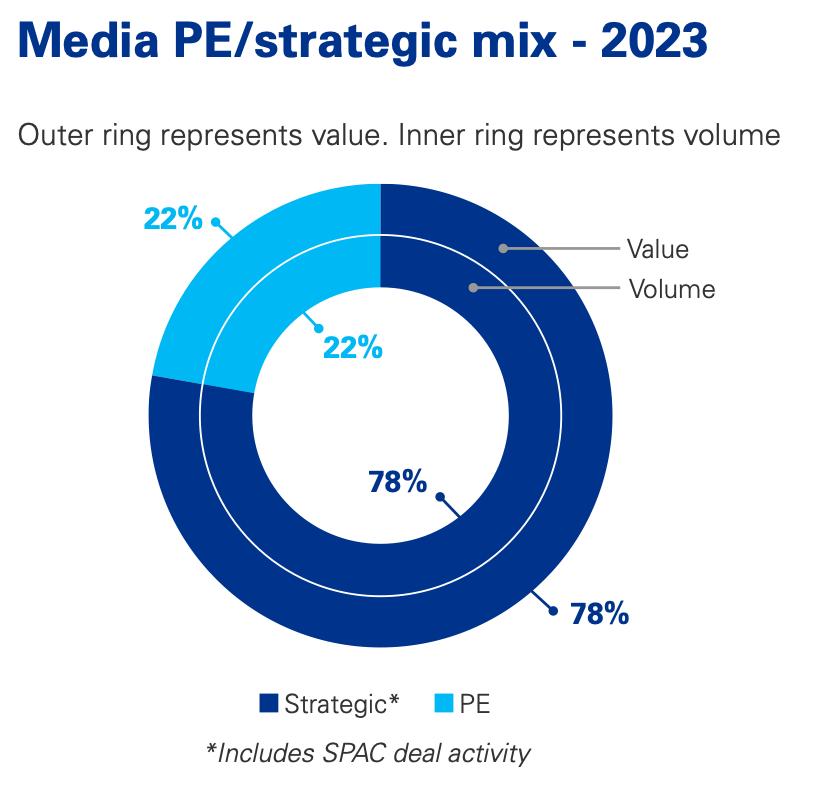

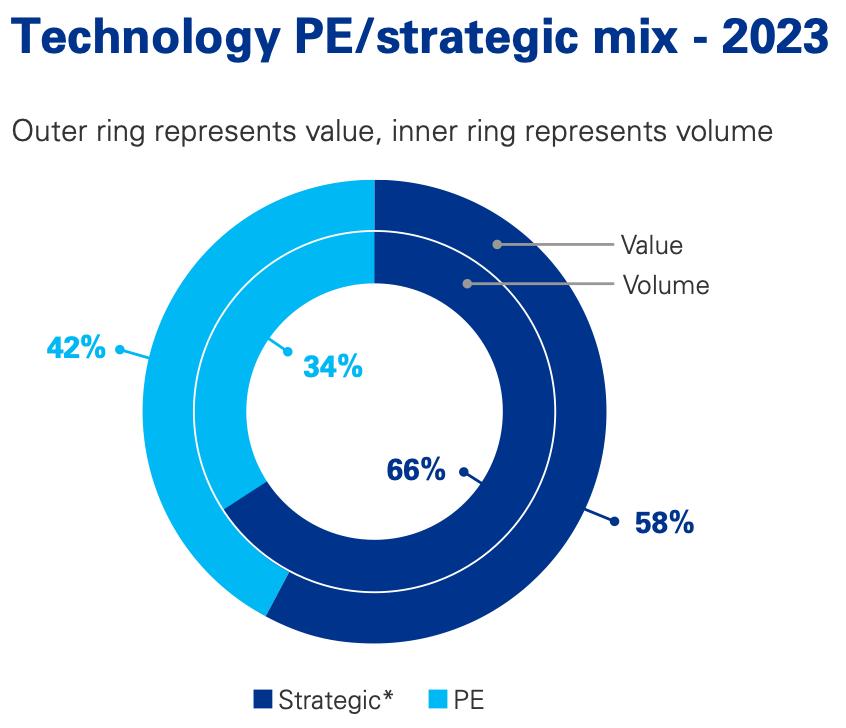

Source: PWC 2024 Outlook

IndustryTrends:

Software continues to be an attractive opportunityforinvestors.Assubscriptionbased servicesappealtoprivateequityfirmseveninthe slowgrowthenvironment

GenerativeAIisrisinginenterprisesoftware.As the technology is introduced, there are varying approaches to pricing models and distribution. AI has been synthesizing a large amount of information, however there are criticisms in determiningtheaccuracyofthemodels.

Digitaladvertising iscontinuing togrow. Media companiesareabletomonetizeoffuserdataand patterns.Manymediacompaniesarecontinuing to enhance its digital offerings through platforms.

NotableDeals:

Although deals have declined within the technology,telecom,andmediaspace,therewere still large transactions over FY23. Walt Disney Co. acquired Hulu from Comcast for $8.6 billion.Thestrategicrationalebehindthedealis for Disney to increase market share in the streamingspaceandmergestreamingintoasingle platform.Additionally,NasdaqacquiredAdenza Group,IncfromThomasBravofor$10.5billion toimprovetheirtechnologies,riskmanagement, and softwaresystems.

Netflix (NASDAQ: NFLX) Outperforms Their Outperformance

Netflix is a leading streaming entertainment service offering a broad array of TV shows, movies, and original content accessible on internet-connected devices worldwide. The company has three primary segments: Domestic (in the U.S.) and International (outside the U.S.) Streaming.. Netflix's content can be watched directly on any internetconnected device that offers the Netflix app. The company also produces its own original content. Netflix's business model emphasises customer satisfaction, ease of access, and providing a diverse content library to meet varied consumer preferences.

Investment Thesis:

Netflix's strategic moves including a significant $5 billion World Wrestling Entertainment (WWE) streaming deal and a partnership with Skydance Animation signal a robust expansion strategy, diversifying Netflix’s content and revenue streams and enhancing its competitive stance in the global entertainment market. The WWE agreement marks Netflix’s entry into sports entertainment, a sector with considerable growth potential, while the Skydance collaboration positions Netflix to tap into the lucrative consumer products arena. Additionally, innovative advertising formats like Title Sponsorships and Binge Ads could redefine viewer engagement and ad revenue models. These strategic developments suggest a positive trajectory for Netflix’s market valuation, driving stock price up projected 21.9%, presenting a compelling investment case, highlighting the potential for significant stock appreciation in the medium to long term.

Valuation/Financial Modeling:

As of April 24, Netflix is trading at $611.15 per share. Based on my analysis, I project that the share price could reach $744.72 within the year. This valuation is derived from a detailed Discounted Cash Flow (DCF) analysis utlising an 8% WACC. I utilized an EV/EBITDA multiple and a product revenue/subscribers approach, reflecting sector norms and operational synergies, to arrive at the implied share price. This method ensures a robust comparison and aligns my valuation with current industry standards and expectations.

WWE Deal:

On January 23, 2024, it was announced that a 10-year, $5 billion deal has been signed to bring WWE content exclusively to Netflix, starting in January 2025. This significant agreement includes the streaming of Monday Night Raw among other offerings. Over the past five years, WWE has experienced a Compound Annual Growth Rate (CAGR) of 19.4%. Additionally, WWE's YouTube channel boasts 99.4 million subscribers and has accumulated 12.4 billion views, underscoring its substantial presence in the streaming sector. WWE's dedicated, loyal fanbase, alongside the potential for securing long-term subscriptions, presents a valuable opportunity for Netflix. Furthermore, with 60% of WWE's viewership originating from outside the U.S. This deal also offers Netflix a chance to enhance its international reach and promotional efforts.The stock therefore saw an initial increase, indicating the market's positive reaction to the news resulting in the stock’s increase of ~24.19%. However, I believe the full extent of the increase has not yet been realised presenting an investment opportunity.

Kaleb Kavuma

What the Market is Missing:

This deal can act as a pathway to future sports streaming on Netflix with additional partnerships. Netflix has dramatically increased free cash flows net dividends, by ~311% since 2019 and 327% from last year, leaving ~$7 billion to be used to finance collaborations or acquisitions of other major sporting entities. Netflix’s strong earnings report is a sign of strong business performance, and the WWE deal shows management’s willingness to pursue. The industry has already shown an emerging trend of these deals with ESPN, Warner Bros, and Disney already trying to create a sports streaming platform that is scheduled for fall 2024. However, it is estimated to be $40/month on a new separate app, making it a costly alternative that Netflix can undercut. Netflix can capitalize by the end of the year to complete its own sports media deal leveraging its platform to undercut competitors providing a cheaper, easier alternative to enjoy movies and sports.

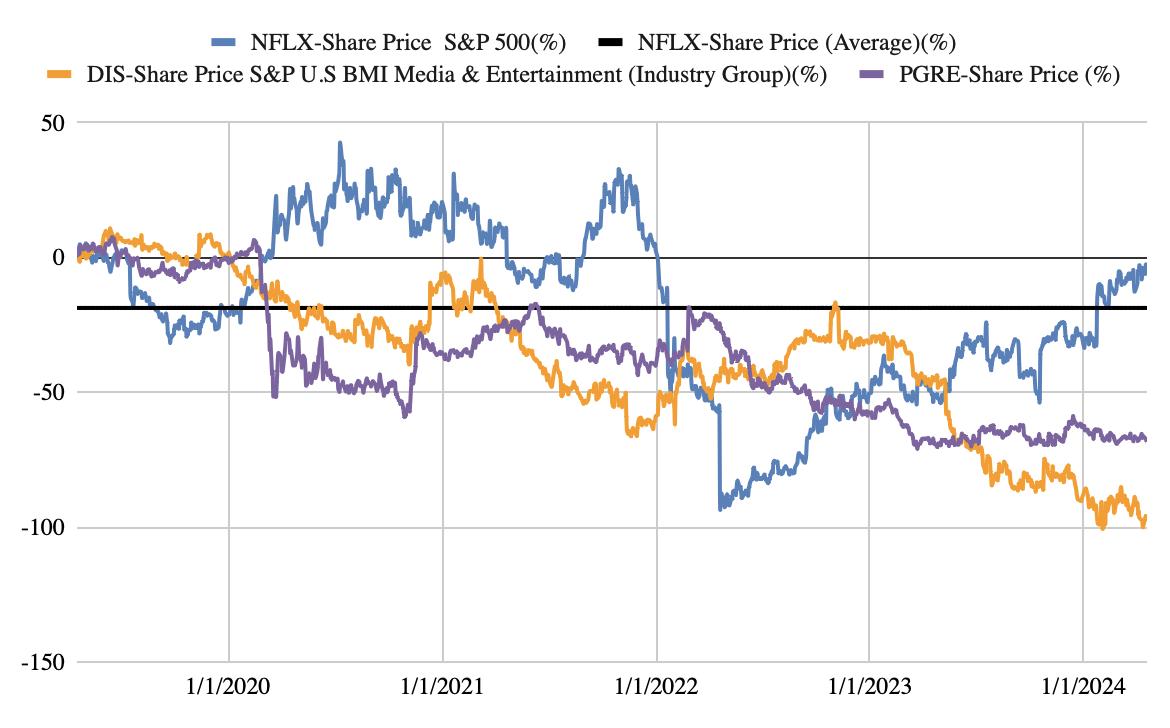

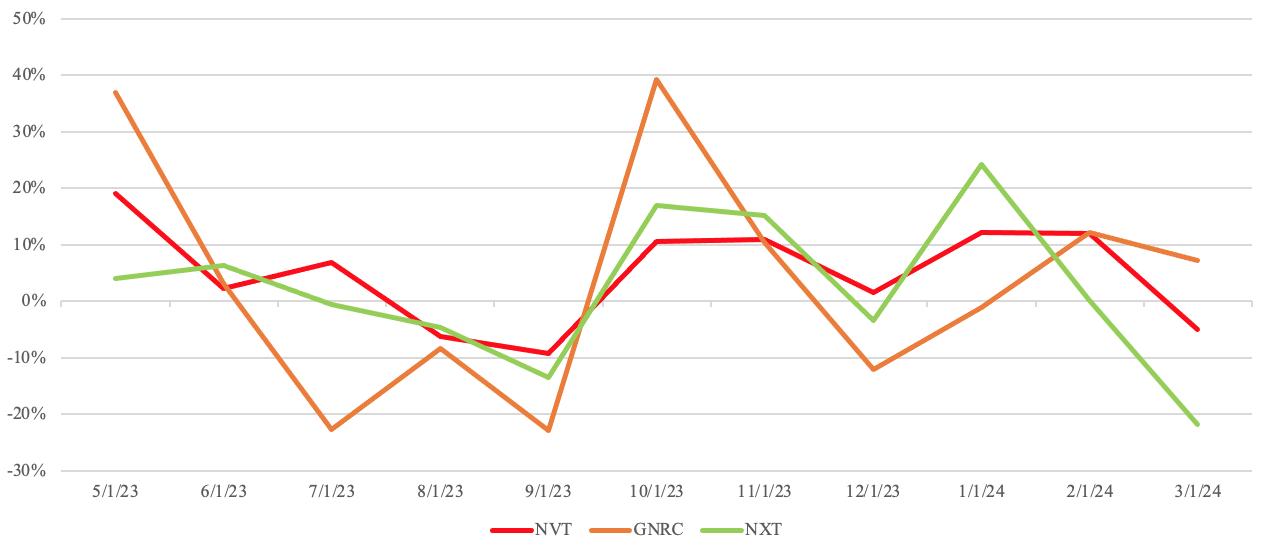

Stock Performance vs Competitors and Benchmark

The graph above shows NFLX’s performance relative to its major competitors Disney and Paramount, relative to the S&P BMI Media and Entertainment industry Index benchmark. This shows that while the top players in the streaming industry have been underperforming, Netflix is performing significantly better than its peers DIS and and PGRE. NFLX share price % change average over the last 5 years has been higher than both DIS and PGRE effectively for the two and a half years while having a higher % change than the other 2 since mid2023. Finally, NFLX is the only stock showing a positive long-run trend in 2024, and with the momentum created in early 2024, is expected to continue its upward trend, in contrast to the major competitors.

Source: Capital IQ

Kaleb Kavuma

Opportunities for Growth

Entry into the lucrative consumer products market:

In October 2023, Netflix entered into a multi-year agreement with Skydance Animation to develop animated feature films that will be released exclusively on Netflix. Skydance Animation is led by John Lasseter, the former head of Walt Disney Animation and co-founder of Pixar. Lasseter, who was the driving force behind mega-hit animations such as "Toy Story" and "Cars," brings a wealth of experience and a proven track record to the partnership. This collaboration comes at a pivotal time for Netflix, which recently won its first Oscar and Emmy in the animation category. The combination of producing proprietary animated content and leveraging Netflix’s extensive distribution network presents a significant opportunity for Netflix to establish itself as a formidable player in the animation industry.

What the market is missing:

The potential of launching Consumer Products (CP) through successful animation remains underappreciated. This strategic move allows Netflix to pivot towards introducing merchandising of fully owned intellectual property (IP), thereby opening up a high-growth revenue stream that mirrors the successful model established by Disney. For reference, consumer products generated $2 billion in income for Disney in both 2022 and 2023. By venturing into this area, Netflix not only stands to enhance its revenue streams but also cement its status as a household name. The integration of animation with consumer products provides Netflix with a dual opportunity to diversify and maximize its revenue, leveraging its growing library of animated content to create a more robust, multi-dimensional brand.

New Advertising Model: Title Sponsorships & Binge Ads:

Netflix is poised to revolutionize advertising in the streaming sector by adopting innovative advertising strategies such as Title Sponsorships and Binge Ads, leveraging its massive viewership. These strategies are expected to become key drivers of revenue per user in 2024.

Title Sponsorships involve partnerships where advertisers gain exclusive advertising rights aligned with Netflix's most popular series. With 13.1 million net subscription additions and a total of 230 million subscribers, Netflix stands as the largest streaming platform, providing it with significant leverage to attract major advertisers like PepsiCo, T-Mobile, and Nespresso. High-profile series such as "Squid Game: The Challenge" and the final season of "The Crown," both slated for release in 2024, are already moving towards incorporating specific sponsors.

Binge Ads introduce a new format for viewers on the “Standard with ads” subscription, allowing them to watch three consecutive episodes with ads and then a fourth without commercial interruption. This model is designed to enhance the viewing experience for the 15 million users (30% of subscribers in regions where available) subscribed to this plan. By improving content consumption and viewer satisfaction, Netflix aims to increase the Average Revenue Per User (ARPU).

What the Market is Missing:

These strategies are not merely marketing tactics; they represent a significant shift in how advertising is integrated within streaming platforms. Netflix's approach could redefine advertising norms, potentially redirecting global ad spending towards models that prioritize viewer engagement and satisfaction. By strategically grouping ad placements to reward consistent viewership and facilitate large-scale firm collaborations, Netflix is positioning itself not only as a pioneer in this new advertising market but also as a leader that maximizes its brand and scale. This is in stark contrast to the traditional advertising models seen in cable TV, which often include up to 17 minutes of unrelated ads per hour and may disincentivize consumers, leaving competitors reliant on an outdated revenue model.

Risk Overview

Kaleb Kavuma

Market Saturation & Competitor Response:

Despite holding a substantial 60% market share, Netflix faces challenges from major competitors making strategic moves to counter its dominance. For instance, Disney's acquisition of Hulu is a direct effort to mitigate Netflix's market control. Additionally, with consumer purchasing power having declined by 16% since 2020, there is a trend towards consumers limiting their subscriptions, which could impact Netflix’s net subscription totals as consumers explore alternative services.

Nevertheless, Netflix remains committed to retaining and growing its user base. The company has managed to sustain its Average Revenue Per User (ARPU) with approximately 1% annual growth and is expected to retain its position as the preferred choice for most consumers, positioning it to be resilient to consumers holding multiple streaming services looking to cut one or more.

Quality of Netflix Originals:

While Netflix aims to emulate Disney's model of creating unique intellectual property and beloved movies and shows, success heavily relies on the consistent quality and variety of these offerings. Unlike Disney, which has created numerous pop culture classics, Netflix has faced challenges in producing originals that consistently resonate well with audiences, which could hinder the effectiveness of this strategy.

Be that as it may, Netflix is not standing still; it has prioritized creating compelling hooks in the first few minutes of its shows to retain viewers’ attention. Furthermore, a significant increase in focus on high-quality production, evidenced by winning 22 Academy awards, and forming partnerships with established companies like Skydance Animation, is set to enhance the quality of Netflix’s offerings.

Risk of Entry into Consumer Products:

Venturing into the consumer products sector presents a learning curve for Netflix, involving mastering new distribution channels, developing appropriate organizational capabilities, and adapting to a different cost structure. This move introduces materially more volatile revenue streams with higher risks and uncertainties compared to its streaming business.

However, Netflix can streamline these costs by utilizing online distribution platforms rather than physical retail outlets. With a continued focus on high-quality production and strategic partnerships, the hit rates of its offerings should be higher, and revenue volatility could be reduced. Extending merchandising across a wider range of intellectual property products will also help mitigate these risks, capitalizing on its well-established brand and diverse content library.

Sources: Netflix Investor Relations | Yahoo Finance | Disney Investor Relations | Bloomberg | Capital IQ | Financial Times | yaragura.co | Statista

David Wu| May 15, 2024

Rating: Hold

Current Price: $946.32

Price Target: $938.42

Company Updates / News

● Market Cap: $2.32T

● 52 Week Range: $298.06-$974.00

● P/E: 79.39

● EPS: 11.93

● Beta: 1.75

● Revenue: $60,922M

● Gross Margin: 72.7%

● Accelerated supercomputer and quantum computing efforts for cutting-edge scientific research

● Purchased its current Bay Area headquarters for $326 million, becoming its own landlord

● Jensen Huang, the CEO, realized a 60% pay raise amid strong FY 2024 financial performance

Competitor Statistics

from FY 2023

Revenue: $22.680M

Gross Margin: 50.3%

Revenue: $54,228M

Gross Margin: 40.0%

Revenue: $35,820M

Gross Margin: 55.7%

NVIDIA Corporation Proven Leader Too Hot?

Investment Thesis:

NVIDIA Corporation has positioned itself on the frontiers of the semiconductor industry, riding the waves of the heightened attention of AI’s indisputable role in all industry verticals. The company’s GPUs are critical infrastructure for AI algorithms and machine learning applications, indicating that NVIDIA and its semiconductor peers will play an indispensable role in AI’s significant growth for the next decade. NVIDIA’s leadership in AI hardware, data center performance, and industrial manufacturing market expansion are the underpinning rationales for investment. Nonetheless, due to the considerable investor (institutional and retail) attention of AI, the stock has experienced volatility, and, understandably, high valuation and potential near-term market fluctuations. Due to this, I personally believe the hold rating is more prudent, inviting the investors to benefit from the long-term growth prospects while mitigating the short-term equity value uncertainties influenced by higher trading volumes.

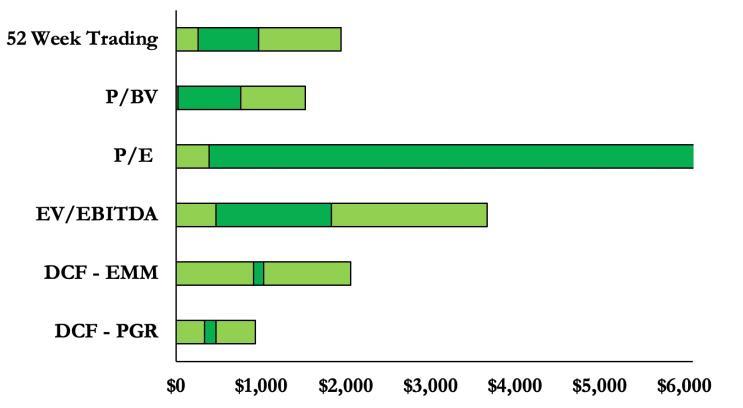

Valuation/Financial Modeling:

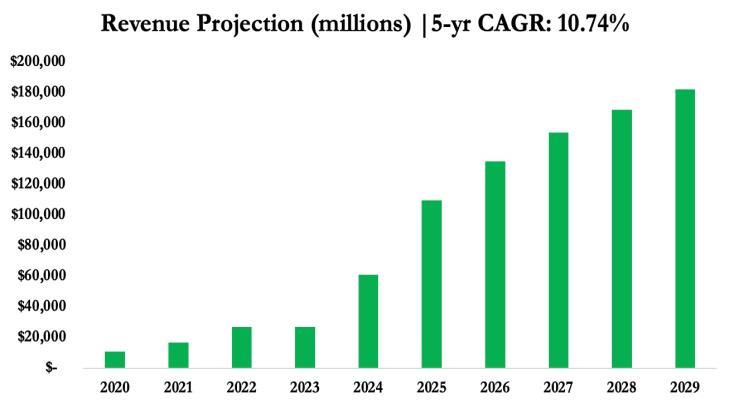

As of May 15, 2024, NVIDIA traded at $946.32 on the NASDAQ. To provide the most effective valuation, I conducted a DCF and comparable company analysis. The WACC (after un-levering and re-levering beta) yielded 11.05%, and the median EV/EBITDA, in comparison to other companies, was 29.8x. Most of my revenue projections were in-line with the analysts’ expectations; however, data center revenue was more conservative but the automotive was more aggressive.

Competitive Strength:

NVIDIA’s GPUs are the golden standard for the AI and machine learning industry; the CUDA programming model and Tensor Core are unmatched by NVIDIA’s competitors. The most important aspect of NVIDIA’s strength is its comprehensive product packages that offer full enterprise AI deployment from software to hardware to platforms (chips to CUDA to DGX) includes everything for comprehensive AI utilization, creating substantial barriers to entry to firms aiming to match similar levels of product line. NVIDIA’s strategic partnerships, a mirror of the loyal customer base and technological edge, include key players in the TMT industry (Microsoft, Google, Amazon); new partnerships with automotive companies such as Mercedes Benz demonstrate diversification.

Organic Growth Potential:

Data centers continued to be the driver of growth, especially with AI’s soaring demand for GPUs; however, the growth story expands to new industry verticals, such as industrials, finance, and healthcare - something new that’s heavily mentioned in the company’s earnings transcripts. High performance computing in these unique verticals is most decorated through the self-driving developments in the automotives space; NVIDIA has effectively entered markets for automotive manufacturing and frontier research for driving, demonstrating future potential.

David Wu| May 15, 2024

NVIDIA Valuation Comparison & Revenue Projection

Source: Bloomberg, Refinitiv, and Institutional Results

Risk Potential

Backlogs and Demand Challenges: Customers’ demands are constantly evolving in response to the rapid development of AI and emerging technologies; although NVIDIA’s technological competitiveness mitigates parts of this risk, the demand has exceeded the company’s supply capacities. Extreme demand hikes for the GPUs at unseen magnitudes (driven by machine learning algorithms) has led to supply chain constraints. Because of the demand and supply imbalance, the company may experience challenges converting backlogs to revenue in a timely manner; furthermore, delivery delays in these scenarios may affect customer retention rates and loyalty.

Asia Geopolitical Risk: NVIDIA sources most of its production from Asia-Pacific; semiconductor wafers are sourced from TSMC & Samsung; memories are originated from Micron, SK Hynix, and Samsung; assembly & packaging are outsourced to Hon Hai and numerous other Asian independent contractors. Due to political sensitivity of Taiwan, China’s foreign policy uncertainties, and US trade restrictions affect both sales to Asia and costs associated with the Asia-Pacific dominant supply chain.

Short-Term Price Volatility: The stock price, as of late, has been driven by higher volumes of trading, especially from retail investors. These activities are often driven by market trends, social media, and other nonfundamental factors. As such, price fluctuations detached from the company’s fundamental valuation happen more frequently; speculative trading can create an unpredictable market condition.

Sources: NVIDIA Investor Relations | AMD Investor Relations| Intel Investor Relations| Bloomberg | LSEG Refinitiv | Capital IQ Bank of America Global Research | Evercore ISI |UBS Global Research | Morgan Stanley Research | HSBC | SEC.gov |

Griffin Murphy| April 24, 2024

Rating: Hold

Current Price: $29.60

Price Target: $32.22

Company Updates / News

● Market Cap: $435.32M

● Beta: 1.34

● LTM EPS: 0.85

● EV/Rev: 1.4x

● EV/ EBITDA: 14.0x

● 52 Week High: $50.82

● 52 Week Low: $22.91

● Clearfield sets Q2 2024 Earnings Call for Thursday, May 2

● Roger Harding, Independent Director, recently bought 28% more shares in Clearfield

● Clearfield Q1 2024 earnings beat expectations

Competitor Statistics from Q1 2024

EV/Rev: 2.3x

Revenue: $217.6M

EV/Rev: 0.8x

Revenue: $1,149.1M

EV/Rev: 1.2x

Revenue: $357.3M

Clearfield Inc (CLFD) The Bottom?

Investment Thesis:

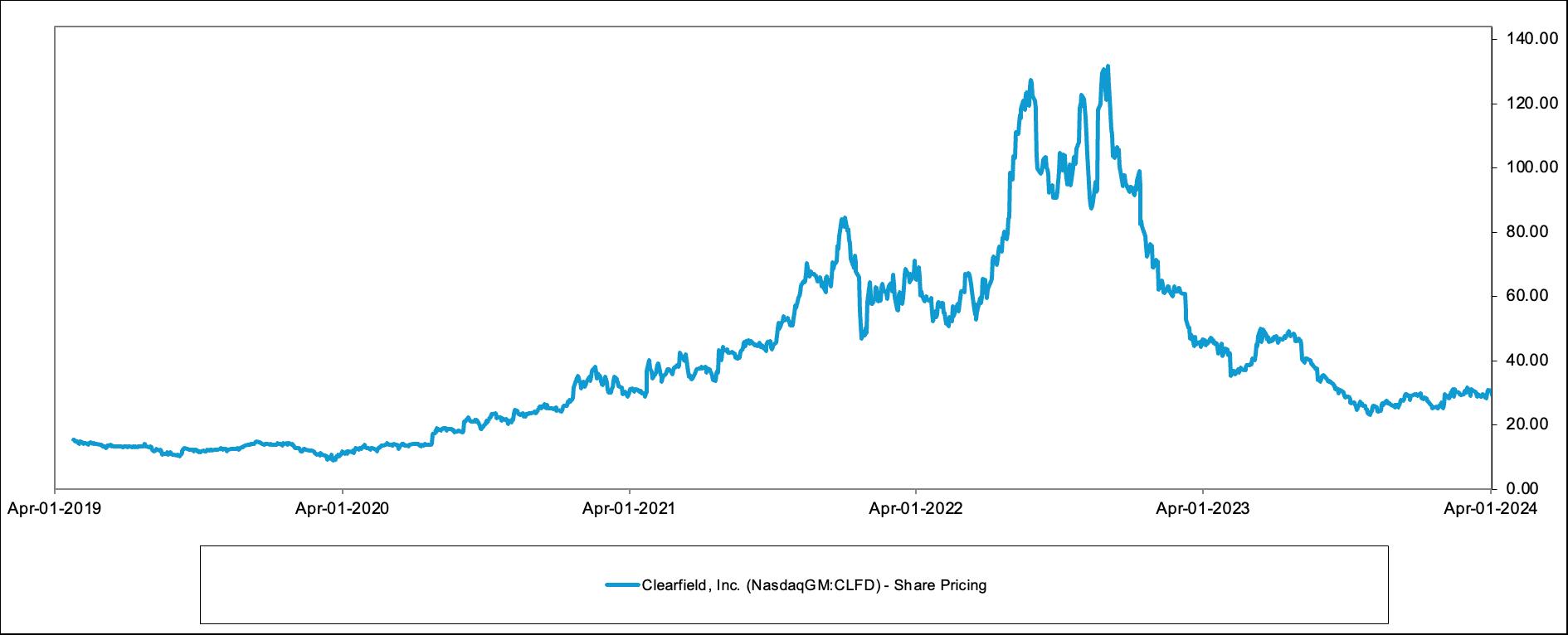

Clearfield is a designer and manufacturer of fiber optic connectivity and management products for the broadband service provider industry. During the COVID-19 pandemic fiber optic saw a surge in demand, shooting Clearfield’s stock price into the triple digits and pricing for perfection. In 2023, however, the company was hit with a reality check, and as demand came down so did the company’s share price While the company’s revenue is expected to decline in 2024 due to short term headwinds, the fiber industry still has a strong long term outlook, and Clearfield is attractively priced. The risks are not to be understated and Clearfield’s management team has faced difficulties in the past, but the long term outlook looks cautiously optimistic.

Valuation/Financial Modeling:

As of April 24th , 2024, Clearfield Inc is trading at $29 60 per share To value this company I conducted a discounted cash flow analysis, using a weighted average cost of capital (WACC) of 10.9% and a terminal growth rate of 3.0%. My revenue and FCF assumptions are in line with analyst and management projections of Clearfield’s revenue declining in 2024, rebounding in 2025, and growing at around the industry’s projected rate of growth in the years after. Using these assumptions, I came to a valuation of around $32 22, implying a slight upside of around 9 5%

BEAD Program:

The Broadband Equity Access and Deployment (BEAD) Program aims to expand high-speed internet access by funding planning, infrastructure deployment, and adoption programs, and is endowed with $42 billion Projects are to begin receiving funding in 2025, which is expected to lead to an increase in demand for fiber optics and grow Clearfield’s revenues. However, customers significantly increased orders throughout 2022 and 2023 to account for both the high demand for fiber optics during this time as well as the expected demand from the BEAD program. Consequently, many customers find themselves with excess inventory As such, there is lowered current demand for fiber optics, which has led to a poor 2024 projected revenue outlook. Management remains optimistic about the long term growth potential from the BEAD program.

Nestor Cables Acquisition:

In July 2022, Clearfield acquired Nestor Cables, a manufacturer of fiber optic cable solutions. The acquisition serves not only to generate revenues but also to bolster Clearfield’s manufacturing capacity, which is crucial especially considering the potential for future demand increases. In 2023, the Nestor Cables segment provided 16% of the company’s revenue. At the same time, the acquisition along with industry headwinds have begun squeezing Clearfield’s profit margins, with a current gross profit margin of 27.34% and EBITDA margin of 11.34%. This acquisition may serve to be extremely useful if demand does surge in 2025 and the years after, but could also create complications if short term industry headwinds continue to persist.

Griffin Murphy| April 24, 2024

Clearfield 5 Year Stock Chart

Source: S&P Capital IQ

Risk Potential

Excess Inventory:

One of the risks facing Clearfield is that, due to high anticipated demand, they have significant amounts of inventory on hand. If they are unable to recover from the decrease in sales in recent quarters, they could have difficulties emptying their inventory, leading to higher expenses and decreased cash flow from operations. Clearfield also may need to consider reducing their workforce to avoid unabsorbed labor costs in the face of weak demand.

High Customer Concentration:

In 2023, 16% of net sales were provided by the company’s largest customer. This indicates high customer concentration, and a decrease in orders from this customer or a cessation of their relationship could significantly impact Clearfield’s top line.

Uncertainties With BEAD Program:

The success of Clearfield relies heavily on the success of the BEAD Program creating demand within the fiber optic industry. Clearfield should be able to overcome the short term headwinds facing the industry and macroeconomy due to their strong balance sheet, but need their revenues to rebound in 2025 if they want to remain a growing and profitable company. The impacts of the BEAD Program are difficult to measure, and it is unclear how Clearfield and the broader fiber optic industry will respond once funding is allocated and put to use.

Sources:

Clearfield Investor Relations| CFRA Equity Research| Yahoo Finance | S&P Capital IQ | The Wall Street Journal | Nestor Cables Company Website

Vasu Patel| Apr 22, 2024

Rating: Buy

Current Price: $1 0.40

Price Target: $12 .50

Company Updates / News

● Market Cap: $2.14B

● 52 Week Range: 5.22 – 12.50

● EPS: 0.29

● Revenue: $325.1M

● Gross Margin: 87.3%

● Hired Marketing Veteran David Gee as Chief Marketing Officer

● Launched FedRAMP

Authorization Process to Provide Federal Customers with Enhanced Cloud Security

Competitor Statistics from FY 2023

Revenue: $4.48B

Gross Margin: 76.8%

Revenue: $910.39M

Gross Margin: 70.3%

Revenue: $448.8M

Gross Margin: 70.9%

Cellebrite DI Ltd. (CLBT)

Accelerating Justice Through Digital Security

Investment Thesis:

Cellebrite is a key player in digital intelligence, offering advanced solutions for data analysis crucial for law enforcement and intelligence agencies.

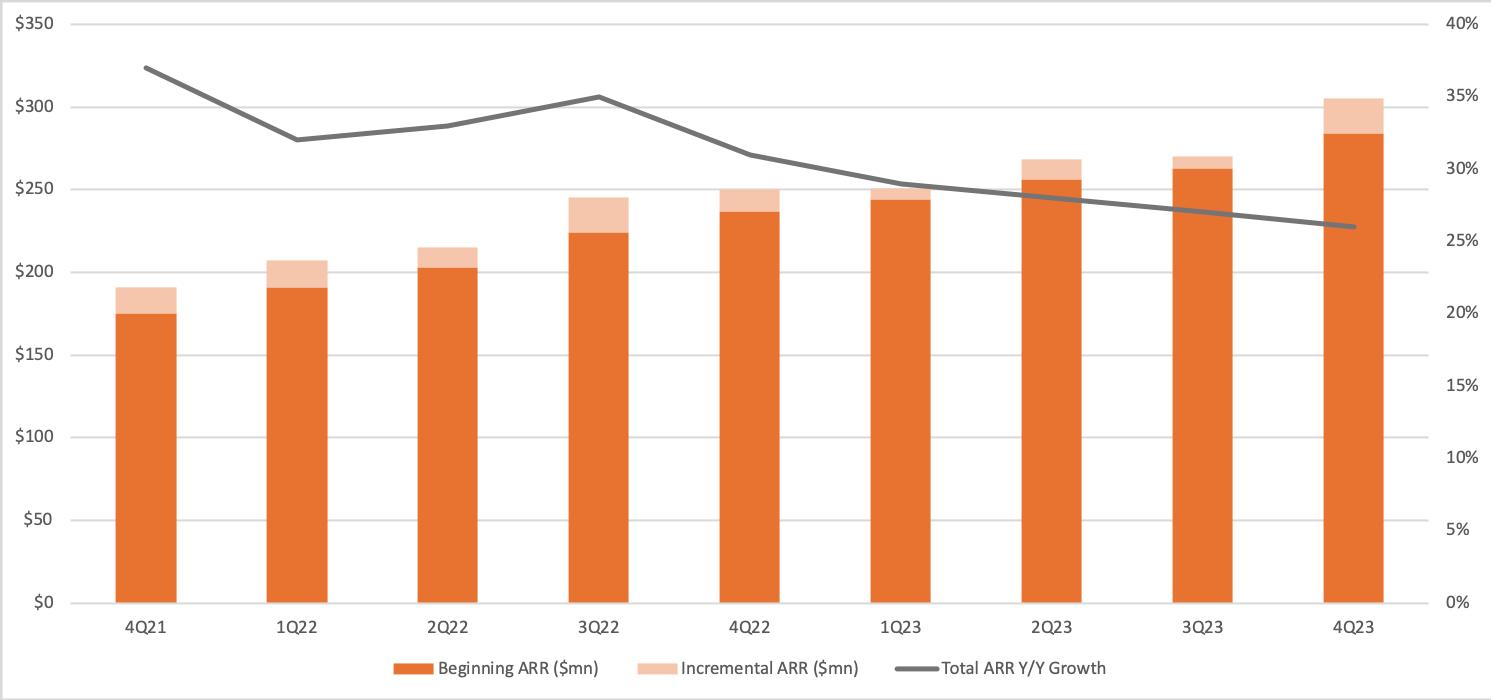

My buy recommendation for Cellebrite is based on its innovative edge, solid financials, and growth potential. The company's focus on automation, AI, and advanced data analytics drove a 26% year-over-year increase in ARR, which reached a record $315.7 million. With a strong balance sheet and a growing market, I believe Cellebrite is well-positioned for future success.

Valuation/Financial Modeling :

As of April 22nd, Cellebrite (CLBR) is trading at $10.40. I believe it's undervalued and expected to rise to $12.50 within the next twelve months. This conclusion stems from comparable analysis using historical and peer revenue data. Cellebrite’s shares trade at an Enterprise Value of less than 5 times annualized revenue, a discount compared to its peers and recent acquisitions in the sector. Based on my analysis, Cellebrite has a low enterprise value/EBITDA multiple of 7.6x, while the peer average is 15.1x.

Strategic Edge:

Cellebrite stands at the forefront of the digital intelligence market, offering stateof-the-art technology that revolutionizes productivity and efficiency. Their innovative solutions, infused with automation and artificial intelligence, cater to a wide range of industries, simplifying the investigative process for both public and private sectors. Through continuous investment in advanced technologies, Cellebrite delivers a comprehensive suite of services, ensuring seamless integration and optimal performance.

The company’s strong financial performance, including a durable top -line expansion and a healthy balance sheet, supports further profitability improvements. Strategic investments and innovation have expanded the Total Addressable Market (TAM), ensuring it remains well-positioned to capitalize on the powerful tailwinds driving the digital intelligence sector forward.

Fast & Consistent Growth:

Cellebrite stands out as an appealing investment with a robust business model that is on track for a 25% growth rate. The company has demonstrated its ability to innovate and has the potential to increase prices, which could significantly boost operational efficiency.

For FY23, Cellebrite reports a record ARR of $315.7 million, marking a 26% year-over-year increase. The fourth quarter alone saw a revenue of $93.0 million, up 27% year-over-year, primarily driven by a 30% growth in subscription revenue, alongside a record adjusted EBITDA of $22.7 million.

Vasu Patel| Apr 22, 2024

Cellebrite Quarterly Revenue Growt h

Source: Deutsche Bank Securities Inc.

Risk Potential

Cross-Sell and Upsell : To reach a $1 billion ARR by 2028, Cellebrite must focus on cross-selling and upselling to its existing customer base. The company has successfully completed its initial “land” phase, securing around 5,000 public sector customers, which represent approximately 90% of the target market for its offerings. Moving forward, Cellebrite’s growth largely hinges on its capacity to roll out innovative solutions and add-ons, enhancing the value proposition for these established clients.

Public Sentiment: Cellebrite’s financial reliance on law enforcement, with 90% of its revenue stemming from this sector, makes it vulnerable to shifts in public policy and sentiment, such as the “Defund the Police” movement. This advocacy for reallocating police funds could lead to budget cuts, affecting Cellebrite’s sales and contract renewals. Additionally, changes in spending priorities could result in decreased revenue for the company, as law enforcement agencies may reduce their investment in Cellebrite’s digital intelligence solutions.

Operating Expense Exposure:

Cellebrite’s exposure to the Israeli New Shekel (ILS) as a significant part of its operating expenses means that fluctuations in the currency can have a direct impact on the company’s financials. Approximately 40% of Cellebrite’s expenses, primarily payroll and rent, are paid in ILS. In the context of the Middle East, geopolitical tensions can lead to economic instability, which often results in currency volatility.

Sources: Cellebrite Investor Relations | Needham & Company | Everbridge Investor Relations | Bloomberg | Capital IQ | OpenText Investor Relations | Verint Investor Relations | Deutsche Bank Securities Inc | SEC.gov | JP Morgan |

1Q2024Recap-OzempicOlympics

Healthcare names generally underperformed theS&P 500in1Q24followingcalmersentimentsurrounding GLP-1sandotherweightlossdrugsandJanuaryCMS ratecuts,butupsideliesinhighlyanticipa drugdevelopmentsin2H24.

Weight loss drugs remain in the spotlight: Although analysts believe weight loss drugs have already peaked, the spotlight. As of April 2024, there are 11 FD medications for weight loss, with 14 more showing supporting data in clinical trials so far 1 Viking Therapeutics other challengers encroach on Ozempic and Weg leadership in the market, touting easier delivery methods with similar effectiveness Increased regulatory scrutiny of Medicaid/Medicare coverage of the drugs also limit addressable market for those in higher income brac drawbacks, LLY and NOVO remain key players in the market with highly anticipated pipeline products while also boosting the performance of smaller players in the space.

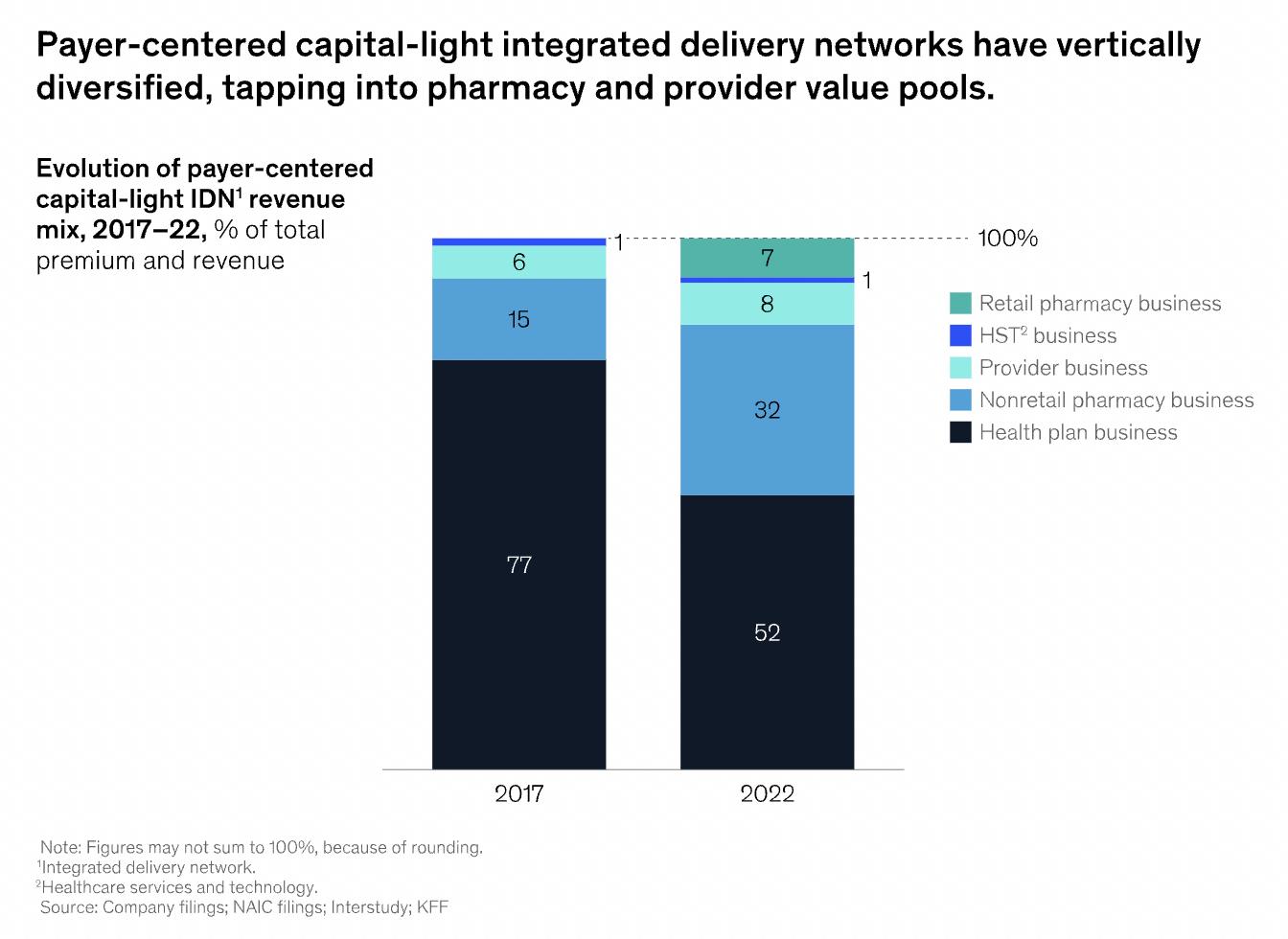

networks have vertically diversified, tapping into pharmacy and provider value pools” (McKinsey)

Payors re-examine the efficacy of new technologies: The year started off with UnitedHealth Group suffering a cybersecurity attack on subsidiary Charge Healthcare, which disrupted 94% of providers’ ability to be reimbursed by insurers and fill medication orders, disrupting hospital revenue cycles nationwide.2 This cyberattack not only impacted UNHs stock with a 6% drop on the announcement date, but the unprecedented magnitude of the attack may accelerate the adoption of cybersecurity measures in the healthcare payors and telehealth industries. This follows insurance giant Cigna’s $172M settlement in late 2023 where the Department of Justice investigated claims that Cigna's PxDx (procedure-to-diagnosis) algorithm wrongfully rejected over 300,000 payment claims.3 Large payors use technology to speed up day-to-day processes, but social and ethical directives are being left behind. Moreover, major payors are now 10x the size of the largest health systems, giving them a huge advantage when negotiating payments

“The Centers for Medicare & Medicaid Services (CMS) rate declined for the first time since 2015” (McKinsey)

Medicare spending cuts and 2024 Election Spotlight: Medicare spending cuts through revisions at the beginning of 2024. If these trends continue, many insurers are considering cutting benefits in 2025 if CMS proceeds with the cuts Medicare Advantage, a politically contested system, now covers over half of those eligible for Medicare, and is backed by many big payors, even when CMS overpaid Medicare Advantage organizations an estimated $16.6 billion in FY 2023.4 Although healthcare is not dubbed as a key issue during the election, both Democrats and Republicans are worried about the rising costs of social security and further cuts in public healthcare funding systems. The anticipated largest point of debate will surround the continuation of the 2010 Affordable Care Act (Obamacare), but both Trump and Biden are concerned about bringing down medical and pharmaceutical inflation. 5

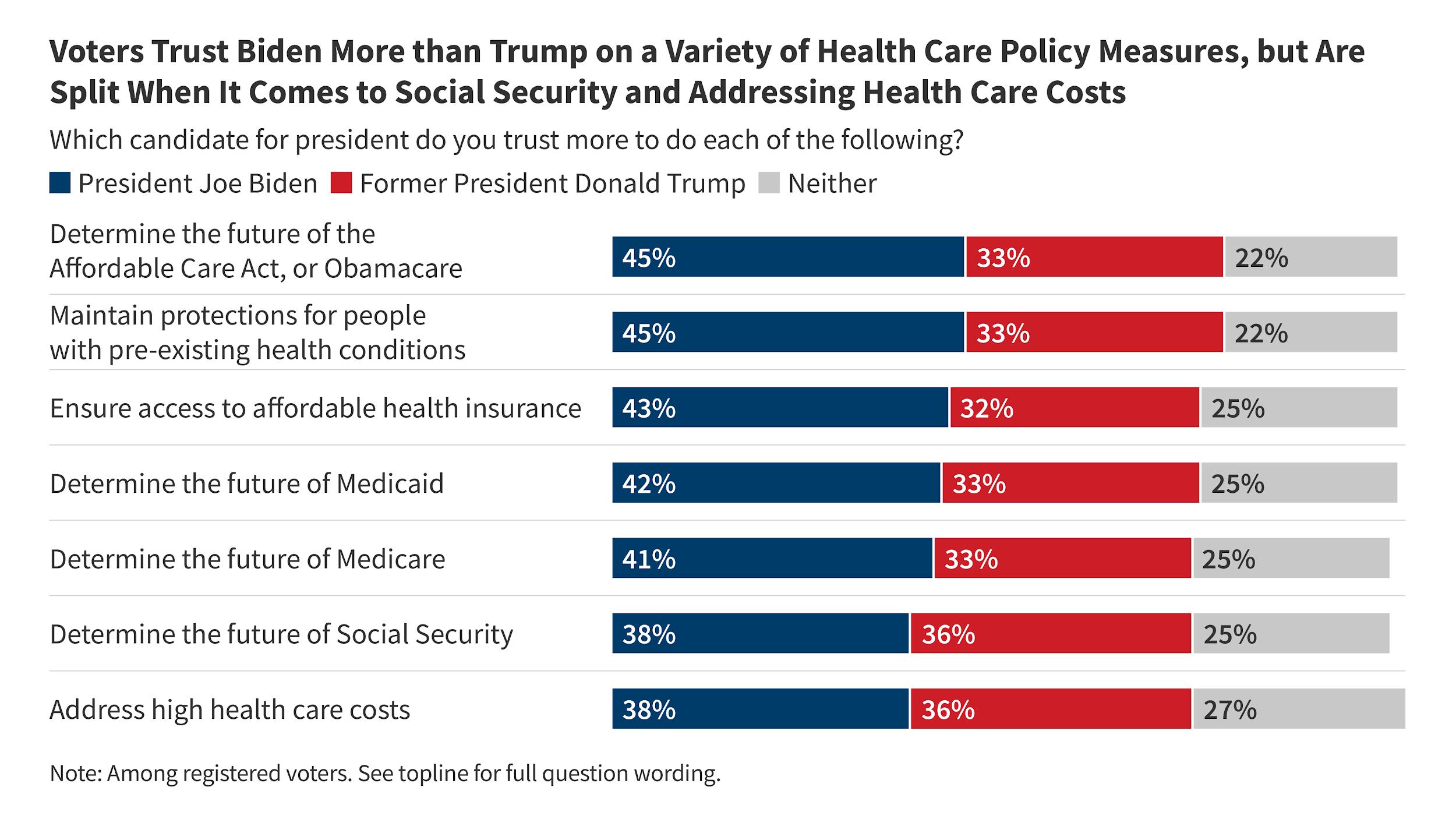

Voters are more on Biden’s side when it comes to managing healthcare policy (KFF Survey)

Orphan drug developments to drive pharma outperformance: The most anticipated drug launches of 2024 include KarXT, a schizophrenia treatment from biotech Karuna Therapeutics which was acquired by Bristol Myers Squibb in 2023.6 Sales estimation platform Evaluate projects sales of $2.8B in sales of the drug by 2028. Other hopefuls include donanemab for Alzheimer’s from Eli Lilly, and resmetirom for non-alcoholic fatty liver from Madrigal Pharmaceuticals. As schizophrenia is uncommon, there are few effective treatments and symptoms can be severe. With two promising phase 3 candidates

and the advantage of superior clinical performance as well as an absence of side effects as are in existing schitzophrenia treatments, the company stands to capture share in the market. This drug is a part of the larger trend towards more orphan drug and gene therapy commercialization, incentivized by the FDA’s Accelerating Rare disease Cures (ARC) Program, launched in May 2022. Although these are big steps towards treating rare diseases, the sustainability of financial incentives will be called into question if Medicare/Medicaid funding decreases. Many pharmaceuticals have already had prices challenged and the patent cliff between 2024-2028 could significantly decrease drugmakers’ pricing power.

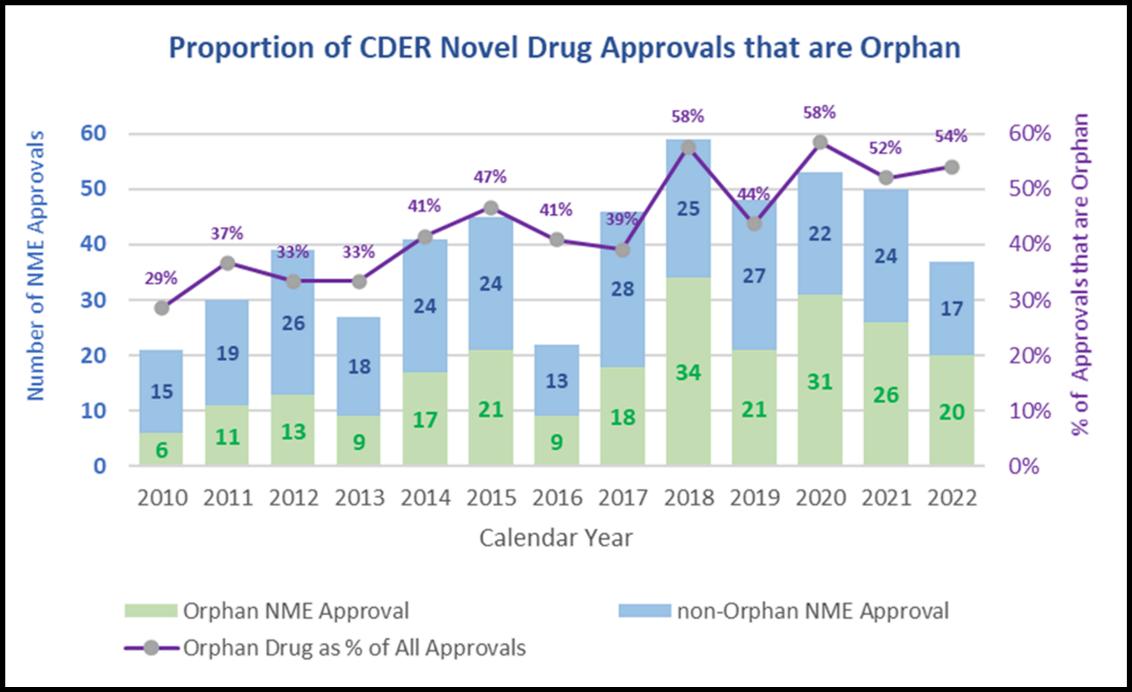

Not pictured: Record number of orphan drug approvals in 2023 (28) under the ARC program (Center for Drug Evaluation and Research)

Conclusion: While repercussions and backlog from the pandemic years are mostly resolved, the Healthcare Sector continues to underperform the index as demands slow and cost-cutting policies are on the horizon. Key catalysts and risks for investors to look out for in 2H 2024 include key drug approvals and potential interest rate cuts Major risks include the policy implications of the US 2024 election including future CMS rate cuts, and Medicare Advantage-associated demand drops due to increased costs to the patient. Overall, the healthcare industry is a hold, but due to low valuation investors are encouraged to pick stocks. 6

Emma Braff | 21 April 2024

Rating: Hold

Current Price: $501.00

Price Target: $516.00

Company Updates

● 52 Week Range: $436.38- $554.70

● Market Cap: $462B

● Dividend: 7.52

● P/E (TTM): 19.45

● Revenue: $371.62B

● Debt to Equity: 75.98

Competitor Statistics TTM

Revenue: $379.49B

Net Income: $22.38B

Revenue: $357.77B Net Income: $8.34B

Revenue: $195.19B Net Income: $5.16B

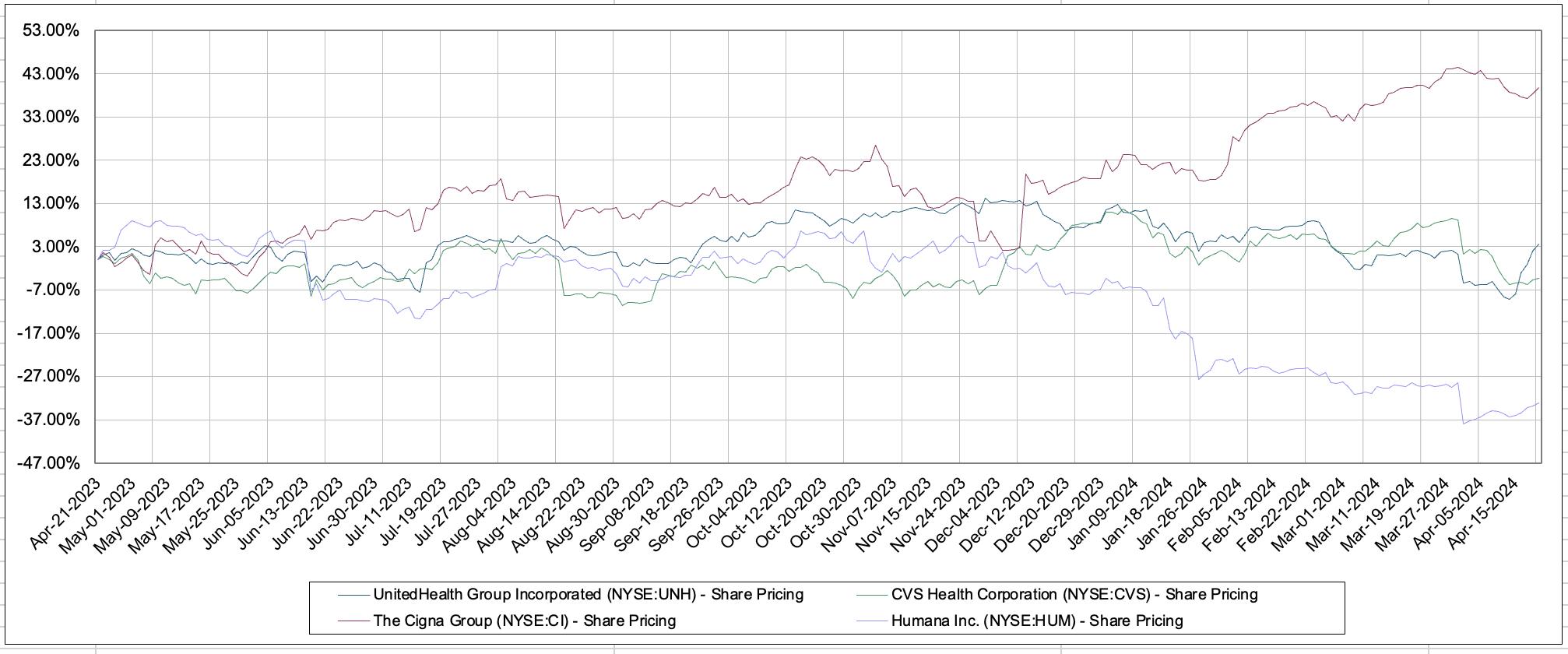

UnitedHealth Group Inc. (UNH) Waiting Out the Storm

Investment Thesis:

UnitedHealth Group Inc represents a combination of the Optum and UnitedHealthcare business platforms across four reportable segments (Optum Health, Optum Insight, Optum Rx, and UnitedHealthcare). This diversified business model and industry-leading size offer economies of scale in health plans, delivery, and optimization.

My hold recommendation reflects a belief that the market has digested recent upside surprises, including better-than-expected earnings, while risks stemming from the Change Healthcare cyberattack and CMS rates persist.

Valuation:

As of April 21st, UnitedHealth Group Inc. (UNH) is trading at $501.00. I expect this equity to see a modest increase up to $516.00 within the next twelve months. This conclusion reflects quantitative comparable analysis based on historical EPS data. I expect EPS for 2024 to reach 28.68, based on a projection of the average growth since 2020. I use an 18x multiple to reconcile the scale of the company and resilient fundamentals with an expected poorer performance for the coming year due to CMS policy and other downward pressures.

Overview:

In 2023, UnitedHealth Group Inc. saw total assets increase from $245.7B to $273.7B (11.4%) and total liabilities increase from $159.4B to $174.8B (9.7%).

The company continues to use high levels of debt in its business model and prioritizes strategic acquisitions The company’s Q1 results show adjusted earnings of $6.26 per share compared to Wall Street’s expected $6.16 per share The medical-loss ratio was also 82.2% below expectations As such, UNH has seen gains throughout the past week.

The company also engaged in strong dividend and buyback programs in 2023, giving out $6.8B in dividends and $8.0B in repurchases, up from $6B and $7.0B respectively in 2022.

In 2021, UNH acquired Change Healthcare in an $8B deal to improve its data and analytics. Along with the Optum business segment, this addition demonstrates UNH’s movement into the healthcare technology space—an increasingly lucrative industry.

Emma Braff | 21 April 2024

Historical Comparable Share Pricing (TTM)

Source: S&P Capital IQ

Risk Potential

Cyberattack: The Change Healthcare February 21 data breach forced the company to pause its extensive payment and billing service in the largest domestic healthcare disruption since the COVID-19 pandemic. Months later, claims and benefits continue to be inaccessible or disrupted for many users. Although the initial financial consequences have been minimal, this attack presents substantial reputational risk to the company as stakeholders continue to suffer the consequences, and represents a setback in the reliance on electronic technology in the sector.

CMS Rates: Companies across the sector have seen share prices fall due to increased cost pressures on Medicare insurers. On April 1, the Centers for Medicare & Medicaid Services (CMS) released lower-than-expected rates for Calendar Year (CY) 2025, at an estimated decrease of 0.16%. Following the announcement, UNH fell 6% while CVS dropped 7% and Humana over 10%.

Rising Medicare Costs and Legal Pressures: Medicare insurers have cited increasing medical costs, with seniors utilizing more care than expected, more inpatient hospital stays, increased doctor visits, and higher demand for outpatient services The federal Medicare regulatory agency has also introduced regulatory adjustments, while the Biden administration has historically taken action against for-profit activities in the healthcare sector with bipartisan support. One such preventative measure includes the No Surprises Act. Healthcare reform continues with increased talks regarding private equity investment in the industry and health plan structure UNH remains vulnerable to any material changes or increased speculation in this dynamic political space, especially as regulation increases

Sources: UnitedHealth Group Inc Investor Relations | S&P Capital IQ | CFRA Equity Research | Yahoo Finance | The Wall Street Journal | Bloomberg | CMS gov | Forbes

Bement| 04/21/2024

Rating: Buy

Current Price: $125.40

Price Target: $136.21

Company Updates / News

● Market Cap: $318.60B

● Beta: 0.40

● EPS: 0.14

● PE Ratio: 68.7

● 52 Week High: $133.10

● 52 Week Low: $99.14

● Recent Acquisition of Harpoon Therapeutics, Prometheus Bio, Acceleron Pharma

● The petcare industry is thriving with a 5.22% compound annual growth rate

Competitor Statistics

TTM

EV/EBITDA: 50.18

Revenue: $60.12B

EV/EBITDA: 19.55

Revenue: $18.53B

EV/EBITDA: 21.49

Revenue: $58.50

Investment Thesis:

Merck stands out as a dominant force in both the human and animal pharmaceutical sectors It offers over 50 products targeting crucial areas such as cancer treatment and prevention, diabetes management, and COVID-19 therapies. In the animal health domain, Merck is a top provider of flea, tick, and heartworm prevention solutions. The company has been aggressively expanding through acquisitions, including the purchase of Acceleron Pharma in 2021, Prometheus Bio in the third quarter of 2023, and Harpoon Therapeutics in February These substantial investments have temporarily reduced earnings per share as Merck gears up for a new growth phase A significant driver of revenue, the cancer medication Keytruda, is set to lose patent protection in 2028, highlighting the importance of these strategic acquisitions Given these dynamics and the expected growth in the animal healthcare sector, I recommend a buy on Merck shares, anticipating that these moves will propel the company beyond its current market value

Valuation:

As of April 21st , 2024, Merck was trading at $125 40 per share I believe that the stock is undervalued with an increase to $136.21. This evaluation was arrived at using a Discounted Cash Flow with a terminal growth rate of 2.0% and weighted average cost of capital of 8 71% across 10 years These assumptions are based on Merck's historical growth rate and an optimistic viewpoint of its performance in new healthcare markets as well as the growing animal healthcare market in the United States

Expansion:

Recently, Merck has made significant strategic acquisitions to bolster its pipeline, particularly in immunology and neurodegenerative diseases. In 2023, Merck acquired Prometheus Biosciences for approximately $11 billion, a move that enhances its capabilities in treating immune-mediated diseases like ulcerative colitis and Crohn's disease. This acquisition brings a promising candidate, PRA023 (now MK-7240), a monoclonal antibody aimed at inflammatory bowel disease, into Merck's portfolio In another move to expand its research in neurodegenerative diseases, Merck acquired Harpoon Therapeutics for up to $610 million. This acquisition is part of Merck's strategy to delve deeper into treatments for conditions such as Parkinson's and Alzheimer's diseases, emphasizing their commitment to addressing complex brain disorders

Product Breakdown:

Merck's revenue distribution is heavily skewed towards human healthcare predominately in prescription medications, which contributes about 90% of its total revenue, while animal healthcare, divided between livestock and companion animals, accounts for 9% In the fourth quarter of 2023, Keytruda a cancer immunotherapy drug effective against various head and neck cancers represented 45% of Merck's Additionally, Keytruda's sales made up 42% of total revenue in 2023. With Keytruda's patent protection expiring in 2028, this significant revenue stream is a key motivator behind Merck's recent strategy to acquire other pharmaceutical companies.

Julian Bement| 04/21/2024

Zoetis vs Merck Monthly Share Price (YTD)

Source: S&P Capital IQ

Risk Potential Investment Uncertainty:

Merck's acquisitions carry several risks, including integration challenges that could lead to operational disruptions and cultural clashes. Regulatory hurdles and development risks pose significant threats, as failures in clinical trials or regulatory approvals could impede the success of newly acquired treatments like PRA023 (MK-7240). The financial commitment, notably the $11 billion spent on Prometheus Biosciences, exposes Merck to substantial financial risk if these assets do not yield expected returns. Additionally, market adoption uncertainties and potential intellectual property disputes could further complicate the outcomes of these strategic investments.

Market Uncertainty:

Over the past decade, spending in the petcare industry has surged by more than 100%, but this rapid growth may stabilize in the coming years The surge in pet ownership during the pandemic has led to an increase in expenditures for initial vaccinations, like those for distemper and rabies However, as these pets grow older, spending on such vaccines might decline

Cigna Corporation, headquartered in the United States, is a global health services company that provides medical, dental, disability, life, and accident insurance, as well as related products and services. The firm is also planning a big move recently as it is anticipated at least $5 billion will be used for repurchases by the end of June 2024. This repurchase reflects Cigna's belief that the stock price is significantly undervalued.

Cigna consistently shows growth potential, with a compounded revenue growth rate of 32% over the last five years and net profit reaching $5.2 billion in 2023. In terms of market share growth, as of December 31, 2023, Cigna's total pharmacy customer base increased by 5% yoy, reaching 98.6 million, indicating significant success in expanding its customer base and market share.

Valuation:

As of April 13, 2024, Cigna (CI) is trading at $349.84. I conducted a comparable company analysis (using the EV/R multiple) incorporating data from UnitedHealth, Humana, Molina Healthcare, HCA Healthcare and Davita which arrived at an implied share price of $392.34. Therefore, I believe that CI is undervalued and will increase in price over the next 24 months

Innovation and technology investment:

In the healthcare industry, innovation and technology investment are key drivers for long-term growth. Cigna announced an additional $450 million investment in its corporate venture fund, Cigna Ventures, focusing on identifying and partnering with health tech startups This demonstrates the company's commitment to fostering innovation and transformation in the healthcare sector For example, Cigna Ventures participated in a $52 million Series C funding round for 'Octave' to drive the nationwide expansion of web-based psychiatric clinic services, indicating that Cigna is actively exploring and developing new areas of health technology

Overview:

In terms of market concentration, the business model under the U.S managed care system has matured, and the market concentration is relatively high. There are several major managed care companies (such as UnitedHealth and Humana) that dominate the industry, and leading enterprises are expected to gain significant share in the next two years.

Amy Ren | April 12, 2024

Stock Price with Competitors:

Source: Yahoo Finance

Risk Potential

Regulatory Changes: MCOs are heavily regulated, and any changes in government policies or regulations can significantly impact their operations This includes potential modifications to laws like the Affordable Care Act (ACA) or Medicare and Medicaid policies

Market Competition: The market for healthcare services is competitive, with MCOs competing not only with each other (new entrants) but also with other types of healthcare providers and emerging models of care delivery.

Economic Downturns: Economic uncertainty or downturns can affect the ability of individuals and employers to pay for health insurance, which in turn impacts the revenue of MCOs.

Sources: Pickers Research| Wind|Reuters | Company Official Website(Investor Relations)|PR Newswire|IHC|JP Morgan

Cole Gaines | 4/23/2024

Rating: Buy

Current Price:

$900.16

Price Target: $978.47

Company Updates

● 52 Week Range:

$648.81-$998.33

● Shares Outstanding: 106.3M

● Market Cap: $98.44B

● P/E (TTM): 25.90

● Revenue: $13.12B

● Debt to Equity: 10.74%

Competitor Statistics from Q3 2021

Revenue: 13.12B

Net Income: 3.95B

Revenue: 9.87B

Net Income: 3.62B

R Net Income: 1.59B

Regeneron Pharmaceuticals Inc. (REGN) Pipeline to Success

Investment Thesis:

Regeneron Pharmaceuticals Inc (NASDAQ: REGN) is a biotechnology company engaged in the discovery, development, and commercialization of drug treatments across several fields including ophthalmology, oncology, cardiology, as well as inflammatory and immune disorders, infectious diseases, and genomic medicine. My buy recommendation is motivated by Regeneron’s strong financials, with strong revenue growth (excluding Ronapreve) of 14% for Q42022 to Q42023. Furthermore, it has optimistic growth potential after receiving approval in the US, Europe, and Japan for the treatment of patients with EYLEA 8 mg which outperformed analyst predictions in earnings and EPS.

Valuation/Financial Modeling:

As of April 22nd, Regeneron (REGN) is trading at $900.16. I believe Regeneron to be slightly undervalued and expected to reach a price of $978.47 within this year, which yields an 8.7% upside. I came to this conclusion by conducting a Comparable Company Analysis (CCA) between Regeneron, Vertex Pharmaceuticals, Sanofi, Boston Scientific, Amgen, and Bristol-Myers Squibb using a 1.8% Average GDP Growth rate. These companies were chosen for their comparable market cap, similar regulatory compliance and business models, and similar stages of maturity and growth.

Overview

Regeneron’s business relies on its blockbuster medication EYLEA, which treats age-related macular degeneration, diabetic macular oedema, and diabetic retinopathy. Recent FDA approval for a high dose (8 mg) of the drug is projected to motivate its growth and shields the company from the threat of biosimilar products soon to enter the market to compete with the 2 mg variation.

Regeneron’s partnership with Sanofi (SNY) to develop Dupixent, a drug with broad applicability to several inflammatory conditions, has been highly profitable and has become one of the fastest-growing drugs in the biotechnology sector with ongoing approval to expand into further markets Predictions for the annual sales of Dupixent reach nearly $20 billion by some analysts. The development of Libtayo is expected to become a blockbuster product and has nearly doubled in global revenues from 2022-2023. These give Regeneron a diversified product lineup.

Finally, Regeneron has been highly recognized for its success in developing a robust R&D pipeline, hosting 35 ongoing clinical trials, and utilizes new technologies in genomics and gene modification. Their emphasis on human gene research has been proven very effective in increasing clinical success. They also announced plans to work with Intellia Therapeutics on expanding gene-editing therapies.

Regeneron has a PE ratio of 25.9, which is about 0.79x less than the industry average, contributing to an optimistic outlook on potential growth. Furthermore, Regeneron repurchased ~2.2B of shares in 2023 and is investing nearly ~5B in R&D in 2024.

Historical TTM Comparable Share Pricing

Risk Potential

Decline in Earnings:

Despite Regeneron’s decline in EPS during Q4 of 2023 as compared to Q4 of 2022, their earnings decline can be partly explained by a $0.21 impact from the acquired IPR&D charge However, projections for Q1 of 2024 have earnings growth at 4.02% with Regeneron having outperformed earnings projections for the last 4 quarters Furthermore, there is optimism for earnings growth as EYLEA HD is rolled out to reignite falling revenue from EYLEA 2 mg

DOJ Complaint:

Shares dropped earlier this month after the United States Department of Justice filed a complaint against Regeneron, accusing the company of fraudulent drug pricing The DOJ filed this complaint under the False Claims Act, alleging the company inflated the Medicare reimbursement rates for Eylea, which could have allowed Eylea to become the market leader in its space If found guilty, the government is allowed to recover 3x the amount of its losses from the company Sources:

Julian Dahl| 4/21/2024

Rating: Buy

Current Price: $117.43

Price Target: $126.10

Company Updates

● Market Cap: $18.701B

● Beta: 1.19

● EPS: $0.81

● PE Ratio: 149.58

● 52 Week High: 229.55

● 52 Week Low: 89.00

● Biotechnology industry and Illumina specifically outperformed sales expectations in the past quarter

● Appointment of a new CEO at the end of 2023 and a new CFO this year increase prospects of future shareholder value

Competitor Statistics from Q4 2023

Revenue: $10.89B

Revenue: $ 1.69B

Illumina (ILMN)

Capitalizing on New Leadership and AI

Investment Thesis:

Since Illumina’s founding in 1998, the company has focused on innovation in the field of genomics and has experienced extensive growth with its creation of integrated systems for the analysis of genetic variation.

My buy recommendation reflects a belief that Illumina will experience increased profitability under new leadership and with the advancement of its CRISPR gene editing technology through developments in AI.

Valuation/Financial Modeling:

As of April 4th, Illumina (ILMN) is trading at $117.43. I believe that this equity is undervalued and expected to increase to $126.19 this year. I arrived at this conclusion by conducting a DCF analysis with a 4% growth, 17.5% operating margin, and a WACC of 8.97% across 5 years. I used these assumptions based on historical data and an optimistic view given Illumina’s performance history and the outlook of the biotechnology industry as a whole.

Genetic Sequencing, AI and Illumina’s Advantage:

Illumina is known to have the most advanced systems that carry out DNA sequencing at capacity, speeds and costs that are unrivaled within the healthcare industry. This technological advantage places Illumina at the forefront of the healthcare industry as more companies enter the healthcare space with new ways for Illumina to implement its systems

Additionally, the emergence of AI allows Illumina to create more sophisticated genomic analysis and further innovate its systems Illumina has already unveiled AI software that can predict disease-causing genetic mutations in patients

Overview:

Within the past 5 years, Illumina’s stock has experienced significant turmoil, breaking a stock price of $500 in 2021 and falling below a price of $100 at the end of 2023 as investors began to realistically evaluate the financials after a subpar earnings report. Yet, the company’s promising technology has solidified Illumina as a leader in the genomics market, which needs to be taken into consideration when valuing the company.

Therefore, my categorization of ILMN as a buy takes growing forecasted earnings and continued industry dominance into account as well as the assumption that new company leadership will realize untapped growth.

Julian Dahl| 4/21/2024

Forecasted Consistency and Rebound from 2023 Q4 Lackluster Performance

Source: Yahoo Finance Risk Potential

2024 Q1 Earnings Report: A significant factor that will heavily impact Illumina’s stock price in the near future is its 2024 Q1 earnings report, which will be released on May 2. If Illumina outperforms earnings expectations, it will immediately cause an increase in the stock price as a stellar performance shows that Illumina’s new leadership is steering the company in the right direction.

Legal Disputes: Illumina had been dealing with an antitrust lawsuit from the FTC until the end of 2023, which led to Illumina’s divestment from Grail, a manufacturer of cancer detection tests This lawsuit reversed Illumina’s progress in the cancer treatment market, in which Illumina wanted to increase its market share However, the loss of this lawsuit does not remove Illumina from contention for market share as this ruling only made the cancer treatment more competitive. Illumina’s innovative technology still gives the firm a competitive edge.

Sources:

Financials

1Q2024Recap:TheBadNewsDon’tStop

The �nancial industry is still playing it close to the chest in early 2024. Even as some individual companies maybeoutpacingtheirpeersasthingsreturnto“normal”, no one wants to get caught in a whirlwind of potential economic woes. The mostdebatedtopicintheindustryis stillwhetherornotthemarketwillachievethecovetedsoft landing. Adding fuel to the �re, �rst quarter earnings showed a wide range of results from individual names. Common themes include lower net interest income, concern about in�ation, and higher fees returning for investmentbankingbusiness.Thetrueimpacthasyettobe seenbuttherestoftheyearissuretobeatumulta�air.

Worse than expected economic data continues to put pressure on the Fed to keep interest rates high. At the beginning of 2024, the market, investors, and economists were optimistic that the Federal Reserve would cut interest rates down around 6 -7 times from their 20-year high of 5.5%. The Fed raised their target Federal Funds Rate in response to soaring inflation in 2021. Now that sentiment has all but been eliminated. The most bullish experts now are planning for only around 3 rate cuts for the full year. Bearish investors are arguing for the possibility of a hard landing and the economy heading into a recession.

Inflation has still not come down to the 2% goal, sitting at an average of 3.4% for FY23 and ~2.8% for the first three months of the year. In parallel, unemployment has remained surprisingly lowbased on a belief from employers who don’t want to get caught short staffed like directly after the pandemic Whereas, the inflation we are currently experiencing should typically drive up unemployment. Furthermore, 1Q GDP dropped to 1.6% from 3.4% a quarter prior, significantly lower than expected. This combined negative economic data puts the Fed at an awkward position - trying to stifle inflation while not driving down growth so much that the economy falls into a recession. Fed chairman, Jerome Powell, has retained a conservative attitude and method of attack towards this problem and the market seemingly expects him to continue this approach.

Metrics and Graphs (Put titles/description under graph)

Investment banking and Private Equity business, blah blah - fighting back. Space. As they lock eyes, what world they know is flipped completely towards the southern sky, and the pool ushers them swiftly towards the edge of the horizon’s curve. The fox and the dog free-fall off the edge into nothing, which is to say, they were fine Landing promptly on the other side of the world, they look up into what is somehow a giant hand, impossibly looking back at them. The hand bends toward them without beckoning, and the dog and fox survey their new landscape, the under-pool or their second world.The hand bends toward them without beck

Known for his sweetness, this dog shakes himself awake with a gentle groan and cranes his loaf-like head towards the fox with a quizzical bent. As they lock eyes, what world they know is flipped completely towards the southern sky, and the pool ushers them swiftly towards the edge of the horizon’s curve The fox and the dog free-fall off the edge into nothing, which is to say, they were fine

FinTech leading the charge as the industry settles into the 21st Century. One of the biggest changes in the financial space is the implementation of technology into the

leaves fall without a plan to the ground, mirroring the unhurried chestnut thatch of the fox’s dense coat. The fox looks to the west, only then realising the horizon has begun to curve towards them. Perhaps they should not have jumped so soon. The hem of the pool expands indefinitely, ringing the sleeping dog and now worried fox with concentric circles of glowing liquid.

Basel III Endgame and other expected regulations upsetting companies Only one bank has failed so far this year - Republic First, compared to the spiraling trend of similar failures in 2023. The FDIC took over the failed banks in an attempt to recover depositors’ funds, and subsequently regulators sold the banks’ assets to peers

This comes at a time when US regulators are proposing stepped up requirements for banks. The proposals are based on the recommendations of the Basel Committee in response to the Great Financial Crisis of ‘09. They include higher reserve requirements, stricter risk testing, and heightening the requirements for banks with smaller amounts of assets.

The industry has pushed back against the current Endgame prospal, which would not go into effect until July 2025. The industry argues that the suggested guidelines would lower profitability and reduce competition, ultimately causing more banks to fail.

Augustus Paluzzi | 4/22/2024

Rating: Sell

Current Price: $231.04

Price Target: $164.02

Company Updates

● P/E: 19.03

● Equity Value: $168B

● EPS: $11.21

● 52 Week Low: $140.91

● 52 Week High: $242.30

● Shares Outstanding: $723M

Competitor Statistics from Q4 2023

Cards issued: 2.9B

Revenue: $32.7B

Cards issued: 2.7B

Revenue: $25.09B

Cards Issued: 44M

Revenue: $49.48B

American Express (AXP) The Future of Retail Lending

Investment Thesis:

American Express (AXP) serves a wide range of different customers across the globe, offering consumer credit and lending services, as well as loan opportunities As of April 2024, the firm maintains 4.61% of total global credit card usage as compared to 38.7% and 24% for Visa and Mastercard respectively

My sell recommendation reflects a belief that the firm’s COGS has steadily risen over the past few years cutting into margins year on year, and additionally, the firm has undergone several instances of restructuring but still has a fairly poor BBB+ rating With the anticipation of high future interest rates and internal issues within the firm.

Valuation/Financial Modeling:

As of April 22nd, American Express (AXP) is trading at $231.04 I believe that this equity is overvalued and expected to decrease to $164.02 over the next few years. I arrived at this conclusion by conducting a DCF analysis with a tax rate of 23%, risk free rate of 2.944%, beta of 1.23, and a WACC of 5.2%. based on the firm’s bond rating and market premium from the S&P average. This gives an implied downside for the firm and supports a view of the sell rating primarily driven by the firm's high COGS growth limiting cashflows.

High Interest Environment:

The US federal reserve is currently targeting a higher for longer interest rate which will cut directly into the firm’s lending and loan revenue. Additionally, the US government is exploring higher liquidity requirements following the implosion of Silicon Valley Bank and other regional banks. These potential changes may also change the lending environment which will further cut into future revenues. In order to mitigate these changes the firm may need to explore a modification of its current lending model and its interest deposit structure in order to meet liquidity guidelines.

Overview:

In 2024 the firm had a 10.7% market share and has demonstrated strong YTD growth, contributing to a view of being overvalued as a factor of the actual underlying equity. The firm’s shares have realized a 22% YTD growth although the firm only experienced a 9.8% growth in total gross revenues (after loan losses) and a 10.39% increase in COGS

Augustus Paluzzi | 4/22/2024

Opening Price of Visa and American Express YTD:

Source: Yahoo Finance

Risk Potential: Potential Upsides

The firm has seen strong year-to-year revenue growth across several of its divisions which has bolstered the firm's earnings performance increasing bullish sentiment on the firm. The firm also maintains a great deal of cash reserves in the form of cash and short-term investments, which provides a cushion to future liquidity issues if they occur.

The firm has also seen a revamping of its member rewards programs which has injected fresh capital into the company's reserves as customers aim to fully utilize their points. This led to a greater amount of cash for the firm, which was promptly used on advertising expenses and reinvested in the firm's core operations to contribute to further revenue generation.

The firm’s primary competitive advantage over its competitors is its offerings to high net worth individuals such as the platinum and black cards, which contribute to the firm’s strong brand image and cache as the choice of the perceived wealthy. These offerings provide the firm not only with very productive revenue streams but also create a public perception which favors the brand publicly.

Gregory Bucher | 23 May 2024

Rating: Buy

Current Price: 124.42

Price Target: 193.42

Company Updates

● Market Cap: $13.33B

● Beta: 0.81

● EPS: 5.54

● PE Ratio: 22.9

● 52 Week High: $127.00

● 52 Week Low: $72.60

Competitor Statistics

Revenue: $1.865B

Interactive Brokers Group Inc. (IBKR) Riding the Wave

Investment Thesis:

Interactive Brokers Group Inc is an online trading brokerage that allows consumers to execute trades at low costs while providing advanced analytic tools. Interactive Brokers provides services to retail investors, hedge funds, proprietary traders, and financial advisors. The main source of revenue for this company is trading commissions.

My buy recommendation reflects the belief that Interactive Brokers will be able to beat its quarter two earnings report due to the strong financials that it has posted over the past few years. Namely, the company has increased revenue at a compound rate of 17.9% over the past five years with net income experiencing growth as well. Additionally, the firm has been pushing to expose itself to more clients including retail investors and institutional clients.

Valuation:

As of May 23rd, Interactive Brokers Group Inc. (IBKR) is trading at $124.42. I expect this equity to see a sharp increase up to $193.42 within the next twelve months. This conclusion reflects quantitative comparable analysis based on historical increases in revenue data. I expect revenue for the end of 2024 to reach 5.945B TTM, based on a projection of the average growth since 2020. I compared Interactive Brokers to a number of competitors and examined trading multiples such as EV/Revenue, EV/EBITDA, and P/E ratio to determine a target share price for the company

Overview:

In 2023, Interactive Brokers saw total assets increase from $245.7B to $273.7B and total liabilities increase from $159.4B to $174.8B It is important to note that Interactive Brokers is heavily affected by larger economic conditions one of the largest ones being interest rates When interest rates are high, trading activity tends to lessen and vice versa. It is expected that the federal reserve will cut rates later this year due to stabilizing inflation. This may cause traders to be more active.

The firm is also actively working to expand its client base. On May 22, 2024, news broke that the firm was invited to join a derivatives trading market in Europe. The market in question is the Cboe European derivatives market which will give the firm much more exposure to clients. On the same day, it was announced that Interactive Brokers would partner with FusionIQ, a wealth management solutions platform used by advisors and institutions. Both of these events will expand the firm’s reach and may lead to more users.

Gregory Bucher | 23 May 2024

Historical Comparable Share Pricing (TTM)

Source: S&P Capital IQ

Risk Potential

Data Breach: In May of 2024, Interactive Brokers filed a notice of data breach with the attorney general of Massachusetts This data breach was caused by a third party achieving access to an employee’s email account. This allowed the third party to get access to sensitive customer information including social security numbers, financial account information, and driver's license numbers This has caused some consumers to lose trust in the firm. It could be worth investing in stronger encryption for employee emails which may mitigate the chances of this occurring in the future

Liquidity Risk: Interactive Brokers provides customers with the option to trade on margin. This entails loaning the customer currency with the expectation that it will be paid back. Trouble could arise if customers do not repay what they owe the firm. This could be heavily reliant on unemployment trends

Competition Pressures: Online trading brokerages have become increasingly popular in the past decade. This has led many platforms to reduce trading commission and option contract fees which makes the landscape more competitive Being that commissions are a huge part of Interactive Brokers’ revenue, this could negatively impact earnings. It is essential that the firm continuously lowers its commissions in comparison to competitors or it will start to lose customers. Another potential route to keep revenue intact is to incorporate advertisements on the app and website.

Sources: S&P Capital IQ | Yahoo Finance | Advisorhub | PR Newswire | JD Supra

Hospitality&RealEstate

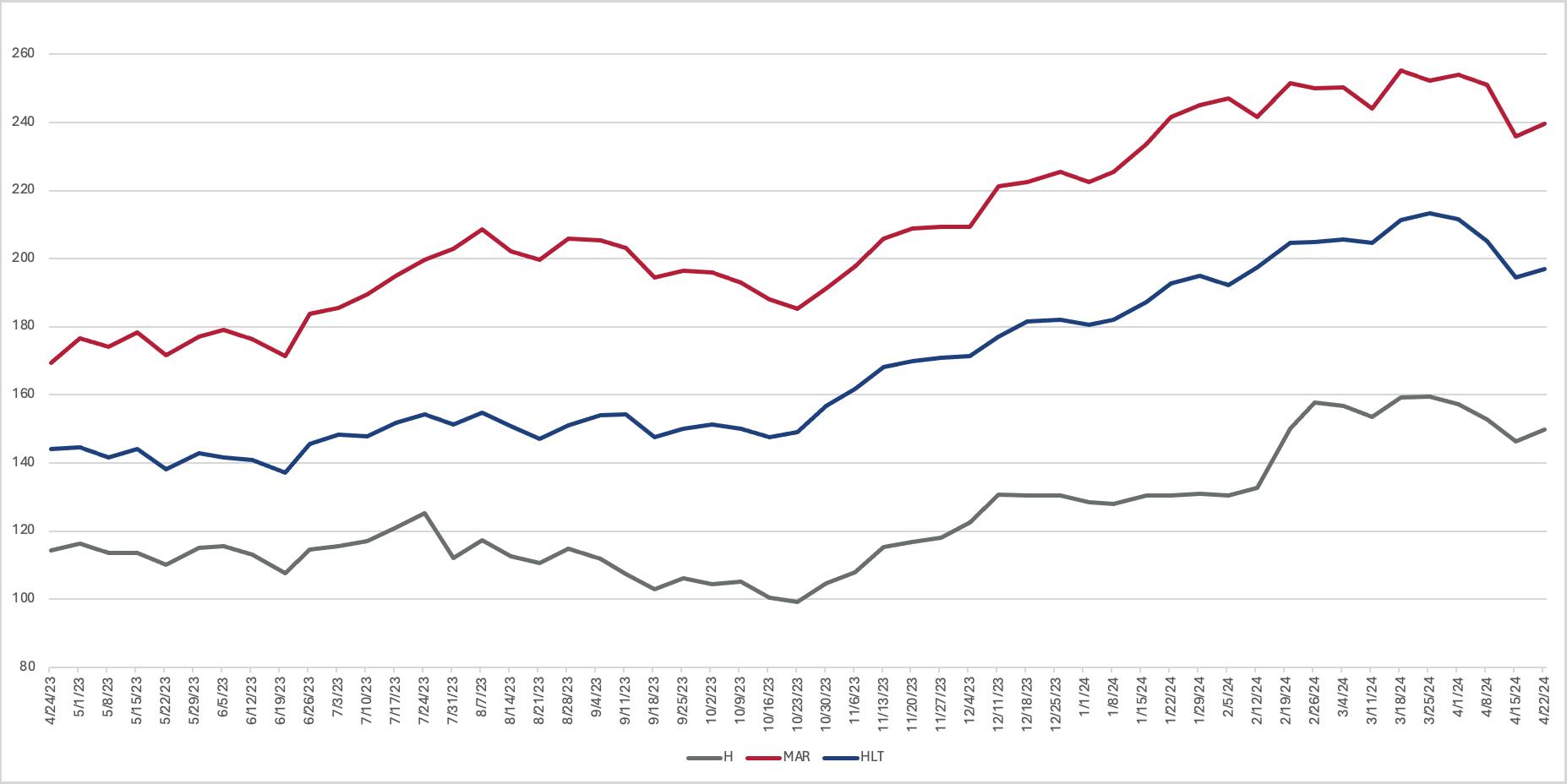

4Q2023Recap:BackandBetterthanEver

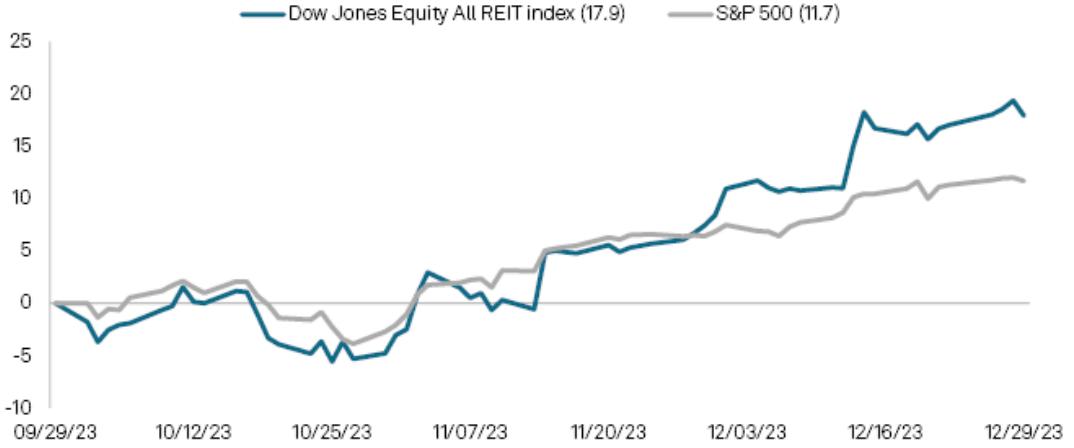

US real estate investment trust stocks outperformed the broad market in the fourth quarter of 2023, signalling success in the sector. Real estate stocks include residential, commercial, healthcare, and specialty properties. Additionally, they may include certaintrustsandmortgageREITs.Whilenottheentire sector, the Dow Jones Equity All REIT may be able to predictthesectorbroadly,astheyclosedthequarterwitha 17.9%totalreturn,outperformingtheS&P500whichwas up 11.7% for the quarter. The prior quarter lefttheDow JonesEquityAllREITIndexnegative8.4%.

The Dow Jones US Real Estate Regional Malls Index closed the fourth quarter of 2023 with the highest total return of 34.3%. This signals the success of malls and the return of retail post-pandemic Macerich Co. had a quarterly return of an outstanding 43.8% and Simon Property Group Inc. closed with a 33.9% return. While these equities performed well this quarter, it is likely more productive to look toward e-commerce stocks over brick-and-mortar stocks in terms of long-term investments. Commercial real estate lending remains tight. High interest rates have meant that capital for commercial real estate was costly and difficult to raise. As a result, developers switched toward private credit markets in the hope of boosting supply despite the rocky territory. Indeed, high interest rates likely curbed transaction activity. Transaction volume estimates show that transaction activity was down approximately 37% year-over-year.

While not as significant, the Dow Jones US Real Estate Apartments Index closed the fourth quarter with a return of 8.9%. The supply of single-family homes was on the rise with inflation subsiding and a strong economy This combination of factors makes it economical for developers to increase the construction of new properties Nonetheless, demand still outweighs supply in the market as supply is at a historic low

Q4 2023 total return for the Dow Jones Equity All REIT Index (%) (Source: S&P Global Market Intelligence)

Commercial Real Estate lending standards showed relief (Source: Bloomberg Finance)

Capitalization rates over investment-grade bonds narrowed and remained low at the end of the fourth quarter of 2023. Shopping centres and offices were the most attractive with the highest cap rates. Nonetheless, they have seen recent challenges with the shift to remote work and the rise of e-commerce. The Fed signalling a decrease in interest rates would mean that commercial real estate spreads would become more attractive as the cost of capital would decrease as a result.

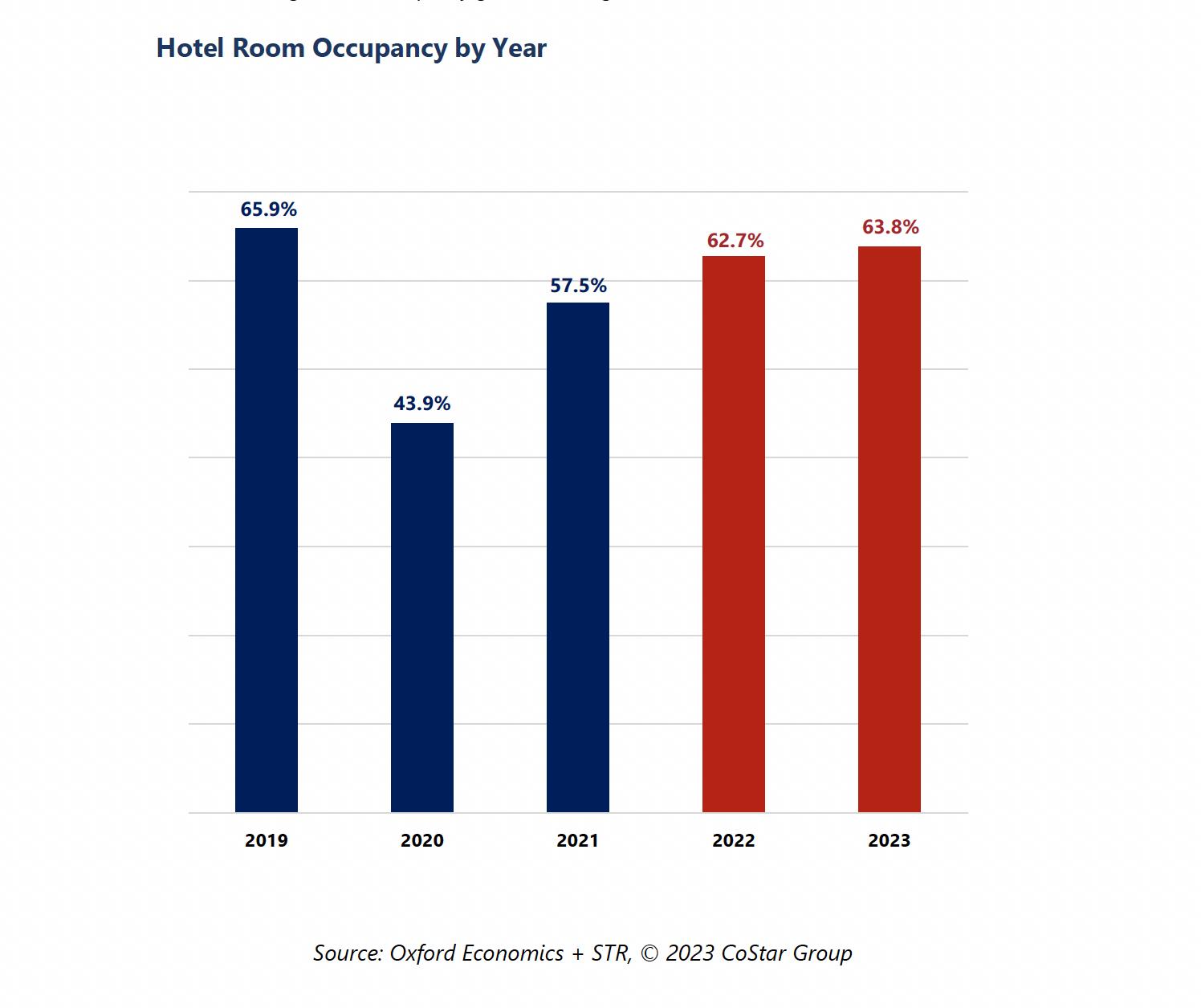

Hotel Room Occupancy by Year (Source: Oxford Economics + STR)

Hotel stocks rallied in 2023; up 40% when compared to numbers in 2022. The Baird/STR Hotel Stock Index, which includes 20 of the largest publicly traded real estate investment trusts and hotel brand companies on the US Stock exchange by market capitalization, was up 10.5% for Q4 of 2023 and 38.4% for 2023. The hotel industry has seen a steady recovery since its lowest point during the COVID-19 pandemic in 2020. Thus, it is said that the year 2023 has been referred to as “normalizing.” The returns are therefore somewhat relatively inflated given how low the lowest drop was in the sector. Revenue per available room, “RevPAR” increased 5% from the previous year and averaged 3.1%; the long-term quarterly average is 2.9%. While this is up from 2020 during the pandemic, when compared to numbers from 2019, RevPAR was still above the benchmark. While these numbers were up, quarterly occupancy rates fell 160 basis points.

This is likely a byproduct of decreased demand for corporate and leisure travel in the face of economic uncertainty and high inflation at the end of 2023.

As we enter into 2024, the housing market shifts. Indeed, mortgage rates remain high, forcing many out of the option to purchase a home. This coupled with staggeringly high home prices and low housing stocks means limited options for many. For the housing market to recover, a few factors must unfold. Indeed, mortgage rates would need to decrease The fall in rates can be a little slow, however If they descend too quickly, there may be an increase in demand that would diminish the inventory and once again increase the price of homes Mortgage rates returning to a normal rate, of about 4%-5%, rather than the current 7.17% would signal a healthier market.

Blackrock predicts that today’s volatile macroeconomic environment is the perfect opportunity for an investor to choose assets at ‘attractive prices.’ Real estate trends will likely shift as millennials grow families, increasing demand for affordable housing stock. With this comes the demand for retail in nearby neighborhoods and such accompanying service providers. Meanwhile, baby Boomers will boost demand for destination retail and hospitality. They will also be increasing the demand for medical offices. Investors should look toward these changes in the real estate market as an opportunity to take advantage of social shifts.

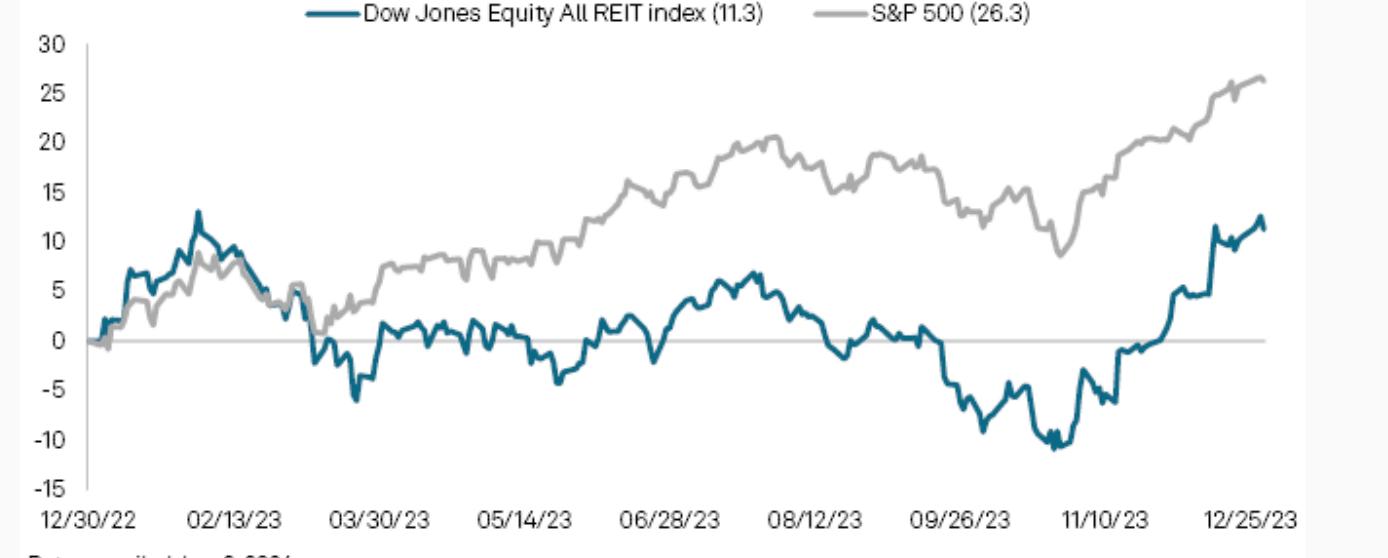

1-year total return for Dow Jones Equity All REIT Index (2023) (Source: S&P Global Market Intelligence)

Krish Patel | 30 April 2024

Rating: Buy

Current Price: $87.94

Price Target: $100

Company Updates

● Market Cap: $26.81B

● EV/EBITDA: 17.74

● Forward P/E: 21.41

● Return on Assets: 3.63%

● Quarterly Revenue Growth (YoY): 9.20%

● Dividend Yield: 1.72%

Competitor Statistics from Q1 2024

EV: $30.37B Revenue: $5.18B

EV: $7.34B Revenue: $4.33B

EV: $1B Revenue: $645M

CBRE (CBRE)

Fortune’s “Most Innovative” Commercial RE

Investment Thesis:

Despite facing numerous significant threats to its core business, CBRE has delivered an outstanding return of over +1000% since its listing on the NYSE in 2004. The company's ability to thrive in the commercial real estate sector despite challenging macroeconomic conditions such as the subprime mortgage crisis and the COVID-19 pandemic underscores its resilience.

My buy recommendation of CBRE stock is based on the company's position as the world's largest commercial real estate services provider, coupled with its diverse range of services, which will continue to support robust financial growth.

All-Encompassing Commercial RE Services:

CBRE leads the real estate services industry with six core offerings: customized consulting, client financial advisory, real estate asset management, and property design and construction. Notably, its property design and construction service boasts a 7:1 Value-to-Fee ratio globally. CBRE's extensive in-house capabilities allow it to capture more market share and effectively cross-sell services. For 2024, CBRE expects to achieve core earnings-per-share of $4.25 to $4.65, implying mid-teens percentage growth at the midpoint of the range up from 2023 EPS of $3.84, but still notably short of 2022 EPS of $5.69

Overview:

The financial metrics comparing Q4 2022 to Q4 2023 demonstrate several notable improvements Revenue increased from $8,194M to $8,950M, marking a 9.2% rise, while net revenue saw a 4.3% increase from $4,975M to $5,187M. Moreover, GAAP net income showed a significant surge, increasing from $81M to $477M, marking a staggering 487.9% rise Additionally, core EBITDA increased by 10.4% from $668M to $737M. These positive figures reflect the company's robust performance and its ability to generate strong revenue and profitability.

Krish Patel | 30 April 2024

CBRE Stock Performance vs Comps (Q3 2022 - April 30, 2024)

Source: Yahoo Finance

Risk Potential:

Office Space Downturn: The COVID-19 pandemic's shift to remote work has changed workforce operations, with large occupiers reducing office footprints by 20% to 30%, and some cutting by 50% or more (Collier Report, 2023). This has led property owners to sell assets at reduced prices. For CBRE, this presents both opportunities and threats. CBRE can offer financial solutions to help clients navigate these challenges, but macroeconomic factors pose risks of significant losses and potential loss of client trust.

Economic Uncertainty: In the volatile market, commercial real estate stakeholders are cautious, navigating price discovery. PwC reports lenders imposing stricter borrowing requirements, raising financing costs and challenging companies seeking capital. This has decreased competition for deals and pressured certain assets. Colliers' 2023 report predicts distress across all asset classes.

Consumer Behavior on Retail Real Estate: The average lease size of retail shops is expected to decline due to rising interest rates, disrupted supply chains, and the growth of online shopping. Retailers are optimizing space quality to maintain their bottom line. Business Insider reports over 2,100 store closures in the US for 2023. For example, Foot Locker plans to close around 400 mall stores in North America by 2026, aiming to introduce new play-focused outlets This trend highlights the 2024 shift from traditional stores to new-concept outlets

Sources: CBRE Webpage | Yahoo Finance | SEC gov | Capital IQ | Financial Times | LinkedIn - Nakisa Real Estate

Isabella Mourelle| April 10, 2024