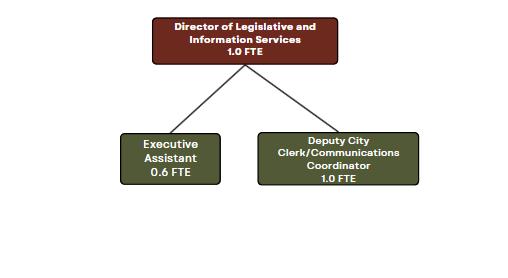

Jessica Matson, Legislative & Information Services Director/City Clerk

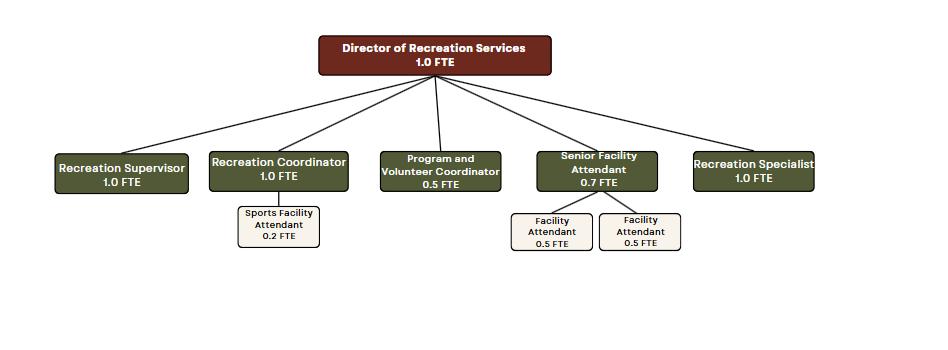

Sheridan Bohlken, Recreation Services Director

Other Key Staff Involved in the Budget Process:

Kevin Waddy, Information Technology Manager

Megan Schotborgh Accounting Manager

Shannon Sweeney, City Engineer

Theresa Wren, Capital Projects Manager

Dan Kies, Public Works Manager

Shane Taylor, Utilities Manager

Aleah Bergam, Management Analyst

Reader’s Guide

This is an overview of the structure of the FY2025-27 Biennial Budget, designed to help readers understand the annual budget process. To focus on what is achieved through spending, the budget includes funding levels and expected program outcomes, taking into consideration the current economic situation.

INTRODUCTION TO ARROYO GRANDE

A brief introduction to the City Council and Council-Manager form of government, the district map of Arroyo Grande, and details on services, structure, and organization chart The introduction also includes a community profile with history, geographic and regional context, and demographics

BUDGET SUMMARY

Overview of the City’s budget process, financial policies, funding sources, department budget updates, and the 10-year Capital Improvement Program (CIP).

• City Manager’s Budget Message

The City Manager’s address to the Mayor and City Council to highlight budget development priorities and any significant changes from the prior year adopted budget.

• Guide to the Budget

An overview of the budget process that explains budget purpose, the development of the base budget, and the final adoption and appropriation of the budget, budget basics, budget reporting, budget amendments, and fund structure.

• Financial Planning

An overview of key financial policies that govern the City’s approach to debt management, maintenance of fund balances, long-term financial planning, and other financial responsibilities.

• Budget Overview

A summary of all major and non-major funds.

• Department Budget Overview

An overview of each department’s purpose and structure, significant accomplishments, performance measures, department work plans, authorized personnel, including an organizational chart, and FY 2025-27 Biennial Budget.

• Debt Service Overview

An overview of the City’s debt management with outstanding debt service requirements and a debt payment schedule.

• Capital Improvement Program (CIP) Overview

An overview of the City’s 10-Year CIP plan, sources of funding, budgeted expenditures, project timelines, and project descriptions by program, project, and fund.

APPENDIX

Included in the appendix is a copy of the City Council adopted Budget and GANN Appropriation Resolutions, the GANN Appropriation Limits, a list of funds by number, and a glossary of terms.

GOVERNMENT FINANCE OFFICERS ASSOCIATION (GFOA)

DISTINGUISHED BUDGET PRESENTATION AWARD

The Government Finance Officers Association of the United States and Canada (GFOA) presented a Distinguished Budget Presentation Award to the City of Arroyo Grande, California for its Biennial Budget covering the period beginning July 1, 2023, and ending June 30, 2025

This award reflects the City’s commitment to meeting the highest standards in government budgeting. In order to receive this award, a governmental unit must publish a budget document that meets program criteria as a policy document, as an operations guide, as a financial plan, and as a communications device.

The City of Arroyo Grande is confident that the City’s Fiscal Year 202527 Biennial Budget continues to meet the GFOA’s rigorous criteria. Accordingly, this budget document will be submitted to the GFOA for review and consideration.

CALIFORNIA SOCIETY OF MUNICIPAL FINANCE OFFICERS (CSMFO) OPERATING BUDGET MERITORIOUS AWARD

The California Society of Municipal Finance Officers (CSMFO) presented an Operating Budget Meritorious Award to the City of Arroyo Grande, California for the City’s Fiscal Year 2023-25 Biennial Budget.

The City of Arroyo Grande is confident that the City’s Fiscal Year 2025-27 Biennial Budget will continue to conform to award requirements. Accordingly, this budget document will be sent to CSMFO.

INTRODUCTION TO ARROYO GRANDE

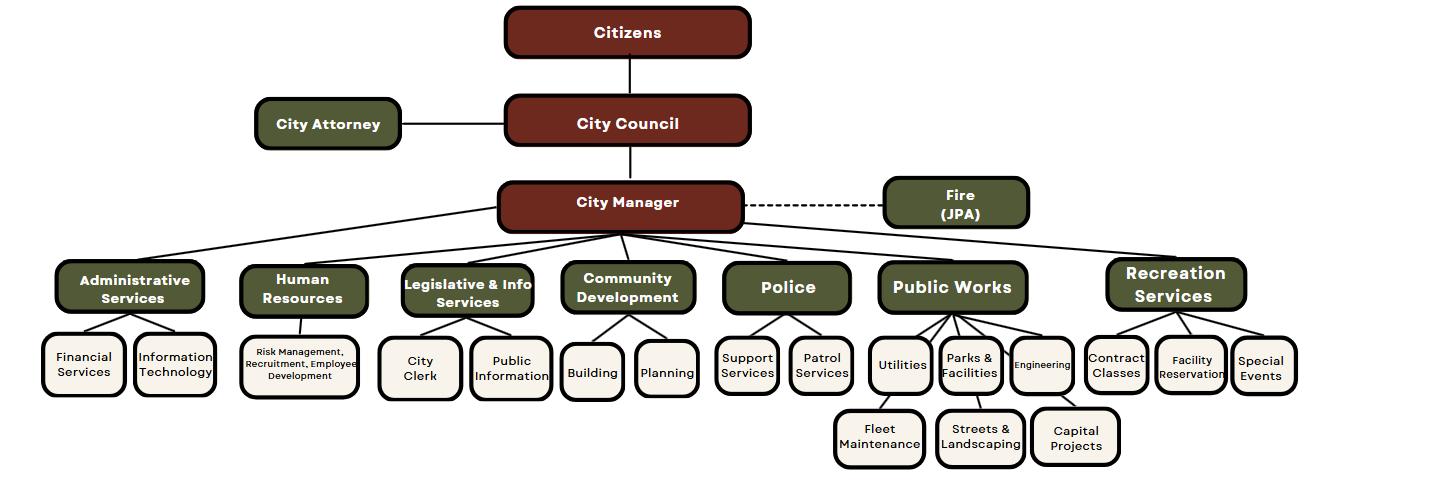

CITY STRUCTURE

City Structure

MAYOR AND CITY COUNCIL

GOVERNMENT STRUCTURE

The City of Arroyo Grande is a general law city and operates under the Council-Manager form of government, with a five-member City Council elected by district for four-year overlapping terms. The Council is elected on a non-partisan basis, and Council members must live in the district they represent. The mayor is elected at-large for a two-year term and is the presiding officer of the Council. The City Council is responsible for, among other things, passing ordinances, adopting the budget, appointing committees, and hiring the City Manager and City Attorney.

City Structure

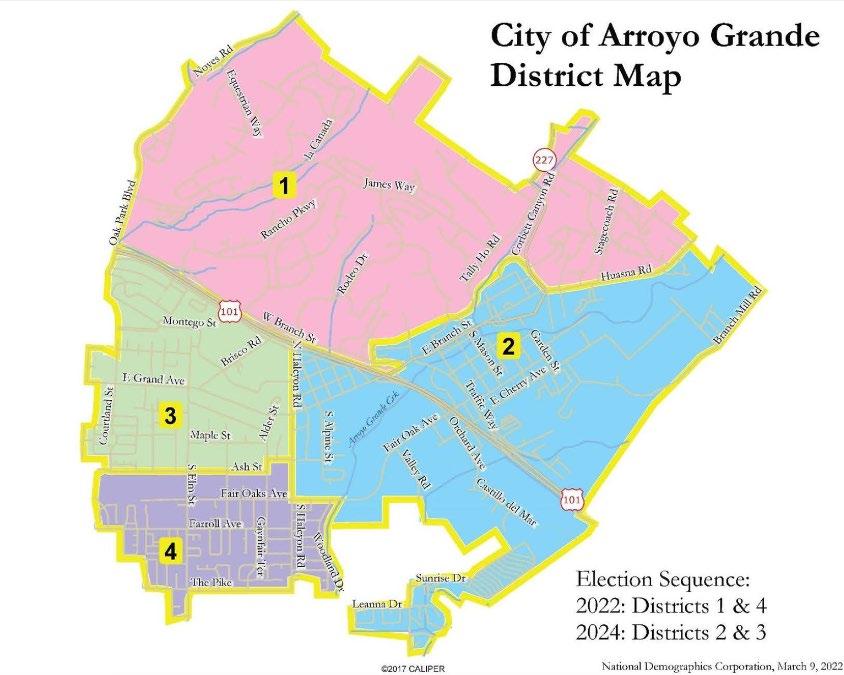

DISTRICT MAPS

CITY BOARDS AND COMMISSIONS

City Boards and Commissions are the underpinnings of the Arroyo Grande community – they are how the community navigates the daily and weekly decisions that make Arroyo Grande run smoothly to become the kind of community desired by City stakeholders. Boards and Commissions may forward matters to the City Council, as appropriate. Membership on City Boards and Commissions are voluntary positions. Members, with the exception of the Downtown Parking Advisory Board (DPAB) and Tourism Business Improvement District (TBID) Board must be registered voters of Arroyo Grande. Applicants for the DPAB shall have a business within the Arroyo Grande City Parking and Business Improvement Area. The TBID Board shall consist of five (5) members, with a preference that at least three (3) members shall be owners of lodging businesses within the Arroyo Grande TBID, or others with knowledge of tourism and/or the lodging industry. Members of each respective Commission/Board/Committee shall serve for a term ending the January 31st following the expiration of the term of the respective appointing Mayor or Council Member, as applicable.

City Structure

Members of each respective Commission/Committee/Board may be removed prior to expiration of their term by a majority vote of the Council. The following is a list of current City Boards and Commissions:

• Planning Commission

• Downtown Parking Advisory Board

• Architectural Review Committee

• Tourism Business Improvement District (TBID) Board

• Community Service Grant Program (CSGP) Committee

• Citizen Sales Tax Oversight Committee (CSTOC)

CITY DEPARTMENTS

The City Municipal Code (Chapter 2. Administration and Personnel) provides the basis for the departmental structure of the City and establishes that the City Manager be appointed by the City Council to manage the affairs of the City. The City’s Municipal code establishes the administrative organizational structure of the City under the control and direction of the City Manager. The City’s use of resources is budgeted in eight departments City Manager’s Office, Administrative Services, Legislative and Information Services, Community Development, Police, Public Works, Fire (JPA), and Recreation Services.

FULL - SERVICE CITY

The City of Arroyo Grande is considered a full-service city, meaning that all or most municipal services are provided by the City, as opposed to being contracted out to third-party providers. Some services commonly contracted out by municipalities include public safety and utility services; however, only fire services, sanitation treatment, and solid waste disposal are contracted out by the City of Arroyo Grande.

COMMUNITY PROFILE

Community Profile

OVERVIEW

The City of Arroyo Grande is a dynamic and historic community located along California’s Central Coast, approximately two miles inland from the Pacific Ocean in San Luis Obispo County. With a population of just over 18,000 residents, Arroyo Grande combines the charm of a small town with the amenities of a modern city. Known for its agricultural productivity, wine region designation, and strong community identity, the City continues to thrive as a regional hub for tourism, retail, and cultural activity.

The City’s mission is to be the best place possible for everyone who lives, works, and visits. It strives to achieve this mission by providing efficient and responsive government services

GEOGRAPHIC AND REGIONAL CONTEXT

Arroyo Grande is situated in a fertile valley carved by the Arroyo Grande Creek and is bordered by the cities of Pismo Beach and Grover Beach, along with the unincorporated community of Oceano. The City is part of the "Five Cities" area, a coastal cluster that also includes Shell Beach. This region enjoys a temperate climate, scenic coastal landscapes, and a collaborative regional economy centered on tourism, agriculture, and small business.

HISTORY AND INCORPORATION

Arroyo Grande was officially incorporated on July 10, 1911. However, its historical roots extend back much further, beginning with the Chumash people who originally inhabited the region. During the Mexican land grant era, the area became part of Rancho Arroyo Grande, later purchased and settled by Francis Ziba Branch and his family. The city developed as a hub for agriculture and commerce in the late 19th century, aided by the construction of a railroad depot in 1882. Today, Arroyo Grande honors its history through preservation of landmarks like the historic Swinging Bridge and the Santa Manuela Schoolhouse.

ECONOMIC CHARACTERISTICS

Arroyo Grande’s economy is supported by a diverse mix of sectors, including agriculture, retail, tourism, and professional services. The city's historic Village area serves as a focal point for community events, small businesses, restaurants, and artisan shops, attracting both residents and visitors. As part of the broader Five Cities area, Arroyo Grande benefits from strong regional visitation and a tourism-based economy that drives local revenue through transient occupancy and sales taxes.

Community Profile

COMMUNITY IDENTITY AND QUALITY OF LIFE

Arroyo Grande is recognized for its small-town feel, scenic beauty, and commitment to preserving its cultural and architectural legacy. Community character is reflected in historic features such as the Swinging Bridge, the Santa Manuela Schoolhouse, and preserved buildings in the Village. The city offers a high quality of life, with well-maintained parks, walking trails, and community services. Residents enjoy a safe, familyfriendly environment with access to excellent schools, healthcare, and recreational opportunities.

CITY RECREATION AREAS & PROGRAMS

The City provides several parks with picnic, barbecue, and playground areas. Strother Community Park, located along the bank of the Arroyo Grande Creek, is ideal for reunions, picnics, and barbecues. Elm Street Park has tennis, pickleball, and playground equipment for all ages. Heritage Square Park, connected to the Village area by the historic Swinging Bridge, is a favorite place for tourists and locals to enjoy lunchtime.

The Hart-Collett Memorial Park, the Terra De Oro Park, and the Kiwanis Park are small parks with picnic tables and benches only. Rancho Grande Park is also ideal for family gatherings or special celebrations.

The twenty-six-acre Soto Sports Complex serves the Five Cities region by providing four lighted tennis courts, baseball fields, four lighted softball fields, and two unlit ball fields. The fields are converted to soccer and football use in the fall.

Community Profile

The James Way Oak Habitat and Wildlife Preserve has equestrian and jogging/walking trails for public use. The habitat, winding along a hillside in an oak preserve, has an abundant array of wildlife.

The City offers a wide variety of recreational opportunities for local residents and visitors. From youth and adult sports leagues, and special events to classes for seniors and summer youth camps, there are programs available for nearly every age.

DEMOGRAPHICS

A city is defined by its assets, the most important being the people who live, work, and contribute within its boundaries. Arroyo Grande takes pride in its close-knit, community-oriented population, rich heritage, and strong sense of place. The City has thoughtfully managed growth while preserving its historic character and natural beauty, balancing its roots in farming and viticulture with a modern, vibrant lifestyle.

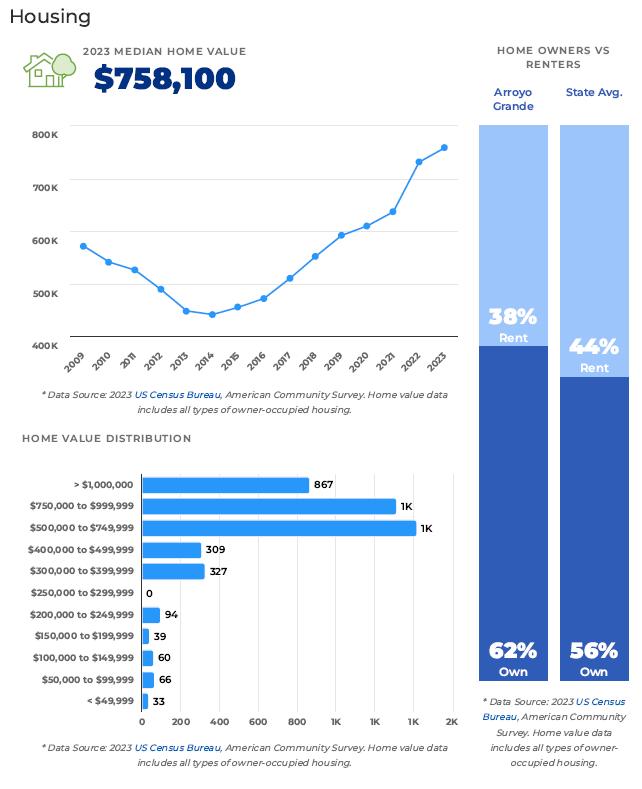

With a median single-family home sale price of approximately $758,100 as of 2023 1, Arroyo Grande attracts families seeking a high quality of life on California’s Central Coast. The city appeals to a diverse range of residents, from young families to retirees, drawn by the area’s scenic surroundings, historic charm, and a variety of housing options. The historic Village district offers a unique blend of local shops, dining, and cultural events that foster a strong community spirit.

Arroyo Grande’s economy is anchored in agriculture, tourism, small businesses, and retail, with a growing presence in viticulture recognized as part of the Arroyo Grande Valley American Viticultural Area (AVA). Employment opportunities span farming, hospitality, healthcare, professional services, and retail sectors. The City continues to support economic development efforts that enhance local job growth while maintaining its small-town character.

Education is a vital part of the community, with quality public and private schools serving students from kindergarten through high school. Additionally, residents have convenient access to nearby higher

1 Data Source: 2023 US Census Bureau, American Community Survey. Home value data includes all types of owneroccupied housing.

Community Profile

education institutions in San Luis Obispo County and along the Central Coast, providing a range of educational pathways for lifelong learning.

Arroyo Grande is a welcoming and vibrant community that honors its agricultural legacy while embracing sustainable growth, making it a desirable place to live, work, and visit on California’s beautiful Central Coast.

Community Profile

Community Profile

Community Profile

Community Profile

Arroyo Grande at a Glance

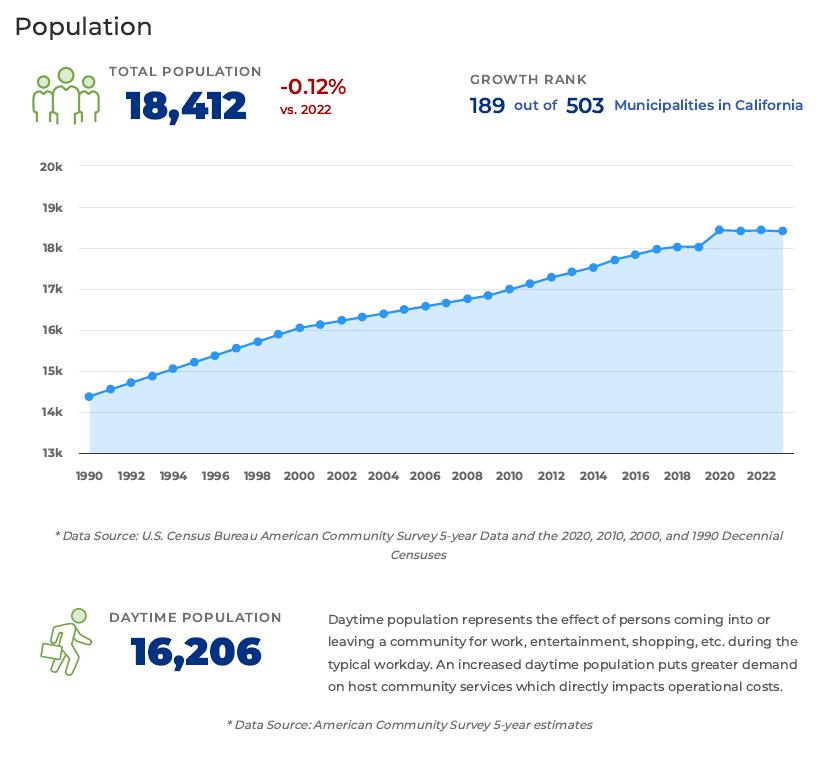

The City of Arroyo Grande was incorporated in 1911 and operates as a general-law city under the CouncilManager form of government. Nestled approximately two miles inland from the Pacific Ocean along California’s Central Coast, Arroyo Grande is part of San Luis Obispo County and the vibrant “Five Cities” region. The city is known for its rich agricultural heritage, scenic valley setting, and charming historic Village district. Arroyo Grande attracts visitors and residents alike with its mild climate, picturesque vineyards, local wineries, and a welcoming small-town atmosphere. As of January 1, 2023, the California Department of Finance estimates the City’s population at approximately 18,412 residents. While much of the city remains residential, there is ongoing development that balances growth with preservation of the community’s unique character and natural beauty.

At a Glance

Incorporation

1911

Government

Full-service, general-law city

County

San Luis Obispo County https://www.slocounty.ca.gov/

School Districts

Lucia Mar Unified School District http://www.luciamarschools.org

Location

Located on the Central Coast, approximately two miles inland from the Pacific Ocean in San Luis Obispo County, midway between Los Angeles and San Francisco

Climate

Moderate

Population 18,412

State legislature

17th Senate District

Democrat John Laird

30th Assembly District

Democrat Dawn Addis

U.S. Congress

Representative:

California's 24th Congressional District

Democrat Salud Carbajal

Organizational Chart

BUDGET SUMMARY

CITY MANAGER’S BUDGET MESSAGE

Budget Message

July 1, 2025

To the Residents of Arroyo Grande, Honorable Mayor, and Members of the City Council:

I am pleased to present the Fiscal Years (FY) 2025-27 Biennial Budget. This is the first two-year budget I have submitted as City Manager, and as was the case with budgets past, this budget reflects the unwavering commitment to strategic financial management, promoting financial stability, growing the economy, and enhancing the quality of life for all Arroyo Grande residents. The proposed budget is balanced, incorporates all City funds, funds major efforts toward implementing the City Council’s goals, includes important initiatives to upgrade the City’s infrastructure, continues to fund the high-quality services that the community has come to expect, and will invest in the future through capital improvements and maintenance activities.

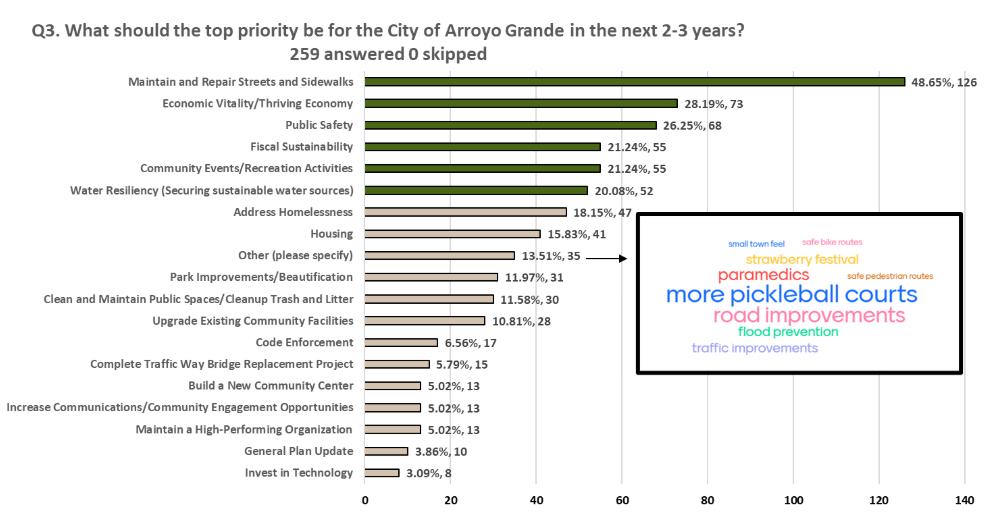

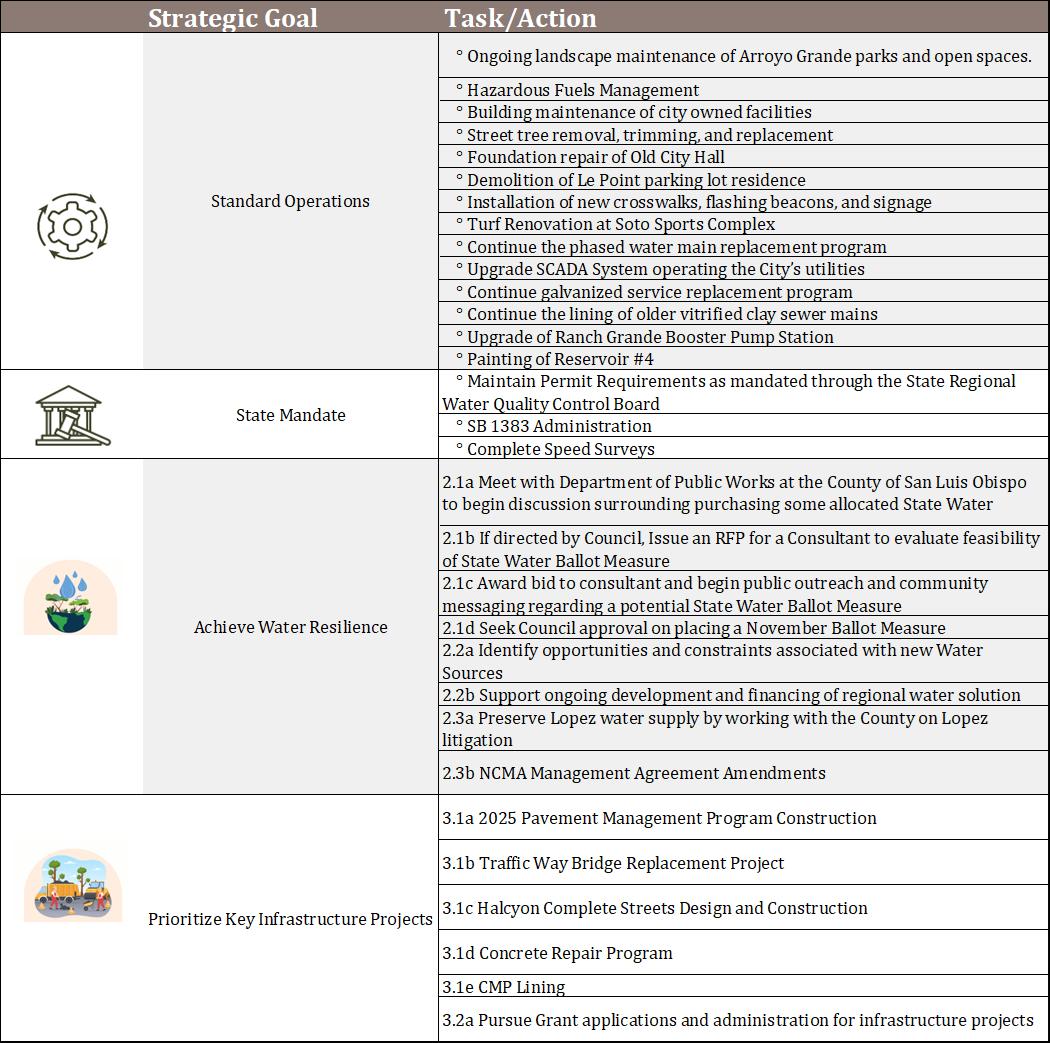

Process for Creating City Goals

In preparation for this two-year budget, the City Council actively involved the community in shaping our direction through the Community Priorities Survey. This four-question survey was posted on the City website and promoted on social media channels. The survey enabled community members to provide input regarding their thoughts on the top priorities for the City over the next 2-3 years. A summary of the responses was reviewed by the Council before establishing five (5) major Council goals for staff to prioritize for the upcoming biennial budget. This set of priorities has been used by staff to create work plans for the proposed biennial budget. The Council Goals have been used as a foundation for recommending where to allocate scarce City resources.

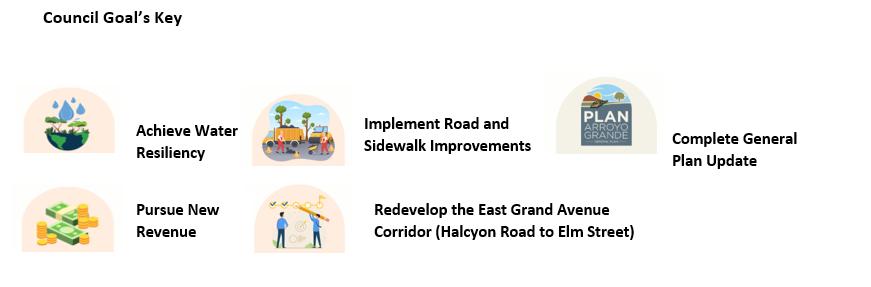

The five major goals are:

• Complete the General Plan Update

• Redevelop the East Grand Avenue Corridor (Halcyon Road to Elm Street)

• Pursue New Revenue Sources

• Implement Road and Sidewalk Improvements

• Achieve Water Resilience

How FY 2025-27 City Goals Compare to the FY 2023-25 Council Goals

The FY 2025-26 & FY 2026-27 Council Goals build upon the success of the FY 2023-24 & FY 2024-25 Council goals from the last two-year budget. Similar to the last two-year budget, the Council continues to focus on providing resources toward funding, infrastructure, and the general plan update. A major factor in helping address the funding goal was the passage of Measure E-24, a local 1% sales tax approved by the City's voters in November 2024. Measure E-24’s intent is to fund city services, such as fixing potholes, maintaining city streets, sidewalks, parks, aging infrastructure, and community facilities; providing local fire protection, police, and 9-1-1 emergency services; cleaning up litter/graffiti, and addressing homelessness. This goal will continue into the FY 2025-27 biennial budget with the consideration of cannabis as a means for economic development and consideration of modifications to Transient Occupancy Tax (TOT). The former fire services goal was achieved as of January 1, 2025, with the updated Joint Powers Authority Agreement with Grover Beach and the contract with the County of San Luis Obispo to provide fire service to the community of Oceano. The infrastructure goal will continue from the last two-year budget, with the addition of specific projects identified: Redevelop the East Grant Avenue Corridor and Implement Road and Sidewalk Improvements. A new goal was added for FY 2025-27: Achieve Water Resilience. This new goal supports regional efforts to address the ongoing Lopez Litigation and by pursuing a ballot measure in November 2026, to potentially allow the City to purchase State Water outside of declared water emergencies

Budget Message

How the City Plans to Accomplish

the FY 2025-27

City Goals

The Adopted Budget strategically allocates resources to projects that align with our five Council Goals. Each initiative reflects a deep understanding of community needs, is strengthened by collaborative partnerships, and is made possible by the City’s strong financial position. These efforts are focused on preserving and enhancing the quality of life for both current residents and future generations. Looking ahead, the future is bright for Arroyo Grande its residents and visitors alike thanks to strategic investments that will deliver lasting, positive impacts.

Financial Overview

The overall financial goals for the FY 2025-27 budget period is to have a fiscally sound two-year budget, enhance current service levels, and address critical capital projects. The FY 2025-27 Adopted Budgets present a structurally balanced budget, with excess operating revenues sufficient to cover Adopted Operating Budget expenditures.

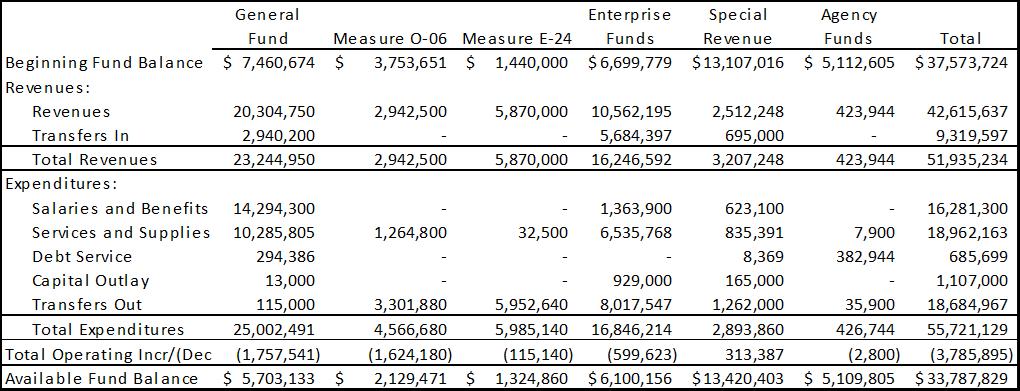

The FY 2025-26 proposed budget includes a total of $32.1 million in revenues and $35.6 million in operating and capital budget for a net of $3.5 million more expenditures than revenues. The operating budget is balanced, with a $2 million net operating surplus. The expenditures that exceed revenues are for one-time projects that the City has been anticipating. Fund balances accumulated over time offset the additional expenditures and exceed the City’s policy goal of 20% by 5.8%.

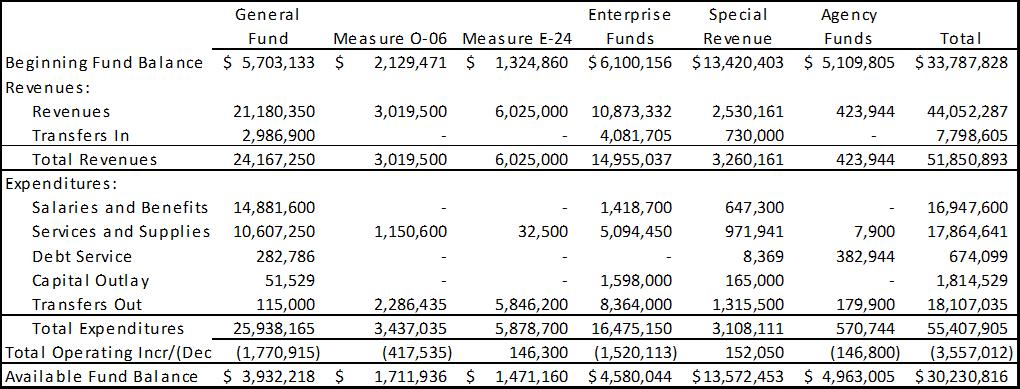

The FY 2026-27 proposed budget includes a total of $33.2 million in revenues and $35.3 million in operating and capital expenditures for a net of $2.1 million more expenditures than revenues. The operating budget is balanced, with a $64,534 net operating surplus. Fund balances accumulated over time offset the additional expenditures and are still at the City’s policy goal of 20%.

Historically, the City has adopted a rolling 5-Year Capital Improvement Program (CIP) that identifies, prioritizes, and budgets for capital infrastructure needs such as roads, water and sewer systems, parks, and facilities. While this approach has served the organization well, growing infrastructure demands and increasingly complex funding environments have highlighted the need for a longer planning horizon. This report has transitioned the CIP from a 5-Year CIP framework to a 10-Year planning horizon, a change intended to improve long-range financial planning, infrastructure forecasting, and alignment with strategic goals.

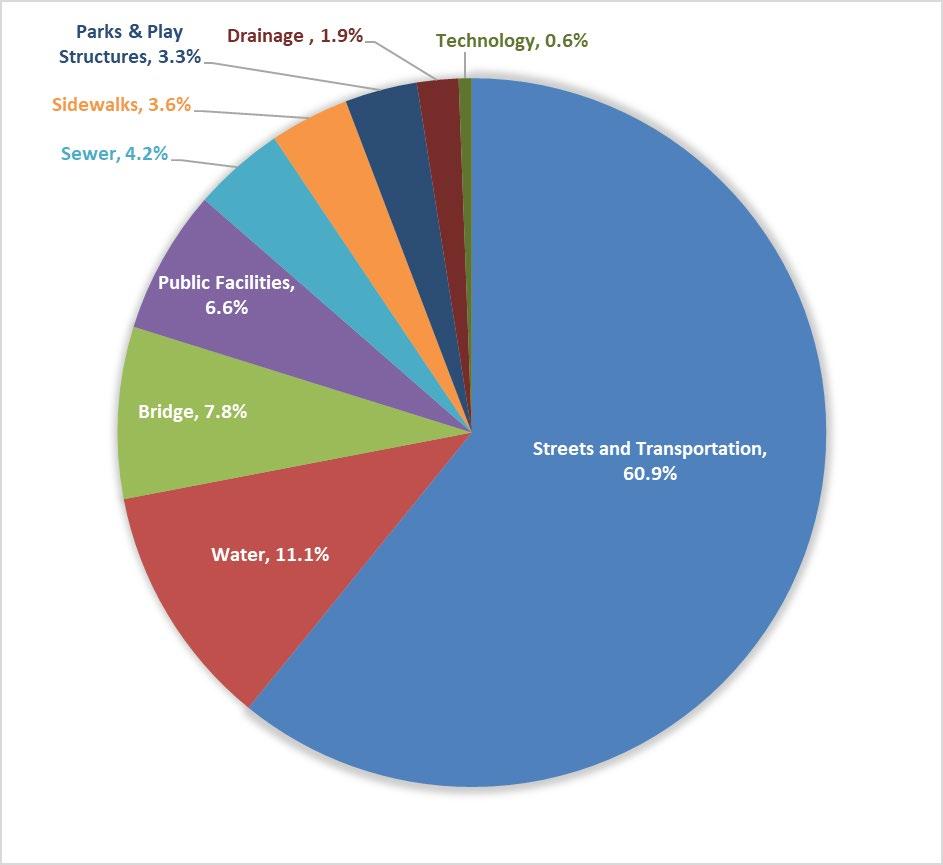

This Capital Improvement Program (CIP) outlines anticipated City infrastructure improvements for FY 202526 through FY 2034-35 and serves as a public information document to advise residents and property owners on how the City plans to address significant capital needs. The CIP is divided into nine categories – Bridges, Drainage, Parks & Play Structures, Public Facilities, Sewer, Sidewalks, Streets and Transportation, Technology, and Water. It contains information about the scope, location, and funding for these projects.

Each year, the overall goal for capital improvements and the means for accomplishing them are assessed. Every project in the plan has been considered for its financial feasibility, environmental impact, conformance with previously adopted plans, priorities established by the City Council, and ability to meet public needs.

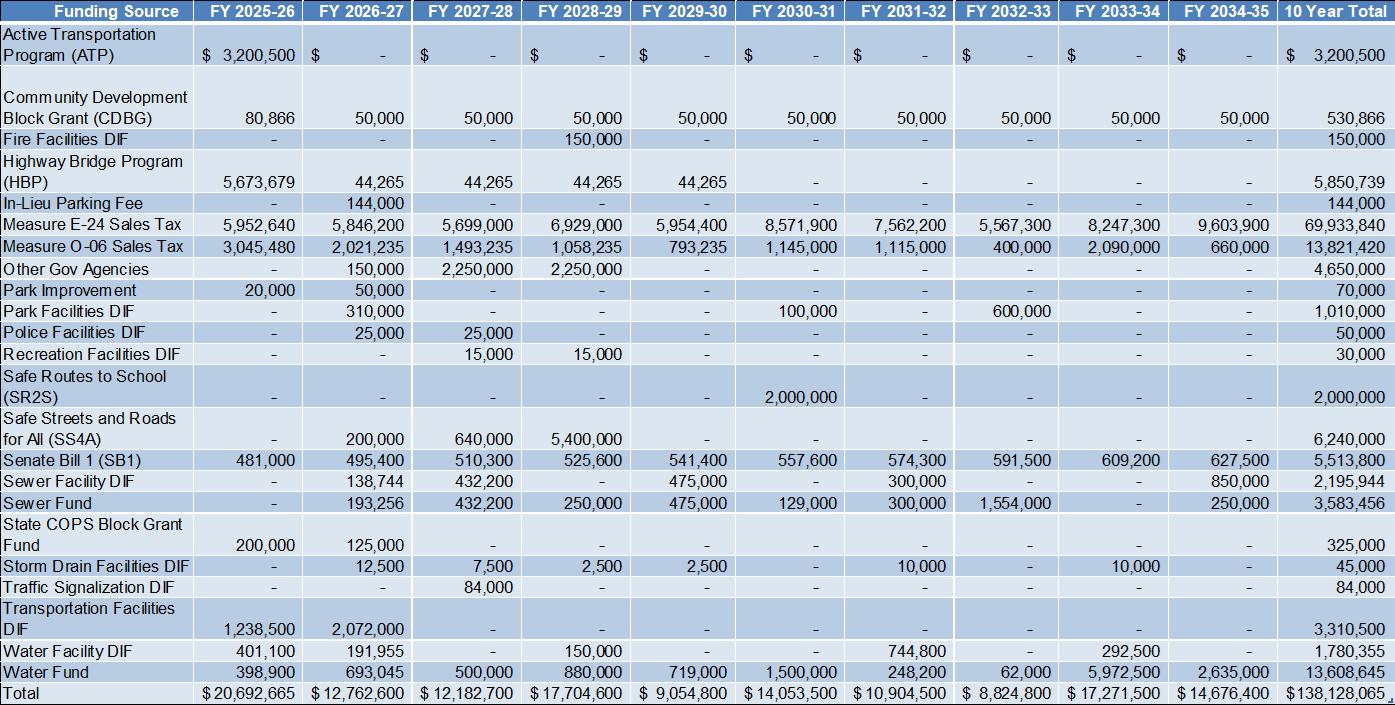

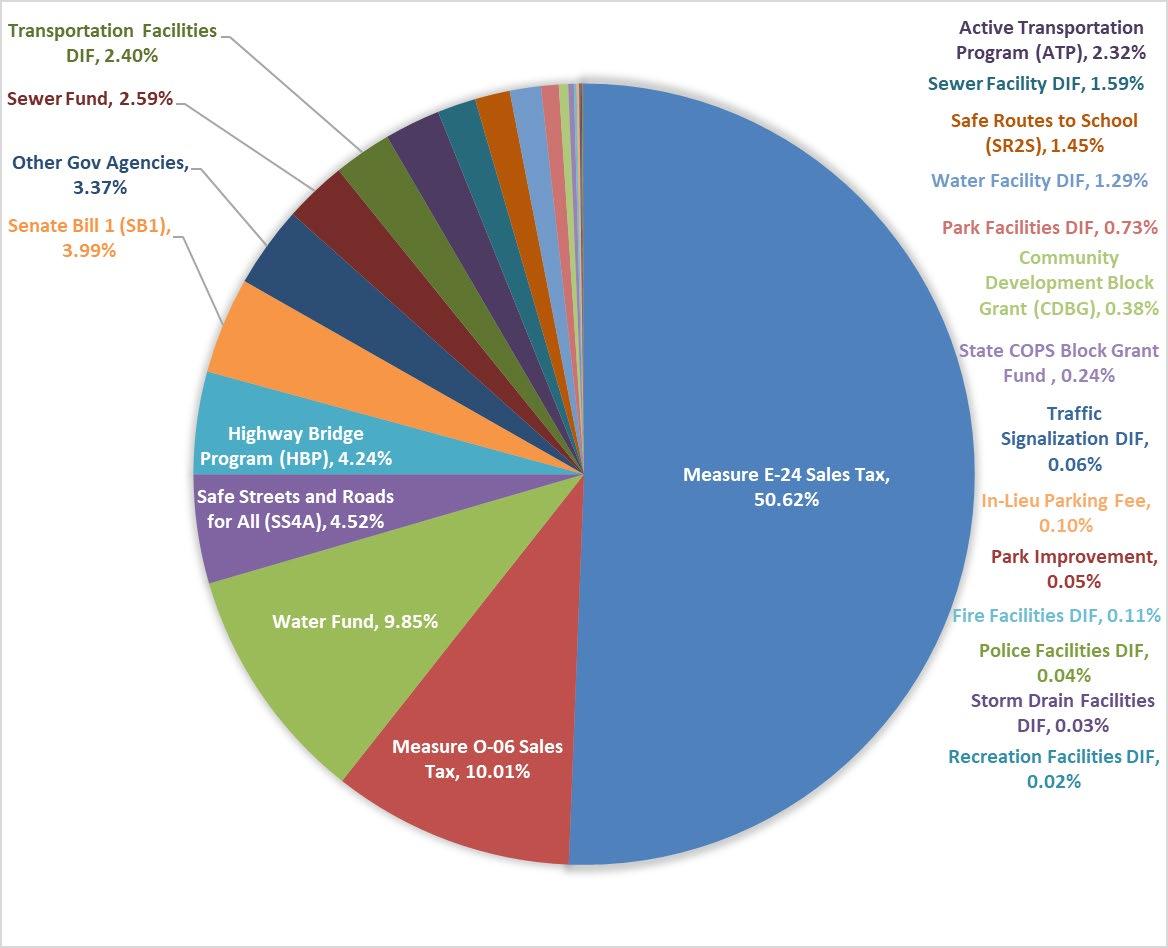

The FY 2025-26 through FY 2034-35 CIP totals $138,128,065. It is a flexible plan that can be altered as conditions, funding, priorities, and regulations change.

Budget Message

Acknowledgements

I would like to express my sincere appreciation to the dedicated teams across all City departments from leadership to frontline staff for their collaborative efforts in developing the FY 2025-27 Biennial Budget. Their ongoing commitment to interdepartmental collaboration, community well-being, and the City’s fiscal stability has been instrumental throughout this process. This document is a true reflection of a united and dedicated team effort.

A special thank you goes to the Administrative Services Department for their outstanding support, including training, financial analysis, expert guidance, and steadfast adherence to critical deadlines.

Finally, I am deeply grateful to the City Council The overall objective is to meet the community’s needs and provide services in the most effective, efficient, and responsive manner. With the City Council’s strong leadership, strategic direction, and clear vision, we have accomplished that objective

Closing

Our commitment to making this the best place possible for everyone who lives, works, and visits Arroyo Grande is reflected in the strategic investments we are making today, investments that support a sustainable and vibrant future. Through sound financial stewardship and thoughtful community-focused initiatives, we continue to enhance the experiences of both residents and visitors. The City of Arroyo Grande is wellpositioned for continued success. I am especially encouraged by the spirit of collaboration shared by our community members, partner agencies, volunteers, business owners, nonprofit leaders, and elected officials. Together, we are creating a community where everyone can thrive. It is truly a privilege to work alongside such dedicated and inspiring individuals.

Sincerely,

MATTHEW J. DOWNING – CITY MANAGER

GUIDE TO THE BUDGET

Guide to the Budget

PURPOSE OF THE BUDGET

The City budget sets forth a strategic resource allocation plan that addresses the City Council’s Strategic Goals. The Budget is a policy document, financial plan, operations guide, and communication device all in one. Through the budget document, the City demonstrates its accountability to its residents, customers, and the community-at-large.

The City’s Budget accomplishes the following:

• Determines the quality and quantity of City programs and services;

• Details expenditure requirements and the estimated revenue available to meet these requirements;

• Connects the activities of individual City Departments to the City Council’s Strategic Goals;

• Sets targets and provides a means of measuring actual accomplishments against goals; and

• Serves as a communication device that promotes the City’s vision and direction, fiscal health and vitality, and what the public is getting for its tax dollars.

Additionally, the budget provides the legal authority for expenditures and a means for control of municipal operations throughout the fiscal year. Accordingly, the City Charter mandates that a budget be adopted prior to the beginning of the fiscal year.

The budget process furnishes departments with an opportunity to justify departmental work programs, to propose changes in services, and to recommend revisions in organizational structure and work methods. It also enables the City Manager to review these aspects and make appropriate recommendations to the City Council.

Presentation of the budget to the City Council provides an opportunity to explain municipal programs and organizational structures. It also allows the Council to judge the adequacy of the proposed operating programs, to determine basic organizational and personnel staffing patterns, and to establish the level of municipal services to be provided with the available resources. In order to accomplish these objectives, the budget must combine an explanation of anticipated financial resources for the ensuing fiscal year with proposed expenditures, supported by sufficient information on the proposed programs and activities to assess the appropriateness of the recommended levels of services.

THE OPERATING BUDGET, CAPITAL BUDGET, AND CAPITAL IMPROVEMENT PROGRAM

The budget document contains information about both the City’s operating and capital budgets. The operating budget details the funding for the day-to-day operations and obligations of the City for a specific fiscal year such as personnel costs, vendors and contractors, utilities, building maintenance, and debt payments. The capital budget details planned expenditures for the same fiscal year to construct, maintain, or improve City facilities such as fire and police stations, libraries and museums, parks, recreation centers, streets, sewers, and electric and water infrastructure.

Guide to the Budget

The Capital Improvement Program (CIP) is a separate ten-year planning document that details planned capital expenditures. Capital projects range from road maintenance or construction to the renovation of municipal buildings, recreation centers and play structures, and water main and sewer system replacement. The CIP relates capital project needs to the financial sources that will support their realization and the timeframe in which both the financing and work will take place. Often spanning multiple years, capital improvement projects typically carry considerable future impact. Because of the more long-term nature of the CIP and the complex nature of capital project financing, the CIP is presented in a separate document. However, the first two years of the CIP are integrally related to the Biennial Budget document, and therefore a summary of the CIP is provided in the Capital Improvement Program Overview section of this budget, beginning on page 167

BUDGET PROCESS

The City of Arroyo Grande’s fiscal year begins July 1 and concludes on June 30. In accordance with fundamental democratic principles, the City embraces the notion and practice of citizen participation, especially in key planning and resource allocation activities. Therefore, the development of the budget process begins early in the prior fiscal year to ensure adequate planning and community input into that planning. Engagement with City leadership, commissions and the community occur throughout the process.

At the beginning of budget development, the City initiated community engagement with online surveys to gather input from residents and business owners. A Community Priorities Survey assessed residents' satisfaction and priorities. This feedback informed resource allocation decisions for the upcoming budget.

Guide to the Budget

DEVELOPMENT OF THE BUDGET PROCESS

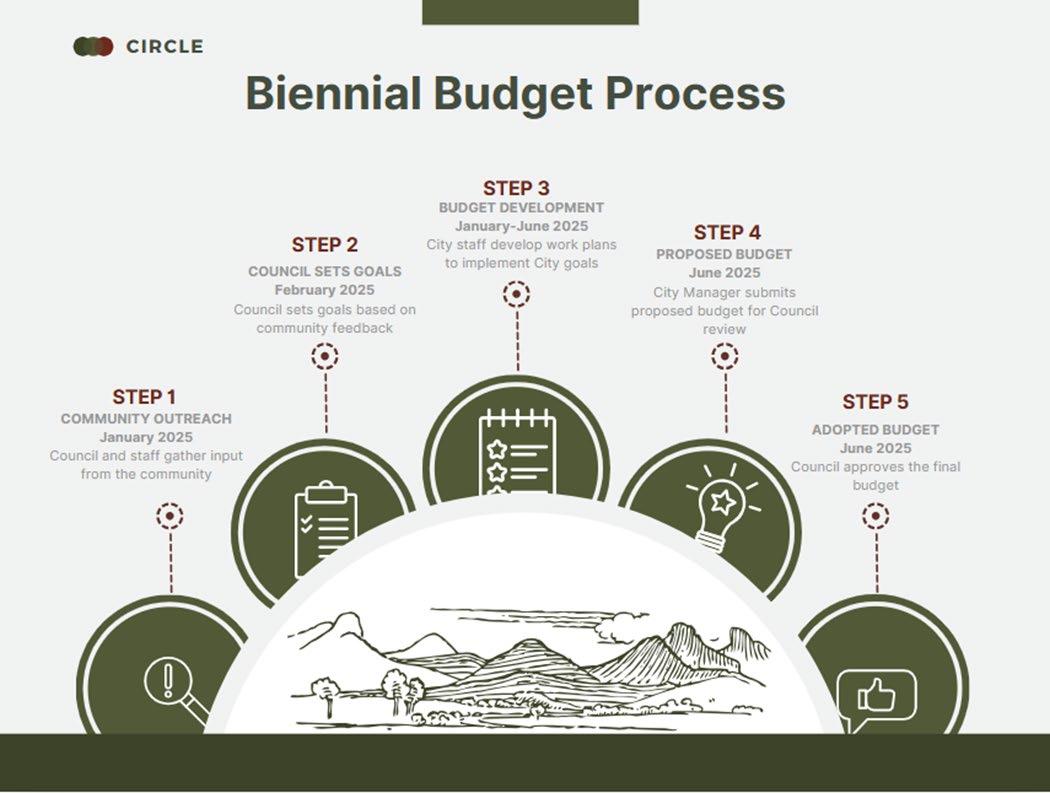

Every two years, staff and Council prepare a Biennial Budget document, which commits government resources and services to accomplish the City’s mission of making Arroyo Grande the best place possible for everyone who lives, works, and visits here. To develop the biennial budget for Fiscal Years 2025-27. The 5-step process and timeline tat was used for this budget cycle is depicted below

Step 1: On December 9, 2024, an Arroyo Grande Community Priorities Survey was published. This 4question online survey was posted on the City website and promoted on social media channels. The survey was open for one month and closed on January 15, 2025. The survey allowed community members to provide input regarding their thoughts on what the top priorities should be for the City over the next 2-3 years. The survey included a combination of multiple-choice and short-response questions. A summary of the responses is included in Attachment 2 of Item 4: City Council Goal Setting Workshop, at the February 10, 2025, Special Council Meeting.

Guide to the Budget

Step 2: At the February 10, 2025, Special Council Meeting, Council established 5 major goals for staff to prioritize for the upcoming biennial budget cycle. The goals were determined based on the results of the community survey and input from the public and staff. This set of priorities will be used by staff to create work plans and a proposed biennial budget.

Step 3: Following completion of the study session, staff developed a proposed budget by implementing the following steps:

• January 28, 2025 - Financial Forecast

o Staff presented a 5-year financial forecast with budget assumptions, challenges, goals, and strategies. January 28, 2025, Council Meeting – 11.a Five-Year Financial Forecast

• Spring 2025 - Staff Develop Work Plans

o The budget process begins in the Finance Department, with the preparation of baseline revenue and expenditure assumptions. Baseline expenditures include personnel assumptions, with a comprehensive assessment of the impact of current or anticipated employee Memorandums of Understanding (MOU) which govern employee costs such as benefits and cost of living adjustments. Other known costs, such as debt obligations and self-insurance funding requirements are also projected, to arrive at a baseline budget.

o City departments attend a budget kickoff meeting where they receive the budget development calendar, a summary of the baseline budget, and direction on balancing measures, if applicable. The baseline budget represents the amount of funding available to maintain programs and current service levels and make progress towards achieving the City’s major goals. Departments define budgetary needs in relation to services, programs, and related strategic goals. Departments also identify capital projects and funding sources for those projects during this time. Internal review of department budget submissions takes place, with executive leadership recommending adjustments and providing guidance on the budget submissions of each City department.

o Staff will finalize operating and Capital Improvement Plan (CIP) preliminary budgets that reflect the established major City goals and the financial forecast.

• May 13, 2025 - Review of CIP

o Staff presented a 10-Year CIP for review and input from the City Council and by the Planning Commission for determination of consistency with the General Plan. May 13, 2025 Council Meeting – 11.c Ten Year Capital Improvement Program, Measure E-24 Local Sales Tax Fund Expenditure Program, and Measure O-06 Local Sales Tax Fund Expenditure Program

Step 4: The proposed operating budgets, work plans, and CIP were incorporated into a proposed FY 202527 Biennial Budget for discussion and consideration by the Council on May 27, 2025. May 27, 2025 Council Meeting – 11.a Review Preliminary FY 2025-27 Biennial Operating Budget

Step 5: Adoption of the FY 2025-27 Biennial Budget occurred on June 10, 2025, with funds appropriated on July 1, 2025. June 10, 2025 – Council Meeting 10.a Fiscal Year 2025-27 Biennial Budget

Guide to the Budget

MID - CYCLE BUDGET UPDATE/QUARTERLY REPORTS

The City Manager presents a Mid-Cycle Budget Update in June of the second year of a biennial budget cycle. This update includes necessary adjustments to the operating budget and personnel detail that have been identified by staff since the adoption of the Biennial Budget. For all budgets adopted, whether annual or biennial, quarterly fiscal updates are presented to the City Council to keep City leadership and the public apprised of the City’s financial condition throughout the budget period. The quarterly updates include recommended budget adjustments and fiscal strategies as needed to respond to the current fiscal state of the City.

ADJUSTMENTS TO THE ADOPTED BUDGET

The City Council may amend or supplement the adopted budget with the majority vote of at least three members to authorize the transfer of unused balances appropriated to one department or fund to another department or fund or to appropriate available funds not included in the budget. The City Manager is legally authorized to transfer budgeted amounts between divisions and accounts within the same department and fund over the course of a fiscal year. Through City Council adoption of the budget resolution (page 205), the Director of Administrative Services/City Treasurer may authorize interfund transfers as required provided funds are available, or as authorized by the City Council through the adoption of the budget. City Council approval is required for all transfers from unappropriated fund balances or fund balance contingency reserves.

BASIS OF BUDGETING

The modified accrual basis of accounting is used by all General, Special Revenue, Debt Service, and Capital Projects Funds. This means that revenues are recognized when they become both measurable and available. Measurable means the amount of the transaction can be determined, and available means collectible within the current period or soon enough thereafter to be used to pay liabilities of the current period. Expenditures are recorded when liabilities are incurred, except that principal and interest payments on long-term debt are recognized as expenditures when due. The full accrual basis of accounting is utilized by all Enterprise and Internal Service Funds. This means that revenues are recorded when earned and that expenses are recorded at the time liabilities are incurred.

The City’s basis for budgeting is consistent with accounting principles generally accepted in the United States of America and with the City’s financial statements as presented in the Annual Comprehensive Financial Report (ACFR). Exceptions are as follows:

• Capital expenditures within the Enterprise Funds are recorded as assets on an accounting basis but are shown as expenditures on a budgetary basis.

• Depreciation of capital assets and amortization of various deferred charges are recorded on an accounting basis only. These charges are not reflected in the budget document.

Guide to the Budget

• Continued/Carryover appropriations represent previously budgeted funds unexpended at the end of the applicable budget period. Carryover requests approved by the City Council are added to the City’s current budget period but are not included in the budget document or original budget submission to the City Council.

• Certain funding, such as grant funding, is not included in the budget document; these items are appropriated as needed throughout the fiscal year with approval from the City Council.

Fund Structure

BUDGETARY FUND BALANCE

In a governmental agency, fund balance is considered in two separate, but intrinsically related, settings: budgetary fund balance and Annual Comprehensive Financial Report (ACFR) fund balance. Budgetary fund balance is a prospective calculation of ending fund balance based on estimated revenues and expenditures, whereas ACFR fund balance is a retrospective calculation based on the difference between fiscal year end assets and liabilities, and deferred inflows or outflows of resources. Following the financial audit of the active fiscal year, budgetary ending fund balance is reconciled to ACFR fund balance, accounting for actual fiscal year performance and any differences in the budgetary versus accounting basis of reporting.

ACFR fund balance may be classified in one of five classifications defined in GASB Statement 54: Fund Balance Reporting and Governmental Fund Type Definitions as described below:

• Non-spendable Fund Balance: Cannot be spent due to form or must be maintained intact legally or contractually.

• Restricted Fund Balance: Subject to externally enforceable limitations by law, enabling legislation, or limitations imposed by creditors or grantors.

• Committed Fund Balance: May only be used for specific purposes due to formal action of the City Council through adoption of a resolution prior to the end of the fiscal year.

• Assigned Fund Balance: Reflects the City’s intended use of resources.

• Unassigned Fund Balance: The residual classification that includes all spendable amounts not contained in the other classifications.

For the purposes of budgetary fund balance, the last three classifications listed above (Committed, Assigned, and Unassigned) are generally not legally restricted by external parties or forces.

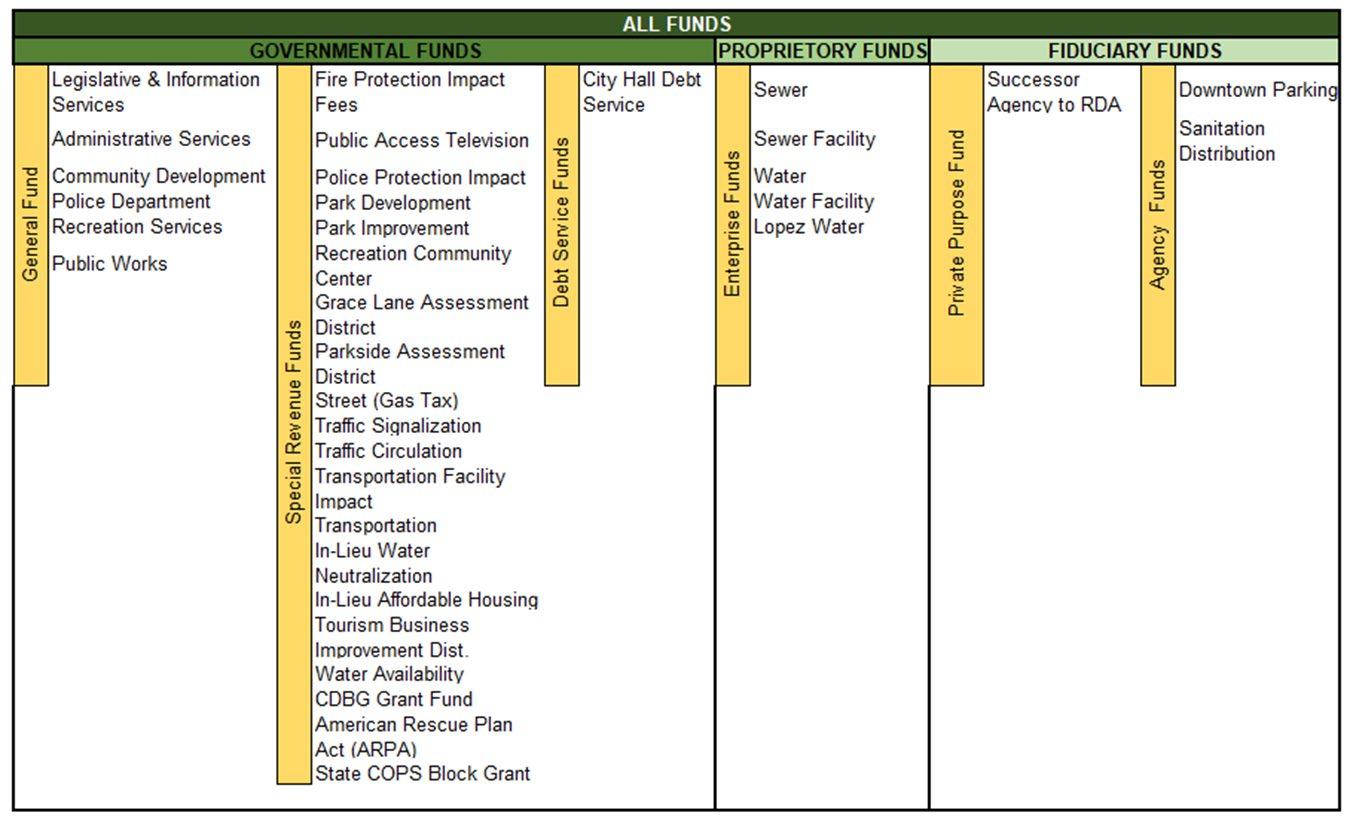

FUND STRUCTURE

The City records financial activity in six fund types as guided by generally accepted accounting principles (GAAP): General Fund, Special Revenue Funds, Debt Service Funds, Enterprise Funds, Private Purpose Funds, and Agency (Fiduciary) Funds. Within each fund type are multiple funds that relate to a city department or multiple city departments.

General Fund

The General Fund is the government’s primary operating fund. It accounts for all financial resources of the general government, except those required to be accounted for in another fund. The General Fund is generally used to account for functions of the City that are principally supported by taxes and intergovernmental revenues. The General Fund budget provides the majority of services commonly associated with local city government (e.g. public safety, recreation, community development, general government, and public works).

Measure O-06 Sales Tax Fund

The Measure O-06 Fund is a component of the General Fund and is used to separately account for and report the use of Measure O-06 revenue derived from a local 1/2% sales tax approved by the City's voters in November 2006.

Fund Structure

Measure E-24 Sales Tax Fund

The Measure E-24 Fund is a component of the General Fund and is used to separately account for and report the use of Measure E-24 revenue derived from a local 1% sales tax approved by the City's voters in November 2024.

Special Revenue Fund

Special Revenue Funds are used to account for specific monies that are legally restricted for use for a particular purpose. Miscellaneous grants and other restricted funding are recorded as Grants of within a Restricted Programs fund. Grants are budgeted by individual Council action, whereas restricted funding, if recurring, guaranteed, and predictable, is budgeted in the City’s budget.

• Developer Impact Fees are collected from developers for the expansion of the existing City service in order to serve future development, the budget includes 9 Special Revenue Funds:

o Fire Protection Fund: impact fees collected from developers for the expansion of the existing fire station in order to serve future development.

o Police Protection Fund: impact fees collected from developers for the expansion of the existing police facility in order to serve future development.

o Park Development (Quimby) Fund: This fund accounts for the receipts of park-in-lieu fees (Quimby) and grant revenues that are used for construction, park acquisition, and development of park facilities.

o Recreation Community Center Fund: impact fees collected from developers and used for recreation facilities in order to maintain the adopted level of service of recreation/community center facilities of 542 square feet per thousand population.

o Park Improvement Fund: Impact fees collected from developers for park improvements are to be used to maintain the adopted level of service for neighborhood and community parks of 4.0 acres per thousand population. This fund accounts for the receipt and use of these monies.

o Traffic Signalization Fund: impact fees collected from developers and used for the future cost of traffic signals.

o Traffic Circulation Fund: developer traffic mitigation measure fees charged as a result of an environmental review.

o Transportation Facility Fund: impact fees (AB1600 fees) paid to protect the public health, safety, and welfare by maintaining the existing level of public services for existing and future residents within the City of Arroyo Grande.

o Drainage Facility Fund: impact fees paid by development and are restricted to improving drainage within the City.

• The Community Development Department budget includes three Special Revenue Funds:

o In-Lieu Affordable Housing Fund: This fund accounts for monies paid by developers in meeting the City's mandatory affordable housing requirements.

o In-Lieu Underground Utility Fund: This fund accounts for monies paid by developers in meeting the City's underground utility requirements.

o Community Development Block Grant (CDBG) Fund: This program is a flexible program that provides the City with resources to address a wide range of unique community development needs.

• The Police Department budget includes one Special Revenue Fund:

Fund Structure

o State COPS Block Grant Fund: This fund accounts for the receipt and use of monies from the State of California restricted to the purchase of police equipment and technology for crime prevention.

• The Public Works Department’s budget includes seven Special Revenue Funds:

o Three Landscape Maintenance District Funds account for and report on the activities of landscape maintenance districts.

o The Special Gas Tax Fund is used to account for the construction and maintenance of city streets funded by the City’s share of State gasoline taxes.

o Transportation Fund: This revenue source is provided by the San Luis Obispo County of Government’s (SLOCOG) Local Transportation Fund (LTF). The annual appropriation is restricted to transportation systems, including transit, pedestrian, street and road maintenance.

o Water Neutralization Fund: The City requires development projects that increase total water consumption in the City to “neutralize” that demand by reducing water consumption in existing development by an equivalent amount or by paying a fee in-lieu of performing water consumption reductions. This fund accounts for the amount collected from developers and is used towards the City’s water conservation efforts.

o Water Availability Fund: Pursuant to the provisions of Section 38743 of the Government Code, water availability charges is a “special charge” which is levied to each parcel of property not served with city water. These charges are restricted for the sole purpose of expanding water supply such as a desalination plant, recycled water, a scalping plant, etc.

• The Recreation Services Department budget includes one Special Revenue Fund:

o Tourism Business Improvement District (TBID) Fund: The purpose of the Tourism Business Improvement District (TBID) is to provide projects, programs and activities that benefit lodging businesses located and operating within the City of Arroyo Grande. A two percent (2%) assessment is levied on all lodging businesses of the rent charged by the operator per occupied room per night for all transient occupancies. Revenue collected is used to promote the lodging industry within the City.

• Other Special Revenue Funds include:

o Public Access Television Fund: This fund accounts for fees collected from Charter Communications that are restricted for support of public, education, and government access programming and equipment.

Enterprise Funds

The City’s enterprise funds are a type of proprietary fund used to manage services delivered to the public on a user-fee basis, operating much like a private business. These funds are self supporting; revenues come primarily from service charges, and they cover both operating expenses and capital costs. The City has 5 Enterprise Funds: Sewer, Sewer Facility, Water, Lopez, and Water Facility.

Agency Funds

The City’s agency funds are used to account for assets held temporarily on behalf of others such as the Successor Agency to RDA, Downtown Parking, and the Sanitation Distribution funds. They are not City revenues and are excluded from government-wide financial reporting of expenses or fund balances.

Fund Structure

Fund Structure

GOVERNMENTAL FUND TYPES

General Fund – is the general operating fund of the City and accounts for all unrestricted financial resources except those required to be accounted for in another fund.

Special Revenue Funds – to account for the proceeds of specific revenue sources (other than special assessments, expendable trusts, or capital projects) that are restricted by law or administrative action to expenditures for specific purposes.

Debt Service Funds – to account for the accumulation of resources for and the payment of interest and principal on general long-term debt and related costs. The City currently does not have general long-term debt that would be obligated to use a debt service fund.

Capital Project Funds – to account for financial resources segregated for the acquisition of major capital projects or facilities (other than those financed by proprietary fund types).

PROPRIETARY FUND TYPES

Enterprise Funds – to account for operations in a manner similar to private business enterprises, where the intent is to have the costs (expenses, including depreciation) of providing goods or services to the general public to be financed or recovered primarily through user charges.

FIDUCIARY FUND TYPES

Agency Funds – to account for assets held by the City as trustee or agent for individuals, private organizations, or other governmental units, and/or other funds. These funds are custodial in nature (assets correspond with liabilities) and do not involve measurement of results of o

FINANCIAL POLICIES

Financial Policies

A Fiscal Policy is an adopted guideline that establishes goals for the allocation of public resources in the manner best suited to the efficient provision of services to residents and visitors within the City. While not all of the goals may be achievable in the current year, the existence of such goals will serve to guide the City Council in its decision-making.

The budget document is a policy statement and financial plan that allocates City resources, such as personnel, materials, and equipment, in tangible ways to achieve the general goal of a balanced community. It is, therefore, prudent for the City Council to have adopted a Fiscal Policy to guide staff through the budget-development process. The Fiscal Policy is a guideline, not an absolute. The Policy describes goals the Council seeks to achieve to secure fiscal solvency, superior levels of customer service, and maximum cost efficiency. The Policy components are as follows:

FISCAL MANAGEMENT

• Maintain safety and liquidity while maximizing investment revenue.

• Utilize grants and subsidies from other sources when possible and cost-effective.

• Charge fees for services that reflect the cost of providing such services.

• Review fees annually, establish actual costs, adjust existing fees, and establish new fees as needed.

• Recover costs when possible for facility use, planning and building services, code enforcement, community events and administrative costs.

• Develop short and long-term financial plans.

• Develop fiscal models to reflect development and planning policies to ensure resources are adequate to provide service needs.

• Maintain a PERS Retirement Fund in which the City funds retirement costs on an annual basis at no lower than the projected long-term average rates in order to eliminate the fluctuations in PERS costs and provide long-term stability.

NEW SERVICES

Add new services only when a need has been identified and when adequate staffing and funding sources have been provided.

PUBLIC SAFETY

Provide funding to maintain the safety of the citizens of Arroyo Grande at a level that ensures that Arroyo Grande maintains its position as one of the safest cities in San Luis Obispo County.

FACILITIES

• Plan for new facilities only if operations and maintenance costs for those new facilities will not negatively impact the operating budget.

Financial Policies

• Provide adequate routine maintenance each year to avoid the cost of deferred maintenance.

OPERATIONAL EFFICIENCIES

• Provide City services in the most cost-effective manner.

• Provide staffing levels that allow employees to respond promptly to service requests from the public.

• Utilize consultants and temporary help for special projects or peak workload periods.

• Utilize community expertise on a voluntary basis as appropriate.

• Ensure that fee-supported services are staffed appropriately to render the services for which customers have paid.

• Work through regional agencies to share costs for local and mandated programs whenever possible.

EMPLOYEE DEVELOPMENT

Attract and retain competent employees for the City workforce by compensating employees fairly, providing adequate training opportunities, ensuring safe working conditions, and maintaining a professional work environment.

ECONOMIC DEVELOPMENT

• Promote a mix of businesses that contribute to a balanced community, develop programs to enhance and retain existing businesses, and pursue new developments and businesses that add to but do not detract from the City’s economic base.

• Maximize opportunities for the existing business community, thereby increasing existing sources of revenue to meet the increasing demands for service.

RETIREE MEDICAL

Pre-fund retiree medical benefit costs.

Financial Policies

DESCRIPTION OF FUNDS

Fund Accounting Systems

The City uses funds and account groups to report on its financial position and the results of its operations. Fund accounting is designed to demonstrate legal compliance and to aid financial management by segregating transactions related to certain City functions or activities.

A fund is an accounting entity with a self-balancing set of accounts established to record the financial position and results of operations of a specific governmental activity. An account group is a financial reporting device designed to provide accountability for certain assets and liabilities that are not recorded in the funds because they do not directly affect net expendable available resources. The City maintains the following fund types and account groups:

TYPES OF FUNDS

Governmental Fund Types

General Fund – the general operating fund of the City and accounts for all unrestricted financial resources except those required to be accounted for in another fund.

Special Revenue Funds – to account for the proceeds of specific revenue sources (other than special assessments, expendable trusts, or capital projects) that are restricted by law or administrative action to expenditures for specific purposes.

Debt Service Funds – to account for the accumulation of resources for and the payment of, interest and principal on general long-term debt and related costs. The City currently does not have general long term debt that would be obligated to use a debt service fund.

Capital Project Funds – to account for financial resources segregated for the acquisition of major capital projects or facilities (other than those financed by proprietary fund types).

Proprietary Fund Types

Enterprise Funds – to account for operations in a manner similar to private business enterprises where the intent is to have the costs (expenses, including depreciation) of providing goods or services to the general public to be financed or recovered primarily through user charges.

Fiduciary Fund Types

Agency Funds – to account for assets held by the City as trustee or agent for individuals, private organizations, or other governmental units, and/or other funds. These funds are custodial in nature (assets correspond with liabilities) and do not involve measurement of results of operations.

Financial Policies

Basis of Accounting

Basis of accounting refers to when revenues and expenditures or expenses are recognized in the accounts and reported in the financial statements. Specifically, it relates to the timing of the measurements made, regardless of the nature of the measurement. All Governmental funds and Agency funds are accounted for using the modified accrual basis of accounting. Revenues are recognized when they become measurable and available as net current assets. In those funds where revenue is recognized on a modified accrual basis the following revenues may be accrued: property and sales taxes, revenue from the use of money and property, interfund transfers, unbilled service receivables and intergovernmental revenue. Licenses, permits, fines and forfeitures and similar items are, for the most part, not accrued and consequently are not recorded until received. Agency funds are purely custodial (assets equal liabilities) and thus do not involve measurement of results of operations. The assets and liabilities are accounted for on a modified accrual basis with the exception of the City’s Deferred Compensation Plan, which is accounted for on a market value basis in accordance with Statement No. 2 of the Governmental Accounting Standards Board (GASB).

Property tax revenue is recognized in the fiscal year for which the taxes have been levied providing they become available, in accordance with National Council of Governmental Accounting GASB 33. In this context, available means when receivable and due, when payment is expected within the current period, or within sixty (60) days of year end, and thus available to pay debts of the current period.

Grants, entitlements, or shared revenues recorded in governmental funds are recognized as revenue in the accounting period when they become susceptible to accrual, i.e. both measurable and available (modified accrual basis).

Expenditures are generally recognized under the modified accrual basis of accounting when the related fund liability is incurred. Principal and interest on general long-term debt is recognized when due.

All proprietary funds are accounted for using the accrual basis of accounting. Their revenues are recognized when they are earned and become measurable, expenses are recognized when they are incurred if measurable.

The City reports deferred revenue on its combined balance sheet. Deferred revenues arise when potential revenue does not meet both the “measurable” and “available” criteria for recognition in the current period. Deferred revenues also arise when the City receives resources before it has a legal claim to them, as when grant monies are received prior to the incurrence of qualifying expenditures. In subsequent periods, when both revenue recognition criteria are met, or when the City has a legal claim to the resources, the liability for deferred revenue is removed from the combined balance sheet and revenue is recognized.

Financial Policies

BUDGETARY PROCESS

The City uses the following procedures in establishing the budgetary data reflected in the financial statements: after January 1, Department Directors prepare estimates for required appropriations for the fiscal year commencing the following July 1. The departmental estimates are presented to the City Manager for review. A Preliminary Budget is prepared that includes estimated expenditures and forecasted revenues for the fiscal year. Prior to July 1, the City Manager submits a Preliminary Budget for the upcoming fiscal year to the City Council. The Preliminary Budget includes a summary of the proposed expenditures and financial resources of the City, as well as historical data for preceding fiscal periods. Public meetings are conducted to obtain citizens’ comments. The City Council adopts the budget by June 30. Budgets are legally adopted for the general, special revenue, enterprise funds, agency funds and all capital projects programs during the fiscal year ended June 30. The appropriated budget covers substantially all City expenditures. All appropriated amounts shown are as originally adopted or as amended by the City Council. During the year, supplementary appropriations may be approved. Unexpended appropriations lapse at the year-end, unless approved for carryover by the City Manager to address multi-year projects or initiatives.

Department Directors are authorized to transfer budgeted amounts within their departments, within the same fund, with the approval of the City Manager. The City Manager has authority to make transfers of appropriations between departments, provided those changes do not impact budgeted year-end fund balances. Only the City Council may authorize transfers of appropriations between funds. Formal budgetary integration is employed as a management control device during the fiscal year for all governmental funds.

ENCUMBRANCES

Encumbrances represent commitments related to unperformed contracts for goods or services. Encumbrance accounting, under which purchase orders, contracts, and other commitments for the expenditure of resources are recorded to reserve that portion of the applicable appropriation, is utilized in all funds. Encumbrances outstanding at year-end are reported as reservations of fund balances and do not constitute expenditures or liabilities because the commitments will be honored during the subsequent year. Amounts encumbered at year-end are reappropriated in the following year.

BUDGET BASIS OF ACCOUNTING

Budgets for governmental funds are adopted on a basis consistent with generally accepted accounting principles (GAAP).

CASH AND INVESTMENTS

Cash includes amounts in demand deposits. Investments, including accrued interest, are stated at fair market value.

Financial Policies

INTERFUND TRANSACTIONS

During the course of operations, numerous transactions occur between individual funds for goods provided or services rendered. These receivables and payables are classified as “due from other funds” or “due to other funds” on the balance sheet.

INVENTORIES

Inventories of materials and supplies are carried at cost on a first-in, first-out basis. The City uses the consumption method for accounting for inventories.

FIXED ASSETS

All purchased fixed assets are valued at cost where historical records are available, and at an estimated historical cost where no historical records exist. Donated fixed assets are valued at their estimated fair market value on the date received.

The costs of normal maintenance and repairs that do not add to the value of the asset or materially extend asset lives are not capitalized. Improvements are capitalized and depreciated, as applicable, over the remaining useful lives of the related fixed assets.

In accordance with GASB 34, all Public domain (“infrastructure”) fixed assets are now capitalized. Examples of infrastructure assets are: roads, bridges, curbs and gutters, streets and sidewalks, drainage and lighting systems.

Depreciation of fixed assets is computed using the straight-line method. The estimated useful lives are as follows:

Buildings and structures

40 – 55 years

3 – 10 years

5 – 20 years

COMPENSATED ABSENCES

Vested or accumulated personal leave of employees, that is expected to be liquidated with expendable available financial resources, is reported as an expenditure and a fund liability of the governmental fund that will pay it. Amounts of vested or accumulated personal leave not expected to be liquidated with expendable available financial resources are reported in the City’s financial statements as long-term debt. No expenditure is reported for those amounts. Vested or accumulated personal leave of proprietary funds is recorded as an expense and liability of those funds as the benefits accrue to employees.

Financial Policies

PROPERTY TAXES

The San Luis Obispo County Assessor and Tax Collector perform the duties of assessing and collecting property tax, respectively. Tax levies cover the period from July 1 to June 30 of each year. All tax liens attach annually on the first day in March proceeding the fiscal year for which the taxes are levied. Taxes are levied on both real and personal property as of March 1.

Secured property taxes are levied against real property and are due and payable in two equal installments. The first installment is due on November 1 and becomes delinquent if not paid by December 10. The second installment is due on February 1 and becomes delinquent if not paid by April 10. Unsecured personal property taxes are due on July 1 each year. These taxes become delinquent if not paid by August 31.

GRANTS

Federal and state grant revenues are accrued to the extent expenditures are incurred. All such grants are subject to audit and adjustment by the grantor.

LONG-TERM OBLIGATIONS

Long-term debt is recognized as a liability of a governmental fund when due or when resources have been accumulated in the debt service fund for payment early in the following year. Other long-term obligations to be financed from expendable available financial resources are reported as a fund liability of a governmental fund. The remaining portion of such obligations is reported in the financial statements. Long-term liabilities to be financed from proprietary fund operations are accounted for in those funds.

FUND EQUITY

Contributed capital is recorded in proprietary funds that have received capital grants or contributions from developers, customers or other funds. These reserves represent those portions of fund equity not available for expenditure or that are legally segregated for a specific future use of financial resources. Fund designations are established to indicate tentative plans for the use of current financial resources in the future.

Financial Policies - Fund Balance

INTRODUCTION

This policy was adopted by the City Council on June 11, 2024 with Resolution 5371. The purpose of this document is to state the policy goals of the City of Arroyo Grandes’ General Fund reserves, and the budgeting practices that maintain such reserves. Although there is no formula that defines a completely adequate Fund Balance, a conservative approach should enable the City to finance its operations and meet unplanned expenditures without having to incur short-term debt or raise new revenues.

These policies are intended to provide guidelines for budget decisions as to the appropriate use of General Fund resources and the maintenance of adequate reserves for contingencies, emergencies, capital improvements, and other such uses as determined by the City Council. After amounts projected to be available from the year-end fund balance of the General Fund are allocated to Assigned categories, the remaining amount, referred to as the Unassigned Fund Balance, will be reserved for contingencies as further set forth below.

PURPOSE

The purpose of the Fund Balance and Reserve Policy is to ensure strong fiscal management to guide the City of Arroyo Grande’s financial planning, while continuing to provide services to the residents of the City. Additionally, the policy will: aide in reducing financial impacts of temporary revenue short falls and unpredicted one-time expenditures, such as disasters or catastrophic events; assist the City in responding to challenges of a changing economic environment; and preserve adequate reserve levels to improve or maintain the City’s credit worthiness. The Fund Balance and Reserve Policy establishes the appropriate level of reserves in the Consolidated General Fund. The policy sets conditions warranting the use of reserves and outlines the plan to replenish them if the balances fall below the levels established in this policy.

BACKGROUND

Governmental Accounting Standards Board (GASB) Statement No. 54, Fund Balance Reporting and Governmental Fund Type Definitions, was implemented in FY 2010-11 with the intent of improving financial reporting by providing fund balance categories that will be more easily understood. The categories are more clearly defined to make the nature and extent of the constraints placed on a government’s fund balance more transparent. This Fund Balance and Reserve Policy establishes the procedures for reporting unrestricted fund balance in the financial statements. The policy also authorizes and directs the Administrative Services Director to prepare financial reports which accurately categorize fund balance as per GASB Statement No. 54.

Financial Policies - Fund Balance

POLICY

Fund balance is essentially the difference between the assets and liabilities reported in a governmental fund. There are five separate components of fund balance, each of which identifies the extent to which the City is bound to honor constraints on the specific purposes for which amounts can be spent.

• Non-spendable fund balance: Amounts that cannot be spent because they are either (a) not in spendable form or (b) legally or contractually required to be maintained intact.

• Restricted fund balance: To be used for specific purposes stipulated by external resource providers, constitution, or through enabling legislation

• Committed fund balance: To be used for specific purposes as established by City Council.

• Assigned fund balance: Amounts intended for a specific purpose as authorized by the City Manager, but are neither restricted nor committed.

• Unassigned fund balance: The residual amount not contained in the other classifications. The first two components listed above, non-spendable and restricted fund balances, are not addressed in this policy due to the nature of the restrictions. Examples of non-spendable fund balance include prepaid expenses, loan receivables, and inventory. Restricted fund balance is either imposed by laws or constrained by grantors, contributors, or laws or regulations of other governments. This policy is focused on financial reporting of unrestricted fund balance, which is the last three components listed above. These three components are further defined below.

These funds may be pooled for investment earning purposes only and interest earned shall be credited to each individual fund based upon the proportionate share of the revenues invested.

Committed Fund Balance

The City Council, as the City’s highest level of decision-making authority, may commit fund balance for specific purposes pursuant to constraints imposed by formal actions taken, such as an ordinance or resolution. These Committed amounts cannot be used for any other purpose unless the City Council removes or changes the specified use through the same type of formal action taken to establish the commitment. Five types of committed reserves are set aside by the City including Operating Reserve, Pension and Other Post-Employment Benefits Reserve, Information Technology Reserve, Fleet Replacement Reserve, and Facility Repairs Reserve. The intended use of each reserve and the Fund(s) in which they are held is outlined below. To develop the appropriate amount of reserves, the City considered guidance from the Government Finance Officers Association (GFOA), as well as the current economic conditions and needs of the City. Reserve balances will be reviewed at the end of each fiscal year to ensure compliance with this Policy.

• Operating Reserve – The GFOA recommends that general-purpose governments maintain reserves in the general fund of no less than two months (16.67%) of annual general fund operating revenues or annual general fund operating expenditures. The City has established an Operating Reserve in the Consolidated General Fund to mitigate financial and service delivery risk due to

Financial Policies - Fund Balance

unexpected revenue shortfalls or unanticipated critical expenditures. The purpose of this reserve is to provide budgetary stabilization and not to serve as an alternative funding source for new programs and ongoing operating expenditures. It is for one-time needs and expenditures identified in the budget and not ongoing structural challenges. The City will aim to maintain a minimum balance in the Operating Reserves equal to approximately 15%, with a goal of 20% of the City’s annual operating expenditures.

• Pension and Other Post-Employment Benefits Reserve – Funds set aside under this reserve in the Consolidated General Fund to be used to further mitigate costs associated with pensions and other post-employment benefits. These funds will be used: as a funding source for potential additional discretionary payments to pay down unfunded liability; or held in the reserve account; or placed in a City Council approved trust instrument. Funds may be used for such purposes as a supplemental funding source for unanticipated increases to the annual pension and/or other post-employment benefit costs resulting from future actuarial assumptions and investment market volatility, or to make the City’s annual payments during times of economic uncertainty as brought on by such circumstances as a recession resulting in funding gaps.

• Information Technology Reserve – This fund, established in the Consolidated General Fund, provides for information system and technology projects including communications systems, hardware, and software, which are capital in nature. Technology can change rapidly within the information systems sphere and often comes at a large cost. This reserve helps the City keep pace with changes in information technology and take advantage of improvement/efficiency opportunities in this area. This reserve will not exceed 1.0% of annual Consolidated General Fund operating expenditures.

• Fleet Replacement Reserve – The City will maintain a Fleet Replacement Reserve in the Consolidated General Fund to provide for the timely replacement of existing vehicles should they come to the end of their useful life or become inoperable. This reserve will not exceed 1.0% of annual Consolidated General Fund operating expenditures.

• Facility Repairs Reserve – This reserve is set up in the Consolidated General Fund to address any unforeseen maintenance and repairs or planned replacements within City owned facilities. This reserve will not exceed 1.0% of annual Consolidated General Fund operating expenditures.

Assigned Fund Balance

Amounts that are constrained by the City’s intent to be used for specific purposes, but are neither restricted nor committed, should be reported as assigned fund balance. This policy herby delegates the authority to assign amounts to be used for specific purposes to the City Manager or designee for the purpose of reporting these amounts in the annual financial statements. Examples of assigned fund balance include:

Financial Policies - Fund Balance

• Encumbered Fund balance levels must be sufficient to meet funding requirements for materials or services ordered, but not received, before the end of the fiscal year.

• Continuing Appropriations Fund balance levels must be sufficient to meet funding requirements for projects approved in prior years and which must be carried forward into the new fiscal year.

• Other Designations Assigned fund balance can also include amounts designated for certain programs, additional reduction of debt, special events, or other non-recurring expenditure needs of the City.

Unassigned Fund Balance

Unassigned fund balance is the residual positive net resources in excess of what can properly be classified in one of the other four categories. The Consolidated General Fund is the only fund that may report a positive (surplus) unassigned balance. Conversely, any governmental fund in a negative (deficit) position could report a negative amount of unassigned fund balance.

Fund Balance Classification

The accounting policies of the City consider restricted fund balance to have been spent first when the expenditure is incurred for purposes for which both restricted and unrestricted fund balance is available. Similarly, when the expenditure is incurred for purposes for which amounts in any of the unrestricted classifications of fund balance could be used, the City considers committed amounts to be reduced first, followed by assigned amounts and the unassigned amounts.

Surplus

Since a surplus of unassigned fund balance does not represent a recurring source of revenue, it shall not be used to fund a recurring expense; however, the surplus may be appropriated for use to fund a onetime expenditure or use not already funded through an appropriation. If it is determined there is an operating surplus, the City Council may appropriate funds for the following nonrecurring purposes, listed in order of priority:

• Surplus funds may be used to meet the minimum Operating Reserve requirement;

• Any surplus may be transferred to reduce the unfunded pension liability and/or any other unfunded postemployment benefit liabilities;

• If there is short-term debt within the General Fund, the surplus may be applied to reduce, or eliminate, the debt if determined to be advantageous for the City. If a borrowing is scheduled, the surplus may be used to reduce the principal amount the City needs to obtain if determined to be advantageous for the City; and

• Surplus funds may be used for capital improvements and equipment purchases that are not financed with borrowings or other contributions.

Financial Policies - Fund Balance

Replenishment of Reserves

If the Operating Reserve balance established in this policy falls below the minimum required level, the City shall strive to restore it to the minimum required balance by any feasible means, including, but not limited to, adopting a budgetary surplus; applying any cost savings, over-realized revenues, and/or surpluses realized within the applicable fund.

If the Information Technology Reserve, Fleet Replacement Reserve, or Facility Repairs Reserve fall below the 1.0% of annual Consolidated General Fund operating expenditures. The levels will be replenished when surplus funds become available.

These guidelines may be suspended, in whole or part, if financial or economic circumstances prevent meeting any or all of the timelines. These policy guidelines may also be amended by action of the City Council from time to time.

This policy is instituted to provide a measure of protection for the City against unforeseen circumstances and to comply with GASB Statement No. 54. No other policy or procedure supersedes the authority and provisions of this policy.

Enterprise Fund Reserves

Reserves for Enterprise Funds – Water and Wastewater (Sewer): Revenues contained in these funds are restricted and may only be used for their described purposes below. In no event will these funds be used to fund general fund services.

• Operating Reserve – The purpose of the Enterprise Fund Operating Reserve is to provide working capital to meet cash flow needs during normal operations and support the operation, maintenance and administration of the utility. This reserve ensures that operations can continue should there be significant events that impact cash flows. The target balance to be maintained is 90 days (25 percent) of the current annual operating expense budget.

• Capital Reserve – The purpose of the Enterprise Fund Capital Reserve is to fund future replacement of assets and CIP projects. The Capital reserves are used to fund the construction of the projects as the projects progress and the funds are expended. The reserve target has been established at $500,000 each for the water and wastewater systems through prior cost of service studies.

Lopez Fund Reserve – The Enterprise Fund Lopez Fund accounts for the revenue and expenditures of the surface water purchases from the County. Revenues are collected through the water rates in sufficient amounts to provide for a transfer of revenue to meet the expenses in the Lopez Fund. A reserve is maintained in the fund at least equal to annual Lopez debt service

Financial Policies – Debt Management

INTRODUCTION