Singapore’s plan to become a premier networking hub

Special Interconnect World Supplement

W.Media is a Technology Publisher & Community Hub.

We serve the cloud/IT, data centers and network infrastructure professionals through media solutions and business events.

4 From the Editor ’s Desk

50 In Closing When innovation meets the heat

COVER STORY

12 Why all roads lead to liquid cooling

15 Can liquid cooling aid India’s tryst with a new destiny ?

18 Can floating data centers solve the heat crisis?

20 The science of monitoring data center airflows

FEATURES

41 Can it take the heat? Reassessing timber ’s role in data centers

44 Can Southeast Asia’s data centers thrive in a global trade storm

HIGHLIGHTS

21 Powering possibilities: The role of data centers in cloud and hybrid evolution

23 Shaping the global digital inf rastructure landscape

48 Chennai: The beating heart of South Asia’s interconnected digital ecosystem

INTERCONNECT WORLD SUPPLEMENT

31 What lies beneath

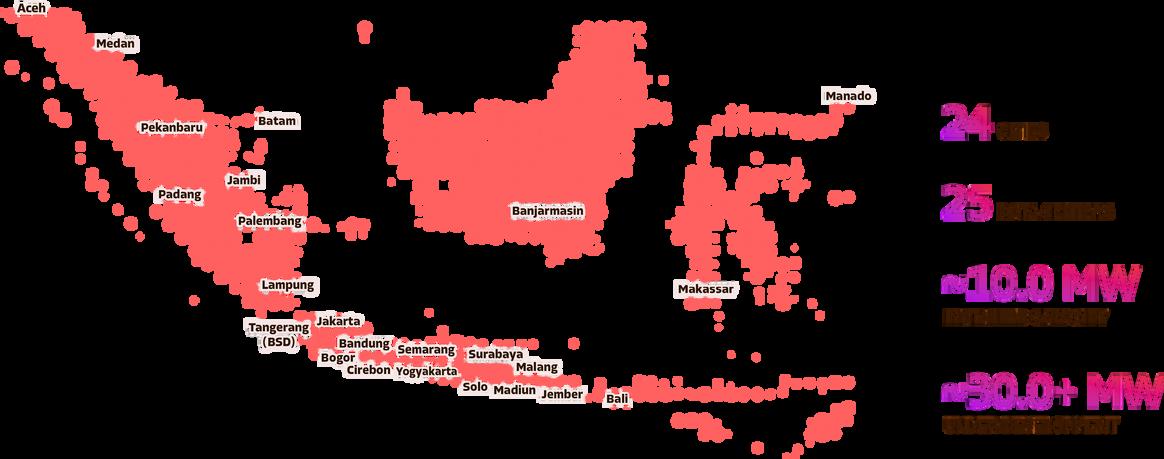

33 Singapore’s plan to become a premier networking hub

35 Sun, sand, subsea cables: The Middle East’s rise as a global digital crossroads

38 Discover APAC’s Connectivity Ecosystem with InterconnectWorld Asia 2025

From the Editor ’s Desk

Liquid cooling has emerged as quite a hot topic across the global cloud and data center industry.

With ever increasing need for energy efficient heat management in data centers, especially in the age of ar tificial intelligence (AI), different methods of liquid cooling are attracting the attention of digital inf rastructure developers and users.

So who is embracing liquid cooling? Is immersion cooling more popular than direct-to-chip or precision cooling? What kind of changes or upgrades are data center owners and operators willing to make to adopt liquid cooling? Will liquid cooling eventually make traditional cooling methods obsolete?

In this issue, we take a closer look at all these exciting elements of this evolving field of technology.

Also included is a special supplement examining the global connectivity ecosystem, where we take a deep dive into subsea cables, internet exchanges, telecommunications and peering across APAC and MENA

We hope you enjoy reading this issue as much as we enjoyed putting it together

Deborah Grey Editor-in-Chief W.Media

Meet the team

Deborah Grey Editor-in-Chief

Jan Yong SEA Editor

Paul Mah Executive Editor

9–10 July 2025 | 8:00 AM – 5:00 PM | Marina Bay Sands Expo & Convention Centre, Singapore

Open Compute Project SEA Tech Day

Driving Scalable, Sustainable Infrastructure for Southeast Asia’s Digital Future

As Southeast Asia cements its position as one of the world’s fastest-growing digital hubs, the region faces complex challenges: rising AI workloads, denser compute environments, and the urgent need for sustainable, future-ready infrastructure.

In response, the Open Compute Project (OCP)—in collaboration with W.Media—is hosting OCP SEA Tech Day, a full-day technical exchange spotlighting the open hardware and software innovations reshaping the data center landscape.

Designed for hyperscalers, data center operators, silicon providers, OEMs, and network architects, this gathering is rooted in practical insights and cross-industry collaboration. From silicon to system, rack to facility, OCP’s open standards are setting new benchmarks in efficiency, performance, and deployment at scale.

Join Us in Singapore

What to Expect

• In-depth sessions on AI infrastructure, Open Rack V3, power architecture, and liquid cooling

• First-hand insights into regulatory trends shaping DC growth in SEA

• Real-world case studies from hyperscalers, chipmakers, and systems integrators

• Networking with top-tier decision-makers and open hardware leaders

• Explore OCP Ready™ Certification and open standards for scalable sustainability

We’re opening the floor to sponsors and delegates who are helping shape the region’s digital future. Whether you’re building the tech or setting the strategy—this is where your voice belongs.

Interested in sponsoring?

Reach out to us at focus@w.media

Want to attend?

Secure your pass now: https://w.media/ocp/ocp-sea-tech-day

STT GDC breaks ground on Johor data center

In recent years, Johor has gained a reputation as the fastest-growing data center hub in Southeast Asia with some of the world’s biggest data center companies marking their presence there.

One of them is ST Telemedia Global Data Centres (STT GDC), one of the world’s fastest-growing data centre providers. According to news reports, it broke ground for its first data center facility in the STT Johor data centre campus – STT Johor 1 in February. Designed with an IT load capacity of 16MW, it is expected to be fully operational by the end of 2026.

STT GDC’s data centre campus has a development potential of 120MW of IT load. Spanning over 22 acres of land within the Nusa Cemerlang Industrial Park in Iskandar Puteri, Johor, just 15 kilometres from Singapore, its prime location ensures seamless connectivity, including integration with STT Singapore 5, STT GDC’s regional interconnection hub. STT Johor 1 is equipped to handle advanced computational workloads for enterprises, government agencies, and cloud service providers, capable

of rapidly deploying resourceintensive applications across various industries. This will support cuttingedge research, complex simulations and data-driven decision-making processes.

In addition to STT Singapore 5, STT Johor 1 will also be connected to STT Kuala Lumpur 1 and STT GDC’s other data centre interconnection hubs in Thailand, Vietnam and Philippines via a Data Centre Interconnect (DCI) service, providing customers in STT Johor 1 with highly reliable and seamless access to business opportunities in other major economies in the region. The campus will be powered by renewable and low-carbon energy sources with ongoing discussions with several renewable energy providers, such as Ditrolic Energy, to become the renewable electricity supplier.

India attracts billion-dollar investments into data centers at WEF 2025

This year, several big-ticket announcements were made at the World Economic Forum (WEF) at Davos, surrounding huge investments into digital infrastructure in India.

Amazon Web Services (AWS) exchanged a signed memorandum of understanding (MoU) with the Government of Maharashtra at WEF, to formalise its plan to invest US$ 8.3 billion into cloud infrastructure in the AWS Asia-Pacific (Mumbai) Region in Maharashtra, to further expand cloud computing capacity in India. This investment is estimated to contribute US$ 15.3 billion to India’s gross domestic product (GDP) and support more than 81,300 full-time jobs annually in the local data centre supply chain by 2030. Also at WEF, Sify Technologies Limited, one of India’s most prominent Digital ICT solutions providers, revealed plans to invest a whopping US$ 5 billion into expanding its data hubs, and integrating Artificial Intelligence (AI) operations with cutting-edge GPUs. Sify’s plans include building smaller AI inferencing facilities in 20 Tier II cities. Meanwhile, CtrlS Datacenters, a major player in the Indian data center market, signed an MoU with the government of the southern Indian state of Telangana to build a cluster of AI-ready data centers with a proposed investment of over Rs 10,000 crores.

Tilman Global Holdings, a USbased holding company focused on creating, operating and investing in telecommunications and energy infrastructure, signed an MoU with Telangana indicating plans to invest Rs 15,000 crores in a 300MW hyperscale data center facility in the state. This facility will also support AI workloads, and will feature advanced cooling technologies and energy efficient systems.

Ursa Clusters, a US-based data center company also signed an MoU with the Telangana government. It plans to invest Rs 5,000 crore to build a 100MW AI data center hub in Hyderabad. The facility will reportedly utilize hybrid AI chips to foster an ecosystem for start-ups and enterprises.

Executives of STT GDC and officials from the Johor government come together for the groundbreaking ceremony of STT Johor 1.

Blackstone may sell two AirTrunk DCs in Australia

Bloomberg, has reported that Blackstone is considering the sale of two of AirTrunk’s Australian data centers.

Blackstone bought AirTrunk in a deal worth $16.1 billion last year, but is now reported to be considering selling the firm’s facilities in Sydney and Melbourne. The sale of the two data centers could raise up to AU$4 billion ($2.6bn). Blackstone would reinvest this money in AirTrunk with the reported objective of helping the company expand into new markets.

People familiar with the matter have told Bloomberg that Blackstone has engaged advisors to explore the sale but no final decision has been made. Which of the two AirTrunk data centers currently operational in Sydney would be put up for sale is unclear. The company’s SYD1 campus was completed in 2022 and offers a capacity of 130MW. SYD2 offers a capacity of over 120MW. A third Sydney campus is currently in development with a capacity of up to 320MW. Additionally, in Melbourne, the company operates a single data center campus which opened in 2017, and once expansion work is completed will

offer a capacity of 185MW. From its Australian origins, AirTrunk has moved in recent years to expand its footprint outside Australia, especially into Asia including a planned 270MW data center campus in Johor, Malaysia.

AI at the heart of investments into digital infrastructure in the Middle East

While India was attracting global attention at Davos, the Middle East saw a slew of big billion-dollar investment announcements at LEAP 2025 in Riyadh, Saudi Arabia. LEAP 2025 is organized by the Ministry of Communications and Information Technology, the Saudi Federation for Cybersecurity, Programming, and Drones (SAFCSP), and Tahaluf Company, supported by the Events Investment Fund. Here are some of the most noteworthy announcements.

Equinix, a global player in the digital technology and connectivity ecosystem, announced plans to invest US$ 1 billion into building digital infrastructure in Saudi Arabia. Equinix will develop carrier neutral data center facilities, to meet the growing demand for cloud, AI, and enterprise workloads. The data center facilities will deliver high-performance

interconnection solutions for enterprises and hyperscalers through the Equinix fabric platform.

Meanwhile, DataVolt, a major player in the digital infrastructure market in the Middle East, announced plans to develop a 1.5GW net zero AI factory campus in Oxagon, which is an underdevelopment industrial zone that is part of the wider futuristic NEOM project. The project would see investment worth US$ 5 billion. DataVolt also signed an agreement with the Saudi Authority for Industrial Cities and Technology Zones (MODON), to invest US$ 660 million into developing a data center in Riyadh’s Tech City. Etihad Etisalat Company (Mobily), a renowned technology, media, and telecommunications company in Saudi Arabia, also announced big investment plans at LEAP saying that it will invest a whopping SAR 3.4

billion (US$ 905 million) into digital infrastructure such as data centers, submarine cables, and fiber networks in the Middle East.

Tencent Cloud, the cloud business of global technology company Tencent, announced the launch of its first Middle East Cloud Region in Saudi Arabia. The Region will feature two availability zones with full redundancy, advanced cloud services, and AI capabilities. The announcement was followed by a business operation commitment of over US$ 150 million in infrastructure, resources, and investment over the next few years. The new availability zones are expected to be operational by 2025, and aim to enable the delivery of an expanded suite of SaaS and PaaS solutions to the Middle East.

AirTrunk’s SYD1 Sydney West data center is speculated to be a possible candidate to be sold but no confirmation yet from the company.

PHOTO BY AirTrunk

Vietnam on cusp of data center boom

Vietnam’s data center market is gaining momentum with investment projections rising to US$ 1.75 billion by 2030 from US$ 654 million in 2024, a CAGR of 17.93%, according to a recent report by Vietnam Data Center Market – Investment Analysis & Growth Opportunities 2025-2030 .

The growth is driven by digital transformation, government policies, and increasing investments from both domestic and international players. Other favourable factors boosting Vietnam’s attractiveness as a key data centre hub in Southeast Asia include the relative affordability of its land and construction costs. According to Cushman & Wakefield’s Asia Pacific Data Centre Construction Cost Guide 2025, Vietnam has some of the lowest construction costs in the region. Its construction costs range from US$ 5.5-8.5 million per megawatt, with an average of US $6.935 million per MW, with land costs representing only 5% of total construction costs. Suburban land with available infrastructure in Ho Chi Minh City and Hanoi averages US$ 209 per square meter.The report also highlighted substantial investment opportunities in IT infrastructure, power, cooling, and general construction services. Improving infrastructure, increasing reliance on cloud services, thriving colocation market, growing enterprise digitalization initiatives and rapid adoption of AI, all point towards Vietnam’s increasing attractiveness as

Iron Mountain Data Centers takes over Web Werks

Iron Mountain Data Centers, a major player in the global data center industry which was thus far in a joint venture with Indian data center company Web Werks, has now taken over the latter. The change is effective April 1, 2025, and Web Werks will now

a data center hub in Southeast Asia. In addition, the data center industry is increasingly focused on energyefficient infrastructure such as liquid cooling and renewable energy. An example is Viettel’s green AI-ready data center, launched in April 2024 with a power capacity of 30MW. This aligns with the Vietnamese government’s pledge to achieve 39% renewable energy in the country’s energy mix by 2030.Vietnam is also planning to establish 10 new submarine cables by 2030, further bolstering its connectivity. In another significant move, the Vietnamese government has in July 2024 allowed foreign investors full ownership of data centers. The recent announcement of the setting up of SAM DigitalHub, a 50-ha (124-

acre), 150-MW data center campus initiative with a targeted investment of up to US$1.5 billion is yet further proof that demand for data centres is surging. This followed the entrance in 2024 of new players such as Epsilon Telecommunications (KT Corporation), Gaw Capital, and Infracrowd Capital.Despite challenges such as infrastructure limitations, cybersecurity risks, and talent shortages, the new entrants are coming well-prepared to face them. Operators are reportedly racing to expand their capacities to meet surging demand for cloud computing, fintech services, and AIdriven applications in key cities like Hanoi and Ho Chi Minh City. Currently, data centres number about 26 with 11 in the pipeline.

be known as Iron Mountain Data Centers.

In an official statement published on its website, Iron Mountain Data Centers explained how this came about, saying, “Since Iron Mountain and Web Werks first set up a joint venture four years ago, we have worked as a single team to meet customer needs in both existing and new data centers across India. To help this happen, Iron Mountain’s investment in the business increased over the years to 100% ownership, and we are

now ready to complete the integration of Web Werks within our global data center business.”

The acquisition has come with leadership change at the top. Web Werks founder Nikhil Rathi has stepped down as CEO. Rajesh Tapadia has taken over the day-to-day direction of the data center business in India as CEO, and will work very closely with Arvind Subramanian, Managing Director of Iron Mountain in India.

Ho Chi Minh City’s traffic scene

Photo by Jan Yong

Microsoft pulls plug on 2GW DC builds

Microsoft had abandoned data center projects with 2GW capacity in the U.S. and Europe in the last six months due to an oversupply relative to its current demand forecast, TD Cowen analysts said recently.

The tech giant’s withdrawal from new capacity leasing was largely led by the decision not to support additional training workloads from ChatGPT

maker OpenAI, the analysts led by Michael Elias said in a note, according to Reuters.Investor skepticism about the hefty artificial intelligence spending by U.S. tech firms has increased due to slow payoffs and the rise of Chinese startup DeepSeek, which showcased AI technology at a much lower cost than its Western rivals.

TD Cowen’s supply chain checks indicate that Microsoft’s pullback has led to Alphabet’s Google stepping in to backfill the capacity in international markets, while Meta Platforms does the same in the U.S. Microsoft, whose shares were down more than 1% on Wednesday, said, while

US$100B needed to fund APAC data center pipeline

Over US$116 billion will be needed to build out the existing colocation data centre pipeline across Asia Pacific in the coming five to seven years as demand for the sector grows, Cushman & Wakefield estimates in its recent report.

The H2 2024 Asia Pacific Data Centre Market Update report shows the pipeline of colocation projects (excluding hyperscale projects) in the region either currently under construction or in late-stage planning stands at 12,452 megawatts (MW). Using the construction cost of a mid-specification data centre for each market as a benchmark, the total capital required to build out the pipeline currently sits at US$116.2 billion. The estimated returns is over US$14.9 billion in annual colocation rent which can potentially achieve almost 13% yield-on-cost ratio for developers.Of the 12.45 gigawatts (GW) in the pipeline (which excludes land banking activity and projects in early planning stages), over 80% is held in five markets: Japan,

India, Australia, the Chinese mainland and Malaysia.

At a city level, Tokyo has the strongest pipeline within Asia Pacific at 1,656 MW, followed by Mumbai (1,143 MW), Johor (1,049 MW), Sydney (783 MW), and Beijing (613 MW). In these key cities, gross yield on cost increases to 14%. Pritesh Swamy, Head of Research & Insights, Data Centre Group, Asia Pacific said amid rising demand, the Asia Pacific development pipeline has exceeded existing operational capacity by three times. This has increased investment in this sector as investors are drawn by the massive potential. “This is evidenced by the sector’s increasing share of annual real estate investment volumes,” he concluded. Gordon Marsden, Head of Capital

it ay “strategically pace or adjust our infrastructure in some areas, we will continue to grow strongly in all regions”. It added its plans to spend US$80 billion on AI infrastructure this fiscal year are on track.In February, TD Cowen analysts had said that Microsoft had scrapped leases totalling “a couple of hundred megawatts” of capacity with at least two private data center operators. AI cloud startup CoreWeave, which provides access to data centers, earlier this month said it had not seen any contract cancellations after the Financial Times reported that Microsoft, its largest customer, had moved away from some agreements.

Markets, Asia Pacific, said that the high CAGR of about 20-plus per cent and great rental returns mean that the sector would continue to attract more investors. Although consolidation is expected as the sector matures, in the near term, “the capital requirements mean the sector continues to attract vast capital at a faster rate than other asset classes in the CRE universe.” He added that a flurry of valuation activity in response to recent transactions in Japan, Korea and Singapore mostly involving legacy data centres has provided some clarity around pricing in the past 18 months.

Pritesh Swamy

SIJORI WEEK 2025

4,500+ MW

Be part of the conversation with global leaders focused on the future of digital infrastructure in the SIJORI region, including Singapore, Johor, and the Riau Islands. Discover new insights and opportunities in this vital area.

SIJORI Golf

Open Batam

Padang Golf

Sukajadi, Batam

6 July 2025 Batam Interconnect World + Business Mission Trip

Batam Marriott Hotel Harbour Bay

7 July 2025 Johor Interconnect World 2025

3,000

AI-Ready with DAOU AI SUCCESS

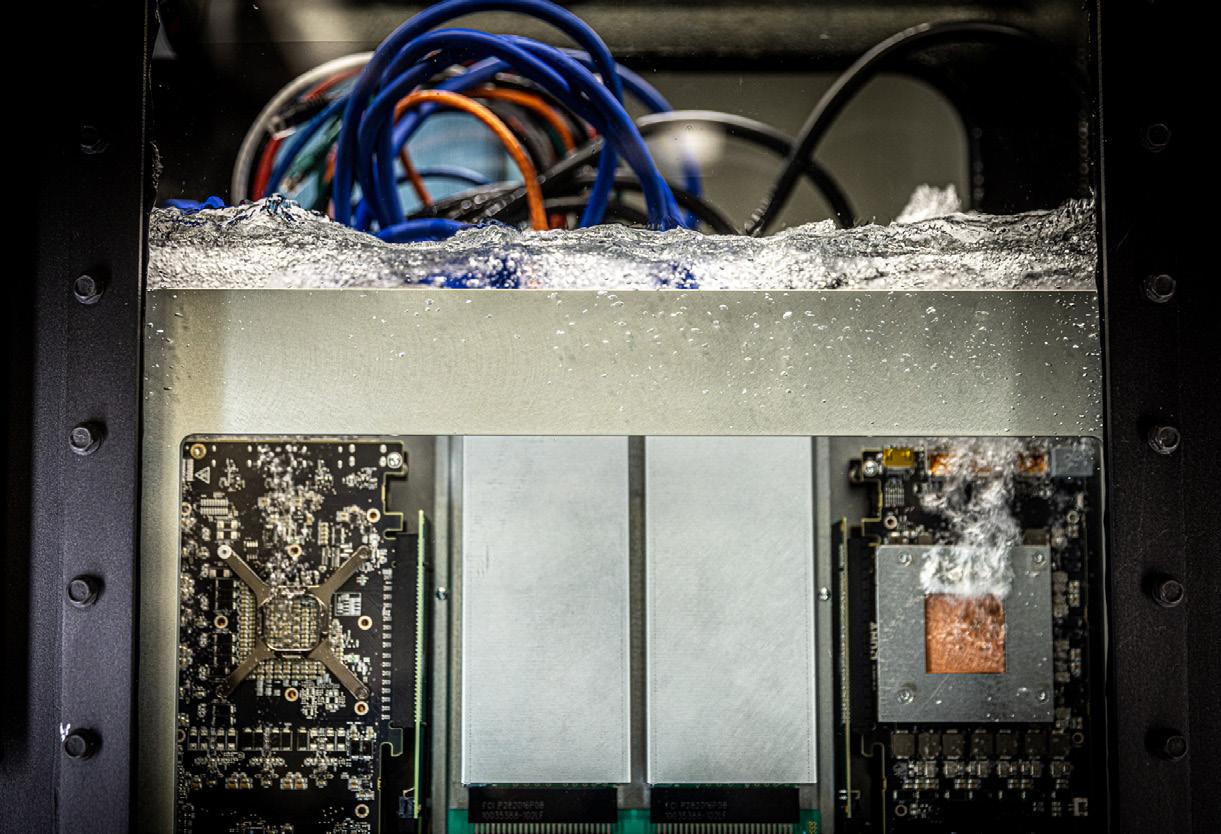

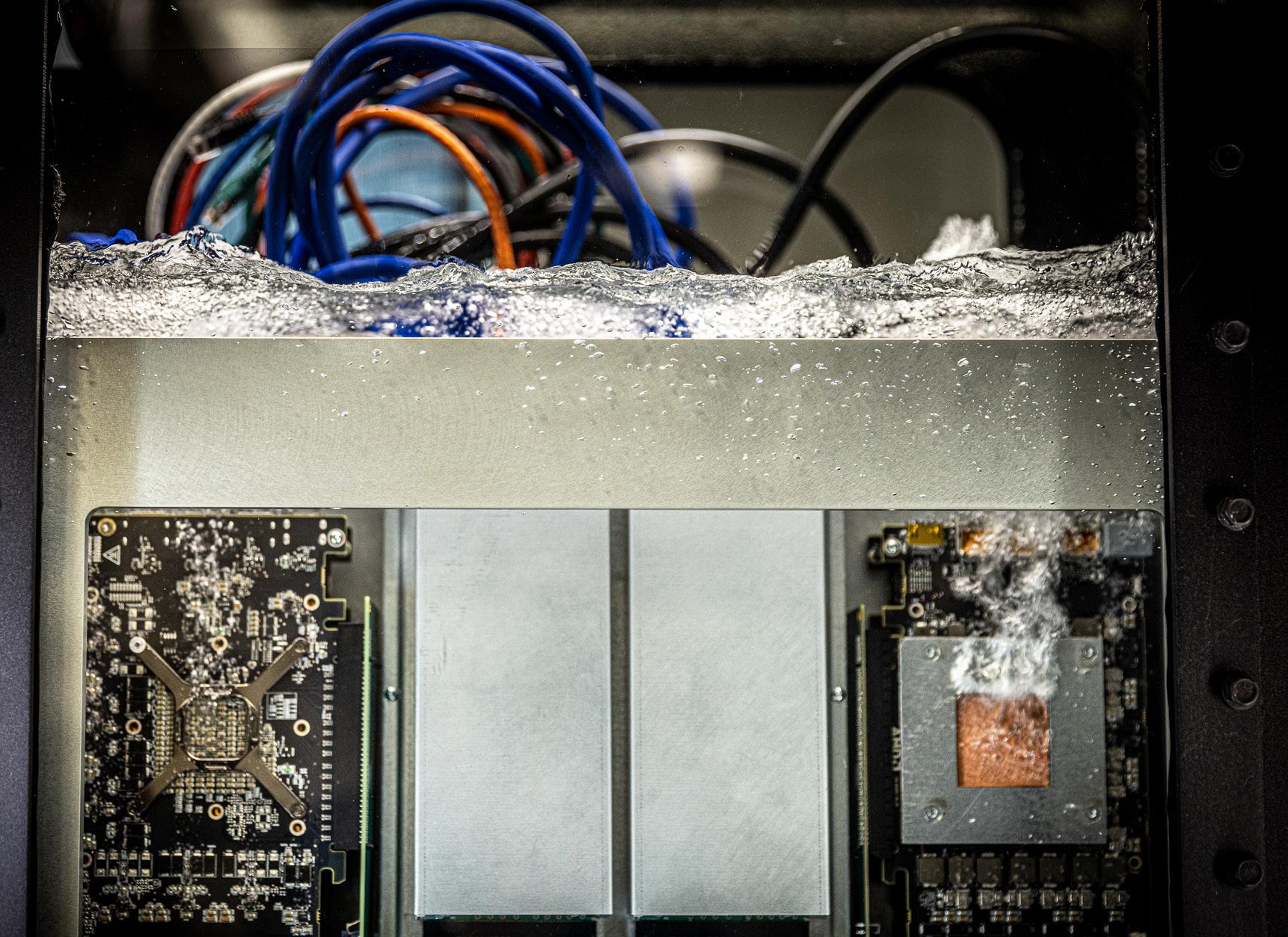

Why all roads lead to Liquid Cooling

Beyond 50kW per rack, traditional air cooling becomes impractical, both due to excessive noise and the energy demands of driving fans fast

enough to keep temperatures in check.

By Paul Mah

For decades, these facilities were optimized for traditional workloads: steady, predictable, and relatively easy to cool. But the landscape has shifted dramatically in recent years, as enterprise GPUs entered the picture and pushed power densities to unprecedented levels.

Compared to legacy compute, GPUs consume far more power and generate significantly more heat, straining the limits of traditional cooling methods. Consequently, liquid cooling, once reserved for niche, high-performance environments, is now emerging as a practical and scalable solution. Its growing role in AI deployments is now prompting a broader re-evaluation of traditional workloads that were not previously considered.

Slowly, ploddingly, then all at once

To be clear, the rise of average kilowatt per rack has been forecasted for many years. But while virtualization, hyper converged infrastructure, and later containerization did drive gradual increases, the growth was far less dramatic than many expected. Rack densities did rise – but only in small steps. According to the latest Uptime Institute survey, the average remains around 8kW per rack in 2024.

The launch of ChatGPT on the last day of November in 2022 arguably changed everything. Suddenly, the scaling law for AI, once familiar mainly to researchers, captured mainstream

Source: Adobe’s Stock

attention, as ChatGPT showed how larger models could deliver striking gains in capability. Overnight, demand for GPU deployments surged, as tech giants raced to build new data centers and stake their claim in the next era of computing.

And every new generation of GPUs draws even more power than the last. A resurgent Nvidia has helped redefine the industry, cementing its pole position with increasingly powerful GPUs. The H200, the current mainstay in most parts of the world requires up to 50kW per fully populated rack. The Blackwell-based Nvidia NVL72 supercomputer is up to 130kW. And at GTC 2025 this year, Nvidia advised

Liquid cooling is no longer optional; it’s the only viable solution.

the industry to plan for an astonishing 600kW of power per rack by 2027.

At these dizzying power densities, traditional air cooling becomes unworkable. Beyond 50kW per rack, the airflow required becomes impractical, both due to excessive noise and the energy demands of driving fans fast enough to keep temperatures in check.

Liquid cooling is no longer optional; it’s the only viable solution. Accordingly, liquid cooling is being built into AI data centers designed to power the next generation of AI models.

The rise of liquid cooling

Unsurprisingly, this shift has spurred a wave of new systems purpose-built to support liquid cooling at higher rack densities. At the same time, the industry is beginning to reconsider liquid cooling’s role in non-AI environments. Inference workloads are also moving beyond hyperscalers and into traditional data centers, driving rack densities higher and bringing new cooling demands with them.

This broader applicability has fueled a rapid expansion of liquid cooling technologies, each designed to suit different deployment models and operational requirements. So, what are the viable options available today? Several types of systems are now on the market, each with its own trade-offs in complexity, efficiency, and ease of integration.

• Rear door active cooling (RDHx): Uses a liquid-cooled heat exchanger mounted on the server rack’s rear door to remove hot air before it enters the room.

• Direct to chip cooling: Circulates coolant through cold plates

mounted directly on CPUs and GPUs, efficiently extracting heat at the source inside the server.

• Immersion cooling: Entire servers are submerged in dielectric fluid, allowing heat to dissipate passively or actively without using traditional air-based cooling systems.

• As with any technology, cooling efficiency is just one part of the equation. Cost, compatibility with existing infrastructure, maintenance needs, and total cost of ownership all play a role. While immersion cooling offers the highest efficiency, it comes with significant upfront investment and requires careful preparation of equipment for both deployment and servicing. RDHx, on the other hand, is well-suited for retrofits but has limits in how much heat it can effectively manage.

Handle with care

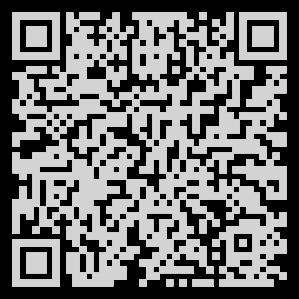

To be clear, liquid cooling isn’t a silver bullet for every data center. While it offers undeniable advantages at high power densities, it introduces a new set of engineering and operational challenges. For one, it tends to be more expensive and complex to install and maintain. Servicing is also less straightforward than with air-cooled systems, often requiring additional care and longer downtimes.

Over time, even microscopic particles can damage pumps, clog microchannels, or trigger corrosion.

There is the added risk of leaks. Even with well-designed systems, the presence of liquid in close proximity to sensitive electronics requires cautious handling. Contamination is another major concern. Installation and retrofitting work inside a data center can introduce metal shavings, construction debris, or lubricants into the system. Over time, even microscopic particles can damage pumps, clog microchannels, or trigger corrosion. These problems are often difficult to detect early and can be costly to resolve once they appear.

Managing liquid differs significantly from traditional air cooling. It calls for a shift in operational responsibilities, including the need to maintain coolant quality, adopt shared procedures across facilities teams and IT, and provide cross-training for operators and technical staff. In some environments, these added complexities may outweigh the benefits; the decision to adopt liquid cooling should therefore be based on clear operational needs

Source: Rittal

Rather than full-scale replacement, operators are layering liquid cooling into existing environments where it delivers clear value, typically for AI clusters and other high-density workloads. Etlsewhere, air cooling continues to perform reliably.

Designed for what’s next and what’s now

This is why a hybrid approach is taking hold. Rather than fullscale replacement, operators are layering liquid cooling into existing environments where it delivers clear value, typically for AI clusters and other high-density workloads. Elsewhere, air cooling continues to perform reliably. This pragmatic stance reflects both economic reality and operational caution, allowing organizations to leverage the benefits of liquid cooling where needed most while avoiding unnecessary disruption to established infrastructure.

center in Jakarta is taking a similar approach, allocating specific areas for high-density deployments.

This zoned model gives operators the agility to scale liquid cooling adoption over time while keeping proven air-cooled systems in place where appropriate. It provides teams with the opportunity to build up operational expertise gradually, rather than having to manage an abrupt shift across the entire facility. As infrastructure demands evolve, data centers can be adapted without requiring a complete overhaul.

In the long run, as AI workloads grow more complex and rack densities continue to rise, the case for liquid cooling will only strengthen. Whether adopted gradually through hybrid builds or embraced in purpose-built high-density zones, the direction of travel is clear. For those shaping the future of infrastructure, all roads increasingly lead to liquid cooling. Source:

Despite the growing momentum behind liquid cooling, air cooling will remain the default for most non-AI data centers in the near term. Much of that comes down to familiarity. Air cooling is well understood, widely deployed, and supported by a mature ecosystem of systems and tools. The risks are fewer, with concerns like leaks or fluid contamination largely off the table.

In new builds, flexibility is now a design priority. Increasingly, data centers are being constructed to support both air and liquid cooling, with different floors or halls optimized for different workload profiles. For example, Empyrion Digital’s upcoming KR1 facility in Seoul will have some levels designed for traditional air cooling, while others support liquid-cooled infrastructure. The SM+ SMX01 data

Can liquid cooling aid India’s tryst with a new destiny?

“Long years ago, we made a tryst with destiny…” said India’s first Prime Minister Jawaharlal Nehru, in a historic speech delivered on the eve of its Independence in 1947. Now, three quarters of a century later, India is poised to embrace its new destiny as a hub of modern technology and communications.

By Deborah Grey

Today India accounts for over 1GW of data center capacity, and even that falls miserably short of the demand generated by its 1.4 billion tech savvy citizens who account for one of the largest user bases of smart phones, using apps to cater to every need from grocery delivery to booking cabs to online shopping every day. India has also emerged as one of the fastest adopters of AI, and the demand for High Performance Computing (HPC) is also growing. This makes it imperative for its data centers to find innovative ways to effectively manage the considerably greater amount of heat generated by AI and HPC workloads.

But given India’s tropical location, and climate change induced extreme weather events such as heat waves that have become increasingly frequent, this is easier said than done with just traditional air-based cooling or even using water for heat removal.

CRACking the cooling code

In a geographically diverse country like India, favourable ambient temperature is present only in the northern and mountainous regions, where it is usually unfeasible to build data centers due to uneven terrain and seismic activity. The rest of the country has average temperatures ranging from 28 to 32

degrees Celsius, and these can go upwards of 40 degrees Celsius during summer. This can put a lot of pressure on air-based cooling systems in data centers.

Moreover, traditional air-cooling systems such as using computer room air conditioning (CRAC) units and airflow management techniques often require more space to accommodate raised floors, air ducts etc. Additionally, air cooling is less energy efficient, especially for high-density computing environments.

Meanwhile, liquids have higher thermal conductivity than air, meaning they conduct heat up to 1,000 times better than air, making them far more efficient in cooling high-power processors. Moreover, by eliminating the need for excessive air conditioning, liquid cooling lowers operational costs in the long run. Additionally, liquidcooled systems require fewer air ducts and cooling units, enabling more compact and efficient data center designs.

Chemours technical manager explaining liquid cooling heat transfer process using Opteon™ 2P50 dielectric fluid in Chemours immersion cooling lab|Image courtesy: Chemours

Water, water, (not) everywhere…

Now, the first liquid that comes to mind is water, and for decades using water has been a popular heat management technique across the world. But India’s ground realities such as water scarcity, as well as its inherent limitations are fast making this technique unviable. Even if one were to switch to recycled water, that too requires investments into recycling infrastructure, and then building and maintaining the apparatus that brings the recycled water to the data center. Other alternatives are also just glorified bandaid solutions in the long run.

“The industry has already begun moving to direct-to-chip cooling using water, glycol, and additives to remove heat directly from components. While this solution works for now, water also has physical limitations; as chips get hotter and the required water temperatures get lower, this technology would become increasingly impractical,” says Dhruv Varma, AP Liquid Cooling Business Development Leader, Chemours. “As the number of components requiring liquid cooling inside a server increases, we expect the industry to continue evolving from this spot-cooling approach to consider alternative liquid cooling solutions, such as two-phase direct-to-chip and immersion cooling.”

Therefore, India’s data centers are considering dipping their toes into

the new and exciting world of Liquid Cooling.

What do the numbers say?

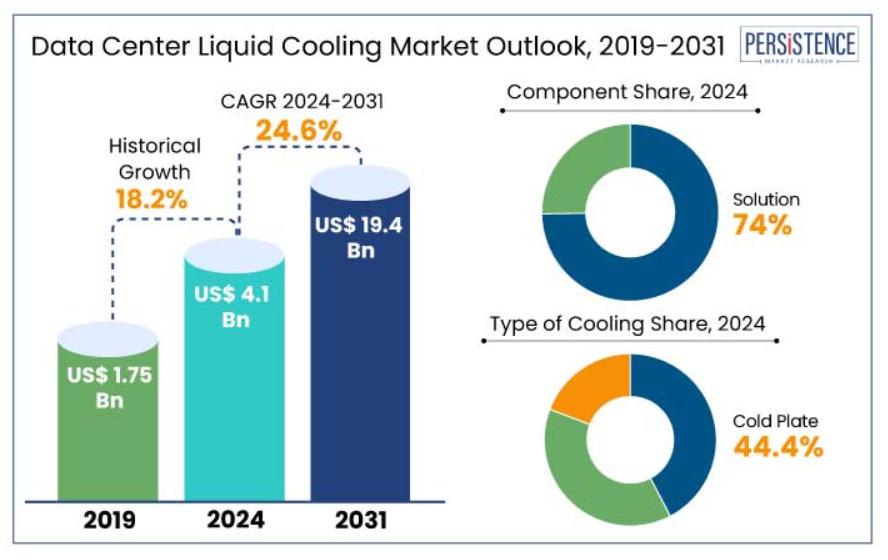

According to Persistence Market Research’s Data Center Liquid Cooling Market report, the global data center liquid cooling market is set to grow from US$ 4.1 billion in 2024 to US$ 19.4 billion by 2031, at a Compounded Average Growth Rate (CAGR) of 24.6 percent. Increasing data center density, demand for energy efficiency, and high-performance computing are driving adoption. Liquid cooling is 40 percent more energy-efficient than air cooling, making it ideal for hyperscale data centers, AI, and cloud computing.

Trends are similar in India as well.

“The India Data Center Cooling Market size is estimated at US$ 2.38 billion in 2025, and is expected to reach US$ 8.32 billion by 2031, at a CAGR of 23.21 percent during the forecast period (2025-2031),” says Mordor Intelligence in its India Data Center Cooling Market Size & Share Analysis Report (2025-2031).

The report further explains the reasons behind this enthusiastic adoption saying, “Direct liquid cooling (DLC) solutions consistently achieve impressive partial power usage effectiveness (PUE) ratings, typically ranging from 1.02 to 1.03. This places them ahead of even the most efficient air cooling systems, surpassing them by a slight margin, usually in the low single-digit percentage range.”

“As AI workloads push the boundaries of thermal design and power density, liquid cooling enables us to achieve superior energy efficiency and thermal control. It significantly reduces PUE and supports sustainability goals by lowering our carbon footprint.”

Chatterjee, Managing Director & Head, Data Centre, India, CapitaLand Investment

Liquid Cooling adoption in India

“As AI workloads push the boundaries of thermal design and power density, liquid cooling enables us to achieve superior energy efficiency and thermal control. It significantly reduces PUE and supports sustainability goals by lowering our carbon footprint,” says Surajit Chatterjee, Managing Director & Head, Data Centre, India, CapitaLand Investment. “While air cooling will remain relevant for traditional loads, we see liquid cooling becoming the default for high-density, performance-intensive environments.”

Even manufacturers of modular data centers are looking to incorporate liquid cooling in their designs.

“One of the primary advantages of modular data centers is their ability to incorporate advanced cooling technologies like direct-to-chip liquid cooling, immersion cooling, rear door heat exchangers etc.,” says Anjani Kumar Kommisetti, Head of Business, Rhine XCircle. “These technologies can be deployed more effectively in a modular setup, offering precise temperature control and lowering energy consumption, which directly reduces the carbon footprint.”

Surajit

Persistence Research Data Gfx

“As the number of components requiring liquid cooling inside a server increases, we expect the industry to continue evolving from this spotcooling approach to consider alternative liquid cooling solutions, such as two-phase direct-to-chip and immersion cooling.”

Choosing the right cooling mix

There are already a variety of solutions for users with different needs and conditions. While some are opting for Immersion Cooling, where entire servers are immersed in a dielectric fluid, others are looking at precision cooling where the cooling fluid is directed to specific parts of the server that need cooling. Direct to chip cooling where fluid is directed to the heated chip has emerged as a popular method of cooling. So how do you choose the right cooling method for your data center?

“An optimised cooling mix, using direct-to-chip liquid cooling for dense AI clusters, combined with enhanced air cooling for general-purpose IT loads, ensures operational flexibility and energy optimisation,” says Surajit

Chatterjee. “The ideal blend depends on workload types, rack densities, and sustainability targets, and we continuously calibrate our designs to align with evolving customer and environmental needs.”

“In today’s landscape, the application defines the chips and the hardware, which in turn define what type of infrastructure may be needed to support that hardware and hence application. As a result, facilities teams need to look at their organization’s technology roadmap to better anticipate what type of hardware they may need in the future,” says Dhruv Varma. “The power density of the chips and the hardware, in addition to any anticipated constraints of space, power, water, location, and budget should all be factored in while picking what’s right for you,” he advises.

Dhruv Varma, AP Liquid Cooling Business Development Leader, Chemours

Floating data centers promise to address land, power, and cooling woes.

By Jan Yong

The idea of floating data centers has been bobbing around for some time now.

The latest announcement of a floating data center about to be built off Yokohama in autumn 2025 has people excited again. Although only a Memorandum of Understanding (MOU) has been signed by a consortium of Japanese companies, the prospect of an offshore floating data center utilizing 100% renewable energy is looking very bright indeed.

The parties to the MOU, Nippon Yusen Kabushiki Kaisha, NTT Facilities, Eurus Energy Holdings Corporation, MUFG Bank, and the city of Yokohama, are looking to build an experimental green data center that they have described as the world’s first offshore floating green data center.

More than cooling

To be built on a mini float or “floating berthing facility”, the demonstration project would be initially powered by both solar and battery energy, to be

supplemented later with wind power. If successful, further developments in the waterfront and sea areas of Yokohama port would be explored. According to Eurus’ press release, this project would set new standards for future data centers which are envisioned to operate entirely on renewable energy and emit no greenhouse gases during operation.

The future data centers would ideally utilise offshore wind power by being situated near offshore wind farms to maximise off-grid use of electricity. It would also eliminate the challenges of onshore data center construction, such as shortages of land and construction contractors, as well as extended construction lead times.

Globally, data centers face four structural bottlenecks: land scarcity – especially in urban and coastal regions – power grid limitations, water shortages and climate risk such as earthquakes, floodings and temperature fluctuation. The floating data centers offer a potential solution to all these challenges.

In addition, its modular construction allows for flexible deployment. The container-like modular design is optimised for

salt-resistance, modularity and rapid deployment. The floating data center would be monitored real time on temperature, humidity, vibration, energy stability, and uptime. Energy storage and cooling redundancy are retained to maintain autonomous operations.

Globally, data centers face four structural bottlenecks: land scarcity – especially in urban and coastal regions – power grid limitations, water shortages and climate risk such as earthquakes, floodings and temperature fluctuation. The floating data centers offer a potential solution to all these challenges.

Singapore’s floating data center

Meanwhile, Singapore’s own experimental floating data center project, a first on the island nation, is still in the preparatory stage. The Keppel Data Centres’ Floating Data Centre Park (FDCP) project aims to alleviate land, water and energy constraints of traditional data centres. Similar to the Yokohama debut model, the FDCP also features a modular design and aims to harness seawater for cooling, thereby increasing cooling efficiency by up to 80%, by their estimate. Indeed, the

Architectural image of Keppel Floating Data Centre Park

Source: Keppel

proposed seawater district cooling system will be 10 times larger than the largest built in the world.

The planned floating data center also avoids the use of potable or industrial water in cooling towers and is envisioned to optimize energy usage by integrating LNG and possibly hydrogen infrastructure for onsite power generation.

In conclusion, a floating data center may be preferable if cooling efficiency,access to renewable energy, or coastal proximity are critical. They also help when land is costly or scarce, and maritime risks are manageable. These factors apply to Yokohama and Singapore, and could benefit other coastal regions too. Whether this becomes the standard model for future data centers is still uncertain. Key challenges remain, especially in maintenance and reliable renewable power.

Architectural image of Eurus-led floating data center off Yokohama

Comparison between floating and land-based data centers

Cooling Efficiency

Renewable Energy Integration

Land & Building costs

Connectivity

Disaster Resilience

Security

Environmental Concerns

Engineering and Maintenance

Legal Issues

Floating DC

Utilise the surrounding sea as a heat sink for cooling and hence reducing treated water consumption.

Potential synergy with offshore wind, tidal, or wave energy sources

Avoids high land costs in urban/coastal areas while modular designs may offer scalable & cost-effective expansion

Placement near coastal cities can reduce latency issue and improve connectivity.

Less vulnerable to land-based risks e.g., earthquakes, floods but must withstand maritime hazards e.g. storms, tsunamis & saltwater corrosion.

Physical isolation may deter unauthorized access but vulnerable to maritime threats e.g. piracy, collisions.

Discharging warm water could harm marine ecosystems.

Higher initial costs for marine-grade infrastructure (corrosion-resistant materials, stabilization systems) while maintenance requires specialized marine access.

Jurisdictional ambiguities in international waters and compliance with maritime/environmental regulations add complexity.

Land-based DC

Higher energy expenditure for cooling, especially in warm climates, unless using geothermal, etc.

Depending on location, wind and solar can be harnessed.

Space constraints & high land costs in urban areas while environmental impact from land-use changes (e.g., habitat disruption). But established construction practices and infrastructure reduce upfront investment.

Reliable grid connections and terrestrial fiber networks ensure consistent operation.

Susceptible to earthquakes, floods, or wildfires, depending on location

Tight 24-hour security is possible with state-of-the-art equipment.

Not an issue so far.

Accessible for repairs, maintenance, and physical security measures without marine logistics.

Clear compliance with local laws, data sovereignty requirements, and environmental standards.

Source: Eurus

The science of monitoring data center airflows

By Paul Mah

Data center deployments are often messy.Real-world deployment conditions rarely mirror what we envision on paper. And as new equipment is swapped in or server utilisation changes over time, assumptions and conditions that once worked might no longer reflect new operational realities.

It doesn’t help that rack densities are slowly but inexorably rising. A decade ago, the typical workload drew around 3kW per rack. Today, that figure has jumped to an average of 8kW, according to the 2024 Uptime Institute survey. And with the rise of AI workloads, demands are set to grow even steeper. AI training and inference rely on high-performance GPUs, with the latest servers consuming up to 50kW per rack, and in the case of Blackwell deployments, even hitting 130kW.

Removing the guesswork

Traditional air-cooling strategies, including hot aisle and cold aisle layouts as well as containment techniques, are increasingly struggling to keep up. On paper, everything might look good: airflow simulations, power estimates, cooling layouts. But reality rarely follows the script. As rack densities climb and workloads grow more complex, data centers become hotter, more unpredictable, and far harder to manage. One of the biggest challenges is the lack of real-time visibility into airflow. Without accurate, continuous measurements, operators are left to rely on guesswork or theoretical models that may no longer apply. What if we could take this guesswork out of the equation – even in live production environments? That’s one of the premises behind EkkoSense Critical, a cloud-based data center management platform. It brings together advanced analytics, machine learning, and integration with both its proprietary and existing sensor

infrastructure to give operators a realtime view of thermal performance.

Rather than relying on static designs, data center teams can now respond to airflow changes to adjust cooling strategies. This reduces inefficiencies, improves sustainability, and shifts operations from reactive maintenance to proactive optimization. Operators can move beyond reactive maintenance and toward proactive optimization to target the right zones, at the right time, and with the right amount of energy.

Robert Linsdell, APAC general manager at EkkoSense, says the platform has delivered average power savings of 15%. He explains that EkkoSense uses repurposed video game platforms combined with dense instrumentation to visualise airflows within data halls or rooms using easyto-understand colour codes. For a data hall with between 100 and 150 racks, it takes just a day to build the model, two days to instrument, and one day to go live, he says.

When data meets thermal reality

One of the most powerful features of advanced telemetry, as shared by Peter Simon, technology lead for EkkoSense APAC during a presentation at the Sydney Cloud & Datacenter Convention last year, is its ability to replay the thermal state of a room at any point in time. With everything recorded, operators can roll back to a specific date to see exactly what was happening: airflow patterns, cooling effectiveness, and even potential risks. “It’s like having a thermal time machine,” he said.

This before-and-after comparison allows data center teams to visualise improvements, troubleshoot anomalies, and defend service-level agreements with hard evidence. Issues that previously went unnoticed, such as reversed airflow, blanking panels left ajar, or underperforming containment, can now be flagged, diagnosed, and resolved quickly.

Perhaps the most surprising aspect of the solution is its simplicity. It consists of sensors strategically positioned across the data hall, paired with a

suitable number of controller units. Once installed, data collection begins immediately, giving facility managers the ability to monitor live changes in real time – and do so remotely. This enables timely interventions when something goes wrong and gives operational teams a clear, continuous view of conditions that were previously hidden. As a result, cooling is no longer managed on assumptions but on insight, shifting responses from reactive to precise.

Smarter airflow monitoring promises a lot: real-time insight, datadriven precision, and the potential to unlock significant energy savings. But like many innovations in the data center world, its impact will ultimately depend on execution. Sensors and dashboards alone won’t fix airflow inefficiencies unless operational teams are willing and equipped to act on what the data shows.Even so, the broader trend points in a promising direction. As workloads grow denser and cooling margins tighter, tools that help make the invisible visible are a welcome step forward. If nothing else, they give operators a fighting chance to do more with less. And in today’s landscape, that may be the most crucial advantage of all.

Peter Simon demonstrating EkkoSense at Sydney CDC 2024.

Powering possibilities: The role of Data Centers in Cloud and Hybrid evolution

Blending on-premise infrastructure with cloud platforms, hybrid clouds offer a bespoke solution that strikes the perfect balance between performance, cost, and security.

By Rohan Sheth, Head, Colocation, Data Centre Build and Global Expansion, Yotta

Every moment we send a message, stream a video, or place an online order, we tap into a vast, hidden network that connects our world. In the background, data centers power these links, unlocking the explosive growth of cloud services and the seamless integration of hybrid environments.

Today, data centers are much more than mere storage facilities – they propel the evolution of the digital economy. This industry is currently experiencing unprecedented growth across both advanced and developing economies. Take India, for instance; CareEdge Ratings projects that India’s data center capacity will double to approximately 2,000 MW by 2026, making the nation a key player in the global data center market.

Fueling the cloud revolution

The global cloud market is currently valued at $1.2 trillion and none of this

would’ve been possible without data centers. After all, data centers form the physical foundation that empowers cloud platforms to scale effortlessly, delivering flexibility and innovative solutions to businesses across the planet. This scalability allows cloud providers to accommodate varying workloads and user demands efficiently.

In recent years, their capabilities have further enhanced, especially with the integration of artificial intelligence and machine learning. AI-powered automation optimizes resource allocation and energy consumption, resulting in more efficient operations.

In practical terms, this is transforming multiple sectors: in healthcare, for example, data centers combined with AI can rapidly analyze patient data for quicker diagnoses and enable telemedicine in remote areas; in finance, advanced infrastructure underpins real-time transaction processing and sophisticated fraud detection; and in education, scalable cloud platforms support personalized

learning experiences for millions of students worldwide.

The best of both worlds

The advent of the cloud significantly altered the IT landscape; however, it is the rise of hybrid environments that is truly redefining how businesses optimize their operations. Blending on-premise infrastructure with cloud platforms, hybrid clouds offer a bespoke solution that strikes the perfect balance between performance, cost, and security. This model allows critical data to remain on-premises while leveraging the scalability cloud environment offers for fluctuating workloads, ensuring optimal performance.

From a broader perspective, it helps balance capital and operational expenses, which can help businesses stretch the lifecycle of existing infrastructure while avoiding overinvestment.

Hybrid clouds also improve resilience, offering seamless workload distributions during outages while allowing

Today, data centers are much more than mere storage facilities—they propel the evolution of the digital economy while driving innovation and efficiency.

innovation to thrive and supporting rapid development in the cloud without disrupting core operations.

Hybrid environments unlock the avenues for future technologies such as edge computing, where real-time data processing happens locally while leveraging cloud analytics for broader insights. Even though managing a hybrid model demands robust tools and strategies, its adaptability makes it essential for organizations looking to drive agility, innovation, and growth.

What’s

in it for business leaders

For business leaders, the integration of data centers and cloud technologies presents both opportunities and challenges – they can help reduce the time-to-market for new products with scalable resources for rapid prototyping and testing and foster a culture of innovation for the organization. With a robust and scalable infrastructure, customers can have seamless interactions with digital platforms, boosting satisfaction and loyalty.

Early adopters of advanced technologies can gain a considerable edge over competitors by bettering operational efficiency and enabling novel business models. Advanced analytics and AI capabilities made possible by modern data centers can offer actionable insights, empowering business leaders with better decisionmaking and strategic planning.

However, the journey to getting there is cluttered with obstacles.

Navigating the transition

For an effective transition to cloud services and hybrid environments, careful planning and execution is imperative. It starts by developing a comprehensive IT strategy that aligns with business goals. This includes assessing current infrastructure, identifying existing gaps, and charting out clear objectives for migration.

Additionally, investing in training programs to upskill existing staff while attracting new talent proficient in cloud technologies, data analytics, and cybersecurity is equally important. What’s also critical is implementing robust risk management practices. These measures help address potential security threats while ensuring compliance with data protection laws and other regulations.

Lastly, collaborating with reputable cloud service providers and data center operators can help unlock expertise and support throughout the transition process, moving past the risks that often engulf such transitions.

The road ahead

The next 10 years will see hyperscale facilities evolve to support the growing demand for AI, machine learning, and resource-intensive workloads. We will also witness the rapid proliferation of smaller, edge data centers, which will

reduce latency and support applications such as 5G and the Internet of Things (IoT). This shift towards both hyperscale and edge data centers will cater to diverse needs while enhancing performance across industries.

Moreover, AI and machine learning will play a central role in the operation of data centers, from optimizing power consumption and cooling systems to enabling predictive maintenance and resource allocation. The incorporation of sustainable practices such as renewable energy, liquid cooling, and waste heat recycling will drive the green revolution within data centers, making them more eco-friendly and energy-efficient.

As data centers become smarter and more autonomous, we will see the rise of self-healing infrastructures, capable of predicting and correcting failures with minimal human intervention. Modular, prefabricated data centers will also become more common, enabling rapid deployment and scaling in remote locations and catering to businesses with specific needs. At the same time, compliance with local data sovereignty laws will push for more localized data storage and more stringent data protection measures.

The next decade will see data centers evolve to become smarter, more resilient, and greener, supporting a vast array of applications across sectors.

Shaping the global digital infrastructure landscape

As global demand for data storage, AI workloads, and cloud services continues to rise, Malaysia has emerged as a key player in Southeast Asia’s data centre market.

By Renee Ho, Director,

The increasing need for highperformance computing infrastructure to support AI-driven innovation is accelerating investments in digital infrastructure. Guided by the National Investment Aspirations (NIA), the country prioritizes highvalue sectors such as Electrical & Electronics, the Digital Economy, and Pharmaceuticals, positioning itself as a regional hub for future-ready technologies and investments.

In Malaysia, the Malaysian Investment Development Authority (MIDA) and the Malaysia Digital Economy Corporation (MDEC) play a crucial role in facilitating both foreign and local digital investments. As part of this initiative, the Data Centre Task Force (DCTF), co-chaired by International Trade and Industry (MITI) Minister Tengku Datuk Seri Zafrul Tengku Abdul Aziz and Digital Minister Gobind Singh Deo, addresses industry concerns, plans investment strategies, and ensures sustainable growth in

the data centre sector. The DCTF will introduce policies to streamline data centre development and improve coordination within the ecosystem. The government also provides incentives, regulatory facilitation, and a supportive environment to boost digital investments and growth.

Digital infrastructure investments and milestones

Since 2021, the government has approved 21 data centre projects under the Digital Ecosystem Acceleration Scheme, totaling USD23.9 billion in investment. Foreign investment remains the primary driver, contributing 90% (USD21.5 billion) of the total, with the remaining 10% (USD2.4 billion) coming from domestic sources.

Several high-profile projects have propelled Malaysia’s data centre industry forward. The rise of hyperscalers began in 2022, marked by Bridge Data Centres launching its first phase in Johor, with ByteDance as the anchor tenant, solidifying the region’s status as a hub for multinational corporations. Johor, catering primarily to regional markets, complements Greater Kuala Lumpur, which serves the growing domestic demand for digital infrastructure. Since then, Malaysia has attracted data centre investors from both the East and West, including major players such as DayOne (previously known as ‘GDS’), Princeton Digital Group, Yondr, and others— reinforcing the country’s position as a digital infrastructure hotspot in Southeast Asia.

In 2024, technology giants like Oracle, Amazon, Google, and Microsoft are setting up cloud regions in Malaysia, reflecting the country’s growing significance in the digital economy. This influx of major players is driven by the increasing demand for AI Infrastructure as a Service, spurred by the rapid advancements in Generative AI (GenAI) technologies. Johor, in particular, is experiencing a data centre boom, largely fueled by multinational corporations with regional operations, while other parts of Malaysia focus on meeting domestic demand.

Government policies and incentives

Malaysia combines fiscal and nonfiscal incentives to support digital infrastructure investments. The Digital Ecosystem Acceleration (DESAC) Schemes provides significant tax relief for promoted digital activities, offering up to 10 years tax incentive based on value of investments or lower corporate tax rate. Notably, DESAC takes a holistic approach to digital infrastructure development—beyond data centres and cloud infrastructure, submarine cable landing stations are also recognized as activities qualify for tax incentive. This inclusion reflects the government’s recognition that robust and secure global connectivity is essential to supporting Malaysia’s digital ecosystem.

Furthermore, the Malaysia Digital Status provides a range of tax and non-tax incentives, such as duty-free importation and sales tax exemptions for multimedia equipment, unrestricted employment of foreign knowledge

Deloitte Malaysia

workers, 100% foreign ownership of local entities, and the ability to source funding and raise capital internationally, enhancing the country’s appeal to investors.

Balancing FDI and sustainability

Sustainability is increasingly central to Malaysia’s approach to attracting foreign direct investment (FDI), particularly in the digital infrastructure sector. The government encourages alignment with ESG principles, integrating economic, social, and environmental factors into investment planning. While Malaysia provides a strong framework for digital infrastructure investments, ensuring long-term sustainability requires navigating challenges such as regulatory complexities, cost thresholds, and evolving guidelines— especially in Johor, which has become a key destination for data centre investments. To facilitate coordinated and sustainable growth, the Johor state government, in partnership with PLANMalaysia Johor, introduced the Johor State Data Centre Development Planning Guideline in June 2024 to better manage and facilitate data centre activities in the region.

In addition to incentives, the Malaysian government ensures that growth aligns with sustainability by addressing the resource-intensive nature of data centre investments. The launch of the Guideline for Sustainable Development of Data Centres in December 2024, alongside the Digital Ecosystem Acceleration (DESAC)

scheme, aims to attract high-quality digital infrastructure projects while promoting responsible development. The guidelines focus on minimizing energy, water, and carbon footprints of data centres, particularly given the sector’s high resource demands with key sustainability metrics, such as Power Usage Effectiveness (PUE), Water Usage Effectiveness (WUE), and Carbon Usage Effectiveness (CUE), benchmarked across data centre categories like colocation and hyperscalers, reinforcing Malaysia’s leadership in sustainable digital infrastructure.

The Johor-Singapore SEZ

The Johor-Singapore Special Economic Zone (JS-SEZ) represents a strategic convergence of infrastructure, policy, and cross-border cooperation— poised to become a leading node in Southeast Asia’s digital infrastructure landscape. Adjacent to Singapore, one of the world’s most mature data centre markets, JS-SEZ offers a natural extension of regional capacity by blending Singapore’s global connectivity and operational excellence with Malaysia’s land availability, skilled talent pool, and cost competitiveness.

This synergy positions JS-SEZ as a regional data centre powerhouse— not just in terms of hosting capacity, but also through the development of end-to-end digital infrastructure components. Johor is seeing increased localization of the value chain, with the establishment of server rack manufacturing (e.g., Wiwynn

Malaysia, along with its regional partners, is poised to lead Southeast Asia’s digital transformation, positioning the region as a significant player in the global digital infrastructure landscape

Corporation’s plant), renewable energy investments, and mechanical, electrical, and plumbing (MEP) engineering capabilities like TECO Electric & Machinery Co.’s acquisition of NCL Energy Sdn Bhd.

Looking forward, the adoption of advanced technologies such as battery energy storage systems (BESS) will further enhance energy resilience and sustainability. These developments collectively reinforce the JS-SEZ’s role as a pivotal regional gateway—powering the next wave of AI-ready, sustainable, and globally connected data centre solutions in Southeast Asia.

Malaysia, along with its regional partners, is poised to lead Southeast Asia’s digital transformation, positioning the region as a significant player in the global digital infrastructure landscape. The expanding digital economy, supported by robust government policies and strategic investments, creates abundant opportunities for investors and operators. This holistic vision of a digitally connected and sustainable Southeast Asia offers immense potential to shape the future of the global digital economy.

Raising the bar for AI infrastructure in Asia

Building a new generation of AI-ready data centers

The data center landscape in Asia Pacific is dynamic and rapidly expanding, with the market projected to reach an estimated US$4 trillion by 2030[1]. Driving this trajectory is intensifying digitalization, the rise of cloud computing, and a sharp increase in data consumption – further amplified by emerging technologies like AI. With this momentum, it’s no surprise that Asia Pacific is now a global hot spot for data center investment and innovation.

In a time of such transformation and breakneck growth, what if you could design a data center from scratch? What might it look like, and how would it be different from the data centers of the past? Across the region, the opportunity to rethink digital infrastructure from the ground up is opening the door to new standards of scalability, performance and sustainability.

Engineered to be AI-ready

Founded in 2021, Empyrion Digital emerged at the cusp of Asia’s rapid data center growth. Following its acquisition of the SG1 Dodid Data Centre in Singapore that same year, the company has announced new developments in South Korea, Japan, Taiwan and Thailand. Based on its current growth trajectory, Empyrion Digital is on track to expand its panAsian platform to over 170MW of IT load across the region by the end of 2025.

Fueling this expansion is a customer-first mindset, shaped by the needs of its customers who include the major hyperscalers and enterprises. These customers prefer facilities in central business and metropolitan districts that are located in close proximity to internet exchanges, prompting Empyrion Digital to focus on sites in core Asia markets where demand is strongest.

One example of this would be the upcoming AI-ready KR1 data center located in South Korea. KR1 will be the first new data center built in over a decade within Seoul’s Gangnam area, often referred to as the Silicon Valley of Seoul – and South Korea’s future AI hub. Despite power moratoriums in place across Seoul, KR1 has secured 40MW of power to support AI-intensive workloads. This is especially significant given that many of the existing facilities in the vicinity, and within the country, are aging and unable to cope with rising demands of AI and HPC.

Empyrion has also taken a fundamentally different approach to their builds by bridging thoughtful design and sustainable operations. From power and cooling to network infrastructure, every aspect has been reimagined to shape a product that meets future demand. While it brings strong capabilities in data center development and operations, it partners with specialists in fiber connectivity, cooling and AI hardware to address market opportunities and environmental concerns. By tapping

Empyrion has also taken a fundamentally different approach to their builds by bridging thoughtful design and sustainable operations.

into these partnerships, Empyrion ensures its facilities are not only efficient but well supported by a comprehensive ecosystem that attracts and retains key customers, freeing itself to focus on delivering reliable, future-ready infrastructure.

Sustainable development

At a time when sustainability is no longer optional, how did Empyrion Digital approach the challenge? The journey began with SG1 in Singapore, a city that presents various environmental hurdles, from high humidity to limited space. Despite these constraints, SG1 achieved strong operational efficiency by optimizing water consumption and using a green wall running across two facades to lower ambient temperatures. It’s a design choice that contributed to SG1

earning the BCA-IMDA Green Mark for Data Centers Platinum certification, and achieving a stabilized PUE of 1.43 today.

Newer data centers are built on this foundation. KR1 in Seoul, for instance, uses StatePoint Liquid Cooling (SPLC), a technology that combines a liquid-to-air membrane exchanger with a closed-loop system to improve energy efficiency and reduce water consumption. The facility is also designed with AI workloads in mind – selected data halls are already fitted with piping for Direct Liquid Cooling (DLC), while others are engineered for a seamless conversion to DLC as demand grows.

Additional sustainability features include rooftop solar panels, a rainwater management system, and the use of eco-friendly construction materials. By choosing materials with a lower carbon footprint that also support recycling and contain minimal harmful substances, KR1 is designed to reduce its overall environmental impact. For now, the team is also working toward achieving

Korea’s equivalent of the Green Mark certification.

Full speed ahead

Ultimately, data center design is about matching the right technology with the right market and climate. With a relatively new but proven platform, Empyrion isn’t weighed down by legacy systems or outdated facilities that it must retrofit or upgrade. This gives the company the flexibility to move quickly and design infrastructure that supports the latest technologies from the outset.

Another key advantage lies in Empyrion’s parent group and platform, Seraya Partners. Based in Singapore and deeply focused on Asia, Seraya Partners brings a regional perspective and an emphasis on long-term infrastructure growth. They’ve also made significant investments in renewable energy storage, creating opportunities for Empyrion to collaborate with sister companies on sourcing green power, particularly in markets where both are expanding. This alignment helps bridge digital

infrastructure with sustainable energy development, a focal point for real estate and infrastructure investors

Empyrion Digital is quietly redefining what data centers in Asia’s urban cores can look like. While many players chase sprawling hyperscale campuses or stick to smaller retail colocation builds, Empyrion is carving out a niche with its wholesale facilities in central, metropolitan locations serving hyperscalers, enterprises and content delivery networks. It’s a segment that few peers are targeting, at least for the moment.

With its focus on strategic site selection, integrated design, and flexible future upgrades to support the evolving demand of AI workloads, Empyrion is raising the bar for data center development. It’s a sharper, more intentional approach to infrastructure delivery: agile, efficient, and built to scale. And with sustainability woven into every project from day one, Empyrion is setting a new benchmark for what future-ready infrastructure should be.

2025 Events Calendar

SIJORI Week 6 July

SIJORI Golf Cup Batam

SIJORI Week 7 July Batam Interconnect World Forum Batam

SIJORI Week 8 July

Johor Interconnect World Forum

Johor

SIJORI Week 9 & 10 July Open Compute Project –South East Asia Tech Day

Singapore

SIJORI Week 10 July

SIJORI Cloud and Datacenter Convention

Singapore

SIJORI Week 10 July The Future of Network Acquisition: Trends & Strategic Shifts

Singapore

SIJORI Week 12 July

SIJORI Football Singapore 24 July Big Catch up

Chi Minh

Special

Interconnect World Supplement

Inside: What lies beneath Singapore’s plan to become a premier networking hub

Sun, sand, subsea cables: The Middle East’s rise as a global digital crossroads

Discover APAC’s Connectivity Ecosystem with InterconnectWorld Asia 2025

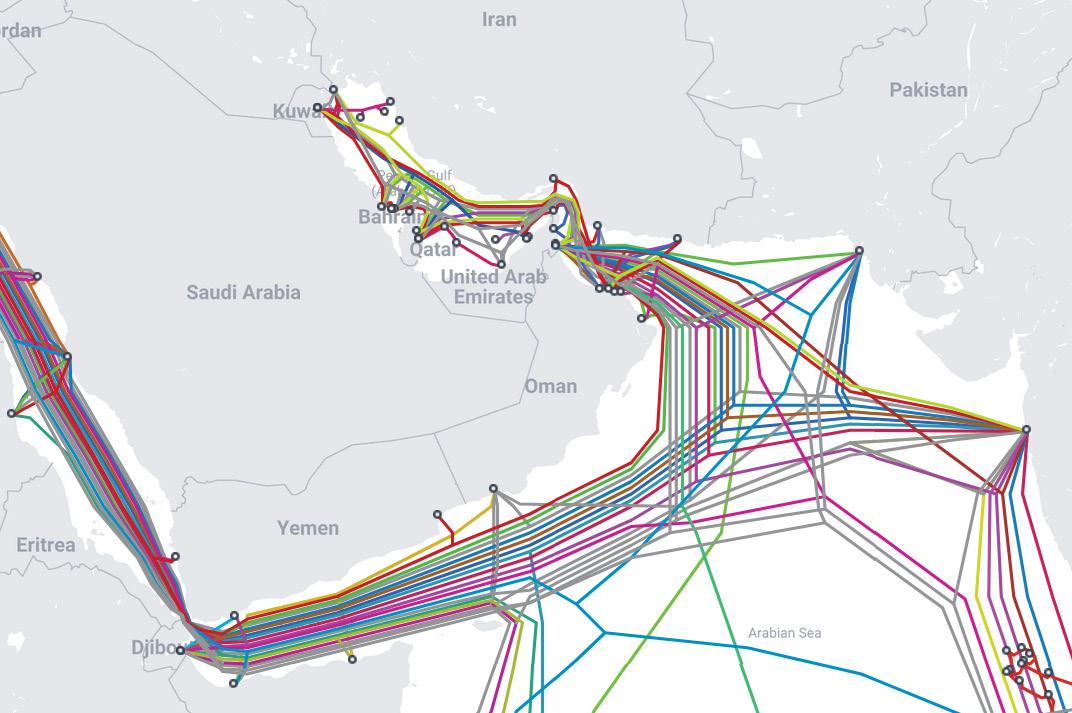

What lies beneath

The hidden mysteries of subsea cables unveiled

By Jan Yong

Subsea (or submarine) cables are a bit of a mystery to many, buried as they are under the water and silently doing their job of transmitting data traffic and power. But these cables have an outsized role in our everyday lives today. Cable outage means we cannot go online to do our work, shop, bank, email or stream movies. Many institutions and businesses including financial institutions, stock markets, and even medical care would be seriously affected. Financial institutions alone transact an estimated US$ 22 trillion per workday through these cable systems. Without them, there will be a big pause on earth.

Back in 2006, a magnitude 7.0 earthquake struck off the southwest coast of Taiwan, damaging eight submarine cables and disrupting internet services in much of the region. It took weeks to repair them, hence exposing the urgent need for a diversity of routes and improvements in the safety and resiliency of the cables to avoid similar disruptions in future.

For such a critical piece of infrastructure, little is known about them. So, we have prepared a primer here to shed some light into this hidden world.

Subsea cables are specially engineered cables laid on or buried beneath the ocean floor. They are designed to transmit data, voice, and increasingly, electrical power over vast distances between continents and islands. They are typically made of fiber-optic cables that convert electrical signals into pulses of light, enabling rapid and high-capacity data transmission. The other type of subsea cables transmit electrical power, often used for connecting offshore renewable energy installations (like wind farms) to onshore grids.

Specialized cable-laying ships

Domestic Submarine Cable of Maldives (DSCoM) invested by telecommunication companies Dhiraagu and Ooredoo lands on the shores of Hulhumale’, Maldives.

Cable Components

Subsea cables are specially engineered cables laid on or buried beneath the ocean floor. They are designed to transmit data, voice, and increasingly, electrical power over vast distances between continents and islands.

deploy the cables along predetermined routes, often burying them under the seabed to protect against fishing gear and anchors. Prior to that, engineers will select routes based on seabed geology, risk factors, and environmental considerations.

The cables require regular monitoring which can detect potential threats while octcasional repairs are necessary due to wear from environmental conditions or accidental damage.

• Thickness varies from about 1cm to 20 cm comprising:

Fiber Strands: These are the corecomponents that transmit data

• Buffering Gel: Protects the fiber strands.

Copper Cables: Provide power for repeaters and branching units.

• Armor Layers: Made from materials like steel and armoured polyethylene to protect against marine life and hazards.

• Outer Membrane: Prevents seawater intrusion.

• Conductors in Power Cables: Conductors are typically made of copper or aluminum. Copper is preferred due to its smaller cross-section and better corrosion resistance, though aluminum is sometimes used for cost reasons.

Cable Landing in Maldives

Challenges and solutions

Subsea cables lie directly on the seabed floor and are vulnerable to natural disasters such as volcanoes and earthquakes, accidents from dropped ship anchors, or intentional cuts. Most cuts are accidental, usually from fishing vessels or cargo ships that drop anchors without realizing what lies beneath them. The International Cable Protection Committee (ICPC) estimates that an average of 150–200 faults occur globally each year.

The recent news about a Chinese ship which is able to cut cable lines at depths of up to 4,000 meters (13,123 feet) has the industry a bit worried due to the perceived threat it poses to cables in geopolitically sensitive areas like the Taiwan Strait and South China Sea. Taiwan has previously hinted that its subsea cables were cut courtesy of Chinese ships.

Apart from geopolitical risks, cables also face the risk of sabotage, cyber threats and terrorism. Other less dramatic threats include ecological disruptions on seabed during installation and maintenance of cables, cable bottlenecks, and lack of experienced manpower and specialised equipment.

Hence, there is an urgent need to build resiliency and redundancy into the systems especially in the face of exponential growth globally arising from digital transformations and increased cloud adoptions and AI workloads. This issue will become more pronounced in the years ahead as more subsea cables are built.

Joint patrols should also be conducted especially in waters where there are active conflicts and chokepoints, or geostrategic waters. There should be more cooperation between the private sector and governments including enacting or amending international laws to protect the subsea cable network.

Dominance of big tech

Until recently, intercontinental undersea cables were mostly laid by large consortia of national telecommunications companies. For example, 2Africa, currently the longest cable in the world, was laid by a consortium of telcos plus Meta as an anchor customer. This consortium model is due to the high cost of building. But over the past decade, there has been a shift in which subsea cables are increasingly being built by large individual technology companies themselves. For example, Google has deployed several wholly owned private cables, such as the Curie, Dunant, Grace Hopper, and Equiano. Meta has also previously procured the private Transatlantic Anjana cable and is about to start on a 50,000km subsea cable project that connects five continents. The multibillion-dollar project will take years to complete.

Hence, rather than renting capacity from infrastructure providers, the firms are vertically integrating infrastructure with their content services. Amazon, Google, Meta, and Microsoft now own or lease around half of all undersea bandwidth worldwide.

Today, the global network is made up of about 450 cable systems spanning more than 1.5 million kms of subsea fiber-optic cables that carry 99 per cent of intercontinental data traffic. These cables enable the flow of terabits of information per second compared to a gigabit of data per second transmitted by satellites, according to Center for Strategic & International Studies (CSIS).