TMM: Why you should add KiwiSaver to your advice business

04 EDITORIAL

Why do we recommend you offer Kiwisaver? Because relying on just simple home loans is a recipe for failure. 06

NEWS

Advisers dismayed at the DoshWestpac tie-up; and a new fintech offers floating home mortgages funded by Generate, at rates well below the major banks. 10

BETTER BUSINESS PODCAST

In the latest TMM Better Business podcast we talk to Xceda chief executive Daniel McGrath about the company’s transformation and its new loan products.

12

PEOPLE

Shakers on the move at Mike Pero Mortgages, Finsure, Link Financial Group, First Mortgage Trust & Financial Advice NZ. 14

PROPERTY NEWS

Landlords fired over healthyhomes compliance – and the millions owed by the property sector in undeclared tax.

16

HOUSING COMMENTARY

Cotality head of research Nick Goodall explains why he has changed this house price forecasts.

SALES AND MARKETING

The ‘10-minute marketing plan’ to target the large slice of potential clients who live or work close to you. 32 INSURANCE

Are you giving your life advisers the professional support they need? 34 THE TMM

Here are the most read stories online recently.

KIWISAVER IS NOT JUST FOR FINANCIAL PLANNERS

KiwiSaver – it’s arguably the biggest thing going and growing in financial services right now. Get amongst the action.

IIn our discussions with a number of mortgage advisers it became clear many wanted to add KiwiSaver to their product offering this year. In some ways it’s a no brainer when you think about the importance of the first home withdrawal.

So, I would like to introduce our feature on how and why you should add KiwiSaver to your offering.

This also sits with one of our core beliefs. That is, we believe mortgage advisers need to have a broad product knowledge and not just focus on clean skin home loans.

Indeed, relying on straight forward home loans is likely to be a recipe for failure as banks and now fintechs (more on this further on) are focussed on this space.

Advisers, we believe, need to know about things like KiwiSaver, small business lending, development finance, asset finance, home equity release and so forth.

It is one of our goals to provide advisers with information to help

Head office & Advertising

Publisher Philip Macalister

Staff writer Sally Lindsay

Design Michelle Veysey

achieve this goal.

Here’s a good case study of why adding KiwiSaver makes sense. Currently there is around $120 billion in KiwiSaver and according to Harbour Asset Management co-chief executive Andrew Bascand, that will grow to $400 billion in 10 year year’s time.

As it grows more and more KiwiSaver members will want advice. Speaking at the launch of Evidential KiwiSaver scheme, he reckoned in 10 year’s time one million Kiwis will be wanting advice on their KiwiSaver.

He also outlined how it will be a profitable business.

Not all KiwiSaver providers work with mortgage advisers but there are enough out there who want to play who offer a range of different options.

Our news this issue has a tech focus based on some stories we have run online. Fintech Dosh, backed by Westpac, has ruffled feather with its online offering which has no advice.

Likewise, Indi, another fintech start up established by ex-Kiwibankers, is

offering home loans.

Advisers, in their comments have raised clear concerns that its not a level regulatory playing field.

The fintechs can get away with no advice while advisers have clear regulatory hurdles. This is something which needs to be addressed by regulators, especially as open banking creeps closer.

While advisers have, understandably, been annoyed by these offerings it reinforces the idea that mortgage advisers need to focus on the more complex home loans, helping first home buyers and having broad product knowledge as outlined earlier in this editorial.

Philip Macalister Publisher

Navigating the Future of Mortgage Advice

BY PAUL BARNES, GENERAL MANAGER, FRANCHISE & DISTRIBUTION – NZHL

The market is shifting rapidly. Economic uncertainty, subdued house prices, rising refinancing activity, and increased job insecurity are all shaping client behaviour. At the same time, advisers are contending with tighter regulatory frameworks shifting compliance requirements, and intensifying competition.

Geopolitical tensions are adding another layer of complexity, fuelling global market volatility and reshaping the financial landscape.

In this environment, clients are more cautious, more informed, and more focused on value. They’re not just looking for a good rate—they want clarity, confidence, and a trusted adviser who can help them make smart, long-term financial decisions.

Despite the size of the financial commitment, many New Zealanders still enter into home loans – typically over 30-year terms - without a full understanding of how they work. Critical decisions—such as borrowing limits, loan structure, and repayment options—are often made without clear guidance or explanation. This knowledge gap can lead to missed opportunities, increased stress, and difficulty establishing strong, longterm financial habits.

Advisers play a critical role in closing this gap and guiding client behaviour through market cycles. But to do so effectively, they need the right support—that reduces complexity and enhances client engagement.

At NZHL, we believe in adviserled advice—supported, not replaced, by technology. That’s why we invest in training to keep advisers at the forefront of industry knowledge, marketing initiatives, and business systems that reduce admin and

ABOUT NZHL GROUP

amplify advisers’ positive financial impact on New Zealanders.

We offer a highly resourced, supportive environment focused on simplifying processes, removing friction, and driving innovation through AI tools that boost productivity.

NZHL’s model is built around longterm relationships, we help clients create a plan, monitor progress, and adapt as life changes. To support this, our clients have access to DebtNav, NZHL’s unique online monitoring tool.

DebtNav allows clients to track their progress, factor in short-term goals or unexpected expenses, and see how these changes impact their mortgage. It’s a simple and accessible way to stay engaged with their mortgage plan and make informed decisions along with their adviser.

For advisers, NZHL offers a unique balance: the ability to drive their own business backed by the scale and strength of a national network. With around 70 locally owned franchises, we’ve become one of the largest New Zealand-owned home loan and insurance advisory businesseswithout compromising on our values.

At NZHL, we actively support strengthening the voice of advisers across the industry. Through strong partnerships with regulators, industry bodies, and suppliers, we actively provide feedback to help shape compliance frameworks and provider processes that support, rather than have unintended consequences on quality advice. Our goal is to ensure client outcomes are supported without adding unnecessary administrative burdens that don’t serve the best interests of the client.

It’s important that adviser practitioners work together to shape a better future—for clients, businesses, and for the industry as a whole.

The focus of financial advisers hasn’t changed: it’s still about being in front of people. In a world consumed by constant change, advisers need the right partners and tools to stay focused on seeing their clients and delivering great outcomes - this is critical to ensure advice is accessible.

At NZHL, we’re committed to keeping advice personal, scalable, and sustainable. Because when you do the right thing for the client, the business results follow. ✚

NZHL is a Kiwi-owned, respected, and trusted brand - a purpose-driven (financial freedom, faster) home loan and insurance network that offers a solution to support advisers and help put Kiwis in a better financial position. Part of Kiwi Group Capital Ltd (KGC) which is 100% Government owned, NZHL Group operates with an Independent Board and local business owners nationwide.

PAUL BARNES

Advisers dismayed at Dosh and Westpac tie-up

Mortgage advisers say they have been slapped in the face by Westpac powering fintech Dosh to offer home loans without financial advice and giving a cashback reward of up to 0.20% over the term of a mortgage.

Invercargill-based adviser Brenda Nom says Westpac claims more than 50% of its mortgage business comes through third party advisers, yet it is doing the dirty behind advisers' backs as its tie-up with Dosh has not been communicated well.

"It's upsetting that a client can go online, apply for a Westpac mortgage through Dosh, get no financial advice whatsoever and trail income paid back to them, which will just decimate advisers' books," Nom says.

Mortgage advisers are paid about 0.2% trail from Westpac, and mortgagesonline founder Hamish

Patel says the Dosh scheme gives away about 60% of that trail to the home owner, with no financial advice. "It is something third party mortgages advisers absolutely cannot do."

Dosh teamed up with Westpac in March to offer an online platform where customers can apply for home loans in minutes with rewards. Under Dosh Streak, homeowners get cash payments equal to 0.01% of the loan balance, up to 0.20%, over the mortgage lifetime.

Patel says Dosh is effectively set up to steal advisers' Westpac clients and massacre their books. "If I advertised and gave away 60% of my Westpac trail to clients who refixed exclusively through me, the bank would have a massive fit, but it is what Dosh is doing."

Westpac NZ head of consumer banking Helen Ryder says because Dosh operates differently to traditional mortgage advisers, the bank does not consider it part of its adviser channel, noting Dosh is online-only and provides information-only service without financial advice.

Industry reaction has been strong, with one adviser saying after 20 years supporting Westpac, this feels like "a kick in the backside.” Another said using Dosh is “akin to ordering a kit set cabinet online with 100 pieces and not been provided with any assembly instructions”, while others questioned how Westpac meets CoFI regulations and urged the FMA to get involved.

KiwiSaver scheme funding new cheap floating rate startup

A new fintech is offering residential floating mortgages funded by KiwiSaver scheme Generate at rates well below the major banks.

Indi (The Independent Mortgage Company) is offering a floating rate of 5.19% compared to the average major bank rate of 6.46%. Generate, providing the funding, has 165,000 KiwiSaver members and $6.6 billion under management.

Unlike big banks, Indi offers only floating rate mortgages with no fixed rates, revolving credit or offset loans. Like Dosh's Westpac tie-up, Indi doesn't offer mortgage or financial advice. It says client should seek that themselves.

Helmed by Anand Ranchord, a previous Kiwibank innovation chief,

and David Woods, former Kiwibank head of model development. Board member Craig Stobo is FMA and Local Government Funding Agency chairman.

Indi's philosophy is having floating rates at least 0.20% cheaper than big bank fixed rates over the year. Major banks' floating rates are usually 1.50% higher than their fixed rates.

"There is actually no reason why major banks' floating rates are so much higher than their fixed rates. In Australia, floating rates are about the same as fixed rates," Ranchord says.

Indi can offer cheaper rates despite lacking big banks' "cheap deposits" from everyday Kiwis' accounts. It gets funding from institutions wanting reasonable returns, creating higher funding costs than big banks.

However, Indi has much lower operational costs than inefficient big banks and requires lower profit

than banks which siphon profits to Australian owners.

Ranchord says major banks prefer borrowers on fixed rates because that locks them in. "Big banks want customers to be on fixed rates, so they make floating rates unreasonably high.”

The website says applications take 10-15 minutes for borrowers with property and income information ready. Indi covers conveyancing costs through panel lawyers.

Advisers have expressed concern at another provider cutting out financial advice, despite the recent introduction of CoFI. “This is appalling,” a commenter said. “Borrowing a home loan is one of the single biggest financial commitments a person can make in his or her lifetime, hence "somebody" needs to be providing advice to the client.”

BRENDA

NOM

Getting rid of those repetitive tasks

A project which started out as a better way to run a mortgage adviser business is now being taken to the wider market.

Auckland-based Float Mortgages set off on a project several years back to use technology and AI to make its business more efficient.

The idea was to automate the repetitive and time consuming tasks involved in preparing a mortgage application for a bank.

Float was set up by former banker Geoff Christopher. The automation process, now called Afterburner, came to life when one of Float’s clients, computer engineer named Jacob Munoz, decided to join the firm.

Jake was doing a role in which he basically automated within three months.

Christopher says there was never any intention when this started that they would take it to the rest of the industry.

“It was purely designed to help us

be more efficient, get more done, and provide quicker service for our clients.

“There was never any intention to go and help the rest of the adviser market.

But that has changed.

The system is CRM agnostic and Afterburner is talking to all the aggregators about creating APIs to allow their members to use the tool.

Of the 100 or so advisers using it most are through Kiwi Adviser Network (which Float belongs to) or NZ Financial Services Group.

So the software stack improves tenfold because of getting all the advice and all the improvements and all these best practises from all these different advisors, all coming into one great product

Christopher says there are 10 to 15 repetitive tasks at every mortgage adviser has to do, and Afterburner automates them integrating them into existing CRM systems using secure OpenAI.

Amongst the automated tasks are client interviews, application forms, bank submissions, and compliance

documentation.

It can take information uploaded and create a state in a position split out immediately the maximum bank, borrowing capacity for all the banks.

Another task is it can upload a bank approval letter and write the an email that summarises it as in layperson's terms.

There are other developments in beta testing at the moment

One of the questions is will AI tools like this replace advisers?

Christopher is clear the answer is no. “No, never. No, never.”

The tool means “clients are going to get a far more comprehensive service out of us because we're not focussed on the stuff that we've be focussed on before.”

“It's not designed to do the job. It does a lot of the job for the adviser, but it's assistance not advice.”

He suggests firms using tools like Afterburner will not have to employ as many support staff as they currently do.

Advisers well positioned to fill SME lending gap left by banks

Small businesses struggling to access capital as bank lending slows.

Small businesses are finding it tougher to get bank loans, leaving some struggling to manage their cash flow.

According to Reserve Bank data, the compound annual growth rate of bank lending to businesses has slowed from 6% in 2013 to just 1.5% today. Business lending from ANZ has declined, while Westpac’s SME lending has remained flat since 2020. With banks increasingly favouring capital-efficient home loans over commercial credit, many small business owners are left with fewer funding options.

Despite this, small businesses aren't losing hope. In fact, the latest research paints a picture of resilience and renewed ambition. Prospa’s SME Sentiment Tracker revealed 63% of Kiwi small business owners feel optimistic about their growth over the next 12 months, and 57% rate their current business health as “good” or

“very good.”

The latest 2degrees’ Shaping Business study, reported New Zealand’s highest level of business optimism since 2021 with 45% of business leaders more upbeat about this year compared to last and 65% expecting revenue growth in the year ahead.

However, this optimism exists alongside real financial pressure, particularly when it comes to managing cashflow. Prospa’s SME Sentiment Tracker found that 59% of small businesses have just three months or less in cash reserves, and nearly a quarter have less than a month’s reserves.

Adrienne Begbie, managing director at Prospa New Zealand, says the shift away from SME lending by banks is not a short-term trend, and advisers have a vital role to play in addressing the funding gap.

“Kiwi small businesses are feeling positive and productivity is improving, but access to capital remains a major roadblock,” she says. “The retreat from SME lending by major banks is not new and it’s not temporary, so

there’s a real opportunity for advisers and alternative lenders to step in and support this vital part of the economy.”

More and more small business owners are turning to advisers to help them get the funding they need. In New Zealand, more than 55% of Prospa customers now come via advisers. The trend is even more established across the Tasman, where mortgage brokers command more than 76% of market share, with seven out of 10 borrowers choosing to work with a broker or adviser.

“There’s still plenty of room for growth here,” says Begbie. “As traditional funding options become harder to access, small business owners need someone they can trust to help them understand their options. Without that support, it can hold them back from growing or running their business at full speed.”

As bank business lending slows and with small business confidence on the rise, advisers have a timely opportunity to step up, grow their client base, and play a central role in helping local small businesses thrive. ✚

Advisers’ fraudulent activity to be rooted out by FMA

Adv isers selling mortgages and insurance through misleading or fraudulent activities are coming under the beady eye of the Financial Markets Authority (FMA).

The regulator has noticed increasing fraudulent activity, particularly in relation to mortgages and insurance.

It says while these instances are the exception rather than the norm, the severity of the conduct, exacerbated by the existing economic climate, makes this a priority.

In its recently released Financial Conduct Report, the FMA says it has seen advisers taking advantage of new migrants’ lack of understanding of what products they need, including advisers from within their own communities.

These advisers have exposed them to unsuitable products and/or unnecessary costs.

The FMA says it will prioritise investigation of complaints from product providers about advisers

adversely impacting people in vulnerable circumstances and use its full range of regulatory interventions to address poor conduct.

FMA chief executive Samantha Barrass says it is taking a no surprises approach to enable the financial sector to make sure they’re doing the right thing by their customers.

“This report shows we value transparency, accountability and engagement.”

Fees and incentives

Other priority areas include consumers and investors understanding fees, incentives and commissions.

In its monitoring last year, the FMA says many FAPs demonstrated good practices, but there were some gaps that pose risks to their clients including lack of clarity regarding commissions, incentives and fees; missing or inconsistent information; some disclosure not being provided in

a timely manner, in some cases weeks after the advice was provided.

The focus in the next year includes reviewing the disclosure provided by financial advisers through a thematic review to increase the FMA’s understanding of FAP business models and remuneration structures.

Custody of investments

FAPs will also be monitored over their arrangements in place to oversee the outsourcing of client money or property handling to a custodian.

The FMA says it has seen instances where weakness in custody have contributed to fraud or business failure resulting in investor loss.

The rules around client money and property handling are complex, so the FMA will review the governance and supervision of the custody service as well as how custody reports are provided to clients to ensure appropriate protections are in place. ✚

In the latest TMM Better Business podcast we talk to Xceda chief executive Daniel McGrath about the company’s transformation and its new loan products.

Xceda Finance has been around more than 35 years and after a change of ownership and regulatory changes is positioning itself to be one of the main non-bank lenders.

McGrath tells TMM that in the past its main lending product was a bridging loan which had done very well, but these loans tended to be churned quite heavily – as is their nature.

Recently it has rolled out a property investment loan with a five-year interest only option or principal and interest at attractive interest rates.

It’s similar to a product which was in the market previously which had proved popular.

Another of the big changes is that the government’s Deposit Compensation Scheme started on July 1 meaning that all deposits up to $100,000 are guaranteed if the company got into trouble.

McGrath says already there has been a surge in new deposits which means it has more funds to lend out.

Also, it means that non-bank

deposit takers like Xceda will be able to self-fund and won’t have to rely on securitisation or bank lines for funding.

McGrath says there is tremendous opportunities for lenders like Xceda and he can see the sector growing from a lending market share of 2% to closer to between 8-10% as is the case in Australia.

In this podcast McGrath gives his thoughts on changes to the Credit Contracts and Consumer Finance Act (CCCFA) and how new conduct regulations work. ” ✚

The TMM Better Business podcast is available at tmmonline. nz and all the popular streaming platforms.

DANIEL MCGRATH

•

•

•

•

•

People on the move

MPM finally gets new GM

Liberty has appointed a new general manager to the Mike Pero group nine months after the former GM left.

Lenska Papich has been appointed Mike Pero Mortgages general manager, taking the helm in June 2025. Papich has been involved with Liberty for a number of years.

Chief executive Aaron Skilton said Papich understands the 35-yearold business and the opportunity to differentiate through sales and marketing. "We have a strong, iconic brand and network of businesses who will benefit from Lenska's franchise background and determined focus on sales, marketing and delivering value for advisers," he said.

Papich was the acting general

manager of Mike Pero Real Estate after the company was sold to Raine and Horne in 2023. Former general manager Rob Klenner left the role in September last year.

Finsure increases NZ staff

Aggregation business Finsure Group has appointed a compliance manager to help mortgage advisers deal with regulatory changes and compliance issues.

Jess Hulena has been hired as Compliance Manager for Finsure advisers. Hulena has six years of experience in risk roles at AA, Westpac, ASB and AIA.

Finsure New Zealand Country Head

Jenny Campbell said the group has made assisting advisers a priority with regulatory and operational compliance obligations.

"For the last 18 months, advisers have been inundated by news around regulatory changes and compliance guidelines, all of which is causing stress," Campbell says. "We believe Jess's appointment has helped relieve some of that stress."

The company has introduced live online Q&A sessions hosted by Hulena where advisers can ask questions directly and get immediate answers.

Got a new appointment you would like to tell advisers about? Email details and a pic to editor@tarawera.co.nz

Link appoints new compliance manager

Link Financial Group NZ has appointed Anton Wicken as its new compliance manager. Wicken brings financial services experience and expertise in regulatory compliance, privacy law, risk analytics, and policy development across New Zealand and the Pacific. Before joining Link, Wicken was at Southern Cross Healthcare. Earlier roles include Tower, Allianz Partners and AIA.

Chief executive Josh Bronkhorst says Wicken's leadership will help drive the company's commitment to supporting advisers with clear compliance frameworks as the LFG network grows.

Financial Advice NZ appoints new chairman

After four and a half years as chair, Heather Roy is stepping down from the Financial Advice NZ board.

Director Tiumalu Peter Fa'afiu, who has served two years on the board, has been appointed Independent Chair and continues to provide a consumer perspective.

"It is now time for me to pass the baton to someone I know is going to take the association through its next

phase," Roy says. "Peter's time on the board has given him the experience to lead the board into a new era."

Fa'afiu said he looks forward to leading the association and continuing to champion financial advice in New Zealand. "I look forward to continuing to work with the board and support our chief executive Nick Hakes and his team in executing our strategic plan and strengthen our position in

the community as an adviser-driven, high-engagement professional body,” Fa’afiu said.

“Now is a perfect time for building new pathways for Kiwis to obtain financial advice to help manage their financial wellbeing now and in the future.”

The board is advertising for a new independent director.

First Mortgage Trust appoints chief risk officer

First Mortgage Trust has appointed Sam Johnstone as its inaugural chief risk officer.

This newly created role reflects FMT's commitment to robust risk management for delivering consistent investment returns and providing specialist property lending solutions.

Johnstone brings more than 20 years of experience in banking and risk management. He began his career as an agribusiness lender at Rabobank and progressed into senior risk leadership roles. Most recently, he served as global head of risk change and implementation at Rabobank's head office in the Netherlands.

“We’re really pleased to welcome Sam to FMT,” FMT chief executive

Paul Bendall says. “His extensive expertise across credit and operational risk, along with a strong commercial mindset, makes him a great addition to our leadership team."

The role reinforces FMT's commitment to strong risk governance as it grows its funds under management. Johnstone will play a pivotal role in enhancing FMT’s risk frameworks and supporting its dual mission: to provide consistent, reliable returns to investors and offer flexible, property lending solutions.

“Effective, proactive risk management is critical to successful execution in both the investment and lending functions," Johnstone says.

SAM JOHNSTONE

Landlords fired over healthy homes compliance

BY SALLY LINDSAY

Property managers are firing landlords who refuse to bring their rentals up to the Healthy Homes Standards (HHS) by July 1.

They say some landlords are dragging their feet over making improvements they have known about for years.

Making a call to fire a landlord is difficult, but property management businesses say they don’t want to be responsible for non-compliant homes and non-compliant landlords, leaving tenants vulnerable.

All rental properties must comply with minimum standards for heating, insulation, ventilation, moisture ingress, and drainage and draught stopping by July 1. For many, the solution is simply adding a heat pump or underfloor insulation.

The new law was first announced in 2019, and landlords were given between July 1, 2021 and July 1 this

year to ensure their properties were up to scratch.

The Ministry of Housing and Urban Development found in its most recent survey of HHS compliance, 17% of landlords claimed they had fully met the standards and almost three-quarters had done something to prepare.

Landlords who do not meet their obligations under the standards are in breach of the Residential Tenancies Act - and may face financial penalties of up to $7,200.

In addition to the financial penalty, landlords may also be ordered to pay compensation to the tenant and to carry out necessary repairs to bring the property up to standard.

Some landlords unaware

The Auckland Property Investors Association says there is still a lack of awareness about how the deadline applies.

This knowledge gap appears to be split between seasoned landlords and property managers, who have had it drummed into them since 2019, and less experienced landlords and property managers who don’t seem to be aware their properties must be fully compliant by July 1 - and that there is no grace period.

The New Zealand Property Investors Federation says some “accidental landlords”, who put their properties into the rental pool when they didn’t sell for the price they wanted, could be unaware of their obligations and the deadline.

If landlords do not comply, the Tenancy Tribunal and the Tenancy Services Compliance and Investigations Team (TCIT) are expected to come down hard on them.

MBIE is also likely to monitor bond forms for a change of landlord, from a property manager to a private arrangement, and then audit those properties.

Tax crack down on property sector finds millions owing

More than $150 million has been coughed up by the property sector in undeclared tax and GST to the IRD.

After taking a closer look at the tax affairs of landlords, developers and those covered by the Brightline test as part of stepped-up compliance work, the IRD found a $153.5 million discrepancy for the first nine months of the current financial year.

That is almost the same as the $156.8 million figure for the whole of the 20232024 financial year.

Developers have been the main culprits, owing $72,937,921.00 in discrepancies – a 48% increase on the same time last year.

The IRD says while some of the errors will be accidental, it is also seeing a pattern: property developers claiming

significant refunds as they incur costs upfront, but then failing to file and pay once properties sell.

Where it expects a GST payment from a property sale and it doesn’t see the sale in the return, it will contact the developer to make enquiries.

If there is no response or no return filed, IR takes enforcement action quickly.

Incorrect GST increasing

The tax collector says it is seeing a growing number of issues involving companies or individuals making multiple land transactions where GST needs to be correctly accounted for.

So far, this financial year it has found $59,959,470.00 in discrepancies – a 39% increase for the same time last financial year.

Sometimes companies or individuals

are changing the intended use of the land or frequently transferring ownership between entities with or without GST registrations. These actions appear to be attempts to circumvent their GST obligations, IR says.

Bright-line campaign

The IRD started a campaign in March to help people understand their brightline obligations.

It has helped more than 550 clients with bright-line issues and processed $3.68m in voluntary disclosures. The discrepancy found in the bright-line area is $14,152,162 – a 9% increase.

The department is advising people that if they’ve sold a property recently, they should check the property tax decision tool and work out if they need to pay tax.

Landlords seek better systems for handling rent arrears

Rent arrears claims are clogging up the Tenancy Tribunal, sparking calls for a separate division to handle these cases remotely - without time-consuming in-person hearings.

The New Zealand Property Investors Federation (NZPIF) says the time taken to secure a tribunal hearing, even for a simple rent-arrears case, places an unfair financial burden on landlords through no fault of their own.

According to Tribunal data, at the end of February, the average wait time from submitting an application to securing a hearing was more than nine weeks.

The average wait time for mediation, a first step in the process, was just over five weeks.

NZPIF vice-president Peter Lewis says the existing system is too slow for landlords dealing with accumulating unpaid rent, often leaving them with significant financial burdens while waiting for a resolution.

The long wait times mean, on average, a tenant can live rent-free for up to 55 days – or nearly two months – before the matter is resolved.

“For landlords, even with a maximum bond claim, unpaid rent then exceeds the bond amount, leaving them struggling to pay their own unavoidable costs,” Lewis says.

Big losses in unpaid rent

Figures based on Tribunal data reveal that in the first two months of last year, landlords faced about $1.3 million in

unpaid rent arrears.

Most of the tribunal’s arrears orders were for amounts between $2,000 and $3,000, with some reaching up to $10,000.

The loss to the industry each year is well over $100m, Tribunal figures show.

One factor affecting wait times is the volume of arrears applications lodged with the Tribunal. It received more than 29,000 applications last year, a 14% increase on the previous year and a 43% rise from 2022.

In the fourth quarter of last year, 62.25% of the 6,093 landlord applications to the tribunal were for rent arrears.

This suggests about 6% of all tenancies are going into arrears and about 2% of landlords every quarter take rent arrears cases to the tribunal.

Despite the wait times, Tenancy Tribunal hearing timeframes compare favourably with other tribunals, says Katie Gordon, MBIE’s dispute resolution national manger.

While 63% (18,557) of the applications to the Tribunal last year included matters relating to rent arrears, those applications usually involved other issues such as compensation or claims for the bond.

When an application included other matters, this contributed to the complexity of a case and therefore the time needed to determine it, Gordon says.

Other causes of longer wait times include incomplete information being provided with applications, adjournment requests, amended

claims, cross claims or late filing of evidence.

Arrears outside tribunal

Property Brokers property management general manager David Faulkner says an efficient solution would be to handle rent arrears cases remotely outside the tribunal.

“After the tenant is 21 days in arrears, the landlord could submit an application with all the necessary evidence, such as rent statements, arrears notices, a copy of the tenancy agreement and the tenant’s contact address for service. Under s 55 of the RTA, if the tribunal is satisfied the tenant is at least 21 days in arrears, it must make an order terminating the tenancy.”

“This process would limit the risk to the landlord to approximately five weeks of rent arrears,” he says.

Dealing with rent arrears cases remotely would also reduce the tribunal’s workload by about 120 cases a week.

Adjudicators could provide faster resolutions for complex cases, with a lighter caseload, and there would be consistency and transparency by using standardised procedures for rent arrears cases – along with economic efficiency from avoiding unnecessary hearings for both landlords and tenants.

Faulkner says implementing this reform required careful planning, but the potential gains in efficiency and justice made it worthwhile. ✚

House price forecast lowered

Cotality head of research Nick Goodall says economic conditions have led him to revise his house price forecasts.

BY NICK GOODALL

Property values across Aotearoa New Zealand hit a minor speed bump in May, dipping 0.1% to a median value just over $818,000. While values remain 0.4% higher than at the start of the year, the already-muted recovery is looking increasingly fragile.

This flattening trend is especially evident in our main centres. Over the

past 6 to 9 months, value movements have been largely stagnant. Kirikiriroa Hamilton stands out as the only major city to maintain momentum, with a 1.0% lift over the last quarter. In contrast, Te Whanganui-a-Tara Wellington and Ōtautahi Christchurch saw modest declines of -0.2%, while Ōtepoti Dunedin dropped -0.8%.

These fluctuations aren’t unexpected.

Market headwinds have been well signposted: elevated property listings, a sluggish economy, a soft labour market, and the slow transmission of falling interest rates into household budgets. The Government’s May Budget was predictably cautious, reinforcing the likelihood that monetary policy will continue to shoulder the burden of economic recovery.

The Reserve Bank’s latest Monetary Policy Statement aligned with expectations, revising the Official Cash Rate (OCR) forecast downward and prompting further mortgage rate reductions. However, the tone of the statement - and a split vote among committee members - suggests future decisions may be less clear-cut, hinging on up-to-date economic measures and

inflation data.

With over 40% of mortgages due to refix in the next six months and another 12.8% currently floating, there’s hope that lower repayments will free up household spending and stimulate the domestic economy.

Interestingly, we’re seeing a twospeed economy emerge. Regional areas - particularly those with

strong agricultural ties - are showing resilience. Ngāmotu New Plymouth and Waihōpai Invercargill have already returned to their post-Covid peak values for residential property.

Queenstown-Lakes is just 2.7% below its peak, and Ōtautahi Christchurch is only 6% off. In contrast, other urban centres remain more than 10% below their highs.

First home buyers remain active, buoyed by increased borrowing capacity and access to low-deposit loans. However, they’re entering the market later in life.

According to our inaugural cobranded Cotality-Westpac First Home Buyer report, the average age of a first home buyer is now 36, up from 34 in 2019. We’re also seeing more buyers stretch their debt-to-income ratios, though the flat market suggests they’re still exercising caution.

Investor activity is also picking up, particularly among those with smaller portfolios.

Listings have started to decline, albeit slowly and from a high base, which means buyers may retain pricing power for a while yet.

On the construction front, activity appears to be stabilising. Cost growth has moderated, and greenfield development is picking up - especially outside Auckland. This should help balance supply as the market gradually recovers.

Our revised outlook anticipates national property values to grow by a reduced level of 3-4% (from 5% previously) over the 2025 calendar year. While subdued by historical standards, this projection reflects a cautious optimism as the market adjusts to new economic realities.

A Global Footnote

While this article focuses on domestic trends, it’s important to acknowledge the broader geopolitical context. The recent escalation in the Iran–Israel conflict - and the growing involvement of the United States - has introduced fresh uncertainty into global markets. While the direct impact on New Zealand’s housing sector remains limited for now, the potential for volatility in petrol prices, trade flows, and investor sentiment is real.

As always, we’ll be watching closely for any ripple effects that could influence our local economy and property market. ✚

Nick Goodall is Head of Research at Cotality NZ.

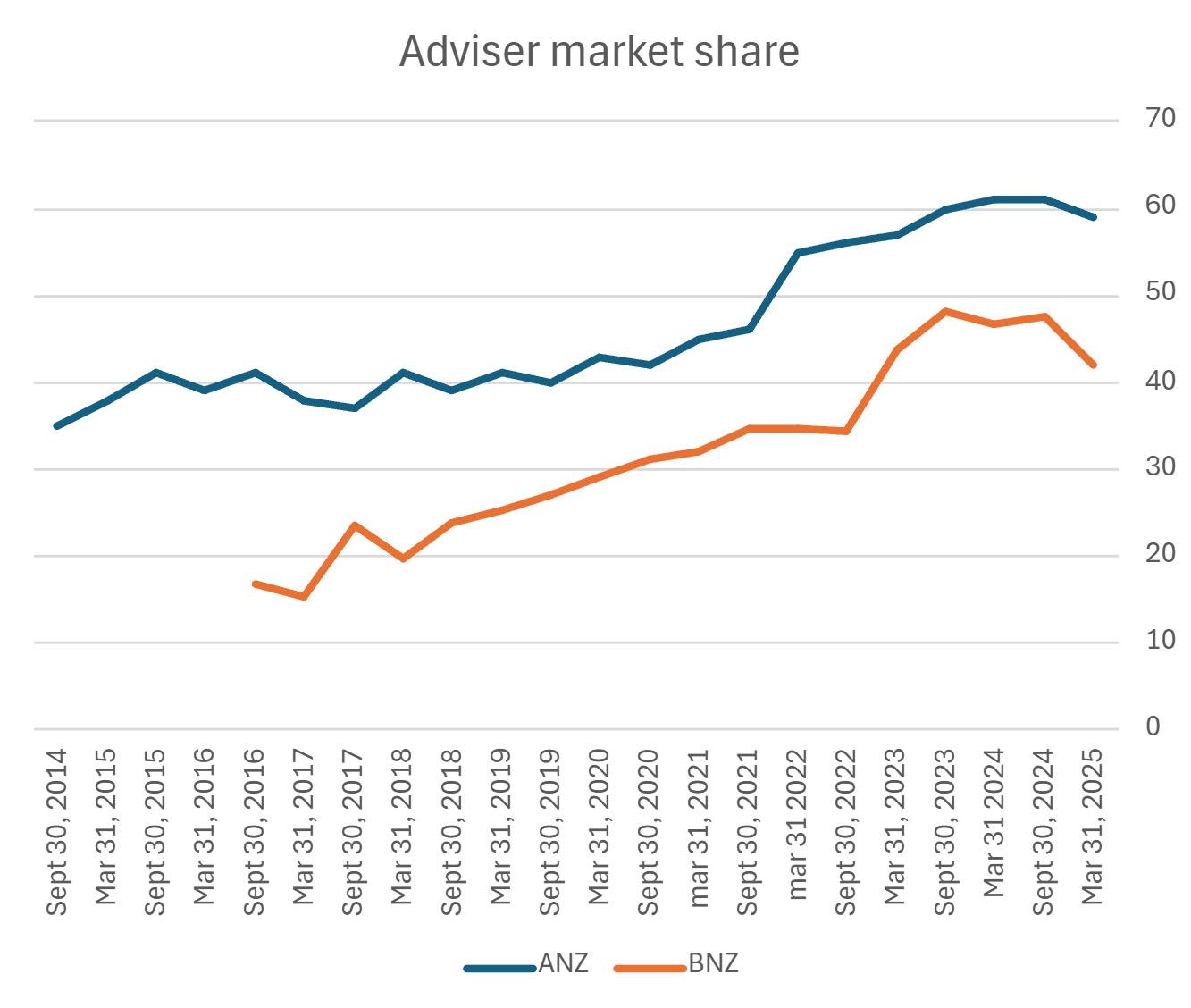

Kiwibank, BNZ gain mortgage market share at expense of ASB and Westpac

Jenny Ruth digs into the data to see which banks are winning the most business from advisers.

The size of the mortgage market is so large that changes in each bank’s market share tends to move at a glacial pace.

The Reserve Bank’s bank financial strength dashboard data showed mortgages held by registered banks totalled $368.27 billion at March 31, meaning 1% of it was $3.68 billion.

But there have been a few striking changes since RBNZ started its dashboard in the March quarter of 2018, although not at our largest bank.

The market share of ANZ Bank New Zealand has changed little over that period, going from 30.19% in March 2018 down to 30.15% in March this year, although its mortgage book has grown by $38.64 billion.

But the government-owned Kiwibank has lifted its share by more than a percentage point from 6.7% to 7.8%, taking its book to $28.85 billion at March 31, up by $12.69 billion since March 2018.

And Bank of New Zealand has lifted its market share from less than 16% to nearly 17%. The smallest of the big four Australianowned banks in mortgages, it has lifted its book by $23.95 billion since March 2018 to $62.14 billion at March 31 this year.

On the other hand, ASB has seen its market share slip from nearly 22.3% to 21.1% and Westpac’s share has dropped from nearly 20% to 18.7%.

In dollar terms, ASB’s mortgage book has still grown by $24.44 billion in March 2018 to $77.78 billion at March 31 this year while Westpac’s has grown by $21.25 billion to $68.97 billion.

The stand-out reason for ASB’s loss of share was its parent’s desire to try to protect profit margins and that led to ASB failing to offer competitive mortgage rates for an extended period, although more recently the bank has shown itself back in the game.

For example, in the March quarter this year, ASB accounted for 24.5% of net new mortgage lending by banks compared with just 0.4% in the year ended March 2024.

The question of how much of a role mortgage advisers have played in these market shifts is harder to determine, other than that it’s obvious advisers are originating more and more mortgages. It’s always been difficult to assess how much of new mortgages advisers originate, but the indications are that they now account for more than 60% at the big four banks and Kiwibank, up from about 25% through the first decade of this century.

ANZ’s Australian parent has been providing comprehensive data on its business with advisers since the GFC.

Advisers accounted for 28% of its mortgage book at September 30, 2014 and that had jumped to 52% by March 31 this year.

In the year ended September 2014, advisers originated 35% of ANZ’s mortgage business and by the March quarter this year that had grown to 59%, with a little slippage from the September 2024 and March 2024 years.

BNZ has always shown an ambivalent attitude towards mortgage advisers – it stopped dealing with them altogether between June 2003 and May 2015.

BNZ appeared to be trying to make of virtue of necessity because when it shut its doors to advisers, they had been writing only about 5% of the bank’s new mortgages.

Advisers who were operating during the hiatus probably remember well BNZ’s aggressive “we’ve cut out brokers” advertising campaign.

Its reason for re-engaging in 2015 was that it wanted to be able to address the whole market, without excluding its ability to share in mortgages originated by advisers.

As you’d expect, advisers’ share of BNZ’s mortgage book has grown steadily – they originated just 2.9% of its book at March 31, 2016 but reached 38.9% by March 31, 2025.

However, BNZ’s change of heart has always appeared reluctant because although advisers have been placing increasing amounts of business with it, it’s obvious

BNZ is still not well-loved among advisers.

And it appears to be starting to shun them again – for example, when we asked the bank early this year about whether it was providing customers with mortgage pre-approvals, while its answer was yes, it talked only about its “in-house home-loan partners.”

“BNZ is fully open for business and actively processing home loan preapprovals,” it said.

“Our in-house Home Loan Partners

It’s always been difficult to assess how much of new mortgages advisers originate, but the indications are that they now account for more than 60% at the big four banks and Kiwibank

(HLPs) provide personalised service to help guide customers through the application process and ensure we have all the information needed to assess their application efficiently,” BNZ said.

While BNZ does answer such questions via email, unlike the other major banks, its chief executive Sam Huggins hasn’t agreed to interviews with TMM or its sister publication Good Returns for some time.

Our best guess is that perhaps Huggins hasn’t like Good Returns/TMM pointing

out BNZ’s ongoing unpopularity with mortgage advisers.

BNZ’s ambivalence may be starting to show in its numbers again – in the six months ended March 31, advisers originated 42% of the bank’s new mortgages, down from 47.6% in the six months ended September last year and down from its peak at 48.1% in the six months ended September 2023.

ASB built its business outside of its Auckland base through engaging with mortgage advisers and had been a strong supporter through much of the last two decades and more.

But ASB has never provided data on how much of its mortgage book was originated by advisers or how much of its new mortgages they account for.

However, its parent bank does and CBA chief executive Matt Comyn raised eyebrows and the ire of advisers last year when he claimed the broker channel was a more expensive one for acquiring mortgages than those its own staff originated.

Comyn asserted that the bank’s mortgages

written by its own proprietary channel were between 20% and 30% more profitable than loans originated by advisers.

More recently, CBA has been trying to lure mortgage brokers back to working for it by reportedly offering salaries of up to A$270,000.

According to industry sources, CBA was having some success in attracting brokers at small to medium-sized broking firms.

Westpac has expressed no such antiadviser sentiments – after the bank’s latest results were released in May, a spokesperson said that “mortgage advisers play an important role in helping provide our customers with guidance and expertise through the homebuying process.”

Advisers’ share of its mortgage book has grown steadily from 46.7% of its existing book at September 30, 2021, the first time it provided data, to 55.2% by March 31 this year.

While its Australian parent doesn’t publish data on advisers’ share of new mortgages, local chief executive Catherine McGrath revealed that advisers originated

about 64% of her bank’s mortgages in the latest half year.

Westpac does appear to be trying to regain its lost market share because its net new lending in the March quarter was just over 19% of new lending by registered banks.

And in the six months ended March, it added $1.51 billion in net new mortgages.

But for the year ended March 31, it accounted for only 12.4% of net new mortgage lending.

Kiwibank has assiduously courted mortgage advisers and there seems little doubt that has aided its market share growth.

The bank says third-party advisers, including those from sister-company NZ Home Loans, accounted for about 43% of its book by December 31, when it last published financial results.

In calendar 2024, advisers originated about 70% of Kiwibank’s mortgages with 47% coming from third party advisers and the rest from NZHL. ✚

Percentage of bank home loans written by mortgage advisers

The percentage of loans written by advisers has shown steady growth over the years, but has taken a dip in the most recent half year results for ANZ and BNZ. ASB steadfastly refuses to provide data on its home loan book. Westpac does provide some data but it was too patchy to include in the graph.

Why you should add KiwiSaver to your advice business

KiwiSaver is becoming an important addition to mortgage advisers’ businesses, with a number of providers actively targeting the adviser market. Sally Lindsay looks at the pros of offering KiwiSaver advice – but finds not all advisers are keen.

Nearly $122 billion is lying in the KiwiSaver accounts of 3.4 million people - and most take no active part in managing one of their biggest assets.

The majority let their money lie there, invested in 300 different funds offered by 38 different schemes, until they either buy a house or retire.

Yet KiwiSaver is shaping up to be one of the most pivotal financial platforms for New Zealanders.

With the average working New Zealander likely to contribute to KiwiSaver for more than 40 years, it often becomes one of the largest investment assets they’ll ever own –sometimes even exceeding the value of their home by retirement.

And for the most part, it is treated as an afterthought.

Only 8% getting advice

Only 8% of KiwiSaver members get any sort of professional advice. About 65.2% of unadvised people believe they aren’t wealthy enough to require financial advice and 62.5% feel that obtaining such advice is too costly.

However, research by the Financial Services Council found Kiwis who did get some form of financial advice ended up on average with 50% more in their KiwiSaver account, 3.7% more in savings, and numerous other benefits, including financial stablility.

According to KiwiSaver providers, it’s a “no brainer” for mortgage advisers to add KiwiSaver advice to their businesses, as it is going to be an ever-increasing part of the population’s financial wellbeing.

While there are about 10,743 financial advisers across the country, the number dealing exclusively in mortgages is unknown - but this isn’t dampening KiwiSaver providers’ recruitment drive.

To offer KiwiSaver advice, mortgage advisers need to add the financial strand to their Level 5 Certificate. Some providers are actively encouraging mortgage advisers to do so.

Generate is leading the charge by offering financial support, and also coaching, if advisers need a bit of extra help to pass the extra Level 5 strand.

Any mortgage adviser adding KiwiSaver advice to his or her business is making a good diversification decision, says Weini Winslow, Generate’s third party distribution manager.

“For a transactional adviser, it is a good way to add value. The reality is

most mortgage advisers are talking about KiwiSaver regularly, particularly as every first home buyer uses it as part of their deposit.”

She says mortgage advisers are therefore at an important juncture of a client’s life, when the KiwiSaver conversation adds a huge amount of value.

A high-value addition

Blueprint Finance couldn’t agree more. It has been in business for only 18 months, but KiwiSaver has become a big part of what it offers.

Chief executive and mortgage adviser David Chamberlain says, from a business point of view, it is an additional service that doesn’t cost much to add.

His two other business founders initially offered KiwiSaver advice but realised the approach needed streamlining, hiring a specialist adviser rather than doing multiple streams of advice themselves.

Including Kiwisaver has strengthened Blueprint Finance’s relationships with its clients, Chamberlain says.

“For example, if we have a client interested in buying a first home, but they are not quite ready, we can give them KiwiSaver advice to help them achieve this.

“We wouldn’t be able to help to this extent if we did only mortgages.”

Blueprint started out working with three KiwiSaver providers; it now has relationships with eight and wants to add more.

“Being able to offer a wide variety of products means we can cater to more people and keeps us front of mind when they are ready to buy a house.”

A standard fee of 0.4% is charged for KiwiSaver advice, made up from payments by both the client and provider.

home buyer to share their goals and have the confidence Blueprint Finance can help them with their long-term finances.

Meaningful start to conversations

For financial adviser Sandra Spence, Kiwisaver provides an easy and meaningful way to start conversations with clients about long-term financial wellbeing.

This was the aim of when she added KiwiSaver to her business, Dunedin-based Affinity Mortgage Advisors, in 2007.

The cost to integrate KiwiSaver advice into her business was minimal, says Spence, while the licensing and knowledge requirements were achievable.

As KiwiSaver providers pay upfront commission and ongoing trail income, this supports the time and effort invested in advising clients over the long term.

The key is the small service fee Affinity charges, which supports a range of needs if and when the customer requires them.

While KiwiSaver is not yet making money for Blueprint Finance, Chamberlain says it will - as KiwiSaver members’ savings balances increase.

“It is definitely a long-term proposition, but it will eventually pay off as the book increases every month.”

He can’t see KiwiSaver becoming a bigger part of the business than mortgages, however.

“There might be more work involved with getting mortgages over the line, but the pay-off is much larger than KiwiSaver on a one-for-one basis.”

He says if his company is dealing with a client for a mortgage, it has done the hard work and created enough trust for that

‘Being able to offer a wide variety of [Kiwisaver] products means we can cater to more people and keeps us front of mind when they are ready to buy a house’

David Chamberlain

Proven Performance. Unmatched Support.

When it comes to KiwiSaver, long-term performance matters. We’re proud to report that our Moderate, Growth, and Focused Growth KiwiSaver funds have all ranked in the top three for 10-year returns every quarter they’ve been eligible since June 2023.*

Grow your clients’ wealth with our award-winning funds – backed by expert support when you need it.

And don’t just take our word for it – we’ve also been named the 2025 Consumer NZ People’s Choice Award winner for KiwiSaver.

“With the current market volatility, first home buyers are increasingly reliant on their KiwiSaver deposit to get into a property,” says Spence.

“Being able to guide them here is critical, not only for securing a home, but for building future financial confidence in knowing they are receiving comprehensive, tailored advice, not just about a mortgage, but about their financial future more broadly.”

Spence says clients are often surprised by how much of a difference small, informed changes can make over time.

“In our experience, this kind of engagement not only adds measurable value to their portfolios, but also significantly strengthens trust and deepens the adviserclient relationship.”

Not a cashflow machine

It is this same value mortgagehq has seen by offering KiwiSaver advice though its sister company, wealthhq.

Managing director and owner Andrew Malcolm says mortgagehq often finds many of its clients, when they first meet, are naively stuck with default funds and providers.

The value of giving the right KiwiSaver advice, adding emotional and financial benefit to clients, is evidenced in the number who follow the advice and suggestions given to them.

While KiwiSaver has been a good addition to the business, Malcom says it is not easy and certainly not a cashflow machine - but it does open the conversation with clients regarding long-term support of their finances.

‘My view is an adviser needs to focus. You can’t do two or three things, such as mortgages, insurance and KiwiSaver really well at volume’

Campbell Hastie

Pick and choose carefully

Not all mortgage advisers are keen on offering KiwiSaver advice.

Hastie Mortgages owner Campbell Hastie says he considered adding it to his business but it presented another set of compliancerelated hurdles.

“Doing mortgages is enough on its own.

“While there is not much money to be made upfront by offering KiwiSaver advice, there is trail income, and with that I can see the attraction of waking up in 10 years and realising there is a meaningful amount coming in, but it would have to be a major focus.

“And it takes an enormous amount of time to build that trail income up.

“My view is an adviser needs to focus. You can’t do two or three things, such as mortgages, insurance and KiwiSaver really well at volume.”

Hastie says advisers need to pick and choose: focus on, and be good at, just one discipline.

“In my world, that is the mortgage space and I think we are quite good at it.”

He says adding KiwiSaver, or the classic offering of life insurance, would diminish the mortgage-related work, so he prefers to farm that out to the experts in those fields.

The banks learned this lesson, he says.

They moved into life insurance, KiwiSaver and investments and did well for a while, a decade or more ago, but in more recent times have been looking to divest some of those business strands.

He says part of the reason for selling off segments of their business has to be because they can’t do everything at scale well.

“They are good at banking and should just stick to that.”

Default choice

The big four Australian-owned banks dominate New Zealand’s KiwiSaver market, though.

The latest Consumer NZ research shows banks have long been an almost default choice for people deciding where to invest their KiwiSaver funds.

But that looks like it’s starting to change.

About 29% of new members choose their KiwiSaver scheme independently, and 14% are automatically allocated a default scheme.

There is still some reluctance to change providers, with 12% of people feeling it’s too much hassle; 8% have thought about switching but haven’t gotten around to it, and 5% don’t know where to start.

In terms of members, ANZ’s KiwiSaver Growth Fund is at the top of the pile.

It has 244,754 members, who have $5.2 billion under management invested - mainly in equities, listed property and listed infrastructure.

Over its entire KiwiSaver funds, ANZ has $21.9 billion under management.

Next comes ASB KiwiSaver Growth Fund with 157,862 members and $6.4 billion in managed funds, followed by Westpac KiwiSaver Conservative Fund, with 153,267 members and $3.1 billion of managed funds.

KiwiSaver providers pay advisers in several ways – commission and trail based on a client’s continued investment in their product, which can build up substantially over time.

If commission is paid, a client may not

need to pay anything upfront, but he or she needs to know how this might impact the adviser’s recommendation.

A service fee can also be charged by an adviser as a one-off payment or on a recurring basis.

The fee can be a fixed amount, a percentage of a KiwiSaver member’s assets in the account or a combination of both.

Savers getting serious

KiwiSaver provider Consilium says the country is at an inflection point, where KiwiSaver is mature and investors are starting to say, “My balance is at a point where this is serious, and my actions need to become more serious too”.

Managing director Scott Alman says once a large amount of money is at stake, investors usually understand the value of paying for advice.

More mortgage advisers are starting to grasp this, making inquiries and signing up to offer KiwiSaver advice.

Consilium is in the process of creating the tools and training to help mortgage advisers do that.

It manages $9 billion in assets for more than 20,000 clients and has recently launched Evidential KiwiSaver, which targets mid-market advised members through a mix of three diversified funds, as opposed to the group’s self-select scheme, KiwiWRAP, which boasts an average investor balance of $170,000, the highest of any KiwiSaver provider.

Wealth generator

Consilium’s head of advice, Ben Brinkerhoff, believes KiwiSaver can become

a wealth generator over time for many mortgage advisers.

Taking the now $50,000 average value of a KiwiSaver member’s account, Brinkerhoff says an adviser charging a 0.5% fee will make $250 a year from that client.

“Not only has an adviser added about $1,000 to the value of their business immediately, but also created a valuable income stream - because that investment grows every year as clients put more contributions into their KiwiSaver accounts.”

He says even if a mortgage adviser doesn’t add any new KiwiSaver clients to his or her business in a year, that side of the business will still be worth more than it was at the start of the year.

It all starts when a young client walks in the door, Brinkerhoff says.

By treating these relationships respectfully, it is likely an adviser will be able to manage clients’ money as they grow older.

“What that means is these relationships are valuable to the market.”

Kiwisaver books

Another thing for mortgage advisers to consider, says Generate’s Winslow, is that KiwiSaver books are sought after.

“We see a lot of advisers wanting to buy KiwiSaver books. So, if you've got a mortgage client base with KiwiSaver, then it's quite attractive to someone that is looking to buy your book.”

She says Generate is busy recruiting advisers and that it’s never too late to get

started in offering KiwiSaver advice.

“It doesn’t have to be as complex or costly as advisers initially perceive. We can help them embed it.”

Generate, which has 160,000 KiwiSaver members and $6.6 billion under management, initially had six KiwiSaver products and has now launched three new funds at the higher-risk, aggressive end of the scale.

‘If you’ve got a mortgage client base with Kiwisaver, then it’s quite attractive to someone who is looking to buy your book’

Weini Winslow

An enabler

Getting started with KiwiSaver for many mortgage advisers is on a referral basis.

Koura head of distribution Michele Blake says as KiwiSaver is low margin, mortgage advisers need to find the quickest and easiest way to provide advice.

Koura has three models: referral, facilitated and full advice. The facilitated model leverages Koura’s digital advice tools, allowing advisers without their Level 5 Certificate financial strand to have KiwiSaver conversations.

In Blake’s opinion KiwiSaver is an enabler: it opens the door for other products and touch points.

“Initial payments are small, but the lifetime value is extremely high given we expect to keep clients for 25 years.”

Koura has 6,735 members, with $275 million under management.

“The churn rate for KiwiSaver is about 4%

and given account balances rise at about 15% a year, it can become profitable in the long term. That is where Koura has tried to make the process for advisers relatively easy.”

However, she says Koura does have some concerns about the quality of advice given.

“While advisers will consider all KiwiSaver providers, the majority of their volumes go to a single provider.

“Advisers also use some interesting projection methodologies, assuming a continuation of past performance will mean the fund will make a lot more money in the future.

“Past performance does not equal future performance and we believe there are other factors to consider when providing advice.”

New tool for comparison

Mortgage advisers wanting a comparison of KiwiSaver schemes can turn to Quotemonster, which has launched a new service in conjunction with Morningstar,

which is providing the data.

Quotemonster has focused the tool on KiwiSaver funds available to the general public, showing projections, retirement values, historical performance, fees and fund size.

Advice tech lead Aneel Ravji says in terms of research the full tool is still about a month away, but the site is usable now.

While the Retirement Commission’s Sorted site is generally the most used for KiwiSaver advice, and has a wealth of information, Ravji says it is aimed at a consumer level, “whereas our tool is developed for advisers.”

“The information is effectively similar, but it’s a tool that advisers can use to explain concepts and talk clients through all the various options.”

Quotemonster has 1,100 subscribing members and expects this to increase as more mortgage advisers start offering KiwiSaver advice - something Ravji sees fitting in well with their existing business ✚

‘The churn rate for KiwiSaver is about 4% and given account balances rise at about 15% a year, it can become profitable in the long term’

Michele Blake

From sheep shearer to mortgage adviser

Sarah Hewson started a residential and commercial property portfolio while at university, and owned a sheep-shearing business by her early twenties. Now a mother of two, she talks to TMM about her unusual path to becoming an adviser.

BY SALLY LINDSAY

Sarah Hewson wasn’t just very good at sheep-shearing, one of the hardest physical jobs in existence; she had her own shearing business by the time she was 23.

During the seven-and-a-half years she headed up Higgins Shearing (her maiden name), she saw herself and her fellow shearers as professional athletes. She mentored young shearers, competed with them at the famed Golden Shears, and was featured on Country Calendar in 2020, filmed as she travelled to remote Marlborough farms, shearing thousands of sheep with her gang.

When she married and wanted to start a family, the born-and-bred Marlburian gave woolshed work away – and brought the same work ethic and high standards to the world of mortgage advice.

How did you become of the owner of a shearing business?

At Lincoln University, I did a Bachelor of Commerce in agriculture and thought a logical career would be rural banking, but I had always worked casually in shearing sheds and on farms during the holidays.

I got the opportunity through a friend to do wool handling overseas and started learning to shear. I caught the bug and decided I really wanted to pursue it: I enjoyed it, was good at it, and wanted to see where it would go.

When you get the bug, you get it bad, and I got it badly. I spent 18 months travelling, working and building up my shearing skills in England, Germany and Australia. When I returned, I was given the opportunity to start my own shearing business – Higgins Shearingthrough Marlborough contacts.

We travelled to many farms, some for five days or more, shearing thousands of sheep. On many days, I was shearing 300 sheep plus running the rest of the

business. It was at times hard, but a good life.

Why did you sell your shearing business?

I was ready for a change. I had married and was looking at starting a family, and decided the shearing lifestyle was not very family friendly. I felt like I had a world of options and it was hard to narrow them down. But I said to somebody, “I don’t know anything about it, but if I had the opportunity, I think I’d probably be quite interested in being a mortgage adviser.”

A Nelson business gave me a chance and I took to it, although it was a steep

I did a lot of research, read of lot of books, listened to a lot of podcasts and educated myself about that world, figuring out where it could take me and what it could do.

How big is your property portfolio?

To be fair, I have downsized it a lot. With selling the business, starting a family and a new career, and dealing with high interest rates, financially it meant it was going to be really hard to hold on to the rental portfolio, so it has been downsized in a major way.

But it meant I was mortgage-free on our own home when I had my first child.

‘I’ve drawn more on my life experience than the actual qualification in terms of giving good advice’

learning curve dealing with the banks and other lenders.

Throughout running my business, I had also done quite a lot of property investment and had worked quite closely with a mortgage adviser, so I knew a bit about what was involved.

What had made you start investing in property?

I remember vaguely talking about it with my parents when I was at high school. They owned a commercial property, so I was exposed to property investment from a young age.

My dad died while I was at varsity, and my sister and I used our small inheritance to invest in a commercial property. I eventually bought her out.

Once I was able to buy my own home, I was able to purchase more property and it just snowballed from there.

How did you find a job as an adviser?

I started combing job adverts for mortgage-adviser roles. One came up in Nelson. I called the company, said I wasn’t qualified, ‘but here is my CV and life experience’, and asked if they would potentially look at taking on somebody in Blenheim.

The company said yes, I qualified, and spent two years with them. So, I had an established Nelson company offering me advice and helping me build my own client base and name in Blenheim.

Basically, they got me started and I worked from home.

Not long after I started, I fell pregnant with my first child. It worked out quite well to not necessarily be full time in the job.

I left there a few months ago and

Profile

From

Born and bred in Marlborough.

Family

My husband, Colin, and I have two children – Sean, who is two, and baby Oliver, who was born at the start of June. My two sisters and brother also live in the same region.

Outside Work

Living on a lifestyle farm with animals keeps me busy, along with fishing, cake decorating and playing netball.

TV show Blacklist.

Favourite book

Not really a book reader, but enjoy Informed Investor magazine.

Favourite music Country. Motto

Life is 10% what happens to me and 90% how I react to it.

started at the Mortgage Room, based in Blenheim, which suits me better in terms of being able to have a split of office and home-based work.

Did you find your skills in the shearing business transferable?

My business was service-based and being a mortgage adviser is basically a service-based role, too. There have definitely been some transferable skills in terms of being familiar with business accounts for self-employed people.

It also helped that I had a bit of a profile, although to be honest shearing is a specialist rural business.

[But] the rural people who knew me when I was shearing have come to me for mortgage advice. If I’d started in a new region, it would have been very difficult to build a client base.

Has owning your own property portfolio helped you in your mortgage-advice career?

Absolutely. When clients come to me and want to talk about an investment property, I'm more than comfortable running the cashflow numbers for them, discussing the pros and cons of property investment, their goals, what they want to achieve and what sort of properties they should be looking at.

However, I probably work more with first-home buyers, as that is the nature of the market in Blenheim.

Is it important for advisers to have previous real-world work experience?

Yes. In my opinion, the Level 5 certificate mortgage advisers get is a low entry bar.

Getting the certificate is not overly difficult and then the adviser is free to offer advice to clients when they have not actually had much life experience. I’ve drawn more on my life experience than the actual qualification in terms of giving good advice.

It’s easy when qualified to learn the different banks’ policies and lending criteria inside out, but the job is about more than that in terms of understanding clients, what they want to achieve and how we can help them get there.

Many clients have more than one lending option and they need help to find the best option. We end up being the main point of contact for clients, especially for first-home buyers who often don’t understand the process of selling and buying.

Having real world experience means

‘The rural people who knew me when I was shearing have come to me for mortgage advice’

advisers can suggest questions buyers might not have thought of to ask their lawyer or other professionals. It gives the edge to an adviser’s business.

How have you found it dealing with the banks?

That's probably been the biggest learning curve. And probably the most difficult part about becoming an adviser was learning all the different bank polices and small intricacies in each different policy.

I don’t have any special tips. It’s just a matter of the more you do, the more you learn. The more you commit, you become a better adviser. And have a good mentor.

Does there need to be any change in the industry?

It's happening now with the use of AI to upload bank policy documents and to quickly and easily search for an answer you want. It is going to be huge

for new advisers, especially as things change quickly.

Previously, advisers might have learned something new in a policy and then the next week it changes.

Each bank makes slightly different changes that have to be relearned and recommitted to memory.

Having an AI system which can make the changes quickly will make life a lot easier.

At the Mortgage Room, we are definitely looking at adapting to the AI technology that is available. It is quite remarkable what AI can achieve in terms of helping with productivity.

I would also love to see a more open relationship between banks and advisers where our existing clients’ updated loan details and offered interest rates could be available at our fingertips, along with any other relevant mortgage information such as eligible cash and commission clawbacks. ✚

COMING SOON

HYPERLOCAL MARKETING: THE ‘10-MINUTE MARKETING PLAN’

Looking at your potential clients, a large proportion probably lives or works close to your office. Paul Watkins looks at low-cost – mostly free – ways to target them effectively.

Many years ago, letterbox flyers would work for a mortgage adviser.

Real estate agents, property maintenance workers and some tradies still use such devices effectively - but in 2025, will they still work for advisers?

Today’s potential clients aren’t rifling through their letterboxes, as it’s rare that they receive any addressed mail now.

But the idea of promoting to a small local crowd is still a goer, albeit in new formats.

Instead of the letterbox, we spend time scanning community and Facebook marketplace pages, checking the school newsletter, or Googling "mortgage adviser near me" while waiting for a coffee.

Put another way, a very large proportion of your clients is likely to be within a very small radius of your office – probably a 10-minute drive or less away (hence the ‘10-minute marketing plan’).

So, to build a steady stream of leads and long-term trust, the key is to stop shouting and start showing up.

Be known, not found

Hyperlocal marketing is about being known, not just found.

It means embedding yourself in your local area in ways that build connection, not just brand recognition.

‘Warm, word-ofmouth leads are far more likely to convert than cold clicks on Google ads’

Here's how it can work without stuffing a single letterbox.

Big ads on the radio or on billboards may look impressive, but they rarely build the

kind of trust that gets clients referring their mates.

Hyperlocal marketing works because it's grounded in relevance. You're focusing on people within a 10-minute drive who are likely to run into you at the supermarket or the school gate.

There’s power in the “familiar face” effect. If people see your name pop up regularly in helpful, low-key ways, they start to feel like they know you.

And people do business with those they know and trust.

When you last wanted a plumber or electrician, who did you choose?

Bet it wasn’t the one with the flashiest ads, but rather the one your neighbour recommended. Be that one.

Social is crucial

While online options have become at times bewildering, we are still one of the most prolific social-media-using countries.

According to datareportal.com, 78% of Kiwis are actively users of social media, compared to a worldwide average of 64%.

New Zealand is also the biggest user of LinkedIn in the world, with over half the population on the platform.

But it’s not just about running ads. A highly effective (and free!) tool is your local community Facebook group.

Most towns and suburbs have one: "Rangiora Buy/Sell/Chat," "Papamoa Noticeboard," or "Porirua Parents Page." Community Facebook groups are the modern town hall

Don’t sell, educate

The golden rule? Don’t sell - offer education.

Instead of pushing mortgage rates or loan products, offer knowledge.

Answer questions. Be a calm, helpful presence.

Weekly posts such as, “Three things to check before locking in a new fixed rate,” or “Tips for using KiwiSaver for your first home,” or “Six ways to pay off your mortgage quicker” will position you as a local expert.

They might sound clichéd and old hat, but they still hit home.

Be consistent, be polite and follow the group rules. Over time, people will start tagging you in posts when someone asks for a mortgage adviser.

And those warm, word-of-mouth leads are far more likely to convert than cold clicks on Google ads, which are blatant selling.

Target school parents

If you’re looking for a captive, local audience that’s often making big life decisions – such as buying a home or upsizing – target school parents.

With kids at school, most will have mortgages of a reasonable size which need refixing, or a new one for the new home.