TMM What do commerce commission findings mean for advisers? 05/2024

Go further with Finsure

More than just an aggregator, we offer a range of business support solutions to help you maximise your potential.

Intuitive CRM Software

Personalised Marketing Support

Virtual Assistant Solutions

Staff Recruitment Services

Ongoing Training & Education

And much more!

If you would like to discover how Finsure can help you unlock your full potential, scan the code below to book an appointment with our friendly team!

More

22% of New Zealanders are “not familiar at all” with what advisers actually do; Squirrel expands in the South Island; the FMA plans to investigate mortgage-advice transparency; and more news from adviserland.

The latest movers and shakers at The Mortgage Supply Co, CFML Loans, Heartland and more.

Will the OCR cuts see a rise in house prices?

Homeowners are moving house more frequently than ever before.

What to do when business is slow.

A client’s experience provides a timely reminder.

What is advice risk? Steve Wright explains some of the risks advisers face when dealing with life and health insurance.

MORE SCRUTINY AHEAD FOR MORTGAGE ADVISERS

Ido worry regulators are going to make life for mortgage advisers unnecessarily tougher. In this issue we update you on the Commerce Commission’s thinking around mortgage advice. It does seem that they really do not understand how mortgage advice works as some of the ideas floated are frankly daft.

TMM did offer to provide some research to the Commission on how the sector operates but the response was lukewarm.

What is just as concerning is a comment from the Financial Markets Authority that it plans to investigate the mortgage advice sector on the back of the Commerce Commission’s comments.

Give me strength people. Why? What’s the problem they are trying to solve?

For far too many years the FMA has been focussed on financial advice in general, sort of claiming it is a big area of risk.

Yet there is little evidence to back this up.

Where it should be focussing its attention is on what it calls the “boundary” players who offer financial products or services, but which are outside of its official remit.

Of course, the big one currently is Du Val.

But there are plenty of others like crypto players, foreign investment offers you see on social media, and all the foreign exchange/derivatives players. They pose a much higher risk to Kiwis than someone taking out a mortgage.

As an aside, the FMA released its annual report along with the results of a stakeholder survey.

The survey isn’t good reading, showing that fewer stakeholders think the regulator is doing a good job in many areas.

Standing up for advisers

One of the recent developments for advisers has been the birth of a new association, FAMNZ. In this issue we look at the difference between Financial Advice NZ and Financial and Mortgage Advisers Association of NZ.

Here at TMM we are agnostic and not backing one over another. There is clearly a role for an industry organisation, or some group, to go in and bat for mortgage advisers.

Both organisations have differing visions for what they provide members.

At the end of the day any group must deliver value to members.

In some ways mortgage advisers could do with a union type of organisation which stands up to lenders (particularly banks) just like a traditional union represents employees’ rights to employers.

Sure, the relationship in mortgage advice is not an employee/employer one, but there are similarities.

Banks have too much unilateral power of advisers, which is wrong. One example I use is a well-known and highly respected adviser wanted to write a piece for TMM about something a big bank did. This person flagged it with the bank and the head of third party distribution responded saying to the adviser, if you publish that article we will remove your accreditation. Frankly, that is an abuse of power.

On a more positive note!

MARK YOUR DIARY

The sixth annual TMM Better Business is locked in for February 25 in Auckland.

You can find details at www. tmmonline.nz

Philip Macalister Publisher

Head office & Advertising

1448A Hinemoa Street, Rotorua

PO Box 2011, Rotorua

P: 0274 377 527

E: philip@tmmonline.nz

Publisher Philip Macalister

Staff writer Sally Lindsay

Contributors

Paul Watkins, Jenny Ruth, Steve Wright Design Michelle Veysey

The Evolution of Financial Advice

BY KIP HANNA, NZHL GROUP CEO

Despite the challenging economic environment and ongoing concerns around job security, optimism is on the horizon as we look toward 2025.

According to the NZHL 2024 Client Survey:

• 47% of clients believe they will be financially better off in the next 12 months (+2%)

• 13% predict they will be worse off (-19%).

Heading into a more positive economic environment, as interest rates decrease and clients become increasingly financially savvy, more options will become available to homeowners. Advisers will need to rise to the challenge by offering indepth, customised advice to meet the needs of their clients.

Positively, in alignment with what is happening across the Tasman, we see growing demand month on month for advisory services. There is no onesize-fits-all solution for homeowners or investors - the adviser's role is to support informed decision-making with tailored approaches. Whether the goal is wealth creation through property investment or KiwiSaver, paying down debt, or pursuing other financial goals, the solution must match the client’s circumstances.

Personalised advice is becoming an expectation, not a value-add service. To stay competitive and ensure client satisfaction, proactive connection with clients, timely insights (local and international), and looking ahead with options that consider future scenarios

are needed.

We expect to see continued consolidation in the financial advice industry, alongside increased investment in branding, marketing, and technology - allowing advisers to focus on their core role (advice) and meet growing client expectations.

With the industry in growth mode, we anticipate more advisers entering the market to meet the demand for personalised advice- which is critical for the financial well-being of New Zealanders.

At NZHL Group, we also continue in growth mode. As an independent business, we have made strategic investments in technology and growing strong supplier partnerships, allowing us to streamline processes and offer faster turnaround times with market-leading Electronic Applications.

NZHL Group is dedicated to ensuring homeowners and investors have a plan supporting their current financial needs while safeguarding their future. It is vital the protection of client’s assets, income streams, and health and family through insurance, are not treated as discretionary in tough times. This is why NZHL advocates for personalised advice with the right loan and risk protection structures, helping clients make smarter more informed financial decisions.

Our managed home loans, protection options, and the personalised service provided by Mortgage Mentors enable a truly customised approach with access

THERE IS NO ONE-SIZE-FITS-ALL SOLUTION FOR HOMEOWNERS OR INVESTORS - THE ADVISER'S ROLE IS TO SUPPORT INFORMED DECISION-MAKING WITH TAILORED APPROACHES.

to a full panel of suppliers depending on the individual needs of a client.

For NZHL Group, our commitment to clients and advisers is unwavering - financial freedom means supporting them in reaching their goals.

As the industry evolves, we are expanding our services to meet changing needs, such as through our Fire and General and KiwiSaver referral programmes - more holistic options for clients.

NZHL Group is continually investing in technology and focusing on growth - to support more New Zealanders in making the right financial decisions at the right time. Because, at the end of the day, a ‘one-and-done’ approach simply will not cut it.

ABOUT NZHL GROUP

NZHL Group is a Kiwi-owned, respected, and trusted brand – a purpose-driven (financial freedom, faster) home loan and insurance network that offers a solution to support advisers and help put Kiwi in a better financial position.

Part of Kiwi Group Capital Ltd (KGC) which is 100% Government owned, NZHL Group operates with an Independent Board and local business owners nationwide. ✚

Kip Hanna is the CEO at NZHL and has written this opinion piece based on his experience. This article is intended to be general in nature and should not replace personalised business or career advice.

FMA to investigate mortgage advice Retirement Commission backs reverse mortgages – in some cases

The Financial Markets Authority has said it plans to review the mortgage advice sector in the wake of the Commerce Commission's report into banking.

FMA chief executive Samantha Barrass told the recent FSC conference the regulator would be looking to do what it could in the months ahead to respond to the Commerce Commission’s banking report.

The key issue, she said, was transparency in mortgage advice.

"The Minister and the Commerce Commission have clearly expressed concerns about practices in this space," she said.

"We will be looking to work with financial advice providers and firms across the mortgage spectrum to consider how to tackle this issue.

"As the CoFI regime settles in from early next year, there will also be opportunities for us to use our

supervisory engagement with banks to look at the issues raised in the market study from this angle."

The Commerce Commission wanted standardised loan applications and also wanted pro-rata clawbacks and ban on banks using conversion rates. It wants advisers to not only say which lenders are on their panel but also which lenders they don't work with.

Ratings agency positive about Avanti’s marketing position

Ratings agency S&P has kept Avanti Finance's rating at the BB and noted the nonbank lender is becoming less reliant on bank funding.

"Avanti Finance continues to diversify its funding base away from its primary bank provider. As a result, we revised upward our assessment of the company's funding," S&P says.

The company has reduced its reliance on a single bank funding provider, to about 30% as of June 30, from about 80% in 2015.

"We expect Avanti to further diversify its funding. The company's

reliance on funding from a single bank could drop to about 20% over the next six months. As such, we now see the company's funding profile as consistent with more highly rated peers."

S&P expects Avanti will continue to diversify its funding sources by issuing residential mortgage-backed securities, medium-term notes, and asset-backed securities as it grows. "An expanded cross section of banking relationships providing a larger number of warehouse facilities will provide further funding support."

It said Avanti was likely to maintain its niche position in the financial industry.

Research from the Retirement Commission says reverse mortgage products can be a solution for some retirees who are asset-rich but cash-poor.

The report says there is evidence that people are finding it difficult to downsize into smaller homes due to a lack of appropriate properties. On average these households have home equity of just over $600,000.

However, home equity release products - reverse mortgages and home reversions - are not well understood here due to the complexity and costs involved.

Retirement Commission policy lead, Dr Michelle Reyers says while NZ home equity release products appear to be costlier than in larger markets, they can provide an alternative source of income, less costly, than other forms of lending.

“The key to using home equity release products is understanding the costs and benefits and seeking financial advice to see if they are right for you,” she says.

“It’s important to understand that home equity release products have relatively high costs. For reverse mortgages it’s the interest cost. Loan balances on reverse mortgages can grow to a large amount within a short period due to the compounding effect of interest.

“People opting for a reverse mortgage should consider only using the minimum they need to supplement their monthly income rather than larger lump sum withdrawals, as this will slow the rate at which the interest owing builds up over time.”

SAMANTHA BARRASS

DR MICHELLE REYERS

New Zealanders’ limited knowledge about mortgage advice Squirrel expands in South Island

Research commissioned by the Finance and Mortgage Advisers Association of NZ shows the majority of New Zealanders are unfamiliar with the services offered by mortgage advisers, with only 28% indicating that they are extremely or very familiar.

Twenty-two per cent are “not familiar at all”, rising to 34% of nonmortgage holders.

The results come as a surprise considering nearly two-thirds of home loans originated by the big banks come from mortgage advisers and the percentage is arguably higher for the small banks.

FAMNZ managing director Peter

White says the lack of awareness about mortgage advisers is “alarming and embarrassing.”

“It’s clear that we must do things differently so that more New Zealanders understand the advantages we bring,” he said.

Squirrel has acquired a majority stake in Christchurch-based NZ Mortgages and the business will merge with the Squirrel brand. Nathan Miglani founded NZ Mortgages (formerly Loan Market Paramount) in 2017. Miglani has expanded the business from a solo operation to a team of more than 20, serving clients in Christchurch, Rolleston, and beyond.

This is the second major acquisition for Squirrel in recent years, following its merger with Wellington mortgage advisory business The Home Loan Shop in 2022.

Squirrel chief executive David Cunningham said this latest move marked an important next step on the company’s mission of becoming an iconic New Zealand brand with a nationwide presence, and waking New Zealanders up to an easier way of getting a home loan. ✚

Basecorp, our brokers know us for our dependability with straightforward and We offer:

• Competitive, fair rates

• Most approvals within two days of loan application

• Strong industry knowledge, experience and relationships developed from over 25 years in the business

PETER WHITE

People on the move

Where have the Resimac and Bluestone staffers gone?

Resimac and Bluestone both shut up shop in New Zealand recently. TMM asked where have their key staff gone? As reported earlier Resimac NZ chief executive Luke Jackson has moved to Arrow Finance, a relatively new non-bank lender in New Zealand which is currently developing its product offering.

His key offsider at Resimac, head of credit Vincent van der Kraaij, is still with the business. Resimac indicated it intended to put

Mike Pero Mortgages looks for a new boss

Rob Klenner has left Liberty where he was the head of the Mike Pero Mortgages business.

Klenner had been in the role for two years and previously worked at Tower, Vero and Apex Insurance. He has taken up a role with Vero as strategic partnership manager – international brokers.

Liberty is currently advertising the role and says the successful candidate will be responsible for delivering sustainable growth and performance across its Mike Pero Mortgages business. “You will have the opportunity to enhance and leverage the business' special distribution, product, operational and financial assets.”

Amongst other listed requirements

its $600 million book into rundown, but TMM understands both the Resi book and the Bluestone one are now up for sale.

Former Resimac business development manager Ashlene Prasad has taken a similar role at CFML Loans.

CMFL has recently brought the bulk of its distribution in-house, after previously outsourcing it to Funding Partners. It has also launched a new range of lending products this year.

CMFL chief executive Johny Kale says Prasad is a standout in the non-bank market, bringing a wealth of experience and deep industry relationships that will be a tremendous asset to CFML.

"Her addition will not only strengthen our BDM team but also help position us for continued growth.”

Fellow Resi BDM Ben Jamieson is understood to have returned to Heartland Bank. Before joining Resimac he worked for Heartland with

the new MPM head will be, “Driving direction and sales results of the Mike Pero Mortgages sales team while identifying, building and maintaining cross-portfolio relationships.”

And “direct and oversee effective negotiations and ongoing relationships in relation to strategic Mike Pero Mortgages distribution partnerships and alliances.”

its reverse mortgage product.

Resimac lending manager Dannie Wang is due to be start with a financial adviser group soon.

Meanwhile only one of two of Bluestone’s BDMs have announced a new role. Christchurch-based Luke Roberts has joined the Link group as a national growth manager (aka BDM).

During his time with Bluestone, he worked closely with LFG (as a sponsor) to help drive engagement and says he can’t wait to continue to build on the strong relationships he has built across LFG in his new role as national growth manager.

“I’m passionate about helping others succeed, and I’m excited to support the LFG network to grow. What drew me to LFG was the genuine care that advisers show for their clients and each other."

TMM has not heard back from fellow Bluestone BDM Mike Kinley about what he is doing now.

Meanwhile Astute gets a new CE

Astute Financial, which manages the Mortgage Express and Mortgage Supply groups, has quietly appointed a new New Zealand head.

Kona Hatalafale was recently appointed chief executive.

Describing himself as 'an experienced general manager with experience in the banking sector', Hatafale spent three years as the general manager at Fisher and Paykel Credit Union and earlier was general manager at NZCU Employees Credit Union. Earlier in his career he worked at Heartland Bank and ANZ.

His appointment frees up Rose Acton-Adams to return to more of a sales manager role. Also, in recent times former Mortgage Link and Lifetime executive Vicky Devine has assisted with running Astute’s New Zealand operations. She is based in Brisbane with Astute.

ASHLENE PRASAD

ROB KLENNER

David Hart retires

The Mortgage Supply Co co-director David Hart retired at the end of September.

Hart has been an integral part of The Mortgage Supply Co for more than 11 years, bringing leadership, expertise, and professionalism to his role. His career started in 1989, when he

Gold Band Finance expands

Gold Band Finance has appointed Dave Sanders as its manager west coast (South Island) and Sean Trengrove as manager for the top of the South Island, based in Nelson.

Trengrove's recent management experience includes a stint as general manager at McCashin's Brewery and general manager at Raine Group.

He also spent 40 years in the NZ Defence Force rising to Brigadier where he assumed responsibility of all part time military personnel in the NZDF, Cadet Forces and was responsible for expanding the youth development programme by a factor of three.

This last appointment was as the first director of health and safety for the NZDF.

"These appointments reflect a growing client base and demand in these regions in both the investment and borrowing sectors,” Goldband managing director Martin Brennan said.

Liberty appoints underwriter Olga Nicholson has joined Liberty as an underwriter.

quickly become a highly respected figure in the real estate and mortgage brokering industry.

He became the chief executive of Loan Market in 2004. Ten years later he chose to return to his roots as a mortgage adviser, joining The Mortgage Supply Co as both adviser and a director.

Throughout his career, Hart has made significant contributions to the mortgage industry, earning the respect

She has been in banking for almost 10 years in the United Kingdom and New Zealand.

Her career includes stints with NatWest and Barclays banks.

Nicholson said she was looking forward to working with advisers and using her passion for problem-solving to help more customers.

NZFSG splits distribution team

NZFSG has split its distribution team as Loan Market builds a dedicated support network.

NZFSG northern regional manager William Laban and Shaun Fafeita, who looks after the central/southern regions, will now be solely focussed on NZFSG advisers.

Loan Market national director Nicole Ferguson is building her own dedicated support of a team. Recently she appointed Devaney Davis, regional manager, Auckland and Karina Reardon, national support lead.

Meanwhile, Zane Low has joined NZFSG as an Auckland-based regional manager. Previously he was at ANZ as a commercial relationship associate and Partners Life as a BDM.

and admiration of colleagues, clients, and industry partners alike.

Hart’s wife Robyn is also retiring after a similarly distinguished career in banking and mortgage brokering with 10 years of service with The Mortgage Supply Co.

Heartland Group has appointed Andrew Dixson as its chief executive, replacing Jeff Greenslade who earlier this year indicated to the board his intention to step down by the end of this calendar year.

Dixson is currently group chief financial officer and has been with Heartland since 2010.

During that he has been involved in all key parts of Heartland’s evolution, including the initial merger in 2011, New Zealand bank registration in 2012 and Heartland’s listing on the NZX and ASX. He has also played a critical role in the execution of several major strategic acquisitions, including the acquisition of the reverse mortgage businesses in 2014, StockCo Australia in 2022 and Challenger Bank in 2024.

Dixson’s appointment enables a thorough handover to be completed sooner, allowing Greenslade to retire earlier, the company told the NZX. ✚

Account manager Tania Styche has taken on a new role as induction training manager. New chief executive for Heartland

DAVID HART

Homeowners moving more frequently than ever before

Kiwis are moving house more frequently than ever, holding on to their homes for an average of just fiveand-a-half years.

According to new data at realestate. co.nz, Aucklanders move more often than other homeowners – every five years and three months on average –while at the other end of the scale Kiwis stay put for the longest in Taranaki (six years, five months) and Manawatu/

Whanganui (six years, four months).

Spokesperson Vanessa Williams says people move for many reasons: employment opportunities, more space, accommodating aging parents, or downsizing.

“This frequent movement is likely a reflection of changing lifestyle needs and opportunities across New Zealand.”

She says Auckland offers good employment opportunities while catering for lifestyle changes of all kinds, including for those looking for a second home or wanting to downsize

into retirement.

“This could explain why properties are sold more often in this region."

Williams says smaller towns tend to have fewer properties available for sale.

"In smaller regions, limited housing options often lead people to stay in their homes longer while waiting for the ideal property to hit the market. In addition, close-knit communities and businesses like farms can create a deeper connection to the area, making people less inclined to move frequently.”

New housing developments to be underwritten with Crown funds

Plans are being drawn up to guarantee the sale of units in private housing developments that are struggling to secure financing.

Under a new underwrite scheme, the Government says it will temporarily underwrite private housing developments - to support

the construction industry during the economic downturn.

Interest rates remain high while building-consent rates are low, meaning developers are struggling to pre-sell enough dwellings to secure finance for a development.

Housing Minister Chris Bishop says the plan will lower the risk for developers and ensure houses are ready for buyers to enter the market as

interest rates drop.

He says developers will need to be "credible", meaning they need to demonstrate a proven track record of successfully building or selling houses of a similar size and scale.

The development must have a minimum of 30 houses and the developer must have ownership or use of the land, along with all the required resource consents.

Investors ignoring new builds in favour of existing properties

Mortgage adviser Kris Pedersen says secondhand properties are back on investors’ radars.

Pederson, who works mainly with investors, says they are looking at yield, which they can get from blocks of flats and similar types of properties – in the provinces rather than the big cities, where housing markets are depressed.

“Investors can pick up an existing multi-income property which has an attractive cash flow and add value to it by a full renovation or by adding extra bedrooms or living areas.”

Until recently, many investors steered away from existing properties, after the previous Labour Government lifted the Brightline test on them to 10 years and stopped investors from claiming tax deductibility on their mortgage repayments when offset against rental income.

But the Brightline test has been pulled back to two years and tax deductibility will be fully reinstated in the next tax year.

Pedersen, of Kris Pedersen Mortgages, said the market had changed a lot over 15 or 20 years.

“Then, the average first-home buyer would target an older, rundown home,

renovate it, live in it few a few years and sell it and move up the housing ladder.

“Now, first-home buyers aren’t willing to put in the work. They want a home where everything has been renovated to a high standard.

“The OCR cuts have kicked off a large amount of activity in the market. There's probably quite a few investors now who are looking, knowing there will be further OCR cuts and a lower interest rate environment than what has been seen in the last 12-18 months.

“If they can make the numbers stack up, or get close to stacking up, they will have the confidence to buy.”

Caution to home-loan borrowers: be realistic

Now that interest rates are dropping again, Squirrel Mortgages founder John Bolton is cautioning homeloan borrowers to have realistic expectations about what a “good” rate looks like.

Bolton says they don’t want to get caught in the trap of using the insanely low rates of the pandemic as the benchmark for comparison.

“Never say never, but those were highly unusual times, so it feels pretty unlikely that we'll see rates that low again any time soon. And considering it’d take something pretty big, scary and unpredictable to get us there, it’s probably not something we're hoping for anyway.”

He says while the economy feels a little more positive after the first OCR cut in August, any sense of euphoria

was short-lived.

“Huge parts of the economy are feeling depressed. Construction, meat exports, retail and tourism are all weak. And with China’s economy off the boil at the moment, that’s having significant flow-on effects for our forestry sector, too—where cutting down trees for Chinese export is now a loss-making exercise.

“So, while rate cuts will provide some much needed relief for borrowers and businesses, we’re coming back off a very low base confidence-wise. And there’s no quick fix for that.”

Bolton says there’s still a glut of listings on the housing market, meaning “it’s very much a buyers’ market”, but buyers are wary of prices continuing to fall.

individual people

JOHN BOLTON

Will house prices go up following the OCR cuts?

Investors and home-owners are pleased with cuts to the official cash rate (OCR), but other factors are also impacting house prices – including the labour market and a surge of new listings.

BY SALLY LINDSAY

Further cuts to the Reserve Bank's official cash rate (OCR) are not expected be enough to drive housingmarket prices up in the short-term.

The central bank made a supersized cut of 50 basis points to the OCR this month, bringing it down to 4.75%, and financial markets are pricing in another drop of the same size next month.

While this is good news for home owners and investors, QV operations manager James Wilson says although it seems there will be a general uplift in property values on the horizon, conditions aren't yet conducive to growth.

However, the rate at which values are dropping has slowed, from 2% in the three months to August to 1.6% for the three months to September.

QV's September House Price Index shows the average value of New Zealand homes fell to $901,920 in September, from $905,357 in August.

That's a decline of $3,437 for the month, which means average property values dropped by the equivalent of almost $800 a week last month. In the September quarter, the biggest decline of 4.2% was in Napier.

In other main urban districts, Auckland's average value was down 1.7% for the quarter, Hamilton was down 1.2%, along with Tauranga 2.1%, Wellington 3,2% and Christchurch 0.8%.

The only major urban districts to post gains in average dwelling values in the third quarter were Nelson City 0.6%, Queenstown-Lakes 1% and Invercargill 0.2%.

Multi-factor squeeze

Wilson says despite the OCR drop, the cost of borrowing still remains relatively high, the cost of living is restrictive, and there are significant worries about job security - especially in Wellington.

He says a high level of stock for sale was also putting pressure on prices, with more than enough houses for sale to meet the current level of demand.

However, he expects the market to shift as interest rates continued to fall.

“While current market conditions are positive for first-time buyers, falling interest rates will likely increase competition with more investors expected to return to the market.

"This will ramp up the level of competition in the housing market and help to absorb some of that excess stock.

“Values will inevitably tighten again when prospective buyers aren't so spoilt for choice."

Confidence lift

CoreLogic chief property economist Kelvin Davidson says while the OCR is now clearly on a steady downward path and mortgage interest rates are likely to continue to drop, easily producing

a short-term lift in confidence and a stop to falling house prices, there are also plenty of reasons why prices are unlikely to surge upwards again.

“For a start, housing affordability remains stretched, and elevated listings are certainly putting finance-approved buyers in a strong position when it comes to price negotiations.”

But perhaps the most important restraint right now, Davidson says, is the labour market.

Job losses themselves will tend to limit house sales and prices.

“There’s also the knock-on effect on sentiment, even for those people who keep their jobs but don’t feel as secure in their role as they did before. In addition, flatter wages will also tend to subdue the housing market.”

The property data company's Home Value Index, which tracks the estimated value of all residential dwellings throughout the country, declined by a further 0.5% nationally in September.

That was the seventh consecutive monthly fall in the country's median dwelling value. The national median dwelling value has declined from $844,825 in February this year to $805,426 in September, a drop of $39,999 (-4.7%).

The main centres showed a mixed bag of results, with Hamilton down 1.2%, Auckland falling a further 0.7% (pushing the recent falls to a total of more than 7%), and Wellington by 0.5%. Yet Tauranga saw a more modest drop of 0.3%, Christchurch was flat, and Dunedin edged up by 0.1%.

Looking ahead, Davidson says it wouldn’t be a surprise to see limited growth in house prices next year, as mortgage rates drop.

“But keep in mind that lower rates will simply bring forward the timing for the debt-to-income restrictions to start biting; another reason to be cautious about the speed and duration of the next housing cycle.”

DTIs are effectively an “insurance policy” for the Reserve Bank in this cycle. Previously, they might have been wary of cutting too soon, at the risk of driving house prices up. But now DTIs will act to curb that growth.

Sales up, prices down

After the first OCR cut in August, Barfoot & Thomson saw a noticeable increase in its September sales to 986, up from 889 in August and 825 in September last year.

The number of sales were the highest they have been for the month of September since 2020.

The city’s biggest real estate agency says it could signal the the usual spring bounce is underway.

Prices, however, are headed in the opposite direction. The median selling price fell for the third consecutive month to $934,500. That's down from $1,020,000 in June, a drop of $85,500, or -8.4% in three months.

September's median price was also the lowest it has been for the month since 2020.

Barfoot & Thompson’s average selling price declined for the sixth consecutive month to $1,081,269.

The agency received 1,560 new listings in September, the most it has received in September since 2020.

That helped maintain the total number of properties the agency has available for sale at the higher than normal level of 5,039, up 20.2% compared to September last year.

The agency’s stock levels have been above 5,000 since February this year, although they have been slowly dropping for the past five months. The last time Barfoot & Thompson had more than 5,000 residential properties on its books at the end of September was in 2010, which means stock levels are at a 14-year high.

That gives buyers plenty of choice and should help to keep downward pressure on prices over the spring selling season.

Surge of new listings

Although home owners and investors will be rejoicing at the OCR cuts, more homes are expected to come onto the market in the new few months - particularly from people who put them in the rental pool over the past 18 months after prices fell and they couldn’t get a sale at the level they wanted.

Already high stock levels will keep a brake on housing prices, meaning buyers will continue to have plenty to choose from as the market pushes through spring.

Total stock of properties for sale on the realestate.co.nz website is at a 10-year high for September. Listings surged by 9,276, up 15.3% compared to August, and up 18.7% compared to September last year.

That pushed the total stock of residential properties available for sale on the website to 30,028,

up 1.5% compared to August, and up a whopping 27.4% compared to September last year.

The national average asking price of properties on the website remained within its recent range at $870,110.

Vanessa Williams, realestate.co.nz spokeswoman, says, "For almost two years the national average asking price has hovered between $860,000 and $890,000."

That's the longest stretch of price stability on the website since its records began 17 years ago.

"We've never seen prices remain flat for this long," she says.

The combination of high overall stock levels, plenty of fresh stock and flat asking prices suggests buyers are spoilt for choice.

Pass through swift

With most borrowers now on shortterm fixed or floating rates, economist Tony Alexander says the pass-through of falling borrowing costs into the economy and the housing market will be quite swift.

This means the strength in residential real estate activity in his monthly surveys will continue to build.

For instance, a net 39% of mortgage brokers say they are seeing more firsthome buyers in the market. A net 47% are seeing more investors.

“Agents say banks are responding to the improving outlook for housing credit demand by easing their lending criteria bit by bit, although processing times are blowing out once more and this is going to soon start frustrating buyers looking to catch the bottom of the price cycle.”

But just because the real estate market is picking up and facing the future with optimism, Alexander says that does not mean the economy is out of the woods.

“Households are likely to face rising unemployment for much of next year as well as hikes in insurance costs, council rates and power bills. Net migration flows are dropping away rapidly and there is still a net 5% of consumers in my monthly Spending Plans Survey saying that they plan to cut their spending in the next three to six months – not raise it.”

He says overall the acceleration in monetary policy easing is positive for the New Zealand economy – but the main impact probably won’t show for many until the second half of 2025. ✚

What do Commerce Commission recommendations mean for advisers?

The Government says it will act on them, but the way forward still not clear.

Significant changes could lie ahead for mortgage advisers – but what they are and when they might take effect is still unknown.

The Commerce Commission has completed its market study into banking and produced a range of recommendations. The Government is now also conducting its enquiry into banking.

The commission paid significant attention to the role of mortgage advisers throughout the process, and in its final report.

It said mortgage advisers were increasingly being used to navigate the complexity of the home loan market. “They assist customers with the process of obtaining a home loan and can help find lenders who are willing to fund loans that are less straightforward.”

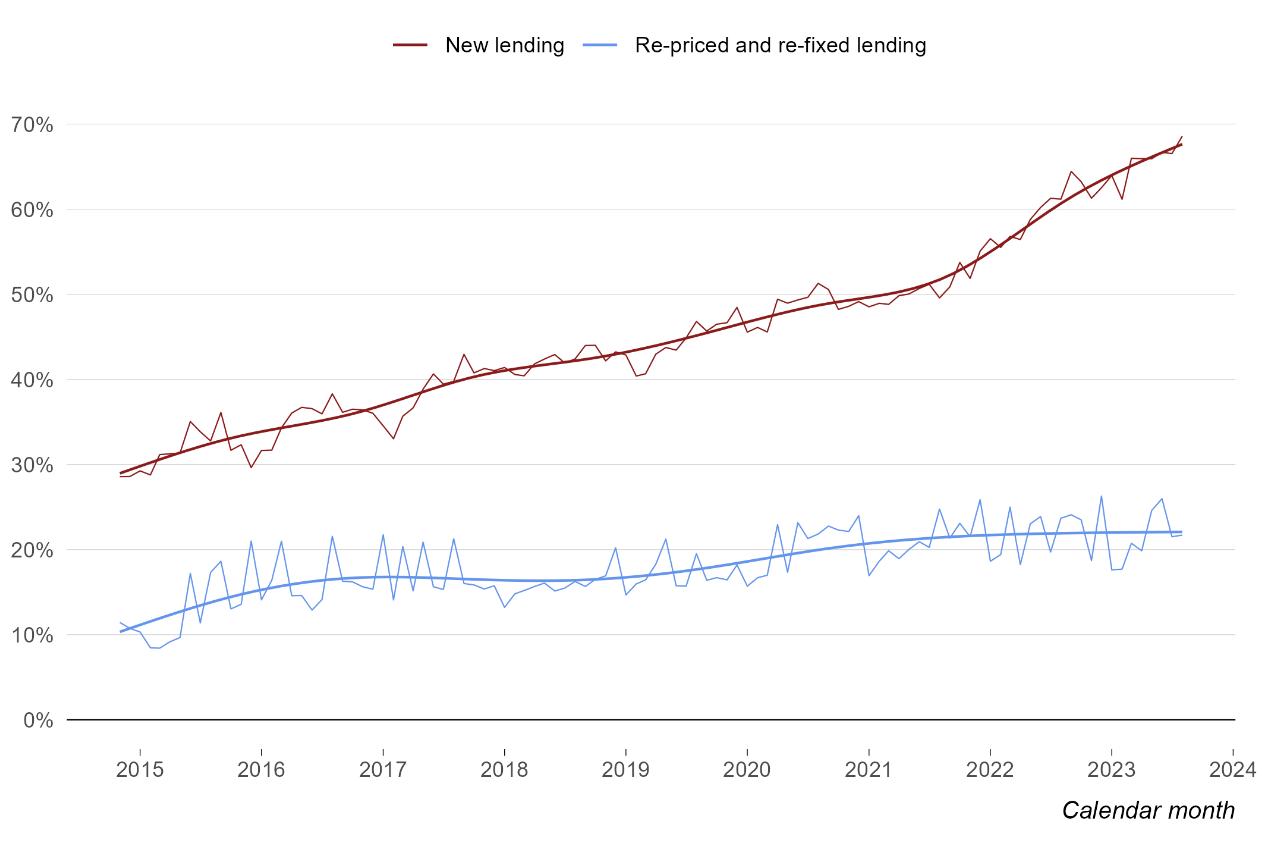

The commission noted that about two-thirds of new home loan lending to owner-occupiers was now happening through mortgage advisers.

“In 2014, just under 30% of new lending and about 11% of repriced lending was facilitated via advisers. By 2023, those figures had increased to 66% and 20%, respectively.

“This trend mirrors the rise of advisers in Australia and the UK.”

It made 14 recommendations that Finance Minister Nicola Willis and Commerce and Consumer Affairs

Minister Andrew Bayly said the Government would act on.

Price focus

The commission said advisers should be “champions of price competition” while also providing holistic financial advice. “We believe the industry needs to go further to promote the best interests of clients. This requires mortgage advisers to be champions of price competition.”

It said while advisers had told it that interest rates were often not the primary consideration for borrowers, it did not accept that price – or the total cost of a home loan more broadly –should not be the number one priority for lenders and mortgage advisers.

The commission said, where possible, advisers should present at least three “actual offers” to clients.

Leigh Hodgetts, country manager for the Finance and Mortgage Advisers Association in New Zealand, said this was the most concerning of the report’s recommendations.

“They’ve picked this up from Australia. Australia do that in practice because they don’t give financial advice – mortgage brokers there have a credit license, they do credit assistance and present three offers.”

She said Australian advisers were not trying to tell clients which offer they would recommend, as advisers in New

Zealand did.

“Mortgage advisers there don’t sit under an advice regime, here in New Zealand they do. Our job is to go and do the research and look at the lenders and who fits best then make recommendations of what the best offer is for the customer.

“It flies in the face of common sense to present three offers here. Banks have at least a 12-day turnaround time. They are blowing up with volume and the market hasn’t even heated up yet with interest rates starting to move down. If we were to have to do a scattergun approach and pick the three best banks and submit three actual offers it would blow up the banking system.”

She said some advisers had already picked up the message that it was what they should be doing and were “scattering” deals. If the turnaround times blew out it would make it harder for people to get finance, she said.

Hodgetts pointed out an adviser might know that a certain client would only be able to get a loan with a particular lender. “Sometimes it’s not a main bank, it’s a non-bank, they might be the only one that would take on a particular client’s circumstances. It’s frustrating for mortgage advisers. There’s no commitment that yes we need to do this now, but we are having discussions.”

Glen McLeod, a mortgage adviser

with Edge Mortgages, said there could be credit score impacts on clients if multiple applications were made on their behalf.

Lenders would not be pleased, either, he said. “If we have to send it out to three, only one is going to win it and the other two are doing it for nothing. How is that going to work? They’re already struggling with volumes… you wouldn’t go to the dairy and get three bottles of milk and taste test them and say ‘I’ll take this one thanks’, it’s a similar situation. We’re meant to be financial experts qualified to be able to give advice.”

Bank processes needed to make it easier for advisers to focus on price and choice of provider, and get those offers, the commission said. It said New Zealand processes were timeconsuming and relatively manual, with applications being submitted

via email, unlike Australia’s more automated processes.

“While we understand and acknowledge that processing loan applications is not without cost, we do not have to look far to see how to reduce costs. In Australia, mortgage advisers can easily access actual prices for multiple providers, and loan applications are placed through standardised online portals rather than by email or phone.”

Claire Matthews, a banking expert at Massey University, said McLeod was right that banks would not be pleased to be part of a quoting process. “The lenders will simply recognise they’re being asked to provide a quote or an offer for comparative purposes and what is the advantage of that? The reality is that mortgage advisers know their market. They know the providers, the lenders, they know the client and

what the client is trying to do, they know which lender is likely best for the client. What is the point of wasting everyone’s time with a whole lot of effort that is simply not worthwhile and potentially becomes confusing for the client?”

The commission also wants offers to be made in a standardised way so that it is easier to compare them.

Panel

The commission said advisers should highlight to customers which banks they were not working with and point out better interest rates available from other lenders that they did not deal with.

“Any reasonable consumer would be surprised to learn that some mortgage advisers only consider a small subset of lenders.”

The commission said it was ’

Mortgage adviser proportion of floating and fixed-term lending up to 2 years to owner-occupiers (monthly values and smoothed trends)

Source: Calculated from data provided by banks to the Commission for the Commerce Commission Personal banking services Final competition report

generally “lucky dip” as to whether people approached a mortgage adviser who could provide complete mortgage advice.

“While by law, an adviser must disclose who they do work with, it is up to the consumer to realise which providers are missing.

“In the consultation conference, we discussed the idea of negative disclosure. This would involveYproviders having an obligation to disclose which providers they do not work with in addition to who they do work with. This idea was criticised by mortgage advisers as impractical and unhelpful for consumers given the large number of lenders.

“We acknowledge that a long list of lenders an adviser does not work with is probably unhelpful for most consumers, but we would expect that advisers would always disclose publicly and discuss with potential clients up front if they cannot work with any of the registered banks that offer residential mortgages. For advisers with a broad panel, we would not expect this to be a very long list at all.”

The commission said there would also be benefits in advisers being more upfront about which lenders they preferred to work with. If the best option for a client was not one the adviser dealt with, they should make that clear in their recommendations.

“Advisers already have terms in their contracts with clients that allow them to charge fees if, after providing advice, the client chooses to go elsewhere, so such practices do not need to leave advisers out of pocket.”

Hamish Patel, of Mortgages

Online, said in his submission to the commission that there was the potential for this requirement to be too onerous. “No other industry is subject to this kind of very vast type of requirement. This is akin to asking mortgage advisers to compare and take into account products that they lack knowledge of. It is almost impossible to police.”

Outcome focus

Hodgetts said it could be that the industry came to an agreement of how it could produce the outcomes the commission wanted, even if the process of getting there was not quite the same.

“If we can open the dialogue and talk about the way things work now with an advice process, maybe we document the three best lenders that we look at or what we researched and checked - and at the end of the day present one offer.”

The industry needed to ask what it was that the commission thought was broken, she said.,

“If you’re giving advice you go through the advice process – maybe we might need to document things better, perhaps putting a bit more information there about what you looked at and considered… it might be just adding an additional step in the process of

‘You wouldn’t go to the dairy and get three bottles of milk and taste test them and say ‘I’ll take this one thanks’’

Glen McLeod

documenting why we went with the lender we have. That’s all done in the statement of advice now by most people. We’re doing it now, we’re just not giving three offers.”

She said advisers would know what the rates were that were being offered by a range of lenders and what cashbacks might be available, or other policies that could apply to clients. “We can come to a determination of what’s the best for a customer.”

McLeod said file reviews already gave advisers the means to justify why they had given certain advice. “It’s not like the old days where you just went in with a calculator and a pen and application form and sent it in. It’s quite sophisticated with what we have to dop these days.”

Hodgetts said advisers had been through a lot of change already. “The FMA did the monitoring report and with the mortgage advisers who were looked at, everything there was looking good. Nothing was fundamentally broken and totally out of hand they need to resolve.”

She said there was no harm in looking at what happened in Australia. “But we follow a different licensing regime. We go above and beyond what Australia does. It’s not broken here at all.”

‘While by law, an adviser must disclose who they do work with, it is up to the consumer to realise which providers are missing.’

Commerce Commission

Best interest, or priority?

The commission said advisers had potential conflicts of interest where they were incentivised to recommend a lender due to a higher commission, or to suggest a higher borrowing amount. It recommended a ban on conversation rate conditions and suggested that clawbacks on mortgage adviser commissions should be prorated.

But it said after further engagement with the Financial Markets Authority and the sector it was more comfortable that there were “relatively clear” expectations on advisers for managing potential conflicts of interest.

Matthews said she would be concerned if the commission conversation were opened again. “While I understand the concern to an extent I’m not convinced there’s evidence it has sufficiently detrimental impacts. I think not having commission would have the potential to limit the availability of advice.”

Jeremy Muir, partner at Minter Ellison Rudd Watts, said it was notable that the commission had delved into the difference between the current focus on giving priority to client interest, rather than a requirement to act in clients’ best interest.

“I remember around the time the Financial Advisers Act was coming in, there was quite a bit of looking at the Australian test and figuring out what the New Zealand version should be and we ended up with something that was fairly watered down in the sense it was more a process-driven test, disclosing conflicts and ensuring you don’t put yourself in a position of conflict as an adviser.

“That’s arguably a different type of requirement than acting in the best interest which could mean you have to take account of all the options in the market and come up with the best answer.”

Muir said the commission’s recommendations were clearly going further than market practice. “The Commerce Commission thinks it would be a good market outcome if they did more but the Commerce Commission is not the regulator of financial advisers. They can say this but then it’s up to the FMA to interpret the law or the Government to change that law. It’s not clear to me what the change will be.”

Matthews said what happened next would probably come down to easy to implement the recommendations proved to be. “If there’s something that can be implemented that, even if it doesn’t have much impact, looks really good, it’s likely to be. Some of the more substantial recommendations potentially not, because it’s too hard.”

Nick Hakes, chief executive of Financial Advice New Zealand, said it would take collaboration across the industry to address the recommendations. “Advisers are well placed to play an active role in collaborating and looking for a sensible implementation framework for these recommendations but that will take time. The very intent of the report is long-term and requires industry collaboration.”

Hakes said the process would end up affecting all advisers. “The potential for impact to advisers is long-term and potentially far reaching.”

“Financial advisers already deliver choice for consumers, they deliver competition. We know through

‘It flies in the face of common sense to present three offers here’

Leigh Hodgetts

research that they deliver good consumer outcomes. That’s really consistent with the purpose of the market study into personal banking services. The advice sector is interested in forming a collaborative working relationship with all parties around a sensible framework for implementation… advisers are well placed to help solve some of the industry challenges, it’s them who are closes to the client conversation.” ✚

‘This is akin to asking mortgage advisers to compare and take into account products that they lack knowledge of. It is almost impossible to police.’

Hamish Patel

Hyundai

Battle for membership slice of New Zealand’s small mortgage adviser market

Two rival organisations are vying for mortgage adviser members as new research shows the majority of Kiwis aren’t familiar with the services advisers provide. Why should advisers join either?

BY SALLY LINDSAY

Earlier this year the big and brash Finance Brokers Association of Australasia (FBAA) came into New Zealand through its newly formed arm, Finance and Mortgage Advisers Association of New Zealand (FAMNZ). It was determined to sweep up members, led by country manager Leigh Hodgetts, who is a former FANZ staffer.

At the time, the more staid but wellestablished Financial Advice New Zealand (FANZ) - led at the time by Katrina Shanks, but now by Nick Hakes - tried to ignore the Australian upstart and couldn’t understand why the FBAA

would want to move across the ditch to a much smaller market.

It questioned whether there was enough room for another adviser association in New Zealand.

Hakes, a Kiwi, relocated from Singapore, at about the same time as FAMNZ was setting up. He had been market development director for Asia at Kaplan Professional. Before that, he was a general manager of member services, partnerships and campus at the Financial Advice Association Australia (AFA).

There are no official figures for the number of mortgage advisers in New Zealand, but recent estimates have put

the figure at about 2000-plus. However, some have dropped out of the industry in the past year as the housing market has tanked.

Although the FBAA’s move into New Zealand hasn’t started a tit-fortat relationship with FANZ, there are clearly feelings on both sides about what they offer to members the other doesn’t.

FBBA managing director Peter White says FAMNZ wants to represent mortgage advisers better than ever before by expanding the market share for them, increasing professionalism and lifting standards.

While it has dubbed itself New

Zealand’s premier advocacy body for financial and mortgage advisers, it has been slow going for FAMNZ building membership. So far, it has attracted 100-plus members and aims to have about 400 by the end of its second year, compared to FANZ’s more than 1500 members.

FAMNZ’s membership includes finance, asset finance, lenders, affiliates and mortgage advisers, while FANZ’s membership includes mortgage, insurance, investment, financial advisers and financial advice providers (FAPs).

While FANZ has a much bigger membership, it doesn’t have a breakdown on how many are mortgage advisers and how many provide advice on insurance and KiwiSaver.

Fees to join FANZ are $74.85 + GST a month, equating to $898.20 + GST for 12 months. FANZ also has an associate membership fee of $46.01 + GST a month and student membership is free.

It is $660 a year to join FAMNZ as an accredited member – either as individuals, partnerships or companies. This includes financial advisers (FA) or FAPs licensed to provide advice on finance or mortgages. Applicants must have a minimum of two years of experience.

There are also a raft of other FAMNZ memberships from $50 a year for a retired member to $3300 a year for a corporate. It is free for students.

What do they offer?

New research, commissioned by FAMNZ, shows only an “alarming and

embarrassing” 28% of New Zealanders are familiar with mortgage advisers.

The results come as a surprise considering nearly two-thirds of home loans by the big banks are originated from mortgage advisers and the percentage may be higher for the small banks.

White says it is clear advisers must do things differently so that more Kiwis understand the advantages they bring. So, is belonging to either FANZ or FAMNZ going to change the perception of mortgage advisers and the fact that many people believe they have to pay a fee to use an adviser?

It will need a huge promotional campaign which neither professional body has in place.

Hakes, in a written response, says FANZ promotes the highest professional standards, so more Kiwis have the confidence to actively seek out its members for life-changing quality financial advice.

“We lead the financial advice industry in the acquisition of world-class knowledge, skills, and networks for the modern financial adviser.”

He says FANZ is the authentic voice of financial advice to the Government, regulators, media, and consumers on the value of quality financial advice which grows, manages and protects the financial well-being of New Zealanders.

“Our role is to lead, support and inspire our adviser members and the broader advice community.”

Hodgetts says FAMNZ’s point of difference is its focus on finance and mortgage advisers only and to deliver targeted professional development and

FANZ and FAMNZ say there are advantages for mortgage advisers in belonging to their organisations. Below are some of the reasons.

• Events, courses, yearly conference

• Professional development

• Professional credentials

• Professional liability programme

• Professional networking opportunities

• Keeping up-to-date with regulations and compliance

• Driving the awareness of the value of advice

• Professional development days twice a year

• Masterclasses to further develop specific skills

• Annual FAMNZ conference

• Opportunity to attend FBAA annual conference in Australia

• Regular coffee meetings around the regions

• Webinars

• Meetings to contribute to consultations and provide feedback on matters that are important to our members

support .

“FAMNZ is run by advisers for advisers and provides members with the opportunity to be recognised as part of a professional association, enhancing their credibility as a professional adviser.”

The association’s aim is to grow finance and mortgage advisers’ market share in the loans industry.

To do this it organises a range of networking opportunities to connect with other members face-to -face on a regular basis across the country.

Rules and regulations

FANZ has a specific New Zealand constitution and member rules, including continuing professional development (CPD), certification, conduct, disciplinary and complaints rules, code of ethics and practice standards.

There is a process and criteria for joining the professional body and ongoing membership rights and obligations along with professional development.

On the other hand, FAMNZ does not have its own specific governance

documents. Members have to adhere to the constitution, code of conduct and disciplinary rules of the FBAA, the Australian parent.

Hodgetts says the FBAA rules are being reviewed to further incorporate FAMNZ.

She says having a code of conduct is essential for the industry’s reputation as professional advisers.

“The FBAA has been operating for more than 21 years and has a strong history and knowledge of how to run associations.”

It also runs a global federation for mortgage brokers/advisers, with FAMNZ being a member representing New Zealand.

Hodgetts says through this association FAMNZ can access knowledge and best practice from a global board of governors and not just Australian influences. “This will assist the New Zealand sector to gain credibility and ensure the industry’s reputation is protected.”

Business partners

FAMNZ has a range of business partners providing services to its

members... They do not provide financial advice themselves and include legal, compliance, training, lender, aggregators and other support services.

Hodgetts says they are kept separate from mortgage advisers, but can still be a FAMNZ member.

It also has corporate memberships for lenders. “Corporate members generally want to support mortgage advisers in an association that represents their interests and provides professional development specifically for finance and mortgage advisers.”

She says mentoring and growth of advisers is important and lenders support FAMNZ as a provider of this training. “We don't have an issue with product providers or lenders being members. Mostly non-bank lenders have joined FAMNZ in this category.”

FANZ has strategic partners, who are not members, including lenders and other service organisations aligned with the advice industry. A head of professional development works with member advisory committees and strategic partners to ensure professional development training is made available under a new framework introduced this year. ✚

Pick up the phone or go see someone, every single day.

To move countries successfully as a teenager, you need grit and grace. Claire McArthur continues to employ both those qualities as a mortgage adviser – along with a key daily habit.

BY SALLY LINDSAY

As a teenager, Claire McArthur left South Africa with her family and moved to Pukekohe. She completed her schooling in Papakura, started out as a teller at Westpac and moved into home lending, before - a decade later - setting up business under her own name instead of a generic one. She has been a mortgage adviser for six and-ahalf years.

McArthur talks to TMM about the grit and grace she needed to establish her own business, and about the needs of the industry.

What is the one thing you decided that you would do consistently, every day, when you set up your own business?

I turned up to the office for my new business, sat at my desk, and there were no emails or phone calls coming in, because nobody knew what I was doing or where I was. I decided that every day I would pick up the phone or go see someone, whether a lawyer or accountant, a networking group or having a coffee with somebody – to

proactively go out and do something, rather than sitting there and expecting everyone to ring me.

How long did it take you to build a client base?

I registered the company in April, was accredited by July, hit the ground running and have never looked back.

I’d decided that if I didn't earn any money in the first six months, then I was probably rubbish at what I was doing and would need to rethink my game plan in life.

More than six years later, I've been busy the whole time. It has taken a lot of grit, especially in Pukekohe, on the outskirts of Auckland.

As a woman was it difficult to start your own mortgage advising business?

It was actually the other way. I knew I could do things my own way.

I've never sensed that it’s difficult for women to set up a business in this industry. I set out not to be a banker, but rather an adviser and advocate for my clients.

I do think, as females, we've definitely got more of a nurturing touch when

it comes to working with clients. We bring something different to the table.

How important is it for a mortgage adviser to have a banking background?

It brings some advantage when you enter the industry. You understand the processes and systems. Even though each bank has its own bespoke internal systems, at least you've got an idea of what's happening behind the scenes whenever a loan application is submitted.

What do you like the most about your business?

The people. Everyone who knows me knows I love to have a chat.

My two administrators and I do a lot of face-to-face meetings with our clients, and I still really love that.

I get a real kick out of saying to someone, “You're in a position to buy a home, let's help you through that journey.”

We build quite a strong personal connection with our clients. Hopefully that keeps them with us.

If somebody asked me, ‘What else would you do?’, I honestly don’t

know. I love the industry; and it serves the population well in getting loans approved and people into homes. What do you think about the companies that do just online mortgage advising?

I know a lot of people just want to be able to have something done, sorted, no frills, no hassle.

There’s a place in the market for that. However, I also believe there’s a place for what we do in terms of offering clients the hands-on personal touch, if that's what they want.

Face-to-face connection is still really good for making sure the client understands the process. It also gives them an opportunity to ask questions, and allows us to make sure that what we're offering them is what they want. While online is convenient, it's a whole lot harder to read the room. When a client is sitting in front of me and I can feel they might be uneasy or unsure, or I ask them a question and their response is not quite where it should be, then it's much easier to peel back the onion to find out what's going on – and what we need to do to assist them better.

Does the industry need some change?

There is definitely room for big technology advances.

The industry is still quite manual. We create an application, send it to our banking colleagues and they then manually replicate what we're sending them. I still can't believe that. Systems integration is way behind and not very good.

The other thing is open banking. Every time we want to see a client's loan details, even though we are the loan originator, we have to go back to the client, get confirmation we can receive that information, then go to the bank.

It’s beyond me why we can't log in and see all of our client’s details, especially when we've initiated the loan.

We need to be able to actively service our clients, which is what the banks want us to do.

Which brings me to the commissionclawback issue. Some lenders make it difficult for us to see that information, so we can service our clients on an ongoing basis.

But they're quick to hit us with a clawback if a customer moves and goes to a different lender.

We don't want to be able to transact on clients’ bank accounts, we just want to be able to see their loan balances and what they're up to. If we could manage that, it could save advisers a headache.

Are there other challenges with banks?

Sometimes a client’s mortgage application through an adviser doesn’t get the outcome they want; the client then goes direct to the bank and magically gets what they asked for.

There seems to be some discrepancy in the different channels. The adviser channel might get a no, then a client going directly to the bank suddenly gets a yes.

That doesn't make us look or feel good, but it's quite common.

Whether a bank has different policies or processes that it is following, compared to what advisers are prescribed and need to do, is hard to work out.

I had a client who was approved by a bank for X amount of dollars and then wanted to come through my business for advice and guidance on the whole home-buying process.

When I looked at the numbers, it was beyond me how the loan was

Claire McArthur

From

I was born in Durban, South Africa, and grew up there. I moved here as a teenager and have been in Pukekohe for the past 10 or so years

Family

I've got a couple of furry dogs and my partner. I come from a big blended family, so there's always something going on.

Outside Work

I enjoy going to the gym, getting outside, doing some walks, gardening (although I'm not a very good gardener), and reading.

TV show

I'm on about my third round of reruns of Friends, but I'm not much of a TV watcher. I would rather be doing something else.

Favourite book

April Fool's Day by Bryce Courtney.

Favourite music

I am a sucker for 80 and 90 classics.

Motto

Grit and grace.

approved by the bank, because I couldn't get the numbers to approval. I believed the client could service the mortgage, but how the bank came to that approval versus the tools I've got, the information I had… I couldn't get it to that approval.

I told the client to take the bank mortgage and run with it. What banks and advisers need in terms of numbers and information should be one the same if we are all adhering to the legislation.

The recent Commerce Commission enquiry into banking competition recommended advisers put offers from three lenders in front of clients. Is this realistic?

No, all it does is clog up the system. Our banking partners already get frustrated if we put a mortgage application in front of two lenders. A client is only ever going to go with one lender, so saying go to three is a bit much and it’s only going to result in a lot of work done for nothing, by both advisers and the banks. The regulations and compliance as they

stand, requiring advisers to cover off why a specific lender was approached for a client, should be adequate.

The Commission says it will improve competition. Will it?

Competition should be driven through interest rates, better terms and better product offerings for clients. New Zealand is a small market and I just wonder if the commission is looking too hard at the Australian market, which is much bigger, with a larger range of banks and lenders and more options.

Apart from mortgage advice is your business going to expand?

We are planning to move into KiwiSaver after I complete my assignments. It’s a good add-on product, as KiwiSaver is a big part of home buying, particularly for firsttime buyers.

A lot of people using KiwiSaver just set it and forget it, so there’s a gap in the market for good advice.

We can give that advice, as we go through their daily household expenses, looking at their income and where it is going.

But while KiwiSaver will become part

of the business, I don’t intend hiring advisers. I want to keep the business bespoke, hence my personal name is on it. ✚

WHAT TO DO WHEN BUSINESS IS SLOW

A sluggish market is a signal to be more aggressive, not less, in how your promote yourself.

BY PAUL WATKINS

Marketing is often seen as expensive - and when business is slow, the first thing that normally goes is the marketing budget.

For example, if marketing equals 2% of revenue normally, and revenue slows, then that 2% becomes 1% or stops altogether. Big mistake!

This is not the way to do it, of course. Your marketing spend should remain the same in dollar terms, but change in terms of what you spend it on and the message.

And you can rely on the fact that most of your competition will probably pull back in their marketing activities.

Winning business in a slow market generally comes at the expense of someone else, as there is less business to go round. So be aggressive in such a market.

Find the opportunities

Why is the market slow? There are probably 50 reasons, but a lot of people will be waiting for interest rates to fall before buying or selling, and house prices are lower than they may have bought for.

So where are the opportunities? Education!

Let’s face it: your clients are mostly ignorant of the intricacies of mortgages,

such as how to pay them off quicker, how to structure them to best longterm effect, how interest rates are not the critical issue, and how lower house prices are an opportunity, not a bad thing. The list goes on.

But clients and prospects don’t know that or give time to thinking about such things.

‘Without wanting to insult your clients, you all know that most have no idea about the reality of mortgages’

So, how do you teach them that this is an opportunity, and, at the same time, promote yourself as the expert, to stand out in the crowd?

The primary ways are social media and client comms such as frequent, single-topic newsletters (yes, I know you think these are old-hat, but they

genuinely work. No other media can give the same message.

Video is king

Facebook, Instagram and TikTok still lead the way in terms of the number of eyes and ears on them.

Traditional media is losing the race and can be very expensive, but the more important fact is that video is king. Here is a to-do list for you:

1. Think up 10 topics which would educate specific groups of clients and prospects on how the current market is an opportunity.

2. Make up some video scripts, no more than 90 seconds for each one (use AI to help with both the ideas and the scripts)

3. Video yourself presenting them in a casual, non-sales-like manner. Sort of like a fireside chat. If you are not comfortable with being on video (many are not, which is fine) then find a team member who is.

4. Pick the right media for each one. TikTok for those under 35, Facebook for 30-55-yearolds (refixing and investment property buyers), and Instagram for a slightly female biasbut make sure the video is visually appealing.

‘You can rely on the fact that most of your competition will probably pull back in their marketing activities’

5. Have someone who knows what they are doing edit, brand and place them on the chosen media. Send out single-topic newsletters, which can be based on the scripts for the videos, or with links to the videos on your own website, where you should be running them as blogs.

Why do so few advisers do stuff like this? From my conversations in the sector, it's because it's quite labourintensive.

So don’t do it yourself. Buy in the required expertise – it’s not expensive. Have someone hold the camera and then go and edit and post for you. Your role is just the ideas for the videos and who you want to target.

Room to educate

Without wanting to insult your clients, you all know that most have no idea about the reality of mortgages.

How much of a difference will it make if the interest rate is 0.5 to 1% higher than they want to pay, if the house is $100,000 cheaper than it was a year ago? They will never do the maths.

Media talk of slow-downs and house price falls, with the possibility of falling rates, can significantly influence the public’s thinking.

It’s your job to counter the doom and gloom and put some reality back

into their lives, so they can get what they want.

As a starter for you, I did a quick AI check; the following are some topics which came up for educational videos in a slow market.

1. Promote pre-approval programmes: Many buyers are holding off for lower interest rates.

Offering a pre-approval service which locks in current rates, or offers flexibility for future rate drops, can be attractive. Market it as a way for buyers to be prepared when the rates eventually fall.

2. With prices low, the investment market is an option: Do the maths for them so they can see the opportunity.

3. Refinancing opportunities: Some homeowners might want to know the impact of better terms when the rates drop or how to better structure the borrowings. Prepare them to ease their minds.

4. Target niche markets: This is a key component and one that is mostly ignored. There will never be one message that suits all. I am on the newsletter list for a few brokers, and I don’t get it.

They will be sending the same newsletter to people from ages 25 to 65, under all circumstances, all income levels and all types of mortgages. Break your database into several segments, one for each type of client or stage of life. You may end up with 10 segments, each of which will require a different message. Yes, this is a lot of work, but absolutely worth it. It will pay dividends almost immediately.

5. Buying and selling in the same market: Your house has dropped 10-15%, but so has the one you will be buying. This one always surprises me.

6. Highlight benefits of buying in a down market: Sounds so obvious, so why not tell them?

The advice in this column may sound rather basic, but it’s critical to your bottom line: if business is slow, take advantage of the downtime to pick up your marketing efforts.

Segment your database, work out some educational topics, make videos of these (NOT brand or sale videos), and have an expert post them for maximum impact on your target markets. ✚ Paul Watkins is a marketing adviser to the financial services industry.

PAUL WATKINS

In deep water

Prologue: For many New Zealanders, it goes without saying that buying a home is one of the biggest financial commitments they’ll ever make. But what happens when, due to illness, a person can no longer meet that commitment. Suddenly life seems very uncertain. That’s why having a personal life insurance plan in place that can help relieve the financial burden of not being able to earn an income, is an essential. Our client’s dramatic story is a timely reminder that New Zealanders are looking for quality protection when it really counts…

Morning smoko had just ended. Reece, a 38-year-old experienced builder, needed to get back to work on the house. He placed his feet on the first couple of rungs of the ladder and promptly blacked-out. He fell backwards straight into a wall before slumping to the ground unconscious.

Reece was a super fit guy. Not only was

he a skilled builder, he’d also won several national sailing titles in New Zealand and Australia.

Reece lay unconscious for about 20 seconds. It was touch and go. He was rushed to hospital with a suspected heart attack. After a battery of tests, the doctors diagnosed cardiomyopathy, a condition which had damaged and severely weakened his heart. They inserted a high-tech device in his chest which acts as a defibrillator and pacemaker to assist his heart.

Out of the blue, life had completely changed course for the husband, father, builder, and sailor.

Reece couldn’t continue his dream job. Suddenly, he was imagining years of rehabilitation, stress, and looming financial disaster for him and his family. In that first week in hospital, Reece started to worry about money.

“When they said I couldn’t keep working as a builder, I thought but that’s paying for the roof over our heads. Now what can we do?” says Reece.

“I was a typical young father with a child and we were trying to have another, and we had just bought our first home complete

with a large mortgage.”

As a contract builder, Reece didn’t have sick pay and there was no protection for him other than the life insurances he had taken out. ACC was no help, either. That’s because it wasn’t an accident. If he’d hurt his back when he hit the ground, they would have potentially covered that, but this was a medical event.

The old man and the sea

Luckily, when Reece had bought his house a few years before, he paid attention to a highly experienced financial adviser who also happened to be his father.

“Dad calculated that if something terrible happens to you, your family need to be left with a roof over their heads. They need to be able to hold their ground and then move forward whatever happens. Some people think they need to have lots of insurance so if something happens their family will be better off. But Dad said to me that that’s going to be horribly expensive and that that’s not necessarily the idea of insurance. The idea is to buy what you can afford to give you opportunity so you can move forward. That made sense to me.“