an update Monday 6th July. This week's headlines:

Introducing our all-new full time System Trainer!

We are delighted to confirm that Scarlett Mackenzie, Training Manager has taken up the role as System Trainer for Just Mortgages. Her role is dedicated to helping you make the very most of Smartr365 and the integration with Concert Hub and to also support you in system features and familiarisation challenges.

There will be training events on every week and the first of these are below. As these sessions are designed to be two way, numbers will be capped – but as these sessions are repeated, if one is full you can simply attend the next available session. This resource is at your disposal and we are very keen to hear on specific areas and topics you require help on, please let your Area Director know of these in the first instance.

Tuesday 8 July 11:00

Take charge of your diary management and know what is going on with all your clients!

Tuesday 8 July 13:00

Take charge of your diary management and know what is going on with all your clients! BookHere

Wednesday 9 July 11:00

Take charge of your diary management and know what is going on with all your clients!

Book Here

Smartr Client Portal

Wednesday 9 July 09:30

Bring a new level of professionalism to your services as an Adviser by using the Smartr 365 Portal. Cut down on time entering data, and up the time spent on quality advice.

Book Here

Wednesday 9 July 12:30

Getting a credit report on the client which pre-fills credit commitments and even some of the budget planner for you, can really save time and give a clear picture of the client's financial situation.

Book Here

Further to previous updates and the release of the first sprint week commencing 23 June, we can confirm that work is currently going to plan for the next release week commencing 16 July. This second sprint is planned to contain: rd th

In combination this will remove up to 21 validation links currently being presented to you upon making the jump to Concert Hub and we therefore anticipate this will significantly reduce the time spent in Concert Hub.

We will continue to update you as this work approaches the release date.

During the period 2 June 2025 to 31 August 2025 inclusive, for each referral we receive using the link (see below) will be entered into a prize draw and the first drawn ticket shortly after the competition ends will win this fabulous LG 55” 4k Smart TV!

At the time of writing, TOM MARSDEN still has the most referrals in the hat for our prize draw, but plenty of time remains to add your name in!

We are looking for great candidates to join Just Mortgages! Whether they are currently employed or selfemployed. So, if you have friends, family or simply someone you know who may be interested in a no obligation discussion, please refer them to us.

Along with the chance of winning this fabulous TV, you will still be paid £1000 (£500 paid upon authorisation, further £500 after 6 months). There is no limit to how many candidates you can refer to us.

As a reminder, payment will still be made even if the adviser is to work under the referrer (principal)

Simply click on the following link HERE to refer

The Co-operative Bank have launched its new Access product range. The new Access products from The Cooperative Bank give clients access to products that don’t meet the criteria of high street lenders due to credit blips.

As part of the launch, The Co-operative Bank is moving the point you select a mortgage product to the end of its Decision in Principle. When the Decision in Principle has been completed, and eligibility has been assessed, you will be presented with the product selection screen. The products that are presented will be based on the criteria your client meets. This will either be The Co-operative’s Core products or the new Access product range.

The Co-operative Bank’s new Access products will have their own distinct product codes, which will include ‘AC’ (Example 2X3691ACT6). The Access range provides residential mortgages to applicants who meet the following criteria:

Maximum loan size is £1,000,000

Maximum LTV is 85% for purchase and remortgage only (replacing the existing mortgage £ for £), For all other loan purposes the maximum LTV is 80%

Interest only maximum LTV is 65%. This can be increased to 75% LTV where the extra borrowing over 65% LTV is on a repayment basis

Any value and number of CCJs is acceptable when over 36 months old. If less than or equal to 36 months old, the total value of CCJs must be <= £300. There is no distinction between satisfied and unsatisfied CCJs

Any value default is acceptable when over 36 months old. If less than or equal to 36 months old the total value of defaults must be <=£1,000. There is no distinction between satisfied and unsatisfied defaults

Maximum number of defaults is 5 (satisfied or unsatisfied)

Bankruptcy or Sequestration discharged more than 3 years ago will be considered

Individual voluntary arrangement (IVA) or a Trust

Deed (TD) which ended more than 3 years ago will be considered

Applicants deemed to have high indebtedness will be declined

All other criteria remains unchanged. The time since CCJ/Default/Bankruptcy/IVA occurred is based on when the credit search is completed.

With immediate effect, HSBC have introduced a ‘Cancel’ button on their Broker Platform, allowing you to cancel the application without the need to contact the Broker Helpdesk. Once the Product Switch application has been cancelled, you can then key a new application on a new rate.

Please note, if a booking fee has already been paid, you will still need to contact the Broker Helpdesk using ‘Chat with us’ to request the change.

Current Service Levels – Please note, HSBC Service Levels are now updated daily on the broker website

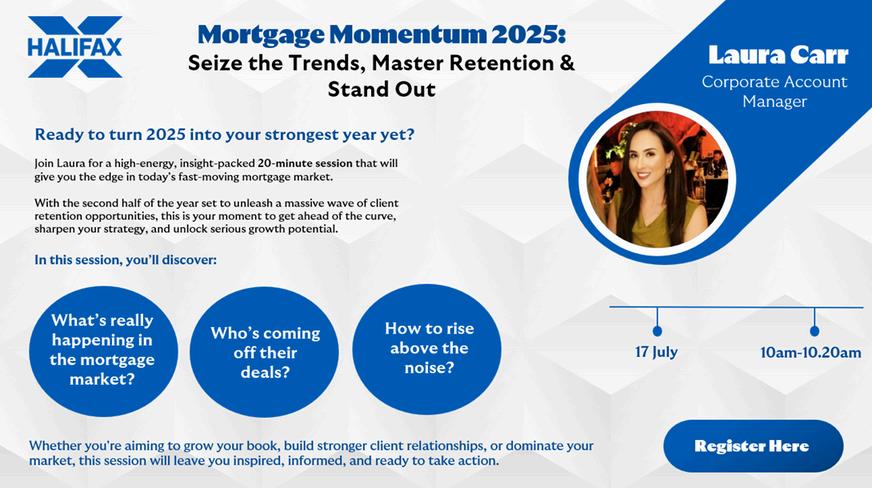

Join Laura Carr, Corporate Account Manager on the 17 July at 10am for a highly informative webinar that will give you some incredibly useful insights into the huge client retention opportunities in H2 2025 th

Simply click on the graphic below to register or click HERE

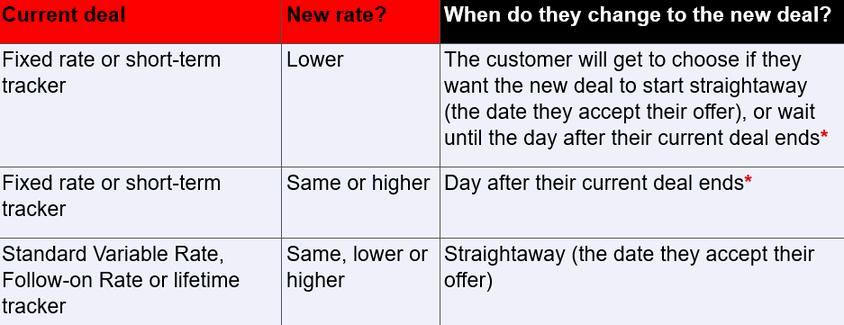

From Friday 4 July, when your client accepts a new product transfer deal with Santander that’s lower than their current one, they’ll get to choose when they want it to start.

*or the day before the completion deadline of the new deal, whichever is first.

If your client chooses to start their new deal straightaway, they won’t be able to change or cancel it. There’s no cooling off period.

For product transfer offers issued before 4 July but not yet accepted, clients will get the option to start their new deal straightaway if it's lower than their current one.

8 July 10:30am-11:30am th

Join Royal London for a Just Mortgages EXCLUSIVE to talk about Family Income Benefit!

They have a special guest Shelley Read, who will delve into the main features of family income benefit policies, including term assurance, life or critical illness cover, and the importance of indexing income-based policies.

They will bring the concept to life with real-world scenarios, such as divorced clients, education costs, renters, and families, demonstrating how family income benefit can add value in various situations.

Additionally, they will discuss the benefits of indexation and how it helps maintain the real value of protection over time.

1. Be able to describe the main features of a family income benefit policy

2. Have a clearer understanding of the types of clients who would benefit from a family income benefit policy and how to position it

3. Have a better understanding of the importance of indexing income-based policies

UK mortgage market entered the summer period with lenders initiating a mini price war by trimming fixed-rate offers. For example, Gen H cut two‐year fixes by up to 50bps and five‐year terms by 5–20bps to stay competitive

Average two‐year fixed mortgage rates fell to around 4.62–5.12%, with five‐year fixes near 4.58–5.09%, reflecting modest easing as the BankofEngland held base rates steady at 4.25% According to NerdWallet and Which?

BoE surveys suggest mortgage demand may soften over the summer, though remortgaging approvals surged in May, reaching the highest level since early 2024. This indicates homeowners are seizing current deals ahead of upcoming rate moves.

The FCA launched Discussion Paper DP25/2 on 25 June, exploring regulatory reform in responsible lending, affordability stress testing, later-life lending, and disclosure rules a public consultation open until 19 September

Chancellor Rachel Reeves is expected to cut the cash ISA allowance for the first time since 1999 to possibly £4–5k, aiming to shift savers into investments. Lenders warn this may tighten mortgage funding, reduce deposits, and ultimately raise borrowing costs