Leadership in professional consulting

Unit:CMI 721

Ofqual Reference F/618/1307

Pathways to Level 7 Professional Consulting| August2020 | v02

Unit:CMI 721

Ofqual Reference F/618/1307

Pathways to Level 7 Professional Consulting| August2020 | v02

Professional consulting requires a multi-dimensional approach to leadership. Within the role, consultants need to be adept, confident and have credibility.

Scenarios for consulting will typically be complex and involve building relationships with other senior leaders.

Consultants may lead internal and/or external teams and work at board level.

Consultants must not only have a macro view of an organisation’s strategic context, they must also understand the impact of digital, technological and geopolitical change.

The aim of this unit is to equip professional consultants with an in-depth understanding of leadership within a consulting context and the strategies which may be used to optimise the way people are developed and led.

Purpose, direction, strategy, leadership,culture, roles, responsibilities,theory, approaches, adaptability,success.

1. Understand the role of leadership in professional consulting

2. Understand strategies for optimising the way people are developed and led

• Learning Outcome 1:

• Understand the role of leadership in professional consulting

AC 1.1 Critically appraise the role of leadership in providingpurpose and direction to clients

AC 1.2 Critique the application of leadership strategies in professional consulting

AC 1.3 Critically reflect on how leadership styles can be adapted to respond to the challenge of delivering client-centric professional consulting

AC 1.1 Criticallyappraisethe role of leadership in providing purpose and direction to clients

CommandVerb is Critically Appraise -Appraise - Assess, estimate the worth, value, quality,performance. Consider carefullyto form an opinion.

Critically Appraise - As with appraise, a systematic process used to identify the strengths and weaknesses of information in order to assess the usefulness and validity.

AC 1.1 Critically appraise the role of leadership in providing purpose and directionto clients

AC 1.1 Role of leadershipwithin professional consulting:

● Defines, shapes and communicates organisationalpurpose, vision, mission, culture and values.

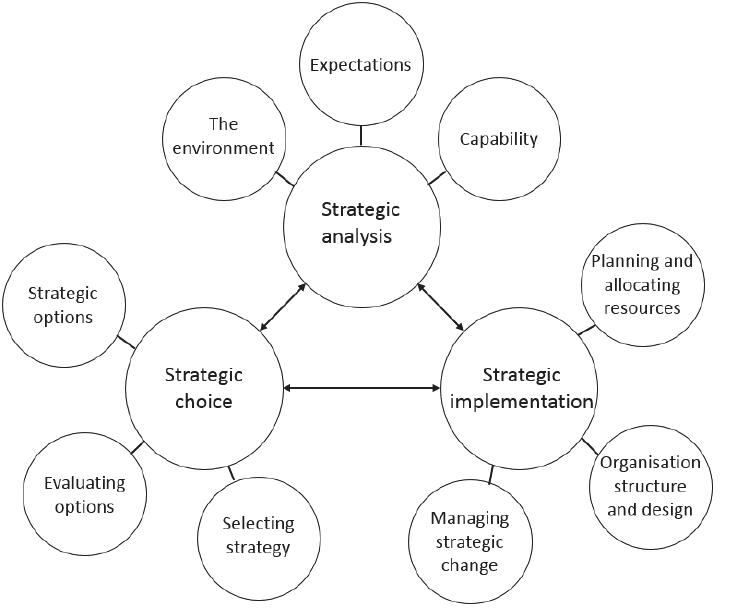

● Develops the strategicdirection of the organisation. Developmentof strategicgoals. Consider strategicoptions (e.g. risk, financial, reputational, legal, management, competitive advantage). Supports implementationof strategicplan.

AC 1.1 Critically appraise the role of leadership in providingpurpose and directionto clients

AC 1.1 Role of leadershipwithin professional consulting:

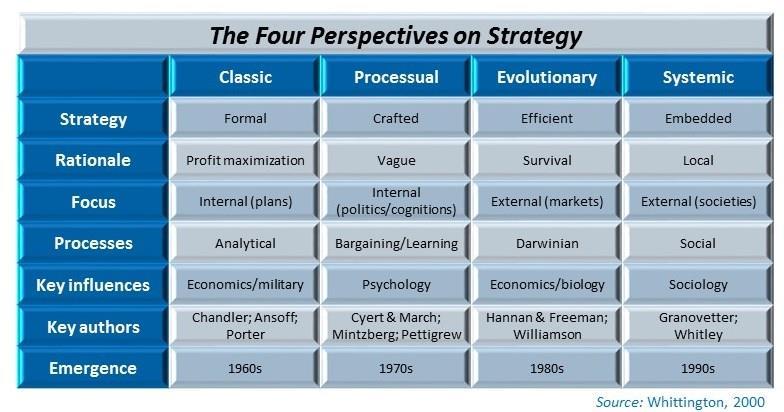

● Creates and selects strategy. (Planned. Intended. Emergent. Deliberate. Opportunistic, Whittington, 2000). Resource based view of the firm (Barney, 1991). Scenario planningand rationalplanningmodel. StrategicPlanningas a Top Down/Bottom up process.

The Five Ps of Strategy (Mintzberg, 1987).

● Leads the organisationethically and legally in line with board and organisationalgovernance. Diversity and Inclusion (Kirton et al. 2014). Definition and Values (Patrick and Kumar, 2012).

AC 1.1 Critically appraise the role of leadership in providingpurpose and directionto clients

AC 1.1 Role of leadershipwithin professional consulting:

● Leads individuals and teams with impact (Belbin, 1981). Develops people and their capabilities.

● Collaborates with partners and manages complexrelationships with multiple and diverse stakeholders/customers. Stakeholder management(Lindgreen et al. 2019).

● Anticipates and predicts future opportunities and threats for industry, sector, technical specialism (Horizon scanning).

AC 1.1 Critically appraise the role of leadership in providingpurpose and directionto clients

AC 1.1 Role of leadershipwithin professional consulting:

● Initiates, leads change and innovation.

Recommends types and approaches of change (e.g. incremental and transformationalchange).

Identifies drivers of change and new ways of working across infrastructure, processes, people and culture and sustainability.

Applies different theories/models of change (e.g. Eight Step Change Model (Kotter, 2012), Radical Change within Traditional Structures (Oswick, 2015)).

Creates an environmentfor innovationand creativity.

Selects and applies tools and techniquesto support innovation and change.

AC 1.1 Critically appraise the role of leadership in providing purpose and direction to clients

AC 1.1 Role of leadership within professional consulting:

● Drives continuous improvement (e.g. Kaizen).

Selects and applies tools and techniques (e.g. LEAN methods (Krafcik, 1988).

Six Sigma (Pyzdek and Keller, 2018).

Statistical Process Control ‘SPC’ (Salacinski, 2015).

● Applies soft systems thinking to understand complexity (Checkland, 1999; Senge, 1990).

● Recognises the importance of brand relationship and reputation management.

● Applies financial measures, considers financial sustainability and accountability. Manages resources and measures outcomes.

AC 1.2 Critique the application of leadershipstrategiesin professionalconsulting

AC Command Verb - Critique -A detailed analysis and assessment of something, especially a literary, philosophical, or political theory.

Analyse - Break the subject or complex situation(s) into separate parts and examine each part in detail; identify the main issues and show how the main ideas are related to practice and why they are important.

Reference to current research or theory may support the analysis.

AC 1.2 Critique the application of leadershipstrategiesin professionalconsulting

AC 1.2 Leadership Strategies

Theoretical concepts:

• Value-driven Leadership (Gentile, 2014).

• Leadingwith integrity (Blanchard,2011).

• Resonant Leadership (McKee, Boyatzis and Goleman 2003).

• Five Practices of Exemplary Leadership (Kouzes and Posner, 1987).

• Ethical Leadership (Mendoncaand Kanungo, 2007).

• Leadership Styles (Goleman, 1995).

• Entrepreneurial Leadership (Roebuck, 2014).

• AuthenticLeadership(Goffee and Jones, 2011).

AC 1.2 Critique the application of leadership strategies in professional consulting

AC 1.2 Leadership Strategies

Theoretical concepts:

• The Servant Leader(Greenleaf, 1977).

• Cross Cultural Leadership (Hofstede, 1991).

• Transformational Leadership (Bass and Riggio, 2006).

• Start with Why (Sinek, 2011).

• Implications/drawback of Western based leadership in global context, Project

• GLOBE ‘Global Leadership and Organisational BehaviourEffectiveness’ (House etal, 2004).

• Situational Leadership (Hersey and Blanchard, 2012).

• Distributed leadership (Gronn, 2000).

• The Combat Estimate (7 Questions) (Ministry of Defence).

AC 1.3 Critically reflect on how leadership styles can be adapted to respondto the challenge of deliveringclient-centricprofessional consulting

AC Command Verb –Critically Reflect - As with reflect, but identifying, questioning, and assessing deeply-held beliefs and assumptions about a topic, the way in which we perceive events and issues, beliefs, feelings, and actions.

Reflect - Consciously contemplate, appraise or give balanced consideration to an action or issue.

AC 1.3 Critically reflect on how leadership styles can be adapted to respond to the challenge of delivering client-centric professional consulting

Criteria LO1

AC 1.3 Challenge of delivering client centric professional consulting

Client-centric: e.g. consulting with individuals, teams, board members.

AC 1.3 Critically reflect on how leadership styles can be adapted to respond to the challenge of delivering clientcentric professional consulting

AC 1.3 Challenge of delivering client centric professional consulting

Challenges in leading others:

• Understanding of who is leading and who is being led.

• Scope of leadership (e.g. leading consultants, clients, researchers, administrators, other team members, suppliers, partners).

• Different organisational behaviours and knowledge requirements.

• Leading without authority.

• Lack of buy-in from individuals within client organisation.

• Ability to adapt leadership style (adaptability).

AC 1.3 Critically reflect on how leadership styles can be adapted to respond to the challenge of deliveringclient-centricprofessional consulting

AC 1.3 Challenge of deliveringclient centric professional consulting

Challenges in leadingothers:

• Establishingcredibility (e.g. leadershipcredentialsnot recognised, disconnect between industry specialists and career consultants).

• Communication breakdown/lack of communication.

• Ability to interpret and articulate solutions back to the client.

• Client perception (e.g. challenges are unique to the sector). Delivering difficult news. Articulatingvalue of consultancy (e.g. financial and non-financial benefits). Reputation/stereotypes regardingconsultants.

AC 1.3 Critically reflect on how leadership styles can be adapted to respond to the challenge of delivering clientcentric professional consulting

AC 1.3 Challenge of delivering client centric professional consulting

Challenge in relation to own and client’s organisation:

• Organisation Type (e.g. local, international, global, project/programme based, operational, departmental or strategic business unit).

• Organisational purpose (strategic definition, vision, mission).

• Strategic narrative (historical perspective).

• Governance (e.g. public, private, third sector).

• Legalstatus of the organisation.

• Levels of organisational maturity.

• External environment.

AC 1.3 Critically reflect on how leadership styles can be adapted to respond to the challenge of deliveringclient-centricprofessional consulting

AC 1.3 Challenge of deliveringclient centric professional consulting

Challenge in relation to organisationalculture :

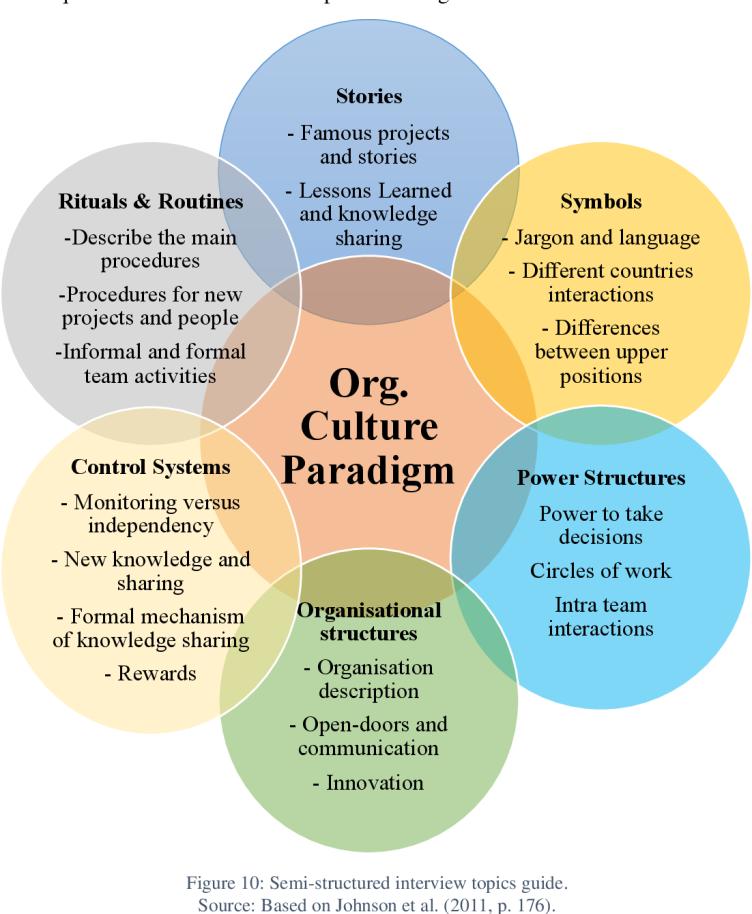

• Myths, stories, systems, processes, structure, internal politics, structure and demographic of the workforce (CulturalWeb Johnson et al., 2011).

• The Three Levels of Culture (Schein, 1992).

• Internal factors. ‘The way we do things around here’ (Deal and Kennedy, 1982 & 2000).

• Internal influences (Hofstede, 1980).

AC 1.3 Critically reflect on how leadership styles can be adapted to respond to the challenge of deliveringclient-centricprofessional consulting

AC 1.3 Challenge of delivering client centricprofessional consulting

Challenge in relation to organisational culture :

• Toxic cultures (e.g. leadership, bullying, discrimination, me firstattitudes, hostility, infighting).

• CompetingValues Framework (Quinn and Rohrbaugh, 1983).

• Performance targets.

• Organisational climate (e.g. short-termpeaks and troughs in operational activity, seasonality).

• Change (e.g. projects, innovation, restructuring, new ways of working, leadership).

Challenges in relation to digital landscape, impact of disruptive technologies.

• Learning Outcome 2:

• Understand strategies for optimising the way people are developed and led

AC 2.1 Critique strategies for building the capability of people

AC2.2 Recommend approaches to valuing people and promoting mental health and wellbeing when leading others

AC 2.1 Critique strategies for buildingthe capability of people

Command Verb - Critique - A detailed analysis and assessment of something, especially a literary, philosophical, or political theory.

Command Verb -Analyse - Break the subject or complex situation(s) intoseparate parts and examine each part in detail;identify the main issues and show how the main ideas are related to practice and why they are important. Reference to current research or theory may support the analysis.

AC 2.1 Critique strategies for building the capability of people

2.1 Strategies for building people capability:

• Learning and skills development.

• Coaching and mentoring.

• Talent management.

• Reward and recognition.

• Role requirements/role modelling.

• Succession/pipeline planning.

• Equality diversity and inclusion (Equality Act, 2010).

• Corporate Social Responsibility and sustainability.

• Human resource management (Beardwell and Thompson, 2017).

• Human resource development (Ulrich and Brockbank, 2005).

People : individuals or teams. Own organisation or client organisation.

2.2 Recommend approaches to valuingpeople and promotingmentalhealth and well-beingwhen leadingothers

Command Verb -Recommend - Put forward proposals, an alternative or suggestion(s) supported by a clear rationale appropriate to the situation/context.

2.2 Recommend approaches to valuing people and promoting mental health and well-being when leading others

2.2 Approaches to valuing people and promoting mental health and well-being:

• Development of healthy work systems.

• Targeted approaches to tackling stress, anxiety, depression.

• Fair and decent work (The Taylor review of modern working practices, 2017).

• Flexible working/work life integration.

• Safeguard of individuals rights and responsibilities.

• Creating safe environments which enable mental health and well-being to be discussed. Removal of structures (e.g. self-determined annual leave, empowered individuals (Ricardo Semler,1993)).

2.2 Recommend approaches to valuing people and promoting mental health and well-being when leading others

2.2 Approaches to valuing people and promoting mental health and well-being:

• Mental Health First Aid.

• Building confidence, rapport, trust.

• Honest conversations (Miles, Munilla and Darroch, 2006; Beer and Eisenstat, 2004)

• Social corporate responsibility as part of community to reduce discrimination and offer opportunities to all.

• Embedding/promoting equality, diversity and inclusion into overarching aims and objectives of an organisation. The case for equality, diversity and inclusion (Kirton et al. 2014).

• Valuing diversity (Griggs, 1995).

• Super-diversity (Vertovec, 2007).

• Turning adversity into competitive advantage (Sutanto, 2010).

Leadership Recommended Reading

● Avolio, B.J. and Gardner, W.L. (2005). Authentic Leadership Development: Getting to the root of positive forms of Leadership. The Leadership Quarterly , 16(3): 315-338.

● Barney, J. (1991). Firm Resources and Sustained Competitive Advantages. Journal of Management. No. 17 (1): 99-120.

● Bass, B.M. and Riggio, R.E. (2006). Transformational Leadership, 2 nd ed. New York, NY: Routledge.

● Covey, S.M.R. (2008). The Speed of Trust: The One Thing that Changes Everything. London: Simon and Schuster.

● Hitt, M., Ireland, D and Hoskinsson R (2014). Strategic Management: Concepts and Cases: Competitiveness and Globalisation , 11 th Edition. Cincinnati, OH: South-Western College Pub.

● Mintzberg, H. (2008). Strategy Safari: The Complete Guide Through the Wilds of Strategic Management, 2 nd Edition. Financial Times Series. Harlow: Pearson Education Limited.

● Roe, K. (2017). Leadership Practice and Perspectives, 2 nd Edition . Oxford: Oxford University Press.

● Whittington, R. (2000). What is Strategy and Does it Matter? 2 nd Edition. Andover: Cengage Learning EMEA

Leadership Recommended Reading

Textbooks/eBooks

● Adair, J, E. (2009). Not Bosses but Leaders: How to Lead the Way to Success . London: Kogan Page.

● Argyris, C. (2001). Breakthrough Leadership. Harvard Business Review, 79(11): 29-29.

● Barr, D. and Campbell, C. (2011). Ethics in DecisionMaking. (Good Practice Guide). London: Institute of Business Ethics.

● Bones, C. (2011). The Cult of the Leader. Chichester: Wiley

● Denis, J.L., Langley, A. and Rouleau, L. (2010) The Practice of Leadership in the Messy World of Organisations, Leadership 6(1): 67-88.

Leadership Recommended Reading

Textbooks/eBooks

● Goleman, D. (1996). Emotional Intelligence: Why It Can Matter More Than IQ . London: Bloomsbury Publishing.

● Handy, C. (2002). The Age of Unreason. New Thinking for a New World . New York, NY: Random House Business

● Institute of Business Ethics. (2011). Ethics in Decision-making. Good Practice Guide. London: Institute of Business Ethics.

● Judge, T.A. and Bono, J.E. (2000). ‘Five-Factor Model of Personality and Transformational Leadership’. Journal of Applied Psychology, 85(5): 751-765.

Leadership Recommended Reading

Textbooks/eBooks

● Katzenbach, J. R. and Smith, D.K. (2005). Wisdom of Teams. Creating the High Performance Organisation . Maidenhead: McGraw-Hill.

● Kotter, J.P. (2012). Leading Change. Brighton, MA: Harvard Business Publishing/Harvard Business Review Press.

● Lewis, S. (2016). Positive Psychology and Change: How Leadership, Collaboration and

Appreciative Inquiry Create Transformational Results. Chichester: Wiley-Blackwell.

● Lindgreen, A., Maon, F., Vanhamme, J., Florencio, B. Vallaster, C. and Strong, C. (2018).

Engaging with Stakeholders: A Relational Perspective on Responsible Business. Oxon: Routledge.

● Mullins, L.J. (2016). Management and Organisational Behaviour,. 11 th Edition . Harlow: Pearson Education.

Leadership Recommended Reading

Textbooks/eBooks

● Pedler, M., Burgoyne, J. and Boydell, T. (2013). A Manager's Guide to Self-Development .

Maidenhead: McGraw-Hill.

● Perkins, D.N.T. (2013). Leading at the Edge: Leadership Lessons from the Extraordinary Saga of Shackleton's Antarctic Expedition, 2 nd Edition. New York, NY: American Management Association (AMA)

● Quirke, B. (2017). Making the connections: Using internal communication to turn strategy into action. London: Routledge.

● Schein, E. and Schein, P. (2017). Organizational culture and leadership, 5 th Edition. San Francisco: Jossey-Bass.

Leadership RecommendedReading

Textbooks/eBooks

● Sinek, S. (2014). Leaders Eat Last: Why some teams pull together and others don’t. New York, NY: Penguin Random House USA.

● Tricker, B. (2015). Corporate Governance: Principles, Policies, and Practices, 3 rd Edition. Oxford: Oxford University Press.

● Whitmore, J. (2017). Coa ching for Performance : The Principles and Practice of Coachingand Leadership,25th Anniversary edition . London: Nicholas Brealey PublishingLimited.

Leadership Recommended Reading

Well-being

● Coles, R., Vaz Costa, S. and Watson, S. eds. (2018). Pathways to WellBeing in Design Examples from the Arts, Humanities and the Built Environment. London: Routledge.

● Cooper, C. and Hesketh, I. (2019). Wellbeing at Work: How to Design, Implement and Evaluate an Effective Strategy. London: Kogan Page/CIPD.

● Tailor, M. (2017) Good Work: The Taylor Review of Modern Working Practices. Assets publishing service.gov.uk.

● Van Velderhofen, M. and Peccei, R. eds. (2014). Well-Being and Performance at Work the Role of Context. London: Psychology Press.

● Worrall, L et al. (2016) The Quality of Working Life. Exploring Managers’ Wellbeing, motivation, productivity. London: Chartered Management Institute.

Leadership Recommended Reading Equality, diversity and Inclusion

● Fujimoto, Y., Härtel, C. and Azmat, F. (2013). Towards a diversity justice management model: integrating organizational justice and diversity management. Social Responsibility Journal, [online] 9(1), 148–166. (Available from https://doi.org/10.5465/256486 [15 August 2018].)

● Kirton, G. and Greene, A-M. (2016). The Dynamics of Managing Diversity. A Critical Approach . 4 th Edition . Oxon: Routledge.

● Malone, T. (2019). Equality, Diversity & Inclusion: A practical guide: Terminology, Communities and Dignity .

Leadership Recommended Reading

● Patrick, H., and Kumar, V. (2012). Managing Workplace Diversity: Issues and Challenges. Sage Open , 2 (3), 346-351.

● Sutanto, M. (2009). Turning Diversity into Competitive Advantage: A Case Study of Managing Diversity in the United States of America. Jurnal Manajemen Dan Kewirausahaan [online] 11(2) 154-160. (Available from https://doi.org/10.9744/jmk.11.2.pp.%20154-160 [15 August 2018].)

• Block, P. (2011). Flawless Consulting:A Guide to GettingYour Expertise Used, 3 rd Edition. San Francisco, CA: Jossey Bass.

• Chappell, T. (2008). Moral Perception, Philosophy, 83 (326), pp. 421-437.

• Cheng, V. (2012). Case Interview Secrets: A Former McKinsey Interviewer Reveals How to Get Multiple Job Offers in Consulting. Wheeling, W.VA:InnovationPress.

• Coles, R., Vaz Costa, S. and Watson, S. eds. (2018). Pathways to Well-Beingin Design Examples from the Arts, Humanities and the Built Environment. Oxford:Routledge.

• Cooper, C. and Hesketh, I. (2019). Wellbeingat Work: How to Design, Implement and Evaluate an Effective Strategy. London:Kogan Page/CIPD.

• Fisher, R., Ury, W. and Patton, B. (2012). Getting to Yes: Negotiating an agreement without giving in. London: Random House Business.

• Freed, R. and Romano, J. (2010). Writing Winning Business Proposals: Your Guide to Landing the Client, Making the Sale and Persuading the Boss, 3 rd Edition. New York, NY: McGraw-Hill.

• Gould, S. (2017). The Shape of Engagement: The Art of Building Enduring Connections with Your Customers, Employees and Communities. Scotts Valley, CA: CreateSpace Independent Publishing Platform.

• Hargie. O. (2018). The Handbook of Communication Skills, 4 th Edition. London: Routledge.

• Harrison, C. (2012). The Consultant with Pink Hair. Nashville, TN: RockBench Publishing Corp.

• Harvard Business Review, Christensen, C.M. Drucker, P.F., Goleman, D., and Porter, M.E. (2010). HBR’s 10 Must Reads: The Essentials. Brighton, MA:Harvard Business Review Press.

• Lopata, A. (2011). Recommended:How to Sell Through Networkingand Referrals. Upper Saddle River, NJ: FT Prentice Hall.

• Maister, D.H., Green, C. and Galford, R. (2001). The Trusted Advisor. London:Simon and Schuster UK.

• McKenna, C. (2010). The World’s Newest Profession: Management Consultingin the Twentieth Century. Cambridge: Cambridge University Press.

• McKinsey and Company Inc., Goedhart, M., Koller, T., and Wessels, D. (2010). Valuation: Measuringand Managing the Value of Companies,5th Edition. Hoboken, NJ: Wiley.

• Minto, B. (2010). The Pyramid Principle: Logic in Writing and Thinking, 3 rd Edition. Upper Saddle River, NJ: FT Prentice Hall.

• Newton, R. (2019). The ManagementConsultant: Masteringthe Art of Consultancy, Second Edition. Financial Times Series. Harlow: Pearson Education Limited.

• Patterson,K., Grenny, J., McMillan, R. and Switzler, A. (2011). Crucial Conversations for Talking When Stakes are High, 2 nd Edition. New York, NY: McGraw-Hill Education.

• Rasiel, E. (1999). The McKinsey Way. New York, NY: McGraw-Hill Education.

• The Mckinsey Way- Ethan M Rasiel 2003

• The Trusted Adviser - David H Maister, Robert Galford, Charles Green 2002

• Case Interview Secrets - Victor Cheng 2012

• The Pyramid Principle: Logic in Writing and Thinking –Barbara Minto 2009

• The Practice of Professional Consulting- Edward G Verlander 2012

• Valuation: Measuring and Managing the Value of Companies- Tim Koller , Marc Goedhart, David Wessels 2010

• The Back of the Napkin: Solving Problems and Selling Ideas with Pictures- Dan Roam 2008

• McKinsey’s -Marvin Bower, Elizabeth Haas Edersheim 2010

• The Art of Consultancy- Stuart Wyatt 2019

• The New Business of Consulting - Elaine Biech 2019

• The Management Consultant - Richard Newton 2019

• The Execution Essentials -StephenR Covey 2018

• Humble Consulting -Edgar H Schein 2016

• Flawless Consulting - Peter Block 2011

• Value –Based Fees- Alan Weiss 2008

• The Consultant’s Handbook- Samir Parikh 2015

• The New Consultants Quick Start Guide - Elaine Biech 2019

• Getting Started in Consulting- Alan Weiss 2019

• Essential Tools for ManagementConsulting- Simon Burton Shaw-Gunn 2010

• It Starts With Clients- Andrew Sobel 2020

• Out Think - G Shawn Hunter 2013

• The ConsultingBible- Alan Weiss 2011

• Million Dollar ConsultingProposals- Alan Weiss 2011

• ReinventingProfessional Services - Ari Kaplan 2011

• The Trusted Advisor Field book -Charles H Green & Andrea P Howe 2011

• The Performance Consultant’s Field book- Judith Hale 2012

• Guerrilla Marketing For Consultants - Jay Conrad Levinson 2011

• Non Profit ConsultingEssentials- Penelope Cagney 2010

• Effective Group Coaching - Jennifer J Britton 2010

• Creatinga Successful ConsultingPractice- Gary W Randazzo 2018

• The Highly Paid Expert -Debbie Allen 2015

• EvaluatingOrganizationDevelopment - Maureen Connelly Jones, William J Rothwell 2017

• ManagementConsultingToday and TomorrowFlemming Poulfelt, Thomas H. Olson 2017

• Argyris and Schön (1996)Consultants as agentof change. Business consultancy is a process through which organisations learn. Business consultants are perceived as agents of change.

• Kaarst-Brown (1999)Role of consultants- There are five symbolic roles of the external consultantExternal consultants when called into work on an assignmentare actually beingmanipulated by theirclientwhose agenda has already been setin advance.

• Lippitt and Lippitt (1986)Role of consultants .There is no established role in business consultancy. Consultants fulfil a number of roles that they judge to be appropriate for the client’s situation.

• McKinley and Scherer (2000)Consultants as agents of change .Consultants’ writings on organisational changes drive topexecutives to restructure organisations. Consultants are agent of change

• Kinsely (1979) Role performance fluctuation. In business services, one must be aware that employees and managers efficiency fluctuates on a day to day basis.

• Kubr (1996) Role of consultants . Consultants have two basic roles: resource role and process role

• Lindon (1995) Role of consultants .Consultants role is to help managers to understand their problem, whilst not being responsible for solving it.

• Lippitt and Lippitt (1986)Role of consultants .There is no established role in business consultancy. Consultants fulfil a number of roles that they judge to be appropriate for theclient’s situation.

• McKinley and Scherer (2000)Consultants as agents of change Consultants’ writings on organisationalchanges drive top-executives to restructure organisations. Consultants are agent of change

• Pellegrinelli(2002: 353)Consultant /clientrelationship Investigated the interplay and tensions ofconsulting interventions.

• Schein (1988)Role of consultants in the consultancy process There are three types of consultancy: the expert, the doctor/patient relationship and the“ process consultation”. Schein focused his researchthe role that “consultation process”on plays on organisational development.

• Steele (1975)The learning process in consulting‘Learning is the essence of consulting’ (Steele, 1975: 190)

• Walker and Massey (1999)Skills transfer inconsulting Business consultancy is about transferring skills to both organisations and managers.

• Williams (2001) Client’s role inconsulting Consultants’ esoteric language gives meaning to concepts and actually help managers to understand better the problems they arefacing.

• Professional consultingrequires a multi-dimensional approach to leadership.

• Within the role, consultantsneed to be adept, confident and have credibility.

• Scenarios for consultingwill typically be complex and involve building relationships with other senior leaders.

• Consultantsmay lead internal and/or external teams and work at board level.

• Consultantsmust not only have a macro view of an organisation’s strategiccontext, they must also understand the impact of digital, technological and geo-political change.

• Defines, shapes and communicates organisational purpose,vision, mission, culture and values.

• Develops the strategic direction of the organisation.

• Developmentof strategic goals.

• Consider strategic options (e.g. risk, financial,reputational,legal, management, competitive advantage).

• Supports implementation of strategic plan.

• Creates and selects strategy. (Planned. Intended. Emergent. Deliberate. Opportunistic,Whittington,2000).

• Resource based view of the firm (Barney, 1991).

• Scenario planningand rational planningmodel. Strategic Planning as a Top Down/Bottom up process. The Five Ps of Strategy (Mintzberg, 1987).

• Leads the organisation ethically and legally in line with board and organisational governance.

• Diversity and Inclusion (Kirton et al. 2014).

• Definition and Values (Patrick and Kumar, 2012).

• Leads individuals and teams with impact (Belbin, 1981)

• Develops people and their capabilities.

• Collaborates with partners and manages complex relationships with multiple and diverse stakeholders/customers.

• Stakeholder management (Lindgreen et al. 2019).

• Anticipates and predicts future opportunities and threats for industry, sector, technical specialism (Horizon scanning).

• Initiates, leads change and innovation.

• Recommends types and approaches of change (e.g. incremental and transformational change).

• Identifies drivers of change and new ways of working across infrastructure, processes, people and culture and sustainability.

• Applies different theories/models of change (e.g. Eight Step Change Model (Kotter, 2012),

• Radical Change within Traditional Structures (Oswick, 2015)).

• Creates an environment for innovation and creativity.

• Selects and applies tools and techniques to support innovation and change.

• Drives continuous improvement (e.g. Kaizen).

• Selects and applies tools and techniques (e.g. LEAN methods (Krafcik, 1988).

• Six Sigma (Pyzdek and Keller, 2018).

• Statistical Process Control ‘SPC’(Salacinski, 2015).

• Applies soft systems thinking to understand complexity(Checkland, 1999; Senge, 1990).

• Recognises the importance of brand relationship and reputation management.

• Applies financial measures, considers financial sustainability and accountability.

• Manages resources and measures outcomes

• Professional consulting can be transformational, shaping the way organisations think and operate.

• Consultants may assist clients to develop strategic objectives, consider new market opportunities, explore innovative ways of working and build organisational and staffcapability.

• For professional consultants to deliver effectiveclient-centric consulting they must have an in-depth understanding of consulting practice.

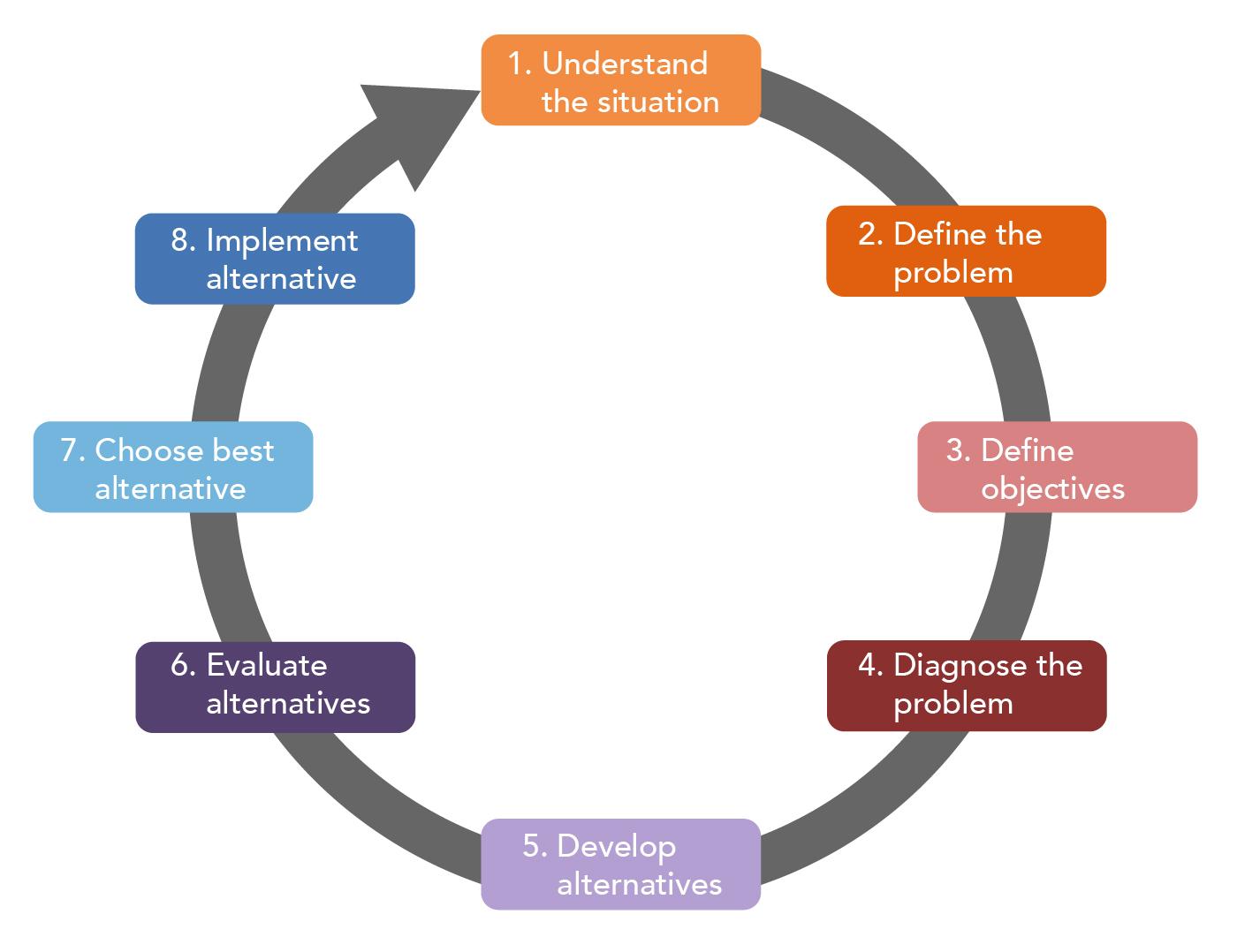

Conceptualise a process for client-centric professional consulting

Conceptualise: Diagram, model, chart or graphic with annotations. Holistic overview of process.

Process for client-centricconsulting:

• Process tailored to the needs of client/own organisation (process can begin at any stage dependenton clientrequirement).

• Cycle of consultancy. Dimensions of consultingengagement(Newton, 2019).

• The Seven C’s of Consulting(Cope, 2010).

• Clientengagement(relationship building, trusted advisor). Customer Relationship Management(CRM).

• Identification of clientissue/requirementforconsulting.

• Consultingtype (e.g. process/expert).

Process for client-centric consulting:

• Identify/establish hypothesis for consulting.

• Proposal development (Freed and Romano, 2010).

• Negotiation (‘Getting to Yes’ Fisher et al., 2012).

• Gain agreement to proceed.

• Contracting.

• Data and information collection and analysis to test a hypothesis.

• Reaching a conclusion.

• Make recommendations.

Process for client-centric consulting:

• Develop plans to deliver the consulting recommendationsto respond to client issues/requirements for consulting.

• Implementplans (deliver consulting).

• Articulate lessons learnt.

• Evaluate outcomes.

• Close consultancy engagement(withdrawal phase).

• Conductimpact assessmentof consultancy.

• Assess learning needs of client.

• Determine opportunities for further consulting.

• Networking to develop client base (e.g. personal,professional,affiliations, associations,contacts).

• Marketing (e.g. developmentof strategies for new/existingclients (local, regional, national,global)).

• Marketing Mix (7 Ps of the Marketing Mix, Kotler, 2013).

• Frameworks for digital marketing communication platforms (e.g. R.A.C.E. model – Reach, Act, Convertand Engage (Chaffey, 2010)).

• S.W.O.T. Analysis.

• Ansoff’s Growth Vector Matrix (1957).

Approaches to identify and generate consulting opportunities:

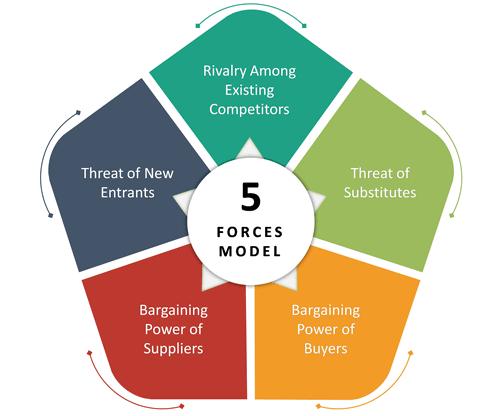

• Porter’s 5 Forces Analysis Framework (1979).

• Facing the external environment (P.E.S.T.L.E.Analysis).

• Use of social media.

• Branding.

• Customer relationship management (CRM) operations.

• Referrals from existing clients.

• Register to receive consulting opportunities.

• Respond to consulting opportunities (e.g. RFP (Request for Proposal)). RFI (Request for Information).

• ITT (Invitation to Tender).

• Overview of proposed consultancy (Terms of Reference).

• Rationale for consultancy.

• Value proposition (the value the clientwill gain if they proceed with the

• consultancy).

• Statementof clientissue (e.g. areas to be addressed, beneficiaries of consulting, strategiccontext).

• Methodology (approach taken to consultwith client, activities/people involved in the consultancy, communication strategy).

• Evaluation/summary.

• Quality assurance (e.g. progress reviews/evaluation (lessons learned)).

• Terms of contract (e.g. cost, payment terms/schedule, liabilities, indemnities, confidentiality, ownership, delivery of consulting KPIs, risk management and mitigation).

• Additional information as specifically required by the client (e.g. client references, data and information, financial statements).

• Policies (e.g. equality and diversity, sustainability, conflict of interest, confidentiality).

• Clarification and conditions for consulting (e.g. reporting structure, organisational, legal and regulatory requirements).

• Proposal development is underpinned by professionalism (e.g. ethics, cultural norms, transparency, confidentiality, corporate social responsibility and sustainability, compliance with organisational, legal and regulatory frameworks).

Different clients:

• Publicsector (local and national government).

• Private.

• Third sector.

• Local, international, global, cross-borderorganisations.

• Internal.

• Projectand programme-based organisations.

• SMEs. Partnerships.

• Sole Traders.

• Limited liabilities Companies (LLPs).

• Consultancy engagement begins (e.g. Review aims, objectives, assumptions, hypothesis which form the basis of consulting.

• Determine/allocate resources.

• Scope and plan delivery.

• Appraise type/level of involvement with client.

• Risk management strategy).

• Collect, analyse data and information/evaluation of the impact of data and information on hypothesis for consulting.

• Apply principles of design thinking (Dorst, 2015 and Kolko, 2018).

• Consider evidence against original hypothesis for consulting.

• Make sense of ambiguity (e.g. accept, reject, develop, revise findings.

• Negotiate.

• Make trade-offs.

• Agree nature, content, format, delivery of outcomes).

Methodologiesfor deliveringclient-centricconsulting:

• Communicate recommendationsin a straightforward, understandable and non-technical manner (Communicate,counsel, consult, provide advice and guidance to client throughout engagement (Patterson et al., 2011).

• Implement delivery methodologies (e.g. Project management methodologies: PRINCE2, PMBOK, Agile, Waterfall, Six Sigma Project, SCRUM).

• Organisational strategies/tools.

• Devise quality assurance strategy (reporting and monitoring against KPIs, ROI and SROI (Social Return on Investment)).

• Resource management plan (e.g. finance, people,

• Deliver recommendations which add value to the client’s organisation/individual on conclusion of contract.

• Measure success (short, medium, long term).

• Determine client satisfaction.

• Maintain and grow client contact/strategic business network.

• Add value through coaching, education (for an agreed period) to support client in new ways of working/transfer of capability.

• Offer networking opportunities/introductions for client.

• Compliance to organisational, ethical and legal frameworks (e.g. Bribery Act, 2010).

• The ability to drive innovation and change is an essential skill for a professional consultant.

• Innovation defined simply as ‘doing something new or different’, is a powerful catalyst for change.

• It can revolutionise an organisation’s operational activities, create dynamic new opportunities, and contribute to the achievement of strategic goals.

• Change occurs in many forms and professional consultants must be able to lead changes, which may be radical, incremental or evolutionary.

Innovation and change: Innovation is the activity of doing something new or different.

• Achievementof objectives, environmental, internal and situational factors,changing market positioning, entry to new markets products and services.

• New operational processes and procedures.

• Response to customer demands.

• Impact of big data, information,knowledge capital and creativity.

• Stakeholder involvement(individuals, pressure groups,interestgroups,media).

The rationale for innovation and change

• Competitiveness, reputation, good practice, ethics,

• Corporate Social Responsibility (CSR), shiftingcultures, diversity, emergingstrategy, governance.

• Improvingorganisational performance, systems, quality and efficiency, service delivery, processes.

• Organisational survival, consolidation.

• Upgradingthe business model (e.g. offer complementary services or products).

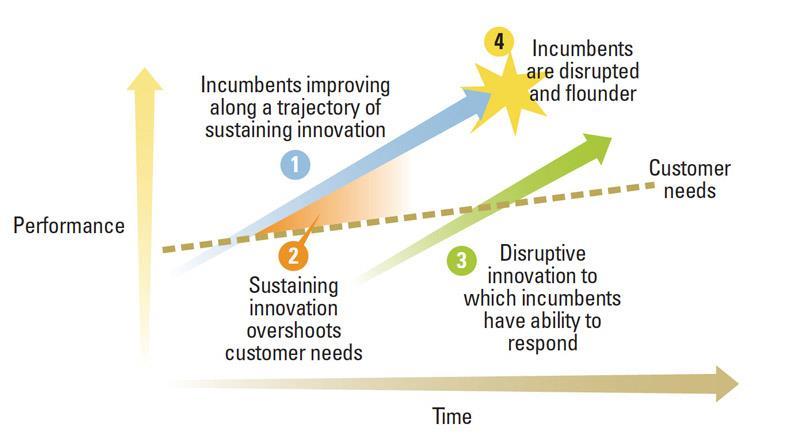

• Response to digitalisation, technological change, disruptive technologies (Christensen, 1997; World Bank, 2019).

• Finance and resourcing, legal and regulatory and organisationalrequirements.

Leading innovation and change through professionalconsulting

• Organisational contexts:

• Type and purpose of the organisation (operational, local, international, global, project/programme management, departmental and strategic business unit),

• TRIZ/TIPS ‘inventive problem solving’ (Altshuller, 1984).

• Open and closed innovation (Chesbrough, 2003).

• Commercialisation and viability of the process, idea, opportunity. Assessing the competition, using research to drive ideas. Ideasdriven innovation.

• Educate “growth mindset”, learning from mistakes.

• Market/customer driven innovation.

• Analysis driven innovation.

• Continuous product and process improvement.

• Service design (Shostack et al., 1982).

• Design thinking, IDEO (Stefan and Nimgade, 2000, revised 2017).

• Synectics – creativity and problem solving(Arthur. D Little Invention Design Unit, 1950s; Gordon, 1961; Boland Jr. et al., 2008).

• Networking and Communities of Practice (CoPs).

• Value propositiondesign (Osterwalder et al., 2010).

• The entrepreneur as a disruptor. The use of disruptive technologies and digitaltechnologies (Christensen, 1997).

• Behavioural approaches to promote innovation: (e.g. inclusive, agile, flexible, creative (Amabile, 2012), enterprising, solution focused).

• Recruitment and employment of innovators (value individuals who think differently).

• Incentivised innovation (e.g. reward and recognition).

• Responsive to challenges and barriers which impede innovation and change.

• Use of coaching and mentoring.

• Negotiates, influences, communicates using emotional intelligence (Goleman, 1998).

• Collaborative approaches to innovation across sector, company and teams.

Traditional approaches to change:

• Leadership-driven (top down) tried and tested, experience based, transactional, change agents. Focus on the past to act in the present, cultural change.

• Powerthrough hierarchy, mission and vision, makingsense through rationale argument. Freeze phases (Lewin, 1947).

• Force Field analysis (Lewin, 1948).

• Change rollercoaster (Kubler-Ross, 1969).

• The Prosci change model ‘ADKAR’ (Hiatt, 2003).

• Eight guidingprinciples forchange management(Kotter, 1995).

• The change equation (Beckhard, 1969).

• Navigatingthe transitions of change (Bridges, 1991).

• The four stages of major change (Longaker, 1993).

• Managing at the speed of change (Conner, 1992).

• The Change Masters (Hailey and Balogun, 2002).

• Change Equation (Moss-Kanter, 1983).

Contemporary approaches to change:

• Acting in the present to impact the future: Top down and bottom up leadership, emergent, tropic, rhizomatic and spontaneous, power through connections and networks, shared purpose (Oswick, 2010).

• Purpose of a system is what it does ‘ POSIWID’ (Beer, 1960).

• Making sense through emotional connections.

• Open approaches, sharing ideas, co-creating change.

• Relationships and networks.

• Taking a holistic ‘Helicopter view’ (Morgan, 1985).

• Outcomes driven. Co-creation. Open and closed systems. Inter and intra relations (Ulrich, 1983).

Contemporary approaches to change:

• Multiple perspectives analysis (Linstone, 1976).

• Boundary critique (Ulrich, 2002).

• Divergent and convergent thinking.

• Radical Change within Traditional Structures (Oswick, 2015).

• Organisational congruence model (Nadler and Tushman, 1997).

• Managing change ‘Systems Intervention Strategy’ (Mayon-White,1985).

• Appreciative Inquiry (Cooperrider and Srivasta, 1987).

• AuthenticLeadership (Goffee and Jones, 2011).

• Entrepreneurial Leadership (Roebuck, 2014).

• Transformational Leadership (Bass and Riggio,

• 2006). Situational Leadership (Hersey and Blanchard, 1969).

• Five Practices of Exemplary Leadership (Kouzes and Posner, 1987).

• Leadership Styles (Goleman, 1995).

• Distributed Leadership (Roe, 2020).

• The Servant Leader(Greenleaf, 1977).

• Approaches which supportmental health and wellbeing.

• Stress management.

• Employee engagement.

• Minimise unwanted disruption.

• Manage conflicts and tensions (e.g. within and between stakeholdergroups).

Client requirements

• External and internal business drivers.

• Responseto digitalisation, new, disruptivetechnologies (Brand, 2005).

• Markets and customer expectations.

• Legal and regulatory requirements.

• Environmental factors.

• CSR and sustainability.

• Economic opportunities.

• Diversification.

• Cultural shift.

• Process improvement.

• Leadership change.

• Organisational changedevelopmentand design.

• Restructure.

• Consolidation.

• Innovation.

• Expansion. Merger. Partnership.

• Divest.

Develop strategy:

• Application of theoretical approaches to change (e.g. to scope, plan, drive,

• deliver, and evaluate change).

• Leadership and managementapproaches to engage with stakeholders throughoutprocess.

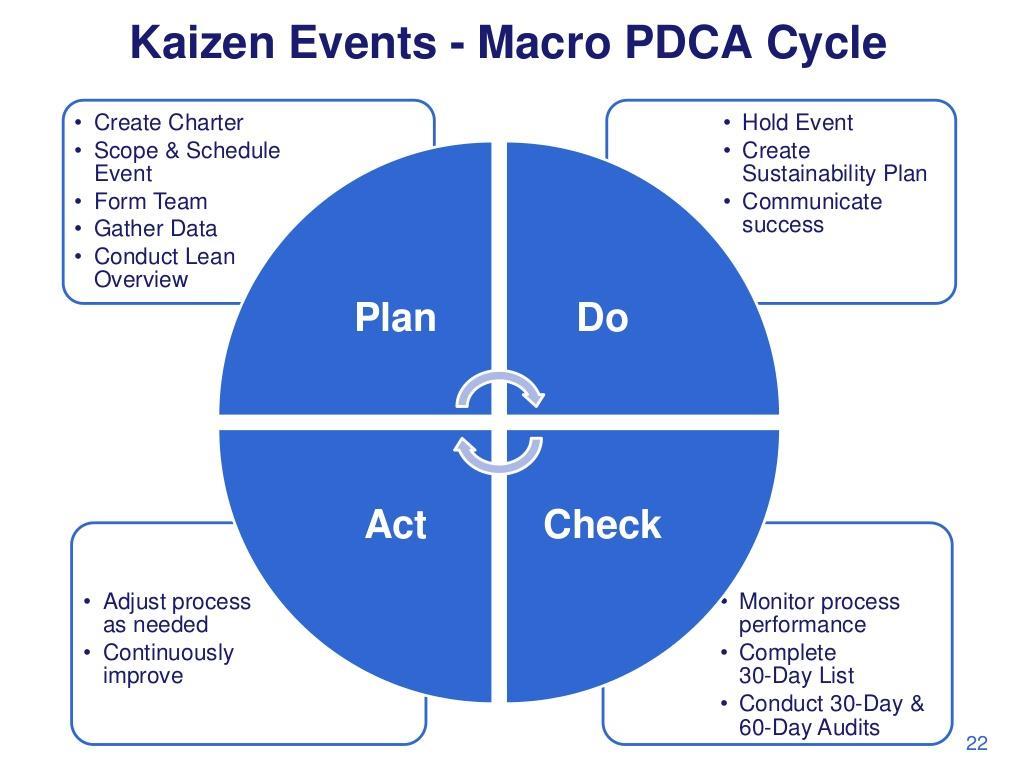

Implementation strategy:

• Big bang strategy.

• Kaizen.

• Prototyping.

• Developingapilot.

• Parallel operations

Implementation plan to lead/drive the change process:

• Key features (e.g. scope of change, objectives, actions, stages, milestones, resource requirements, learningand development).

• Establish roles and responsibilities.

• Set KPIs.

• Establish a culture of continuous improvement.

• Risk management.

• Quality assurance.

• Communication strategy and plan (internal and external communications, i.e. presentations, meetings and briefings, use of media, consultations, huddles,

• webinars, podcasts, conference calls, blogposts, letters, articles, case studies).

• Communicationskills (e.g. emotional and social intelligence, influencingand persuasion, use of clear, succinct language appropriate to the audience.

Implementation plan to lead/drive the change process: Assessment and response to barriers and challenges (internal and external):

• Logistical barriers.

• Working patterns such as remote, virtual, shift working. Finance.

• Influence of trades union and professional bodies.

• Changingmanagement priorities.

• Levels of commitment, motivation, delayingtactics.

• Cultural dimensions of innovation(diversity, ethnicity and gender divide to entrepreneurial practice).

• Group Think (Janis, 1982).

• Organisational politics.

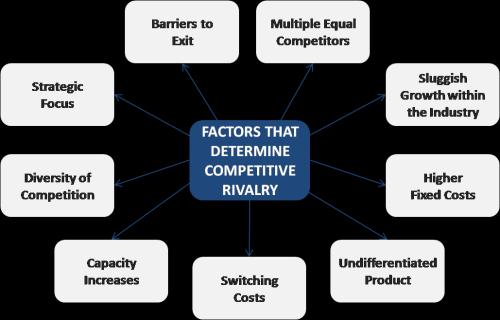

• Supplier power. Buyer power. Bargainingpower. Competition. Threat of substitution. (Porter, 1979).

Implementation plan to lead/drive the change process:

Application of decision-making tools, techniques:

• Attribute trade off models (MRD/ARM Analysis).

• Use of Logframes (U.S. Agency for International Development,1969).

• The Pugh matrix (Pugh,1980).

• Quality Function Deployment ‘QFD’ (Akao, 1966).

• Pareto analysis.

• Decision trees.

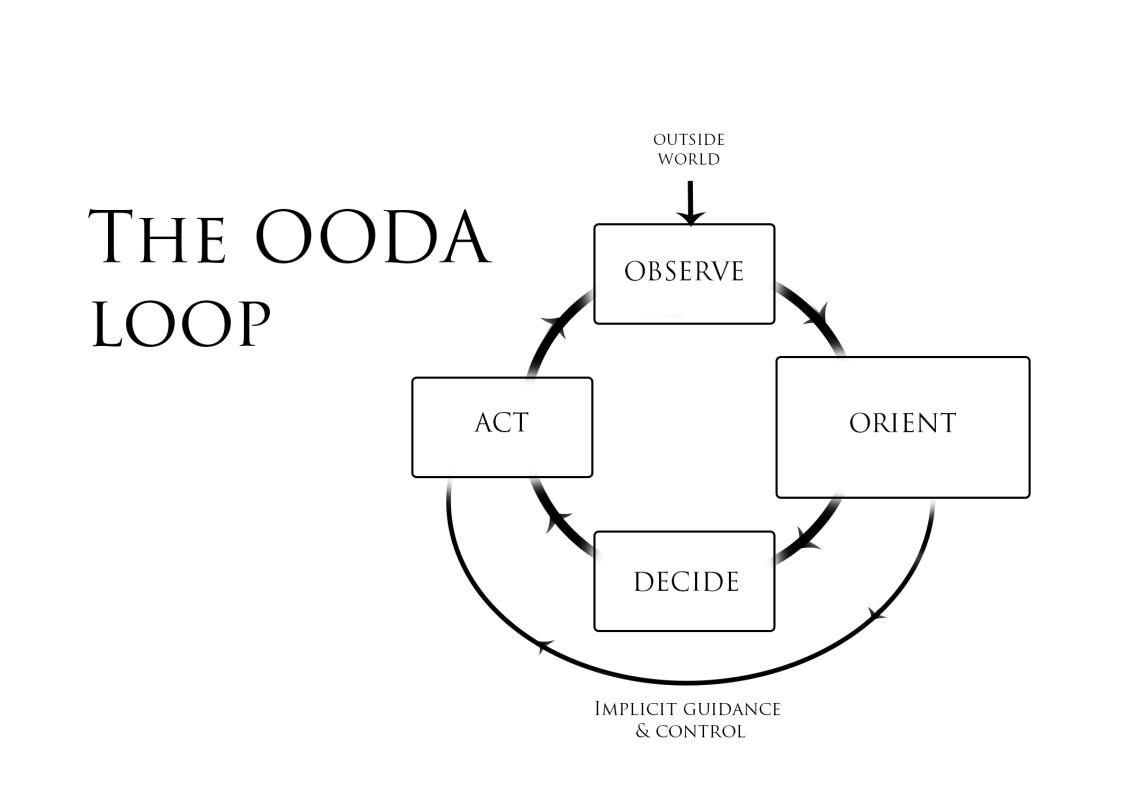

• Sensitivity and what if analysis. OODA loops (Boyd ,1985).

• Monte Carlo Simulation Method (Ulam, 1947).

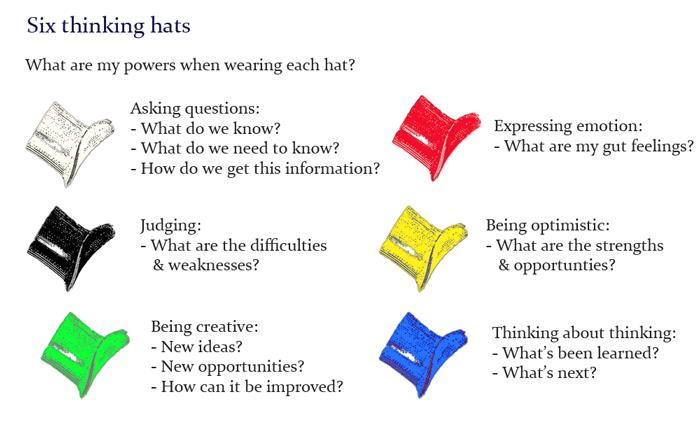

• Six Thinking Hats technique (De Bono, 1985).

• Multi Voting / Delphi Technique (1944).

Develop a strategy for leading and managing change in response to a client requirement

Implementation plan to lead/drive the change process:

Application of project management approaches

• PRINCE2, PMI (Project ManagementInstitute).

• APM (Association of Project Managers).

• PMBOK (Project ManagementBody of Knowledge).

Implementation plan to lead/drive the change process:

• Application of tool/s to review the impact of change:

• Periodic reporting, surveys and questionnaires, benchmarking activities, balanced scorecards (Nolan and Norton, 1992).

• Post implementation reviews.

• Application of quantitative techniques e.g. data and metrics, audits, targets, statistical analysis (e.g. SPC).

• Qualitative techniques e.g. interviews, observation, walk through,

• conversations.

• Framework Analysis (Pope et al., 2000).

• Thematic Network Analysis (Attride-Stirling, 2001).

• Systematic/systemic triangulation (Urich, 1983).

Client-centric: e.g. consulting with individuals, teams, board members.

Challenges in leading others:

• Understanding of who is leading and who is being led.

• Scope of leadership (e.g. leading consultants, clients, researchers, administrators, other team members, suppliers, partners).

• Different organisational behaviours and knowledge requirements.

• Leading without authority.

• Lack of buy-in from individuals within client organisation.

• Ability to adapt leadership style (adaptability).

Client-centric: e.g. consulting with individuals, teams, board members.

Challenges in leading others:

• Establishing credibility (e.g. leadership credentials not recognised, disconnect between industry specialists and career consultants).

• Communication breakdown/lack of communication.

• Ability to interpret and articulate solutions back to the client.

• Client perception (e.g. challenges are unique to the sector).

• Delivering difficult news.

• Articulating value of consultancy (e.g. financial and non-financial benefits). Reputation/stereotypes regarding consultants.

Challenge in relation to own and client’s organisation:

• Organisation Type (e.g. local, international, global, project/programme based, operational, departmental or strategic business unit).

• Organisational purpose (strategic definition, vision, mission).

• Strategic narrative (historical perspective).

• Governance (e.g. public, private, third sector).

• Legal status of the organisation.

• Levels of organisational maturity.

• External environment.

Challenge in relation to organisational culture

• Myths, stories, systems, processes, structure, internal politics, structure and demographic of the workforce (Cultural Web Johnson et al., 2011).

• The Three Levels of Culture (Schein, 1992).

• Internal factors. ‘The way we do things around here’ (Deal and Kennedy, 1982 & 2000).

• Internal influences (Hofstede, 1980).

• Toxic cultures (e.g. leadership, bullying, discrimination, me first attitudes, hostility, infighting).

• Competing Values Framework (Quinn and Rohrbaugh, 1983).

• Performance targets.

• Organisational climate (e.g. short-term peaks and troughs in operational activity, seasonality).

• Change (e.g. projects, innovation, restructuring, new ways of working, leadership).

• Challenges in relation to digital landscape, impact of disruptive technologies.

Learning and skills development.

• Coaching and mentoring.

• Talent management.

• Reward and recognition.

• Role requirements/role modelling.

• Succession/pipeline planning.

• Equality diversity and inclusion (Equality Act, 2010).

• Corporate Social Responsibility and sustainability.

• Human resource management (Beardwell and Thompson, 2017).

• Human resource development (Ulrich and Brockbank, 2005).

• People : individuals or teams.

• Own organisation or client organisation.

• Development of healthy work systems.

• Targeted approaches to tacklingstress, anxiety, depression.

• Fair and decent work (The Taylor review of modern working practices, 2017).

• Flexible working/work life integration.

• Safeguard of individualsrights and responsibilities.

• Creatingsafe environments which enable mental health and well-beingto be discussed.

• Removal of structures (e.g. selfdetermined annualleave, empowered individuals (Ricardo Semler,1993)).

Approaches to valuing people and promoting mental health and well-being:

• Mental Health First Aid.

• Building confidence, rapport,trust.

• Honest conversations (Miles,Munilla and Darroch,2006; Beer and Eisenstat, 2004).

• Social corporate responsibility as part of community to reduce discrimination and offer opportunities to all.

• Embedding/promotingequality, diversity and inclusion into overarchingaims and objectives of an organisation.

• The case for equality, diversity and inclusion (Kirton et al. 2014).

• Valuing diversity (Griggs, 1995).

• Super-diversity (Vertovec, 2007).

• Turningadversity into competitive advantage (Sutanto,2010).

• Relationship between initial proposal and delivery of professional consulting

• Delivery of client benefits and quality assurance (e.g. achievement of the value proposition against client requirements (e.g. achievement of KPIs, ROI, SROI and milestones).

• Ability to take responsibility, recommend modifications. Make decisions (strategic/tactical) take corrective action on major issues (e.g. scope creep, time, failure to achieve KPIs/milestones, budget overruns, quality)).

• The effectiveness of strategies/theories/ advice used and/or provided during the consulting engagement (e.g. ability to apply principles of design thinking (Dorst, 2015 and Kolko, 2018)).

• Ability to balance client needs with own organisation’s values (e.g. applicationof policy, procedure, legal, ethical requirements, corporate social responsibility and sustainability).

• Ability to remain a trusted advisor. Develop professional relationships and network with client/relevant stakeholders.

• Communicate with key stakeholders effectively (short, medium, long term).

• Communicate, counsel, consult, provide advice and guidance to client throughout engagement (Patterson et al. 2011).

Reflective practice approaches:

• Model of Structured Reflection (Johns, 1995; 2006).

• Reflective cycle (Gibbs, 1988).

• Experiential/learning cycle (Kolb, 1984).

• 3 stem questions (What? So What?

• Now What?) (Borton, 1970; Driscoll, 1994, 2000, 2007).

• Reflection before action-reflection in action-reflection on action (Schön, 1983).

• Appreciative Inquiry (Cooperrider and Srivastra, 1987).

Recommendations to improve the delivery and strategic impact of professional consulting:

• Ability to lead self and others.

• Lead change.

• Manage conflicts.

• Communicate and build stakeholder relationships.

• Application of theories, models and frameworks. Terms of contract (e.g. KPIs, ROI, SROI).

• Resource managementplan (e.g. finance, people, technology, materials). Use of technology.

• Compliance with organisational,ethical and legal frameworks.

• Managementof data and information.

• Time management.

• Managementand mitigation of risk.

• Building client capability.

• After establishing the aims and objectives, the actual process of consultation will need to be planned, i.e.:

• Who are the key stakeholder groups?

• How accessible are they?

• Are there any hard-to-reach groups?

• How can their co-operation and engagement be gained?

• What is the best method of consulting with the groups?

• What do they need to see beforehand?

• How can this be disseminated?

• Will any pre-consultation be required to prepare stakeholders for the exercise?

• The method of consultation will need to be identified, balancing the resources available and the level of feedback required.

• The “process” stage is the “doing” stage; this involves carrying out the consultation. Good planning will ensure this stage runs smoothly. Considerations in this stage mainly centre on developing effective relationships with stakeholders and facilitating open and honest sharing of views, and accurate recording of the process and the data.

• The next stage, “presentation“, is concerned with the analysis and the reporting of the data. The data will need to be analysed and reporting prepared for the relevant audiences i.e. back to the corporation, to policy makers, etc. but also feedback to those who have engaged in the process and taken part. The form of reporting will need to take into account audiences and ensure the highest possibility of actions as a result of the consultation.

• The final stage relates to actions as a result of the consultation; the “promise“. Part of the process of engaging with stakeholders is the investment in a longer-term relationship of mutual benefit and trust.

• Without demonstrable use of stakeholder feedback in resultant action, this can be damaged. The final stage, therefore, has an element of PR contained within it; communications about resultant actions need to be carefully considered to reach stakeholder audiences.

• Ability to build and sustain extensive/diverse stakeholder networks and collaborate with others in target organisations,industry bodies,intermediaries and in own organisation(Lindgreen et al., 2019).

• Ability to influence, persuade,motivate and engage others to realise objectives (Jung, 1921; Graves,1970; Carnegie, 1936).

• Ability to show a genuine interestin stakeholders’thoughts,ideas and expectations.

• Ability to create an environmentin which team members find common ground, builds mutual respect and fosters team cohesion (Belbin, 1981).

• The term stakeholderfirst “appeared in the management literaturein an internal memorandum at the Stanford Research Institute, in 1963” (Freeman, 1984, p. 31).

• The word means “any group or individual who can affect or is affected by the achievementof the organization'sobjectives” (Freeman, 1984, p. 46).

• Bryson (1995, p. 27) proposed a more comprehensive definition for the term: “A stakeholderis defined as any person, group, or organization thatcan place a claim on an organization'sattention, resources, or output or is affected by that output”.

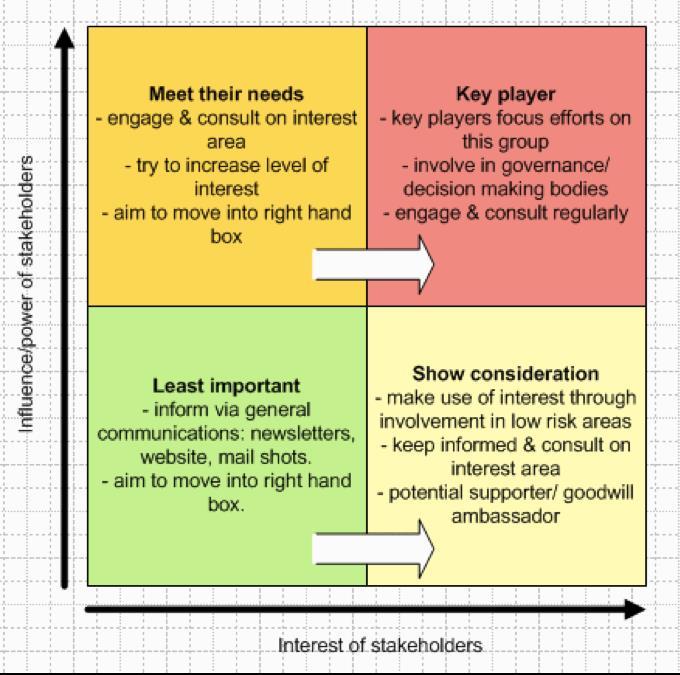

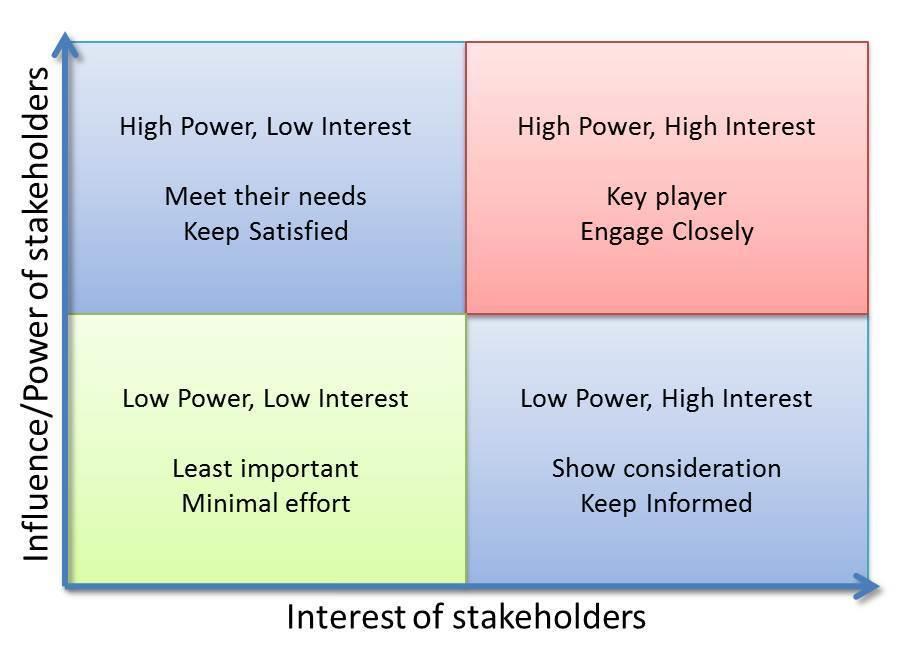

• Power-Interest Grid Source: Eden and Ackermann (1998) cited in Bryson, John 2004. “What to do When Stakeholders Matter: Stakeholder Identification and Analysis Techniques.” Policy Management Review 6(1): 2153.

• The power-interest grid, as shown to the right, helps to visualise the positions of individual stakeholders and the relations among them. The two dimensions of the grid – power and interest – speak to the reality that not all of the players who have an interest in agricultural land use planning also have power to influence decisions. The two-dimensional grid generates four categories of stakeholders:

Players: have both an interest and significant power

Subjects: have an interest but little power

Context setters: have power but little direct interest

Crowd: have little interest or power

•

• "There is no one 'right' or 'best'culture for an organisation - only the appropriate culture for the business environment (Gareth Jones and Rob Goffee)."

• This concept explores how organisations build up their own culture through tradition, history and structure. It also suggests that culture provides organisations with a sense of identity.

• Organisational culture is a pattern of basicassumptions invented, discovered or developed by a given group within an organisationas it learns to cope with its problems of external adaptationand internal integration. The pattern has worked well enough to be considered valid and therefore is to be taught to new members as the correct way to perceive, think and feel in relation to problems (Schein, 1988; 1996).

"It is now widely accepted that leaders of an organisationshape its culture (Northouse, 2001)."

• Highly effective leaders develop styles that are clearly aligned with their team and organisational culture. Important differences between leadershipstyles are described, with case studies from across industries to highlight the benefits and drawbacks.

• Kurt Lewin and his colleagues conducted research on different leadershipstyles, classifyingthem into three types: democratic, autocratic, and laissez-faire (Lewin et al., 1939). These styles can be placed on a continuum of control:Firstly, Autocraticwhere the leader tells people what to do, an authoritarianstyle. Democratic, where teams participate and collaborate in decision making, but the leader still has final say. Finally, laissez-faire - a hands off approach where employees choose for themselves what the best option is with little to no control from the leader (Robinson, 2010).

BUSINESS ETHICS AND CORPORATE SOCIAL RESPONSIBILITY

• Respectfor Others: Leaders with ethical qualities act theirfollowers with esteem and regard. This indicates that ethical leaders act individuals as results in their own rather than as channels for arriving at their results.

• Service to Others: Among the qualities of ethical leadership is servingthe followers. They act in a humane manner which is in contrary to acting in an ethical egoistway. This kind of leaders regard theirfollowers very highly. Theirmain purpose of life is to espouse and encourage theirfollowers. Providingservice to other individuals is demonstrated by means of conducts includingcounselling, creating teams and authorizing(Mendonca and Kanungo, 2007).

• Impartiality for Others:Leaders with ethical attributes guarantee that impartiality and righteousness are critical qualities of theircourse of decision making. This suggests that every single followeris treated in rather comparable manners excludingthe case that there is an obvious requirementforspecial handlingand the reason for this special handlingis clearly known. Alongwith this clearness, the reason forthe special handlingneed to be ethically sensible and acceptable (Mendonca and Kanungo, 2007).

• Honesty towards Others: Honesty is another critical quality of ethical leadership. The lack of honesty undermines trustwhich is an essential feature of an association between leaders and their followers. Conversely, honesty nurtures trust and establishes the association between the leaderand the followers.

• "The prevailingapproachesto CSR are so disconnected from business as to obscure many of the greatest opportunities for companies to benefit society (Porter and Kramer, 2006)."

• This concept explores the differentways in which CSR is defined and provides an account of success factors and business evidence.

• Corporate Social Responsibility Definition

• Corporate social responsibility (CSR) is the continuingcommitmentby business to behave ethically and contribute to economic developmentwhile improvingthe quality of life of the workforce and their families as well as of the local community and society at large (World Business Council for Sustainable Development,1999).

• "When firms “act”, they are expected to meet a minimum set of standards and obligations as morally defined and evaluated by these individuals and groups (Werhane and Freeman, 1999)."

• Businesses face ethical issues and decisions almost every day. The concept explores what is means for companies and what they can do to coordinate the interests of their stakeholders.

• Business Ethics Definition

• Business ethics is “the degree of moral obligation that may be ascribed to corporations beyond simple obedience to the laws of the state” (Kilcullen and Kooistra, 1999). It concerns “business situations, activities, and decisions where the issue of right and wrong are addressed…[meaning] morally right or wrong as opposed to, for example, commercially, strategically, or financially right or wrong” (Crane and Matten, 2007).

• Professional Ethics - Moral principles and standards that govern the conduct of the members of an organisation.

• Ethical Fundamental Principles – Integrity, Objectivity, Confidentiality, Professional Behaviour and Professional Competence and Due Care

• Corporate Code of Ethics – it is a formal written Code of ethical behaviour, created by the boards of directors of a business that is available to all employees and serve as guide to all decisions and actions.

• Corporate Social Responsibility – is business' commitment to carry out all activities in an ethical way, taking account the social, economic and environmental impact, and human rights.

• Moral and Social Responsibility - businesses are accountable for comply with their social responsibility and all actions and decisions of the business must not disrupt stakeholders interest - balance between economic growth, welfare of society and environment

Stakeholders - is any person, organization, local community who can affect or be affectedby the business's actions, goals and policies.

Primary Stakeholders

• Shareholders

Customers

Employees

Business Partners

Community and Environment

• Have more interest in the business outcomes since are directly benefiting from or affected by the business activity

Secondary Stakeholders

• Government and Regulatory Bodies

Competitors

Trade Groups

Civic Organizations

Media

• Don not have a direct participation in the activities of the business but they are affected by or can affect its actions

• Primary Stakeholders have a higherinterestin the business due to higherrelevance in the business. Customers have high interest in the CSR activities of the business, since they want know how this will impact the products and services provided by the businesses.

• Employees, in otherside, have interestin the benefits and improvements that CSR can bring to their workplace and balance between work and personal life.

• Finally, Shareholders, as main investors in the business, have interest in the financial benefits that CSR can bringto their operations.

• Secondary Stakeholders as Governmentand Regulatory Bodies evaluate how businesses are followingCSRprocedures and comply with their legal duties. Otherstakeholders as Trade Unions will look for compliance of the business in the employment law.

• The main benefits for a business for the complianceof the CSR regulationsare:

• Customer satisfaction and retention, and increase of future contracts

• Increase reputation and differentiation from the competitors

• Boost shareholders and investors confidence

• Happier and more skilled workforce

• Administration and operation costs reduction

• Attractive position in market and more funding accessible

• Financial reports are formal records of all financial transactions of the business which are used to communicate final informationto the stakeholders.

• Financial reportingincludes the following:

• Income statement – shows the profit and loss duringa period of time. The amount of profit or loss is calculated by addingall revenues and subtractingall expenses relatedto operatingand non-operating activities.

• Balance sheet – shows the financial position of the business where displays the assets and how the assets are financed, by either debt or equity. Business can calculate their profitability (gross profit margin, ROCE and OperatingProfit Margin), liquidity (current and acid test ratio) and financial (Receivable, Payable and Inventory Collection and Turnover) efficiency with the figures shown in the statement.

• Statement of cash flows - acts as a connection between the income statement and balance sheet, this is by showing the cash inflows and outflows. An analyse of operating activities ( principal revenue-generating activities of an organization and other activities that are not investing or financing),

• Investing Activities ( cash flows from the acquisition and disposal of long-term assets and other investments not included in cash equivalents) and

• Financing Activities ( cash flows that result in changes in the size and composition of the contributed equity capital or borrowings of the entity )

• Statement of stockholders'equity -shows the changes in all of the major equity accounts which reports the transactions that increase or decrease the equity accounts during an accounting period.

• Finally Notes to the financial statements – they are disclosures which allow additional information not included in the financial statements such as accounting methods used, change in methods used in previous reporting periods and in future transactions that may affect future profitability.

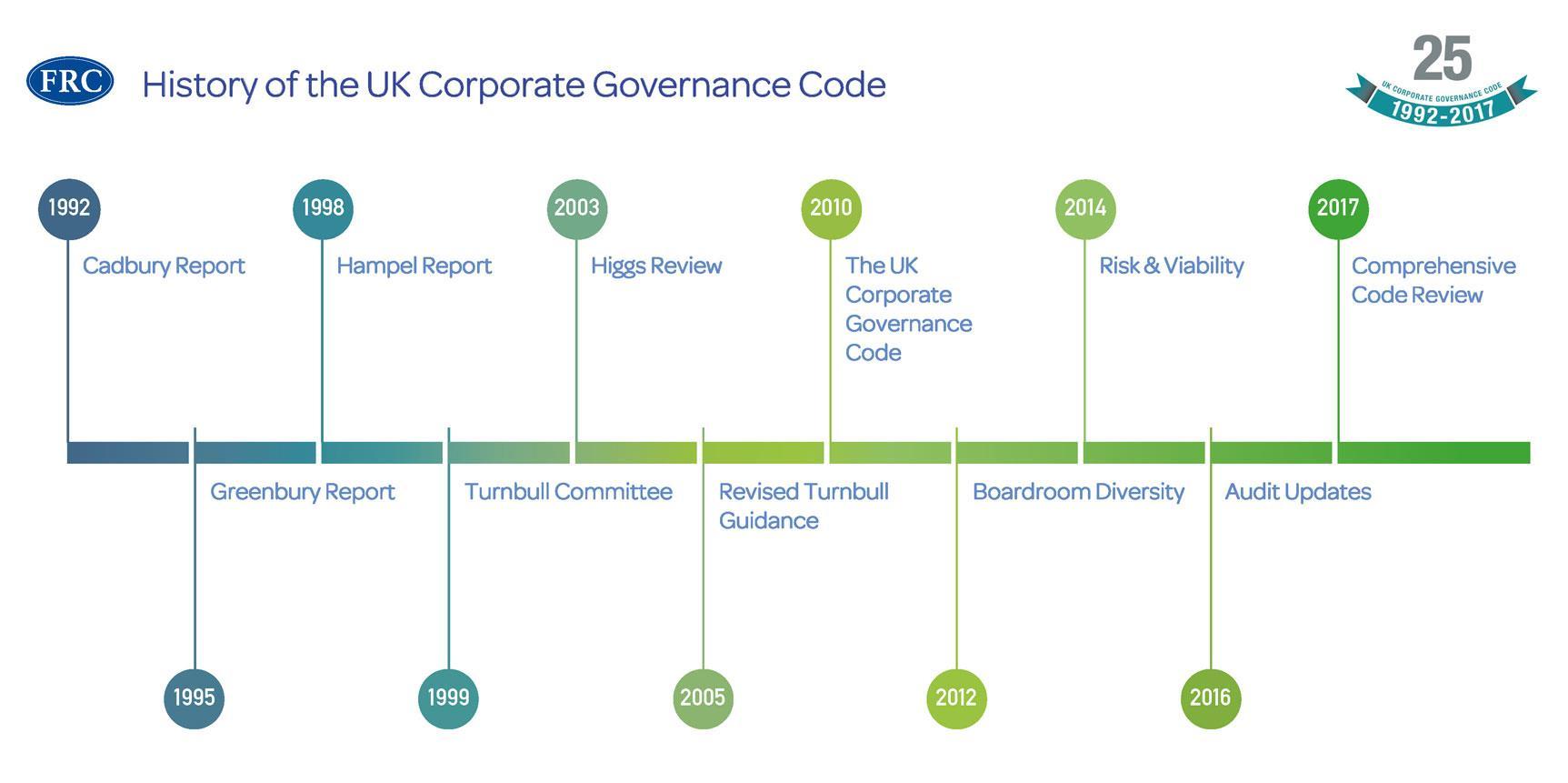

• “Corporate Governance is the system by which companies are directed and controlled”

– Cadbury Report 1992

• CorporateGovernance is a set of relationshipsbetween the directors of a business,shareholders and remain stakeholders and also provides the structure which builds the foundationwhere the objectives of the company are set, and how those objectives will be achieved and monitored duringthe business activity.

• Fairness – All decisions and values must be balanced by taking into account all stakeholders who has a legitimate interestin the business.

• Transparency – Open and clear disclosure of all information and financial statements to all shareholders and stakeholders.

• Innovation – Recognize that the needs of the business and stakeholders an change and this can impact how a business complies with codes of corporate governance.

• Scepticism – Be open and questioningdecisions mustbe always be engaged to effectively challenge managementdecisions.

• Independence – Independentof mind and appearance according ethical code

• Honesty – Truth tellingand not misleadingstakeholders

• Responsibility – Management is responsible and should act when corrective actions are required and penalize mismanagementof any level.

• Accountability – Be answerable forthe consequences of theirdecisions to shareholders and stakeholders

• Reputation – Follow corporate governance ethical behaviourand neverjeopardize business by poormanagement

• Judgement – Take decisions thatenhance business prosperity

• Integrity – Straightforward dealing, honesty and completeness.

• Corporate Governance is important for the good governance of a business. This is creates and develop:

• Management, awareness, evaluation and mitigation of risk – have an adequate and appropriate systems in place;

• Overall performance is enhanced by good management within set practice guidelines in place;

• Attract new investment and improve credibility next to the investors

• Wiliness to apply the good practices and have clear roles and duties establishin all business areas.

• Be accountable in all governance framework not only to the shareholders but all stakeholders

• Provides a framework to pursue the objectives of the business in an ethical and effective way which create safeguards against misuse of resources and information of the business

• Corporate Governance compliance gives a good reputationand confidence next to publicand government authorities and regulatorswhich protects value of shareholder’s investment

• Ethical behaviour can be achieve through:

• Effective management – unsure adherence to ethical behaviour

• Convey and reinforce the guidelines related to corporate governance

• Promote integrity – meaningstraightforward deals and completeness

• Underpin investor confidence

• Maintain the independence and ensure ethical principles are reinforced alongthe business, increasingcredibility with the workforce and working towards the same objectives

• Encourage more proactive involvement – increasingteam work and productivity

• Provide accurate and timely reportingand operationaldata, allowingto rectify and plan the business activities in a more beneficial way for the business and for employees.

• Business can increase their operational risk - risk that arises from the way in which an organisationoperates its business functions such as Reputational risk, Process risk – processes used by organisation,People risk

• System risk – control over access to system information and use of it, Legal risk, Event risk and Risk of unethical behaviour– code of conduct. In a business when ethical issues arise, the issue must be identify and the correct course of action take in ethical issues and eliminateor minimize the issue.

• Examples of ethical issues are, as followed:

• Decision making issues – arisingfrom puttingprofits above the consumer protection and fair treatment (example tax avoidance)

• Inappropriate behaviours and discriminationinside the workplace – ensure all employees feel secure and respected (example falsifyingdocuments and reports).

• Inappropriate incentive systemsin place which not give the same opportunities to employees and compensationare not distributed fairly (example fraud);

• Failingto comply with government regulationand laws, manipulate financialstatements to enhance position next to the investors and jeopardize the reputationof the business (illegally evadingtaxes).

• Practical steps that should be taken to deal with ethical situations:

• Analysis of the situation

• Identifyingthe ethical issues

• Consideringthe alternative options according corporate governance guideline

• State the best course of action based on the steps above

• Document and report the situation to higher management

• Codes of conduct:

• Professional Code of Ethics

• IESBA Code of Ethics

• IFAC Code of Ethics

• UK Corporate Governance Code

• Greenbury Code, Hamper & Cadbury Report

• OECD (Organisation forEconomic Co-operation and Development)

• Development of a leadership culture within the firm that pressures the importance of obedience with corporate governance and act in the stakeholders interest

• Policies and procedures to apply and evaluate quality control of engagements

• Policies are documented relatedto the identification of threats, compliance with the fundamental principles of governance, the evaluation of the significance of threats and the identificationand the application of safeguards to eliminate or reduce the threats

• Timely communication of a business’s policies and procedures, includingany changes to them •

• Educational, training and continuous professional development requires to maintain professional due care in all matters of business

• Disciplinary systems in place to promote compliance with the policies and procedures of business

• Create and make available policies and procedures to encourage and empower every member to communicate to management within the firm any issue related to compliance with the fundamental principles.

• Discussing ethical issues in board meeting to assess the strategies adopted by the entity will not be affected by any ethical issue.

• Effective systems operated by the employing organisation, which allow colleagues, employers and any member of the public to identify unprofessional or unethical behaviour

• An explicitly responsibility and duty to report breaches of ethical requirements.

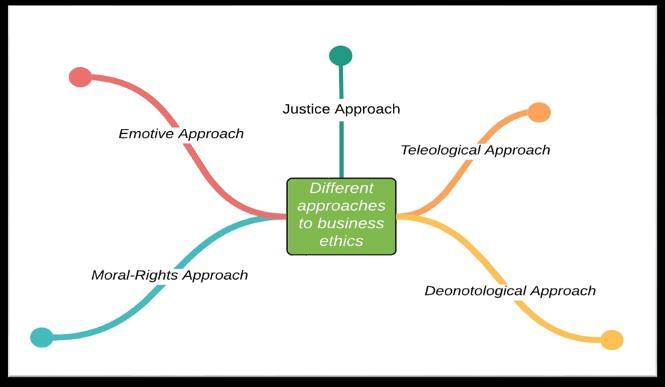

Chand, S. 5 Different Approaches towards Ethical Behaviour in Business

1. Teleological approach:moral conduct is determined based on an activity’s consequences

2. Deontological approach:the focus is placed on what the most “right” option is, based on moral principles

3. Emotive approach:based on an individual’s emotions, not on morals and ethics

4. Moral-rights approach:views behaviour as protectingand respectingfundamental humanrights and equal treatment on behalf of the law

5. Justice approach:based on the fair treatment of all people accordingto specified standards

Chand, S. 5 Different Approaches towards Ethical Behaviour in Business

• The UK Governmenthas played a very importantrole in regard to the promotion of corporate social responsibility for the last 40 years.

• There are four main strands to the United Kingdom Government’s involvements regardingCSR and their activities:

1. Environment(environmentand estates): The UK Governmentis committed to reducing their direct impact on the environmentthrough the active managementof their emissions, consumption of natural resources,and waste.

2. Procurement(purchasingand finance): Regardingthe lifespan of a project, the UK Governmenttries its utmost to establish a procurementroute which is the most beneficial as far as CSR is concerned. This means that 90% of the government’s supply train contracts are implemented and maintained via the use of government frameworks.

3. Community (skills matching, fundraising and volunteering): The UK Government believes that it is important to build a sense of community and have a positive impact on society, and therefore, it has created a culture which promotes employee skills matching, fundraising,and volunteering.The government also actively supports local communities and businesses in which it operates.

4. People (health, wellbeing and human resources):

The UK Government aims to develop a workplace that encourages equal opportunitiesfor everyone as well as diversity. It serves to support employee wellbeing and health and it actively encourages personal developmentthrough a program called “five-days-a-year” learning programme.

Financial sustainability, accountability, competitive advantage (Hoskisson, Hitt and Ireland, 2004).

Applies emotional and social intelligence (Goleman, 2006).

Organisational silence ‘why organisations don’t communicate’ (Morrison and Milliken, 2000).

Ethical, authentic (George, 2003).

Elements of strategic management, adapted from Johnson and Scholes (1993).

"Strategic planningconcerns how an organisationmakes sense of where it is going, and the path it will adopt to get there (Kaplan and Beinhocker, 2003)"

This concept reviews the process of strategic planningand shows how companies can implementstrategies to enhance company and productcompetitiveness. It also offers a summary of the benefits of the process and examples of its application.

Strategic planningis a disciplined effortto produce fundamental decisions and actions aimed at shapingthe nature and direction of an organisation’s activities (Bryson,1988; Rudd et al., 2008).

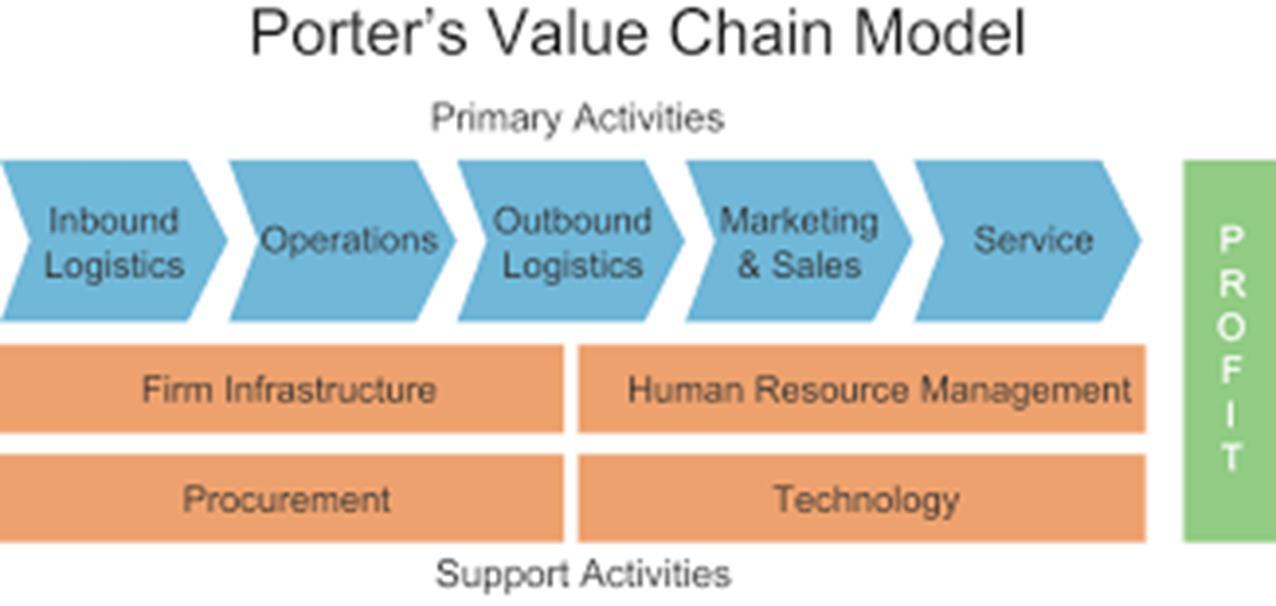

"Strategy should reflecta distinctive value chain that configures all key business processes and operations (operations, HRM, marketing, service delivery, etc.) in a unique way that is difficultforcompetitors to imitate (Porter, 2001)."

This concept reviews the formal and rational processes that can help organisations achieve the strategic positioningof theirproducts and brands. It also addresses the success factors and implementation recommendations.

Strategic positioningis concerned with the way in which a business as a whole distinguishes itself in avaluable way from its competitors and delivers value to specificcustomer segments (Wickham, 2001: 230).

"Organisations can be described as a collection of departments or functions that align together to cope with uncertainty (Hickson et al., 1971)."

Power and politics are understood as fundamental and important factors in managing strategic contingencies. Relevant practical case evidence and implication advice provided helps leaders to minimise the potential impact caused by a risk factor, threat or emergency.