BELTON ISD BENEFITS 2023-2024 EFFECTIVE 09/01/2023 - 08/31/2024 YOURHEALTH YOUR FAMILY YOURLIFE WWW.MYBENEFITSHUB.COM/BELTONISD

Dana Reed

Employee Benefits Office

Office: (254)215-2074

Fax: (254) 215-2038

Email: Dana.Reed@bisd.net

Erica Ramos

Employee Benefits Office

Office: (254)215-2072

Fax: (254)215-2038

Email: Erica.Ramos@bisd.net

Tanya Bane

Employee Benefits Office

Office: (254) 215-2019

Fax: (254) 215-2038

Email: Tanya.Bane@bisd.net

Medical – TRS

Basic (District Paid) Life -MetLife

Voluntary Life - MetLife

Cancer – Guardian

Accident - MetLife

Hospital Indemnity - MetLife

Dental - Ameritas

Vision – Vision Service Plan (VSP)

Site Access To access your employer online enrollment site, , you can ebsite

mployee ame Robert Smith, SS# 123-45-6789

Default Password

User Name: smith 6789

Password password once you enter the site.

INTRODUCTION

HOW DO I ENROLL?

or cancel coverage during the year if you have a qualifying change in the family or employment status that causes you to include:

• •

WHO IS AN ELIGIBLE DEPENDENT?

• • • •

NEW HIRE ENROLLMENT

of the following month.

Loss or gain of eligibility for other insurance (including

WHEN WILL I RECEIVE ID CARDS? ti rary ID card or give your provider the insurance company’s phone number to call and verify your coverage if you do not havean ID card at the time of service. VISION cards are NOT provided.

@

Annual Open Enrollment

The period once per year during which existing employees are given the opportunity to enroll in or change their current elections.

Enrollment Plan Year

September 1 – August 31st

New Hire Eligibility

You have 31 days from your new hire date to make your benefit elections.

Qualifying Event

IRS guidelines allow you to make changes outside of Open Enrollment for the following defined reasons:

Marriage/Divorce

Birth or Adoption

Death of spouse or covered dependent

Change in your spouse’s work status that affects eligibility

Medicare eligibility

Annual Deductible

The amount you pay each plan year before the plan begins to pay covered expenses.

Co- Insurance

After any applicable deductible, your share of the cost of a covered health care service, calculated as a percentage (for example,20%)of the allowed amount for the service.

Co-Payment

Specific dollar amount you mustpay your providerper visit.

Balance Billing

Occurs when providers bill a patient for the difference between the amount they charge and the amount that the patient’s insurance pays. This normally happens when using services out of network. If this happens please call your medical insurance provider to reconcile the charges.

In- and- Out of Network Coverage

In-network doctors, hospitals, optometrists, dentists and other providers who have contracted with the plan as a network provider. Lowers chargesand reduces out pocket expenses. Out of network charges a higher payment and higherout of pocket cost. Check your plan to ensurethey provide out-of-network coverage.

Out- of- Pocket/Out- of- Pocket Maximum

Out-of-Pocket:expensesyou mustpay for health related services that are above your monthly premium. Out-ofPocket Maximum: the mostan eligible or insured person can pay in co-insuranceforcovered expenses per plan year.

High Deductible Plan

Plan does not pay until deductible is met

Pay less out of each paycheck

Pay more out of pocket at doctor until deductible is met

Higher Deductible

Wellness visits 100%

Same deductible for medical and prescription

Enroll in HAS/Flexible Spending to help pay for out of pocket cost

In and out of network coverage – with two separate deductibles

HMO/PPO Plans

Pay more out of paycheck

Pay less at doctor

Lower deductible

Medical and prescription have different deductibles

Co-payments for office visits

Must use a provider within the network

Facility Fee

A facility fee is a charge that you have to pay when you see a doctor at a clinic that is not owned by that doctor. Facility fees are charged in addition to any other charges for the visit. Not all clinics or hospital charges a facility fee.

New Rx Benefits!

• Express Scripts is your new pharmacy benefits manager! CVS pharmacies and most of your preferred pharmacies and medication are still included.

•Certain specialty drugs are still $0 through SaveOnSP

*Pre-certification for genetic and specialty testing may apply. Contact a PHG at

questions.

TRS contracts with HMOs in certain regions to bring participants in those areas additional options. HMOs set their own rates and premiums. They’re fully insured products who pay their own claims.

You can choose this plan if you live in one of these counties: Austin, Bastrop, Bell, Blanco, Bosque, Brazos, Burleson, Burnet, Caldwell, Collin, Coryell, Dallas, Denton, Ellis, Erath, Falls, Freestone, Grimes, Hamilton, Hays, Hill, Hood, Houston, Johnson, Lampasas, Lee, Leon, Limestone, Madison, McLennan, Milam, Mills, Navarro, Robertson, Rockwall, Somervell, Tarrant, Travis, Walker, Waller, Washington, Williamson

You can choose this plan if you live in one of these counties: Cameron, Hildalgo, Starr, Willacy

You can choose this plan if you live in one of these counties: Andrews, Armstrong, Bailey, Borden, Brewster, Briscoe, Callahan, Carson, Castro, Childress, Cochran, Coke, Coleman, Collingsworth, Comanche, Concho, Cottle, Crane, Crockett, Crosby, Dallam, Dawson, Deaf Smith, Dickens, Donley, Eastland, Ector, Fisher, Floyd, Gaines, Garza, Glasscock, Gray, Hale, Hall, Hansford, Hartley, Haskell, Hemphill, Hockley, Howard, Hutchinson, Irion, Jones, Kent, Kimble, King, Knox, Lamb, Lipscomb, Llano, Loving, Lubbock, Lynn, Martin, Mason, McCulloch, Menard, Midland, Mitchell, Moore, Motley, Nolan, Ochiltree, Oldham, Parmer, Pecos, Potter, Randall, Reagan, Reeves, Roberts, Runnels, San Saba, Schleicher, Scurry, Shackelford, Sherman, Stephens, Sterling, Stonewall, Sutton, Swisher, Taylor, Terry, Throckmorton, Tom Green, Upton, Ward, Wheeler, Winkler, Yoakum

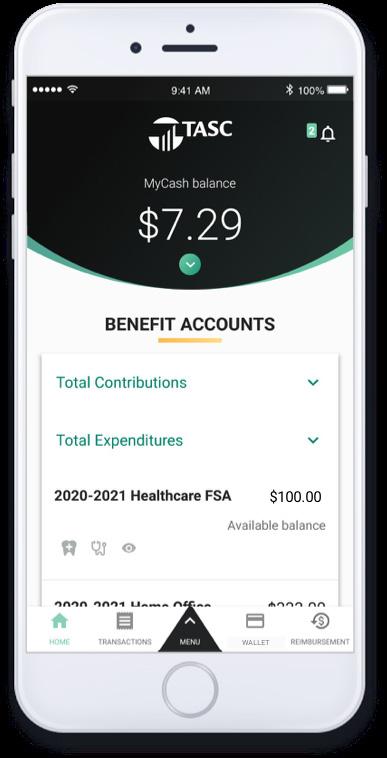

Maximize your savings

A Health Savings Account, or HSA, is a tax-advantaged savings account you can use for healthcare expenses. Along with saving you money on taxes, HSAs can help you grow your nest egg for retirement.

• Contribute to your HSA by payroll deduction, online banking transfer or personal check.

• Pay for qualified medical expenses for yourself, your spouse and your dependents. Both current and past expenses are covered if they’re from after you opened your HSA.

• Use your HSA Bank Health Benefits Debit Card to pay directly, or pay out of pocket for reimbursement or to grow your HSA funds.

• Roll over any unused funds year to year. It’s your money — for life.

• Invest your HSA funds and potentially grow your savings.¹

You can use your HSA funds to pay for any IRS-qualified medical expenses, like doctor visits, hospital fees, prescriptions, dental exams, vision appointments, over-the-counter medications and more. Visit hsabank.com/QME for a full list.

You’re most likely eligible to open an HSA if:

• You have a qualified high-deductible health plan (HDHP).

• You’re not covered by any other non-HSA-compatible health plan, like Medicare Parts A and B.

• You’re not covered by TriCare.

• No one (other than your spouse) claims you as a dependent on their tax return.

The IRS limits how much you can contribute to your HSA every year. This includes contributions from your employer, spouse, parents and anyone else.2 Maximum contribution limit

$3,850

You may be eligible to make a $1,000 HSA catch-up contribution if you’re:

• Over 55.

• An HSA accountholder.

• Not enrolled in Medicare (if you enroll mid-year, annual contributions are prorated).

A huge way that HSAs can benefit you is they let you save on taxes in three ways.

1 You don’t pay federal taxes on contributions to your HSA.3

2 Earnings from interest and investments are tax-free.

3

Distributions are tax free when used for qualified medical expenses.

¹ Investment accounts are not FDIC insured, may lose value and are not a deposit or other obligation of, or guarantee by the bank. Investment losses which are replaced are subject to the annual contribution limits of the HSA.

2 HSA contributions in excess of IRS limits are subject to penalty and tax unless the excess and earnings are withdrawn prior to the tax filing deadline as explained in IRS Publication 969.

3 Federal tax savings are available regardless of your state. State tax laws may vary. Consult a tax professional for more information.

Educator Options Voluntary Long Term Disability Coverage Highlights – Texas Belton Independent School District

Voluntary Long Term Disability Insurance

Standard Insurance Company hasdeveloped this document to provide you withinformation about the optional insurance coverage youmay select throughBelton Independent School District.Writtenin non-technical language, this is notintended as a complete descriptionof the coverage.If you have additional questions, please check with yourhuman resources representative.

Eligibility

To become insured, you must be:

A regular employee of Belton Independent School District, excluding temporary or seasonal employees, full-time members of the armed forces, leased employees or independent contractors

Actively at work at least 15 hours each week

A citizen or resident of the United States or Canada

Please contact your human resources representative for more information regarding the following requirements that must be satisfied for your insurance to become effective. You must satisfy:

Eligibility requirements

An eligibility waiting period of 0 days

An evidence of insurability requirement, if applicable

An active work requirement. This means that if you are not actively at work on the day before the scheduled effective date of insurance, your insurance will not become effective until the day after you complete one full day of active work as an eligible employee.

Benefit Amount

You may select a monthly benefit amount in $100 increments from $200 to $8,000; based on the tables and guidelines presented in the Rates section of these Coverage Highlights. The monthly benefit amount must not exceed 66 2/3 percent of your monthly earnings.

Benefits are payable for non-occupational disabilities only. Occupational disabilities are not covered.

Plan Maximum Monthly Benefit: 66 2/3 percent of predisability earnings

Plan MinimumMonthly Benefit: 10percent of your LTD benefit before reduction by deductible income

The benefit waiting period is the period of time that you must be continuously disabled before benefits become payable. Benefits are not payable during the benefit waiting period. The maximum benefit period is the period for which benefits are payable. The benefit waiting period and maximum benefit period associated with your plan options are shown below:

Options1-6: Maximum Benefit Period of 3 years for Sickness

If you become disabledbefore age 64, LTD benefits may continue during disability for 3 years. If you become disabled at age 64or older, the benefit duration is determined by your age when disability begins:

Options1-6: Maximum Benefit Period To Age 65 for Accident

If you become disabled before age 62, LTD benefits may continue during disability until you reach age 65. If you become disabled at age 62 or older, the benefit duration is determined by your age when disability begins: AgeMaximum Benefit Period

Preexisting Condition Exclusion

A general description of the preexisting condition exclusion is included in the Group Voluntary Long Term Disability Insurance for Educators and Administrators brochure. If you have questions, please check with your human resources representative.

Preexisting Condition Period: The 90-dayperiod just before your insurance becomes effective

Exclusion Period: 12 months

For the first 30 days of disability, The Standard will pay full benefits even if you have a preexisting condition. After 30 days, The Standard will continue benefits only if the preexisting condition exclusion does not apply.

Coverage Highlights – Texas Belton Independent School District

For the plan’s definition of disability, as described in your brochure, the own occupation period is the first 24months for which LTD benefits are paid.

The any occupation period begins at the end of the own occupation period and continues until the end of the maximum benefit period.

Employee Assistance Program (EAP) – This program offers support, guidance and resources that can help an employee resolve personal issues and meet life’s challenges.

Family Care Expense Adjustment – Disabled employees faced with the added expense of family care when returning to work may receive combined income from LTD benefits and work earnings in excess of 100 percent of indexed predisability earnings during the first 12 months immediately after a disabled employee’s return to work.

Special Dismemberment Provision – If an employee suffers a lost as a result of an accident, the employee will be considered disabled for the applicable Minimum Benefit Period and can extend beyond the end of the Maximum Benefit Period

Reasonable Accommodation Expense Benefit –Subject to The Standard’s prior approval, this benefit allows us to pay up to $25,000 of an employer’s expenses toward work-site modifications that result in a disabled employee’s return to work.

Survivor Benefit –A Survivor Benefit may also be payable. This benefit can help to address a family’s financial need in the event of the employee’s death.

Return to Work (RTW) Incentive –The Standard’s RTW Incentive is one of the most comprehensive in the employee benefits history. For the first 12 months after returning to work, the employee’s LTD benefit will not be reduced by work earnings until work earnings plus the LTD benefit exceed 100 percent of predisability earnings. After that period, only 50 percent of work earnings are deducted.

Rehabilitation Plan Provision –Subject to The Standard’s prior approval, rehabilitation incentives may include training and education expense, family (child and elder) care expenses, and job-related and job search expenses.

LTD benefits end automatically on the earliest of:

The date you are no longer disabled

The date your maximum benefit period ends

The date you die

The date benefits become payable under any other LTD plan under which you become insured through employment during a period of temporary recovery

The date you fail to provide proof of continued disability and entitlement to benefits

Employees can select a monthly LTD benefit ranging from a minimum of $200 to a maximum amount based on how much they earn. Referencing the appropriate attached charts, follow these steps to find the monthly cost for your desired level of monthly LTD benefit and benefit waiting period:

1.Find the maximum LTD benefit by locating the amount of your earnings in either the Annual Earnings or Monthly Earnings column. The LTD benefit amount shown associated with these earnings is the maximum amount you can receive. If your earnings fall between two amounts, you must select the lower amount.

2.Select the desired monthly LTD benefitbetween the minimum of $200 and the determined maximum amount, making sure not to exceed the maximum for your earnings.

3.In the same row, select the desired benefit waiting period to see the monthly cost for that selection.

If you have questions regarding how to determine your monthly LTD benefit, the benefit waiting period, or the premium payment of your desired benefit, please contact your human resources representative.

If you become insured, you will receive a group insurance certificate containing a detailed description of the insurance coverage. The information presented above is controlled by the group policy and does not modify it in any way. The controlling provisions are in the group policy issued by Standard Insurance Company.

You are eligible for a maximum monthly benefit

Educator Options Voluntary Long Term

Educator

Options Voluntary Long Term Disability Coverage Highlights – Texas Belton Independent School District

You are eligible for a maxim um 0/7 Eliminatio n Period

benefit 14/14 Eliminatio n Period

30/30 Eliminatio n Period

60/60 Eliminatio n Period

90/90 Eliminatio n Period

180/180 Eliminatio n Period $73,800 $4,100 $107.42 $83.64 $61.50 $58.22 $46.74 $44.28 $75,600 $4,200 $110.04 $85.68 $63.00 $59.64 $47.88 $45.36 $77,400 $4,300 $112.66 $87.72 $64.50 $61.06 $49.02 $46.44 $79,200 $4,400 $115.28 $89.76 $66.00 $62.48 $50.16 $47.52 $81,000 $4,500 $117.90 $91.80 $67.50 $63.90 $51.30 $48.60 $82,800 $4,600 $120.52 $93.84 $69.00 $65.32 $52.44 $49.68 $84,600 $4,700 $123.14 $95.88 $70.50 $66.74 $53.58 $50.76 $86,400 $4,800 $125.76 $97.92 $72.00 $68.16 $54.72 $51.84 $88,200 $4,900 $128.38 $99.96 $73.50 $69.58 $55.86 $52.92 $90,000 $5,000 $131.00 $102.00 $75.00 $71.00 $57.00 $54.00 $91,800 $5,100 $133.62 $104.04 $76.50 $72.42 $58.14 $55.08 $93,600 $5,200 $136.24 $106.08 $78.00 $73.84 $59.28 $56.16 $95,400 $5,300 $138.86 $108.12 $79.50 $75.26 $60.42 $57.24 $97,200 $5,400 $141.48 $110.16 $81.00 $76.68 $61.56 $58.32 $99,000 $5,500 $144.10 $112.20 $82.50 $78.10 $62.70 $59.40 $100,800 $5,600 $146.72 $114.24 $84.00 $79.52 $63.84 $60.48 $102,600 $5,700 $149.34 $116.28 $85.50 $80.94 $64.98 $61.56 $104,400 $5,800 $151.96 $118.32 $87.00 $82.36 $66.12 $62.64 $106,200 $5,900 $154.58 $120.36 $88.50 $83.78 $67.26 $63.72 $108,000 $6,000 $157.20 $122.40 $90.00 $85.20 $68.40 $64.80 $109,800 $6,100 $159.82 $124.44 $91.50 $86.62 $69.54 $65.88 $111,600 $6,200 $162.44 $126.48 $93.00 $88.04 $70.68 $66.96 $114,400 $6,300 $165.06 $128.52 $94.50 $89.46 $71.82 $68.04 $115,200 $6,400 $167.68 $130.56 $96.00 $90.88 $72.96 $69.12 $117,000 $6,500 $170.30 $132.60 $97.50 $92.30 $74.10 $70.20 $118,800 $6,600 $172.92 $134.64 $99.00 $93.72 $75.24 $71.28 $120,600 $6,700 $175.54 $136.68 $100.50 $95.14 $76.38 $72.36 $122,400 $6,800 $178.16 $138.72 $102.00 $96.56 $77.52 $73.44 $124,200 $6,900 $180.78 $140.76 $103.50 $97.98 $78.66 $74.52 $126,000 $7,000 $183.40 $142.80 $105.00 $99.40 $79.80 $75.60 $127,800 $7,100 $186.02 $144.84 $106.50 $100.82 $80.94 $76.68 $129,600 $7,200 $188.64 $146.88 $108.00 $102.24 $82.08 $77.76 $131,400 $7,300 $191.26 $148.92 $109.50 $103.66 $83.22 $78.84 $133,200 $7,400 $193.88 $150.96 $111.00 $105.08 $84.36 $79.92 $135,000 $7,500 $196.50 $153.00 $112.50 $106.50 $85.50 $81.00 $136,800 $7,600 $199.12 $155.04 $114.00 $107.92 $86.64 $82.08 $138,600 $7,700 $201.74 $157.08 $115.50 $109.34 $87.78 $83.16 $140,400 $7,800 $204.36 $159.12 $117.00 $110.76 $88.92 $84.24 $142,200 $7,900 $206.98 $161.16 $118.50 $112.18 $90.06 $85.32 $144,000 $8,000 $209.60 $163.20 $120.00 $113.60 $91.20 $86.40

24

You own it

Youcanqualifybyanswering just3questions–noexamsorneedles.

You can take it with you when you change jobs or retire

purelife-plus

You pay for it through convenient payroll deductions

You can get a living benefit if you become terminally ill3 It’s Affordable

DURING

1.Beenactivelyatworkonafulltimebasis,performingusualduties?

2.Beenabsentfromworkduetoillnessormedicaltreatmentforaperiodof morethan5consecutiveworkingdays?

3.Beendisabledorreceivedtests,treatmentorcareofanykindinahospital ornursinghomeorreceivedchemotherapy,hormonaltherapyforcancer, radiation,dialysistreatment,ortreatmentforalcoholordrugabuse?

PureLife-plusisaFlexiblePremiumAdjustableLifeInsurancetoAge121.Aswithmostlifeinsuranceproducts, TexasLifecontractsandriderscontaincertain exclusions,limitations,exceptions,reductionsofbenefits,waitingperiodsandtermsforkeepingtheminforce.PleasecontactaTexasLiferepresentativeorsee thePureLife-plusbrochureforcostsandcompletedetails.ContractformICC18PRFNG-NI-18orFormSeriesPRFNG-NI-18.TexasLifeislicensedtodobusinessin theDistrictofColumbiaandeverystatebutNewYork.

21M058-CGeneric2001(exp0523)

PureLife-plusispermanentlifeinsurancetoAttainedAge121thatcanneverbecancelledaslongasyoupaythenecessarypremiums.Afterthe GuaranteedPeriod,thepremiumscanbelower,thesame,orhigherthantheTablePremium.Seethebrochureunder”PermanentCoverage”.

PureLife-plusispermanentlifeinsurancetoAttainedAge121thatcanneverbecancelledaslongasyoupaythenecessarypremiums.Afterthe GuaranteedPeriod,thepremiumscanbelower,thesame,orhigherthantheTablePremium.Seethebrochureunder”PermanentCoverage”.

Explore the coverage that makes it easy to give yourself and your loved ones more security today…and in the future

Basic Term Life

You employer provides you with Basic Term Life insurance coverage in the amount of $10,000.

For You

For Your Spouse

$20,000 increments to a maximum of the lesser of 4 times pay or $200,000

$10,000 increments to a maximum of the lesser of 100% of employee’s Supplemental Life Benefitor $100,000

For Your Dependent Children* $10,000

*Child(ren)’s Eligibility: Dependent children ages from birth to 26years oldand unmarriedare eligible for coverage.In TX, regardless of student status, child(ren) are covered until age 25.

You have the option to purchase SupplementalTerm Life Insurance. Listedbelow are your monthly rates (based onyour age) aswell as those for yourspouse(based on yourspouse age).Rates to cover your child(ren) are also shown.

*Note: rates are subject to the policy’s right to change premium rates, and the employer’s right to change employee contributions.

Use the table below to calculate your premium based on the amount of life insurance you will need.

1. Enter the rate from the table (example age 36)

2. Enter the amount of insurance in thousands of dollars (Example: for $100,000 of coverage enter $100)

3. Monthly premium (1) x (2)

The Total Control Account® settlement option provides your loved ones with a safe and convenient way to manage the proceeds of a life policy for claim payments of $5,000 or more, backed by the financial strength and claims paying ability of Metropolitan Life Insurance Company. They'll have the convenience of immediate access to any or all of their proceeds, through an interest bearing account with unlimited draftwriting privileges. The Total Control Account gives beneficiaries time to decide what to do with their proceeds, which can be very helpful to them during a difficult time.

To help ensure your decisionsare carried out

Like life insurance, a carefully prepared Will (SimpleorComplex), living will and Power of Attorney are important.

A willletsyou define your most important decisions, such as who will care for your childrenor inherit your property.

A living will ensures your wishes are carried out, and protects your loved ones from making these very difficult and personal medical decisions by themselves. Also called an “advanced directive,” it is a document authorized by statutes in all statesthat allows youto provide written instructions regarding use of extraordinary life-support measures, and appoint someone as yourproxy or representative to make decisions on maintainingextraordinary life-support if youshould become incapacitated and can’tcommunicate yourwishes.

Powers of Attorney allow you to plan ahead by designating someone you know and trust to act on your behalf in the event of unexpected occurrences, or if you become incapacitated. It is a written document that grants an individual the power to act on yourbehalf.

When you enroll forSupplementalTerm Life coverage, you will automatically receive Will Preparation Service at no extra cost to you. Both you and your spousewill have access to one of Hyatt Legal Plans nationwide network of 13,000participating attorneysfor face-to-face preparation or updating of a will, living will or powers of attorney.* When you use a participating plan attorney, there will be no charge for the services*. Call 1-800-821-6400 and a Client Service Representative will assist you.

*You also have the flexibility of using an attorney who is not participating in the Hyatt Legal Plans’ network and being reimbursed for covered services according to a set fee schedule. In that case you will be responsible for any attorney’s fees that exceed the reimbursed amount.

Personal service and compassion assistance to help probate your and yourspouse’s estates.

MetLife Estate Resolution Services is a valuable service included when you enroll for SupplementalTerm Life coverage. When your estate representative uses a participating Hyatt Legal plan attorney therewill be no charge for the services. A Hyatt Legal Plan attorney will consultface-to-face withyour beneficiariesorby telephone regarding the probate process for your estate. The attorney will also handle the probate of your andyour spouse’sestatesfor your executor or administrator. This can help alleviate the financial and administrative burden upon your loved ones in their time of need.

So you can keep your coverage even if you leave your current employer

Should you leave Belton Independent School Districtfor any reason, and your Supplementaland Dependent Term Lifeinsurance under this plan terminates, you will have an opportunity to continue group term coverage (“portability”) under a different policy, subject to plan design and state availability. Rates will be based on the experience of the ported group and MetLife will bill you directly. Rates may be higher than your current rates. To take advantage of this feature, you must have coverage of atleast $10,000 up to a maximum of $2,000,000.

Portability is also available on coverage you’ve selected for your spouseand dependent child(ren). The maximum amount of coverage for spouses is $250,000; the maximum amount of dependent child coverage is $25,000. Increases, decreases and maximums are subject to state availability.

Generally, there is no minimum time for you to be covered by the plan before you can take advantage of the portability feature. Please see your employerfor specific details.

Please note that if you experience an event that makes you eligible for portable coverage, please call a MetLife representative at 1-888-252-3607 or contact your employerfor more information.

Transition Solutions is a service designed to help provide assistance in making financial decisions based on the major events in your life including changes in employment, retirement or your benefits status. Contact your employer or plan administrator for more information.

This insurance offering from your employer and MetLife comes with additional features that can provide assistance to you and your family.

You can receive up to 80% of your SupplementalTerm Life insurance proceeds to a maximum of $200,000 in the event that you become terminally ill and are diagnosed with less than 24months to live. This can go a long way toward helping your family meet medical and other related expenses at this difficult time. The Accelerated Benefit Option is also available to spousesinsured under Dependent Life insurance plans. This option is not available for dependent child coverage.

You can generally convert your Group Term Life insurance benefits to an Individual Whole Life insurance policy if your coverage terminates in whole or in part due to your retirement, termination of employment, or, a change in your employee class. Conversion is available on all Group Life insurance coverages. If you experience an event that makes you eligible to convert your coverage, you can speak with a MetLife representative by calling: 1-877-275-6387. Please contact your employer for more information.

Offering continued coverage when you need it most

If you become Totally Disabled, you may qualify to continue certain insurance. You may also be eligible for waiver of your Supplementaland Dependent Term Life insurance premium until you reach age 65, die or recover from your disability, whichever is sooner.

Total Disability or Totally Disabled means you are unable to do your job and any other job for which you are fit by education, training or experience, due to injury or sickness. The Total Disability must begin before age 60, and your waiver will begin after you have satisfied a 9-month waiting period of continuous disability. The Waiver of Premium will end when you turn age 65, die or recover. Please note that this benefit is available after you have participated in the SupplementalTerm Life Plan for one year and it is only available to you. This one-year requirement applies to new participants in the plan.

Like most insurance plans, this plan has exclusions. Supplementaland Dependent Life Insurancedoes not provide payment of benefits for death caused by suicide within the first two years (one year for group policies issued in Missouri, North Dakota and Colorado) of the effective date of the certificate or an increase in coverage. This exclusionary period is one year for residents of Missouri and North Dakota. If the group policy was issued in Massachusetts, the suicide exclusion does not apply to dependent life coverage. The suicide exclusion does not apply to residents of Washington, or to individuals covered under a group policy issued in Washington.

Complete your enrollment form and return it today! Be sure to indicate your Beneficiary.

Act Now During the Enrollment Period.

Note: If you do not wish to make a change to your coverage, you do not need to do anything.

*All applications are subject to review and approval by Metropolitan Life Insurance Company. Based on the plan design and the amount of coverage requested, a Statement of Health may need to be submitted to complete your application.

Enrollment in this SupplementalTerm Life insurance plan is available without providing medical informationas long as:

The enrollment takes place prior to the enrollment deadline, and You are continuing the coverage you had in the last year

The enrollment takes place within 31 days from the date you become eligible for benefits.

If you do not meet all of the conditions stated above, you will need to provide additional medical information by completing a Statement of Health form.

You must be covered in order to obtain coverage for your spouseand child(ren).

Your spouseand dependent children do not need to provide medical information as long as:

The enrollment takes place prior to the enrollment deadline, and You are continuing the coverage you had for your spouseand child(ren) in the last year

The enrollment takes place within 31 days from the date you become eligible for benefits, and You are enrolling for spousecoverage equal to/less than $50,000.

If you do not meet all of the conditions stated above, you will need to provide additional medical information by completing a Statement of Health form.

You must be Actively at Work on thedate your coverage becomes effective. Your coverage must be in effect in order for your spouse’s and eligible children’s coverage to take effect. In addition, your spouseand eligible child(ren) must not be home or hospital confined or receiving or applying to receive disability benefits from any source when their coverage becomes effective.

If Actively at Work requirements are met, coverage will become effective onthe first of the month following the receipt of your completed application for all requests that do not require additional medical information. A request for Your amount that requires additional medical information and is not approved by the date listed above will not be effective until the later of the date thatnotice is received that MetLife has approved the coverage or increase if you meet Actively at Work requirements on that date, or the date that Actively at Work requirements are met after MetLife has approved the coverage or increase. The coverage for your spouseand eligible child(ren) will take effect on the date they are no longer confined, receiving or applying for disability benefits from any source or hospitalized.

You can select any beneficiary(ies) other than your employerfor your Supplementalcoverage, and you may change your beneficiary(ies) at any time. You can also designate more than one beneficiary. You are the beneficiary for your Dependent coverage.

Pursuant to IRS Circular 230, MetLife is providing you with the following notification: The information contained in this document is not intended to (and cannot) be used by anyone to avoid IRS penalties. This document supports the promotion and marketing of insurance products. You should seek advice based on your particular circumstances from an independent tax advisor.

3 Subject to state law, and/or group policyholder direction, the Total Control Account is provided for all Life and AD&D benefits of $5,000 or more. The TCA is not insured by the Federal Deposit Insurance Corporation or any government agency. The assets backing the TCA are maintained in MetLife’s general account and are subject to MetLife’s creditors. MetLife bears the investment risk of the assets backing the TCA, and expects to earn income sufficient to pay interest to TCA Accountholders and to provide a profit on the operation of the TCAs. Guarantees are subject to the financial strength and claims paying ability of MetLife.

5 Will Preparation Services are offered by Hyatt Legal Plans, Inc.,a MetLife company, Cleveland, Ohio. In certain states, Will Preparation services are provided through insurance coverage underwritten by Metropolitan Property and Casualty Insurance Company and Affiliates, Warwick, Rhode Island. For New York sitused cases, the Will Preparation service is an expanded offering that includes office consultations and telephone advice for certain other legal matters beyond Will Preparation. Tax Planning and preparation of Living Trusts are not covered by the Will Preparation Service.

6 Estate Resolution Services are offered by Hyatt Legal Plans, Inc., a MetLife company, Cleveland, Ohio. In certain states, Estate Resolution Services are provided through insurance coverage underwritten by Metropolitan Property and Casualty Insurance Company and Affiliates, Warwick, Rhode Island. The following are not covered by the Estate Resolution Service: Matters in which there is a conflict of interest between the executor, administrator, any beneficiary or heir and the estate; any disputes with the Policyholder, Employer, Plan Attorneys, MetLife and/or any of its affiliates; any disputes involving statutory benefits; Will contests or litigation outside Probate Court; Appeals; Court costs, filing fees, recording fees, transcripts, witness fees, expenses to a third party, judgments or fines; and frivolous or unethical matters.

9 Transition Solutions Specialists are Financial Services Representatives of MetLife or New England Financial, a MetLife company. Certain conditions apply.

10 The Accelerated Benefits Option is subject to state availability and regulation. The accelerated life insurance benefits offered under your certificate are intended to qualify for favorable federal tax treatment. If the accelerated benefits qualify for favorable tax treatment, the benefits will be excludable from your income and not subject to federal taxation.

This information was written as a supplement to the marketing of life insurance products. Tax laws relating to accelerated benefits are complex and limitations may apply. You are advised to consult with and rely on an independent tax advisor about your own particular circumstances.

Receipt of accelerated benefits may affect your eligibility, or that of your spouse or your family, for public assistance programs such as medical assistance (Medicaid), Temporary Assistance to Needy Families (TANF), Supplementary Social Security Income (SSI) and drug assistance programs. You are advised to consult with social service agencies concerning the effect that receipt of accelerated benefits will have on public assistance eligibility for you, your spouse or your family.

This summary provides an overview of your plan’s benefits. These benefits are subject to the terms and conditions of the contract between MetLife and Belton Independent School District and are subject to each state’s laws and availability. Specific details regarding these provisions can be found in the booklet certificate.

Life coverage isprovided under a group insurance policy (Policy Form GPNP99) issued to your employer by MetLife. Life coverage under your employer’s plan terminates when your employment ceases when your Life contributions cease, or upon termination of the group contract. Dependent Life coverage will terminate when a dependent no longer qualifies as a dependent. Should your life insurance coverage terminate for reasons other than non-payment of premium, you may convertit to a MetLife individual permanent policy without providing medical evidence of insurability.

L0814388435[exp1218][All States][DC,GU,MP,PR,VI]

GroupNumber: 00575448

ACancerinsuranceplanthroughGuardianprovides:

•Lump-sumcashpaymentsforcertainprocedures,screeningsandtreatmentsrelatedtoacoveredcancerdiagnosis,inaddition towhateveryourmedicalplancovers

•Paymentsaremadedirectlytoyouandcanbeusedforanypurpose

•Abilitytotakethecoveragewithyouifyouchangejobsorretire

•Affordablegrouprates

AboutYourBenefits:

COVERAGE-DETAILSOption1:AdvantagePlanOption2:PremierPlan

INITIALDIAGNOSISBENEFIT- BenefitispaidwhenyouarediagnosedwithInternalcancerforthefirsttimewhileinsuredunderthisPlan.

BenefitWaitingPeriod- Aspecifiedperiodoftimeafteryour effectivedateduringwhichtheInitialDiagnosisbenefitswillnotbe payable.

BenefitAmount

RADIATIONTHERAPYORCHEMOTHERAPY

Benefit

Pre-ExistingConditionsLimitation: Apre-existingcondition includesanyconditionforwhichyou,inthespecifiedtimeperiodprior tocoverageinthisplan,consultedwithaphysician,received treatment,ortookprescribeddrugs.

Portability: AllowsyoutotakeyourCancercoveragewithyouif youterminateemployment.PortedCancerplanterminatesatage70.

Child(ren)AgeLimits

FEATURES

AirAmbulance

$75;$75forFollow-Upscreening$125;$125forFollow-Up screening

Scheduleamountsuptoa$10,000 benefityearmaximum.

3monthsprior/6months treatmentfree/12monthsafter.

Scheduleamountsuptoa$15,000 benefityearmaximum.

3monthsprior/6months treatmentfree/12monthsafter.

Childrenagebirthto26yearsChildrenagebirthto26years

AttendingPhysician

Benefit information illustrated within this material reflects the plan covered by Guardian as of 05/21/2020 ALL ELIGIBLE EMPLOYEES Benefit Summary

The Guardian Life Insurance Company of America, New York, NY

BoneMarrow/StemCell

ExperimentalTreatment

$100/dayupto$1,000/month$200/dayupto$2,400/month

ExtendedCareFacility/SkilledNursingcare $ 100/dayupto90daysperyear$150/dayupto90daysperyear

GovernmentorCharityHospital

HomeHealthCare

HormoneTherapy

$300perdayinlieuofallother benefits

$400perdayinlieuofallother benefits

$50/visitupto30visitsperyear$100/visitupto30visitsperyear

$25/treatmentupto12treatments peryear

$50/treatmentupto12treatments peryear

Hospice $50/dayupto100days/lifetime$100/dayupto100days/lifetime

HospitalConfinement $300/dayforfirst30days; $600/dayfor31stdaythereafter perconfinement

ICUConfinement

Immunotherapy

InpatientSpecialNursing

MedicalImaging

Outpatientandfamilymemberlodging-Lodgingmustbemorethan 50milesfromyourhome.

OutpatientorAmbulatorySurgicalCenter

PhysicalorSpeechTherapy

Prosthetic

ReconstructiveSurgery

ReproductiveBenefit

$400/dayforfirst30days; $600/dayfor31stdaythereafter perconfinement

$500permonth,$2,500lifetime max

$400/dayforfirst30days; $800/dayfor31stdaythereafter perconfinement

$600/dayforfirst30days; $800/dayfor31stdaythereafter perconfinement

$500permonth,$2500lifetime max

$100/dayupto30daysperyear$150/dayupto30daysperyear

$75/day,upto90daysperyear$100/day,upto90daysperyear

$25/visitupto4visitspermonth, $400lifetimemax

SurgicallyImplanted:$2,000/device, $4,000lifetimemax

Non-Surgically:$200/device,$400 lifetimemax

BreastTRAMFlap$2,000

Breastreconstruction$500

BreastSymmetry$250

Facialreconstruction$500

$50/visitupto4visitspermonth, $1,000lifetimemax

SurgicallyImplanted:$3,000/device, $6,000lifetimemax

Non-Surgically:$300/device,$600 lifetimemax

BreastTRAM$3,000

Breastreconstruction$700

BreastSymmetry$350

Facialreconstruction$700

NoBenefit$1,500eggharvesting,$500eggor spermstorage,$2,000lifetimemax

SecondSurgicalOpinion $200/surgeryprocedure $300/surgeryprocedure

BiopsyOnly:$100

ReconstructiveSurgery:$250

BiopsyOnly:$100

SkinCancer

Excisionofaskincancer:$375

Excisionofaskincancerwithflap orgraft:$600

ReconstructiveSurgery:$250 Excisionofaskincancer:$375

Excisionofaskincancerwithflap orgraft:$600

SurgicalBenefit

$0.50/mileupto$1,000perround trip/equalbenefitforcompanion

Scheduleamountupto$4,125Scheduleamountupto$5,500 Transportation/CompanionTransportation-Benefitispaidifyou havetotravelmorethan50milesonewaytoreceivetreatmentfor internalcancer.

$0.50/mileupto$1,500perround trip/equalbenefitforcompanion

WaiverofPremium-Ifyoubecomedisabledduetocancerthatis diagnosedaftertheemployee'seffectivedate,andyouremain disabledfor90days,wewillwaivethepremiumdueaftersuch90 daysforaslongasyouremaindisabled.

UNDERSTANDINGYOURBENEFITS:

• Alternative Care – Benefit is paid for palliative care (bio-feedback or hypnosis) or lifestyle benefits such as visits to an accredited practitioner for smoking cessation, yoga, meditation, relaxation techniques and nutritional counseling.

•

• Cancer –Cancermeansyouhavebeendiagnosedwithadisease manifestedbythepresenceofamalignanttumor characterizedbytheuncontrolledgrowthandspreadofmalignantcellsinanypartofthebody.Thisincludesleukemia, Hodgkin'sdisease,lymphoma,sarcoma,malignanttumorsandmelanoma.Cancerincludescarcinomasin-situ(inthenaturalor normalplace,confinedtothesiteoforigin,withouthavinginvadedneighboringtissue).Pre-malignantconditionsorconditions withmalignantpotential,suchasmyelodyplasticandmyeloproliferativedisorders,carcinoid,leukoplakia,hyperplasia,actinic keratosis,polycythemia,andnonmalignantmelanoma,molesorsimilardiseasesorlesionswillnotbeconsideredcancer. CancermustbediagnosedwhileinsuredundertheGuardiancancerplan.

• ExperimentalTreatment –Benefitswillbepaidforexperimentaltreatmentprescribedbyadoctorforthepurposeof destroyingorchangingabnormaltissue.AlltreatmentmustbeNCIlistedasviableexperimentaltreatmentforInternal Cancer.

ManageYourBenefits:

Gotowww.GuardianAnytime.comto accesssecureinformation aboutyourGuardianbenefits.Youron-lineaccountwillbeset upwithin30daysafteryourplaneffectivedate.

LIMITATIONSANDEXCLUSIONS:

ASUMMARYOFCANCERLIMITATIONSANDEXCLUSIONS:

ConditionalIssueunderwritingisrequiredonthoseenrollingoutsideofthe initialenrollmentperiodorannualopenenrollmentperiod.

Thisplanwillnotpaybenefitsfor:Servicesortreatmentnotincludedinthe Features.Servicesortreatmentprovidedbyafamilymember.Servicesor treatmentrenderedforhospitalconfinementoutsidetheUnitedStates.Any cancerdiagnosedsolelyoutsideoftheUnitedStates.Servicesortreatment providedprimarilyforcosmeticpurposes.Servicesortreatmentfor premalignantconditions.Servicesortreatmentforconditionswithmalignant potential.Servicesortreatmentfornon-cancersicknesses.

NeedAssistance?

CalltheGuardianHelpline(888)600-1600,weekdays,8:00AM to8:30PM,EST.RefertoyourmemberID(socialsecurity number)andyourplannumber:00575448

Cancercausedby,contributedtoby,orresultingfrom:participatinginafelony, riotorinsurrection;intentionallycausingaself-inflictedinjury;committingor attemptingtocommitsuicidewhilesaneorinsane;acoveredperson’smentalor emotionaldisorder,alcoholismordrugaddiction;engaginginanyillegalactivity; orservinginthearmedforcesoranyauxiliaryunitofthearmedforcesofany country.

IfCancerinsurancepremiumispaidforonapretaxbasis,thebenefitmaybetaxable. Pleasecontactyourtaxorlegaladvisorregardingthetaxtreatmentofyourpolicy benefits.

Thisdocumentisasummaryofthemajorfeaturesofthereferencedinsurancecoverage. Itisintendedforillustrativepurposesonlyanddoesnotconstitute acontract.Theinsuranceplandocuments,includingthepolicyandcertificate,comprisethecontractforcoverage.Thefullplandescription,incl udingthe benefitsandallterms,limitationsandexclusionsthatapplywillbecontainedinyourinsurancecertificate.Theplandocumentsarethefinalarbiterof coverage.Coveragetermsmayvarybystateandactualsoldplan.Thepremiumamountsreflectedinthissummaryareanapproximation;ifthereisa discrepancybetweenthisamountandthepremiumactuallybilled,thelatterprevails.

ALL ELIGIBLE EMPLOYEES Benefit Summary

The Guardian Life Insurance Company of America, New York, NY

Contract#GP-1-CAN-IC-12Protection for the treatment of cancer and 23 specified diseases

Receiving a cancer diagnosis can be one of life’s most frightening events. Unfortunately, statistics show you probably know someone who has been in this situation.

With Cancer insurance from Allstate Benefits, you can rest a little easier. Our coverage pays you a cash benefit to help with the costs associated with treatments, to pay for daily living expenses, and more importantly, to empower you to seek the care you need.

You choose the coverage that’s right for you and your family. Our Cancer insurance pays cash benefits for cancer and 23 specified diseases to help with the cost of treatments and expenses as they happen. Benefits are paid directly to you unless otherwise assigned. With the cash benefits you can receive from this coverage, you may not need to use the funds from your Health Savings Account (HSA) for cancer or specified disease treatments and expenses.

• Includes coverage for cancer and 23 specified diseases

• Benefits are paid directly to you unless otherwise assigned

• Coverage available for you or your entire family

• Waiver of premium after 90 days of disability due to cancer for as long as your disability lasts (primary insured only)

• Premiums do not increase due to age

• Additional rider benefits may be added to enhance your coverage, if your employer has chosen to make them available to you

With Allstate Benefits, you can protect your finances if faced with an unexpected cancer or specified disease diagnosis. Are you in Good Hands? You can be.

THIS IS NOT A POLICY OF WORKERS’ COMPENSATION INSURANCE. THE EMPLOYER DOES NOT BECOME A SUBSCRIBER TO THE WORKERS’ COMPENSATION SYSTEM BY PURCHASING THIS POLICY, AND IF THE EMPLOYER IS A NON-SUBSCRIBER, THE EMPLOYER LOSES THOSE BENEFITS WHICH WOULD OTHERWISE ACCRUE UNDER THE WORKERS’ COMPENSATION LAWS. THE EMPLOYER MUST COMPLY WITH THE WORKERS’ COMPENSATION LAW AS IT PERTAINS TO NON-SUBSCRIBERS AND THE REQUIRED NOTIFICATIONS THAT MUST BE FILED AND POSTED.

?

Early detection, improved treatments and access to care are factors that influence cancer survival1

19 million

The number of cancer survivors in the U.S. is increasing, and is expected to jump to nearly 19 million by 2024 2

1http://tinyurl.com/jp8tuaq

2Cancer Treatment & Survivorship Facts & Figures, 2014-2015

Jane is like anyone else who has been diagnosed with cancer. She is concerned about her family and how they will cope with her disease and its treatment. Most importantly, she worries about how she will pay for her treatment.

Here is what weighs heavily on her mind:

•Major medical only pays a portion of the expenses associated with my treatment

•I have copays I am responsible for until I meet my deductible

•If I am not working due to treatments, I must cover my bills, rent/mortgage, groceries and my child’s education

•If the right treatment is not available locally, I will have to travel to get the treatment I need

Jane chooses benefits to help protect herself and her family members if diagnosed with cancer or a specified disease

Jane undergoes her annual wellness test and is diagnosed for the first time with cancer.

Jane’s doctor reviews the results with her and recommends pre-op testing and surgery. He provides her with the location of a hospital that specializes in her cancer. However, Jane must travel 400 miles, where she undergoes pre-op testing (medical imaging) and is admitted to the hospital for surgery.

Jane undergoes surgery, anesthesia, radiation/ chemo, and is visited by a doctor during a 3-day hospital stay. And every 2 weeks she has radiation/ chemotherapy at a local facility, is given antinausea medication, and sees her doctor during her follow-up visits.

Following each visit, Jane goes online to file her claims, where she is able to track each and have the benefit payments direct deposited to her bank account.

Jane’s Cancer claim paid her cash benefits for the following:

Variable Wellness

Cancer Initial Diagnosis

Continuous Hospital Confinement

Non-Local Transportation

Surgery

Anesthesia

Radiation and Chemotherapy

Medical Imaging

Inpatient Drugs and Medicine

Physician Attendance

Anti-Nausea

For a listing of benefits and benefit amounts, see your company’s rate insert.

Here’s how Jane’s story of diagnosis and treatment turned into a happy ending, because she had supplemental Cancer Insurance to help with expenses.

Using your cash benefits

Cash benefits provide you with options, because you decide how to use them.

Finances

Can help protect HSAs, savings, retirement plans and 401(k)s from being depleted.

Travel

Can help pay for expenses while receiving treatment in another city.

Home

Can help pay the mortgage, continue rental payments, or perform needed home repairs for after care.

Expenses

Can help pay your family’s living expenses such as bills, electricity, and gas.

Benefits (subject to maximums as listed on the attached rate insert)

Continuous Hospital Confinement - inpatient confinement

Government or Charity Hospital - confinements in lieu of other benefits, except Waiver of Premium

Private Duty Nursing Services - nurse cannot be employed by confining hospital

Extended Care Facility - within 14 days of a hospital stay, up to the number of days of the hospital stay

At Home Nursing - private nursing care, up to the number of days of the previous hospital stay

Hospice Care Center or Team - terminal illness care in a facility or at home; one visit per day

RADIATION/CHEMOTHERAPY AND RELATED BENEFITS

Radiation/Chemotherapy for Cancer - covered treatments to destroy or modify cancerous tissue

Blood, Plasma and Platelets - transfusions, administration, processing, procurement, cross matching

Medical Imaging - initial diagnosis or follow-up evaluation based on covered imaging exam

Hematological Drugs - boosts cell lines for white/red cell counts and platelets; payable when Radiation/ Chemotherapy for Cancer benefit is paid

SURGERY AND RELATED BENEFITS

Surgery* - based on Schedule of Surgical Procedures; per operation on an inpatient/outpatient basis

Anesthesia - 25% of Surgery benefit for anesthesia received by an anesthetist

Ambulatory Surgical Center - payable only if Surgery benefit is paid

Second Opinion - second surgery or treatment opinion by a doctor not in practice with your doctor

Bone Marrow Transplant

Stem Cell Transplant

MISCELLANEOUS BENEFITS

Inpatient Drugs and Medicine - not including drugs/medicine covered under the Radiation/Chemotherapy for Cancer or Anti-Nausea benefits

Physician’s Attendance - one inpatient visit by one physician

Ambulance - transfer to or from hospital by licensed service or hospital-owned ambulance

MyBenefits: 24/7 Access allstatebenefits.com/mybenefits

An easy-to-use website that offers 24/7 access to important information about your benefits. Plus, you can submit and check your claims (including claim history), request your cash benefit to be direct deposited, make changes to personal information, and more.

Variable Wellness Benefit

Category 1: Blood tests for triglycerides, CA15-3 (breast cancer), CA125 (ovarian cancer), CEA (colon cancer) and PSA (prostate cancer); Hemoccult stool analysis; HPV (Human Papillomavirus) Vaccination; Lipid panel (total cholesterol count); Pap Smear, including ThinPrep Pap Test; Serum Protein Electrophoresis (test for myeloma).

Category 2: Biopsy for skin cancer; Mammography, including Breast Ultrasound; Thermography; Doppler screening for carotids or peripheral vascular disease; Echocardiogram; EKG; Chest X-ray; Stress test on bike or treadmill.

Category 3: Bone Marrow Testing; Colonoscopy; Flexible sigmoidoscopy; Ultrasound screening for abdominal aorticaneurysms.

Non-Local Transportation - obtaining treatment not available locally

Outpatient Lodging - payable only if Radiation/Chemotherapy for Cancer benefit is paid; more than 100 miles from home Family Member Lodging and Transportation - adult family member travels with you during non-local hospital stays for specialized treatment. Transportation not paid if Non-Local Transportation benefit paid

Physical or Speech Therapy - to restore normal body function

New or Experimental Treatment - payable if physician judges to be necessary, and only for treatment not covered under other policy benefits

Prosthesis - surgical implantation of prosthetic device for each amputation

Hair Prosthesis - wig or hairpiece every two years due to hair loss

Nonsurgical External Breast Prosthesis - initial prosthesis after a covered mastectomy

Anti-Nausea Drugs - prescribed anti-nausea medication administered on outpatient basis

National Cancer Institute Evaluation/Consultation - evaluation/consultation as a result of cancer

Egg Harvesting and Storage - harvesting of oocytes and storage of oocytes/sperm at licensed facility

Waiver of Premium** - must be disabled 90 days in a row due to cancer; pays as long as disability lasts, up to 5 years

ADDITIONAL RIDER BENEFITS

Cancer Initial Diagnosis Level Benefit - for first-time diagnosis of cancer other than skin cancer

Variable Wellness Benefit - per day, once per category per year; see left for list of wellness services and tests

OPTIONAL RIDER BENEFITS

Intensive Care (ICU)

a. ICU Confinement - Illness or accident confinements up to 45 days/stay

b. Step-Down ICU Confinement - Confinements up to 45 days/stay

c. Ground/Air Ambulance - Not paid if the policy’s Ambulance benefit is paid

Cancer and Specified Disease Additional Benefit - increases the benefit paid on the following base policy benefits: Continuous Hospital Confinement; Government or Charity Hospital; Private Duty Nursing Services; Extended Care Facility; At Home Nursing; Hospice Care; Radiation/Chemotherapy for Cancer; Blood, Plasma and Platelets; Hematological Drugs; Medical Imaging; Surgery; Anesthesia; Bone Marrow Transplant; Stem Cell Transplant; Ambulatory Surgical Center and Second Opinion

*Two or more surgeries done at the same time are considered one operation. The operation with the largest benefit will be paid. Outpatient is paid at 150% of the amount listed in the Schedule of Surgical Procedures. **Premiums waived for primary insured only.

Eligibility

Coverage may include you, your spouse or domestic partner and children under age 26.

Termination of Coverage

(a)Policy coverage terminates at the end of the grace period or your death (except that your covered spouse or domestic partner becomes the new insured; coverage will continue until their death). The riders terminate at the end of the grace period, if the policy terminates, or on the next renewal date after you request termination. Rider coverage under the Cancer Initial Diagnosis Rider also terminates when a benefit is paid on all covered persons.

(b)Spouse/domestic partner coverage ends upon divorce/ termination of partnership. (c) Coverage for children ends when the child reaches age 26, unless he or she continues to meet the requirements of an eligible dependent.

Renewability

The policy is guaranteed renewable for life, subject to change in premiums by class. All premiums may change on a class basis. A notice is mailed in advance of any change.

23 Specified Diseases Covered - Addison’s Disease; Amyotrophic Lateral Sclerosis (Lou Gehrig’s Disease); Brucellosis; Diphtheria; Encephalitis; Hansen’s Disease; Hepatitis (Chronic B or Chronic C with liver failure or hepatoma); Legionnaires’ Disease (confirmation by culture or sputum); Lyme Disease; Multiple Sclerosis; Muscular Dystrophy; Myasthenia Gravis; Primary Biliary Cirrhosis; Rabies; Reye’s Syndrome; Rocky Mountain Spotted Fever; Sickle Cell Anemia; Systemic Lupus Erythematosus; Tetanus; Thalassemia; Tuberculosis; Tularemia; Typhoid Fever.

Pre-Existing Condition Limitation

(a) We do not pay benefits for a pre-existing condition during the 12-month period (6 months for persons age 65 and over) beginning on the date that person’s coverage starts. (b) A pre-existing condition is a disease or condition for which: there existed symptoms which would cause a prudent person to seek diagnosis, care, or treatment within the 12-month period prior to the effective date; or medical advice or treatment was recommended or received from a medical professional within the 12-month period prior to the effective date. (c) A pre-existing condition can exist even though a diagnosis has not yet been made.

Policy Exclusions and Limitations

(a)Benefits are not paid for any loss, except for losses due to cancer or a specified disease. (b) Benefits are not paid for losses caused or aggravated by cancer or a specified disease or as a result of treatment.

(c)Treatment must be received in the United States or its territories.

Hospice Care Team Limitation: Services are not covered for food or meals, well-baby care, volunteers or support for the family after covered person’s death.

Blood, Plasma and Platelets Limitation: Does not include blood replaced by donors or for immunoglobulins.

For the Radiation/Chemotherapy for Cancer; Blood, Plasma and Platelets; and New or Experimental Treatment benefits, we pay 50% of the billed amount if the actual costs are not obtainable as proof of loss.

For the Radiation/Chemotherapy for Cancer benefit, we do not pay for treatment or emergency or room charges; treatment planning, management, devices, or supplies; medications or drugs covered elsewhere in the policy; X-rays, scans, and their interpretations; or any other drug, charge or expense that does not directly modify or destroy cancerous tissues.

Intensive Care Rider Exclusions and Limitations

(a) Benefits are not paid for: (1) attempted suicide or intentional self-inflicted injury; (2) intoxication or being under the influence of drugs not prescribed by a physician; or (3) alcoholism or drug addiction. (b) Benefits are not paid for confinements to a care unit that does not qualify as intensive care unit including progressive care, subacute intensive care, intermediate care, private rooms with monitoring, step-down and other lesser care units. (c) Benefits are not paid for step-down confinements in the following units: telemetry or surgical recovery rooms; post-anesthesia care; progressive care; intermediate care; private monitored rooms; observation units in emergency rooms or outpatient surgery units; beds, wards, or private or semi-private rooms; emergency, labor or delivery rooms; or other facilities that do not meet the standards for a step-down hospital intensive care unit. (d) Benefits are not paid for confinements occurring during a hospitalization prior to the effective date. (e) Children born within 10 months of the rider date are not covered for confinement occurring or beginning during the first 30 days of the child’s life.

This brochure is for use in TX and is incomplete without the accompanying rate insert. This material is valid as long as information remains current, but in no event later than March 1, 2021. Cancer and Specified Disease benefits are provided by policy form CP12, or state variations thereof. Cancer Rider benefits provided by the following rider forms, or state variations thereof: Variable Wellness Benefit Rider WBR7; Intensive Care Rider ICR5; Cancer Initial Diagnosis Level Benefit Rider CLR3; Cancer and Specified Disease Additional Benefit Rider CABR3.

The policy and riders provide Limited Benefit Supplemental Cancer and Specified Disease Insurance. The policy is not a Medicare Supplement Policy. If eligible for Medicare, review the Medicare Supplement Buyer’s Guide available from Allstate Benefits. This information highlights some features of the policy but is not the insurance contract. Only the actual policy provisions control. For complete details, contact your Allstate Benefits Agent. Underwritten by American Heritage Life Insurance Company (Home Office, Jacksonville, FL).

The coverage does not constitute comprehensive health insurance coverage (often referred to as “major medical coverage”) and does not satisfy the requirement of minimum essential coverage under the Affordable Care Act.

Includes coverage for 23 Specified Diseases from Allstate Benefits

BENEFIT AMOUNTS

PLAN 1 MONTHLY PREMIUMS

PLAN 2 MONTHLY

† Up to number of days of previous hospital confinement.

1 Pays actual cost up to amount listed.

2 Pays up to amount listed in policy Schedule of Surgical Procedures. Amount paid depends on surgery.

3 Benefit amount includes the Cancer and Specified Disease Additional Benefit Rider (CABR) which increases the base policy benefit.

Maximum of 700 miles.

For use in: TX

This rate insert is part of form ABJ34538X and is not to be used on its own.

This material is valid as long as information remains current, but in no event later than March 1, 2021. Allstate Benefits is the marketing name used by American Heritage Life Insurance Company (Home Office, Jacksonville, FL), a subsidiary of The Allstate Corporation. ©2018 Allstate Insurance Company. www.allstate.com or allstatebenefits.com

Conditions and Limits – When an injury results in a covered loss within 90 days (180 days for dismemberment or accidental death), unless otherwise stated, from the date of an accident, and is diagnosed by a physician, Allstate Benefits will pay benefits as stated. Treatment must be received in the United States or its territories.

Your Eligibility – Your employer decides who is eligible for your group (such as length of service and hours worked each week). Issue ages are 18 and over.

Dependent Eligibility/Termination – (a) Coverage may include you, your spouse or domestic partner, and your children. (b) Coverage for children ends when the child reaches age 26, unless he or she continues to meet the requirements of an eligible dependent. (c) Spouse coverage ends upon valid decree of divorce or your death. (d)Domestic partner coverage ends upon termination of domestic partnership or your death.

When Coverage Ends – Coverage under the policy ends on the earliest of: (a) the date the policy is canceled; (b) the last day of the period for which you made any required contributions; (c) the last day you are in active employment, except as provided under the Temporary Layoff, Leave of Absence, or Family and Medical Leave of Absence provision; (d)the date you are no longer in an eligible class; (e) the date your class is no longer eligible; or (f) upon discovery of fraud or material misrepresentation when filing a claim.

Continuation of Coverage – You may be eligible to continue coverage when coverage under the policy ends. You have 60 days after coverage under the policy ends to let us know if you wish to continue coverage.

Accident and Benefit Enhancement Exclusions and Limitations – Benefits are not paid for: (a) injury incurred before the effectiv e date; (b) injury as a result of an on-the-job accident; (c) any act of war or participation in a riot, insurrection or rebellion; (d) self-inflicted injury; (e) suicide or attempted suicide; (f) being under the influence of alcohol or narcotics unless taken on the advice of a physician; (g) bacterial infection (except pyogenic infections from an accidental cut or wound); (h) participation in aeronautics unless a fare-paying passenger on a licensed common-carrier aircraft; (i) engaging in an illegal occupation, assault or felony; (j) driving in any race or speed test or testing any vehicle on any racetrack or speedway; (k) serving as an active member of the Military, Naval, or Air Forces of any country; and (l) hernia, including complications.

Outpatient Physician’s Benefit Rider Exclusions and Limitations – Benefits are not paid for: (a) losses incurred before the effective date; (b) a loss as a result of an onthe-job accident; (c) any act of war or part icipation in a riot, insurrection or rebellion; (d) suicide or attempted suicide; (e) self-inflicted action; (f) being under the influence of alcohol or narcotics unless taken on the advice of a physician; (g) participation in aeronautics unless a farepaying passenger on a licensed common-carrier aircraft; (h)engaging in an illegal occupation, assault or felony; (i)driving in any race or speed test or testing any vehicle on any racetrack or speedway; (j) serving as an active member of the Military, Naval, or Air Forces of any country.

Arkansas (changes affect page 4) – In the Accident and Benefit Enhancement Exclusions and Limitations paragraph, item (f) is replaced with: injury resulting from being intoxicated or under the influence of any controlled substance unless taken on the advice of a physician; items (g) and (l) are deleted. In the Outpatient Physician’s Benefit Rider Exclusions and Limitations paragraph, item (f) is replaced with: loss resulting from being intoxicated or under the influence of any controlled substance, unless taken on the advice of a physician.

Georgia (changes affect pages 3 and 4) – In the Benefit Enhancements, the Coma with Respiratory Assistance benefit is deleted. The When Coverage Ends paragraph, specification includes: (g) the date you request to discontinue coverage in writing

Louisiana (changes affect pages 3 and 4) – In the Physical Therapy benefit, chiropractic services are payable. In the Accident and Benefit Enhancement Exclusions and Limitations paragraph, item (f) is replaced with: injury resulting from being intoxicated or under the influence of any narcotic not prescribed or recommended by a physician. In the Outpatient Physician’s Benefit Rider Exclusions and Limitations paragraph, item (f) is replaced with: loss resulting from being intoxicated or under the influence of any narcotic not prescribed or recommended by a physician.

New Mexico (change affects page 2) – The Accident Physician Treatment benefit includes coverage for Temporomandibular joint disorders and Craniomandibular joint disorders if a result of injury. We will not pay for orthodontic appliances and treatment, crowns, bridges and dentures, unless the disorder results from an injury.

Texas (changes affect page 4) – In the Conditions and Limits paragraph, the last sentence is replaced with the following: For the Hospital Confinement, Accident Physician Treatment, X-Ray, and Emergency Room Services benefits, treatment must be received in the United States or its territories, unless the treatment is the result of an emergency. Treatments included in all other benefits must be received in the U.S. or its territories. In the Accident and Benefit Enhancement Exclusions and Limitations paragraph, item (f)is replaced with: injury resulting from being intoxicated or under the influence of any narcotic unless taken on the advice of a physician; item (g) is replaced with: any bacterial infection (except food poisoning and pyogenic infections from an accidental cut or wound); item (i) is replaced with: engaging in an illegal occupation or felony. In the Outpatient Physician’s Benefit Rider Exclusions and Limitations paragraph, item (f) is replaced with: injury resulting from being intoxicated or under the influence of any narcotic unless taken on the advice of a physician; item (h) is replaced with: engaging in an illegal occupation or felony.

⚫

⚫

⚫

⚫ Endodontics (nonsurgical)

⚫ Endodontics (surgical)

⚫ Periodontics (nonsurgical)

⚫ Periodontics (surgical)

⚫ Prosthodontics (fixed bridge; removable complete/partial dentures) (1 in 10 years)

Ameritas Information

We're Here to Help: This plan was designed specifically for the associates of BELTON I.S.D. At Ameritas Group, we do more than provide coveragewe make sure there's always a friendly voice to explain your benefits, listen to your concerns, and answer your questions. Our customer relations associates will be pleased to assist you 7 a.m. to midnight (Central Time) Monday through Thursday, and 7 a.m. to 6:30 p.m. on Friday. You can speak to them by calling toll-free: 800-487-5553. For plan information any time go online to ameritas.com.

How would you rate your dental health? In 2016, you can receive your Dental Health Report Card by signing into your secure member account online. Your assessment is based on claims submitted. The report card also offers suggestions if you strive to improve your dental health. Ameritas members can access the personalized report card by going to ameritas.com, click Account Access in the top right corner and choose the Dental/Vision/Hearing drop down. Select the Secure Member Account link and sign in to see your report.

Our valued plan members and their covered dependents can save on prescription medications at over 60,000 pharmacies across the nation including CVS, Walgreens, Rite Aid and Walmart. This Rx discount is offered at no additional cost, and it is not insurance. To receive this Rx discount, Ameritas plan members just need to visit us at ameritas.com and sign into (or create) a secure member account where they can access and print an onlineonly Rx discount savings ID card. 53

Eyewear Savings

Ameritas plan members may receive up to 10% off eyewear frames and lenses purchased at any Walmart Vision Center nationwide. Members may also bring in their current vision prescription from any vision care provider and purchase eyewear at Walmart. This savings arrangement is not insurance: it is available to members at no additional cost to their plan premium. To receive the eyewear savings identification card, Ameritas plan members can visit ameritas.com and sign-in (or create) a secure member account. Members must present the Ameritas Eyewear Savings Card at time of purchase to receive the discount.

Dental Rewards®

Employees and their covered dependents may accumulate rewards up to the stated maximum carryover amount, and then use those rewards for any covered dental procedures subject to applicable coinsurance and plan provisions. If a plan member doesn't submit a dental claim during a benefit year, all accumulated rewards are lost. But he or she can begin earning rewards again the very next year.

benefits received for the year cannot exceed this amount

Type 3 Waiting Period - new enrollees only

The group of initial employees who enroll in this plan have no waiting period for Type 3 benefits. Anyone hired after the initial plan enrollment will have a 12-month waiting period, after they enroll in this dental plan, before they are eligible to receive Type 3 benefits.

Orthodontia Waiting Period - new enrollees only

The group of initial employees who enroll in this plan have no waiting period for orthodontia benefits. Anyone hired after the initial plan enrollment will have a 12-month waiting period, after they enroll in this dental plan, before they are eligible to receive orthodontia benefits.

Dental Network Information

To find a provider, visit ameritas.com and select FIND A PROVIDER, then DENTAL. Enter your criteria to search by location or for a specific dentist or practice. California Residents: When prompted to select your network found on your ID Card or contact Customer Connections at 800-487-5553.

Pretreatment

While we don't require a pretreatment authorization form for any procedure, we recommend them for any dental work you consider expensive. As a smart consumer, it's best for you to know your share of the cost up front. Simply ask your dentist to submit the information for a pretreatment estimate to our customer relations department. We'll inform both you and your dentist of the exact amount your insurance will cover and the amount that you will be responsible for. That way, there won't be any surprises once the work has been completed.

If a member does not elect to participate when initially eligible, the member may elect to participate at the policyholder's next enrollment period. This enrollment period will be held each year and those who elect to participate in this policy at that time will have their insurance become effective on September 1. If you do not enroll during your company's open enrollment period, you will be subject to the Late Entrant Provision.

We strongly encourage you to sign up for coverage when you are initially eligible. If you choose not to sign up during this initial enrollment period, you will become a late entrant. Late entrants will be eligible for only exams, cleanings, and fluoride applications for the first 12 months they are covered.

Section 125

This plan is provided as part of the Policyholder's Section 125 Plan. Each employee has the option under the Section 125 Plan of participating or not participating in this plan. If an employee does not elect to participate when initially eligible, he/she may elect to participate at the Policyholder's next Annual Election Period.

Members can search by ZIP Code for a specific dental procedure and see fee range estimates for out-of-network general dentists in that area. Of course, we always suggest that members partner with their dentists, so they know what’s involved in any recommended treatment plan. The estimator tool is powered by Go2Dental and uses FAIR Health data that is updated annually. Please note, cost estimates do not reflect discounted rates available through provider networks, and the estimator does not include orthodontic estimates at this time.

We recognize the importance of communicating with our growing number of multilingual customers. That is why we offer a language assistance program that gives you access to: Spanish-speaking claims contact center representatives, telephone interpretation services in a wide range of languages, online dental network provider search in Spanish and a variety of Spanish documents such as enrollment forms, claim forms and certificates of insurance. This document is

Why enroll in VSP? We invest in the things you value most— the best care at the lowest out-of-pocket costs. Because we’re the only national not-for-profit vision care company, you can trust that we’ll always put your wellness first.

You’ll like what you see with VSP.

Value and Savings. You’ll enjoy more value and the lowest out-of-pocket costs.

High Quality Vision Care. You’ll get the best care from a VSP provider, including a WellVision Exam®—the most comprehensive exam designed to detect eye and health conditions.

Choice of Providers. The decision is yours to make—choose a VSP doctor, a participating retail chain, or any out-of-network provider.

Great Eyewear. It’s easy to find the perfect frame at a price that fits your budget.

Create an account at vsp.com. Once your plan is effective, review your benefit information.

Find an eye care provider who’s right for you. To find a VSP provider, visit vsp.com or call 800.877.7195 .

At your appointment, tell them you have VSP. There’s no ID card necessary. If you’d like a card as a reference, you can print one on vsp.com

That’s it! We’ll handle the rest—there are no claim forms to complete when you see a VSP provider.

From classic styles to the latest designer frames, you’ll find hundreds of options. Choose from featured frame brands like bebe®, Calvin Klein, Cole Haan, Flexon®, Lacoste, Nike, Nine West, and more1. Visit vsp.com to find a Premier Program location that carries these brands. Prefer to shop online? Check out all of the brands at Eyeconic.com, VSP's online eyewear store.

BELTON INDEPENDENT SCHOOL DISTRICT and VSP provide you with an affordable eye care plan.

Lenses

Lens Enhancements

Contacts (instead of glasses)

Diabetic Eyecare Plus Program

$150 allowance for a wide selection of frames

$170 allowance for featured frame brands

20% savings on the amount over your allowance

$85 Costco® frame allowance

Single vision, lined bifocal, and lined trifocal lenses Polycarbonate lenses for dependent children

Standard progressive lenses

Premium progressive lenses

Custom progressive lenses

Average savings of 20-25% on other lens enhancements

$150 allowance for contacts; copay does not apply Contact lens exam (fitting and evaluation)

Services related to diabetic eye disease, glaucoma and age-related macular degeneration (AMD). Retinal screening for eligible members with diabetes. Limitations and coordination with medical coverage may apply. Ask your VSP doctor for details.

Glasses and Sunglasses

$95 - $105

$150 - $175

Every

Extra Savings

Extra $20 to spend on featured frame brands. Go to vsp.com/specialoffers for details.

20% savings on additional glasses and sunglasses, including lens enhancements, from any VSP provider within 12 months of your last WellVision Exam.

Retinal Screening

No more than a $39 copay on routine retinal screening as an enhancement to a WellVision Exam

Laser Vision Correction

Average 15% off the regular price or 5% off the promotional price; discounts only available from contracted facilities