As the spring selling season progresses, the property market is showing signs of moderation despite increased sales volume. While national property values remain in growth territory, the pace has notably softened, with houses recording a modest 0.2 per cent monthly gain and units edging up by just 0.1 per cent.

Market conditions are increasingly favourable for prospective buyers. An expansion in available listings has broadened choice, while the decelerating price growth has created opportunities, particularly for first-time homebuyers. Adding to the positive outlook, the September quarter inflation figure has dropped to 2.8 per cent, strengthening expectations of an interest rate cut in early 2025.

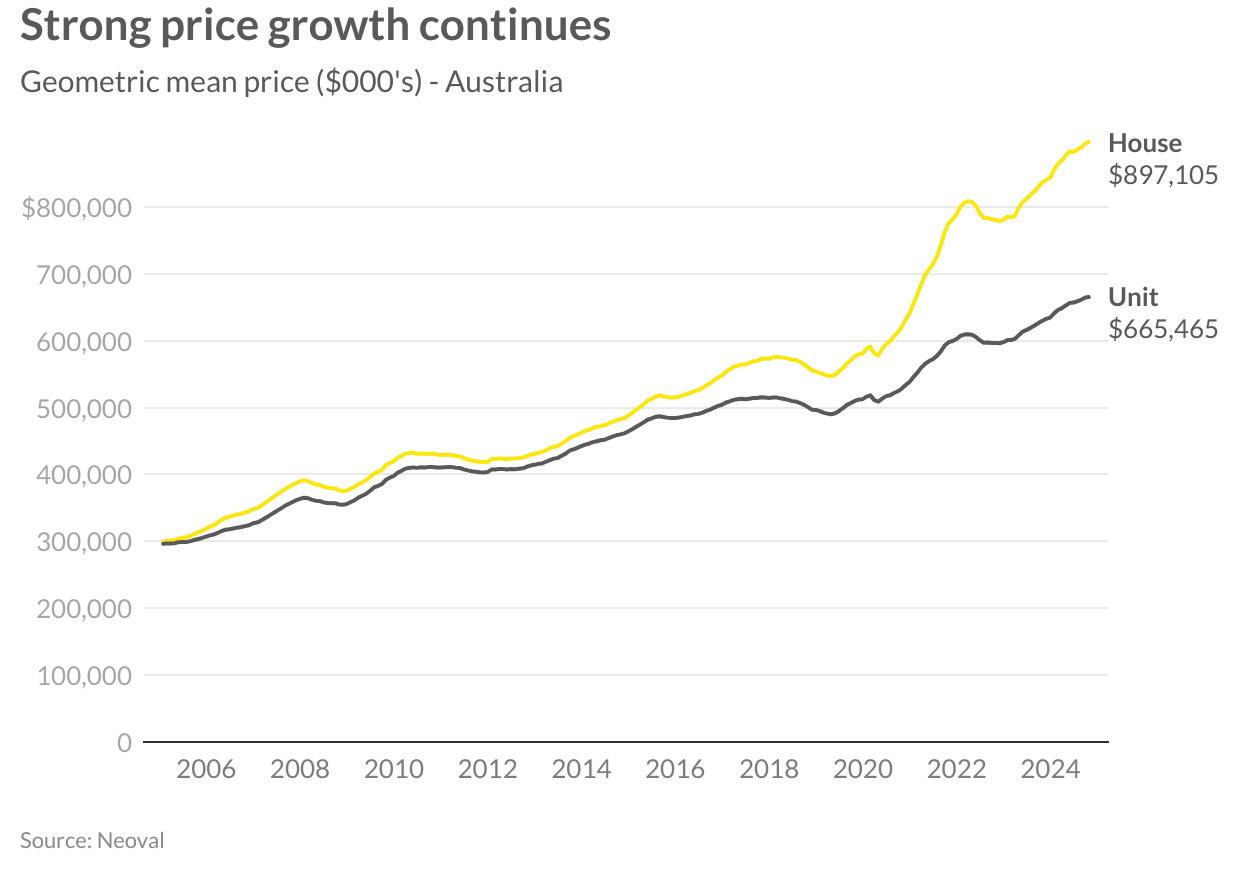

Despite this recent moderation, the property market’s annual performance remains robust. Over the past 12 months, house prices have recorded a significant 7.3 per cent increase, bringing the national average to $897,105. The unit sector, though growing more moderately, has achieved a solid 5.6 per cent annual gain, with the national mean price now reaching $665,465.

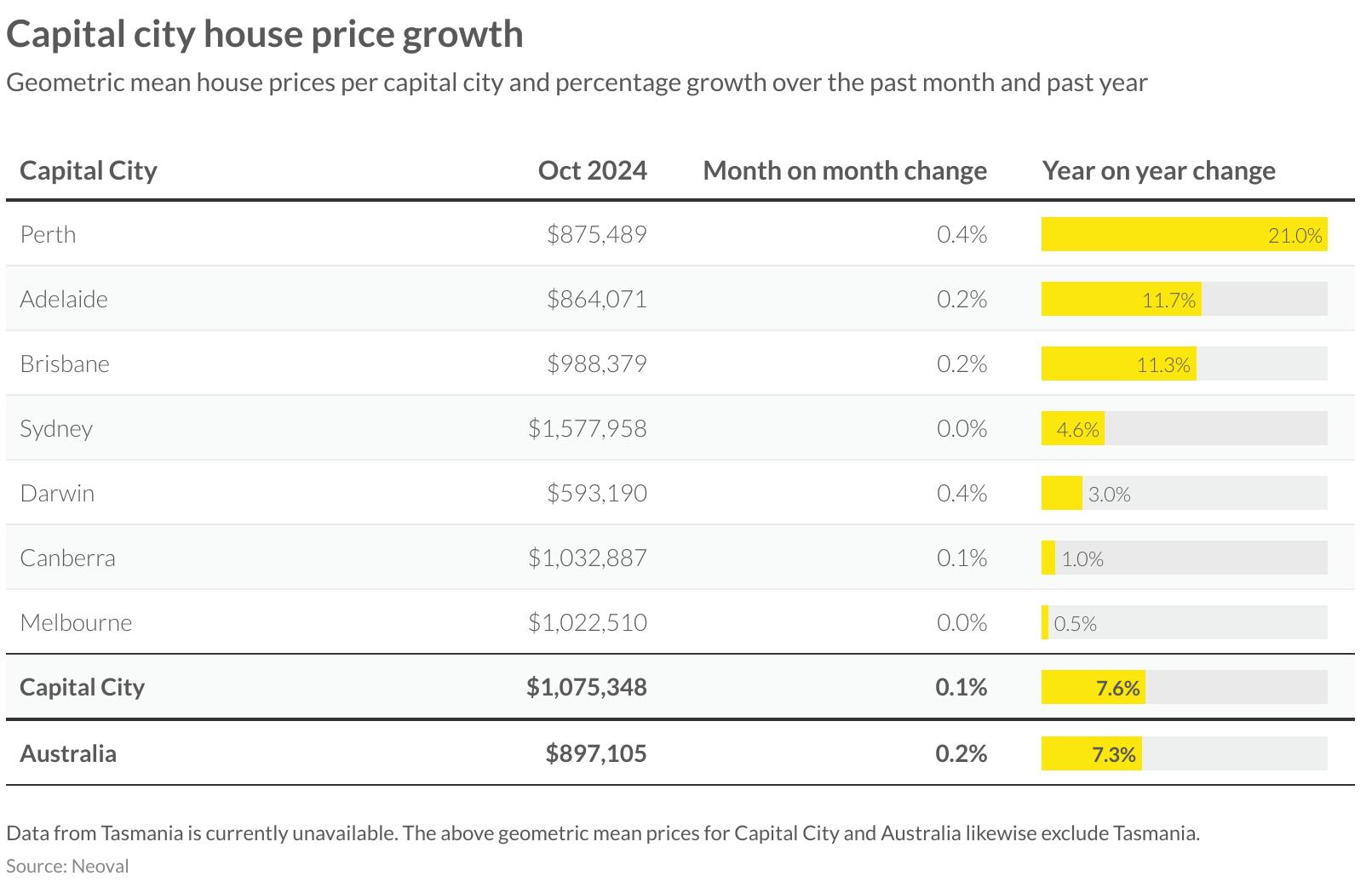

The pace of house price appreciation across Australian regions has begun to moderate this month. The nation’s largest property markets, Sydney and Melbourne, have plateaued, recording no movement in their respective mean prices of $1,577,958 and $1,022,510. Both cities’ annual growth trajectories now sit below the national capital city average of 7.6 per cent.

In a notable market shift, Adelaide has emerged as a standout performer, overtaking Brisbane in terms of yearly growth. While both cities posted modest 0.2 per cent gains this month, Adelaide’s annual increase of 11.7 per cent has edged ahead of Brisbane’s 11.3 per cent. This sustained growth has pushed Adelaide’s mean house price to $864,071, approaching Perth’s market levels.

Brisbane’s continued appreciation has brought its mean price to $988,379, positioning it on the cusp of the milliondollar threshold currently occupied by Melbourne and Canberra. This trajectory raises growing affordability concerns, particularly given these latter markets have experienced more subdued growth over the past year.

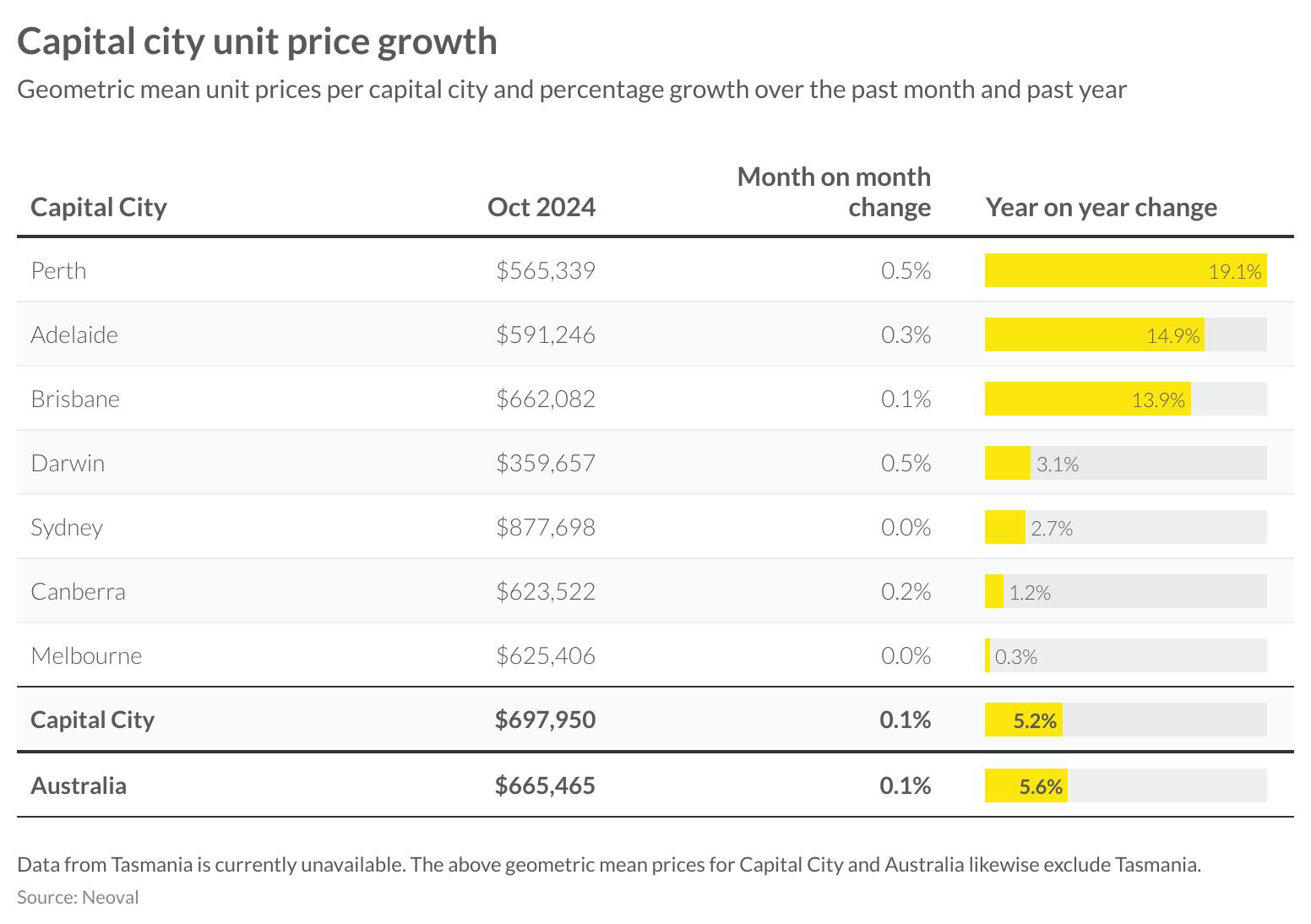

The unit market across Australia’s capital cities mirrors the broader housing sector’s performance, with varying dynamics across regions. The country’s largest markets, Sydney and Melbourne, have remained static this month, with prices holding steady at $877,698 and $625,406 respectively.

Perth and Darwin have emerged as the month’s strongest performers, each posting a 0.5 per cent increase. Perth continues to dominate the market in terms of annual growth, achieving an impressive 19.1 per cent increase to reach $565,339. In contrast, Darwin’s annual growth of 3.1 per cent falls short of the capital city average of 5.2 per cent.

Adelaide has demonstrated robust performance with a 0.3 per cent monthly increase, translating to a substantial 14.9 per cent annual growth, bringing its mean price to $591,246. Brisbane, despite a modest 0.1 per cent monthly gain to $662,082, maintains strong annual growth of 13.9 per cent. Canberra’s unit market presents a mixed picture, recording a 0.2 per cent monthly increase with mean prices at $623,522, though its annual growth remains modest at 1.2 per cent.

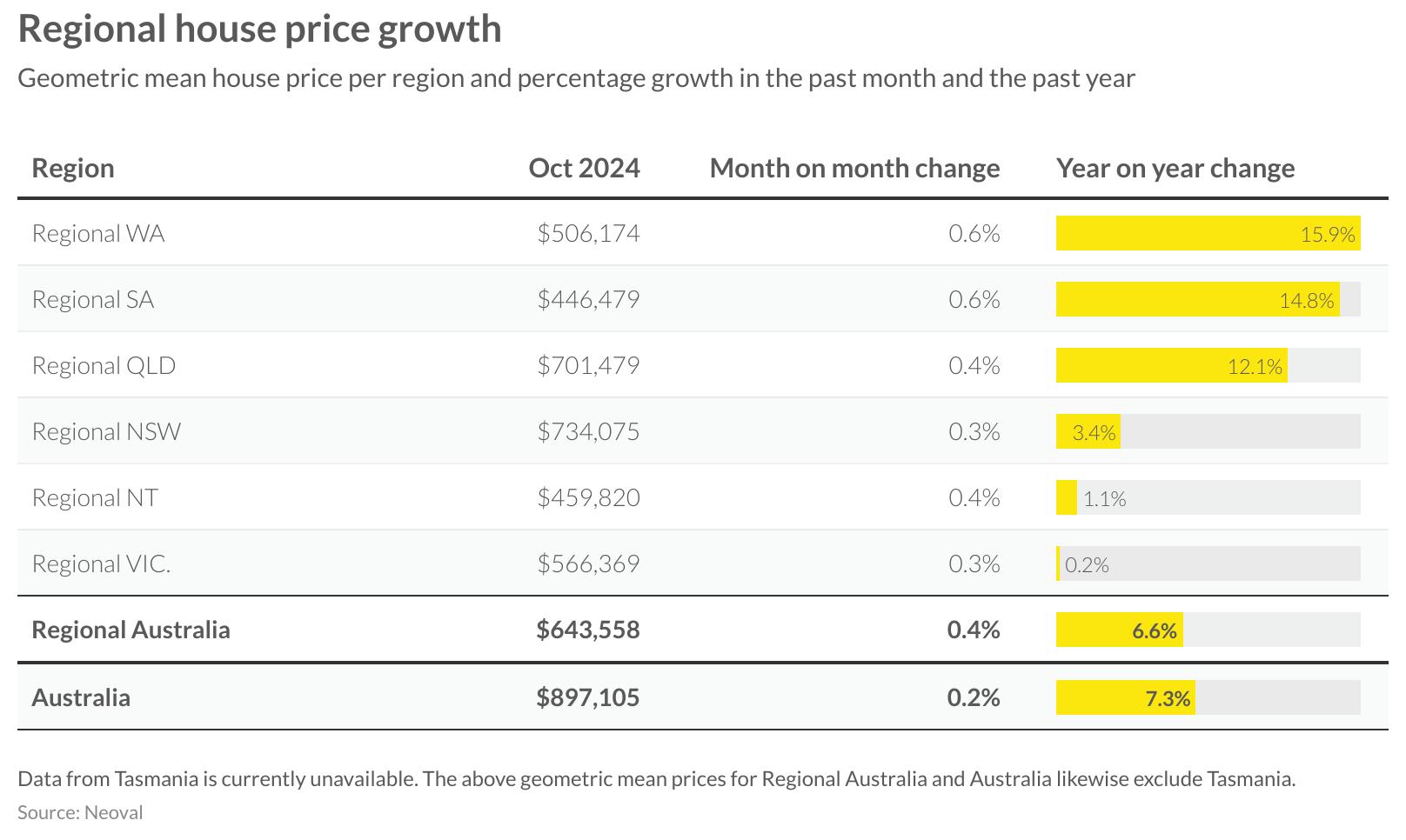

Regional property house markets have surpassed their capital city counterparts this month, achieving an average increase of 0.4 per cent. Leading this growth are Regional Western Australia and South Australia, both recording 0.6 per cent monthly gains. Western Australia’s regional market has reached an average price of $506,174, representing a substantial 15.9 per cent annual increase, while South Australia maintains its position as the most affordable regional market at $446,479, despite having achieved an impressive 14.8 per cent yearly growth.

Queensland’s regional market continues its strong trajectory, with property values now exceeding $700,000. The region posted a 0.4 per cent monthly improvement, contributing to a robust 12.1 per cent annual appreciation. The Northern Territory’s regional market matched Queensland’s monthly gain of 0.4 per cent, though its yearly growth remains modest at 1.1 per cent.

Regional markets in New South Wales and Victoria have shown signs of revival, each recording a 0.3 per cent monthly increase. New South Wales demonstrates stronger long-term performance with a 3.4 per cent annual growth and an average price of $734,075. Victoria’s more subdued annual growth of 0.2 per cent and mean price of $566,369 potentially presents opportunities for prospective buyers in this market.

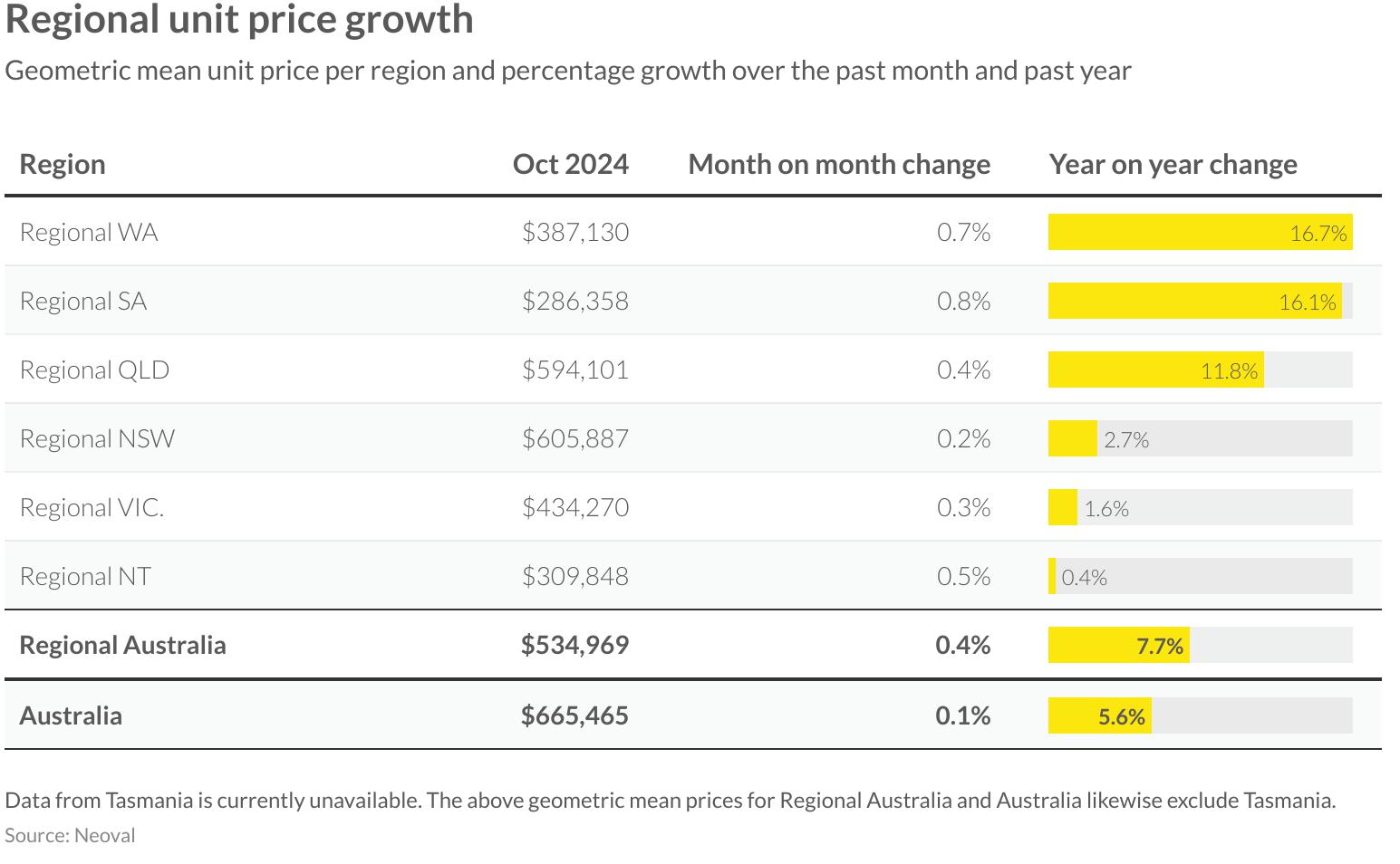

The regional unit sector continues to demonstrate strong performance, posting an average monthly gain of 0.4 per cent across the country. With an annual appreciation of 7.7 per cent, these markets are outperforming their regional housing counterparts.

South Australia’s regional unit market leads the monthly gains with a 0.8 per cent increase, bringing the mean price to $286,358. This represents a substantial annual growth of 16.1 per cent. Regional Western Australia follows closely with a 0.7 per cent monthly rise and maintains the strongest yearly growth at 16.7 per cent.

Queensland’s regional unit market has shown positive momentum with a 0.4 per cent monthly increase and an 11.8 per cent annual growth rate. The average price of $594,101 positions it just below regional New South Wales, where units average $605,887 despite a more modest annual growth of 2.7 per cent.

Regional Victoria and the Northern Territory have recorded monthly improvements of 0.3 per cent and 0.5 per cent respectively. However, both regions show more conservative annual growth, with Victoria up 1.6 per cent and the Northern Territory registering just 0.4 per cent over the year.

CAPITAL

SINCE

LISTINGS ACTIVITY

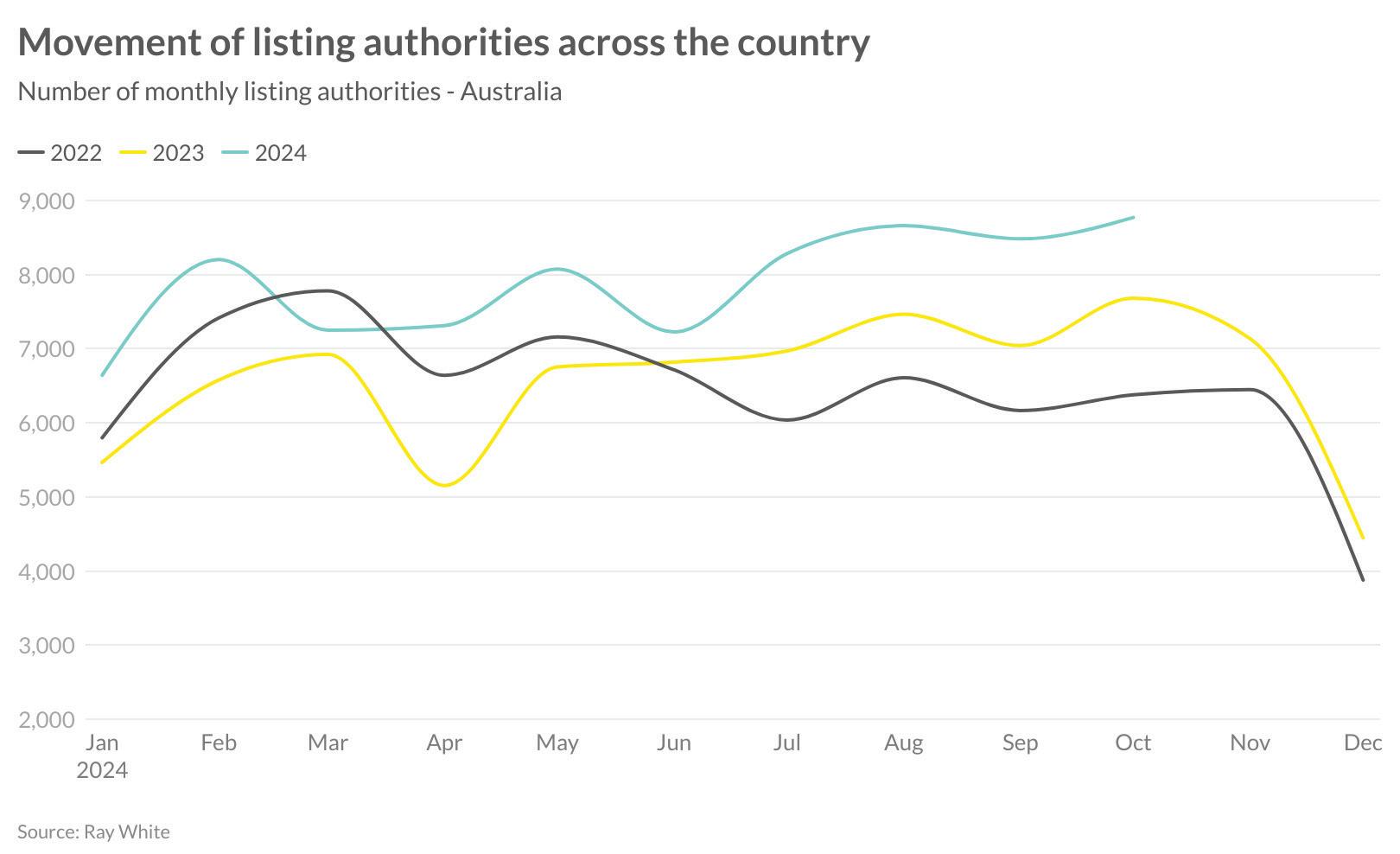

Analysis of Ray White’s listing authorities - the formal agreements between vendors and agents - provides valuable insight into future market supply. Particularly as we command over 15 per cent market share, these metrics offer a meaningful snapshot of broader market trends. Current data shows the national 28-day rolling sum of listing authorities has reached unprecedented levels, continuing its upward trajectory through the year.

The strength in listing volumes varies by region, with Victoria and Tasmania showing the strongest momentum, closely followed by South Australia and Northern Territory. The New South Wales and ACT region, while still positive, demonstrates more modest growth compared to the previous year. Several market dynamics are driving this surge in listing authorities, including change in price growth, affordability, taxation and population movements.

This unprecedented level of listing authorities suggests the spring selling season could extend beyond its traditional timeline. For buyers, this signals an expanding range of options and potentially reduced competition for individual properties. However, the ultimate impact on prices remains uncertain, as many markets still demonstrate substantial underlying demand despite the increasing supply.

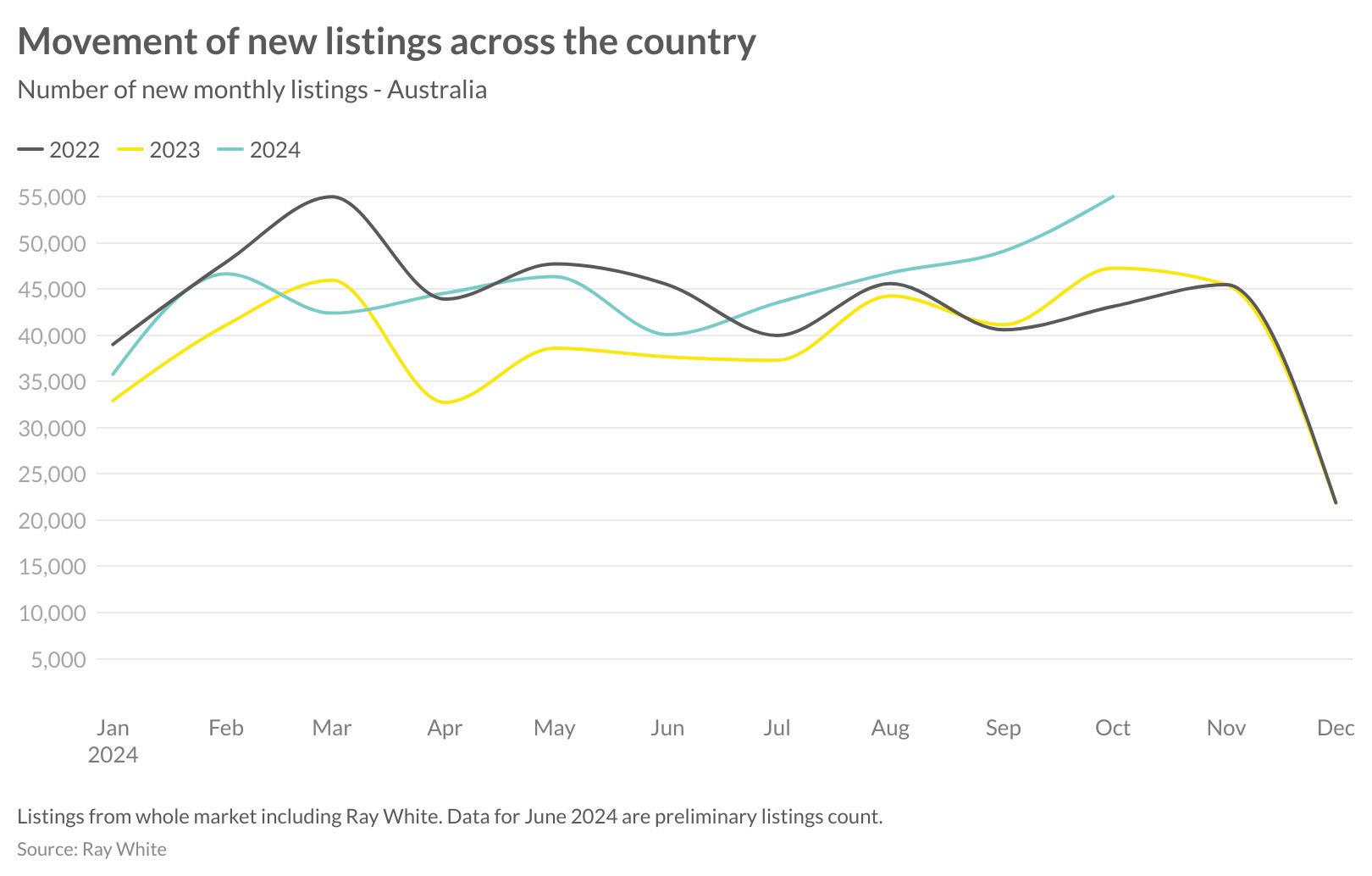

The property market has experienced a notable revival in listing activity during the recent quarter, with October’s preliminary figures revealing a substantial increase to nearly 55,000 listings. This marks a significant shift from the cautious winter period, when inflationary concerns had prompted both buyers and sellers to adopt a more conservative stance toward property decisions.

Recent momentum has surpassed previous years’ levels, buoyed by encouraging economic indicators that point to potential interest rate adjustments in the new year. This improved outlook has helped reinvigorate market participation from both buyers and sellers who had previously remained on the sidelines.

Property owners who had been hesitant to list their homes are now showing increased readiness to enter the market. This anticipated expansion in available properties could fundamentally alter market dynamics, presenting enhanced opportunities for prospective buyers who have been awaiting more favourable conditions.

As we look toward 2025, the market appears poised for increased activity. The combination of improving economic conditions, potential interest rate relief, and growing seller confidence suggests a more vibrant and dynamic property landscape in the months ahead.

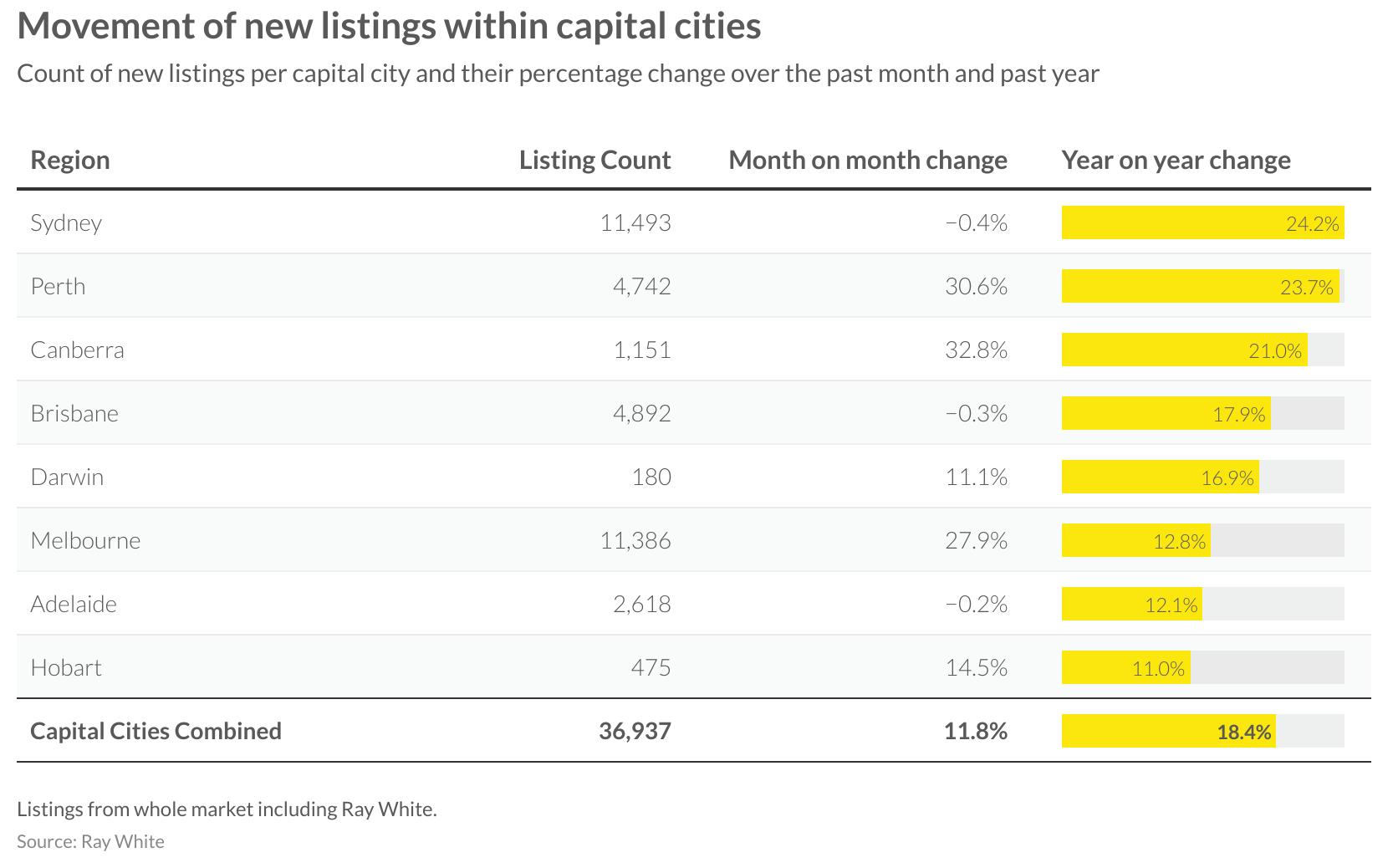

This month’s listing data reveals contrasting patterns across Australia’s capital cities, reflecting diverse market conditions nationwide. The aggregated capital city listing volumes show robust growth, up 11.8 per cent for the month and 18.4 per cent annually.

Sydney, while maintaining its position as the market with the highest listing volume, has experienced a deceleration this month, though still recording the strongest annual percentage change. Melbourne presents an intriguing counterpoint, matching Sydney’s volume but demonstrating more dramatic growth with a 27.9 per cent monthly increase and a 12.8 per cent annual rise, as property owners increasingly move to market their assets.

Perth’s listing numbers have surged by over 30 per cent this month, driven by owners seeking to capitalise on substantial price appreciation. In contrast, Adelaide’s competitive buying environment has led to a reduction in available listings. Brisbane’s market shows increasing owner caution, with listings declining 0.3 per cent this month, despite maintaining a strong 17.9 per cent annual increase.

These varying trends across capital cities highlight the localised nature of property market conditions, with each region responding differently to price movements, buyer demand, and broader economic factors.

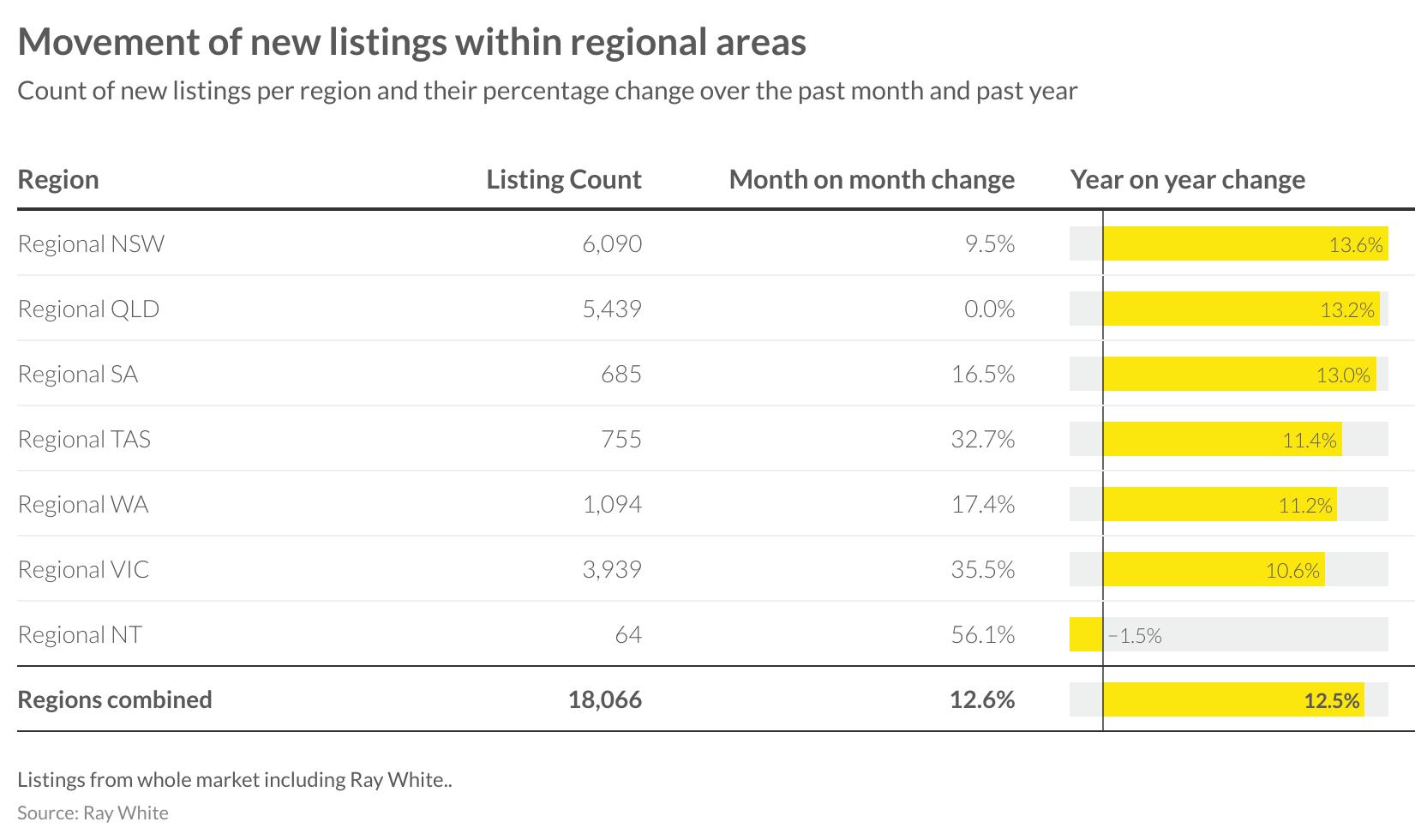

Regional property markets have demonstrated a different listing trajectory compared to their metropolitan counterparts, with annual growth reaching 12.5 per cent. However, the monthly data shows more vigorous activity with a 12.6 per cent increase, suggesting a recent acceleration in market activity.

The NT regional market recorded the most substantial monthly increase in listings, though this growth stems from a relatively small base. Regional Victoria emerged as a particularly active market, with an impressive 35.5 per cent monthly surge bringing total listings to 3,939 properties.

Regional New South Wales continues to dominate in terms of absolute listing volumes, posting a 13.6 per cent annual increase. This is closely followed by regional Queensland, which, despite showing no monthly change, has achieved a 13.2 per cent year-on-year growth. Regional SA shows similar momentum with a 13 per cent annual increase.

This pattern of growth across regional markets suggests a more measured pace of expansion compared to capital cities, while still maintaining steady upward momentum in most areas.

AUCTION INSIGHTS

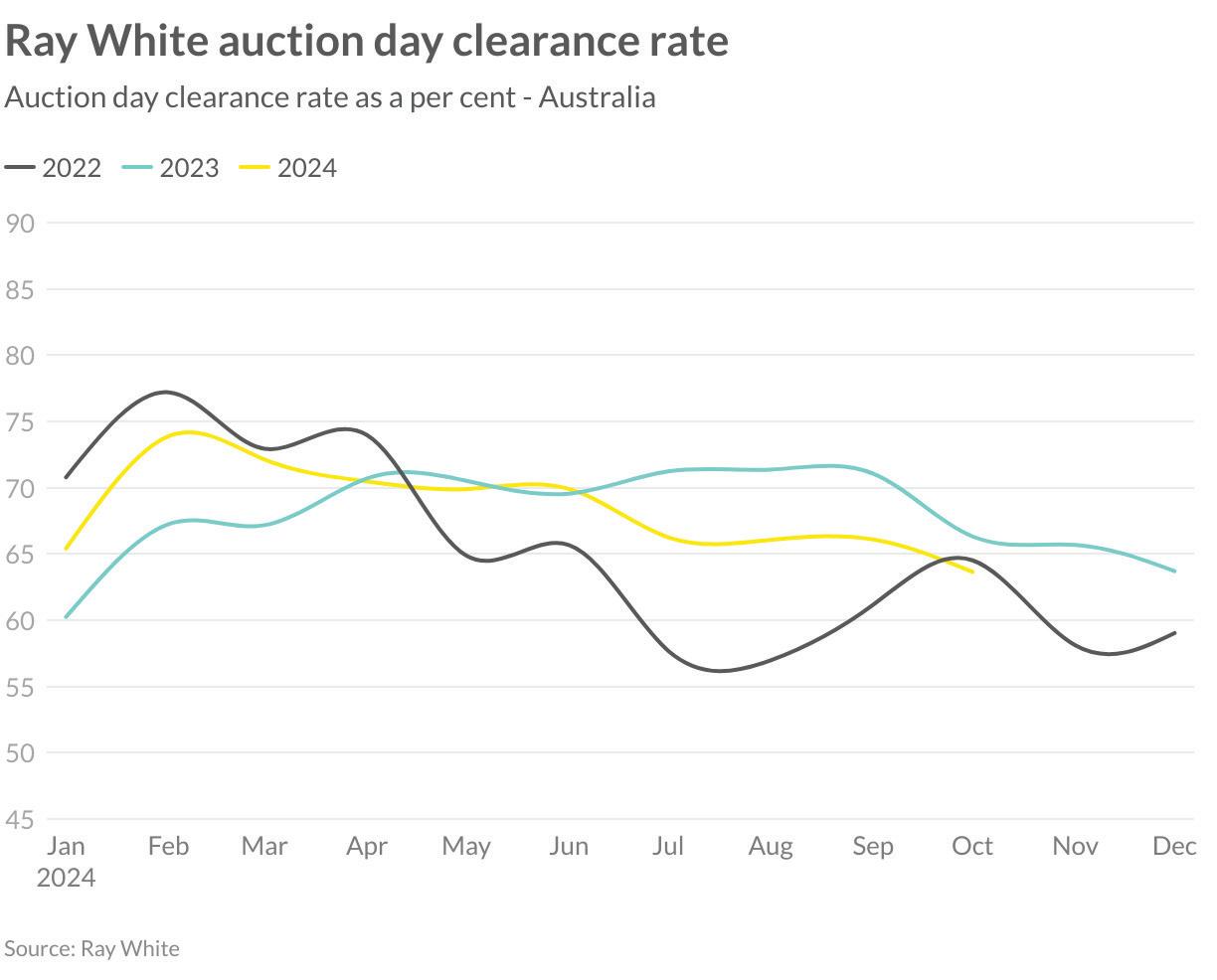

October has marked a shift in Australia’s auction market dynamics, with clearance rates dipping below 65 per cent. While this represents a decline from both 2022 and 2023 levels, the pattern mirrors the seasonal trends observed in previous years’ final quarters. The softening of price growth has notably stimulated buyer engagement, a factor expected to help maintain auction performance through the remainder of 2024.

Despite the recent moderation in clearance rates, several positive indicators suggest a resilient market ahead. Growing anticipation of interest rate reductions in the coming 12 months has begun to influence market sentiment, while the traditional spring selling season continues to drive activity. This combination of factors could provide fresh momentum to the auction sector.

The current market environment presents an interesting paradox: while clearance rates have eased, buyer participation remains robust. This dynamic, coupled with the potential for interest rate relief and seasonal market patterns, suggests the auction sector may find renewed strength as the year progresses. The interplay between moderating prices and sustained buyer interest points to a market that, while evolving, continues to demonstrate underlying resilience.

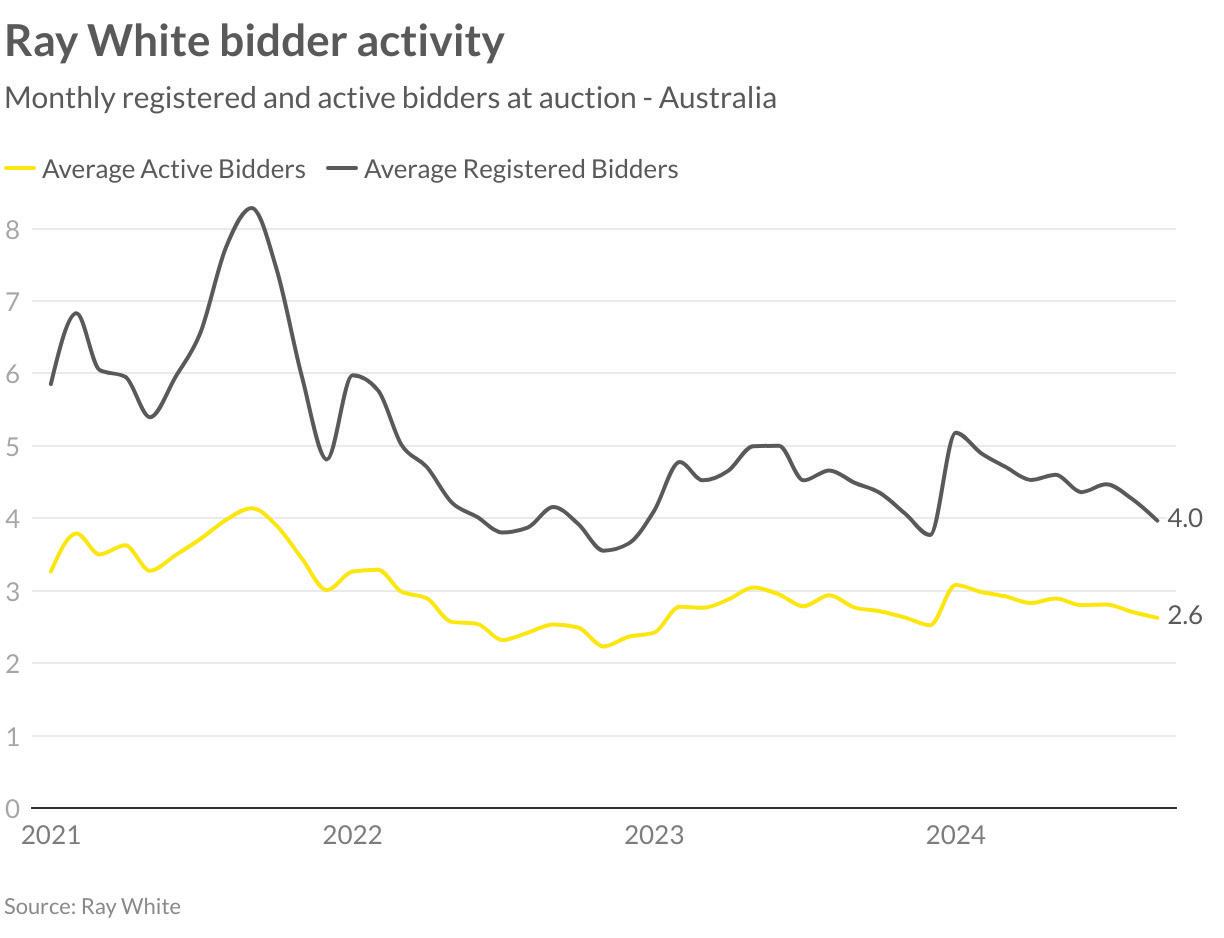

to auction participation.

The convergence of these factors - broader property choice, potential financing cost reductions, and seasonal market patterns - may create conditions conducive to strengthening participation rates back above four percent. However, the extent of this revival will largely depend on the volume and quality of new listings entering the market. An expanded selection of properties could prove crucial in stimulating broader buyer engagement and maintaining competitive tension at auctions.

The Ray White Group has marked a robust spring selling season, characterised by expanded market share, price appreciation, and increased property listings nationwide. While listing authorities indicate sustained strong supply levels ahead, the pace of price growth has begun to moderate in the key markets of Sydney and Melbourne.

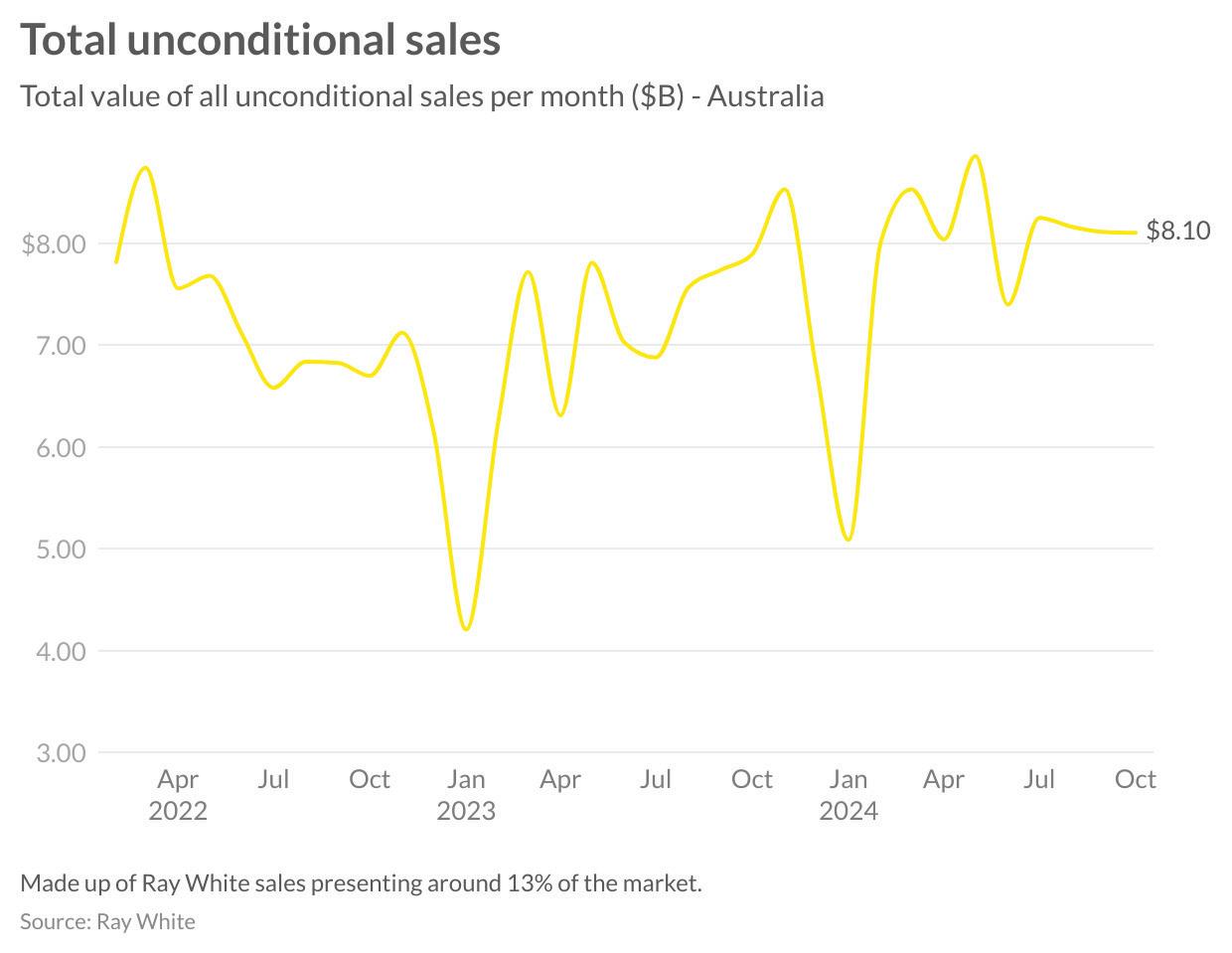

Monthly unconditional sales have maintained stability at $8.1 billion, matching the previous period’s performance and achieving a 2.7 per cent improvement compared to the prior year. Notably strong performance has emerged in smaller territories, with the NT and ACT recording substantial year-on-year increases of 43.3 per cent and 9.2 per cent respectively.

Victoria’s market has responded positively to increased listing activity, resulting in a 10.9 per cent improvement in sales (compared to October 2023). While Queensland and New South Wales have experienced more modest annual growth, both markets continue to demonstrate positive momentum.