Brazil’s International Air Network: All The Flights And Destinations

Page 79

Calendar Of Events

Page 80

Brazilian Tourists In The USA

Page 89

Trends Revealed By Similarweb Research Tools

Page 94

Internet And Use Of Social Media In Brazil

Page 103

List Of Representatives Of International Destinations For The Brazilian Market

Page 109

List Of Tour Operators Associated To Braztoa

Page 113

List Of Directors Of Airlines With Operation In Brazil

Page 115

Brazilian Luxury Travelers Profile

Page 124 How PANROTAS Can Help You Doing Business With Brazil

Page 132 Contact Us

WTTC

BRAZIL

ANALYSIS OF THE TRAVEL AND TOURISM INDUSTRY IN BRAZIL

(2024 -2034): 2

(2024 -2034): 2.4%

(2024 -2034):

CAGR (2024 -2034):

2024 Annual Research: Key Highlights1

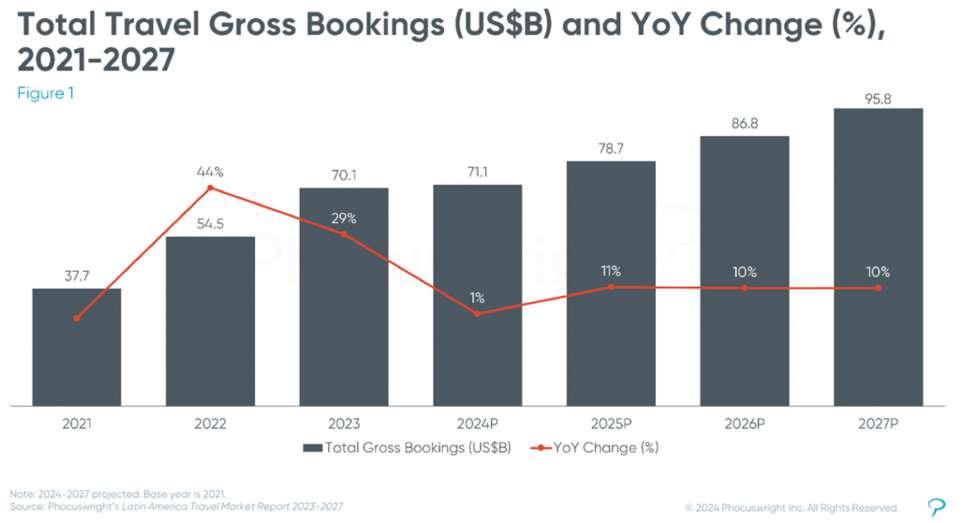

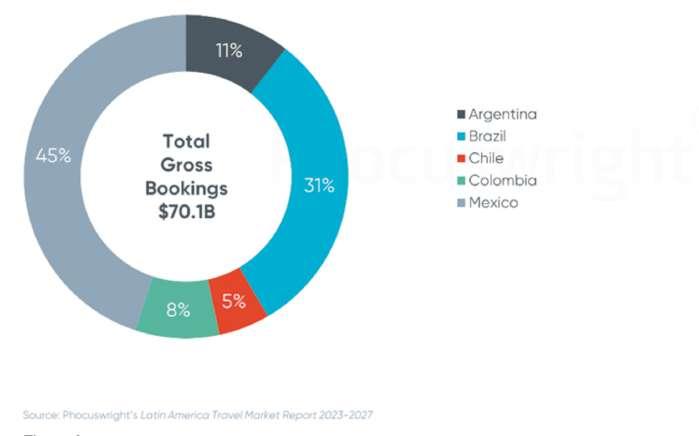

PHOCUSWRIGHT’S

AMERICA REPORT 2024

LATAM

LATAM

LATAM

LATAM

ECONOMIC OUTLOOK

GUILHERME DIETZE, FECOMERCIOSP

After a period of global tension caused by the increase in tariffs by the United States and China's response, both countries sat down at the table for more reasonable negotiations, easing the crisis and creating, at least in the short term, an environment of greater moderation and predictability. This scenario contributes to reducing the risks of a more pronounced deterioration in the global economy. Whenever risks decrease, emerging economies benefit from the flow of capital, seeking greater profitability at the expense of safety. After the devaluation of the real in early April, when it reached close to R$6 per dollar, the Brazilian currency has appreciated again, driven by the improvement in the external environment, and has sought the level of R$5.50. Travelers, therefore, are working with this level when planning their trips for the rest of 2025.

One factor contributing to the appreciation of the real is the increase in the Brazilian

interest rate. In early May, the Central Bank's Monetary Policy Committee (Copom) decided to increase the Selic rate yet again, from 14.25% to the current 14.75% per year, without any clear indication that the hike cycle was over. At the same time, the Federal Reserve (FED) in the United States decided to maintain its interest rate, which widens the differential in relation to Brazil and attracts speculative capital. In addition, the real interest rate, after discounting inflation, is around 9%, making it highly attractive to investors.

INFLATION IS A CONCERN

Brazilian inflation is the Central Bank's main concern. In April, it accumulated an increase of 5.53% in the last 12 months. Inflation is expected to continue rising, reaching a peak of close to 6% in September, before falling back to around 5% by the end of the year. Even so, this level will remain above the inflation target ceiling of 4.5%, which practically eliminates the

possibility of an inversion in the interest rate curve this year.

The Brazilian economy, in turn, is beginning to show signs of being impacted by rising interest rates and high inflation. Until recently, the monthly reports produced by FecomercioSP and PANROTAS indicated favorable sectoral figures in the first two months. However, the March data for retail, with a 1.2% drop in the annual comparison, reveals that sales have begun to lose momentum. Even considering the bimonthly average of February and March, to neutralize the effects of the Carnival calendar, growth was modest, at 0.5%, with a decline of almost 1% in supermarkets. The automotive segment, which had double-digit growth, grew only 3.4% in this bimonthly average, according to the IBGE.

Complementing the retail data, FecomercioSP released the default rate in the capital of São Paulo, which reached 20.6% of families with overdue bills in April, marking the second consecutive increase. In the previous month, the rate was 19.3%.

Between July of last year and March of this year, the default rate fluctuated around 19%, but now indicates the beginning of a trend of greater imbalance in household finances.

Even with the lowest unemployment rate in history for a first quarter — 7% — and with a record level of resources available to workers, high and persistent inflation, combined with rising interest rates, has gradually eroded families' purchasing power. Credit, an important tool for supplementing income, continues to expand, albeit at a slower pace. In the first three months of the year, credit granted to Brazilian families grew 4.1%.

The national tourism sector has shown resilience in the face of this scenario. According to FecomercioSP, there was growth of 6.6% in March, with an accumulated increase of 5.8% for the year, and practically all segments recorded revenues higher than those observed in 2024. However, at some point, there will be some – negative – impact on the sector. The Brazilian economy would hardly survive

unscathed by a scenario with inflation above 5% for more than six months and an interest rate close to 15% per year. The impact, inevitable, tends to occur gradually. Data from March and April already indicate this negative signal, marking the beginning of a deceleration process.

POSITIVE 2025

Expectations for 2025 are still positive, although at a slower pace: after a growth of 3.4% in 2024, the current projection is for expansion of 2% for this year. The government, in turn, announced an expectation higher than the market, of 2.5%, a number that would not be surprising if confirmed. It is worth remembering that there is a strong fiscal stimulus underway, which tends to benefit the economy in the short term, but also keeps inflation high and interest rates high for longer.

CONFIDENCE INDEXES:

• Consumer Confidence (ICC): The index fell to its lowest level since August 2022. In April, there was a drop of 3.6%, going from 115.2 points in March to 111 points. In the annual comparison, the decline was 14.3%. These are four consecutive drops, reflecting The population's dissatisfaction with high inflation and more expensive credit is impacting purchasing power.

• Business Confidence in Commerce (ICEC): The index also fell, reaching 97.6 points in April — the lowest level since June 2021. There was a 0.5% drop compared to March and a 10.3% drop compared to April of the previous year. Business owners are concerned about the impact of high interest rates on financial flow and household consumption, aggravated by inflation. Note: The ICC and ICEC range from 0 to 200. From 100 to 200 points is considered an optimistic level, and below 100 points pessimistic.

Although the indicators are from the city of São Paulo, they follow the trend of what is happening in the rest of the country, since the city, the largest in Brazil, represents 11% of the national GDP.

BRAZIL OFFICIAL INFORMATION

OFFICIAL NAME: Federative Republic of Brazil

GOVERNMENT SYSTEM: Federal Presidential Republic

PRESIDENT: Luiz Inácio Lula da Silva

CAPITAL: Brasília

LANGUAGE: Portuguese (we recommend that your promotional material, either printed or digital, should be written in Portuguese)

LOCATION: South America

AREA: 8.516 million km² or 3.288 million mi²

POPULATION: 212.583.750 million (IBGE Population Prospects 2024 Revision – Date of Reference: July 01, 2024)

CURRENCY: REAL

CITIES: 5,570

DIVISION: Brazil is divided into five regions with 26 states and one Federal District

MAJOR CITIES: São Paulo, Rio de Janeiro, Brasília, Fortaleza, Salvador, Belo Horizonte, Manaus, Curitiba, Recife, Goiânia, Porto Alegre and Belém.

OFFICIAL TIME ZONE: GMT-3

INTERNET TERMINOLOGY: .br

INTERNATIONAL DIALING CODE: +55

LIFE EXPECTANCY: 76,4 years (considering the year of 2023)

OFFICIAL WEBSITES: https://www.gov.br/planalto/en and https:// visitbrasil.com/en/

MINISTER OF TOURISM: Celso Sabino

EMBRATUR PRESIDENT: Marcelo Freixo

São Paulo

Porto Alegre

Rio de Janeiro

Brasília

Manaus

Salvador

Recife

BRAZIL'S ECONOMIC FORCE

BRAZIL IS THE 10TH GLOBAL ECONOMY

Brazil’s GDP was US$ 2.18 TRILLION (or R$ 12.7 trillion) in 2024

2024 GDP growth: 3.4%

Projection for 2025: + 2.4% (ACCORDING TO IPEA IN MAY/2025)

ECONOMIC PERFORMANCE

Inflation 2024: 4.83% (ACCORDING TO IPCA)

Projection for 2025: 5.53%

ACCORDING TO BRAZIL FEDERAL BANK FOCUS REPORT)

Unemployment rate 2024: 6.2% IN THE LAST QUARTER

Projection for 2025: 7.5% (ACCORDING TO BRAZIL FEDERAL BANK)

Interest rate 2024: 14.75%

Projection for 2025: 15%

Exchange rate average 2024± R$ 5.39 BRL to US$ 1

Projection for 2025: ± R$ 5.86 to US$ 1

Consumer confidence (dec/24): 92 (was 93.7 one year before – dec/23)

Family expenditures 2024: + 4.8%

Services growth 2024: + 3.1%

Sources: BCB, CNI, FGV, IBGE, IMF, Ipea

BRAZIL HAS THE LARGEST GDP IN LATIN AMERICA

Trinidad and Tobago

Source: The World Bank, IMF, UNWTO and TRADING ECONOMICS. https://www.unwto.org/tourism-data/global-and-regional-tourism-performance

BRAZILIAN POPULATION

STATES WITH BIGGEST POPULATION

BRAZILIAN’S EXPENDITURES IN INTERNATIONAL TRANSACTIONS (INCLUDES TRAVEL AND OTHER PURCHASES)

2024: US$ 14.82 billion

2023: US$ 14.05 billion

2022: US$ 12.18 billion

2021: US$ 5.2 billion

2020: US$ 5.3 billion

2019: US$ 17.6 billion

2018: US$ 18.26 billion

2017: US$ 19 billion

2016: US$ 14.5 billion

2015: US$ 17.36 billion

2014: US$ 25.57 billion

2013: US$ 25 billion

Source: Banco Central do Brasil (Brazil Federal Bank)

BRAZILIAN INTERNATIONAL AIR NETWORK

Airlines have increased their international operations to Brazil by +15% this year, adding almost 18 million seats. According to ForwardKeys, this growth is reflected in the main airlines operating in the country, with highlights for Gol (+48%) and Azul (+39%).

ORIGIN CONTINENT

SOURCE: EMBRATUR

SOURCE: EMBRATUR

ORIGIN

AFRICA AND MIDDLE EAST

SOURCE: EMBRATUR

SOURCE: EMBRATUR

AMERICAS

SOURCE: EMBRATUR

AMERICAS

SOURCE: EMBRATUR

EUROPE

SOURCE: EMBRATUR

AFRICA AND MIDDLE EAST

EAST

SOURCE: EMBRATUR

AFRICA AND MIDDLE EAST

NORTH AFRICA CASABLANCA

SUBSAHARAN AFRICA ADDIS ABABA

SOURCE: EMBRATUR

AFRICA AND MIDDLE EAST

SOURCE: EMBRATUR

AFRICA AND MIDDLE EAST

SOURCE: EMBRATUR

SOURCE: EMBRATUR

AMERICAS

CARIBBEAN

SOURCE: EMBRATUR

CARIBBEAN

CARIBBEAN

SOURCE: EMBRATUR

CENTRAL AMERICA

SOURCE: EMBRATUR

NORTH AMERICA

SOURCE: EMBRATUR

NORTH AMERICA

NORTH AMERICA

NORTH AMERICA DALLAS

NORTH AMERICA FORT LAUDERDALE

SOURCE: EMBRATUR

SOURCE: EMBRATUR

NORTH AMERICA

SOURCE: EMBRATUR

NORTH AMERICA

SOURCE: EMBRATUR

NORTH AMERICA

SOURCE: EMBRATUR

NORTH AMERICA

SOURCE: EMBRATUR

NORTH AMERICA

SOUTH AMERICA

SOUTH AMERICA BOGOTA

SOUTH AMERICA BUENOS AIRES

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOUTH AMERICA

SOURCE: EMBRATUR

SOUTH AMERICA

SOURCE: EMBRATUR

SOUTH AMERICA

SOUTH AMERICA

SOUTH AMERICA ROSARIO

SOURCE: EMBRATUR

SOUTH AMERICA

SOUTH AMERICA SANTA CRUZ

SOURCE: EMBRATUR

SOUTH AMERICA

SOUTH AMERICA SUCRE

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOUTHERN EUROPE

SOUTHERN EUROPE

SOUTHERN EUROPE LISBON

SOUTHERN EUROPE

SOURCE: EMBRATUR

SOUTHERN EUROPE

SOUTHERN EUROPE PORTO

SOUTHERN EUROPE ROME

SOURCE: EMBRATUR

WESTERN EUROPE

WESTERN EUROPE FRANKFURT

SOURCE: EMBRATUR

SOURCE: EMBRATUR

WESTERN EUROPE

ORIGIN CITIES

MAY 2024 X MAY 2025

SOURCE: EMBRATUR

SOURCE: EMBRATUR

DESTINATION IN BRAZIL (BRAZILIAN STATES)

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOURCE: EMBRATUR

DESTINATION CITIES

INTERNATIONAL FLIGHTS –BY BRAZILIAN AIRPORTS

United States, Europe, Argentina... Brazilians with greater purchasing power are relentless in international travel, and the numbers show it. While the domestic air network still lags behind the figures from 2015 (ten years ago) and even 2019 in many states, the number of international flights is only growing.

This year, Brazil will close with 76,200 international flights and 17.9 million seats offered. This represents an increase of 18% and 16% over 2024, respectively. These are record numbers, surpassing the highest figures of the last 10 years: 65,800 flights and 14.6 million seats in 2018. The data comes from Forwardkeys (an Amadeus Company), which conducted a survey at the request of the PANROTAS Portal.

Total International Flights (August to December 2025)

2024: 27,873

2025: 32,501

17% Growth

Total Seats on International Flights (August to December)

2024: 6.7 million

2025: 7.6 million

14% Growth

São Paulo is the state with the most connected international destinations: 51, with flights departing from Guarulhos or Viracopos. It is the only state with two airports with scheduled international flights. It accounts for 60% of International flights and 64% of seats offered. Rio de Janeiro ranks second, with 24 connecting destinations and 20% of total flights.

Simply adding the flights from São Paulo and Rio de Janeiro reveals that 20% of flights remain to be distributed among 14 other airports across the country. Brasília, our capital, ranks third, with less than 4% of total international flights. See below the destinations connected to the main Brazilian cities:

1 st – São Paulo (GRU and VCP, Guarulhos and Viracopos): 51 destinations Addis Ababa, Amsterdam, Aruba, Asunción, Atlanta, Barcelona, Bariloche, Bogotá, Boston, Buenos Aires, Caracas, Casablanca, Chicago, Cape Town, Mexico City, Panama City, Córdoba, Dallas, Doha, Dubai, Fort Lauderdale, Frankfurt, Houston, Istanbul, Johannesburg, Lima, Lisbon, London, Los Angeles, Luanda,

Madrid, Mendoza, Miami, Milan, Montevideo, Montreal, Munich, New York, Orlando, Paris, Porto, Punta Cana, Punta del Este, Rome, Salta, San José (Costa Rica), Santa Cruz de la Sierra, Santiago, Toronto, Washington DC and Zurich

2 nd – Rio de Janeiro: 24 international destinations

Amsterdam, Atlanta, Bogotá, Buenos Aires, Panama City, Córdoba, Dallas, Dubai Frankfurt, Houston, Lima, Lisbon, London, Madrid, Mendoza, Miami, Montevideo, New York, Paris, Porto, Rome, Rosario, Santiago, and Toronto

3 rd – Brasília:

9 international destinations

Bogotá, Buenos Aires, Cancun, Panama City, Lima, Lisbon, Miami, Orlando, and Santiago

4 th – Recife:

8 international destinations

Buenos Aires, Córdoba, Lisbon, Madrid, Montevideo, Orlando, Porto, and Santiago

5 th – Belo Horizonte:

8 international destinations

Bariloche, Buenos Aires, Panama City, Curaçao, Fort Lauderdale, Lisbon, Orlando, and Santiago

6 th – Florianópolis: 7 international destinations Buenos Aires, Panama City, Córdoba, Lima, Lisbon, Montevideo, and Santiago

7 th – Fortaleza: 7 international destinations Buenos Aires, Cayenne, Lisbon, Paris, Miami, Orlando, and Santiago

8 th – Porto Alegre: 6 international destinations

Bariloche, Buenos Aires Aires, Panama City, Lima, Lisbon, and Santiago

9 th – Belém:

6 international destinations

Bogotá, Cayenne, Fort Lauderdale, Lisbon, Miami, and Paramaribo

10 th – Salvador: 5 destinations Buenos Aires, Lisbon, Madrid, Montevideo, and Paris

11 th – Curitiba: 5 international destinations

Asunción, Buenos Aires, Lima, Montevideo, and Santiago

12 th – Manaus:

5 international destinations Bogotá, Panama City, Fort Lauderdale, Miami, and Puerto Ordaz (Venezuela)

13 th – Natal: 2 international destinations Buenos Aires and Lisbon

14 th – Porto Seguro: 1 international destination Buenos Aires

15 th – Foz do Iguaçu: 1 international destination Santiago

16 th – Maceió: 1 international destination Buenos Aires

Source: ForwardKeys (an Amadeus Company)

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOURCE: EMBRATUR

JETSMART (CHILE)

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOURCE: EMBRATUR

SOURCE: EMBRATUR

TAP AIR PORTUGAL

SOURCE: EMBRATUR

June

4 - Festival Das Cataratas

24 - PANROTAS Next 2025 - Florianópolis

July 14 - PANROTAS Special Tour Operators Guide

29 - PANROTAS Next 2025 - Cuiabá

August

5 - PANROTAS Next 2025 – Santos (Sp) 11 - PANROTAS Special “Technology For Tourism” Guide 25 - PANROTAS Special Travel Insurance And Ancillaries Edition

September

CALENDAR OF EVENTS 2025 2026

Experience USA 2025 (Official event from the USA Embassy in Brazil) Date to be announced

15 - Travel Tech Hub Day 23 - PANROTAS Next 2025 - Uberlândia

October

6 - PANROTAS Annual Vacation Guide

8 – 10 - Abav Expo

20 - PANROTAS Special ESG Guide 23 – 24 - BTM Brazil Travel Market

April 14 – 16 - WTM Latin America 22 - Travel Agent National Day

May 4 – 7 - ILTM Latin America

BRAZILIAN TOURISTS

IN THE US

ANNUAL VISITS

2019: 2.1 million

2023: 1.62 million

2024: 1.91 million

2025: 2.08 million (EST)

2026: 2.34 million (EST)

2027: 2.5 million (EST)

2028: 2.62 million (EST)

2029: 2.7 million (EST)

Total expenditures 2023: US$ 8.4 billion

Source: NTTO

BRAZILIAN MONTHLY VISITORS TO THE US

195.164

2024: 178.751

2025: 191.646 FEB 2024: 144.089

2024: 133.395

2025: 145.325

2025: 141.564

First 4 months 2024: 596.853

First 4 months 2025: 629.543 + 32.690 visitors in 2025 +5.4%

Source: NTTO

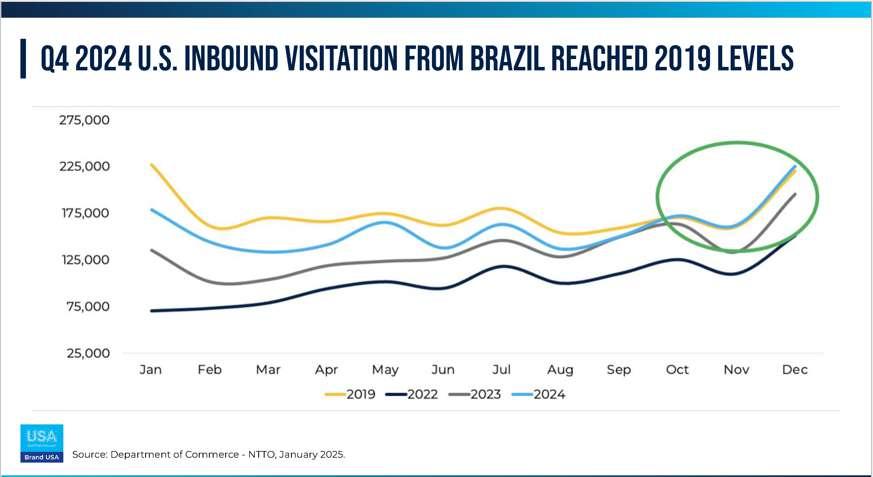

Although total visitation from Brazil in 2024 remained below pre-pandemic levels for most of the year, Q4 marked a significant turning point. In October, visitation from Brazil surpassed 2019 levels, and this upward trend continued through the end of the year. By Q4 2024, visitation had exceeded pre-pandemic levels by 2%, driven largely by the seasonal peak in December and January. This strong finish positioned the market for continued recovery and growth heading into 2025.

According to Brand USA, Brazil is the 2nd largest overseas market YTD through April, with 629,543 visitors. This is a 5.4% YOY increase. This increase is evenly spread across Leisure (+5.3%), Business (+5.8%), and Student (+6.4%) travel.

Preliminary data show a 7% increase in air tickets from Brazil purchased in May for travel later this year.

SURVEY OF INTERNATIONAL AIR TRAVELERS - ANNUAL REPORT BRAZILIAN TRAVELERS TO THE UNITED STATES

(January - December 2024 - Source: NTTO)

Decision to travel: 90 days prior to departure

Air ticket reservation: 60 days prior to departure

Airline reservation: 52% directly with the Airlines

Travelling with Family/Partners: 49%

Travelling alone: 51%

Party of adultus (medium): 1

Party with children (medium) 4

Bought travel insurence: 86%

Main purpose of trip:

Vacation/Holiday (68%)

Visiting Friends and Relatives (15,2%)

Business (6,7%)

Attending a Convention or trade show (5,9%)

Education (3%)

Leisure: 85.6%

Business: 16.2%

Stayed in hotel: 77%

Stayed in private homes: 33.5%

Average of nights: 11.7

First trip to the US: 17.2%

Used air travel between American cities: 32.8%

Source: NTTO

43.6%

PORT

OF ENTRY IN THE US

Miami: 31.1%

New York: 13%

Fort Lauderdale: 7.8%

Atlanta: 5.6%

Chicago: 3.6%

Los Angeles: 3.9%

Houston: 3.4%

Dallas: 2.7%

DC: 2.2%

Boston: 2.1%

MAIN DESTINATION (STATES)

Florida: 52.9%

New York: 13.4%

California: 6.2%

Georgia: 2.6%

Texas: 2.6%

Massachusetts: 2.4%

Nevada: 2%

Illinois: 1.7%

New Jersey: 1.5%

DC: 1.4%

CITIES VISITED

Orlando: 43.47%

Miami: 26.65%

New York City: 20.1%

Los Angeles: 6.74%

Las Vegas: 5%

DC: 3.8%

Boston: 3.79%

Fort Lauderdale: 3.77%

Tampa/St. Pete: 3.64%

Atlanta: 3.61%

Chicago: 3%

West Palm Beach: 2.67%

San Francisco: 2.32%

Dallas: 1.88%

Florida Keys: 1.66%

Houston: 1.65%

Philadelphia: 1.58%

Anaheim: 1.48%

San Diego: 1.32%

Source: NTTO

LEISURE ACTIVITIES

IN THE US

Shopping: 85.3%

Sightseeing: 78.6%

Theme parks: 48%

National Parks: 34.5%

Historic locations: 27.9%

Museums: 25.6%

Small towns: 21.6%

Fine dining: 16.8%

Sporting event: 16.8%

Concerts/Musicals: 13.6%

Cultural/Ethnic Heritage Sights: 10.8%

Nightclubs: 9.1%

Guided tours: 8.7%

Casinos: 3.7%

Snow sports: 1.8%

SPENDING HABITS

Average expenditure per person: US$ 3,200

In the US: US$ 2,100

With shopping: US$ 480

With food and Beverage: US$ 430

ANNUAL INCOME OF VISITORS

41.8% Under US$ 20,000 a year

15% From US$ 20,000 to US$ 40,000 a year

10% From US$ 40,000 to US$ 60,000 a year

7.3% From US$ 60,000 to US$ 80,000 a year

20% Above US$ 100,000 a year

PAYMENT METHOD

DURING THE TRIP IN THE US

30.4% credit card

25.6% debit card

21.7% cash brought from Brazil

11.3% cash withdrawals with cc

11.1% cash withdrawals with dc

52.7% were female

Average age: 42 years

Source: NTTO

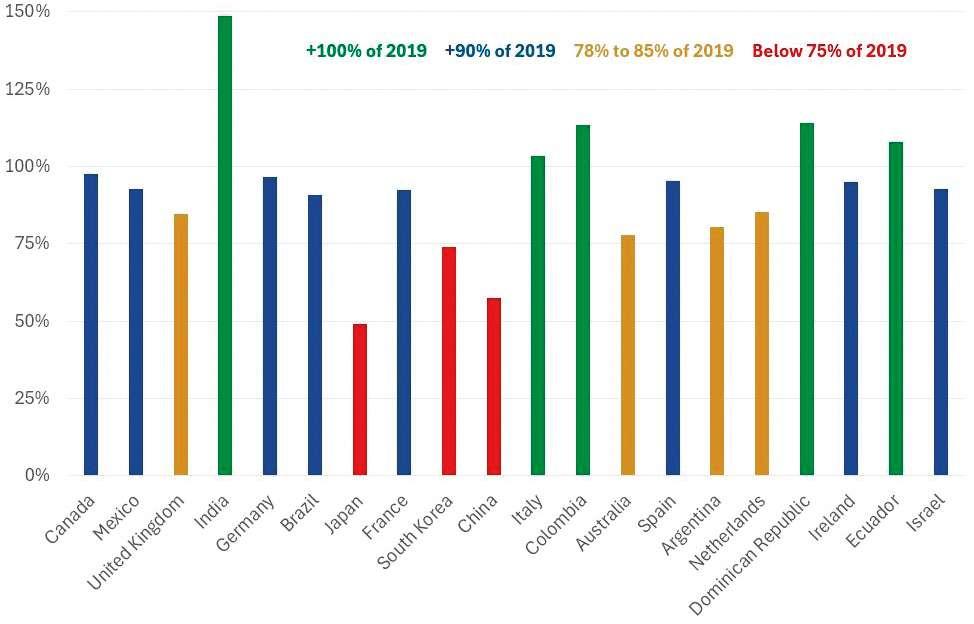

UNITED STATES'

TOP 20 INBOUND

SOURCE MARKETS

FOR INTERNATIONAL VISITATION 2024 VISITATION (SHARE OF 2019 VISITATION)

Source: NTTO

GLOBAL WANDERLUST: WHAT’S DRIVING BRAZILIAN TRAVELERS OVERSEAS?

Brazil remains a key international travel market, driven by a high volume of outbound travelers and rising interest in global destinations year after year.

In a conversation with Vicky Almeida, Similarweb Insights LATAM Leader, we uncovered how her data team is continuously analyzing digital behavior to reveal powerful signals about emerging travel trends.

Using fresh keyword data from Similarweb, we explored what’s inspiring Brazilian travelers to pack their bags. From dream-worthy experiences to iconic landmarks, their search behavior refl ects a growing appetite for culture, adventure, and comfort.

WHAT TRAVEL EXPERIENCES ARE BRAZILIANS SEARCHING FOR?

uTop Bucket-List Experience: Northern Lights

uMost Searched Landmarks: Eiffel Tower (France) and Colosseum (Italy)

uTop U.S. Destination: Hollywood

uPreferred Travel Style: Euro trip

uAccommodation of Choice: All-Inclusive Resorts or Hostel.

Whether it’s chasing the aurora borealis or city-hopping across Europe, Brazilians are prioritizing immersive, shareable travel moments.

Micro-trends: Emerging travel terms gaining traction, with signifi cant potential for sector engagement and the sale of travel packages and accommodations. Emerging micro-trends such as digital nomadism (+10267%), the allure of the Greek Islands (+3395.24%), boat trips (2466.7%), outdoor adventures (+1763.6%), and sports tourism (+1237.7%) are capturing increasing attention among Brazilian travelers.These trends reflect growing demand for tailored packages and content that meets evolving traveler expectations.

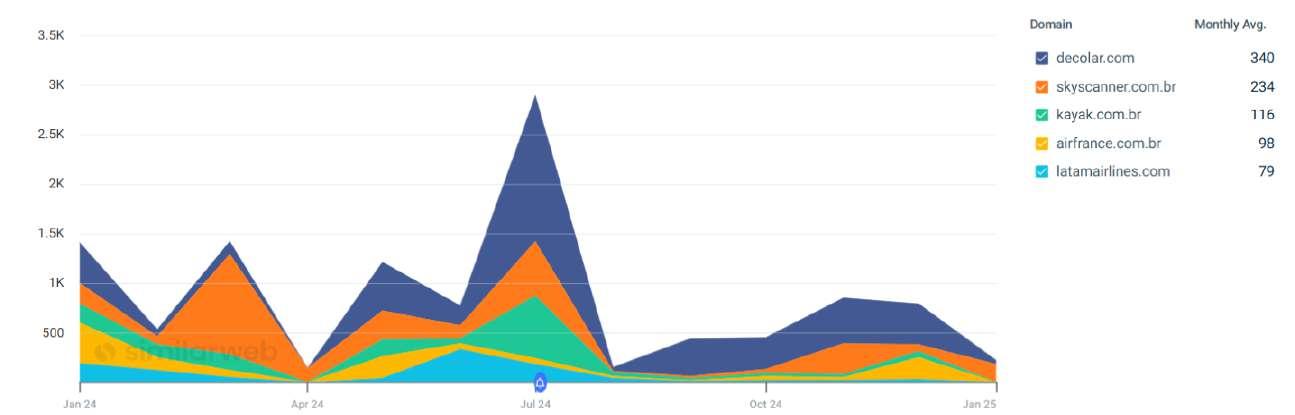

London, New York, Lisbon, Las Vegas, and Orlando are among the top international destinations for flight searches by Brazilian travelers—driven by competitive airfares, frequent flight availability, and strategic positioning for multi-city itineraries. Their combination of cultural richness and connectivity makes them both appealing and affordable entry points to Europe and the U.S.

Source: Similarweb. Desktop & Mobile web, Jan. 2024 – Apr. 2025, Brazil. Note: Searches include variations of city names combined with the words “passagem” (ticket) or “voo” (fl ight), such as “londres passagem” (London ticket) or “londres voo” (London flight).

richness and connectivity makes them both appealing and affordable entry points to Europe and the U S

Which websites are leading in receiving this search traffic?

Based on the data, the leading websites capturing the majority of this search traffic are:

Which websites are leading in receiving this search traffic?

Which websites are leading in receiving this search traffic?

Based on the data, the leading websites capturing the majority of this search traffic are:

● decolar.com

Based on the data, the leading websites capturing the majority of this search traffic are:

● decolar.com

uudecolar.com

● skyscanner.com.br

● skyscanner.com.br

uuskyscanner.com.br

● latamairlines.com

● latamairlines.com

uulatamairlines.com

● kayak.com.br

● kayak.com.br

uukayak.com.br

● google.com

uugoogle.com

● google.com

● airfrance.com.br

uuairfrance.com.br

● airfrance com br

These platforms stand out for their strong SEO strategies and competitive paid media presence — a signal of how performance in search channels translates into visibility and bookings.

These platforms stand out for their strong SEO strategies and competitive paid media pres

These platforms stand out for their strong SEO strategies and competitive paid media presence a signal of how performance in search channels translates into visibility and bookings.

— a signal of how performance in search channels translates into visibility and bookings.

ORGANIC CLICKS OVER TIME

Organic Clicks Over Time

Organic Clicks Over Time

Source: Similarweb Desktop & Mobile web, Jan 2024 – Jan 2025, Brazil Note: Searches include variations of city names combined with the words “passagem” (ticket) or “voo” (flight), such as “londres passagem” (London ticket) or “londres voo” (London flight) Image link: Imagem-1-Panrotas png

Source: Similarweb. Desktop & Mobile web, Jan. 2024 – Jan. 2025, Brazil.Note: Searches include variations of city names co with the words “passagem” (ticket) or “voo” (flight), such as “londres passagem” (London ticket) or “londres voo” (London flig Image link: Imagem-1-Panrotas.png

Source: Similarweb. Desktop & Mobile web, Jan. 2024 – Jan. 2025, Brazil.Note: Searches include variations of city names combined with the words “passagem” (ticket) or “voo” (fl ight), such as “londres passagem” (London ticket) or “londres voo” (London fl ight).

Want to see how these travel trends apply to your business? Get in touch with Similarweb’s team to explore custom insights and data that can help you navigate the digital travel landscape with more precision and confidence.

Want to see how these travel trends apply to your business? Get in touch with Similarweb’s team to explore custom insights and data that can help you navigate the digital travel landscape with more precision and confidence. Contact Similarweb today.

Want to see how these travel trends apply to your business? Get in touch with Similarweb’s team to explore custom insights and data that can help you navigate the digital travel lands with more precision and confidence.

Contact Similarweb today.

Contact Similarweb today.

A partnership

SOCIAL MEDIA AND INTERNET

Brazilian Tourism is increasingly digital and socially influenced, with social networks playing a leading role in travelers' decisions and journeys.

Instagram is the most influential, but YouTube is not far behind. Facebook is losing ground as TikTok gains more users of different ages. Most Brazilian travelers say they are impacted by digital influencers and their habits of accessing the site multiple times a day increase the viewing of the content created.

Latin America leads the world in daily time spent on devices and activities like social media, music streaming and online news

DIGITAL MEDIA WORLD LATIN AMERICA

Mobile 3h48min 4h50min

Desktop/laptop/tablet 2h50min 3h43min

Social/Messaging 2h20min 3h25min

Online press 0h59min 1h47min

Online TV/streaming 1h23min 1h35min

Source: Emarketer/DoubleVerify

Latin America will be the world’s second-fastest growring region for ecommerce between 2022 ans 2028 with a CAGR of 10.5%

Retail ecommerce sales will grow by roughly US$ 20 billion per year from 2024 to 2028, surpassing a quarter of a trillion dollars

Mexico is considered the only mature market in digitalization in Latin America. Brazil, Argentina, Colombia and Chile are digitally emerging, but Brazil is the biggest digital market in Latam

5 of the world’s 10 most active social media markets are in Latin America, with users spending 3+ hours per day on major platforms:

South Africa 3h36min

BRAZIL 3h35min

Philippines 3h30min

Chile 3h21min

Colombia 3h19min

Mexico 3h12min

Argentina 3h10min

Worldwide 2h20min

Source: Emarketer/DoubleVerify

SOCIAL NETWORK USER PENETRATION BY 2028

Latam: 65.8%

Argentina: 79.1%

BRAZIL: 74.1%

Chile: 73.1%

Colombia: 67.2%

Mexico: 66.9%

Peru: 65.8%

Source Emarketer/DoubleVerify

SCROLL & GO

Research conducted by TRVL LAB shows how Brazilians use social media to plan their next trip:

u The main triggers for travel conversion are attractive promotions and discounts, and partnerships and advertising with influencers. However, not just any content makes an impact. They must be visually wellproduced, and photos and short videos are preferred.

u 8 out of 10 Brazilians follow Tourism brands and companies. This means that the digital presence of destinations, hotels, attractions and restaurants is not only desirable, but essential to remain competitive and relevant.

u To play the social media game, you need to invest, and the brands most followed by Brazilian travelers are national and international giants, especially intermediaries.

u The process doesn’t end at the top of the funnel. Almost Half searched for more information through their own social networks and explored related profiles, using search engines to validate information.

USE OF SOCIAL MEDIA

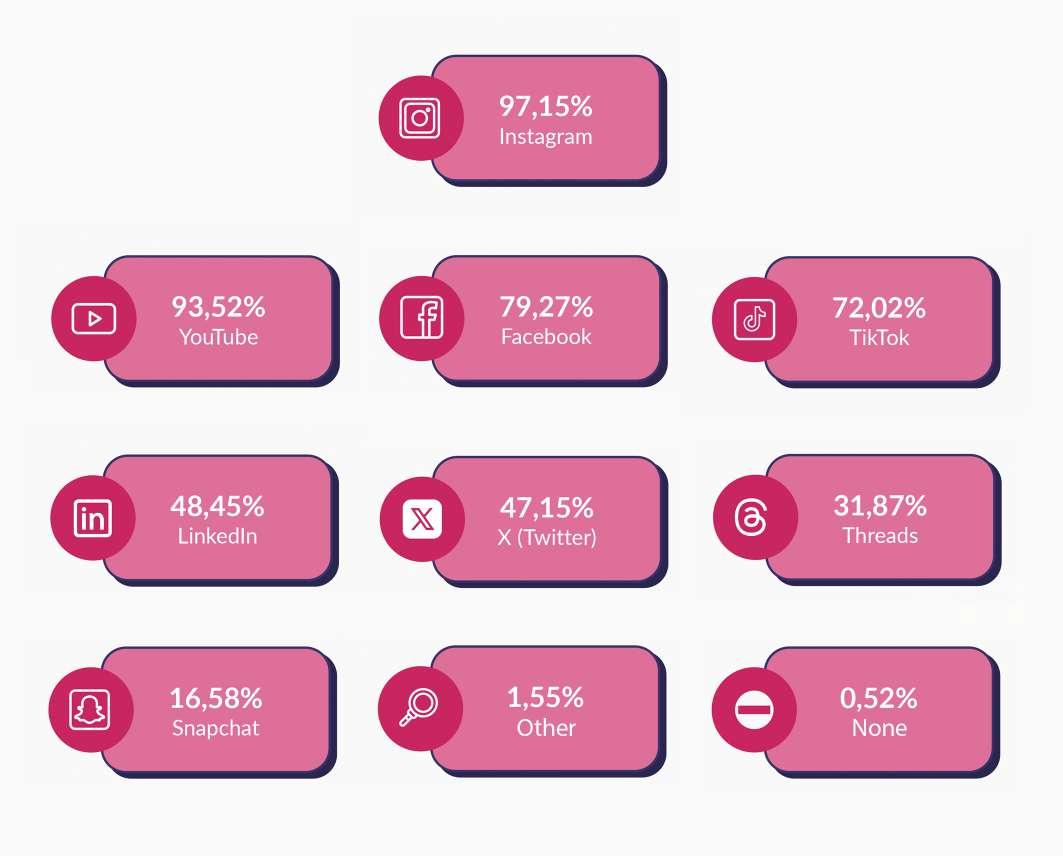

The most used social media by travelers are, respectively, Instagram, YouTube, Facebook and TikTok.

72.32% access social media several times a day and 84.07% believe that their profiles accurately reflect who they are in real life.

As for the frequency of posts, 25.07% post daily and 22.72% every 2 or 3 days.

SOCIAL MEDIA CURRENTLY USED

PROFILES THAT RESULTED IN INSPIRATION FOR LEISURE TRAVEL

Influencers and creators

OTAs

Friends and Family

Hotels or resorts

Restaurantes or bars

Hotel chain

TripAdvisor

Tourist attraction

DMOs

ABOUT THE TYPE OF CONTENT THAT MOST APPEALS ON SOCIAL MEDIA FOR TRAVEL INSPIRATION

Images and pictures

Videos with less than 1 min

Videos with more than 1 min

Written post

Link in bio or similar

ON THE TYPE OF CONTENT THAT MOST INFLUENCED TRAVEL IN THE LAST 12 MONTHS

Promotions

Partnerships

MOST POPULAR NATIONAL DESTINATIONS DUE TO THE

OF SOCIAL NETWORKS

ABOUT SOCIAL MEDIA ACTIVITIES CARRIED OUT DURING LEISURE TRIPS

I posted content from the trip on Stories or similar

I posted travel content on the feed or similar

I marked a destination in my posts

I posted travel content on Reels or similar

I tagged a travel-related supplier or brand in my posts (e.g. tour, hotel, restaurant, etc.)

I have received contacts (DMs or comments) from people wanting travel recommendations

I reposted or forwarded a target (third party) piece of contente

I reposted or forwarded travel brand content (from a third party)

None of the above

TRAVELERS PROFILE

ACCORDING TO THIS RESEARCH

u Most international travelers have a household income between R$7,501 and R$30,000 (60.74%) and have taken at least one leisure trip in the last 12 months.

u These travelers claim to frequently use social media to get inspiration about travel, recognize accounts that can provide reliable information on the subject, and tend to actively search for information about travel (54.05%).

u In addition to considering friends, family, and influencers, they consider online travel agency profiles as a source of inspiration (77.66% versus 52.08% of those who have not traveled abroad).

u The vast majority (91.26%) follow brands associated with travel.

u Instagram and YouTube are the most used networks for research and choices regarding destinations, accommodation, transportation, and activities, however, Facebook continues to be relevant among this group when compared to those who have not traveled internationally.

u This survey was conducted through an online questionnaire and sent to Brazilians from all regions of Brazil who had taken at least one leisure trip in the last 12 months.

u 422 responses were obtained with a 90% confidence level and a 3.5% margin of error.

INTERNATIONAL DESTINATIONS WITH REPRESENTATIVES IN BRAZIL

• DRAGONFLY AFRICASouth Africa / Botswana / Mauritius Islands / Mozambique / Namibia / Kenya / Rwanda / Seychelles / Tanzania / Uganda / Zambia / Zimbabwe (MICE and Leisure)

• EMECO TRAVEL - Egypt (MICE and Leisure)

• ACCESS HOLIDAYS AND EVENTSMorocco (MICE and Leisure)

• ARABIAN ADVENTURES - United Arab Emirates / Oman (MICE)

• ESHET - Israel (MICE)

• KHARMA HOUSE - Jordan / Saudi Arabia (MICE and Leisure)

• FOUS SEASONS TRAVEL - Austria / Hungary / The Czech Republic (MICE)

• BDP NEXT - Denmark / Finland / Norway / Sweden (MICE)

• SPANISH HERITAGE - Spain (MICE)

• HORIZON - Greece (MICE and Leisure)

• ICELAND TRAVEL - Iceland / Greenland (MICE and Leisure)

• GASTALDI GLOBAL DMCItaly (MICE)

• MAZURKAS DMC POLANDPoland (MICE and Leisure)

• OSIRIS TRAVEL AND EVENTSPortugal (MICE and Leisure)

• TEKSER - Türkiye / Azerbaijan / Georgia / Armenia / Uzbekistan (MICE and Leisure)

• DESTINATION ASIA - Cambodia / Hong Kong / Indonesia / Japan / Laos / Malaysia / Myanmar / Singapore / Thailand / Vietnam (MICE and Leisure)

• CREATIVE TRAVEL - Bhutan / Maldive Islands / India / Nepal / Sri Lanka (MICE and Leisure)

• EASTSTAR - China (MICE)

• ACCESS – Morocco (FIT & MICE)

• MARBER - Croatia (MICE)

• MONTENEGRO CONCIERGEMontenegro (MICE and Leisure)

IDEAS4BRAND

Maria Camilla Alcorta mariacamilla@ideas4brand.com linkedin.com/company/ideas4brand/ about/

• DIESENHAUS UNITOURS - Israel diesenhaus.com

• ATHENS EXPRESS - Greece athens-express.gr

• CARRANI TOURS - Italy carrani.com

• MERIDIAN TOURS - Türkiye meridian.com.tr

• BUS TURISTICO DE BUENOS

AIRES BY GRAYLINE - Argentina graylineargentina.com

VERTEBRATTA – AGÊNCIA DE MARKETING

Sheila Nassar sheila@vertebratta.com

55 (11) 98888-8879 vertebratta.com

• GLOBAL TOURISME CANADA globaltourisme.com/pt

• RIDA INTERNATIONAL - Egypt / Morocco / Tunisia / Jordan / Lebanon / Oman / Qatar / Saudi Arabia / United Arab Emirates / Abu Dhabi/ Dubai / Türkiye / East And West Europe / Africa ridaint.com

R. Dom Jaime Câmara, 170, Sala 904 – Centro Florianópolis – SC - 88015-120 (48) 3211-5600 fabio@incomum.com www.incomum.com

Fabio Cesar Frassetto

INTEREP

R. Leopoldo Couto de Magalhães Júnior, 758, 2º andar – Itaim Bibi

São Paulo – SP - 04542-000 (11) 3035-2811 rosana@interep.com.br www.interep.com.br

Cynthia Rodrigues

INTERPOINT

Al. Jaú, 1717, Casa 03Jardim Paulistano

São Paulo – SP - 01420-002 (11) 3087-9400 heloisa@interpoint.com.br www.interpoint.com.br

Heloisa Levy

LUSANOVA TOURS

Av. São Luís, 112, 14º andar – Centro São Paulo – SP - 01046-000 (11) 2879-6767 sergio.vianna@lusanova.com.br www.lusanova.com.br

Sergio Vianna

MATUETÉ

Av. Nove de Julho, 5109, 6º andar - Jardim Paulista São Paulo – SP - 01407-200 (11) 3071-4515 viajar@matuete.com www.matuete.com

Robert Betenson

MSC CRUZEIROS

Av. das Nações Unidas, 14171, 4º andar, Torre Crystal – Vila Gertrudes São Paulo – SP - 04794-000 (11) 5053-5300 info@msccruzeiros.com.br www.msccruzeiros.com.br

Adrian Ursilli

NCL - NORWEGIAN CRUISE LINE

R. Peixoto Gomide, 996, sala 740Jardim Paulista São Paulo – SP - 01409-001 (11) 3177-3131 info@ncl.com.br www.ncl.com.br

Estela Farina

NEW AGE TOUR OPERATOR

Al. Rio Negro, 503, sala 2020Alphaville Barueri – SP - 06454-000 (11) 4395-7078 atendimento@newage.tur.br www.newage.tur.br

Leonardo Mignani

NEW IT

R. Sete de Setembro, 99, 8º/11º e 12º andares – Centro Rio de Janeiro – RJ - 20050-005 (21) 3077-0200 newit@newit.com.br www.newit.com.br Alexandre Lima

R. Bandeira Paulista, 600, 10º andar, CJ 102/103 – Itaim Bibi

São Paulo – SP - 04532-001 (11) 3083-4411 / (11) 3898-2646 polvani@polvani.com.br www.polvani.com.br

Gerardo Landulfo

PURE BRASIL

R. João Ramalho, 717, CJ 92 - Perdizes São Paulo – SP - 05008-001 (11) 2638-6068 incoming@purebrasil.net www.purebrasil.net

Giancarlo Valias

QUEENSBERRY

Av. São Luís, 165, 4º andar – Centro São Paulo – SP - 01046-911 (11) 3217-7100 lourenco@queensberry.com.br www.queensberry.com.br

Marco Lourenço

R11 TRAVEL

R. Espírito Santo, 315 - Santo Antônio São Caetano do Sul – SP - 09530-700 (11) 3090-7200 cferrete@r11travel.com.br www.r11travel.com.br

Ricardo Amaral

RAIDHO

Av. dos Carinás, 595 – Moema

São Paulo – SP - 04086-011 (11) 3383-1200 atendimento@raidho.com.br www.raidho.com.br

Roberto Haro Nedelciu

RCA

R. São Luís, 50, 30º andar, CJ 302 – República São Paulo – SP - 01046-926 (11) 3017-8700 rca@rcaturismo.com.br www.rcaturismo.com.br

Rodolpho Gerstner

SCHULTZ OPERADORA

R. Visconde do Rio Branco, 1488, 11° andar, sala 1106 - Centro Curitiba – PR - 80420-210 (41) 3303-6565 atendimento@sp.schultz.com.br www.schultz.com.br

Aroldo Schultz

SMILES VIAGENS

Al. Rio Negro, 585, 4º andar, CJ 41 – Alphaville Barueri – SP - 06454-000 (11) 96745-3280

recebimentos@smiles.com.br www.smiles.com.br

Juan Ignacio Mudeh

SNOW OPERADORA

R. Major Lopes, 457 - São Pedro Belo Horizonte – MG - 30330-050 (31) 3303-7600 oper@snowoperadora.com.br www.snowoperadora.com.br

Paulo Medina

SQUAD VIAGENS

Av. Jerônimo Monteiro, 1000, Sala 1520 - Centro Vitória – ES - 29010-935 (27) 2125-1181 contato@voudesquad.com.br www.voudesquad.com.br/ Deomar Assunção

STELLA BARROS

Av. Brigadeiro Faria Lima, 2070, Sala 05 - Jardim Paulistano São Paulo – SP - 01451-000 (11) 2166-2250 carla.calil@stellabarros.com.br www.stellabarrros.com.br

Carla Callil

TBO HOLIDAYS BRASIL

Av. Nove de Julho, 5966, Sala 20 - Consolação

São Paulo – SP - 01406-200 (11) 3078-1550 tbobrasil@tboholidays.com www.tboholidays.com

Rodrigo Sienra

TRANSEUROPA

R. Visconde de Pirajá, 550, loja 229 - Ipanema Rio de Janeiro – RJ - 22410-901 (21) 2224-2297 transeuropa@transeuropa.com.br www.transeuropaviagem.com.br

Paulo Max

TRANSMUNDI

R. Uruguaiana, 10, grupo 140 - Centro Rio de Janeiro – RJ - 20050-090 (21) 2262-6262 contato@transmundi.com.br www.transmundi.com.br

Miguel Andrade

TREND VIAGENS

R. Catequese, 227, 8º andar, Sala 84 - Bairro Jardim

MAIN INTERNATIONAL DESTINATIONS FOR THE NEXT TRIPS*

ABOUT THE NUMBER OF VISITED COUNTRIES

ABOUT THE PREFERENCES IN LUXURY TRIPS

The Brazilian luxury traveler show a strong preference for “sun and sea” tourism (61.46%), followed by historic-cultural tourism (57.81%) and gastronomic tourism (42.60%).

Their trips are primarily motivated by the desire to visit new places, have fun, relax and rest, with the available period for traveling being a decisive factor in destination selection.

Destinations are typically chosen between 1 year and 6 months before the trip, however the reservations of the flight and accommodation are made 6 to 3 months in advance. Additional bookings, such as for attractions and restaurants, are made closer to the travel date.

The quality of attractions at a des-

tination is relevant for this traveler, however, as previously mentioned, price is also important in the decisive process. According to these respondents, the fact that the destination is hyped, or trendy, holds little significance.

This traveler is multichannel, and predominantly uses direct channels or on-line travel agencies, nonetheless, a significant portion affirm using the services of traditional agencies or travel consultants.

The most used means of transportation is the airplane with a preference for economy and premium economy classes. This choice is guided by factors such as price, comfort, convenience, and ease. As for means of accommodation,

the preference is for comfortable hotels, and the choice is made based on comfort and location.

On leisure trips, the more relevant items regarding means of accommodation are the room comfort, the quality, and variety of breakfast options, and the ease of booking.

Those aspects considered to be less important are leisure activities and children’s entertainment, content curation and a bar with a good cocktail menu.

Most of the travelers affirm to use apps and digital tools regularly during the trips.

For this demographic, traveling is a priority, and the trips are viewed as part of their health and wellness care routine.

CONSIDERED/CHOSEN NICHE FOR THE UPCOMING TRIPS

LUXURY

MAIN PURPOSES OF THE UPCOMING LEISURE TRIPS

Visiting new places

Having fun

Relaxing and resting

Living out memorable experiences

Learning about new cultures

Cherishing life and good moments

Living out exclusive experiences

Gathering family and friends

Learning something new

Disconnecting from the hectic life to reconnect with what matters tourism

Taking care of my health and wellness

Meeting new people

Watching natural phenomena

Attending concerts and shows

Connecting with something bigger and my spirituality

Others

Founded in 1974, 51 years ago, PANROTAS is the leading company for travel professionals in Brazil:

News and communication Proprietary events

Participation and coverage of trade shows (Brazil and abroad)

Analysis and researches for companies and destinations

PORTAL PANROTAS

Unique visitors/month 2024

445,900 2025

491,601

Pageviews/month: 2024

2,458,513 2025 2,655,566

Only trade portal audited (by IVC – similar to the AAM in the US – Audit Bureau of Circulations)

Portal PANROTAS is TOP 50 among travel websites in Brazil – according to Similarweb

PANROTAS

SOCIAL MEDIA

PANROTAS TOOLS TO REACH THE BRAZILIAN TRAVEL

PROFESSIONALS AND CORPORATE TRAVEL MANAGERS

PANROTAS PORTAL

- Real time coverage of events

- Hard news from the industry –people, companies, destinations

- Analysis and special articles

- Dedicated coverage of events

- Special sections at our home page:

Aviation

Luxury Travel

Hotel industry

Destination

Travel professionals

Corporate travel

- Personalized sponsored sections at our home page for your company or event

- Many formats for your banners, ads and activations a tour home page or internal pages and sections

We are the ONLY news portal audited by IVC in the travel industry

PANROTAS Magazine

20+ Special Editions per year

Digital and print versions distributed at main trade shows ans personalized mailing

Special issues on:

• Cruises

• Tour Operators

• Travel to the USA

• ESG

• LGBTravel

• Annual Vacation Guide

• Luxury Travel special issue

• Luxury Travel Annual Report with ILTM

• Tourism Trends (for PANROTAS Forum)

• Visit Florida

• Ancillaries for travel agentes

• Year in review

• Best in Class edition (honoring the best travel agentes)

• Best in Class edition (honoring the best in sales)

Distributed at the main trade shows: Abav Expo, WTM Latam, ILTM Latam, Abav Travel SP, Lacte (Corporate travel), Festuris and BTM

Cruise annual guide

Luxury travel edition

Vacation annual guide

PANROTAS FORUM

• March 3rd and 4th 2026

• WTC Events Center São Paulo

• Attendence in 2024: +2,100 travel leaders

Speakers in 2024:

• Fred Dixon (Brand USA), Roberto Sallouti (BTG Pactual), D.T. Minich (Experience Kissimmee), Jerome Cadier (Latam Airlines), John Rodgerson (Azul Airlines), Celso Ferrer (Gol Airlines), Joe Mohan (Abra Group), Marcelo Bento (Aena), Juan Carlos Martinez (Ávoris Corporación), Fabio Godinho (CVC Corp), Cinthia Douglas (Disney Destinations), Bruno Reis (Embratur), Luiza Helena Trajano (Magazine Luiza), Chinmai Sharma (Sabre), Donovan Ferreti (Ticketmaster),

Main Travel Leaders event in

Brazil, with quality players at the stage and in the audience.

Francisco Mattos (F1), Juliana Trujillo (Disney Institute), Muryad de Bruin (Curaçao Tourism Board), Ron Pohl (WorldHotels and BWH Hotels), Samantha Almeida (Globo TV) and Thomas Dubaere (Accor), among others.

Sponsors 2024:

• BWH Hotels, Ancoradouro, CVC Corp, CNC, Copastur, Gol, Air France-KLM, Latam Airlines, Delta Air Lines, Disney Destinations, Disney Cruise Line, Omnibees, Mato Grosso do Sul Tourism, Abreu, Accor, Assist Card, Sabre, Decolar/Despegar, Iberia, British Airways, Movida, BTG Pactual, Dominican Republic, Paraná Tourism Civitatis, Experience Kissimmee, Orinter and Embratur, among others.

PANROTAS Events and Initiatives

• PANROTAS Next – Roadshow in 6 Brazilian cities

• PANROTAS Best in Class Awards, sponsored by Amadeus – at WTM Latin America

• New Corporate Travel Event –October – São Paulo

• Travel Tech Hub Day – September, 15th – São Paulo

• Mentoria Preta (Black Mentoring) – Initiative to help foster black corporate leadership in Brazilian Tourism. More at: www. mentoriapreta.com.br

• Travel Leaders Hub – A new Community of Leaders, coordinated by PANROTAS, Mapie, Travel Tech Hub and TRVL Lab. More at: comercial@panrotas.com.br

• Anchor booths at the main trade shows: WTM Latam, Festuris, Abav Expo, BTM and Abav TravelSP

• PANROTAS Daily Newsletter – with the main hard news from the industry: 27,052 e-mails registered

• PANCORP Newsletter: 10,259 travel managers and supplier e-mails

• Sponsored e-blasts: 19,452 target e-mails

• Brazilian Overview Monthly Report – our Monthly newsletter, in English, for our internacional readers

EXCLUSIVE Newsletters for your brand

News, pictures and info about your brand, event or new products –directed to 20,000 travel agentes

PANROTAS at WhatsApp and Telegram

Our communities receive news and the digital version of PANROTAS Magazine

Lives and vídeos

Talk live with our audience and keep momentum with the on demand vídeos. Or use our channels to promote your vídeos or social media pieces. Lives in our Instagram also possible.

Use our mailing list

Distribute print or digital promotional material to up tp 27,000 travel professionals

Our Partners

Researches, market studies and reports for the travel industry. Visit trvl.com.br.

Access all Latin America travel trade with Ladevi/La Agencia de Viajes

Be part of our ILTM & PANROTAS Annual Luxury Travel Report –Brazil & Latin America

Anchor booth at the biggest trade show in Brazil

Anchor booth at the international trade show

A community dedicated to tech professionals focused on Tourism tools, solutions and softwares; we will organize our first event on October, in São Paulo

Be part of our Travel Leaders community.

José Guillermo Condomí Alcorta President and founder guillermo@panrotas.com.br

José Guilherme Alcorta CEO guilherme@panrotas.com.br

Ricardo Sidaras Commercial Director rsidaras@panrotas.com.br

Artur Luiz Andrade Editor-in-chief and chief communication officer artur@panrotas.com.br +55 11 97336-7236

Adrian Bertini Special projects for the US Market, both at PANROTAS platform and publications and LADEVI’s. abertini@ladevi.com +1 305 680 2683