Spring 2024

Wind Energy 5.0 – Our Competence. Our Responsibility.

Wind Turbine Automation

More than 140,000 wind turbines automated

Condition Monitoring

Comprehensive protection for your operating assets

Retrofit

Extend turbine lifecycles

www.bachmann.info

Grid Protection and Control Safe, fast and stable power management

Wind Power SCADA Access protection and operation control

Automation solutions for every area of wind energy

Wind Europe March 20-22, 2024 Bilbao, Spain Booth: 1-B100 Join us: energy.industry.maritime.

240311_AZ_059_Image_Wind_EnergyGlobal_216x303mm_EN.indd 1 11.03.2024 11:11:03

CONTENTS

03. Guest comment

04. Renewables in Europe

Théodore Reed-Martin, Editorial Assistant, Energy Global, summarises the current state of renewable energy in Europe.

10. A promising lithium discovery to power the future

Brian Quock and Michele Cox, ANA Corp., USA, look at new US lithium deposits that could power future battery production.

16. Communicating battery storage

Blesson Thomas, Head of Grid at Clearstone Energy, highlights the urgent need for the industry to take steps to educate developers, communities, planners and politicians on grid scale battery safety.

22. Unlocking the power of AI

Charlene Lee, Product Manager and Antonio Notaristefano, Director of Product Management, Fluence, discuss the use of artificial intelligence to help resolve asset management challenges.

28. Transmission technology for the energy transition

Peter Sandeberg, Hitachi Energy, Sweden, provides insight into employing voltage sourced converter-based high-voltage direct current for offshore connections.

SPRING 2024

32. Winds of change

Jon Salazar, CEO, Gazelle Wind Power, UAE, examines how collaboration across industries can enable the growth of floating offshore wind.

38. Changing gears: A look at wind turbines

The wind turbine industry faces an ever-increasing challenge to reduce the cost of energy production, decrease operational and maintenance costs, and increase lifespan. All of this must happen while scaling up technology to multi-megawatt, offshore machines operating in harsh environments. Gary Rodgers, CEO of Magnomatics, details the role magnetic gears play in helping achieve these goals.

42. Advanced turbine monitoring

Dr Joe Donnelly, CEO and Co-Founder, Windscope, makes the case for strengthening operational resilience in a volatile wind market.

46. The future of lightning risk control

Wind Power LAB explores the evolving landscape of lightning risk control for wind turbines and the proactive measures required to ensure their operational efficiency and longevity.

50. Pioneering a safe palette

Allan Bonde Jensen, Business Development Manager, Infrastructure and Energy, and Palle Gustafsson, Chemical Engineer, Teknos, consider the rise of isocyanate-free and epoxy-free industrial coatings.

56. Mobilising a zero-emissions future with hydrogen

Lucrezia Morabito, Comau Product and Solution Manager, talks about the importance of hydrogen as a key factor for sustainable mobility in a Q&A with Jessica Casey, Editor of Energy Global

60. Maximising solar power

Lorna Smith, EcoFlow, UK, analyses how energy storage can help maximise solar power.

64. Global news

ANA Energy offers an advanced hybrid energy system that sets the standard for power efficiency, sustainability, and cost savings. The battery has a 30-year lifecycle, and the system delivers maximum power with a low environmental impact. This unit offers three-phase and single-phase output voltages simultaneously and is made to withstand any environment. The ANA Energy BossTM represents a new era in energy efficiency, by reducing fuel consumption, extending generator life, reducing maintenance costs, and emitting fewer greenhouse gases.

Copyright © Palladian Publications Ltd 2024. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the copyright owner. All views expressed in this journal are those of the respective contributors and are not necessarily the opinions of the publisher, neither do the publishers endorse any of the claims made in the articles or the advertisements. ENERGY GLOBAL 04

enquiries [enquiries@energyglobal.com]

Reader

ON THIS ISSUE'S COVER Théodore Reed-Martin, Editorial Assistant, Energy Global summarises the current state of renewable energy in Europe. T well countries were faring according to their targets. Though it did not yield any new information (there is a renowned mitigation gap between the current trajectory of emissions and the desire to halt global warming at 1.5˚C), the Stocktake will help inform the two renewable alternatives increased in generation by 90 TWh and an installed capacity of 73 GW. outside of the EU, as will be outlined. However, as impressive as these 4 5 ENERGY GLOBAL SPRING 2024 Spring 2024

Protect your assets for a lifetime with our everlasting and cost effective solution.

Easy-Qote is a corrosion prevention coating applied as a patch with minimum surface preparation requirements. Or as we like to say: easy as 1, 2, 3. Simply clean, patch and let the coating do the work while you relax.

The easy solution for wind turbines.

as 1, 2, 3 clean,

For more information visit easyqote.com

Easy

patch, unwind

MANAGING EDITOR

James Little james.little@palladianpublications.com

EDITOR

Jessica Casey jessica.casey@palladianpublications.com

EDITORIAL ASSISTANT

Théodore Reed-Martin theodore.reedmartin@palladianpublications.com

SALES DIRECTOR

Rod Hardy rod.hardy@palladianpublications.com

SALES MANAGER

Will Powell will.powell@palladianpublications.com

PRODUCTION DESIGNER

Kate Wilkerson kate.wilkerson@palladianpublications.com

EVENTS MANAGER

Louise Cameron louise.cameron@palladianpublications.com

DIGITAL EVENTS COORDINATOR

Merili Jurivete merili.jurivete@palladianpublications.com

DIGITAL ADMINISTRATOR

Nicole Harman-Smith nicole.harman-smith@palladianpublications.com

DIGITAL CONTENT ASSISTANT

Kristian Ilasko kristian.ilasko@palladianpublications.com

ADMINISTRATION MANAGER

Laura White laura.white@palladianpublications.com

Editorial/Ad vertisement Offices:

Palladian Publications Ltd

15 South Street, Farnham, Surrey, GU9 7QU, UK +44 (0) 1252 718 999 www.energyglobal.com

COMMENT

Luke Gibson

Chief Operating Officer, Field

Last year, the UK’s electricity system under-utilised battery storage capacity. In the balancing mechanism, gas power plants provided 72% of capacity the Electricity System Operator (ESO) requested at short notice, with control rooms ‘skipping’ over battery storage at a rate of around 80% in some instances.1

‘Skipping’ storage released an additional 70 000 t of carbon dioxide emissions – equivalent to the annual emissions of 44 000 petrol cars –compared to operating available storage instead. All while the UK grew battery storage capacity to 3.5 GWh in the same year.1

When the ESO faces a shortfall in supply, generators called on to plug the gap tend to offer more expensive, carbon-intensive forms of power, such as gas peaking plants – in contrast to cheaper, cleaner battery storage sites. Batteries typically charge up when the price is low (when there’s more renewable power on the grid) to discharge when the price is higher (and there’s less renewable generation).

Skipping suitable battery storage is a significant challenge to decarbonising the UK’s energy system.

Like curtailment (paying wind farms to switch off when there isn’t enough storage or grid infrastructure to manage output), it’s a flaw in our energy system’s design – the kind which leads to higher bills and emissions.

As the number of batteries connected to the grid has increased, the challenge facing the ESO has become integrating these smaller, flexible, more distributed assets into the centralised energy system. This presents an IT architecture upgrade problem that it must manage, while maintaining security of supply.

It’s taking the right steps forward. The launch of the Open Balancing Platform and proposed Grid Code changes aim to help the ESO increasingly dispatch batteries. They should offer batteries

greater visibility across the country, including how long they can charge or discharge for (called ‘duration’) and what their existing state of charge is (important for knowing the value they provide when called).

As the ESO becomes the National Energy System Operator, greater resources (whether funding or talent) would help it deliver a more flexible electricity system, one where batteries can play a greater role in delivering a cheaper, greener and ever-reliable system.

There are still circumstances in the medium-term where the ESO continues deploying carbon-intensive energy. However, new tools, markets, and capabilities in the control room will provide the opportunity for batteries to play a bigger role in delivering a net zero power system by 2035.

Although skipping is gradually being resolved, curtailment remains one of the biggest challenges to the energy transition. Carbon Tracker warned that it could cost bill payers £3.5 billion a year by 2030 and generate 6.8 million t of avoidable carbon emissions.2

To tackle this growing issue, we have to better use the technology already available to us: energy storage.

Last year was the year of electricity grids, with vital reforms announced to accelerate new connections. While this could make it easier to bring new storage capacity online, 2024 needs to be the year the energy system adapts to fully enable batteries.

Powering the grid with renewables means we need battery storage. And we need batteries to be supported with market mechanisms that can reward them for reducing curtailment costs, enabling their financing at pace.

References

References available upon request.

ENERGY GLOBAL SPRING 2024 3

4 ENERGY GLOBAL SPRING 2024

TThéodore Reed-Martin, Editorial Assistant, Energy Global, summarises the current state of renewable energy in Europe.

he end of 2023 saw the world’s climate leaders agree to make a unanimous transition away from fossil fuels at COP28. Here, for the first time since the climate pledges of the 2015 Paris Agreement, a ‘Global Stocktake’ was taken providing an assessment of how well countries were faring according to their targets.1 Though it did not yield any new information (there is a renowned mitigation gap between the current trajectory of emissions and the desire to halt global warming at 1.5˚C), the Stocktake will help inform the next set of nationally determined contributions (NDCs).

In 2023 44% of the EU’s electricity mix was sourced from renewables, with wind and solar contributing 27%. Combined, these two renewable alternatives increased in generation by 90 TWh and an installed capacity of 73 GW. 2 Similar trends can be seen in countries outside of the EU, as will be outlined. However, as impressive as these statistics may seem, they are inconsistent with the trajectory required for the net-zero by 2050 scenario. This report will examine the current state of renewable energy in Europe, both inside and outside the EU.

5

Solar

A good starting point would be the fastest growing renewable alternative: solar energy. The decade between 2010 and 2020 saw the price of photovoltaic (PV) energy production plummet by 82%, which has made it an affordable option. 2 Moreover, with the planet unavoidably heating up, the sun will not be going anywhere any time soon; therefore, for many countries, solar is a wise investment. After all, the Earth is exposed to 173 000 TWh of untapped solar energy throughout the day, which is 10 000 times the amount that is required in the same timeframe. 3

Latest trends show a robust growth in solar usage within the EU, as 9% of the EU’s electricity was generated using solar in 2023. Sustaining the momentum of 2022, the installation increased by 40%, resulting in a deployment of 55.9 GW across all 27 member-states, bringing the total installed capacity from 204.09 GW, to 259.99 GW at the year’s end. 2 While the EU is well on track to reach REpowerEU’s goal of 320 GW of PV by 2025, in terms of generation, it struggled as the +48 TWh growth rate of 2022 went down to +36 TWh. Noteworthy solar additions by country within the EU include Germany, leading at 62 TWh, followed by Spain (45 TWh), Italy (31 TWh), and France (23 TWh). 2

The EU’s solar landscape in 2023 saw widespread success, with 20 member-states achieving their best solar years, and 25 surpassing the previous year. The Netherlands emerged as the frontrunner for the highest solar energy production per capita within the EU, boasting 1044 W/capita. Germany followed with 816 W/capita, and then Denmark at 675 W/capita. Germany also had the greatest amount of contributions to solar expansion with 14.1 GW. Spain and Italy followed suit with installations of 8.2 GW and 4.8 GW respectively, with Spain generating the most energy at +9.4 TWh. 2

Outside of the EU strides have been made in numerous nations’ solar additions. In the UK, for example, solar constitutes just over 4% of its electricity, with the total installed capacity being 15 GW at the end of 2023; this figure is expected to grow five-fold to 70 GW by 2030. 4 This trend was echoed in Switzerland, who added 1500 MW in 2023, bringing nation’s total solar energy capacity to 6200 MW. 5 This was also shown in Norway, who added 300 MW in 2023, which is almost half of its total capacity of 597 MW. 6 Moreover, Voltalia announced the production of the first megawatt-hours of the largest solar farm in the western Balkans, Karavasta (Albania) that has a capacity of 140 MW, as the nation’s solar debut.7

Of course, the effectiveness of solar radiation will always face nature’s constraints. Last year, a lack of solar radiation in various parts of Europe meant that there was only an increase of about 20%. 2 Geographical positioning has a pivotal role in a nation’s capacity in producing solar energy: Spain is a country that benefits from longer daylight hours and solar exposure. 8 In contrast, nations like Iceland grapple with the inherent limitations

of higher latitude that renders solar initiatives virtually redundant. These geographical nuances always need to be considered when examining countries performances, for southern Europe will always do better than its northernmost counterparts as far as solar is concerned.

That being said, 2024 is to be an exciting year for solar energy in Europe, with an expected spike in solar radiation and a string of big projects and plans in the pipeline. Some of the latest news regarding this includes RWE and PPC’s 450 MWp Orycheio Dei Amynteo farm in Greece that will be commissioned in 2025; 9 the MET Group’s 23 MWp PV plant in Hungary which is to start operation in 2H24; 10 Innova’s 14 MW Parkhill South solar farm in Scotland having just been granted permission,11 or SSE Renewable’s acquisition of a 400 MW portfolio of early-stage Polish PV projects.12 For many countries, the future is in solar.

Wind

In 2023, the wind’s share of electricity rose to 18% of the EU’s electricity (475 TWh), surpassing gas for the first time. Wind capacity additions fell short when compared to the 56 GW of solar, adding only 17 GW in 2023. 2

The lion’s share of wind brought online in 2023 was onshore, amounting to a total of 14 GW, with only 3 GW being offshore. 2 Germany continued to lead in terms of largest additions with 29 000 turbines in operation, and a total of 61 GW in function. Projections indicate that there will be an additional 4 GW of new turbine capacity in 2024, though it is still a long way off the 13 GW/y to reach their 2030 targets. That being said, onshore wind has solidified itself as the work horse of Germany’s electricity system and now generates one-quarter of it.13

France also saw a large generation increase, adding 10 TWh in 2023, followed by the Netherlands with 7.8 TWh. The latter, with its advantageous conditions for offshore wind in the shallow waters and windy environs of the North Sea, surpassed its 4.5 GW target of offshore wind additions by achieving 4.7 GW. This accounted for 15% of the nation’s total electricity demand, with one particularly notable addition being the 1.5 GW Hollandse Kust Zuid offshore wind farm. Other notable contributions were Denmark and Ireland who managed wind shares of 58% and 36% respectively. 2

Outside of the EU, the UK saw the start of the electricity production at Dogger Bank wind farm off the Yorkshire coast, following the installation of an industry-first Haliade-X 13 MW turbine, as well as the 1.1 GW Seagreen wind farm being brought online. The UK managed to generate 29.4% of electricity using wind, which was only slightly smaller than its use of gas (32%).14

Switzerland had a 12.5% increase on 2022, though wind still only accounted for 0.3% of the total electricity consumed.15 Ukraine, despite the war, has still done a good job on the wind front, as the country continues to build the Tyliguska windfarm, with 114 MW of the project built. Upon completion the project will be 500 MW in capacity

ENERGY GLOBAL SPRING 2024 6

■ Many companies rely on Boehlerit‘s innovative technology to manufacture their products.The Aust rian carbide specialist Boehlerit is guaranteed to be behind many everyday products.

Boehlerit GmbH & Co.KG, Werk VI-Straße 100, 8605 Kapfenberg, Telefon +43 3862 300-0, www.boehlerit.com

Boehlerit is behind it

and able to produce 1.7 TWh of electricity (enough for 900 000 households).16

Over the coming years, there is to be an expected increase in wind. Indeed, the International Agency has predicted the EU to produce 23 GW/y between 2024 – 2028. While this is clearly a significant increase there remains considerable distance to cover before the EU is on track for its 30 GW/y target.17 More large scale projects like Hollandse Kust Zuid – expected to be completed in 2024 –and Dogger Bank – completion to be in 2026 – are needed to get on track.

Hydropower

Europe’s renewable energy transition will also be hinged on its hydropower sector. Though of course, droughts will inevitably cause issues for energy systems that rely too heavily on hydropower. Therefore, in the colder and wetter climates of northern Europe, hydropower is more effective than it is in the south, where there are more frequent dry spells, particularly given the heatwaves of last summer.

Hydropower made up 12% of the EU’s electricity last year and accounted for 32% of renewable energy. Sweden was the largest producer of hydropower in 2023, producing 66 TWh, followed by France (53 TWh), and Austria. Latvia recorded the highest electricity share at 61%, followed by Austria (59%), and then Croatia (46%). Heat waves caused issues for many countries, though there was a 15% increase on 2022. 2

Beyond the EU, particularly in northern Europe, there are good statistics that highlight the importance of hydropower. In 2023, Norway generated 15 541 MW of electricity using hydropower, constituting 90% of the nation’s electricity production. Iceland, not far behind, also relies on hydro for 70% of its electricity needs, showcasing the efficacy of using water in Europe’s northernmost regions.19

Switzerland, endowed with a favourable mountainous landscape, is home to over 600 hydropower plants contributing to approximately 58% of the nation’s electricity generation. While these figures may not match the scale of Norway and Iceland, it still showcases the potential within Switzerland of harnessing hydropower, especially compared to its lower statistics in solar and wind energy. 20

Meanwhile, in Albania, a lot of electricity production is from state-owned hydropower. Despite being a population of 3 million, Albania’s total hydropower market amounts to about 7.5 TWh. With hydropower being state-owned, it keeps the price of energy steady, which de-incentivises private investment: for when the country inevitably has a dry season, or even year (quite common considering its hot climate), prices of electricity would soar. 21

There will be exciting upcoming movements in the hydropower sector in the coming years. With examples of Statkraft announcing plans to invest €6 billion in upgrades to Norwegian turbines, more investments will occur and help streamline the production of hydropower. 22

Other renewables

This section will take a look at other renewable energy sources that have a much smaller share of the European energy economy.

There has been a change in the climate surrounding the use of bioenergy lately, as research now suggests that large quantities of biomass, particularly wood-based biomass, can emit extensively. Therefore, it is no longer viewed as entirely carbon neutral, and given the risk of emitting, countries are aiming to minimise this impact by keeping the share in energy economies small. In 2023, bioenergy contributed 153 TWh of electricity in the EU, constituting 5.7%. Germany again led production with 47 TWh, followed by Italy and Sweden at 16 TWh and 12 TWh, respectively. Denmark had the highest percentage of electricity from bioenergy at 21%, while Poland was the only country that experienced an increase, standing at 0.5 TWh. Since the latter half of 2023, bioenergy generation has consistently hovered at a five-year low. 2

Green hydrogen projects are starting to become more frequent. In 2024, Lhyfe will build a green hydrogen production plant in Brake, Germany, producing up to 1150 tpy of green hydrogen. 23 Similarly, in the UK and Ireland, Source Galileo and Lhyfe have also announced a joint agreement to develop commercial scale green and renewable hydrogen units. 24 Lastly, encouraging results from Sealhyfe, Lhyfe’s offshore hydrogen pilot, have spurred in the HOPE project: a 10 MW offshore initiative with the aim of producing 4 tpd of green hydrogen by 2026. 25

Finally, shifting the focus to geothermal energy, Iceland emerges as a global leader relative to its population. A remarkable 65% of Iceland’s primary energy and 90% of its household heating stems from geothermal resources, though of course the country’s situation on a volcanic ridge sets it up nicely for geothermal energy.19 On the other hand, geothermal is still small in the EU, producing 0.2% of electricity, 26 and is used to heat just 2 million of the EU’s 100 million heating systems. However, there are ambitious goals of using geothermal heat pumps to satisfy 25% of Europe’s energy needs by 2030. There is a lot of work to do, but the potential is there. 27

Conclusion

Europe stands at a critical juncture between its current trajectory, and the emission reduction required to halt global warming at 1.5˚C. While renewables now have a far more important share in European energy economies, as is shown by the figures in this article, there is still a long way to go. Over the next coming years, it will be vital to ramp up the production of renewable energy in order to achieve global warming goals.

References

A comprehensive list of references is available upon request.

ENERGY GLOBAL SPRING 2024 8

Trust the experts.

Our priority is the safe on-time delivery of your global energy projects. CRC Evans utilises market-leading welding and coating services, technologies and advanced data solutions, combined with a right first time approach.

crcevans.com

Brian Quock and Michele Cox, ANA Corp., USA, look at new US lithium deposits that could power future battery production.

There are international efforts to adopt net zero emissions by 2050, and lithium is the battery chemistry of choice. The valuable metal is the key active material in rechargeable batteries for both consumer electronics, electric vehicles (EVs), and renewable energy systems, although the percentage of batteries that contain lithium will vary depending on the battery application, type, and size. In 2022,

according to sources, lithium-ion dominant technology for electric renewable energy systems of the global battery market, reaching 85% by 2030. Albeit, that all lithium-ion batteries of lithium, as different chemistries compositions and performance top five lithium batteries are:

ENERGY GLOBAL SPRING 2024 10

lithium-ion batteries were the electric vehicles and some which account for 60% market, with the prediction of Albeit, this does not mean batteries use the same amount chemistries have different performance characteristics. The are:

> Lithium iron phosphate.

> Lithium nickel manganese cobalt oxide.

> Lithium manganese oxide.

> Lithium nickel cobalt aluminium.

> Lithium titanate.

It depends on the want and need of the features, such as energy density, power performance, safety, lifespan, and cost to highlight the correct battery.

Since 1996, the National Minerals Information Center has provided mineral yearbooks and mineral commodity summaries on the worldwide supply, demand, and flow of the mineral commodity lithium in the yearly U.S. Geological Survey (USGS). In the USGS’s 2023 global report, lithium reserves were estimated at 21 million t and distributed among various regions and countries. The top five countries with the largest lithium reserves were:

11

Chile (9.3 million t), Australia (6.2 million t), Argentina (2.2 million t), China (1.5 million t), and the US (1.1 million t).

One of the largest known lithium deposits identified in the US

Concerning energy storage and battery technology, the recent identification of one of the largest lithium deposits in the US has sparked profound interest and anticipation within the energy sector. The vast new lithium deposit has been discovered in the Nevada-Oregon border region in a volcano crater, marking a significant milestone in the realm of sustainable energy. This newfound source of lithium has sparked intrigue across multiple industries which are reliant on battery technology and energy storage solutions. The deposit is estimated between 20 – 40 million t, which could make it the world’s largest source of lithium. This discovery is set to revolutionise the landscape of battery production and energy storage projects moving forward, particularly in Nevada and California. Battery manufacturers, energy storage companies, and researchers are eagerly anticipating the potential implications of tapping into these newfound lithium resources.

Excitement in the industry

The industry’s response to this groundbreaking discovery has been nothing short of electrifying. Battery manufacturers, energy storage companies, and researchers are eagerly anticipating the potential implications of tapping into these newfound lithium resources. The abundance of lithium in the US signifies a significant stride towards self-sufficiency in battery materials, reducing dependency on imports and potentially lowering costs for consumers.

The prospects of leveraging these vast lithium deposits for battery technology are tantalising. Manufacturers are considering how this newfound resource could enhance the efficiency and performance of batteries, leading to advancements in electric vehicle capabilities and grid scale energy storage solutions. The excitement in the industry is palpable, fuelling ambitions for applications and sustainable energy practices.

Inferred resource estimates

The inferred resource estimates associated with these lithium deposits hold immense promise for driving future lithium extraction projects in the US. These estimates provide crucial insights into the potential size and quality of the deposits, guiding investment decisions and operational strategies for mining companies.

With the increased focus on sustainable energy sources and the urgent need to transition towards cleaner technologies, the significance of inferred resource estimates cannot be overstated. The data derived from these estimates will play a pivotal role in shaping the development of extraction methods, environmental mitigation strategies, and supply chain management practices within the lithium mining sector.

As the industry shifts towards a more sustainable and eco-conscious approach to energy storage, the reliable and extensive availability of lithium in the US offers a strategic advantage. By harnessing these inferred resources effectively, stakeholders aim to bolster domestic battery production, foster innovation in long-duration energy storage systems, and contribute to the global shift towards renewable energy sources.

Addressing global energy needs

This lithium deposit comes at a crucial time when the demand for energy storage solutions is skyrocketing worldwide. With the rapid expansion of renewable energy sources such as solar and wind power, the need for efficient and reliable energy storage systems has never been more urgent. The abundance of lithium in the US can play a pivotal role in meeting these escalating energy requirements and reducing our dependence on fossil fuels.

Implications for energy storage systems

The discovery of this vast lithium resource has far-reaching implications for the development of long-duration energy storage systems. As the backbone of the transition to clean energy, advanced energy storage technologies are essential for stabilising the grid and ensuring a sustainable power supply. The availability of such a significant lithium deposit in the US paves the way for the accelerated deployment of cutting-edge storage solutions that can store immense amounts of energy for extended periods, enabling grid flexibility and enhancing renewable integration.

Figure 2 BOSS25-15 Hybrid Generator, equipped with ultra-high cycle lithium titanate oxide (LTO) battery modules (shown with available solar option).

ENERGY GLOBAL SPRING 2024 12

Figure 1 . Brine pools used for lithium mining at Silver Peak Mine, located in Nevada, USA. The mine produces around 5000 t of usable lithium each year (1% of the world total).

padding machine

AND

INNOVATIVE AND CUSTOMIZED SOLUTIONS FOR EVERY

SOLUTIONS FOR EVERY CHALLENGE since 1958

CHALLENGE INNOVATIVE

Parma, Italy

FOR MORE INFORMATION SCAN HERE spd series 150 / 160 / 250 / 350 / 450 EFFICIENT PRODUCTION FULL RADIO CONTROL SCAIPNET REMOTE ACCESS AUTOLEVELING SYSTEM www.scaipspa.com

CUSTOMIZED

spd - 150 evo

This monumental discovery of one of the largest lithium deposits in the US heralds a new era of possibilities for battery technology and energy storage initiatives, paving the way for a greener and more resilient energy future.

ExxonMobil drilling first lithium well in Arkansas

ExxonMobil’s recent endeavour in drilling the first lithium well in Arkansas marks a significant milestone in the quest for a sustainable supply of lithium, a crucial component in the production of batteries for EV and energy storage systems. The company announced plans to become a leading producer of lithium in November 2023, and has started construction this year with plans to begin production in 2027. The company will utilise direct lithium extraction (DLE) technology to access lithium-rich saltwater reservoirs, 10 000 ft underground. The company’s proactive approach towards lithium extraction not only demonstrates technological advancement, but also underscores their commitment to meeting the growing demands of the automotive industry.

Sustainable lithium supply

ExxonMobil’s initiatives in drilling the first lithium well in Arkansas are aimed at ensuring a sustainable supply of lithium for the automotive industry. By exploring new sources of lithium within the US, ExxonMobil seeks to reduce reliance on imports and promote domestic production of this essential resource. This strategic move aligns with the global shift towards sustainable energy solutions and emphasises the importance of securing a stable lithium supply chain for future generations.

Meeting EV production demands

As the demand for EVs continues to rise, ExxonMobil’s foray into lithium extraction signifies a proactive approach to meeting the lithium demands for manufacturing EVs. By strategically positioning itself in the lithium market, ExxonMobil aims to support the growth of the EV sector by ensuring a reliable and sufficient supply of lithium-ion batteries. This initiative not only contributes to the expansion of sustainable transportation, but also underscores the company’s commitment to innovation and environmental responsibility in the automotive industry.

ExxonMobil’s pioneering efforts in drilling the first lithium well in Arkansas reflect a strategic manoeuvre towards securing a sustainable supply of lithium and meeting the demands of EV production. By investing in domestic lithium resources, ExxonMobil is poised to play a pivotal role in advancing the transition towards clean energy and driving the future of battery manufacturing for EVs and long-duration energy storage systems.

Revolutionising EV batteries

These newfound reserves are set to revolutionise the production of EV batteries and pave the way for a greener and more sustainable future.

DLE technology advancements

Advancements in DLE technology have emerged as a game-changer in the quest for enhancing lithium production for EV batteries. This cutting-edge technology, which allows for the

direct extraction of lithium from brine sources, promises increased efficiency and reduced environmental impact in the extraction process. The development of DLE technologies opens new possibilities for harnessing lithium resources effectively, ensuring a stable supply for the growing demand for EV batteries.

Scaling up lithium production

As the EV market continues to expand, the feasibility of scaling up lithium production becomes a critical priority. The discovery of abundant lithium deposits in the US presents an unprecedented opportunity to boost domestic lithium production and reduce reliance on imports. By ramping up production capacity and streamlining extraction processes, the industry can meet the escalating demands of the electric vehicle sector and drive forward the transition to clean energy solutions.

Effect of the Inflation Reduction Act

Policies like the Inflation Reduction Act hold the potential to shape the utilisation of the newly-discovered lithium deposits and impact battery production within the US. By implementing measures to streamline regulatory processes and incentivise domestic manufacturing, such legislation can catalyse the efficient extraction and processing of lithium resources. This, in turn, paves the way for accelerated battery production, driving down costs and enhancing supply chain resilience. The strategic alignment of government initiatives with the burgeoning lithium industry is crucial for fostering a conducive environment for investment and technological advancement. Through targeted policies that support sustainable practices and innovation, the Inflation Reduction Act sets the stage for a sustainable energy future powered by homegrown lithium solutions.

The evolving landscape of battery production and energy projects in the wake of these new lithium discoveries heralds a transformative era of cleaner, more efficient power storage and distribution. As the US seizes the opportunities presented by its abundant lithium reservoirs, the ripple effects across industries and economies are poised to shape a greener and more sustainable tomorrow.

Conclusion

The recent discovery of significant lithium deposits in the US marks a pivotal moment in the realm of battery production and energy projects. With one of the largest lithium reserves identified in the country, the landscape for battery manufacturers and energy storage systems is set to undergo a transformative shift. This discovery not only ensures a more sustainable and domestic source of lithium for battery production but also paves the way for enhanced energy storage solutions.

The implications of this discovery extend beyond just the realm of battery manufacturing; it holds the potential to revolutionise the future of sustainable energy solutions. As global energy demands continue to rise, these newfound lithium deposits offer a promising opportunity to meet these challenges head-on. The availability of such vast lithium resources in the US will not only bolster the domestic energy sector, but also contribute significantly to the advancement of clean and renewable energy technologies worldwide.

ENERGY GLOBAL SPRING 2024 14

Communicating

16 ENERGY GLOBAL SPRING 2024

Blesson Thomas, Head of Grid at Clearstone Energy, highlights the urgent need for the industry to take steps to educate developers, communities, planners and politicians on grid scale battery safety.

As the climate crisis continues and the world transitions to renewable energy sources, storage is set to play an increasingly important role. Battery energy storage systems (BESS) are particularly important in improving the quality and reliability of electricity networks for net zero.

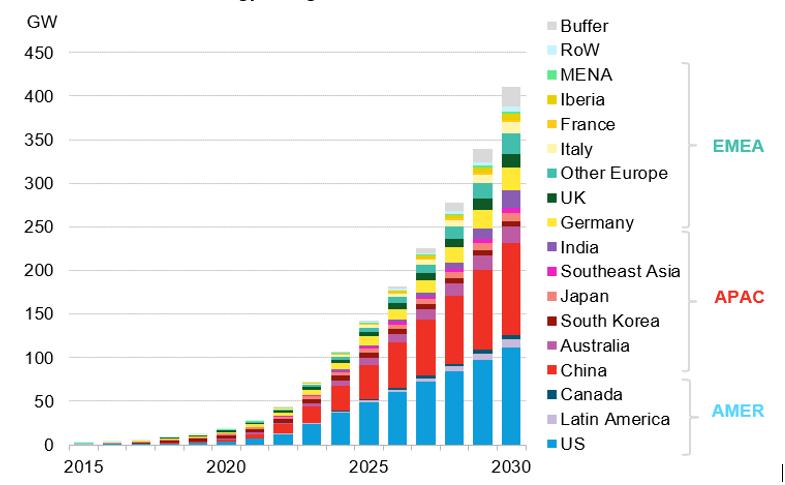

Bloomberg is forecasting a 15-fold increase in energy storage globally by 2030, representing 387 GW/1143 GWh of new energy storage capacity (Figure 1).1 There are a wide range of storage technologies aiming to meet this demand, including compressed air, thermal energy, and gravity-based storage. However, BESS using lithium iron phosphate batteries (LFP) and nickel manganese cobalt (NMC) technology are predicted to deliver the majority of new storage capacity in the coming decade.

Australia, China, the UK, and the US are among the first movers in battery storage deployments. In the UK, battery storage is expected to deliver 24 GW of its 2030 target of 30 GW installed storage capacity, a ten-fold increase on today’s BESS installed base of 2.1 GW.2

In many regions of the world, governments are advocating for BESS installations and putting ambitious targets in place in order to support the transition to renewable energy sources. However, growing public concern about the safety of lithium-ion-based battery storage projects threatens to delay (or even derail) projects.

The risk of thermal runaway in lithium-ion batteries is well-documented, and much has been learned from previous safety incidents. Tier one BESS manufacturers have invested significantly in incorporating new safety features into hardware and software. International standards have been updated, and testing regimes are more rigorous.

Communicating battery safety

17

However, despite these efforts, there is still a lack of a comprehensive and industry-wide narrative regarding the safety of large scale battery systems. As a result, it can be a significant challenge to communicate these efforts and reassure local communities, politicians and planning authorities about the safety of grid scale battery systems.

What are the safety risks with battery storage?

The primary risk is fire. The process leading to a lithium-ion battery catching fire is called thermal runaway. Thermal runaway is an uncontrolled exothermic reaction that raises cell temperature and can propagate between cells, occurring when a cell achieves elevated temperatures. Thermal runaway can be triggered by various factors, such as: mechanical and electrical breakdown, thermal failure, and internal/external short-circuiting or electrochemical abuse.

The risks to public safety from a battery unit catching fire are threefold:

> The potential for explosion due to the build-up of flammable gases within a battery unit.

> Fire and the presence of toxic gases in the smoke plume from a fire.

> The contamination of water used to tackle a fire and the possibility of this water getting into local water supplies.

How prevalent are battery safety incidents?

Despite high-profile media reporting, there have been relatively few safety incidents at battery energy storage facilities.

A recent report from Pacific Northwest National Laboratory (PNNL), aimed at educating local planners, cited 14 safety incidents at grid-connected BESS facilities in the US.3 None of the incidents led to a loss of life. For context, there are 491 utility scale projects operational in the US.

In the UK, there are more than 100 grid-connected BESS in operation, with a total energy storage capacity of close

to 3 GWh. There has been one reported UK BESS fire that required Fire & Rescue Service (FRS) attendance, in Liverpool, in September 2020. The fire was contained and there was no third-party collateral damage or injury to firefighters or the public. For context, this equates to one incident in almost 550 years of combined operation across UK projects.

How can safe battery energy storage facilities be ensured?

The UK National Fire Chiefs Council (NFCC)4 guidance and the National Fire Protection Agency (NFPA)5 international standards have specified requirements on the technology characteristics, design, and operation of utility scale battery energy storage facilities. There is some variation between UK and US guidance, so Clearstone’s battery safety standards merge elements of both to ensure compliance with both and comprehensiveness.

There are a number of standards aimed at ensuring that battery units are designed in a way that minimises the risk of thermal runaway and limits propagation if an incident happens.

One of the key ones is UL 9450a testing. Battery units are fire tested to confirm the effectiveness of fire suppression systems and design features at preventing thermal runaway from spreading from one BESS unit to adjacent ones. UL 9450a certification is a requirement in many jurisdictions and any technology provider under consideration for a project should be able to provide certification and testing data to support it.

Additionally, facility design guidelines include safe distances from battery units to site boundaries, public footpaths, and occupied buildings to ensure that the public is protected in a fire situation, enhancing the safety of the overall BESS.

Gases being given off by battery cells is an early indicator that a thermal runaway event is occurring, so early detection of gases is critical before a build-up can become volatile. A competent battery management system (BMS) and integrated battery assembly will identify, control, and eliminate potential risk scenarios through:

> Monitoring and sensor systems which can detect gases, such as methane and hydrogen.

> Fire detection systems which are industry standard certified, such as NFPA855 or equivalent.

> Ventilation systems which are able to remove flammable gas to prevent a build-up which could result in explosion.

> Temperature and moisture management systems which can maintain the optimum conditions for the batteries.

Thought also needs to be given to water containment in the design of drainage systems. These systems should be able to contain firefighting water on site and isolate it from public water courses and sewers in case of a fire. Once the incident has been safely brought under control, the water will need to be removed and treated. For project developers who are familiar with design guidelines and technical standards, much of this will be straight forward to incorporate

ENERGY GLOBAL SPRING 2024 18

Figure 1 . Global cumulative energy storage installations, 2015 – 2030. Source: BloombergNEF. Note: ‘MENA’ refers to the Middle East and North Africa; ‘RoW’ refers to the rest of the world. ‘Buffer’ represents markets and use cases the BNEF is unable to forecast due to lack of visability.

LOW TO ZER EMISSIONS

ANA Inc. offers a line of eco-friendly equipment that is designed to increase productivity and uptime, control operating costs, improve resale value, and minimize environmental impact.

ANA is a supplier of AIRMAN® generators and air compressors, as well as Hybrid Energy Systems.

We invite you to join ANA, on our

UP TO 20X THE CYCLE LIFE OF LFP BATTERIES

SAFE BATTERY TECHNOLOGY NO THERMAL RUNAWAY

SIMULTANEOUS OUTPUT VOLTAGES

REMOTE ACCESS MONITORING & TRACKING

INDUSTRIAL GRADE INVERTERS

WIDEST TEMPERATURE OPERATING RANGE

THE INDUSTRY’S HIGHEST-QUALITY HYBRID POWER SYSTEMS ANACORP.COM

into project proposals. However, assistance may be required with regard to developing a project in collaboration with local fire services, providing risk assessments and emergency response planning.

Engagement with local fire services

The NFPA and NFCC both provide guidance on designing BESS sites to enable fire service personnel to manage an incident on site effectively. This includes water supply requirements, access arrangements, and observation points. Each site and each fire service is different, making it important that local fire service personnel are involved at an early stage of development so that their requirements can be taken into account in site design. For instance, ensuring that access gates and perimeter roads are sized appropriately for local fire service vehicles.

Injuries that have resulted from BESS fires to date have primarily involved fire service personnel and could probably have been avoided with better knowledge sharing between developer and fire service. For example, the Regional Fire Service that responded to the 2020 battery fire in the UK was unaware of the site’s existence. As part of the engagement process, developers must learn how local fire service personnel assess and monitor fire risk sites within their response area and what information they require to do so.

The NFCC guidance advocates that dialogue between developers and local fire service starts before the submission of a planning application and continues through to operation. At Clearstone Energy, this process of engagement ends in two key shared documents: a risk management plan and emergency response plan. The risk management plan identifies risks, safety systems, and site practicalities for responding to an incident while the emergency response plan details the actions that will be taken in response to an incident, from notification through to clean up and recommissioning.

Local uncertainty is presenting a challenge to all project

There is a lack of communication and co-ordination between the national and local levels when it comes to assessing the safety of BESS.

Local planning officers are often required to make decisions about the suitability of proposed BESS projects, but may

not have the necessary knowledge and expertise to make judgements on safety. Similarly, local fire services may be asked to review developers’ fire safety plans but have not had any experience with a BESS emergency response plan or received training on national guidance.

This situation is further compounded by the fact that communities living near proposed battery storage sites are more likely to find media stories about safety incidents than about the efforts the industry is making to ensure safety. Unfortunately, these incidents are often sensationalised and not always reported accurately.

Resulting in project delays and refusals

As a result, projects across both the UK and the US have been rejected by planners over safety concerns, and uncertainty over safety is causing delays in reviewing other projects. This delay is affecting project financing and the ability to secure construction contractors, leading some developers to withdraw their projects.

Education is key to overcoming these challenges

Developers need to provide planners and fire services with a comprehensive assessment of the risks associated with BESS facilities and assurance that these risks can be managed effectively through technology choices, site design and emergency response plans. The information to do so exists but is often hidden behind NDAs at manufacturers or buried in the evidence files that support appeals against battery projects that local planners have refused.

Clearstone Energy has collaborated with battery safety experts, manufacturers, and fire service personnel to develop a comprehensive risk assessment methodology and a holistic view of how those risks are mitigated by combining technology, site design, and process. This approach is a model for other developers to engage in constructive dialogue with planning officers and fire service personnel when proposing new projects.

However, there is still work to be done. Although there is a significant amount of post-incident assessments and test data available today that focuses on fire propagation between units and explosion characteristics, the potential toxicity of smoke plumes from BESS fires and dispersion areas is not well understood. This area requires further research to draw parallels with existing data on fires involving plastics.

Additionally, not all manufacturers are conducting the levels of testing that fire services are requesting in their assessments of projects.

The industry needs to educate at scale

Developers such as Clearstone Energy are educating planners and fire services, project by project, but the urgent need to scale battery storage capacity to support the energy transition dictates that a faster model is required.

Governments have a major role to play, and there are signs that this is happening. The PNNL report was commissioned by the US Department of Energy to assist local planners in the US with decision-making.3 The UK Government has integrated NFCC Guidance into its National Planning Policy Framework.

ENERGY GLOBAL SPRING 2024 20

Figure 2 . Fire safety certification and testing data should be used to support a planning application. Source: Energy Safety Response Group (ESRG).

In the UK, local fire services are taking on board the guidance from their national council and knowledge is being shared between regions.

The next step is collaboration between developers, manufacturers, EPC contractors, and industry associations to share best practice on safe project design and collaborate on the creation of educational resources for planners, fire services, and communities.

Building confidence

Safety continues to be a significant focus area for tier one battery storage manufacturers. More frequent and extensive testing is demonstrating the robustness of safety systems. There are good standards and guidance that incorporate safety into site design. Alongside increasing collaboration with fire services in the development of projects this should provide confidence to planners, fire services, and communities that battery energy storage projects are safe.

To earn that confidence the industry needs to work together to deliver battery safety best practice across all projects and invest in programmes that increase knowledge and understanding of battery safety among these key stakeholders. Until this happens, reputational issues surrounding battery safety present a significant challenge to delivering the rapid build-out of energy storage capacity required to secure the clean energy transition.

References

1. ‘Global Energy Storage Market to Grow 15-Fold by 2030’, Bloomberg NEF, (12 October 2022). https://about.bnef.com/blog/global-energy-storage-market-to-grow-15-fold-by-2030/

2. ‘Charging Up: UK utility-scale battery storage to surge by 2030, attracting investments of up to $20 billion’, Rystad Energy, (21 April 2023), www.rystadenergy.com/news/charging-up-ukutility-scale-battery-storage-to-surge-by-2030-attracting-investme

3. ‘Energy Storage in Local Zoning Ordinances’, Pacific Northwest National Laboratory (October 2023), www.pnnl.gov/main/publications/external/technical_reports/PNNL-34462.pdf

4. ‘Grid Scale Battery Energy Storage System planning – Guidance for FRS’, National Fire Chiefs Council, (April 2023), https://nfcc.org.uk/wp-content/uploads/2023/10/GridScale-Battery-Energy-Storage-System-planning-Guidance-for-FRS

5. ‘NFPA 855: Standard for the Installation of Stationary Energy Storage’, National Fire Protection Association, (2023), www.nfpa.org/codes-and-standards/8/5/5/ nfpa-855

ENERGY GLOBAL SPRING 2024 21

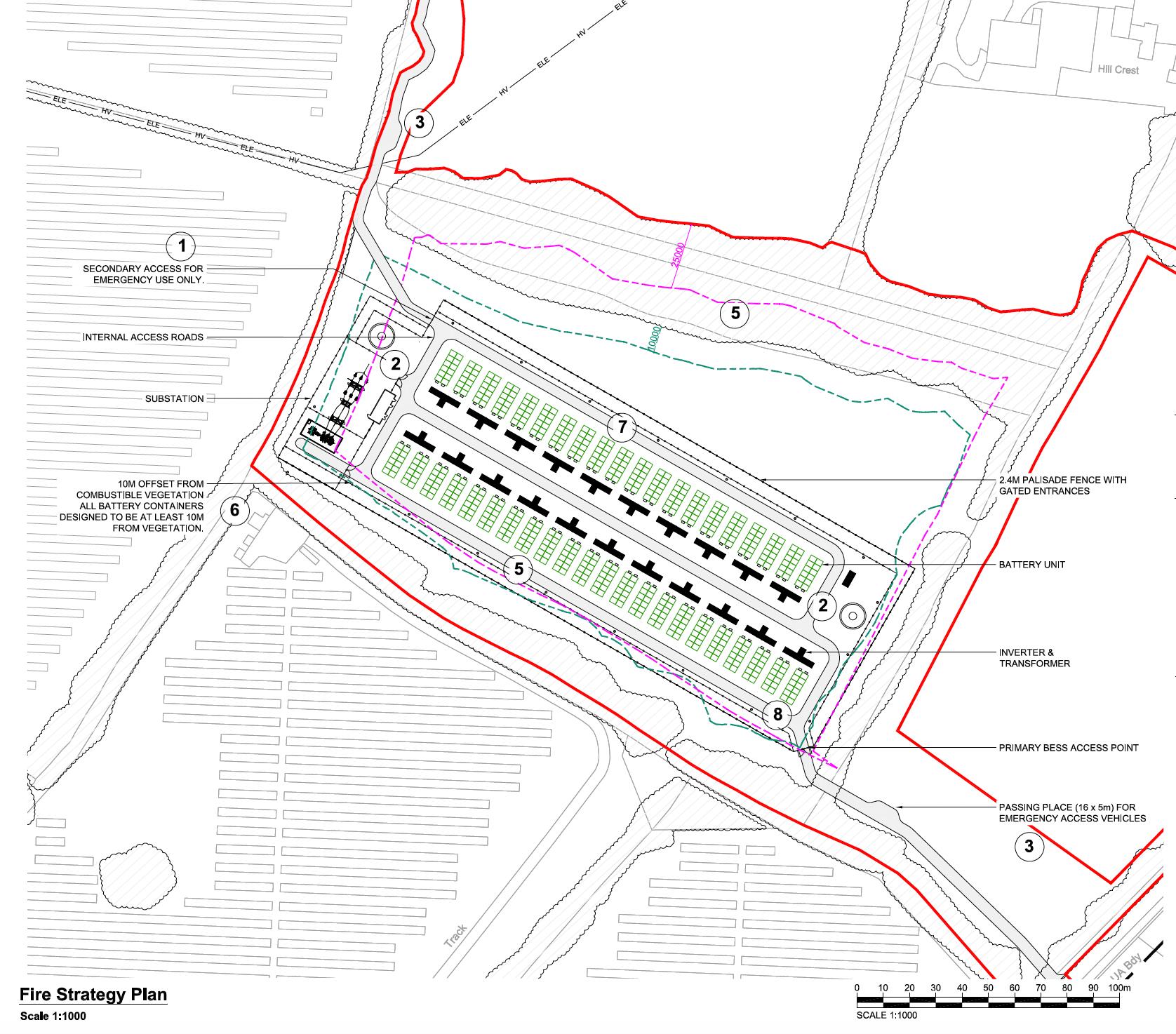

Figure 3 . A fire safety plan can simplify fire service consultation by visually highlighting compliance to local regulations.

Unlocking the power of AI

Charlene Lee, Product Manager and Antonio Notaristefano, Director of Product Management, Fluence, discuss the use of artificial intelligence to help resolve asset management challenges.

22 ENERGY GLOBAL SPRING 2024

The increasing pace of deployment for large scale renewable projects is incredibly encouraging for carbon emissions reduction. While deploying renewables is important, energy storage is becoming increasingly recognised as a critical element for incorporating renewable generation into power systems and achieving deep decarbonisation. In fact, one study by NREL found that a four-hour storage system could reduce renewable curtailment by 24 – 38%.1

However, as more energy storage assets come online, owners and managers are facing an emerging set of common challenges that must be addressed, such as issue identification and prioritisation, maintenance planning, data management, etc. These challenges hamper profitability, increase downtime, and stymie the deployment of new assets.

To mitigate these issues, asset owners and managers find an increased necessity to address them through asset performance management software. This article looks into the challenges and how asset performance management software helps asset owners and managers overcome them, helping spend less time managing data and more time acting on it.

Data overload causes ineffective issue identification and prioritisation

With hundreds of millions of battery cells, the average 1 GW battery-based energy storage system produces 100 times the data points of a conventional 1 GW power generation plant. With data coming in every second, knowing where to look for signs of trouble is effectively impossible. Even if an asset manager did know where to look, close monitoring of a single asset

would not be cost-effective because that would require the work of multiple full-time analysts.

Instead, the status quo has moved on to waiting for SCADA systems to surface alerts, which are lacking in a few key ways:

> The SCADA systems are only triggered when some battery component is malfunctioning, at which point the system could already be experiencing costly loss.

> The SCADA systems offer very little detail into the shape of that loss, and virtually no window into potential future capacity loss from the issue.

> The timing of SCADA alerts makes it difficult for asset managers to diagnose problems as they arise, often finding out precious minutes or hours later, when irreparable damage has already been done.

All of this puts asset managers on their backfoot, monitoring ad-hoc and reactively troubleshooting. Operations and maintenance (O&M) technicians face the same challenge, running from one issue to the next with virtually no time or ability to proactively check the health of their systems.

Making energy storage system maintenance proactive rather than reactive

Asset managers face three top maintenance planning difficulties:

1. Anticipating where and when maintenance will be necessary.

2. Communicating maintenance priorities in time to prevent downtime or costly asset damage.

3. Tracking asset performance before and after performed maintenance to quantify impact.

Relying on SCADA alerts for system maintenance planning forces a reactive stance. Trying to deduce

23

battery component failures before they happen, such as when they are showing above average temperatures for their operating conditions or when their temperatures are rising at an unusual rate, would be time consuming and inaccurate for an analyst looking at SCADA data alone.

Deducing battery component failures needs to happen proactively rather than reactively. Having a granular system performance view without the need for visual rotating inspections allows teams to prioritise maintenance tasks and ultimately prevent costly downtime. Granular data also offers the needed verification to ensure issues are properly resolved after maintenance tasks are complete.

Predictive maintenance capability to overcome challenges

Solution 1: How to leverage predictive maintenance for issue identification and prioritisation

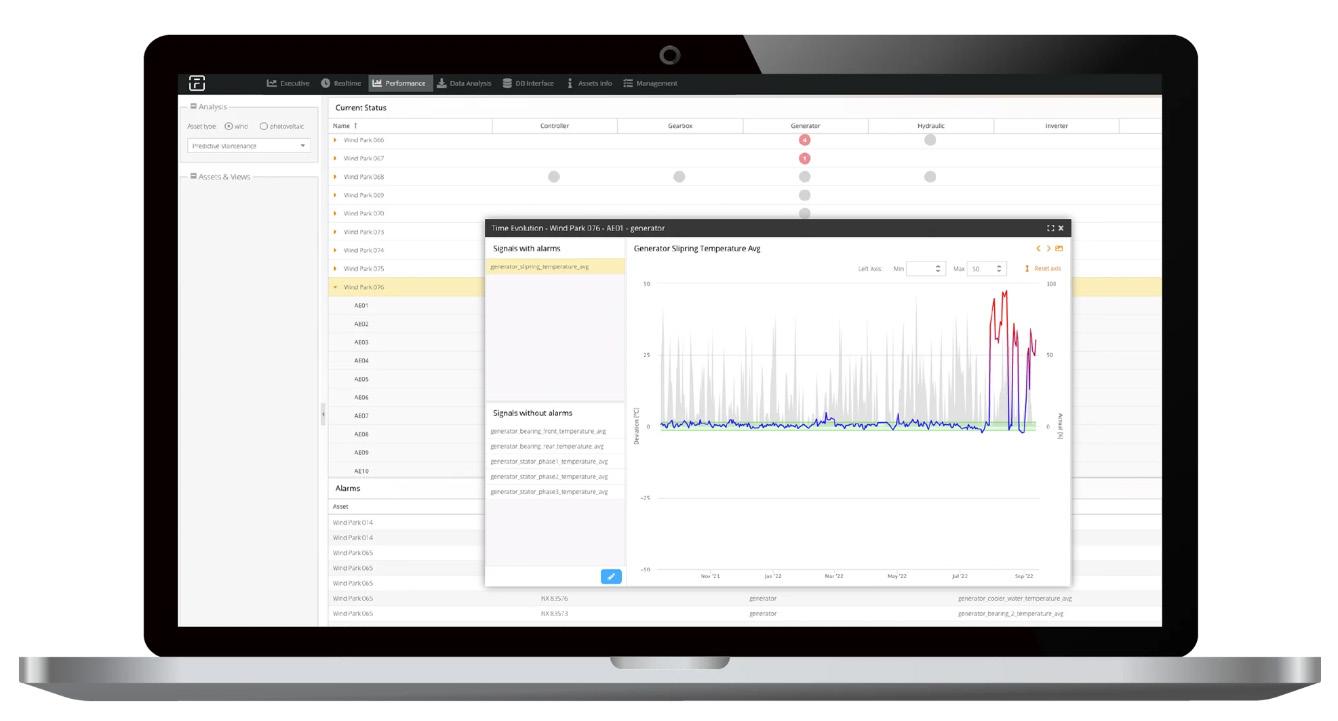

Nispera leverages artificial intelligence (AI) to learn what normal and anomalous battery cell behaviour looks like across a vast range of operating conditions by studying huge amounts of linked SCADA data. It learns when cells are simply running hot because of extenuating circumstances and when their behaviour is a sign of impending failure.

Nispera deploys AI on energy storage systems without adding any hardware to predict what maximum cell temperatures should be under current operating conditions (e.g. level of charge and discharge, cooling system temperatures) and issues an alarm if measured temperatures exceed that value by a certain threshold or trend. These alarms come an average of

three days before a battery outage actually occurs, giving technicians critical insights and enabling them to investigate and resolve issues before the SCADA system triggers an alert.

The software can process far more data, faster and more accurately than analysts, and it works around the clock, every day of the year. The software is manufacturer agnostic, integrating data from any battery original equipment manufacturer (OEM) on the same platform, and scalable enough to monitor a full energy storage portfolio. This results in a round-the-clock sentinel monitoring energy storage system from different manufacturers at various locations, delivering actionable alerts behind a single pane of glass.

Solution 2: How to leverage predictive maintenance capability to switch from reactive to proactive asset management

Nispera’s predictive maintenance tool anticipates issues at a level of granularity that makes proactive communication with on-site teams easy. Instead of asking O&M teams to perform rotating visual inspections of every chiller/HVAC, the software gives asset managers and on-site teams the same view of components that need attention.

Technicians can get to work before downtime occurs, diagnosing and resolving the problem, which could be anything from rack failure to chiller malfunction to unusual environmental factors. When the work is done, Nispera’s data collection makes it easy to ensure the issue is resolved and the system is performing as expected.

Data management

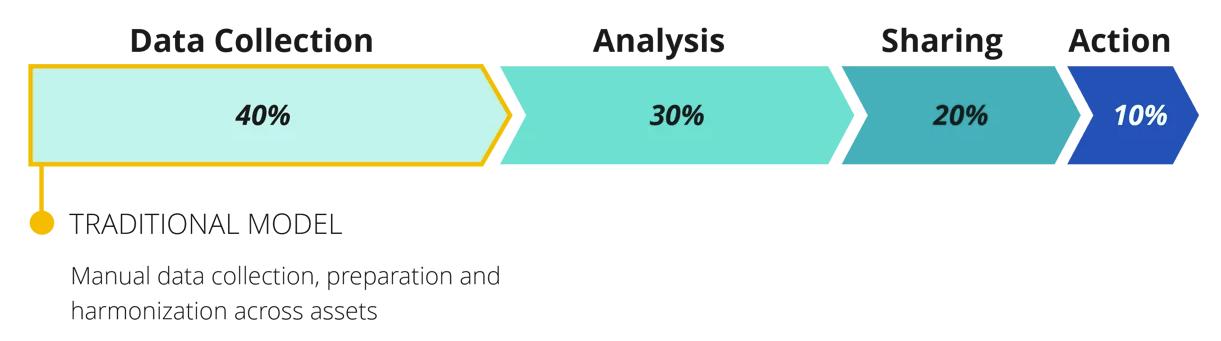

The asset management challenges presented by the ever-growing volume of dispersed data in renewable and storage assets are substantial. Traditional data management strategies simply cannot keep pace with the data intensity required to get optimal performance out of renewable and storage assets (Figure 2).

Even more, fragmentation of data caused by siloed systems is leading asset management teams to spend most of their time manually collecting and harmonising data across assets. This leaves little time for analysing, sharing, and acting upon that data.

In recent years, asset performance management teams have often spent almost half of their time on data collection. It is highly time-consuming and error-prone work for dedicated resources to manually collect, clean, prepare, and harmonise data across assets just so it can be examined in one place. Fluence tends to see almost one-third of teams’ time spent analysing that data, looking for patterns and anomalies that can be acted on to improve asset performance. That leaves very little time for sharing data analysis findings to mobilise action and even less to act on the issues that have been discovered. This is nowhere near enough to make meaningful improvements to asset performance, leaving assets performing sub-optimally.

Figure 1 . Nispera software predictive maintenance interface.

ENERGY GLOBAL SPRING 2024 24

Figure 2 . Traditional time allocation for data management.

Capturing green opportunities

Carbon capture and storage or utilization (CCS/CCU) is a key strategy that businesses can adopt to reduce their CO2 emissions. By selecting the right technologies, pressing climate change mitigation targets can be met while benefitting from new revenue streams.

Sulzer Chemtech offers cost-effective solutions for solvent-based CO2 absorption, which maximize the amount of CO2 captured and minimize the energy consumption. To successfully overcome technical and economic challenges of this capture application, we specifically developed the structured packing MellapakCC™. This packing is currently applied in several leading CCS/CCU facilities worldwide, delivering considerable process advantages.

By partnering with Sulzer Chemtech – a mass transfer specialist with extensive experience in separation technology for carbon capture –businesses can implement tailored solutions that maximize their return on investment (ROI). With highly effective CCS/CCU facilities, decarbonization becomes an undertaking that can enhance sustainability and competitiveness at the same time. For more information: sulzer.com/chemtech

Visit us at ACHEMA in Frankfurt Hall 4 Stand D48

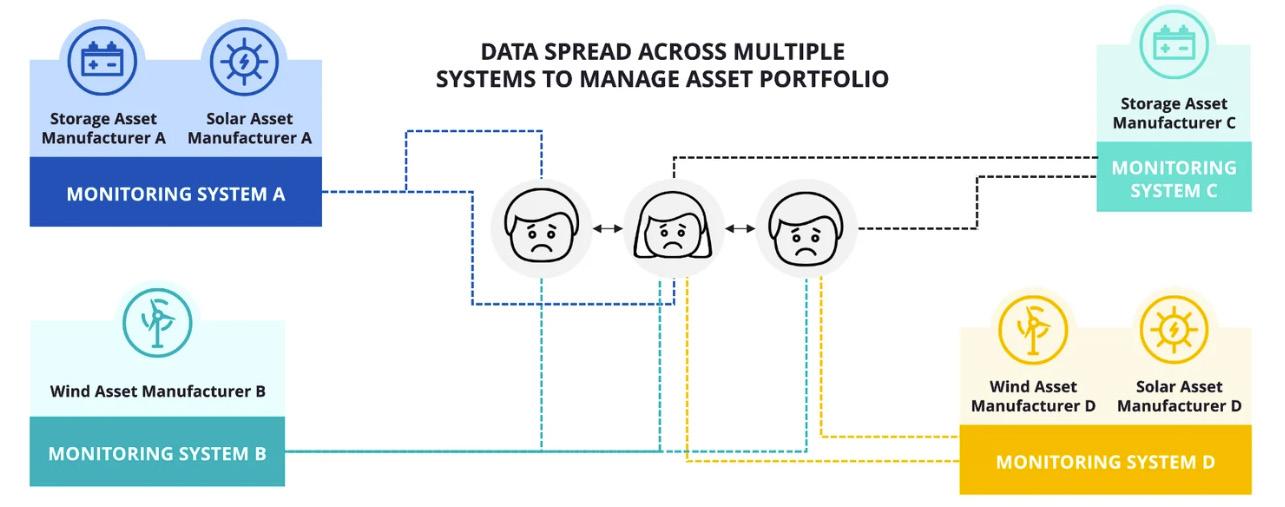

A typical wind turbine produces thousands of data points per minute. 2 For a portfolio of 10 farms and an average of 50 turbines per farm, that can easily translate to millions of data points per minute. Complex storage assets can produce ten-fold that number of data points per minute. This volume is, in part, why the collection, integration, and management of renewables and storage performance data can be so time-consuming. The team members needed to execute that manual work, however, require specialised knowledge and, in turn, are often expensive. As teams look to scale their portfolios of renewables and storage assets, this manual work often means they end up scaling resources linearly with asset size.

Moreover, these scaling portfolios are often increasingly diverse, with a variety of technology types, OEMs, OEM SCADA systems, and O&M service providers involved. When data is spread across solar, wind, hydroelectric, and storage assets, made by different manufacturers and located in different geographies, asset managers end up with data siloed into the SCADA systems set up for each asset, or at best each location. This further adds to the complexity of data coming off of one portfolio’s assets and increases the time and complexity of manually gathering and integrating data across all sites.

Accessing data trends over time requires manual analyses querying large data, which takes time and leaves room for data translation error and increases risk of relying on institutional knowledge. Simply obtaining log-in details for different systems can be cumbersome and time-consuming, let alone finding the relevant data in each system. This fragmentation makes it virtually impossible to get a holistic understanding of portfolio performance, make informed decisions, and operate effectively.

Some asset performance management teams are taking a different route and turning to a centralised platform where data from various SCADA systems can be collated, extracted, and stored. They are leveraging automated, reliable, and actionable analysis that does not drain the time of team members and enables on-site technicians to work proactively.

Data harmonisation capabilities help clear data management hurdles

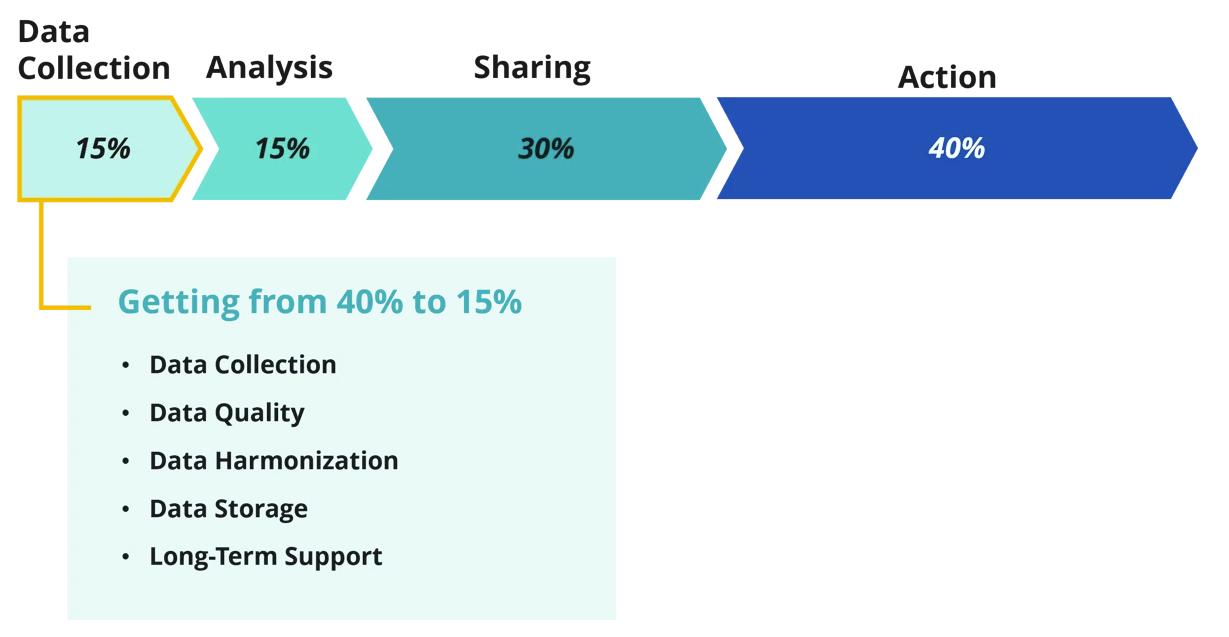

Asset performance management software, such as Nispera, allows asset managers to reduce the amount of time spent on gathering, harmonising, and analysing the data so they can spend more time acting on data insights to grow their portfolios and to drive value across them (Figure 4). The harmonised data is then represented in intuitive dashboards that show real-time and historical, high-level and detailed views of asset and portfolio performance over any specific time period.

Automated data harmonisation

Nispera automates data cleaning and integration across asset types (solar, wind, hydro, and storage), sources, and technology providers. This means asset owners and operators can scale large and diverse portfolios of renewables and storage assets without scaling resources to manage manual data collection and analysis. It also significantly reduces risk of human error in these processes.

Elevated insights

The company’s software brings together both historical data and a steady flow of near real-time data into a single pane of glass, providing historical asset data as far back as commissioning and to-the-minute insights into asset component performance. AI-based modules, such as Predictive Maintenance Alerts,

Figure 3 . Disparate assets and technologies limit scalability.

ENERGY GLOBAL SPRING 2024 26

Figure 4 Improved time allocation for data management.

use both datasets to spotlight anomalous behaviour before it hampers power output.

Optimal asset performance management goes beyond just tracking performance data. By integrating data from multiple external sources, Nispera enables customers to see and automatically analyse deeper performance trends and relate them to financial, market, weather, and O&M insights.

Enhanced cybersecurity

With mounting cybersecurity threats to renewable and storage assets, Nispera incorporates best-in-class cybersecurity practices in data management with secure storage in a European data centre. The product’s API provides a secure path for clients to access their data via third-party applications.

The future of data management in the renewable energy sector is clear: asset managers need a more efficient, secure, and insightful approach to data management across asset portfolios. Nispera’s data harmonisation feature offers asset management teams a way forward.

Providing a centralised platform that collates and organises data from various sources, empowers asset managers and on-site technicians to spend more time on strategic actions and less on wrangling data. With enhanced visibility, configurable dashboards, historical and real-time data, and improved cybersecurity, Nispera not

only simplifies data management, but also significantly enhances the effectiveness of asset management teams.

Rising to the challenge of energy storage needs ahead

The International Energy Agency predicts that 2400 GW of renewable energy will be deployed globally in the next five years, which is equal to the amount deployed in the past 20 years. 3 To be optimally integrated into the grid, all this intermittent renewable energy will require the flexibility of energy storage systems. BloombergNEF estimates that there will be 15 times the amount of energy storage online by the end of 2030 compared to now. 4

This exponential growth has the potential to exacerbate the challenges asset managers are already facing. Tools such as Nispera are key to making the transition smooth, and empowering asset managers to scale up.

References

1. DENHOLM, P., and MAI, T., ‘Timescales of Energy Storage Needed to Reduce Renewable Energy Curtailment: Report Summary’, National Renewable Energy Laboratory, (October 2017), www.nrel.gov/docs/fy18osti/70238.pdf

2. TEGTMEIER, M., ‘Real-Time Wind Turbine Monitoring: Data Challenges, and Rewards’, POWER, (10 July 2020), www.powermag.com/real-time-wind-turbinemonitoring-data-challenges-and-rewards

3. ‘Renewable power’s growth is being turbocharged as countries seek to strengthen energy security’, International Energy Agency, (6 December 2022), www.iea.org/news/renewable-power-s-growth-is-being-turbocharged-ascountries-seek-to-strengthen-energy-security

4. ‘Global Energy Storage Market to Grow 15-Fold by 2030’, BloombergNEF (12 October 2022), https://about.bnef.com/blog/global-energy-storage-marketto-grow-15-fold-by-2030/

EXHIBIT AT CANADA’S NATIONAL ENERGY EVENT June 11-13, 2024 Calgary, Alberta 30,000+ ATTENDEES 500+ EXHIBITING COMPANIES 400+ PRESENTING SPEAKERS 50+ HOURS OF EDUCATION SCAN TO BOOK YOUR STAND globalenergyshow.com

Transmission technology Transmission technology

Peter Sandeberg, Hitachi Energy, Sweden, provides insight into employing voltage sourced converter-based high-voltage direct current for offshore connections.

ENERGY GLOBAL SPRING 2024 28

Figure 1 DolWin 2 offshore platform.

for the energy transition for the energy transition

Motivated by minimising the environmental impact of generating electrical energy, coupled with increasing demand, energy producers continuously search to utilise more of the earth’s natural resources to harvest additional generating power.

While many parts of the world bask in glorious sunshine, other regions experience strong and consistent winds. Wind power turbines successfully exploit these conditions to produce clean and sustainable energy. Given that the higher average offshore wind speeds can result in an energy yield of up to 70% higher than that generated on land, together with the scarcity of available onshore sites, it is no wonder that there is now an increasing number of offshore wind farms being built.

However, as the nearshore sites are being occupied, the further out to sea, the greater the challenge of ensuring the transmission of a stable energy supply to the mainland. This challenge is being met with Hitachi Energy’s voltage sourced converter (VSC)-based high-voltage direct current (HVDC) Light® technology.

Background

Propelled by political initiatives in different regions of the world, governments have set forth ambitious targets with regard to renewable energy generation. In Europe, the ‘Fit for 55’ legislative package and the Repower EU plan introduced by the EU Commission set targets for all its 27 member states. The revised Renewable Energy Directive EU/2023/2413 entered into force on 20 November 2023 raises the EU’s binding target for the share of renewable energy sources to a minimum of 42.5% for 2030 with an aspiration to reach 45%.

The UK’s Net Zero Strategy aims to decarbonise electricity in the country by 2035 by placing low carbon investment as important to achieving net zero. Driven by the increased global demand for electricity, the need to phase out fossil-based generation, and stay on the 1.5˚C pathway, an annual deployment of approximately 1000 GW of renewable power is required between 2023 and 2050.1 Translated into offshore wind, the global installed capacity would need to reach almost 500 GW by 2030 and 2500 GW by 2050.1 This target will require the wind industry to massively invest and increase its capacity.

Such radical changes in the amount and type of electricity generation injected in new nodes in the grid will result in changed power flows both in terms of ratings and routing within and between national grids. This would inevitably lead to persistent grid congestion if not properly addressed. Transmission System Operators (TSO) are making significant investments in new transmission assets to reinforce the existing infrastructure, creating strong electricity transmission grids capable of withstanding the future power system’s dynamics. The energy transition required to meet the targets at the needed speed will lead to a complete redesign of the grids. Some of the challenges

29

that will need to be tackled are complex permitting procedures, lack of skilled labour, local opposition against new mega projects, and access to necessary funding.

As a consequence of these demands, the number of HVDC transmission systems is growing at an unprecedented scale. Over the years, HVDC has proven to be a cost-efficient solution for integrating large scale offshore wind power. When wind farm developers are searching for areas with shallow waters together to intercept better wind profiles, the distance from the onshore connection point to the wind farm sites tends to increase. The combination of high power, long distance, and sometimes weak connection points makes HVDC transmission the perfect fit, providing superior grid support and flexibility while at the same time maintaining low operating losses and high availability.

Besides integrating offshore wind power, HVDC is the technology of choice when connecting different markets over long distances, as well as reinforcing existing AC grids. In addition, in several examples, when transmission corridors are being planned to minimise adverse environmental impacts and preserve nature and landscape, HVDC technology plays a pivotal role by allowing the use of underground transmission cables, even for long distances.

The technical development of the VSC technology, as well as the extruded HVDC cable technology, has been intense over the last 25 years. The increase in power and voltage capability has enabled new applications for VSC-based HVDC systems and future scenarios suggest that VSC technology will develop further to meet new and demanding challenges.

HVDC VSC technology development

It is now more than 25 years since the first pioneering VSC-based HVDC system was installed close to Hitachi Energy’s HVDC unit in Sweden. With its capability to transmit 3 MW at ±10 kV DC, it was the beginning of a new power transmission technology era, enabling, among others, the great expansion of offshore wind generation seen today.

Until now, the development of the VSC technology has largely been focused on reducing losses, footprint, and increasing reliability, power capacity and voltage levels to create a more sustainable and cost-optimised solution. Many features essential to meeting today’s requirements, such as independent active and reactive power control, black start, etc. were available already from the beginning.

Hitachi Energy has developed today’s multi-modular converter (MMC) topology based on experience from earlier designs. The first generation VSC technology was built around a two-level converter using pulse width modulation (PWM) with high switching frequency. The next step was to increase power and voltage ratings by high-current insulated-gate bipolar transistor (IGBTs) in a three-level converter configuration. With the changed topology, the switching frequency could be reduced while at the same time lowering the harmonic content and, consequently, fewer filters.

The third-generation VSC technology was introduced already in 2005 and went back to a two-level converter topology but with an optimised PWM switching pattern. It retained the losses at the same level but reduced the number of IGBTs while still maintaining low harmonic generation. This resulted in a compact design and reduced footprint, making it especially fit for offshore wind applications.

With a design based on cells (modules), each containing half-bridge two-level converters, the cascaded two-level (CTL) converter was introduced in 2010. To further increase DC voltage, power capacity, reliability, and decrease losses and footprint, the CTL was further developed into an MMC (Figure 2). With a rated semiconductor voltage of approximately 5.2 kV, the MMC has smaller voltage steps than the CTL converter, leading to less distortion of the voltage and current. The improved topology enables a decreased switching frequency and an improved output voltage; thus, the converter losses were decreased even further. It was also possible to reduce the footprint both through optimised mechanical design and by utilising bi-mode insulated gate transistors (BIGT), combining the IGBT and the diode functions in the same chip.

Today’s VSC and cable solutions have taken the next step both in voltage and power. It is possible to design HVDC stations able to transfer about 3 GW in bipole configurations at ± 525 kV, with DC current ratings of about 3 kA. These larger systems can be foreseen mainly together with overhead lines. In links with cables, the current is often limited to about 2 kA depending on the conditions of the soil or seabed. These ratings are approaching levels that may impose a major impact on the transmission grid, and all possible aspects regarding grid resilience must be carefully considered. In many parts of the world, these power levels may set an upper limit due to the potentially severe consequences in the unlikely event of a failure leading to an HVDC trip.

Offshore HVDC development and experiences

For more than 20 years, the offshore wind industry has provided flexible, resilient, and sustainable energy. The global offshore wind outlook estimates that 380 GW of offshore wind in 30+ countries will be installed in the next 10 years.2 Driven by political ambitions and commitments, the plans for large scale integration stretch over every continent in the world contributing to the green energy transition.

The world’s first offshore wind connection by HVDC VSC technology was commissioned in 2009 in the German Bight, connecting 400 MW offshore wind to the mainland grid in Germany.3 At that time, the wind farms were connected to the AC collector platform by a 33 kV inter-array cable network. After stepping up the AC voltage to 155kV, the energy was transmitted

ENERGY GLOBAL SPRING 2024 30

Figure 2 . MMC valve structures from Hitachi Energy.

to an HVDC station on a separate platform that converted the AC voltage into ±150 kV DC for further transmission to the mainland grid.

The German ‘hub and spoke’ concept and the setup with the TSO, also responsible for the offshore transmission infrastructure, served its purpose well and created a stable framework for the stakeholders to comply with. On the flip side, it required many AC collector platforms that could be avoided, and in 2019, the world’s first HVDC project, DolWin 5, with wind turbine generators (WTGs) directly connected via the 66 kV collection grid, was awarded. The DolWin 5 project is planned to be in operation by 2024.

While 66 kV inter-array collection grids have become standard today, discussions are ongoing to increase the voltage to 132 kV. This is a natural development step, along with the increased power ratings of the wind turbine generators. From an HVDC perspective, this means that the design has to adapt accordingly, but the assessment is that it will not pose a major challenge. On the contrary, for a given power rating, the number of incoming feeders to the platform will be less.