trade policy brief

Measuring distortions in international markets: the case of below-market finance

May 2021

Government support for industrial producers in the form of below-market finance (loans or equity funding on non-market terms) is significant. This support is relatively large and common in sectors such as aluminium, cement, glass and ceramics, and solar panels, with firms with more than 25% government investment benefitting relatively more. Below-market finance has a number of implications for the design of trade rules, notably in relation to transparency, the scope of subsidy disciplines, and state ownership.

What’s the issue? The support that governments provide to their industrial producers has been a growing source of trade tensions, including amid concerns about unfair competition and excess capacity. Yet unlike support to agricultural producers, the scope and scale of government support in manufacturing remains opaque and poorly documented. This is particularly concerning since a growing body of evidence suggests such support to be harmful for global competition and, potentially, to subsidising countries themselves. Recent OECD studies on government support in the aluminium and semiconductor value chains indicate that much producer support in manufacturing takes the form of below-market finance. Below-market finance covers support instruments that operate through the financial system, whether in the form of debt provided on below-market terms (e.g. preferential interest rates and government loan guarantees) or in the form of below-market equity funding

(e.g. government equity infusions that are provided on non-market terms, or government shareholders tolerating lower ongoing equity returns than private investors would demand). In both cases, this support serves to lower companies’ cost of capital, thereby helping them invest more than they would otherwise or allowing them to tolerate heavier losses.

What the OECD did Most governments do not disclose detailed information about which firms and sectors obtain government support, much less the individual financial transactions underpinning below-market finance. By necessity, the OECD therefore looked at the recipients of support (i.e. industrial firms) rather than providers (i.e. governments). A focus on the recipient firms also enabled work to identify the significant below-market finance channelled through state enterprises acting as intermediaries (e.g. state banks and government guidance funds).

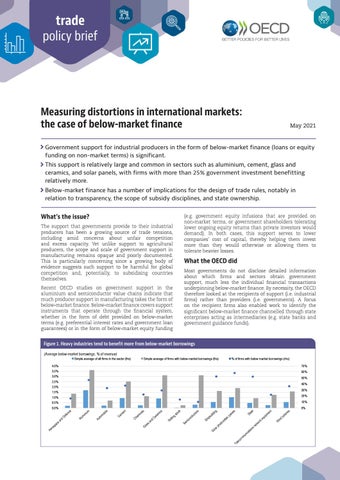

Figure 1. Heavy industries tend to benefit more from below-market borrowings (Average below-market borrowings, % of revenue)

Simple average of all firms in the sector (lhs)

Simple average of firms with below-market borrowings (lhs)

% of firms with below market borrowings (rhs)

4.0%

70%

3.5%

60%

3.0% 2.5% 2.0% 1.5% 1.0%

50% 40% 30% 20%

0.5%

10%

0.0%

0%