6. Retirement Reality Check: Are Your Current Savings Sufficient For Retirement?

10. Enock’s Savings Strategy For Life’s Uncertainties

Story

12. Experts Share Tips on Building a Strong Savings Culture

14. Facts And Figures

16. Pooling Our Way to Prosperity: How Savings Can Power Uganda’s Transformation

20. Picking a Leaf from Countries with High Savings Rate

22. NSSF Awards Top Compliant Businesses in Regional Employer Outreach

Interview

24. The 3M’s That Stand Between You and Financial Independence

28. NSSF Rolls out Financial Literacy and Savings Campaign for Kampala Market Vendors

Personal Finance

29. Building Wealth in Uganda’s Gig Economy News

32. NSSF Hi-Innovator Program Boosts 45 Women-led Businesses with UGX3.3 Billion

Market Insights

34. Economic Drivers and Markets Implications

Regional News

36. Cybersecurity: Morocco, Australia Funds Hacked

38. Kenya’s Pension Assets Quadruple in 10 Years

Personal Finance

39. Nurturing a Savings Culture in Children

41. Making a Voluntary Top-Up to your NSSF Mandatory Saving Scheme

42. Overcoming Financial Challenges During a Career Break: How to Cope in Times of Job Loss

The Case For Increasing Social Security Contributions.

Esteemed Readers,

Across the border to the East, and Southwest, two significant social security reforms were recently implemented.

Rwanda adopted a Presidential Order increasing the rate of contributions for the mandatory scheme – the Rwanda Social Security Board (RSSB) to 12%, and it will rise to 20% in four years. The increase is intended to ensure “a sustainable pension system.”

In Kenya, despite ill-informed opposition from the political class, and a few employers, NSSF Kenya implemented reforms that saw adjustment of the upper-income limit and lower-income limit from KSh 36,000 (approx. USh1m) to KSh 72,000 (approx. USh2million) and KSh 7,000 (approx. Ugx198,000) to KSh 8,000 (approx. USh227,000), respectively.

Workers in Kenya earning KSh 50,000 (approx. USh1.4m) monthly, now contribute KSh 3,000 (approx. Ush85,000) up from KSh 2,160 (approx. Ush61,000), while employees taking home KSh 72,000 (approx. USh2m) have KSh 4,320 (approx. Ush122,000) deducted, up from KSh 2,160 (approx. Ush61,000).

The increase of the rates by both countries addresses the question of adequacy – whether social security contributions made during one’s working life are sufficient to meet their retirement needs.

About 83% of the Fund’s total membership has only USh10m or less. In addition, only 8% have balances of USh 50m or more.

In Uganda, the contributions rate stands at 15% - the employer deducts 5% from the employee’s total gross monthly wage and adds 10% of the total gross monthly wage.

However, inspite of this seemingly sufficient rate, two astounding statistics stand out: about 83% of the Fund’s total membership has only USh10m or less. In addition, only 8% have balances of USh 50m or more. Are we saving enough?

In this issue, we tackle the question of adequacy of savings. In attempting to answer the difficult question of “what is enough?”, we put forward a guiding worksheet that you can navigate to determine what may be considered “enough” savings for your retirement, depending on your current income, age, lifestyle, and retirement you desire.

At a macro level, we spotlight the common thread about countries that have the highest savings rate, and how they got there.

Our analysis raises some uncomfortable questions:

• Do we Ugandans meet the International Labour Organization’s (ILO) recommendation of a replacement ratio of 75%? (Replacement ratio is, in simple terms, the percentage of pre-retirement employment income that is replaced by income in retirement).

• Do the recent reforms that culminated in the current NSSF Act (Cap 230) go far enough?

• Is it time to consider increasing the current contributions rate from 15% to perhaps 20% by voluntary top-up?

Victor Karamagi Editor

Barbra Teddy Arimi Executive Editor

Edwin Rwemigabo Contributor

Victor Karamagi Editor

Carol Beyanga Consulting Editor

Paul Busharizi Contributing Editor

Tito Winyi Design Editor

Christine Kasemiire Copy Editor

John Ssenkeezi Digital Editor

Julius Businge Lead Writer

Stephen Omojong Contributor

Ian Namanya Graphics

Anna Maria Sanyu Contributor

Reality Check: Are Your Current Savings Sufficient For Retirement?

Stephen Omojong Research & Product Development Manager

The foundation of social security is based on the recognition of the vulnerability faced by workers once they are no longer able to earn an income. The International Labor Organization (ILO) conventions bring this out clearly by recommending protection for workers through the social protection floors embodied in the ILO convention 102 and other derived resolutions and principles thereafter. In this article we focus on the adequacy of savings.

This topic is motivated by the observed trends of pension schemes in East Africa increasing contribution rates; Kenya and Rwanda both increased contributions to their man-

datory retirement saving schemes of NSSF and RSSB respectively.

For many people in Uganda, retirement is a foreign concept, due to the large informal sector which many people consider as “Self Employment”. In essence a self employed person does not retire due to age. This is a myth that requires further interrogation. For now however, we will address ourselves to the general expectation that every working person today will retire some day, as long as God blesses them with a long life. If people will retire, then they will need a source of income during retirement to survive on long after the monthly, daily or weekly wages run dry.

The eminence of retirement among other contingencies that stop or reduce a worker’s income is the reason why social security schemes and programs exist world over. While it is easier to come to terms with the fact that retirement will come for everyone lucky enough to live long enough, the question of how well to prepare for that time is less obvious.

For many people in Uganda, retirement is a foreign concept, due to the large informal sector which many people consider as “Self Employment”.

About

661,935

The number of civil servants covered by the Public Service Pension Scheme, out of over 9.9 million working Ugandans.

There are two main strategies people use when planning for their survival in retirement – investing in assets which will give one sufficient cash flows, or maintaining membership to a social security scheme which offers one an assured pension in addition to an income-generating venture. The latter is the least risky retirement option, and is offered by Define Benefit Schemes, however, only one exists in Uganda – the public service pension scheme covering civil servants who are about 661,935 (excluding Uganda People’s Defence Force (UPDF), Internal Security Organization (ISO), External Security Organisation (ESO) and parastatals) out of a total labour force of just over 9.9 million. This implies that for most

working Ugandans, their retirement is hinged entirely on how much they save or invest in long term value preserving assets today.

Therefore, how much must one save to assure themselves of a comfortable retirement? The simple answer to this question is save as much as you can for your retirement. But that’s cliché and rather unhelpful. The correct answer cannot be arrived at without first finding out a few facts about what influences how much one will need in retirement as a way of knowing how much then, one must save now. The amount one will need in retirement depends on what lifestyle they plan to live then. Most models assume that a typical retiree is likely to continue living a life similar to one they lived while they worked but toned down in a few areas.

For example, a retiree may not need to commute from home to the office everyday reducing the expenses related to that. They may choose to live in a retirement friendly neighbourhood e.g. relocating to the country home, and may adjust wardrobe expenses and social networking expenses among other work influenced expense. It can also be assumed that the retiree will have reasonably less dependents to take care of and should have paid off all debts by the time

they retire. Retirees will not need to save for retirement anymore and may be exempt from income tax if they invested in a dedicated retirement asset like a pension account. However, while the retiree is expected to spend less in some areas, they are expected to spend more on others such as health care and other services which may have been accessed free of charge or cheaply courtesy of their employment perks.

The second question relates to whether the retiree plans to survive as a single person or if they plan to retire and live together as a couple. This question is relevant where a couple has both partners working and therefore both are able to contribute towards their retirement income. This implies that as individuals, they would need

For most working Ugandans, their retirement is hinged entirely on how much they save or invest in long term value-preserving assets today.

to each save a little less than people planning to retire as single individuals regardless of the cause.

The third question relates to whether the retiree already has another source of retirement income financed outside the retirement savings e.g. transfer income from children, income from assets already in one’s possession and any such reliable long term income. Possession of such income reduces how much one would need to save now while absence implies a requirement for a higher saving rate.

Other questions relate to time, that is, how long one has to work, when they hope to retire, and therefore how long they can save before they have to rely on the savings for post retirement survival. This affects three variables. First is the amount one will be able to save up in the period they have. Second is the ability for their savings to compound over time if they are saved in an interest earning account (which every long term saver must do to guard against erosion of value due to inflation). Third is how long you will have to survive off the providence of your savings; this is rather subject to natural exogenous factors but can be estimated based on life expectancy and life tables. A long saving period implies a less aggressive saving regime and a long post retire-

ment period requires one to build a stronger and bigger post retirement chest.

After considering the above personal factors, we can take an informed guess about the income a retiree will need and work backwards to deduce how much they need to save now. This method uses the income replacement ratio which is a measure of what percentage of preretirement income you will need to maintain your preretirement lifestyle. For example, if you currently earn a gross income of UGX 3,000,000 and retired tomorrow, a replacement ratio of 75% would imply that your monthly retirement income is Ugx 2,250,000 (75% of 3,000,000).

ILO’s Convention No. 102, sets a minimum standard of 40% replacement of pre-retirement income for pensions. The ILO also emphasizes that the ideal replacement ratio for retirees is 75% or higher to maintain their pre-retirement lifestyle while www.moneyweb.co.za recommends a ratio between 70% and 80%. The logic behind the 75% recommendation is based on the expectation that post-retirement, retirees don’t have to pay income taxes and do not have to continue incurring pension saving deductions. Those two waivers account for 25% of someone’s gross income in

most countries. However, in Uganda, the average income tax rate (PAYE) is 30% whereas the social security savings deductions are 5%. This implies that following the same logic, a replacement ratio of 65% can match one’s preretirement net take-home.

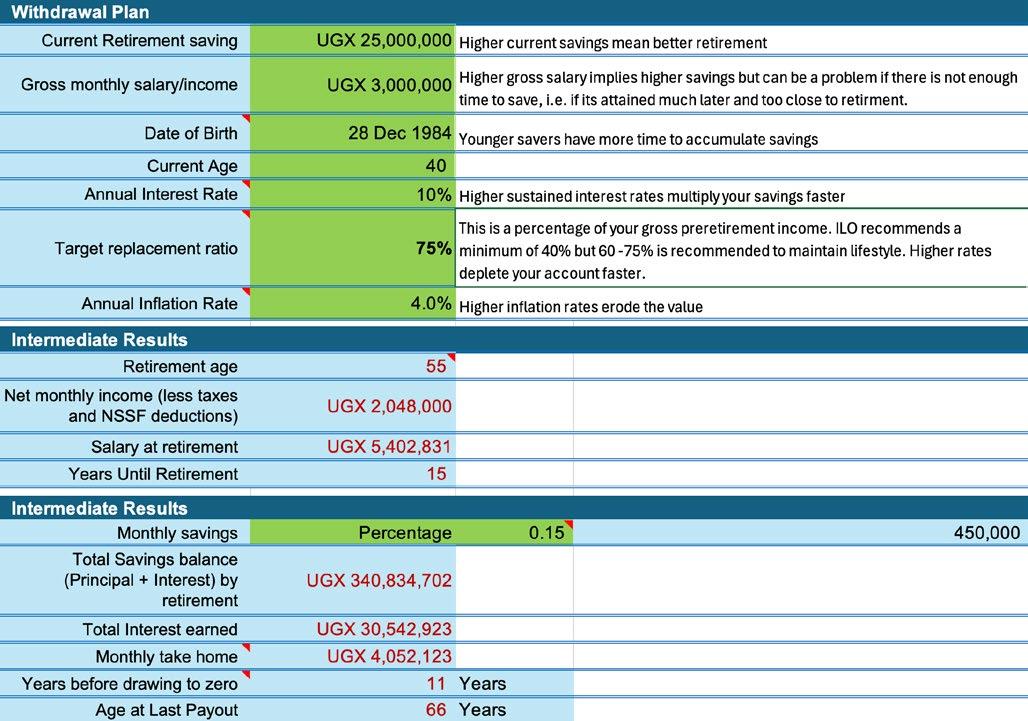

Let us assume a saver hopes to have a preretirement income of Ugx 3,000,000, and their net income is Ugx 2,048,000 after PAYE and NSSF deductions. We are going to assume a replacement ratio that maintains a retiree’s take home which is 68%. With this replacement income in mind, we can use the examples below to visualise the saving target for the different profiles of savers.

Ideal replacement ratio for retirees

International Labour Organisation (ILO)

If you currently earn gross income of UGX 3,000,000 and retired tomorrow, a replacement ratio of 75% would imply that your monthly retirement income is Ugx 2,250,000 (75% of

3,000,000).

When both partners are working, retiring as a couple means that each individual can save a little less than people planning to retire single.

save more for longer periods in high interest earning accounts, they stand a better chance of replacing their preretirement income.

Key notes about the tool

The main determinants of sufficiency of one’s monthly take home in retirement are; how much one has saved, interest to be earned on the savings, age of the saver and therefore how long their money will compound as well as their saving rate. When savers

In this example, the saver has UgX 25 million in their retirement account, they earn a net income of UGX 2.04 million from a gross of UGX 3 million while saving 15% of their gross salary each month. Being 40 years of age implies that they have 15 years of saving and compounding of interest before they can draw from their retirement account. In that period, they will be able to grow their savings from the current 25 million to 340 million thanks to interest compounding and the additional savings.

We note that in spite of the growth in deposits, the preretirement income/salary also increased over time now requiring a higher monthly take home from the savings account in order to maintain the member’s lifestyle at current prices. This strains the savings and can only support the mem-

ber for 11 years until they are 66 years old. When members find themselves in this situation, they would have to sacrifice some elements of their lifestyle to reduce the monthly takehome in order to prolong the draw down period rather than running out of retirement funds early.

Key assumptions

Salary increments are solely based on inflation. Inflation is constant through out the projected period and so is the return on one’s savings. We also assume that savers do not make unscheduled drawing or deposits from or into the accounts respectively. Unscheduled deposits improve the replacement ratio while drawings like midterm withdrawals worsen the post retirement income situation.

Enock’s Savings Strategy For Life’s Uncertainties

Julius Businge Financial Journalist

Enock Ndinywa is living proof that it does not matter how much you earn, setting aside extra savings today can provide peace of mind and protection against the uncertainties of tomorrow. While he already contributes to the National Social Security Fund (NSSF) under Uganda’s mandatory saving scheme with UGX60,000, Enock went a step further by embracing voluntary saving — consistently adding at least UGX10,000 more every month. He sat down with Julius Businge to share his story.

Let’s start with a little bit about who you are. What do you do for a living, what’s your family like, and what brings you fulfillment in your daily work?

My name is Enock Ndinywa. I wear two hats professionally — I work as a driver and also as a teacher at Big Dream Kindergarten and Primary School located in Nakuwade, Bulenga. I’m married to Nassazi Phiona Esther, and together, we are raising four beautiful daughters. What truly brings me joy in my work is the knowledge that I’m making a meaningful difference — whether it’s ensuring people get to their destinations safely or playing a role in shaping young minds in the classroom. That feeling of purpose keeps me going every day.

There are many Ugandans who haven’t started saving seriously yet, let alone thinking about retirement. What inspired you to begin your saving journey with NSSF, and how long ago was that?

I started saving with NSSF a few years back, driven by a simple but powerful motivation — to build a secure and dignified future for myself and my loved ones. As a husband and father of four, I’ve come to understand just how unpredictable life can be. The idea of growing old and being financially dependent on others worried me. I wanted to take responsibility for my future, and saving with NSSF gave me that opportunity. It wasn’t just about retirement — it was about gaining peace of mind today by preparing for tomorrow. I started saving in March 2022 (mandatory), and the savings (UGX60,000) are from my

teaching job. The voluntary saving of UGX10,000 is from the driving job and is done under NSSF SmartLife Flexi.

Many people settle for the mandatory savings and don’t consider contributing more. Why did you decide to go the extra mile and make voluntary contributions in addition to the mandatory ones?

The truth is, I did some thinking and realized that mandatory savings alone wouldn’t be enough — especially for someone with a family of six like mine. Life is expensive, and the older we get, the more financial responsibilities we have. I didn’t want to get to retirement and be caught off guard. Voluntary saving gave me a way to take more control of my financial future. It allows me to increase my savings at a pace I’m

comfortable with — and it gives me a sense of empowerment.

Saving extra hasn’t always been easy, but consistency has been my anchor. I treat voluntary saving as a non-negotiable expense, just like rent or school fees. Once I get my earnings, I save first before I spend on anything else. Over time, it has become a habit. I also try to live within my means and avoid spending on things that aren’t urgent or necessary. The key is discipline, but also keeping your goals in mind. When you know what you’re working toward, it becomes easier to make sacrifices.

Since you began making these extra contributions, have you experienced any personal or financial benefits?

Absolutely. The biggest benefit has been peace of mind. I don’t feel as anxious about the future as I used to. I also feel more in control of my financial life. Saving more has forced me to be intentional with how I budget and spend my money. It has changed how I think about both short and longterm planning. I now view money as a tool for building stability, not just for surviving from month to month.

In what ways do you believe your voluntary savings with NSSF are helping you prepare not just for retirement but for unexpected life events along the way?

Voluntary savings act as a safety cushion. Yes, they’re meant for retirement — but they also represent hope and security in case life throws a curveball. Whether it’s a medical emergency, a school fee shortfall, or a business opportunity, I know I’ve got something growing in the background. It’s like planting a tree. You may not see the fruit immediately, but one day, it will provide shade when you need it most.

Some people think mandatory savings are enough and don’t see the need to go beyond that. What would you tell someone who holds that belief?

future self will be incredibly grateful.

Finally, what advice would you give to young professionals or informal sector workers who haven’t yet begun saving — or who feel that saving more is out of reach for them?

I would say this: Don’t wait until you’re older or earning more to start saving. The best time to begin is now. Even if you’re making a modest income, you can always find a small amount to put aside. It’s not about how much you save at once but how consistent you are. Over time, those small amounts add up. And for informal workers especially, voluntary saving is a powerful tool. It’s flexible, and it helps you build a safety net that you control. If you value your future, start building it now.

It’s often said that saving is easier said than done, especially for people juggling daily expenses. How do you manage to set aside extra money each month for voluntary saving? Are there any habits or disciplines that help you stay consistent?

I would tell them, respectfully, that mandatory savings are only the starting point. They are not a full solution. If you want to live comfortably later in life — and avoid becoming a financial burden to your children or relatives — you have to take extra steps. Even if you start small, those small voluntary top-ups compound over time. The earlier and more consistently you do it, the more prepared you’ll be when the storms of life come. You may not realize it now, but your

The key is discipline, but also keeping your goals in mind. When you know what you are working towards, it becomes easier to make sacrifices.

Enock Ndinywa Driver and Teacher

Experts Share Tips on Building a Strong Savings Culture

Industry experts weigh in on the best time to start saving, practical strategies for saving on a low income, and the essential tools that can make the process easier

Julius Businge Financial Journalist

Rehema Kahunde, a research analyst at Makerere University’s Economic Policy Research Centre (EPRC), begins her day with two things in mind — discipline and purpose. For her, saving money isn’t an abstract financial goal; it’s a way of life rooted in intention.

“Before people can start saving, they need to understand why saving is essential,” she explains. “Financial literacy and awareness play a crucial role in shaping the right mindset towards savings.”

Her approach is simple yet powerful: set clear goals and start small. “Even saving just Shs2,000 or Shs5,000 a day or week can go a long way,” she says, adding that consistency is more important than the amount. Kahunde saves for a range of life goals

Even saving just Shs2,000 or Shs5,000 a day or week

can go a long way

— from future business investments to emergencies — and she urges others to do the same.

She is also a member of a community savings group that takes a creative approach to accountability and discipline, using a mobile money line with multiple custodians to ensure transparency and long-term commitment. Kahunde strongly believes in diversifying income and embracing mobile savings tools such as MoKash. “Platforms like MoKash simplify the pro-

cess and help people save automatically, which is especially helpful for people with spending temptations,” she adds.

Tools of the trade

Uganda’s financial ecosystem offers a variety of saving tools that cater to low and middle-income earners. These include mobile money platforms like MTN Mobile Money and Airtel Money, which allow users to save, send, and withdraw money at their convenience. Community-based models such as Village Savings and Loan Associations (VSLAs) and Savings and Credit Cooperative Organizations (SACCOs) offer peer support, small loans, and a sense of collective accountability.

Formal banking institutions provide savings accounts with flexible plans and low minimum balances. Products like the NSSF SmartLife plan, a voluntary savings scheme by the National Social Security Fund, are tailored for short to medium-term goals. The SmartLife plan allows individuals to contribute in small amounts and grow their funds over time through investment.

For those with more financial knowledge, unit trusts, government bonds, and Treasury Bills offer investment options with varying risk and return profiles.

These tools provide savers with the opportunity to grow their wealth while minimizing risk through diversification. Fixed deposit accounts, available in banks and microfinance institutions, also offer a safe way to earn interest over a set period, encouraging longer-term saving.

Meanwhile, behind Uganda’s growing savings infrastructure is a robust

When saving, consistency is more important than the amount.

Set clear goals and start small, consistency is more important than the amount.

regulatory foundation laid by the Uganda Retirement Benefits Regulatory Authority Act, 2011.

This law, enforced by the Uganda Retirement Benefits Regulatory Authority (URBRA), introduced reforms to make retirement saving more accessible and flexible. One such reform is the legalization of voluntary retirement benefits schemes, which enable individuals — including informal sector workers — to save small amounts, even as low as UGX2,000 per day.

The law also provides for the portability of benefits, ensuring that savings are not lost when one changes jobs or schemes. Furthermore, trustees can tailor benefits to the needs of savers, including income drawdowns and medical cover, making retirement schemes more relevant to Ugandans.

According to Daisy Lynda Nabakooza, Chief Manager of Supervision and Market Conduct at URBRA, the Authority actively works with Parliamentarians and universities to promote early adoption of saving habits.

“We emphasize financial education and awareness as core elements of policy,” she explains.

URBRA also recognizes the importance of digitization and flexible policies to support low-income earners. As mobile phone and internet penetration rise, regulatory frameworks are being designed to support digital savings products.

Nabakooza adds that government incentives and transparency around

payouts can enhance trust and encourage more people to save. URBRA is also building frameworks around cybersecurity and technology supervision under the National Payment System to ensure that funds are securely transferred and protected.

Recent research supports these efforts. The FinScope Uganda 2023 Survey, conducted by the Bank of Uganda and partners, reveals that while 60% of Ugandans do save, most do so irregularly. Only 14% save for emergencies. Financial literacy, low income, and high cost of living remain major barriers. Women tend to rely more on informal savings groups but often face additional economic pressures that limit their capacity to save.

On the global front, the Organization for Economic Cooperation and Development (OECD) Pensions Outlook 2020 stresses the importance of early and increased personal savings, especially in today’s dynamic labor markets. It recommends voluntary savings schemes and consistent contributions as a path to financial security in old age.

“Saving more and saving earlier can significantly improve retirement income adequacy,” the report reads in part.

The bigger picture

The benefits of saving extend far beyond the individual. At the micro level, savings provide a safety net during emergencies, help people achieve life goals, and reduce reliance on debt.

Saving needs a purpose or goal, which could be education, housing, starting an agro-business, or buying a dream car, and must be tied to a timeline.

Dr. Thaddeus Musoke Nagenda Chairman, KACITA

At the macro level, higher national savings contribute to economic growth by increasing the capital available for investment, reducing poverty, and boosting financial stability.

Even in tough economic times, experts say, the government can accelerate the saving culture by investing in financial literacy, supporting digital savings infrastructure, providing tax incentives, and ensuring that saving is safe, transparent, and rewarding.

As Kahunde puts it, “Saving is not just a financial decision — it’s a mindset. With the right tools, policies, and awareness, every Ugandan can build a future worth looking forward to.”

You are likely to live much longer after retirement, research shows that you can live for an extra 18 to 20 additional years. This means your current savings or investments may not be enough to sustain you through this period. Start saving early and explore individual voluntary savings options in addition to your employerbased plan. If possible, consider matching your employer’s contributions to your mandatory savings to maximise the power of compound interest.

Geoffrey Sajjabi NSSF Chief Commercial Officer

Rehema Kahunde Research analyst at Makerere University’s Economic Policy Research Centre (EPRC)

ASSETS UNDER MANAGEMENT, APRIL 2025

Over 25 Trillion Facts & figures

UGX 11.5 Billion NSSF SMARTLIFE FLEXI CONTRIBUTIONS, APRIL 2025

NSSF ASSET ALLOCATION, MARCH 2025

The National Social Security Fund (NSSF) Uganda is a multi-trillion shillings Fund mandated by the Government through the NSSF Act (Cap 230) to provide social security services to all eligible employees in Uganda. It is a contributory scheme funded by contributions from employees and employers of 5% and 10%, respectively, of the employee’s gross monthly wage.

The Fund is a secure, innovative, and dynamic social security provider that guarantees safety, security, and a return on members’ savings of at least 2% above the 10-year inflation average.

Our Vision

To be the Social Security Provider of choice.

Our Mission

To be a relevant partner to our members through continuous innovation in the provision of social security.

Our Purpose

To make lives better by passionately dedicating ourselves to making saving a way of life, to enable more and more people improve their wellbeing.

3,660.12 28.2843 2.5835 1.3884 5YRS 10YRS 15YRS

Pooling Our Way to Prosperity: How Savings Can Power Uganda’s Transformation

Paul Busharizi Financial Journalist

Development is never gifted—it is earned.

The world’s most prosperous nations got there not by leaning on foreign aid or donor support, but by mastering the art of selfreliance. At the heart of this self-reliance lies a powerful tool: the ability to pool and mobilize domestic savings.

Uganda, now deep into its third National Development Plan (NDP III), must pay closer attention to this lesson if it is to transform from a low-income country into a modern, inclusive economy.

The NDP III, launched in 2020, seeks to raise household incomes, promote sustainable industrialization, enhance value addition in agriculture, invest in human capital, and deepen the financial sector. These objectives are noble and necessary and requires long-term financing anchored in domestic savings. And there is no better symbol of this possibility than the National Social Security Fund (NSSF).

Today, the NSSF manages over UGX 20 trillion in assets, pooled from the monthly savings of over a million Ugandans. These savings are not idle.

An image of the Kampala Flyover in Uganda. Domestic savings, when pooled and wisely invested, are not just a financial instrument—they are a nation-building tool.

Vendors review the Smartlife Flexi product during a market activation in Kampala recently.

Photo by UNRA

The 2022 amendment to the NSSF Act, which now allows for voluntary contributions from self-employed and informal workers, is a game-changer. If fully implemented and embraced, it could unlock an entirely new frontier of domestic capital.

They are deployed in government securities, equities, and real estate— supporting everything from infrastructure development to macroeconomic stability. In fact, with UGX 11 trillion invested in government paper, the NSSF is arguably the biggest domestic enabler of public investment and inflation control in the country. This stabilizing effect is rarely applauded but is quietly foundational to economic growth.

But NSSF alone cannot bear the weight of Uganda’s transformation.

Pooled Savings fuel economic development

Other countries show us how the power of pooled savings can be expanded and directed to national priorities. In Canada, the Canada Pension Plan Investment Board (CPPIB) manages over $400 billion and actively invests in infrastructure, energy, and global equities. This long-term capital is used to build bridges, hospitals, and clean energy projects—precisely the kind of investments Uganda needs to meet the NDP’s infrastructure and industrialization goals. NSSF’s own real estate projects at Lubowa and Temangalo, which will soon inject thousands of housing units into the market, are a small but promising example of what can be done.

India presents another model, albeit from the grassroots. There, self-help groups (SHGs), often made up of ru-

ral women, pool their tiny savings to create lending cooperatives that support small businesses and farming. Uganda’s SACCOs and Emyooga initiatives mirror this approach but lack the scale, structure, and integration into broader development plans. If better managed and supported, these community-level savings pools could inject much-needed capital into Uganda’s agro-industrial transformation.

Then there’s Ethiopia, which offered diaspora bonds to fund its Grand Renaissance Dam. Patriotic pride met financial innovation, resulting in a unique model for nation-building. Uganda’s diaspora—educated, patriotic, and relatively wealthy—remains an untapped resource. A structured Diaspora Investment Fund could mobilize billions for key national projects in housing, tourism, and renewable energy.

Kenya’s experience with mutual funds and money market instruments also offers valuable insights. With proper regulatory support, retail investors can pool savings into investment vehicles that offer attractive returns and support national development. This model is critical to deepening Uganda’s capital markets and widening financial inclusion, especially among the growing middle class and informal sector workers.

India presents another model, albeit from the grassroots. There, selfhelp groups (SHGs), often made up of rural women, pool their tiny savings to create lending cooperatives that support small businesses and farming. Uganda’s SACCOs and Emyooga initiatives mirror this approach but lack the scale, structure, and integration into broader development plans. If better managed and supported, these community-level savings pools could inject muchneeded capital into Uganda’s agro-industrial transformation.”

Photo by Bakerjarvis, dreamstime

Canada Pension Plan Investment Board (CPPIB) manages over $400 billion and actively invests in infrastructure, energy, and global equities.

Making a case for Uganda

One cannot ignore the gold standard: Norway. Its sovereign wealth fund, built from oil revenues, now manages more than $1.5 trillion and supports the national budget. Uganda’s own Petroleum Fund, if safeguarded from political interference and invested prudently, could play a similar role—ensuring that oil wealth benefits not just this generation but those to come.

The lesson from all these examples is simple: aggregation is power. When people come together to save and invest, they do more than build personal wealth—they create the financial bedrock of national progress. NSSF has already shown that Ugandans can save. The next step is to expand this culture beyond the formal sector.

The 2022 amendment to the NSSF Act, which now allows for voluntary contributions from self-employed and informal workers, is a game-changer. If fully implemented and embraced,

it could unlock an entirely new frontier of domestic capital.

But we must also be sober. Saving alone is not enough. The true test lies in how those savings are deployed. Poorly executed projects and misallocated capital will do little to improve livelihoods. Human development, as measured by the UN’s human Development Index (HDI), depends on how effectively a country invests in health, education, and basic services. Of the high-saving African countries, only Mauritius and Singapore have translated savings into consistently high quality of life for their citizens. Execution matters.

Uganda’s savings-to-GDP ratio

Uganda’s savings-to-GDP ratio remains under 10 percent, a far cry from the 25 percent threshold that economists like NSSF CEO Patrick Ayota argue is necessary for sustained development. Countries like Cambodia, with 57 percent, or Norway and Singapore, both above 40 percent, have shown what disciplined savings and good governance can do. Even in Africa, countries like Algeria and Botswana, powered by natural resource revenues and effective sovereign funds, lead the continent in this metric.

So while the path ahead is long, the blueprint is clear. Domestic savings,

when pooled and wisely invested, are not just a financial instrument—they are a nation-building tool. Uganda’s NDP III provides the vision. The NSSF and other emerging savings mechanisms provide the foundation. What remains is the political will, institutional discipline, and public trust to convert these pooled funds into lasting transformation.

Ugandans are already showing they can save. The question now is whether we can convert that discipline into national destiny. The real development dividend will not come from handouts or external loans, but from the collective sweat of our brows— mobilized, managed, and invested in a future we build for ourselves.

These countries have achieved high savings rates through various strategies and economic structures as shared below:

• Economic Growth: This growth has increased national income, enabling higher savings.

• Foreign Direct Investment (FDI): The country has attracted significant FDI, contributing to capital accumulation and national savings.

• Oil and Gas Revenues: Brunei’s economy is heavily reliant on its extensive oil and gas reserves. The substantial income from hydrocarbon exports has led to high national savings.

• Sovereign Wealth Fund: The Brunei Investment Agency manages surplus revenues, investing them to ensure long-term financial stability and wealth preservation.

3. Norway

• Oil Wealth Management: Norway has effectively managed its oil revenues by establishing the Government Pension Fund Global, one of the world’s largest sovereign wealth funds, to save and invest surplus income for future generations.

• Fiscal Responsibility: Prudent fiscal policies and a strong emphasis on social welfare have contributed to substantial public savings.

4. Algeria

• Hydrocarbon Exports: Algeria’s economy benefits significantly from oil and natural gas exports, which constitute a major portion of its GDP. The revenues from these exports have been a primary source of national savings.

• Public Investment: The government has directed a portion of its resource revenues into public investment programs, contributing to the national savings rate.

5. Singapore

• Economic Diversification: Singapore has developed a highly diversified and export-oriented economy, excelling in finance, manufacturing, and services. This diversification has led to substantial income and savings.

• Central Provident Fund (CPF): A mandatory savings scheme requiring contributions from both employers and employees has significantly boosted national savings.

These countries have leveraged their unique economic advantages, such as natural resource wealth or strategic economic policies, to achieve high gross savings rates.

1. Cambodia

2. Brunei

NSSF Awards Top Compliant Businesses in Regional Employer Outreach

Christine Kasemiire Public Relations Officer

In March, the National Social Security Fund (NSSF) in a concerted effort to enhance compliance and deepen retirement planning awareness, conducted a nationwide employer engagement tour. Over 1,500 employers across three regions: Fort Portal (Western Region), Mbale (Eastern Region), and Arua (West Nile Region) participated.

The Regional CEO Employer Meetings are part of NSSF’s deliberate efforts to build strong relationships with employers, ensure transparency, and promote a savings culture among Ugandans.

Eastern Region Contributions on the rise

NSSF Managing Director Patrick M. Ayota commended the Eastern Region for its contribution growth, rising by 35.8% from UGX 145.2 billion in FY 2022/23 to UGX 197.2 billion in FY 2023/24. The number

of active contributing employers also jumped from 4,441 to 5,696 in the same period.

Ayota attributed this sustained growth to increased stakeholder engagement and better understanding among employees about the role of social security in long-term financial planning.

A Call for Voluntary Saving and Compliance

Echoing the call for proactive planning, NSSF Chief Commercial Officer Geoffrey Sajjabi reminded employers that non-compliance with the NSSF Act is a criminal offence.

He also encouraged employees to top up their savings through voluntary contributions.

TOP 30 MOST COMPLIANT COMPANIES FROM EACH REGION

NORTHERN REGION

• Mentor Secondary School

• Path Ministries International

• Capable International

• Kitgum Cooperative Savings and Credit Society

• Village of Hope Uganda

• Uthuman Mixed Primary School

• St James Secondary School

• St Peter’s High School Hoima

• West Nile Regional Civil Society Network

• Arua Diocese Procure

EASTERN REGION

• Nile Breweries Limited

• Madhvani Group Limited

• Tororo Cement Ind.

• Salem Brotherhood

• Hima Cement Limited

• Kawacom (u) Ltd

• Local Partner health Services Karamoja (ANECCA LPHS-K)

• Soroti University

• Village Enterprise Fund

• Mountain Harvest Smc Ltd

“If your employer saves 10% for you, why not match it with your own 10%?” Sajjabi said.

“NSSF savings alone may not be enough. Retirement can be long, and poverty in old age is hard to manage.”

This message resonated with many attendees, as large crowds showed keen interest in SmartLife Flexi, NSSF’s voluntary savings product, with numerous inquiries made about registration and contributions.

Recognizing top Compliant Companies

In a show of appreciation, NSSF awarded the top 30 most compliant companies from each region, celebrating their dedication to transparency and timely contributions.

WESTERN REGION

• Agri Evolve Uganda Ltd

• Rwenzori Commodities Ltd (Buzirasagama)

• Amos Dairies Ltd

• Karoli Lwanga Nyakibale Hospital

• Opul Sango Bay Ltd

• Rakai Health Sciences Program

• Kabale University

• Lyamujungu Co-Operative Financial Service

• The Peace Centre Uganda

• Ibanda Hospital

NSSF Staff led by Patrick Ayota and top NSSF compliant businesses in West Nile region pose for a photograph.

Interview: The 3M’s That Stand Between You and Financial Independence

Public Relations Officer

As Uganda’s life expectancy rises and informal earnings remain the norm, the conversation around saving for the future is now more relevant. In this insightful interview, Joseph Lutwama, Director of Programmes at Financial Sector Deepening Uganda (FSD Uganda), unpacks the evolving savings landscape, and why boosting earning capacity could unlock a dignified retirement for Ugandans.

1. Tell us a bit about yourself and what you do?

My name is Joseph Lutwama and I am the Director of Programmes at Financial Sector Deepening Uganda. Financial Sector Deepening Uganda is a non-profit company limited by guarantee, it is fully funded by external donors, the Gates Foundation, Mastercard Foundation and the Eu-

ropean Union. Our focus is on making financial markets work for the underserved and unserved segments of Uganda. We mainly work with the private sector especially financial institutions and financial sector players and public sector to address the market imperfections that hinder service delivery to those segments. We work with government to ensure that there is an enabling environment to facilitate the delivery of quality services to the underserved population.

2. What is the savings trend of Ugandans today, in comparison to the past, are more Ugandans saving or less?

FSDU sponsors a nation-wide household survey every other four years, and we track the demand for financial services at household level. The last survey we did was in 2023 and the findings from that study showed us that there has been a slight increase in the number of Ugandans who are saving. In 2018, when it was last carried out, the proportion of Ugandans that were saving was 54% and in

2023, that had gone up to 60%. So you could say a substantial number of Ugandans are saving. It means that out of every 10 adult-aged Ugandans (16 years and above), six are saving.

3. That is good news, and how much on average are Ugandans saving?

On average, people are saving roughly under 300,000 annually, but that is for all income classes. When you break it down further, you find that majority of Ugandans, 80% of adult Ugandans are saving less than 250,000 per year. And when you analyze it even further, six out of 10 Ugandans actually save less than 150,000. What that essentially means is that their savings are not for purposes of earning return, most of the savings are to be able to cater for unexpected or even expected expenses. It is also worth noting that most Ugandans save before consumption, meaning that whatever money they save is for a specific purpose. They don’t save after consumption, because someone who saves after consumption has disposable income which they can afford to put away for a long time. Most of them have little savings, they cannot afford to put it in the bank because

Percentage of Ugandans saving in 2023

Boosting earning capacity could unlock a dignified retirement for Ugandans.

Christine Kasemiire

If you are earning UGX200,000 before your retirement, you should be able to earn at least UGX150,000 in retirement” “

Joseph Lutwama Director of Programmes at the Financial Sector Deepening Uganda

5. What do you make of those insights, why is this so?

7. Could you please elaborate on the 3Ms?

300,000

their day to day needs far exceed the money they have put aside and the limitation of accessibility and bank charges. Meaning that at any one point in time, that money will have a use.

4. The last part of your response ushers us into the next question. What did you discover are the common saving/investment vehicles that Ugandans are using?

Most Ugandans are saving informally, they are saving at home. They keep their money under the pillow. There is also a substantial number of people who keep their money on the mobile phone. However, the number of people who are keeping money at home has more than doubled. In 2018 this number was at 27%, and in 2023 that had grown to 44%. Those saving with the banks have also increased. They have slightly increased from 11% in 2018 to 15% in 2023.

There is still a lot of challenge in saving formally due to a wide range of factors. The most predominant of all is the low levels of income and the high level of informality of Ugandan economic activity, which makes it very difficult for someone to consistently save. Because their income is not regular both in terms of payment and amounts, they cannot follow a consistent pattern of saving. So that, coupled with low levels of financial literacy (your ability to make money, manage it and multiply it), make it difficult to save formally, because saving formally requires a consistent income, some level of discipline, which is not expected informally.

6. What then is the solution for Ugandans, majority of who are low income earners, to grow their savings?

There is a phenomenon I call the 3Ms. The First M stands for making money; that means that you need to work currently to make enough money. Secondly, you need to know how to manage that money ie to get the discipline of saving, budgeting, allocating it to different investment opportunities and lastly, multiplying it which is an outcome of the investments that you have made. You need to be able to juggle and master those three, if you are going to have a fulfilling life and retirement.

To make money, the ultimate solution is for low-income earners to engage in economically viable and scalable economic activity to curb the uncertainty around their economic livelihood. If they have been in subsistence farming, they need to get into commercial, something similar to what the Parish Development Model is trying to do, giving them seeds, extension services, assets that they can work with, skills to then move away from unpredictable, uncertain economic activity to more commercial system, where you are connected to markets. You know that if I take out a loan, it alone will help me expand. I will earn this much money, and that same business will be able to pay off my loan.

8. And the second M?

Managing money and this ties in with the third M, multiplying money. For starters, everyone has to save. Whether you are saving under the pillow or whatever it is, you have to save. The issue is where to save. It makes no sense to put your money in the formal financial system if one, you have little money, and it is irregular. Formal financial institutions require you to consistently invest a certain amount of money regularly for you to be able to earn something, meaning that for Ugandans who are in the low-income brackets, the community-based savings are still the most preferable because they are more flexible to suit their needs. It is not until they have UGX

The amount of money an average Ugandan saves annually

Low-income earners need to engage in economically viable and scalable economic activity to curb the uncertainty around their economic livelihood.

68.5 yrs

The longer you live, the more challenging it becomes. The quality of your retirement is really based on the quality of your work life. For you to have fairly decent income to sustain you through your retirement, you need to have developed a solid asset base that can continually generate income in your retirement. “

grown to a certain level where they are engaged in commercial activity with decent, regular, consistent incomes, that they then graduate to the formal financial system which includes unit trusts, treasury bills and bonds, equities among others.

9. Uganda’s life expectancy rates have been steadily increasing over the years, and according to the 2024 Census, it is currently at 68.5 years. What does this mean for the population with regards to saving and a decent retirement?

The longer you live, the more challenging it becomes. The quality of your retirement is really based on the quality of your work life. For you to have fairly decent income to sustain you through your retirement, you need to have developed a solid asset base that can continually generate income in your retirement. This could be land, rentals, investments etc. Now for that to happen, you must have worked hard so there’s no silver bullet. The rule of thumb is you should be able to earn at least 75% of the income that you were earn-

ing at the time of your retirement. So, for instance, if you are earning UGX200,000 at the time of your retirement, you should at least be able to earn UGX150,000 in retirement, but remember, you are not working, so it’s the asset you build that is paying for you. Your assets should have the capacity of generating at least 75%, meaning that there is no shortcut, whichever you look at it, you need to increase your earning capacity.

10. Regionally, pension/retirement funds have increased their mandatory member contributions. Do you believe this is the way to go?

There is nothing wrong with increasing your savings, because we all have to grow, but it must be proportionate to your capacity. It will not make sense if your earning capacity has not changed. If I am still informal with inconsistent incomes, in fact it makes it difficult because you are taking away what can solve my problems today and yet even the money you are keeping will not be of much value at retirement.

The quality of your retirement is based on the quality of your work life.

NSSF Rolls out Financial Literacy and Savings Campaign for Kampala Market Vendors

Christine

The National Social Security Fund (NSSF) in February rolled out a three-month campaign to promote financial literacy and foster a savings culture among vendors in Kampala’s government markets.

Through this effort, NSSF aims to enrol informal sector workers into its recently launched Smartlife Flexi Voluntary Savings Plan, ensuring financial security among market vendors.

Speaking at the launch event held at St. Balikuddembe (Owino) Market in Kampala which hosts about 40,000 vendors, Rebekah Kabugo-Mugisha, NSSF’s Senior Manager for Partnerships and Business Development said that the initiative aims to integrate market vendors into the social security system, ensuring they have savings to address their short and medium-term needs.

“Currently, NSSF has about 2.3million members majority representing the formal sector. With the amendment of the NSSF Act and the gazzetting of the Voluntary Contributions and Benefits Regulations in

November last year, NSSF has now been empowered to extend social security and make it accessible to all Ugandans. To achieve this, it is critical that we go to the grassroots, where the people work and stay. NSSF is going everywhere, because we believe every Ugandan deserves to enjoy the

40,000

peace of a financially stable future,” Kabugo said.

The market outreaches, Kabugo added, further demonstrate NSSF’s commitment to achieving its vision of securing the financial future of 15 million Ugandans, with emphasis on the informal sector.

Improving savings culture in markets

The initiative was to be rolled out to seven major government markets in Kampala, including St. Balikuddem-

be (Owino), Nakasero, Wandegeya, Bugolobi, Nakawa, Sseeta, and Kasubi.

In her remarks at the launch, Deputy Presidential Advisor on Markets, Winnie Twine, commended NSSF for aligning with the government’s goal of fostering a savings culture for financial freedom in Uganda.

“Government has introduced numerous initiatives such as the Parish Development Model, Youth support programs, but minimal impact is registered because people lack financial discipline and fail to save. Therefore, an initiative such as Smartlife Flexi supports government’s interventions because it encourages savings,” she said, encouraging the vendors to enrol for Smartlife Flexi.

Ronald Mutebi, the Market Master responsible for overseeing administration of the markets at Kampala Capital City Authority (KCCA) welcomed the initiative noting that the market vendors have consistently been cheated out of their savings through unregulated merry-gorounds and informal savings groups.

He urged the market vendors to enrol for Smartlife Flexi, a safe and profitable investment.

The campaign launch followed the recent unveiling of Smartlife Flexi, NSSF’s voluntary savings plan developed to expand social security coverage throughout the country by providing a flexible, convenient and competitive product for all Ugandans.

To sign up for Smartlife Flexi, follow this link and start your savings journey:

https://nssfgo.app/landing

An NSSF Staff member sensitises market vendors in Owino Market on saving.

Kasemiire Public Relations Officer

Number of vendors in Owino market

Building Wealth in Uganda’s Gig Economy

John Ssenkeezi Digital Editor

Uganda’s economy is buzzing with a new energy, much of it powered by the rise of the gig economy. Driven by digital transformation and a growing need for flexible work, more Ugandans than ever are embracing freelance assignments, online tasks, boda boda transport services, artisanal work, and countless other short-term contracts. This shift offers unprecedented freedom and the potential for instant income, attracting many, especially young people seeking opportunities outside the traditional job market.

However, this flexibility often comes at a price. The very nature of gig work, project-based and dependent on fluctuating demand, means income can be unpredictable. Unlike traditional employees, gig workers typically lack the safety net of employer-sponsored benefits like medical insurance, paid leave, or contributions to the National Social Security Fund (NSSF). This financial uncertainty makes personal savings not just a good idea, but an absolute necessity for handling emergencies and building a foundation for the future.

Fortunately, the same digital wave powering the gig economy also provides the tools to manage its financial challenges. These digital tools can be powerful allies, helping gig workers to consolidate income from various sources, implement effective savings habits, manage budgets, and even access pathways to investment.

Understanding gig finances in Uganda.

Before building a savings strategy, it is crucial to acknowledge the specific financial landscape Ugandan gig workers navigate. Understanding these realities ensures realistic planning and highlights the urgency of proactive financial management.

The most significant challenge is income volatility. Earnings often fluctuate based on the availability of gigs, seasonal demand, platform algorithms, and intense competition from other workers. This unpredictability makes traditional monthly budgeting extremely difficult. One month might bring a feast, the next a famine, requiring careful management to smooth out these peaks and troughs.

Many young people are turning to gig-based work for flexibility and independence. Photography is one of the common gigs in Uganda.

Personal Finance

Compounding this is the lack of traditional benefits. Gig workers are typically classified as independent contractors, meaning they miss out on employer contributions to NSSF, medical insurance schemes, and paid time off for sickness. This places the entire burden of saving for retirement, covering medical emergencies, and managing time off squarely on the individual’s shoulders.

Acknowledging these factors is the essential first step. It highlights a fundamental tension: the very instability of gig work creates a profound need for personal savings to act as a buffer against income dips and unexpected costs like healthcare. Yet, the same factors, low or irregular pay and the lack of a safety net, make consistent saving challenging.

Fortunately, Uganda boasts a vibrant digital financial ecosystem that offers powerful tools for managing the complexities of gig income. These tools can help consolidate earnings, track spending, and provide access to essential financial services.

Track Everything: The first step is understanding where the money comes from and where it goes. This involves diligently tracking all income sources and expenses for a period, perhaps one to three months, using a simple notebook, spreadsheet, or a budgeting app. This exercise reveals spending habits and establishes an average income baseline.

Flexible Budgeting: Rigid monthly budgets often fail gig workers due to income inconsistency. More adaptable approaches are needed:

• Percentage Budgeting (e.g., 50/30/20 Rule): A popular guideline suggests allocating income towards Needs (50%), Wants (30%), and Savings/Debt (20%). For gig workers, this rule can be applied to each payment received. When money comes in,

Prioritise the Emergency Fund: For workers without sick pay or job security, an emergency fund is non-negotiable. This fund should ideally cover 3 to 6 months of essential living expenses (rent, food, utilities, basic transport). Building it takes time. Start small, allocating a portion of every income. This cushion prevents unexpected events from derailing long-term financial goals or forcing reliance on expensive debt.

Leverage the Peaks: Income tracking will reveal higher-earning periods. During these “feast” times, it is crucial to resist lifestyle inflation and instead consciously allocate a significantly larger portion of income towards savings goals, particularly building the emergency fund or paying down debt.

immediately allocate percentages to essential bills, miscellaneous spending, and savings goals.

• Zero-Based Budgeting: This method requires assigning every single shilling of income a specific purpose, rent, food, transport, savings goal, debt payment, etc, until the entire amount is allocated. It forces intentionality.

• Budgeting Based on Lowest Expected Income: Estimate the lowest likely monthly income based on past tracking. Create a core budget covering essential expenses based on this figure. Any income earned above this baseline is then channelled directly into savings, debt repayment, or building buffers.

To help you on this journey, here are some effective planning and top free personal finance tools for 2025.

Top free personal finance tools for 2025.

Compounding Money Safely: For funds needed in the short-to-medium term, keeping large amounts of cash at home is risky and loses value to inflation. Instead, “park” this money in safe, easily accessible, interest-earning options. The goal is capital preservation with a return, keeping the funds liquid enough for their intended purpose. Linking these strategies to specific goals is vital. Defining clear, tangible goals makes the abstract act of saving more purposeful and motivating, shifting behaviour from simply coping towards proactively building a desired future. An NSSF Smartlife Flexi account can help gig workers to start saving from as low as UGX 5,000 towards clearly defined goals, with competitive returns and easy mobile money deposit options.

The journey from hustle to financial security requires commitment. Start small, leverage the digital tools at your fingertips, stay consistent, and seek out financial knowledge NSSF Uganda has a robust Financial Literacy program which is accessible at no extra cost. Supported by a growing ecosystem that includes initiatives promoting financial literacy from institutions like the Bank of Uganda, Ugandan gig workers have the means to take control of their finances and build a more secure and prosperous future.

NSSF Hi-Innovator Program Boosts 45 Women-led Businesses with UGX3.3 Billion

Christine Kasemiire Public Relations Officer

The National Social Security Fund (NSSF) and Mastercard Foundation have extended funding to 45 women-led businesses worth UGX 3.3Billion under their Hi-innovator program.

Each business will receive UGX 75 million in seed funding, subject to the completion of a due diligence exercise to ensure compliance with program requirements and operational efficiency.

This followed a competitive pitching exercise held in Kampala, where a total of 56 women-led businesses presented before a panel of seasoned entrepreneurship experts.

The Hi-Innovator is an initiative of

Each business will receive

UGX 75m in seed funding

the National Social Security Fund (NSSF) in partnership with the Mastercard Foundation and implemented by Outbox, aimed at cultivating an enabling ecosystem for indigenous Small and Growing Businesses (SGBs) to evolve into viable and scalable enterprises.

The businesses were evaluated based on their scalability, potential to generate employment opportunities for youth, and the strength of their management teams.

The sectors represented in this pitching round include agriculture, digital economy, light manufacturing, tourism, health, green business, and Edtech, reflecting a deliberate focus on industries with high growth potential and social impact.

Derrick Sebbaale representing the NSSF Head of Strategy said: “We are proud to witness women entrepreneurs leading the way and shaping the future of their businesses. Building on the success of our previous window, we are committed to empowering these businesses to cement their operations, drive sustained economic growth and make a lasting impact on the nation’s development.”

Women-led businesses supported

This selection brings the latest number of women businesses supported

A group photo of the representatives of the 45 women-led businesses that will receive funding from the NSSF Hi-innovator program.

The NSSF Hi-innovator program is in partnership with Mastercard Foundation.

to 249 following the successful funding of the previous pitching window which saw 32 women-led businesses acquire UGX1.1Billion.

Richard Zulu, Founder of Outbox, the lead implementing partner for the Hi-Innovator program, highlighted the rationale behind prioritizing these sectors. “This round of selections was guided by the potential of these industries to create dignified and sustainable employment opportunities, particularly for youth and women, who are critical drivers of Uganda’s economic transformation,” he explained.

The Hi-Innovator program has significantly contributed to Uganda’s entrepreneurial ecosystem by equipping small and growing businesses with the financial, technical, and mentorship support needed to scale. Through its targeted investments, the program has fostered innovation, created thousands of jobs, and strengthened local enterprises, driving economic growth and long-term sustainability.

Since its inception in 2021, the program has supported 390 businesses with a total allocation of UGX28Billion resulting in the creation of 224,755 jobs affirming the program’s mission to foster innovation and entrepreneurship across Uganda.

Sebbaale underscored the program’s strategic vision, stating that today’s selection reaffirms the programme’s commitment to supporting 500 businesses by the end of 2025.

Enroll for the Hi-innovator Business Foundational Courses through this link: https://hi-innovatorbusinessacademy.nssfug.org/courses/ hi-innovatorbusinessacademy.

The 45 women-led businesses that will receive funding from the Hi-Innovator Program

Africa Haven Limited

Agrabo Enterprises Limited

Ainana Holdings Ltd

Atelier Mayanja Ltd

Atmosave International Limited

Bafaso Agro Tourism Mixed Farm

Bennett Agency & Advisory Limited

Busiiro Electricals Services Limited

Cakely Uganda Limited

Callistra Trading Ltd

Cefla U) Limited

Crispacc Logistics

D&M Group International Limited

Dine Farms (U) Ltd

Eco Group Limited

Elgwin Fresh Agro Food’S Limited

Evertrust Enterprises Limited

Fruit Design Uganda

Gensys Organic Foods Limited

Gogo Flo General Agencies Limited

Greendoor Supplies Uganda Limited

Greensafety Inventors Limited

Guardian Multi Service Axis Ltd

House Of Mama Natural Condiments Ltd

Huthart Enterprise Smc Ltd

Jada Coffee Ltd

King of Kings Limited

Lash Technical Services Ltd

Lock Stock & Barrel (Lsb) Ltd

Mama Mucyara Enterprises Limited

Mukyaro General Traders Limited

Nazareth Agribusiness Solutions Ltd

Ness Nutrition Consultancy Limited

Pristine Dental Surgery Ltd

Psalms Mixed Farm & General

Enterprises Limited

Quera Innovations Smc Ltd

Reticent General Enterprises Limited

Rinaha International Limited

Ritoba Services Limited

Sarami Agencies Limited

Sparky Driers Enterprises Limited

Spul Foods Limited

Sterling Seeds Ltd

Stina Enterprises Limited

Tulye Agriventure Limited

Number of Small & Growing Businesses seed funded under Hi-Innovator to date:

390

Number of jobs created since program inception in 2021:

224,755 jobs of which 152,214 are youth.

Seed funding provided:

Over UGX

28 billion

Entrepreneurs trained through the NSSF Hi-Innovator Business Academy: 60,232

Youth trained through the NSSF Hi-Innovator Business Academy: 45,367 (75%)

Women trained through the NSSF Hi-Innovator Business Academy:

35,868 (60%)

Female Entrepreneurs pose for a photo during the NSSF Hi-innovator women accelerator window held in March 2025 in Kampala.

Market Insights

Economic Drivers and Markets Implications

Edwin Rwemigabo, CFA Fixed Income Specialist

Global Economy: US Trade Policy Coming to the Fore of Global Uncertainty

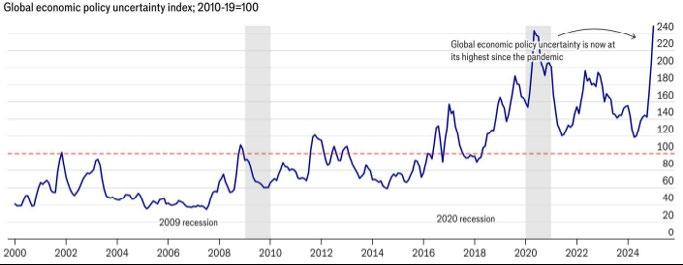

At the start of 2025, the International Monetary Fund projected global GDP growth would hold steady at 3.3% in 2025 and 2026. More recent insights by economists point to growing downside risks, mainly driven by the escalating trade policy uncertainty under the Trump administration, among other pre-existing factors. The Economic Intelligence Unit (EIU) now projects 2025 global growth at 2.4% while the OECD projects 3.1% growth. The US is expected to grow at 2.7% fueled by strong demand and policy support. In contrast, the euro area is forecasted to lag at 1.0%, while China will continue to face structural headwinds. Inflation is gradually easing — projected at 4.2% globally in 2025 — but central bank strategies are diverging, with some tightening amid sticky services inflation and a stronger US dollar.

Africa’s economic momentum is picking up modestly, with growth forecasted to rise from 3.8% in 2024 to 4.2% in 2025. This improvement is backed by easing inflation, continued infrastructure investment and a rebound in private consumption. Downside risks are likely to emanate from weaker external demand (particularly China and Europe), a stronger US dollar and reduced global liquidity as easing cycles are checked. Fiscal consolidation remains a priority across much of the continent, though public debt remains elevated in several economies.

Figure 1: Policy uncertainty has reached historical highs

Source: EIU, 2025

Inflation trends vary, but the continental average is easing. Countries such as Nigeria and South Africa are benefiting from lower fuel and food prices, although inflation remains elevated in net importers and post-conflict states. Central banks are signaling a more neutral stance, with cautious rate cuts expected in 2025 depending on external conditions.

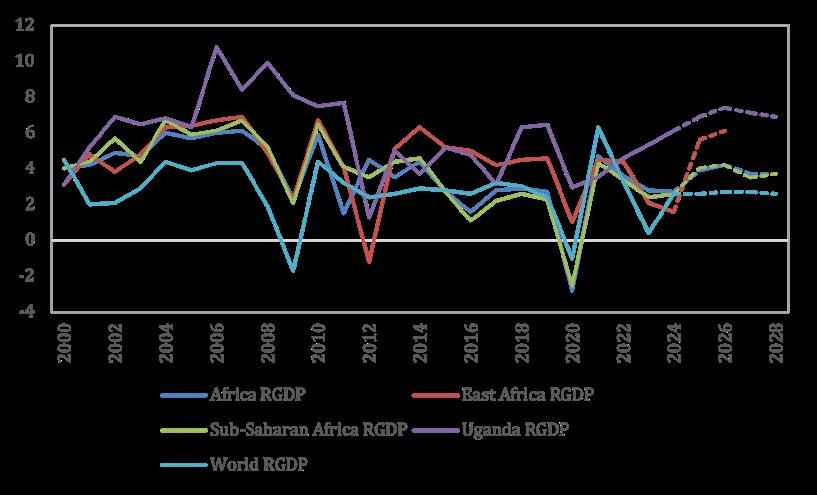

East Africa: Growth Resilient, but Domestic and External Risks

Mount

East Africa remains one of the continent’s fastest-growing regions, with the regional Central Banks projecting 2025 growth above 5% across Kenya, Tanzania, Rwanda, and Uganda. The region is supported by agriculture recovery, infrastructure investment, and an expanding services sector. However, political uncertainty ahead of the 2025 and 2026 general elections in Uganda and Tanzania respectively, may weigh on investor confidence and tighten fiscal spaces, slowing down expected investments in the region and affecting macroeconomic stability.

Regionally, inflation in Kenya, Uganda and Tanzania remains low and below the central banks’ target ranges but has been slowly ticking up during the first quarter of 2025. The low inflationary environment however allowed for a 50-bps policy rate cut in Kenya and holding stances in Uganda and Tanzania during the quarter.

A strong US dollar — driven by still elevated US rates and tariff fears — may however keep central banks cautious by limiting monetary flexibility in 2025, amidst rising external debt servicing costs and import bills.

Uganda: Stability and Oil Prospects Drive Optimism

Uganda’s outlook stands out for its strong fundamentals. The country is projected to grow by 6.0% in 2025, supported by ongoing oil sector investments, infrastructure development, strong agriculture performance and a favorable macroeconomic environment anchored by a stable currency and low inflation.

Vulnerabilities are however notable with public debt crossing 50% of GDP in FY2024/25, requiring fiscal discipline even as spending demands rise in the face of an upcoming election year and infrastructure investments. Like her regional counterparts, external risks weigh in, particularly with reduced demand from China and potential spillovers from tariff related trade disruptions.

The country is projected to grow by 6.0%

Implications for Regional Financial Markets and the Fund’s Investment Strategy

Bond Markets: Anchored inflation will continue to provide positive real yields but also allow for lower or stable central bank policy rates. However, the US dollar’s strength and risk-off sentiment may pressure long-term yields upward, especially if fiscal deficits rise during election cycles. Yield curves are therefore likely to steepen further down the year, with front-end support and back-end caution, favoring long term investment opportunities.

FX Markets: Regional currencies are likely to face depreciation pressure from a strong dollar and tighter global liquidity. While Uganda’s shilling has been more stable, it remains vulnerable to fiscal slippage. Central banks may lean on reserves or limit easing stances to defend currency stability. With likely pressure on currencies, investment in regional currencies may be limited to high alpha opportunities.

Equities: Falling domestic rates may support local equity sentiment, especially in financial and consumption-linked sectors. However, foreign investor flows may remain

constrained by low global risk appetite and pre-election uncertainty in 2025, with risks of amplified volatility from shallow market depth. Over the next one year though, foreign exits could create good entry levels in pockets of the market.

Capital Flows: Investors remain selective, with capital favoring economies showing policy consistency and macro stability. Uganda’s oil-driven story may attract selective flows, but execution and election stability will be decisive. ESG and green financing remain promising themes across the region and may provide diversification opportunities.

Africa and East Africa remain resilient growth zones, but global spillovers, tighter financing, and political transitions could narrow fiscal space and test policy agility. Uganda, meanwhile, retains a strong growth trajectory, anchored in domestic investment and macroeconomic stability, but must navigate electoral pressures and rising global uncertainty carefully.

Conclusively, 2025 is not a year of crisis — but one of complexity. Navigating the road ahead will require policy dexterity and external resilience.

Figure 2: East Africa Growth on a High Source: EIU

Cybersecurity: Morocco, Australia Funds Hacked

A cyber attack on Morocco’s National Social Security Fund which is known as Caisse Nationale de Sécurité Sociale (CNSS), is suspected to have compromised the personal data of nearly 2 million employees from thousands of companies in the country, risking unauthorised use of its members’ personal data.

Various media reports suggested that the attack may have exposed personal data of employees across approximately 500,000 businesses registered with the Morocco Fund.

In a media release CNSS confirmed that its information system was subjected to a series of cyberattacks aimed at circumventing security measures, noting that these attacks caused a data leak, the origins and scope of which are currently being assessed.

However, it also revealed that initial verifications showed that these data were often falsified, inaccurate, or truncated.

The attack prompted the country’s National Commission for the Control and Protection of Personal Data to warn of risks linked to the unau-

thorized use of personal data in the aftermath of the breach of the Fund.

CNSS in the statement urged “all citizens and media to exercise caution, a sense of responsibility, and to avoid any act of disseminating or sharing leaked or falsified data, under penalty of legal consequences.”

Adapted from Security Affairs

Photo by 7 News Morocco

Passwords stolen from AustralianSuper, the 3.5 million members’ industry leader Australia

Adapted from Reuters

Across the oceans in Australia, hackers are reported to have attacked Australia’s major pension funds, compromising over 20,000 member accounts and stealing some members’ savings.

The attacks targeted the cash rich retirement savings sector, with funds

such as AustralianSuper, and Australian Retirement Trust compromised.

The attacks were confirmed by National Cyber Security Coordinator Michelle McGuinness, who, according to Reuters, said in a statement that cyber criminals targetted accounts in the country’s $2.63 trillion retirement savings sector. The country was organising a response across the government, regulators, and industry.

The Association of Superannuation Funds of Australia, the industry body, confirmed the attack that several funds were impacted.

AustralianSuper, Australian Retirement Trust, Rest, Insignia and Hostplus also on April 4, 2025, confirmed they were compromised by the cyberattacks.

Cybersecurity Tips

How schemes can protect members’ data

1. Secure your IT infrastructure – Protect your company information technology infrastructure by setting up firewalls and encrypting information. Ensure automatic backup of company data regularly, depending on the activity level within your company, which prevents complete data loss in case of a data breach.

2. Educate your staff – Regularly train your staff about their obligation to ensure information security, and ensure they adhere to the information security policies in place

3. Create security policies and practices – Put in place company policies to guide your company IT security practices. Policies may include guidelines on system accessibility, devices, and issue resolution, flagging, and resolution of potential threats, reward and punishment for policy adherence and breach, respectively.

4. Invest in data security professionals – onboard own competent staff, specially trained in technology and information security, or contract world-renowned information security firms

5. Involve partners and customers –involve key customers who may have access to your systems as a result of data sharing agreements and integration requirements. Limit what information they can access and share.

6. Be wary of unsolicited emails, messages, and unknown calls – screening mechanisms should be put in place to ensure unsolicited communication does not bypass IT security procedures. This is more critical in times of crisis or business uncertainty

How you can protect yourself from cybercrime

1. Beware of AI-generated content - Inconsistencies and anomalies in content, such as image and voice distortions, unnatural actions like

Worryingly, AustralianSuper, the country’s largest fund with over 3.5 million members, confirmed that up to 600 member passwords had been stolen to access accounts and there was attempted fraud.

The Fund however assured members and the country that it took action and locked the compromised accounts and communicated to affected members, while there has been coordinated remedial action from the Australian Government, industry leaders, and regulators.