North Coast Building Industry Association (NCBIA) BUILDER newsletter is the official newsletter of the NCBIA and is published monthly by the NCBIA. The NCBIA is an affiliate of the Ohio Home Builders Association (OHBA) & the National Association of Home Builders (NAHB).

Advertising Policy - The North Coast Building Industry Association reserves the right to reject advertising in the Builder newsletter based on content. Acceptance of advertising does not imply endorsement of the product or service advertised.

5321 Meadow Lane Court - B, Suite #23 Sheffield Village, OH

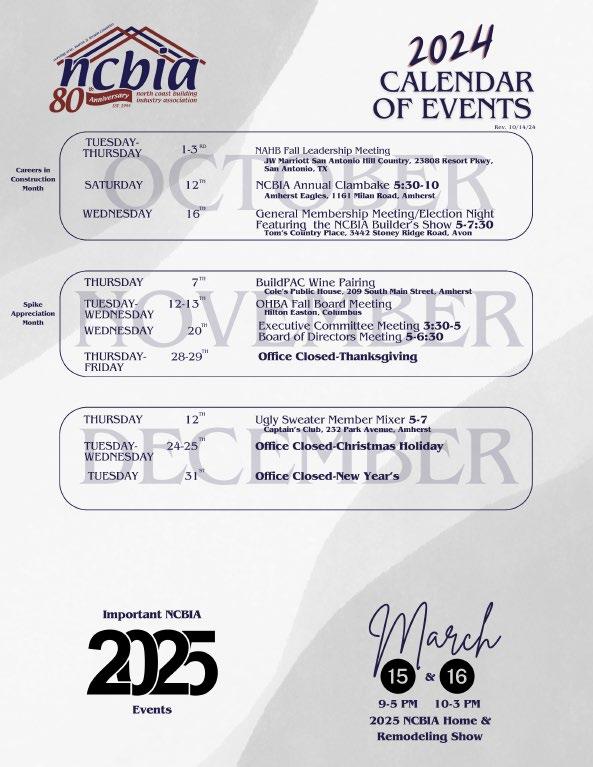

Check the website at www.ncbia.com for up-to-date changes, additions, and corrections to these events!

Business anniversaries, accomplishments, awards, publications, etc.? Send to judie@ncbia.com. We want to hear from you!

Congratulations to Mark McClaine (84 Lumber) and his beautiful wife Angela married in August 2024!

Congratulations!!!!

Best Home Builder

Dale Yost Construction, Elyria

OCTOBER IS Careers in Construction Month

Top Reasons Parents Should Consider a Career in Construction for Children

As you probably know the residential construction industry is filled with talented and creative individuals who build homes that strengthen communities. Not only does a career in the industry provide a sense of personal achievement, but it also provides many practical benefits, such as strong earning potential, job security, and opportunities for advancement.

If you are a parent, your children’s future is always one of your top priorities. Two major factors that influence their future are education and their eventual career, which are usually closely tied together. Acquiring knowledge and skills, and then putting them to use, is part of the process where they transition to being independent and successful adults.

High Demand for Careers

• 94% of parents approve of expanding access to career and vocational programs.

• 86% of parents and students say that they wish they could get more real-world knowledge and skills during school.

• 54% of business leaders do not think the educational system is teaching skills needed for the workforce.

A Variety of Jobs for Every Skill Level Are Available

Occupations such as carpenters, plumbers, electricians, masons and HVACR technicians are in high demand. These types of jobs require individuals who have skills such as being detail-oriented and active problem solvers troubleshooting a range of challenges.

Skilled Trades Offer Individuals High Earning Potential

Individuals entering the residential construction industry have the potential to earn a great salary. The top 25% in most construction trades professions earn at least $60,000 annually. And you do not need to follow the traditional college path to get there. Join our Workforce Development Committee

I welcome any member that would like to help spread the benefits of a career in the trades and be a part of this committee email either myself (tking@khov.com ) or Judie Docs at (judie@ncbia.com ).

Tim King, K. Hovnanian Homes

by Judie Docs, CSP, MCSP, MIRM, CMP, CGP

A HEARTFELT THANK YOU to Our Event Sponsors

I would like to extend our sincerest gratitude to the members who have generously sponsored our events over the past year. Your support has been instrumental in helping the North Coast Building Industry Association bring valuable and engaging events to our members.

With your help, we have been able to make a significant impact on our community, and we look forward to continuing this collaboration in the future. Thank you for your unwavering support!

84 Lumber

All Construction Services, Inc.

Buckeye Community Bank

Carter Lumber

Caruso Cabinets

Dale Yost Construction

Dollar Bank

E.H. Roberts Co.

Fifth Third Bank

First Federal Savings of Lorain

First National Bank

Floor Coverings International

Granite Works Stone Design

Greyhawk Development

Guardian Title

Home Appliance Sales & Service

Honey Dudes Handyman Service

K. Hovnanian Homes

Kopf Builders

Luxury Heating Co.

National Design Mart

Network Land Title Agency

O'Neal Tax & Bookkeeping, LLC

Peacock Water

Reaser Construction

Repros Engineering

Royalty Roofing

Screenmobile of West Cleveland

Sedgwick

Shamrock Development Co.

Stewart Title

Stewart's TV & Appliances, Inc.

Strauss Construction, Inc.

Sweetbriar Golf Course

Tammy Koleski -Howard Hanna Real Estate

The Nelson Agency

The S.J.R. Building Co.

Third Federal

Walker Wealth Management & Great Lakes Properties & Investments

WCCV Flooring LLC

EVENT SPONSOR

Member: $2000

Non-Member: $2500

Event Sponsors:

Everything on Supporting Sponsor list, PLUS radio interview, booth space, logo on staff t-shirts and all printed advertising, mention in radio advertisements and option to have your company’s banner hung at show entrance!

Saturday, March 15th 9-5 Sunday, March 16th 10-3

Spitzer Conference CenterLorain County Community College 1005 North Abbe Road, Elyria

My company would like to sponsor the 2025 NCBIA Home Show. (Please select below)

Event Sponsor($2000) Member Supporting Sponsor ($300)

Event Sponsor ($2500) Supporting Sponsor ($500)

SPONSOR INFORMATION

SPONSOR

Member: $300

Non-Member: $500

Includes: mention in radio ads, your logo in event program, Facebook event page, slideshow during event, option to put promotional items in swag bag, and recognition in BUILDER newsletter.

PAYMENT METHOD:

Please Indicate how you would like to pay for your sponsorship.

QUESTIONS? CONTACT THE NCBIA www.ncbia.com (440) 934-1090 judie@ncbia.com

Supporting Sponsors:

Bag Sponsor: ___Invoice ___Check Enclosed ___VISA/MC/AMEX/DISC* *If you select credit card, our office will call for your card information.

ON HOUSING

HOME BUYERS WANT TECHNOLOGY TO Improve Energy Efficiency and Increase Safety

NAHB published research earlier this year on home buyer preferences called What Home Buyers Really Want1. Consumers were asked to rate how 19 technology features would influence their home purchase decision, if at all, using the following four-point scale:

• Do not want – not likely to buy a home with this design or feature.

• Indifferent – wouldn’t influence decision.

• Desirable – would be seriously influenced to purchase a home because this design or feature was included.

• Essential/Must have – unlikely to purchase a home without this design or feature

Seventy-eight percent of home buyers rated a programmable thermostat as either essential/must have or desirable, followed by security cameras (76%), video doorbell (74%), and wireless home security system (70%). Sixteen of the 19 technology features had at least 50% of home buyers rating them as essential or desirable. The top eight features reveal that home buyers are looking for technology that helps them achieve two main goals:

1. Improve Energy Efficiency (programmable thermostat, multi-zone HVAC system, lighting control system, energy management system/display) AND 2. Increase Safety (security cameras, video doorbell, wireless & wired home security system)

Additionally, like the other areas of the home covered in the study, every question on technology features is tabulated by the buyer’s income, age, geography, race, household type, and the price they expect to pay for the home. These details can be very useful in particular cases. For example, the study discusses the five technology features that have the largest preference margins between the youngest and oldest buyers along with analyzing the prevalence of virtual tours by income and price point.

BY: ERIC LYNCH

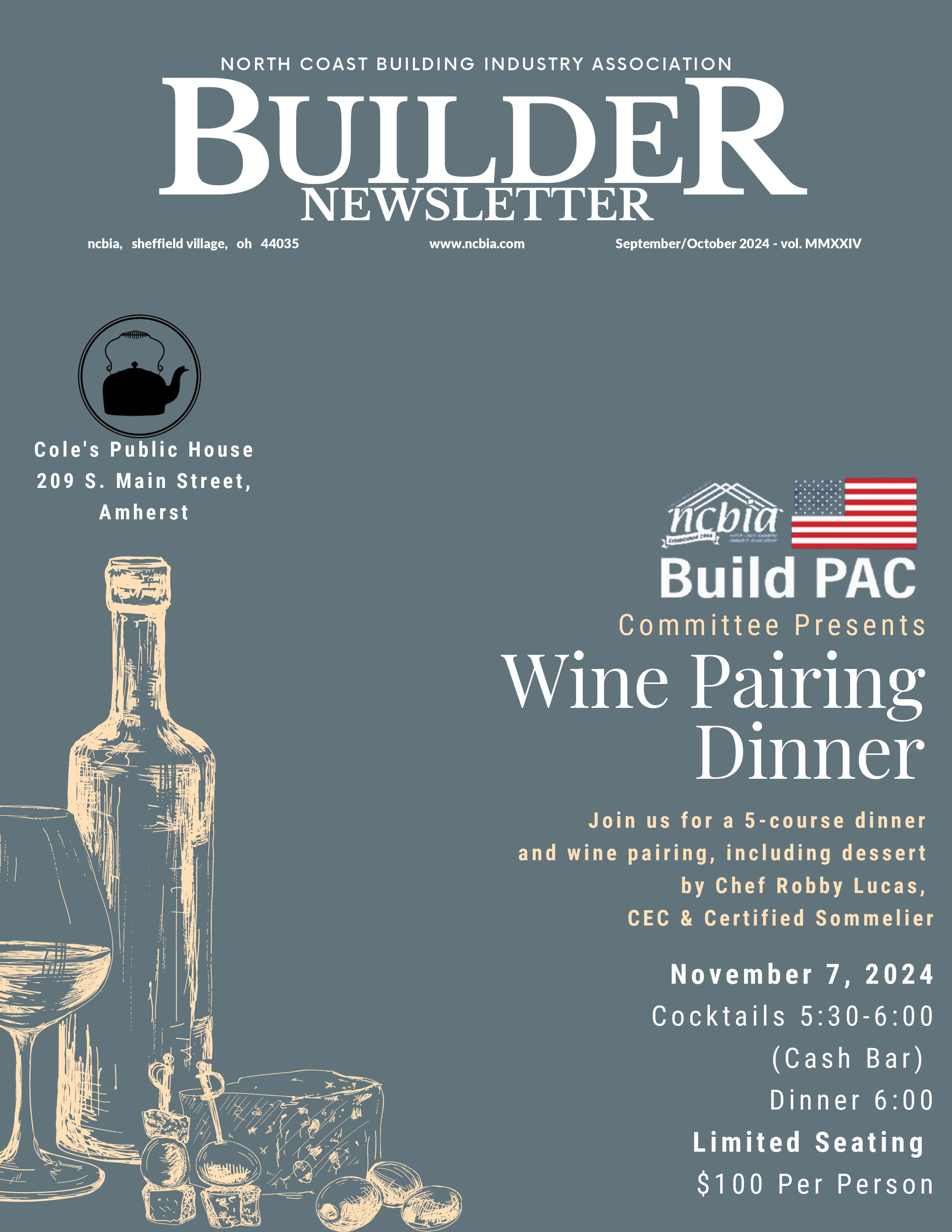

C o l e ' s P u b l i c H o u s e

2 0 9 S . M a i n S t r e e t ,

A m h e r s t

C o m m i t t e e P r e s e n t s

Wine Pairing Dinner

J o i n u s f o r a 5 - c o u r s e d i n n e r

a n d w i n e p a i r i n g , i n c l u d i n g d e s s e r t

b y C h e f R o b b y L u c a s ,

C E C & C e r t i f i e d S o m m e l i e r N o v e m b e r 7 , 2 0 2 4

C o c k t a i l s 5 : 3 0 - 6 : 0 0 ( C a s h B a r ) D i n n e r 6 : 0 0

L i m i t e d S e a t i n g $ 1 0 0 P e r P e r s o n

P l e a s e b r i n g B u i l d P A C d o n a t i o n t o t h e

e v e n t o r s e n d d i r e c t l y t o t h e N C B I A o f f i c e

( 5 3 2 1 M e a d o w L a n e C o u r t - B , S u i t e 2 3 ,

S h e f f i e l d V i l l a g e O H 4 4 0 3 5

R e s e r v e y o u r s e a t b y O c t o b e r 3 0 , 2 0 2 4 , b y

c a l l i n g 4 4 0 . 9 3 4 . 1 0 9 0 ,

e m a i l j u d i e @ n c b i a . c o m o r r e g i s t e r o n l i n e .

Q u e s t i o n s - C o n t a c t C o - C h a i r s , M a r y F e l t o n 4 4 0 . 7 5 9 . 4 3 4 1 , o r L i z S c h n e i d e r 4 4 0 . 4

COMPLETION DATES AND DOWN PAYMENTS

Homeowners want their projects to start timely, and probably even more, finish timely. Contractors know that a number of different factors can affect the timing of their work: homeowner decisions or changes, material or equipment delivery delays, the work of other contractors, weather, etc. As a result of the uncertainty of construction, contractors do not like to put a completion date or duration in their contracts. Ohio law is not sympathetic.

For new home builds, the Home Construction Service Suppliers Act (which generally covers new home builds and larger remodels, aka “the HCSSA”) requires that the contract includes the planned start and finish dates, or the anticipated duration of the work. For home remodels and repair projects, the Consumer Sales Practices Act (“the CSPA”) also requires an estimated completion date. And per the CSPA, contractors have no more than 8 weeks from receipt of deposit to complete or at least start the work, unless a written contract says otherwise. In other words, Ohio law requires that contracts include a completion date or duration of the work from the project start.

That said, the law does not prohibit contractors from qualifying the completion date or anticipated duration with matters outside the contractor’s control that may delay the time period in question. Things like homeowner decisions or changes, material or equipment delivery delays, the work of other contractors, weather, global pandemics, etc. If matters outside the contractor’s control impact the timing of the work, it’s also a best practice to timely notify the homeowner of the delay event and how much time that’s expected to delay the work or delivery.

But simply avoiding a completion date or expected time period for construction because it makes you uncomfortable is not the answer.

How about Down Payments? Many contractors require a down payment in their contracts. This is smart. Invariably there are costs at mobilization that are significant, and it’s fair for the homeowner to make initial payments to cover those costs. However, there are restrictions in the law.

If the project is a new home build (or a home remodel or repair costing more than $25,000), the contractor cannot ask for more than 10% upfront before work starts. That is, unless there are custom or specialty orders for equipment or materials. Otherwise, down payments of more than 10% of the contract price or estimated price violate the HCSSA.

If the project is a home remodel or repair priced less than $25,000, there is not a specific restriction on the amount of the down payment. But, contractors must provide a written receipt when the down payment is paid, and the receipt must state whether the deposit is refundable or non-refundable. Additionally, once the contractor receives the initial deposit, the contractor has no more than 8 weeks to complete, or at least start, the work. Otherwise, the contractor is supposed to inform the homeowner of the delay and offer to give the deposit back during the wait. Failure to comply with these requirements is a violation of the CSPA, and can lead to a treble (triple) damages award to the homeowner.

Regardless, requesting and accepting down payments from homeowners is not to be taken lightly, and contractors should be sure to document both the receipt of any deposits and how those deposits are used.

Contact us to discuss your legal needs:

EYE ON HOUSING

HOME PRICE Growth Slowing

Home prices remain elevated but price growth continues to decelerate, according to the S&P CoreLogic Case-Shiller Home Price Index (HPI) recent release . The S&P CoreLogic Case-Shiller HPI (seasonally adjusted) reached its 14th monthly consecutive record high in July 2024. The index increased at a seasonally adjusted annual rate of 2.15%, down slightly from a revised June rate of 2.19%. This rate has slowed over the past six months, from a high of 6.53% in February 2024. The index has not seen an outright decrease since January of 2023 (nineteen months). Separately, the House Price Index released by the Federal Housing Finance Agency (FHFA; SA) posted its sixth monthly consecutive record high, after having decreased slightly in January of this year. The FHFA HPI recorded a 1.57% increase in July, upward from a revised 0.03% rate in June.

Year-Over-Year

Home prices experienced a fifth consecutive year-overyear declaration in July, tabulated by both indexes. The S&P CoreLogic Case-Shiller HPI (not seasonally adjusted – NSA) posted a 4.96% annual gain in July, down from a revised 5.50% increase in June. Meanwhile, the FHFA HPI (NSA) index rose 4.56%, down from a revised 5.37% in June. Both indexes have seen yearly growth rates slow since February 2024, when the S&P CoreLogic Case-Shiller stood at 6.54% and the FHFA at 7.23%.

By

Metro Area

In addition to tracking national home price changes, the S&P CoreLogic Index (SA) also reports home price indexes across 20 metro areas. At an annual rate, only two out of 20 metro areas reported a home price decline: San Francisco at -4.98 and Tampa at -3.10%. Among the 20 metro areas, 14 exceeded the national rate of 2.15%. Seattle had the highest rate at 13.78%, followed by New York at 6.11%, and Las Vegas at 5.76%. The monthly trends are shown in the graph below.

Monthly, the FHFA HPI (SA) releases not only national but also census division house price indexes. Out of the nine census divisions, three posted negative monthly depreciation (adjusted to an annual rate) for July: South Atlantic at -7.88%, West South Central at -6.80%, and East South Central at -0.66%. The divisions with positive home price appreciation ranged from 2.02% in West North Central to 11.57% in East South Central. The FHFA HPI releases its metro and state data on a quarterly basis, which NAHB analyzed in a previous post.

BY: ONNAH DERESKI

THANK YOU SPIKES!

STATESMAN SPIKE (500-999 SPIKE CREDITS)

SUPER SPIKE (250-499 SPIKE CREDITS)

Terry

RED SPIKE (100-149 SPIKE CREDITS)

Dave

Tom

GREEN SPIKE (50-99 SPIKE CREDITS)

Chris Mead ................... Maloney & Novotny, LLC .........................

Aaron Kalizewski ........ Grande Maison Construction....................

Jeremy Vorndran 84 Lumber

Jason Scott Greyhawk Development

Liz Schneider Dollar Bank

Tim King K. Hovnanian Homes

LIFE SPIKE (25-49 SPIKE CREDITS)

Steve Schafer ................ Schafer Development .................................

John Daly Network Land Title 28.50

BLUE SPIKE (6-24 SPIKE CREDITS)

Mark McClaine 84 Lumber

John Toth ...................... Floor Coverings International ...................

Dave LeHotan .............. All Construction Services ..........................

Chris Collins Carter Lumber

Ken Cassell Cassell Construction 13.50

Ashley Oates 84 Lumber 12.00

John Blakeslee Blakeslee Excavating, Inc 12.00

Scott Kosman Lakeland Glass 9.50

Mike Meszes ................ DRC Construction ...................................... 8.00

Tim Hinkle ................. Green Quest Homes ............................... 6.50

Jim Tipple Maranatha Homes 6.50

Lindsay Yost Bott Dale Yost Construction 6.00

Lou LaGuardia Repros Engineering 6.00

Dennis Reber, Apollo Supply

Cynthia Gore, Stewart Title

Ted Carson, Apollo Supply

Rosanna Hrabnicky, Marketplace Events Thanks for Renewing!

Jeremy Vorndran, 84 Lumber

Mike Meszes, DRC Construction

Michelle Williamson, Fidelity National Title

Melanie Stock, First Federal Savings of Lorain

Mary H. Felton, Guardian Title

Jim Dosztal, JD Custom Designs, LLC

Ray Swift, K. Hovnanian Homes

Douglas Gerber, Landscaping by Gerbers, LLC

Michael Griffith, M.J. Griffith Paving, Inc.

Mike Sherrill, Raymond Plumbing Heating & Air Conditioning, LLC

Kevin Bolden, Bolden Home Improvements

Kristine Burdick, Howard Hanna Real Estate

Bob Pogorelc, Pogie’s Catering & Club House

Debra Seeley, Third Federal

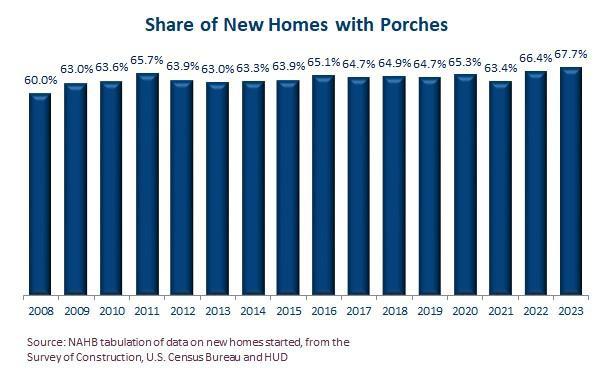

OVER TWO-THIRDS OF NEW HOMES in 2023 Feature Porches

Porches continue to rank as the most common outdoor feature on new homes, according to NAHB tabulation of the latest data from the Survey of Construction (SOC, conducted by the U.S. Census Bureau with partial funding from HUD). Of the roughly 950,000 single-family homes started in 2023, the SOC data show that 67.7% were built with porches. This is four full percentage points higher than the 63.7% reported for patios , and marks the first time the share of new homes with porches has surpassed two-thirds since the re-design of the SOC in 2005.

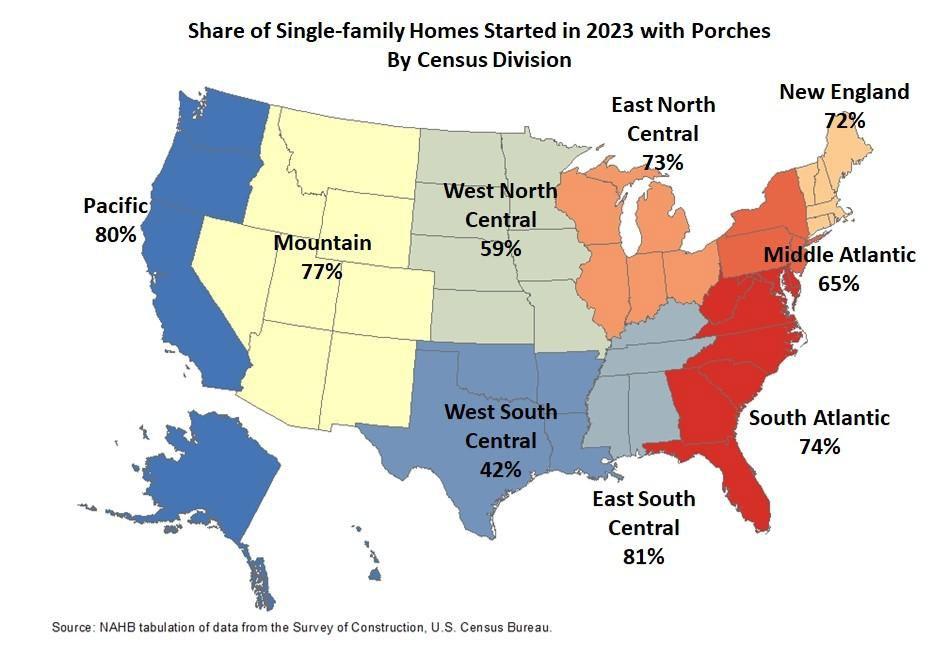

Traditionally, porches on new homes have been most common in the four states that make up the East South Central Census division. That was true again in 2023, although by the narrowest of margins. While 81% of new homes in the East South Central had porches in 2023, that was only a single percentage point higher than the 80% recorded in the Pacific Division. The share was also over 70% in four other divisions: the Mountain (77%), South Atlantic (74%), East North Central (73%) and New England (72%). Once again, the division with the smallest share of poches on new homes was the West South Central (42%). After some significant changes between 2021 and 2022, the 2023 divisional percentages were not drastically different from the ones reported for 2022 in last year’s post.

Detail about the characteristics of porches on new homes is available from the Builder Practices Survey (BPS), conducted annually by Home Innovation Research Labs. Among other things, the 2024 BPS report (based on homes built in 2023) shows that porches continue to be most common on the front of new single-family homes, rather than on the side or rear. When on the front, porches average approximately 100 square feet of floor area, compared to 140 square feet for a side or rear porch, and 200 square feet for a screened-in porch.

On a square foot basis, builders continue to use concrete more than any other material in new-home porches—except in New England, where composite (a blend of usually recycled wood fibers and plastic) is most common, and treated wood, PVC or other plastics, cedar, and natural stone are each used more than concrete.

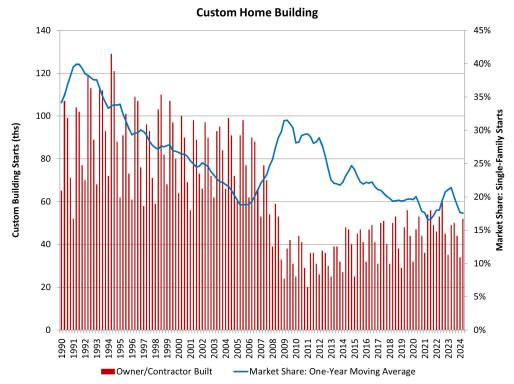

BEST QUARTER FOR CUSTOM HOME Building in Almost Two Years

NAHB's analysis of Census Data from the Quarterly Starts and Completions by Purpose and Design survey indicates gains for custom home building after some recent slowing. Custom home building typically involves home buyers less sensitive to changes for interest rates.

There were 52,000 total custom building starts during the second quarter of 2024. This marks an almost 6% increase compared to the second quarter of 2023 and the best reading since the third quarter of 2022. Over the last four quarters, custom housing starts totaled 180,000 homes, a 5% decline compared to the prior four quarter total (189,000) due to

weakness in prior quarters. After share declines due to a rise in spec building in the wake of the pandemic, the market share for custom homes increased until 2023 and then entered a period of retrenchment. As measured on a one-year moving average, the market share of custom home building, in terms of total single-family starts, has fallen back to just under 18%. This is down from a prior cycle peak of 31.5% set during the second quarter of 2009 and a 21% local peak rate at the beginning of 2023.

Note that this definition of custom home building does not include homes intended for sale, so the analysis in this post uses a narrow definition of the sector. It represents home construction undertaken on a contract basis for which the builder does not hold tax basis in the structure during construction.

BY: ROBERT DIETZ

IMAGINE THE POSSIBILITIES

There has never been a better time to be a Carter Lumber customer in the Cleveland/Akron area. We now have even more resources to provide our customers with quality materials and exceptional service. We’re more than just a lumberyard!

Contact your nearest store location to see how having Carter Lumber as a part of your team can help you grow your business and your bottom line.

BUILDER SENTIMENT IMPROVES Before Critical Fed Meeting

The NAHB/Wells Fargo Housing Market Index (HMI), a measure of home builder confidence , improved off its lowest reading since December 2023 as the housing industry anticipates the beginning of an easing cycle from the Federal Reserve. The HMI rose two points to a level of 41 in September. Home builders are expecting future housing demand will rise as mortgage interest rates settle lower, and that interest rates will improve for construction and development loans. The HMI had weakened during the first part of 2024 amid a higher-for-longer interest rate environment.

However, inflation and labor market data are now clearly reflecting a slowing macroeconomic environment. After failing to show much improvement for a considerable part of the second half of 2023 and early 2024, the broadest measure of consumer inflation — the Consumer Price Index (CPI) — is now back on a cooling trend. The CPI recorded a 2.5% year-over-year pace in August. Shelter inflation — the cost of renting and a proxy for homeownership — continues to be the primary source of inflation, increasing at an elevated 5.2% rate. Shelter inflation has been responsible for a staggering 70% of total consumer inflation over the last year, which is an important reminder of the need for policymakers to find ways to reduce construction costs.

The labor market is slowing as well. For the overall economy, the total number of open jobs has now fallen to 7.67 million, after peaking at 12.2 million in March 2022. The higher the count of open jobs, the tighter the labor market is and the higher the risk of wage-push inflation. However, for the past year, NAHB had estimated that the Fed needed to see the job opening count fall below 8 million in order to begin reducing short-term interest rates. We are now at that point of the business cycle, and monetary policy risk has shifted from overheating inflation risk to weakening labor market risk.

BY: DR. ROBERT DIETZ

The construction labor market has cooled rapidly in recent months as well. The number of open construction market jobs stood at 248,000 in June, after averaging near 400,000 in recent quarters. The demand for construction labor has softened as the number of single-family homes actively under construction has declined and the multifamily development market has rapidly cooled.

The overall labor market has shown other signs of weakening. In August, net job growth was only 142,000 after a downwardly revised estimate of 89,000 in July. The unemployment rate ticked lower to 4.2%; however, it is expected to rise in the coming months as businesses seek to reduce labor costs amid higher interest rates.

Taken together, the Fed is clearly in position to finally reduce the short-term federal funds interest rate on Wednesday. The Fed has held the fed funds top target rate at 5.5% for more than a year and, per the NAHB forecast, is now set to begin a series of rate reductions, ultimately lowering that rate to approximately 3% in the coming quarters. This monetary policy action will reduce lending rates for home builders and land developers, while also continuing to place downward pressure on long-term mortgage interest rates. Thus, while a slowing economy and rising existing home inventory represent housing market risks, lower interest rates will provide upward support for the housing market.

Talking Points on Key Hous ing Issues

October

2024

The following talking points help tell the residential construction industry story to the media, policymakers, NAHB members, local/civic organizations, and consumers.

Key NAHB Housing Issues

1. NAHB has developed a 10-point housing plan to keep housing front and center during this election season. From local state houses to the White House, politicians at all levels of government are taking notice. And our presence at the Republican and Democratic National Conventions this summer helped to keep housing at the forefront of the national agenda.

2. You can help send the message to your local housing or planning officials that housing production should be a priority and that the residential construction industry will be sending a lot of voters to the polls. Learn more at nahb.org/signs.

3. With the expiration of the Tax Cuts and Jobs Act at the end of 2025, tax policy will take center stage next year. If Congress does not act, the nation faces more than $4 trillion in tax increases in 2026. NAHB will fight for our priorities and look at how the tax code might be improved.

4. The Rhode Island Office of Energy Resources and the Rhode Island Builders Association (RIBA) have received a $1.6 million grant from the U.S. Department of Energy to provide energy code training to home builders and other stakeholders. NAHB and RIBA have developed an industry-based training program that can be used as a resource for other state HBAs that may need to adopt updated energy codes.

5. During two separate congressional hearings in July, NAHB testified against an onerous energy codes mandate instituted by HUD and the USDA that requires the agencies to insure mortgages for new single-family homes only if they are built to the 2021 International Energy Conservation Code (IECC). We are asking our members to contact their federal lawmakers and urge them to cosponsor congressional resolution H.J. Res. 170, which would rescind this harmful energy codes rule.

6. In a major victory for NAHB and the housing community, the U.S. Supreme Court cut back sharply on the power of federal agencies to interpret the laws they administer and ruled that courts should rely on their own interpretation of ambiguous laws. The case may prove to be a game-changer for builders and developers who must interact with any part of the federal government.

7. The Federal Reserve began the first of what is expected to be a series of rate cuts in September. This is good news for builders, housing demand and housing affordability. Given the Fed outlook, we expect mortgage rates to decline during 2024 and 2025. Rates on builder and developer loans should moderate as well.

8. The Department of Labor has issued a final rule significantly increasing the salary level for determining overtime pay requirements for certain salaried employees. Effective July 1, 2024, the salary threshold increased the annual salary level from $35,568 to $43,888. It will rise again to $58,656 on Jan. 1, 2025.

9. Housing market snapshot: Single-family housing starts increased in August while multifamily production and new and existing home sales posted declines. Meanwhile, builder confidence in September increased two points to a reading of 41.

Making Housing a Major Election-Year Issue

• This spring, NAHB issued a 10-point housing plan that calls for concrete steps at the local, state and federal levels to address the root of the nation’s housing affordability crisis – the impediments to increasing the nation’s housing supply.

• Our message is strong and concise: The best way to tame shelter inflation (homeownership and rental costs) and to address the nation’s housing affordability challenges is to build more homes.

• This is a message we have hammered home to Congress, the news media, social media, state and local elected officials, and other interested stakeholders who can influence the political debate. You can learn more about our housing plan at nahb.org/plan.

• From local state houses to the White House, our collective voice is being heard as we keep housing front and center during this election season.

• This summer, NAHB Chairman Carl Harris and First Vice Chair Buddy Hughes attended the Republican and Democratic National Convention. Our presence at the national conventions was meant to keep housing at the forefront of the national agenda.

• Thanks to our efforts, the two major parties have put housing front and center as this election campaign enters its home stretch.

• The Republican Party platform calls for cutting regulations that raise housing costs and reducing mortgage rates by slashing inflation.

• It also calls for promoting homeownership through tax incentives and support for first-time buyers.

• Vice President Harris on Aug. 16 announced a plan to build 3 million additional housing units. During the presidential debate on Sept. 10 Harris said she wanted to work with home builders to achieve this goal.

• While NAHB commends Harris for seeking to boost housing production, we also believe her plan needs to address federal regulatory barriers that are preventing builders from boosting housing supply.

• The Harris plan includes a tax credit to help builders construct more entry-level housing and seeks to expand and strengthen the Low-Income Housing Tax Credit.

• On the demand side, Harris is proposing a $10,000 tax credit for first-time buyers and $25,000 downpayment assistance.

• NAHB will continue to work to keep housing atop the national agenda well beyond the election season.

• We look forward to working with Democratic and Republican lawmakers at all levels of government to put into place policies that will allow builders to increase housing production and enable more hardworking families to achieve homeownership and rental housing opportunities.

You Can Help Keep Housing in the Spotlight

• At the Fall Leadership Council meeting in San Antonio, our members had signs that said “We Build, We Vote” on one side and “Let Builders Build” on the flip side of the sign.

• These signs are meant to show that home builders and housing play an important role in this election.

• You can download the signs at nahb.org/signs, and print them at your home office.

• Gather your HBA members for a great photo op.

• When posting your pics, be sure to tag your local housing or planning officials.

• Use the NAHB hashtags #LetBuildersBuild and #WeBuildWeVote.

• This is a great way to spread the message that housing production should be a priority and that the residential construction industry will be sending a lot of voters to the polls.

• Elections have consequences. So be sure to vote.

• And remember: the “Let Builders Build” message can be used all-year round as we know the fight for housing will not end after the election.

Tax Policy an Emerging Issue

• Tax policy will take center stage in Congress in 2025.

• If Congress does not act, the nation faces more than $4 trillion in tax increases in 2026.

• This is because the 2017 Tax Cuts and Jobs Act – which overhauled the tax code and lowered tax rates – expires at the end of 2025.

• Because of this looming giant increase, one thing is certain: Congress will not allow the Tax Cuts and Jobs Act to expire as a whole.

• Each party has its own tax priorities, and the November elections will determine what the future tax code looks like.

• NAHB will fight for our priorities – including keeping the 20% pass-through tax deduction, the full deductibility of net business interest expense for real estate, the higher Alternative Minimum Tax exemption, and higher estate tax threshold, to mention a few.

• This also presents an opportunity to look at how the tax code might be improved.

• For example, because the tax law raised the standard deduction, most home owners no longer claim the mortgage interest deduction.

• This makes the mortgage interest deduction vulnerable to repeal, but also raises the question whether it should be modernized to work effectively.

• We are laying out the issue and soliciting feedback.

• We discussed this looming tax fight at the Fall Leadership meeting. We are also conducting a series of tax listening sessions with our members about our strategy as well as soliciting input on whether we should look at changes to the mortgage interest deduction to make it more effective.

Landmark Codes Training Deal for NAHB, Rhode Island HBA

• The Rhode Island Office of Energy Resources and the Rhode Island Builders Association (RIBA) have received a $1.6 million grant from the U.S. Department of Energy (DOE) to provide energy code training and educational resources to building inspectors, designers, home builders and construction trades professionals in the state.

• RIBA will focus on training home building professionals on the new state energy code using materials developed through a partnership with NAHB.

• The new state code is based on the 2024 International Energy Conservation Code (IECC) and is a significant change from the previous requirements. RIBA’s goal is to bring the building industry in the state up to speed on the new code quickly to ensure continuous supply of homes and remodels.

• NAHB began working with RIBA last year to help the HBA develop training modules on various aspects of the new code. The two organizations worked over a short period of time to produce and launch a comprehensive and easy-to-understand series of course modules designed for builders by builders.

• This industry-based training program creates a resource for other state HBAs who may need to adopt updated energy codes.

• For more information, go to nahb.org/codes or contact Vladimir Kochkin at 202-2668574.

NAHB Testifies on Capitol Hill Against Onerous Energy Codes

• During two separate congressional hearings on July 10 and July 24, NAHB testified against an onerous codes policy implemented by the U.S. Department of Housing and Urban Development and the U.S. Department of Agriculture. The policy requires the agencies to insure mortgages for new single-family homes only if they are built to the 2021 International Energy Conservation Code (IECC) and HUD-financed multifamily housing is built to 2021 IECC or ASHRAE 90.1-2019.

• Studies have shown that requiring new construction to adopt to the 2021 IECC can add as much as $31,000 to the price of a new home and that it would require up to 90 years for a home buyer to realize a payback on the added upfront cost of the home. That’s not a reasonable trade-off for a new home buyer.

• In addition to negatively impacting potential home buyers, these increased requirements and higher costs stemming from the stringent 2021 IECC can result in decreased production and longer permitting and construction times, further exacerbating housing affordability challenges.

• Our message on the need to reverse this ill-conceived policy is resonating with many members of Congress and we have made progress on several fronts to halt this costly codes mandate in its tracks.

• On June 27, the House Transportation, Housing and Urban Development appropriations committee approved language that will prevent HUD from using federal funds to implement this rule. This is the exact ask that NAHB members were seeking in their meetings with their lawmakers during the June 12 Legislative Conference

• At NAHB’s urging, Rep. Warren Davidson (R-Ohio), along with 38 other lawmakers, on June 27 introduced a Congressional Review Act resolution of disapproval (H.J. Res. 170) to allow Congress to overturn this harmful energy codes rule.

• We are asking our members to contact their member of Congress and call on them to cosponsor this important resolution. Please take a couple of minutes and log on to https://builderlink.org/take-action-now/. This site will allow you to send a letter to your lawmaker calling on them to support H.J. Res. 170.

• It should also be noted that thanks largely to NAHB’s efforts HUD did extend the compliance dates for these new requirements. The effective date of the rule is May 28, 2024, but the compliance dates for the building code mandates are:

o 18 months after the effective date for single-family homes;

o 12 months after the effective date for multifamily projects; and

o 24 months after the effective date for homes in “persistent poverty rural areas.”

• NAHB will continue to pursue every possible means to prevent HUD and USDA’s adoption of the 2021 IECC.

Supreme Court Verdict a Win for Common-Sense Regulations

• In a major victory for NAHB and the housing community, the U.S. Supreme Court has issued a ruling to reform the nation’s broken regulatory rulemaking process ensuring that federal courts interpret federal statutes and no longer defer to the interpretations of federal bureaucrats.

• The Supreme Court ruling is an important step forward to advance meaningful regulatory reform because it means that federal agencies can no longer continuously change the law – and the intent of Congress – by implementing their own interpretation of statutes as long as those interpretations are viewed as being “reasonable.”

• The case may prove to be a game-changer for builders and developers who must interact with any part of the federal government.

• For home building, this means that every federal agency that builders and developers must deal with – from the U.S. Department of Housing and Urban Development, to the Environmental Protection Agency, the Department of Labor, the Occupational Safety and Health Administration, and more – will have less discretion to impose new regulations that Congress did not clearly authorize.

• The Supreme Court verdict was made in two cases – Relentless v. Dept. of Commerce and Loper Bright Enterprises v. Raimondo – where the plaintiffs sought to overturn a previous decision made by the nation’s highest court 40 years ago that gave the government an unfair advantage when someone challenges a regulation in court. NAHB filed a friend-of-the-court brief on behalf of both plaintiffs.

• In 1984, the Supreme Court issued an opinion that created the “Chevron deference,” which requires courts to abide by a statute if it is “clear,” but also requires courts to defer to a federal agency’s interpretation of an unclear statute if the interpretation is “reasonable,” even if it is not the best interpretation.

• In other words, Chevron gave federal agencies wide latitude to interpret the scope of the nation’s laws.

• The Supreme Court’s verdict ensures the power of the legislature, executive and judicial branches will no longer be merged in the hands of unelected bureaucrats.

Fed Starts Cutting Interest Rates

• In September, the Federal Reserve began the first in a series of rate cuts.

• This is a positive development that will help lower mortgage rates and costs on builder and developer loans.

• Lower interest rates will provide upward support for the housing market. By the end of 2025, NAHB expects mortgage rates will be around 5.75% and move down to about 5.5% by the end of 2026.

• However, the declines in coming quarters will be choppy, not a smooth decline.

• Moderating rates should boost housing demand in most markets and opportunities will expand for prospective home buyers currently waiting on the sidelines.

• highlighting the latest initiatives. Available on nahb.org, these videos are easy to download and share with local lawmakers or industry colleagues via social media.

Federal Overtime Threshold to Rise Again on Jan. 1, 2025

• The U.S. Department of Labor (DOL) issued a final rule this summer that significantly increasing the salary level for determining overtime pay requirements for certain salaried employees.

• Effective July 1, 2024, the annual salary level threshold increased from $35,568 to $43,888. It will rise again to $58,656 on Jan. 1, 2025.

• Additionally, beginning July 1, 2027, salary levels will update every three years using upto-date wage data.

• NAHB has joined a coalition of business groups challenging the new overtime rule, alleging in a lawsuit that the Department of Labor exceeded its statutory authority and acted arbitrarily and capriciously.

• NAHB also submitted comments when DOL issued the proposed rule in late 2023, citing the negative impact such a significant increase would have on housing affordability, among other concerns.

• Additionally, during multiple DOL listening sessions, NAHB members questioned the timing of a salary level update, as the latest update went into effect less than five years ago.

Housing Market Snapshot

Housing Starts (August 2024)

Home Sales* (August 2024)

New: 716,000↓

: 3.86 million↓

Median Home Prices (July 2024)

New: $420,600↓

Existing: SF: $422,100↑

*Seasonally Adjusted Annual Rate; Arrows indicate direction from previous month for starts and sales and year for prices.

NAHB/Wells Fargo Housing Market Index – The index, which measures builder confidence in the market for newly built single-family homes, rose two points to 41 in September from a reading of 39 in August. Any number below 50 indicates that more builders view sales conditions as poor than good.

NAHB Chief Economist Robert Dietz’s analysis: “The Federal Reserve began what is expected to be the first in a series of rate cuts in September. Easing monetary policy over the next year will produce downward pressure on mortgage interest rates and also lower the interest rates on land development and home construction business loans. However, due to the mortgage interest lock-in effect, declining interest rates will mean rising existing home inventories and some additional new competition for home builders. And while a more favorable interest rate environment is welcome news, the industry must still deal with a shortage of workers and lots, and supply chain concerns for some building materials. The only sustainable way to ease high housing costs is to implement policies that allow builders to construct more attainable, affordable housing.”

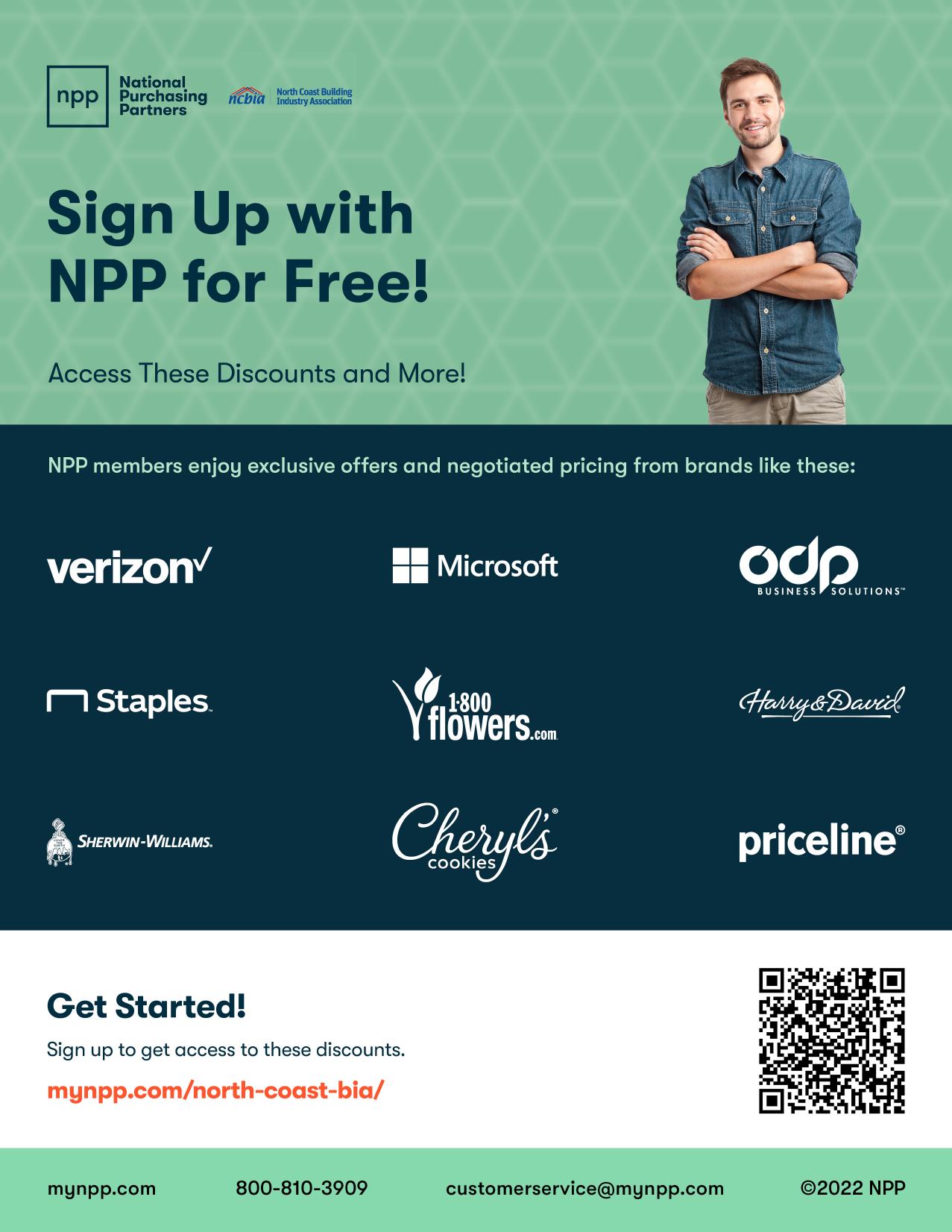

ScotchBlue™

pricing on popular products

821-8026 – 24mm | Ea.

• Once your account is verified, you can log in and save Contractor Series

SIGN UP TODAY!

• Visit mynpp.com/north-coast-bia/ North Coast BIA members can sign up with NPP for free to access this discount and more.

• Fill out and submit the registration form

offers contract pricing to more than 350,000 company and employee members coast-to-coast, giving the buying power of large corporations to businesses of all sizes. NPP has contributed millions of dollars in proceeds to research autoimmune diseases. Join NPP for free. There is no obligation to purchase.

Booth spaces are LIMITED and available on a 1st Come, 1st Served Basis! 2024 SOLD OUT - Act now to secure your booth!

BOOTH INFORMATION

Electric is optional and available on a 1st Come, 1st Served Basis!

Will you need electricity? _______ YES _______ NO ______# of Booth Spaces ____________TOTAL AMOUNT DUE

I understand that I have contracted for exhibit space by signing this contract and I am liable for the full cost of the booth space. I also understand that the final location of space will be determined by show management when payment is made in full. The undersigned represents that he/she is fully authorized to execute and complete this agreement. The undersigned also understands and agrees to the rules and regulations on the reverse side of this contract.

Authorized Exhibitor Signature

PAYMENT METHOD:

Please Indicate how you would like to pay for your booth space.

Printed Name ___Invoice ___Check Enclosed ___VISA/MC/AMEX/DISC*

*If you select credit card, our office will call for your card information.

Please send completed form to Judie@ncbia.com or 5321 Meadow Lane Court - B, Suite 23 Sheffield Village, OH 44035

Event Sponsors: **A $5.00 Convenience Fee will be charged for all Credit Card Payments

NAHB SEEKS MEMBER INPUT ON Modernizing the Mortgage Interest Deduction

With the 2017 tax cuts expiring at the end of 2025, one of NAHB’s key initiatives in the coming months will be fighting for our tax priorities as Congress addresses the upcom ing tax cliff. NAHB will host five online listening sessions with the membership to discuss next year’s federal tax debate. The listening sessions will provide an overview of NAHB’s 2025 tax strategy, with a focus on incentivizing homeownership.

We will seek input on modernizing the mortgage interest deduction by converting it into a tax credit, which could have a broad effect on the housing industry.

Members are welcome to attend the session specific for their region, which will include regional details, or the session that best suits their schedule. View NAHB’s regional leadership map to confirm your region.

Please use the appropriate registration form to secure your spot. (Member login is required.) Registration will close on Oct. 27 at 5 p.m. ET.

LIMITED TIME OFFER!

Earn 30¢ per gallon for the first three months once you reach 100 gallons in each calendar month. Thereafter, save 6cpg for every gallon pumped.*

Th e 7-Eleven Comm er ci al Fl ee t M ast er ca rd

Fleet Savings Made Easy

Perfect fit for mid-sized to larger fleets that need the added convenience of fueling where Mastercard® is accepted. With the 7-Eleven Commercial Fleet Mastercard®, your fleet can customize reports for a complete fuel management solution.

Rebates & Savings

Earn 30¢ per gallon for the first three months once you reach 100 gallons in each calendar month. Thereafter, save 6cpg for every gallon pumped.*

Security & Fraud Controls

Enjoy the security of advanced card prompts.

Earn 30¢ per gallon for the first three months once you reach 100 gallons in each calendar month. Thereafter, save 6cpg for every gallon pumped.*

Customize and download cost and performance reports monthly or in real-time.

Monitor transactions and manage your account online, in real-time.

Use card prompts to help prevent misuse. Simple online access.

Accepted at your favorite 7-Eleven & Speedway locations and anywhere Mastercard is accepted, regardless of fuel brand.**

Name

Online Control & Visibility

Set card controls and access detailed reporting online anytime.

The 7F LEET Diesel Network Ma stercard ®

Fueling your fleet for the road ahead.

Diesel Network Mastercard offers significant discounts on diesel at the over 260 locations that make up the 7FLEET Diesel Network as well as discounts on commercial truck lane diesel across the AMBEST network.

Network Discounts

Save an average of 53cpg on truck diesel lane gallons fueled in the 7FLEET Diesel Network.*

Security & Fraud Controls

Enjoy the security of advanced card prompts.

Online Control & Visibility

Set card controls and access detailed reporting online anytime.

Customize and download cost and performance reports monthly or in real-time.

Monitor transactions and manage your account online, in real-time.

Use card prompts to help prevent misuse.

Simple online access.

Accepted at your favorite 7-Eleven & Speedway locations and anywhere Mastercard is accepted, regardless of fuel brand.**

7-Eleven Fleet Card Program Application

Please send the application to

INFORMATION – Required.

below.

AUTHORIZED REPRESENTATIVE – Required.

Application Terms: By signing this Application, the Authorized Representative represents, warrants, and agrees that: (a) he or she is authorized to apply to FLEETCOR TechnologiesOperating Company, LLC (“FLEETCOR”), a Louisiana limited liability company, for an unsecured, partially secured, or fully secured line of credit (“Account”) on behalf of the company identified above (“Client”); (b) FLEETCOR may obtain Client’s credit report and check Client’s credit standing when processing this Application or periodically evaluating any resulting Account’s creditworthiness; (c) this Application is subject to approval and acceptance by FLEETCOR; (d) if the Application is approved by FLEETCOR in Louisiana, the resulting Account: (i) will be governed by Louisiana law; (ii) will not be a revolving credit account and the Amount Due/Total Amount Due shown on each Account Statement will be due and payable on the Due Date shown on the Statement; (iii) will be used solely for commercial purposes and not for personal or household purposes; (iv) will be suspended, and the Client’s redit history may be reported to credit reporting agencies, if the Client’s unpaid balance ever meets the Account’s Credit/Spend Limit; and (e) acceptance, signing (in whatever form), or use of any of the Cards issued to Client will constitute Client’s acceptance of the Client Agreement available at www.fleetcor.com/terms/7-Eleven-mc or www.fleetcor.com/terms/7-Eleven-dn Equal Credit Opportunity Act Notice. The Federal Equal Credit Opportunity Act prohibits creditors from discriminating against credit applicants on the basis of race, color, religion, national origin, sex, marital status, age (provided that the applicant has the capacity to enter into a binding contract); because all or part of the applicant’s income derives from any public assistance program; or because the applicant has in good faith exercised any right under the Consumer Credit Protection Act. The federal agency that administers compliance with this law concerning this creditor is the Federal Trade Commission, Equal Credit Opportunity Act, Washington, D.C. 2 0580. FLEETCOR considers your privacy important. View our privacy policy available at www.fleetcor.com/privacy-policy to find out more.

I agree to the Application Terms and the Client Agreement (Please check box) ☐

BUSINESS OWNER(S) / PERSON WITH SIGNIFICANT MANAGEMENT RESPONSIBILITY – Required.

To help fight financial crimes, the U.S. Department of Treasury require financial institutions to obtain, verify, and record information about beneficial owners of entities opening accounts. Beneficial owners are persons who, directly or indirectly, own 25% or more of the entity. We may use third-party resources to verify your identity. For questions about this regulation and how FLEETCOR uses and protects this data, please speak with your sales representative. Patriot Act Notice. Section 326 of the USA PATRIOT Act mandates that FLEETCOR verify and record certain information about you (the Client, Authorized Representative, or anyco-maker or guarantor) while processing this Application.

Beneficial Owner (Individuals who own 25% or more of a Legal Entity)* ☐ Not Applicable, Sole Proprietor, Government Entity, Not

this person have significant responsibility for managing the legal entity listed above?