North Coast Building Industry Association (NCBIA) BUILDER newsletter is the official newsletter of the NCBIA and is published monthly by the NCBIA. The NCBIA is an affiliate of the Ohio Home Builders Association (OHBA) & the National Association of Home Builders (NAHB).

Advertising Policy - The North Coast Building Industry Association reserves the right to reject advertising in the Builder newsletter based on content. Acceptance of advertising does not imply endorsement of the product or service advertised.

5321 Meadow Lane Court - B, Suite #23 Sheffield Village, OH

Thursday, January 16, 2025

January Member Mixer5 - 7 PM

Rusty Barrel 27026 Center Ridge Road, Westlake

Saturday, February 22, 2025

2025 Installation Night 5:30-8:00 PM

American Legion Post 211 31972 Walker Road, Avon Lake

Tuesday-Thursday

February 25-27, 2025

NAHB International Builders Show Las Vegas Convention Center Las Vegas, Nevada

Check the website at www.ncbia.com for up-to-date changes, additions, and corrections to these events!

URGENT REQUEST

Needed: 1 Delegate for NAHB & 1 Alternate

Please contact Judie Docs if you are interested by January 15, 2025 (judie@ncbia.com – 440-934-1090/2).

WELCOME OUR 2025 NCBIA President

Happy New Year! I’m John Toth, the 2025 NCBIA president. I want to thank Tim King of K. Hovnanian Homes for his leadership and guidance in 2023 & 2024. Tim generously served as President for two years for the NCBIA.

I look forward to working with our Executive Officer, Judie Docs, her staff, the board of directors, committee chairs, and volunteers to move the association forward.

I invite you to get involved if you’re a newer association member. The association and its members have so much to offer. We can learn from each other. If you’re a veteran member of the association, I invite you to introduce yourself to new members, get to know them, and share with them what the NCBIA has to offer & how being a member has helped you and your business grow. The association grows because all of its members work together. If you aren’t involved, I challenge all members to become more involved- we have many opportunities to volunteer or sponsor industry, social, & educational events. I challenge all current and past leaders of the association to become more involved. New members look to us as an example.

Our focus is on bringing brand awareness to the public, new members, and potential new members, as well as workforce development and mentoring our younger members to help prepare them to be future leaders of the association. The North Coast Building Industry Association and its members are a great resource to the public whether they’re looking to build that dream home, remodel their current home, or need a roofer to fix that leaky roof. One of the reasons the building industry’s recovery is lagging is due to a labor shortage, even though there is a housing shortage. College isn’t for everyone & we need to encourage our younger generation to look at a career in the trades. Starting salaries for trades are good, and the training isn’t too long or expensive compared to 4 years of college. If the association continues to grow and thrive, we have to look at more of our younger members getting involved and becoming leaders of the future. We all have something to offer to each other & the association. Let’s grow together!

Also remember that your membership in the NCBIA is really three memberships in one—you are also a member of the National Association of Home Builders and Ohio Home Builders Association. We have lobbyists working on our industry’s behalf every day in Washington and the state house. I encourage all members to log on to the NAHB and NCBIA websites and see what’s going on. If you need help with logging on to the NCBIA or NAHB websites, the NCBIA staff can help.

I welcome your thoughts and comments and am always available to listen. We learn by listening more and talking less. Here’s to a successful 2025.

John Toth, Floor Coverings International

HELP US Build!

by Judie Docs, CSP, MCSP, MIRM, CMP, CGP

As you know, membership in the North Coast Building Industry Association offers numerous benefits and keeps business owners informed about important, ever-changing issues, trends, and legislation in their marketplace.

Therefore, we ask for your help in recruiting new members to benefit them and us. Some business owners might say their schedule is demanding enough now, and the thought of adding one more activity to their busy calendar is unbearable. So why should they try to cram time into their already-hectic schedules to join an industry association or other professional organization? I think if you ask them what they need help with, who they want to meet, or what they want to learn, we can help them.

The NCBIA, OHBA, and NAHB know what is going on in the industry, and it is shared. Benefits are many, including opportunities in leadership roles, education and hundreds of discounts.

Membership can benefit your company's employees; it also projects a positive image of your firm to your customers. Membership in associations shows a business’ initiative, its engagement in a particular trade, and its commitment to staying abreast of current developments in the market. Refer to the cover for other ways membership can help.

Again, one of the most significant advantages of association membership is the networking and camaraderie among members. However, to benefit from this, you must participate and be an active member within your association. Paying your annual dues is not enough to reap the benefits of association membership. You must also invest time and effort in association activities and become involved. Simply put, what you get out of association membership is directly relative to what you put in.

We appreciate all who renew their membership, and we ask you to share the value with other business owners you know. Please refer to the helpful list of potential companies that will make the NCBIA even stronger than it is today.

Event Sponsors:

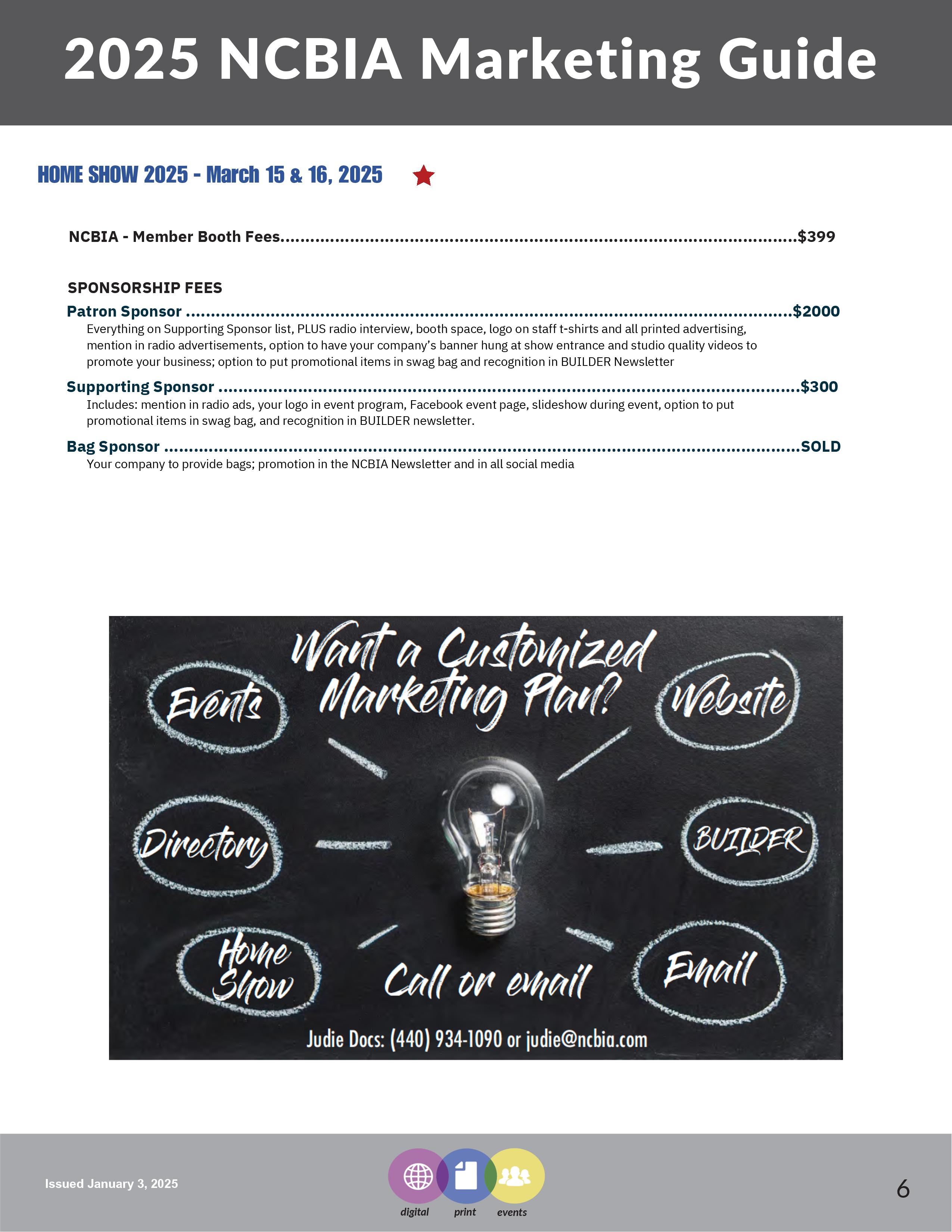

EVENT SPONSOR

Member: $2000

Non-Member: $2500

Everything on Supporting Sponsor list, PLUS radio interview, booth space, logo on staff t-shirts and all printed advertising, mention in radio advertisements and option to have your company’s banner hung at show entrance!

Saturday, March 15th 9-5 Sunday, March 16th 10-3

Spitzer Conference CenterLorain County Community College 1005 North Abbe Road, Elyria

My company would like to sponsor the 2025 NCBIA Home Show. (Please select below)

Event Sponsor($2000) Member Supporting Sponsor ($300)

SPONSOR INFORMATION

SPONSOR

Member: $300

Non-Member: $500

Includes: mention in radio ads, your logo in event program, Facebook event page, slideshow during event, option to put promotional items in swag bag, and recognition in BUILDER newsletter.

PAYMENT METHOD:

Please Indicate how you would like to pay for your sponsorship.

*If you select credit card, our office will call for your card information.

QUESTIONS? CONTACT THE NCBIA www.ncbia.com (440) 934-1090 judie@ncbia.com

Supporting Sponsors:

Sponsor:

PEYE ON HOUSING

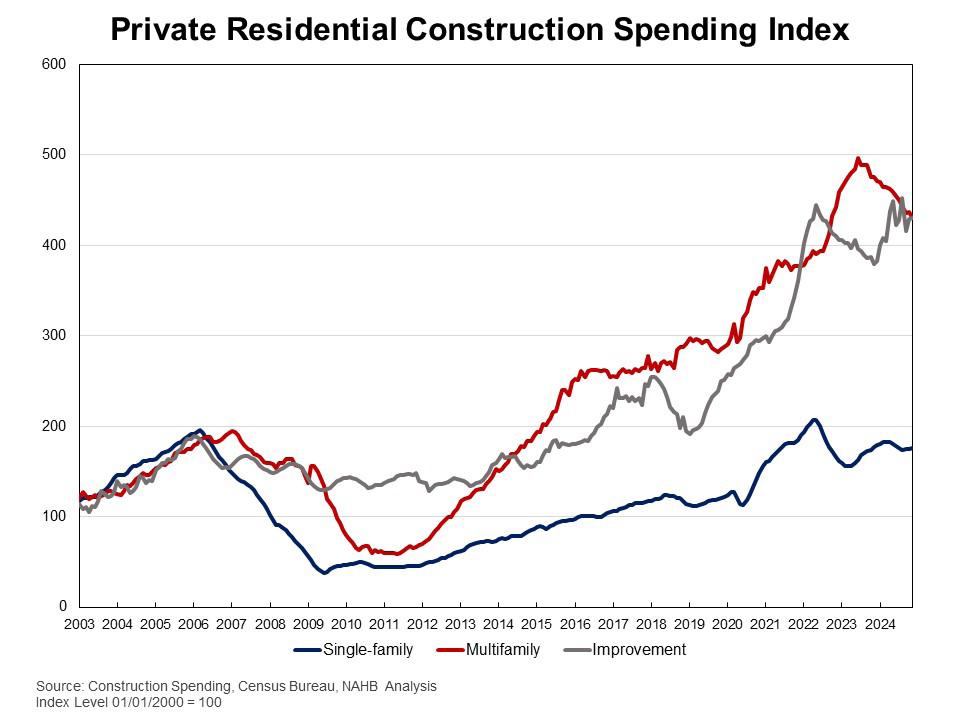

PRIVATE RESIDENTIAL CONSTRUCTION Spending Inches

rivate residential construction spending edged up by 0.1% in November 2024, according to the latest U.S. Census Construction Spending data. Year-over-year, the November report showed a 3.1% increase.

The monthly increase in total private construction spending was primarily driven by higher spending on single-family construction and residential improvements. Single-family construction spending inched up by 0.3% for the month. This marks a continuation of growth after a five-month decline from April to August, aligning with steady builder confidence seen in the Housing Market Index . However, single-family construction remained 0.7% lower than a year ago. Improvement spending rose by 0.4% in November and was 13.4% higher compared to the same period last year. In contrast, multifamily construction spending declined by 1.3% in November, following a 0.3% increase in October. Compared to a year ago, multifamily construction spending was still 9.5% lower.

Up in November

BY: NA ZHAO

Spending on private nonresidential construction was up 1.7% over a year ago. The annual private nonresidential spending increase was mainly due to higher spending for the class of manufacturing ($23.4 billion), followed by the power category ($6.1 billion).

ON HOUSING

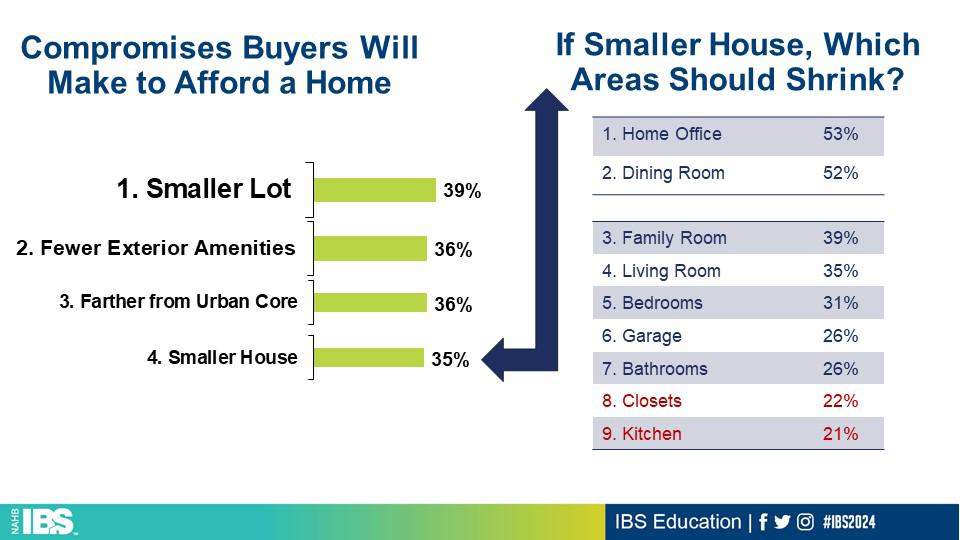

TOP POSTS – TOP COMPROMISES Buyers Will Make to Reach Homeownership

BY: ROSE QUINT

With the end of 2024 approaching, NAHB’s Eye on Housing is reviewing the posts that attracted the most readers over the last year. In May, Rose Quint shared key takeaways of NAHB’s study of home buyers. High mortgage rates and double-digit growth in home prices since COVID-19 have brought housing affordability to its lowest level in more than a decade. Given this reality, a recent NAHB study on housing preferences* asked home buyers about which specific compromises they would be willing to make to achieve homeownership. For 39% of buyers, accepting a smaller lot is the path to affording a home. This finding highlights the paramount importance of reforming zoning laws that mandate lot sizes, as nearly 4 out of 10 buyers would be willing to give up land in exchange for owning a home. For 36% of buyers, accepting fewer exterior amenities is the way to homeownership—they will simply add that deck or patio at some point in the future. Another 36% were willing to move farther from the urban core and 35% will accept a smaller house if that’s what it takes to buy it. But what areas of the home, specifically, should shrink to reduce the overall footprint of the home? Most buyers who will take the smaller house compromise sent builders and architects a clear message: shrink the home office (53%) and the dining room (52%) to save on square footage. Also, loud and clear in the message: leave the kitchen (only 21% would want that smaller) and closet space (22%) alone.

* What Home Buyers Really Want, 2024 Edition sheds light on the housing preferences of the typical home buyer and is based on a national survey of more than 3,000 recent and prospective home buyers. Because of the inherent diversity in buyer backgrounds, the study provides granular specificity based on demographic factors such as generation, geographic location, race/ethnicity, income, and price point.

Terry

THANK YOU SPIKES!

Jason

Chris Majzun Sr.

GREEN SPIKE (50-99 SPIKE CREDITS)

Jim

Jason Scott Greyhawk Development

Liz Schneider Dollar Bank

LIFE SPIKE (25-49 SPIKE CREDITS)

Steve Schafer ................ Schafer Development .................................

BLUE SPIKE (6-24 SPIKE CREDITS)

Mark McClaine 84 Lumber

John

Dave LeHotan

Chris Collins Carter Lumber

Ken Cassell Cassell Construction

Ashley Oates 84 Lumber

John Blakeslee Blakeslee Excavating, Inc 12.00

Scott Kosman Lakeland Glass 9.50

Mike Meszes ................ DRC Construction ...................................... 8.00

Tim Hinkle ................. Green Quest Homes ............................... 6.50

Jim Tipple Maranatha Homes 6.50

Lou LaGuardia Repros Engineering 6.00

IMAGINE THE POSSIBILITIES

Thanks for Renewing! Applying for Membership

Sam Hudspath, All Construction Services, Inc.

Fred Miller, Azek Co., Building Products Division

Dan Bennett, Bennett Builders & Remodelers

Kenneth Brady, Brady Plumbing & Heating

Drew Alurovic, Buckeye Community Bank

Tom Caruso, Caruso Cabinets

Chris Ferguson, Ferguson Construction

Joe Schill, Green Impressions

Jason Scott, Greyhawk Development, LLC.

Matt Hobart, Honey Dudes Handyman Service

Tammy Koleski, Howard Hanna Real Estate

Tim King, K. Hovnanian Homes

Brett Kopf, Kopf Builders

Scott Kosman, Lakeland Glass

Bill Perritt, Perritt Building

Rikk Mayer, Renaissance Restoration

Theresa Riddell, The Nelson Agency

Lindsay Yost-Bott, Dale Yost Construction

Gary Kaminski, Kaminski Roofing

Dustin Gray, Gotcha Covered of Avon

EYE ON HOUSING

NEW HOME SALES Rose in November

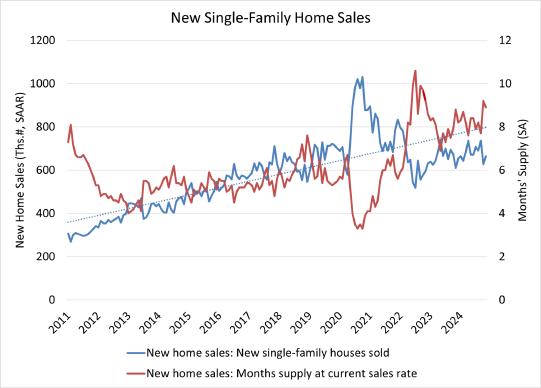

In November 2024, the U.S. housing market experienced a significant boost, with sales of new single-family homes reaching a seasonally adjusted annual rate of 664,000, according to newly released data from the U.S. Department of Housing and Urban Development and the U.S. Census Bureau. This marks a 5.9% increase from October’s revised figures and an 8.7% rise compared to November 2023. November new home sales are up 2.4% on a year-to-date basis.

A new home sale occurs when a sales contract is signed, or a deposit is accepted. The home can be in any stage of construction: not yet started, under construction or completed. In addition to adjusting for seasonal effects, the November reading of 664,000 units is the number of homes that would sell if this pace continued for the next 12 months.

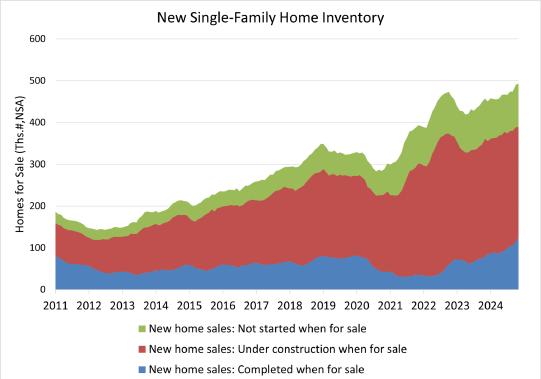

New single-family home inventory in November remained elevated at a level of 490,000, up 8.9% compared to a year earlier. This represents an 8.9 months’ supply at the current building pace. A measure near a six months’ supply is considered balanced.

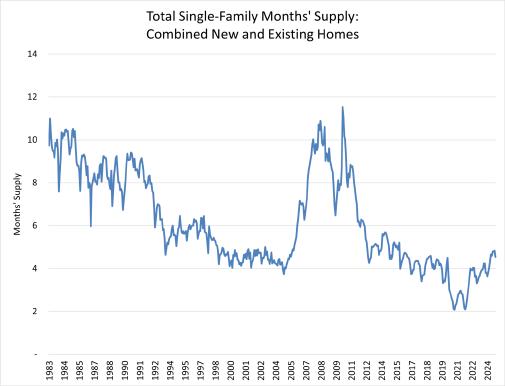

While an 8.9 months’ supply may be considered elevated in normal market conditions, there is currently only a 3.8 months’ supply of existing single-family homes on the market. Combined, new and existing total months’ supply remains below historic norms at approximately 4.5 months, although this measure is expected to increase as more home sellers test the market in the months ahead.

A year ago, there were 79,000 completed, ready-to-occupy homes available for sale (not seasonally adjusted). By the end of November 2024, that number increased 57% to 124,000. However, completed, ready-to-occupy inventory remains just 25% of total inventory, while homes under construction account for 54% of the inventory. The remaining 21% of new homes sold in November were homes that had not started construction when the sales contract was signed.

The median new home sale price in November edged down 5.4% to $402,600 and is down 6.3% from a year ago. In terms of affordability, the share of entry-level homes priced below $300,000 has been steadily falling in recent years. Only 25% of the homes were priced in this entrylevel affordable range, while 31% of the homes were priced above $500,000. Most of the homes were priced between $300,000-$500,000.

Regionally, on a year-over-year basis, new home sales are up 13.6% in the South and 10.0% in the Midwest. New home sales are down 1.4% in the West and 11.5% in the Northeast.

EYE ON HOUSING

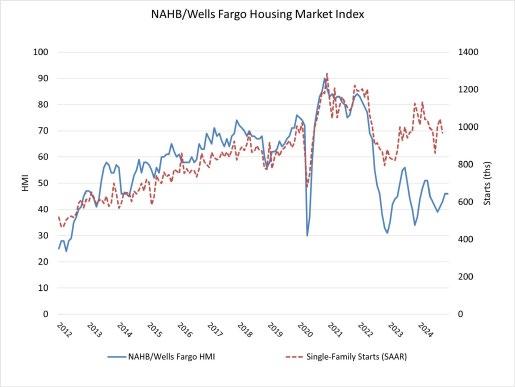

BUILDER CONFIDENCE STEADY BUT SIGNS of Future Optimism in 2025

BY: ROBERT DIETZ

Builder sentiment held steady to end the year as high home prices and mortgage rates offset renewed hope about a better regulatory business climate in 2025. Along those lines, builders expressed increased optimism for higher sales expectations in the next months.

Builder confidence in the market for newly built singlefamily homes was 46 in December, the same reading as last month, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI).

While builders are expressing concerns that high interest rates, elevated construction costs and a lack of buildable lots continue to act as headwinds, they are also anticipating future regulatory relief in the aftermath of the election. This is reflected in the fact that future sales expectations have increased to a nearly three-year high.

NAHB is forecasting additional interest rate cuts from the Federal Reserve in 2025, but with inflation pressures still present, we have reduced that forecast from 100 basis points to 75 basis points for the federal funds rate. Concerns over inflation risks in 2025 will keep long-term interest rates, like mortgage rates, near current levels with mortgage rates remaining above 6%.

The latest HMI survey also revealed that 31% of builders cut home prices in December, unchanged from November. Meanwhile, the average price reduction was 5% in December, the same rate as in November. The use of sales incentives was 60% in December, also unchanged from November.

Derived from a monthly survey that NAHB has been conducting for more than 35 years, the NAHB/Wells Fargo HMI gauges builder perceptions of current single-family home sales and sales expectations for the next six months as “good,” “fair” or “poor.” The survey also asks builders to rate traffic of prospective buyers as “high to very high,” “average” or “low to very low.” Scores for each component are then used to calculate a seasonally adjusted index where any number over 50 indicates that more builders view conditions as good than poor.

The HMI index gauging current sales conditions held steady at 48 while the gauge charting traffic of prospective buyers posted a one-point decline to 31. The component measuring sales expectations in the next six months rose three points to 66, the highest level since April 2022.

Looking at the three-month moving averages for regional HMI scores, the Northeast increased two points to 57, the Midwest moved two points higher to 46, the South posted a two-point gain to 44 and the West fell one point to 40. The HMI tables can be found at nahb.org/hmi.

2024 OHBA YEAR IN REVIEW

OHBA ACCOMPLISHED HUGE FEAT IN ENSURING REMODELING COVERED UNDER HOME CONSTRUCTION SERVICE SUPPLIER ACT

After multiple appeals court opinions ruling ‘remodeling’ was not construction, thus covered by the Consumer Sales Practices Act and subject to strict liability and treble damages, OHBA went to the legislature to clarify the law, as intended. In a huge feat before the legislature broke for summer recess, OHBA was successful with an amendment to include remodeling in the definition of ‘home construction service’ to be covered by the Home Construction Services Suppliers Act.

OHBA STREAMLINED RESIDENTIAL DEVELOPMENT PROPERTY TAX EXEMPTION PROCESS

After successfully getting changes in the law enacted to exempt the increase in value of residential development property until the lot is sold or construction begins, OHBA was again victorious in streamlining the application process. Changes in the approving authority and appeals process shortened the implementation timing significantly

OHBA TESTIFIED ON LACK OF SUPPLY IN

SENATE SELECT COMMITTEE ON HOUSING

OHBA President, Enzo Perfetto, and Executive Officer, Vince Squillace testified on behalf of OHBA bringing both experience as a builder and industry expert to reiterate the impact of regulation and the importance of private development in the critical lack of housing supply.

OHBA provided a list of recommendations, including but not limited to line extension costs, building code review, land development standards, referenda and zoning reform, among others.

TECHNICAL FEASIBILITY OF ARC FAULT PROVISIONS CHALLENGED

With the most recent adoption of the 2023 NEC and expansion in prior versions of the NEC, OHBA urged members having any issues with Arc fault and Dual function breakers across multi-family and single-family business to send along to the Residential Construction Advisory Committee (RCAC) and OHBA for consideration. One of the statutory requirements for the review of any code change is ‘technical feasibility’ giving OHBA an avenue to challenge based in the revised code.

MISTAKE IN ADOPTION OF NEC 2023 OHIO EXCEPTION CORRECTED

The 2023 NEC was set to become effective March 1, 2024. After learning an exception to GFCI requirements intended by the RCAC/BBS to be included in the new code was mistakenly left out of the final rule, OHBA ensured it was to be corrected immediately.

The GFCI exception for sump pumps maintained from the current code remains in the 2023 NEC after the Board of Building Standards refiled the corrected rule with the Joint Committee on Agency Rule Review (JCARR). The need to refile resulted in the effective date being pushed back by at least 30 days while the corrected rule went through the JCARR review before final filing.

OHBA SUPPORTED VARIOUS APPROACHES TO ADDRESS HOUSING SHORTAGE

OHBA continued to urge legislators, regulators, and industry partners to look at the impact of regulation and land development costs. Developed lots are a crucial piece to the housing puzzle; this remained the consistent message from OHBA in these ongoing discussions. OHBA urged lawmakers and industry partners to focus on what can be done to deal with the shortage of available, reasonably priced lots where additional homes can be built. Infrastructure needs, development standards, utility capacity, referenda, and a meaningful comprehensive plan were a few discussion points.

OHBA SUPPORTED VARIOUS APPROACHES TO ADDRESS HOUSING SHORTAGE

OHBA continued to urge legislators, regulators, and industry partners to look at the impact of regulation and land development costs. Developed lots are a crucial piece to the housing puzzle; this remained the consistent message from OHBA in these ongoing discussions. OHBA urged lawmakers and industry partners to focus on what can be done to deal with the shortage of available, reasonably priced lots where additional homes can be built. Infrastructure needs, development standards, utility capacity, referenda, and a meaningful comprehensive plan were a few discussion points.

MONITORED IMPLEMENTATION OF ELEVATOR CONTRACTOR/MECHANIC LICENSING RULES

After passage of legislation, those who install or maintain elevators had one year to obtain an elevator contractor's or elevator mechanic's license. Contractors and mechanics will have until Nov. 1, 2025, to be licensed. Previously, only elevator inspectors were required to be licensed.

OHBA was successful in exempting licensure for those performing work in a private residence and on platform lifts and stairway chairlifts within the scope of the safety standard adopted by the American society of mechanical engineers commonly referred to as ASME A18.1.

There were grandfathering provisions included in the legislation for those contractors/mechanics already practicing in the field and able to show meet the experience requirements.

OHIO DEPARTMENT OF DEVELOPMENT LOOKED TO OHBA FOR FUNDING IDEAS

Ohio Department of Development Director and staff reached out to OHBA for insight as the department considered how funding could help bring more housing opportunities around the state.

OHBA JOINED IN EFFORTS TO ADDRESS ISSUES WITH BUFFALO DISTRICT

OHBA joined efforts urging action to address issues with the Army Corp of Engineers Buffalo District. Industry groups and numerous members of the Ohio Congressional Delegation signed on in support of consolidating Ohio under one district to combat ongoing issues.

ANNUAL MEETING WITH BUREAU OF WORKERS COMPENSATION ASSOCIATION REPRESENTATIVE

OHBA held its required meeting with the BWC Association representative on its group rating program, as well as, all other products and services offered by the Bureau.

OHBA CONTINUED STRONG

REPRESENTATION ON BUILDING CODE BOARDS

Both the Residential Construction Advisory Committee (RCAC) and Board of Building Standards (BBS) include active members of OHBA engaging in the code review and adoption process. Maintaining a reasonable residential building code for Ohio is a top priority for OHBA. This goal is constantly being threatened by more stringent codes being proposed at the National level. Both the IECC and NEC are two recent examples. Fortunately, the Residential Construction Advisory Committee is statutorily required to perform a thorough review of these codes including cost impact and technical feasibility. The members of the RCAC and BBS play a crucial role in keeping Ohio’s code reasonable.

CONTINUED ENGAGEMENT WITH UTILITY PARTNERS

Throughout the year, OHBA met with numerous utilities, both gas and electric, to engage the groups on potential development standards or ways to provide more consistent expectations. Additionally, OHBA worked with the Public Utility Commission (PUCO) to explore what comes under its authority.

SKILLSUSA OHIO TEAMWORKS SPONSORSHIP AND PARTICIPATION

OHBA continued to be the main sponsor for the SkillsUSA Teamworks competition which brought an impressive turnout of young men and women competing in the various construction trades. Several OHBA past presidents served as judges and volunteered throughout the competition.

LEGISLATIVE REVIEW

REVIEW AND

ADOPTION

OF MINIMUM QUANTIFIABLE STANDARDS UPDATES

As the adopting body of the workmanlike standards for the industry, OHBA reviewed and adopted the Seventh Edition of the Minimum Quantifiable Standards.

CONTINUING AGENCY AND LEGISLATIVE FOLLOW UP

While agency issues are always ongoing, many of the legislative issues from 2024 will likely continue into the new year. Throughout the year, OHBA received questions from around the state on enforcement of multiple regulations, including, but not limited to utility, environmental and building code issues. OHBA provided valuable insight and contacts to help mitigate issues brought to OHBA’s attention.

MONITORED LEGISLATION

HB 203 Construction Projects; HB 327 Employee Verification; HB 466 Real Estate Transactions; SB 41 Building Inspections; SB 238 Construction Contractors; SB 243 Zoning Regulations; SB 245 Housing;

Ohio Home Builders Association Phone- 614/228-6647

EYE ON HOUSING

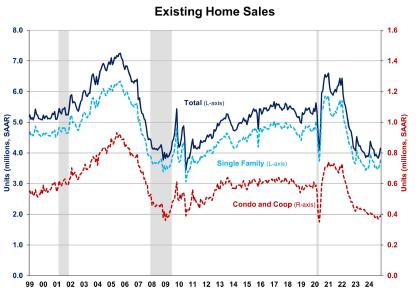

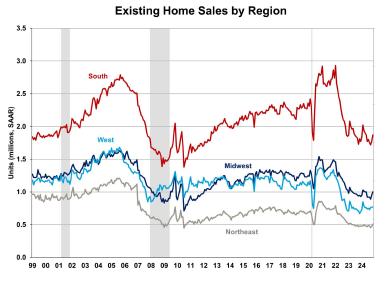

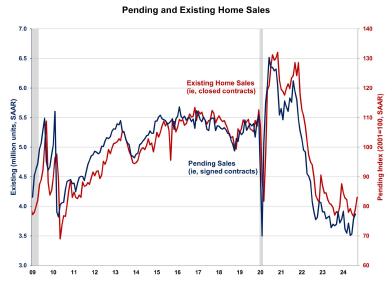

EXISTING HOME SALES Increase in November

Despite higher mortgage rates and elevated home prices, existing home sales jumped to an 8-month high in November, marking the second month of annual increase in more than three years, according to the National Association of Realtors (NAR). While inventory improves and the Fed continues lowering rates, the market faces headwinds as mortgage rates are expected to stay above 6% for longer due to an anticipated slower easing pace in 2025. The prolonged rates may continue to discourage homeowners from trading existing mortgages for new ones with higher rates, keeping supply tight and prices elevated. However, as mortgage rates continue trending lower, the gradual improvement in inventory should help slow home price growth and enhance affordability. As such, the recent gains for existing home sales may give way in the coming months of data.

Total existing home sales, including single-family homes, townhomes, condominiums, and co-ops, rose 4.8% to a seasonally adjusted annual rate of 4.15 million in November, the highest level since March 2024. On a yearover-year basis, sales were 6.1% higher than a year ago, the largest annual gain since June 2021.

The firsttime buyer share rose to 30% in November, up from 27% in October but down from 31% in November 2023.

The existing home inventory level

fell from 1.37 million in October to 1.33 million units in November but is up 17.7% from a year ago. At the current sales rate, November unsold inventory sits at a 3.8-months supply, down from 4.2-months last month but up 3.5-months a year ago. This inventory level remains low compared to balanced market conditions (4.5 to 6 months’ supply) and illustrates the long-run need for more home construction.

Homes stayed on the market for an average of 32 days in November, up from 29 days in October and 25 days in November 2023.

BY: FAN-YU KUO

The November all-cash sales share was 25% of transactions, down from 27% experienced in both October 2024 and November 2023. All-cash buyers are less affected by changes in interest rates.

The November median sales price of all existing homes was $406,100, up 4.7% from last year. This marked the 17th consecutive month of year-over-year increases. The median condominium/co-op price in November was up 2.8% from a year ago at $359,800. This rate of price growth will slow as inventory increases.

Geographically, three of four regions saw an increase in existing home sales in November, ranging from 5.3% in the Midwest to 8.5% in the Northeast. Sales in the West stayed unchanged in November. On a year-overyear basis, sales grew in all four regions, ranging from 3.3% in the South to 14.9% in the West.

The Pending Home Sales Index (PHSI) is a forwardlooking indicator based on signed contracts. The PHSI rose from 75.9 to 77.4 in October due to improved inventory. On a year-over-year basis, pending sales were 5.4% higher than a year ago per National Association of Realtors data.

TWO DAY SHOW!!!!!

EXHIBITOR CONTRACT

Company Name (as it will appear in show) __________________________________________

Booth spaces are LIMITED and available on a 1st Come, 1st Served Basis! 2024 SOLD OUT - Act now to secure your booth!

BOOTH INFORMATION

Electric is optional and available on a 1st Come, 1st Served Basis!

Will you need electricity? _______ YES _______ NO ______# of Booth Spaces ____________TOTAL AMOUNT DUE

I understand that I have contracted for exhibit space by signing this contract and I am liable for the full cost of the booth space. I also understand that the final location of space will be determined by show management when payment is made in full. The undersigned represents that he/she is fully authorized to execute and complete this agreement. The undersigned also understands and agrees to the rules and regulations on the reverse side of this contract.

Authorized Exhibitor Signature

PAYMENT METHOD:

Please Indicate how you would like to pay for your booth space.

Printed Name ___Invoice ___Check Enclosed ___VISA/MC/AMEX/DISC*

*If you select credit card, our office will call for your card information.

Please send completed form to Judie@ncbia.com or 5321 Meadow Lane Court - B, Suite 23 Sheffield Village, OH 44035

**A $5.00 Convenience Fee will be charged for all Credit Card Payments

INTEREST RATE RISKS for the New Year

The election results lifted expectations for economic growth and housing activity on hopes for regulatory reform and an extension of the 2017 tax cuts. However, while such factors have increased stock market prices, the bond market has reservations about possible inflationary impacts from a larger government deficit and tariffs. As a result, the 10-year Treasury rate increased from 3.6% in mid-September to near 4.2% this week. Mortgage interest rates increased as well, hovering near 6.7% last week.

Those higher interest rates took a toll on new home sales in October. Sales of newly built single-family homes declined 17% in October to a 610,000 seasonally adjusted annual rate. New home inventory increased almost 9% from a year ago to a count of 481,000. This marks a 9.5-month supply, although that high level (six months is considered balanced) is justified given the ongoing, nearly 4-month supply for the single-family resale market.

Despite affordability issues, the median new home sale price in October edged up 2.5% to $437,300 and is up 4.7% from a year ago. The share of entry-level homes priced below $300,000 has been steadily falling. Only 13% of new homes were priced in this entry-level range, while 37% of the homes were priced above $500,000. Most of the homes were priced between $300,000-$500,000.

The geography of new home construction continues to be tied to lower-density areas following the pandemic. The NAHB Home Building Geography Index (HBGI) finds that high-density counties (counties in the top 10% of population) constituted just under 40% of single-family construction in the first quarter of 2018, on a four-quarter moving average basis. But since then, the market share for these areas has fallen to 36%.

BY: ROBERT DIETZ

Despite higher interest rates, the labor market continues to be solid. Total nonfarm payroll employment rose by 227,000 in November, a sharp rebound from an upwardly revised increase of 36,000 jobs in October. Since January 2021, the U.S. job market has added jobs for 47 consecutive months, making it the thirdlongest period of employment expansion on record. The unemployment rate rose slightly to 4.2%, after holding at 4.1% through the previous two months.

Residential construction employment in November stood at 3.4 million (958,000 builders and 2.4 million residential specialty trade contractors). The 6-month moving average of job gains for residential construction was 2,983 a month. Over the last 12 months, home builders and remodelers added 52,400 jobs on a net basis. Since the low point following the Great Recession, residential construction has gained nearly 1.4 million positions.

EYE ON THE ECONOMY

CREDIT STILL TIGHT, BUT BUILDERS Finally Get Some Relief from Interest Rates

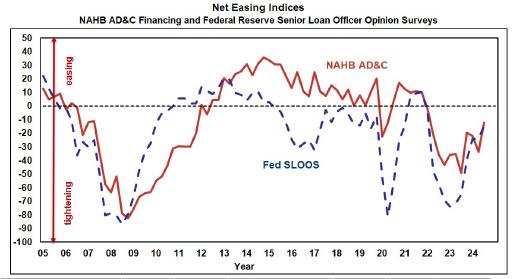

In the third quarter of 2024, borrowers and lenders agreed, as they have over most of the past three years, that credit for residential Land Acquisition, Development & Construction (AD&C) tightened. On the borrower’s side, the net easing index from NAHB’s survey on AD&C Financing posted a reading of -12.0 (the negative number indicates credit was tighter than in the previous quarter). On the lender’s side, the comparable net easing index based on the Federal Reserve’s survey of senior loan officers posted a similar reading of -14.8. Although the additional net tightening was relatively mild in the third quarter (as indicated by negative numbers that were smaller, in absolute terms, than they had been at any time since 2022 Q1), both surveys indicate that credit has tightened for eleven consecutive quarters—so credit for AD&C must now be significantly tighter than it was in 2021.

According to NAHB’s survey, the most common ways in which lenders tightened in the third quarter were by lowering the loan-to-value (or loan-to-cost) ratio, and requiring personal guarantees or collateral not related to the project—each reported by 61% of builders and developers. After those two, reducing the amount lenders are willing to lend was in the third place, with 56%.

Additional information from the Fed’s survey of lenders— including measures of demand and net easing for residential mortgages—is discussed in an earlier post.

BY: PAUL EMRATH

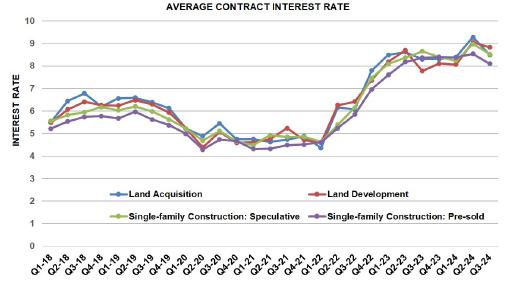

Although the availability of credit for residential AD&C was tighter in the third quarter, builders and developers finally got some relief from the elevated cost of credit that has prevailed recently. In the third quarter, the contract interest rate decreased on all four categories of AD&C loans tracked in the NAHB survey. The average rate declined from 9.28% in 2024 Q2 to 8.50% on loans for land acquisition, from 9.05% to 8.83% on loans for land development, from 8.98% to 8.54% on loans for speculative single-family construction, and from 8.55% to 8.11% on loans for pre-sold single-family construction.

More detail on credit conditions for builders and developers is available on NAHB’s AD&C Financing Survey web page.

NAHB HOUSING HEADLINES

Yahoo Finance

This could lead to a 'golden age of housing production': NAHB C EO (video)

The National Association of Home Builders (NAHB) reported that US homebuilder confidence is holding steady at 46 for December, according to its Housing Market Index.

Associated Press

Fast Market

Economists’ 2025 housing market forecasts largely call for mortgage rates to stay above 6% next year

Home shoppers hoping for more attractive mortgage rates next year may be disappointed. That’s the takeaway from several economists’ 2025 housing forecasts, most released over the past couple of weeks.

10 states where housing market inventory just spiked back

As housing markets across the U.S. continue to stabilize from the frenzied highs of the pandemic housing boom, active listings and inventory levels have become critical indicators of market health. ResiClub tracks these metrics closely, as they offer insights into the balance of supply and demand—and what that balance might mean for future home prices.

Reuters

US single-family housing starts rebound in November

U.S. single-family homebuilding rebounded in November as the drag from hurricanes faded, but the threat of tariffs on imported goods and potential labor shortages from mass deportations could hamper new construction next year

Associated Press

Average rate on 30-year mortgage snaps 3-week slide and rises to highest level since late November

The average rate on a 30-year mortgage in the U.S. rose this week to its highest level since late November, reflecting a recent uptick in the bond yields that lenders use as a guide to price home loans. The rate rose to 6.72% from 6.6% last week, mortgage buyer Freddie Mac said Thursday. The rate is now higher than it was a year ago, when it averaged 6.67%.

CNBC

Mortgage demand drops for the first time in 5 weeks, after inte rest rates rise Mortgage rates moved markedly higher last week, causing overall mortgage demand to drop. Total application volume fell 0.7% compared with the previous week, according to the Mortgage Bankers Association’s seasonally adjusted index. That was the first decline in five weeks.

Reuters

US existing home sales jump to eight-month high in November

U.S. existing home sales surged to an eight-month high in November, but higher mortgage rates and house prices remain a constraint heading into 2025.

USA Today

Homeownership has been 'okay' for Boomers... and their kids wil l luck out too Owning a home has long been considered a surefire wealth builder, and new research confirms just how lucky Baby Boomers have had it when it comes to homeownership. (Subscription may be required.)

Business Insider

Buying a home probably won't get much easier in 2025, says Fann ie Mae. But it's not all bad news. Affordability might improve a little bit next year for homebuyers, especially as mortgage rates ease and incomes rise, but don't expect buying a home to get significantly easier in 2025. (Subscription may be required.)

Marketplace

Realtors group issues rosy forecast for housing market in ’25 It’s not big news to announce that 2024 has not been a blockbuster year for housing. Mortgage rates topped 7% for a while back in the spring. They fell in the summer to near 6% in anticipation of lower inflation and the Federal Reserve cutting interest rates. That was promising, until the 30-year shot back up again. It’s now hovering near 6.7%.

NAHB HOUSING HEADLINES

INSURANCE

The Wall Street Journal

Insurance startup Stand has a plan to cover ‘uninsurable’ homes

The new insurance company raised $30 million and is writing policies in California wildfire zones. (Subscription may be required.)

Newsweek

Insurance crisis could spark housing market crash worse than 20 08: Report

The growing instability in the U.S. homeowners insurance markets could lead to a housing crash worse than the 2008 one unless policymakers act fast, warns the Senate Budget Committee in a new report.

PRODUCT NEWS

Simpson Strong-Tie

Powerful Software for Building Construction Documents. LotSpec gives you a smart way to optimize the building process. You can quickly manage design options in 2D or 3D workflows, generate construction documents, and automate the task of creating both master plan and lot-specific sets. Turn hours of work into minutes with LotSpec.

GSEs

National Mortgage News

"As-is" release of GSEs would be fraught with pain

For all of you who hoped for a peaceful, uneventful year in 2025 with the re-election of President Donald Trump, think again. Over the past four years, mortgage lenders had to contend with progressive policy nonsense, punitive fines from the Consumer Financial Protection Bureau, and an abject state of incompetence among many government officials. (Subscription may be required.)

INTERNATIONAL NEWS

The Wall Street Journal

The housing affordability crisis is going global Home prices and rents are rising faster than incomes in big cities in Europe and beyond. 'The price in Ireland is mental.' (Subscription may be required.)

LIMITED TIME OFFER!

Earn 30¢ per gallon for the first three months once you reach 100 gallons in each calendar month. Thereafter, save 6cpg for every gallon pumped.*

Th e 7-Eleven Comm er ci al Fl ee t M ast er ca rd

Fleet Savings Made Easy

Perfect fit for mid-sized to larger fleets that need the added convenience of fueling where Mastercard® is accepted. With the 7-Eleven Commercial Fleet Mastercard®, your fleet can customize reports for a complete fuel management solution.

Rebates & Savings

Earn 30¢ per gallon for the first three months once you reach 100 gallons in each calendar month. Thereafter, save 6cpg for every gallon pumped.*

Security & Fraud Controls

Enjoy the security of advanced card prompts.

Earn 30¢ per gallon for the first three months once you reach 100 gallons in each calendar month. Thereafter, save 6cpg for every gallon pumped.*

Customize and download cost and performance reports monthly or in real-time.

Monitor transactions and manage your account online, in real-time.

Use card prompts to help prevent misuse. Simple online access.

Accepted at your favorite 7-Eleven & Speedway locations and anywhere Mastercard is accepted, regardless of fuel brand.**

Name

Online Control & Visibility

Set card controls and access detailed reporting online anytime.

The 7F LEET Diesel Network Ma stercard ®

Fueling your fleet for the road ahead.

Diesel Network Mastercard offers significant discounts on diesel at the over 260 locations that make up the 7FLEET Diesel Network as well as discounts on commercial truck lane diesel across the AMBEST network.

Network Discounts

Save an average of 53cpg on truck diesel lane gallons fueled in the 7FLEET Diesel Network.*

Security & Fraud Controls

Enjoy the security of advanced card prompts.

Online Control & Visibility

Set card controls and access detailed reporting online anytime.

Customize and download cost and performance reports monthly or in real-time.

Monitor transactions and manage your account online, in real-time.

Use card prompts to help prevent misuse.

Simple online access.

Accepted at your favorite 7-Eleven & Speedway locations and anywhere Mastercard is accepted, regardless of fuel brand.**

7-Eleven Fleet Card Program Application

Please send the application to

INFORMATION – Required.

below.

AUTHORIZED REPRESENTATIVE – Required.

Application Terms: By signing this Application, the Authorized Representative represents, warrants, and agrees that: (a) he or she is authorized to apply to FLEETCOR TechnologiesOperating Company, LLC (“FLEETCOR”), a Louisiana limited liability company, for an unsecured, partially secured, or fully secured line of credit (“Account”) on behalf of the company identified above (“Client”); (b) FLEETCOR may obtain Client’s credit report and check Client’s credit standing when processing this Application or periodically evaluating any resulting Account’s creditworthiness; (c) this Application is subject to approval and acceptance by FLEETCOR; (d) if the Application is approved by FLEETCOR in Louisiana, the resulting Account: (i) will be governed by Louisiana law; (ii) will not be a revolving credit account and the Amount Due/Total Amount Due shown on each Account Statement will be due and payable on the Due Date shown on the Statement; (iii) will be used solely for commercial purposes and not for personal or household purposes; (iv) will be suspended, and the Client’s redit history may be reported to credit reporting agencies, if the Client’s unpaid balance ever meets the Account’s Credit/Spend Limit; and (e) acceptance, signing (in whatever form), or use of any of the Cards issued to Client will constitute Client’s acceptance of the Client Agreement available at www.fleetcor.com/terms/7-Eleven-mc or www.fleetcor.com/terms/7-Eleven-dn Equal Credit Opportunity Act Notice. The Federal Equal Credit Opportunity Act prohibits creditors from discriminating against credit applicants on the basis of race, color, religion, national origin, sex, marital status, age (provided that the applicant has the capacity to enter into a binding contract); because all or part of the applicant’s income derives from any public assistance program; or because the applicant has in good faith exercised any right under the Consumer Credit Protection Act. The federal agency that administers compliance with this law concerning this creditor is the Federal Trade Commission, Equal Credit Opportunity Act, Washington, D.C. 2 0580. FLEETCOR considers your privacy important. View our privacy policy available at www.fleetcor.com/privacy-policy to find out more.

I agree to the Application Terms and the Client Agreement (Please check box) ☐

BUSINESS OWNER(S) / PERSON WITH SIGNIFICANT MANAGEMENT RESPONSIBILITY – Required.

To help fight financial crimes, the U.S. Department of Treasury require financial institutions to obtain, verify, and record information about beneficial owners of entities opening accounts. Beneficial owners are persons who, directly or indirectly, own 25% or more of the entity. We may use third-party resources to verify your identity. For questions about this regulation and how FLEETCOR uses and protects this data, please speak with your sales representative. Patriot Act Notice. Section 326 of the USA PATRIOT Act mandates that FLEETCOR verify and record certain information about you (the Client, Authorized Representative, or anyco-maker or guarantor) while processing this Application.

Beneficial Owner (Individuals who own 25% or more of a Legal Entity)* ☐ Not Applicable, Sole Proprietor, Government Entity, Not

this person have significant responsibility for managing the legal entity listed above?