What do people look for when seeking out a financial adviser? While qualifications are important, even more so are trustworthiness, integrity and the ability to communicate effectively.

Pg 10–11

INVESTING IN AFRICA

Despite the many challenges that exist in Africa, there is a growing appetite for investment, particularly amid increased global volatility.

Pg 12–14

GLOBAL INVESTING OUTLOOK

Find out what younger investors and those from emerging economies are demanding when it comes to investments.

Pg 22

INSURANCE

Key trends facing the industry; the diversifying of policies; and problems facing short-term insurance.

Pgs 24-30

WANT MORE VALUE FROM YOUR INBOX?

Scan to subscribe to our weekly newsletters.

By Siobhan Cassidy MoneyMarketing contributor

ISurvey shows steady progress in SA as global chaos unfolds

t was hard to ignore the fact that the release of the latest Alexforbes’ Manager Watch™ Survey –which reveals solid, steady growth and evolution within the local asset management industry –came exactly a week after Donald Trump’s 2 April tariff announcements, which unleashed chaos on global markets.

The post-election developments in the US had no bearing on the data in the 2025 edition of Alexforbes’ Manager Watch™ Survey of Retirement Funds Investment Managers, which delivers insights into the evolving South African asset management landscape based on data up to December 2024. The paradox was, nonetheless, striking.

The juxtaposition of solid and steady progress locally against external events is an interesting representation of the investment industry’s dilemma around ‘controlling the controllables’. Investors are often told they should focus on factors within their control, such as how much they save and how long they leave their savings invested. However, they are also frequently reminded that factors beyond their control will also have an impact on their investments, which will often test their resolve.

Often, an adviser’s toughest job is to help clients from reacting emotionally to events. As Linda Eedes, Investment Professional at Foord Asset Management, puts it, financial advisers must “hold their clients’ hands through difficult times and make sure they don’t make emotionally driven mistakes”.

The survey is the first in the Alexforbes’ Manager Watch™ Survey of Retirement Funds Investment Managers series that is starting to reveal the effects of the lifting of the offshore investment cap on retirement investments under Regulation 28 of the Pension Funds Act to 45%. Bearing this in mind, it would be reasonable to expect that global developments might have a more significant effect on next year’s survey. However, even as investors around the world brace for what is to come in the unfolding global storm, the evolution reflected in the survey deserves our attention.

A reliable tracker of local trends

Established in 1994, the Manager Watch™ Survey has tracked trends in the South African asset management landscape for 30 years. A key aspect

has been the growth in the number of participating asset managers, as well as investment strategies as more firms are offering specialist strategies and alternative asset classes, giving investors more options. In the early 1990s, retirement funds mainly sought the “best balanced managers from a small pool”, and a “handful of life-owned asset management companies dominated the space”. As the industry matured, specialist mandates gained prominence, and managers began specialising in equities, bonds and alternatives. Over time, the market diversified, with both large financial institutions and boutique investment firms competing to offer innovative solutions.

The Alexforbes Manager Watch™ Survey 2025 indicates a significant increase in participation, with 92 asset managers and 797 strategies taking part in 2024, a 5.7% and 6.4% increase respectively over the year before, demonstrating the extensive range of investment opportunities now available.

Another significant development over the decades has been the shift from a few dominant players to a wide variety of asset managers, creating innovation and competition. The number of BEE strategies has also seen significant increase. The growth in assets under management to more than R8.2tn in the 2025 edition of Alexforbes’ Manager Watch™ Survey reflects “increasing trust in South Africa’s investment industry” and “growing investor demand for tailored, innovative investment solutions”.

The rise of the multi-manager and transparency

The survey also showed a notable rise of multimanagers, who have significantly gained ground on single managers, indicating a growing investor interest in diversified strategies. “In 2019, for every R1 managed by single managers, multi-managers held 15 cents. By 2024, this had increased to 29 cents.”

Also included was the finding of an increasing emphasis on transparency, fair fees and responsible investing across the sector. Regulatory changes have played a crucial role, “pushing for better governance and transparency”. In response to demands of regulations for clearer reporting and fairer fees, Alexforbes says, “forward-thinking asset managers are already adopting these best practices”.

As an independent DFM, we empower you to prioritise your clients and business growth with our optimised, advice-led solutions.

Continued from previous page

The survey confirms that steady progress continues to be made in transformation of the South African investment industry. The 2024 Assets Under Management survey shows that all the top 10 asset managers, and 19 of the top 20, had achieved Level 1 B-BBEE status. Just 10 years ago, none of the managers in the top 20 had achieved this status.

Furthermore, the top five black-owned asset managers experienced a 48% increase in total assets, compared with June 2023, with five BEE survey participants entering the top 10 of the AUM survey for the first time. This progress “underscores the ongoing transformation within the sector, highlighting both the commitment and impact of BEE in shaping a more inclusive financial landscape”.

“There is an increasing emphasis on transparency, fair fees and responsible investing across the sector”

ESG in focus

Pointing to the remarkable changes in the South African investment industry documented by the Manager Watch series, Alexforbes pledges that the surveys would continue to push for higher standards, better comparisons, and stronger trust in the industry. “As part of this ongoing evolution, we also recognise the growing importance of sustainability. Soon, we plan to incorporate sustainability-focused reporting into the surveys, ensuring that investors and trustees have the tools they need to assess ESG-focused investments.”

Even in the context of the current US backlash against Environmental, Social and Governance (ESG) considerations, the survey points out that over the past three decades, ESG had moved from a “niche approach to a core investment philosophy” in South Africa.

Writing in a companion piece released with the survey, Premal Ranchod, Head, ESG Investments, Alexforbes Investments, says:

“By the early 2000s, ESG analysis became more mainstream, bolstered by regulatory frameworks, investor advocacy, and landmark initiatives like the United Nations’ Principles for Responsible Investment (PRI). South Africa, a pioneer in responsible investing, introduced key regulations in Pension Fund management, Regulation 28, which emphasised ESG considerations in pension fund allocations.”

A maturing industry

As much as the survey presents evidence that the investment industry in South Africa continues to add layers of sophistication, investors are showing signs of maturity, too. Janina Slawski, Head of Investment Consulting at Alexforbes, says she had not received a single query from a member who needed reassuring as the markets hit the skids after Trump’s announcements. Normally she would receive many queries.

Admittedly, Slawski says, Alexforbes has got very practiced at communicating with members during market turbulence. “Every time there’s a Russian invasion of Ukraine, a Covid, a Trump being aggressive, you communicate with members, reminding them about the fundamentals of good investing. We have become very practiced at this because we have had so many crises.”

In terms of the global context, the 2025 Outlook in the Alexforbes’ Manager Watch™ Survey anticipates “murky” prospects with “material policy changes on the horizon from the new US administration” and “heightened trade policy uncertainty and geopolitical tensions”. These global uncertainties contrast with the positive trends observed within the South African asset management industry in 2024.

The Alexforbes Manager Watch™ Survey 2025 reflects a South African asset management industry that is growing and evolving surely and steadily, which will hopefully build resilience amid a complex and potentially volatile global environment.

EARN YOUR CPD POINTS

The FPI recognises the quality of the content of MoneyMarketing’s May 2025 issue and would like to reward its professional members with 2 verifiable CPD points/hours for reading the publication and gaining knowledge on relevant topics. For more information, visit our website at www.moneymarketing.co.za

ED'S LETTER

As I write this Ed’s Letter, it has been 100 days since Donald Trump took office. It’s been a crazy whirlwind of chaotic decisions that have sent markets spiralling, alienated countries against the US (not least China), and created confusion around the war in Ukraine. Tariffs have not been effective, creating upsets in supply chains and impacting businesses across the globe.

Meanwhile, countries around the world have realised it’s time to stop relying on the US and to look at other alternatives for trade and investments. Those in Africa are no exception, and there’s a growing realisation that Africa needs to start looking inward and focus on the opportunities that exist at home. We get some comments from the experts in this issue.

We’re also looking at the move towards alternative investment models, largely because of the need for downside protection in an atmosphere of uncertainty. In this issue, we get some opinions from those working with African investments on the way forward.

Remember, as dazed and confused as you might feel about current global developments, your clients are feeling even worse. Now, more than ever, is the time to be there for them, to give reassurances, encourage them to stay the course, and give the best possible advice you can.

Stay financially savvy.

Sandy Welch Editor, MoneyMarketing

Note: If you subscribe to our MoneyMarketing newsletter, see QR code on the cover, you will receive a special discount off a News24 or Netwerk24 subscription*. *Offer available to new subscribers only.

By Bjorn Ladewig Head of Business Development, Just SA

TCalming the waves of Trumpian storms in retirement

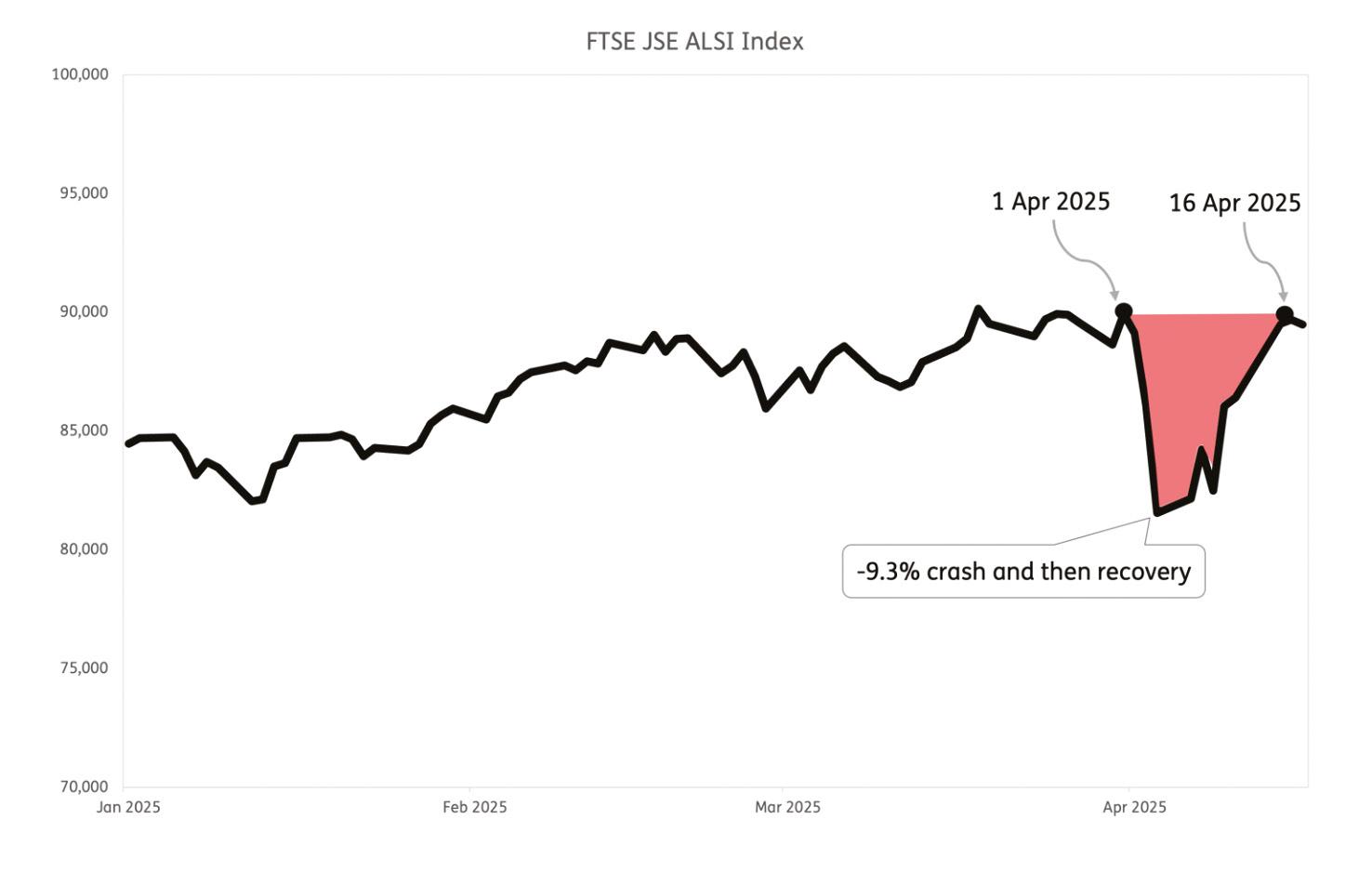

he first 16 days of April 2025 were a scary time for investors, as President Trump’s successive announcements of sweeping tariffs triggered the ‘Liberation Day’ market meltdown that spread across global investment markets. In South Africa, the ALSI Index fell 9.3% over this period, as shown in the graph, a drop the likes of which was last seen in March 2020 during the height of market uncertainty as a result of Covid-19.

For investors in the accumulation (contribution) phase of their retirement planning, investment market declines and recoveries don’t significantly impact their overall savings as they remain in the market. In fact, you can get lucky and put money into the market during a decline and find that your money grows very quickly. However, for those in the decumulation (withdrawal) phase such as retirees, drawing an income means selling their units at a lower price and locking in a loss that may never be recovered. This magnifies the impact of market volatility on their overall savings.

This is especially true for retirees invested in pure living annuities, where they have a great deal of flexibility in terms of the drawdown rate they choose, and the funds their capital is invested in.

Source: Investing.com

On the other hand, if you’re invested in a pure life annuity, investment market declines aren’t a concern as the monthly income cannot decrease, and it is guaranteed for life.

For those retirees that want the best of both – certainty and flexibility – the optimal solution is to blend a lifetime income (a life annuity) within a living annuity. In a blended annuity solution, a significant part or all of your drawdown would come from the lifetime income component of the investment, keeping the rest of the savings intact. This cushions the blow of market fluctuations (such as the period early in April 2025) as it allows for a better recovery of the savings component.

Here is a simple example. Let’s say a retiree has R1m invested in a pure living annuity from which she draws down 10% once per year, i.e. R100 000. Let’s now consider two scenarios:

• Scenario A: 10% market decline, then recovery (for which a 11.1% return is required)

Scenario B: no market decline or recovery

If we present the results in a table: Scenario

Starting value R 1 000 000 R 1 000 000

Value after crash R 900 000 N/A

Drawdown R 100 000 R 100 000

Value after withdrawal R 800 000 R 900 000

Value after recovery R 888 800 N/A

End value R 888 800 R 900 000

Loss (A vs B) R11 200

The R11 200 loss (1.12%) that resulted from this illustrates the negative impact of drawdowns during market drops, albeit quite an extreme example given that a single annual drawdown was assumed. The second term of President Trump is likely to continue to spark market volatility, just as it did in his first term. In fact, it could even produce more of a bumpy ride for investors as this time his actions are less constrained by the fact that he will want to seek re-election, as US presidents may only serve for two terms. Against this backdrop, and given the fact that US politics have a great impact on global and local investment markets, reducing risk in a living annuity by blending –investing a part in a lifetime income – is a good decision. Blending allows retirees to better ride through such waves of volatility, as it reduces or can eliminate the need to sell valuable units at a time when prices are low.

“Blending allows retirees to better ride through such waves of volatility”

Graph: April 2025’s market crash and recovery

By Francois du Toit CFP® PROpulsion

“WBuilding a professional services business: The next step

hat should I do next?” It’s a question that haunts us all, regardless of where we are in our professional journey – whether we’re just starting out, somewhere in the middle, or approaching the end. And it’s a question I’ve been wrestling with as we continue to build our own business. Today, I want to share some reflections on the realities of building a professional services business, especially in 2025 when the landscape continues to evolve so rapidly.

The job vs the business

One of the biggest revelations I’ve had recently is understanding the fundamental difference between having a job and building a business. These two things are not the same, yet many of us confuse them, especially when transitioning from being employed to owning our practice. When you start your own business, you’re doing both, performing the job and building the business, simultaneously. Initially, you can manage everything. There seems to be time for all tasks, and you wonder what others are complaining about. But inevitably, sometimes three months in, sometimes three years, you hit a wall where you simply cannot take the next step. Why? Because the job is taking all your time, leaving nothing for business development.

The three growth curves

I’ve come to recognise that there are three interconnected curves that determine our progress:

1. Professional Maturity Curve: How your technical skills, knowledge, and value proposition develop over time.

2. Business Maturity Curve: How your business infrastructure, revenue model, and operations evolve.

3. Personal Development Curve: How your self-awareness, emotional intelligence, and understanding of your own strengths grow.

These three curves work in tandem. Neglect one, and the others suffer.

Revenue

first, systems later

When starting a new business, there’s an almost irresistible urge to focus on systems, processes, workflows and technology. These are important, but not on day one.

The only thing you should be doing when first starting is selling and generating revenue. I wish with my whole heart I had learned this lesson when I started my business in 2015.

The most critical question is: how do you build predictable, recurring revenue streams? Whatever you sell needs to generate revenue that grows consistently. Without this financial foundation, you’ll never have the time or resources to focus on taking your business to the next level.

Emotional realities

Building a business comes with significant mental and emotional challenges. Anxiety, stress, and uncertainty are part of the journey. For me, anxiety often strikes when facing tasks where I don’t have all the answers, be it how to structure a new project, how to price it, or how to present it. These moments can be paralysing, staring at a blank screen with nothing happening for hours.

But if you’re truly meant to be building a business or practice, these challenges aren’t obstacles, they’re part of the process that pushes you forward. The passion to make a

difference at scale gives you the resilience to work through these moments.

What’s next?

The most challenging question is always: what’s next? Here’s what I’ve learned: you don’t need to know all the steps to reach your destination. Having a clear vision of where you want to end up is crucial, but the path there reveals itself one step at a time.

Focus on the step you’re taking now. When you complete it, the next step often becomes evident. If it doesn’t, talk to people. Some of the most valuable insights come from conversations with others who can see what you can’t.

Challenging traditional models

Many of us had to build our businesses through cold calling and hard-won client acquisition. But do we need to perpetuate this model? Must everyone pay the same ‘blood, sweat and tears’ price we did? What if we created better systems for lead generation and prospecting at the business level? What if we invested in structured internships and training programs that give new professionals a sustainable path to success?

That said, I do strongly believe in earning your stripes. It’s crucial for appreciating and valuing what you gain and to ensure you look after it for a long time to come. But we need to figure out a new way of letting new entrants earn their keep.

Stay curious and keep raising the bar.

Du Toit started PROpulsion, a community for financial planners and advisers to help them grow and succeed. He hosts the weekly PROpulsion LIVE show on YouTube, with over 295 episodes. With 30 years of experience, he invites local and international guests to educate and inform. Committed to using AI and new technology, he aims to make a big impact. For more details, visit www.propulsion.co.za.

It’s

personal: Understanding what drives client decisions

Choosing a financial adviser is one of the most important decisions a client will make on their journey to financial security – and it’s rarely just about credentials or investment returns. Clients are looking for someone they can trust, who understands their unique circumstances, and who offers clear, personalised advice. In an increasingly competitive and regulated environment, advisers need to think beyond technical expertise and consider the factors that truly shape client decisions: communication style, transparency, emotional intelligence, and a commitment to long-term partnership. MoneyMarketing spoke to Cape Town-based financial adviser Cameron McCallum, CFP® CA(SA) Managing Director & Wealth Manager at Netto Invest, to get his opinions on how clients go about choosing a financial adviser.

How can people tell if a financial adviser truly has their best interests at heart?

A good financial adviser listens more than they talk. They ask thoughtful questions, listen intently, and aim to fully understand your situation before making any recommendations. Rather than simply instructing their client, the right adviser empowers them to make informed decisions, acting more like a financial coach who is here to guide and support through every step. Their advice is never one-size-fits-all; instead, it’s tailored to each client’s unique needs, with clear explanations and context behind each recommendation. Transparency is also key. They should be able to make clients feel at ease discussing fees and any potential conflicts of interest. An adviser with integrity won’t shy away from these conversations.

What are the most important qualities someone should look for in a financial adviser, beyond qualifications?

A strong adviser-client relationship is built on mutual trust and rapport. Since financial planning is a long-term journey, it’s essential to feel personally comfortable with your adviser and confident in their integrity. Beyond trust, a good adviser takes a truly client-centric approach – investing time in understanding your family, values, background, and unique circumstances to tailor advice to your specific needs. It’s also beneficial when advisers operate within a team environment. This not only ensures continuity of service if your primary adviser is unavailable, but also enhances the quality of advice through collaboration, shared experience and collective research.

What kind of questions should advisers be prepared for from new clients before they sign anything or make a decision?

Can I speak to a few of your long-term clients as references? How do you structure your advice process and what is your investment philosophy?

• How are you remunerated – do you receive commissions or rebates from any providers?

• What services do you offer beyond investment advice? What level of ongoing support can I expect – how often will we review my plan, and how do you communicate between meetings?

“A good financial adviser listens more than they talk”

What red flags should clients watch out for when meeting a potential adviser for the first time?

Advisers should never talk more than they listen. Dominating the conversation or focusing more on themselves is a massive red flag for clients. Never make a client feel rushed or pressured into making a decision; high-pressure tactics are a warning sign. Transparency is also essential – if an adviser is unclear or evasive about how they’re compensated, it sends the wrong message. Unrealistic promises, such as guaranteeing high returns or downplaying the risks associated with investing, will also make clients wary.

How important is it for an adviser to be independent, and how does that impact the advice given?

Independence often allows for a wider range of solutions and fewer restrictions, which can lead to better advice. While not always essential, it generally reduces the risk of bias. What matters most is transparency. Clients should understand whether the adviser is limited in the products they can recommend, and whether any conflicts of interest exist that could influence the advice.

Notwithstanding recent market volatility, institutional investors have been positive on Africa. Speaking at The Network Forum’s (TNF) Africa Meeting, Hari Chaitanya, Head of Investor Services, Africa at Standard Bank Corporate and Investment Banking (CIB), looks at the investor dynamics in the region, and how market reforms have acted as a catalyst for inbound capital flows.

Investors reposition their portfolios towards Africa

Hungry for yield and better risk diversification, institutions are doubling down on their Africa exposures. This is a trend that has been facilitated by the region’s growing index inclusion, diminished concerns about market risk, and eased foreign exchange (FX) headwinds.

Previously, fears about FX repatriation – or lack thereof – had been a major stumbling block for investors when accessing certain African markets, most notably Nigeria.

In Nigeria, there was a four-year backlog whereby it was challenging for global investors to repatriate FX. However, over the last few years, Nigeria’s government and the Central Bank have addressed the issue, so repatriation is no longer the problem it once was for global investors. As macroeconomic drivers improved, so too did investor flows.

According to World to Africa survey study by The Value Exchange, in partnership with Standard Bank, 50% of institutions plan to grow their Africa allocations over the next two years, with mid-sized asset managers and asset owners leading the charge. The biggest shift is happening in North America, where 67% of allocators said they intend to invest in the continent – a three-fold increase since 2022.

In addition, investors from the Middle East, particularly development organisations, are zeroing in on Africa as an investment destination of choice. This comes as 72% of Middle East institutions told The Value Exchange’s study that they have portfolio holdings in the region.

Cross-border investment

“Due to the limited domestic investment opportunities, we are seeing a growing number of African pension funds looking outside of their home markets, which is fuelling growth across the region,” adds Chaitanya. Foreign investors are diversifying beyond the top-tier African economies, i.e. South Africa, Nigeria, Kenya, and

incorporating a more diverse range of markets into their portfolios. “We are starting to see allocators ramp up their exposures to other countries within East Africa and also Ghana,” says Chaitanya.

Positive reforms expedite inward flows

Ease of market access and the region’s ambitious reform zeal have helped raise Africa’s profile among foreign investors. Although there are still a few lingering barriers to entry, accessing local markets is largely frictionless for investors. “Relative to many other beneficial ownership markets, i.e. China, India, Korea, etc, opening up accounts in Africa is a relatively straightforward process,” says Chaitanya.

Market reforms strike a chord

“Despite all of the various crises and issues facing African countries, the region has been consistent in its desire to improve its capital market infrastructure; whether it is consolidating the number of regional stock exchanges, launching derivatives trading, upgrading systems at CSDs, introducing new investment products (i.e. securities lending/borrowing, derivatives, green bonds), or by ensuring their domestic markets adhere to globally accepted best practices,” says Chaitanya.

As with many other parts of the world, a handful of African countries are shortening their trade settlement cycles, a move that will help shore up liquidity even further. This comes as Zimbabwe is poised to migrate from T+3 to T+2 later this month, while Nigeria’s CSCS, having initially flirted with the idea of going straight from T+3 to T+1, is instead moving to

T+2, following consultations with domestic and foreign investors and custodians.

Regulators are also doing their bit to attract inward investment. In Nigeria, the Investment and Securities Act was recently introduced, a piece of legislation that will overhaul the country’s capital markets by enhancing investor protections and improving transparency.

Education as an enabler

If African markets are to keep up this momentum, education and dialogue will be critical – firstly to dispel foreign investors’ misperceptions about the region, but also to ensure that local regulations make for a conducive investment environment.

“If we look at China and Kuwait’s inclusion into MSCI, it was underpinned by clear, transparent conversations between the index providers and the market authorities in those countries, based around one key question: ‘How can we do better?’ For me, a significant part of that journey is education,” says Barnaby Nelson, CEO, the Value Exchange.

“A lot of the money going into Africa will be sourced from funds domiciled in Luxembourg and Dublin, or investors based in the US. Any regulatory changes being made in Africa need to consider rules such as UCITS V, the 40 Act and ERISA, as this will ultimately predicate whether these changes are successful or not,” concludes Nelson.

“Hungry for yield and better risk diversification, institutions are doubling down on their Africa exposures”

Image: Getty Images

Hari

Chaitanya

Celebrating excellence in South Africa’s Capital Markets

In April, the Spire Awards once again brought together some of the brightest stars in South Africa’s financial world for a night of recognition, celebration and inspiration. Known as the gold standard for excellence in the country’s capital markets, the awards are voted on by South Africa’s largest institutional investors – making them a true reflection of industry respect and achievement.

This year’s event was filled with energy and pride as leading institutions were acknowledged for their impact in shaping the future of our markets. Speaking at the ceremony, Valdene Reddy, Director of Capital Markets, reflected on what sets top performers apart: “It’s often said that exceptional individuals don’t just endure tough times – they thrive, no matter the conditions. They seize every opportunity to lead, innovate, and excel.”

Standard Bank and Rand Merchant Bank (RMB) stole the spotlight, each taking home an impressive 11 awards across various categories. Standard Bank walked away with top honours like Best Forex House and Best Market Making Team: Interest Rate Derivatives, while RMB was named Best Fixed Income & Forex House, Best Bond House, and Best Interest Rate Derivatives House, among others.

But it wasn’t just about the big players –the evening also recognised outstanding contributions from other key market participants. Absa CIB, BVG Commodities, CJS Securities, Goldman Sachs, Nedbank, Peresec Derivatives, Prescient Securities, and Tradition were among those honoured with wins across various sectors.

From bonds and currencies to interest rate and commodity derivatives, the 2025 Spire Awards celebrated the skill, innovation, and dedication

that keep South Africa’s capital markets dynamic and competitive.

“We witnessed some of the country’s leading capital market participants continue to showcase their commitment to excellence in their client service and overall market contribution. Awards like these are significant not only because they celebrate incredible capability, but also because they recognise and inspire new solutions across the sector. Such innovation is essential in building robust and sustainable Capital Markets, and by extension, the local economy,” said Thembi Mda-Maluleka, Head of Bonds, Currencies, and Interest Rates Derivatives at the JSE.

See the full list of award winners below:

Best Broker: Agricultural Derivatives Research

CJS Securities

Best Commodity Broker: Physical Deliveries

BVG Commodities

Best Commodity Broker: Options BVG Commodities

Best Broker: Commodity Derivatives

BVG Commodities

Best Market Making Team: Cash Settled Commodity

Derivatives Rand Merchant Bank

Best Research Team: Africa Standard Bank

Best Research Team: Forex Absa CIB

Best Research Team: Credit Standard Bank

Best Research Team: Economics Standard Bank

Best Research Team: Fixed Income Absa CIB

Best Agency Broker: Listed Interest Rate Derivatives

Peresec Derivatives

Best Inter Dealer Broker: Interest Rate Derivatives

Tradition

Best Market Making Team: Listed Interest Rate

Derivatives Rand Merchant Bank

Best Sales Team: Interest Rate Derivatives

Standard Bank

Best Market Making Team: Interest Rate Derivatives

Standard Bank

Best Agency Broker: Listed FX Futures Peresec Derivatives

Best Agency Broker: Listed FX Options Tradition

Best Market Making Team: On-Screen Listed FX Derivatives Rand Merchant Bank

Best Sales Team: Forex and Forex Derivatives Standard Bank

Best Market Making Team: Forex & Forex Futures

Standard Bank

Best Market Making Team: Forex Options

Standard Bank

Best Agency Broker: Bonds Prescient Securities

Best Inter Dealer Broker: Bonds as voted by Agency Brokers Tradition

Best Inter Dealer Broker: Bonds as voted by Banks Tradition

Best Structuring Team: Fixed Income\Inflation\ Credit\FX Standard Bank

Best Structured Notes Issuer Standard Bank

Best Debt Origination Team Rand Merchant Bank

Best Team: Credit Bonds Standard Bank

Best Team: Inflation Linked Bonds

Rand Merchant Bank

Best Repo Team Rand Merchant Bank

Best Sales Team: Bonds Rand Merchant Bank

Best Sales Team: Bonds (Weighted Buy-side) Nedbank

Best Bond ETP Market Maker Nedbank

Best Market Making Team: Government Bonds

Rand Merchant Bank

Best Market Making Team: Government Bonds (Weighted Buy-side) Goldman Sachs

Best IDB: Fixed Income Tradition

Best Research House Absa CIB

Best Interest Rate Derivative House

Rand Merchant Bank

Best Forex House Standard Bank

Best Bond House Rand Merchant Bank

Best Fixed Income & Forex House Rand Merchant Bank

Best Research House: Absa CIB

Best

& Forex House: Rand Merchant Bank

Recognising innovation and impact in the ETF industry

Now in its eighth year, the South African Listed Tracker Awards (SALTA) shine a spotlight on excellence in the local ETF industry. Created by independent service providers – etfSA.co.za, ProfileData, JSE, and LSEG – who support but do not issue ETFs themselves, SALTA recognises the standout performers in South Africa’s rapidly growing exchange-traded product (ETP) space.

These awards go beyond just tracking the best total investment returns over three to 10 years. They also celebrate the skill and innovation behind successful ETF offerings – from how efficiently issuers replicate index performance (tracking error), to how well they attract new investors and capital via JSE listings.

Adding a personal touch, SALTA also includes the People’s Choice Awards, where South Africans cast their votes for their favourite local and global ETFs. It’s a celebration of both performance and impact in the ETF landscape.

The biggest winner on the day was Satrix, who walked off with nine of the 26 awards, including the People’s Choice Award for the sixth time. For the company, the highlight of the day was winning the Tracking Efficiency award, affirming Satrix’s ability to pioneer high-performing tracking products that

fulfil strong investor demand. “This award is significant for us because the Satrix Capped All Share ETF is the first of its kind on the JSE. As an ‘All Share’ tracking fund, it has the difficult task of managing around the small and illiquid shares in the index. For this fund to win this award, given the complexity of what it aims to achieve, is testament to the effort we put into our processes,” says Kingsley Williams, Chief Investment Officer at Satrix**.

The winners were as follows:

Total Investment Returns

Performance is measured for a lump sum investment, on a total return, net asset value basis, with distributions reinvested. There are four periods of assessment – the three-, five- and 10-years Total Investment Returns – all to the end of December 2024.

The ability to raise new capital is recognised – either additional capital for existing ETPs, or new capital for the listing of new ETPs.

Capital Raising

3 Years: SA Equity

Satrix 40 ETF

Capital Raising

3 Years: SA Non-Equity

10X Wealth GOVI Bond ETF

“It’s a celebration of both performance and impact in the ETF landscape”

FNB also sealed its success with three wins (see article on opposite page), including a second win for its FNB Top 40 ETF in the South African equity ETPs category.

Capital Raising

3 Years: Foreign Equity

Satrix MSCI World Feeder ETF

Capital Raising

3 Years: Foreign Non-Equity (Bonds, Income & Listed Property)

Satrix Global Aggregate Bond Feeder ETF

Capital Raising

3 Years: Foreign Commodity & Currency

1nvest Gold ETF

Total Capital Raising

3 Years: Total Capital Raised – by Issuing House

Satrix Managers (Pty) Ltd

Capital Raising

3 Years: Actively Managed ETPs (AMCs/ AMETFs)

Nedbank Private Wealth Global Portfolio AMC

People’s Choice

The public vote for their favourite ETPs, in both local and foreign markets.

People’s Choice – Local Exchange Traded Product

Satrix 40 ETF

People’s Choice – Foreign Exchange Traded Product

Satrix MSCI World Feeder ETF

**Satrix is a division of Sanlam Investment Management.

Consistency, commitment and client trust

FNB’s winning streak continues with its Top 40 Exchange Traded Fund (ETF) being recognised at the SALTA Awards for the second year in a row. Editor Sandy Welch spoke to Bheki Mkhize, CEO of FNB Wealth and Investments, who attributes this achievement to a combination of a skilled team, smart strategy and a clear commitment to delivering value for clients.

“We’ve got a great team,” says Mkhize. “In the passive space, it’s all about small margins. It requires skill because if you trade too much, you increase friction costs, which can negatively impact performance. Managing trading and keeping tracking error to a minimum is crucial.”

He notes that the ETF’s growth has also played a key role in its performance. “The more assets under management you have in the product, the easier it becomes to reduce tracking error and even generate some outperformance.,” he explains. “But this has been a consistent, longterm effort to provide a reliable solution for clients – one that does what it promises.”

That consistency has fostered trust among investors and deepened the brand’s credibility in the market. “We’ve been doing this for a while, and clients understand where our ETF fits, either within a broader portfolio or as a standalone investment,” Mkhize says. “And it’s the team’s ability to get the best trading rates and keep costs low that really supports performance.”

Standing out in a competitive market

With the ETF space growing increasingly competitive, FNB is focused on integrated, client-centric solutions to stay ahead. “We differentiate by integrating the ETF into a broader value proposition,” says Mkhize. “For instance, we use our ETFs as building blocks within our unit trusts, blending active and passive strategies so that clients don’t need to decide how much to allocate to each.”

This ETF is also accessible via FNB’s taxfree savings offerings, making it available to clients with smaller monthly contributions –while still reaping the benefits of long-term investing. “We also integrate it into our rewards programme,” he adds. “For example, clients who invest through a tax-free savings wrapper can earn eBucks rewards. It’s another way we try to encourage a culture of saving.”

Breaking down barriers to entry

One of FNB’s key strategies is making investing feel achievable, even for those with limited financial knowledge. “We’ve simplified the digital journey on our app and introduced products like Share Zero, which offers zero monthly account fees and zero brokerage on ETFs,” Mkhize explains. “That removes friction costs and makes it easier for people, especially

those in lower-income brackets, to participate in the market.”

FNB also places a strong emphasis on financial education. “Many people think investing is only for the wealthy or sophisticated,” says Mkhize. “We aim to change that by showing that even small, regular investments can make a big difference.”

Global access, local simplicity

Beyond local exposure, FNB is helping clients invest globally without the complexity of offshore banking. “We’ve launched Exchange traded Notes (ETNs) that allow clients to invest in global giants like Apple, Microsoft, Amazon, and Nvidia, from as little as R10,” says Mkhize. “These are available in rand, and clients can choose whether they want currency exposure or not.” This removes the need for foreign currency conversion or offshore allowances, further simplifying global investing for South Africans.

Simplifying access with smart bundles

FNB has taken a unique approach to making investing more accessible for everyday South Africans. One such innovation is ShareSaver, a bundled investment product. “ShareSaver is essentially a combination of the Top 40 ETF and the Midcap 60,” explains Mkhize. “You’re basically getting exposure to the top 100 companies in a bundled structure.”

Rather than competing solely on standalone ETFs, FNB builds value around them with bundled products and supporting tools, helping clients benefit from diversified exposure while minimising complexity.

A digital-first investment experience

FNB’s award-winning digital platform is central to its accessibility strategy. Mkhize highlights the importance of intuitive user journeys and proactive communication. “We’ve built simple onboarding journeys on our app, including a seven-day welcome followed by touchpoints over the first 90 days,” he says. Many assume investing is for the sophisticated or the rich. We educate clients that they can start with any amount. Everything makes a difference.”

“We want to make it easy for advisers to focus on advice while we handle the product”

Broadening exposure through global tools

FNB is also extending its global reach through innovative solutions such as ETNs and actively managed certificates (AMCs). “We have listed ETNs giving exposure to offshore companies like Microsoft, Apple, NVIDIA, and Amazon, from as little as R10,” says Mkhize. These instruments offer global access without the need for offshore allowances or complex FX transactions, another example of FNB’s inclusive investment approach.

The AMC advantage

The UBS FNB Global Equity Growth AMC, which received recognition at the recent awards, plays a key role in FNB’s active strategy. “We’ve created a few AMCs, two of which are offshore. They’re used as building blocks within portfolios rather than sold directly to clients,” Mkhize says. “Globally, AMCs are significant. We’ll likely see more local uptake, especially as independent advisers use them to offer custom portfolios with less friction and lower setup costs than unit trusts.”

Supporting financial advisers

FNB’s platform supports both retail clients and financial advisers, especially independents. “We want to make it easy for advisers to focus on advice while we handle the product,” Mkhize notes.

Looking ahead, FNB is expanding into alternative investments, including private equity, infrastructure and credit. “We’ve already been recognised in this space, winning an award for Best Alternative Investments at the Global Private Banking Euromoney Awards,” he shares.

The road ahead

As the digital world evolves, FNB continues to invest in tools that enhance client experience. “We’re constantly looking at how we improve. AI will help us go even further in personalising and enhancing the experience,” says Mkhize. With offshore investing expected to remain a dominant theme, FNB has new initiatives planned for later this year. “There’s more coming, especially in the offshore space, which will resonate with both clients and independent advisers,” he concludes.

Why unit trusts still make sense for SA investors

South Africa’s unit trust industry is experiencing notable shifts driven by regulatory updates, changing investor preferences, and a dynamic economic landscape. MoneyMarketing asked Jade Houreld, Global Business Development Manager, and Mandi Ngqoza, Head of Client Strategy and Investor Relations at All Weather, to give their input as to what to expect from unit trusts in the near future.

When it comes to investing, what sets unit trusts apart from other investment vehicles, and why might they be a good fit for the average South African investor now?

A unit trust fund is a pooled resource, which means that it allows a group of investors to combine their cash and invest it. While individuals invest in a unit trust fund, the fund itself is run by a fund manager, whose aim is to grow the overall value of a unit trust fund, making adjustments based on market conditions. One of the benefits of unit trusts is that by investing a small amount, you can be exposed to a wide range of assets. This offers diversification and lower levels of risk. Unit trusts are well regulated and flexible with the ease with which they can be liquidated.

All Weather has positioned itself as a resilient investment partner. How do your unit trust offerings reflect this philosophy in terms of strategy and asset allocation? We believe intrinsic value is a pragmatic philosophy that allows us to adapt to prevailing market conditions. This philosophy, along with being style agnostic, provides the flexibility to invest in both, depending on what’s working at a specific point in time. Risk management is a key part of our process for each of our eight unit trusts. Although we have an active bottom-up investment process, we also apply a macro geopolitical overlay to assist us in avoiding unnecessary risk.

With market volatility on the rise, how should financial advisers assess the risk profile of unit trusts, and what role can they play in a diversified portfolio?

There is a plethora of unit trusts in South Africa. They are diverse in their offerings –from the most liquid and low-risk unit trusts that provide cash and cash equivalents, to the most high-risk, high-reward categories of unit trusts such as global equities and the likes. Each unit trust serves a purpose, and it is up to the financial advisors to determine each client’s unique risk appetite, provide a holistic financial plan that provides for the client’s needs, stay within the clients’ risk budget, and provide a solution that meets all the client’s needs. If the assessment is done properly, the client can weather any market volatility through a well-structured, well-diversified portfolio that can withstand market risk and volatility.

There are hundreds of unit trusts on the market. What practical steps can advisers take when evaluating and selecting funds for their clients?

As mentioned above, it’s important to first understand clients’ needs and risk appetite preferences. There are various steps and metrics involved in evaluating managers and products, aside for traditional due diligence methodologies. Using technology like online filtering and comparison tools is also helpful.

“It is up to the financial advisors to determine each and every client’s unique risk appetite”

What trends are you currently seeing in the unit trust space, both in terms of investor behaviour and fund innovation?

Aside from recent reports from ASISA that show a significant increase in flows towards unit trusts, there has also been a shift in the ‘knowledge gap’ in relation to hedge funds. Volatile times call for alternative sources of returns and risk protection, which has led to innovation in terms of industry regulation and adoption for hedge funds to be more easily accessible to the average South African via a unit trust structure.

How does All Weather ensure transparency and value for investors in its unit trusts, especially when it comes to fees, performance and reporting?

We value authentic relationships and promote transparency by communicating with clients according to best practises. Sharing information that is clear, concise and relevant, but avoiding overly complex reporting.

SA fund managers now favour domestic assets

Asurvey conducted by the Bank of America in April found that for the first time in five years, South African fund managers are now net sellers of offshore assets, favouring instead domestic assets. Of the 13 fund managers who took part in the survey, 15% said that over the next three months, they intend to decrease their exposure to offshore assets, effectively becoming net sellers.

There is an overriding sentiment that offshore assets don’t match up to the 45% of assets that can be held offshore, according to regulatory requirements. The research showed that the change is largely due to uncertainty about global macroeconomic policies, mostly created by US President Donald Trump’s tariffs.

SA in focus

The fund managers picture for South Africa was not overwhelmingly positive, with many of the fund managers predicting

By Sean Munsie Portfolio Manager of the Allan Gray Stable Fund

a downturn in GDP growth. This is in line with the International Monetary Fund downsizing South Africa’s growth prospects and cutting its GDP 2025 growth figure by half a percentage point to just 1.0%. It’s also predicted that the effects of the US tariffs will be felt far and wide, with no countries escaping totally unscathed.

South African fund

managers are now net sellers of offshore assets”

There were also negative sentiments around internal developments within South Africa, with 38% of managers surveyed seeing reforms slowing, a sharp contradiction to the 2024 reading of 56% expecting an acceleration. The prospect of a recession also looms large – just 38% of managers think a recession is unlikely, whereas 67% felt this way the previous month.

Defensively positioned to navigate challenges

For conservative long-term investors, typical goals in today’s environment may include preserving capital while still achieving above-inflation returns over the long term. Considering the local and global risks that abound, Allan Gray portfolio manager Sean Munsie reflects on the first quarter of 2025’s performance, opportunities in the environment, and what this may mean for conservative investors going forward.

The first quarter of 2025 saw the local equity market add to the strong gains posted in the preceding year, with the FTSE/JSE All Share Index returning 5.9%. Among the largest contributors to returns at the index level were precious metal miners, telecommunications providers, and the dual-listed consumer goods companies, including AB InBev, British American Tobacco and Richemont. Gains for the local banks, insurers and retailers have either begun to stall or go backwards, while the diversified miners and other cyclical rand hedges Sasol and Mondi have continued to struggle in the new year. The FTSE/JSE All Bond Index eked out a 0.7% gain for the quarter, as the risk premium

ascribed to local government bonds increased, particularly on longer-dated instruments. The faltering US market contributed to declines in the MSCI World Index and the S&P 500, which returned -1.8% and -4.4% in US dollars respectively over the quarter.

Against this backdrop, the Allan Gray Stable Fund returned 3.1% for the quarter – 1.0% ahead of its benchmark.

Gains for AngloGold Ashanti, Gold Fields and DRDGOLD have been particularly strong, with share prices more than 50% higher year-to-date in rands – this as the gold price breached $3 000 per ounce for the first time and continued to set new highs. Predominant trends, including diversification away from the US dollar with increased interest in gold as a reserve asset, fears of stagflation in developed economies as growth slows, and political and trade uncertainties, remain more relevant than ever. Despite this, equity investors remain sceptical of the trajectory of the gold price, with valuations of the miners, including those mentioned above, screening as very compelling at the spot price.

The offshore component of the Stable Fund was a contributor to overall returns, primarily driven by stock selection. Defence-related holdings were among the leading contributors, having benefited from increased global

Where the money is going

When it comes to investing, the sectors most preferred by investors are banks, software and apparel retail. Domestic defensives and mining assets have also gained in popularity, but real estate, life insurance and chemicals were the stocks least preferred.

A net 54% said equities are undervalued, but only 8% are overweight on local equities. A higher net 69% of managers (33% in March) said local bonds are undervalued, marking the 71st straight month of undervaluation in a row.

Cash and gold still rule

More managers are looking to invest cash in South Africa, but none plan to increase overall cash holdings. Gold has returned to neutral from underweight, with positioning near record highs. The asset has repeatedly hit new peaks over the past year, driven by global uncertainty.

defence spending and European government commitments to future defence investment. US dollar weakness also aided returns, given the Stable Fund’s underweight exposure. The offshore component has been positioned against the narrative of American exceptionalism for some time and continues to have limited US exposure.

Looking ahead

It is worthwhile noting that continuing market upheaval poses a possible threat to wider risk asset returns – namely, the sustainability of the government of national unity locally following the conflict-ridden Budget process and the ratcheting up of global trade tensions after President Donald Trump’s ‘Liberation Day’ tariff announcements. We have concerns regarding unsustainable valuation levels both locally and globally, and what this may mean for future returns. This, coupled with geopolitical pressures and elevated uncertainty, makes for increased market volatility ahead.

In our opinion, the Stable Fund’s current defensive positioning in terms of stock selection, a 25% net equity weight (which is below the 40% maximum), its sizeable asset allocation towards hedged equities, and its lower-duration bond holdings ensures that we are well placed to navigate these challenges.

Time is the greatest gift of all. And we all want more time to spend on the things that are important to us. Whatever those things may be, the good news is that if you invest early, time gives you money. And then, money gives you more time to spend on the things you love. Speak to us to make the most of your time. Call Allan Gray on 0860 000 654, or your financial adviser, or visit www.allangray.co.za.

Allan Gray is an authorised FSP.

By Roger Eskinazi Managing Partner at Tickmill

WHow bonds can balance your trading strategy in uncertain times

hile global markets have been on somewhat of a rollercoaster since Trump’s re-election in November 2024, traders’ nerves have been particularly tested this past month. The CBOE Volatility Index (VIX) U – one of the most widely used gauges of market turbulence – recently spiked to its highest level since the Covid-19 pandemic. This latest surge followed growing fears of a global recession, sparked by Trump’s sweeping new tariffs.

In these times of extreme market uncertainty, Roger Eskinazi, Managing Partner at Tickmill South Africa, believes that a balanced trading strategy is key. “If you haven’t done so before, now may be a good time to consider incorporating bonds into your portfolio,” he suggests. “While no asset is entirely immune to volatility, bonds tend to exhibit lower correlation with highrisk assets, making them valuable during periods of market stress.”

The core appeal of bonds lies in three characteristics: relative stability, predictable income, and portfolio diversification. Unlike equities, which are subject to price swings based on earnings, sentiment, and macroeconomic data, bonds typically deliver fixed interest payments over a set period. This predictability can be invaluable when broader markets are whipsawing in response to political headlines or economic indicators.

Balancing risk with strategic bond exposure

“Diversifying with bonds doesn’t mean giving up on returns,” Eskinazi adds. “It’s about managing volatility and protecting capital. Sovereign bonds, for example, often perform well when equities are under pressure, while corporate bonds can offer more attractive yields depending on the credit profile and market outlook.”

Sovereign bonds, such as US Treasuries or German bunds, are backed by governments and generally offer the lowest risk – but also lower yields. These are often the first port of call for traders seeking to de-risk during periods of uncertainty. Corporate bonds, issued by companies to raise capital, present a broader risk-reward spectrum.

High-grade corporate bonds can provide a yield premium over sovereign bonds with moderate risk, while high-yield (or junk) bonds offer even greater returns but come with elevated credit risk.

Traders can also use bond duration and credit risk profiles tactically. Shorterduration bonds tend to be less sensitive to interest rate movements, while longerduration instruments may benefit from falling rates. “With central banks around the world navigating inflation and growth concerns, understanding these dynamics is essential,” notes Eskinazi.

“Diversifying with bonds doesn’t mean giving up on returns”

How to trade bonds

Unlike stocks, Eskinazi explains that there’s no central exchange to buy and sell bonds. “The bond market is an ‘over-the-counter’ market, which is much bigger than the stock market. It’s also important to note that, as a trader, you aren’t directly buying or selling the bond, you’re simply speculating about how the bond will appreciate or depreciate in value over time.”

Tickmill traders can access leveraged bonds via Contracts for Differences (CFDs). The platform currently offers trading on seven bonds, including German Government Bonds, with spreads from 0 pips and leverage up to 1:100, allowing traders to diversify effectively while managing risk.

A note of caution: No asset is risk-free. While bonds can be a valuable tool for managing volatility, Eskinazi emphasises that they are not risk-free. “Bond prices can fall due to rising interest rates, inflation expectations, or credit events. Sovereign defaults, though rare in developed markets, are not impossible, and liquidity in corporate bond markets can also dry up quickly in times of stress. That said, in a market this unpredictable, the potential of bonds as a stabilising force in a trading strategy should not be ignored,” he concludes.

From generation to generation: Securing tomorrow’s clients today

By Nic Smit Product and Pricing Executive at Bidvest Life

Many financial advisers are facing a very real concern: the clients you have built longstanding relationships with are ageing, and their life insurance needs are declining. If your books are weighted toward clients nearing retirement age, it can feel like the market is shrinking. But there is another way to look at it.

According to ASISA’s 2022 Life and Disability Insurance Gap Study1, 56% of South African income earners are under 40 – but are considerably underinsured. Of those who have life insurance, income earners under the age of 30 have R1.7m less disability cover and R1.6m less life cover than what they might realistically need. For those aged 30-39, the gap is R1.8m (disability) and R1.4m (life).

This is not just a statistical gap. It is an upselling business opportunity, if you can navigate your way around these clients’ main concern: affordability. Being able to structure the right product mix for younger clients’ budgets and real risks can go a long way towards providing the cover they need, and your starting point should always be income protection.

The need for income protection shows up in our Bidvest Life Claims Report every year. In 2022, we had 200 times more income protection than lump sum disability claims2. When it comes to younger clients’ claims, full-time tertiary students were the occupation group most likely to claim on income protection among Gen Zs (aged 13-28) in 2023.

These are not abstract trends. They are real-life situations affecting real young people, right now.

Understanding the lifecycle of cover is key. Students may not need death cover now but, as the claims statistics show, they need income protection in case a temporary illness or disability keeps them from completing their studies. Young professionals buying their first homes need a different mix of benefits, as do those who are starting families. Early engagement with these clients means better understanding and affordability, and your ability to position yourself as relevant at every life stage can play a huge role in whether your student clients are still with you after they graduate.

This next generation is not a cold-start audience. You have already built years of trust with your existing clients; clients who are now parents, mentors and role models. Encourage them to think beyond their own cover, and to have life insurance conversations with their children, who may be students, young professionals, or new parents. Start with the families you already know and begin with the fact that you are not just a retirement specialist – you are there for every stage of life, for every member of the family.

Partnering with a life insurer that equips you to have these conversations, and that provides holistic support to back up a range of products that protect your clients from childhood through all their life stages, can make all the difference.

Tomorrow’s clients are not strangers. They are already sitting at the dinner table with today’s clients. By sitting with them now, you can secure your place at the table for decades to come.

“More than 76% of medical devices in the South African market are imported, like some myoelectric arms (a high-tech prosthesis controlled by bio-electrical signals), so the cost of this technology is often prohibitively high,” says Friedlander. “The MedTech Booster payments, however, are made as an upfront payment, and provide payments every three years to assist with the costs of the ongoing maintenance of the technology.”

The Severe Illness Benefit

The Dollar Life Plan’s Severe Illness Benefit pays out a lump sum in USD for over 200 conditions. Policyholders can have cover until they are 65, or for their entire lifetime. This benefit offers a host of additional benefits, such as a Global Treatment Benefit, which covers policyholders for international healthcare procedures and gives them access to expert medical practitioners and facilities around the world, a Cancer Relapse Benefit, an Early Cancer Benefit, and the Cancer Exome Sequencing Benefit, which provides a payout to assist in funding the costs of sequencing of certain highrisk tumours.

“We see a very real need for clients to match their highly specialised medical needs. Complex treatments for cancer can cost more than R1m a year. These costs are growing at a faster rate than South African inflation, as a lot of research and development occurs internationally,” notes Friedlander.

The Dollar Global Education Protector

The Dollar Global Education Protector covers the education costs for a policyholder’s children, from crèche through to tertiary education, in the event of the policyholder’s death, severe illness or disability. By managing health and wellness, policyholders can fund up to 100% of their children’s tertiary tuition fees, even if they don’t claim.

“Some brokers still only consider risk protection plans in a single, local currency”

“Our research shows that for the last five years, at least 12 000 South African students have been studying abroad every year, while education inflation is consistently around 2.5% higher than normal inflation, locally and abroad. The top three universities in the 2024 Times Higher Education World University Rankings – University of Oxford, Stanford University, and Massachusetts Institute of Technology (MIT)18 – cost multiples of what top local universities charge,” notes Friedlander. “It’s no surprise that Discovery Life continues to see a strong demand from our clients to hedge against education costs where there is the possibility of a child studying overseas.”

Brokers need to adopt a global mindset

“Comprehensive and relevant life insurance means that policyholders can weather the financial impact that life-changing events bring. A well-structured life insurance policy can assist in providing financial protection, so that finances are one less thing to worry about,” highlights Friedlander.

“As more South Africans see value in a global way of life, it is important that their trusted financial advisers keep abreast of global financial planning and risk protection options,” advises Friedlander. “Impetus is definitely there. From just a handful of advisers using the Dollar Life Plan as part of their risk-planning approach for their clients in 2014, the number has grown to 1 190 advisers countrywide who have used this option with their clients.

“Affordable, accessible and diversified life insurance – that pays out in dollars – helps to future-proof whatever responsibilities, liabilities or aspirations policyholders may have, no matter where they are in the world.”

By

Matthew Gezane Franchise Development Manager at Consult by Momentum

TTrade shocks and the short-term insurance squeeze

he short-term insurance industry is facing increased pressure from global trade uncertainty caused by US President Donald Trump’s erratic policies. These developments are likely to deepen financial strain on policyholders while simultaneously threatening the growth and stability of the insurance sector itself.

For businesses in particular, the situation is complex. Earlier this year, the United States announced a 31% tariff on South African exports – since paused for 90 days, but with a 10% flat-rate tariff still in effect. These tariffs erode the benefits previously enjoyed under the African Growth and Opportunity Act (AGOA), making South African goods less competitive in the US market. Businesses are now facing tough choices: absorb the cost, raise prices, or cut expenses somewhere.

“The net effect for insurers is a shrinking pool of insurable economic activity”

Short-term insurance is often viewed as a grudge purchase – important, but ultimately expendable when budgets are tight. This places insurance in the firing line when businesses look for ways to reduce overheads and protect profit margins.

The consequences are likely to ripple through the broader insurance industry. Shortterm insurers rely on robust economic activity – especially in manufacturing and exports – to drive premium growth and policy retention. A slowdown in

production or the withdrawal of South African businesses from international markets could lead to reduced cover levels, cancelled policies or increased claims volatility.

At a macro level, this contributes to a broader economic dilemma. South Africa is a small, open, consumptionled economy. We import more than we export, which leaves us with a trade deficit. When exports decline – either due to punitive tariffs or declining competitiveness – our balance of payments weakens further, adding to the fragility of the rand and dampening investor confidence.

The net effect for insurers is a shrinking pool of insurable economic activity, heightened policyholder risk, and pressure on margins. For policyholders, it means navigating a shifting landscape where prices rise, coverage narrows, and the fine print becomes ever more important.

Now, more than ever, sound financial advice matters. At Consult, our advisers are equipped to help clients understand these dynamics –not just to find affordable cover, but to make strategic decisions that protect their long-term financial dreams.

When it comes to reassessing business risk in a volatile trade environment, the right advice can be the difference between surviving the storm or being overwhelmed by it.

In uncertain times, insurance may be one of the first expenses to face the axe. But in uncertain times – and coupled with the right guidance – it is one of the most valuable weapons of defence in your arsenal.

By Paul Sanders Regional Managing Director at GIB Inland, and

TTracy McLaughlin Regional Managing Director at GIB Coastal

he insurance industry, like many others, is undergoing significant transformation, driven largely by disruptive technologies, changing consumer behaviour, and an increasingly complex global landscape. As we move further into 2025, these shifts are creating both opportunities and challenges for insurers, brokers, and customers alike. Here we shed light on the key trends defining the future of the industry.

1

Softening of London markets

Over the past two years, investor capital has flowed into global insurance markets, increasing capacity and competition, particularly in London, which has led to lower rates for corporate insurance. Locally, however, the market remains more stable.

“The increased capacity in London is reshaping the competitive environment,” says Sanders. But locally, markets are holding steady. This dynamic will be crucial in 2025, especially for businesses seeking coverage that aligns with their unique risk profiles, industry-specific exposures, and financial strategies.”

2

Economic pressures and evolving consumer behaviour

Affordability is top of mind for consumers as economic pressures persist. Many are reducing their insurance spend, especially in personal lines, and direct insurers are benefitting from this shift with their lower-cost, online-first offerings.

“Consumers are increasingly focused on price, but brokers remain uniquely positioned to provide tailored advice, particularly in complex areas like life insurance and comprehensive household cover,” adds McLaughlin.

3 The rise of Insurtech startups

The rise of Insurtech startups, such as Naked and Partnership, is a trend that brings efficiency and streamlined processes to the forefront, providing lower-cost solutions for consumers. However, Sanders highlights that while Insurtech firms excel at efficiency, they can’t replicate the personal relationships brokers offer, especially when it comes to managing claims. “The human element is a huge differentiator, particularly for clients with complex needs or higher-value claims.”

4

AI and automation: A double-edged sword

AI and automation enable faster, more accurate assessments, reducing human error and operational bottlenecks. However, this

Key trends shaping the insurance industry in 2025

shift has its challenges. Automation improves efficiency, for example, but it limits the broker’s ability to negotiate terms, which remains a vital part of their role. Even in the case of larger clients, AI-driven analytics are essential for offering insights into things like self-retention structures, but it’s the broker’s personal touch that adds real value.

5 Geopolitical and global market uncertainty

Events in major markets, from tariff shifts to political instability, have far-reaching implications for South African businesses.

“The geopolitical landscape can affect insurance availability, pricing, and even regulatory frameworks,” explains Sanders. “Unexpected global events are now part of the risk matrix our clients face daily.”

6 Personalised insurance through behavioural data

With the proliferation of IoT devices, wearable tech and telematics, insurers now have access to unprecedented volumes of data. This allows for personalised pricing models based on individual behaviour, not just traditional demographic factors. “There’s a big opportunity here,” says McLaughlin. “If used right, data can help us proactively guide clients – not just respond to risk but help prevent it.”

7 Shifts in customer loyalty and purchasing behaviour

Loyalty in personal insurance is decreasing. Many customers, especially younger ones, prefer simplicity, speed, and low costs. Direct insurance companies are becoming advanced online platforms to meet these demands.

For more complex needs, like commercial or household insurance, brokers are still important. “They help clients understand their risks and the coverage they need,” says Tracy.

8 Proactive risk management and shifting insurer expectations

Demand for insurance remains steady, but the requirements from insurers have changed. There is an increasing focus on proactive risk management and stronger client governance. “Insurers are asking more questions now,” says Sanders. “They want to see that clients are actively managing their risk environment before they offer capacity. This is where brokers play a vital role in helping clients prepare and demonstrate their readiness.”

9 Adapting to the climate crisis

The escalating frequency and severity of natural disasters are leading to higher insurance premiums, particularly in highrisk areas. Insurers are reassessing coverage strategies and collaborating with governments to manage the financial implications of climate-related events. This trend is pushing insurers to develop innovative solutions to mitigate the financial risks posed by climate change, while also striving for greater sustainability in their operations and offerings. Additionally, third-party valuations and more detailed risk assessments are becoming standard practice, reflecting the sector’s commitment to precision and adaptability. As the industry continues to mature, there’s a stronger focus on professionalism – not just for regulatory reasons, but to truly add value to clients

“While Insurtech firms excel at efficiency, they can’t replicate the personal relationships brokers offer”

By Dr Andrew Dickson Engineering Executive, CBi-electric: low voltage

MWhat SA’s insurance industry gets wrong about surge protection

eeting insurer requirements doesn’t necessarily guarantee that South Africans are sufficiently protected against power surges. In a country where lightning strikes, loadshedding and grid instability are everyday occurrences, this oversight could have costly consequences for both parties.

Insurers are increasingly requiring surge protection devices (SPDs) for property owners. However, do these requirements genuinely safeguard policyholders and their assets, or are they simply fulfilling a compliance obligation without offering meaningful protection against real-world electrical threats?

Not all surges are the same

Electrical surges vary in origin and intensity. Some are dramatic, like those caused by direct lightning strikes. Others are smaller but equally damaging, such as switching transients triggered when power is lost and restored during loadshedding, or by everyday fluctuations caused by short circuits and other electrical faults.

These surges behave differently and pose unique risks. Yet many insurance policies recommend a one-size-fits-all approach to protection – typically requiring the same type of SPD regardless of a property’s location, use case, or exposure level. This blanket approach may fall short of protecting the very assets these policies are designed to cover.

What insurers require vs what properties need

While insurers have some alignment with the national wiring code by mandating Class 2 SPDs for low-voltage installations, their insistence on higher kA ratings reflects a misconception that higher peak values are a silver bullet in providing effective protection, which is not necessarily the case.

For reference, there are three classes of SPDs, namely 1, 2 and 3. Class 1 SPDs are designed to handle extreme surges from direct lightning strikes and are typically installed where power enters a premises or building. They act as the first line of defence, intercepting high-energy surges before they

“Many insurance policies recommend a onesize-fits-all approach to surge protection”

can enter the internal electrical distribution system. These devices are also typically used in remote areas, locations at high risk of direct lightning strikes on incoming services, or where there’s a threat of explosions or damage to sensitive equipment.

More common in domestic settings, Class 2 devices offer protection from smaller surges associated with indirect lightning strikes or switching transients in urban areas.

Class 3 protectors provide localised protection for sensitive electronics like televisions, routers, or gaming systems and are located at the point of consumption. Each class serves a different purpose, and the best protection often involves a layered approach. Tailoring the solution to the property’s risk profile is essential.

The truth about 40kA ratings

While the SPD class defines the type of surges the device is designed to handle, the kA rating is another piece of the protection puzzle. This rating indicates the maximum current the device can divert in a single event.

Insurers often specify a 40kA rating, based on the belief that higher ratings equate to better protection. But that’s not always true. It’s like using a 10-pound hammer to drive in a 10mm nail: it might work, but it’s excessive and inefficient.

In practice, what matters more is how the SPD performs under repeated smaller surges –the kind that happen most often and result in

cumulative wear. Devices degrade over time, regardless of their kA rating. That’s why the joule rating, which indicates how much total energy the SPD can absorb, is an important guide to long-term protection. Both values – the kA rating and the joule rating – should be considered together when specifying SPD requirements for an installation. This ensures a more holistic approach to surge protection and means more effective, practical policy guidelines from insurers.

Moving beyond compliance to genuine protection

It’s encouraging that insurers are starting to mandate SPDs, but these recommendations must go further. Relying solely on class and kA rating, without considering real-world electrical threats, can leave gaps in protection or provide a false sense of security.