Women are increasingly shaping the financial services landscape – as advisers, leaders and clients. We celebrate their progress, examine their challenges and evaulate the powerful impact of gender diversity.

Pg 7-11

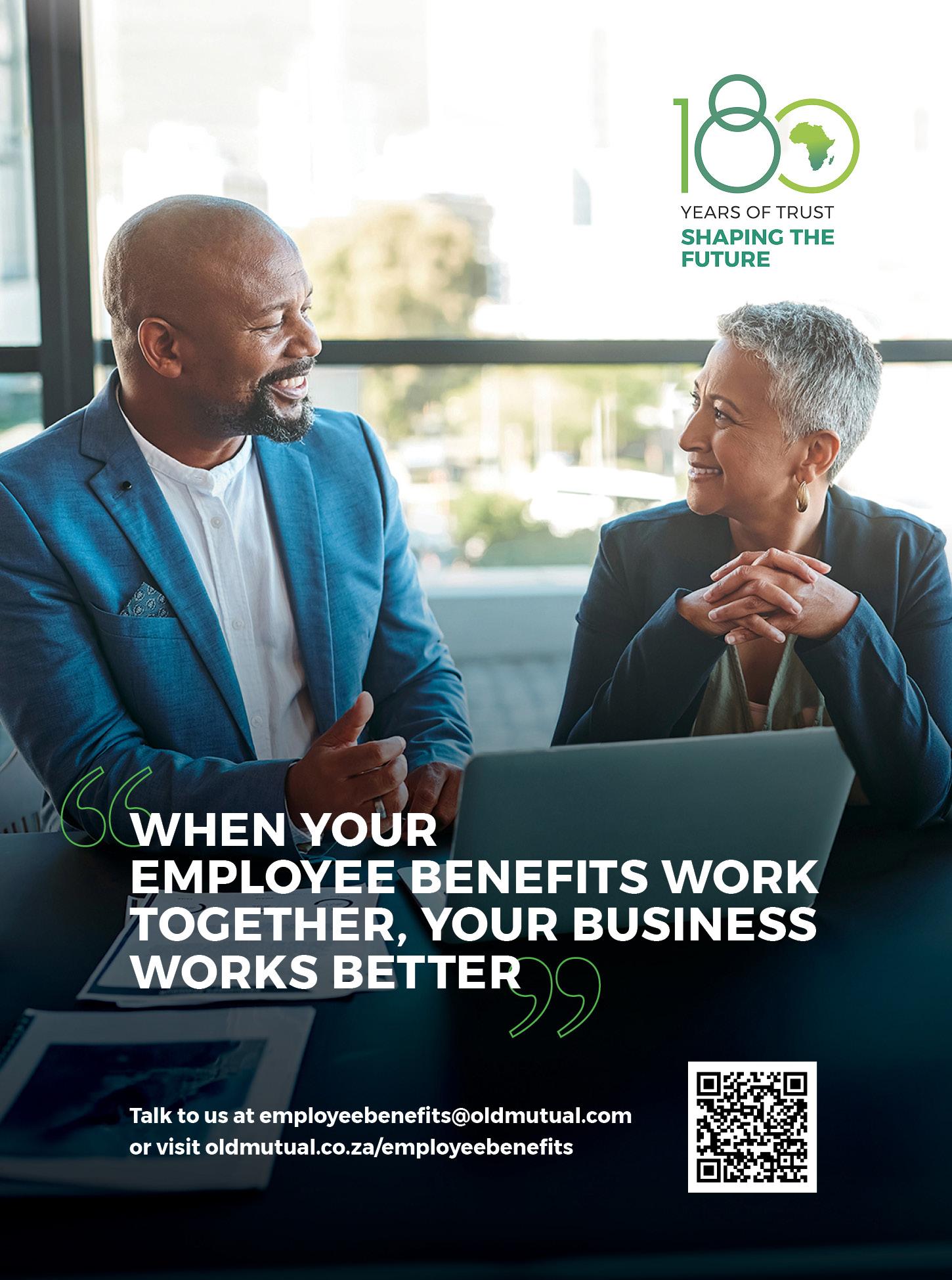

EMPLOYEE BENEFITS

With rising employee expectations and economic uncertainty, benefits strategies are changing swiftly. This article explores how financial advisers can help clients build competitive, cost-effective offerings that attract and retain talent. Cover story + Pg 14 - 16

SHARI’AH INVESTING

Demand for ethical, faith-based investing is growing steadily. We look at how Shari’ah-compliant investment solutions offer both financial returns and values-driven impact.

Pg 17 - 18

BEHAVIOURAL FINANCE

Understanding how clients think about money is as important as the numbers themselves. This feature unpacks key behavioural finance insights to help advisers better guide decision-making and manage bias.

Pg 20-23

WANT MORE VALUE FROM YOUR INBOX?

Scan to subscribe to our weekly newsletters.

Reframing Investments for Employee Benefits:

Why cost, clarity and indexing matter more than ever

By Sandy Welch Editor, MoneyMarketing

As the financial landscape grows more complex, the way we think about employee benefits, especially within the retirement space, must evolve. According to Louis Theron, Head of Investments at Liberty Corporate Benefits, this evolution is already well underway. “For us, it’s not just about umbrella funds anymore,” he says. “It’s about becoming a relevant and trusted institutional-grade investment brand in our own right.”

Shifting the perception of value

Liberty, as part of the Standard Bank Group’s Insurance and Asset Management cluster, has had a longstanding presence in the corporate benefits space.

But in recent years, says Theron, Liberty Corporate Benefits has placed renewed focus on positioning itself as more than just an insurer. “We’ve invested significantly in our institutional investment capabilities, and our portfolios and annuity products for this market segment have been performing well,” he notes.

“That’s why we want to be seen not only as a provider of umbrella fund solutions, but as a serious player when it comes to broader structured, policy-backed investment offerings.”

To support this strategic direction, Liberty Corporate Benefits has combined its internal teams, merging investment, annuity product and operational capabilities into a single integrated unit of approximately 40 experienced professionals. This ensures end-to-end delivery, from product and proposition design to risk management and daily asset-liability matching and other investment operation functions. “In the past, our teams were a bit siloed,” admits Theron. “But if we want to grow our assets under management and stay relevant in the market, the back end has to be as streamlined as the front.”

A strategic focus on cost efficiency

One of the biggest drivers of this repositioning has been a sharpened focus on fees –something that matters deeply to both pre- and post-retirement outcomes. “The reality is that lower costs translate into better retirement savings and better retirement income levels for members,” says Theron. “And trustees now have a much more active role in negotiating

institutional-level fees, thanks to the 2019 Default Regulations under the Pension Funds Act. Fees are no longer just a number on a fact sheet,” says Theron. “They’re part of the value conversation. And as advisers, that’s where you have the power to make a real difference.”

This has created an opportunity for Liberty Corporate Benefits to offer not just umbrella fund solutions, but competitively priced annuity products, including living annuities, guaranteed increasing life annuities, and with-profit life annuity options, all at institutional rates. “Even if a client works with an independent adviser, they can access these annuities, provided their retirement fund has contracted with us,” he explains.

The role of index tracking

At the heart of Liberty Corporate Benefits’ investment customer value proposition is a strong commitment to index tracking as the solution for a relevant customer need. While active management certainly has a role to play, Theron believes index solutions are gaining serious traction, especially in South Africa’s institutional retirement space. Theron quoted research done by 10X Investments, showing that “in the US, more than 50% of all investable assets are in index-tracking funds. In South Africa, that number is still below 10%. That leaves a massive opportunity – in the trillions of rands – for growth in this space. If that same expectation was to flow into South Africa, then we are going to see a lot of opportunities for index tracking providers,” says Theron. The rationale is compelling, according to the S&P Indices Versus Active (SPIVA) South Africa Scorecard: not only are 92% of active equity managers underperforming their benchmarks over the past decade, but they also tend to charge higher fees, creating a double burden for members. “That’s a bleak outcome,” he adds. “Traditional, vanilla index tracking portfolios by design aim to meet the market, giving trustees more certainty and stability when matching long-term investment objectives.”

Image:

DIFFERENT THINKING.

BETTER OUTCOMES.

At Mazi, diversity isn't a buzzword - it's strategy in action. We intentionally build teams with diverse qualifications, experiences, and perspectives. This breadth of thinking sharpens our decision-making and helps us uncover opportunities others might miss.

It's how we deliver high-impact results and uncover value in unexpected places. High Equity Balanced Fund New - Stable Fund New - South African Equity Fund Africa Equuity Fund - Globaal Equity Fund - Money Market - Hedge Funds

Continued from previous page

The key drivers? Cost, transparency and consistency. “Index tracking offers low fees and dependable performance in a world where traditional active managers are under pressure to deliver alpha,” says Theron. “And that’s not just an investment trend; it’s a structural shift.”

Tracking more than just the market

The index-tracking space itself has matured significantly. It now offers sophisticated tools beyond traditional passive investing. ESGfocused indices, for example, allow trustees to align investment choices with sustainability mandates without the administrative burden of defining, adhering to and continuously monitoring complex criteria. “The ESG philosophy is already baked into the index,” Theron explains.

Other innovations, like smart beta and factor investing, further refine performance potential while remaining rules-based and cost-effective. “These strategies still remove the subjectivity of active stock picking, but they allow for enhancements – like targeting high-dividendyielding stocks or lower volatility,” says Theron.

A cradle-to-grave investment philosophy

Theron points out that Liberty Corporate Benefits’ commitment to index tracking spans the entire retirement lifecycle of a member, from accumulation through to post-retirement solutions. “Someone can be invested in the same diversified market exposure for 60 years, which would be from their first contribution to their last annuity payout,” he says.

This level of continuity is particularly attractive for employers looking to offer competitive, transparent and cost-efficient pre- and postretirement benefits. Liberty Corporate Benefits’ internal umbrella fund and several external standalone funds under its care have adopted this approach, with over ten (10) billion rand invested in index solutions and consistently strong performance.

“What often gets overlooked is that these bespoke approaches can also deliver real financial advantages”

Balancing simplicity with precision

While index investing offers simplicity and transparency, Theron is quick to point out the increasing demand for bespoke customer solutions. It’s clear that employee benefits (retirement funding as well as other types of employee benefits) have entered a new era that requires greater customisation, smarter use of technology, and

a deeper understanding of each member’s long-term financial needs.

Whether it’s integrating longevity protection into post-retirement medical aid subsidy funding solutions or designing blended portfolios that combine index tracking with additional risk-return layers, Liberty Corporate Benefits focuses on understanding the employer’s underlying need before building tailored solutions. “The higher the level of customisation and the more risk that’s transferred or managed, the more expensive the solution,” says Theron. “But what often gets overlooked is that these bespoke approaches can also deliver real financial advantages, like accelerated tax benefits for employers when certain insurance-backed solutions are implemented.

“Some employers are struggling with legacy medical aid subsidy liabilities. Others want to retain control while ensuring pensioners are secure,” he says. “We break down the obligation into its smaller, easierto-understand components, and then build a customised, often multi-layered solution, backed by both investment performance and insurance peace of mind.”

Certainty in an uncertain world

Theron points to policy-backed investments as a major stabilising force in uncertain times. These investment structures provide peace of mind, not only by simplifying complex backend processes but by offering clearly defined outcomes to members. Whether that’s a guaranteed income for life for pensioners or index-tracking certainty for members with a market-linked appetite, these policies help members and employers navigate volatility with greater clarity.

Then there’s the much-debated two-pot retirement system, which, while bringing short-term liquidity to members, also opens the door to longer-term reforms, most notably in annuitisation. “Right now, cash is still king. But that’s going to change,” Theron predicts. “The new rules will slowly but surely increase demand for both life and living annuities. It’s no longer just about saving up to retirement, it’s about planning from the first paycheck right through to the end of life.”

Liberty Corporate Benefits is already preparing for that shift, designing liquid portfolios that process two-pot withdrawals efficiently, while keeping a firm eye on longterm investment goals. And while artificial intelligence is quietly reshaping back-end investment modelling and client services, Theron is adamant that “showing up for individuals – whether through a chatbot or a warm voice on the phone – remains non-negotiable”.

What this means for advisers

For financial advisers, the implications are clear. Firstly, there is growing access to sophisticated, institutional-grade solutions at

ED'S LETTER

Towards the end of July, I attended the online Glacier Life Covered Investments Summit 2025, and it offered no shortage of valuable insights. One comment that really resonated came from Jeremy Gardiner, Director at Ninety One, who spoke about the critical role financial advisers play in helping clients navigate uncertainty. Reflecting on the wave of calls they received following Trump’s so-called Liberation Day announcement in early April, he highlighted how essential it is for advisers to help clients resist emotionally driven decisions. In volatile times, behavioural finance becomes one of the most important tools in an adviser’s arsenal. This month, we explore how advisers can ensure rationality prevails – especially as AI becomes more integrated into client experiences. Technology may be advancing rapidly, but the need for human judgement is more vital than ever.

August is also Women’s Month, and we’re proud to shine a spotlight on some of the inspiring women reshaping the finance industry. Their stories of challenge, grit and achievement are worth celebrating.

We also explore the ever-changing employee benefits landscape. As employers seek to attract and retain top talent, offering meaningful, well-structured benefits is critical. But how do companies ensure they’re providing the best value and solutions for their workforce?

Lastly, we take a closer look at Shari’ah investing. More than just a religious imperative, it reflects a growing appetite for ethical and responsible investment choices. Stay financially savvy,

Sandy Welch Editor, MoneyMarketing

Note: If you subscribe to our MoneyMarketing newsletter, see QR code on the cover, you will receive a special discount off a News24 or Netwerk24 subscription*.

*Offer available to new subscribers only.

competitive prices, which can greatly benefit clients. Secondly, understanding the nuances of index tracking and the fee landscape has never been more critical. And lastly, engaging with providers who can offer integrated, endto-end solutions ensures both compliance with regulation and alignment with client outcomes. As the industry adapts, one thing is certain: employee benefits are no longer just a safety net. Done right, they’re a platform for resilience, reinvention and lifelong financial dignity, which will provide much-needed peace of mind to employees and their families.

Louis Theron

Yvonne Makwela

Key Accounts Manager, Fairheads Benefit Services

How did you get involved in financial services – was it something you always wanted to do? Financial services never really crossed my mind when I was thinking about Matric subject choices and a career. Engineering was what I had considered at first. However, for various reasons I landed up doing a BCom in Economics at university and I loved it. On graduating, I did a learnership with FNB as a credit analyst and then worked at Tracker also as a credit analyst before moving into financial advice at Liberty. In 2008, I saw a position advertised by Fairheads for a trust consultant. I was intrigued and applied for the job. I learnt from the bottom up and gained broad exposure to Fairheads’ overall business. For example, if one is to work advising people on umbrella trusts, you need to know how the administration behind that works. In 2015 I was appointed to Key Accounts Manager and have continued to work in the trust and beneficiary fund consulting arena, including trustee training. Looking back, I can see

What was your first investment – and do you still have it?

My first investment was into a retirement annuity – 14 years on, I still have it! My parents set an excellent example to me in terms of being able to retire comfortably. I believe each and every one of us is responsible for our retirement and you can never start saving early enough. I would never like my children to have to support me in my old age.

What have been your best – and worst –financial moments?

My worst financial moment is a salutary lesson. My father had set aside funds for my education into an endowment policy. At age 21 I was able to access the money and instead of using it prudently I went on a spending spree. I often think of this when advising Fairheads members and beneficiaries about taking their funds at age 18. As a company we have long lobbied the authorities to change the account termination age of 18 to 21, for precisely the reason that most 18-year-olds are still at school and not financially savvy enough to handle large sums of money.

“We have a long way to go still to make financial matters more inclusive and accessible to the average citizen”

My best financial moment was when I used a bonus to pay off my car. It was the best decision ever to get rid of debt and that is why I always advise people to live with as little debt as possible.

What are some of the biggest lessons you have learnt in and about the finance industry?

The financial industry is not for the man in the street. We have a long way to go still to make financial matters more inclusive and accessible to the average citizen. Consider that many large corporations still do not communicate with their clients in plain language. Consumer literacy needs to be improved and urgently, so that people can be empowered to take care of their financial future for themselves and their loved ones –and know how to avoid scams.

It is important for young people to develop a healthy relationship with money. Parents should not be shy to talk finances and budgets with their children and should encourage them to ask questions.

What makes a good investment in today’s economic environment?

There are many savings instruments available. Unless you are skilled in investing it is essential to enlist the services of an adviser. The markets are always up and down and so Investing 101 is to set goals, design a plan around the goals and then stick to that plan. And it is very important to be patient.

I have found that a useful savings vehicle for my children’s education has been government retail bonds as these are costeffective and produce steady returns. An RA is a sensible retirement savings option given their tax advantages. Equities, of course, have the potential for higher growth; however, unless you are an expert, the best course of action is to invest through an experienced and reputable investment manager.

What finance/investment trends and macroeconomic realities are currently on your watchlist?

Like everyone else I know, events in the USA are on my watchlist, and checking what the Trump and Fed are going to do next as the US economy has an impact on the global stage. I also watch local politics.

What are some of the best books on finance/ investing that you’ve ever read – and why would you recommend them to others?

Millions of people have read Rich Dad Poor Dad, a 1997 book written by Robert T. Kiyosaki and Sharon Lechter. It advocates the importance of financial literacy, financial independence and building wealth. I have found it to be an easy and fun read and could recommend it to anyone wanting to learn more about finances.

Then, I also enjoyed and can recommend The Psychology of Money. Here, awardwinning author Morgan Housel shares 19 short stories exploring the strange ways people think about money and teaches you how to make better sense of one of life’s most important topics.

By Anri Dippenaar Masthead Head of Compliance, and Shanal Boodiram Masthead Compliance Manager

Are you ready for COFI?

You’ve reviewed your systems and processes to ensure your FSP complies with the proposed Conduct of Financial Institutions (COFI) Bill and supports data-driven regulatory reporting – are you really prepared for the impact of these upcoming changes?

The most advanced data capturing or client management system will mean little if your team isn’t properly trained to use it. Do they know how to operate the new systems and understand what data needs to be captured? Are they aware of the importance of that same data in the context of measuring Treating Customers Fairly (TCF) Outcomes and how they can promote and improve these outcomes within the business? FSPs that take proactive steps to train their staff now will benefit greatly.

How your business will benefit COFI will bring a greater focus on fostering TCF. And while the FSCA recently announced that it is stepping away from the original Omni-CBR format as part of their digital transformation strategy, the revised approach and planned supervisory technology platform – the Integrated Regulatory Solution (IRS) – will still require FSPs to collect and submit data to the regulator. Financial institutions will have to demonstrate that they’re delivering fair outcomes, backed by solid data.

The benefits of using technology and tools to enhance data collection and risk management are clear: FSPs that can use these tools to improve their view of business performance and results, focusing on customer outcomes, will be a step ahead of those who don’t, regardless of when COFI comes into effect.

However, advanced tools and business processes mean little without proper and ongoing staff training. Employees may not

fully understand how the changed business approach relates to TCF, how their roles will change, or how to operate the new systems and tools – and how all these elements are critical to management information (MI). This can lead to inefficiencies, inadequate data, increased costs, compliance gaps and even potential regulatory sanctions.

Crucially, a one-size-fits-all approach to training won’t suffice. Training programmes should be customised to the specific needs of the business concerning existing regulations, like the FAIS Act, the impact of future regulations, like COFI, and the particular roles and responsibilities of employees as they evolve under the new legislation.

Outcomes-based regulation focuses on TCF Outcomes and ensuring that financial products and services meet client needs. All staff must be well-versed in the TCF Outcomes and how they can promote these principles in the business, client relations, handling complaints efficiently, and maintaining high standards of customer service.

Common training pitfalls to avoid

• Generic training programmes: Standardised training sessions don’t cater to the specific needs of distinct roles within the organisation. Tailored training programmes that address the unique responsibilities of various staff members are crucial.

• Neglecting administrative staff: Training should not be limited to client-facing roles and management. Administrative staff play a critical role in data management and compliance reporting. Neglecting their training can lead to inaccuracies and inefficiencies.

• Procrastination: Delaying training until the regulatory deadlines approach can result in rushed, ineffective programmes. Early and continuous training ensures a smoother transition and better preparedness.

• Insufficient practical training: Theoretical knowledge alone is not enough. Practical, hands-on training that simulates real-world scenarios is essential for effective learning and application.

Tips for effective staff training

• Start early: Initially, Omni-CBR was expected to kick off in 2024 with a two-year transitional period. However, there have been delays,

and as mentioned before, the FSCA has announced a change in direction with their IRS platform. The COFI enactment date hasn’t been confirmed, but it’s expected to reach Parliament by next year. Still, this doesn’t mean you should delay training.

• Role-specific training: Customise training programmes to address the specific responsibilities of different roles. For example, if your administrative staff is responsible for recordkeeping, their training should focus on the data-capturing systems and what data needs to be collected. This will enable them to spot missing information, such as a representative forgetting to add the client’s age on a new client form. If your management team is responsible for root cause analysis, ensure they know how to analyse data effectively. When clients contact the FSP with a complaint, the first person they speak to should be trained on handling complaints and managing difficult conversations. Does everyone in the business know the six TCF Outcomes and how their actions can foster a culture of TCF?

• Practical exercises: Incorporate practical exercises and simulations into training sessions. Real-world scenarios help staff understand how to apply their knowledge effectively.

• Continuous learning: Make training an ongoing process rather than a one-time event. Regular refresher courses and updates on regulatory changes keep staff informed and competent.

• Utilise external expertise: Partner with compliance experts or training providers to ensure high-quality, comprehensive training programmes. External experts can provide insights and guidance tailored to your organisation’s needs.

• Leadership involvement: Senior management should lead by example and participate in training sessions. Their involvement underscores the importance of proper training and motivates staff to take training seriously.

Give your staff the tools they need to succeed

By addressing common training pitfalls and implementing effective training strategies, FSPs can navigate the changing regulatory landscape with confidence. Early, role-specific and practical training programmes, supported by continuous learning and external expertise, will prepare staff to meet the challenges and opportunities presented by these new regulations.

EARN YOUR CPD POINTS

The FPI recognises the quality of the content of MoneyMarketing’s August 2025 issue and would like to reward its professional members with 2 verifiable CPD points/hours for reading the publication and gaining knowledge on relevant topics. For more information, visit our website at www.moneymarketing.co.za

By Francois du Toit CFP® PROpulsion

WThe habits that help you build a legendary practice

hat separates financial planners and advisers who thrive from those who stay stuck? I believe it comes down to habits. Not big ideas or grand strategies, but small, consistent actions that shape how we show up every day.

Here are seven habits that have helped me, and many others, build a stronger, more focused, and more fulfilling practice.

1

Know yourself and lead yourself

You can’t build anything sustainable if you don’t know who you are. Start by understanding what gives you energy, what drains you, and what comes naturally. Use tools, ask others, reflect. When you know yourself, you’ll stop chasing the wrong things and start aligning your work with your strengths. Everything else becomes easier.

2

Focus on what generates income first

Every day, ask yourself: what are the three things I need to do today that bring in income? Not the admin, not the to-do list, not the endless tasks that keep you busy. The actual things that drive revenue. Make sure everyone in your team does the same. Know what your role is and make it count.

3

Build on strong foundations

Don’t let your practice look good on the outside but be fragile behind the scenes. Keep your finances up to date. Defer the lifestyle upgrades. Take your own advice. Have cash buffers, put money aside for tax, and review your

numbers regularly. If you give advice to clients, make sure you’re following it too. Consider working with your own financial planner. Accountability matters.

4

Learn to say no

This one’s tough. But you can’t do everything. If you say yes to everyone and everything, your focus gets watered down. Set boundaries. Use buffers if needed. Have someone in your team protect your time. Saying no isn’t rude. It’s professional. It’s how you protect your energy and make space for the right things.

5

Build strong client relationships

Clients don’t need you for information anymore. They’ve got that at their fingertips. What they do need is care, understanding, and trust. Focus on the relationship, not the product. Make sure they feel seen, heard, and valued. Stay in touch regularly. Be there when it matters. That’s how you build loyalty.

6

Stay in your zone of genius

You’re not supposed to be good at everything. Trying to be will burn you out. Focus on what you do best. Delegate or outsource the rest. You don’t need to hire a full-time team right away. Start small. But do get help. You can’t push the car and steer it at the same time. Build a business that can move without you doing all the pushing.

7

Show up consistently

Success isn’t built on big bursts of effort. It’s built on reliability. Keep showing up. Do the reviews. Follow up. Stick to your commitments. When motivation dips (because it will), let systems and routines carry you through. Intensity comes and goes. Consistency is what compounds over time.

You don’t need to overhaul your life overnight. Just pick one habit and start there. Build it in. Make it automatic. Then stack the next one on top. Over time, you’ll create something powerful, one habit at a time. If I could add one last piece of advice: never stop learning. Whether it’s reading, courses, mentors, or talking with others, stay curious, keep growing, and don’t be afraid to ask questions.

That’s how legendary practices are built.

Stay curious!

It’s all about embracing strengths

Nicola Langridge, CFP®, Wealth Manager at Private Client Holdings

What unique challenges have you faced as a woman in your field, and how have you navigated them?

My biggest challenge has been believing in my own capabilities and trusting that what I bring to the table is of value. As a wealth manager, regardless of gender, we each have unique strengths to offer our clients. Embracing those strengths, rather than trying to be someone I’m not, was a turning point for me. There is a great deal of opportunity in our industry; however, it comes down to backing yourself and being willing to embrace those opportunities to grow.

How have you seen the landscape for women in the financial industry evolve, and what changes would you still like to see?

There are more women in wealth management now than when I started out. You notice it immediately when attending industry seminars and events. However, when speaking to young women in junior positions, many are still hesitant to take the leap into client-facing advisory roles. Their fears often centre around confidence in dealing with clients and the shift from a salaried position to a fee-based income. I would love to see more mentorship programmes that help young women build confidence in their abilities.

What advice would you give to young women who aspire to take on leadership roles in traditionally male-dominated fields?

One mistake we make as women is trying to do things the same way as our male colleagues, especially when it comes to networking or building a client base. Instead of fitting into a mould that doesn’t serve you, embrace what makes you different and let it strengthen your strategy. Find a mentor in the industry who embodies what you aspire to achieve. Throughout my career, having guidance from a variety of mentors – both within and outside of my organisation – has made all the difference.

Anshe Swart, CFP® AMLC Prac (SA), Head of Compliance at Private Client Holdings

What unique challenges have you faced as a woman in your field, and how have you navigated them?

I’ve struggled with imposter syndrome at times – doubting myself, not because of how others have

treated me, but because there aren’t many women at executive level or people to turn to for guidance. In medium-sized FSPs, where compliance is still evolving into a cornerstone of the business, that sense of isolation can feel even stronger. I have learned to manage this by focusing on the value I add, building supportive networks, and trusting that growth comes from showing up – even when I don’t feel 100% ready.

How have you seen the landscape for women in the financial industry evolve, and what changes would you still like to see?

The landscape has progressed meaningfully, with more women stepping into senior roles and a growing recognition of the value of inclusive leadership. That said, there’s still room for growth, particularly at executive and board level. There is a need for more deliberate succession planning that empowers women into leadership roles, along with supportive policies that recognise the realities of maternity, parenting, and the different stages of a woman’s career journey.

What advice would you give to young women who aspire to take on leadership roles in traditionally male-dominated fields?

Back yourself. Your perspective brings value, especially in a space like financial services where ethics, resilience, and adaptability are critical. Don’t wait to be invited to the table –prepare, show up, and make your voice heard.

Sue Blake, CFP® CA (SA), Head of the Tax team at Private Client Financial

What unique challenges have you faced as a woman in your field, and how have you navigated them?

I have observed that my communication style, which tends to be more emotionally expressive, can be interpreted differently compared to that of my male colleagues. While I believe this approach is not necessarily negative, as it allows for fostering stronger connections with clients and team members, it can be perceived as less valuable by others. I demonstrate my value by focusing on delivering a consistent, high level of service to clients – actively looking for opportunities to add value.

How have you seen the landscape for women in the financial industry evolve, and what changes would you still like to see?

Over time, I have observed a positive shift toward recognising and promoting women within the industry. The younger generation – growing up in an increasingly global and

dynamic world – seem especially receptive to women in leadership roles, which is encouraging. With new opportunities emerging, I think now more than ever is an exciting time to be in the industry.

What advice would you give to young women who aspire to take on leadership roles in traditionally male-dominated fields?

Let the quality of your work demonstrate your capability and potential. Consistent performance will distinguish you from others and in time lead to new opportunities. Prioritise clear, honest communication and maintain a long-term perspective. By staying focused on your own goals rather than comparing yourself to others, you will sustain the momentum necessary to achieve success.

Sarah Love, CFP® FPSA® TEP, Head of the Fiduciary team at Private Client Trust

What unique challenges have you faced as a woman in your field, and how have you navigated them?

Being respected as a subject matter specialist and learning that one needs to speak with confidence and certainty to be taken seriously. If you doubt yourself others will too. You don’t need to know everything, but you do need to be able to position your response in a manner that allows you to do the research without discrediting yourself.

How have you seen the landscape for women in the financial industry evolve, and what changes would you still like to see?

There are more women joining the industry in roles other than administration. These women are owning their space and showing that gender doesn’t determine worth. There is also a greater acceptance of women in these roles in the younger generations, as they have grown up in a society with greater exposure to diversity in general.

What advice would you give to young women who aspire to take on leadership roles in traditionally male-dominated fields?

Take every opportunity to learn, nothing is more valuable than your education. The more you learn, the more you discover nuances and depth within a topic and how much more there still is to uncover. Know your worth, back up your arguments with credible sources, then argue with confidence. This does not mean, however, that you are always right, but rather that you are open to new discoveries and credible alternative opinions.

Investing in inclusion: Women rewriting the rules of portfolio management and leadership

In an investment industry long shaped by tradition, where progress is often measured in performance metrics and decimal points, women continue to face challenges that hinder full representation and inclusion across roles, from asset management to advisor professions. These obstacles persist despite meaningful strides toward equity.

Yet, in spaces like Melville Douglas, the boutique investment management company for Standard Bank Group, a quiet but powerful shift is redefining what inclusion looks like – where leadership is rooted in empathy and teams are being strengthened by diversity of thought.

“Being the only woman in the room can be intimidating but it can also be powerful. It becomes a platform where you can offer fresh perspective and deliver value to the team,” says Natalie van Rooyen, Head of Diversified SA at Melville Douglas.

Natalie leads an allwomen team of portfolio managers who curate discretionary portfolios by weaving together best-in-class third-party investment strategies, through market insights and in-depth qualitative and quantitative research.

decision-making. Yet the barriers to getting more women to that table often begin early. New entrants to the field frequently lack access to mentorship and networks that support long-term career growth. Many still navigate corporate structures built around traditional leadership profiles, which can reinforce outdated perceptions of who belongs in finance.

Instead of relying on traditional hierarchies, Natalie says she has found growth through informal support networks that include trusted friends, peers, and former colleagues. “I like to refer to all these people as my personal board of directors. They’ve become sounding boards for tough decisions and brave conversations. It’s through these relational webs that professionals build sustainable leadership.”

“Real collaboration happens when every voice in the room is heard and valued”

Reflecting on her own journey, teammate and Portfolio Manager Christine Naidu says the decision to pursue investments was deeply personal. “I witnessed a family member struggle through retirement because of inadequate financial planning. That experience made me realise how critical it is to democratise access to investment tools,” she says.

Her path ignited a career committed to wealth creation. Christine leads with quiet conviction, mentoring colleagues and building a team culture rooted in curiosity, humility and collaboration. She sees performance not as individual accolades, but as collective achievement where “superior outcomes come from thoughtful debate and disciplined engagement”.

Associate Portfolio Manager Zinhle Gombera adds, “Real collaboration happens when every voice in the room is heard and valued. Diverse thinking isn’t a trend; it’s a source of resilience.” Her analogy is powerful: just as varied investment strategies strengthen portfolio performance, varied human experiences strengthen team decision-making.

Natalie echoes this belief: “Diversity fuels creativity. The most effective investment teams are the ones that bring different experiences and ways of thinking to the table.”

These different perspectives, ignited by personal experiences, bring immense value to

Progress in the financial sector still requires intentionality, particularly in recruitment and retention of women. Natalie has seen encouraging movement in how the industry approaches the recruitment and development of women, with more awareness, more targeted graduate programmes, and an increasing number of women entering the field. However, Zinhle notes, “Support for female professionals must go beyond tick-box exercises. Development should be authentic and long term.”

The Citywire Alpha Female Report 2024 showed that women face a higher turnover rate globally. Many exit not due to a lack of skill, but due to rigid structures that fail to accommodate evolving life stages. To advance employment equity meaningfully, the investment industry must rethink how talent is cultivated. Structured mentorship, transparent development pathways, and support systems that honour both performance and humanity are essential. Particularly during mid-career transitions, which often mark inflection points for women leaders navigating complexity and change.

“Creating workplaces that ensure appropriate maternity cover, offering flexible work arrangements, and building a culture that supports women through different life stages without penalising their career progression, is critical,” says Natalie. While each woman’s journey is distinct, their collective impact paints a powerful picture. Together, they’re reshaping what leadership, resilience, and sustainability mean in investments and not as abstract metrics, but as tangible, relational outcomes.

Diversity and inclusivity challenge established norms – not through bold proclamations, but through day-to-day choices. When varied voices have a seat at the table, investment professionals are empowered to lead with

empathy, share knowledge and cultivate inclusive spaces. And this philosophy isn’t confined to internal dynamics. It extends into client relationships, where care, connection, and cultural awareness are paramount. Zinhle recalls how investment conversations often evolve.

“You start by reviewing a portfolio and end up learning about someone’s grandchildren. That connection is part of the return,” she says.

For the women of Melville Douglas, inclusivity isn’t performative, it’s personal. Christine puts it simply, “I strive to understand the person behind the portfolio, who they are, what they value, what they’ve experienced. When clients feel seen and heard, trust naturally follows.”

In this Women’s Month, as the financial industry reflects on equality and progress, the women of Melville Douglas offer a compelling blueprint for powering change – not only in how portfolios are built, but in how people are seen, heard and valued in the process. Their success isn’t just in performance, it’s in purpose.

Natalie van Rooyen

Christine Naidu

Zinhle Gombera

What has been the most defining career moment, and how did it shape your leadership journey?

The most defining moment for me was the transition from customer success into product operations and, ultimately, joining Binance. I had already worked with other innovative fintech and cryptocurrency platforms, but it was at Binance, where the scale matched the ambition, that I truly found the platform to execute my vision, which was using crypto to create meaningful, inclusive financial access for millions. This shift centralised my purpose. It taught me that leadership is not just about operational excellence, but rather about building with empathy, understanding local needs, and delivering tools that empower real people to change their lives.

What unique challenges have you faced as a woman in a senior position, and how have you navigated them?

Overcoming imposter syndrome, especially in spaces where women are underrepresented and expectations are framed through a male lens. In crypto and tech, you often have to prove your credibility before you’re even heard. What’s helped me navigate this is confidence in my capability earned through hands-on experience and a deep understanding of the industry; and

Earning her seat at the table

Yande Nomvete, Operations Manager – South Africa, Binance

mentorship. At Binance, I’ve been fortunate to learn from a respected female leader who showed me there’s no single ‘right way’ to lead. That support reminded me that we, as women, bring a different but equally powerful perspective – and that deserves a seat at the table. I’m also proud that over 30% of leadership roles at Binance are held by women, reflecting the company’s commitment to building an inclusive culture.

How do you approach mentoring or supporting the next generation of women leaders in your organisation or industry?

I believe in creating visibility and access. That means showing up as a woman in leadership unapologetically and being open about the journey, the pivots, and the learnings. It also means making the time to engage with young women professionals who are looking to enter the space. Whether it’s through informal mentorship, participating in panels, or just offering advice at our Community Meetups, I see it as my responsibility to demystify the industry and show that there’s room for women at every level.

What advice would you give to young women who aspire to take on leadership roles?

Don’t wait until you feel 100% ready because growth happens when you take the leap despite

being uncertain. Be intentional about building your confidence, stay curious, and don’t underestimate the value of your lived experience. Additionally, understand that your voice and presence are enough. You don’t have to mimic what leadership ‘looks like’ to be effective.

How have you seen the landscape for women in the crypto industry evolve, and what changes would you still like to see?

The crypto space has come a long way. In South Africa alone, women make up 48% of Binance users, a testament to the growing participation of women in crypto and Web3. When I started, women in technical or operational leadership roles were extremely rare. Today, we’re seeing more women join the ecosystem, not just as users, but as builders, founders, and decision-makers. But there’s still progress to be made. We need to normalise female leadership in crypto, as part of the industry’s DNA. That means better pipelines for women in product and engineering, more funding for female-led ventures, and continued efforts to challenge the biases that keep women from advancing. Crypto is about decentralisation, about breaking down old systems. That promise means little if we don’t also decentralise who gets to lead.

South Africans continue to diversify their wealth beyond borders into developed markets. However, this in itself creates a myriad of other complexities, including an assessment of offshore jurisdictions, cross-border tax, and estate duty planning.

A leadership journey forged through courage and reinvention

Gudani Mukatuni, Chief Information Officer, Glacier by Sanlam

What has been the most defining moment in your career, and how did it shape your leadership journey?

A key turning point in my career was pivoting from working for one of the big four consulting firms as a manager to leading an IT department for one of the business units at one of South Africa’s major banks. Although it was daunting to leave a promising and rewarding consulting career path, I wanted more growth and exposure in financial services, which I’d been introduced to as a consultant. In the first year of joining the bank, the move seemed like a lateral shift, but I believed that short-term sacrifice would lead to long-term gains. My success in financial services was made possible by supportive leadership and managers, whose trust inspired me to excel. Building strong relationships with leaders and working diligently helped ensure that their confidence in me was well placed. From this experience, I learned that the magic happens when you stop clinging to what was and lean into what could be. When the path no longer serves you, rerouting isn’t weakness, it’s evolution. Ever since this bold move, I have never looked back, and I enjoy being one of the leaders within the financial services industry.

Another defining moment in my career was when I was in middle management and decided to complete an MBA degree. I was fortunate that the organisation I was working for at the time paid for my MBA tuition fees. I graduated with my MBA in 2017, and the MBA qualification enabled me to be more confident in my leadership role, enhanced my business savvy, as well as my overall business acumen.

What unique challenges have you faced as a woman in a senior position, and how have you navigated them?

Working in male-dominated industries can present a range of structural, cultural, and interpersonal challenges. Gender bias and stereotypes portraying women as less competent or less suited for leadership positions remain prevalent, particularly in technical sectors. Additionally, leadership roles tend to be disproportionately occupied by men, which may result in fewer role models, sponsors or advocates for women. Another common

challenge is imposter syndrome among women in senior positions and across all career levels, given our diverse backgrounds. However, through my upbringing, education, and always ensuring that I work hard towards achieving organisational goals, I have developed the skills and confidence to contribute effectively within professional teams. I participate equally in discussions and decision-making processes alongside male colleagues and regard all team members as peers, regardless of gender.

“My success in financial services was made possible by supportive leadership and managers, whose trust inspired me to excel”

How do you approach mentoring or supporting the next generation of women leaders in your organisation or industry?

I am passionate about mentorship and I currently mentor three women from different backgrounds and career levels. Personally, both formal and informal mentors have been instrumental throughout my career, sometimes even becoming advocates for me. An effective mentor is someone you respect and trust to have your best interests at heart. As a mentee, it’s important to be proactive, clarify your own goals, and be prepared to put in the work.

What advice would you give to young women who aspire to take on leadership roles in traditionally male-dominated fields such as finance?

Stepping into leadership in male-dominated fields takes grit, strategy, and a strong sense of self. Be willing to grow deep knowledge in your field and hone your craft, as credibility is your strongest armour.

Speak up clearly, confidently in meetings and decision-making spaces, even if you’re the only woman in the room. There is no stupid question; however, it is important to read the room and tailor your communication to different personalities and power dynamics.

Seek mentors and sponsors regardless of gender. Challenge imposter syndrome and know that you do belong, do not wait to feel ‘ready’, step up and learn as you go. Don’t shy away from ambitious targets, make them known and ask for support.

If your current environment doesn’t support your growth, pivot when needed. Career paths aren’t always linear. Sideways moves can build broader skills and can ultimately lead to a fulfilling career.

How have you seen the landscape for women in the financial industry evolve?

According to Forbes.com, women now hold about 30% of senior roles in financial services globally. Bringing this back to South Africa, in the past two years we have seen positive changes, including the appointment of Jeannette Marais as CEO of Momentum Group, and Mary Vilakazi as CEO of the Firstrand Group. These are some of the women I look up to and admire how they have broken the glass ceiling in the financial services industry. While these are important steps forward, hiring and promotion practices still favour traditional (often male) leadership traits, according to Private Banker International. Objective evaluation metrics and diverse panels are key. Women need more access to mentors who understand their unique challenges and sponsors who will advocate for them.

By Ann Sebastian Head of Equity, Terebinth Capital

Strengthening women in leadership to improve client experience

The investment management industry has gradually recognised the importance of female representation, with increasing efforts to promote diversity. While acknowledging this progress is essential, it is equally critical to understand that representation alone is not enough; it must translate into decision-making roles to have a meaningful impact on policies, strategies and practices within the industry.

Women make up 19% of portfolio manager roles in South Africa. When the scope of the analysis is widened to include support staff, who represent 79% of the total workforce, female presence in the asset management industry expands to 59%. Women are overrepresented in support staff positions and underrepresented in senior investment roles. This suggests that the industry has not fully leveraged this diversity.

Research consistently demonstrates that diverse teams drive performance improvement relative to their homogenous counterparts. When it comes to investment management, the stakes are particularly high, as clients rely on managers to provide informed decisions that

align with their goals, return and risk tolerances. A lack of female voices at the decision-making table can inadvertently result in a narrow understanding of client needs and investment opportunities.

Female clients approach investing differently than men, shaped by unique experiences, risk appetites, and financial goals. They often seek financial advisers who build trust and prioritise communication, transparency, and education. With women projected to control c.$30tn in global wealth by 2030, investment management firms must reflect this demographic at their decision-making levels.

Companies must create pathways for women to progress into leadership roles. This means setting up mentorship and sponsorship initiatives that connect junior female staff to experienced leaders. Such programmes can offer women essential guidance and advocacy to help them advance in their careers and address systemic challenges. Firms should emphasise increasing female representation on decision-making committees and boards. It is not enough for women to simply fill positions; they also need the power to influence business direction and initiatives.

Fostering an inclusive culture is vital. Encouraging

open communication and valuing diverse opinions can enhance collaboration, resulting in innovative solutions. Additionally, businesses should commit themselves to transparency and accountability. By publicly sharing gender diversity data and setting specific targets, they can evaluate their progress and take responsibility. This transparency not only shows a genuine desire for change but also enhances the organisation’s standing with clients and investors who care about ethical and inclusive practices.

Translating female representation into decisionmaking roles is vital to unlocking the full potential of female talent and achieving material change in the investment management industry. At Terebinth Capital, we have since the start incorporated this into our vision and mission. We pride ourselves on inclusion of female participation and leadership across all spheres of the business. In addition, we support others in their bid to contribute by way of various industry programmes, including the ASISA Fezeka Programme and the CFA South Africa Day of the Girl Job Shadowing initiative. The time for action is now, as the future of investment management depends on diverse perspectives, driving innovative decision-making and sustainable growth.

By Reo Botes Managing Executive at Essential Employee Benefits

GGen Z is rewriting the rules of work – and benefits need to catch up

en Z is entering the workforce in numbers too large to ignore. By 2030, they’ll make up nearly 40% of South Africa’s working population. They are young, ambitious, techsavvy, and largely uninsured.

In a country where private medical aid remains unaffordable for many, a worrying number of Gen Z employees are going without any form of health cover. This isn’t due to negligence. It’s economics. The average Gen Z worker, either fresh out of university or early in their career, simply doesn’t earn enough to justify paying thousands of rands a month for traditional medical aid schemes. As a result, many are walking a tightrope without a safety net.

The high cost of poor cover

apps, wellness dashboards, AIdriven health assessments, and proactive outreach go a long way in building trust and engagement. Gen Z doesn’t want to call a helpline and wait on hold. They want intuitive platforms that put their health in their hands.

The implications for employers are bigger than they may realise. A generation under financial pressure and health-related stress is not a productive, engaged, or loyal workforce. Gen Z’s top stressors include money (58%), career anxiety (54%), and family responsibilities (45%), making mental and physical wellness not just a nice-to-have but a survival priority. Yet, without access to affordable health insurance through their employers, too many are forced to choose between a GP visit and groceries.

This is where businesses need to step in; not only from a moral standpoint but from a practical one. Offering tailored, affordable health insurance benefits isn’t just the right thing to do; it’s a strategic move to attract and retain top talent in an increasingly competitive market.

One-size-fits-all is a thing of the past

But the days of one-size-fits-all medical schemes are over. Gen Z is rewriting the rulebook. They want healthcare benefits that are flexible, accessible, and aligned with their lifestyle. They want access to mental health support, telemedicine, and preventative care. And most importantly, they want to be able to afford it.

This generation grew up with personalised digital experiences. From curated music

playlists to AI-driven fitness coaching, Gen Z expects the same level of customisation in every aspect of life, including healthcare. It’s why, globally, 66% use wearable devices and 55% are already engaging with telemedicine platforms. Therefore, healthcare must be digital, personalised and easy to access.

The power of tailored benefits

That’s where progressive employers can make a difference, by partnering with expert health insurance providers who understand that benefits need to reflect the DNA of the organisation. These providers don’t just slap on a standard medical aid offering; they assess the age, income brackets, life stages, and wellbeing priorities of the workforce to create truly tailored solutions.

For a company with a young, predominantly Gen Z team, that might look like affordable hospital plans, basic cover with optional add-ons, or plans that prioritise mental health and lifestyle disease management over expensive in-hospital procedures. And let’s be honest: at this life stage, Gen Z isn’t thinking about knee replacements or chronic disease cover. They want the peace of mind of knowing they can see a doctor when they need to, access therapy without paying out of pocket, and get affordable medication without standing in long queues at public clinics.

Delivery is just as important as the benefit

And it’s not just about the healthcare itself. The way it’s delivered matters. Real-time access to benefits information via mobile

There’s also the matter of mental health; a silent crisis for many young professionals. Burnout, anxiety, and depression are rising, particularly among entry-level workers facing unstable economic conditions and sky-high living costs. Providing access to mental health services through Employee Assistance Programmes, therapy benefits, or even just mental health days integrated into leave policies can have a huge impact. These are necessities in a generation that deeply values holistic wellbeing.

The future belongs to businesses that care

The bottom line is this: if businesses want to attract and retain the next generation of talent, they must rethink how they structure their benefits, starting with health insurance. And they can’t do it alone. Partnering with health insurance providers who specialise in designing benefits aligned to an organisation’s workforce makeup is essential. These partners can unpack the demographics, job roles, and income levels of the company and build flexible solutions that speak to each group, whether it’s entrylevel Gen Zs, mid-career Millennials, or preretirement Gen Xers.

Ultimately, businesses that invest in benefits that matter – not just benefits that look good on paper – will gain the edge. In a world where rising living costs and health risks are constant threats, providing affordable, flexible healthcare isn’t a perk; it’s a responsibility. It’s also the smartest way to futureproof your workforce. And companies that invest in personalised, accessible healthcare will earn the trust – and longterm commitment – of the workforce that’s shaping our future.

Why group gap cover is a win for employers and employees

Rising healthcare costs are placing increasing pressure on South African employees, even those with medical aid. Unexpected medical expense shortfalls for hospital stays, surgeries, or specialist care can leave individuals facing bills in the tens of thousands – leading to financial stress that affects their health, morale and productivity in the workplace.

Bridging the gap between cover and care

Medical aids often don’t cover the full cost of treatment in private healthcare. The result?

Employees are left covering the difference themselves, sometimes with serious financial consequences. Many delay treatment, endure chronic pain, or turn to debt to fund care – all of which take a toll on their performance at work.

Group gap cover offers an effective, affordable solution. It closes the gap between what medical schemes pay and what private healthcare providers charge, covering shortfalls, co-payments, sub-limits, and even extending to extras like trauma counselling or

anxiety of high out-of-pocket expenses. This improves recovery time and job performance.

A strategic benefit for forward-thinking brokers

For brokers, group gap cover is a powerful tool to help employers enhance their employee wellness strategies. It goes beyond compliance, providing real value in a competitive market.

But for maximum impact, gap cover needs to be aligned with the existing medical aid options within an organisation. By tailoring solutions to the workforce’s specific needs – whether that’s by life stage, income level or healthcare usage – brokers can deliver smart, relevant benefits that boost their and client satisfaction.

Meeting real needs in a tough economic climate

Medical inflation is rising faster than general inflation, placing further strain on both employers and employees. Many companies have been forced to downgrade their medical aid contributions, leaving workers more exposed to risk. Group gap cover offers

protection without the expense of upgrading medical aid plans – many of which still don’t cover all costs. It’s also tax-efficient and simple to administer via payroll.

Supporting recruitment, retention and reputation

In a highly competitive job market, offering group gap cover as part of a total rewards package sends a strong message: this company values its people. In industries where employee churn is high, the impact of showing genuine care can be significant.

Today’s candidates are looking for more than a salary. They want security, support and a sense of being looked after. Providing financial protection during medical emergencies builds loyalty, fosters trust, and strengthens long-term employee engagement.

More than a benefit – a business advantage

Group gap cover delivers where it matters most –supporting health, financial wellbeing and peace of mind. At the same time, it helps businesses maintain productivity, reduce absenteeism, and enhance their reputation as caring employers.

As economic pressures mount, solutions like group gap cover stand out for their practicality, affordability and impact. It’s not just a tick-box benefit – it’s a smart investment in your people and your business.

Meet the Liberty Corporate Benefits team

As mentioned in our cover story, Liberty Corporate Benefits has combined its internal teams, merging investment, annuity products and operational capabilities into a single integrated unit of approximately 40 experienced professionals. This ensures end-to-end delivery, from product and proposition design to risk management and daily asset-liability matching and other investment operation functions. Here are the key players.

Louis Theron Head of Investment Liberty Corporate Benefits

Theron is a highly accomplished investment specialist with over 18 years of experience in institutional investments. Known for his expertise in strategic execution, he has successfully led the launch and management of Liberty’s institutional investment proposition and framework. His leadership style focuses on coaching individuals to find their own strength and confidence, making him a key driver of organisational success.

Kgotso Thipa

Head: Investment Distribution and Servicing

Thipa began his financial services career in 2011 in asset consulting. Working in this field for over a decade, he developed extensive knowledge of the investment and retirement industries, the regulatory environment, and the specific needs of funds and their members. In 2023, he joined Liberty Corporate Benefits to work within a team developing distinctive solutions for this market. He distributes Liberty Corporate Benefits Investment offerings across both pre- and post-retirement solutions, where he can realise his passion for empowering trustees and members to improve their financial outcomes.

Avikar Somaroo Head of Investment Proposition

Somaroo is a qualified actuary who has close to 15 years’ experience in the investment field. He has worked with both clients and products, understanding investors’ needs and how best to meet them. He has a deep interest in behavioural finance and the role that it can play in improving investment outcomes. At Liberty Corporate Benefits, he is responsible for getting the most out of members’ retirement savings through developing low-cost solutions that enhance returns and reduce risks.

Shari’ah investing: What

you need to know and why it matters

Shari’ah investing refers to an investment approach that complies with Islamic law (Shari’ah), derived from the Qur’an and Hadith. It is guided by ethical and religious principles that influence how money is earned, invested, and spent.

The core principles

Avoidance of interest (Riba)

Earning or paying interest is prohibited. This excludes conventional interest-bearing instruments like bonds or bank deposits.

Prohibition of haram activities

Investments cannot be made in companies involved in: Alcohol

Excessive speculation or uncertainty is discouraged. Investments must be based on real economic activity and transparency.

Profit and loss sharing

Shari’ah-compliant investments often involve equity participation, where investors share in the profits and losses of the venture.

Asset-backed investments

Investments must involve tangible, productive assets. Derivatives and complex financial instruments are typically excluded.

Shari’ah-compliant investment instruments

• Equity funds: Invest in screened companies that comply with Shari’ah principles

Sukuk (Islamic bonds): Asset-backed securities that offer returns through profit-sharing, not interest

• Property funds and REITs: Acceptable if they avoid impermissible activities

• Islamic unit trusts and portfolios: Actively managed by Shari’ah boards to ensure compliance.

“Advisers with knowledge of Shari’ah investing can broaden their client base”

Southern Africa’s first Shari’ah-compliant overdraft

In June this year, Standard Bank launched the first-ever Shari’ah-compliant overdraft facility in Southern Africa, marking a transformative milestone for Islamic Finance on the continent. Designed to empower business owners with more Shari’ahcompliant solutions, the product adds to Standard Bank’s solutions to meet the unique needs of Africa’s growing demand for Islamic Finance.

Structured under the Shari’ah principle of Wakaalah, the Shari’ah Overdraft facility is a non-interest-based alternative that provides businesses with instant access to short-term funding. Linked to the Shari’ah Business Current Account, the new product will allow clients to drawdown up to a preapproved limit.

“This is not just a product launch, it’s a response to a critical gap in Africa’s Islamic Finance ecosystem,” said Ameen Hassen, Head of Shari’ah Banking at Standard Bank. “For too long, businesses that required Shari’ah-compliant financing options lacked fluidity of a working capital solution that an overdraft brings. This overdraft facility

empowers entrepreneurs to manage cash flow fluctuations without compromising their values and need for Shari’ah compliance.”

With Sub-Saharan Africa home to 18% of the global Muslim population but accounting for just 1% of worldwide Islamic Finance assets, Standard Bank’s innovation arrives as the region seeks scalable, Shari’ah-compliant solutions. The overdraft facility will directly address working capital challenges faced by businesses.

Key benefits of the new product include:

Competitive market-related pricing

Direct linkage to the Shari’ah Business Current Account for streamlined operations • Certified compliance: The facility is certified by Standard Bank’s Shari’ah Advisory Committee.

Not only for Muslims

While Shari’ah Banking adheres to Islamic principles like Wakaalah bi al-Istithmar (agency-based investment), and the prohibition of interest (riba), Hassen said the bank’s offering transcends religious

Why financial advisers should understand Shari’ah investing

South Africa has a significant and growing Muslim population who seek ethical, faithaligned investment solutions. Advisers with knowledge of Shari’ah investing can broaden their client base by offering more inclusive financial planning. Understanding Shari’ahcompliant finance can support advisers in offering ethically screened, socially responsible options, appealing to both faith-based and values-driven investors.

Competence in this area boosts adviser credibility and helps ensure compliance with FAIS Treating Customers Fairly (TCF) principles by aligning advice with client beliefs. Several South African financial institutions now offer Shari’ah-compliant investment products. Advisers who understand the mechanics can guide clients effectively through these offerings.

A growing part of the ecosystem

Shari’ah investing is more than a niche offering; it’s a growing part of South Africa’s financial ecosystem. For financial advisers, understanding its principles and implications is essential to delivering holistic, ethical and client-centric advice. In a country as diverse as South Africa, cultural and religious competence isn’t just good practice – it’s good business.

boundaries, with approximately 35% of Standard Bank’s South African Shari’ah clients identifying as non-Muslim. “This isn’t just for Muslims, it’s for anyone seeking transparent, non-interest, asset-based or backed financial solutions,” said Hassen.

“This is not just a product launch, it’s a response to a critical gap in Africa’s Islamic Finance ecosystem"

The launch builds on Standard Bank’s legacy of Islamic Finance innovation, including the world’s first Shari’ah-compliant Diners Club product and South Africa’s inaugural Shari’ah tax-efficient endowment.

“Africa’s economic future hinges on inclusive, innovative finance,” said Hassen. “With this product, we’re not just serving clients, we’re innovating, industrialising and advancing a system of finance rooted in tradition and shared prosperity.”

An untapped growth opportunity in South Africa

Shari’ah-compliant investing is gaining serious traction in South Africa, both among high-net-worth individuals, family offices and institutional investors. With a market opportunity estimated at R90bn, the space is expanding rapidly, yet remains underserved. One of the newer players answering that call is Wealthvest Investment Management, a Cape Town-based asset manager co-founded by Zaid Paruk (pictured).

“We launched Wealthvest because we saw a clear gap,” says Paruk. “There are only a handful of asset managers meaningfully engaged in Shari’ah investing, but the demand is growing, especially from family offices and a new generation of investors seeking ethically aligned financial products.”

Since its launch in February 2024, Wealthvest has attracted both retail and institutional clients, managing an estimated R350m in assets by mid-2025. Paruk and his team have spent the last few months meeting with more than 50 families and offices across the country, from the Western Cape, KwaZulu-Natal and Gauteng to Mpumalanga, many of whom are actively looking for Shari’ah-compliant investment solutions with solid track records and sound governance.

“One local Shari’ah fund ranked among the top 10 funds yearto-date, thanks in part to market volatility"

At its core, Shari’ah investing is values-based. It excludes sectors such as alcohol, gambling, arms and interest-based financial services, and filters companies through both quantitative and qualitative screens to ensure compliance. But this is no niche offering – it’s an investment strategy built on principles of low leverage, ethical business practices and real economic activity. “There’s a strong overlap with ESG and impact investing,” notes Paruk. “We’re essentially investing for both performance and purpose.”

While global access to Shari’ah-compliant investments is steadily improving, local investors still face some structural constraints. “You do have global Shari’ah index funds,” explains Paruk. “Big players like HSBC and BlackRock all offer Shari’ah-compliant index funds, similar to ESG index funds. Index providers like FTSE Russell and Yasaar International also provide data for Shari’ahcompliant shares.”

However, in the South African context, options are far more limited. “Locally, we have the FTSE/JSE Shari’ah Top 40 index,

but it’s very concentrated, predominantly in gold and mining stocks,” Paruk says. “This creates a challenge from a diversification and risk management perspective. Therefore, we launched the Wealthvest Shari'ah Equity Fund, which provides an investor with an index agnostic diversified portfolio of local and global equities.”

A further complication is that Shari’ah compliance isn’t static. “These companies aren’t trying to be Shari’ah-compliant – they’re just running their businesses,” he says. As a result, market dynamics can affect whether a stock qualifies. For example, Sasol’s market cap decline at one point led to it falling out of compliance, triggering a review.

Shari’ah boards vary in how they respond. Some may require immediate divestment when a company drops out of compliance. Others allow a grace period, typically six to 12 months, to see if the company can restore its Shari’ah credentials. “But after 12 months, if the company is still non-compliant, the fund manager has to sell out,” Paruk confirms.

Competitive returns

Despite these constraints, Shari’ah-compliant funds can offer strong performance. “You’re still getting access to quality, conservative companies, often at attractive prices,” says Paruk. He notes that one local Shari’ah equity fund ranked among the top 10 funds year-todate, thanks in part to market volatility, and strong commodity prices.

“In times of crisis, companies with high debt exposure tend to fall harder. Shari’ah-compliant funds, which avoid such companies, can hold up better,” he explains. The recent strength in gold – up over 27% – also benefited Shari’ah funds, which are typically overweight in resources due to the exclusion of financials like banks and insurers.

Beyond listed equity by building holistic solutions

While listed equity forms the backbone of most Shari’ah-compliant investment portfolios, Wealthvest combines its core listed equity capabilities with a wider range of family office services aimed at high-net-worth individuals and large families.

“We try to provide more than just a vanilla structure,” says Paruk. “For clients with more complex needs, we offer access to unlisted assets through partnerships with private equity firms. These opportunities, which may otherwise be difficult to source, span various industries and allow for a cross-pollination of deal flow across our client base.”

This tailored approach includes services such as global structuring, tax and accounting, M&A advisory, and payment solutions, supporting clients in a much more integrated way.

For Wealthvest, this model fosters deeper relationships and longer-term client retention. “A client who works with us across multiple layers of their financial life is far less likely to move their listed equity elsewhere,” notes Paruk.

This comprehensive model also extends to Shari’ah-compliant fixed income instruments like sukuks. “Sukuks are the equivalent of a conventional bond in the Shari’ah world,” Paruk explains. “But instead of being backed by a company’s balance sheet, they are backed by tangible assets like roads, dams or infrastructure projects.” This asset-backing makes sukuks particularly attractive to Shari’ah investors, offering predictable income while complying with the prohibition against interest (riba).

Digital assets and the Shari’ah debate

As the financial landscape evolves, digital assets such as cryptocurrencies are also drawing increasing attention from Muslim investors. However, their compliance with Shari’ah principles remains under debate.

“There’s a strong scholarly discussion around whether crypto is halal,” says Paruk. “The fiat currency system itself isn’t inherently Shari’ahcompliant, but we operate within it out of necessity, people need to buy bread and milk. Crypto is going through a similar process of scholarly interpretation.”

While Wealthvest doesn’t manage crypto funds, Paruk confirms there’s growing interest from the Shari’ah investment community.

“We’re definitely seeing demand from younger, tech-savvy investors who are curious about how digital assets can fit within a Shari’ah framework,” he says.

Finding broader appeal

Importantly, Shari’ah funds are attracting investors beyond the Muslim community.

“There’s a growing group of values-based investors, not necessarily of the Islamic faith, who want to avoid sectors like alcohol, gambling and arms,” Paruk says. In an era of global conflict and heightened ethical scrutiny, the appeal of ‘clean’ portfolios is spreading.

This ethical alignment reflects a broader global trend: investors, especially younger ones, are paying closer attention to the social impact of their capital. “We’re seeing a heightened focus on industries that are doing good. People are taking a closer look at the social impact of their investments, not just from a religious standpoint, but from a moral and reputational one as well. Investors are increasingly interrogating their portfolios to make sure they’re not indirectly supporting social ills.”

If you subscribe to our MoneyMarketing newsletter you will receive a special discount off a News24 or Netwerk24 subscription. Scan the QR code to subscribe today!

Fresh look, same powerful financial insights.