DAIRY MARKET REPORT VOLUME 28 | ISSUE 8

8/25/2025

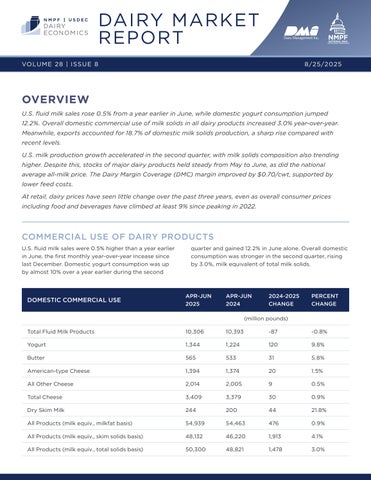

OVERVIEW U.S. fluid milk sales rose 0.5% from a year earlier in June, while domestic yogurt consumption jumped 12.2%. Overall domestic commercial use of milk solids in all dairy products increased 3.0% year-over-year. Meanwhile, exports accounted for 18.7% of domestic milk solids production, a sharp rise compared with recent levels. U.S. milk production growth accelerated in the second quarter, with milk solids composition also trending higher. Despite this, stocks of major dairy products held steady from May to June, as did the national average all-milk price. The Dairy Margin Coverage (DMC) margin improved by $0.70/cwt, supported by lower feed costs. At retail, dairy prices have seen little change over the past three years, even as overall consumer prices including food and beverages have climbed at least 9% since peaking in 2022.

COMMERCIAL USE OF DAIRY PRODUCTS U.S. fluid milk sales were 0.5% higher than a year earlier in June, the first monthly year-over-year incease since last December. Domestic yogurt consumption was up by almost 10% over a year earlier during the second

DOMESTIC COMMERCIAL USE

quarter and gained 12.2% in June alone. Overall domestic consumption was stronger in the second quarter, rising by 3.0%, milk equivalent of total milk solids.

APR-JUN 2025

APR-JUN 2024

2024-2025 CHANGE

PERCENT CHANGE

(million pounds) Total Fluid Milk Products

10,306

10,393

-87

-0.8%

Yogurt

1,344

1,224

120

9.8%

Butter

565

533

31

5.8%

American-type Cheese

1,394

1,374

20

1.5%

All Other Cheese

2,014

2,005

9

0.5%

Total Cheese

3,409

3,379

30

0.9%

Dry Skim Milk

244

200

44

21.8%

All Products (milk equiv., milkfat basis)

54,939

54,463

476

0.9%

All Products (milk equiv., skim solids basis)

48,132

46,220

1,913

4.1%

All Products (milk equiv., total solids basis)

50,300

48,821

1,478

3.0%