DAIRY MARKET REPORT VOLUME 28 | ISSUE 9

9/ 18/2025

OVERVIEW Overall domestic commercial use of milk in all dairy products increased by 2.2% year-over-year during the May-July period. Exports also showed strong growth. U.S. milk production grew by 3% during this period, while total milk solids production increased by 3.9%, as the average solids composition of producer milk continues to increase. Lower average milk prices in July from a month earlier were mostly offset by lower feed costs, resulting in a $0.16/cwt lower DMC margin of $10.94/cwt. Retail price inflation ticked up in August as overall consumer prices rose by 2.9% from a year earlier. Dairy continued to show its inflation-fighting bonafides, with its average retail prices increasing by 1.3% from a year earlier versus 3.1% for all food and beverages.

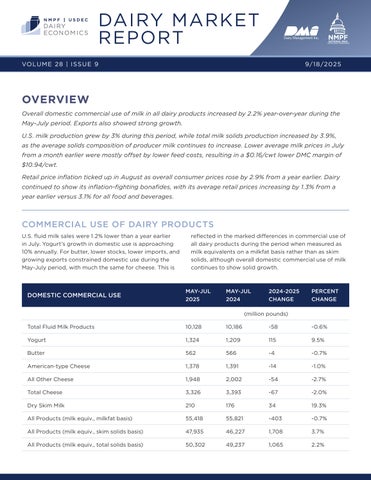

COMMERCIAL USE OF DAIRY PRODUCTS U.S. fluid milk sales were 1.2% lower than a year earlier in July. Yogurt’s growth in domestic use is approaching 10% annually. For butter, lower stocks, lower imports, and growing exports constrained domestic use during the May-July period, with much the same for cheese. This is

DOMESTIC COMMERCIAL USE

reflected in the marked differences in commercial use of all dairy products during the period when measured as milk equivalents on a milkfat basis rather than as skim solids, although overall domestic commercial use of milk continues to show solid growth.

MAY-JUL 2025

MAY-JUL 2024

2024-2025 CHANGE

PERCENT CHANGE

(million pounds) Total Fluid Milk Products

10,128

10,186

-58

-0.6%

Yogurt

1,324

1,209

115

9.5%

Butter

562

566

-4

-0.7%

American-type Cheese

1,378

1,391

-14

-1.0%

All Other Cheese

1,948

2,002

-54

-2.7%

Total Cheese

3,326

3,393

-67

-2.0%

Dry Skim Milk

210

176

34

19.3%

All Products (milk equiv., milkfat basis)

55,418

55,821

-403

-0.7%

All Products (milk equiv., skim solids basis)

47,935

46,227

1,708

3.7%

All Products (milk equiv., total solids basis)

50,302

49,237

1,065

2.2%