FREESTATE FREESTATE S P R I N G 2 0 2 4 MarylandIntroduces PrivateLetterRulings A Brief Review of the Buy Maryland Cybersecurity Tax Credit: Enhancing Statewide Digital Security ED Corner: 2024 Legislative Priorities and the Year Ahead MSATP’s 2024 Legislative Report

SPRING 2024

Ellen

Hannah

Jonathan

Ann

Matthew

Michael

Michael

Nicole

President 1st Vice President 2nd Vice President Secretary Treasurer Delegate Delegate Delegate Delegate Delegate Past President Board of Trustees Delegate Executive Director Donya Oneto, CPA

Silverstein, CPA

Coyle, EA

Rivlin, CPA

F. Elliott, EA

T Eddleman, EA

McIlhargey, CPA

L. Kohler, EA

Moore, EA

Coggins, CPA

J. Smith, CPA Christine Giovetti, CPA Gigi Hawkins CONTENTS 2 Executive Director's Corner 3 A Brief Review of the Buy Maryland Cybersecurity Tax Credit: Enhancing Statewide Digital Security 6 A Taste of Pro Bono Recap 7 Persistent Inequities in the Federal Income Tax System 9 Move The Needle Forward for Your Clients 10 Maryland Introduces Private Letter Rulings 12 Navigating My Accounting Journey: Top Courses That Shaped My Experience 13 MSATP’s 2024 Legislative Report 19 The Stop Scam Tax Preparers Act: Safeguarding Maryland Taxpayers

Sean

Barbara

THE FREESTATE | 1 2023-2024 Board of Directors

Executive Director's Corner

Never doubt that a small group of thoughtful, committed citizens can change the world; indeed, it's the only thing that ever has.

- Margaret Mead

As we reflect on the recently concluded legislative session, I want to highlight the impactful advocacy efforts that define our organization. Our dedication to representing and advancing the interests of our profession in Maryland was unwavering, and our activities during this period underscore the critical importance of our collective voice

Our proactive stance in supporting or opposing legislation directly affected our industry and, by extension, the communities we serve For instance, our support for bills that sought to enhance the professional environment for tax preparers and accountants demonstrated our commitment to safeguarding the integrity of our field and fostering an atmosphere of continuous improvement and ethical practice

This past year, we, as a united front, tackled a range of issues from tax modifications that benefited both individuals and businesses, to regulatory changes that ensured our profession remains on the cutting edge of accountability and service. Our significant strides through written testimonies, in-person advocacy, and relentless follow-up culminated in the passage of several bills we supported, a testament to our collective diligence and the respect our society commands in legislative circles.

Why did we fight? We fought because the stakes were high our professional standards, economic well-being, and the trust of those we serve depended on it Each bill we supported or opposed was chosen based on its potential to enhance our members’ professional lives and ensure that Maryland remains a great state for accounting and tax professionals to thrive

As part of our ongoing commitment to this cause, we urge each of you to consider contributing to the Political Action Committee (PAC) Your individual contributions are the fuel that powers our advocacy efforts and enhances our ability to influence legislation that affects our profession Together, as a united community of dedicated professionals, we can continue to make significant impacts.

Thank you for your continued support and commitment to excellence. Let's keep striving together for a brighter future for all Maryland accounting and tax professionals.

Warm regards,

Gigi Hawkins

THE FREESTATE | 2

A BRIEF REVIEW OF THE BUY MARYLAND CYBERSECURITY

TAX CREDIT: ENHANCING STATEWIDE DIGITAL SECURITY

By Jacob Linn, Strategic Tax Planning

In 2023 there were approximately 3200 cases of compromised data across the United States. Hundreds of millions of individuals were affected by these data compromises. In recent months the United States has continued to see businesses targeted for the private information they hold. Following the Bank of America data breach earlier this February, where sensitive information on countless customers was compromised due to vulnerabilities at a third-party provider, the importance of robust cybersecurity has never been clearer.

Maryland’s response to these threats includes a strategic, yet underutilized tool: the Buy Maryland Cybersecurity Tax Credit. Designed to incentivize local businesses to enhance their cybersecurity measures, this tax credit not only aims to safeguard Maryland’s digital infrastructure but also foster a resilient economic environment in an increasingly interconnected world.

In addition to the Buy Maryland Cybersecurity Tax Credit, Maryland's strategic approach to cybersecurity includes the Maryland Cybersecurity Investment Incentive Tax Credit, a vital component designed to attract and retain new cybersecurity businesses within the state. This comprehensive strategy underscores Maryland’s commitment to creating a robust digital security infrastructure by supporting cybersecurity ventures through significant financial incentives.

The Investment Incentive Tax Credit specifically targets cybersecurity firms and investors, encouraging them to establish roots in Maryland. This, coupled with the Buy Maryland Cybersecurity Tax Credit, which focuses on enhancing the cybersecurity measures of existing local businesses, forms a comprehensive support system for both the economic and digital security of the state.

The collaborative impact between these tax credits plays a critical role in Maryland’s cybersecurity strategy, highlighting the state's proactive steps to support and secure its digital landscape against the complexities of modern cyber threats. Engaging with these incentives allows businesses to leverage state support to significantly enhance their cybersecurity measures, making them less susceptible to cyber-attacks and contributing to a safer, more secure digital environment in Maryland.

The Buy Maryland Cybersecurity Tax Credit was enacted in 2018 and provides a tax credit against the State income tax for qualified buyers who purchase cybersecurity technology or services from a qualified seller. When making these purchases a qualified buyer may claim an income tax credit equal to 50% of the costs of purchasing the cybersecurity technology or service, up to $50,000 per qualified buyer.

The Maryland Department of Commerce maintains a list of qualified sellers in the state. Currently, there are 25 businesses in Maryland designated as a qualified seller on the list. A qualified seller is defined as a for-profit business that (1) is engaged primarily in the development of innovative and proprietary cybersecurity technology or the provision of cybersecurity service; (2) has its headquarters and base of operations in the State; (3) has less than $5.0 million in annual revenue; (4) is a minority-owned, woman-owned, veteranowned, or service-disabled-veteran-owned business or located in a historically underutilized business zone designated by the U.S. Small Business Administration; (5) owns or has properly licensed any proprietary technology or provide cybersecurity services; and (6) is in good standing. A qualified buyer is any entity that has less than 50 employees in the State and is required to file a state income tax return.

To claim the credit, Maryland businesses must fill out an application with the Maryland Department of Commerce which administers the funds. The Secretary of Commerce is authorized to approve a total of $4.0 million annually in Buy Maryland Cybersecurity tax credits. However, the Secretary must award 25% of the total tax credits awarded each year to qualified buyers who purchase cybersecurity services.

In 2018 when the Buy Maryland Cybersecurity Tax Credit was passed, Maryland was already a state at the forefront of the cybersecurity industry. With over 500 cybersecurity organizations located in Maryland, many are located around large federal organizations, including the National Security Agency and Fort Meade. Cybersecurity workers in Maryland are highly specialized and sought after with many having experience working at Maryland-based national security organizations such as the Defense Information Systems Agency, the National Institute of Standards and Technology, Intelligence Advanced Research Projects Activity, U.S. Cyber Command, and the Department of Defense Cyber Crime Center.

THE FREESTATE | 4

The cybersecurity industry in Maryland has always been a significant economic driver for the State. However, despite the critical nature of cybersecurity and the state’s leading role in the industry, the Buy Maryland Cyber Security Tax Credit remains markedly underutilized. An evaluation completed by the Maryland Department of Legislative Services shows that less than 0.1% of small businesses are taking advantage of the program, suggesting a gap between the program’s offerings and its reach or appeal to eligible businesses. Theories for the underutilization include a lack of necessity felt by small businesses, the potential high cost of cybersecurity solutions even after the credit, limited awareness of the credit, and its non-refundable nature which offers no benefit for businesses without tax liability

The Department of Legislative Services report shows that of the 25 qualified cybersecurity sellers in the state, many of these sellers are located in central Maryland, with 60% of the sellers being located in Anne Arundel, Howard, or Montgomery counties. The Department of Commerce has certified only 86 businesses since 2018 for a total of $2.1 million in credits through June of 2023. On average, each year, there are approximately 34 buyers awarded the credit for buying cybersecurity technologies and services.

Tax professionals in Maryland are uniquely positioned to bridge this gap. As a tax professional, you hold the key to informing and guiding local businesses through the landscape of available tax credits, turning what is an underutilized asset into a formidable shield against cyber threats. By integrating the Buy Maryland Cybersecurity Tax Credit into the financial strategies of your clients, you can play a pivotal role in not just reducing their state income tax burden, but also in elevating the state's overall cybersecurity posture.

The time is now for tax professionals to step forward and lead the charge in fostering a more secure and economically resilient Maryland. The Buy Maryland Cybersecurity Tax Credit is more than a fiscal incentive; it's a tool for fortifying businesses against the digital threats of tomorrow.

A TASTE OF PRO BONO

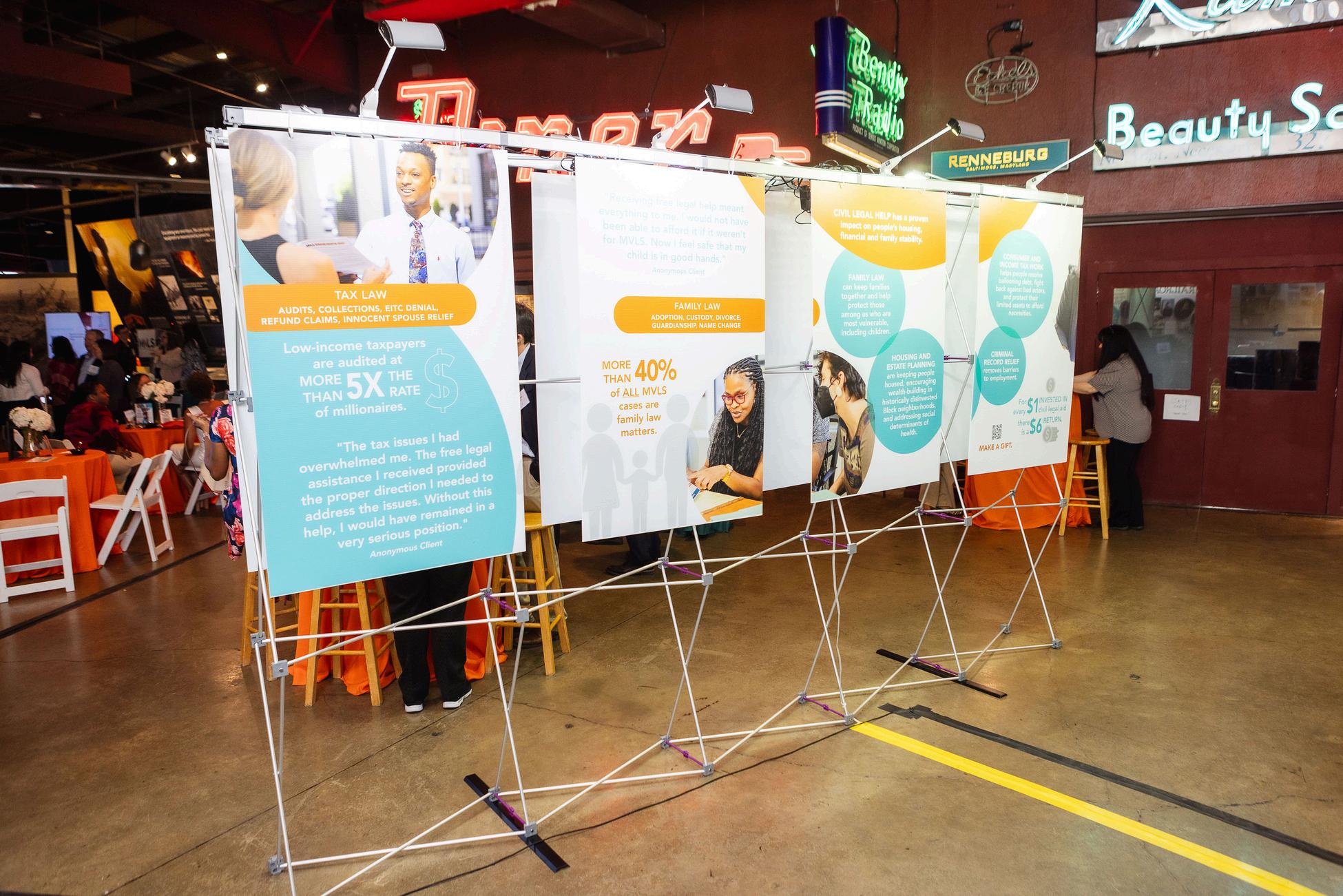

On April 16, Maryland Volunteer Lawyers Service (MVLS) was thrilled to be joined by 260 of the area's top attorneys, accounting and tax professionals, and other community leaders for their annual A Taste for Pro Bono benefit at the Baltimore Museum of Industry

Sponsors of the event, including the Maryland Society of Accounting and Tax Professionals, as well as generous individual donors collectively raised over $160,000 to provide free legal help to Marylanders in need The state's largest provider of pro bono services, MVLS connects clients with pro bono volunteers who can resolve their case. By providing mentoring, free training, and a plethora of other resources, MVLS makes it easy to do pro bono. In turn, MVLS volunteers make a profound impact on the lives of clients, resolving issues related to family law, housing instability, consumer issues, tax controversy, criminal record expungement, and estate planning and administration.

To see more photos of this year's event, and to learn more about MVLS, you can visit www mvlslaw org/taste

THE FREESTATE | 6

PERSISTENT INEQUITIES IN THE FEDERAL INCOME TAX SYSTEM

John Hardt, LITC Director, Maryland Volunteer Lawyers Service

The policymakers who create and administer the U.S. Tax system have almost always championed “fairness” as one of the most important guiding principles in how the system should be designed. At the same time, “unfairness” has perpetually been one of the most common criticisms of the U.S. Tax System as a whole.

When some commenters reference “fairness,” they refer to only equal treatment; that the Tax Code and the IRS apply the same rules to everyone with an even hand. On a basic level, the Tax Code is mostly fair by this definition. For example, there is no mention of race in the text of the U.S. Tax Code, nor does the IRS even collect information on taxpayer’s race. Two similarly situated taxpayers with the same income would, in theory, pay the same income tax. But it has become increasingly clear that the application of these facially neutral ruleset is not producing equitable results.

It is widely recognized, even within the IRS, that low-income taxpayers have more difficulty navigating the tax system than other taxpayers. As part of the IRS Restructuring and Reform Act of 1998, Congress funded the IRS’ creation of the Low-Income Taxpayer Clinic program, a grant program which led to the creation of more than a hundred independently-run clinics throughout the nation, with the mission of providing free tax and legal assistance to those in need of representation but without the ability to afford it. At our clinic in Baltimore, we see how aspects of the tax system’s design, while facially neutral, pose great challenges to our clients specifically.

Low-Income taxpayers are less likely to have stable housing and reliable internet access. Currently the IRS communicates with taxpayers primarily through mail, presenting an obvious issue for clients who are without housing or are quickly moving between short-term housing. While the IRS avoids contacting taxpayers by phone due to the prevalence of phone scams impersonating the IRS, this does not require getting in touch with the IRS to be as difficult as it is. Current wait times with the IRS assistance phone lines, while not as long as they were during the pandemic, are still extremely long.

The IRS has been trying to respond to this issue, in addition to hiring more staff, by increasing the features available on the IRS website, but this runs into the parallel problem of low-income taxpayers not having reliable internet access at home, or being less technologically proficient.

THE FREESTATE | 7

Older taxpayers similarly have difficulty accessing these online services. These barriers to service which are especially present for low-income taxpayers mean they are less likely to quickly resolve any audits or controversies with their accounts – meaning more penalties and accumulating debts.

Analyses of internal IRS systems have recently found that Black taxpayers are audited more frequently than non-Black taxpayers. In early 2023, the Stanford Institute for Economic Policy Research (SIEPR) released a report (“Measuring and Mitigating Racial Disparities in Tax Audits”. Elayzn, et al.) showing that Black taxpayers are audited at 2.9 to 4.7 times the rate of non-Black taxpayers. This report concluded that most of this disparity was focused on the IRS’s process for selecting which returns claiming the Earned Income Tax Credit (EITC) to audit.

The EITC is one of the most important tax credits available for low and middle-income families, with the size of the credit depending on the taxpayer’s wage income and number of qualifying dependents. Because the EITC is often misclaimed, in part due to the complex rules as to who qualifies for what amount, returns which claim the EITC are often subject to additional scrutiny. This means lower-income taxpayers who claim the EITC are more likely to be audited. However, the SIEPR report went further in uncovering that Black taxpayers who claimed the EITC were still more likely to be audited with non-Black taxpayers who also claimed the EITC! The report's authors suspected that this is a result of facially neutral IRS automated systems prioritizing auditing the maximum total number of suspected flawed returns, rather than aiming to detect the maximum total amount of unreported income. Had the systems selected more complicated returns, which take longer to audit, then the discrepancy between the number of audits of Black and non-Black taxpayers would not have been so severe.

In the wake of the SIEPR report, the IRS released a public statement committing to reexamining its policies and working to find a fairer solution, but time will tell if this practice does change. After the long wait times on the IRS phone service during the pandemic, the IRS likewise committed to reform, and has made some progress. American taxpayers should continue to speak out regarding inequalities in the U.S. tax system, so that we can all have a tax system that treats us all fairly.

Tax Professionals should also be aware of how they can call attention to problems in the federal tax system, as well as potentially offer help. The IRS Systemic Advocacy Management System (SAMS) available on the IRS website collects descriptions of systemic or reoccurring issues with IRS systems and procedures. Anyone can make a SAMS report on any issue they have seen affecting more than one taxpayer. Tax professionals can work to reduce the gap in taxpayer knowledge by working with an LITC, offering whatever amount of pro bono representation they can offer to assist low-income taxpayers in their tax controversies. In Maryland, our LITC at Maryland Volunteer Lawyers service accepts volunteer Attorneys, CPAs, and Enrolled Agents and upon request, pairs them with a Low-income Taxpayer in need of representation. You can learn more about MVLS and volunteering at www.mvlslaw.org.

THE FREESTATE | 8

Move The Needle Forward for Your Clients

USB Payment Processing

The title of a ‘trusted advisor' often comes with the connotation that you are an experienced, resourceful, and fully capable individual who provides guidance and direction to small business owners. In today's world that means being ahead of the curve when it comes to client needs.

The business landscape is constantly evolving, causing business owners to seek ways to run their businesses more efficiently Increasingly, they are diverting their time and energy into things such as evaluating processes, costs, hiring and other variables that affect their bottomline The result is having less time to optimize other aspects of your business. When your practice can utilize simple tools and understand the simple nuances of payments, you begin to provide a unique optimization service that is not found across the board

In the 90s movie Jerry Maguire, we watch the journey that a fired football agent embarks on to

keep his star client. At the end of the movie, there is a scene where Jerry Maguire embraces Rod Tidwell, the star player, after he receives a huge touchdown pass. Maguire and Tidewell have experienced years of working together through the highs and lows of their industry, creating a bond and excitement around the win. A teammate of Tidewell witnessed the two embrace in joy over this touchdown, causing him to look over to his agent and question, “Why don't we have a relationship like that?” The agent gave an inauthentic response and rebuffed him.

What we can take away from this dynamic is how going above and beyond for your client can create genuine relationships and retention. That means being a resource to your clients and seeking to improve all areas of your client's business, even when certain things might not be broken or asked of you.

Payments can be a confusing landscape to navigate with landmines that can appear daunting for accounting professionals. However, there is a tool that can help guide the way. The Merchant Comparison Tool allows professionals to compare a client's costs against others in the same industry, without giving up client privacy. With 4 data points and 60 seconds, you will receive information that could be very consequential to their bottom line.

This data will allow you to increase your ability to add value without straining your valuable time. Being able to provide your clients with accurate and insightful information about their payments standing will prove to be a game changer for bettering your clients and trusted advisor relationship.

Moving the needle does not always have to come from an elaborate service or data. When you use simple solutions, you can affect EVERY small business in America that accepts electronic payments Become a hero to your clients and provide them with invaluable information that could help them move the needle forward. Visit us at www.merchantcomparisontool.com or email hjennings@usbne.com to learn more about how you can become a hero today!

THE FREESTATE | 9

MarylandIntroduces PrivateLetter Rulings

AUTHOR: ROBERT BRALAND, ESQ., LL. M.

On January 8, 2024, new regulations adopted by the Office of the Comptroller took effect establishing a program for Private Letter Rulings (PLRs) within the State of Maryland. These regulations usher in a new era for Maryland taxpayers seeking clarity as to the tax treatment of certain transactions With the introduction of this program, Maryland aligns itself with established practices at the federal level, where PLRs have long been instrumental in navigating complex tax issues.

During the 2022 Maryland General Assembly Session, Comptroller Lierman in her capacity as then-delegate sponsored HB366, a measure to establish a new Legal Division of the Office of the Comptroller to provide necessary guidance for taxpayers seeking certainty of tax treatment when taking a position on complex matters This measure, as adopted under SB477 and now codified under §13-1A-02 Md. Code Ann., created the PLR program through the Office of the Comptroller. On December 19, 2023, these procedures were adopted as regulations under a new chapter of the Code of Maryland Regulations, COMAR 03 01 05 Three days later the Office of the Comptroller provided further guidance for PLRs with the release of Technical Bulletin No 44, effective December 22, 2023

A PLR is a final, written, non-appealable determination issued by the Comptroller of Maryland that is applicable to a specific set of facts submitted by a written petition. There is no fee associated with submitting a petition for a PLR

In general, a PLR is binding on the Comptroller for a period of 7 years from the date the private letter ruling is issued unless voided, modified, or revoked.

A petition for a PLR may be submitted by either a person who is a party to the subject transaction or an authorized representative on behalf of a party to the subject transaction. The petition for a PLR may not be submitted by a person or group of persons that are not related parties to the subject transaction, such as trade associations

The petition for a PLR must:

1

Identify the petitioner and all parties involved in the transaction or question;

2.

Contain a concise statement of the question or issue on which the petition is based;

3

Contain a detailed statement of the facts on which the petition in based;

4

Contain a redacted or anonymized version of the statement of facts upon which the petition is based to be published;

5

Identify all statutes, regulations, judicial decisions, or other published federal or state guidance relevant to the petition, including authority adverse to the petitioner’s position;

7

Include a discussion of whether, and in what manner, the statutes, regulations, judicial decisions, and other published federal or state guidance apply to the petitioner under the facts outlined in the petition;

6 Contain a description of the petitioner’s interest in the private letter ruling, which shall include the following:

A statement as to whether the PLR sought is intended to affect the tax consequences of any transaction or transactions entered into or contemplated by the petitioner or related parties which are known by the petitioner to be the subject of a Comptroller inquiry, audit, refund, or assessment proceeding

THE FREESTATE | 10

A statement as to whether the PLR sought is intended to affect the petitioner’s status under any of the licensing, regulatory, or statutory provisions administered by the Comptroller, which is known by the petitioner to be the subject of a Comptroller inquiry, inspection, investigation, audit, refund request, voluntary disclosure, or other proceeding in the Comptroller’s Office; and An explanation of the circumstances surrounding the inquiry, audit, refund, assessment, inspection, investigation, or other proceedings, if any;

8. Contain a statement as to whether the petitioner has sought or is seeking a PLR or other guidance from the IRS, another State, or another taxing authority on the transaction or question that is the subject of the petition for a PLR, and if so, identify that other state or taxing authority;

9 Contain, if the petitioner asserts a position or alternative positions, a concise proposed draft ruling;

10. Contain the signature of the petitioner or the petitioner’s authorized representative; and 11. Include, if the petition is submitted by an authorized representative, a completed Maryland Form 548 Power of Attorney.

It is important to note that a petitioner is not bound by a PLR, though a petitioner’s failure to follow a PLR may be considered in determining whether interest and penalty should be reduced or abated for reasonable cause in a subsequent challenge of an assessment or denial of a refund on the issue covered by the PLR. A PLR may also be used as evidence of a petitioner’s knowledge or intent in a subsequent proceeding and the Comptroller may use information submitted in a petition for a private letter ruling for subsequent audit purposes A PLR may not be appealed to the Comptroller’s Hearing and Appeals Division, the Maryland Tax Court, any other administrative agency, nor any State or federal court.

For Maryland taxpayers, the creation of this PLR program provides tax clarity surrounding complex transactions Individuals and businesses contemplating a unique transaction this year should consult a trusted tax professional about the benefits of this program when evaluating the viability of any such transaction.

THE FREESTATE | 11

Navigating My Accounting Journey: Top Courses That Shaped My Experience

By Abby Benton, Student of the University of Maryland

My name is Abby Benton, and I am a senior at the University of Maryland, double majoring in accounting and information systems, with a minor in nonprofit leadership and social innovation I am also part of a Plus 1 program, in which I have completed one-third of a Master of Science in Accounting degree as an undergraduate, and will complete the rest during the 2024-2025 school year

As an accounting student, my experiences over the past four years have been incredible The rewards of my studies have been tremendous, and the opportunities accounting has offered me have been incredible. Throughout my undergraduate career, I have had the opportunity to take many great accounting courses. Each of these has contributed to my great success as an undergraduate and given me the skills and knowledge to move forward with my education and career.

Of the classes I have taken, four have had the most impact on my learning experience. These include intermediate accounting II, accounting analytics, taxation of individuals, and forensic accounting These classes, in particular, have been impactful because of the content and form of instruction Intermediate accounting II provided me with a great understanding of financial statements and accounting transactions My professor made the course approachable by providing guided notes that were completed during class Accounting analytics gave me hands-on learning opportunities to connect my accounting knowledge with practical industry software This course helped me tremendously in my internships, as I had already learned about some of the technology being used, such as Tableau and Power BI. Individual taxation provided me with a vast understanding of the Form 1040 and its associated schedules. This class was heavily interactive and discussion based, which made learning the content much more effective.

Lastly, Forensic accounting was the most interesting accounting course I have taken I learned so much about the connection between accounting and white-collar crimes, as well as how to be an ethical accountant This was my favorite class because of the depth of content and interesting readings While all of my other courses have provided me with a strong foundation for accounting knowledge, these four stand out as I look back on my previous semesters

As my undergraduate career comes to a close, I am so happy I chose accounting From the things I have learned, to the opportunities ahead of me, accounting has been at the root of it all. As I continue my education and career in accounting, I am excited for what is to come.

THE FREESTATE | 12

2024 LEGISLATIVE REPORT

B Y : J A M E S A R N I E

The MSATP Legislative Report provides a concise overview of the Maryland General Assembly's 2024 session, which convened from January 10, 2024, to April 8, 2024

During this period both houses held in-person committee hearings additionally providing an option for virtual testimony The session was marked by a high volume of legislative activity, with 1,526 bills introduced in the House and 1,188 in the Senate, covering a broad spectrum of issues pertinent to our profession

The Society's advocacy efforts were robust, focusing on 106 bills that directly impacted our field This involved both written submissions and in-person testimonies on critical legislative items Notably, the MSATP supported two significant bills introduced by the Comptroller which were favorable to tax professionals Furthermore, we played a crucial role in opposing HB1515, a bill that sought to extend the sales tax to tax preparation services, successfully preventing its advancement

CORPORATE INCOME TAX

Corporations and Associations –Definitions, Emergencies, and Outstanding Stock – Revisions

HB 0749

SB 0400

This bill generally (1) authorizes a corporation to adopt emergency bylaws and establishes related provisions applicable to an “ emergency (as defined in the bill); (2) clarifies statutory provisions related to a corporation’s acquisition of its own stock; and (3) alters specified definitions Effective October 1, 2024

ESTATES AND TRUSTS

Estates and Trusts – Appointment of Personal Representative – Objections

HB 0326

SB 0080

This bill alters a provision in the notice of appointment of the personal representative of an estate, published by the register of wills, by limiting those whom the notice indicates may object to the appointment to “all interested persons or unpaid claimants” rather than “all persons ” Effective October 1 2024

Estates and Trusts –Interested Person – Definition

HB 0325

SB 0164

Alters the definition of an “interested person ” in the Estates and Trusts Article

by (1) establishing that a legatee ceases to be an interested person if the legatee’s interest has been fully deemed; (2) adding as interested persons a surviving spouse who has timely filed an election to take an elective share and a person who timely files a petition to caveat a will; and (3) establishing that an assignee of a legatee or an heir is not an interested person Effective October 1, 2024

PERSONAL INCOME TAX

Income Tax – Subtraction

Modification – Police Auxiliary and Reserve Volunteers

HB 0646

SB 0108

Consolidates the existing subtraction modification programs for volunteer police personnel and volunteer fire, rescue, and emergency services personnel under a public safety volunteer” subtraction modification and makes various related changes; and (2) increases the value of the subtraction modification for police auxiliaries and reserve volunteers from $5 000 to $7 000 beginning in tax year 2024 (consistent with the value of the existing subtraction modification for volunteer fire, rescue, and emergency services personnel Shall take effect July 1, 2024, and shall be applicable to all taxable years beginning after December 31, 2023

THE FREESTATE | 13

2024 LEGISLATIVE REPORT

Catalytic Revitalization Project

Tax Credit Alterations

SB 0394

This bill makes various alterations to the catalytic revitalization project tax credit A recipient of a tax credit certificate for a phased project that is issued on completion of a phase may claim the full amount stated on the final tax credit certificate in the tax year in which the certificate was issued The Secretary of Housing and Community Development may award initial tax credit certificates for more than one catalytic revitalization project within a twoyear period; however, the Secretary may not (1) accept applications and award initial tax credit certificates for projects more than once within a two-year period or (2) issue tax credit certificated totaling more than $15 million in aggregate within a twoyear period (consistent with the existing per-project limit) The bill also authorizes the Secretary to revoke an initial tax credit certificate under specified circumstances and requires the Secretary to establish procedures for the approval of project phases. Effective July 1, 2024, and applies to tax year 2024 and beyond

Income Tax Credit – Venison Donation

HB 0477

SB 0440

Re-establishes, with modifications, the non-refundable venison donation

income tax credit An individual who hunts and harvests an antlerless deer for donation to a charitable venison donation program may claim a credit of up to $75 of expenses incurred to butcher and process an antlerless deer for human consumption if the hunting and harvesting of the deer complies with State hunting laws and regulations An individual may not claim more than #300 in tax credits in any tax year unless the individual harvested each deer for which the credits are claimed in accordance with a deer management permit. Any amount of unused credit may not be carried over to any other tax year By January 31 each year each venison donation program that accepts a donation must report specified information to the Comptroller Effective July 1, 2024, and applies to tax years 2024 through 2028 The bill terminates on June 30, 2029

Income

Tax – Subtraction

Modification for Donations to Diaper Banks and Other Charitable Entities –Sunset Repeal

HB 0490

Extends through tax year 2026 the State income tax subtraction modification for donations of disposable diapers, other hygiene products for infants and children, feminine personal hygiene products, or cash specifically designated

for the purchase of such items to diaper banks and other qualified charitable entities Effective June 1, 2024

Income Tax – Subtraction Modification – State Law Enforcement Officers

SB 0822

Expands eligibility for the existing subtraction modification for law enforcement officers who reside in political subdivisions with specified crime rates to include State law enforcement officers who reside in these qualifying political subdivisions Effective July 1, 2024, and applies to tax year 2024 and beyond

Income Tax Subtraction Modification – Death Benefits – Law Enforcement Officers and Fire Fighters

HB 1064

SB 0897

This emergency bill allows a subtraction modification against the personal income tax for a payment of a death benefit (to the extent included in federal adjusted gross income) under a collective bargaining agreement from a county or municipality in the State to the surviving spouse or other beneficiary of a law enforcement officer or firefighter whose death arises out of or in the course of employment as a law enforcement officer or firefighter and applying the Act retroactively to taxable years beginning after December 31, 2021

THE FREESTATE | 14

2024 LEGISLATIVE REPORT

Income Tax – Individual Income Tax Credit Eligibility Awareness Campaign

HB 0845

SB 1105

This departmental bill requires the Comptroller to implement and administer an individual income tax credit eligibility awareness campaign to identify underserved individuals who may be eligible to claim an individual income tax credit and encourage them to apply for credits. To assist in identifying underserved individuals who may be eligible to claim an individual income tax credit the Comptroller may partner with other State agencies by entering into datasharing agreements that comply with proper data use standards, as specified In each of fiscal 2026 through 20230, the Governor must include $300,000 in the annual budget bill for the awareness campaign. Effective July 1 2024 and terminates December 31 2030

REGULATORY

State Board of Individual Tax Preparers – Sunset Extension

SB 0288

This departmental bill extends the termination date for the State Board of Individual Tax Preparers within the Maryland Department of Labor (MDL) by one year to July 1 2027 subject to the evaluation and reestablishment provisions of the Maryland Program

Evaluation Act (MPEA) It also requires MDL to submit a report to the Joint Audit and Evaluation Committee (JAEC) by July 1 2025 with information –regarding the State Board of Individual Tax Preparers – to be determined by JAEC Effective July 1, 2024

Tax Assistance for Low-Income

Marylanders – Funding

HB 0451

SB 1142

Reinstates, beginning in fiscal 2025, a previously mandated annual distribution from the State’s Unclaimed Property Fund to the Tax Clinics for Low-Income Marylanders Fund A(TCLIM) at an increased amount of $500,000 (compared to $250,000, as mandated under previous law) Also, beginning in fiscal 2026, the bill (1) increases the amount of the annual mandated appropriation for the Creating Assets, Savings, and Hope (CASH) Campaign of Maryland from $500,000 to $800,000 and (2) requires that at least $150 000 be used to provide grants to external entities for providing tax assistance through on-demand or mobile tax clinics that serve senior populations, rural communities, or under-resourced communities Effective July 1, 2023

Individual Tax Preparers – Code of Ethics, Notification of Actions, Enforcement, and Penalties (Stop Scam Tax Preparers Act)

HB 0452

SB 0675

This departmental bill (1) requires the State Board of Individual Tax Preparers, by January 1, 2026, to publish on its website a code of ethics and rules of professional conduct for engaging in the practice of individual tax preparation; (2) requires the board to notify the Comptroller’s Office of specified actions and violations under the Maryland Individual Tax Preparer’s Act; (3) grants authorized employees of the Field Enforcement Bureau with the powers, duties, and responsibilities of a peace officer for the purpose of enforcing the laws pertaining to income tax preparation; and (4) requires the Comptroller to notify the board after prohibiting an income tax return preparer from submitting income tax returns electronically Lastly the bill prohibits an income tax preparer from willfully preparing assisting in preparing or causing the preparation of an income tax return or claim for refund without being properly licensed or registered to provide income tax preparation services in the State; a violation is a misdemeanor subject to a fine of up to $5,000 to be paid into the Tax Clinics for Low-income Marylanders Fund (TCLIM) Effective October 1 2024.

THE FREESTATE | 15

2024 LEGISLATIVE REPORT

Low-income Marylanders Fund (TCLIM). Effective October 1, 2024

Income Tax – Technical Corrections

HB 0453

SB 0678

This departmental bill repeals obsolete provision of the Tax-General Article relating to the distribution of income tax revenue and corrects an erroneous cross-reference relating to the catalytic revitalization project tax credit Effective July 1 2024

Disclosure of Tax Information –Tax Compliance Activity and Binding Data Use Agreements

HB 0454

This departmental bill authorizes the disclosure of tax information to a person, governmental entity, or tax compliance organization for the purpose of assisting the Comptroller in tax compliance activity and requires specified parties to whom confidential tax information is to be disclosed to enter into a binding written data use agreement An officer, employee, former officer or former employee of a person, governmental entity, or tax compliance organization to which tax information has been disclosed in accordance with the bill’s authorization may not disclose in any manner, any tax information obtained in accordance with the data use agreement, unless the disclosure is authorized expressly by State or federal law, authorized by the data use agreement, or required by a

court order Consistent with existing law an officer employee former officer or former employee of a person, governmental entity, or tax compliance organization to which tax information has been disclosed who makes a disclosure in violation of State law is guilty of a misdemeanor subject to a fine of up to $1,000 and/or up to six months imprisonment. Effective July 1, 2024.

Comptroller – Electronic Tax and Fee Return Filing Requirements

HB 0455

SB 0677

This departmental bill generally requires the electronic filing of specified fee and tax returns, specifically; (1) for periods beginning after December 31, 2026, tire recycling fee returns, bay restoration fee returns, admissions and amusement tax returns alcoholic beverage tax returns digital advertising gross revenues tax returns motor fuel tax returns sales and use tax returns, and tobacco tax returns; (2) beginning in tax year 2027, income tax withholding returns, income tax returns for pass-through entities, and income tax returns for corporation with at least 15 employees; and (3) beginning in tax year 2030, individual income to returns, subject to specified exceptions. Additionally the bill prohibits a tax return preparer or software company from charging a separate fee for the electronic filing of authorized tax documents; a violation is subject to a civil penalty of $500 for a first violation or $1,000 for a second or subsequent violation The bill generally takes effect

July 1 2024; prohibitions relating to tax return preparers and software companies take effect January 1, 2030

Department of Aging – Caregiver Expense Grant Program – Established

SB 0202

Establishes a Caregiver Expense Grant Program within the Maryland Department of Aging (MDOA) to award grants for qualified expenses paid or incurred by an individual who provides care to a qualified family member and whose federal adjusted gross income does not exceed $75,000 ($150,000 if a joint tax filer) An eligible caregiver may apply for a grant equal to 30% of the amount of qualified expenses that exceeds $2,000, up to a maximum grant of $2,500 per fiscal year The Governor may include an appropriation in the annual budget bill of up to $5 0 million for the program for any fiscal year MDOA may adopt regulations to implement the bill’s provisions Effective July 1, 2024 (NOTE: This bill began as a subtraction modification)

Income Tax – Opportunity for Filers to Register to Make Anatomical Gift

HB 1068

SB 0577

Requires the Comptroller to implement procedures to offer an individual filing a Maryland resident individual income tax return electronically the opportunity to register to make an anatomical gift in

THE FREESTATE | 16

2024 LEGISLATIVE REPORT

accordance with the Maryland Anatomical Gift Act through a hyperlink to the anatomical gift donor registry established under the Act Effective July 1 2024 and applies to tax year 2024 and beyond

Maryland Department of Health and Department of Aging –

Earned Income Tax Credit –

Distribution of Information and Training

HB 1304

Requires the Maryland Department of Health (MDH) to develop a process for providing information about the availability of the State’s earned income tax credit to enrollees and potential enrollees in specified programs and other individuals receiving specified services The bill further requires the Maryland Department of Aging (MDOA) to provide periodic training to the Maryland Access Point network to increase awareness of the availability of the State’s earned income tax credit Effective October 1, 2024

SMALL BUSINESSES

Wage Payment and Collection –

Pay Stubs and Pay Statements –

Required Information

HB 0385

SB 0038

Expands information that an employer must give to an employee

for each pay period The notice required under current law of the employees’ rate of pay, regular paydays, and leave benefits that an employer must provide to a new employee at the time of hiring must be a written notice The Commissioner of Labor and Industry must create and make freely available to employers a pay stub template that employers may use to comply with this bill The bill specifies enforcement provisions, which include authorizing the Commissioner of Labor and Industry to (1) issue orders to comply with the bill; (2) impose an administrative penalty of up to $500 for each employee who was not provided a pay stub or online pay statement in accordance with the bill; and (3) bring an action to enforce the orders under specified conditions An employer may request an administrative hearing under specified conditions Effective October 1, 2024

Under the bill an employer must give to each employee for each pay period, a written statement on the physical pay stub or the online pay statement that includes:

The employers name registered with the State, address, and telephone number;

The date of payment and the beginning and ending dates of the pay period;

The number of hours worked during the pay period, unless the employee is exempt from federal and State overtime requirements;

The rates of pay;

The gross and net pay earned during the pay period;

The amount and name of all deductions;

A list of additional bases of pay including bonuses commissions on sales, or other bases; and

The applicable piece rate of pay and the number of pieces completed at each piece rate for each employee paid at a piece rate

Workplace Fraud and Prevailing Wage – Violations – Civil Penalty and Referrals

HB 0465

Increases the maximum civil penalty from $5,000 to $10,000 for each employee that an employer is found to have knowingly failed to properly classify under the Workplace Fraud Act On a showing of clear and convincing evidence that a relevant Workplace Fraud Act or State Prevailing Wage Law violation has occurred, the Commissioner of Labor and Industry must refer any complaint that alleges a violation of specified tax withholding and tax fraud provisions in the TaxGeneral Article to the Comptroller, the State s Attorney with jurisdiction over the alleged violation, the U S Department of Justice, the U S Department of Labor (USDOL), and the U S Department of the Treasury

Effective October 1, 2024

THE FREESTATE | 17

2024 LEGISLATIVE REPORT

Family and Medical Leave

Insurance Program –

Modifications

HB 0571

SB 0485

Modifies the Family and Medical Leave Insurance (FAMLI) Program by altering key administrative deadlines, definitions, and components of the program ’ s administration and authorizing the Maryland Department of Labor (MDL) to adopt regulations that establish fees for private employer plans The start dates are delayed by nine months to July 1, 2025, for required contributions and six months to July 1, 2026, for benefit payments Effective October 1, 2024

Labor and Employment – Equal Pay for Equal Work – Wage Range Transparency

HB 0649

SB 0525

Expands the applicability, requirements, and penalties of the State s Equal Pay for Equal Work

Law Generally, an employer must disclose specified wage, benefit, and any other compensation information in public or internal job postings and to applicants to which the job posting was not made available The proactive disclosures have additional specified requirements and replace the existing requirement to disclose a wage range to an applicant on request The wage range must be set by the employer in good faith

The Commissioner of Labor and Industry must develop and make available to employers a form that an employer may use to comply with the bill Existing retaliation provisions are updated to incorporate employee promotions or transfers Employers must keep records of compliance with the updated requirements for at least three years, as specified Effective October 1, 2024

SALES AND USE TAX

Sales and Use Tax Exemption –

Aircraft Parts and Equipment –

Repeal of Reporting Requirement and Extension of Sunset

HB 0557

SB 0574

Extends, from June 30, 2025, to June 30, 2030, the termination date of Chapter 638 of 2020, which exempted the sale of specified aircraft parts and equipment from the State sales and use tax The bill also repeals a specified reporting requirement Effective July 1 2024

Sales and Use Tax – Nonprofit Organizations Maintaining Memorials

– Exemption

SB 0580

Exempts from state sales and use tax sales made by specified nonprofit organizations that maintain a memorial on property owned by the state if the proceeds of the sale are used to maintain a memorial on state-owned property Effective July 1, 2024

Disclaimer: This report provides a summary of the legislation that was passed by the Maryland General Assembly during the 2024 session and signed into law by the Governor or Enacted Under Article II, Section 17(b) of the Maryland Constitution This report does not list every requirement that must be met to be in compliance with the legislation and any individual or business that must comply with or be knowledgeable of the legislation enacted into law should review the bills on the Maryland General Assembly website to ensure they are aware of and in compliance with all requirements of the legislation

THE FREESTATE | 18

The Maryland Society of Accounting and Tax Professionals (MSATP) has long been a stalwart advocate for ethical practices in the tax preparation industry. Our recent triumph in supporting the passage of the Stop Scam Tax Preparers Act (Senate Bill 675) underscores our commitment to protecting Maryland taxpayers from fraudulent tax preparers who exploit the most vulnerable populations.

The Need for the Stop Scam Tax Preparers Act

Fraudulent tax preparers pose a significant threat to the financial well-being of Marylanders, especially minorities, lowincome families, and ethical tax professionals.

These scam artists often promise inflated refunds or engage in other deceptive practices, leaving taxpayers to face the consequences of incorrect filings, including fines, audits, and even criminal charges. The Stop Scam Tax Preparers Act aims to curb these practices by instituting stricter regulations and enforcement mechanisms

Key Provisions of the Act

The Act introduces several critical measures to ensure the integrity of tax preparation services in Maryland: Code of Ethics and Professional Conduct: The State Board of Individual Tax Preparers is mandated to publish a comprehensive code of ethics and rules of professional conduct by January 1, 2026 This code will be developed with input from the tax preparer community to ensure it addresses real-world challenges and ethical considerations

THE FREESTATE | 19

Enhanced Reporting and Enforcement:

The Board is required to notify the Comptroller and the Field Enforcement Bureau of the Comptroller’s Office within five business days of any disciplinary action or alleged violation This rapid reporting mechanism ensures swift action against violators

Penalties for Violations: The Act introduces stringent penalties for tax preparers who engage in fraudulent activities or operate without proper licensing Convicted individuals may face fines up to $10,000 or imprisonment up to five years, with each false return constituting a separate violation

Support for Low-Income Taxpayers: Fines collected under the Act will be directed to the Tax Clinics for Low-Income Marylanders Fund This fund supports legal clinics that assist low-income residents with tax-related issues, ensuring they have access to professional help and advocacy

MSATP's Role in Advancing the Legislation

MSATP's journey from proposing the Stop Scam Tax Preparers Act to witnessing its passage has been marked by unwavering dedication and proactive advocacy. Our Executive Director, Giavante’ Hawkins, played a pivotal role in this process, bringing to light the devastating impact of tax scams on minorities, low-income families, and ethical tax professionals.

Advocacy and Testimony

Giavante’ Hawkins testified before the legislative committees, sharing firsthand accounts and data on how fraudulent tax preparers exploit vulnerable communities Her compelling testimony highlighted the need for robust regulatory frameworks and stringent enforcement to protect taxpayers and uphold the integrity of the tax preparation profession

Collaboration and Support

MSATP collaborated with key stakeholders, including the Office of the Comptroller and the State Board of Individual Tax Preparers, to draft and refine the provisions of the Act Our members provided valuable insights and feedback, ensuring the legislation addressed practical concerns and industryspecific challenges.

Looking Ahead

The passage of the Stop Scam Tax Preparers Act marks a significant victory for Maryland taxpayers and the tax preparation industry. However, our work is far from over. MSATP will continue to monitor the implementation of the Act, advocate for necessary adjustments, and provide ongoing support to our members and the broader community.

We remain committed to fostering an ethical, inclusive, and professional tax preparation environment in Maryland. Together, we can ensure that all Marylanders receive the honest, competent, and reliable tax services they deserve

THE FREESTATE | 20

Are You Getting the Most Out of Your MSATP Membership?

To learn more about how you can maximize your MSATP membership or if you have any questions, please don't hesitate to reach out. Reply to this email or contact our member services team at (800) 922-9672 We're here to help you get the most out of your membership and support your professional success.

MSATP members enjoy exclusive discounts on seminars and events, allowing you to stay up-to-date with the latest industry trends and best practices while saving money on registration fees

on Seminars & Webinars Exclusive Verifyle Platinum Subscription

As an MSATP member, you receive an exclusive Verifyle Platinum subscription, which provides unlimited digital signatures This feature streamlines your client interactions and simplifies the document signing process

Ethics CPE Credits

Maintain your professional designations with ease by earning FREE Ethics CPE credits through MSATP This benefit helps you meet your designation's requirements without additional costs Enjoy exclusive discounts on essential resources such as Talking with TaxSpeaker, the TaxBook, QuickFinder, and many others These discounts help you access the tools and information you need while keeping costs down

Discounts on Essential Resources Free Access to CCH TaxAware

Stay informed about tax-related matters with free access to CCH TaxAware, a valuable resource for tax professionals

Complimentary Unlimited Subscription to Earmark CPE

Earn CPE credits on the go with a complimentary unlimited subscription to Earmark CPE This benefit allows you to conveniently maintain your professional development whenever and wherever you choose

Attendance to Monthly Business Builders ThinkTank Groups

Benefit from attending MSATP's monthly Business Builders ThinkTank groups, where you can learn from and collaborate with other solo and small firm professionals

Vibrant Community of Solo and Small Firm Professionals

As an MSATP member, you become part of a vibrant community of solo and small firm professionals who offer support, collaboration, and a wealth of knowledge to help you succeed in your practice

Free

Discounts

Exclusive

Member Benefits Spotlight

FREE access to Verifyle Platinum If you haven't done so already, it’s time to safeguard your client’s information and enhance your practice’s efficiency Verifyle Platinum is an ultra-secure document storage and communication platform designed with professionals like you in mind It offers a space to share, store, and communicate securely

Earmark CPE

With Earmark's Unlimited Subscription, members can enjoy unlimited free CPE courses every week, an ad-free experience within the app, and the option to skip sponsor messages during registration for sponsored courses. It's a game-changer for professionals in small firms, providing a convenient and affordable education.

As a NASBA-approved CPE sponsor and IRS-approved CE provider, Earmark offers a vast range of courses covering accounting, tax, technology, fraud detection, personal development, practice management, and more. Our CPAs, CMAs, and EAs can now meet their continuing education requirements simply by tuning in to insightful podcasts. We're particularly excited about the exclusive Federal Tax Updates podcast, which provides biweekly federal tax news and analysis.

CCH TaxAware

Quickly and easily get answers to all your federal and state tax questions in one place! Don’t waste time searching various resources for crucial news and information that you need quickly.

Housed on the powerhouse platform, CCH® IntelliConnect®, the Wolters Kluwer TaxAware Center has all the state and federal tax news, information, and tools necessary for today’s tax professionals.

Verifyle

CORPORATE SPONSORS Become a Sponsor Today Gain access to one of the largest inclusive financial societies in the nation. Email Kelly Ebaugh at kebaugh@msatp.org for more information PeopleWorX is an end-to-end workforce management company providing payroll, HR, Time & Attendance, Employee Benefits, and more We offer a complete, integrated, single sign-on solution while pairing our technology with expert support Customers can also package our solutions with our add-on HR services We help tax professionals and their clients who own lease, residential rental, multi-family and commercial properties by providing the calculations that accelerate depreciation and save income taxes USB Payment Processing is a 26-year-old small business solutions company specializing in payment acceptance, point of sale, and software technology, helping you and your clients save money. JERRY LOTZ | 410.960.8269 JONATHAN POCIUS | 240.699.0060 MARC REIBMAN | 410.828.4286 WWW.PAYROLLSERVICESLLC.COM WWW.COSTSEGES.COM WWW.USBNE.COM