Tokyo

• Steady tenant demand whilevacancyratesremainlimitedandnetabsorptionispositivealthoughlimitednew supplywas completed thisquarter

• Rents riseforthesixthconsecutive quarter

• Furtherdecline invacancy rateswithalmostnoremaining spaceinOtemachi/Marunouchi

According totheTankanSurveyinJune, thediffusionindex oflarge manufacturersrose1point to13,thefirstriseintwoquartersdueto solidrecovery intheironandsteelsector.Theindex oflargenonmanufacturersfell1point to34duetoinbound demand. Strong demand forofficesisseenduetoheadcount increasesandflight-toqualityrelocations. Netabsorptionwasaround 30,800sqminQ2 2025.Byindustry,thefigurewasdriven byinformation services, wholesaleandretailtrade,andprofessional services.

Onenew GradeAofficebuildingwascompleted inQ22025.Tokyo's vacancy rateintheGradeAofficemarketinQ2averaged 2.4%andfell 10bpsq-o-q and120bpsy-o-y. Bysubmarket,thevacancyratefor Otemachi/MarunouchiandAkasaka/Roppongi submarketsfurther compressed, withsub-1%levels seenintheformer.

Rents averaged JPY36,237pertsubo,permonth, up2.0%q-o-q and 5.9%y-o-y byendQ22025.Rents inbothAkasaka/Roppongi and

Otemachi/Marunouchisubmarketswereupaslandlord-favourable marketconditions continue duetotightsupplyanddemand. Capital valuesinQ22025wereup2.9%q-o-q and9.5%y-o-y, reflecting the continualriseinrents andunchanged capratesfrom theprevious quarter.Anotabletransactionannounced thisquarterwasthe acquisitionofAkasakaParkBuildingbyMitsubishiEstate.

Outlook

According toOxfordEconomics' forecastasofJune 2025,theGDP growthforyear-end 2025is0.8%andtheCPIis2.8%.Risksinclude theimpactoftariffsoncorporate activityandadownturn inoverseas economies. Leasingvolumesareexpected tostaysolidinthesecond halfoftheyearasdemand forexistingbuildingsisvery robustdueto strongappetite fromcorporates. Capitalvaluesarealsoexpected to risehigherasrentincreasesexceed projections.

Fundamentals

Note:Financialandphysical indicatorsareforthe5KusGradeAofficemarket.Datais onanNLAbasis.

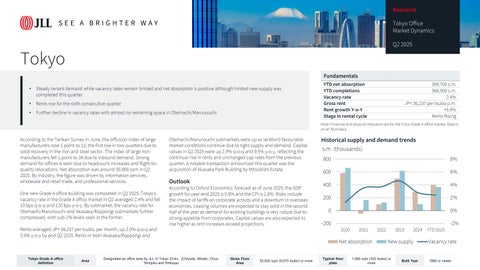

Historicalsupplyanddemandtrends

COPYRIGHT ©JONESLANGLASALLEIP,INC.2025

Thisreport hasbeenprepared solelyforinformation purposesanddoesnotnecessarilypurport tobeacomplete analysisofthetopics discussed,whichareinherently unpredictable. Ithasbeen basedonsourceswebelievetobereliable,butwehavenotindependently verifiedthosesourcesandwedonot guaranteethattheinformation inthe report isaccurateorcomplete. Anyviewsexpressed inthereport reflect ourjudgment atthisdateandaresubjecttochange withoutnotice. Statements thatareforward-looking involve known andunknown risksanduncertaintiesthatmaycausefuturerealitiestobemateriallydifferent fromthoseimplied bysuchforward-looking statements.Advice wegive toclients inparticularsituationsmaydifferfromtheviewsexpressed inthisreport. Noinvestment orotherbusinessdecisions shouldbemadebasedsolelyon theviewsexpressed in thisreport.