OPEN ENROLLMENT

When choosing health insurance, consider your specific healthcare needs. Be suretomake sureany proposed planscover your prescriptions, any chronic conditionsand provide mental health andsubstance abuse coverage.

Prescript ion d ru gc overa ge

Comparehealth insuranceplansbased on their formulariesand costsharing str uctures. If youtake prescription medications, be surethe plan covers them.

The Affordable CareAct made itmandatory for individualand small group health plans effectivefrom2014 tocover prescription dr ug benefits as par tofessential health benefits.

Different health plans coverprescriptiondrugs in various ways Here arethe main options:

• Copays: The dr ug tier determines the amount your payfor prescriptions.

• Coinsurance: Youpay ashareofthe prescriptioncost with insurance paying the rest.

• Deductibles: Some planshavecombineddeductiblesthatcover medical and prescription costs, whileothers haveseparate prescription deductibles.

• Out-of-pocket maximum: Some planscap totalspending for in-networkexpenses formedical andprescriptioncosts Your health plan’s formular yisthe list of dr ugs it covers.Insurers can createtheir formularies and make changes but must followstate and federal rules.

The plans group dr ugs into tiers, with Tier 1beingthe least costly and higher tierscovering the most expensivedrugs.

Top-tierdru gs tend to bespecialty dr ugs like injectables and biologics and typically requirecoinsurancepayments.

Under the Affordable CareAct,plans in the individual and smallgroup markets must coveratleast onedruginevery U.S.Pharmacopeia categor y andclass.

Plans must coverthe same number of dr ugs in each categor yasthe essential health benefits benchmarkplan selected by the state.

The USP MedicareModelGuidelines require coverage for ever ygeneral categor yofmedications, but specific medicationsdonot have to be coveredbyevery plan.For example,whileevery plan must coverrapidacting insulin, it may designate apreferred brand. Similarly,the AffordableCareAct requireshealth plans to coverall types of FDA-approved contraceptionfor women. Each plancan decide which specificcontraception to coverwithin each type and mayrequire costsharingfor other versionsornot coverthem.

Formulariesoften restrict medications through prior authorization, quality caredosing, and step therapy.Priorauthorization means insurance approval beforefilling prescriptions, quality caredosing ensures FDArecommended quantity and dosage, and step therapy mayrequire tr ying a less expensivemedication first.

Chronic cond itions

Most health plans coverchronic conditions or long-term health issues. It’s essential to knowthe detailsofany planyou consider Forexample:

•Job-based and self-purchased plans must coverpre-existing conditions due to the AffordableCareAct

•Plans star ting in 2014 or later must coveressentialhealth benefits for most long-term conditions.

•Large company and self-funded plans may onlycover some essential health benefits.

•Some plans, like shor t-term health insurance, don’t coverpre-existing conditions or essential health benefits.

Here arefour factors to consider when selecting aplan:

1. Provider network: With achronic condition, you’ll need regular carefromspecific medical providers, includingspecialists. Be sureyour

preferreddoctorsand specialists arein-networkand remember that providernetworkscan change.

2. Out-of-networkcoverage: If youneed to see specialists outside your localarea, understand howthe plan’s provider networksand out-ofnetworkcoverageworks

3. Coveredmedications: Different planshavedifferent lists of covered dr ugs,socheck if your medications areincluded andunderstand the cost tiers

4. Total costs: Consider boththe monthly premiums andthe out-ofpocketcostsfor medicalcare. Most planshaveamaximumout-of-pocket limits for in-network care, and youmight be eligible for cost-sharing reductions based on your income.

Me ntal heal th and subst ance ab use cove rage Federaland Colorado laws mandate equal coverage for mentaland behavioral health conditions and othermedical conditions,known as “parity.”

This means insurance plans canno tbemorerestrictiveinproviding mental health benefits than medicaland surgical ones.

Mental health parity laws requireinsurance plans to covermental health and substance abusetreatment. It’s impor tant to knowwhat mentalhealth benefits different plans provide Allplans mustcover:

•Counseling and therapy for behavioral health

•Inpatient ser vicesfor mental and behavioralhealth

•Treatment for substance use disorder (substance abuse)

Be sureyou understand:

• Your costs: Copays,coinsurance, deductibles, andout-of-pocket maximums areall part of your cost-sharing.

• Treatmentlimits: Theremay be restrictions on the number of inpatient or outpatient visits covered.

• Managementtools: This could include requirements for pre-approval.

• Choosing doctors: The planwill coverin-networkproviders andmay alsoconsider coveragefor out-of-networkproviders andlocations

• Coverage criteria: Howthe insurance company determines which treatments aremedically necessary “Mental Health”and “BehavioralHealth”are terms sometimes used interchangeably but refer to different things.

Mental health is about howa person feels andthinks, while behavioral health is abroadertermthat includesthings thataffect aperson’s wellbeing, growth, and actions

This includesmental health conditions, substance useissues, eating habits, and outside factors like poverty, unstable housing, andtrauma Plans covermental and behavioral health conditions without spending limits.Marketplace plans cannotrefuse to coveryou or charge youmore becauseyou have apre-existing condition,such as mentalhealth or substance use disorder

Co lo ra do healt hi nsu ra nce re so urce s

Connect for Health Colorado: This is the state’smarketplace/exchange.

Residents can useConnect for Health Colorado to enroll in individual/ family healthplans,receive income-based subsidies,and enroll in Health FirstColorado.You can contact Connect for HealthColorado at 855-7526749 or visit connectforhealthco.com.

Colorado DivisionofInsurance: Regulates the insurance industr yin Colorado and assistsconsumers and businesses with insurance-related questionsand concerns Colorado Depar tmentofHealth Policy andFinancing (HCPF): Administers Medicaid (Health FirstColorado),Child Health Plan Plus (CHP+), and other health careprograms.

Colorado Senior Health Care and MedicareA ssistance: Aser vice for Colorado Medicare beneficiariesand their caregivers, providing informationand assistance with questions related to Medicareeligibility enrollment,and claims

Staying informed aboutMedicarechangesfor 2025 is crucial forconsumers to make the best decisions abouttheirhealthcarecoverage. By being awareofthe changes, youcan proactively assessyourhealthcare needs and make any necessar yadjustments to ensureyou have the most comprehensivecoverage.

MedicarePartA

MedicarePartA covers hospital stays, skilled nursingfacility care, hospice care,and some home healthcare. Almost99% of Medicare beneficiaries get Part Afor free becausethey paid Medicaretaxes whileworking

Medicare Part B

MedicarePartB covers services like doctors’visits and outpatientcare. Part Bisoptional, andin2024, Part B’spremiumwas $174.70 permonth Rates for 2025 haveyet to be announced.

If youreceiveSocial Securitybenefits,your monthly premium is deducted from your monthly benefit payments.

People who don’t receive benefits can pay their MedicarePartB premiums ever ythree months.

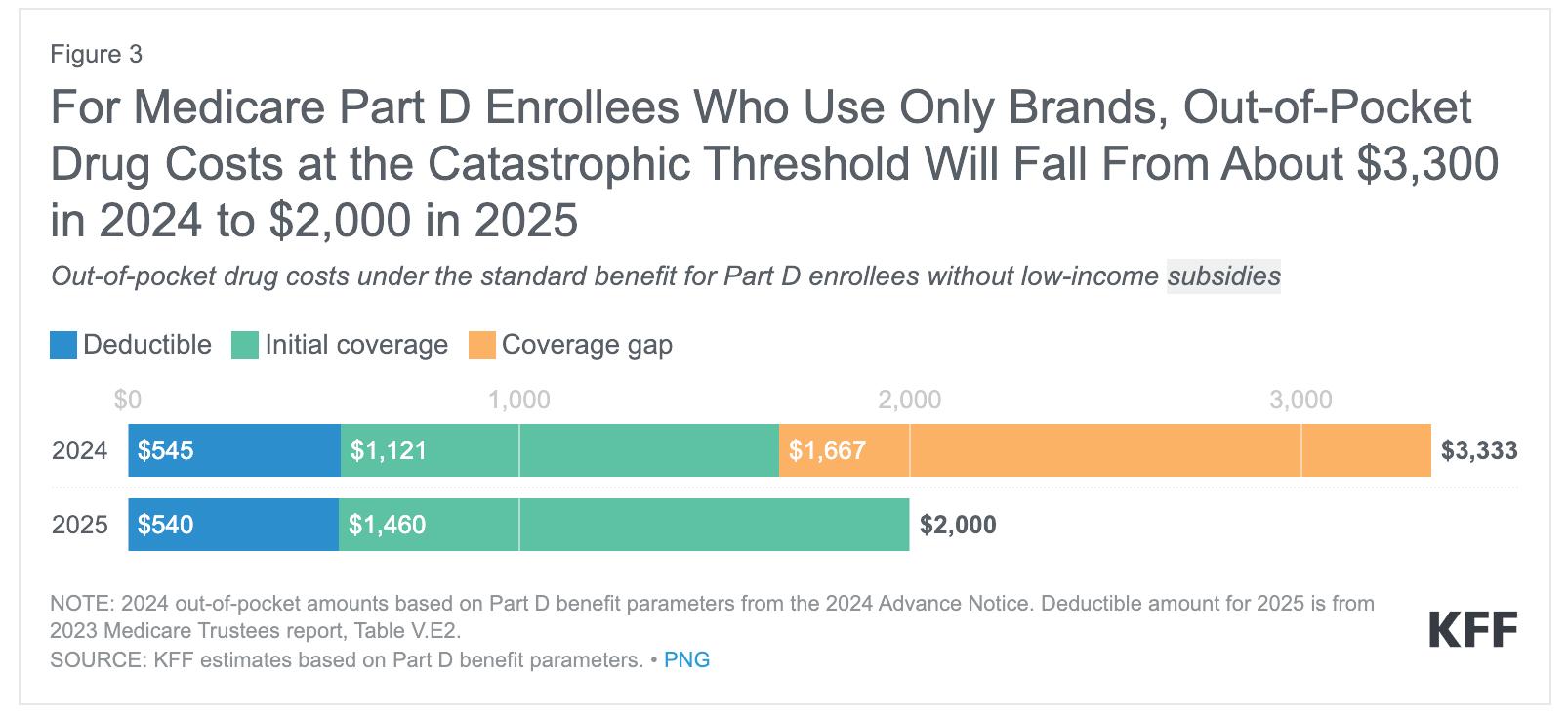

MedicarePartD covers prescription drug costs and the monthlypremium is based on income and deducted from your Social Securitybenefitcheck or paid directly to Medicare Part Dplans must cap out-of-pocket spending on covereddrugs at $2,000 annuallystarting in 2025.

The $2,000 cap includesdeductibles,copayments, andcoinsurance for covereddrugs. It doesn’t applytopremiums or any drugs that your plan doesn’tcover

The projected averagetotal Part Dbeneficiar ypremium is settodecrease by $7.45, from $53.95 in 2024 to $46.50 in 2025. Theaverage stand-alone Part Dplantotal premium is projected to decrease from $41.63 in 2024 to $40.00 in 2025.

These projections do notinclude the Part Dpremium reductions applied by MedicareAdvantage plans withprescriptiondrugcoverage using rebate dollars.

MedicarePartC or Medicare Advantage Plans

MedicareAdvantage is acomprehensiveplanthattypically includes Part A, B, and Dcoverage. Like an HMO or PPO, it oftenrequires using in-networkdoctors and may havelower out-of-pocketexpenses than traditional Medicare.

The plans may provide additionalbenefits such as vision, hearing, and dental servicesthat originalMedicare does not cover.

MedicareAdvantage plans areexpectedtoser ve 35.7 million Americans in 2025 and represent about 51% of all Medicarerecipients.

AverageMedicare Advantage premiumswill remain stable or decrease in 2025. If enrollees continue the same plan,approximately83% will have the same or lowerpremium in 2025.

Consumerswill continue to havechoices.

In 2025, 98% of people withMedicare will have access to ten or moreplans, including Special NeedsPlans.SpecialNeeds Plansprovidebenefits and servicestopeople withspecificsevereand chronic diseases,certain health careneeds, or who alsohaveMedicaid.

The number of Special NeedsPlans also will increase and areexpected to serveabout 28% of MedicareAdvantage users.

The federal governmentrunsoriginal Medicare, including Part Aand Part B. Private insurance companies administer MedicareAdvantage or Medicare supplement plans With Medicare,you canvisit any provider that accepts Medicare, while Medicare Advantage plansmay offer additional coverage forvision, dental, hearing, and prescriptiondrugs. Choose the right plan type

There arefiveMedicare Advantage plans:

1. Health maintenance organization (HMO) plans: Requireyou to see in-networkproviders, except in emergencies, and often need areferral to see aspecialist.

2. Preferred provider organization (PPO) plans: Allowyou to seeboth in-networkand out-of-networkproviders, but it’s usually more expensiveto go out of network.

3. Private fee-for-service (PFFS) plans: Allow youtosee any Medicareapproved providerifthey accept the plan’s payment terms. Youmay also haveaccess to aprovider network.

4. Special needs plans (SNPs): Created to improvecarefor Medicare beneficiaries with specific conditionsorcareneeds.

5. Medicalsavings account(MSA) plans: Combine ahigh-deductible insuranceplan with amedical savings account for health care costs. Comparep lans

The InflationReduction Actof2022 redesigned the MedicarePartD benefit to capannualout-of-pocket spending on prescription drugs at $2,000 starting in January2025.

This change willhelp alleviate the financial burden on MedicarePartD enrollees According to an analysisby AARP,the price cap is expected to benefit over 36,000enrollees in 2025.

The analysis shows that the impact of the newPartDout-of-pocket cap will vary. In 2025, around 1.5 million Part Denrollees aged 75-84 will reach the out-of-pocketlimit.

Enrollees reaching the cap will saveanaverage of$1,500 in 2025, and approximately 420,000 enrollees(12 percent) will experience savings of $3,000 or morebetween 2025 and 2029.

MedicarePartDwill eliminate the coverage gap phasein2025. The coverage gap previouslyoccurred whenenrollees moved outofthe initial coverage phase.

In 2025, drug manufacturersmust offer a10% discount on brand-name drugs during the initial coverage phase,replacing the previous 70% discount in thegap phase. Part Dplans willcover 65%ofthe costs of brand-name drugs.

Additionally,starting in 2025, Part Denrollees can spread outtheir out-ofpocketcosts over the year instead of facinghighcosts in any given month.

Saving money MedicarePartDcovers vaccineswith no out-of-pocketcosts, including shingles

and whooping cough vaccines.

The cost of aone-month supply of either Part D- or Part B-coveredinsulin products is capped at $35, and youdon’t havetopay a deductible for insulin.

If youget a3-month supply,the cost can’t be morethan $35 foreach month’s supply

Prescription costs will continue to drop in 2026.

The United States Depar tment of Health and Human Services reached agreements with all par ticipating manufacturersonnewly negotiated, lower dr ug prices for the first10drugs selected forthe Medicaredrugprice negotiation program

The ne wprices will cut the list price of these dr ugsbetween 38 and 79 percent.

Those dr ugs include:

•Diabetes treatments Jardiance and Januvia.

•Autoimmune disease treatment Enbrel.

•Hear tfailuredrugEntresto

•Diabetes and hear tfailuretreatment Farxiga.

•Blood thinners Eliquis and Xarelto

•Blood cancer treatment Imbr uvica

•Stelara, an IV treatment for psoriasis and other inflammator y disorders.

•Several versions of Fiasp,afast-acting insulin.

Exploreour Medicare Advantageplans— at a premium of $0

Getabudget-friendly plan designed with people like youinmind WithHumanaGoldPlusGivebackH0028-063 (HMO), youcould getmorethanyou expec tfor aprice youwouldn’texpec t. That’s becausewebring ever ything you’d getfromOriginalMedicare, plus more —and youpay amonthly premiumof$0.

Thisplanalsoincludesbenef it slike:

$1,750 allowancetospend peryearon preventive dental care,yearlyexams, f illings, cleanings, extrac tions, X-rays,crowns, dentures andmore*

Part Bpremium reduction, mayput up to $76backintoyourSocialSecurit y check each month†

•Visioncoveragewhich includes annual exam,f itting and$20 0allowance for glasses or contac tlenses

Call alicensedHumanasales agent

BenTorrez 720-501-7912 (T TY:711) Monday throughSunday, 8a.m.– 8p.m btorrez@humana.com

Amorehuman way to healthcare®

*Dentalallowance forin-networkser viceswithnocopaysorcoinsurance, excludingcosmetic. Allowanceamounts cannot be combined with otherbenef it allowances. Limitationsand restrictions mayapply.Dentalbenef it smay notcover all AmericanDentalAssociation procedurecodes.Information regardingeachplan is availableatHumana.com/sb † Part BGivebackBenef it pays part or allofyourPar tBpremium;the amount may changebased on the amount youpay forPar tB HumanaisaMedicareAdvantage HMOorganization with aMedicarecontrac t. Enrollmentinany Humana plan dependsoncontrac trenewal.Applicableto HumanaGoldPlusGivebackH0028-063 (HMO). At Humana,itisimpor tant you are treatedfairly. Humana Inc. andits subsidiaries comply with applicable federal civil rights laws anddonot discriminateonthe basisofrace, color, national origin, age,disability,sex,sexualorientation,gender, gender identity,ancestr y, ethnicity, maritalstatus, religion or language English: AT TENTION: If youdonot speak English, languageassistanceser vices, free of charge,are availabletoyou.Call 877-320 -1235( TT Y: 711).Español (Spanish): ATENCIÓN:Sihabla español, tienea su disposiciónser vicios gratuitosdeasistencialingüística.Llame al 877-320-1235 ( TT Y: 711) 繁體中文 (Chinese)