APPLIED PROTECTS THE TITANS OF INDUSTRY.® ©2022 Applied Underwriters, Inc. Rated A (Excellent) by AM Best. Insurance plans protected U.S. Patent No. 7,908,157. IT PAYS TO GET A QUOTE FROM APPLIED®

Accepting large workers’ compensation risks. Most classes. All states, all areas, including New York City, Boston, and Chicago. Few capacity and concentration restrictions. Simplified financial structure covers all exposures. EXPECT THE WINNING DEAL ON LARGE WORKERS’ COMPENSATION. Call (877) 234-4450 or visit auw.com to get a quote.

4 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM Contents News Markets& 10 P/C Underwriting Profitability to Worsen as Inflation, Hard Market Persist 12 COVID Impacts Linger in Courtrooms, Often a Disadvantage for Defendants 14 Q2 Commercial P/C Premiums Up 6.1%: CIAB 20 Record-Breaking Pace for U.S. Product Recalls, Says Sedgwick 24 Reinsurance Capital to Drop $40 Billion at Year-End 2022: AM Best Departments 6 Opening Note 16 Figures 18 Declarations 22 People 27 Business Moves ExchangeIdea 41 Ask the Insurance Recruiter: Tools Every Insurance Agency Needs to Recruit Account Managers 42 Real Price of Being an Insurance Customer 44 Recruiting and Retaining Claims Talent in the Candidate’s Market 46 Minding Your Business: Effective Sales Management & Producer Performance 50 Closing Quote: Drilling Down to Access Capabilities WholesalersBetween ReportSpecial 30 Special Report: Senior Care BoomCompetitionExperiencingMarketRevivedAmidHi-Tech 34 Special Report: It’s a Great Time in Surplus Lines 36 Spotlight: 25 Years: The Journey of Cyber Insurance 38 Closer Look: Forged Signatures, Fake Policies? Lawsuits Raise Questions About Captive Insurance Plan September 5, 2022 • Vol. 100 No. 16

Underwriting courage takes practice. For over 50 years, we’ve built a legacy of expertise and market leadership. From Main Street to Wall Street, we optimize solutions across an array of risks. Let’s talk. lexingtoninsurance.com/2022 The bestis PROTECTION EXPERIENCE. Lexington Insurance and Western World, both AIG companies, are U.S.-based surplus lines insurers. AIG is the marketing name for the worldwide property-casualty, life and retirement, and general insurance operations of American International Group, Inc. For additional information, please visit www.aig.com. Products and services are written or provided by subsidiaries or affiliates of American International Group, Inc. Not all products and services are available in every jurisdiction, and insurance coverage is governed by actual policy language. Certain products and services may be provided by independent third parties. Insurance products may be distributed through affiliated or unaffiliated entities. Surplus lines insurers do not generally participate in state guaranty funds and insureds are therefore not protected by such funds. INTENDED FOR LICENSED SURPLUS LINES INSURANCE BROKERS ONLY. Copyright © 2022 American International Group, Inc. All rights reserved.

6 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 Write the Editor: awells@insurancejournal.com Opening Note Andrea Wells Editor-in-Chief CallSUBSCRIPTIONS:(855) 814-9547 or visit ijmag.com/subscribe Outside the US, call (847) 400-5951 Insurance Journal, The National Property/Casualty Magazine (ISSN: 00204714) is published 22 times annually by Wells Media Group, Inc., 3570 Camino del Rio North, Suite 100, San Diego, CA 92108-1747. Periodicals Postage Paid at San Diego, CA and at additional mailing offices. SUBSCRIPTION RATES: $7.95 per copy, $12.95 per special issue copy, $195 per year in the U.S., $295 per year all other countries. DISCLAIMER: While the information in this publication is derived from sources believed reliable and is subject to reasonable care in preparation and editing, it is not intended to be legal, accounting, tax, technical or other professional advice. Readers are advised to consult competent professionals for application to their particular situation. Copyright 202 Wells Media Group, Inc. All Rights Reserved. Content may not be photocopied, reproduced or redistributed without written permission. Insurance Journal is a publication of Wells Media Group, Inc.

‘More than a quarter of the United States, including a large patch of the Upper Midwest, will face days with temperatures above 125 degrees and will see almost three times as many days above 103 degrees.’

Turning Up the Heat My home base is in Austin, Texas, and anyone who lives here knows — it’s been an excruciatingly hot and dry summer. Nearly the entire state of Texas is experiencing a severe level of drought — the worst since 2011. And while the state is finally receiving much needed rainfall in late August, it won't be enough to replenish our valuable water

“Across the country, dangerous days — days exceeding the 100°F threshold from the National Weather Service — occur more commonly in the southern half of contiguous United States and impact a greater number of properties in Florida and Texas,” First Street said. “Since warmer air has a higher capacity to hold water, increasing evaporation will result in more humid conditions. Increased average temperatures and humidity have a compounding effect on heat indexes, which make health impacts more likely.”The6th Annual National Risk Assessment report, based on government weather data, third-party data, and computer modeling, found extreme heat will likely be concentrated in some unexpected places. Although parts of the Deep South and Southwest have long felt the heat, the 125-degree days will be seen as far north as Illinois, Indiana, Iowa and Wisconsin. Parts of the Eastern Seaboard, including counties in North Carolina, South Carolina and Virginia, will also experience superheated summer days.

Chairman of the Board Mark Wells | mwells@wellsmedia.com Chief Executive Officer Joshua Carlson | jcarlson@insurancejournal.com ADMINISTRATION / CIRCULATION Chief Financial Officer Mark Wooster | mwooster@wellsmedia.com Circulation Manager Elizabeth Duffy | eduffy@wellsmedia.com Staff Accountant Sarah Kersbergen | skersbergen@wellsmedia.com V.P.EDITORIALofContent Andrea Wells | awells@insurancejournal.com National Editor Chad Hemenway | chemenway@insurancejournal.com Southeast Editor William Rabb | wrabb@insurancejournal.com South Central Editor/Midwest Editor Ezra Amacher | eamacher@insurancejournal.com West Editor Don Jergler | djergler@insurancejournal.com International Editor L.S. Howard | lhoward@insurancejournal.com Assistant Editor Jahna Jacobson | jjacobson@insurancejournal.com Columnists & Contributors Contributors: Steven Earley, Amy Hieatt, Karen Lopez, Jim Sams, Andrew G. Simpson, Kurtis Suhs Columnists: Mary Newgard, Catherine Oak, Barry Rabkin SALES / MARKETING Chief Marketing Officer Julie Tinney | jtinney@insurancejournal.com West Sales Dena Kaplan | dkaplan@insurancejournal.com Romeo Valdez | rvaldez@insurancejournal.com Kelly DeLaMora | kdelamora@wellsmedia.com South Central Sales Mindy Trammell | mtrammell@insurancejournal.com Southeast and East Sales (except for NY, PA, CT) Howard Simkin | hsimkin@insurancejournal.com Midwest Sales Lisa Whalen | (800) 897-9965 x180 East Sales (NY, PA and CT only) Dave Molchan | (800) 897-9965 x145 Advertising Coordinator Erin Burns | eburns@insurancejournal.com Insurance Markets Manager Kristine Honey | khoney@insurancejournal.com Sr. Sales & Marketing Coordinator Laura Roy | lroy@insurancejournal.com Marketing Administrator Alberto Vazquez | avazquez@insurancejournal.com Marketing Director Derence Walk | dwalk@insurancejournal.com DESIGN / WEB / VIDEO V.P. of Design Guy Boccia | gboccia@insurancejournal.com Web Team Lead Josh Whitlow | jwhitlow@insurancejournal.com Ad Ops Specialist Jeff Cardrant | jcardrant@insurancejournal.com Web Developer Terrance Woest | twoest@wellsmedia.com Web Developer Jason Chipp | jchipp@wellsmedia.com V.P. of New Media Bobbie Dodge | bdodge@insurancejournal.com Videographer/Editor Ashley Waldrop | awaldrop@insurancejournal.com ACADEMY OF INSURANCE Director Patrick Wraight | pwraight@ijacademy.com Online Training Coordinator George Jack | gjack@ijacademy.com

The more persistent and more extreme temperatures will have impact everything from health, to wildlife, to electricity costs, to infrastructure and public transport, the report noted.

POSTMASTER: Send Circulation PO Box Northbrook, IL

ARTICLE REPRINTS: Contact (800) 897-9965 x125 or visit insurancejournal.com/reprints

change of address form to Insurance Journal,

60065-9967

Highersupply.temperatures and dwindling water supply might be something we’ll have to get used to. According to a recent study by First Street Foundation, in just 30 years, more than a quarter of the U.S., including a large patch of the Upper Midwest, will face days with temperatures above 125 degrees and will see nearly three times as many days above 103 degrees. After experiencing more than 50 days of triple-digit temperatures in 2022 so far, the thought of that number tripling is quite unsettling.

708,

Dept,

First Street Foundation, which in recent years has analyzed data to show flooding impacts and wildfire risk due to climate change, predicted in its study that the Miami area will feel the most severe shift in temperatures in coming years. Miami-Dade County, which already experiences at least seven days at 103 degrees or higher, will see 34 such days, classified as “dangerous days” by the group.

WHEN YOU KNOW JUST HOW AN INDUSTRY TICKS, YOU CAN DO MORE TO PROTECT IT. TheHartford.com We make it our business to know the business of healthcare. That specialization translates to exceptional service. With expertise in underwriting, risk engineering and claims, we help develop customized product solutions that mitigate risk for mid- to large-size businesses across many industries. The Buck’s Got Your Back.® The Hartford® is The Hartford Financial Services Group, Inc. and its property and casualty subsidiaries, including Hartford Fire Insurance Company. Its headquarters is in Hartford, CT. 21-ML-918201 © October 2021 The Hartford

Client-focused. Performance-driven. Future-oriented. amwins.com We prize expertise and relationships equally - creating partnerships that deliver and last. With Amwins by your side, you not only get the best opportunities and data-driven insights, you get a direct extension of your team. Your challenges are our privilege. And when you win, we all win. Finding solutions together. 12 countries $26.4B annual premium placements 155+ offices

Projections: A Forward View, was pre sented during an exclusive members only webinar.Michel Léonard, chief economist and data scientist at Triple-I, discussed key macroeconomic trends impacting the property/casualty industry results includ ing underlying growth and replacement costs.Léonard noted insurance growth continues to be constrained by economic fundamentals, with replacement cost increases at multiples of pre-COVID levels and subpar underlying growth.

“P&C underlying growth of 0.35%, while more resilient than the economy’s -0.93%, are both down year-over-year and year to date,” Léonard said, noting that it is too early to determine whether improvements in used auto and construction materials prices are sustainable.

On personal auto, Porfilio said that the 2022 net combined ratio is forecast to be 105.2, 3.8 points higher than 2021, driven primarily by significant deterioration in auto physical damage coverages.

Dave Moore, president of Moore Actuarial Consulting, said the 2022 com bined ratio for commercial auto is forecast to be “W101.4.eareforecasting underwriting losses for 2022 through 2024 due to prior year development and the impact of inflation — both social inflation and economic inflation,” Moore said.

“We would like to see at least another quarter of improvements before fully factoring their impact into homeowners, commercial property, and auto insurance replacement costs,” Léonard said.

Dale Porfilio, chief insurance officer at Triple-I, discussed the overall P&C industry underwriting projections.

Looking at the workers’ compensation line, Kurtz noted that the line’s multi-year run of underwriting profits is expected to continue, although margins are expected to shrink further through 2024.

P/C

The 2022 combined ratio for the prop erty/casualty insurance industry is forecast to be 100.7, a worsening of 1.2 points relative to 2021, driven by significant deterioration in the personal auto line. Loss pressures and a hard P/C market are expected to continue due to inflation, supply chain disruptions, and geopolitical risk, according to the latest underwriting projections by actuaries at the Insurance Information Institute (Triple-I) and Milliman.Thequarterly report, Insurance Information Institute (Triple-I) /Milliman Insurance Economics and Underwriting

“For personal auto in total, quarterly direct loss ratios deteriorated rapidly from the pandemic low of 47.5% for Q2 2020 to an average of 72.8% for the most recent three quarters of Q3 2021 to Q1 2022. Recent deterioration has been driven by physical damage coverages, with an average direct loss ratio of 78.6% in the most recent three quarters being the worst in two decades,” he said.

“Underwriting losses are expected to continue as more rate increases are needed to offset economic and social inflation loss pressures,” Kurtz said. For the commercial property line, the industry is seeing strong premium growth and rate increases should help to alleviate some of the pressure from catastrophe losses, he added.

News Markets

Underwriting Profitability to Worsen as Inflation, Hard Market Persist

Jason B. Kurtz, a principal and consult ing actuary at Milliman, said that another year of underwriting losses are likely for the commercial multi-peril line.

&

10 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM

“We forecast 2022 premium growth of 8.5%, lower than the 9.2% growth in 2021, but still strong due to the economic recov ery and a hard market,” Porfilio said. He added that while 2022 catastrophe losses were lower in the first half than in 20202021, they were higher than 2018-2019.

Powering your possible.

Thomas Gmelich

Face masks also make it harder for defense attorneys to “read” the jurors reaction to testimony, said Kathryn “Kamil” Canale, who is also a partner with the Bradley law firm. She said COVID precautions have also forced the defense to use virtual witnesses who testify via videotape. Canale said video testimony doesn’t resonate with jurors.Video depositions present their own problems. Often the defense attorney has to work against poor lighting or awkward angles. Gmelich said in one case, he received a deposition where the witness’ chin was prominently displayed, but obscured the rest of her face. Gmelich said plaintiff’s attorneys follow a predictable script: They try to get a defense witness to agree with a good safety rule. Then they try to get the witness to admit a rule wasn’t followed. He said defense attorneys need to carefully prepare for testimony before trial. Often the extra expense of a jury consultant is a good investment, he added.

At the same time, corporations have cre ated an impossibly high bar for themselves by constantly communicating their dedi cation to protect public safety, he said. If a plaintiff’s attorney presents evidence that any safety rule has been violated — even a rule that is not relevant to the case — jurors may react with exaggerated outrage. Safety measures imposed in court rooms to protect potential jurors from infection have also tilted jury pools toward people who believe in following rules, a personality trait that generally disfavors the defense, Gmelich said. People who dislike masking and strict social distancing rules tend to evade jury duty, leaving only the more fastidious citizens left to serve. Defense attorneys have another common bias to overcome. “Jurors distrust corporations,” said panelist Anne Marie Stoerck, a claim consultant for CNA Insurance. Stoerck said her job duties include sitting through trials and writing daily reports. She said her observations have made her a proponent of using mock juries to test out various arguments before a case goes to trial. They can be expensive, but are often worth the investment, she said. Stoerck said courtroom COVID rules can also make it more difficult for defense attorneys to present their case. She said in one recent trail, she noticed that the plain tiff’s attorneys wore mics so they could be heard through their face masks that are still required in Los Angeles County.

12 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM

Gmelich said the plaintiff’s bar has honed the skill of inciting jurors’ survival instincts, often called the “reptile brain,” to generate anger toward defendants and inflate verdicts. He said the COVID-19 pandemic has made jurors more mindful of public safety and more concerned about their own health, economic security and employ ment prospects.

‘I think COVID and the orga nization of the plaintiff’s bar has caused jurors to be desensitized to high verdicts and the value of money.’

In cases where there is clearly some liability, defense attorneys should offer the jury a potential amount of damages early in the trial to serve as an “anchor” that can counter the plaintiff’s overzealous demands. “If no anchor is given, the jury is left with just a crazy number and zero,” Gmelich said. Sams is the editor of ClaimsJournal.com, a sister publication to Insurance Journal.

News & Markets

COVID Impacts Linger in Courtrooms, Often a Disadvantage for

Defendants

By Jim Sams Courts have reopened and trials have resumed, but the impacts of COVID-19 continue to linger in the judicial system, a panel of claims litigation experts said during the Combined Claims Conference last month.

For one thing, jurors are far more sympathetic to plaintiffs if there is any indication that safety rules have been ignored, said Thomas P. Gmelich, a partner with the Bradley Gmelich + Wellerstein law firm in Glendale, California.

“I think COVID and the organization of the plaintiff’s bar has caused jurors to be desensitized to high verdicts and the value of money,” he said during a presentation on litigation trends as society emerges from the pandemic. “The numbers are crazy.”

We’ll cover just about anything on earth. And cyberspace too. Conventional to complicated. Traditional to atypical. No matter the complexity, we’ve got you burnsandwilcox.comcovered.

The average premium increase across all lines of commercial business during Q2 was 6.1%, compared with 5.7% during Q1 2022.Asin recent quarters parts, cyber insur ance led the way with average Q2 premium increases of 26.8%. Cyber insurance buyers have seen average premium increases of of more than 25% for five straight quarters. Demand continues to be very strong for cyber insurance, with 85% of respondents noting they had seen an increase, said CIAB.The only other line with a double-digit with no rate relief. In wildfire ainfmiumsquartersseenauto,place.businessrespondentsareas,saidinhardtoIncommercialwhichhas44consecutiveofpreincreases,lationwasalsofactor.Theprice of goods are up in general and inflation is pushing up loss and administrative costs, resulting in higher claims and subsequent pricing pressure. Looking at account sizes, large accounts saw average premiums increase 7.5% compared with 6.2% during Q1. Small and medium accounts held stead at 6.4% and 7.3%, respectively.

And as a Travelers company, our A++ rating* for financial strength and stability provides confidence and security – a difference few other carriers can match.

Head north.

Northfield offers coverage for hard-to-place business through our appointed Excess & Surplus Lines wholesalers. We provide the advantages that make a difference in quoting new business and winning it.

Nothing stated herein affects the terms, conditions and coverages of any insurance policy issued by Northfield or its affiliates, nor does it imply that coverage does or does not exist for any particular claim or type of claim under any such policy. The information in this document is provided for general informational purposes and does not constitute an offer to sell or a solicitation. The information is for surplus lines licensees only. Advertising of surplus lines products may be restricted by state law; surplus lines licensees are responsible for compliance with all such laws. Northfield is a U.S. based surplus lines insurer, operating in all states except IA, MA and MO. State law requires notification that Northfield is not licensed in California or New York.

For over 40 years, NORTHFIELD, a Travelers company, has been a home to businesses that don’t fit into the standard lines marketplace.

Visit us northfieldinstoday..com

average 7.2%8.3%,premiumsQ2autoandtorsproperty,CommercialumbrellaQ2increasepremiuminwas(11.3%).direcandofficers,commercialfinishedwithaverageup7.9%,andrespectively.Inflationwasoften

Q2 Commercial P/C Premiums Up 6.1%: CIAB

Hard-to-place business?

14 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM News & Markets LINESSURPLUS&EXCESS

© 2021 The Travelers Indemnity Company. All rights reserved. BNFAD.000B-P Rev. 10-21 * A.M. Best’s rating of A++ applies to certain insurance subsidiaries of Travelers that are members of the Travelers Insurance Companies pool; other subsidiaries are included in another rating pool or are separately rated. For a listing of companies rated by A.M. Best and other rating services, visit travelers.com. Ratings listed herein are current, are used with permission, and are subject to changes by the rating services. For the latest rating, access ambest.com

cited as a driver of recent premium trends in the marketplace, according to the report. Inflation continues to increase property valuations in com mercial property and, according to respon dents, businesses in areas prone to natural catastrophes are seeing high deductibles

The second quarter 2022 marked a full five years of premium increases for across all lines of commercial insurance business, according to the latest report from the Council of Insurance Agents and Brokers (CIAB).

$310,000

Degrees125That’sthetemperature,Fahrenheit,thatmorethanaquarteroftheUnitedStateswillexperienceonsomedaysinthesummerintheyear2053,accordingtoastudybyFirstStreetFoundation.Afewcountiesnowfeelthattemperature,buthundredsofcountiesasfarnorthasWisconsinandIllinoiswillbakeintheextremeheatincomingdecades,thankstoclimatechange,thereportsaid.

Figures

The amount a Texas wood crate and pallet manufacturer was fined by the Occupational Safety and Health Administration (OSHA) for workplace safety violations. OSHA found in a February 2022 inspection that Jacksonville-based M&H Crates Inc. exposed workers to amputation hazards. OSHA determined the company failed to develop, docu ment or use lockout/tagout procedures to prevent sudden machine start-ups. They also said M&H Crates failed to ensure required machine guarding, exposing workers to hazards, including $249,000amputation.

39That’showmanycountsofinsurancefraudBrandenHeywood,30,ofChino,California,wasarraignedonafteraninvestigationfoundheallegedlyactedastheleaderofa“papercollision”ringtocollectmorethan$80,000ininsurancepayouts.“Papercollision”accidentsneveroccur;theperpetratorsusefalsedocumentstocommitfraud.TheamountanIndianametalworkinglubricantscompanyagreedtopaytosettleallegedClearAirActviolations.Inacomplaint,theEnvironmentalProtectionAgencyandtheIndianaDepartmentofEnvironmentalManagementsaidMetalworkingLubricantsemittedmorethan25tonsofhazardousairpollutantsperyear,includingnaphthalene,ethylbenzene,xylene,phenol,andtoluene,inviolationofitsexistingpermit. Underthetermsofthesettlement,thecompanywillpayapenaltyof$155,000totheUnitedStatesand$155,000tothestateofIndiana.

Think again. By constantly looking at opportunities for growth, we’ve become a market-leading specialty insurance group. With over 100 years under our belt, we now have more business lines, more specialty products and more claims handling expertise than ever before. Let our specialists help navigate your business risks. There’s no better time to discover what we can do for you. For smooth sailing, THINK HUDSON. Rated A by A.M. Best, FSC XV HudsonInsGroup.com MANAGEMENT FINANCIALPROFESSIONALLIABILITYLIABILITYINSTITUTIONS LIABILITY MEDICAL PROFESSIONAL LIABILITY PRIMARYTRUCKINGGENERAL LIABILITY & EXCESS LIABILITY GENERAL LIABILITY & PACKAGE PERSONAL UMBRELLA SPECIALTY LIABILITY SURETYCROP

“We were living in ashes. The kids were filthy constantly from that black ash. … We didn’t have any community left. All our friends had either moved to (nearby) Chico or … somewhere across the country. There was nothing left that we loved. There were no trees, no forest.”

“Never in my life have I seen anything quite like this.”

Sexual Harassment Suit

“Everyone deserves to feel safe at work and no one should be pushed out of her workplace by pervasive jokes about sexual violence.”

18 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM

“Siskiyou County residents have endured wildfire emergencies over the past three years and protecting their insurance is essential to recovery.”

Declarations

— Alexa Lang, a U.S. Equal Employment Opportunity Commission (EEOC) attorney, comments on allegations that SkyWest Airlines violated federal law by subjecting a female parts clerk to sexual harassment. In a lawsuit, EEOC alleges explicit sexual conversations and conduct were a daily feature of the work environment at the overwhelmingly male Parts and Maintenance Divisions of SkyWest’s Dallas operation. Multiple employees and at least one manager made crude sexual comments, including the suggestion that the female employee make money via prostitution, according to the EEOC.

— Grassroots Development sustainability consultant Sydney Glup on a one-of-a-kind construction and research project in Fargo, North Dakota, that uses hemp material to build a house. The walls of the experiment house are built with a raw material called hurd, which is the inner woody core of the hemp plant, chipped into small pieces. Hemp is touted as a healthier alternative to insulation, reducing mold by creating walls that breathe, providing excellent insulating properties and serving as thermal mass, storing heat. The material is also flame resistant.

— Ellie Holden describes the experiences she, her husband, James, and their family suffered after their house was reduced to ashes in the 2018 Paradise, California fire. Unable to find a home in the area for the family of seven, the Holdens looked farther afield for a place that, unlike California, did not seem under constant threat from wildfires, droughts and earthquakes. They found a new home in Vermont.

— California Insurance Commissioner Ricardo Lara in mid-August ordered insurers to preserve residential insurance coverage for 8,500 affected homes follow ing Gov. Gavin Newsom’s emergency declaration as wildfires in Siskiyou County threatened homeowners.

Hemp Homes “You blend the mixture to a consistency, a nice sort of chicken salad, is our joke, consistency.”

Captive Fraud?

— A captive insurance expert comments on alleged fraud schemes led by Ambassador Captive Solutions and its principals. Lawsuits by Lexington Insurance Co., State National Insurance and others allege that the principals forged insurance carriers’ signatures and created thousands of fake insurance policies for youth sports teams and others around the country, using offshore captive cells to provide reinsurance for the bogus policies.

No More Talc “As part of a worldwide portfolio assess ment, we have made the commercial deci sion to transition to an all cornstarch-based baby powder portfolio.”

— Johnson & Johnson said it will stop selling talcbased baby powder globally in 2023, more than two years after it ended U.S. sales of a product that drew thousands of consumer safety lawsuits. It added that cornstarch-based baby powder is already sold in countries around the world. The company faces about 38,000 lawsuits from consumers and their survivors claiming its talc products caused cancer due to contamination with asbestos, a known carcinogen. J&J denies the allegations.

Wildfire Emergencies

Living in Ashes

Philadelphia Insurance Companies is the marketing name for the property and casualty insurance operations of Philadelphia Consolidated Holding Corp., a member of Tokio Marine Group. All admitted coverages are written by Philadelphia Indemnity Insurance Company. Coverages are subject to actual policy language. CONTRACTING I ENVIRONMENTAL I EXCESS I HOSPITALITY I MANUFACTURING I REAL ESTATE I RETAIL Your Insurance package should sweeten your chances to succeed—freeing you to grow your business. PHLY Excess & Surplus Solutions offers excess protection for small niches like plumbing, taverns, machine shops, environmental contractors, commercial real estate, vacant properties, manufacturers, and flea markets. Even box makers. PHLY E&S Solutions. Neatly packaged to make a big difference, even in your small niche. GOT A NICHE? CALL 800.873.4552 I PHLY.COM EXCESS & SURPLUS PROTECTION. NOW IN NEAT LITTLE PACKAGES.

U.S. Food and Drug Administration food and beverage recall events increased to 120 in Q2, up 9.1% from Q1. However, the number of impacted units decreased significantly (81.3%) to 27.5 million units.

Highlights from the Q2 recall data: Automotive recall events increased in the second quarter 2022 to 245, following two consecutive quarters of decline.

For a second consecutive quarter, there were a total of 94 pharmaceutical recall events. The number of impacted units fell to their lowest level in over a year, at 20.6 million units in Q2.

The National Highway Traffic Safety Administration had an active Q2, finalizing several standards for fuel efficiency and increasing civil penalties — meaning the automotive industry may soon be liable for millions of dollars in fines.

Per- and polyfluoroalkyl substance (PFAS) chemicals are rising to the top of regulators’ and litigators’ list of harmful substances to target with regulations and lawsuits.Infantfood recalls continue to have a lasting impact on the food and beverage industry, as the FDA and other regula tory agencies examine the causes, poor response times and preventative measures. for food importers. As medical device technology advances, the FDA is releasing guidance to protect devices from cyberattacks. This space will likely remain a focus for the FDA, as will enforcement in the pharmaceutical industry.

insights into how companies can safeguard their reputations and brands.

20 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM News & Markets

U.S. Department of Agriculture food recalls increased to their highest level in more than two years, with 13 events.

While medical device recalls increased 34% (to a two-year high, with 268 events), the number of impacted units fell 96.8% to their lowest level in 10 years (10 million).

Record-Breaking Pace for U.S. Product Recalls, Says Sedgwick

The number of U.S. products recalled this year has already surpassed 1 billion, according to the U.S. product recall index released by Sedgwick’s brand protection division. Only two other years on record have seen more than 1 billion units recalled: 2018 and 2021. In those years, it took a full year to hit that threshold. In 2022, it only took seven months.“Thisis the second consecutive year in which we have seen more than 1 billion units impacted by U.S. product recalls. If the first half of the year is any indication, we should expect 2022 to eclipse all previous years on record for recalled products,” said Amanda Combs, recall advisor in Sedgwick’s brand protection division. “While regulatory agencies may not be back to pre-pandemic work levels, companies can’t relax their focus on product safety. Inspections enforcementandactions are stillindustriesconsumerTheoccurring.”automotive,product,foodandbeverage,medicaldeviceandpharmaceuticalcontinue

The number of consumer product recalls decreased 15.6% in Q2 from 77 events in Q1 to 65. The total number of units recalled also decreased in Q2, but by only 3.5% to 6.7 million units.

to face challenges from increased regulatory scrutiny, as well as geopolitical issues and ongoing public health issues, including COVID-19 and monkeypox. Sedgwick’s brand protection quarterly report provides an in-depth look at the economic, regulatory and legal challenges affecting various industries, as well as

Partner with Prime SPECIALTY LIABILITY SOLUTIONS, PRIMARY & EXCESS > Specialty Liability Solutions, Primary & Excess > Specialty Coverage offered in all 50 States, with same date quotes when needed > General Liability including Professional Liability & Completed Operations/Products > Directors & Officers Liability > Commercial Auto, including Trucking > Property Coverage > Risk Management & Superior Claims Results WITH US, YOU HAVE…. To learn more visit www.primeis.com Contact us at 1.800.257.5590 or info@primeis.com Prime Insurance Company (“PIC”) is an excess and surplus lines insurance company, which is domiciled in the State of Illinois and has its principal place of business in Sandy, UT. Full disclaimer at www.primeis.com/legal. Scan the QR code to learn more 40+ Years of Experience For latest ratings, access www.ambest.com

Jessica Snyder

Michael Smith

22 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM People all over North America, and serves as the agency’s cyber insurance practice leader. He began his career with Arthur Hall Insurance in 2014. Midwest Chicago-based Ryan Specialty appointed three to new senior leadership roles within the Underwriting Managers specialty.

East Arthur Hall Insurance named Dan Mackarevich a principal shareholder. He assumes the title of vice president.Mackarevich joins James Denham, Glenn Burcham, Mark Sammarone, Nicole Grebloskie, Josh Isler and Karen Leary as an agency partner and member of the managing leadership team of the West Chester, Pennsylvania, firm. Mackarevich advises clients consultant Alex Gibson joined Alliant Insurance Services as vice president in its employee benefits group. Gibson’s exper tise encompasses the areas of analytics, strategic planning, HR consulting, employee wellness, pharmacy benefit consulting, and compliance. Prior to joining Alliant, Gibson was an employee benefits consultant with a national insurance brokerage and consulting firm. He also is a musicGrammy-nominatedengineer,producer, and founder of a music production and management company.

South Central Steven Anderson joined the Safety National cyber insurance team as director of Cyber Underwriting. Anderson is based in the company’s Dallas office. With nearly 30 years of industry experience, Anderson has served in various underwriting and product leader positions at global cyber insurance carriers and, most recently, an insure-tech startup.Truist subsidiary McGriff, an insurance broker, announced that Doug Hodo will rejoin the firm as chief strategic growth officer, based in

nashipslargedirectorworkingtheHTexas.odospentpastyearasofrelationforationalbrokerage.

Brian Lillis, chief operating officer, has been with Ryan Specialty andManagersUnderwritingfornineyears,hasservedinvariety of operational, technology, M&A, and finance leadership roles, serving most recently as senior vice president. Eric Quinn, senior vice president, has been with Ryan Specialty Underwriting Managers for two years as vice president of Program Development. Chris Taggart, senior vice president –

National Argo Group International Holdings Ltd., an underwriter of appointedinsurance,specialty SnyderJessica U.S.president,asinsurance.Withalmost

HumanservingRyanDevelopment,OrganizationalhasbeenwithSpecialtyforeightyearsasvicepresident–Resources.

Previously he served more than 25 years at McGriff in Houston, most recently as president of the West Region. Southeast Michael Smith joined the Palomar Insurance Corp. sales team as an specializingexecutiveaccount ment.risktransportationinmanagePalomarInsuranceisheadquartered in Montgomery, Alabama, with offices in Georgia, Tennessee, and South Carolina. It offers programs for U.S. and interna tional companies. Smith has a background in transportation risk management and is involved in trucking associations in four Southern states.

30 years of industry experience, Snyder joins Argo from GuideOne Insurance where she most recently served as its president and chief executive officer from 2017 through 2022. Prior to GuideOne, Snyder served as senior vice president of commercial and specialty lines at State Auto Insurance. Doug Kovach joined Concert Insurance as senior vice president, underwriting and program management. Kovach has over 30 years of experience in the insurance and reinsurance industries. He joins Concert after 10 years at American Family Insurance Co. Kovach also served in senior underwriting roles placing commercial accounts for national brokers, including Brown & Brown, Willis and Aon.

Greg Delleney, former assistant captives director at the South Carolina Department of Insurance, joined the capital management firm, Risk Partners, as captive account manager.Delleney began working for the SCDOI in 2010. Most recently, he was chief financial analyst and assistant director of captives in the Financial Regulation and Solvency division, according to Captive InsuranceOrlandoTimes.,Florida-based Doug Hodo

West Nevada-based Outsource Insurance Professionals announced senior leadership changes. Martina Seferovic takes over as president and CEO. Prior to this role, Seferovic was the managing director for the past five years. Milos Petrovic becomes chief operating officer. Snezana Obradovic was named chief financial officer. The global knowledge process outsourcing company (KPO) is headquartered in Nevada, with locations in Arizona, Croatia and Serbia, and client throughoutpartnershipstheU.S.,UK and Canada. Alliant ConsultingRetirement , a division of Alliant Insurance Services, hired Kathy Aicher as vice president in its Los Angeles office.Aicher has experience designing and delivering retirement programs. Aicher was previously a partner and senior retirement consultant.

Local expertise with global capabilities. Coverages are underwritten by the following insurance company subsidiaries of Intact Insurance Group USA, LLC: Atlantic Specialty Insurance Company, Homeland Insurance Company of New York, Homeland Insurance Company of Delaware, OBI America Insurance Company, OBI National Insurance Company, located in Plymouth, MN, or The Guarantee Company of North America USA, located in Southfield, MI. With our deep product and industry expertise spanning more than 20 specialized segments, we deliver global solutions to address the unique risks you face. Our inland marine experts have a comprehensive understanding of your construction, transportation, fine arts business and more. Let us tailor a solution for your specialized insurance needs. To learn more, talk to your broker or visit intactspecialty.com

News & Markets

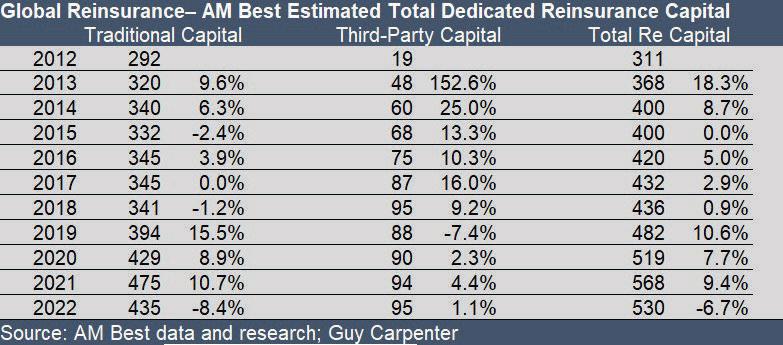

The report explained the 10.7% jump in traditional reinsurance capital in 2021 highlighting substantially improved underwriting returns and strong equity market growth fueling the increase in shareholders equity of reinsurance market participants. In fact, AM Best’s Global Reinsurance Composite reported its lowest combined ratio in five years in 2021 — 96.4 — and equity values soared 17% for the group.The biggest year-over-year jump in capital recorded in the AM Best report was a 15.5% increase in 2019. AM Best’s 2020 report on capital levels explained that even though most reinsurers were underwriting at, or just above, breakeven in 2019, the vast majority of companies had been adversely impacted by mark-to-market unrealized losses from both fixed-income securities and equity holdings toward the end of 2018, which reversed in 2019.

AM Best’s estimate of traditional reinsurance capacity takes into account the allocations by business classification.

Overall, elevated catastrophe losses have been characterized as “earnings events” rather than capital depleting ones in recent years, the report says, noting that many reinsurers’ underwriting returns have been close to breakeven but that capital grew through investment gains and the ability to access affordable debt financing.

AM Best estimates that traditional reinsurance capital will drop by roughly $40 billion to $435 billion at year-end 2022, after hefty jumps recorded in each of the prior three years.

This article first was published in Insurance Journal’s sister publication, Carrier Management.

24 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM

AM Best is also considering continued geopolitical turmoil and a potential decline in global GDP for the forecast, the rating agency said in a report, “Dedicated Reinsurance Capital Growth of 2021 May Not Continue.”

The AM Best report also includes a decade-long record of third-party reinsur ance capital levels and a projection that third-party capital overall will stay steady at about $95 billion for 2022, compared to $94 billion in 2021. Even though the downturn in the U.S. equity market has presented capital supply challenges for some insurance-linked securities funds, AM Best says the pullback of traditional reinsurance in catastro phe-exposed markets such as Florida may be creating opportunities for ILS funds.

“With interest rates on the rise and equity markets declining, we do anticipate a rather substantial mark-to-market loss in traditional reinsurance capital levels,” Dan Hofmeister, senior financial analyst, AM Best, said in a video accompanying the report on the AM Best website. Working in the opposite direction, reinsurance capital has been boosted by underwriting results in spite of heightened cat loss activity in the first half of the year, he said. As hurricane season plays out, “if we do see a reversal in these underwriting trends, it could prove to be very problematic for the industry’s capital levels,” he said.

“Since year-end 2018, our estimate has been less than 60% of total shareholders’ equity of the consolidated figures for groups identifying as reinsurance writers,” the report says. A Bit of History

AM Best works in conjunction with Guy Carpenter to estimate the total amount of capital supporting the reinsurance industry. AM Best determines traditional reinsurance capital; Guy Carpenter deter mines third-party capital.

The projected 8.4% decline to $435 billion for 2022 from $475 billion in 2021, following increases of 15.5% for 2019, 8.9% for 2020 and 10.7% in 2021, takes into account both the tailwinds of the under writing market and the headwinds of the capital and investment markets.

The report notes that pure reinsurers with a global reach are rare, necessitating an “incisive analysis” on AM Best’s part to present an accurate picture of capital backing the reinsurance market. Global reinsurers are typically also engaged in businesses such as specialty insurance and large commercial, for example.

Where traditional capacity is lacking, ILS funds can take advantage of significant price increases and tighter terms and conditions, the report says. Putting traditional and third-party capital together, AM Best is estimating a 6.7% drop in reinsurance capital from both sources — the first drop in a decade of figures compiled by the rating agency.

Reinsurance

Capital to Drop $40 Billion at Year-End 2022: AM Best

While the report notes that many reinsurers substantially decreased property exposure through the last renewal cycle, some are still exposed to material amounts of multiyear reinsurance contracts. Those reinsurers that did not manage risk exposures prudently could be exposed to material capital deterioration, AM Best said, referring to a double-whammy of underwriting losses and adverse invest ment market returns in 2022.

Company. All rights reserved. We

UFG Specialty is a growing company with an appetite to match. Whether it’s building partnerships or providing excellent service in the evolving excess and surplus marketplace, we adapt to meet our brokers where they need us most. We pride ourselves on being a responsive carrier that provides innovative solutions for complex risks. At UFG Specialty, we want your tough accounts. For more information, visit ufgspecialty.com. Casualty want your tough accounts.

© 2022 United Fire &

Puttingmarkel.com customersourfirst. In an ever-changing world, it’s hard to plan for all of life’s uncertainties. At Markel, we specialize in understanding the unique needs of our customers and providing innovative insurance solutions.

Former Washington State Coach Files Wrongful Termination Claim

Former Washington State football coach Nick Rolovich has filed a claim against the university seeking $25 million for wrongful termination after he was fired last year for refusing to get vaccinated against COVID-19. The claim was filed on Rolovich’s behalf with the state’s Office of Risk Management on April 27. Such a claim is a prerequisite for filing a lawsuit against a state agency, said Brionna Aho, spokesperson for state Attorney General Bob Ferguson. A person must wait 60 days to sue after a tort claim is Rolovich’sfiled.attorney, Brian Fahling of Kenmore, did not return a telephone message left at his office. He has previously indicated Rolovich would take legal action, claiming religious discrimination.Rolovich,who is Catholic, was denied a religious exemption from Gov. Jay Inslee’s mandate requiring state employees to get the vaccine. He was fired in October after he had coached just 11 games with the Cougars over two seasons, going 5-6. Assistant coach Jake Dickert was temporarily ele vated to interim head coach and then was named replacementRolovich’safter leading the Cougars to the Sun FahlingBowl.filed a 34-page letter with the university appealing Rolovich’s firing in November. That appeal was denied. At the time of his firing, Rolovich was working under a five-year contract, on which three seasons remained. He was paid $3.2 million per year, the highest public salary in the state.

W2 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM 2022 JM Wilson INS Journal OUTLINES.indd 1 12/6/21 1:11 PM

Copyright 2022 Associated Press. All rights reserved.

News & Markets

Francis Okyere, 70, a previously licensed insurance agent in Westlake Village, California, was arrested in relation to a scheme that involved him allegedly stealing multiple victims’ identities and using them to open a fraudulent insurance agency. The victims’ identities were also reportedly used on small business loan applications to fund the agency, known as Cyber Access Insurance Agency.

Former California Insurance Agent Arrested for Theft,

W4 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM Contact us for a quote today: Matt 916.780.7000Matt_Abram@RPSins.comAbram High value, high risk, and hard to place? We have the experts for your Umbrella and Excess risks. © 2022 Risk Placement Services, Inc. RPS43055

The California Department of Insurance began an investigation after a complaint from one of Okyere’s ex-relatives, who alleged he had stolen the identities of several people to open a new insurance agency. The CDI’s reportedlyinvestigationconfirmed that Okyere stole the identities of four victims to open Cyber Access Insurance Agency.

Operating Fraudulent Agency

Okyere’s bail was set at $815,000 and Freeman’s bail is set at $100,000. The case is being prosecuted by the Healthcare Fraud Division of the Los Angeles County District Attorney’s Office.

News & Markets

The department’s investigation discov ered Okyere had also applied for a series of Small Business Administration and Paycheck Protection Program loans, the federal program to help businesses during the COVID-19 pandemic. The documents related to those loans reportedly showed two of the same stolen victims’ identities had been used to fraudulently secure loan funds for $38,963. Okyere used the same stolen identities when he applied for forgiveness of one of the loans. This is the second time fraud accusa tions have been brought against Okyere, who has previously been convicted of grand theft following another CDI inves tigation, which found he stole $65,186 in insurance premiums from small business owners. The department ordered Okyere to surrender his license in 2019 and he is pending sentencing in that matter.

Okyere was charged with 17 felony counts including identity theft and grand theft by false pretenses. Okyere’s alleged accomplice, Holly Freeman, 40, was also arrested and charged with four counts of felony identity theft for her alleged involvement in the same scheme.

$18M Settlement in Lawsuit over Boy’s Death at California School

District officials didn’t immediately return a call seeking comment on the settlement.Thefamily filed the lawsuit in Los Angeles County Superior Court in 2018. Copyright 2022 Associated Press. All rights reserved.

Theentsparof an 8-yearold boy with Down syndrome who died after falling strappedwhileto a chair in class five years ago have reached an $18 million settlement in their wrongful death lawsuit against a Southern California school district, attor neys said. Lawyers for the family of Moises Murrillo announced the deal during a news conference in the city of La Puente, east of Los Angeles, where he attended Sunset Elementary School. Moises was unsupervised on May 31, 2017 when he fell backwards, striking his head on the floor and fracturing his neck, according to the lawsuit brought by Martin Murrillo and Roberta Gomez. The boy had been taken out of his special adaptive stroller by staff and strapped to a school chair, the lawsuit stated. He went into cardiac arrest and was taken to a hospital, where he died on June 4, 2017 of spinal cord trauma, the court filing said.

News Markets

&

AM Best Places Credit Ratings of American Reliable in Arizona Under Review AM Best has placed under review with negative implications the Financial Strength Rating (FSR) of A (Excellent) and the Long-Term Issuer Credit Rating (Long-Term ICR) of “a” (Excellent) of American Reliable Insurance Co. in Scottsdale, Arizona. American Reliable is a member of Global Indemnity Group LLC. The actions follow the recent announcement that ARIC completed the disposition of its farm, ranch and equine book of renewal business to Everett Cash Mutual Insurance Co. Global Indemnity also announced that it agreed to sell ARIC to ECM. Under the proposed agreement, Global Indemnity will receive roughly $85 million, including the release of capital currently supporting ARIC’s operations. Until ECM acquires ARIC, ECM will be providing Global Indemnity with 100% quota share reinsurance subject to the renewal rights agreement with ECM. The sale of ARIC is expected to close sometime in the first quarter of 2023 and is subject to customary regulatory approvals, according to AM Best.After the deal closes, ARIC will no longer be part of Global Indemnity and will no longer be a member of Global Indemnity’s intercompany pooling agreement, from which its ratings are derived. The under review with negative implications status reflects the antici pated removal of the group rating and the anticipated transfer of risk to ECM from Global Indemnity, according to AM Best.

In addition, the lawsuit said, the district did not have a policy in place to adequately supervise students with spe cial needs like Moises inside and outside of their classrooms.

W6 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM

Hacienda La Puente Unified School District “failed to provide safe surround ings” and allowed the vulnerable boy “to be unsupervised and unrestrained during his class,” the filing alleged.

W8 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM

In May, Walgreens reached a $683 million settlement with the state of Florida in a lawsuit accusing the company of improperly dispensing millions of painkillers that contributed to the opioid crisis.The company also faces litigation in Alabama, Michigan and New Mexico, among other states.

News &

A Walgreens spokesman said the chain is disappointed in the outcome, which he said is not supported by the facts and the law.“As we have said throughout this pro cess, we never manufactured or marketed opioids, nor did we distribute them to the ‘pill mills’ and internet pharmacies that fueled this crisis,” spokesman Fraser Engerman said in a statement. “The plaintiff’s attempt to resolve the opioid crisis with an unprecedented expansion of public nuisance law is misguided and unsustainable. We look forward to the opportunity to address these issues on appeal.”Several drug manufacturers and pharmacies opted to settle with the city previously as part of the case, including opioid makers Allergan and Teva, which agreed to pay $54 million on the eve of closing arguments in the trial, leaving Walgreens as the sole defendant.

Associated Press writer Tom Murphy in Indianapolis contributed to this story. Copyright 2022 Associated Press. All rights reserved. Markets

Judge Rules Walgreens Contributed to San Francisco’s Opioid Crisis

The ruling did not include a ruling on monetary damages, which will be determined in a future trial. Drug overdose deaths have surged in the country, including in San Francisco. Mayor London Breed declared a state of emergency last year in the Tenderloin neighborhood, saying something had to be done about the high concentration of drug dealers and people consuming drugs in public.Thecity attorney’s office says San Francisco saw a nearly 500% increase in opioid-related overdose deaths between 2015 and 2020 and that on a typical day, roughly a quarter of visits at the Zuckerberg San Francisco General Hospital Emergency Department are opioid-related.

“Pharmacists were pressured to fill, fill, fill,” he said, “and as a result, Walgreens filled our streets with opioids.”

Deerfield, Illinois-based Walgreens Boots Alliance Inc. runs a network of around 9,000 drugstores in the United States. Walgreens and other prescription drug distributors have faced a slew of lawsuits over the opioid crisis.

Afederal judge ruled in mid-August that Walgreens can be held responsible for contributing to San Francisco’s opioid crisis for over-dis pensing opioids for years without proper oversight and failing to identify and report suspicious orders as required by law.

By Juliet Williams

U.S. District Judge Charles Breyer ruled that for 15 years, Walgreens dispensed hundreds of thousands of pills, eventually contributing to the city’s hospitals being overwhelmed with opioid patients, libraries being forced to close because of syringe-clogged toilets, and syringes littering children’s playgrounds in San Francisco.

San Francisco City Attorney David Chiu said the pharmacy chain “continually violated what they were required to do under the federal Controlled Substances Act,” failing to track opioid prescriptions, preventing pharmacists from vetting prescriptions and “nor did they see the many red flags of physicians and others who were dramatically over-prescribing.”

SEPTEMBER 5, 2022 INSURANCE JOURNAL | 27

INSURANCEJOURNAL.COM

Based in the Dorchester neighborhood of Boston, Lighthouse specializes in personal and commercial insurance for transportation risks with a focus on livery and taxis. The agency also offers personal auto, homeowners and umbrellas, as well as coverages for small businesses, restaurants and contractors.

South Central Truist, BenefitMall Charlotte-based Truist Insurance Holdings has agreed to acquire Dallasheadquartered BenefitMall, a wholesale

Richmond, Virginia-based Hilb Group is a portfolio company of The Carlyle Group, a global investment firm.

National Applied Systems, Tarmika Applied Systems acquired Tarmika, a commercial lines rating solution that streamlines small business insurance. Tarmika will be integrated with Applied Epic and EZLynx. Over time, users can expect embedded commercial lines quoting capabilities powered by Tarmika natively in the management systems. Additionally, Tarmika’s panel of commer cial lines products will be integrated into Ivans Distribution Platform to streamline the submission process through standard ized digital connections to agency-facing systems.Recently, Pie Insurance, an insurtech company specializing in workers’ comp insurance for small businesses, announced a strategic partnership with Tarmika. East Hub Buys Delaware’s KT&D Insurance broker Hub International Limited has acquired KT&D Inc. in Wilmington, Delaware.

Midwest Inszone, First Bosnian Inszone Insurance Services acquired First Bosnian Insurance, its second acquisi tion in the state of Missouri.

KT&D provides multi-line insurance services, including medical malpractice, commercial and personal, and employee benefits coverage. Scott Yerkes, CEO, and Kelly McGovern, president, and the KT&D team will join Hub Mid-Atlantic.

Steven Oakes is president and Ed Timmerman is sales manager. Eastern Insurance Group, headquartered in Natick, Massachusetts, is a subsidiary of Eastern Bank and is licensed to do business in every state, Hilb Group, Lighthouse The Hilb Group acquired Massachusettsbased Lighthouse Insurance Agency.

Cross Insurance, Maine Insurance Agency Cross Insurance racquired Maine Insurance Agency of Portland. The acquisition of Maine Insurance Agency, a fifth-generation family-owned business, expands the coastal region division of Cross.Founded in 1905, Maine Insurance Agency offers insurance for homes, autos, recreational products and small businesses. The agency’s two offices in Portland and Gray will be rebranded under the Cross Insurance name. Cross said it will retain Jeff Steinman, president and CEO, and all personnel affiliated with the agency.Dave Messersmith, president of Cross Insurance-Coastal Region, said the firm plans to continue to expand in the coastal region. Cross acquired three Massachusetts agencies this year: Northern Benefits, Harold Humphrey Agency and Byfield Agency. Cross also opened a Newburyport, Mass,. branch office, further bolstering its presence in the coastal market.

Eastern Insurance, Burns Agency Eastern Insurance Group has acquired the John T. Burns Insurance Agency in Newton, Massachusetts. Family-owned since 1892, Burns Insurance offers personal auto and home insurance from carriers including Arbella, Safety, Plymouth Rock, Hanover, Quincy Mutual and Vermont Mutual. It also offers business and professional lines coverages and life insurance.

First Bosnian Insurance opened in 2005 with the goal of helping the growing com munity of Balkan and Eastern European people coming to America.

Ibrahim Vajzovic and his wife Fazira were able to provide information and coverage to a vastly underserved commu nity that wanted assistance from a native Bosnian speaker. As the community grew, many businesses and commercial truckers were emerging, and First Bosnian Insurance was able to be at the forefront of supporting their insurance needs.

Maine-based Cross owns more than 120 insurance agencies throughout the Northeast and has employees in Maine, New Hampshire, Vermont, Rhode Island, Massachusetts, Connecticut, New York and Florida.

Agency principal Brian Boucher and his staff will join Hilb Group’s New England regional operations and Hilb Group’s transportation practice.

Business Moves continued on page 28

28 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM

Virtus was founded in 2013. Andrew Gray is CEO. Kemmons Wilson was formed in 1952 to insure Kemmons Wilson’s hotel properties. It is now a full-service agency focused on the hospitality sector. Higginbotham, Holman Higginbotham, a Texas-based indepen dent insurance and human resources firm, acquired Georgia-headquartered Holman and Co., a commercial and personal lines property/casualty insurance and benefits broker.Holman and Co., founded in 1983, is based in Alpharetta. It is led by Bill Holman with his brothers Alan Holman and Bob Holman, who purchased the agency from their father, Penn Holman, in 2021. Holman and Co. serves mid-sized companies and specializes in coverage for the forest products, real estate, food and beverage, manufacturing, distribution and wholesale and construction sectors.

benefits general agency. Truist officials said in a news release that the purchase will bring in an extra $150 million a year for Truist’s wholesale is expected to close in the third quarter of this year.

Arthur J. Gallagher & Co., Denver Agency

Eric Gordon, Chip McKeever, Katy Hyman Roth and their team will continue to operate from their current location under the direction of Jeff Saunders, head of Gallagher’s U.S. personal lines business, and Jay Eshelman, head of Gallagher Select, its U.S. P/C operations for small businesses.

Through a network of some 20,000 retail brokers, BenefitMall provides employee benefits to more than 140,000 small and medium-sized businesses across theTrcountry.uistisa subsidiary of publicly traded Truist Financial Corp. BenefitMall will become part of Truist's CRC Insurance division, a spokesperson said. Hub, Bubrig Hub International Limited announced that it has acquired the assets of Bubrig Insurance Agency Ltd. Located in Belle Chasse, Louisiana, Bubrig Insurance Agency is an indepen dent agency providing personal insurance solutions, including home, auto, flood, life andBillrecreation.Bubrig,president, and the entire Bubrig Insurance Agency team will join Hub Gulf South. Southeast World Insurance, Consumers Choice Underwriters World Insurance Associates LLC has acquired Consumers Choice Underwriters Inc. of Miramar, Florida. Consumers Choice writes property/ casualty insurance throughout Florida including homeowners, commercial and special event insurance. The agency was founded in 2010 by Maria Pineda and is currently owned by Giovanni Gutierrez. World Insurance Associates, based in Iselin, New Jersey, ranks No. 24 on Insurance Journal’s Top 100 Agencies. Alera, Jowers-Sklar Insurance Alera Group has acquired Jowers-Sklar Insurance, a Georgia-based independent agency specializing in property/casualty insurance in the Southeast. The agency serves Floyd County, Georgia, and the surrounding area, as well as clients in 16 states. It offers business and personal insurance, with specialities in equipment rental, childcare and restau rants.Jowers-Sklar joins Alera Group through Propel Insurance, an Alera Group company headquartered in Tacoma, Wash.

Arthur J. Gallagher & Co. acquired Denver, Colorado-based Denver Agency. Denver Agency is a personal lines-fo cused insurance agency that serves high-net-worth and ultra-high-net-worth clients throughout the U.S. It also offers commercial property/casualty services.

RPS is Arthur J. Gallagher’s U.S. whole sale brokerage, binding authority and programs division. Arthur J. Gallagher, an insurance bro kerage, risk management and consulting services firm, is headquartered in Rolling Meadows, Illinois.

The Jowers-Sklar team will continue serving clients in their existing roles. Alera is headquartered in Deerfield, Illinois, and has offices around the country. It was formed in 2017 from the merger of 24 companies.

Arthur J. Gallagher & Co.’s Risk Placement Services Inc. acquired Hillsboro, Oregon-based Evergreen Insurance Managers Inc. Dyan Bates, Nancy Schultz and their associates will remain in their current location.Evergreen Insurance Managers is a wholesale insurance broker and managing general agency offering commercial insur ance services for a variety of industries. The team serves clients throughout the Pacific Northwest.

division.Thedeal

West Arthur J. Gallagher, Evergreen Insurance Managers

Business

PCF Insurance, A Insurance PCF Insurance Services acquired A Insurance Agencies in Utah, a personal lines insurance provider specializing in life, home, auto, and business. The firm has offices in Syracuse, Kaysville, and MarriottSlaterville.Lehi,Utah-based PCF is a consultant and insurance brokerage firm offering a broad array of commercial, life and health, employee benefits, and workers’ compensation services.

Moves continued from page 27

Virtus Brokerage, Kemmons Wilson Virtus LLC, a Kansas City-based insurance brokerage and consulting firm, has joined forces with Kemmons Wilson Insurance Group, a Memphis company that specializes in insuring hospitality and hotelThefirms.combined firm will have more than 100 employees and a book of business of more than $250 million in premium and $20 million in revenue, according to the announcement regarding the transaction.

Real Expertise. Real Specialization. Excess & Surplus Products unavailable except through a licensed surplus line broker. Availability varies by state. Policy eligibility is subject to underwriting qualifications and approval by the insurer writing the policy. Insurance products underwritten by eligible surplus lines insurer affiliates of Nationwide Mutual Insurance Company, One Nationwide Plaza, Columbus, Ohio, 43215-2220, including Scottsdale Insurance Company (unlicensed except in AZ, DE and OH), Scottsdale Indemnity Company (unlicensed in AZ and DE), or Scottsdale Surplus Lines Insurance Company (unlicensed except in AZ and NJ). Scottsdale Surplus Lines Insurance Company is not an eligible surplus lines insurer in CA. Nationwide, the Nationwide N and Eagle, and Nationwide is on your side are service marks of Nationwide Mutual Insurance Company. AM Best A+ (12/2021, The second highest of 16 ratings). Standard & Poor’s A+ (5/2021, The fifth highest of 21 ratings). ©2022 Nationwide. From property and casualty to personal lines, our excess and surplus team specializes in complex and hard-to-place risks with tailor-made solutions that work. AMA+BestFSCXV StandardA+&Poor’s 100companyFortune (12/22/2021) (5/7/2021) Experience our expertise: nationwide.com/experience is on your side Commercial general contractor

Special Report: Assisted Living and Senior Care

Hamilton handles both skilled nursing home and assisted living risks, which Zuccari stresses are very different risks and some carriers will only write one or the other. Skilled nursing cares for patients in facilities; assisted living and senior housing are communities with residents. But when it comes to liability, he feels the

“I think during the pandemic things got shook up. I believe we’ve seen a lot of things leveling off,” Jason Zuccari at Hamilton Insurance Agency in Fairfax, Virginia, told Insurance Journal. Hamilton specializes in insurance and risk manage ment for the senior community. Zuccari, vice president of business development, calls Hamilton a “one-stop shop for insurance in a senior care community.”

Premiums that were going up considerably are moderating in some subclasses and carriers that pulled away are returning and competing with new entrants.Atthesame time, the sector is witness ing a technology explosion that promises to address some of the most difficult claims scenarios.

“Obviously, during the beginning and in the height of the pandemic, we saw a lot of carriers reining back, being a lot more con servative, or just not writing anything at all. But as things have been loosening up, the carriers have gotten back to business as usual,” he said “There’s still a few carriers that don’t write in a senior space anymore, but then others that have been out for years are getting back in.”

30 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM

The insurance market for senior care and housing facilities has emerged from the volatile period of the pandemic and is again responsive and competitive.

Senior Care Market Experiencing Revived Competition Amid Hi-Tech Boom By Andrew G. Simpson

The “liability piece” is the bailiwick of James McNitt, healthcare practices leader with specialty broker Risk Placement Services (RPS) in its Chicago-area office. In a recent report, McNitt noted that since summer 2021, many medical professional liability insurers have “made an abrupt change in direction” in underwriting longterm care facilities. After several years of rate increases from 12% to 15%, many long-term care facility premiums are now flat on renewal, although other senior facilities continue to see rate increases. Some MPL insurers are even offer ing two-year rate guarantees to long-term care facilities, according to “RPS.So,whereas there’s a need for rate on certain facilities and groups of facilities, we are seeing compe tition from new market entrants that is keeping that increase down,” McNitt told Insurance Journal. “We had quite a bit of flat renewals and competitive carriers coming in trying to underprice business. There’s a little bit of what I like to call ‘FOMO’ still in existence here — the fear of missing out where carriers are still trying to compete on accounts that, in my opinion, are ones that should not be competed on.”

two sectors are becoming more alike. “The big thing was that assisted living would say, ‘No, we’re not a nursing home.’ But now assisted living facilities are also facing high liability risks and having to learn how to manage them.” He thinks the “liability piece” is the one of the most pressing concerns for all senior care operators.

“It’s a combination of just new parent companies that are entering the space or carriers that exited in the past and are more satisfied with the rate adequacy of the marketplace today,” he added.

“And it’s gotten expensive. You can understand why — you’re driving elderly people and if you look across the board, just auto in general has gone up.”

Auto is the biggest headache. Insurers are taking a much closer look at hired nonowned auto coverage where employees may use their own vehicles to transport assisted living residents to appointments.

In another area, sexual misconduct and abuse claims remain a concern and carriers are now limiting and even excluding this coverage in some policies, RPS reports.

page 32

One of the coverage issues that McNitt says is still in flux is COVID exclusionary language.

“That is something that we still do see for the majority across the board from all of our carriers. It is some sort of airborne pathogen communicable disease, COVIDspecific, exclusionary language. However, some carriers are willing to remove that exclusion for an additional premium,” he noted.Overall, McNitt assesses the current market as one with some challenges but also one where continued on

According to RPS, for the first time many insurers are asking policyholders to share more of the risk through deductibles and retentions. This trend, McNitt believes, helps explain what appears to be an overall drop in claims frequency because “the small stuff“ is being reported less often.

INSURANCEJOURNAL.COM

Research on the most common senior market professional liability claims (Aging Services Claims Report) by CNA, a leading senior care insurer, shows resident falls and pressure injuries continue to make up about two-thirds of all claims. Other top causes are improper care, failure to monitor, delay in seeking care, resident abuse, and medication errors. Elopement claims are only 1.8% but are the costliest per claim, averaging $360,840.

McNitt describes it as an “opportunistic” market where some established carriers are letting accounts walk rather than underprice them and the new entries are typically professionals with experience in the market and have a “pretty darn good understanding” of what they’re doing.

“That’s something that, five years ago, was thrown in for free,” McNitt noted. However, now claims severity is a major concern. “Those total losses have been pretty brutal and in the past 12 to 18 months, we’ve seen carriers really taking a harder look at that.” He called auto for a senior living facility one of the “most difficult placements in insurance today” because it involves a fragile patient population oftentimes in non-ambulatory situations. There are issues with wheelchair tie downs not being correct and gurneys not being strapped correctly. Also, the non-emergency medi cal transport industry suffers from driver shortages.Zuccariagrees that auto is a big chal lenge, with some states’ liability climates worse than others and driver shortages everywhere. He said carriers are underwriting the individual driver whereas before they’d offer blanket coverage, and they are requiring background checks, which can be irksome in a field with a lot of turnovers.

SEPTEMBER 5, 2022 INSURANCE JOURNAL | 31

Technology Boom Risk-reducing technologies that are being introduced at a rapid pace are part of the conversation brokers have with their senior care clients and insurers. These technologies are addressing a number of the most common risks in senior care from inadequate staffing and medication errors to falls and loneliness. Wearables track a resident’s physical condition, heart rate, stress levels and sleep patterns. Virtual assistants help senior living staffs with day-to-day tasks like reminders for appointments, medi cations and meals and answer questions for seniors. GPS devices track residents’ location to prevent elopements. Telehealth services provide video consultations, remote patient monitoring and secure messaging. Alexa-like voice activated devices let families and caregivers remote ly check in on seniors. Machines accurately dispense medications. Caregivers use data from electronic incident reports to optimize care and safety plans. Telehealth services provide quick access to medical teams.Hamilton

he’s still “able to get stuff done.” That is a contrast to two years ago in the middle of 2020, when he felt that there were risks that he called “uninsurable” or where the premium was so high that the insured couldn’t afford it. Since 2020, he thinks the market has been “pretty darn consistent.” He uses the terminology of Goldilocks, “not too hot, not too cold” in his outlook.

“COVID really threw a big curve ball to this industry. I think people are fatigued. I think the stress got to people,” Zuccari said. “Workers and laborers are leaving the industry completely; it’s the stress, the intensity, and the responsibility is hard.”

RPS points out in its report that solving one problem often leads to creating a new one.“That’s insurance, right? Nowhere to hide,” commented McNitt.

Both McNitt and Zuccari see the indus try’s labor shortage as a major risk factor. It is a challenge not only in caregiving but also in transportation.

Telehealth services can raise issues around remote diagnoses and treatment, confusion about where a claim can be brought, licensing of doctors, or missed instructions due to service interruptions.

According to a 2020 claims study by insurer CNA, almost 60% of fall-related claim allegations involve a resident with a prior history of falls and claims where there was a history are more costly.

Skilled nursing facilities are graded on a staffing metric. Facilities that have more medical professionals on staff are presumed to have less adverse medical outcomes. Technology may be able to help here, too. “During COVID, there were facilities that had basically the equivalent of a robotic cat or dog-looking creature that would bring meals to residents. It had artificial intelligence to understand where it was going through the facility and also had the ability for somebody on the other end of it to do the communications. That was a way to bring both a smile and a meal to a fragile patient population, especially during the height of COVID,” McNitt said. Telemedicine took off during the pandemic and remains popular for both diagnosis and screening to determine if an office visit is needed. Among the benefits of telehealth services are its communication capabilities that counter social isolation and loneliness, which are associated with about a 30% increased risk of heart attack or stroke, according to the American Heart Association.

“The loneliness metric was something that was pretty darn stark during COVID,” McNitt recalled. “We saw the ability to bring in a machine that would not just communicate back and forth with them, play music, show a video, et cetera, but also communicate with their family when visitors weren’t allowed. It seemed simple, but it enabled a happier lifestyle for some of these more fragile patients.”

Zuccari has noticed considerable money going in healthcare technology and a believes a “lot of really fascinating compa nies” are on the way. He wonders which firms and technologies will win the race to set the industry standard. “Is it wearable? Is it sensor? Is it infrared?” he queried.

Insurance performs onsite surveys during which a consultant walks the building with the client and notes deficiencies such as a medicine chest on a certain floor being unlocked. Incidents are input into the proprietary risk management system, Servarus, which can issue reports, trends analyses and alerts. Caregivers may be alerted that a patient has fallen multiple times in the past 30 days. “If we don’t figure out a remedy, next time he’s going to go to the hospital,” Zuccari explained. The program also tracks hospital readmissions and lets owners see which of their facilities are having more incidents.

“All of these data points have been able to help reduce claims and falls, and the whole idea is building this culture of awareness. If we see something, we’re going to try to correct it,” Zuccari added.

Better communication leads to happier outcomes. “They’re going to live longer and probably feel better throughout the process and a lot of claims that we do see are a result of just being a disgruntled patient,” the RPS broker said. As much good as technologies are doing, there are downsides. The main one is that they raise cybersecurity risks and insurance costs. Cyber insurance has “gotten super, super expensive,” said Zuccari, while stressing how important it is for an industry that is dealing with HIPAA compliance and people’s medical records.

32 | INSURANCE JOURNAL | SEPTEMBER 5, 2022 INSURANCEJOURNAL.COM

Special Report: Assisted Living and Senior Care

‘There’s a little bit of what I like to call ‘FOMO’ still in existence here — the fear of missing out where carri ers are still trying to compete on accounts that, in my opinion, are ones that should not be competed on.’

continued from page 31