Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Difference. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started.

Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

Spotlight: Why Some Transportation Risks Could Find Options With Captives: Risky Future

Spotlight: Inflation, Rising Claim Costs, Riskier Business Reasons Cited for Rate Increases in A&E Market: Survey

Special Report: Today’s Commercial Property Market in ‘Better Place’

Special Report: An Insurance Journalist’s Perspective on Southern California’s Wildfires

Closer Look: Understanding the Risks and Coverages in Condo Association D&O

Workforce Wellbeing

Rising medical costs and economic uncertainty are stressing out today’s workforce.

That’s according to MetLife’s 2025 U.S. Employee Benefit Trends Study which revealed a decline in employees’ holistic health (-5%), productivity (-5%), and engagement (-7%) across the board and found that a majority of employees are worried about finances.

Rising medical costs (77%) and economic uncertainty (68%) were listed as employees’ primary source of stress amid social and economic turmoil, the survey said. Employees are turning to their employers for stability and support, according to MetLife’s EBTS. Some 81% of employees reported holding their employer accountable for building trust at work, while employees overall are 1.5x more likely to trust their employer than other institutions.

That’s a “great responsibility” for any employer. Building trust comes with a significant opportunity to improve workplace outcomes, according to MetLife’s study, which noted that trust, when combined with employee care, has a profound impact on employees.

“Employees who trust and feel cared for by their employer are more likely to feel holistically healthy (3.8x), engaged (2.4x), and more productive (1.9x) than those with either or neither,” the study said.

MetLife recommends that employers can build trust by fostering a supportive culture and promoting positive benefits experiences.

Workplaces that promote recognition of achievements and hold a culture with transparent leadership and empathy are more likely to foster trust between employees and employers, MetLife’s report said. Combining the right mix of benefits with a positive utilization experience is also highly correlated to increased trust and improved outcomes, the study said.

According to MetLife’s study, employees who use and have positive experiences with their employee benefits are:

• 2.4x more likely to feel holistically healthy.

• 2.1x more likely to trust that their employer will protect them in economic downturns.

• 1.8x more likely to trust their employer’s leadership.

‘Employees who trust and feel cared for by their employer are more likely to feel holistically healthy, engaged, and more productive than those with either

or neither.’

“Our research continues to validate that employers who demonstrate care for their employees see improved workplace health and outcomes,” said Todd Katz, head of Group Benefits at MetLife, when releasing the survey report. “What we’ve newly uncovered this year, given macro challenges, is an opportunity to fortify care by fostering trust.” Employers that focus on prioritizing benefit experiences and culture can effectively build high-trust and high-performing workplaces, he added.

To view MetLife’s 2025 Employee Benefit Trends Study, visit www.metlife.com/ebts2025.

| mwells@wellsmedia.com

Officer

Chief

Carlson | jcarlson@insurancejournal.com

ADMINISTRATION / CIRCULATION

Chief Financial Officer Terry Freeburg | tfreeburg@wellsmedia.com

Circulation Manager Elizabeth Duffy | eduffy@wellsmedia.com

Staff Accountant Sarah Kersbergen | skersbergen@wellsmedia.com

EDITORIAL

V.P. of Content

Andrea Wells | awells@insurancejournal.com

Executive Editor Emeritus

Andrew Simpson | asimpson@wellsmedia.com

National Editor

Chad Hemenway | chemenway@insurancejournal.com

Southeast Editor

William Rabb | wrabb@insurancejournal.com

South Central Editor/Midwest Editor Ezra Amacher | eamacher@insurancejournal.com

West Editor Don Jergler | djergler@insurancejournal.com

International Editor L.S. Howard | lhoward@insurancejournal.com

Content Editor Allen Laman | alaman@wellsmedia.com

Assistant Editors

Jahna Jacobson | jjacobson@insurancejournal.com

Kimberly Tallon | ktallon@carriermanagement.com

Columnists & Contributors

Contributors: Dawn Bennett-Alexander, Russ Banham, Denise Johnson, James Felton Keith, Chris Lack, Francisco Lopes, Mike Zdrojewski

Columnists: Chris Burand, Mary Newgard, Bill Wilson

Marketing Administrator Alberto Vazquez | avazquez@insurancejournal.com

Marketing Director Derence Walk | dwalk@insurancejournal.com

DESIGN / WEB / VIDEO

V.P. of Design

Guy Boccia | gboccia@insurancejournal.com

Web Team Lead

Josh Whitlow | jwhitlow@insurancejournal.com

Ad Ops Specialist

Jeff Cardrant | jcardrant@insurancejournal.com

Web Developer Terrance Woest | twoest@wellsmedia.com

Web Developer

Jason Chipp | jchipp@wellsmedia.com

Digital Content Manager

Ashley Cochrane | acochrane@insurancejournal.com

Videographer/Editor

Ashley Waldrop | awaldrop@insurancejournal.com

ACADEMY OF INSURANCE

Director Patrick Wraight | pwraight@ijacademy.com

Online Training Coordinator George Jack | gjack@ijacademy.com

Every day, we create unique risk solutions for unique businesses.

When it comes to insurance for midsize and large businesses, we get it. We do it for all kinds of industries, tailoring our policy solutions from traditional to specialized coverage. With our experience in underwriting, innovative service, and claims, we are your one-stop shop.

Connect with your underwriter at The Hartford.

News & Markets

States’ AI-Related Legislation Aimed at Insurance Is ‘Unfounded’, Says NAMIC

By Chad Hemenway

Policy discussions on the use of artificial intelligence in insurance are “unfounded” and “detrimental to policyholders,” according to an analysis from the National Association of Mutual Insurance Companies (NAMIC).

The use of AI in insurance underwriting and rate making has led to concern from some regulators, advocates, and policymakers over whether AI would lead to proxy discrimination, an algorithmic bias,

and eventual changes to the affordability and availability of insurance products in certain areas or for certain classes.

NAMIC said 18 states are currently debating “flawed” AI-related legislation.

Guidance from the National Association of Insurance Commissioners (NAIC) has added to the “nebulous concept of algorithmic bias,” NAMIC said.

“Contrary to what may be perceived as well-intentioned social efforts by regulators, policyholders will be harmed by growing efforts to elevate

concepts of ‘fairness’ divorced from actuarial science,” wrote Lindsey Klarkowski, NAMIC’s policy vice president in data science, AI/[machine learning], and cybersecurity. This will result in “an inevitable break of the insurance product at its core,” she added.

Klarkowski authored the report, meant to dispel five myths about the use of AI and Big Data in the insurance industry.

“In setting rules of the road, policymakers must recognize that insurance is distinct in function and pricing

from many other consumer products,” Klarkowski added in a statement. “Insurance classifies based on risk, and insurance law requires those risk classifications to be actuarially sound and not unfairly discriminatory.”

Any regulation aimed at the industry’s use of AI in pricing has to be unique to the industry, and any restriction on an insurer’s ability to price a policyholder’s risk will lead to more availability and affordability issues, NAMIC concluded, adding that the notion that AI will lead to

US P/C Insurance Industry Income Tops $100B in 2024: Verisk, APCIA

The U.S. property/casualty insurance industry reported its first full-year underwriting gain in four years, fueling a jump in net income to $170 billion, according to a joint report from Verisk and The American Property Casualty Insurance Association (APCIA).

The global data analytics and technology provider and insurance company trade association noted that the net income figure included $70 billion from capital gains realized by insurers in Berkshire Hathaway group. Excluding that hefty investment gain for one enterprise, full-year 2024 net income is estimated to be $100 billion for the industry overall.

Anticipating the $100 billionplus figure last month, S&P GMI reported that this marked the first time in a calendar year that the industry posted net income over $100 billion. Both the S&P GMI and the Verisk/APCIA reports highlight a swing in underwriting results—moving from a net underwriting loss of more than $20 billion in 2023 to an aggregate industry net underwriting profit of more than $20 billion in 2024. Specifically, the Verisk/APCIA report puts the 2024 underwriting gain at $24.8 billion, compared to a $21.8 billion underwriting loss for 2023.

$851 billion in 2023. Earned premiums grew 9.8% to $895 billion.

The combined ratio improved to 96.4 in 2024, down more than 5 points from the 101.6 aggregate industry figure recorded for 2023.

of late-season storms, drove fourth-quarter catastrophe claims to surge 113% higher than the same period in 2023, highlighting both the volatility and financial strain insurers face,” he said.

“While many of the loss drivers of 2023 persisted into 2024, the industry’s ability to bring premiums closer to the requisite levels has led to an underwriting gain for the first time since 2020,” said Saurabh Khemka, co-president of underwriting solutions at Verisk, in a statement.

Net written premiums overall jumped 8.7% to $926 billion in 2024, compared to

Khemka noted necessary premium adjustments in personal auto, in particular, drove improved results for personal lines. “While commercial auto premiums followed a similar trend, its growth rate did not match the levels seen in 2023,” he said.

Among challenges that continue to fuel losses for the industry are property catastrophes, Khemka said, noting that last year marked the second worst year for catastrophic losses since 1950.

“Most notably, Hurricane Milton, along with a series

Robert Gordon, senior vice president, policy, research, and international at APCIA, took note of continuing catastrophes in 2025. “By this time next year, homeowners insurers will have likely reported seven consecutive years of net underwriting losses, including record insured losses caused by the California wildfires this January,” he said.

In spite of the catastrophe losses in 2024, the fourfold jump in net income (including the investment gains recorded for Berkshire’s National Indemnity, National Fire and Marine, and Columbia Insurance Company) helped push policyholders surplus up to nearly $1.1 billion.

bias or disparate impact is in conflict with the risk-based foundation of insurance.

“The data insurers use for risk-based pricing is data that is actuarially sound and correlated with risk and does not include nor use certain protected class attributes,” Klarkowski wrote. “To argue that insurer use of data, algorithms, or AI in risk-based pricing is biased or skewed would be to say that the actuarially sound data is not representative of the risk the policyholder represents, which insurance laws already prohibit.”

Separately, if a disparate impact standard were applied

to insurance, the industry’s pricing approach would no longer be based on underlying

insurance costs and result in rates that are unfairly discriminatory. The industry already

adheres to the legal standard of unfair discrimination, NAMIC said.

AM Best: US P/C Industry in 2024 Posts First Underwriting Profit in Four Years

By Chad Hemenway

For the first time in four years, the U.S. property/ casualty industry will finish a year with an underwriting profit.

AM Best in a “First Look” at U.S. P/C financial results said the industry left 2024 with a $22.9 billion net underwriting

gain. The industry booked an underwriting loss of $21.3 billion in 2023.

The industry combined ratio for 2024 was 96.6 compared to 101.6 the year prior.

Industry policyholder surplus grew about 7% in 2024 to $1.1 trillion.

Data in the special report are provided by companies that

submitted year-end statutory statements as of March 11, AM Best said. The companies account for about 97% of industry net premiums and 96% of policyholder surplus, the rating agency added.

In a larger report on the U.S. P/C segment released in February, which included an estimate of underwriting

income for 2024, AM Best said the industry would take an underwriting loss of $2.6 billion—still an improvement from the loss recorded in 2023 but far from the agency’s early insight now of a nearly $23 billion underwriting profit. AM Best once again pointed to personal lines as the primary reason for the turnaround in underwriting results.

AM Best has said it expects the industry in 2025 to “build on its solid rebound” with improved underwriting and operating results, even as insurers field more losses from secondary perils and continued adverse litigation trends.

Net catastrophe losses in 2024 were about $76.3 billion compared to about $67.7 billion in 2023. AM Best said it estimates catastrophe losses added 8.7 points to the 2024 combined ratio.

News & Markets

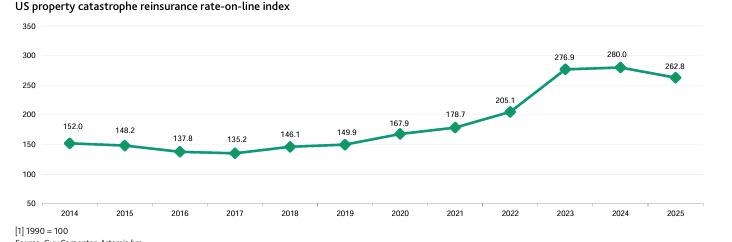

US Property/Catastrophe Reinsurance Rates Likely to Stabilize During Midyear Renewals

By L.S. Howard

Reinsurance renewal rates continued dropping during January renewals, but U.S. property/catastrophe reinsurance pricing is likely to stabilize during the coming midyear renewals, according to a report from Moody’s Ratings.

“The upcoming midyear 2025 reinsurance renewals, which focus on the U.S., will be influenced by large U.S. catastrophe loss events over the past year—particularly Hurricanes Helene and Milton and the Los Angeles wildfires—which are likely to provide support to reinsurance pricing for U.S. exposures,” said the Moody’s report, titled “January renewal prices dip, but US catastrophe events could slow decline,” which was published on March 13.

As a result, Moody’s believes it is likely that U.S. P/C reinsurance pricing will stabilize, “supported by the potential for significant price increases for accounts that have had sizable losses over the past year.”

At the Jan. 1, 2025 renewals, there were moderate risk-adjusted pricing decreases for property coverage, said Moody’s, noting, however, that prices depended on the geographic region and whether accounts were hit by losses last year.

Despite significant global insured catastrophe losses over the past several years, “reinsurers have reported strong results as higher attachment points for P/C reinsurance improved underwriting results for reinsurers and boosted capital across the sector,” which meant there was sufficient reinsurance capacity to meet

demand, Moody’s said.

January Renewals

Typically, between 40% and 60% of a global reinsurer’s portfolio is renewed on Jan. 1, including a substantial majority of European business, Moody’s continued.

“Several European-based global reinsurers reported premium growth for reinsurance business renewed 1 January, as firms sought to deploy capital in a still-attractive pricing environment. Gross premiums written increased at Swiss Re (7.0%), SCOR (9.6%) and Hannover Re (7.6%), while Munich Re’s premium volume was down 2.4% because of underwriting actions intended to reduce business not meeting its return hurdles.”

decreased by 6.2% at the January renewals, which was the first decrease since the January 2017 renewal period that marked the end of the soft market for reinsurance.

• Commercial Directors and Officers

• Employment Practices Liability

• Excess Casualty

• Financial Institutions

• Cyber Liability

Pricing across the portfolios of these European reinsurers was generally flat, ranging from a 2.1% decrease, reported by Hannover Re, to a 2.8% overall increase, reported by Swiss Re, Moody’s said.

• Private Company Liability

“For its nonproportional business, SCOR reported the first pricing decrease (-0.8%) since the January 2017 renewals.”

For the key U.S. property catastrophe reinsurance segment, reinsurance broker Guy Carpenter reported overall pricing

Source: Guy Carpenter and Artemis.bm via Moodys’ Ratings

“Generally, pricing was largely stable in working layers—the lower levels of reinsurance used for more frequent and smaller claims. However, pricing was lower at the top end of reinsurance programs where there was plenty of capacity available for coverage of less frequent and larger claims, for which pricing remains attractive on a risk-adjusted basis.”

Casualty Business

Beyond property coverages, Moody’s said, pricing for casualty business was mixed and largely dependent on the performance of individual treaties.

European casualty was flat to down 10% for loss-free accounts and flat to up 10% for loss-impacted accounts, said Moody’s quoting reinsurance broker Gallagher Re. “In the US, general liability was down 5% to up 5% for loss-free accounts and flat to up 10% for loss-impacted accounts.”

The report noted that ceding commissions were broadly stable at the January renewals “as reinsurers held the line on payments to ceding companies given the increase in loss-cost trends due to social inflation in recent years.”

This satellite image provided by CSU/CIRA & NOAA taken 1:10 GMT on Feb. 25, 2025, shows three cyclones, from left, Alfred, Seru and Rae east of Australia in the South Pacific. (CSU/CIRA & NOAA via AP, File)

1

2

3

News & Markets

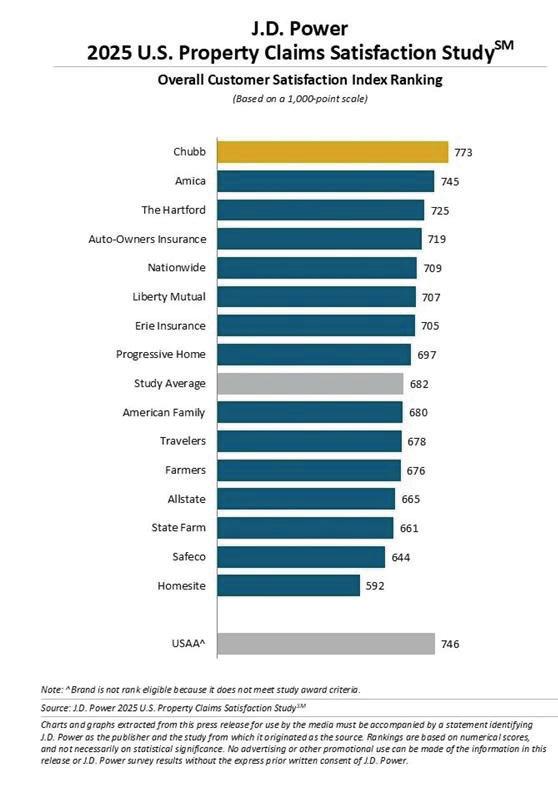

JD Power: Customers Not Happy With Carrier Property Claims Service

By Jahna Jacobson

Higher premiums and longer wait times make property owners less satisfied with their insurers.

These not-very-surprising results from J.D. Power’s 2025 U.S. Property Claims Satisfaction Study align with today’s climate of increasingly longer claim cycle times and higher costs for homeowners’ insurance.

“Customers are, in essence, paying higher prices for slower service,” said Mark Garrett, director of insurance intelligence at J.D. Power. “The average claimant does not receive final payment on a claim until 44 days after the first notice of loss, and unless insurers communicate frequently and clearly along the way, customer satisfaction suffers.”

Overall, the customer satisfaction score came in at 682 (on a 1,000 point scale).

Chubb ranks highest in property insurance claims experience with a score of 773. Amica (745) ranks second and The Hartford (725) ranks third.

Impact of Longer Waits, Higher Premiums

The average claim cycle time from filing the claim to finished repairs is now 32.4 days, and the average cycle time from first notice of loss to final payment is now more than 44 days—the longest time since 2008. Claims completed within 10 days score 762, while repairs taking more than 31 days score 595.

Half the customers surveyed experienced insurer-initiated premium increases in the past 12 months. Overall satisfaction scores are 101 points lower (629 vs 730) when insurers initiate a premium increase unrelated to having a claim than those who did not experience a premium increase.

“There were 27 catastrophic events in 2024 and 28 the year before,” Garrett said. “Homeowners insurers are currently losing roughly one nickel on every dollar of premium they collect, and with total cost of events like the California wildfires still being assessed, there seems to be no end in sight.”

How Can Insurers Improve Satisfaction Scores?

Communication can be

key to mitigating insureds’ aggravation, J.D. Power said. Overall satisfaction scores are more than twice as high (777) when customers feel it is very easy to communicate with their insurer than when it is very difficult or somewhat difficult to communicate (337). Common communication failure points include often needing to leave voicemails, needing to call with questions repeatedly, and not receiving timely follow-up emails and text messages.

Overall satisfaction is also higher among customers who use digital tools when filing a claim, submitting photos that are used in the estimate and receiving proactive updates. Among digital channels, app usage results in the highest levels of satisfaction. Eighty-seven percent of Gen Z and Millennials indicate they are comfortable managing the entire claims process digitally. Only 60% of Baby Boomers and Pre-Boomers say they are comfortable managing claims online.

Study Parameters

J.D. Power’s U.S. Property Claims Satisfaction Study was redesigned for 2025, so scores are not comparable with previous-year studies. The study measures satisfaction with the property claims experience among 5,178 homeowner insurance customers who filed a claim within the previous nine months. The study was fielded from January 2024 through December 2024.

Open more doors with Foremost ®

Foremost Insurance makes writing preferred Homeowners & Auto easy with customizable coverage, discounts, and excellent claim service. Our innovative Foremost Signature® products offers all this and more. And don’t forget about our well-rounded suite of Foremost Choice® specialty products. Let Foremost help you open more doors and close more sales.

84.8%

The percentage of surveyed cannabis users reporting they drive the same day they consume cannabis versus waiting eight or more hours. A survey of 2,000 cannabis users across eight states found nearly 1 in 5 believed their driving was worse after cannabis use; 49.6% said their driving was the same; 14.7% said a little better; and 19.4% said much better. Just 29.2% believed a police officer could detect the influence of cannabis; 46.7% did not think they could detect it; and 24.1% were unsure.

$70,000

The approximate amount former Michigan agent Brian Lietzau must pay in restitution to the estate of a now-deceased elderly client from whom Lietzau was charged with embezzling. Lietzau, the former owner of Farm Bureau-Lietzau Insurance, was also sentenced to 36 months’ probation—with six months under house arrest.

204

The number of mergers and acquisitions in the insurance industry in 2024, down from 346 in 2023. Global insurance carrier M&As slumped to a 16-year low in 2024 amid a wave of uncertainty and volatility throughout the year, Clyde & Co.’s annual Insurance Growth Report revealed. The U.S. market saw the most M&A activity during 2024 with 69 deals completed, due to increased activity in the life sector. The UK and Europe saw the largest slump in M&A activity, with a 48% drop.

$50 Million

The amount awarded to a delivery driver injured when a Starbucks drink spilled in his lap at a California drive-through. A Los Angeles County jury found for Michael Garcia, who underwent skin grafts and other procedures on his genitals after a venti-sized tea drink spilled moments after he collected it on Feb. 8, 2020. He has suffered permanent and life-changing disfigurement, according to his attorneys.

Declarations

‘Monster’

Event Inevitable

“Climate change may have been announcing its arrival. However, no ‘monster’ event occurred during 2024. Someday, any day, a truly staggering insurance loss will occur—and there is no guarantee that there will be only one per annum.”

— Warren Buffett in Berkshire Hathaway’s 2024 annual report to shareholders.

Filling the Talent Pool

“The concerns that I have tie into that birth rate discussion, but more broadly around companies as they think about succession planning and building a talent pool for the future... This perhaps paints a bit of a bleak story for the ability for the industry to create those roles going into the future.”

— Jeff Rieder, partner and head of Strategy and Technology Group Performance Benchmarking at Aon, during a jobs outlook webinar. This year saw a significant drop in the percentage of expected entry-level hires for underwriting activities—14% in January 2025, down from 21% in January 2024 and 38% in January 2023. This year, carriers say only 15% of the actuarial roles filled in the next 12 months will go to job seekers new to the actuarial profession.

Community Coverage

“Ultimately, local governments will need to reduce risk through appropriate land use, zoning, and building controls. Without this, parametric insurance might not even be available in the future.”

— Jesse Keenan, a professor at Tulane University who studies cities and climate risk, responding to the idea of high-risk California communities obtaining parametric insurance. Without proactive planning, he said, cities would basically be kicking the can down the road.

AI Underwriting

“One of the key governance controls and duties with AI technology is that it does require human oversight, so while AI could perform some underwriting stages, you would hope that there is still a human reviewing its output and sense-checking that.”

— Claire Davey, head of product innovation at Relm Insurance, headquartered in Hamilton, Bermuda, on the evolution of AI in insurance underwriting. However, she said, major AI shifts are already happening in other areas of insurance that involve more administrative tasks.

Investing in Storm Safeguards

“Unfortunately, it’s not if but when another powerful storm will take aim at Florida. This legislation is a proactive step toward safeguarding our communities from hurricanes and keeping insurance costs in check.”

— Florida CFO Jimmy Patronis said in a statement about the state’s new My Safe Florida Home Trust Fund, which he said would “funnel necessary funds into our local economies but also incentivize homeowners to fortify their residences.”

Earth, Wind, and Fire

“Whoa, is this coming? Oh, it’s here. It’s here… Look at all that debris. Ohhh. My God, we are in a torn…”

— Tad Peters, in a video, as a tornado bore down on him and his father, Richard Peters. The two had pulled over to fuel up their pickup truck in Rolla, Missouri, on March 14 when they heard tornado sirens and saw other motorists fleeing the interstate to park. They were headed to Indiana for a weightlifting competition but decided to head back home to Norman, Oklahoma, about six hours away, where they encountered wildfires.

Business Moves

National

The Doctors Company, ProAssurance

The Doctors Company said it has entered an agreement to acquire ProAssurance Corp. for $1.3 billion, taking the company private.

Birmingham, Alabama-headquartered ProAssurance is a specialty insurer with expertise in medical liability, products liability for medical technology and life sciences, and workers' compensation insurance. The Doctors Co. of Napa, California is the nation's largest physician-owned medical malpractice insurer.

The transaction is expected to close in the first half of 2026. Upon completion, ProAssurance's common stock will no longer be listed on the New York Stock Exchange, and ProAssurance will become a wholly owned subsidiary of The Doctors Co., creating a combined company with assets of approximately $12 billion.

Rating agency AM Best said The Doctors Company Insurance Group is the second-largest writer of medical professional liability (MPL) insurance in the U.S. based on 2023 direct premiums written (AM Best said it is in the process of collecting 2024 data). ProAssurance is the fourth largest. Berkshire Hathaway is first with more than 18% market share. Together with ProAssurance, Doctors Co. would have nearly 16% of the MPL market.

Munich Re, Next Insurance

Munich Re said it has acquired Next Insurance, which will become part of the reinsurer's major primary insurance

business, Ergo.

The agreement in place values Next Insurance at $2.6 billion. Ergo already owned nearly 30% of the digital insurance company's shares. Munich Re was an early investor in Next Insurance.

Closing is expected during the third quarter pending regulatory approvals. Munich Re has said it expects $23.1 billion in general insurance revenue from Ergo in 2025.

East

World Insurance Associates, Archambault Insurance Associates

World Insurance Associates LLC, headquartered in Iselin, New Jersey, acquired the business of Archambault Insurance Associates of Putnam, Connecticut. Terms of the transaction were not disclosed.

Archambault was founded in 1928 by Joseph A. Archambault. The third-generation, family-owned, full-service agency serves individuals, families and businesses in Connecticut, Rhode Island and Massachusetts. Archambault provides personal, commercial, life and health, and surety insurance.

King Risk Partners, The Insurance Center

King Risk Partners, headquartered in Gainesville, Florida, acquired The Insurance Center, an independent agency in Warwick, Rhode Island. Terms were not disclosed.

Founded in 1973, The Insurance Center serves individuals, families, and busi-

nesses in Warwick and throughout Rhode Island.

This acquisition is Florida-based King’s first agency in Rhode Island, reflecting the firm’s commitment to expanding its service to the Eastern and Southeastern regions of the country.

In addition to 15 offices in Florida, and now one in Rhode Island, King Insurance has locations in Alabama, Connecticut, Florida, Georgia, Massachusetts, New Hampshire, New Jersey, New York, North Carolina, South Carolina, Tennessee, Virginia, and West Virginia.

NFP, Lyons Insurance Agency Inc.

Property/casualty middle-market insurance broker NFP, an Aon company, recently announced its acquisition of Lyons Insurance Agency Inc., a multiline insurance broker located in Wilmington, Delaware.

David Lyons and Tim Lyons, vice presidents of Lyons, will join NFP as senior vice presidents and report to Meg McSherry, managing director of Property and Casualty in NFP’s Atlantic region.

Founded more than 40 years ago by David F. Lyons, Sr., Lyons provides middle-market businesses with commercial, personal lines and employee benefits solutions.

Aon closed on its $13 billion acquisition of NFP last April. NFP has more than 7,700 colleagues in the U.S., Puerto Rico, Canada, UK and Ireland.

Midwest

Alacrity Solutions Group, InspectionConnection

Alacrity Solutions Group announced the acquisition of InspectionConnection from Latitude Subrogation Services LLC. The transaction marks Alacrity’s 16th acquisition since 2015.

InspectionConnection, founded in 2018 and based in Columbus, Ohio, is a full-service appraisal and desktop review company specializing in autos, specialty vehicles, and heavy equipment, including construction vehicles, tractor-trailers, and farm machinery.

Alacrity Solutions, based in Fishers,

Indiana, is one of the largest independent providers of insurance claims management services in North America.

South Central

Sierra Financial Holdings LLC, Preferred Security Life Insurance Company

Sierra Financial Holdings LLC, headquartered in Houston, received final regulatory approval from the Texas Department of Insurance to acquire Preferred Security Life Insurance Company, a TexasDomiciled Life Insurance carrier. Closing is expected to occur on April 1, 2025.

Sierra Financial Holdings LLC is a privately held company focused on the financial services industry. The companies include Sierra Mortgage Capital LLC, Sierra Lending Group LLC, Sierra Lending Corporation and Sierra Insurance Services LLC.

Founded in 1994, Preferred Security Life Insurance Company is a Stipulated Premium Life insurance company with operational headquarters in Colorado Springs, Colorado.

CRC Group, Risk Transfer Partners

CRC Group, an independent wholesale specialty insurance distributor in North America, announced the acquisition of Risk Transfer Partners (RTP), a casualty-focused wholesale brokerage business. This strategic acquisition enhances CRC’s capabilities and market reach, particularly in the construction, energy, environmental, and manufacturing sectors.

Founded in 2013 and based in Dallas, Texas, RTP has established a national platform with a track record of organic growth. RTP, under its existing leadership team, including Dave Barrett, RTP President, will join the CRC Specialty division and report to Brokerage President Brent Tredway. Keystone Agency Partners, Ascent Insurance Group

Keystone Agency Partners (KAP), headquartered in Harrisburg, Pennsylvania, acquired Ascent Insurance Group, a prominent Oklahoma-based insurance agency. The deal includes Cole, Paine & Carlin Insurance Agency, Inc., which will join Ascent Insurance Group.

Aaron Bogie will serve as CEO of Ascent Insurance Group. Ascent’s Oklahoma City home office will be joined by branch locations in Tulsa and Tonkawa.

This partnership bolsters KAP’s commercial and personal lines insurance capabilities, empowering Ascent and CPC to leverage KAP’s extensive resources, specialized expertise, and national network to drive growth, innovation, and enhanced client experiences.

The River Company, Rogers Insurance

Two Arkansas independent agencies

The River Company and Rogers Insurance merged to create ANKR. The new entity, which employs 80 professionals across Arkansas and Texas, will operate under the ANKR brand, with full integration expected by January 1, 2026. Together, ANKR will offer a full suite of personal and commercial insurance, bonds, payroll and tax solutions.

The River Company, based in central Arkansas, has grown steadily over the past decade, completing five acquisitions and expanding its services to include payroll and tax solutions alongside its core insurance offerings.

Rogers Insurance is a century-old firm with locations in both central and northwest Arkansas.

Southeast

Atlas Insurance Agency,

Atlas Employee Benefits

Atlas Insurance Agency, based in Sarasota, Florida, acquired its sister company, Atlas Employee Benefits. The firms will now operate under a single brand name. Atlas Employee Benefits will operate under the Atlas Insurance brand, offering a wider range and streamlined services.

Atlas Insurance, founded in 1953, serves clients in 45 states, providing business and personal lines coverage through local and national carriers. The company has more than 60 professionals on staff. Rob Brown is president.

Hub International, C&L Marine Insurance

Chicago-based Hub International

acquired the assets of C&L Marine Insurance, based in Boca Raton, Florida. President Scott Costolo and his team will join Hub Florida, which will be known as C&L Marine, a Hub International company. It’s the latest acquisition for Hub, which has grown to more than 19,000 employees across the continent.

Chris Gardner is CEO of Hub Florida. C&L has more than 30 years of experience working with major insurance carriers. The firm has focused on boat builders, dealers, marinas, marine contractors, yachts and more.

West

PrestigePEO, Concurrent HRO

PrestigePEO, headquartered in Melville, New York, acquired Concurrent HRO, a Colorado-based professional employer organization. Concurrent HRO’s team will remain in place.

The acquisition is PrestigePEO’s fifth, and it expands PrestigePEO’s presence in the Midwest and Mountain regions. Concurrent HRO provides human resources, payroll and employee benefits services for businesses of all sizes.

PrestigePEO provides HR services that include payroll management, employee benefits, compliance support and risk management services.

Chicago-based Hub International has acquired the assets of Malloy Imrie & Vasconi Insurance Services LLC in California’s Napa Valley.

Partners Timothy Malloy, David Capponi, Ted Bystrowski, Kevin Dickenson, and the MIV Insurance team will join Hub Central & Northern California.

MIV Insurance will be referred to as MIV Insurance, a Hub International company. MIV Insurance, which has offices in Saint Helena and Napa, is an independent firm that provides commercial, employee benefits, and personal insurance to clients throughout California. The firm specializes in agribusiness, particularly in the wine industry.

News & Markets

Maryland Could Have Reduced Risk of Key Bridge Collapse: NTSB

By Andrew G. Simpson

The National Transportation Safety Board (NTSB) is harshly criticizing Maryland officials for failing to conduct a risk assessment of the Francis Scott Key Bridge before it collapsed a year ago and is recommending that 30 owners of 68 bridges across 19 states conduct a vulnerability assessment to determine the risk of bridge collapse from a vessel collision.

The agency indicated that had Maryland conducted such an assessment, it could have taken steps to reduce the risk of and possibly prevented last year’s tragic Key Bridge collapse in Baltimore. In its own assessment, NTSB found that the Key Bridge was considerably above the acceptable risk threshold for essential bridges.

The federal agency warned that many of the nation’s bridges may be above the acceptable level of risk, although it stopped short of suggesting they are in

danger of imminent collapse.

The report is part of the ongoing investigation into the Key Bridge collapse. The NTSB found that the Key Bridge, which collapsed after being struck by the containership Dali on March 26, 2024, was almost 30 times above the acceptable risk threshold for critical or essential bridges, according to guidance established by the American Association of State Highway and Transportation Officials (AASHTO).

Over the last year, the NTSB said it identified 68 bridges including the Key Bridge that were designed before 1991 when the AASHTO guidance was established and do not have a current vulnerability assessment using AASHTO’s calculation.

The NTSB is recommending that the 30 owners of these bridges evaluate whether their bridges are above the AASHTO acceptable level of risk and implement a risk reduction plan if needed.

Since 1994, the Federal Highway Administration (FHWA) has required new

bridges be designed to minimize the risk of a catastrophic bridge collapse from a vessel collision, given the size, speed, and other characteristics of vessels navigating the channel under the bridge. The Key Bridge was built before vulnerability assessments were required by FHWA.

Neither the FHWA nor AASHTO can require a bridge owner to complete a vulnerability assessment for a bridge designed before the release of the 1991 guidelines.

Maryland Assessment

The Maryland Transportation Authority (MDTA) had not performed, nor was it required to perform, a vulnerability analysis on the Key Bridge, NTSB noted.

However, the NTSB concluded that had the MDTA conducted a vulnerability assessment based on recent vessel traffic, it would have learned that the Key Bridge was above the AASHTO threshold of risk for catastrophic collapse from a vessel collision before the Dali collision occurred

and MDTA would have had information to “proactively reduce the bridge’s risk of a collapse and loss of lives associated with a vessel collision with the bridge.”

NTSB chair Jennifer Homendy said during its investigation her agency asked Maryland for the data needed to conduct an assessment based on current traffic volume but MDTA was unable to provide the data. NTSB had to develop the data itself. She said MDTA had still not done a vulnerability assessment based on current data as of October.

“Bridge owners need to know the risk and determine what action they need to take,” she told reporters.

MDTA said that an evaluation using AASHTO methodology was underway when the NTSB requested its results last fall and is still underway.

The MDTA said it is reviewing the NTSB recommendations but maintains the catastrophe and the tragic loss of life was the “sole fault of the DALI and the gross negligence of her owners and operators who put profits above safety.” It noted that the Key Bridge was approved and permitted by the federal government and in compliance with those permits.

MDTA said it will provide an update to the NTSB within 30 days.

NTSB has alerted officials in California, Delaware, Florida, Georgia, Illinois, Louisiana, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, Ohio, Oregon, Pennsylvania, Rhode Island, Texas, Washington, and Wisconsin. Baltimore’s Bay Bridge is among those on the NTSB list.

The NTSB is also recommending that FHWA, the U.S. Coast Guard, and the U.S. Army Corps of Engineers establish an inter-

disciplinary team to assist bridge owners on evaluating and reducing the risk, which could mean infrastructure improvements or operational changes.

The Collision

The 984-foot Singapore-flagged cargo vessel Dali was transiting out of Baltimore Harbor when it experienced a loss of electrical power and propulsion and struck the southern pier supporting the central truss spans of the Key Bridge, which subsequently collapsed. Six construction crewmembers were killed and another was injured, as well as one person onboard the vessel.

The Key Bridge and its pier protection systems were subject to regular safety inspections by nationally certified bridge inspectors. The Key Bridge’s most recent inspections in March 2021 and May 2023 found the condition of the deck, the superstructure, and the substructure as being in satisfactory condition, and the pier protection was rated as in place and functioning properly.

Researchers at Johns Hopkins University in Baltimore are working on a project assessing the country’s bridges to determine the likelihood of another disaster like the one that collapsed the Key Bridge.

A spokesperson for the research team told Insurance Journal that preliminary findings would be released soon.

The state of Maryland is suing the owner and operator of the Dali cargo ship that caused the collapse of the bridge, as have the families of six workers killed in the tragedy, the city of Baltimore, small businesses, and others.

The owner and manager of the Dali have denied responsibility and cast blame on the state for not better protecting the bridge against ship strikes.

The U.S. Department of Justice settled claims against the cargo ship Dali’s owner Grace Ocean Private Limited and operator Synergy Marine for $103 million last October.

The National Transportation Safety Board’s Marine Investigation Report is available online at: www.ntsb.gov/investigations/AccidentReports/Reports/MIR2510. pdf.

National

WSIA members elected Phillip McCrorie to serve as 2025-2026 WSIA Chair. McCrorie serves as CEO and chairman of RSUI. He joined the WSIA Board in 2021 and the executive committee in 2024. Others elected for one-year terms as officers include Vice Chair Patrick Albrecht, Associated Insurance Administrators, Inc., Montgomery, Alabama; Secretary Wendy Houser, Markel Specialty, Dallas, Texas; Treasurer Coryn Thalmann, Jimcor Agencies, Montvale, New Jersey; Immediate Past Chair Brenda (Ballard) Austenfeld, RT Specialty, Naples, Florida. Members elected to three-year terms as directors include Steve Boyd, Bridge Specialty Group, San Diego, California; Gerald Dupre, Core Specialty, Atlanta, Georgia; Danny Kaufman, Burns & Wilcox, Farmington Hills, Michigan; Neil Kessler, CRC Group, Dallas, Texas; Lou Levinson, Lexington Insurance Company, New York, New York; and Danielle Wade, Jackson Sumner & Associates, Boone, North Carolina. Outgoing directors include Annie Dawson, XS Brokers, Louisville, Kentucky (20242025) and Dave Obenauer, CRC Group, Charlotte, North Carolina (2015-2025).

Coalition, headquartered in San Francisco, hired Maha Virudhagiri as the company’s first chief technology officer (CTO). Virudhagiri will lead engineering, IT, infosec, data, Maha Virudhagiri

and artificial intelligence (AI) efforts. Virudhagiri spent nearly seven years at Tesla. Before Tesla, Virudhagiri held leadership roles at Ancestry® and Walmart Labs.

Porch Group Inc., headquartered in Seattle, named four new members to its leadership team. Porch Group named Eric Lemieur as head of insurance sales and distribution. Previously, Lemieur held sales leadership roles at Farmers Insurance and Foremost. Chad Mirock was named senior director, insurance product and strategy. He previously held product management leadership positions at Country Financial, The Hartford, and Travelers.

in Northbrook, Illinois, hired Andréa Carter as executive vice president and chief human resources officer, effective May 12. With nearly 30 years of experience, Carter joins Allstate from Global Payments Inc. Carter has also held human resources leadership roles at Habitat for Humanity, Ralph Lauren, Newell Rubbermaid and The Home Depot.

Tokio Marine HCC President Mike Schell will retire on March 31. Barry Cook, CEO of Tokio Marine HCC International, will additionally assume the newly created position of deputy CEO, effective April 1. Schell joined Houston-based Tokio Marine HCC in 2002 and retires after more than 50 years in the insurance industry.

Markel Group named Simon Wilson as CEO of Markel Insurance, which includes Markel Specialty, Markel International and Markel Global Reinsurance. Wilson was president of Markel International. Wilson joined the group in 2010 to lead international business development.

Anthony F. (Tony) Markel, currently vice chairman of the board, will retire as a company director in May and assume the honorary position of chairman emeritus of the board. Jon Michael was appointed to Markel’s board of directors.

Andréa Ferrari was named director, underwriting. Ferrari has over 20 years of industry experience and previously led underwriting at Kin and Hippo Emmanuel Bellegarde was named head of reinsurance. Bellegarde previously led North America Casualty Facultative reinsurance at McGill and Partners, and held reinsurance leadership roles at Aon Benfield, with additional insurance experience at Willis Towers Watson.

The Allstate Corp., based

Nationwide, headquartered in Columbus, Ohio, appointed Tonya Courtney to lead its new excess and surplus (E&S) brokerage property unit to open in the second half of the year. She joined Nationwide in December with more than 30 years of experience in commercial lines insurance.

Beazley, headquartered in London, England, appointed Lindsay Shipper as head of commercial property, North America. Based in Atlanta, Shipper has close to two decades of experience in the property market. She joins from Marsh, where in her 16-year career, she held several senior positions, most recently managing director and southeast zone property leader.

RateFast, headquartered in Santa Rosa, California, hired Joyce Reitman as its new CEO. She has over 30 years of industry experience, recently serving as CEO of Motionloft. The company also hired Michael Bongiovanni as its chief information officer. Bongiovanni has over 30 years of industry experience, most recently serving as vice president of sales at Sage Software. Marsha Bluto is RateFast’s new executive vice president of sales. She most recently served as vice

Eric Lemieur

Chad Mirock

Emmanuel Bellegarde

Tonya Courtney

Simon Wilson

Anthony Markel

Joyce Reitman

Marsha Bluto

president of medical management at PPMSI.

Ryan Specialty, headquartered in Chicago, promoted Matt Havey to president of its alternative risk underwriting business, Ryan Alternative Risk. Havey joined Ryan Specialty in 2024 as senior vice president of underwriting. With this promotion, CEO Kieran Dempsey separates president from his title.

East

Satellite Agency Network Group, Inc. (SAN), headquartered in Hampton, New Hampshire, appointed Michael Sakraida as regional vice president for Massachusetts, New Hampshire and Maine. Sakraida most recently served as senior project manager for Comparion Insurance Agency.

Executive Vice President and Head of Claim Paul Brady as CEO, effective June 1. Brady has been with Arbella for nearly 15 years, serving as chief information officer and senior vice president of operations. He succeeds John Donohue, who will continue as chairman of the board and CEO of the Arbella Insurance Foundation.

underwriting officer and chief claims officer.

Midwest

Southeast

Pro-Praxis, a Starwind Specialty Insurance Services program headquartered in New York City, appointed Joseph Washington as vice president of underwriting. With 30 years of underwriting experience, he previsouly served as an underwriting manager at Beazley, vice president at Berkshire Hathaway Specialty Insurance and assistant vice president at Zurich North America.

Arbella Insurance Group, headquartered in Quincy, Massachusetts, named

NJM Insurance Group’s President and Chief Executive Officer Mitch Livingston will retire on July 31 after 19 years at the company, including the past seven as its leader. The company’s board of directors has selected Carol Voorhees, NJM’s executive vice president and chief operating officer, to succeed Livingston. Voorhees joined NJM, based in Trenton, New Jersey, in 1996 and was named executive vice president & chief operating officer in 2024.

The Great Bay Insurance Group, headquartered in West Atlantic City, New Jersey, named Timothy J. Byrne, Jr., president of the group and Ronald R. Lovatt as president of Great Bay Insurance Company, a wholly owned affiliate of the group. Byrne Jr. previously served as the group’s chief operating officer. Lovatt, Lovatt, a founding member of the company, has 40 years of broad insurance industry experience. He currently serves as chief

NFP, an Aon company based in New York City, hired Priya Nathan as senior vice president, sales, in its Central region. Based in Austin, Texas, Nathan has over 25 years of multinational insurance experience and was a client executive in the tech practice at Marsh, vice president, insurance technology sales, for the Midwest region of Ventiv Technology (now Riskonnect), and director, sales operations, breach response, at AllClear ID (now Experian, Inc.).

Alera Group, headquartered in Deerfield, Illinois, appointed Talicia Bashford as managing director of the Midwest region. Bashford joined Alera Group in 2024 as the Mid-Atlantic property and casualty practice leader. With over 20 years of leadership experience, she most recently served as president of AssuredPartners of Chicago.

Brown & Riding, headquartered in Dallas, hired Nick Calabro as senior vice president of its national casualty practice. Based in Florida, Calabro has over 13 years of industry experience, previously serving as a casualty broker at CRC Insurance Services.

West

California Insurance Commissioner Ricardo Lara reappointed members Mitch Steiger and C. Bryan Little to the California Workers’ Compensation Insurance Rating Bureau (WCIRB) Governing Committee Lara also reappointed member Dr. Fabiola Cobarrubias to the Insurance Diversity Task Force.

Concert Group, headquartered in Chicago, appointed Thomas G. Sweeney as chief credit officer. Sweeney oversees all aspects of credit risk for Concert Group, including its admitted carrier, Concert Insurance Company, its non-admitted carrier, Concert Specialty Insurance Company, and its risk retention vehicle, Harmony Re. Sweeney has over 20 years of experience in finance and corporate development in the property and casualty re/insurance industry.

EPIC Insurance Brokers & Consultants, headquartered in San Francisco, named Matt Allen principal of its private client team. With over 18 years of experience in the insurance industry, Allen has dedicated his career to providing sports professionals with specialized risk management, disability insurance and asset protection solutions. He founded The Professional Athlete Insurance Group, a boutique agency designed to manage the unique lifestyles and insurance risks of individuals in sports. Most recently, Allen served as director of sports and entertainment at Gregory & Appel.

Michael Sakraida

Joseph Washington

Mitch Livingston

Carol Voorhees

Matt Allen

Nick Calabro

Thomas Sweeney

News & Markets

Claims Service, Tech, Communication Top Independent Agent Concerns

By Denise Johnson

Claims, communication, and technology are the top three concerns for independent agents when placing new business with a carrier, according to insurtech Vertafore.

The findings were the result of a survey of nearly 1,300 insurance professionals including account managers, agency owners and principals, producers (and others with sales titles), customer service representatives (CSRs), and operations professionals. A smaller segment of responses came from administrative, human resources (HR), data, or accounting professionals.

The report highlights the wants, needs, and challenges agents encounter in their daily interactions with carriers and the technology carriers can use to strengthen relationships.

The largest segment (33.2%) work with 11-20 carriers regularly.

The sur vey’s most well-rep-

resented respondents can be summarized as: Gen X, women, having 20 or more years of experience in insurance, being in an account manager role, at independent agencies with 7 to 25 employees, and working on behalf of 11 to 20 carrier partners.

Agents’ Top Factors When Placing Business With a Carrier

When asked how carriers could get more of their business, 84% respondents indicated that besides offering competitive products and pricing, responsiveness of underwriting ranked as the most important consideration. Claims ser vice emerged as a very significant factor influencing independent agents when plac ing business with a particular carrier. Delving into the impact of specific factors on placing business, producers and account managers ranked claims service as their most important criteria, with 75% of respondents deeming it a must-have. The second-ranked specific factor

considered when placing business is personal relationships—a must-have for 60%.

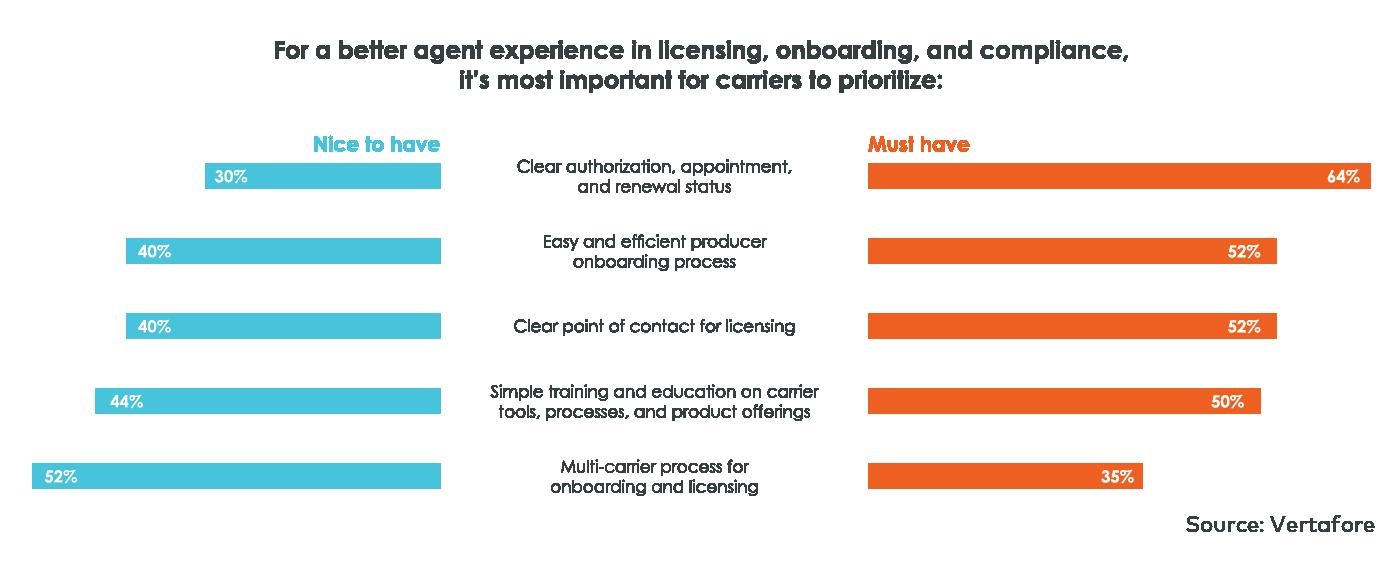

More than three-quarters (77%) of independent agent respondents agreed carriers should invest in better onboarding and licensing tools and processes. Only 33% of all respondents felt their primary carrier partners offered great service in their onboarding, licensing, and compliance practices.

Sixty-four percent said a must-have for a better onboarding and licensing experience is being able to easily view authorization, appointment, and renewal status.

Further insights into onboarding and licensing are summarized in the graphic on page 23.

Continuing on the theme of recommended carrier investments, 77% of producers and account managers also said that efficient, effective, and navigable carrier portals is a top area to improve. Fifty percent said participation in commercial lines raters is also

an important area for carriers to invest in. That contrasts with just 42% who cited the high importance of the ability to bind within a comparative rater for personal lines.

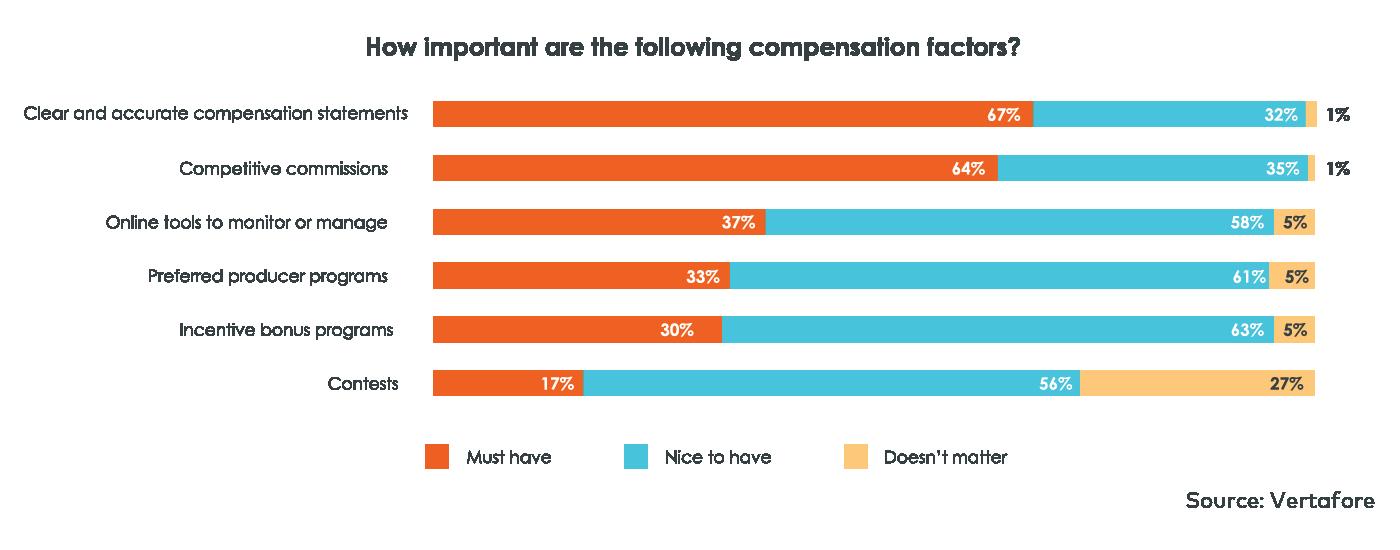

Roughly two-thirds of respondents (67%) indicated clear and accurate compensation statements as the top compensation-related factor for working with carriers, while competitive commissions came in second among various compensation factors that respondents ranked as important (64%).

Weighing the importance of various carrier technologies, 69% of independent agents said digital personal lines rating and submission was a must-have—the most for any technology.

Under writing service is an area where carriers could improve, according to the survey. A little over a quarter of respondents (28%) indicated top carriers provided great under writing service. Almost half (46%) described their carrier partners’ service as average, and 26% of respon-

dents said they typically experienced below-average service.

The top three underwriting capabilities sought by independent agents included responsiveness, competitive products, and pricing.

In the ser vicing category, 83% of independent agents listed the ability to check policyholder billing status online as the most important area for carriers to invest in. Nearly as many—80% of customer service representatives—also shared that the ability to view and make changes to policies online remains an important area for carrier investment.

On the claims front, survey analysis revealed that only 23% considered their primary carrier’s claims service to be excellent.

Seventy-eight percent of survey takers ranked ease of communication as a way for carriers to get more of their business, while 77% said the availability of efficient, effective, and navigable carrier portals is a critical area for investment.

Increasing Carrier-Agent Bond With Better Technology

Overall, responses show that a key differentiator in the agent experience is whether carriers use modern technology.

Customer service representatives (CSRs) said the ability to both check policyholder billing status (83%) and view and make changes to policies online (80%) should be the top priorities for carrier investment.

At the top of the rankings, survey respondents cited the necessity of digital rating and submission in personal lines as the most important technology capability, with 69% rating it a must-have. For digital rating and submission in commercial lines, 51% called this a must-have.

Digital document and policy delivery demonstrated its widespread utility, too, with 59% of respondents agreeing it was a must-have technology. Direct bill and commissions download (57%) and digital appetite and eligibility solutions (53%) ranked highly, as well.

Carriers that invest in

integrated, easy-to-navigate systems reduce the time agents spend on manual tasks, allowing them to increase the volume and quality of business the independent agent channel generates, the survey noted.

Not unexpectedly, carrier chatbots were viewed negatively.

Areas Where Carriers Can Place Less Emphasis

Respondents also provided insights on areas where carriers could reduce spending. These included mobile tools, with 23% of respondents indicating mobile tools are only of minor value in terms of how carriers could get more of their business.

Vertafore suggests this could be due to agents primarily working on their laptops while relying on their mobile devices for on-the-go or ancillary support.

As expected, there were some generational differences when it came to mobile app preferences.

Younger agents were significantly more likely to consider mobile apps to be

more than a convenience: 37% of respondents aged 18 to 27 and 32% of those aged 28 to 43 labeled carrier mobile apps a must-have technology.

Likewise, contests, incentives, or preferred producer programs were of relatively minor importance to 25% of respondents, mainly with those who have worked in the industry longest. However for new agents, 53% felt contests and incentives were a musthave when choosing a carrier.

Marketing materials were deemed the least important factor and, as such, an area where carriers could reduce investment.

“Efficient, streamlined processes are the foundation of the agent-carrier relationship and a positive agent experience,” said Kelly Maheu, vice president of partnerships and industry relations at Vertafore.

“This report highlights how carriers and agents rely on technology to make agents’ work easier while bringing the human element into the process to strengthen relationships across the distribution channel,” Maheu said.

Spotlight: Trucks & Fleets

Why Some Transportation Risks Could Find Options With Captives: Risky Future Webinar

By Allen Laman

Standard market woes, captive growth, and the increased importance of navigating relationships with third-party administrators—insurance experts in the commercial trucking arena have helped their clients traverse a challenging road in recent years.

Earlier this month, a panel of transportation insurance experts dissected these issues and more during an Insurance Journal webinar.

Traditional Insurance Market Overview

Kenny Planeta, the senior vice president and transportation practice leader at Heffernan Insurance Brokers, explained that 5-10% premium increases in the standard market are considered wins for trucking clients.

Flat renewals and decreases are “unheard of,” Planeta said,

pointing to carrier losses in the commercial trucking line.

“The good performers are kind of subsidizing the bad performers,” he said. “Everybody’s heard the term ‘nuclear verdicts.’ I think the biggest impact we see on trucking companies is not necessarily fleets that are getting hit with that nuclear verdict … it’s the fear of that big verdict and not wanting anything to go to trial.”

Planeta continued: “Darn near any loss does not go to trial anymore. Everything gets settled outside of court, goes to mediation, and these settlements just keep growing. These attorneys rack up these bills, and in turn, it causes the premiums to go up.”

Cheri McGonagill-Spann, national sales and account manager for transportation and cargo at claims management and outsourcing provider Crawford and Company, echoed Planeta’s comments. She said claims have increased

and that “nuclear verdicts are especially troublesome” in commercial transportation.

“Companies are … increasingly frustrated with the traditional landscape,” said David Hoag, AVP and business development manager at Crawford. Hoag said the hard insurance market makes it a “difficult market to place business sometimes.”

“The value added for [companies] in a captive is they have more control,” he added.

Alternative Market Options: Member-Owned Captives

Garrett Yates, vice president at Heffernan, said a knowledge gap exists between insurance agencies and the captive insurance arena.

Member-owned captive insurance programs are designed to give companies more control over premiums. Successful captive managers communicate with members and assemble teams of CPAs to

handle finances and work with third-party administrators, reinsurers, loss control, and brokers.

The product is essentially an insurance company; the key difference is that trucking companies have “a lot more skin in the game” than they would with a traditional insurance policy, Planeta said. Transparency, accountability, and predictability are also increased.

Upfront costs notwithstanding, costs are lower, Hoag explained, and captives can be designed to fit a business model or need.

“Obviously, there is an initial cost, and that varies depending upon what the risk is and what have you,” Hoag said, later adding that the positive results of that are “that you’re forming a captive, designing it, and you can control your costs as long as you have that dedicated team working that captive on a daily basis.”

Structural elements of captives like claim-funding models and collateralization vary. TPAs like Crawford play a key role in handling and administering claims. In some cases, insurance companies serving as reinsurance for the captive will handle claims with their claims team.

“That model can be really good if it’s a good partner on the claims handling with the reinsurance,” Planeta said. “But a lot of the member-owned group captives have gone to kind of like an à la carte type situation … and the reason why you would want to split those up potentially is because the members get to look at it and say, ‘Are we happy with the claims handling that we’re getting? Is this TPA doing a good job getting on top of these claims [and] keeping us informed?’”

Heffernan has worked with multiple captives who have fired multiple TPAs because members don’t believe they’re doing a good job and voted them out. Similarly, Planeta explained they’ve also seen insurance companies lose reinsurance and claims handling responsibilities.

Hoag added that while group captives are a fit for more businesses, when it comes to a single captive, “that’s something for a Fortune 500 company. That’s a high consideration for a Fortune 500 company.”

Who Is Best Suited for a Captive?

In a nutshell, joining a captive makes sense for trucking clients who believe they are performing better than their peers claim-wise and still see their premium increasing annually, Planeta explained.

“In a group captive … you’re individually underwritten,” he said. “You know when your insurance premium is going to go up because your five years [of] loss history is worse than it was when you joined the group.”

From a high-level perspective, Planeta said that trucking companies need to have their house in order, from a safety standpoint, “because you’re going to be taking on more risk. You’re no longer transferring it all to the insurance company.”

Those who don’t are gambling and won’t win, he added. Most member-owned group captives have entry barriers like safety scores and claims history. Planeta said the captives that Heffernan works with make requirements and collateral entry and exit timelines clear.

Future Captive Growth and Opportunities

A decade or so ago, businesses would talk about group captives and large deductibles when their fleets had 50 trucks. That’s how many it

would take for premiums to hit $250,000, Planeta explained, but as premium dollars have increased, that starting point now looks like a 25-unit fleet.

And if they have their risk management and safety in order and have a predictable, good claims history, “now it makes sense for them,” he continued. “And 10 years ago, when they were paying $100,000 for 25 trucks, they just weren’t large enough to have it make sense.”

Heffernan has watched most of the trucking captives the brokerage has worked with double in size in the last five years. They continue to spin off new groups, Planeta said, because the market is there.

Plucking the best risks in the market and formulating and creating a rating structure based on individual performance present “a tremendous opportunity for a lot of companies,” Yates said.

“There’s a couple of major players in the captive arena,” Yates shared later. “The new captives that do continue to pop up are still within the same captive managers, which I think is really important, because you’ve got the history, the longevity, [and] the performance.”

He also explained that some direct markets are seeing that there is money to be made in the captive arena, “because there are a lot of really good

risks out there.”

His advice to clients: Pick experienced partners when choosing or building a captive that has a history of doing a good job. This is important not just from a captive, claims, and reinsurance management perspective but also for the money managers overseeing the captive’s investment fund.

“There’s a large amount of income for the clients that could be achieved through that process as well,” Yates said.

Go Deeper

This webinar marked the first in a series leading into Insurance Journal’s Risky Future Summit on Nov. 4. Attendees of that online event will learn from risk managers with a proven track record in safeguarding companies and clients as they showcase the benefits of robust risk management and highlight the consequences of oversight. Visit RiskyFuture.com to learn more and save your seat.

To watch a recording of the transportation panel discussion outlined in this story, visit the Insurance Journal Research and Trends website.

To view the full webinar, A Risky Future Webinar: Transportation, Captives, and Alternative Markets, visit https://www.insurancejournal. com/research/

Garrett Yates Kenny Planeta

Cheri McGonagill-Spann

David Hoag

Spotlight: Architects & Engineers

Inflation, Rising Claim Costs, Riskier Business Reasons Cited for Rate Increases in A&E Market: Survey

Architects and engineers

professional liability insurers report concerns about the persistent effects of inflation on claim expenses, uncertainty about the U.S. economy, higher risk project types and professional design disciplines, as well as new exposures from artificial intelligence (AI), according to a recent industry survey by specialty broker Ames & Gough.

The survey, which polled 17 insurance companies that represent a significant percentage of the overall marketplace providing professional liability insurance to architects and engineers in the U.S., revealed that most insurers plan to raise rates this year.

According to the survey, 71% of A&E insurers are planning rate increases in 2025, 24% plan to keep rates flat, and only one insurer expects to reduce rates. Among the insurers raising rates, all but one are planning modest increases (up to 5%), with the other planning a rate increase of 6-10%.

Inflation and Claims Costs

Of the insurers surveyed, 53% experienced higher claim severity in 2024 compared with 41% the prior year. Meanwhile, only 12% reported lower claim severity year-over-year.

Even with overall inflation reportedly easing in 2024, most (83%) insurers cited inflation as having an impact on their decision to raise rates. Higher costs for construction materials, supplies, and labor was cited as leading to higher damages and settlements. But most insurers pointed to social

inflation, particularly jury awards and litigation trends, as contributing to higher claim payouts as well. One insurer estimated claim costs are rising 3-5% annually.

Nearly all insurers surveyed reported paying multi-milliondollar claims in 2024, with 82% paying a claim between $1 million and $4.9 million, and one insurer reported playing a claim of $5 million or more; that claim exceeded $20 million.

When asked to rank the top three disciplines for claim severity, 70% of the insurers surveyed cited structural engineering; the same percentage identified architecture, followed by civil engineering (59%).

Added Capacity

Although the insurers surveyed reported no change in the availability of professional liability limits, some now appear willing to offer more capacity. This year, 53% indicated they can provide limits exceeding $5 million (up from 40% in 2024). In addition, 29%

indicated they can offer limits of up to $10 million; 6%, up to $15 million; 6%, up to $20 million; and 12%, $25 million or above.

“Even though some insurers can offer higher limits, they still apply greater underwriting scrutiny to these requests,” said Jared Maxwell, vice president and partner, Ames & Gough and author of the survey. “When faced with these requirements, design firms should try negotiating with owners to ascertain that higher limits are warranted. If so, they might consider alternative structures, such as specific additional limits endorsements/project excess or try building layers with multiple insurers.”

2025 Rates

This year, 67% of the insurers surveyed plan to target rate increases on accounts with adverse loss experience; 42% will target firms with what they consider higher-risk projects, such as condominiums and other residential construction, and

infrastructure. Some 42% reported targeting higher-risk disciplines, including structural engineering, geotech, civil, and mechanical engineering. One-third (33%) reported planning increases across their entire book of business.

M&A and AI

Insurers also had concerns about the jump in merger and acquisition activity among design firms, noting the involvement of private equity firms may hasten the speed of the transactions and cause principals to overlook effective integration of risk management.

With more design firms integrating AI into their processes, 76% of the insurers surveyed indicated they are carefully monitoring these developments and their potential effects on claim activity. A potential scenario: A/E firms incorporating outdated or incorrect designs from internal AI libraries may be vulnerable to repetitive design errors and violations of technical standards or codes of conduct.

News & Markets

California Cites Contractor $157K Following Fatal Trench Accident

Aconstruction company was fined $157,500 by California for multiple violations of workplace safety regulations following a fatal trench collapse.

W.A. Rasic Construction was fined by the California Division of Occupational Safety and Health incident over the death of an employee working in an unprotected excavation on Aug. 28, 2024, according to

Cal/OSHA.

The worker was reportedly inside a 17-foot-deep trench when a portion of it collapsed and caused a concrete pipe to be displaced, pinning and killing the employee.

Cal/OSHA’s investigation identified serious violations of workplace safety regulations related to excavation and trench safety.

Reported Cal/OSHA include:

• Failure to implement an effective injury and illness prevention program. W. A. Rasic Construction did not implement an effective injury and illness prevention program to identify, evaluate, and correct workplace hazards, and provide training. The failure exposed employees to the hazards associated with working in an unshored trench.

• The employer failed to conduct a proper site inspection and failed to identify conditions that could lead to dangerous cave-in hazards or the lack of necessary protective systems, such as trench boxes or shoring.

• The employer did not provide the necessary cave-in protection for employees working in an excavation roughly 17 feet deep. This safety failure exposed workers to the risk of fatal injury, as evidenced by the incident.

Employers have the right to appeal any Cal/OSHA citation and notification of penalty by filing an appeal with the Occupational Safety and Health Appeals Board within 15 working days from the receipt of notification.

Nearly a Quarter of Homes in New Mexico Uninsured, Report Shows

New Mexico has the highest rate of uninsured homes in a report that also shows nearly one-in-seven U.S. homes are uninsured, and 11.3 million out of 82.9 million owner-occupied homes (13.6%) are uninsured.

A rerport from LendingTree that used Federal Emergency Management Agency data and U.S. Census data to calculate uninsured rates. It also used FEMA data to examine uninsured rates in the 25 most at-risk counties, which it categorized uninsured homes as owner-occupied homes with annual home insurance costs of less than $100.

The report found New Mexico had the highest rate of uninsured homes at 23.3%. West Virginia (23.0%) and Mississippi (22.9%) were two and three on the list.

Other findings show:

• Among the largest U.S. metros, McAllen,

Texas, has the highest uninsured rate at 43.3%. El Paso (23.0%), and Miami (21.0%) followed.

• The counties with the highest National Risk Index scores most at risk are Miami-Dade County, which tops the list at 23.5%. Florida counties of Broward (22.7%) and Lee (17.9%) followed.

• The District of Columbia has the lowest rate of uninsured homes (8.9%). New Hampshire (9.2%), Oregon (9.6%), Massachusetts (9.7%) and Utah (9.7%) are metros others below 10.0%

LendingTree home insurance expert surmised that homeowners in states with high rates of uninsured homes may overlook crucial risks.

“Wind and hail damage is the most common homeowners insurance claim,” he stated. “Of the top three states, this is especially true in Mississippi. Wind and hail damage is covered by standard homeowners insurance in most parts of the country. However, you have to buy windstorm coverage separately in some of Mississippi’s coastal areas.”

My New Markets

Service Contractor Surety Bond

Market Detail: RevBond writes an extensive line of surety products on A.M. Best Rated A- (Excellent) paper and is licensed in all 50 states. RevBond can support service contract needs by focusing on the small to mid-size surety market (Single bonds up to $10,000,000 and Aggregations up to $10,000,000). Has pen and writes the following: environmental spill response, guard services, waste hauling/recycling, janitorial service contractors, student bus transportation services, landscaping, highway maintenance/mowing, aggregate supply, railroad repair and road maintenance.

Available Limits: Not disclosed.

Carrier: Not disclosed.

States: All 50 states and the District of Columbia

Contact: Chris Dobbs; chris.dobbs@ revbond.com; 623-469-5821.

Builder’s Risk Insurance

Market Detail: Insight Risk offers comprehensive Builder’s Risk insurance coverage to protect vertical construction projects against property losses and delay, including ground-up and renovation risks. As a technology-driven MGA, Insight Risk Technologies is reinventing Builder’s Risk insurance through a unique combination of granular, fact-based underwriting, proactive risk management, and proven risk mitigation IoT technologies deployed on each project. Superior financial and operational results for all stakeholders: contractors, developers, risk managers, brokers, and carriers. Target Class: Fire-resistive and non-combustible construction. Referral Classes: Wood frame and joisted-masonry construction. Target

Occupancies: Offices, Educational (K-12 & Post-Secondary), Healthcare, Institutional, Apartments, and Hotels. Construction Size: $25M to $250M in TIV. Capabilities: 100% and lead Q/S lines with limited follow-line Q/S capacity -- Project Specific, Master Builder’s Risk, or Multi-building Available Limits: Not disclosed. Carrier: Not disclosed.

States: All 50 states and the District of Columbia Contact: Lisa Behning; lisa.behning@ insightrisktec.com; 475-259-2837.

Short-Term Liability - Auto Physical Damage (DST)

Market Detail: This coverage is available when moving a unit from one location to another. Has pen.