FEATURE THE EVOLUTION OF ROLLOVER ADVISING

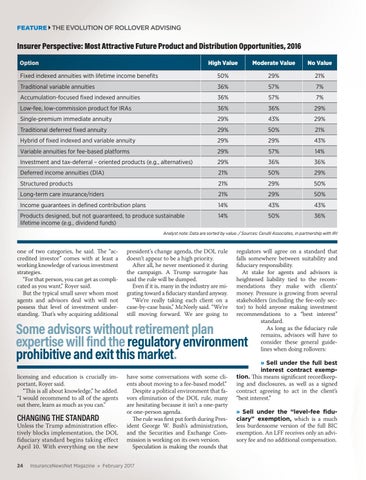

Insurer Perspective: Most Attractive Future Product and Distribution Opportunities, 2016 Option

High Value

Moderate Value

No Value

Fixed indexed annuities with lifetime income benefits

50%

29%

21%

Traditional variable annuities

36%

57%

7%

Accumulation-focused fixed indexed annuities

36%

57%

7%

Low-fee, low-commission product for IRAs

36%

36%

29%

Single-premium immediate annuity

29%

43%

29%

Traditional deferred fixed annuity

29%

50%

21%

Hybrid of fixed indexed and variable annuity

29%

29%

43%

Variable annuities for fee-based platforms

29%

57%

14%

Investment and tax-deferral – oriented products (e.g., alternatives)

29%

36%

36%

Deferred income annuities (DIA)

21%

50%

29%

Structured products

21%

29%

50%

Long-term care insurance/riders

21%

29%

50%

Income guarantees in defined contribution plans

14%

43%

43%

Products designed, but not guaranteed, to produce sustainable lifetime income (e.g., dividend funds)

14%

50%

36%

Analyst note: Data are sorted by value. / Sources: Cerulli Associates, in partnership with IRI

one of two categories, he said. The “accredited investor” comes with at least a working knowledge of various investment strategies. “For that person, you can get as complicated as you want,” Royer said. But the typical small saver whom most agents and advisors deal with will not possess that level of investment understanding. That’s why acquiring additional

president’s change agenda, the DOL rule doesn’t appear to be a high priority. After all, he never mentioned it during the campaign. A Trump surrogate has said the rule will be dumped. Even if it is, many in the industry are migrating toward a fiduciary standard anyway. “We’re really taking each client on a case-by-case basis,” McNeely said. “We’re still moving forward. We are going to

regulators will agree on a standard that falls somewhere between suitability and fiduciary responsibility. At stake for agents and advisors is heightened liability tied to the recommendations they make with clients’ money. Pressure is growing from several stakeholders (including the fee-only sector) to hold anyone making investment recommendations to a “best interest” standard. As long as the fiduciary rule remains, advisors will have to consider these general guidelines when doing rollovers:

Some advisors without retirement plan expertise will find the regulatory environment prohibitive and exit this market. licensing and education is crucially important, Royer said. “This is all about knowledge,” he added. “I would recommend to all of the agents out there, learn as much as you can.”

CHANGING THE STANDARD

Unless the Trump administration effectively blocks implementation, the DOL fiduciary standard begins taking effect April 10. With everything on the new 24

have some conversations with some clients about moving to a fee-based model.” Despite a political environment that favors elimination of the DOL rule, many are hesitating because it isn’t a one-party or one-person agenda. The rule was first put forth during President George W. Bush’s administration, and the Securities and Exchange Commission is working on its own version. Speculation is making the rounds that

InsuranceNewsNet Magazine » February 2017

» Sell under the full best interest contract exemption. This means significant recordkeeping and disclosures, as well as a signed contract agreeing to act in the client’s “best interest.” » Sell under the “level-fee fiduciary” exemption, which is a much less burdensome version of the full BIC exemption. An LFF receives only an advisory fee and no additional compensation.