Advisors turn their attention to helping younger women form good financial habits and protect what’s important to them.

PAGE 8

Annuities: Unlocking the tech advantage with SILAC’s Dan Acker PAGE 4

How health care costs change the face of women’s planning PAGE 26

Offshore reinsurance booms as regulators play catch-up PAGE 34

THE GREATEST ANNUITY MOVIE EVER CREATED FOR ADVISORS!

Introducing Retirement Everest—the groundbreaking new film where producers travel to Mount Everest to share the most compelling story ever told for financial advisors and their clients. Now, YOU can even star in this incredible film and harness its power!

The Big Idea: Decumulation is the OPPOSITE of Accumulation!

Reaching Everest’s summit is tough, but the descent is more dangerous. Similarly, retirement’s biggest challenges— market risk, inflation, and healthcare—come after retirement. Retirement Everest shows why retirees need a guaranteed income strategy and a Decumulation Expert, with insights from Nobel Prize-winning economists and expert advisors.

5 Reasons Theater Events Are the Best Way to Generate Appointments

1. The Perfect Pitch Every Time – This film brings your message to life.

2. Speed to Conversion – Nothing turns cold prospects to buyers faster.

3. The Perfect Environment – Attendees are focused and engaged.

4. No Presentations Required – Welcome the audience, play the movie, and let it do the work.

5. Demonstration – Visually shows the benefits of annuities and guaranteed income.

Included in this FREE package:

• See the movie trailer with actual footage from Mount Everest, worldrenowned climbing experts, and reallife client stories.

» The Results?

Movie theater events crush traditional workshops!

The average event produces…

• 105 leads

• 23 appointments

• $500K to $2M in premium

Plus, they’re exclusive, fun, and give you a major edge

• Case study “How Greg is writing over $1M on EVERY movie event.

• The A to Z guide on how to use movie events to explode your business.

• See how you can even star in the film!

IN THIS ISSUE

INTERVIEW

4 Annuities: Unlocking the tech advantage

Dan Acker, president of SILAC, describes the company’s growth in the annuity market and why technology is the key.

IN THE FIELD

12 Leading from the front

By Susan Rupe

Sam Philbrook took the lessons in leadership and service he learned in the Army to serve his clients and community.

FEATURE

Help women become CFOs of their own lives

By Susan Rupe

Advisors are finding younger women to be a demographic that needs help planning and protecting.

18 Overcoming ‘I need to think about it’

By Drew Gurley

The most common objections to buying life insurance and how to turn them around.

ADVISORNEWS

30 Weathering the storm: Investing with confidence in volatile markets

By Nicholas Breit

Adhering to an investment plan is crucial during periods of market stress.

BUSINESS

32 The six golden rules of client scheduling By Gina Pellegrini

Ways to ensure a steady flow of opportunities while nurturing your client base.

ANNUITY

22 Defined benefit annuity: The next great innovation

By David Macchia

Transformative technology creates the first personal defined benefit pension funded by a fixed indexed annuity.

HEALTH/BENEFITS

26 How health care costs change the face of women’s planning

By Holly Westervelt

Rising health care costs and unpaid caregiving responsibilities impact women’s retirement security.

IN THE KNOW

34 Offshore reinsurance booms as regulators play catch-up

By John Hilton

Regulators are growing concerned about the increasing amounts of life and annuity blocks reinsured outside the U.S.

Navigating the great wealth transfer

The landscape of wealth management is undergoing an enormous transformation, driven by the “great wealth transfer.” This shift, involving the transfer of trillions of dollars from baby boomers to younger generations, is placing women at the forefront of financial decision-making and wealth administration. For agents and advisors, understanding these evolving roles is crucial to effectively supporting their female clients.

About 70% to 80% of widows change their financial advisors within a year of their husband’s death, according to a number of studies. This often happens because many women believe their previous advisors primarily communicated with their husbands and didn’t build a strong relationship with them. This signals a significant opportunity for agents and advisors to build stronger relationships with both partners. Reaching out to ensure that women are involved, informed and educated about family finances before they become the primary decision-maker is crucial to ensure continuity and support during such transitions.

The great wealth transfer: A historic shift

The great wealth transfer is projected to involve the transfer of approximately $124 trillion over the next few decades. By 2030, it is estimated that two-thirds of private wealth in the U.S. will be held by women. This shift is not just about the transfer of assets; it represents a fundamental change in who controls wealth and how it is managed.

Women as wealth administrators

The great wealth transfer comes with unique challenges and opportunities that financial advisors must navigate to provide effective guidance.

1. Increased financial responsibility: Women are now responsible for managing significant assets, often for the first time.

This includes making investment deci sions, planning for retirement and ensur ing long-term financial security. Advisors should provide comprehensive financial education to empower women with the knowledge and confidence needed to man age their wealth effectively.

2. Longer life expectancy and lon gevity risk: Women, on average, live longer than men, which means women’s retirement savings must last longer. This increases the risk of outliving their savings, making it essential to plan for long-term income sustainability. Advisors should consider strategies such as delaying Social Security benefits to maximize payouts and exploring annuities and other lifetime income options.

3. Navigating emotional and finan cial complexities: Wealth transfers often occur during times of great loss, such as the death of a spouse. Managing financial transitions while navigating grief can be daunting. Advisors should provide support and guidance to help women manage immediate complexities while planning long-term strategies.

for longer life expectancy, career breaks and caregiving responsibilities. Use holistic approaches that consider both emotional and financial aspects.

4. Career breaks and caregiving responsibilities: Many women take time off to care for children or aging parents, leading to gaps in earnings and reduced Social Security benefits. Advisors should encourage continued contributions to individual retirement accounts or spousal IRAs during career breaks and consider longterm care insurance to cover future caregiving expenses.

Strategies for financial advisors

To effectively support female clients in their new roles as wealth administrators and decision-makers, financial advisors and insurance agents should adopt a proactive and empathetic approach. Here are some strategies.

1. Educate and empower: Provide financial literacy education tailored to women’s unique needs. Empower them to take control of their financial futures by

3. Maximize Social Security benefits: Help clients understand their Social Security options and optimize their benefits. Explore spousal or survivor benefits for those who have taken career breaks.

4. Diversify income sources: Encourage diversification of retirement income sources beyond Social Security and pensions: annuities, insurance, investments and other income-generating assets.

5. Support during transitions: Provide compassionate support during major life transitions, such as widowhood. Offer guidance to navigate emotional and financial complexities in order to ensure longterm financial stability.

By understanding the unique challenges women face and adopting strategies that empower and educate, advisors can help their female clients achieve financial independence and security in retirement.

John Forcucci Editor-in-chief

How will tariffs impact the insurance industry?

The insurance industry, already girding for the impact President Donald Trump’s tariffs will bring to its business, is facing even broader repercussions from the administration’s policies, well beyond what tariffs could bear.

Auto and home insurance are likely to be affected by the shifting policies, raising prices for consumers and eating into insurers’ profits.

Because homes and cars are “bundles of lumber, steel, aluminum, and semiconductors,” the president’s plans to tax all those materials at double-digit rates will spur inflation that will course through repair or replace costs for autos, said Rep. Jay Auchincloss, D-Mass.

Home insurance may be even more sensitive to the president’s agenda, said Auchincloss, who was an executive at Liberty Mutual, where he led product development before running for Congress. Because nearly 15% of total U.S. imports are in construction-related goods (Canada alone accounts for 50% of wood imports), the material costs of home construction and repairs will surge, along with labor costs.

US HOUSEHOLDS ARE RUNNING OUT OF EMERGENCY FUNDS

Pandemic cash has run out and inflation has taken its toll on household finances. The result is that more Americans are finding it difficult to come up with money to cover an unexpected expense, the New York Federal Reserve reported.

The bank’s Survey of Consumer Expectations found that the average likelihood of Americans being able to come up with $2,000 within a month if an unexpected need arose hit 62.7%. That’s the lowest level since the survey began tracking the data point in October 2015.

The inability of households to keep up financially, combined with uncertainty

about the future, has spilled over into the retail arena as well. Walmart CEO Doug McMillon recently told an audience at an Economic Club of Chicago event that he has seen some customers who are under budget pressures exhibit stress behaviors.

“You can see that the money runs out before the month is gone. You can see that people are buying smaller pack sizes at the end of the month,” he said.

AMERICANS LOST $5.7B TO INVESTMENT SCAMS

Americans reported losing $5.7 billion to investment scams in 2024, according to the Federal Trade Commission, with the typical victim losing more than $9,000 on average.

We need policy clarity. Until then, markets will have a hard time finding their footing.”

— Brian Levitt, Invesco global market strategist

The FTC warned of what it called “pig-butchering scams,” a common investment fraud whereby scammers develop a relationship with victims, entice them to invest money and then swindle them.

Three common signs of fraud that can help people avoid being duped are: an investment pitch that has a sense of urgency attached to it, an offer that asks you to pay in cryptocurrency or gift cards, and anyone who asks you not to tell others about the offer.

POLITICAL TURMOIL OUTSTRIPS INFLATION AS AMERICANS’ TOP FINANCIAL WORRY

While more than 4 in 10 Americans surveyed named inflation as a major economic concern, the U.S. political environment topped inflation as their top financial worry

These were the findings according to a new report by Hearts & Wallets, “Advice, Technology & Actions: Engagement with Human and Digital Influences and the Connection to Outcomes.” Top financial worries, in order, were:

• U.S. political environment: 47%

• Inflation: 44%

• Future of Social Security: 39%

• U.S. economy: 39%

• Future of health care in the U.S.: 35%

• U.S. deficit/future tax increases: 34%

• Conflict around the world: 33%

Building on SILAC’s annuity success, President and Chief Marketing Officer Dan Acker sees technology as the key to unlocking future growth.

An interview with Paul Feldman, publisher

When Dan Acker met Conseco founder and current SILAC CEO Steve Hilbert in 2016, it led to a relationship that eventually brought Acker to SILAC and an opportunity to help build an annuity juggernaut.

Today, riding high on the crest of annuity growth, Acker sees technology as key to building on the company’s current success.

“The average age for someone who’s buying one of our annuity products is

69 years old,” explains Acker. “And that’s probably consistent across the industry. But in my mind, there’s no reason more people in their 40s shouldn’t buy our products. They may not have $100,000 or more to put into an annuity, but there’s no reason they can’t start smaller and have a safer component within their portfolio.”

Technology is also key to working with independent agents, he says. “At SILAC, we’re trying to put ourselves in the shoes of a producer at that point of sale. How can we make it easier?”

In this interview with InsuranceNewsNet

Publisher Paul Feldman, Acker describes his journey into the top echelons of the industry and how he and SILAC are working to “change the industry for the better in our own way.”

Paul Feldman: How did you get into the industry?

Dan Acker: I was going to school at the University of Utah to finish my bachelor’s degree, and in 1998 I needed a job

to pay for school. There was a company that was advertising at the University of Utah named Educators Mutual. I joined the company in August 1998 as a billing clerk. I worked there up until 2005. And when I left in 2005, I was assistant vice president of finance — I had been given an opportunity to be controller that I probably didn’t deserve. But I had a great boss who gave me that opportunity, and that’s what really set the stage for my future career in the insurance industry. So it was not by design that I got into the industry, it was out of necessity. The industry has been tremendous to me professionally and personally. And I think it’s undervalued, underestimated. It seems like a boring industry, and it’s not that.

Feldman: Tell me about SILAC. You were involved in the early days of the company, correct?

Acker: Yes. Prior to joining SILAC, I worked for a company called Sentinel Security Life. When I joined Sentinel in 2005, it had 12 employees, and it was selling final expense coverage. I was hired to try to figure out a way to grow the company because they were losing more policyholders than they were gaining every year.

I already had the finance side, the statutory accounting side, down from working at Educators Mutual in the finance accounting area. Since Sentinel was such a small company, I had the opportunity to work in all other areas of insurance and have hands-on experience developing new products: Medicare supplement, hospital indemnity and, most importantly, annuities.

When I left in 2018 to join SILAC, Sentinel had gone from 12 employees to close to 300. I met the CEO of SILAC — our current CEO, Steve Hilbert — in 2016, just by chance at an industry event. Steve had previously founded Conseco, one of the largest insurance companies in the country. In 2017, he acquired a company called Equitable in Salt Lake City that was just down the street from Sentinel’s headquarters. After he acquired Equitable — which is now SILAC — in 2017, he’d come to Salt Lake City and we’d get together every once in a while. Fast-forward to 2018,

I called Steve and said, “Look, if you’re ever looking for somebody or there’s an opportunity, I’d love to join your team.” I joined SILAC in June 2018. For me it was a chance to learn from one of the greatest CEOs our industry has ever seen, and it was also an opportunity.

At the time, Equitable was not in the annuity space; it was in long-term care, Medicare supplement, traditional senior

is complexity of the annuities and getting the story out there. There are a lot of misperceptions. Our products are complex by design, just given their nature. So we don’t need to make them any more complex. Our goal from the start was to make these products as simple as possible and easier for the producer to understand and sell, and easier for the consumer to understand.

market products. My directive was to eventually close down all those product lines and get SILAC into the annuity space. For me, it was an opportunity to be part of building a second annuity carrier — Sentinel being my first, SILAC being the second.

It was a unique opportunity: one, working with Steve Hilbert; two, getting to help another carrier in the annuity space. SILAC/Equitable has a long history, with more than 87 years in business. I would say we’re still in our startup phase. Our goal is to change the industry for the better in our own way. That’s what we’ve been doing since 2018.

Feldman: How are you trying to change the industry for the better?

Acker: Early on, I had the opportunity to hire some great people who I’ve known for a long time and worked with, one being Carrie Freeberg, senior vice president of product and marketing at SILAC. She heads up our product development department and works with our marketing team with me.

But, looking at products, I think one of the challenges facing our industry

One of the positive things about SILAC coming into the industry is to get back to the basics of what a fixed indexed annuity does and that safe accumulation — lifetime income with principal production. No loss of principal. Sometimes a loss of principal comes in the form of fees. That’s another thing we have been able to do with SILAC, which is roll out some very competitive fixed indexed annuities. But we do not charge the consumer any fees. Let’s say we have a year where the S&P is down and we know with an FIA, the consumer is not going to lose any principal. But then the advisor has to sit down with that consumer and say, well, good news, you didn’t lose any principal, but you actually did lose 1% to 2% in the form of fees. That doesn’t leave a good taste in anybody’s mouth. Another way we’re trying to make things better is through education, and not only for advisors. I just finished a call with a young advisor who does business with SILAC and who is very good at teaching agents how to sell annuities, or how to sell a different type of annuity. Early in my career, I used to think the big carriers were providing that type of education, but I’ve come to learn, nobody

Dan Acker (right) with good friend and retired SILAC Vice President Richard (Bubba) Morrow.

is teaching agents how to sell and keep it simple. As an industry, I think we can do a lot more to talk positively about our products and what they do, because there’s no other product in the market like an FIA that offers some upside, some growth, lifetime income and zero downside risk.

Feldman: There are so many advantages to owning an annuity. What can the industry do to better educate the public about annuities?

Acker: There are a lot of positive things going on. For example, the Alliance for Lifetime Income, which carriers have partnered on. I think initiatives where the industry comes together and works to promote our products — not a particular carrier’s product — are positive. We need to take our carrier hats off, set our egos aside, and work together collectively to educate our country about these products and what they do.

Feldman: Indexed annuities are coming off four consecutive years of record growth. Our markets are changing. We have a new administration. Where do you see the market going over the next two years?

Acker: Our industry has seen tremendous growth, but I don’t know how much of that growth is truly organic and new growth. Given the interest rate changes, there’s a lot of replacement going on in our industry, which is great because it’s allowing consumers to move into products with the much higher current rates. However, there’s also a downside, because that means folks are leaving contracts early, which is not always a good thing from a carrier perspective. I would love to see more organic growth, see the number of first-time annuity buyers grow. I think if that was up 300%, that would be tremendously positive for our industry. As the replacement business begins to die down, there are fewer opportunities to move consumers to higher rates. I think overall we’ll probably see sales come down slightly within the next year, but I don’t view that as necessarily negative if we can continue to focus on first-time annuity buyers and increase that number.

Feldman: As an industry, we must do better at communicating the benefits of annuities. I think we would have more organic growth, and I do think that’s a problem in the industry.

Acker: There has been a lot of news obviously since 2016 and even before that with the Department of Labor and various rulings. But I think one thing that has come out of the various conversations and the potential regulation from the Department of Labor is that it has raised awareness of our product. Producers who hold more than an insurance license are beginning to understand the importance of our products and what they do. That’s a positive for the industry. SILAC operates in the independent agent channel, which is made up of insurance producers but also those who hold various securities licenses. The more traditional financial advisors, if you will, who are marketing our products, the better it is for our industry. Again, it’s just another avenue of raising awareness of what fixed indexed annuities and other annuities can do for a consumer.

And annuities shouldn’t be the only thing in a consumer’s portfolio, but there definitely is a place in every consumer’s portfolio, in my mind, for a fixed indexed annuity or other annuity. As an industry — at least at SILAC, traditionally — we haven’t marketed to that younger generation, but that’s something that we plan to change. And we’re trying to come up with some annuity products specifically tailored for a younger generation, allowing more flexibility with what kind of premium, how often it comes in and the amount of the premium.

Feldman: What are some of the features that would be great to offer to somebody to get that buying age down?

Acker: I think technology is the key. Annuities are not bought, they’re sold. Advisors and producers play a very important role in educating the consumer on our products and what they do. These products are complex. I don’t really see a direct-to-consumer model. I know there are carriers out there doing it, and I think with certain annuities, it might

make sense, but for a younger generation, I think there is an opportunity to use technology.

If you think about how many people in this country today don’t have a traditional job. They’re driving for Lyft, they’re driving for Uber, so they don’t have a 401(k), they don’t have traditional retirement. If we could come up with a way where the minimum amount was zero, essentially, they can contribute $20 a week through an online platform. I think that’ll go a long way in attracting a younger generation. I think an annuity could be a step in the right direction for them if we can make it flexible enough and cost-effective for the carrier. And I think technology is where we can do that.

Feldman: How do you see multiyear guaranteed annuities performing in the upcoming year? Now might be the best time to get them.

Acker: There are two things happening in the MYGA space. As you know, with MYGAs — I’ll call them a commodity — the highest rate typically wins. There aren’t a lot of bells and whistles with a MYGA, and that’s the beauty of them. I think there are two things at play with MYGA rates. They’re at very attractive levels. They have been for the last couple of years, primarily because of how fast yields have risen, which is allowing a carrier to pass on higher rates. But I think given the replacement business that’s happening, some carriers have a lot of business going out the door; it’s moving to other carriers. And so the MYGA is a way to generate positive cash flow. As long as we can compete with CD rates, the other advantages of a MYGA, such as the tax-deferred status, should make it an easy decision for consumers.

Feldman: What are the biggest challenges SILAC is facing to compete in this annuity space?

Acker: The annuity space is as competitive as I’ve ever seen it. And not only with some carriers that have been in this space for a long time. There are a lot of new entrants every year or every month, it seems. And we’ve been able to compete. We started in 2018; our sales were

all MYGA in the second half of the year when we started. And our sales in 2018 were just over $150 million. The following year in 2019, we went to $1.7 billion in sales, and we’ve grown ever since. By design, though, a couple of years ago, we became less competitive just to slightly slow sales as we were raising capital, with the goal of improving our ratios and ultimately improving our rating from AM Best.

like Fitch Ratings, from KBRA, which are nationally recognized and have very stringent processes that they go through, like AM Best, but they have other views. And so I think it’s important that producers weigh all of the ratings that a carrier has; speak directly with the carrier, with their management team; and become comfortable with their financials and what their business model is.

The MYGA is a way to generate positive cash flow. As long as we can compete with CD rates, the other advantages of a MYGA, such as the tax-deferred status, should make it an easy decision for consumers.

Even though we’re a new entrant and a small carrier, we’ve been able to compete very successfully and became a top 10 annuity carrier relatively quickly. I think today we’re in the top 15 based on sales, even though that’s not what we focus on. For us, it’s about focusing on the right level of sales based on our capital. Our biggest challenge right now, though, to answer your question specifically, is ratings. And specifically, AM Best. Rating agencies right now are a challenge, and that’s something we’re working through. Given some changes they’ve made over the last couple of years, it’s made it challenging for a company like SILAC, which does rely on reinsurance. We have very strong reinsurance partners, but based on the changes AM Best has made, it’s impacted our rating. And there’s a role AM Best plays in this industry.

They have a view, but it’s one view. There’s a lot to look at when evaluating an insurance company. AM Best is one tool but should not be the only tool. There are five or six other large rating agencies that have different views, and it’s not our job to tell a rating agency their view is wrong. We accept their view. But what we’re trying to do is obtain more ratings from companies

That’s something we try to do at SILAC: give our producers access to the CEO on down. It’s important that producers are comfortable with our model, who we are as people and what our outlook is.

We’re not going to presume to try to change their rating process, because that doesn’t feel appropriate. But in no way should a rating agency undermine an insurance department. We’re already put through very stringent financial tests, examinations, etc.

Feldman: How do you see technology affecting distribution?

Acker: Positively. SILAC is a new entrant, if you will, with a long history. But as a new entrant, I’d say we’re behind the eight ball. There’s a lot we can do with technology, and we’re trying to catch up quickly. As an industry, we’re traditionally not known to be a technology leader.

But I think there’s a tremendous opportunity in direct-to-consumer. I think there may be a path there for certain products, but that’s going to be a challenge. I think using technology to partner with our producers through

the education process, to educate consumers on our products, is where we’re focusing at SILAC. We’ve had electronic apps out there for awhile that make the sales process more efficient, easier. At SILAC, about 70% of every annuity sold is on an electronic platform through Hexure, who we’ve partnered with, and their FireLight eApp.

Besides focusing on products, at SILAC we’re trying to put ourselves in the shoes of a producer at that point of sale. How can we make it easier? For the producers, teach them how to sell our products, teach them how to allocate across various indices. There are more than 100 custom indices in our industry that carriers work with outside of the S&P. And I think that’s a challenge. How do I pick among 100 different indices that are available? We’re coming up with ways to help the producer at the point of sale.

Feldman: SILAC also has an AI index, correct?

Acker: We do. We launched that index about three years ago, roughly, and it’s been a very successful index for us. And there are ideas in the works to expand on that AI index.

Feldman: How has AI impacted SILAC?

Acker: We have a team that is responsible for developing the AI initiatives within SILAC. We’ve been spending the last year testing different ways AI can help us, primarily through our customer service team and internally. And so now we’re rolling that out to all 325 associates. We must streamline as much as we can, whether by extracting emails, reading through emails to just get to the point of the email and save time. AI will be used in a bigger way going forward for SILAC, mostly internally for our associates. As this initiative progresses, I think it’ll then shift to how we can help the producer partner with that point-of sale-process.

Like this article or any other? Take advantage of our award-winning journalism, licensure and reprint options. Find out more at innreprints.com.

Advisors turn their attention to helping younger women form good financial habits and protect what’s important to them.

BY SUSAN RUPE

“Your future self is already grateful for the decision you’ll make today.”

That is one message that Grace Vandecruze includes in her newsletter, “Thrive,” which is aimed at women.

Vandecruze is managing director of Grace Global Capital, a New York consulting firm providing mergers and acquisitions financial advisory, restructuring and valuation to insurance executives, boards and financial regulators. She is the author of “From Homeless to Millionaire: 6 Keys to UPLIFT your Financial Abundance.”

of their time is spent on medical care and expenses, and it is a painful time for them. Many women finish their lives in a way they had not envisioned, and it’s not a positive thing.”

Older men often have an easier time than women in the final stages of their lives because men are more likely than women to have a partner or companion to help them navigate the challenges of older age, Vandecruze said.

But outside her practice, Vandecruze works to empower young women through financial education. She believes women must understand “that they are the drivers of their financial destinies.”

“As young women pursue their dreams, it is more important for them to be less of a consumer and take more of an ownership of their finances, think more long term and be entrepreneurial about their life’s goals,” she said.

Vandecruze said she believes younger women’s financial education would benefit not only from professional advice but also from observing the financial realities of older women.

“They’re not seeing older women who are in their later years and what the reality of that is,” she said. “The reality of women in their later years is that much

“Some women don’t have the luxury of having a partner, and they often don’t have the finances to afford the medical care that they need. And what’s missing in this discussion is that we’re in the middle of a longevity revolution, living longer than any past generations. However, financially, we are so lagging behind. In a woman’s lifespan, she will have more financial detours than a man will. Childbearing years may bring a financial detour to her life, potential illnesses and diseases, caregiving to her children, plus caregiving to her parents — the challenge for women financially has never been higher.”

Young women also must understand what Vandecruze called “the time value of money.”

“It’s about how saving incrementally — saving what you can when you can on a consistent basis over time will make a substantial difference in the way you’re able to spend your latter years and the quality of your life as you age.”

Although Vandecruze provides financial education to young women outside her practice, she believes the industry must understand a few things about that demographic in order to serve them.

“First of all, young women are savvy,” she said. “They understand and grasp the basics of investment. What they’re lacking is education. But I think once you

It’s about how saving incrementally — saving what you can when you can on a consistent basis over time will make a substantial difference in the way you’re able to spend your latter years and the quality of your life as you age.

Another challenge to women’s financial security is that younger women often think they have more time to prepare than they actually do, Vandecruze said.

“When you’re a young woman in your 20s and 30s, your thinking of time is elongated,” she said. “You think you have time. You think, ‘60 is old; it’s going to be a while before I get there.’ But time goes by quickly. When you’re in your 20s and your 30s, you’re probably focused on launching a career, finding your footing in your job, repaying your student loans or getting your first car and your first home. Those are great goals to have; however, they bring a financial burden on you. So one of the things I talk about is there are some debts that will add value to your life and add value to your wealth, and there are some debts that will deplete them. For example, it’s important for young women to distinguish between credit card debt and mortgage debt.”

teach young women the benefits of investing, the benefits of securing a future by insurance, the benefits of compounding savings over time and how that makes a substantial difference in the quality of our life, it will accrue substantial benefits to young women.”

Why work with young women?

Women in younger generations are poised to receive about $47 trillion in inherited wealth by 2048 as part of the great wealth transfer, according to Bank of America Institute’s most recent “Women and Wealth” report.

As a result of the great wealth transfer, which is already underway, “women will soon control more money than ever before,” the report said.

In addition, the report said, women are achieving increasing levels of education and working as much as if not more than their male counterparts, which has

Grace Vandecruze sends a monthly newsletter aimed at women’s financial topics.

Vandecruze

resulted in their rising wages and greater representation in senior leadership positions.

“Increased wage gains, coupled with the ‘great wealth transfer,’ position women to be key drivers of economic growth,” Bank of America Institute’s report said. “As wealth increases, women’s prosperity will help to ‘grow the pie’ of total affluence.”

In her newsletter, Vandecruze said the U.S. is entering what the Federal Reserve Bank of St. Louis specifically identified as a “significant wealth restructuring period” with particular opportunities for women investors

Three forces are creating a once-in-ageneration wealth opportunity.

1. The volatility advantage: Market swings are creating undervalued assets that large institutions are overlooking. According to Bloomberg Financial Analysis, these inefficiencies particularly benefit smaller investors who can move quickly.

2. The $84 trillion transfer: We’re in the early stages of the largest wealth transfer in history as baby boomers pass down assets. The National Bureau of Economic Research projects $84 trillion will change hands by 2045, with the largest portion transferring between 2025 and 2030.

3. The women’s wealth revolution: For the first time, women control more than 51% of U.S. personal wealth, according to McKinsey’s 2024 Women in Finance Report. This is creating new financial products and opportunities specifically designed for women’s needs.

“This 24-to-36-month window offers rare wealth-building opportunities that could literally change your family’s financial future for generations,” Vandecruze wrote in “Thrive.”

Working with ‘accomplished women’

Cathy Mendell enjoys working with two types of women she describes as “accomplished women.”

Mendell’s advice for young women who are raising families and forging their career paths is fourfold: Take control of debt, be intentional about where your money is going, track your spending and your living costs, and realize that your retirement is your responsibility.

been putting money into for the past 10 years or so, and she’s looking at her next job. But she also is saying, ‘Let me set myself up for the future.’ She doesn’t want to save haphazardly. She really wants a plan that says, ‘All this money that I’m accumulating will someday result in a lifestyle that I want to live when I retire.’”

The second type of woman Mendell serves is still working but is thinking ahead to retirement.

“They are ready to think about retirement, but the problem is that while they’ve saved money, they don’t really know what to do next. Do they just start taking withdrawals and hope that everything works out? They didn’t go to work every day and just hope it worked out. They knew what they were doing. But now they go into a new phase of life where now the stock market is in control of their money. That’s a particular group of women we work with closely because we can make a huge difference for them.”

Mendell equates retirement planning to driving a car through fog.

Mendell is founder of Theia Financial in Jacksonville, Ore.

The first type of accomplished woman she works with is in a career transition.

“She is transitioning from one job to another. Maybe she has company stock, and she might have a nice 401(k) that she’s

“You’re driving down the road and you run into low clouds. Suddenly you can’t see, you hunker down over the steering wheel, your blood pressure goes up and you slow down. It’s very disconcerting. I think that’s how a lot of women feel about investments and money. They know they need to do it. They do it. They’re good with it. But the question is, what does that actually translate to later in their lives?”

Mendell described her clients as “women who are making an effort toward their future. They’re doing the hard work, they’re saving money. And I love working with those people.”

Her advice for young women who are raising families and forging their career paths is fourfold: Take control of debt, be intentional about where your money is going, track your spending and your living costs, and realize that your retirement is your responsibility. That last piece of advice is the most important, she said.

“I’ve had some younger people say, ‘I don’t see myself ever stopping work.’ Well, I hate to tell you this, but someday you’re going to be 79 and you’re not going to be employable. So you must have an eye for the future and get into the habit of having money that goes from your checking account into a savings account where you don’t have to do anything with it. It just is an automatic withdrawal. It’s possibly the smartest thing you can do, because there’s no decision to be made.”

An ‘interesting demographic’

Caroline Tanis said that working with women in the 50-and-younger age bracket “is really cool because you get to be there for so many of the big moments in their lives.”

Tanis is founder of Tanis Financial Group in New York, where she focuses on advising the women she describes as “the chief financial officers of their families.”

“My main demographic is women 35 to 50 years old,” she said. “This is an interesting demographic to work with, because it’s women who are having kids, buying a house, trying to save for college. My clients are mainly either the breadwinner or co-breadwinner of their families. They’re trying to build wealth and set themselves

Tanis

Mendell

up well with everything they have going on. It’s fun for me to put these different goals in their financial plans and then, for example, see their kids get accepted into the college they want to attend. And you know you’ve been working with them to plan for that for years, and now you see that moment come to fruition.”

Another reason Tanis enjoys working with women in her target age group is that they have access to so much financial information, yet they have so much going on in their lives that they are happy to work in partnership with a professional instead of trying to plan their financial futures on their own.

happen to you during retirement when you can no longer take care of yourself? It might be far away, but it’s something we have to think about because it’s a different scenario if you are going to be in a nursing home or assisted living versus

or grandmother who had the same set of dynamics they’re facing, so I want to create a safe space for them to be able to say, ‘I don’t have anyone else to talk to about this.’”

Scott said many of her female clients “are managing financial responsibilities beyond themselves.”

Tanis on her most important client need: “It’s to the point where in my practice, I will not work with someone unless we take the time to build this financial plan, because I’ve had clients who breeze through it and they don’t want to do the work. And it is work!”

“They need someone who will be their advocate and fight for them,” she said.

Tanis said the most important thing her clients need is to build their financial plan.

“It’s to the point where in my practice, I will not work with someone unless we take the time to build this financial plan,” she said, “because I’ve had clients who breeze through it and they don’t want to do the work. And it is work! You have to get your documents together, and you have to make time to have that conversation with me.”

As her clients take on life’s financial milestones, such as buying a house or having a child, Tanis will revisit the plan with them.

“It’s the root of everything we do. We want to see how on track we are, because there is only so much time until retirement and a lot of choices need to be made. We don’t want to be scrambling — like, ‘Oh no, the kids are going to college in two years! What do we do?’ It’s taking the time now so that when college comes around, it’s smooth. I can tell my clients, ‘This is exciting. Go and enjoy. Let me know who to write the check to from the appointed accounts.’”

Tanis said that many of her clients are “living in the here and now,” so she gives them a list of questions to help them think about financial concerns that might be decades away.

“A big question is, what’s going to

being at home with a nurse. You need to plant those seeds in their minds because younger women are living in the here and now and they’re limited on time. That’s our job, though — to help them and ask those questions so we can work with them on the answers.”

Breaking barriers, figuring it out

Nicole Garner Scott is a Northwestern Mutual advisor in Atlanta. She specializes in working with women in the 35-to-45-year-old age bracket, describing her typical client as being “a first-generation success in her family.”

“They are possibly the breadwinner for their family and often the most successful in their family,” she said. “They have a unique set of challenges, whether it’s breaking barriers, hitting a new level of ambition, navigating being in the sandwich generation and having to be the first to figure out their financial blueprint,” she said.

“Many are supporting other family members. A lot of them are planning for career shifts. And I think many of that generation are attuned to understanding long-term financial security. There’s an awakening of younger generations to understand that a lot of the responsibility for planning their financial security will fall on them and they need to map out what they want the second half of their life to look like.”

“Integrative planning” is what Scott said she offers her clients. “Many of them are looking at their executive compensation packages and not understanding what they mean. Clients need to understand what they need to do now, from a retirement strategy standpoint, and also understand how to take their risk management into account.”

Scott said she wants her clients to feel empowered, and that means not using jargon or having conversations that go over clients’ heads.

“I want them to feel seen and heard, because a lot of our female clientele might be the first generation to discuss these issues with a professional,” she said. “They might not have had a mother

Insurance also is part of the plan, she said. “It’s important to obtain insurance while they’re still young and while health is on their side.”

Scott said so many of her clients are victims of “information overload,” and her job is to help them understand that information and break it down for them.

“So many individuals who come to me are confused with all the noise that’s out there, and they need to have a trusted partner that can talk through all this with them.”

Susan Rupe is managing editor for InsuranceNewsNet.

She formerly served as communications director for an insurance agents’ association and was an award-winning newspaper reporter and editor. Contact her at susan.rupe@innfeedback.com.

Scott

Sam Philbrook took the lessons in leadership and service he learned in the Army to serve his clients and community.

By Susan Rupe

Many children dream of growing up to become a police officer or a firefighter. Sam Philbrook said he couldn’t wait to become a soldier. Four generations of his family have served in the armed forces, and his goal was to join their ranks.

After 13 years in the Army, Philbrook found that the leadership and organizational skills he learned as an infantry officer transferred well into a new career in the financial services world.

Philbrook is managing director of Commonwealth Financial Group in Boston, where he is responsible for coaching and developing new financial advisors as well as serving a clientele of business owners and young families. He is a registered representative of and offers securities, investment advisory and financial planning services through MML Investors Services.

He was honored with one of Advisor Today’s 4 Under 40 awards for 2023 issued by the National Association of Insurance and Financial Advisors Sept. 20, 2023, and covering the time period between Aug. 31, 2022, and Aug. 31, 2023.

To be considered, an advisor must be under 40 years old and a current NAIFA member. Candidates can self-nominate or be nominated by industry peers and are selected based on professional credentials, industry involvement, volunteerism and community involvement. The award is not an endorsement or indicative of the future performance of the financial adviser. MassMutual is a member firm and pays an annual fee to maintain its membership. MassMutual is not involved in the nomination or final selection process. A fee was paid for consideration.

Growing up in the coastal town of Marion, Mass., Philbrook was eager to follow his other family members into the service. He graduated from Norwich University, a small military college in Vermont, and entered the

Army soon afterward.

“I began as an infantry officer and then graduated to a scout platoon leader, which is typically reserved for the No. 1 infantry lieutenant in the battalion,” he recalled. “I then went on to become a company executive officer for a headquarters company, which is the best [post for a] lieutenant after scout platoon leader. It’s a very diverse role with a lot of moving parts.”

From there, Philbrook became an operations officer, then was deployed to work intelligence in the Middle East, a role that he said is a unique path for an infantry officer.

“Typically, an intelligence officer is an intelligence officer, and an infantry officer is an infantry officer,” he said. “But the Army liked the way I thought about things. I could present data and

Philbrook soon found out that although he thought he was unqualified to work in financial services, the skills he obtained in the Army helped him in his new career.

“It comes down to leading from the front,” he said. “Selfless service is always doing the hard stuff. I’ve always said I will probably outwork everyone around me. This is the reason why I needed something entrepreneurial, because I do not work very well underneath someone when I’m going to outwork them. I will put the team on my back and move forward. If that means working 14-hour days or whatever it takes to get the job done, I will do that. Because that’s what you’re taught in the military. It’s that you will continue to think through different ways of achieving the objective, whatever the objective is.”

talk the language of movement and maneuver as an infantry officer, but I also could look at a data feed and understand what the enemy was doing or trying to accomplish.”

After 11 months in the Middle East, Philbrook was redeployed to Macedonia when Russia invaded Ukraine, and he spent a month or two in that country.

When his military career was over, some friends suggested to Philbrook that he could earn a lot of money doing tech sales in Boston. But he soon found that was not the career for him. Another friend told Philbrook he might be better suited to a financial services career.

“I told him ‘I don’t know anything about the S&P 500, I don’t know anything about mutual funds, I am the least qualified person when it comes to financial planning,’” he said. “But he told me if you’re good at dealing with people, they’ll teach you the rest. And that is how I entered financial services.”

The best of both worlds

In his practice, Philbrook said he has the best of both worlds. He and his wife are living and raising their three children in his hometown of Marion, an hour’s drive from Boston. He travels to Boston three or four times a week to work in his office.

“My team and I do a lot of work with business owners and with families,” he said. “Our clients want to make sure that if anything happens, they don’t want to be a financial burden to their loved ones. They want to make sure they retire on time; they want to make sure they’ve saving money to the right areas.”

Philbrook said his philosophy about planning is rooted in the principles of protection, savings and growth.

“Are we protecting your income in the right way? Are we saving money to the right vehicles, and are we invested correctly? Our job is to pull our clients off the treadmill of life and help them financially plan by design, rather than by default.”

the Fıeld A Visit With Agents of Change

He said many clients are on the default path. “They’re pumping money into their 401(k) account, they’re putting money into savings and their fingers are crossed, thinking they really hope this all works out. Our job is to make sure they’re saving in the right area, they’re protected in the right way and they’re invested correctly.”

Leading by serving

Philbrook has always had a passion for serving others, and one of the most notable ways he spearheaded service was during the U.S. military’s withdrawal from Afghanistan in 2021, ending 20 years of U.S. military involvement in that country.

His unit was assisting in the evacuation of civilians from Afghanistan, most of whom fled with nothing but the clothes on their backs and their meager possessions stuffed into plastic bags.

Philbrook’s birthday was approaching, so he made a social media post requesting that his family and friends donate supplies to the Afghan civilians in honor of his birthday. The request went viral and was shared by several influencers on Instagram. More than $82,000 worth of supplies were donated.

“It was hygiene products, flip-flops, hydration salts — Red Bull donated a pallet of energy drinks,” he said. “We had all these supplies shipped to us to distribute to the displaced population. So that one social media post ended up having a huge impact on those families who were sitting in hangars or on airport runways with nothing.”

Back home in Massachusetts, Philbrook realized he and his family lived in what he called “a kind of bubble.” He looked for a way they could help others and discovered an organization called the Friends of Jack Foundation, whose mission is to provide and support overlooked programs that enhance the physical, mental and emotional health and well-being of children across the South Coast region of Massachusetts and Rhode Island.

Commonwealth Financial Group’s founder started Rally 2 Give, with the goal of raising funds to benefit organizations in the Greater Boston area. Last year, the rally generated $500,000, $30,000 of which was donated to the Friends of Jack Foundation.

The rally attracts about 50 cars. The drivers race over a four-day period through southern New England up into Montreal, Canada, or Burlington, Vt.

“It’s all about an experience and bringing people together to network and enjoy each other’s presence,” Philbrook said. “You stop at a dinner venue, you go to a hotel, and you kind of do the same thing for three or four days throughout New England, up into Canada. All the cars have to raise money, so they reach out to their networks and activate their ambassadors or their communities to donate money, and it has snowballed.”

Between his family, his practice and his community activities, Philbrook leads a busy life. His guiding philosophy is “Time is your greatest asset.”

“You always want to acknowledge the fact that if everything is important, nothing is important,” he said. “There are four priorities I always have, which are: Focus on priorities, not emergencies. Get organized. Delegate, don’t detour. And I think the most important thing is to foster a culture of accountability and excellence in your practice, and if you’re leading a team, infuse that into your team.”

CRN202803-8400425

Susan Rupe is managing editor for InsuranceNewsNet. She formerly served as communications director for an insurance agents’ association and was an award-winning newspaper reporter and editor. Contact her at srupe@insurancenewsnet.com.

1. “Life expectancy for men in U.S. falls to 73 years – six years less than for women”, per study. Statnews.com. November 13, 2023.

2. “Gender pay gap statistics in 2024”. Forbes.com. March 1, 2024.

3. “Caregiver statistics: A data portrait of family caregiving in 2023”. Aplaceformom.com. June 15, 2023.

Please keep in mind that the primary reason to purchase a life insurance product is the death benefit.

Product features and availability may vary by state.

Life insurance products contain charges, such as Cost of Insurance Charge, Cash Extra Charge, and Additional Agreements Charge (which we refer to as mortality charges), and Premium Charge, Monthly Policy Charge, Policy Issue Charge, Transaction Charge, Index Segment Charge, and Surrender Charge (which we refer to as expense charges). These charges may increase over time, and these policies may contain restrictions, such as surrender periods. Policyholders could lose money in these products.

These materials are for informational and educational purposes only and are not designed, or intended, to be applicable to any person’s individual circumstances. It should not be considered investment advice, nor does it constitute a recommendation that anyone engage in (or refrain from) a particular course of action. Securian Financial Group, and its subsidiaries, have a financial interest in the sale of their products.

Insurance products are issued by Minnesota Life Insurance Company in all states except New York. In New York, products are issued by Securian Life Insurance Company, a New York authorized insurer. Minnesota Life is not an authorized New York insurer and does not do insurance business in New York. Both companies are headquartered in St. Paul, MN. Product availability and features may vary by state. Each insurer is solely responsible for the financial obligations under the policies or contracts it issues.

Securian Financial is the marketing name for Securian Financial Group, Inc., and its subsidiaries. Minnesota Life Insurance Company and Securian Life Insurance Company are subsidiaries of Securian Financial Group, Inc.

For financial professional use only. Not for use with the public. This material may not be reproduced in any way where it would be accessible to the general public.

Philbrook sits with over $82,000 worth of donated supplies, fulfilling his birthday wish, ready to give to Afghan civilians.

LIMRA launches new tools to help life insurers adopt AI

With the launch of turnkey templates and strategic guides, LIMRA’s AI Governance Group continues to lead efforts to help U.S. life insurance companies safely and effectively adopt artificial intelligence.

Whether for developing AI in-house or with a vendor, these resources are designed to help companies make informed decisions regarding AI adoption, LIMRA said. These turnkey frameworks include comprehensive cost-benefit analysis templates that can help leaders identify the potential benefits and risks of various strategic paths when considering AI. The AIGG plans to release several more industry frameworks this year.

AI has the potential to transform the financial services sector, modernizing organizational processes and offering significant opportunities to improve customer experience, LIMRA said. This is just the latest AIGG effort to create a foundation for sustainable and inclusive AI practices to improve the life insurance industry.

LIMRA’s AIGG draws expertise from more than 100 business and technology executives representing more than 50 U.S.-based member insurance companies. The group’s goals include educating its members about the current state of AI in the industry and providing a forum for open and collaborative discussion about the most effective uses for the technology.

INDUSTRY FACES FOUR POSSIBLE FUTURE SCENARIOS

The insurance industry faces four possible future scenarios. Insurance executives are optimistic about the major trends influencing their industry but remain aware of critical risks to their organizations. A panel of experts reviewed the findings of The Economist Impact research on the future of the industry.

Those four possible scenarios are:

1. Fractured resilience.

2. Digital harmony.

3. Adaptive alliance.

4. Stagnant turmoil.

Two main drivers of change — the pace of technological change and the level of global cooperation — impact all of these scenarios.

PENN MUTUAL SUED OVER WHOLE LIFE TAX-AVOIDANCE ‘SHAM’

The fourth quarter is nearly always the best quarter of the year for sales.”

of supervised release.

The lawsuit alleges that Penn Mutual and Boll, along with several other law, lending, accounting and financial planning firms also named as defendants, constituted a high-premium insurance enterprise.” Penn Mutual whole life policies were aggressively marketed as offering “significant tax advantages,” plaintiffs say. One type of “sham tax-avoidance strategy” incorporated premium financing life insurance loans to finance the policies, the lawsuit alleges. Using life insurance in a premium financing strategy to manage tax obligations remains a controversial tactic within the industry.

A group of 29 plaintiffs claim that Penn Mutual and several codefendants ran a tax-avoidance scam around whole life insurance policies . The amended complaint, filed in U.S. District Court for the Central District of California, alleges fraud and negligence as well as violations of the Racketeer Influenced and Corrupt Organizations Act. Plaintiffs, which come from states around the country, ask the court for $23.5 million in damages.

The defendants include former Penn Mutual agent Randall Scott Boll, who was indicted in 2021 on four counts related to violations of federal money laundering laws and banking regulations. Boll pleaded guilty to one count of conspiracy to cause a financial institution to fail to file currency transaction reports and to structure financial transactions. He was sentenced to one day behind bars in California, court records say, and two years

PROFITABILITY IS NO. 1 ISSUE FOR INSURERS IN 2025

Profitability will be the biggest top-ofmind issue for insurers in 2025, while advanced data and analytic technologies will be insurers’ top strategic priority this year. That’s according to a Majesco poll of insurers on their strategies and investments for the year.

Insurers also reported they plan to develop new products and new business models for existing markets as well as new markets in 2025. Digital payments is another area of insurer focus in 2025, with more insurers accepting payments through their own apps or digital wallets.

life insurance premium increased 3% in 2024, to $15.9 billion, setting a record for the fourth consecutive year.

— Sheryl J. Moore, CEO of Moore Market Intelligence and Wink Inc.

Overcoming ‘I need to think about it’

The four most common objections to buying life insurance

By Drew Gurley

These six words to salespeople are like fingernails on a chalkboard: “I need to think about it.”

It’s the most difficult common objection to overcome for most life insurance agents, especially those who are new to the business or part-time. It might even be worse than “I’m not interested.” At least with that, you know where you stand and can look at yourself in the mirror and start to figure out where you messed up.

A great sales call rolls like a snowball off the top of a mountain. It starts slow and easy, then gains speed and size to a point where it is unstoppable.

But here’s the key: If you don’t pack the snowball tightly at the top of the mountain, the likelihood of it falling apart when it hits a big rock on the way down is higher.

Let’s zero in on how to set yourself up for success in your sales presentation from the top of the mountain.

What are the four most common objections to life insurance?

You are all too familiar with these if you have been selling life insurance (or any type of financial services or insurance products).

The key here is to build an approach that assumes you will hear all these objections at some point in the discussion. We harp on this in sales training: Create a conversation that focuses on preventing objections before they become objections. Here are the four we hear most and how you can begin preventing them.

» Fear of commitment: Discussing life insurance in general can make people uncomfortable. Most clients do not

know how it works, which creates an internal fear of making the wrong decision on a long-term financial commitment. You must address it early in the discussion, making sure they understand it in the simplest terms. If they can explain it to their spouse or friends, then they will feel empowered to make a purchase decision.

» Financial concerns: These should be addressed early in the discussion. Affordability and the cost of life insurance will always come up. Don’t let “I can’t afford life insurance” snatch defeat from the jaws of victory. LIMRA reports that 72% of Americans overestimate the cost of life insurance and 54% of those are relying on their gut instinct or a guess. This is an opportunity for the agent willing to take the time to better explain how it works and review accurate costs.

Try an approach like this: “Most people I meet with are in two boats. The first is the majority of people believe life insurance is too expensive. The second is that about one-fourth are unsure how it works, which prevents them from making a decision. Which one of those boats would you say you are in?”

» Genuine need for time: This is one of the most common insurance sales objections. And it is legitimate. For example, it’s common for older folks to want to include their loved ones in the discussion. And it’s common for younger folks to want to ask their parents for advice.

This goes back to the first point. You will experience this more often when you haven’t done a thorough job of explaining the “how it works” part of life insurance from the start. The more your prospects understand how it works and can explain it in simple terms, the more confident they will be when making a decision. This won’t eliminate 100% of these concerns, but you can certainly influence the number of times it comes up.

» Going to stay with current life insurance policy: Most agents think the client was just price shopping their current insurance coverage. We disagree. Most people don’t like to deal with life insurance, so if they are talking to you, they have an issue of some sort. This should be dealt with early in the discussion. You should thoroughly review their current policy with them. It will build their confidence for the discussion.

Many older policies, specifically permanent policies such as universal life, are vastly underperforming and set to lapse. This is a fantastic time to call their life insurance company with your prospect on the phone and find out how long the policy is set to stay in force based on their current funding. Your role is to facilitate the discussion with the current insurance company and allow them to tell your prospect (their customer) the news.

Acknowledging these common life insurance objections will help you empathize with the prospect and tailor your response. More importantly, addressing these thoughtfully will dramatically improve your chances of success.

Let the game come to you: Ask great questions

The rock stars of the life insurance sales process build their fact finding around — wait for it — life. They know the path to solving a customer’s issue is through a serious, sometimes involved discussion about where they are and where they want to go.

Too often, agents are in a hurry. Sometimes they jump to conclusions. Or worse, they assume. And we all know where that path ends. The insurance industry is littered with former agents who didn’t have patience.

Football coaches will tell you the greatest quarterbacks are those who can let the game come to them. They analyze the entire field. They are patient. They lure the defense in like a worm does a fish. They can’t be rattled or surprised.

One way of handling objections at the end is to ask thought-provoking questions at the start. These questions invite prospects to share their goals, concerns and aspirations, helping you understand their priorities on a deeper level.

Here are five examples of such questions, with a couple of follow-ups for each:

1. What does financial peace of mind look like for you?

• Specifically, what does financial stability look like in:

° 5-10 years?

° 20 years?

• Where are you on this financial planning journey?

2. What keeps you up at night when you think about your family’s future?

• Describe the three most worrisome scenarios.

• What are you doing currently to address those concerns?

3. How well have you planned for the unthinkable if something were to happen to you?

• Describe the situation your family would face if it happened tomorrow.

• Where are you in the process of planning for this?

4. What kind of mistakes have you seen others make that you won’t make?

• Professionally?

• Intellectually?

• Personally?

5. What kind of legacy would you like to leave?

• For your family?

• For others?

By starting with these high-level questions, you set the stage for a meaningful conversation and show genuine interest in the prospect’s life and goals.

Proactive strategies to overcome life insurance objections

In addition to asking the right questions, there are other proactive steps you can take to minimize objections.

» Build rapport and trust early. Establish a strong connection with your prospect. Demonstrate genuine care by listening actively and showing empathy. Share relatable stories that illustrate the importance of life insurance. Make it personal and memorable.

» Simplify the decision-making process. KISS. Be clear and avoid jargon. Get objections out of the way early, such as explaining how life insurance fits into their budget or how it aligns with their financial goals.

» Create urgency without pressure. Address the risks of delaying without resorting to scare tactics. Share real-life examples of families who benefited from timely decisions. In conclusion, managing “I need to think about it” requires preparation and finesse. Uncover objections through a thoughtful discussion. Remember, each objection is an opportunity to build trust, improve your craft and help your clients make decisions they won’t regret.

Drew Gurley is a licensed life insurance expert with nearly 15 years of experience. During his career as both a licensed life insurance agent and industry executive, he has helped thousands of clients with their life insurance needs through his work at Redbird Advisors and Senior Market Advisors. Contact him at drew.gurley@innfeedback.com.

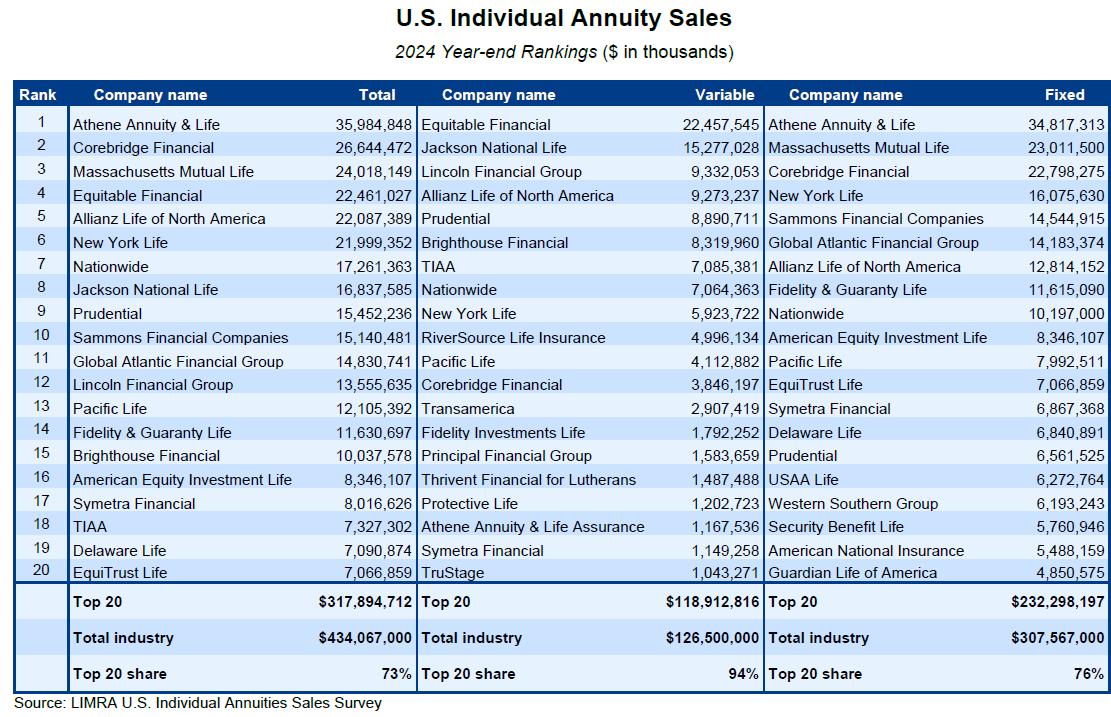

ANNUITY WIRES

Annuity sales a fourquarter hit in 2024

Annuity sellers made history in 2024. For the first time ever, total quarterly annuity sales surpassed $100 billion in all four quarters.

Total annuity sales finished at $434.1 billion, up 13% yearly, according to LIMRA’s U.S. Individual Annuity Sales Survey, representing 83% of the market. It marked the third year of record-high annuity sales, which together represent $1.1 trillion.

Equitable Financial and Allianz Life were two of the big winners, moving into the top five. Athene Annuity & Life again topped the sales charts with $36 billion in sales. But those sales were basically flat year over year.

Meanwhile, the rest of the top five made strong gains. Equitable and Allianz both improved sales by 20% to 25%, respectively, propelling them past New York Life.

In the fourth quarter, U.S. annuity sales totaled $102.1 billion, down 12% from the record-setting results in the fourth quarter of 2023. Falling interest rates dampened fixed-rate deferred and income annuity sales, pulling down overall results.

CALIFORNIA REGULATORS SUED BY CONSUMER GROUP OVER PUBLIC RECORDS

The Life Insurance Consumer Advocacy Center filed a lawsuit against the California Department of Insurance over access to complaints by consumers concerning life insurance and annuities.

The lawsuit claims that CDI’s refusal to provide this data is unlawful based on the California Public Records Act.

LICAC requested the consumer complaint data to “assist in efforts to advocate for consumers of life insurance, including annuities, and to work for passage of laws and regulations that protect life insurance consumers,” the group said in a news release.

The requested information concerns the number and types of complaints received by the department as well as

reports and data used in the department’s annual report.

The statistics requested by LICAC are “important information that could be used, among other things, to establish a baseline against which to compare complaints in the future,” the group said.

AMERICAN NATIONAL TO STOP SELLING LIFE INSURANCE, FOCUS ON ANNUITIES

American National Insurance Co. will stop writing new life insurance policies at the end of May and focus on other products, including the red-hot annuity market.

Based in Galveston, Texas, American National held a 1.34% market share of the $427.7 billion market that is indexed annuities, said Sheryl Moore, CEO of Moore Market Intelligence and Wink Inc. She cited data from Wink’s Sales & Market Report, fourth quarter 2024.

American National recently announced that it is offering fixed annuity products through a secure online platform in addition to its network of agents and advisors.

In May 2022, Brookfield Reinsurance completed the acquisition of American National Group Inc., the parent company of American National Insurance Co., in an all-cash transaction valued at approximately $5.1 billion.

ANNUITIES SAVE SOCIAL SECURITY $100B, ACLI SAYS

New research from the American Council of Life Insurers finds that benefits from annuities enable retirees to postpone receiving Social Security payments, saving the program $100 billion over time as the greatest surge of baby boomers retire.

By delaying Social Security payments until age 70 with the help of annuities, retirees can increase their benefit payments with each year of delay. As a result, the net lifetime payouts from Social Security are less than those of retirees who begin receiving payments at age 67.

“Life insurers are putting life into America, and this research is further evidence of that,” said ACLI President and CEO David Chavern. “Along with the financial and retirement security we provide consumers, life insurers are supporting the long-term financial strength of an important public program.”

Rising to meet life’s ambitious goals

Business cases require the right balance of speed, flexibility and expertise — and that’s exactly what we deliver. With updated underwriting guidelines, a dedicated business solutions team and enhanced processes, Banner Life Insurance Company and William Penn Life Insurance Company of New York, Legal & General America companies, make it easier to place businessowned life insurance for key persons, SBA collateral loans and buy-sell agreements.

Our structured support ensures faster decisions, greater flexibility and a smoother experience at every step. Because while you’re focused on helping clients, we’re focused on making it easier.

Looking for more info? Get started by scanning this QR code.

Defined benefit annuity: The next great innovation

How transformative technology creates the first personal defined benefit pension funded by a fixed indexed annuity.

By David Macchia

Sometimes fate intervenes to give people what they deserve.

I believe that after having their retirement security taken from them, Americans deserve more guaranteed income. It’s time to bring back the defined benefit pension — in a new way.

Here is an innovation that accelerates the growth of annuities without cannibalizing other products. Instead, this strategy expands the market, ensuring that all parties benefit. There are two key markets in which annuities will gain greater prominence: the 401(k) system and individual annuity sales.

From dominance to decline

In the 1960s and 1970s, insurance companies were the dominant custodians of Americans’ pension assets, primarily managing them through group annuity contracts. Leading insurers such as Metropolitan Life, Prudential, Equitable Life and New York Life played a central role in securing retirees’ financial futures. At the time, 62% of private-sector workers benefited from the financial security of a guaranteed pension, with major corporations such as General Motors, AT&T and IBM covering millions of employees through defined benefit plans.

By the 1980s, however, a seismic shift had occurred. The rise of 401(k) plans and the decline of employer-sponsored pensions drastically altered the retirement landscape. Since then, the U.S. has lost 56,000 defined benefit plans — equivalent to losing one pension plan for every resident of Carson City, Nev., or Cedar Rapids,

Iowa. What followed was a catastrophe for American workers but a boon for asset managers such as Vanguard, Fidelity and BlackRock.

Some may argue that 401(k) assets still belong to workers, so this shift shouldn’t be seen as a loss. But that’s the wrong perspective. Wealth does not create a retirement standard of living — income does. Nobel Prize-winning economist Robert C. Merton highlights this critical distinction: While 401(k) plans focus on and report only account balances, defined benefit pensions and Social Security emphasize and report income — the real measure of retirement security.

Income, not wealth

Imagine a woman named Jane who retired in 2000 with $1 million in savings. At the time, she could safely earn $5,800 per month in interest from certificates of deposit. By 2020, that same $1 million

provided Jane an income of just $75 per month — a 98% drop in income, despite her wealth remaining unchanged. This stark reality underscores why income — not account balances — should be the true measure of retirement security.

So how will insurers and annuities rise in prominence — without hurting asset managers?

Scenario No. 1: 401(k) plans

Imagine a solution that strengthens the business of asset managers while elevating insurers. This begins by recognizing that the 401(k) system is here to stay. The challenge is transforming it to function more like a defined benefit pension plan.

The current attempts to integrate annuities directly into 401(k)s are laudable, but they have gained little traction. Plansponsor has described how most plan sponsors lack “annuity fluency.”

According to research from TIAA, “63% of plan sponsors surveyed said they are unable to articulate the value and importance of annuities.” This is a sad reality considering that, according to LIMRA, most 401(k) plan participants want guaranteed retirement income. Annuities will once again become preeminent, serving as the logical endpoint of a vast amount of 401(k) assets. This means an entirely new strategy for IRA rollovers and conversion of assets into annuitized income.

A new defined benefit strategy driven by technology

A major appeal of this new defined benefit strategy is that it makes 401(k) plans resemble pensions without requiring structural changes to the 401(k) itself. This is achieved by wrapping the participant’s account in technology that transforms it into a funding vehicle for a personal defined benefit pension.