Gambling Insider explores the past, present and future of two of the strongest hubs within US gaming: Pennsylvania and New Jersey ROUNDTABLE Four industry suppliers discuss the ins and outs of building a platform GLOBAL GAMING AWARDS UK FOCUS Key contributors reflect on what the White Paper means for the UK market We look back on the history of the Awards since 2014 Sep/Oct 2023 PURSUIT

GREATNESS

OF

EDITOR’S LETTER

COO, EDITOR IN CHIEF

Julian Perry

EDITOR

Tim Poole

Tim.Poole@gamblinginsider.com

STAFF WRITER

Matthew Nicholson

Matthew.Nicholson@gamblinginsider.com

JUNIOR STAFF WRITER

Lucy Wynne

Lucy.Wynne@gamblinginsider.com

LEAD DESIGNER

Olesya Adamska

DESIGNER

Christian Quiling

DESIGN ASSISTANTS

Svetlana Stoyanova, Gabriela Baleva

MARKETING & EVENTS MANAGER

As Las Vegas gears up for not just one but two big gaming-related events (G2E in October and its very own Formula 1 Grand Prix in November), let's not forget that gaming in the US has plenty to offer outside Nevada.

Indeed, with properties like MGM National Harbor, Foxwoods Resort Casino, Encore Boston Harbor and many more displaying the very best of regional gaming, the main focus of this issue looks east of Nevada: to New Jersey and Pennsylvania.

Reporting the monthly numbers for both states at Gambling Insider has almost become an exercise in 'spot the di erence' during 2023, as the two states vie for what are e ectively local bragging rights. As our Facing Facts section shows, the two states have both had individual months to savour this year, with a betting person perhaps not able to call which state will post the higher revenue for any given month. In our cover feature, we assess both states and their pursuit of greatness, speaking to operators, suppliers and consultants to nd out more about the workings within.

Elsewhere in this edition, we hear from regular contributor Paul Sculpher (twice) on various issues affecting the UK market – not least the Gambling Act White Paper. Regular contributor Ranjana Adhikari and her team at IndusLaw also return with an update on the Indian market. A newcomer to our list of contributing guests is Daniela Guerreiro, who goes into impressive detail on the AML issues currently facing Macau.

Away from our guest editorials (a list that also includes John Connelly, E. Sequoyah Simermeyer, Miles Baron and more), we preview the 10th Global Gaming Awards Las Vegas ceremony. Looking back on the Awards since their inception in 2014 (and the birth of the London event in 2018, as well as the Asia-Paci c event in 2022), we highlight some of the major dates – and victories – that helped make this Awards journey so special along the way.

So to all readers, we hope you enjoy this issue as always – and to those attending G2E, we'll see you there!

TP, Editor

FEATURED IN THIS ISSUE

Mariya Savova

PRODUCTION CONTROLLER

Oleksandra Myronova

IT MANAGER

Tom Powling

COMMERCIAL DIRECTOR

Deepak Malkani

Deepak.Malkani@gamblinginsider.com

Tel: +44 (0)20 7729 6279

SENIOR ACCOUNT MANAGER

Michael Juqula

Michael.Juqula@gamblinginsider.com

Tel: +44 (0)20 3487 0498

SENIOR BUSINESS DEVELOPMENT MANAGER - U.S.

Aaron Harvey

Aaron.Harvey@playerspublishing.com

Tel: +1 702 425 7818

ADVERTISING SALES EXECUTIVE - U.S.

Ariel Greenberg

Ariel.Greenberg@playerspublishing.com

Tel: +1.702 833 9581

Tracy Robbison

Tracy.Robbison@playerspublishing.com

Tel: +1 702 485 3377

ACCOUNT MANAGERS

William Aderele

William.Aderele@gamblinginsider.com

Tel: +44 (0)20 7739 2062

Irina Litvinova

Irina.Litvinova@gamblinginsider.com

Tel: +44 207 613 5863

Serena Kwong

Serena.kwong@gamblinginsider.com

Tel: +44 (0)20 3435 5628

ACCOUNT EXECUTIVE Samuel Sud

Samuel.Sud@gamblingInsider.com

Tel: +44 (0)207 729 0643

CREDIT MANAGER Rachel Voit

WITH THANKS TO:

Diane Spiers, Kevin Cunningham, Jody Madigan, Stephen Crystal and Jacob Claesson, Miles Baron, Paul Sculpher, Daniela Guerreiro, Ranjana Adhikari, Ivan Kravchuk, E. Sequoyah Simermeyer, Gilad Naim, Stian Enger Pettersen, Artyom Ustinov, Margarita Cruz, Paul Kavanagh, Ryszard Presch, Dima Reiderman, Irina Cornides, Shaun Zammitt and John Connelly, Advantech, FBM, Inspired, Interblock & Novomatic

Gambling Insider magazine ISSN 2043-9466 Produced and published by Players Publishing Ltd

Julian Perry, COO, Editor-in-Chief

DIANE SPIERS

VP Marketing and PR, Bally's

JODY MADIGAN COO, Mohegan

Tim Poole, Editor

Julian Perry, COO, Editor-in-Chief

DIANE SPIERS

VP Marketing and PR, Bally's

JODY MADIGAN COO, Mohegan

Tim Poole, Editor

All material is strictly copyrighted and all rights reserved. Reproduction without permission is forbidden. Every care is taken in compiling the contents of Gambling Insider but we assume no responsibility for the e ects arising therefrom. The views expressed are not necessarily those of the publisher.

C ONTENTS

10

22 Pursuing greatness Gamb ling Insider explore two of the US's biggest gaming states in New Jersey and Pennsylvania and asks the question: which will become the more dominant market going forward

32 A Sisyphean task

Regular Gambling Insider columnist Paul Sculpher returns for our September/ October issue to discuss the UK White Paper and the process of legislation it must now undertake

34 In the department we trust Sculpher is in action for his second column of our September/October issue, speaking with Michael Byrne from the Department of Trust about the issue of affordability

38 ‘Dirty laundry’

30 “The full 90 minutes” Miles Baron, CEO of the Bingo Association, speaks to Gambling Insider Editor Tim Poole about the impact of the White Paper on the UK land-based bingo sector

Daniela Guerreiro, Associate at MdME, discusses the prevention of money laundering in Macau casinos

40 New rules

Regular Gambling Insider contributors from IndusLaw, Ranjana Adhikari, Shashi Shekhar Misra & Ruhi Kanakia, discuss the latest from the Indian gambling market

ISSUES

the numbers coming

New Jersey and Pennsylvania in

– and the year as a whole

Taking stock

and

prices

six-month period for the New Jersey and Pennsylvania markets GLOBAL GAMING AWARDS

reflect on a decade of the Las

awards, from a concept to a 10-year thriving reality COVER FEATURE

Facing facts Gambling Insider mirrors our cover theme by exploring

from

July 2023

16

Gambling Insider tracks operator

supplier stock

across a

20 A timeline We

Vegas

FEATURE

38 40

48

DANIELA GUERREIRO RANJANA ADHIKARI

E. SEQUOYAH SIMERMEYER

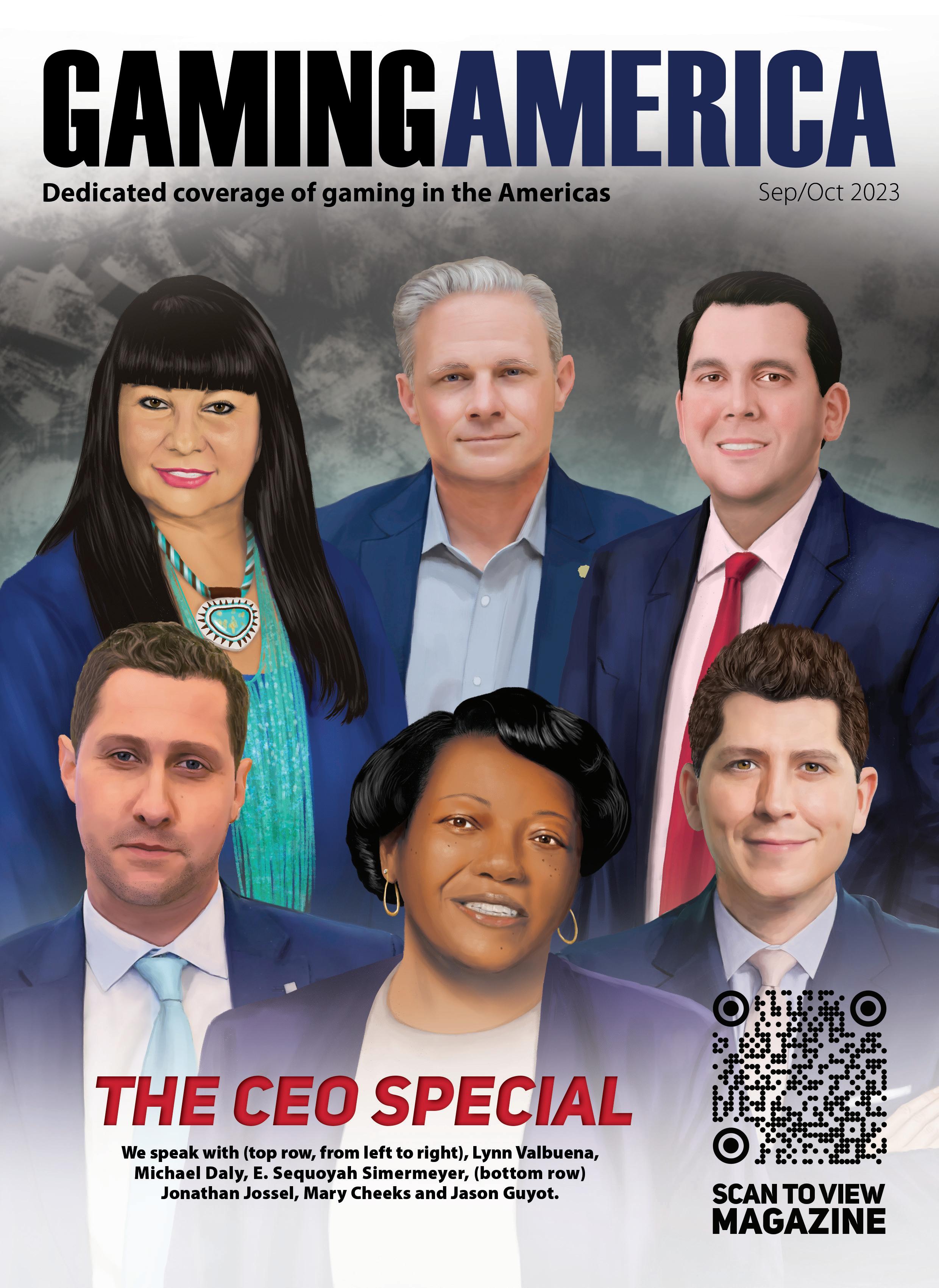

ONTENTS 44 The process of product Gambling Insider speaks with Ivan Kravchuk, Evoplay CEO, to discuss the crossover fusions and what goes into the making of a product 48 Substantial growth E. Sequoyah Simermeyer, NIGC Chairman, reflects on Native Indian gaming's highest gross gaming revenue figures to date 52 Roundtable Gambling Insider takes a look at the world of platform providers with Soft2Bet, EveryMatrix, SoftGamings and Digitain 60 AI in casino marketing Mridula Saini, Chief Revenue Officer at Ikasi, highlights how the use of AI in casino marketing is helping player experiences –and profit levels INSIDERS 64 Paul Kavanagh MiFinity 65 Ryszard Presch Novomatic 66 Dima Reiderman BtoBet 67 Irina Cornides Pragmatic Play 68 Shaun Zammitt Gibtelecom

What's new on the market? Gambling Insider takes a close look at some of the exciting products that are now available on the casino floor

John Connelly Interblock highlights the evolution of table games in the digital age 52 80 MARGARITA CRUZ JOHN CONNELLY 64 PAUL KAVANAGH

PRODUCT REVIEWS 70

FINAL WORD 80

FACING FACTS

In keeping with our cover theme, Gambling Insider compares statistics from New Jersey and Pennsylvania from January to July 2023 – and July alone in more detail – as the neighbouring states tussle to outperform one another

New Jersey vs Pennsylvania total gaming revenue ($M) January – July 2023

Pennsylvania New Jersey

Sources: New Jersey Division of Gaming Enforcement, Pennsylvania Gaming Control Board

• As we can see from out first graph, Pennsylvania generated greater gaming revenue than New Jersey in five out of seven months through January to July. In fact, it outperformed New Jersey for the first five months of 2023, although New Jersey amassed greater revenue for June and then significantly more for July.

• The highest individual monthly total came in March, when Pennsylvania saw $515.3m in total gaming revenue. New Jersey’s highest total was July’s, at $506.2m.

New Jersey vs Pennsylvania sports betting & iGaming ($M) July 2023

Pennsylvania New Jersey

Sources: New Jersey Division of Gaming Enforcement, Pennsylvania Gaming Control Board

• Taking the most recent available results at press time, New Jersey comprehensively outperformed Pennsylvania when it came to sports and online casino. Its sports betting revenue was almost double that of Pennsylvania’s, from sports betting handle (total bets/turnover) of almost twice as much, too.

• For online casino (iGaming), New Jersey also edged Pennsylvania out for July by over $20m in revenue.

10 GAMBLINGINSIDER.COM

FEATURES NUMBER CRUNCHING

2021 1 Adjusted EBITDA Net loss 2021 100 200 0 January February March April May June July January February March April May June July 436.9 464.5 412.2 456.8 24.7 New Jersey vs Pennsylvania total gaming revenue ($m) January – July 2023 New Jersey vs Pennsylvania sports betting & iGaming ($m) Revenue ($ million) 1 3 300 400 500 600 5 10 0 New Jersey vs Pennsylvania monthly increases in gaming revenue (%) January – July 2023 2 15 20 25 487.4 515.3 462.7 476.7 470.9 479.3 457.2 440.5 506.2 467 100 200 0 January February March April May June July January February March April May June July 436.9 464.5 412.2 456.8 New Jersey vs Pennsylvania total gaming revenue ($m) January – July 2023 New Jersey vs Pennsylvania sports betting & iGaming ($m) Revenue ($ million) Revenue ($ million) 200 100 300 400 500 600 0 1 3 300 400 500 600 5 10 0 Sports betting revenue Sports betting handle (turnover) iGaming revenue 61 32.1 587 338.5 New Jersey vs Pennsylvania monthly increases in gaming revenue (%) January – July 2023 2 15 20 25 New Jersey vs Pennsylvania land-based casino revenue ($m) 484.5 4 487.4 515.3 462.7 476.7 470.9 479.3 457.2 440.5 506.2 467 155.2 132.8 298.1 290

New Jersey vs Pennsylvania year-on-year increases in gaming revenue (%) January – July 2023

Pennsylvania New Jersey

Sources: New Jersey Division of Gaming Enforcement, Pennsylvania Gaming Control Board

• Our third graph compares monthly growth for the same period (January to July) in both New Jersey and Pennsylvania. For every month during the period, each state saw growth, although this was strongest in January, when New Jersey’s gaming revenue rose 15% year-on-year – and Pennsylvania’s 18%.

• Growth steadied as the first half of 2023 progressed, with Pennsylvania only seeing a 3% rise in April and, despite having its best month of the year in terms of revenue, New Jersey only enjoying 5% growth. Still, New Jersey saw double-digit growth in five out of a possible seven months; Pennsylvania saw double-digit growth four times.

New Jersey vs Pennsylvania land-based casino revenue ($M) July 2023

Pennsylvania New Jersey

Sources: New Jersey Division of Gaming Enforcement, Pennsylvania Gaming Control Board

• Outside of sports and online casino, it’s interesting to note Pennsylvania was the stronger performer in terms of legacy retail verticals. New Jersey did generate a higher amount of slot machine revenue for July – but only just.

• Pennsylvania’s table games made over $10m more than New Jersey’s, however, ensuring its landbased casino revenue total for July surpassed that of the Garden State. That is a particularly notable statistic given New Jersey was so much higher in overall monthly gaming revenue July.

12 GAMBLINGINSIDER.COM January February March April May June July January February March April May June July New Jersey vs Pennsylvania sports betting & iGaming ($m) 200 100 300 400 500 600 0 5 10 0 Sports betting revenue Sports betting handle (turnover) iGaming revenue 61 32.1 587 338.5 New Jersey vs Pennsylvania monthly increases in gaming revenue (%) January – July 2023 15 20 25 484.5 155.2 132.8 2021 1.8 Adjusted EBITDA Net loss 2021 January February March April May June July New Jersey vs Pennsylvania sports betting & iGaming ($m) Revenue ($ million) 200 100 300 400 500 600 0 3 5 10 0 Sports betting revenue Sports betting handle (turnover) iGaming revenue Slot machine revenue Table game revenue Total casino revenue 61 32.1 587 338.5 72.1 15 20 25 214.7 217.8 Revenue ($ million) 100 50 150 200 250 300 0 238 New Jersey vs Pennsylvania land-based casino revenue ($m) 484.5 4 155.2 132.8 83.4 72.2 298.1 290 Bally’s Tropicana

FEATURES NUMBER CRUNCHING

FEATURES NUMBER CRUNCHING

New Jersey total gaming revenue broken down by operator/segment ($M) July 2023

Sources: New Jersey Division of Gaming Enforcement, Pennsylvania Gaming Control Board

• When broken down by operator, New Jersey’s July revenue was once again dominated by MGM Resorts’ Borgata, which brought in $127.6m in total gaming revenue (up 3% year-on-year).

• Other performers to stand out included Hard Rock Hotel & Casino Atlantic City (revenue: $62.8m), Resorts Digital (revenue: $59.5m) and Golden Nugget (revenue: $54m).

Hollywood Casino York - 8

Hollywood Casino Morgantown - 7.1

Video gaming terminals - 3.4

Parx Shippensburg - 2.7

Lady Luck Casino Nemacolin - 2.1

Bally's Pennsylvania - 1.4

Fantasy contests - 0.7

Sources: New Jersey Division of Gaming Enforcement, Pennsylvania Gaming Control Board

• Compared to New Jersey, Pennsylvania has far more operators that have contributed to its overall total, all with a smaller split.

• Hollywood Casino at Penn National Race Course generated the highest monthly total, at $70.1m, while the likes of Park Casino, Galley Forge Casino Resort and Wind Creek Bethlehem followed closely behind in the $50-57m region. Video gaming terminals and fantasy contests also produced just over $4m in revenue between them.

14 GAMBLINGINSIDER.COM Slot machine revenue Table game revenue Total casino revenue 214.7 217.8 Revenue ($ million) 100 50 150 200 250 0 238 83.4 72.2 127.6 Borgata 56.1 Parx Casino 47 Rivers Casino Philadelphia 31.5 Rivers Casino Pittsburgh 54.6 Valley Forge Casino Resort 25.1 Caesars 25.3 Harrah’s 42.4 Ocean Casino 15.3 Resorts 59.5 Resorts digital 8.6 Caesars Interactive NJ Bally’s 24.1 Wind Creek Bethlehem 51 Presque Isle Downs and Casino 9.7 Hollywood Casino at Penn National Race Course 70.1 Live! Casino Pittsburgh 9.8 Harrah's Philadelphia 19.1 Mohegan Pennsylvania 19.9 Mount Airy Casino Resort 22.8 Live! Casino Philadelphia 24.3 Hollywood Casino at the Meadows 25.7 Tropicana 32.3 Golden Nugget 54 Hard Rock 62.8 Slot machine revenue Table game revenue Total casino revenue Revenue 100 50 0 238 83.4 72.2 pennsylvania 127.6 Borgata 56.1 Parx Casino 47 Rivers Casino Philadelphia 31.5 Rivers Casino Pittsburgh 54.6 Valley Forge Casino Resort 25.1 Caesars 25.3 Harrah’s 42.4 Ocean Casino 15.3 Resorts 59.5 Resorts digital 8.6 Caesars Interactive NJ Bally’s 24.1 Wind Creek Bethlehem 51 Presque Isle Downs and Casino 9.7 Hollywood Casino at Penn National Race Course 70.1 Live! Casino Pittsburgh 9.8 Harrah's Philadelphia 19.1 Mohegan Pennsylvania 19.9 Mount Airy Casino Resort 22.8 Live! Casino Philadelphia 24.3 Hollywood Casino at the Meadows 25.7 Tropicana 32.3 Golden Nugget 54 Hard Rock 62.8

Pennsylvania total gaming revenue broken down by operator/segment ($M) July 2023

TAKING STOCK

Gambling Insider tracks operator prices for companies who operate in New Jersey and/or Pennsylvania, tallying with this issue’s main cover theme. Stock prices are taken across a six-month period (March 2023 to August 2023) – and from the close of the first available date of the month

New Jersey/Pennsylvania operators with market capitalisation of $10bn or greater

• Six-month high - August ($57.69) • Six-month low - June ($41.66)

• Market capitalisation - $12.43bn (As of 1 August)

• Six-month high - August ($50.08)

• Six-month low - June ($39.12)

• Market capitalisation - $18.23bn (As of 1 August)

• Six-month high - May (£157.90)

• Six-month low - March (£134.90)

• Market capitalisation - £35.72bn (As of 1 August)

• Six-month high - August ($31.58)

• Six-month low - March ($18.32)

• Market capitalisation - $34.57bn (As of 1 August)

16 GAMBLINGINSIDER.COM

FEATURES NUMBER CRUNCHING

CAESARS MGM RESORTS FLUTTER ENTERTAINMENT DRAFTKINGS 40 DraftKings 30 20 10 0 March USD April May 80 MGM 60 40 20 0 March USD April May 100 Flutter 50 300 350 250 200 150 0 March GBP April May July August June 80 Caesars 60 40 20 0 March USD April May July August June 40 DraftKings 30 20 10 0 March USD April May June 80 MGM Resorts 60 40 20 0 March USD April May June 100 Flutter 50 300 350 250 200 150 0 March GBP April May July August June 80 Caesars 60 40 20 0 March USD April May July August June 40 DraftKings 30 20 10 0 March USD April May July August June 80 MGM Resorts 60 40 20 0 March USD April May July August June Flutter July August June July August June 40 DraftKings 30 20 10 0 March USD April May July August June 80 MGM Resorts 60 40 20 0 March USD April May July August June Flutter July August June Caesars July August June

New Jersey/Pennsylvania operators with market capitalisation of less than $10bn

• Six-month high - March ($20.35)

• Six-month low - June ($14.13)

• Market capitalisation - $740.2m (As of 1 August)

• Six-month high - March ($4.26)

• Six-month low - June ($3.02)

• Market capitalisation - $841.69m (As of 1 August)

• Six-month high - June (SEK 126.45)

• Six-month low - April (SEK 111.15)

• Market capitalisation - SEK2.72bn (As of 1 August)

• Six-month high - May ($149.08)

• Six-month low - August ($116.86)

• Market capitalisation - $8.76bn (As of 1 August)

18 GAMBLINGINSIDER.COM

BALLY’S RUSH STREET INTERACTIVE CHURCHILL DOWNS KINDRED GROUP

SUPPLIERS 160 180 140 120 100 0 March USD April 25 20 15 10 0 March USD April 160 Kindred Group 180 140 120 100 0 March SEK April May July August June 25 Bally’s 20 15 10 0 March USD April May July August June SUPPLIERS 160 180 140 120 100 0 March USD April 25 20 15 10 0 March USD April 160 Kindred Group 180 140 120 100 0 March SEK April May July August June 25 Bally’s 20 15 10 0 March USD April May July August June 160 Churchill Downs 180 140 120 100 0 March USD April May July August June 25 Rush Street Interactive 20 15 10 0 March USD April May July August June July August July August 160 Churchill Downs 180 140 120 100 0 March USD April May July August June 25 Rush Street Interactive 20 15 10 0 March USD April May July August June July August July August

FEATURES NUMBER CRUNCHING

G LOBAL GAMING AWARDS T IMEL INE

As the 10-year anniversary of the Global Gaming Awards approaches, Gambling Insider takes a look at some of the highlights the last decade has thrown up

MGM wins three Global Gaming Awards in Las Vegas, including Land-Based Operator of the year (for the second year running). Meanwhile, Scientific Games wins Land-Based Industry Supplier of the year

Wynn Resorts takes MGM’s crown and wins the Land-Based Operator of the year Award. Sportradar takes home Responsible Business of the year

The debut Global Gaming Awards ceremony in London takes place at The Hippodrome, with bet365 winning Online Sports Betting Operator of the year

FEATURES 10 YEARS OF WINNERS 2014

2015 2016 2017 2018

The first Las Vegas Awards ceremony is held at The Venetian Hotel & Casino in Las Vegas

MGM completes a hat-trick of Land-Based Operator of the year Awards by winning again in Las Vegas – while Playtech wins Digital Industry Supplier of the year

20 GAMBLINGINSIDER.COM

In Las Vegas, Interblock's Stadium wins Land-based Product of the year Award, while DraftKings wins Digital Operator of the year

10 YEARS OF WINNERS

FEATURES

At the second Asia-Pacific Global Gaming Awards, Marina Bay Sands wins Integrated Casino of the year, while BetConstruct wins Digital Supplier of the year

2019 2020 2022 2023 2021

At the Global Gaming Awards London, Evolution wins Online Casino Supplier of the year, with Paf winning the Corporate Responsibility Programme of the year Award

The first Global Gaming Awards Asia-Pacific takes place with a virtual presentation ceremony, with Bloomberry Resorts winning three Awards that year, including Casino Operator of the year 21 GAMBLINGINSIDER.COM

Aristocrat wins three Awards, including Land-Based Industry Supplier of the year. Meanwhile, Soo Kim, Bally's Chairman, is named American Executive of the year

FEATURES COVER FEATURE 22 GAMBLINGINSIDER.COM

PURSUIT OF GREATNESS

Outside of Nevada, Pennsylvania and New Jersey are two of the strongest hubs within US gaming. Gambling Insider explores both neighbouring markets, the remarkably similar numbers they have been posting and what the

future holds for both

Two markets, two states, two different ways of making vast sums of gross gaming revenue (GGR) – yet markets that are seeing phenomenal success compared to the rest of the US (outside of Las Vegas, of course).

Pennsylvania’s journey with casinos and gambling began with Act 71, which passed in 2004 and established the Pennsylvania Gaming Control Board – allowing racetracks to be legalised for the first time in modern US history.

the huge figures reported by Pennsylvania every quarter are comparable to anywhere in the US behind the ancestral hub of US gambling, Nevada.

Over the course of the next 20 years,

Over the course of the next 20 years, the state saw casinos come into being, while online betting was signed into law in 2017 and sports betting legalised in May 2019. To say that the state took to gambling as a duck does to water may not be a stretch, as

But, of course, Pennsylvania doesn't have to look far for a competitor. Indeed, it is geographically placed right next to another US gambling hub: New Jersey, the home of Atlantic City. In its time, New Jersey has seen many casinos come and go – with stars such as Frank Sinatra and Sam Cooke playing the gambling halls across the decades. Sinatra even allegedly once grabbed Donald Trump by the tie over a disputed contract at the Taj Mahal Atlantic steeped in rich history.

City. So, New Jersey’s gambling history is

23 GAMBLINGINSIDER.COM COVER FEATURE FEATURES

New Jersey and Pennsylvania both have land-based casinos, online sports betting and online casino – and have been live for a number of years – making them a very useful case study in the typical US gaming market that has access to all the major verticals. Bucking the historical trend, in recent times, Pennsylvania has been slightly outperforming New Jersey in terms of revenue but figures vary month to month in an intriguing tussle of GGR. So, Gambling Insider looks into how the two states are performing, how they got to where they are today – and where their next sources of growth lie.

PLAYERS & MARKET TRENDS

Speaking to Gambling Insider about the trends seen in players across both states, Diane Spiers, VP of Marketing & Public Relations at operator Bally’s, highlighted the changes seen since the Covid-19 pandemic, as normality is resumed for land-based gambling. She said: “As the gaming industry returns to normalcy, gaming and non-gaming experiences are being reintroduced to the market, as well as many new offerings aimed at appealing to shifting player trends and tastes. Today’s players are seeking new and exciting experiences that offer more opportunities to win, including new high-tech slot machines, tableside bets and progressives for slot machines and tables.”

Meanwhile, Kambi’s Head of Commercial Pre-Sales, Kevin Cunningham, also commented on both states’ attitude towards sports betting and how New Jersey’s stake size has grown significantly larger than Pennsylvania’s in the last year. He explained: “On a player behaviour level, one of the biggest surprises we have seen

on the Kambi network is that the average stake size in New Jersey in the last 12 months is approximately twice that of what we have seen in Pennsylvania. We’ve also seen more live betting turnover in New Jersey than we have in Pennsylvania, with live accounting for 44% of New Jersey’s turnover in the last year compared to 34% in Pennsylvania.”

Cunningham’s comments are no surprise to anybody that looks at the monthly sports betting figures for both states, as New Jersey’s sports betting market dwarfs that of Pennsylvania. For July 2023, sports betting handle in New Jersey totalled $587m, while Pennsylvania posted $338.5m. What this indicates is that players in New Jersey are significantly more committed to the market than those in Pennsylvania. Cunningham also stated that he believes New Jersey is likely to stay ahead of Pennsylvania: “Despite the proximity, there are a few key nuances as to why New Jersey will likely stay ahead of Pennsylvania. The first is that online sports betting in New Jersey launched nearly a full year before Pennsylvania and they benefit from having more operators for bettors to choose from. New Jersey offers customers 22 online sportsbooks compared to 12 in Pennsylvania.”

He further added: “Pennsylvania’s growth story continues to push forward. Over the last 12 months, Pennsylvania has grown at a higher rate than New Jersey in revenue. With a population of nearly four million more people, there is greater growth upside for the state, but New Jersey’s propensity to wager still appears to be amongst the strongest in the US.”

CASINOS

When it comes to both markets, one of the biggest increases is found in the iGaming vertical. After the pandemic ravaged the land-based casino market, players had to find other ways to play their favourite casino games – and the internet provided the perfect solution to such a problem. However, now that the pandemic is over and casinos are once again welcoming visitors, some are struggling to see the in-person footfall that was seen before Covid.

That said, the extent of the impact this is having on land-based casinos is disputed by Jody Madigan, Mohegan’s COO. He argues that whilst iGaming is growing, it doesn't signal the death of the casino floor. “The impact on retail gaming in the markets we operate or manage is minimal. IGaming and online sports betting are still relatively new, but they have added more excitement and promotional opportunities for players.”

Madigan continued: “While they are convenient and enjoyable, they lack the atmosphere, thrill and social experience that comes with visiting a resort casino. Therefore, many guests still enjoy both iGaming and casino experiences. This trend is likely to continue, especially with the integration of online and retail rewards programs.”

It appears that those who work within the land-based casino market do not see why iGaming and retail can’t work hand in hand, rather than being fierce rivals. Of course, common sense would say iGaming will have a long-term impact on casinos, though casinos themselves will never become obsolete due to the communal nature and destination excitement that can only be felt in property.

SCCG Co-Founder and CEO, Stephen

24 GAMBLINGINSIDER.COM

FEATURES COVER FEATURE

JACOB CLAESSON CEO North America, Evolution

JODY MADIGAN COO, Mohegan

Crystal, also comments on the impact iGaming is having on casinos, as he told Gambling Insider: “The effect this is having on places such as Atlantic City – the hub of New Jersey’s casino industry – is causing many operators to invest heavily in online partnerships and focusing on having a diversified offering to players both online and retail. On a macro level, the overall gaming wallet is going up with online and retail. On a micro level, some operators who have not been able to provide the full 360-degree experience find the brick-and-mortar wallet declining a bit. But, overall, it’s a growing wallet for both retail and online.”

In New Jersey, a place that the famous Atlantic City Boardwalk calls home, the history of landbased casinos runs through the streets. More than the aforementioned famous names such as Sam Cooke and Sinatra, it was a city that had significant connections to organised crime and mob links – now, in 2023, that is all in the past – but the city is still home to gambling on the East Coast and is proud of it.

In discussing Atlantic City and whether or not it can push harder to close the land-based casino GGR gap that exists between New Jersey and Pennsylvania, Madigan stated: “To be honest, we predict that both states will maintain their high rankings in the US regarding casino GGR. Market trends can change rapidly and these changes can significantly affect a casino hub like Atlantic City, as the casinos are located close to each other. Pennsylvania has an advantage because it has more casino destinations spread out across a large state and competition and

market trends differ in this landscape.”

However, Madigan was still keen to highlight the ‘robust’ New Jersey market. He said: “New Jersey’s robust tourism industry will likely continue to be a market strength, especially given the state’s reliable seasonal tourism. In particular, Atlantic City, with its beach, ocean and boardwalk attractions, will continue to attract a range of tourists, especially as the city continues to invest in capital improvements.”

TABLE GAMES IN DECLINE?

There is one area of concern for landbased casinos across both New Jersey and Pennsylvania, though. And it might just be an area of concern across the US: declining table game revenue. The decline has been seen across the board, with the American Gaming Association (AGA) reporting that table games has fallen by 2% in Q2 – though the practice has still drawn in $2.46bn. Madigan highlighted the impact of Covid and how people moving away from urban areas has affected the ‘volatile’ table games figures, saying: “There is always more volatility in table games vs. slot machines – both in volume and in win. Some of the bigger casino guests tend to lean towards tables, so macroeconomics always plays a part in table revenues. And as we have seen with other industries post-Covid, some portions of the population have moved away from the large metropolitan areas such as New York and Philadelphia, which certainly feed both markets. Even if a handful of larger players relocate, it could have a relatively larger impact on your table volumes.”

The impact that this could have on Pennsylvania over New Jersey could tip the balance from one to the other, as Pennsylvania has more of a reliance on table games than New Jersey – although, both report huge figures in table games every month. Spiers spoke of this issue in her comments to Gambling Insider and stated that staffing levels has had a severe impact on table games as a whole: “One of the biggest issues concerning table games is the lack of available dealers nationwide as a result of the pandemic. It is likely, however, that the demand for table games could rebound when staffing returns to pre-pandemic levels. Regional competition has also played a role in any softness, particularly in the northeast market, with the expansion of gaming into new markets over the last few years.” She aadded: “We also recently partnered with Stockton University to create a Dealer Training School program and local dealer training school.”

SPORTS BETTING

The impact that sports betting has had on the US gambling market has been seen in the sheer sums that it has been reporting. In New Jersey, sports wagering revenue hit $501.8m for the

year so far in July, representing a 42% annual increase. This is now ahead of the $426.4m table game win reported by the state for the same 2023 period, which fell by nearly 2%. The rise of sports betting is continuing, too. Every month the growth figures in New Jersey are in the double digits and it shows little sign of slowing down.

As for Pennsylvania, its sports wagering revenue doesn’t compete with New Jersey’s, as stated earlier. For July 2023, it reported $32m in revenue, which is a rise of 26%. When comparing that to Pennsylvania’s table games revenue, table games is still handily ahead at $83.4m (with New Jersey’s July sum totalling $72.2m) – however that sum is still down by 4% annually. So, while sports betting is growing nicely in Pennsylvania, it is nowhere near the levels of New Jersey, which posted $61m in sports wagering revenue in July.

On whether New Jersey and Pennsylvania’s sports betting growth will continue in the long term, Cunningham said: “With Pennsylvania and New Jersey being two of the more mature states, we are still in a phase of growth; however, I think we are seeing signs of maturation within both states. New Jersey saw a 13% decrease in handle, and Pennsylvania only increased 2% in handle over the last 12 months. However, a major portion of this is attributed to the growth of bet builder products and as margins increase, there is a natural squeeze on handle.”

But the question must be asked: ‘Why isn’t Pennsylvania’s sports betting revenue of a

26 GAMBLINGINSIDER.COM FEATURES COVER FEATURE

DIANE SPIERS VP Marketing & PR, Bally's

KEVIN CUNNINGHAM Head of Commercial Pre-Sales, Kambi

similar size to New Jersey’s?” Well, a reason for that is presented by Cunningham, as he noted some differences in the framework of sports betting in both markets: “Every state and jurisdiction also comes with its own set of regulatory frameworks that each operator and supplier must abide by. A specific example between Pennsylvania and New Jersey is the NFL Draft. In New Jersey, regulators allow markets for bettors to wager on draft picks, whereas bettors are not allowed to wager on that specific event in Pennsylvania.”

Although it is a small difference, it shows that New Jersey is slightly more tailored to the sports betting market than Pennsylvania – and showing why the Garden State consistently re cords higher figures month-on-month. Sports betting has become a source of income for both online and land-based operators in New Jersey and Pennsylvania, and the growth statistics show that it hasn’t finished maturing yet.

Madigan also commented on the markets in the long run and which has an advantage over the other: “Both markets are robust, and it remains to be seen which one will perform better in the long run. While New Jersey has a higher income base, Pennsylvania boasts a larger population.”

REGULATION

Of course, regulation has a large impact on the bottom line in both states – and while Pennsylvania and New Jersey both have similar levels of regulation, there are some differences. Jacob Claesson, CEO North America at Evolution, highlights the contrasts found in the tax rates of both states: “Operators in New Jersey pay 17.5% tax on gross revenues regardless of the type of online game. Operators in Pennsylvania, meanwhile, pay 16% on table games like blackjack, roulette and baccarat, but as high as 54% on gross revenues from slots. But in most other respects, aside from branding, our licensees’ casinos in these states have similar specifications.”

THE FUTURE

Looking at both New Jersey and Pennsylvania as a whole, Gambling Insider can't help but ask which will become the more dominant in the next 10 years – will New Jersey’s superior sports betting market push it ahead of Pennsylvania or will Pennsylvania’s strong iGaming and casino market eventually win out? Claesson highlights that both markets are very similar in scale. he stated: “Looking at online casino, New Jersey and Pennsylvania are roughly the same in market

size, with Pennsylvania slightly higher in total gaming revenues each month. Table games are much more significant in Pennsylvania given the more favourable tax treatment in comparison to slots. It’s too close to call. Both have a lot of headroom for growth.”

Meanwhile, the SCCG founder dove straight into his Crystal ball... “Pennsylvania, as it is the less penetrated and less mature market and has the larger population.”

Madigan was less committal when asked the same question, stating: “It’s a tough decision to make, but we believe both states will continue to be major players in the casino industry. They are likely to remain among the top five states when it comes to casino revenue in the country.”

Finally, Spiers was keen to highlight New Jersey’s strengths going forward. She concluded: “We believe the state will serve as an important model, as other states begin to adopt online as a vehicle for offering sports and casino entertainment. Along with this, we envision that New Jersey casinos will band together to support the state as a first-class gaming destination.”

In the end, only time will tell which market pulls ahead in the near future – but, for now, the two states will remain directly in competition, in the pursuit of greatness.

28 GAMBLINGINSIDER.COM FEATURES COVER FEATURE

“THE FULL 90 MINUTES”

Miles Baron , CEO of the Bingo Association, speaks to Gambling Insider Editor Tim Poole about the impact of the White Paper on the UK land-based bingo sector – and why we are only at “half-time” in the process

If we’re to start at a proverbial ground zero, I’d like to start with a very basic question. What was your take on the UK’s Gambling Act White Paper? And how did it affect bingo in particular?

I think there are four areas that particularly

relate to land-based bingo. In no particular order, one is cashless and the use of a debit card directly onto a gaming machine. The second is the removal, or at least the amendment, of the 80-20 rule. This is where you’re only allowed one in five of your machine entitlement to be a category B3 machine. The third would be bingo bets – an attempt to broaden the understanding and definition of what is a game of bingo within a

licensed bingo premise. And then the fourth the four things that are really

licensed bingo premise. And then the fourth area is more of a concern: the threat of a statutory levy, particularly one that’s higher than the current level is now. So those are the four things that are really preoccupying us with regard to the White Paper.

Is it too simplistic to say “three are good and one is potentially bad?” Yeah – you could say three good and one is to be avoided.

Different sectors have been affected in different ways. For example, land-based casinos can now go from 20 slot machines to 80 if the White Paper’s recommendations are written into law, so there’s a huge plus for them. Obviously, for online operators a lot of the recommendations have been more restrictive. Is bingo on the more positive side of what’s been affected by the White Paper?

in different ways. For example, land-based for them. Obviously, for online operators a positive side of what’s been affected by the White Paper?

the first time in a long time, really seeks to differentiate between land-based businesses own different challenges. And I think, for got some opportunities in it. Whereas for rightly say, as more restrictive regulation. licensed bingo premises within Great Britain

Yes, definitely. I think the White Paper, for the first time in a long time, really seeks to differentiate between land-based businesses and online businesses; it acknowledges they’re different and that they have their own different challenges. And I think, for the land-based sector, the White Paper has got some opportunities in it. Whereas for the online world, they will just see it, as you rightly say, as more restrictive regulation. At the Bingo Association, we solely represent licensed bingo premises within Great Britain and not online operators.

Would that mean online bingo operators are effectively your competitors?

operators are effectively your competitors?

Well, when I was giving evidence recently in the House of Commons about the impact of the White Paper, I was asked that very question by the Chair: exactly how and where does online bingo fit in? We’re quite clear that it’s been around a long time and it’s here to stay. It is competition, but so are lots of other things. Would you rather you have no competition? Of course you would. But online bingo is not going away, so we have to learn to compete with it; and some of our members in the Bingo Association do have an online presence as well. So we can’t claim to be categorically landbased only, as the likes of Mecca and Buzz, to name but two, also have online bingo sites.

about the impact of the White Paper, does online bingo fit in? We’re quite clear that it’s been around a competition, but so are lots of other things. Would you rather you have would. But online bingo is not Association do have an online presence as well. So we can’t claim to be categorically landthe and Buzz, to name but two, also

FEATURES UK LAND-BASED BINGO

30 GAMBLINGINSIDER.COM

Miles Baron, CEO, Bingo Association

Could you give us a summary of your main points when providing evidence in the House of Commons?

One of my main points reinforced what we just mentioned, that we’re largely focused on land-based. There was a suggestion from the Chair that TV adverts that were glamorising online bingo may in some way spill over into land-based bingo. But that’s not the case. In our sector, I think there’s a concern that if you glamorise bingo for women, more women will take up gambling and potentially over time become vulnerable to harm. But we’re not seeing any connection at all between online and retail.

I was also asked about the levy. In many ways, the levy was the biggest issue that came up in the hearing. Land-based has a very different model to online. We have staff heating, rent, all these sort of costs to bear. So gross gaming yield is a bit of an unfair way of assessing what we should pay in terms of a levy. We’ve made it quite clear we make something like £40m ($51.9m) a year in profit and that’s probably the most we’re going to make this year; it could be as low as £35m. The current contribution point of 0.1% is worth nearly £500,000, so you can see that even at that level, half a million out of a profit of £35m is still quite a big chunk. If that was to increase or even double to £1m, it eats into industry profits. And then you start to see operators buckle under that sort of fiscal pressure, particularly when we’re perceived to be at the low end of the harm threshold. So we’re fighting really, really hard to make sure that, if there is a statutory levy, it’s not set at a higher rate than it already is.

In terms of what you’re expecting – or at least hoping for – what kind of time frame is there before we see actual change, and the White Paper’s recommendations are written into law, when operators can definitively act on it?

There are commonly quoted as 62 different pieces of work to come out of the White Paper and obviously that’s all going to take time. I think the Gambling Commission have made it quite clear they want to get the big-ticket issues out of the way as they see them; which

are, as you describe, largely online-based and “restrictive.” So the concern of land-based is that it’ll take a long time for any of these liberalisations to come through and, by the time they do, it’ll be too late. It’ll be another year and a half or two years down the line and land-based is finding it hard enough already.

So what we’re trying to argue for, and what we’d like to see, is a bit of parity between some of the restrictive, for lack of a better word, regulation and some of the liberalisation that might come to the industry. Otherwise, it’s going to be front loaded with regulatory restriction and any good to come out of the Act will come towards the end.

If there was one thing you could single out and hope for at this stage, what would it be specifically – other than just a speeding up of the process?

The biggest quick win for us is probably the 80-20 rule on category B and category C gaming machines. If that would come in pretty quickly, there’d be some short-term benefits and that would be incredibly useful. It would also be good to have some certainty about where the levy is going to be set as quickly as possible.

There might not be anything within those two specific examples; but are there any measures bingo operators can pre-emptively take right now?

We know exactly what these initiatives are going look like. We’ve got a White Paper that’s now saying this is what we’re going to do. We’ve got a whole load of consultations that we are going to have to negotiate in terms of how we do it and what it will look like when it’s done. So you could

argue that, actually, we’re only at the halfway mark: we’re at half-time in a football match. We’ve got the decision and that’s taken us a long time to get to. It’s taken us two to three years and lots of different administrations and ministers. But now we’re in a battle to get these things implemented and delivered onto the High Street. There are still a lot of negotiations and a lot of detail to be decided.

Is it at least a relief that we’re at that “half-time” point, because obviously we were waiting for the actual White Paper for so long?

I think the industry would like to be at the full 90 minutes. Yes, we’ve got the White Paper. Finally, we know what it says. Let’s just get on with it and make it happen – good, bad or ugly. But I think there’s going to still be a lot of toing and froing on exactly what it looks like. In between all the bumps in the road, which is energy, the White Paper and a cost of living crisis the underlying business has been quite resilient. And thank goodness, following a really difficult period during the Covid-19 pandemic. Like many others, we’re not the only ones. We know that. But it’d be nice to have a period of time without any bumps in the road, so we can continue to grow, develop, innovate and invest in new businesses. To do that, you need certainty. Every business will tell you they need certainty. Bingo is no different. So we would like to get the White Paper enacted as quickly and as efficiently as possible I would like the DCMS, the Gambling Commission and the industry to work really hard and really quickly – to get these liberalisations and new regulations in place as soon as possible. So that we’ve got a clear vision and we can move forward quickly.

31 GAMBLINGINSIDER.COM UK LAND-BASED BINGO FEATURES

“At the Bingo Association, we solely represent licensed bingo premises within great Britain and not online operators”

A SISYPHEAN TASK

Regular Gambling Insider columnist Paul Sculpher , Director of GRS Recruitment, returns for our September/October issue – this time joined by

Melanie Ellis of Northridge

Law LLP

With the semi-mythical White Paper finally materialising, there have been more than enough opinion pieces on its contents. There are a number of potentially drawn-out consultation processes in play, so it’s safe to say there will a variety of forecast outcomes. Personally, I tend to view these in the same light as the many, many incorrect predictions about the appearance date of the paper itself. In other words, let’s wait and see.

In the meantime, it’s interesting to think

about how the law and its interpretation has shaped how gaming has developed in the UK. Some would tell you that the 2005 Gambling Act was a poorly drafted piece of legislation, but it’s also worth reflecting on the level of scrutiny aimed at the detail by operators keen to gain an edge.

The history of betting shop workarounds can perhaps be traced back to the advent of the National Lottery in 1994. Under the 1968 Act, bookmakers risked losing their permit

if they offered bets on the outcome of the lottery draw, but were nevertheless facing the loss of regular custom to the new gambling opportunity presented by the lottery. Undeterred, bookmakers began offering bets on the outcome of Ireland’s National Lottery and later devised the concept of betting on their own draw of six numbers between 1 and 49.

A group of operators set up a company, 49s, to run the draw (it involved the mechanical

FEATURES UK REGULATION

32 GAMBLINGINSIDER.COM

drawing of balls in a similar way to the National Lottery) and it was televised in betting shops across the country. Camelot sought to challenge the legality of the scheme, bringing a private prosecution against the bookmakers, but this was ultimately unsuccessful. The concept was now established that a bet can be made on a draw of random numbers and that such a bet did not amount to a lottery.

When Fixed-odds betting terminals (FOBT) began to appear in the UK, it was pretty much as simple as someone saying to themselves “what’s the difference between betting on a horse in a 37-runner race and betting on one of 37 numbers on a wheel?”

The previous legal acceptance of betting on a basic draw of numbers facilitated that thought process. Just like that, the face of betting shops and the national conversation about gambling changed forever. We all have our own opinions about how well they fitted into the legislative structure of the industry at the time, but their genesis speaks to the entrepreneurial approach from operators.

Fast forward a little further to around 2005, when “Section 21” and “Section 16” machines appeared on the scene. These machines fell outside the definition of gaming machines because the RNG (random number generator) was located outside of the machine itself and offered a maximum stake of £2 ($2.57) and maximum prize of £25. Again, you’d argue the spirit of the legislation was to limit stakes and prizes on games that looked like slot machines, but nobody foresaw the technology being able to cope with 20 simultaneous games.

Through that omission, it became possible for these machines to doubly swerve around the law by offering 20 simultaneous games of prize bingo – with the prize being cash – at once, for a £500 top prize. Of course, the law ended up having to adapt to try to get ahead of the evolving situation on the ground, but

with inspiration taking seconds and legal change taking months if not years, there’s only ever one winner.

The 2005 Act formalised the status of these machine types through its definition of a gaming machine, which includes any machine offering a game that has its result determined by computer, or which has images generated by computer to represent a real or imaginary game, race or any other event or process. Section 16 and 21 machines were reclassified as category B3 gaming machines and FOBTs as B2 gaming machines.

Putting oneself in the position of the people who will eventually draft the law is a scary prospect. Trying to cover every base when you know some of the sharpest minds in the industry will ferret in the cracks of the legislation must feel a tad Sisyphean – even in the gap between writing the law and it being enacted, some parts of it will be either obsolete, vulnerable to a workaround or both. Simply think back to when arcades were only allowed four higher-prize slots per licence and legislators must have sat back, pleased with their work. Smug mode was probably short lived, however, when some operators simply subdivided existing large properties into, say, four smaller ones, to offer 16 slots in what was essentially the same unit (while respecting mandatory premises licence conditions, planning, fire safety etc etc).

Online gambling also started life as something of a workaround. It had always been lawful for licensed bookmakers to take bets over the telephone so, in the 1990s when computers with internet connections began to become commonplace, they took advantage of the ability to accept bets remotely in a new way. New operators began to apply for bookmakers’ permits simply to enable them to offer online betting.

Online casinos presented a greater challenge. Operators of these sites could not be located in Great Britain without violating the Gaming Act 1968 because it was a requirement that persons participating in gaming offered under a 1968 licence were present on the premises. Eventually, the Gaming Board for Great Britain (the predecessor of the Gambling Commission) accepted that it was not illegal for British customers to gamble on unlicensed offshore websites from their own home, provided advertising restrictions in the 1968 Act were complied with.

The 2005 Act originally left this loophole open – provided operators located their key equipment in an EEA or “white list” jurisdiction, they were free to continue to provide services and advertise to customers in Great Britain. This left a significant amount of potential tax revenue offshore, as well as leaving the Gambling Commission unable to impose regulatory requirements

on the majority of operators servicing British customers. It is perhaps surprising that it took until 2014 for the Government to introduce “point of consumption” licensing. Looking ahead to the implementation of the White Paper’s proposals, a key point for the legislators to get right will be the definition of online slots games, for the purposes of applying the stake limit (wherever that ends up falling between £2 and £15). The Remote Technical Standards currently define slots as “casino games of a reel-based type (including games that have non-traditional reels.)” Reelbased games have an enduring popularity but a stake limit at the lower end of the potential range will create a high incentive to develop games of a similar nature to slots, while not including reels or “non-traditional reels.”

Whatever the result of the consultation process, razor sharp minds will instantly be looking to determine any weak point in the legislation to get the very best angle on the embryonic law. Watch this space...

33 GAMBLINGINSIDER.COM UK REGULATION FEATURES

“Trying to cover every base when you know some of the sharpest minds in the industry will ferret in the cracks of the legislation must feel a tad Sisyphean”

Paul Sculpher

Melanie Ellis

IN THE DEPARTMENT WE TRUST

Paul Sculpher is in action for his second column of our September/October issue, this time speaking with Michael Byrne from the Department of Trust about the pressing issue of a ordability

As the UK’s Gambling White Paper excitement gives way to a mass of consultations, with the final destination perhaps little clearer than it was a year ago, there’s mention in the report of something which to me, as someone with an offline background, prompted a bit of research. Indeed, in the section of the White Paper related to online protections, there’s mention of open banking – although they’ve not even capitalised it. Like perhaps most people, I

only recently realised that open banking was a significant movement in the UK banking industry.

A year or so ago, I opened my company bank account app (NatWest) and was presented with a prompt asking if I’d like to add other bank accounts into the same app so I could see all balances at once. Thinking this was some sort of witchcraft, I followed the process and lo and behold, my personal banking (Nationwide) was listed too, with a balance. At the time, I

thought “well, that’s handy” – obviously only one spot to check now rather than two – but didn’t think much more about it.

However, it has huge implications for the betting and gaming sector, offline and online, in the area of affordability checks. I spoke with Michael Byrne from the Department of Trust about how this impacts operators’ ability to run these checks. Michael told me: “We’ve developed our product, BetBudget, to be as user-friendly as possible. The customer just downloads the app

34 GAMBLINGINSIDER.COM FEATURES OPEN BANKING

or goes through the equivalent process logging in via the web. They link their banking to the app – and they’re all set. The beauty of the system is that you only have to set up once and you can then allow access to any betting provider that’s affiliated.”

I looked a little deeper into the actual nuts and bolts of how the whole system works and it’s pretty intuitive. The basic principle is dead simple – allow BetBudget access to all your banking in one go, so a clear picture of your finances and what you can afford can be built up. Then, as a customer, whenever an operator needs information from you, they send a request and you authorise it on your phone if you’re comfortable. There are various levels of access that operators can request, depending on what they’re trying to verify and how big a player is – and perhaps depending on what trigger levels eventually emerge after consultation is complete and the new law steams into view.

With my offline operator hat on, the possibilities are pretty exciting. They’re the most exciting for, for example, casino shift managers who now spend an inordinate amount of time chasing players for bank statements, payslips (that aren’t forged), company details and so on. The concept that all that could just be replaced by an app where you’ve direct access to the real numbers behind the paperwork is very enticing. That’s a ton of work off those guys’ desks and it also would massively reduce the amount of people who simply stop visiting because of these requests.

A lot of focus on affordability is around people

who genuinely are playing beyond their means or wish to hide their incomes, but we shouldn’t underestimate how many potential customers simply can’t be bothered to participate in the process and go and do something else with their time instead. Clicking an “authorise” button on an app sounds like a whole lot less hassle than sitting down with your paperwork for what feels like an interrogation – from every operator you’d like to frequent.

I also asked Michael about the minimal level of commitment required to download an app – surely that is something of a barrier to some potential players. He told me “not all operators want to have people download the app – some will have a separate re-skinned landing page, developed by us, so the player stays within the comforts of the website they’re used to”.

The authorisation to run searches that is set up via open banking doesn’t affect a player’s credit record at all: it’s a totally different process.

Clearly something has to change in the world of affordability, from two perspectives. The industry can’t go on with flimsy selfcertificated questionnaires and some of the stories of spend levels without even a question being asked don’t paint the industry in a good light. I think that’s all generally accepted, but at the same time the amount of resource needed to manually gather, verify and archive multiple pieces of paperwork is bordering on ludicrous – and a huge number of players are put off by the effort required. Giving operators effectively direct access to the subset of your financial background, that they need to give you the thumbs up, saves an eternity of time for the operator and a fair bit for the player; so this tech is one to watch. Around 500 UK offline casino managers will, one day soon, be eternally thankful for what the Department of Trust, alongside other payments technology suppliers, is doing.

36 GAMBLINGINSIDER.COM

OPEN BANKING

FEATURES

Michael Byrne

"This technology has huge implications for the betting and gaming sector, offline and online, in the area of affordability checks”

Paul Sculpher

‘DIRTY LAUNDRY’

Daniela Guerreiro, Associate at MdME, discusses the prevention of money laundering in Macau casinos

It is no secret that the gaming sector has been called out as being especially vulnerable to the dangers of money laundering. Casino activity is known for being cash intensive and involving high volumes of fast-paced transactions. In other words: music to the ears of money launderers.

Macau, being a vast gaming hub, is no exception. Up until recently, Macau was well known for its ‘junket model.’ Junkets (or ‘gaming promoters’) were vital to luring high rollers to casinos, by offering free accommodation, travel and other perks. Most importantly, gaming promoters were also allowed to provide credit facilities and collect debts. This would mean the junket program allows movement of funds to and from the casino, allowing the concealment of potential dirty funds and identity of money launderers.

The new Macau gaming law has shut down the typical junket model as we knew it. With the new restrictions – including the rule of exclusivity (gaming promoters may only be engaged by one gaming concessionaire) and prohibition of revenue sharing arrangements – junkets still operating in Macau are facing a difficult time. Additionally, to enhance the safeguarding of national security and to address further money-laundering and illegal cross-border flow of capital, the new law now prohibits junkets from depositing chips or funds (by itself or on behalf of others) – to further curb the movement of illegal assets.

The amendments introduced by the new law seem to be on the right track to respond to money laundering concerns. In fact, the changes show Macau’s promise to maintain its technical compliance with the Financial Action Task Force’s (FATF) 40 Recommendations, as previously echoed in the Asia Pacific Group on Money Laundering’s (APG) Mutual Evaluation Follow-up Report, published in 2019. But is it enough?

The anti-money laundering (AML) landscape is constantly changing and should continue to evolve to respond to new, and potentially more sophisticated, means to launder money. With new AML-related rules, such as those mentioned above, criminals will also adopt newer strategies to avoid being detected. Although junkets can no longer be a participant in the movement of funds, money launderers still have a variety of schemes to choose from, including structuring operations, refining techniques, colluding with other players and buying other players’ winnings, etc.

Macau authorities understand the need for an update of AML laws, regulations and guidelines, especially in the gaming sector, which continues to be the meal ticket of Macau’s economy. During the first Interdepartmental AML/ CFT Working Group Plenary Meeting in 2023, coordinated by the Macau Financial Intelligence Office, the Working Group has developed a Strategic Plan, highlighting the goal of continuous

improvement of relevant legal and institutional framework. Moreover, the Working Group also agrees that fostering local and international partnerships is key to combatting money laundering.

What can we expect? In strengthening the AML legal framework, Macau will most likely take inspiration in what the other jurisdictions are doing.

For instance, reviews on Macau AML/CFT legislation could lead to a restriction of cash payments and move towards cashless and digital payments – which is a possibility in land-based casinos in several US states. In fact, digital payments could greatly aid casinos in the enforcement of their compliance programs. Digital payments in casinos can improve patron identification and verification of source of wealth – thus enabling a proper risk profiling of patrons, as well as allowing traceability of funds/ monitoring of transactions.

However, digital payments in land-based casinos could lead to some responsible gaming issues, as cash could be a better option to maintain control over gambling spend. Notwithstanding, as a solution, a limit could be implemented on the payment platform to ensure the patron remains within the established budget.

Another possibility to enhance the current AML/CFT rules in the gaming sector is to lower the casino transaction threshold. Currently, among other situations in which due diligence is required, the gaming sector is required to identify patrons, beneficiaries of gaming credits, representatives and agents whenever they engage in large-sum transactions – which is currently set at MOP$500,000 ($61,972). Lowering the threshold could mean a bigger compliance cost – however, it may be necessary to mitigate the vulnerabilities of the gaming sector.

On another note, the amendments to the current AML/CFT legal framework in the gaming sector could see a re-definition and expansion of the regulator’s obligations and powers, and even the creation of enforcement tools, to deter future breaches.

In conclusion, gaming operators should stay current on regulatory compliance measures. When Macau AML/CFT legislation gets reviewed, the gaming sector should seek to update respective compliance programs and procedures, and organise immediate training of staff.

FEATURES MACAU AML

38 GAMBLINGINSIDER.COM

Daniela Guerreiro Associate at MdME

NEW RULES

IndusLaw's Ranjana Adhikari, Ruhi Kanakia & Shashi Shekhar Misra discuss the Indian gambling market, and how the country is making further regulatory developments as it looks to become the industry's next big hit

India has recently witnessed a spate of new regulations and amendments, which will soon have a significant impact on how online gaming businesses operate and the regulatory compliances that they undertake. In this crisp round-up, we cover three important recent regulatory developments that every online gaming operator offering their products in India should be aware of. Each of these developments affect important aspects of an operator’s realmoney gaming business in India viz. taxation, data protection and verification of online realmoney games.

TAXING TIMES FOR ONLINE REALMONEY GAMING

In mid-July, India’s Goods and Service Tax Council (GST Council), a constitutional body responsible for making recommendations

on issues related to the implementation of the Goods and Services Tax (GST), recommended imposition of 28% GST on the face value of the bet/entry fee in online gaming. Though this was slightly modified subsequently to mean 28% on the initial deposit made by a player with the platform rather than each bet/entry, the recommendations are a body blow to the burgeoning online gaming industry in India. Not only have these recommendations, in effect, obliterated the distinction between games of skill and chance as far as taxation is concerned but arguably also fall foul of the constitutional prohibition against treating unequals equally.

The taxation regime for online gaming was under deliberation for more than two years. A Group of Ministers (GoM) was first constituted by the GST Council in May 2021 and then re-constituted in February 2022 to examine the taxation for casinos, horseracing and online gaming. The first report of the GoM, which was placed before the GST Council in June 2022, had recommended charging GST at a fixed rate of 28% on the entire face value of the stakes, irrespective of the nature of the online game (whether it be of chance or skill). However, the GST Council could not arrive at a decision at that time and had asked the GoM to deliberate further and submit an amended report. The GoM had submitted a revised report in December 2022 but, in the absence of a consensus within it on the issue of GST valuation, had left the final decision to the GST Council.

So, now, if a user intends to add INR 100 to her in-game e-wallet, INR 28 will be additionally charged as GST (under the head of ‘supply of actionable claims’). Reapplication of winnings earned from a past contest of online game will not be subject to the 28% GST. Separately, winnings from online gaming above INR 100 will be subject to a tax-deductionat-source (TDS) under income tax laws at the rate of 30%, which will be triggered on each withdrawal or the year-end balance in the e-wallet.

It is important to note that the GST Council has also recommended that

foreign real-money gaming operators will have to mandatorily register themselves through a simplified registration process to discharge their GST obligations under this new regime. Platforms of non-compliant foreign operators will be blocked.

To give effect to these recommendations, suitable amendments to the central and Statelevel GST laws are required. On 11 August 2023, both Houses of Parliament passed the relevant amendments to the central GST laws and the same received presidential assent soon after. The States are now expected to soon enact the necessary amendments for their GST laws. Additionally, key amendments relating to rate and valuation are also pending to be prescribed by way of amendments to the relevant rules and notifications. This new taxation regime is expected to come into force by 1 October 2023, and the GST Council has agreed to review its recommendations after six months of the new regime coming into force.

A NEW DAWN FOR PERSONAL DATA PROTECTION IN INDIA

On 11 August 2023, the Central Government published the much-awaited Digital Personal Data Protection Act, 2023 (DPDP Act) in the Official Gazette, thus setting the stage for the first-of-its-kind overarching personal data protection law for India. India has witnessed various iterations of a personal data protection law over the years, which have been introduced by the Central Government – the first of which was introduced in 2018 but was soon withdrawn. Subsequently, in 2019, another rendition titled the ‘Personal Data Protection Bill, 2019’ was presented before a Joint Parliamentary

REGULATING INDIA

Ranjana Adhikari

40 GAMBLINGINSIDER.COM

“India has witnessed various iterations of a personal data protection law over the years”

Committee, which tabled its report along with a revised rendition of the bill titled the ‘Data Protection Bill, 2021’ before the Indian Parliament in December 2021. The Data Protection Bill 2021 was thereafter brought up for consideration before the Indian Parliament but later withdrawn.

The DPDP Act is now the fourth and final iteration of the personal data protection legislation in India. It was first presented before the Lower House of the Indian Parliament, which passed it on 7 August 2023. The Upper House of the Indian Parliament subsequently passed the bill on 9 August 2023. On 11 August, pursuant to receiving Presidential assent, the DPDP Act was published by the Central Government in the Official Gazette.

Key aspects of the DPDP Act: The DPDP Act narrows its focus to the protection of ‘digital’ personal data, which is understood as any personal data in the digitised form about an “individual who is identifiable by or in relation to such data.” It seeks to regulate the processing of personal data in a manner that recognises the right of individuals to protect their personal data, and acknowledges the need to process personal data for lawful purposes. It prescribes various obligations on ‘data fiduciaries’ and ‘significant data fiduciaries’ while processing the personal data of ‘data principals’ (i.e. the user).

Applicability: The DPDP Act regulates the processing of personal data within India when collected in the digital form or in non-digital form and subsequently digitised. It also extends to the processing of personal data outside India if it relates to offering goods or services to data principals located in India. However, any data made ‘publicly available’ by the relevant data

principal remains outside the purview of the DPDP Act.

Obligations on data fiduciaries: Various obligations are stipulated for data fiduciaries while collecting, processing and sharing personal data, including, inter alia, stricter notice and consent requirements, obligations while processing personal data of children and persons with disabilities, obligations in instances of personal data breaches, obligations to update, correct and erase personal data and to provide data principals the option to withdraw consent, establishment of a grievance redressal mechanism, etc.

Legitimate uses: Data fiduciaries can process personal data without the prior consent of data principals for certain ‘legitimate uses,’ including when the data principal has voluntarily provided their personal data for a specified purpose and has not explicitly signified that they do not consent to such use.

Penalties: Monetary penalties of up to INR 250 crore ($30.3m) have been prescribed in cases of non-compliance with the provisions of the DPDP Act.

What’s next? Most importantly, the Central Government is yet to notify the date on which the provisions of the DPDP Act will come into force (different dates may be notified for different provisions). Hence, the provisions of the DPDP Act are currently not in force. Until such time as the DPDP Act comes into force, the Information Technology (Reasonable Security Practices and Procedures and Sensitive Personal Data or Information) Rules, 2011 framed under the Information Technology Act, 2000 will continue to apply.

INDUSTRY AWAITS DESIGNATION OF SELFREGULATORY BODIES FOR ONLINE GAMING

In April 2023, the Central Government had notified a new legal framework for online gaming through amendments to the Information Technology (Intermediary Guidelines and Digital Media Ethics Code) Rules 2021. These amendments (Online Gaming Rules) propose a light-touch, co-regulatory regime whereby government-recognised, but independent self-regulatory bodies (SRB) will verify whether an ‘online real money game’ is to be permitted or not – in accordance with the baseline criteria prescribed by the Online Gaming Rules. The Online Gaming Rules will regulate online gaming platforms by treating them as an “online gaming intermediary” and by prescribing due diligence obligations

for them. However, the obligations under the Online Gaming Rules will come into effect on the expiry of three months from the date on which the Central Government recognises a total of three SRBs.

However, at press time, no online gaming SRB has been designated by the Central Government. Initially, it tried to expedite the process of applications by potential SRBs, by stating that it would commence verifying online games itself if the industry did not set up the SRBs as required under the Online Gaming Rules. But even after four applications being filed, the Central Government is yet to approve the applications and designate them as online gaming SRBs. One of the reasons which could have impacted the designation process is a recent petition that was filed by an NGO in the Delhi High Court questioning the constitutional validity of the Online Gaming Rules. The petition is currently pending at the preliminary stage. As per news reports, the four SRB applications have been made by (i) The Esports Players Welfare Association (EPWA), (ii) a consortium supported by two gaming industry associations — the E-Gaming Federation (EGF) and the Federation of Indian Fantasy Sports (FIFS); (iii) the All-India Gaming Federation (AIGF) and (iv) the All-India Gaming Regulator (AIGR) Foundation.

42 GAMBLINGINSIDER.COM FEATURES REGULATING INDIA

Shashi Shekhar Misra

Ruhi Kanakia

CROSSOVER FUSIONS

Gambling Insider speaks with Ivan Kravchuk, Evoplay CEO, about the pioneering of crossover fusions and what goes into the making of an online casino product

At iGB Live in Amsterdam, we discussed Evoplay pioneering crossover fusions with the likes of casino and sports betting. Are there any other fusion crossovers you’re looking into developing?

Our aim has always been to create immersive, cross-platform experiences that captivate a wide spectrum of players. From online casino enthusiasts to sports bettors and from casual gamers to adrenaline-chasing thrill-seekers; our games cater to all tastes and preferences.

We continuously strive to push boundaries, blending genres and defying traditional categories in our relentless pursuit of the next breakthrough in gaming. We’re deeply intrigued by the potential of integrating our games with sports betting. Our third focus is metamechanics. We’re experimenting with various mechanics and activities, such as tournaments and quests.

How do you go about making games as quick as possible for those users in LatAm that don’t have fast internet service and use old devices?

In regions like LatAm, we’re aware that players

may not always have access to the fastest internet services or the latest devices. We’ve also observed that instant games, which are quick and efficient, are significantly more popular than traditional slots here. This understanding shapes our approach to game development and optimisation.

Our goal is to ensure our games can run smoothly on a broad range of devices and internet connections. To facilitate this, we utilise our proprietary Spinential game engine, which

enhances the performance of our games by up to 10 times. This technology enables our games to load faster and perform better, even on slower internet connections or older devices.

What goes into the process of naming a product?

The process is somewhat complex and multilayered. There are substantial legal aspects to consider right from the outset, as we register

44 GAMBLINGINSIDER.COM FEATURES PRODUCT DEVELOPMENT

"Our main focus is to avoid any clashes with existing game mechanics. Beyond that, we believe this feature could significantly enrich our players’ experience across different games, making their gaming journey even more exciting and rewarding"

trademarks for each game to protect our intellectual property. This is a crucial step, although it can sometimes present challenges.

Once we’ve navigated the legal landscape, we shift our focus towards creating a name that aligns with our player’s expectations and the game’s unique attributes. The aim is to encapsulate the essence of the game within its name – think of it as crafting an accurate and enticing summary. This is where our dedicated creative team comes into play. They devote considerable effort to brainstorming and selecting names that are not only descriptive and appropriate but also memorable.

Could you elaborate on the research and development process that’s involved in the creation of innovative features like the random prize drop?