We publish some of the most influential magazines and websites in Africa & the Middle East regions. Please visit the websites below for more information about our publications.

Milling Middle East & Africa is published 6 times a year by FW Africa. Reproduction of the whole or any part of the contents without written permission from the editor is prohibited. All information is published in good faith. While care is taken to prevent inaccuracies, the publishers accept no liability for any errors or omissions or for the consequences of any action taken on the basis of information published.

www.foodbusinessmea.com

www.millingmea.com

www.horecamea.com

www.dairybusinessmea.com

FEE BUSINESS

www.feedbusinessmea.com

www.healthcaremea.com

www.sustainabilitymea.com

www.hpcmagmea.com

Perfecting Your Flour Quality Through Innovation and Expertise

With over 50 years of experience, Pakmaya stands by your side from diagnosis to solution. We offer practical and expert approaches tailored to your needs.

The Focus of Our Business

Flour Improvers Flour Fortification (vitamin and mineral premixes) Flour Standardization Applications

Flour Analysis

Building Grain Resilience through Local Processing: Is the Industry Ready?

The grain industry continues to navigate a landscape defined by volatility, ranging from unpredictable weather patterns and geopolitical disruptions to shifting consumer demands and rising input costs. In such an environment, resilience is no longer optional; it is a strategic imperative for stakeholders across the value chain.

One of the clearest pathways to building this resilience lies in localizing grain processing. Across Africa and other emerging regions, there is a growing realization that strengthening domestic milling capacity is not just about food security, it’s about economic empowerment. Processing locally available grains, such as maize, sorghum, millet, and soybeans, helps reduce post-harvest losses, shortens supply chains, and enhances the relevance of products to local markets. It also creates jobs, supports rural economies, and lays the groundwork for more stable food systems.

Yet, local processing cannot succeed in isolation. The role of milling equipment suppliers is critical. As demand shifts toward smaller and mid-scale milling operations, technology providers must develop solutions that are cost-effective, adaptable, and designed for local conditions. Whether it is roller mills optimized for non-wheat grains or grain handling systems suitable for decentralized networks, suppliers who understand these needs will be best placed to support market growth.

In this 14th issue of Milling Middle East & Africa Magazine, these themes come to the fore. We feature Grainpulse Limited, whose integrated grain, feed, and milling operations in Uganda exemplify the kind of innovation required to thrive under current conditions. The company has leveraged local sourcing, a move that demonstrates Africa's potential for selfsufficiency in local manufacturing. However, getting insights from Nouran Ezzeldin of Granos Oros, who, while applauding efforts in countries that have achieved self-sufficiency in staple grains, is realistic about limitations, “Even if wheat production increases, Egypt’s consumption levels are too high

for us to depend on the domestic supply fully.”

Bringing the Grain Ecosystem Under One Roof

As the industry evolves, it is essential to create spaces for conversation, collaboration, and commercial engagement. Events like the AFMASS Food Manufacturing Expo are one such opportunity. It converges the full spectrum of grain-economy stakeholders, creating platforms where millers, equipment suppliers, ingredient manufacturers, feed producers, regulators, and financiers share innovations, benchmark technologies, and forge partnerships. Slated for July 2–4, 2025, at the Sarit Expo Centre in Nairobi, Kenya, the expo seeks to bring these actors together, transforming isolated supply-side capabilities into collaborative systems. Now in its 10th edition in the Eastern African region, the expo remains a key meeting point for the food, milling, baking, and grain storage sectors worldwide. Notably, the Africa Milling Expo section of the event will showcase the latest milling technologies, grain handling systems, storage solutions, and quality control innovations. It will provide a platform for equipment suppliers to connect directly with millers and processors, as well as for industry professionals to gain insights into best practices and emerging trends.

We encourage all industry players to participate in this important gathering and continue investing in systems that drive sustainable growth in the grains, milling, and baking sectors.

Finally, this issue provides a comprehensive roundup of the latest developments in the baking, milling, grains, and cereals sectors, featuring expert insights and the latest news updates.

Enjoy your read!

Martha Kuria, Senior Editor, FW Africa Publications.

Global grain output set to hit record over 2B tonnes in 2025/26 – IGC

GLOBAL - The International Grains Council (IGC) has projected global grain production to reach a record 2.375 billion tonnes in the 2025/26 season, a 3% increase from the previous year. This rise is largely driven by strong maize harvests in the European Union, Argentina, and the United States, along with solid wheat and soybean outputs across key regions.

The forecast, shared at the IGC’s 62nd Council Session in London, reflects continued momentum in the grains sector. Total use is expected to grow by 2% year-on-year to 2.372 billion tonnes. Global grain stocks are forecast to rise slightly to 585 million tonnes, marking the first increase in four

TRAINING

years, supported by improved inventories in major exporting countries. Trade volumes are also set to increase. The Council projects grain trade will reach 428 million tonnes, fuelled by higher wheat shipments and steady maize exports. Rice and soybean trade are expected to remain firm, with global rice trade forecast at 59 million tonnes. Chaired by Mr. Hamed Oussama Salhi of the Algerian Embassy in London, the Council used the June 12 session to address key trade policy concerns, especially the growing impact of non-tariff barriers.

Members called for enhanced cooperation on sanitary and phytosanitary (SPS) measures and reiterated support for a rules-based trading system. The IGC also renewed the Grains Trade Convention for two more years, supporting ongoing data-sharing and analysis. Strategic outreach under the Algerian chairmanship included launching an Arabic edition of the Grains Market Report and expanding dialogue with prospective new members.

A partnership with the India Middle East Agri Alliance was also unveiled to improve trade transparency between South Asia and the Middle East. The IGC will release a five-year supply and demand outlook in January 2026, covering grains, oilseeds, rice, and pulses.

IAOM MEA launches fully funded milling technology scholarship in Morocco

MOROCCO - The International Association of Operative Millers- Middle East and Africa (IAOM MEA), in partnership with the National Flour Milling Federation (FNM) and Essa Al Ghurair Investment (EGI), has unveiled a fully funded scholarship program aimed at equipping aspiring milling professionals with advanced technical training. Slated to begin on January 12, 2026, the six-month intensive course in Advanced Milling Technology will be hosted at the Centre for Study and Research in the Cereal Industry (CERIC) in Casablanca, Morocco. Applications are open until August 16, 2025. The initiative is designed to strengthen technical capacity across the grain milling sector in the MEA region, providing a new generation of millers with essential skills in a rapidly evolving industry.

According to IAOM MEA, the program will cover full tuition, daily lunch, practice materials, local insurance, industrial visits, and recreational activities throughout the course. Founded in 1896, IAOM is a global professional body serving grain milling professionals. The MEA region is one of its most active chapters, with a strong focus on technical training, knowledge exchange, and regional cooperation. “This scholarship represents a powerful collaboration between key players in the milling

industry to build human capital in regions where technical skills are urgently needed,” IAOM MEA said. Essa Al Ghurair Investment, a leading agribusiness firm with significant operations in flour milling and trading, brings strategic insight to the partnership. FNM, an advocate for technical standards and workforce development, also plays a central role. The CERIC curriculum will combine theory, technical modules, and field exposure, producing graduates aligned with international milling standards. The program is open to candidates across the Middle East and Africa, especially young professionals seeking to enter or advance in grain milling.

Zimbabwe’s corn output to hit 1.3M tonnes in 2025/26

ZIMBABWE - Zimbabwe’s corn production is forecast to more than double in the 2025–26 marketing year, reaching an estimated 1.3 million tonnes, according to the latest report from the Foreign Agricultural Service (FAS) of the U.S. Department of Agriculture (USDA).The rebound follows a prolonged drought that slashed the previous season’s harvest to 635,000 tonnes. FAS attributes the recovery to a stronger La Niña pattern, which brought improved rainfall in the latter half of the growing season. The favourable weather supported crop development and boosted yields, offering relief to a sector strained by climate volatility and input shortages.

Despite the gains, Zimbabwe is projected to remain a net importer of corn, with imports expected at 1 million tonnes in 2025/26, a 300,000-tonne drop from the previous season. Yet, the USDA notes that this figure is still historically high due to strong domestic demand, forecast to rise by 8% year-on-year to 2.2 million tonnes. Most imports are expected from South Africa, which will have around 1.5 million tonnes available for export.

Access to sufficient grain remains a concern. Communal farmers, who cultivate about 60% of the country’s corn acreage, contribute less than 40% of total output due to persistently low yields. Most lack irrigation access, making over 90% of corn production dependent on rainfall. “Farmers have limited access to irrigation technologies; subsequently, more than 90% of corn production is reliant on rainfall,” FAS said. “The ability of farmers to optimize production is further hindered by macro-economic challenges and relatively high input costs.” To support producers, the government has kept maize import tariffs at zero and continues to purchase grain through the Grain Marketing Board, targeting strategic reserves of 500,000 tonnes.

Uganda plans to revive Uganda Grain Milling Company (UGMC)

UGANDA - The Grain Council of Uganda (TGCU) has welcomed the government’s decision to revive the Uganda Grain Milling Company (UGMC), calling it a timely intervention that will enhance the export of Ugandan grains and pulses. Mr. Robert Mwanje, chairman of TGCU, stated that the revival of the company as a regulatory body will help the government understand the challenges faced by stakeholders in the grain sector and reduce the export of unprocessed grain.

“We must discourage the export of raw grain, as it results in lost jobs. With the government’s involvement, they will help ensure quality control, guaranteeing that only aflatoxin-free grain is milled and exported,” he added. Mr. Mwanje made these remarks following the first-ever Grain Millers’ Summit, held last week at the Uganda Manufacturers Association grounds in Lugogo, Kampala.

At the summit, State Minister for Finance in charge of Investment, Evelyn Anite, confirmed that the government would revive UGMC under a new name—the National Commodity Company. She said the initiative is part of broader efforts to organize farmers, improve post-harvest handling, and ensure proper warehousing and grain quality management. “We export grain worth US$1.1 billion to neighboring countries. This is food that eventually reaches people’s tables. We must ensure the grain is clean and properly handled,” said Ms. Anite, noting that warehousing funds have been earmarked under the Parish Development Model.

UGMC was once showcased as a model for value-added processing, producing bread, animal feed, and flour, and storing grain in silos for food security. It declined during the 1990s privatization era and was eventually sold to the defunct Greenland Bank. Maj. Gen. David Kasura, permanent secretary in the Ministry of Agriculture, called the revival a wise decision to address issues in aggregation, quality assurance, and packaging for better market access.

Bühler to host food extrusion workshop in Nairobi, Kenya

KENYA - Bühler, the Swiss-based global leader in food technology and process solutions, will host its flagship Food Extrusion Workshop from July 15 to 18, 2025, at the African Milling School and Bühler’s customer site in Nairobi, Kenya.

The four-day course will offer a comprehensive overview of extrusion technology, a key process in modern food and feed production. Designed for operations supervisors, engineers, and R&D professionals, the training blends theoretical instruction with practical, hands-on sessions using Bühler’s twin-screw extruder. Delivered in English, the workshop will deepen participants’ knowledge of extrusion principles, covering screw elements, energy inputs, and screw configuration for various product types. Advanced modules include steam addition, vacuum degassing, co-extrusion, remote-cut technology, colouring, coating, drying, and toasting.

Technical demonstrations will feature products such as ready-to-eat cereals, snacks, texturised plant proteins, modified flours, and extruded breadcrumbs. Participants will also explore analytical methods for raw material assessment and the transformation of starch and protein during extrusion. Theoretical sessions will cover fortified rice and wet texturised plant proteins, reflecting growing interest in sustainable, plantbased foods.

Attendance costs US$900 (excl. VAT), with an early bird rate of US$850 for registrations by June 10, 2025. The fee includes course materials, daily lunches, a networking dinner, and transport between the hotel and training site. Accommodation, airport transfers, and travel costs are separate. Participants must bring safety shoes and glasses. The workshop underscores Bühler’s broader commitment to innovation and industry development.

In March 2025, Bühler also hosted an aquaculture technical roundtable, highlighting species-specific feed design, processing impacts on feed quality, and the use of local byproducts to reduce costs—reinforcing its leadership in feed technology and capacity building.

INVESTMENTS

Imas completes construction of feed mill for Nurym Group

TURKEY - Imas has successfully completed a 20-ton-per-hour (tph) feed mill for Nurym Group in Shymkent, Kazakhstan, which commenced operations in April. This facility is one of the largest feed mills in the country, producing 480 tonnes of feed daily for cattle, poultry, and small ruminants.

Founded in 1989 in Anatolia, Turkey, Imas is a subsidiary of Ittifak Holding. It operates under the Milleral brand, supplying grain milling machinery and turnkey plants globally. With over 500 references in more than 100 countries, Milleral continues to deliver high-performance solutions in flour and semolina milling.

For this project, Imas provided comprehensive turnkey services, including plant design, process engineering, manufacturing, installation, commissioning, and user training. The steel building was fully designed, manufactured, and erected by Imas as part of the project. Training covered both machinery and plant operations, as well as the use of feed laboratory equipment.

The plant process starts with an intake system connected to steel storage silos. Raw materials are ground, mixed, conditioned, pelleted, treated with molasses, cooled, optionally crumbled, then passed through a vibratory sieve. Finished products are packed into 25 kg sacks. A high-capacity Viteral series pellet press (VPP) was installed, with processing capability of up to 30 tph. It can include a touchscreen panel for managing critical parameters like time and temperature.

Additional equipment includes a Viteral paddle mixer (VMX) and a Viteral hammer mill (VHM). The VHM reaches up to 50 tph thanks to specialized pre-crushing blades and a fixed hammer system.The feed mill is managed through a central automation system that monitors the entire process from intake to packaging, offering real-time data on production, yield, and consumption. Imas’s after-sales team can provide remote technical support through this system.

MERGER

Cimbria launches SEA.XL optical sorter to boost purity in nut industry

ITALY - Cimbria, one of the world’s leading manufacturers in grain processing, handling, and storage, has unveiled SEA. XL, an AI-powered optical sorting machine tailored for the nut processing industry. The innovation promises enhanced purity, productivity, and profitability. Equipped with dualvision hyperspectral technology and intelligent material detection, the SEA.XL raises the bar in sorting accuracy and resource efficiency for nuts such as pistachios and hazelnuts.

With SEA.XL, Cimbria is redefining quality control and contamination removal. At the core of its performance is the AI-driven BRAIN intelligence and a dual-vision system that combines high-definition RGB full-colour cameras with hyperspectral infrared imaging. This enables the SEA.XL to detect and remove contaminants, including shells, stones, glass, plastics, and metals, based on shape, colour, and chemical composition.

Among its key advantages is adaptability. A single SEA. XL unit can process multiple nut types and input variations without hardware changes. This is enabled by an extensive foreign material detection library and multi-frequency infrared scanning. This versatility reduces downtime and boosts uptime, supporting processors to scale and diversify efficiently. SEA. XL is designed for integration into existing facilities, offering 2 to 6 chute configurations for high-volume throughput with minimal operator input.

Models SEA.XL 2, 4, and 6 can be tailored to fit different production needs. Compact and durable, the system suits modern processing demands. Features like vibrating plates with optional aspiration, auto-cleaning systems, and a 21.5-inch touchscreen interface offer full process control. A multilingual interface and detailed reporting simplify operations and reduce training needs. SEA.XL also supports sustainable practices by maximising yield and minimising waste. It meets CE, UL, and CSA standards, ensuring compliance with global food safety and quality requirements.

Cargill partners Biotech Farms to strengthen animal feed production in the Philippines

PHILIPPINES - Cargill has partnered with Biotech Farms Inc. to establish a dedicated animal feed production line at the Biotech Agro-Industrial Complex in Tantangan, South Cotabato, reinforcing its presence in one of the Philippines’ key agricultural regions. The strategic collaboration aims to improve feed supply chain efficiency and service delivery to livestock producers across Mindanao, an area with a fastgrowing base of animal farmers and agribusinesses in need of reliable feed solutions.

“This is about serving our Mindanao customers better, with the reliability, responsiveness, and quality they deserve,” said Sonny Catacutan, senior managing director for Cargill Animal Nutrition & Health Philippines. “The Tantangan Plant gives us a stronger presence in a region essential to the future of the local agricultural industry. It allows us to enhance service to our customers and live our purpose of nourishing the world starting with every bag of feed,” he added.

Selected through a rigorous process aligned with Cargill’s global standards, the Tantangan feed mill is equipped with modern milling technologies, a dedicated monthly output, and a high-performance system designed to meet growing demand. With production now operational, the facility enhances Cargill’s ability to deliver customized, safe, and sustainable nutrition solutions at scale.

“This partnership is a testament to our shared mission of empowering Mindanao’s farmers with innovative, sustainable solutions,” said Rey Chiang, CEO of Biotech Farms. Since 2001, Biotech has been advancing Philippine agriculture through precision farming, renewable energy, and circular economy practices. The company specializes in swine and poultry production, feed manufacturing, and rice milling, producing over 500 tonnes of feed daily.

The partnership supports both companies’ long-term goals to improve livestock productivity while promoting environmental stewardship and strengthening community resilience.

MERGER

Construction set for Sanku’s nutrient premix factory in Ethiopia

ETHIOPIA - Sanku, a social enterprise working to combat hidden hunger through food fortification, has officially marked a key milestone in Ethiopia with the official land handover for its upcoming nutrient premix factory. The facility, to be built in the Kilinto Special Economic Zone, will significantly enhance local capacity to combat hidden hunger. Having launched operations in Ethiopia in September 2024, Sanku has already reached over six million people with access to fortified flour.

The new factory aims to scale that reach to 40 million Ethiopians. Once operational, the facility will produce 3,000 tonnes of nutrient premix annually, enough to serve up to 200 million people across the continent. The event, held on June 17, brought together high-level attendees including Sanku Co-

EXPANSION

founder and Board Chair Dave Dodson, Co-founder and CEO Felix Brooks-church, and members of the Sanku Ethiopia team.

Also present were government officials and partners from the Industrial Parks Development Corporation Ethiopia (IPDC), culminating in the signing of a landmark agreement between Sanku Fortification Ethiopia PLC and IPDC. Kamil Ibrahim, IPDC’s Chief Operating Officer, underscored the project’s alignment with Ethiopia’s health and productivity goals. “The Corporation is committed to supporting this initiative, which contributes to building a healthier and more productive society,” he said.

“This facility is more than infrastructure, it’s a strategic investment in food systems, local economies, and the health of future generations,” said Felix Brooks-church. The Ethiopia project builds on Sanku’s growing regional footprint. The organization recently partnered with the Fortified Whole Grain Alliance (FWGA) to strengthen access to fortified foods across Eastern Africa.

The collaboration has already facilitated key distribution connections in Rwanda, enabling fortified flour access for over 300,000 people. “By working with FWGA and local partners, we’re laying the foundation for nutrition solutions that benefit communities long-term.

Bunge-Viterra merger secures final regulatory nod from

USA - The US$18 billion merger between Bunge Global SA and Viterra Ltd. is now set to close “on or around July 2,” following final regulatory approval from China’s State Administration for Market Regulation. The approval clears the last hurdle in one of the agribusiness sector’s most consequential mergers, originally announced in June 2023.

With China’s green light, Bunge has secured all required regulatory consents, including conditional approvals from Canada and the European Union. Under the deal, Bunge will assume Viterra’s US$9.8 billion in debt. Shareholders of the Glencore-owned trader will receive approximately 65.6 million shares of Bunge stock valued at US$6.2 billion, plus US$2 billion in cash. “This approval underscores the strategic rationale behind bringing Bunge and Viterra together to create a premier global agribusiness company,” said Greg Heckman, CEO of Bunge.

He added that as one team, the merger will accelerate their shared vision for growth and help connect farmers to consumers to deliver essential food, feed, and fuel. The merger brings together two leading crop trading and processing firms, positioning the new entity to compete with industry giants such as Archer Daniels Midland (ADM) and Cargill. The combined company will significantly expand its grain handling

China

and oilseed processing capabilities to better serve a global food chain challenged by climate change, geopolitical risk, and shifting trade flows.

Rotterdam-based Viterra, majority-owned by Glencore PLC since 2012, confirmed that “all regulatory closing conditions have been satisfied.”Delays in securing approvals had pushed back the original timeline. In February, Heckman said Bunge was preparing for closure, including required asset divestments in Europe and talks with Chinese regulators.“Teams of both companies have put in countless hours of planning to ensure smooth integration,” he said.

Limited GrainPulse

Driving Uganda’s Agribusiness

Transformation through Full-Circle Solutions

BY MARTHA KURIA

Uganda’s agricultural sector remains the cornerstone of its economy, employing more than 70% of the population and contributing 24% to the national GDP. However, like much of sub-Saharan Africa, the sector has long grappled with systemic challenges such as low productivity, inadequate value addition, and disjointed supply chains. Grainpulse Limited, an agribusiness company, emerged in this context, evolving from a humble grain supplier into one of Uganda’s most prominent integrated agribusinesses. Today, the company operates across a wide value chain that includes fertilizer blending, grain milling, animal feed production, and coffee processing. In an exclusive interview with Milling Middle East and Africa Magazine, Oudtshoorn, CEO of Grainpulse Limited, discusses the company’s impact, rooted in innovation, sustainability, and farmer empowerment.

MEET THE CEO

Though relatively new to the helm, just three months into his role at the time of this interview, Oudtshoorn brings a grounded, practical outlook. His leadership blends strategic ambition with a clear-eyed understanding of Uganda’s challenges and opportunities. Originally from finance background, Oudtshoorn is clear that Grainpulse is not just in the business of selling agricultural inputs. Backed by a dedicated team, including Business Development Manager Abaho Karuhanga, the new leadership is focused on strengthening partnerships and driving farmercentric growth “We are not traders. We buy directly from the farmer and close the loop by

processing and reselling in a form that adds value back to the community.” This farmer-first philosophy defines Grainpulse’s operations. “We aim to offer full-circle agricultural solutions, from selling the farmer quality fertilizer, to buying their maize, milling it, and then selling back our own flour brand,” he explains.

FROM SAVANNAH COMMODITIES TO GRAINPULSE: PIONEERING FERTILIZER BLENDING IN UGANDA

Grainpulse Limited was founded out of passion to provide solutions that will positively transform the lives of farmers in Uganda. It initially started as Savannah Commodities, primarily involved in the sourcing and processing of both coffee and grain in 2000. A pivotal moment came in 2018 when Savannah then decided to make a significant investment in Uganda’s first & only fertilizer blending facility with an annual capacity of 300 kMT together with K+S, the world’s third largest potash producer based in Kassel, Germany. Together, Savannah and K+S merged with Grainpulse Limited. Today, Grainpulse is Uganda’s leading integrated agri-business with capabilities across soil testing and agronomic advisory, crop-specific and custom fertilizer blending, farmer training and extension services and crop off-take services through which we buy back grains like maize, barley, sorghum, beans and coffee. The company was founded with a vision of being the leading provider of food & nutrition security for every household in Africa; and the mission of formalizing and commercializing local agriculture by providing superior agronomic solutions, and value chain

expansion. Today, we have become a significant player in the agriculture sector by offering end-to-end solutions to both smallholder and commercial farmers locally.

By importing raw materials and customizing blends for specific crops and regions, Grainpulse offers Ugandan farmers scientifically formulated products that match their soil and crop needs.

“One of our biggest milestones is that we’ve created a market for blended fertilizer in Uganda,” Oudtshoorn says. “Before us, it was all straight fertilizer. Now we’re offering cropspecific formulations tailored to local soils and growing conditions.”

Their blends include formulas for maize, beans, soybeans, coffee, tomatoes, bananas, sorghum, millet, Irish potatoes, cassava, and sunflowers. Each product is available in 10kg, 25kg, and 50kg bags, making it accessible to farmers at different scales. This approach helps farmers maximize yields and reduce input wastage.

Despite the milestone, Oudtshoorn notes that the facility’s current utilization hovers around 20%, leaving a vast potential for maximum utilisation. “There’s huge potential,” says Karuhanga. “But first, we have to overcome cultural resistance and misinformation. Many Ugandan farmers still believe fertilizer degrades soil.” Grainpulse tackles these misconceptions head-on through

an extensive network of demonstration plots and farmer training sessions. The company also offers free soil testing and agronomic support and collaborates with the Ministry of Agriculture and international partners under programs such as the Agricultural Cluster Development Project (ACDP).

The company’s demonstration plots, often a quarter of an acre in size, are used to show farmers the difference in yield and crop health between traditional and modern practices. These plots are complemented by three-season training programs, covering pre-planting, in-season, and post-harvest best practices. “We run on-site demos that show, for example, tomatoes grown with fertilizer versus those without,” Karuhanga explains. Seeing is believing. That’s how we’re driving adoption.” The result has been a steady increase in fertilizer adoption, with Grainpulse now commanding approximately 30% of the local fertilizer market.

GRAINPULSE LIMITED TAPS INTO LOCAL MAIZE MILLING TO STRENGTHEN FOOD SECURITY IN UGANDA

Grainpulse Limited has strategically expanded into maize milling as part of its circular agricultural model that supports smallholder farmers, enhances food safety, and increases local food availability. While best known for its fertilizer blending operations, the company’s maize flour brand “JJimu,” is steadily gaining traction among consumers in Uganda’s local markets.

The company’s maize milling plant, located in the Mukono district, processes up to 1,000 tonnes monthly. While this capacity positions it as a smaller player compared to larger millers in Uganda, the company's focus is deliberate, targeting local distribution through its own 28 rural hubs and direct-to-institution sales such as schools and hospitals. “We are not targeting retail chains,” explained CEO Oudtshoorn. “Instead, we are more focused on providing local communities with aflatoxin-free flour, which aligns with our mission to improve food safety and nutrition.”

Recent investments in automation have helped streamline Grainpulse’s milling plant, reducing both labor costs and energy consumption. Grainpulse offers both fortified and unfortified maize flour, responding to rising consumer demand for nutritious, value-added products. “We want to give the consumer a choice,” said the CEO, emphasizing that quality and affordability must go hand-in-hand.However, the company

Grainpulse Fertiliser Brands

Oudtshoorn CEO GrainPulse Limited

is not currently planning to venture into wheat milling, citing Uganda’s limited wheat production and the logistical complications of wheat importation.

ROOTED IN QUALITY AND SAFETY

Quality assurance is central to Grainpulse’s milling operations. The company uses an inhouse laboratory in Mukono to test every batch of Maize and other grains delivered, as well as our finished flour and animal feed products delivered to farmers, with strict rejection policies in place for aflatoxin-contaminated grains. This proactive approach is especially relevant given the lax regulation of aflatoxins in Uganda’s informal milling sector, and growing concerns about food safety in East Africa.

Grainpulse sources maize entirely from Ugandan farmers, often working through intermediaries or cooperatives. Some of the maize is supplied in cob form, a practice that allows better control of quality during processing. Although the company currently mills only maize, it provides storage services for grains like soybeans used internally for animal feed production.

OVERCOMING TRADE BARRIERS IN EAST AFRICA

Despite having a superior maize flour product, acknowledged by international buyers like the World Food Programme, the company has faced barriers in exporting to neighboring Kenya, where demand for maize flour is high. “It’s not the quality that’s the issue,” Oudtshoorn said. “It’s trade policies and transport costs that make cross-border business challenging.”

GRAINPULSE SCALES UP ANIMAL FEED PRODUCTION WITH PREMIUM, LOCALLY SOURCED INGREDIENTS

Grainpulse Limited has steadily emerged as a key player in Uganda’s commercial animal feed sector, leveraging its in-house grain supply chain and quality control infrastructure to deliver premium feed products under the “halisi” brand.

Launched in 2021, Grainpulse’s animal feed division currently produces approximately 2,500 tonnes of feed per month, focusing primarily on poultry (broilers and layers), pigs, and dairy cattle. “It’s still a young segment of our business, but it’s growing rapidly,” said Karuhanga. “We saw a gap in the market for consistent, high-quality, aflatoxin-free feed.” Halisi, the flagship brand,

GRAINPULSE'S ANNUAL FEED OUTPUT IN NUMBERS

30,000T

was developed with a regional outlook. “We wanted a name that resonated across the East African Community,” Karuhanga explained, noting that Uganda, Kenya, and Tanzania share linguistic and agricultural commonalities. Although most of Grainpulse’s animal feed is sold locally through its network of hubs and agents, there are ongoing plans to scale up exports, particularly to Kenya where demand for Ugandan poultry and livestock products continues to rise.

LOCAL STRENGTH, GLOBAL STANDARDS AMID REGULATORY AND TRADE HURDLES

The feed plant is fully integrated with the company’s maize milling and grain aggregation systems, allowing optimal utilization of by-products such as bran and germ. Soybeans, another key ingredient, are also locally sourced and processed in-house. Near-infrared spectroscopy and wet chemistry techniques are used at their laboratory to assess nutritional content and aflatoxin levels in both raw inputs and finished feed products.

However, barriers such as non-tariff trade restrictions and high transportation costs have slowed regional expansion. “We’ve benchmarked our product quality against the best in Kenya,” Karuhanga added. “We believe halisi can compete, but policy needs to catch up with market potential.” Grainpulse is positioning itself as a reliable local alternative to imported feeds from Europe and Asia. By investing in consistent quality,

traceability, and farmer training, the company is addressing key challenges in Africa’s historically informal animal feed sector.

The feed business also complements Grainpulse’s wider goal of agricultural sustainability. “We’re not just selling feed,” noted Oudtshoorn. “We’re promoting healthier livestock, better yields for farmers, and ultimately improved food and nutrition security.” Efforts are also underway to make operations more environmentally sustainable. Biomass from maize cobs is already being used to fuel dryers for coffee and feed production, and further green energy investments are being considered.

COFFEE PROCESSING AND EXPORT: ADDING VALUE TO UGANDA’S SIGNATURE CROP

Coffee is Uganda’s most important agricultural export, and Grainpulse has positioned itself as a key player in this sector. At its Kampala-based Bugolobi facility, the company processes coffee beans for export to Europe and other international markets. A growing emphasis on organic certification and sustainable practices has allowed Grainpulse to tap into premium markets and support farmers in transitioning to higher-value, environmentally friendly production systems. “Organic is the buzzword in Europe,” Oudtshoorn said. “Whatever that means, we are adapting by supplying organic fertilizers and supporting coffee farmers to meet those standards.”

A CIRCULAR AGRIBUSINESS MODEL

Grainpulse’s model is unique in Uganda because it integrates every part of the agricultural value chain. The company supplies farmers with inputs, trains them on best practices, purchases their harvests, processes the commodities, and sells the final products.

This closed-loop system creates a dependable market for farmers and ensures product quality throughout the chain. It also allows for value addition at multiple stages, contributing to rural employment and economic development. Social inclusion is another key area. Grainpulse supports youth and women through its agent network, promotes local entrepreneurship by partnering with agro-dealers, and provides employment to over 110 staff, alongside 50+ casual laborers. The integrated nature of the business ensures job creation across multiple sectors.

In terms of community engagement, the company supplies affordable maize flour to schools and hospitals and continues to roll out CSR initiatives such as farmer field schools and access to soil testing. “It’s not about charity,” Oudtshoorn said. “It’s about enabling people to build their own sustainable futures.”

Grainpulse is also engaged with NGOs and development agencies, having previously partnered with Uganda’s Ministry of Agriculture and IFAD under the Agricultural Cluster Development Project. These collaborations helped expand reach into 57 districts and included support for household food security and diversified cropping. MMEA

Grainpulse Employees at Work

MODERN

FPrecision

Grinding

for a Growing World Roller Milling SYSTEMS

BY MARTHA KURIA

or thousands of years, humans relied on stone mills to process grains. Although effective, these traditional methods had significant limitations. Milling was rudimentary, often involving the pounding or grinding of grain kernels between stones to produce coarse flour. The process was labourintensive, inefficient, and generated substantial heat through friction, potentially degrading the flour’s nutritional quality and resulting in inconsistent particle sizes.

The demand for more efficient and precise flour production led to the development of roller milling, marking a pivotal shift in the history of food processing, offering millers enhanced control over the grinding process and significantly improving the quality, consistency, and efficiency of flour production.

EVOLUTION OF GRAIN ROLLER MILLS

The rise of roller milling began in the late 1860s, drawing its foundation from the Hungarian milling system. Between 1870 and 1872, Wisconsin inventor John Stevens pioneered a transformative design featuring parallel steel rollers operating at differential speeds. This innovation significantly increased milling efficiency, enabling production to rise from

MODERN ROLLER MILLS ARE DESIGNED FOR PRECISION, WITH EACH COMPONENT ENGINEERED FOR FUNCTION AND EFFICIENCY

approximately 200 to 500 barrels per day without the need for additional power.

The adoption of steam power further accelerated the spread of roller mills, supporting the rapid transition to automated systems. This evolution was showcased at Britain’s first International Exhibition of Flour Milling Machinery in 1881, a response to growing demand for refined white flour and increased imports of hard wheat from North America. In Africa, large scale milling remained at infant until 1988, when ‘what is termed as the first small-scale commercial roller mill in the world’, known as the MM500, was established in South Africa by Maize Master. Designed by Andries Greyling (Snr), the mill was a significant development for the African continent, offering an affordable and profitable option for entrepreneurs to add value to their products.

By the early 20th century, electrified, continuous roller mills reached throughputs measured in thousands of tons per day. Today, roller mills operate through a series of break, sizing, and reduction passages. A recent study by HTF Market Intelligence reported that the global flour milling machines market is projected to surge from US$0.9 billion in 2025 to US$1.6 billion by 2032, growing at a robust compound annual growth rate (CAGR) of 8%. This growth reflects the adoption of modern milling systems, with roller mills taking the lead.

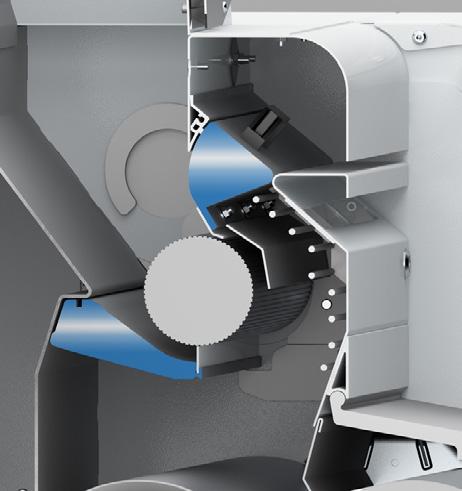

ENGINEERING THE PERFECT MILL

Modern roller mills are designed for precision, with each component engineered for function and efficiency. Feed rolls regulate the flow of grain into the break rolls, which are fluted to grip and shear the kernel. Subsequent smooth rollers continue reducing the endosperm into flour while sifters and purifiers sort the output by particle size. Modern roller mills often incorporate variable speed drives that allow operators to adjust speeds during operation based on grain conditions and desired output characteristics. This flexibility enables millers to respond quickly to changes in grain moisture content, hardness, or other factors that affect the grinding process.

One of the most notable innovations in recent years is the implementation of automated roll gap adjustment. This technology allows millers to calibrate their machines remotely, maintaining optimal grinding conditions even when switching wheat varieties or blends. Paired with flow-rate sensors and force measurement, this enables consistent flour quality

across shifts and locations.

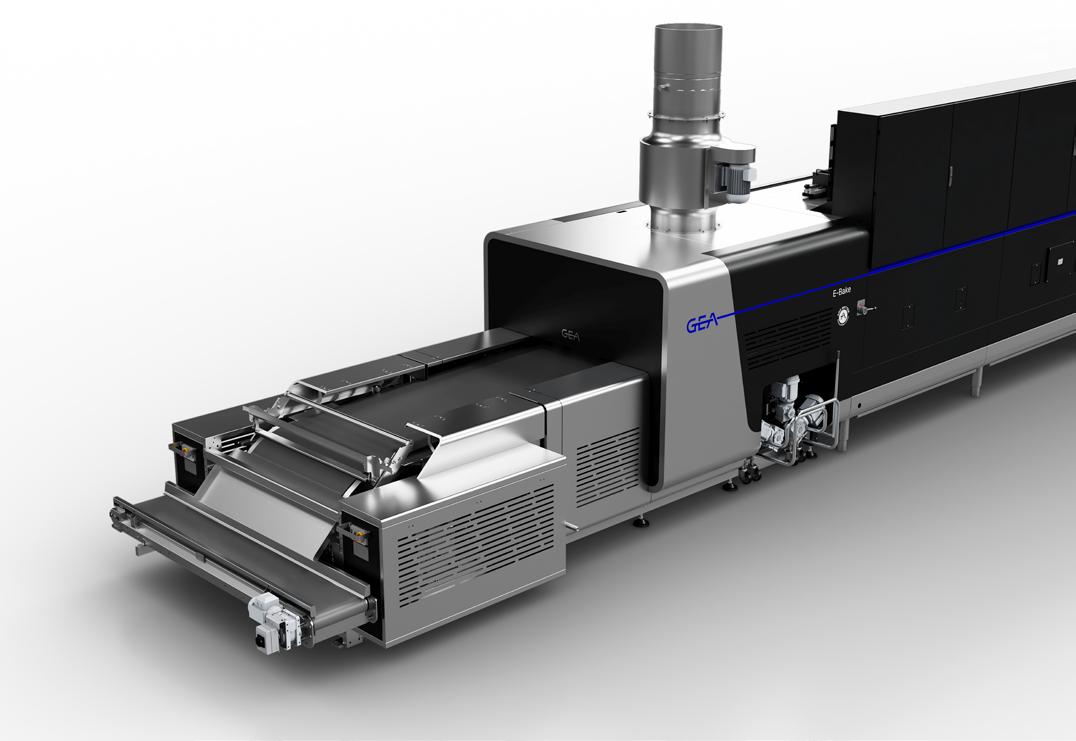

TECHNOLOGIES LEADING THE WAY

Digitalization and energy efficiency are central to the new era of milling. Bühler’s Arrius system, an integrated grinding solution combining roller mill, motor, gearbox, and control system in one compact unit is among the leading drivers in modern milling systems. Its plug-and-play design simplifies installation, reduces energy use by up to 10%, and improves food safety with a sealed, hygienic structure. Meanwhile, the Arrakis mill builds on Bühler’s Airtronic legacy, offering automatic scrapers, centralized lubrication, and remote monitoring for enhanced operational oversight.

Turkish milling equipment giant Imas has made headlines with its Multimilla roller mills, integrating new-generation torque motors into both the feeding and grinding sections. Launched at IDMA 2024, this beltless system reduces energy consumption by up to 25% and eliminates lubrication needs, addressing both cost and cleanliness concerns. Similarly, Omas Industries of Italy is advancing torque motor technology through its Leonardo roller mills. These feature direct-drive motors and a kinetic energy recovery system (KERS) that captures mechanical and thermal energy during braking. Installed at Ag Com's facility in Pennsylvania, the Leonardo system has significantly cut energy use and labour requirements, allowing the plant to run with just one or two operators per shift. For Ocrim, the Turkish equipment supplier recently launched rollermill – RMI, a combination of

4 concepts: simplicity, reliability, competitiveness and italianity. The result is a machine where the innovation and the development coexist in the production process. The concepts of this new rollermill are the same, sturdy and reliable of the RMX model but with an industrial engineering work to offer the machine at maximum levels.

In the UK, Henry Simon Milling, under the Satake umbrella, has introduced the HSRM roller mill for precise and effective grinding operation for wheat, maize (corn) and various grains. This is a new generation roller mill equipped with Advanced Sensor Technology, which enables the tracking of the machine status in real-time and records data for optimum machine operating conditions. Key features include central lubrication, quick roll change capability, and the patented Advanced Sensor Technology, which provides real-time monitoring and optimization of grinding pressure. Stainless steel contact surfaces support allergen control and food safety compliance, which is critical for organic and freefrom-grain applications.

ESTABLISHED PLAYERS ADAPTING TO NEW DEMANDS

Many traditional manufacturers continue to

redefine performance standards through focused innovation. ECOMILL, a company with over 100 years of experience, offers roller mills capable of processing between 400 and 12,000 metric tons per year. Their machines stand out for their ability to handle a broad spectrum of grains, including wheat, rice, rye, buckwheat, and oats. Noteworthy innovations from ECOMILL include a proprietary damping screw conveyor designed for efficient grain tempering and an Aeros centrifugal dresser that minimizes vibration, reduces energy consumption, and features a compact design.

Alapala, a Turkish global milling giant, has deployed over 3,000 units of its Similago II roller mill, featuring a chassis made from thick special carbon steel, which provides exceptional resistance to vibration and wear. This robust design has made it a preferred choice for flour, semolina, and maize mills worldwide. Scherer Inc., based in the U.S., on the other hand, offers custom roller mills and precision-engineered replacement rolls, serving not only traditional grain and feed markets but also soy and mineral processors. Their rapid turnaround and focus on particle size precision have positioned them as a trusted partner for customized milling solutions.

REMOTE MONITORING & IOT CONNECTIVITY SUPPORT REAL-TIME DIAGNOSTICS AND CONTROL, ENSURING THAT MILLS CAN RESPOND TO OPERATIONAL DEMANDS AS THEY ARISE

Similarly, Zaccaria, Brazil’s nearly 100-year-old milling equipment maker, provides turnkey roller mill solutions for corn, rice, pulses, and wheat.

SMARTER MILLS, CLEANER SYSTEMS

Innovation in roller milling extends beyond grinding mechanics. Yenar, another Turkish firm, has introduced the rollCare Profile Measurement Device, a smart tool that uses laser technology to monitor the condition of mill rolls, either during fluting or directly inside the roller mill. This allows for predictive maintenance and improved scheduling, reducing downtime and extending equipment life.

These advancements are underpinned by industry-wide shifts toward sustainability, digitization, and hygienic design. Modular roller mills now allow for flexible plant layouts and phased upgrades. Energy-efficient motors, including directdrive and torque-based systems, cut power consumption and simplify maintenance. Remote monitoring and IoT connectivity

support real-time diagnostics and control, ensuring that mills can respond to operational demands as they arise.

THE ROAD AHEAD: MILLING IN THE AGE OF AI

As the global population edges closer to 10 billion, the demand for efficient, scalable, and sustainable food production becomes urgent. Modern roller milling systems stand at the crossroads of this challenge, quietly but powerfully transforming how the world’s grain is turned into its most essential food staple. In addition, beyond traditional white flour, the demand for whole grain, fortified, and gluten-free flour is rising following increasing consumer awareness of healthy foods.

In tandem with flour micronization, roller mills are increasingly being integrated with flour analysis tools. These systems measure protein quality, starch damage, and enzyme activity in real-time, ensuring the flour meets tight industrial and nutritional specs. This is especially relevant for food manufacturers requiring consistent input for automated production lines. To meet this need, the next frontier for roller milling is full digital integration, an Industry 4.0 approach where mills operate as interconnected, intelligent systems. Predictive algorithms will not just anticipate wear and tear but adjust operating parameters autonomously. Sensors will continue to improve in resolution and sensitivity, and cloudbased platforms will enable remote diagnostics and support, reducing downtime across geographies.

Sustainability, too, is a critical focus. With mounting pressure to reduce carbon footprints, equipment manufacturers are designing systems that minimize water use, maximize energy recovery, and allow for better by-product utilization. Bran, germ, and off-grade flour are being repurposed into value-added food or feed products, ensuring minimal waste from every kernel processed.

Redefining

Trade Commodity

Nouran Ezzeldin on navigating a male-dominated industry with a mission to reshape commodity trade in MENA

BY MARTHA KURIA

When Nouran Ezzeldin first considered a career in commodity trading, she was well aware she was stepping into a world where women were rarely seen, let alone heard. Yet, rather than being deterred, this reality became her motivation. “Commodity trading wasn’t a typical path for women, especially not in our region. But that’s exactly what drew me in,” Ezzeldin recalls.

Her fascination with how agricultural commodities shape economies, combined with a keen awareness of Africa and the Middle East’s untapped potential, set her on a unique professional journey. Today, as the Founder and CEO of Granos Oros for Agribusiness Solutions and Export, Ezzeldin stands as a testament to what can be achieved with vision, resilience, and determination. Sharing her journey with Milling Middle East & Africa Magazine, Ezzeldin takes us through how she managed to breaks barriers in the male-dominated commodity trade industry.

FROM TEACHER TO TRADER: EZZELDIN’S UNCONVENTIONAL PATH

Ezzeldin’s career trajectory is anything but typical. She graduated from the Arab Academy for Science and Technology, specializing in tourism, a field far removed from the world of commodities. Her first job was as a teacher for early years, a role she described as more challenging than her current position.

Her entry into the grain industry was serendipitous. Hired initially as a translator for a grain trading company, Ezzeldin’s talent for business development and marketing quickly became apparent. She soon found herself leading the company’s

import department, successfully managing their grain imports for the first time. This experience ignited her passion for the industry and led her to consider starting her own business in commodity trading.

BUILDING TRADE, EARNING TRUST: THE MISSION OF GRANOS OROS

Ezzeldin’s curiosity about trade systems and the pivotal role of agricultural commodities in shaping economies set her on a path that would see her not only entering the industry but claiming her space within it. With her husband, a sea captain, as her partner, she launched Granos Oros for Agribusiness Solutions and Export. a boutique agribusiness consulting and trading firm.

Her mission is to bridge the gap between international

suppliers and local demand across Africa and the MENA region. From wheat and corn to soybean meal and vegetable oils, Granos Oros offers tailored market entry strategies, brokerage services, and strategic trade facilitation. “It’s not just trade; it’s trust, built transaction by transaction,” she asserts, emphasizing the firm’s focus on intelligence-based consulting and long-term partnerships.

Remarkably, her company is just a year old, yet it has already made significant strides including bringing global grain conferences to Egypt, particularly, the upcoming Global Grain MENA in July 3-4 2025. According to her, launching Granos Oros as a solo founder in a high-stakes sector meant to prove herself daily. Trust, she notes, isn’t easily earned in this industry. However, consistency, transparency, and sharp execution have brought tangible results. Key milestones include establishing a strong presence in Egypt, expanding into Libya and North Africa, and speaking on major agribusiness stages form Geneva to Dubai, Istanbul and Romania. Ezzeldin credits her husband, both life and business partner, and blessings from God. “Despite the challenges of being a woman in this industry, I’ve never felt alone, because God has always been with me, guiding my steps, opening doors, and surrounding me with the right people.”

For women eyeing a future in commodity trading, Ezzeldin’s message is clear: “Go in knowing that you deserve a seat at the table, and if that table doesn’t exist yet, build your own.” She emphasizes the importance of learning the

industry’s language, maintaining professionalism, networking relentlessly, and believing in the unique impact women can bring to the sector.

“Being one of the few women in this industry comes with pressure, but also with pride,” she shares. Each challenge, whether skepticism from industry peers or the complexities of cross-border trade, has only fueled her resolve. “Every barrier I’ve faced only pushed me to grow stronger, louder, and more determined.”

AFRICA’S COMMODITY TRADE: OPPORTUNITIES, CHALLENGES, AND GLOBAL SHIFTS

Africa, Ezzeldin observes, is a continent brimming with opportunity but hampered by structural complexity. Vast natural resources and a burgeoning population are offset by infrastructure gaps and fragmented policies. Yet, there is momentum: regional integration is improving, intra-African trade is on the rise, and the private sector’s role is expanding.

Key commodities driving demand include food security staples like wheat, corn, and soybeans, with increasing consumption of sunflower meal and soybean meal due to the expansion of livestock and poultry sectors. On the export side, specialty crops such as sesame, pulses, and sorghum are gaining traction. “What stands out is political will, where leaders are pro-trade and pro-integration, the results follow,” she adds. Regional blocs like Economic Community of West African States (ECOWAS) and East African Community

(EAC) are working toward harmonized customs procedures and digitized systems, which Ezzeldin sees as positive signs. However, inconsistencies across borders and weak logistical infrastructure continue to challenge efficient trade.

Recent global tariff regimes and trade restrictions have also exposed the fragility of Africa’s supply chains. Export bans, price volatility, and logistics disruptions have prompted a continent-wide reevaluation of sourcing strategies. “It’s been a wake-up call,” says Ezzeldin, stressing the need for more resilient systems and stronger institutional support for exporters, who often operate without sufficient safety nets.

To strengthen resilience, she advocates for diversifying sourcing and distribution, investing in grain reserves, and building regional trade corridors. Egypt, for example, continues to rely on imports of wheat and soybeans, primarily from Russia, Ukraine, and increasingly Romania. However, there is a clear move toward source diversification to protect supply chains from future disruptions.

“Export bans, price volatility, and logistics breakdowns have forced us to rethink sourcing strategies and build resilience,” she says. While Egypt maintains a somewhat balanced model, 40% of grain imports are state-managed and 60% are in the hands of private players. Governments and the private sector must collaborate, fostering innovation, reducing bureaucracy,

and investing in data and logistics to transform responses to global shocks.

INFRASTRUCTURE, POLICY, AND THE ROAD AHEAD

“Unfortunately, many African traders operate without policy support, access to finance, or insurance safety nets. To be competitive globally, we need stronger institutions, trade diplomacy, and supportive frameworks,” she urges. Ezzeldin calls for investments in logistics that match those in production, and for policy frameworks like the African Continental Free Trade Area (AfCFTA) to move from promise to practical implementation. If implemented well, AfCFTA could revolutionize intra-African trade by eliminating unnecessary border delays, standardizing documentation, and creating a single, unified market, reducing Africa’s vulnerability to global externalities.

Looking ahead, Ezzeldin foresees a shift toward local value addition, green sourcing, and digital marketplaces. Technologies like AI and blockchain are already revolutionizing the sector, enabling smaller African traders to access global markets and driving greater transparency and efficiency. For sustained competitiveness, she urges a focus on infrastructure, innovation, and regional integration.

BEYOND SELF-SUFFICIENCY

Ezzeldin remains pragmatic about Africa’s push for selfsufficiency. While applauding efforts in countries like Ethiopia to become wheat self-sufficient, she is realistic about limitations. “Even if wheat production increases, Egypt’s consumption levels are too high for us to fully depend on domestic supply. Imports will remain part of our food security equation,” she states.

She argued that while increased local production is beneficial for food security, it is unlikely to eliminate the need for imports or enable significant intra-African grain trade in the near future. Exporting staple grains like wheat or rice remains a challenge due to domestic demand and government restrictions. The reality is that for many African countries, grain imports will continue to play a stabilizing role in African trade.

A VISION ROOTED IN IMPACT

Though still in its early years, Ezzeldin hopes that Granos Oros for Agribusiness Solutions and Export has ambitious plans to expand across Africa, Gulf region and eventually globally. She attributes her rapid success to hard work and divine blessing, expressing hope that her business will achieve global reach in the coming years.

Ultimately, she hopes her journey will inspire more women and African entrepreneurs to lead in spaces where they were once told they didn’t belong. “I want Granos Oros to be remembered not just as a company, but as a force for inclusion, integrity, and transformation in agribusiness.”

“What bloomed from my battles proves ease was never the goal, that’s the wild, unstoppable magic of being a woman.” MMEA

FOCUS on Türkiye

BY MARTHA KURIA

Türkiye, (formally Turkey) with a total area of 779 45 km², lies between Europe and Asia, has long been recognized as a vital agricultural powerhouse. Its strategic location, diverse climate, and rich soils have shaped a dynamic grains sector that not only feeds its population but also supplies the world. Agriculture remains central to Türkiye’s economy, contributing approximately 7% to its GDP and employing nearly 20% of the workforce, according to United Nations data. The country ranks 8th globally in agricultural output.

Driving Global Grain Markets through Innovation

Cereals, particularly wheat and barley, dominate the landscape, supported by other key crops such as maize, rice, rye, millet, and oats. Globally, Türkiye ranks 17th in total grain production, contributing 1.3% to the world’s output. Despite this modest share, it holds a 2.4% stake in the US$281 billion global grain trade, with US$6.6 billion in export value. However, recent projections paint a mixed picture for the country’s grain output. According to the latest weather data from the Turkish State Meteorological Service, precipitation levels across the country from October-December 2024 were down 16 percent

from the historical average and 28 percent below the same period the previous year. Looking ahead to 2025, forecasts by the Turkish Statistical Institute (TurkStat) and the Ministry of Agriculture and Forestry suggest a further 4.1% decline in overall grain production, down to 37.4 million tons.

WHEAT SECTOR FACES PRODUCTION DIP AMID DROUGHT, SHIFTING TRADE POLICIES

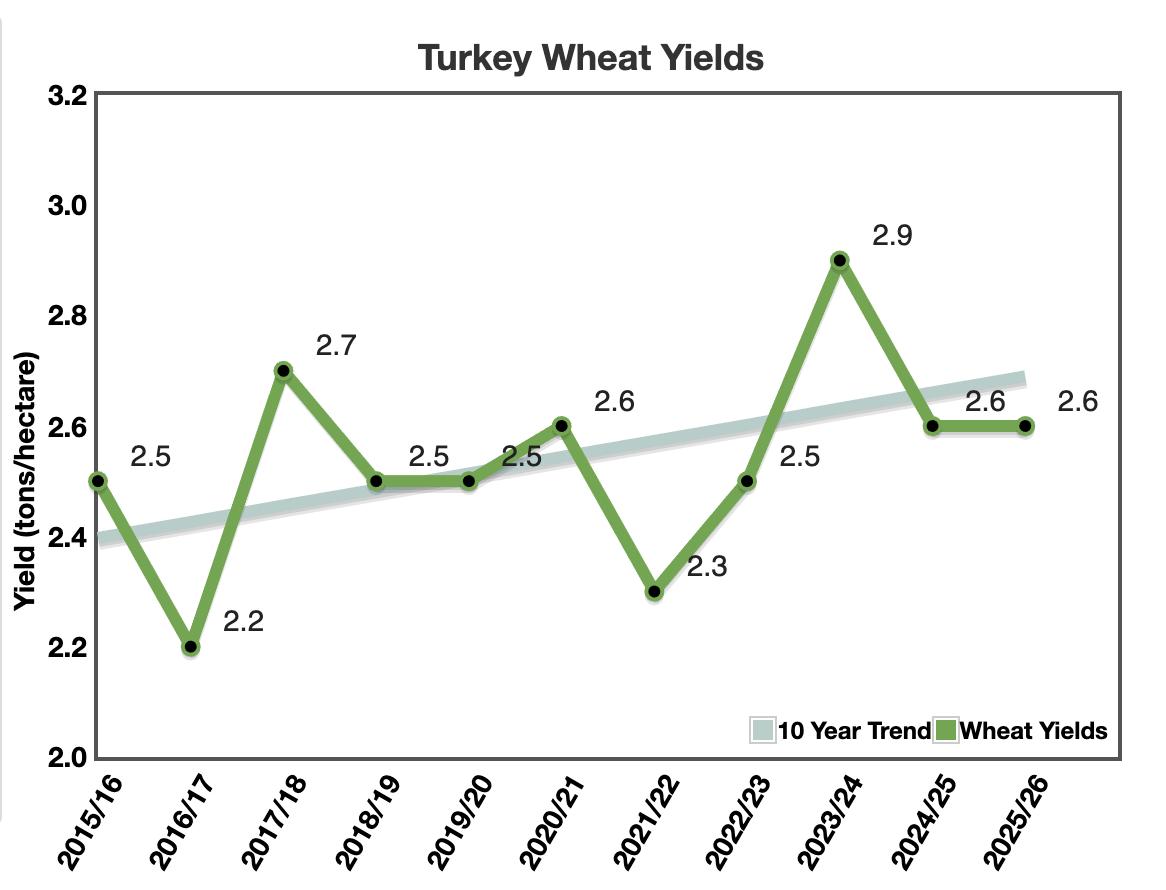

Turkey’s wheat sector, which occupies a central position in the country’s agricultural landscape, is facing renewed pressure from climatic and policy-related challenges. Data from the Turkish Statistical Institute shows that in the 2020–2021 season, Turkey accounted for 3.2% of the global wheat cultivation area, with wheat representing 44% of the country’s total cultivated grain land.

Despite a modest increase in the harvested area, reaching 7.35 million hectares, wheat production for the 2025–2026 season is expected to fall to 18.5 million tonnes, down from 19 million tonnes a year earlier. This decline is attributed primarily to a significant drop in yield following one of the driest fallto-winter periods in 65 years, which has severely affected major wheat-producing regions in Central and Southeastern Anatolia.

Farmer decisions around wheat cultivation are closely tied to the Turkish Grain Board’s (TMO) purchasing policies. TMO plays a key role in market regulation by procuring both local and imported wheat on behalf of the government. For the 2024/25 marketing year, TMO announced procurement

DESPITE A MODEST INCREASE IN THE HARVESTED AREA, REACHING 7.35 MILLION HECTARES, WHEAT PRODUCTION FOR THE 2025–2026 SEASON IS EXPECTED TO FALL TO 18.5 MT

prices of 9,250 Turkish Lira per metric tonne (US$289/MT) for milling wheat and 10,000 TL/MT (US$313/MT) for durum wheat, providing a degree of price stability amid otherwise volatile conditions.

Domestic wheat consumption is projected to remain steady at 19.4 million tonnes. Food-grade wheat, which accounts for approximately 90% of total use, continues to dominate consumption patterns, though demographic changes and rising income levels are gradually shifting preferences away from bread toward a more diverse range of food products. Nonetheless, with a population exceeding 87 million, Turkey remains among the highest consumers of bread on a per capita basis globally.

IN NUMBERS

NATION'S CORN ALLOCATED TO ANIMAL FEED

Wheat production in Turkiye 2016-2025

Marketing Year

To cater for the increasing appetite, the USDA forecasts wheat imports to rise significantly, reaching 8 million tonnes in the 2025–26 marketing year, double the volume imported in the previous year. The increase is largely attributed to the lifting of restrictions related to the inward processing regime (IPR), a trade policy tool that allows duty-free wheat imports for processed product exports. Earlier in 2024, imports had dropped by 40% during the first half of the year due to the temporary suspension of the IPR

TÜRKIYE’S BARLEY MARKET ADJUSTS TO FEED SECTOR DEMANDS

Barley, the world’s second-most cultivated grain after wheat, plays a pivotal role in livestock nutrition and brewing in Turkey. While a modest portion is processed into malt for beer and other beverages, the about 85% is consumed by the livestock industry, which continues to expand in response to rising global demand for meat and dairy.

In 2024/25 marketing year, however, barley production fell sharply from 8

million tonnes to approximately 7 million tonnes. A combination of prolonged dry weather and shifting farmer preferences was attributed to this contraction. According to USDA projections, the harvested area shrank by 7%, falling to 3.5 million hectares. For 2025/2026, production is forecast to further decline 11% year-on-year, landing at just 6.65 million tonnes.

Despite this drop, domestic consumption is expected to hold steady at 7.4 million tonnes, reflecting sustained demand from the animal feed sector and modest growth in the licit brewing segment. To cushion against the production shortfall, the government continues to support farmers through subsidies and the promotion of drought-resistant barley varieties.

Imports for the 2025/26 marketing year are projected to soar to 900,000 tonnes to bridge the gap between dwindling supply and steady demand. This represents a significant leap from the revised 2024/25 import estimate of 170,000 tonnes.

TÜRKIYE BOOSTS CORN IMPORTS AMID RISING FEED DEMAND

Corn stands as Türkiye’s third most significant grain crop, trailing only wheat and barley. With approximately 80% of the nation's corn allocated to animal feed, the remainder supports a thriving starch, oil, and food processing industry. But as consumption surges and climate challenges

loom, Türkiye finds itself at a critical inflection point, caught between rising demand and dwindling water resources. In marketing year (MY) 2025/26, corn area harvested is projected to increase to 610,000 hectares, as farmers shift from crops like cotton and vegetables, driven by high market prices, exceeding 10,000 TL/MT (US$270/MT) in March 2025.

This expansion comes despite government efforts to reduce corn cultivation in water-scarce regions. Türkiye's corn consumption is projected to rise to 9.8 million metric tons (MMT) in MY 2025/26. This growth is largely driven by the expanding needs of the country’s integrated poultry sector, one of the largest in Europe. As the world’s eighth-largest chicken meat producer, Türkiye is forecast to increase poultry output by 8% in 2025, according to USDA’s Production, Supply and Distribution (PSD) data. This, in turn, is fueling greater demand for compound feed, particularly corn-based rations.

To address supply pressures and stabilize prices, the government introduced a 1 millionton corn import quota effective through June 30, 2025, with a reduced 5% customs duty. Imports

are limited to 8,000 tons per shipment, with a seven-day gap between deliveries. After the deadline, the tariff reverts to 130% to protect local producers during harvest.

TURKIYE BETS ON SUNFLOWER AS OILSEED IMPORTS SOAR

In marketing year (MY) 2025/26, Turkiye’s total oilseed production, comprising sunflowerseed, cottonseed, and soybean, is projected to edge up slightly to nearly 2.9 million metric tons (MMT). This modest year-on-year increase is largely driven by a significant rise in sunflowerseed output, which is expected to compensate for a decline in cottonseed production.

Faced with economic and climatic pressures, Turkish farmers are increasingly pivoting away from cotton in favor of sunflowerseed and other row crops. The anticipated expansion in sunflower cultivation is expected to boost production by around 15%, reaching approximately 1.55 MMT in MY 2025/26. This marks a solid recovery, though output still falls short of long-term averages. Soybean production, on the other hand, is expected to remain static at 150,000 metric

Barley production in Turkiye 2016-2025 SOURCE:

Marketing Year

tons, as harvested acreage shows no notable growth. Despite this, domestic demand for soybeans continues to climb. Total soybean consumption is forecast to increase modestly to around 3.73 MMT, reflecting a steady rise in demand from Turkiye’s dynamic animal feed sector, particularly poultry and, increasingly, aquaculture. With local output unable to meet industrial and nutritional needs, Turkiye is set to break records in soybean imports in MY 2025/26. Likewise, the country will continue to rely heavily on foreign supplies of sunflowerseeds, sunflower oil, and sunflower meal to meet its

growing requirements.

TÜRKIYE’S GRAIN SECTOR GEARS UP WITH INNOVATION AND STORAGE UPGRADES

Türkiye is fast becoming a strategic powerhouse in the global grain ecosystem, underpinned by a robust storage network and forward-looking investments in innovation and technology. The Turkish Grain Board (TMO) currently manages 4.5 million tonnes (Mt) of silo capacity, with an additional 2.5 Mt handled through licensed private warehouses, bringing the country’s total grain storage to over 10 Mt, according to the FAO.

To futureproof this capacity, TMO launched modernization projects worth TRY 10 billion (US$370 million) in 2023. These initiatives aim to upgrade existing storage infrastructure and incorporate automation systems, improving efficiency, traceability, and safety across the national grain supply chain.

Complementing this public investment, privately-owned port silos in strategic coastal cities, Mersin, Izmir, and Samsun, further reinforce Türkiye’s role as a critical gateway in the Black Sea grain trade. In parallel with storage modernization, Türkiye is setting the stage for a transformative leap in grain and food technologies. The Association of Milling and Sector Machinery Manufacturers (DESMÜD) has announced a bold initiative: a US$5 million Grain and Grain Products Innovation Centre to be established in the Sincan district of Ankara. Spanning a 4.5-acre site secured through a 25-year protocol with the Ankara Metropolitan Municipality, construction is slated to begin in 2025, with completion expected within three years.

“The facility will feature cutting-edge R&D laboratories and high-level training programs to elevate our grain machinery industry to global standards,” stated DESMÜD President Zeki Demirtaşoğlu. As a grain machinery hub, Demirtaşoğlu

projects that within a decade of operation, exports from Türkiye’s grain machinery sector will also more than double, growing from US$3.7 billion to an estimated US$8 billion. This leap would significantly enhance the sector’s contribution to the national economy and solidify Türkiye’s position as a toptier exporter of grain technologies.

TURKIYE’S REIGN IN GLOBAL FLOUR TRADE

For over a decade, Turkey has stood as the world’s leading wheat flour exporter. On average, Türkiye processes and exports between 7.5 and 8 million tons of grain-based products annually, reaching nearly every corner of the globe. It is the world’s largest exporter of wheat flour, commanding a 22% global market share, and the second-largest pasta exporter with 13%. Türkiye also ranks first in bulgur exports (255,000 tons annually), fifth in biscuit exports (about 200,000 tons), and continues to expand its reach into new markets.

In 2023, Turkey exported wheat flour worth US$1.47 billion, commanding a 21.2% share of the global wheat flour market, which was valued at US$6.96 billion, according to the Turkish Statistical Institute. However, recent shifts in production dynamics and trade policies have seen Turkey's flour exports dip to US$1.159 billion in 2024, a 20.9% decline, with volumes falling from 3.648 million tonnes to 3.022 million tonnes.

The country has over 550 operational flour mills with a combined processing capacity of 33 million tonnes. Its pasta sector includes 25 plants producing nearly 2.9 million tonnes per year, operating at 85% capacity utilization. Additionally, more than 140 factories across the country manufacture bulgur, semolina, cookies, and crackers, reinforcing the depth and breadth of the country’s grain-processing industry.

Speaking at a press briefing, Deputy Trade Minister Mahmut Gürcan affirmed Turkey’s continued leadership in the global flour trade. He acknowledged, however, that the year-on-year decline in export volumes and revenues poses new challenges for the sector. To curb the export downturn and address the decline in flour shipments, Turkish authorities recently replaced the full wheat export ban with a new allocation system. Under this model, processors will be permitted to import only 15% of the volume they export, with the remaining 85% to be sourced from TMO’s domestic grain reserves. The strategy aims to maintain export momentum while protecting domestic supply chains and price stability.

On the pasta export front, Turkey continues to hold its ground. From June 2024 to January 2025, pasta exports totaled over 940,000 tonnes, nearly identical to figures from the same period the previous year. Somalia, Ghana, and Togo emerged as leading destinations. MMEA

What’s Your Wheat

Really Costing You?

Unlocking Value beyond the Wheat Price

BY FABIEN VARAGNAC

In volatile global wheat markets, price is often the first — and sometimes only — factor buyers consider when sourcing grain.

But in the world of flour milling, where profitability hinges on yield and consistency, the cheapest wheat on paper can quickly turn out to be the most expensive in practice.

For millers in the Middle East and Africa, who frequently rely on imports and face strong competitive pressure, it’s time to rethink the way we define wheat value. This article explores how focusing on milling yield, consistency, and overall cost-in-use can significantly impact your bottom line — and why wheat price per ton is only part of the story.

PRICE ISN’T EVERYTHING

Let’s be clear: price matters. A US$5–10/ton difference can swing a procurement decision — especially for high-volume buyers. But what happens if that cheaper wheat delivers 2% less flour, or requires more tempering, or results in out-of-spec batches that increase rejection rates or require expensive corrections?

In real-world conditions, milling yield variation of 3 to 4 percentage points is very possible. On a crop like 2024/25, one wheat may yield 823 kg of flour per ton, while another only reaches 785 kg. If your wheat costs US$250/ton, that 38 kg difference translates into a $14.70 swing in cost per ton of flour — often more than the original price gap.

MILLERS DON’T SELL WHEAT. THEY SELL FLOUR.

This is the core idea behind cost-in-use analysis: what really counts is how much usable flour your wheat can produce — and at what operational cost.

To get the true cost-in-use of your wheat you have to include:

- Dockage: 2% dockage means you’re paying for material that will be removed during cleaning. That’s a US$5.21/t hidden cost.

- Moisture: Initial moisture before tempering increases wheat weight but doesn’t contribute to flour output. Just 1.5% extra moisture can add US$4.10/t of flour.

Together, these factors can add $10–15/t or more to your real flour cost — potentially outweighing the benefits of a lower wheat price.

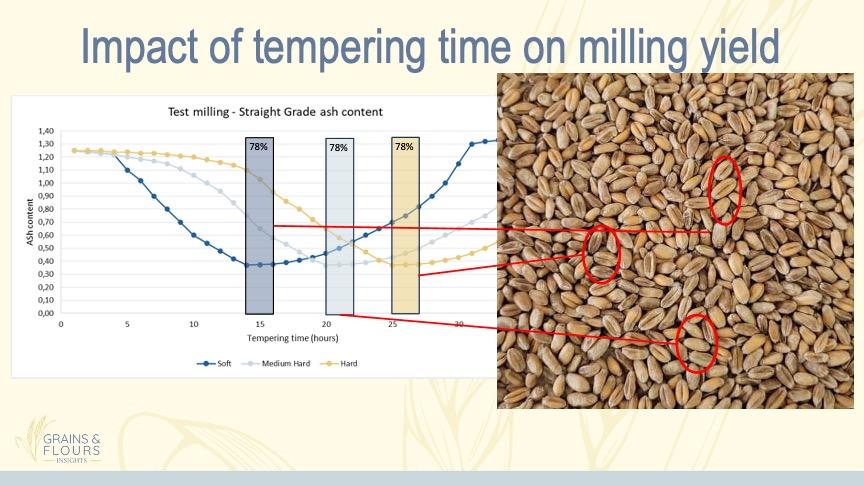

THE POWER OF CONSISTENCY

In addition to yield, consistency across a wheat batch is a major driver of cost efficiency. Why? Because inconsistent wheat forces millers to compromise:

- Variable ash content can lead to quality rejections or force mills to lower extraction rates to meet spec — reducing flour output.

- Unstable performance increases reliance on correctors and technical improvers — all of which eat into margins and can result in inconsistent flour quality and unhappy customers.

- Mismatched tempering times reduce overall yield. A mix of soft, medium, and hard wheat tempered uniformly will result in none of them reaching their optimal extraction rate, leading to an overall lower yield.

As shown in the illustration below, even commercial wheat samples can show high variability — making proper tempering impossible and significantly reducing extraction rates.

Even a 1% drop in yield from inconsistency alone can add US$3–6/t to your cost of flour. In practice, a highly heterogeneous wheat batch can lead to yield losses as high as

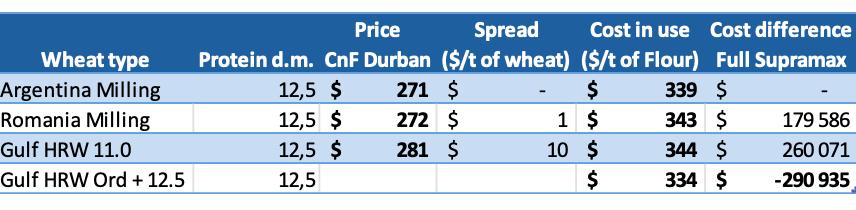

Let’s take a real-world example, in early April, if you were looking for a 12.5% grist for delivery of a full Supramax in Durban, the cheapest option would have been Argentina 12.5%. But if you adjust your cost in use based on wheat milling properties and heterogeneity impact, you would realize that a blend of 2 grades of HRW (Ord and 12.5) would save you around $5/t of flour, resulting in total savings of nearly $300,000 on a full Supramax cargo.

THE TAKEAWAY: COST-IN-USE IS KING

Millers across the Middle East and Africa operate in highly competitive markets, often under cost pressure and logistical constraints. In this context, smart sourcing is not about chasing the lowest price — it’s about maximizing flour output, minimizing risk, and ensuring stability in performance.

So before closing your next wheat purchase, ask yourself:

- What’s the likely flour yield?

- How consistent is the wheat quality?

- What’s the impact of this wheat on my entire process — from cleaning and tempering to mill settings and additive usage?

The best wheat is not always the cheapest on paper. It’s the one that delivers the best value in each and every bag of flour you deliver to the market. MMEA

The Soybean Balancing Act

Fueling MEA’s Food Systems with Foreign Soybeans

BY WANGARI KAMAU

Soybeans have come a long way from their origins as a traditional crop in East Asia to become a cornerstone of modern agriculture and global trade. Once confined mainly to regional cultivation and consumption, the oilseed gained international prominence in the 20th century, especially after large-scale production took root in the United States. Today, soybeans are one of the world’s most strategically important crops, with global production estimated at 420 million metric tons in the 2024/25 season, according to the United States Department of Agriculture (USDA). Brazil, the United States, and Argentina lead the charge, accounting for the vast majority of this output.

Valued for its rich nutritional profile, approximately 40 % protein and 20 % oil, soybean supports diverse uses across human food, livestock feed, edible oil, industrial products, and even medicinal applications. Agronomically, it belongs to the legume family and contributes to soil health through nitrogen fixation, reducing the need for synthetic fertilisers in crop rotations.

In Africa and the Middle East, soybean production remains relatively small, yet the crop's importance is growing fast. Soaring demand for poultry, aquaculture inputs, and processed foods is positioning the regions as key importers and emerging processors in the global soybean economy.

PRODUCTION REFLECTS SMALL BUT SIGNIFICANT GAINS

While the Middle East and Africa (MEA) region contributes less than 1% of global soybean output, local production is gradually gaining ground. This growth is being fueled by rising domestic demand, particularly from the livestock, aquaculture, and food processing sectors, as well as targeted government policies that promote soybean cultivation.