Sugar Reduction: The Future of Sugar Reduction in Africa’s Beverage Industry

Maltodextrins: The Unsung Backbone of the Modern Food Industry

Alternative Protein: A Global Shift Towards Sustainable Proteins

Middle East & Africa

Year 12 | Issue No.67 | Mar - Apr 2025

FOUNDER & PUBLISHER

Francis Juma

SENIOR EDITOR

Martha Kuria

EDITORS

Alphonse Okoth

Francis Watari

Nicholas Ng'ang'a

Fridah Chepkoech

Mercy Mukiri

Lydia Khasoa

Mary Wanjira

BUSINESS DEVELOPMENT DIRECTOR

Virginia Nyoro

BUSINESS DEVELOPMENT ASSOCIATE

Vivian Kebabe

HEAD OF DESIGN

Clare Ngode

ACCOUNTS

Jonah Sambai

Published By: FW Africa

P.O. Box 1874-00621, Nairobi Kenya

Tel: +254725 343932

Email: info@fwafrica.net

Company Website: www.fwafrica.net

www.foodbusinessmea.com www.millingmea.com

Food Business Middle East & Africa (ISSN 2307-3535) is published 6 times a year by FW Africa. Reproduction of the whole or any part of the contents without written permission from the editor is prohibited. All information is published in good faith. While care is taken to prevent inaccuracies, the publishers accept no liability for any errors or omissions or for the consequences of any action taken on the basis of information published.

www.horecamea.com

www.dairybusinessmea.com

FEE BUSINESS

www.feedbusinessmea.com

www.sustainabilitymea.com

www.healthcaremea.com

www.hpcmagmea.com

Ushering in a New Era for the Food and Beverage Industry Across Continents

After more than a decade of chronicling the growth, challenges, and transformation of Africa’s food and beverage industry, we are proud to announce a bold new chapter in our journey: Food Business Africa Magazine is now Food Business Middle East & Africa Magazine. As the food and beverage industry continues to evolve across borders and sectors, so too must the platforms that inform and inspire its stakeholders.

The relaunch is not merely a cosmetic change. It represents a deeper editorial commitment to providing cutting-edge insights and comprehensive coverage of the food and beverage value chain, stretching from Africa through the Middle East and into the Indian subcontinent and Asia. Francis Juma, the Founder and CEO of the publication, emphasizes the rationale behind this shift. “As the leading publisher in the African and Middle East region, we appreciate the tremendous progress we have witnessed in Africa over the last decade, and the work we have done over the years has contributed immensely to the growth of the food and beverage industry on the Continent.

As part of this strategic rebrand, we have introduced Food Ingredients Middle East & Africa, an innovative new insert within the main publication to provide specialized content focused on the ever-evolving landscape of food ingredients. From novel formulation technologies to trends in health and nutrition, this insert will take a deep dive into one of the most critical areas of the food and beverage industry today. It is a platform to explore the wave of innovation driven by urbanization, rising consumer incomes, and shifting dietary preferences across our target regions.

Issue 67, our first under the new brand identity, delivers on this promise with a rich and diverse editorial lineup. The magazine takes a closer look at the growing demand for organic-certified coffee in East Africa, particularly Kenya, where producers are pushing toward certification despite the regulatory and logistical challenges they face. It’s a compelling story of resilience and opportunity in a rapidly expanding

niche segment. A special focus on agroprocessing in Zambia, chemical contamination in the food industry and a special pick from the recent Food and Agriculture Organization (FAO) of the United Nations Food Safety Foresight Programme.

Our spotlight on packaging explores the concept of lightweighting as a modern solution to the plastic crisis, providing insights into how manufacturers can reduce material use while maintaining product integrity and sustainability goals. The issue also features a detailed analysis of port privatization efforts in Africa, examining how these developments are poised to impact logistics and supply chain efficiencies for the food and beverage sector.

In our dedicated food ingredients section, we unpack the role of maltodextrins in modern food processing, explore the rise of alternative proteins, and examine the evolution of dairy ingredients across various product categories. Each feature is designed to offer valuable insights that manufacturers, processors, suppliers, and industry stakeholders can act upon.

This issue concludes with a comprehensive roundup of the latest developments from across the region and the globe, including investments, mergers and acquisitions, supplier innovations, and financial reports that are shaping the direction of the industry.

With this landmark issue, we not only celebrate our new name but also reaffirm our commitment to being the most trusted source of business intelligence for the food and beverage industry in the Middle East and Africa.

As always, we thank you, our readers, partners, and contributors, for your continued support as we embark on this exciting new chapter together.

Enjoy your read!!

Martha Kuria Senior Editor FW Africa

Propak East Africa

May 20-22, 2025

Sarit Center, Nairobi, Kenya www.propakeastafrica.com

Sustainability in Packaging MENA

May 21-22, 2025

Dubai www.sustainability-in-packaging.com/mena

Avocado Africa

May 27-30, 2025

Sarit Centre, Nairobi, Kenya www.avocadoafrica.com

Propak MENA and Fi Africa

June 2 - 4, 2025 Cairo, Egypt www.propakmena.com

World Aquaculture Safari 2025

June 24 -27, 2025

Entebbe, Uganda www.was.org/meeting/code/afraq25

AFMASS Food Manufacturing Eastern Africa

July 2 -4, 2025

Sarit Center, Nairobi, Kenya www.afmass.com

AFRIPAK Expo East Africa

July 2 - 4, 2025 Nairobi, Kenya www.afripackexpo.com

SAAFoST Congress

August 25-27, 2025, Pretoria, South Africa www.saafost.org.za/congress/

Africa Dairy Summit

September 17-19, 2025 Nairobi, Kenya wwww.africadairysummit.com

Gulfood Manufacturing 2025

November 4-6 2025, Dubai www.gulfoodmanufacturing.com

IAOM MEA Conference & Expo

December 1-4, 2025

Jeddah, Saudi Arabia www.iaom.org

All eyes on Nairobi as AFMASS Food Manufacturing Expo 2025 reimagines the Future of Africa’s Food Industry

As the calendar inches closer to July 2-4, 2025, anticipation is swelling across Africa’s food, beverage, and milling industries. All roads will lead to the Sarit Expo Centre in Nairobi, Kenya, where the 10th AFMASS Food Manufacturing Expo Kenya, East African Edition, is set to take place. This milestone edition is poised to be the most comprehensive yet, gathering 180+ exhibitors and 8000+ delegates from more than 30 countries.

A DECADE OF GROWTH, A CONTINENT’S AMBITION

Since its inception in 2013, AFMASS Food Manufacturing Expo has carved a niche as the Pan-African gathering for professionals across the food manufacturing value chain. From ingredients to processing, packaging, and policy, the Expo has become the definitive platform for stakeholders to exchange ideas and evolve. In 2025, the event expands in both size and scope, promising to welcome participants from across the globe, each bringing their unique solutions to food industry challenges.

With the African food industry poised to grow to US$1 trillion by 2030, driven by population growth, urbanisation, and changing dietary preferences, this event arrives at a critical juncture, reflecting these macro trends and providing a space for innovation to meet implementation.

A 6-IN-1 MEGA INDUSTRY EXPERIENCE

A powerful mix of local and international companies has already secured their exhibition space in this year’s six co-located shows,

each reflecting critical segments in the continent’s food ecosystem as highlighted below.

Africa Food Ingredients Expo will present innovations that power modern food development. With increasing consumer awareness about health and transparency, this section will offer a sneak peek into the next generation of food products. Dohler, Kerry, Mane, Freddy Hirsch, Reda Food Ingredients, Decase, Skypex, Fencem Inc., among others, have secured their slots. This is your opportunity to join them.

Africa Healthy & Natural Products Expo is the answer to the rising demand for plant-based, organic, and wellness-centric products. Companies are expected to showcase solutions that align with both global wellness trends and local taste profiles.

Africa Food Market Expo will provide a trading floor for both regional and international brands to present their fresh and packaged products to buyers, retailers, and distributors. Come join Simplifine, Dormans, and Brava Foods, among many others and showcase your products.

Afripack Expo promises a technology spectacle, where global players will display cutting-edge machinery and automation systems. They will demonstrate solutions that enhance safety, traceability, and sustainability, central to food production globally. Lenara Africa (Fischbein), for example, will present packaging equipment, flexible and rigid containers, and specialised logistics services.

Africa Milling Expo will spotlight innovations for grain milling, animal feed, and pet food production. Exhibitors will present

systems designed to optimise yield, reduce energy usage, and meet stringent safety standards. Join Buhler, Altinbilek, Makenas Grain Milling Technology, Cimbria, Cukurova Silo, and Myande, among others and introduce your solutions to the industry.

Food Safety & Quality remains a critical cog in the food and feed industries, and as such, suppliers in this sector will have their say at this premium event. Africa Labtech Expo brings Sorela Scientific East Africa, Bastak Instruments, Acetek Software, Control Union, GAAP, Dairy Consulting and Bioeasy to showcase digital traceability technologies, ERP systems, certification services, and other food safety and quality control services.

Other sectors in the meat & poultry will showcase solutions in the industry. Come join Freddy Hirsch.

CO-LOCATED EVENTS EXPANDING THE SCOPE

The Expo will be co-hosted with FIVE related events, providing a unique opportunity for cross-sector collaboration, knowledge exchange, and business development.

Africa Poultry & Animal Feed Expo

The Africa Poultry & Animal Feed Expo is a pivotal platform for stakeholders in the poultry, aquaculture, and animal nutrition sectors. This expo brings together manufacturers, distributors, and service providers showcasing the latest in breeding technologies, feed formulations, veterinary solutions, and processing equipment.

Africa Fresh Produce Expo (AFPEX)

AFPEX is the premier gathering for professionals in the fresh produce sector. The expo features an array of exhibitors presenting advancements in agro-inputs, post-harvest technologies, packaging solutions, and logistics.

Africa Logistics Expo

Recognising the critical role of logistics in the agri-food industry, the Africa Logistics Expo 2025 debuts as a dedicated event focusing on sustainable and efficient supply chain solutions. This expo will bring cutting-edge technologies in transportation, warehousing, cold chain management, and mobility services.

Africa Hotels & Restaurants Expo

BEYOND EXHIBITION: CELEBRATING TASTE, INNOVATION, AND THOUGHT LEADERSHIP

The expo will also be a festival of ideas, flavour, and recognition, with the launch of the Africa Tastemasters Culinary Festival, an exciting addition featuring masterclasses, competitions, and interactive demos across baking, pastry, meat preparation, coffee brewing, tea crafting, and mixology. Backed by beloved local brands Razco, DPL Festive Bakery, Broadway Bakery, Bakex Millers, and Capwell Industries, the festival will offer both entertainment and learning opportunities for culinary enthusiasts and professionals.

Finally, the icing on the cake will be the re-invigorated Africa Food & Packaging Awards, where leading and impactful individuals and businesses across Africa’s food, beverage and milling industry, as well as the manufacturers of packaging materials and technologies, will be celebrated and honoured at the awards ceremony. These accolades reinforce the Expo’s commitment to raising industry standards across the continent.

JOIN THE CONVERSATION ON SUSTAINABLE FOOD SYSTEMS

Held alongside the Expo, the Africa Future Food Summit (www. africafuturefoodsummit.com) will provide a high-level platform for critical dialogue. This 3-DAY Summit will bring together top decision-makers from industry, government, and academia to tackle themes central to Africa’s food transformation. Topics will span climate-resilient supply chains, policy frameworks for regional trade, digitisation of agri-food systems, and investment in food infrastructure, where key players like Bühler, IFF, Döhler, and AGF Freezers have already secured their technical sponsorship slots.

SECURE YOUR EXHIBITION, SPONSORSHIP SPOT

With momentum building fast, secure your slot as an exhibitor or sponsor now to showcase your products and tap into emerging markets across Africa. Sponsorship packages are available for brands seeking high-impact visibility and targeted engagement. Whether you're looking to grow your brand, launch a product, or explore new partnerships, this is the regional stage to be on.

See you in Nairobi!

The Africa Hotels & Restaurants Expo caters to the hospitality sector, highlighting the intersection between food manufacturing and food service. The hospitality industry will find valuable resources to enhance its offerings, align with culinary trends, and meet the evolving needs of consumers.

Africa Home & Personal Care Expo

Many suppliers serving the food and beverage sector also cater to the home and personal care industry, giving them a platform to present their multi-pronged solutions under one roof. Companies such as IFF and Kerry have diversified ingredient portfolios that span food, beverage, nutraceuticals, and personal care segments, making this event just right for them.

NEWS UPDATES

By www.foodbusinessmea.com

Mansourah Poultry reports 42.39% profit growth in 2024, reaching US$4.88M

EGYPT - Mansourah Poultry Company (MPCO) has reported a substantial 42.39% rise in its consolidated net profit for the year ending 2024, reaching US$ 4.88 million, compared to US$ 3.41 million in 2023. This impressive increase is complemented by a rise in earnings per share, which grew from US$ 0.007 at the end of 2023 to US$ 0.008 by December 2024. Along with the profit increase, MPCO’s revenue also saw a notable jump, climbing from US$ 16.11 million in 2023 to US$ 24.51 million in 2024, reflecting a clear improvement in the company’s financial standing over the 12-month period.

On a standalone basis, MPCO’s net profit mirrored this positive trend, increasing to US$ 4.89 million in 2024, up from US$ 3.41 million the year before. The company, which was founded in April 1983 as an Egyptian joint-stock entity, continues to hold a strong position in the competitive poultry sector. This growth further solidifies its role as a key player in Egypt’s poultry industry.

Mansourah Poultry Company’s shares are listed on the Egyptian Stock Exchange, with a nominal value of 0.20 EGP, and a total of 625 million shares. The company maintains an issued and paid-up capital of US$ 4.06 million (EGP 125 million), and its fiscal year begins on January 1st each year. PKF Auditor

Badr & Co. oversees the company’s audits, ensuring transparency and accountability in its financial reporting.

The company operates within Egypt’s thriving poultry market, which has seen a consistent rise in per capita poultry meat consumption in recent years. In 2021, per capita consumption reached a record high of 21.3 kilograms, reflecting a 7.67% increase compared to the previous year.

JBS moves forward with NYSE listing plans

USA - JBS SA has taken steps toward its long-planned listing on the New York Stock Exchange, according to a regulatory document filed with the U.S. Securities and Exchange Commission (SEC). The company, which is the largest meat processor in the world, submitted a filing on Friday that outlines a possible board meeting on April 22 to propose a general shareholders' meeting.

If approved, the shareholder vote is expected to occur around May 23. Should the process pro ceed without delay, JBS shares could begin trading on the NYSE as early as June 12. This initiative forms part of a dual listing strategy that would see the company’s shares traded in both the U.S. and Brazil, where it is already listed.

The proposed general meeting, however, is contingent on the SEC giving the green light to a registration document known as Form F-4. The form is still under review, and its approval remains a prerequisite before any shareholder

meeting can take place.

A source with knowledge of the matter said the SEC asked JBS to provide an estimated timeline for procedural purposes but emphasized that the dates are not final. Equity analyst Igor Guedes from Genial Investimentos commented that the timeline might indicate optimism from JBS, though the outcome still depends on the regulator’s approval.

Meanwhile, BNDESPar, the investment arm of Brazil’s development bank and the company’s second-largest shareholder, has stated it will abstain from voting. This decision appeared to ease investor concerns, as JBS shares saw gains on the Brazilian market after the announcement.

While JBS pursues its U.S. listing, the company is also expanding its operations in Southeast Asia with an investment of US$100 million in Vietnam. The first facility is scheduled to be built in Hải Phòng’s Nam Đình Vũ industrial park, including a logistics hub along with areas designated for meat cutting, packaging, and pre-processing.

Rashid,

Saudi Arabia Chocolate Market size to reach US$2.00B by 2033

SAUDI ARABIA - The Saudi Arabia chocolate market was valued at US$1.32 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 4.75%, reaching US$2 billion by 2033, according to Research and Markets. This growth is primarily driven by cultural practices, such as gifting during festivals, and rising demand for premium, customized chocolate products. Chocolates are often associated with pleasure and generosity, especially during religious and social celebrations, where gifting plays a central role.

Urbanisation and increasing affluence, particularly in Northern, Central, and Western regions like Jeddah, Mecca, and Medina, have further boosted consumption. The Western region, known for its tourism and religious events, holds a significant share of the chocolate market. As Saudi Arabia moves toward 90% urbanisation by 2030, consumer preferences are shifting toward indulgent and high-quality products. This has encouraged both local and international players to diversify offerings in line with evolving tastes and health consciousness.

However, the market faces key challenges. Saudi Arabia relies heavily on imported cocoa and raw materials, making it vulnerable to global supply chain disruptions, price volatility,

INVESTMENTS

and trade restrictions. Additionally, a growing awareness of health concerns—particularly regarding sugar and fat—has led to increased demand for healthier options, such as sugarfree and organic chocolates.

While this shift presents opportunities, it also demands innovation, reformulation, and potentially higher production costs. Manufacturers unable to adapt risk losing ground in an increasingly competitive market. Despite these challenges, Saudi Arabia’s chocolate market remains robust, with cultural relevance, urban development, and premiumisation trends sustaining its momentum.

Printcare PLC opens advanced packaging plant in Nairobi

KENYA - Printcare PLC, a Sri Lankan company known for its packaging operations, has opened a new production plant in Nairobi, Kenya, as part of its continued global growth strategy. The facility, located in one of East Africa’s key trade hubs, is expected to serve industries including tea, textiles, horticulture, pharmaceuticals, and fast-moving consumer goods.

The launch event in Nairobi drew participation from company executives, government officials, local partners, and industry stakeholders. Printcare’s joint venture partner was also present during the opening ceremony.

The Nairobi plant is equipped to manufacture products

such as mono cartons, corrugated cartons, and paper bags. According to the company, the facility has been built to meet growing demand for environmentally friendly and highquality packaging solutions across the region. It incorporates energy-efficient technologies and uses sustainable materials in line with environmental compliance goals.

The investment reflects a shift in Printcare’s operations, which initially focused on packaging for the tea sector. The company now supplies packaging to a broader range of industries, including beverages, apparel, telecom, publishing, financial services, and pharmaceuticals. Nairobi’s strategic location allows Printcare to distribute products more efficiently across East Africa.

The choice of Nairobi as the location for this landmark facility is both strategic and symbolic. As East Africa’s commercial capital, Nairobi provides direct access to a vibrant and growing market, allowing Printcare to serve regional clients more efficiently with sustainable packaging solutions. Notably, Nairobi is also drawing other international packaging and supply chain players. Nexgen Packaging, a global supplier of garment trims and packaging solutions, recently established its African headquarters in the city. Nexgen’s plant joins its other African operations in Egypt and West Africa and is part of its US$10 million investment in the region.

Twiga Foods makes strategic logistical acquisitions

KENYA - Kenyan agri-tech firm Twiga Foods has bought majority shares in three regional distributors as part of its plan to grow its product range and extend its market coverage beyond fresh produce. The company announced the acquisition of Jumra in Nairobi, Sojpar in Kisumu, and Raisons in Mombasa. These distributors handle a mix of goods including food, drinks, household supplies, cosmetics, and stationery.

While Twiga did not reveal how much the deals cost, it confirmed that the move is aimed at building a stronger and more reliable distribution system. Jumra covers the Nairobi and Central Kenya regions, while Sojpar operates in the Western part of the country. Raisons focuses on the Coastal region.

Twiga will now be able to use these companies’ existing market knowledge and supply links to improve its service delivery, especially in areas it had exited earlier.“This strategic alignment underscores Twiga’s commitment to modernising Kenya’s food distribution landscape, combining these established distributors’ deep market knowledge, operational excellence, and cost-efficient practices with its advanced technology and analytics,” the firm said in a statement.

This new arrangement marks Twiga’s return to the Western region of Kenya. The company had started setting up there in 2021 but slowed down after a change in its business plan and a wave of staff cuts.With the latest move, Twiga aims to tap into a growing demand for digital platforms in food and grocery shopping.

Charles Ballard, who took over as CEO in January 2024, now leads the company following the exit of co-founder Peter Njonjo. Ballard, who previously worked with Jumia Kenya, steps in at a time when the company is trying to rebuild from a difficult phase marked by delayed payments and salary cuts.

LOGISTICS

Maersk opens new warehousing facility in Senegal

SENEGAL - Maersk has recently inaugurated a new 10,000 square metre warehouse in Dakar, Senegal, as part of its broader strategy to strengthen logistics infrastructure across West Africa. Located strategically between the Port of Dakar and the city’s industrial zone, the facility is within 10 kilometres of key transport arteries and commercial hubs—positioning it as a vital node for efficient domestic distribution and crossborder trade to neighbouring countries such as Mali, Guinea, and The Gambia.

The facility boasts 5,100 square metres of indoor storage and can accommodate over 7,000 pallets, with an additional 500 square metres of outdoor space. It is designed to manage a wide range of commodities, including electronics, fashion, retail items, and fast-moving consumer goods (FMCG). Customers can access value-added services such as order management, labelling, packaging, palletisation, and last-mile distribution under one roof.

Maersk’s Dakar warehouse also integrates advanced technology solutions, including a modern Warehouse Management System (WMS) and Electronic Data Interchange (EDI), which enable real-time inventory tracking and seamless communication with customer systems. This digital capability enhances operational efficiency and supply chain transparency, crucial for both multinational corporations and local enterprises.

Environmental sustainability is also a priority at the new facility. Solar panels generate up to 60% of the site’s energy needs, while electric material-handling equipment helps lower emissions. Safety remains paramount, with features such as forklift-mounted cameras, pedestrian detection systems, fire prevention infrastructure, and 24/7 monitoring in place.

This new warehouse adds to Maersk’s growing footprint in West Africa, where the company already operates logistics facilities in eight cities, covering a combined area of over 100,000 square metres. Each site adheres to Maersk’s global standards in health, safety, security, and environmental compliance, reinforcing its commitment to building resilient and sustainable supply chains in the region.

Nestlé Vietnam injects US$73M in factory expansion

VIETNAM - Nestle Vietnam, part of the Swiss multinational food and drink processing conglomerate, Nestle, has announced an additional investment of US$100 million to double the processing capacity of high-quality coffee lines at the Nestle Trị An factory in the southern province of Dong Nai. This additional investment brings the total investment capital at the Tri An factory to over US$500 million.

Binu Jacob, General Director of Nestle Vietnam, emphasized the long-term commitment of Nestlé to investing in Vietnam, stating, “The project is a testament to Nestle’s long-term investment commitment in Viet Nam. It is expected that when the project comes into operation, the factory’s capacity will be double, meeting the domestic market’s consumer demand and effectively exploiting the export potential, making Việt Nam a supply centre for high-quality coffee to the world.”

This additional investment aims to address the increasing demand for coffee, securing Vietnam’s position as a key player in high-quality coffee production and supply for both domestic and global markets.

Currently, products from the Nestle Trị An factory are exported to more than 29 countries and territories worldwide, and Nestle stands as the largest coffee purchasing company,

annually acquiring up to US$700 million worth of coffee from Vietnam.

In addition to increasing capacity, the factory continues to prioritize sustainability. Nestle said the site operates on clean energy and uses biomass derived from coffee waste. These measures reportedly help the company cut down carbon emissions by over 14,000 tonnes per year. Recycled wastewater from the coffee production process is also reused in the boilers, saving more than 112,000 cubic meters of water annually.

PepsiCo phases out its artificial ingredients to meet consumer preferences

USA – PepsiCo, a global leader in the food and beverage industry, announced that it has already been phasing out artificial colours and reducing other ingredients in its products to meet consumer preferences.

During a conference call with analysts on PepsiCo’s fiscal 2025 first-quarter results, Ramon Laguarta, CEO of PepsiCo, mentioned that the company has been at the forefront of transforming the industry by focusing on reducing sodium,

sugar, and using healthier fats. “We’ve been leading the transformation of the industry now for a long time on sodium reduction, sugar reduction and better fats,” Laguarta said, adding that 60% of the company’s food business does not have any artificial colours, so they were undergoing that transition.

“For example, brands like Lay’s will be out of artificial colors by the end of this year, and the same with Tostitos — some of our big brands. So we’re well underway,” he added. The company emphasised confidence in the scientific safety of their products, while acknowledging the growing consumer interest in natural ingredients.

Laguarta said, “We’ll lead that transition, and in the next couple of years, we’ll have migrated all the portfolio into natural colours or at least provide the consumer with natural colour options. And every consumer will have the opportunity to choose what they prefer. So that’s the journey we’re undergoing.” The news comes after Robert F. Kennedy Jr., secretary of the USA Department of Health and Human Services, and Marty Makary, commissioner of the Food and Drug Administration, launched measures to eliminate all petroleum-based synthetic dyes from the US food supply and steer food companies to natural alternatives.

FOOD SAFETY & QUALITY

EGYPT - SIG, a provider of packaging solutions, is working with Plastic Bank, Carta Misr, and TileGreen to introduce what is being described as Egypt’s first end-to-end recycling model for aseptic beverage cartons. The initiative, launched amid the absence of an organized recycling structure in the country, is designed to handle the entire recycling chain— from waste collection to the production of reusable materials. The collaboration aims to convert discarded beverage cartons into products with practical use, targeting improved waste management and material recovery.

Plastic Bank is managing the collection stage using a blockchain-based system that tracks each carton collected. This digital platform records transactions in real time and enables collectors to earn income by exchanging recyclable waste for value, making the process transparent and measurable.

Following collection, the cartons are delivered to Carta Misr, a paper mill in Egypt that processes them by separating the paper fibers from the aluminum and polyethylene layers. The extracted paper is then used to manufacture recycled paper goods.

The non-paper portion, made up of aluminum and polymer known as PolyAl, is sent to TileGreen. The Cairo-based startup repurposes this material into long-lasting construction bricks using its proprietary technology. These bricks are marketed as a greener option for the local building industry. According to SIG, the system is intended to divert waste from landfill sites and provide economic opportunities for those involved in the recycling process. The partners say the project may serve as a template for similar industry-led waste management efforts in the region.

The grand opening celebration, held on April 25, 2025, was attended by Dominik Santner, CEO of Anton Paar GmbH, along with a delegation from the Austrian Federal Economic Chamber’s trade promotion group, Advantage Austria. SIG partners with local firms to establish Egypt’s first recycling system for beverage cartons

UK FSA releases preliminary foodborne disease attribution data

UK - The Food Standards Agency (FSA) is currently analysing how specific pathogens contribute to foodborne illnesses in the UK, drawing on early results from its ongoing “Disease Attribution to Foods for Four UK Pathogens” project. The data stems from the third Intestinal Infectious Disease survey (IID3), commissioned in 2021 to assess the scale of infections, pinpoint causes, and estimate underreporting of cases. The survey is collecting data between September 2023 and August 2025.

This research aims to revise previous figures from 2018, which estimated around 2.4 million food-related illnesses occur in the UK each year. So far, the survey has frequently identified Campylobacter, norovirus, diarrheagenic Escherichia coli (DEC), sapovirus, and toxin-producing Clostridium perfringens. However, the current report focuses specifically on enteropathogenic Escherichia coli (EPEC), sapovirus, hepatitis A virus (HAV), and Toxoplasma gondii.

The findings revealed that EPEC had the highest foodattributable portion, at 64%, followed by T. gondii (results ranging from 28% to 61%), HAV (10% to 42%), and sapovirus (13% to 16%). As only one study was recovered for EPEC, results for grouped diarrheagenic E. coli (DEC) pathotypes, not including Shiga toxin-producing E. coli (STEC), were also included. These suggest that between 25% and 55% of DEC disease could be attributed to foods.

Other studies that apportion foodborne disease to individual food groups attributed fresh produce as the most common foodborne transmission pathway for HAV, with estimates ranging from 45% to 95.4%, and for sapovirus, 58.3%. Sapovirus transmission was mainly attributed to meat and poultry (20.4–50% across models) compared to leafy greens (0–12.4%).

Meanwhile, pork was suggested as a more significant transmission pathway for T. gondii, with a transmission rate ranging from 20% to 41%. Among beef, pork, and poultry, the majority of T. gondii infections were suggested to be derived from non-ready-to-eat (NRTE) minced products.

GOVT REGULATIONS

Kenya moves to lease four sugar factories

KENYA - The Kenyan government’s plan to lease four stateowned sugar factories, Nzoia, Chemilil, Muhoroni, and Sony, has garnered conditional support from key stakeholders, including the Kenya National Federation of Sugarcane Farmers and the Kenya Union of Sugar Plantation and Allied Workers (KUSPAWU). Agriculture Cabinet Secretary Mutahi Kagwe has emphasized that the leasing process will proceed only after addressing all outstanding issues affecting farmers and workers, including the clearance of salary arrears and supplier debts.

However, KUSPAWU has threatened legal action to halt the leasing process unless the government settles over KES 4.7 billion (US$ 36 million) in unpaid salaries and remits KES 10 million (US$ 77,000) in deductions withheld from workers’ pay.

The union insists on having representation on the leasing committee to safeguard workers' interests and ensure that existing Collective Bargaining Agreements are upheld during the transition.

In a significant development, the High Court dismissed a petition challenging the leasing initiative, ruling that adequate public participation had been conducted and that the process complied with the Public Private Partnership Act. This decision clears a major legal hurdle, allowing the government to proceed with the leasing plan aimed at revitalizing the sugar sector through private investment and improved management.

The government has also approved a KES117 billion (US$ 900M) bailout package to clear debts of six state-owned sugar factories, including the four slated for leasing. This financial injection is intended to ensure that the factories are handed over to new investors with clean balance sheets, thereby enhancing their attractiveness to potential lessees.

To further support the sector's revival, the Ministry of Agriculture has finalized new regulations under the Sugar Act 2024, which include the establishment of a unified farmer apex body and measures to regulate sugar imports. These reforms aim to create a more sustainable and competitive sugar industry that benefits all stakeholders.

LIBERIA - Liberia has launched a US$300,000 cold storage facility in Whenlenle, Nimba County, to combat post-harvest losses that affect 30–40% of vegetable yields due to poor handling and lack of refrigeration. Funded by the World Bank and developed through the Ministry of Agriculture’s Rural Economic Transformation Project (RETRAP), the new unit offers 77 cubic meters of cold storage and is designed to improve market access, food quality, and farmer incomes.

The facility, built from a 40-foot container and powered by a 15kVA solar system with a 20kVA generator backup, sits along the key Ganta–Monrovia Highway. Its strategic location enables farmers to preserve perishable produce like tomatoes and mangoes—often lost at rates of 25–35%—before reaching markets. A newly introduced transport van, with a four-ton capacity, will further support vegetable delivery.

RETRAP National Program Coordinator Gala Toto said the project was inspired by the sight of farmers laboring overnight to load fresh cabbages for market. “Why not support them by providing cold storage?” he reflected.

During the opening, Assistant Agriculture Minister Folton Blasin urged farmers to take ownership of the facility, stressing that its success depends on community stewardship. Local

INVESTMENTS

cooperative leaders echoed this sentiment. Ezekiel Sayetee, chairman of the Say No to Hunger Farmers Multipurpose Cooperative Society, called the facility a “much-needed solution” for villages from Nengbein to Beila.

The Ministry views this as a model for future investments to reduce crop losses and improve food security. With the facility now operational, Nimba farmers are better equipped to deliver fresh produce efficiently and profitably.

Coca-Cola Beverages Malawi invests US$14.9M in new production line

MALAWI - Coca-Cola Beverages Malawi Limited (CCBM), a subsidiary of Coca-Cola Beverages Africa (CCBA), has commissioned a new beverage production line at its Lilongwe facility as part of its expansion efforts. In a press release issued on Thursday, April 17, the company confirmed that the project cost US$14.9 million. The new line boosts the plant’s output by 19,200 bottles per hour, handling packaging sizes from 300 milliliters to 2 liters.

Company representatives indicated that the additional capacity is expected to ease product availability within Malawi while enabling the company to expand its export operations into neighboring Zambia. CCBA stated that the investment aligns with its regional approach of manufacturing and sourcing locally, adding that it reflects its outlook on the Malawian economy.

This development comes as the soft drinks market in Southern Africa records strong growth forecasts. According to Statista, projected revenue for Malawi's market is expected to reach US$437.3 million in 2025, while Zambia’s market is projected to hit US$342.6 million in the same year. Both countries are anticipated to see annual growth rates above 8% through 2029.

Still, CCBA will face pressure from both domestic brands and international competitors, including PepsiCo, which remains active in the region. The Lilongwe project adds to CCBA’s broader investment drive across Africa. In July 2024, it launched a US$27 million plant in Uganda, followed by a facility upgrade in Namibia in November 2024. In Kenya, the company has committed up to US$175 million over five years.

Mohammed Khalid Alakeel appointed CEO of Deemah

SAUDI ARABIA – United Food Industries Corporation (Deemah), one of Saudi Arabia’s largest manufacturers of biscuits, confectionery, and snacks, has appointed Mohammed Khalid Alakeel as Chief Executive Officer.

The appointment is part of a strategic leadership transition as Deemah positions itself for continued growth and international expansion. Abdul Aziz Alakeel, Founder and long-standing CEO, will remain as the Chairman of the Board of Directors.

Mohammed Alakeel began his career at Deemah as a management trainee. He rose through the ranks to lead shared services, where he was in charge of human resources and information technology.

As Chief Sales and Marketing Officer since 2019, he has spearheaded initiatives that have revolutionised the company’s distribution, sales, and marketing strategies, elevating Deemah’s position in the market.

Under Mohammed’s leadership, Deemah will prioritise investment in R&D to introduce innovative products that cater to evolving consumer preferences and increase production lines.

The company will also focus on the core business categories, such as biscuits and cakes, while expanding its presence in high-growth products, such as snacks.

John M. Lamola appointed as South African Airways

Group CEO

AFRICA

– South African Airways (SAA) has appointed John M. Lamola as its Group Chief Executive Officer.

Lamola, who has served as interim CEO since May 2022, is well-versed in the airline’s challenges and future direction.

The airline’s Board has credited Lamola with guiding SAA through a financial recovery, ensuring its continued presence as a key player in regional and international aviation.

“The SAA Board is delighted to be able to appoint a solid and dedicated leader well versed in SAA’s fortunes and eager to continue overseeing its take-off into better skies. We wish Professor Lamola and SAA safe flight into an even brighter future,” said the Board.

Under Lamola’s leadership, SAA returned to profitability, reporting a net profit of R252 million (US$13.61 million) in the 2022/23 financial year. The airline’s revenue also grew significantly, reaching R5.7 billion (US$307.8 million), a notable increase from R2 billion (US$108 million) in the previous year.

Unilever Ethiopia appoints Nesibu Temesgen as its new GM

ETHIOPIA – Unilever Ethiopia has appointed Nesibu Temesgen as its new General Manager effective April 1, 2025.

Nesibu replaces George Ansah, who contributed 30 years of global leadership experience to Unilever Ethiopia.

Ansah focused on accelerating growth, nurturing local talent, and positively impacting the communities served.

Nesibu becomes the first Ethiopian national to lead the British multinational fast-moving consumer goods company in the region, bringing over 18 years of experience in the industry.

He has spent nine years at Unilever Ethiopia, most recently serving as a director leading its customer development operations. In this role, he was credited with consolidating the company’s sales and marketing position.

Previously, he held successive management roles at Unilever Ethiopia, Heineken Ethiopia, and Tiger Brands East Africa.

He holds undergraduate and postgraduate degrees in marketing management from Addis Abeba University.

Diageo appoints Hina Nagarajan as President of Africa

AFRICA – Diageo has appointed Hina Nagarajan as the new President of Diageo Africa, effective April 1, 2025.

Nagarajan, who recently transitioned from her role as MD and CEO of Diageo India to a position on Diageo’s Global Executive Committee, will return to the African market, where she previously served as Managing Director of Africa Emerging Markets for the company.

Nagarajan’s move follows her departure from Diageo India earlier this year, where she was succeeded by Praveen Someshwar after nearly four years at the helm.

Before joining Diageo, Nagarajan held key leadership roles, including Senior Vice-President, Regional Director North Asia at Reckitt.

Nagarajan replaces Dayalan Nayager who served as President of Diageo Africa since July 2022.

Nayager assumes the role of President of Diageo Europe, succeeding John Kennedy. He will retain his responsibilities as Diageo’s Chief Commercial Officer.

Over the last 12 years, he has led Diageo’s businesses in Great Britain, Ireland, and France, as well as its Global Travel Retail division.

Andy Osei Okrah appointed acting CEO of Ghana’s TCDA

GHANA – Ghana’s President John Dramani Mahama has appointed Andy Osei Okrah as the Acting Chief Executive Officer of the Tree Crops Development Authority (TCDA).

Okrah previously served as the Director of Human Resources at the Forestry Commission.

“Ghana’s tree crops sector holds immense potential to transform lives, create jobs, and significantly boost our national economy. From cashew to shea, mango to coconut, rubber to oil palm—these crops are a treasure trove of opportunities waiting to be fully harnessed,” Okrah stated.

Established by the Tree Crops Development Authority Act 2019 (Act 1010), TCDA is tasked with regulating and developing the production, processing, and trading of six key tree crops: cashew, shea, mango, coconut, rubber, and oil palm.

The authority plays a crucial role in promoting sustainable agricultural practices and increasing the value chain of these crops.

Okrah outlined plans to work closely with farmers, processors, traders, exporters, and donors to address industry challenges and foster an enabling environment for growth.

Heineken appoints Guillaume Duverdier as President for MEA

MEA – Heineken N.V. has named Guillaume Duverdier as Regional President for Africa Middle East (AME), effective 1 July 2025.

He will also join the Heineken Executive Team.

Duverdier succeeds Roland Pirmez, who is retiring after nearly three decades with the company, including ten years as Regional President AME

Guillaume, currently Managing Director of Heineken México, joined the company in 2000 and has held senior roles across diverse markets.

Throughout his 25-year tenure, Guillaume has consistently delivered strong business results across a range of market types and complexities. He is recognized for his commercial leadership and strategic execution.

In his recent role as MD of Heineken Mexico, he expanded the company’s retail chain, Six, which now comprises 17,000 stores and serves as a pillar of Heineken México’s market strategy.

He also championed digital transformation in sales and oversaw the launch of the Meoqui Can Factory, Heineken’s first can production facility, supporting vertical integration and operational efficiency.

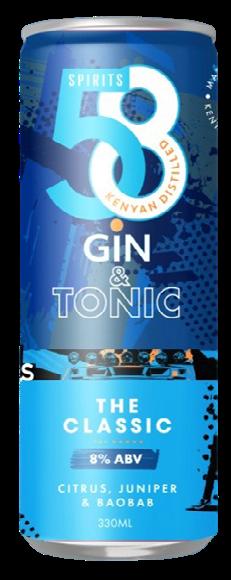

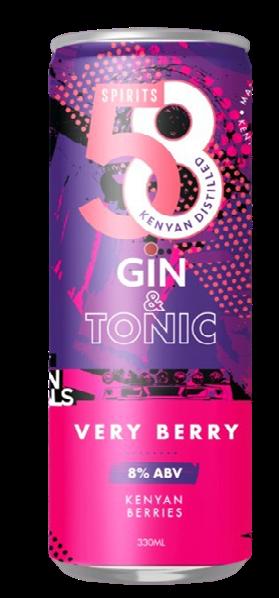

AFRICAN ORIGINALS

5.8 Gin & Tonic

African Originals has expanded its gin portfolio with the official launch of the new range of Ready-to-Drink (RTD) beverages, 5.8 Gin & Tonic.

The 5.8 Gin & Tonic additions come in three distinct flavours: Spiced Orange, The Classic, and Very Berry.

The RTD drinks come in 330 ml can format, each containing 5% alcohol by volume.

www.africanoriginals.com

KENYA BREWERIES LIMITED

Manyatta Pineapple & Mint can

COCA-COLA

Sprite Lemon & Mint

Coca-Cola has introduced two new flavor variants under its Sprite brand in the Gulf region—Sprite Lemon & Mint in the United Arab Emirates and Sprite Citrus & Mint in Saudi Arabia.

The launch marks a strategic expansion aimed at aligning with consumer preferences for citrus-mint beverages that are deeply rooted in local traditions.

“With the introduction of Sprite Lemon & Mint in the UAE and Sprite Citrus & Mint in KSA, we are creating a beverage experience that feels both familiar and exciting,” said Tarek Metwally, Marketing Lead for Sprite Middle East.

www.coca-cola.com/xf/en

Kenya Breweries Ltd (KBL) has introduced its Manyatta Pineapple and Mint cider brand in cans.

The brand will now be available in 330ml aluminium cans and will be distributed nationwide.

Manyatta was originally launched in December 2023 in glass bottles and comes in classic cider, pineapple and mint, lemon and ginger, and mango and ginger flavours.

www.eabl.com

HOLLAND DAIRY

Holland Banana Yoghurt

Holland Dairy has expanded its yoghurt portfolio with the launch of a new flavour; Banana Yoghurt made with authentic Ethiopian bananas.

According to Jean-Paul Rieu, the company’s managing director, the yoghurt is crafted to offer a creamy texture with a natural sweetness, free from artificial flavors, which aligns with growing consumer demand for healthier, authentic food options.

www.holland-dairy.com

BIGTREE BEVERAGES

FIT

BigTree Beverages Ltd has expanded its portfolio with the launch of a new sports drink dubbed ‘FIT’.

The sports drink, crafted in partnership with Vatra is aimed at enhancing the fitness journey for athletes and enthusiasts across Zambia.

Crafted for optimal hydration and replenishment, FIT features a balanced mix of carbohydrates, nutritional minerals, and electrolytes, with a carefully calibrated sugar content to support peak performance.

www.bigtreebev.com

WAMBUGU APPLES

freeze-dried fruits

The Kenyan-based firm, Wambugu Apples , moves into the healthy snack market with a new line of freeze-dried fruits made from 100% Kenyan produce.

“This is a natural evolution of our vision,” said Mr. Wambugu, the company’s Director. “We started Wambugu Apples to introduce a variety that thrives in tropical climates and empowers farmers. But we knew that to fully bring out the potential of this apple, we had to go beyond fresh fruit.”

www.wambuguapples.co.ke

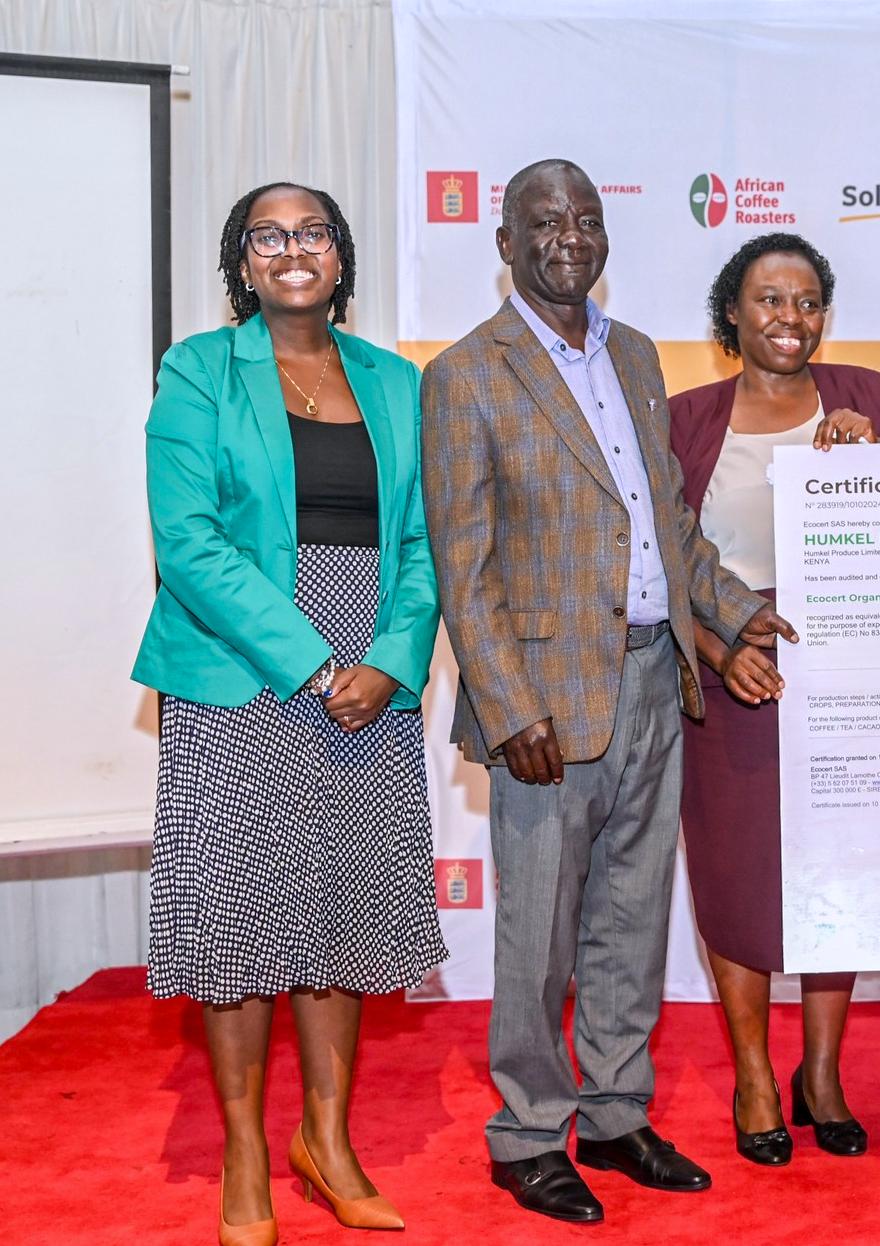

The push towards organiccertified coffee

in Kenya

By Francis Watari

Kenya is renowned for its high-quality coffee, characterized by rich flavors, bright acidity, and aromatic profiles that captivate coffee enthusiasts worldwide. However, as consumer preferences shift toward sustainability, organic certification has become a crucial milestone for coffee farmers seeking to meet global market demands. The transition to organic-certified coffee is not merely a change in farming practices but a rigorous process that requires dedication, financial investment, and adherence to strict international standards. The transition is filled with challenges, achievements, and a promise of a more sustainable and profitable future for Kenyan coffee farmers.

UNDERSTANDING ORGANIC COFFEE CERTIFICATION

Organic certification is a validation process that ensures coffee is grown without synthetic fertilizers, pesticides, or genetically modified organisms (GMOs). Instead, it relies on sustainable farming techniques such as composting, natural pest control, and agroforestry to enhance soil fertility and ecosystem balance. Certification is awarded by accredited bodies such as Africert and Ecocert, which evaluate farms based on compliance with international organic standards, including those set by the European Union, the United States Department of Agriculture (USDA), and Fairtrade organizations.

The certification process typically spans three years, during which farmers must phase out conventional farming inputs and adopt organic practices. This transition period is critical for detoxifying the soil and ensuring crops meet organic requirements. Pius Mutay, Director at Hemkel Produce Ltd, highlighted, "Switching to organic coffee was not easy. It required patience and a willingness to embrace new farming methods, but we knew the rewards would be worth it."

CHALLENGES ON THE ROAD TO CERTIFICATION

Despite the growing demand for organic coffee, the journey to certification is filled with challenges. One of the primary hurdles is the financial cost associated with transitioning to organic farming. Many smallholder farmers struggle to afford organic inputs, certification fees, and training programs. "The initial investment is overwhelming," noted Peter Koech, CEO of Kapkiyai Multi-Purpose Cooperative Society in Nandi County. "Most farmers need external support to make this transition feasible."

Another significant challenge is the risk of reduced yields during the conversion period. Without synthetic fertilizers and chemical pesticides, farmers often experience a temporary drop in productivity as the soil adjusts to organic farming methods. Additionally, knowledge gaps hinder the adoption of organic practices, as many farmers lack access to adequate training and technical assistance. "Organic farming requires a different mindset," noted Rachael Wanyoike, Managing Director at Solidaridad. "Farmers must learn new ways to manage pests, soil fertility, and coffee diseases without relying on conventional chemicals." Synthetic pesticides and fertilizers are replaced with natural alternatives; a shift made more difficult by the scarcity and high cost of organic inputs. The risk of glyphosate contamination from neighboring plots looms large, as it can jeopardize an entire cooperative’s certification. Smallholders, often managing just a few hundred coffee bushes, struggle to create buffer zones without sacrificing precious production.

Further, climate change adds another layer of complexity. Prolonged droughts deplete yields, and erratic rainfall disrupts coffee flowering cycles. The national average production per tree hovers around two kilograms, a mere fraction of the potential 30 kilograms per tree. Access to quality planting materials is also limited, and the Coffee Research Institute struggles to meet the demand for disease-resistant seedlings. “We have a big challenge in regards to access to quality planting materials, and that is because the Coffee Research Institute that is mandated to

provide this does not have the muscle to meet the growing demand in the country, so the much they are able to provide is not able to satisfy all the farmers, and it becomes a challenge because farmers are still planting the older varieties that are vulnerable to diseases can pass. Each eventually affects the productivity,” noted Betty Musembi, Senior Project Manager for Solidaridad ECA.

CULTIVATING CHANGE: THE TRACE KENYA JOURNEY

Recognizing these challenges, various organizations have stepped in to support Kenyan coffee farmers on their journey to organic certification. The Trace Kenya project has been a game-changer for smallholder coffee farmers in Kenya. The initiative has over the last five years and three months, from January 2020 to March 2025, transformed the coffee industry culminating with the launch of Kenya’s first certified organic coffee. This represents the culmination of years of hard work, resilience, and innovation. The Trace Kenya Project has empowered over 15,000 smallholder farmers in Kericho, Nandi, and Bungoma counties by promoting sustainable agricultural practices and offered technical guidance to facilitate the transition to organic coffee farming.

At the heart of this transformation is African Coffee Roasters (ACR), which has played a pivotal role in reshaping Kenya's coffee sector. ACR has not only facilitated the roasting, packaging, and marketing of Kenyan coffee but also developed a model that ensures nearly 60% of the coffee’s value stays within East Africa. This stands in stark contrast to the global norm where producing countries retain less than 10% of the total value. ACR’s commitment to sustainability has extended beyond production to include the development of carbon-negative coffee, aligning with the growing global demand for eco-friendly products. This focus on both quality and environmental responsibility is helping Kenya carve out a place for itself in the competitive organic coffee market.

Solidaridad East and Central Africa has also been integral to the success of the initiative, providing crucial technical expertise, guiding farmers through the

BEYOND FINANCIAL GAINS, ORGANIC FARMING CONTRIBUTES TO

ENVIRONMENTAL CONSERVATION AND IMPROVED SOIL HEALTH BY ELIMINATING CHEMICAL INPUTS.

transition to organic practices. The organization’s support has been key in ensuring that farmers not only meet the strict organic standards required for certification but also implement practices that improve long-term sustainability. Solidaridad’s work is rooted in community engagement, ensuring that farmers receive hands-on training and continued support throughout their organic transition.

The collaboration with Rabobank has introduced an innovative approach to sustainability through carbon farming, enabling farmers to earn income from sequestering carbon in the soil. “A farmer earned Kes 58,000 (US$448.81) from the sale of Carbon Removal Units (CRU’s,” noted Koech, CEO Kapkiyai Multi-Purpose Cooperative Society. This partnership has provided farmers with an additional financial incentive to adopt organic farming methods while contributing to the global

future for our farms and communities," emphasized Hon. Stephen Sang, Governor of Nandi County.

effort to mitigate climate change. Rabobank’s involvement marks a significant milestone, creating new opportunities for smallholder coffee growers in Africa.

Finally, DANIDA, the Danish International Development Agency, has further contributed to this mission by funding projects that enhance organic coffee farming in Kenya. Through capacity-building initiatives, DANIDA has helped bridge knowledge gaps and equipped farmers with the tools necessary for successful organic certification.

ACHIEVEMENTS AND MARKET OPPORTUNITIES

While the journey to organic certification presents numerous challenges, it also brings significant rewards. Certified organic coffee commands premium prices in global markets, offering farmers better income opportunities compared to conventional coffee. "Since we became certified, our coffee fetches higher prices, and buyers seek us out for our quality and commitment to sustainability," shared Koech.

Beyond financial gains, organic farming contributes to environmental conservation and improved soil health. By eliminating chemical inputs, farmers reduce pollution and enhance biodiversity on their farms. The integration of shade trees, for instance, creates a balanced ecosystem that supports beneficial insects and birds while protecting coffee plants from extreme weather conditions. "Organic coffee farming is not just about selling at a higher price; it is about ensuring a better

The demand for organic coffee continues to rise, particularly in Europe and North America, where consumers are increasingly conscious of ethical and environmental considerations. Kenyan farmers who achieve certification can access these lucrative markets and build long-term relationships with specialty coffee buyers. However, sustaining certification requires continuous effort, as annual inspections and compliance with organic standards remain mandatory. "Organic certification is not a one-time achievement—it is an ongoing commitment to sustainable farming," remarked a certification officer.

LOOKING TO THE FUTURE

The journey to organic-certified coffee in Kenya is still evolving, with more farmers recognizing the benefits of sustainable practices. As awareness grows, increased support from government agencies, development partners, and private sector players will be crucial in scaling organic coffee production. Policy interventions, including subsidies for organic inputs and streamlined certification processes, could further ease the burden on smallholder farmers.

Ultimately, organic certification is more than a market requirement—it is a step toward building a resilient coffee industry that aligns with global sustainability goals. By embracing organic farming, Kenyan coffee producers not only secure better livelihoods but also contribute to environmental conservation and the long-term prosperity of the industry. "The future of Kenyan coffee is organic," concluded a coffee expert. "With the right support and determination, we can make it a reality." FBMEA

The Zambian Food Industry: A Sector at Crossroads with Untapped Potential

By Nicholas Ng'ang'a

According to statistical data sourced from ZamStats, the food industry makes a notable contribution of approximately 15.4% to Zambia's overall Gross Domestic Product (GDP). Furthermore, it is a significant employer, accounting for 51.1% of the nation's total employment figures. Looking back at the period between 2010 and 2019, Zambia experienced an average annual economic growth rate of 4.8%. It's noteworthy that the majority of this economic expansion occurred during the earlier years of the decade, indicating a fluctuating growth pattern.

AN OVERVIEW OF ZAMBIA'S FOOD INDUSTRY LANDSCAPE Zambia's agriculture sector is dominated by smallholder

farmers and heavily reliant on maize, the country's dietary staple. Despite significant agricultural potential, much of Zambia’s arable land remains underutilized. A recent IPC Acute Food Insecurity Analysis reported a 22.9% rise in maize production for the 2023/2024 consumption period, increasing from 2.65 million metric tonnes to 3.26 million metric tonnes. This surge reinforces maize’s central role in both food security and the broader economy.

Soybeans have emerged as Zambia’s second-largest crop, underpinning the nation’s push towards agricultural diversification. In the 2023/2024 season, Zambia produced 475,000 metric tonnes of soybeans, as well as 295,000 metric tonnes of soybean meal and 70,000 metric tonnes of soybean oil. This positions Zambia as the second-largest soybean

producer in Southern Africa, following South Africa, and highlights its growing capabilities in crop processing and value addition.

Livestock farming also plays a critical role in Zambia’s agricultural landscape. The 2023 Livestock Survey Report from the Ministry of Fisheries and Livestock revealed that around 1.87 million households are engaged in various livestock activities.

THE ASCENT OF AGRO-PROCESSING IN ZAMBIA

Milling Industry: The Backbone of Zambia's Food System

The milling sector stands as Zambia’s largest food processing industry, playing a critical role in national food security and economic stability. This prominence stems from the country’s heavy dependence on maize, with maize meal being the staple food for most Zambians. According to the IPC Acute Food Insecurity Analysis, the 2022/2023 season saw a sharp increase in maize production, driven by a rise in farming households—from 1,756,340 to 2,534,311. This expansion led to a greater area under cultivation, especially for maize. Including a carry-over stock of 450,891 metric tonnes, Zambia began the consumption year with a total maize stock of 3,712,576 metric tonnes.

The milling industry is made up of both large-scale processors and numerous small and medium-sized enterprises (SMEs), engaged in processing maize, wheat, and other grains into flour and related products. This strategic importance has drawn both local and foreign investment. In March 2025, Roff Milling, a South African firm with over 30 years in the industry, launched a new branch in Kitwe, Zambia. Officially inaugurated on March 13, the facility aims to enhance access to advanced milling equipment for local farmers and processors across Zambia and neighboring maize-producing countries.

Government support, particularly through the Food Reserve Agency (FRA), has further bolstered the sector by ensuring a reliable market for surplus maize, especially from smallholder millers, during challenging periods such as droughts or market disruptions

POULTRY REMAINS THE MOST CONSUMED MEAT IN THE COUNTRY, WITH PRODUCTION PROJECTED TO RISE TO 51,150 METRIC TONNES BY 2026.

The Food Reserve Agency (FRA) plays a stabilizing role by purchasing surplus maize from smallholder farmers, especially in underserved regions. It helps maintain price stability and food availability by selling the grain to millers and other stakeholders.

Meat and Poultry

Zambia’s meat and poultry processing industry has experienced steady growth, driven by increasing urbanisation, a growing middle class, and rising local demand for convenient and highquality protein options. Poultry remains the most consumed meat in the country, with production projected to rise modestly from 50,000 metric tonnes in 2021 to 51,150 metric tonnes by 2026. Between 2017 and 2023, poultry output recorded an average annual increase of 0.4%, with production reaching 50,992 tonnes in 2023—a 0.97% rise from the previous year.

The broiler sector alone produces around 93 million birds annually, though further investment is needed to boost processed poultry output. Industry expansion has been supported by both public policy and significant private sector investment. Zambeef, a key industry player, slaughters 60,000 cattle per year, processes 90,000 hides, and operates five abattoirs and three feedlots with a 24,000-cattle capacity.

IN NUMBERS

LITRES OF MILK PROCESSED FORMALLY

Other major contributors to the sector include RMA Group, Kachema Meat, and Lubona Meat Products Ltd, which have invested in technology and workforce development to enhance production capacity and standards. The government has supported industry growth through policy measures such as a 2020 hike in import duties—from 25% to 40%—on meat and processed meat products from outside SADC and COMESA regions, aiming to encourage local processing. Further regulatory steps have focused on improving animal health and disease control to support sustainable sector development.

Beverage Industry

The beverage sector is also a dominant force in the food industry in Zambia, demonstrating strong growth prospects across both alcoholic and non-alcoholic categories. Beer remains the leading alcoholic drink, while Coca-Cola maintains a dominant position in the carbonated soft drink market. Projections for 2025 indicate

that revenue from at-home consumption of non-alcoholic beverages is expected to reach approximately US$635.97 million, with the total revenue for non-alcoholic drinks estimated at US$668.91 million. In the same year, the athome segment of the alcoholic drinks market is anticipated to generate US$779 million, according to Statista.

Zambian Breweries, founded in 1968 and now a subsidiary of AB InBev, holds a market share exceeding 95%, making it the largest brewing company in the country. It operates significant production facilities in Lusaka and Ndola. The company’s portfolio includes internationally recognised brands such as Budweiser, Corona, and Stella Artois, as well as locally popular beers like Mosi, Eagle, and Castle. Mosi is regarded as a national favourite, while Eagle, introduced in 2017, is brewed using locally sourced cassava, supporting Zambia’s agricultural development.

Reports from 2023 indicated that the country brought in a range of alcoholic beverages, with whiskies accounting for the highest proportion at 35% of the total import value, followed by gin and Geneva at 22%, and liqueurs and cordials at 19.7%. The respective import values stood at US$1.61 million for whiskies, US$1.02 million for gin and Geneva, and US$890 thousand for liqueurs and cordials. To combat the competition, Zambian Breweries is focusing on innovation and product diversification.

Dairy Sector: Promising But Underdeveloped Zambia’s dairy industry is on a growth trajectory, projected to become the world’s 94th largest milk producer by 2026, with production expected to reach 492,070 metric tonnes, a 1.1% increase from 2021 and a significant leap from 1966 levels1. Revenue in the milk market is forecast to hit $132.86 million in 2025, with a robust compound annual growth rate of 9% anticipated between 2025 and 2030. However, only a fraction of the roughly 600 million litres of milk produced annually is processed formally, with the majority handled informally, highlighting a key challenge in processing capacity.

Major industry players include Dairy Gold, Parmalat Zambia Limited, Zambeef Products PLC, and Lactalis Zambia. Zambeef operates one of the largest facilities, while Parmalat and Finta, the top processors, are utilizing less than 65% of their capacity due to supply constraints. In early 2025, Lactalis announced it would close its Zambian factory, citing increased competition from lower-cost local brands and government

policies favoring domestic production, shifting to an import model from South Africa.

The Dairy Association of Zambia has advocated for higher import tariffs and subsidies to protect local producers and promote domestic consumption. Despite the sector’s promise, challenges remain, including infrastructure gaps, limited disease control, and a need for more purebred cows. Continued investment, policy support, and improved supply chains are seen as vital for sustaining growth and meeting rising consumer demand.

CHALLENGES IN ZAMBIA’S AGRI-FOOD SECTOR

The Zambian food and agriculture sector continues to grapple with recurring challenges that impact productivity and food security. Factors such as climate change and ineffective policy implementation have repeatedly hindered progress. A recent and pressing issue has been the ongoing drought, which has led to the loss of 1.5 million metric tonnes of grain, driving up food prices and making maize increasingly unaffordable for lowincome households. According to ACAPS, the food insecurity situation in Zambia was expected to worsen between October 2024 and March 2025 due to insufficient rainfall during the 2023–2024 agricultural season, resulting in lower crop yields and higher food costs.

The industry has also been affected by minor challenges such as power shortages and food safety issues. Load shedding has significantly disrupted agricultural operations, particularly in the poultry sector. For example, in May 2024, the Poultry Association of Zambia highlighted the severe impact of power outages on production and business activities. Small-scale farmers reliant on electricity for incubation and lighting were struggling to sustain their operations due to the high cost of alternative energy sources. Food safety has also been a major concern, with aflatoxin contamination affecting maize flour exports. In 2024, the Democratic Republic of Congo had to suspend imports from several Zambian milling companies

due to contamination.

Food safety issues, especially aflatoxin contamination in maize flour, have hurt exports. In 2024, the Democratic Republic of Congo banned imports from several Zambian millers due to contamination concerns.

GOVERNMENT POLICIES IN MITIGATING CHALLENGES

The Zambian government has actively worked to address both natural and human-made challenges affecting the agricultural sector. To support agro-processing, it encourages private sector participation through initiatives like the Zambia National Agricultural Policy 2012-2030. This policy aims to develop a competitive and diverse agricultural sector by promoting sustainable and equitable growth. It focuses on increasing agricultural productivity in crops with a comparative advantage, improving input and product markets to lower costs and enhance agribusiness profitability, and expanding agricultural exports to maximize the benefits of preferential trade agreements and boost foreign exchange earnings.

Another significant challenge facing Zambia’s agricultural sector is drought. In response, the government implemented the Food Security Pack (FSP), introduced in November 2000 as a social safety net. This program targets vulnerable yet capable farming households that have suffered productivity losses due to adverse climatic conditions and economic restructuring policies. The FSP consists of three main components: Rainfed Cropping, Wetland Cropping, and the Alternative Livelihood Initiative (ALI). Under the Rainfed Cropping program, selected farmers receive a package containing fertilizers (Compound D and Urea) and seeds for cereal and legume cultivation, covering approximately three limas (three-quarters of a hectare) for two consecutive rainy seasons before participants transition out of the program. Similarly, the Wetland Cropping program provides beneficiary households with fertilizers and cereal and vegetable seeds to cultivate one lima during winter, also for two consecutive seasons. The government is also investing in irrigation infrastructure to mitigate the impact of drought.

The Shift Toward Port Privatization in Africa:

Balancing Efficiency, Sovereignty, and Investment

By Fridah Chepkoech

There’s much to say about the intersection of efficiency, sovereignty, and investment in Africa’s port sector, but the challenge lies in finding a balance that drives growth while preserving national interests. In July 2024, the African Development Bank (AfDB) hosted a workshop on the African Ports Connectivity Portal Project (APC-PP), a US$2 million initiative to digitize port data, enhance performance tracking, and slash logistics costs. While this vision holds great promise, one undeniable fact remains: many African ports face ongoing challenges with outdated equipment, inefficiency, and excessive handling costs, which, according to AfDB, are 50% higher than global standards.

To address these issues, African nations are increasingly embracing private sector involvement in port management. Privatization ranges from full private ownership, rare globally, to public service models. The most common approach is the "landlord model," where governments retain infrastructure ownership while private operators manage terminals under long-term concessions. Kenya’s Port Master Plan 2018-2047, for example, aims to adopt this system to boost efficiency.

THE CRITICAL ROLE OF PORTS IN A COUNTRY’S ECONOMY

Port privatization has gained momentum in Africa, but to

understand its impact, it's crucial to recognize the role of ports in economic growth. Ports are gateways for international trade. They facilitate the movement of goods and raw materials and are, hence, indispensable to global commerce.

Ports along the Indian Ocean and the Red Sea are especially vital, serving as key supply chain links, particularly in oil, gas and fresh produce transport. However, despite the presence of major ports in East Africa, for example, their capacities, often measured in twenty-foot equivalent units (TEUs), cannot fairly compete with global standards. For perspective, what Shanghai processes in five days, Dar es Salaam handles in a year, while Mombasa takes a year to match Shanghai’s tenday throughput (TRT Afrika), hence the critical need for this transition.

Efficient ports require accessibility, capacity for large vessels, and economies of scale, key drivers of international trade. As such, to achieve this, many African governments are embracing private investment, benefiting both economies and investors. However, as private firms gain control over critical trade hubs, concerns about sovereignty grow. Case in point, the increasing role of Chinese firms in African ports.

As this debate unfolds, real-world examples highlighting the impact of port privatization suffice to provide a clearer picture. One such case is DP World’s model in Tanzania.

DP WORLD’S 30-YEAR CONCESSION TO OPERATE DAR ES SALAAM PORT

In 2023, DP World signed a 30-year concession to operate and modernize Dar es Salaam Port, marking a significant step in Tanzania’s strategic development plans. The first phase of the investment involves over US$250 million in upgrades, with the potential to increase to US$1 billion over the concession period. The port handles 95% of Tanzania’s international trade and is crucial for landlocked neighbors like Zambia, Uganda, and the DRC.

Since DP World officially took over operations at the port in April 2024, significant improvements have been made in operational efficiency and cargo handling. The company’s impact report shows that container throughput rose from 7,151 units in April 2024 to 20,151 units by July 2024, and the average turnaround time for container ships decreased from seven days to three days. Additionally, the number of ships waiting at anchor reduced from 35 in September 2023 to just 15 by September 2024.

The port’s cargo volume also increased notably by 18.6%, from 141,889 tonnes in May 2024 to 168,336 tonnes in September 2024. These operational gains have been accompanied by improved regional trade connectivity, attracting traders from landlocked East African countries.

East Africa’s transport costs remain among the highest globally, estimated at 60–70 per cent above international benchmarks (African Development Bank, 2024), making regional trade costly and less competitive. DP World’s involvement is thus crucial to reduce inefficiencies such as long cargo clearance times, high logistics costs, and infrastructure constraints that impede trade efficiencies and competitiveness.

KENYA’S PUSH FOR PORT PRIVATIZATION

Kenya’s journey toward port privatization has been gradual, marked by ambitious goals and cautious execution. The Kenya Ports Authority (KPA) has been leasing critical port

assets at Mombasa and Lamu, aligning with the government’s 25-year master plan. The privatization effort aims to enhance operational efficiency, boost competitiveness, and mobilize private sector capital.

To support this transition, Kenya has set a target of generating US$10 billion annually by 2030 through privatized port operations. So far, nine key assets have been leased, including berths 1-3 at Lamu Container Terminal and 11-14 at Mombasa Port. Financial performance has also seen steady growth, with KPA reporting US$15 million in revenue in the last fiscal year. The authority's robust earnings position it as a viable entity for listing on the Nairobi Securities Exchange (NSE).

Despite the promise of greater efficiency, concerns persist regarding transparency and national interests. Some stakeholders worry that private operators might exert undue control over key supply chain nodes, potentially influencing Kenya’s trade dynamics. The government, therefore, remains committed to balancing privatization with strategic oversight, ensuring that Kenya’s ports remain integral to regional and international commerce.

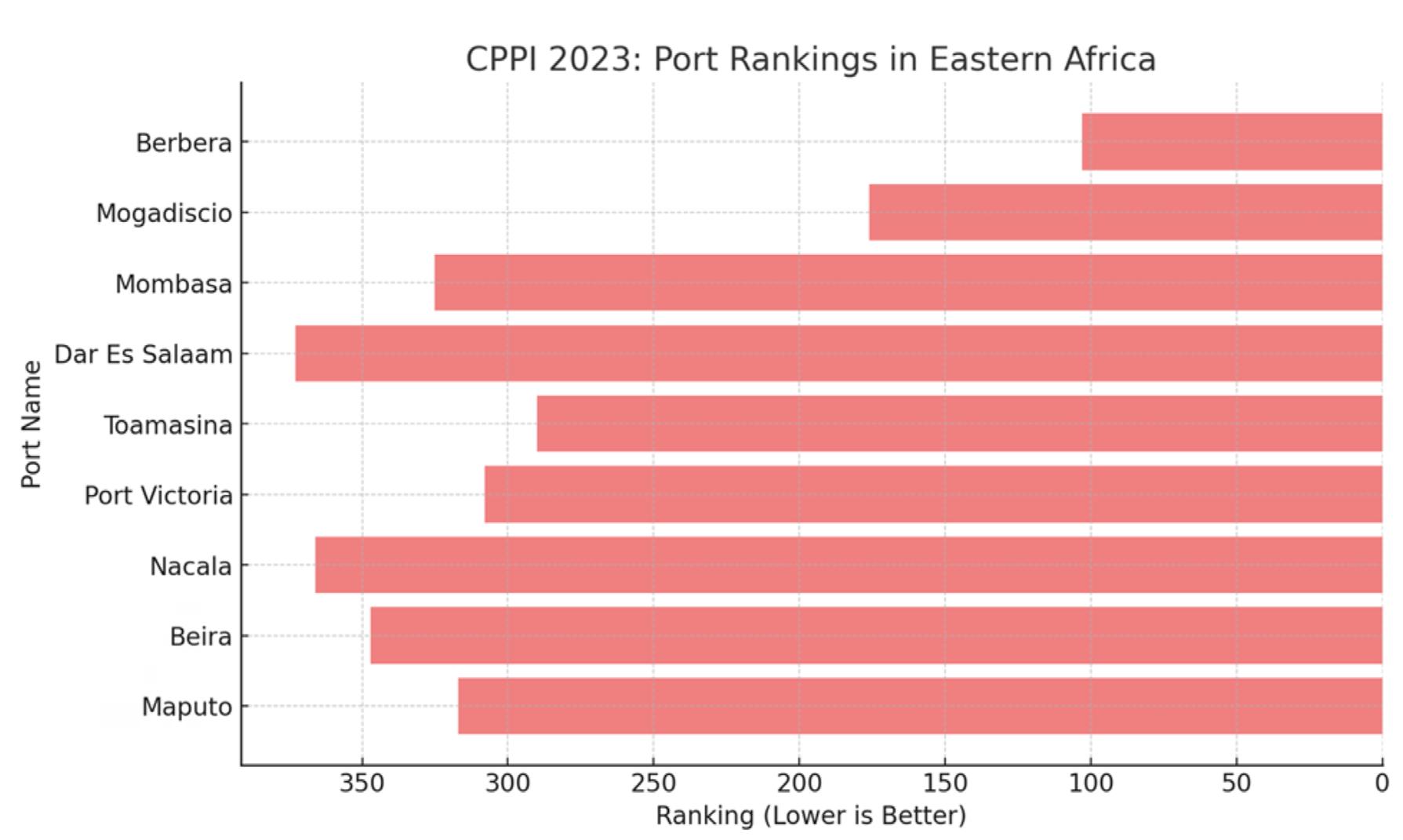

Despite the back-and-forth, a latest World Bank report on global port efficiency reports that the Port of Mombasa has overtaken Tanzania’s Dar es Salaam, challenging its regional dominance. The 2023 Container Port Performance Index (CPPI), released in 2024, ranked Mombasa 328th, while Dar es Salaam fell from 312th to 367th. It should be noted that the data used in this analysis was from 2023, before the DP World deal. Despite improvements, Kenya still lags behind regional peers, with Berbera Port in Somaliland ranked 106th globally, the best-performing port in Sub-Saharan Africa.

While Kenya’s stance on privatization remains cautiously

embraced, South Africa is fully committed to privatizing its ports.

THE CALL FOR PRIVATIZATION IN SOUTH AFRICA