All Media Rights businesses are different – Heuristics are used to support in getting you closer to an answer, but not to solve specific issues – use them wisely!

Media Rights differ by Market, Event Type, Sport and many other variables, please make sure that all Heuristics are relevant to your use case before applying.

These Media Rights Heuristics intend to get you to the start line in client conversations, not the finish.

If you have specific questions or require support, please discuss with the Media Rights captains.

If you require visuals from these Heuristics, please contact the ‘Knowing Fans Best’ team.

The rightsholders who will grow and optimise their media rights over the next years are the rightsholder who will:

Understanding Media Rights

Media rights remains the dominant revenue driver for sports rightsholders

Most rightsholders rely on media rights revenues for a significant chunk of their income (usually 30-50%)

In 2024, the global value of sports media rights surpassed $60bn for the first time, reaching $62.61bn.

Media rights refer to the audiovisual rights of a rightsholders events. Rightsholders need to achieve the right balance of increasing audiences and revenue when distributing media rights.

Different distribution strategies and channels reflect both a rightsholders priorities, and market demand (e.g. FTA vs PTV vs Hybrid vs streaming)

Whilst most rightsholders rely on media rights fees as a key revenue stream, this will fluctuate based on the size of the rightsholder, with smaller rightsholders with less reach being more reliant on sponsorship, ticketing and other event day revenue streams.

Annualised Sports Market Revenue by stream:

Media: 40%

Sponsorship: 29%

Event Day: 17%

Retail: 6%

Other: 10%

of sports rightsholder revenue comes from Media Rights.

Understanding Media Rights

CAGR = Compound Annual Growth Rate: The mean annual growth rate over a period longer than one year

Gone are the days of guaranteed growth every cycle... Industry CAGR is now mostly flat, with shifting consumption patterns meaning traditional broadcasters don’t have the same budgets for sports rights

Media Rights value is hard to compare year on year, given the nature of Media Rights cycles spanning multiple years and spikes can occur depending on the nature of the sporting calendar in given years.

When looking at Media Rights trends, it’s important to look at like for like comparisons for the same rights and how their value is changing while also considering inflation over license periods (some of which can be over 10 years!)

Rights have traditionally been on an upwards trajectory, but the market is starting to correct:

This is in part due to the emergence of new players in the market, new consumption channels, competing forms of entertainment and the rise of streaming platforms.

This fragmentation of demand has impacted key revenue segments for traditional broadcasters (TV advertising and pay-TV subscriptions mostly), meaning rights acquisitions budgets are under pressure.This is affecting Tier 2 and 3 properties more than premium Tier 1 rights, which can still command strong fees.

Tier 1 rights still seeing an increase in fees are often ‘giving more away’ (more matches, more rights) and the underlying value remains flat/declining, with the exception of some major properties. Pressures then remain on buyers gaining a return on their investment across all Tiers of rights.

Understanding Media Rights

The top 10 Sports properties by media value account for 63% of the total industry value.

Several factors combine to determine how much a sports property can command for its media rights. Some of the most important include:

The factors listed above will vary in their importance based on the type of sport, market and buyer landscape.

2023 and 2024 saw new multi-billion-dollar deals for the NFL and NBA and the Indian Premier League, as well as other strong movements in the US.

Understanding Media Rights

Rightsholders can be categorized into “Tier 1” , “Tier 2” , “Tier 3”, and “Tier 4” based on the Average Annual Value (AAV) of their total media rights deals; helpful in showing the dominance of Tier 1 rightsholders in the industry

Tier 1 Rights:

Avg Annual Media Rights Value: >$100m

Market share: >80%

Tier 2 Rights:

Avg Annual Media Rights Value: $50-$100m

Market share: 10%

# Properties: c.100

Tier 3 Rights:

Avg Annual Media Rights Value: $20M-$50m

Market share: 8%

# Properties: c.200

Tier 4 Rights:

Avg Annual Media Rights Value: <$20m

Market share: 0.5%

# Properties: c.2000

Non-Monetised

# Properties: c.2000

of market share of market share of market share

# Properties: c.50 of market share

Understanding Media Rights

Despite a global market for many sports, most rightsholders still drive 80% of media rights revenue from their domestic market

For most rightsholders that have a domestic league, core fans in this market typically drives the lion’s share of media revenue:

Larger, established global properties can expect to drive more value from international deals, but this takes time to build a fanbase (e.g. Premier League 56% global)

Reducing reliance on Domestic Markets can often be a challenge for sports rightsholders.

Rightsholders will often focus on prioritising & protecting their domestic agreements and may be less likely to innovate with new types of distribution

But growing a stronger fanbase in international markets hedges some of the risk of relying on domestic deals, and strengthens the overall brand IP International rights are often determined by avidity of the sport in respective countries, as well as timezone differences, competing national heroes & more…

Average Value of Media Rights driven by domestic markets

Average Value of Media Rights driven by non- domestic markets

Although 80% is the

Media Rights Trends

More people are streaming (sports and non-sports), and by nature fewer people are watching linear TV…meaning traditional broadcasters tend to earn less through advertising & subscriptions and subsequently are valuing rights lower

More

players in the market and better

The last decade has seen an explosion in the number of streaming platforms and subscription services.

Coupled with the acceleration of high-speed internet and Smart TVs, consumers and fans have more choice than ever and can demand more.

Decrease

Subscription providers recognise the power of live sport to drive new subscribers and reduce churn, so more players are entering the market to bid for live sports rights.

in Linear TV (UK)

Sports are working hard to keep up with the streaming wave

Rightsholders are embracing streaming through their own D2C platforms, and through their rights distribution.

Increase in streaming in last 2 years (UK)

Rightsholders need to consider who they are targeting, as different platforms will have differing audiences, viewing patterns

Rightsholders are exploring hybrid distribution models, which includes dissecting rights into packages, with some being sold to TV broadcasters and some to streamers

Whilst the market is correcting, and traditional TV channels have tightened their purse strings, the rise in prominence of streaming platforms presents an interesting crossroads for sports rightsholders

New competition in the market generates tension and growth for rightsholders & creates a need for broadcasters to innovate their offering to fans.

This in turn creates an opportunity to engage with younger fan demographics, who are less inclined to watch linear TV, and tap into casuals/non-sports fans. Done well, you can create strategic links to docuseries and creating new generations of fans for both streamer & rightsholder.

The big streamers are experimenting with more premium rights… which has the potential to further ‘squeeze the middle’. i.e. they only target formats and sports that will provide direct ROI and incrementality of users – further polarising the market.

There can be a lack of discoverability and appointment to view for sports on streaming platforms. Having your events on streaming means a reliance on active viewing, and therefore a potential loss in eyeballs through a reduction in passive viewing achieved on linear TV (although this is declining and aging as a consumption habit).

MLS & Apple TV with a 10-year deal for US rights

Netflix experimenting with ‘standalone’ events inc. Women’s World Cup, NFL Xmas Day & Jake Paul boxing events

Amazon Prime strategically acquiring rights around key windows for their Prime business e.g., EPL matches around Black Friday

Whilst streaming has seen massive growth over the last decade, Traditional TV still accounts for 2/3 of video revenue.

Despite the rise of Streaming in recent year,Traditional TV continues to drive the bulk of media revenue, accounting for $0.66 of

Streaming increasingly can’t be seen as a ‘silver bullet’ when trying to grow your media revenues – with the CAGR of streaming subs slowing to 1% (vs 7% 2017-2022) and the number of streaming services per household plateauing at 3.9 (having increased from 1.4 in 2016) – Sports Media rights will likely remain centered around Traditional TV revenues for the foreseeable future. This is not to say that some rightsholders will buck the trend and drive the majority of their own rights value through streamers!

Media Rights Trends

While the overall media rights industry is correcting, some Premium US rights are bucking the trend, seeing 5% CAGR

Although overall market growth remains flat, premium U.S. rights are bucking the trend with a 5% annual growth rate.

of total industry value

These rights are the most coveted in the industry, accounting for half of the total sector’s value.

Premium US rights growth shows that there is still strong demand for live

The deals are often quite innovative in nature to continue driving growth, e.g. Apple MLS 10-year ‘home of’ partnership

But it’s not all plain sailing… MLB / ESPN terminated their agreement early (due to expire in 2028)

Outside of the USA at 50% of Media Rights, the UK, Indian Subcontinent and Germany are the next largest markets.

While US Media Rights are fuelled by the likes of NFL, NBA and MLB – the popularity of Football (Soccer) leads to large Media Rights value in the UK and the rest of Europe, with Cricket and the IPL having a similar impact on the Indian sub-continent.

Looking at annual data since 2019 – the markets currently with positive growth trajectories are the US, Nordics and Latin America, where the other top 10 markets remaining flat or seeing minor declines.

Younger fans are consuming less live sport on linear TV compared to older fans, and are more actively consuming via streamingservices and social media.

Younger fans’ consumption habits are changing & diversifying

Younger fans have a preference for streaming and shortform viewing on digital channels – they’re less likely to watch linear programming

Linear TV remains popular with older generations but its share of under-35s’ consumption time is significantly less

This is reflected by the increase in demand for short-form content which younger sports fans are consuming through social media & vertical content

Of Gen Z consume sport via streaming devices

Of Baby Boomers consume sport via linear TV channels

Develop a media rights strategy which allows for flexibility through sufficient reserved rights (clips you can post yourself) and short holdback periods for highlights

If younger fans don’t have the attention span to watch a full live event, create a hook for them through cross-promotion with creators, athletes, ancillary programming & BTS content

Understand the evolving channel and content preferences of fans of the future in order to maintain relevance within your strategy… and be alert to what others in the industry are doing to innovate

Setting the scene for Media Rights

Divided attention is the norm with X% 2nd screening and Y% triple-screening

Most fans now use multiple devices while watching live sport

Sports fans are no longer solely focused on the main event when they are watching live sport

Coupled with shortening attention spans for younger fans, rightsholders should utilize other digital engagement channels to keep their fans interested in the live event – and to attract new fans

Rightsholders should create content and products designed for second screens to maximise engagement

Fantasy and other gamification, as well as betting and social media engagement are amongst the most common second screen behaviours for sports fans.

This can be integrated with broadcast propositions and media partners by overlaying graphics, creating shoulder content & programming relating to supporting digital products

Having a good broadcast proposition is not enough; this has to be reinforced by giving fans further ways to engage with their favourite athletes

Setting the scene for Media Rights

To optimise the impact of your highlights packages, you should aim to have your OneBox highlights up within 15 minutes of the match ending.

Get your highlights to the top of Google to maximise viewing

Onebox is the technology behind the first search result when searching for a sports event on Google, which brings up direct links to video clips & scores

Multiple properties could upload highlights of an event within a short window following the final whistle - and being first on the ‘Onebox carousel’ means your content is the first that people see .. And click on to watch

Uploading within 15 minutes gives you the best chance of winning this race, and maximising viewership of your video/highlights, enabling greater ad revenue & engagement on owned channels

Partner with 3rd parties who create AI produced clips

The growth in AI has seen the likes of WSC and Greenfly become specialists in AI produced clips… utilizing these products gives you a better chance at winning the Onebox race

This means highlights clips can be produced much quicker than if someone manually edits them, and can therefore be uploaded and available to fans in a much shorter timeframe whilst the content is at its peak relevance

Setting the scene for Media Rights

The majority of engagement with highlights from a sports event occurs in a narrow window immediately following the event.

Highlights have a short window of opportunity for consumption

Whilst highlights are becoming increasingly important, their window of relevance is short and is limited to the 24hrs immediately following the event.

Uploading as soon as possible within this window, with short concise summaries of key action to capitalize on the peak of attention, and then stagger content after the event.

Imperative

to make highlights visible quickly & flexibly

Within the boundaries of rights restrictions, distribute highlights quickly post-event across multiple channels.

Leverage earned (e.g. Google OneBox) alongside owned & operated channels to capture fans who are searching for highlights outside of your channels.

Create & distribute multiple highlights formats (short-form / extended / full-match). This caters to fans who both want a bite-sized recap and an in-depth summary of the action.

Highlights Views

Of highlights views are in the first 24hrs after the end of an event

Time since Event +24hrs +48hrs +72hrs

Setting the scene for Media Rights

Breakout stars such as Luke Littler and Caitlin Clark can catapult a sport to the forefront of audiences… and rightsholders need to leverage these star assets to drive media value

The rise of social media has allowed athletes to connect directly with fans and build their own brands and narratives

Younger fans are more tied to athletes than teams, and want to connect with their favourite athletes on a ‘personal’ level

When a breakout athlete captures the attention of new and existing fans, this can directly increase TV audiences, and give rightsholders a new opportunity to market their stars to grow media valye

Athletes can develop fanbases away from traditional sports audiences by discussing and producing content on personal interests, or partner with lifestyle, fashion entertainment brands

Athlete effects can be seen through social followings and search numbers – e.g. ‘Luke Littler’ was searched 2.5x ‘World Darts Championship’ during the 2024 Championship (Google Trends)

Rightsowners should work with athletes to grow fan value

Cobranding | Feature star athletes in campaigns, making them the face of leagues and clubs.

Collabs on social to leverage the new audiences – based on aligning goals of athletes and rightsowners

Develop tailored licensing and Media Rights deals where players share league or club content on their platforms.

Most Watched Non Football Event Ever on Sky Sports

Second Most Watched NonFootball Event Ever on Sky Sports

Sky Sports & PDC signed a new 5 year deal worth the current deal, £25m p.a., after years of relatively flat fees

Setting the scene for Media Rights

Throughout any cord-cutting trends, sports broadcast viewership has remained stable.

Sports continue own the biggest “appointment-to-view” moments on TV today.

When looking at the Top 100 Most-Watched U.S. TV Broadcasts of 2024, sports broadcasts accounted for 80 of them, with the NFL accounting for 71.

In 2023, a non-election year, sport accounted for 96 of the Top broadcasts, the NFL accounting for 93 of these.

In today’s streaming era, live sports and news remain among the last major pillars sustaining linear television.

Despite flat media rights revenues overall, sports still delivers unmatched live audiences particularly the NFL.

This means that even if rights fees aren’t climbing at the pace they once did, sports properties have a powerful tool for capturing large, real-time audiences in an age dominated by ondemand viewing.

Top 100 Most Watched U.S. TV Broadcasts of 2024

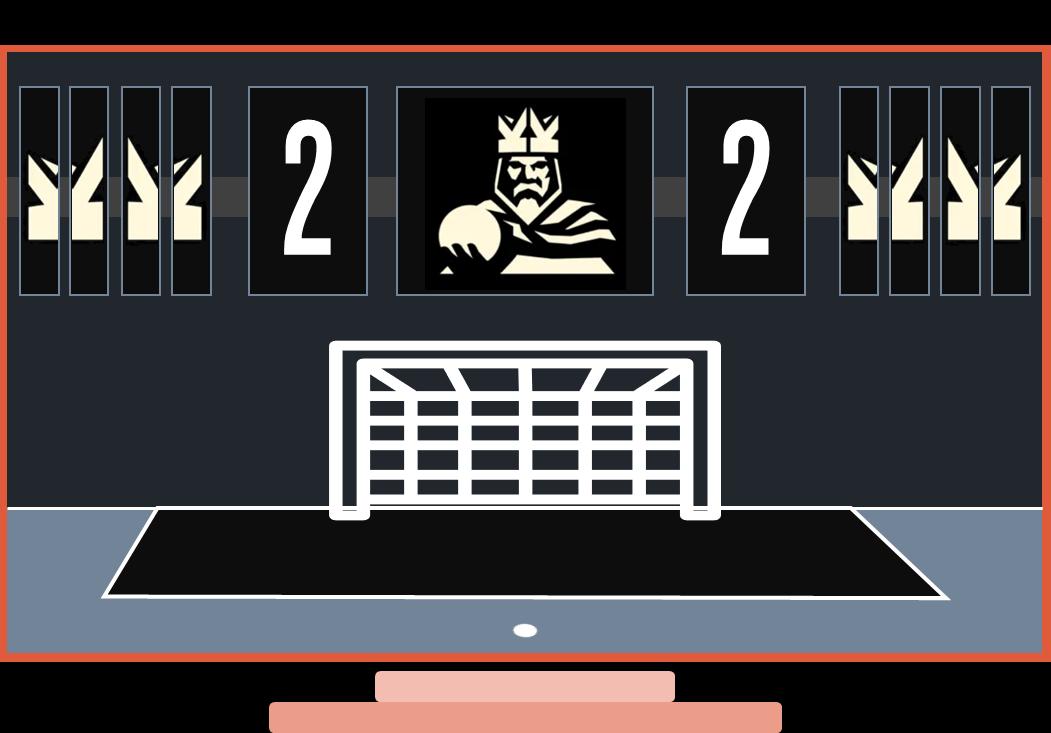

Setting the scene for Media Rights

Kings League is adopting a digital-first approach to connect with younger audiences, making use of popular digital streaming platforms like Twitch and YouTube, complementing this with free-to-air distribution.

New rightsholders breaking into the market, such as Kings League, are still able to capture and grow global audiences.

7-a-side tournament set up in January 2023 as a challenger league by ex-pro soccer player Gerard Pique and Spanish content creator Ibai Llanos.

Year 1 | 47m hours watched

Year 2 | 100m viewers

Media Revenue Estimation: Low Six Figures

Kings league focused not on high performance, but on entertainment and proximity with the talents. Using influencers that are actively participating in the sport to drive big audiences on digital and social, securing additional traditional partnerships to complement the reach.

Source: SportsPro, Two Circles.

International Broadcasting:

The Kings League has secured agreements with major broadcasters, including CBS in the US, DAZN in Japan and Australia, ESPN and Disney+ in Latin America, & Sky Sports in Italy.

These partnerships are non-exclusive, allowing simultaneous streaming on platforms like Twitch, YouTube, and TikTok.

Domestic Broadcasting:

In Spain, Mediaset acquired rights to broadcast select matches on its free-to-air channel Cuatro, starting from the second season in May 2023.

Digital First Approach Then Free-to-Air

On Kings League channels and channels of team’s chairpersons