RED DANISH INVESTMENT ATLAS 2024

PUBLISHED BY IN COLLABORATION WITH

ENGLISH EDITION

HOTEL RETAIL OFFICE LOGISTICS RESIDENTIAL ANNUAL REVIEW

COPENHAGEN 12.5 BN DKK 29% COPENHAGEN 8.8 BN DKK 20% 6.8 BN DKK 16% OTHER ZEALAND 2.1 BN DKK 5% FUNEN GREATER COPENHAGEN Danish 66% Foreign 34% Danish 58% Foreign 42% Danish 83% Foreign 17% Danish 88% Foreign 12% 12.5 BN DKK 29% COPENHAGEN 8.8 BN DKK 20% 6.8 BN DKK 16% OTHER ZEALAND 2.1 BN DKK 5% FUNEN 43.4 VOLUME IN TOTAL GREATER COPENHAGEN Danish 66% Foreign 34% Danish 58% Foreign 42% Danish 83% Foreign 17% Danish 88% Foreign 12% BN DKK 100% 12.5 BN DKK 29% COPENHAGEN 8.8 BN DKK 20% 6.8 BN DKK 16% OTHER ZEALAND 2.1 BN DKK 5% FUNEN GREATER COPENHAGEN Danish 66% Foreign 34% Danish 58% Foreign 42% Danish 83% Foreign 17% Danish 88% Foreign 12% 12.5 BN DKK 29% COPENHAGEN 8.8 BN DKK 20% 6.8 BN DKK 16% OTHER ZEALAND 2.1 BN DKK 5% FUNEN 1.7 BN DKK 4% AARHUS AALBORG 43.4 VOLUME IN TOTAL GREATER COPENHAGEN Danish 66% Foreign 34% Danish 74% Foreign Danish 58% Foreign 42% Danish 83% Foreign 17% Danish 88% Foreign 12% Danish 88% Foreign 12% BN DKK 100% 12.5 BN DKK 29% COPENHAGEN 8.8 BN DKK 20% 6.8 BN DKK 16% OTHER ZEALAND 2.1 BN DKK 5% FUNEN 1.7 BN DKK 4% AARHUS 0.8 BN DKK 2% AALBORG 43.4 VOLUME IN TOTAL GREATER COPENHAGEN Danish 66% Foreign 34% Danish 74% Foreign 26% Danish 58% Foreign 42% Danish 83% Foreign 17% Danish 88% Foreign 12% Danish 88% Foreign 12% Danish 93% Foreign 7% BN DKK 100% 8.8 BN DKK 20% 6.8 BN DKK 16% OTHER ZEALAND 2.1 BN DKK 5% FUNEN 1.7 BN DKK 4% AARHUS 0.8 BN DKK 2% AALBORG 10.6 BN DKK 24% OTHER JUTLAND GREATER COPENHAGEN Danish 58% Foreign 42% Danish 83% Foreign 17% Danish 88% Foreign 12% Danish 88% Foreign 12% Danish 93% Foreign 7% Danish 85% Foreign 15% 1.7 BN DKK 4% AARHUS 0.8 BN DKK 2% AALBORG 10.6 BN DKK 24% OTHER JUTLAND Danish 88% Foreign 12% Danish 93% Foreign 7% Danish 85% Foreign 15% 8.8 BN DKK 20% 6.8 BN DKK 16% OTHER ZEALAND 2.1 BN DKK 5% FUNEN 1.7 BN DKK 4% AARHUS 0.8 BN DKK 2% AALBORG 10.6 BN DKK 24% OTHER JUTLAND GREATER COPENHAGEN Danish 58% Foreign 42% Danish 83% Foreign 17% Danish 88% Foreign 12% Danish 88% Foreign 12% Danish 93% Foreign 7% Danish 85% Foreign 15% Source: ReData

& INVESTORS 2023

VOLUME

INTRODUCTION

Dear reader,

Welcome to ”RED Danish Investment Atlas 2024”.

The past year became a year where the real estate market faced a new reality. After several years with attractive conditions for real estate investments, the players had to navigate under new turbulent circumstances in 2023. Despite continuing strong underlying conditions in the occupier market, substantial interest rate increases and uncertainties about the future brought the investment market to a standstill.

However, the year ended with low inflation, several interest rate cuts, several large transactions, and a general increasing optimism among the industry’s players.

On the following pages, you can get a detailed insight into the Danish commercial real estate market in the past year, as well as RED’s forecast on how we expect the market to develop in the coming year.

The report is structured as an easily accessible reference work, where you can either get a quick overview of a single segment or immerse yourself in all the tendencies segment by segment.

The data for this year’s report is made in collaboration with ReData, which collects and validates data on every single transaction on the Danish real estate market.

Enjoy the report.

Nicholas Thurø, Managing Partner Cushman & Wakefield | RED

RED assisted ATP Ejendomme with the letting of 1,205 m² of offices in the architect designed property at Nicolai Eigtveds Gade 28 in Copenhagen.

| 3

HOTEL RETAIL OFFICE LOGISTICS RESIDENTIAL ANNUAL REVIEW

EXECUTIVE SUMMARY

A PARALYSED INVESTMENT MARKET

2023 was a year in which the new high interest rates paralysed all parts of the investment market. Despite strong underlying conditions on the occupier markets, buyers and sellers could not meet each other’s price expectations. Regardless of investor types, segments, and geographical areas, we saw a slowdown in the investment activity. Therefore, the total transaction volume only reached DKK 43.4 bn, and the volume was thus more than halved from 2022 to 2023.

FOREIGN CAPITAL ON RETREAT

In recent years, the Danish market has been characterised by an increasing degree of professionalism, which can largely be attributed to the fact that foreign capital has been behind a significant share of the investment activity. However, foreign investors have been characterised by leveraging their investments, and they were, therefore, particularly challenged by the new high interest rates. Consequently, foreign investors only accounted for 26% of the total volume in 2023, which is the lowest share in nine years.

THE MARKET’S DARLING CONTINUES ITS DOMINANCE

Despite the fact that demand for rental housing was intensified by a skyrocketing housing burden for owner-occupied homes, the transaction volume in the residential segment decreased by almost 60%. However, the segment was still the investors’ most preferred segment, and with a transaction volume of DKK 16.8 bn the residential segment maintained its position as the largest segment. The activity was primarily driven by the fact that the foreign investors acquired prime residential properties in Copenhagen, while the Danish investors, in search of returns, invested more broadly in the country.

THE HUNT FOR YIELD DEFINED THE LOGISTICS MARKET

A search for returns characterised the logistics segment in 2023, but this search resulted in two opposing trends. For many years, the segment for modern logistics properties has benefited from offering higher yields than our neighbouring countries. However, in 2023, this advantage

disappeared as we did not experience the same price corrections as seen in other comparable countries. Consequently, the investors allocated their capital to other markets with higher yields. One asset type that did, however, become particularly attractive in Denmark was value-add logistics properties. This was due to the fact that investments in these properties could still be leveraged and that investors have great confidence in the future leasing terms.

Despite the absence of investments in prime logistics properties (and that it was, therefore, investments in the cheaper value-add properties that were to drive the activity), the logistics segment took the position as the second-largest real estate segment for the first time, with a volume of DKK 8.9 bn.

THE OFFICE MARKET WAS UNDER PRESSURE FROM SEVERAL FRONTS

With a transaction volume of only DKK 8.6 bn, the office segment had to see itself defeated in the battle for the place as the second-largest segment in Denmark for the second year in a row. This can be attributed to the fact that the office market (in addition to the general conditions that challenged the real estate market) was also challenged by international concerns that an increasing share of remote work would result in a fundamentally changed office market with increasing vacancy rates and decreasing rent levels. As a result, many investors sought to reduce their exposure in the office segment, which resulted in foreign investors accounting for only 2% of the capital invested in the segment.

NOTHING COULD SAVE THE RETAIL SEGMENT, BUT WHY NOT?

Even though the retail segment includes widely different asset types, each with its unique appeal to investors, the investor appetite for retail assets remained limited, and in contrast to 2022, there were no portfolio or standalone transactions in the billion-kroner range to boost the volume. Therefore, investments in retail properties decreased by 74%, and the segment thus became the segment that experienced the largest decrease in volume from 2022 to 2023.

However, several factors indicate that retail assets may once again become interesting in the search for attractive risk-adjusted returns. For instance, the yield levels for high street properties located in Copenhagen are more or less on par with those for logistics properties and hotel properties, where there has traditionally been a significant risk premium differentiating the yields.

THE HOTEL SEGMENT MIGHT BE THE NEW BIG THING

Historically, investment activity in the hotel segment has been characterised by large standalone transactions, and 2023 was no exception. The volume in the hotel segment reached DKK 1.2 bn, which was primarily driven by NREP’s acquisition of Comfort Hotel Vesterbro. However, the hotel market in Copenhagen has shown positive trends, with high occupancy rates and increasing room prices. Several factors, therefore, indicate that there may be potential for generating attractive returns in the segment going forward.

RECORD-HIGH VOLUMES BELONG TO THE PAST

The year ended with increasing optimism, which was driven by a belief in interest rate reductions, continued strong underlying conditions on the occupier markets and a general confidence in the Danish market. As buyers’ and sellers’ price expectations are approaching each other and the interest rate stabilises, we expect to see increasing activity on the real estate market once again.

However, we do not expect to see the same high volumes in 2024 as we have been used to in recent years. This is, among others, due to the fact that the leveraged returns on real estate investments will be significantly lower than before. At the same time, attractive and more liquid assets, such as bonds, will continue to give investors an attractive risk-adjusted return, thereby reducing the appetite for real estate investments.

4 | RED Danish Investment Atlas 2024

Investment highlights

| 5 BN DKK RESIDENTIAL VOLUME IN TOTAL 16.8 BN DKK LOGISTICS VOLUME IN TOTAL 8.9 8.6 BN DKK OFFICE VOLUME IN TOTAL BN DKK RETAIL VOLUME IN TOTAL 4.9 BN DKK HOTEL VOLUME IN TOTAL 1.2 Foreign34% Foreign44% Foreign22% Danish66% Danish56% Danish98% Danish78% Danish94% RESIDENTIAL RETAIL OFFICE HOTEL LOGISTICS

2023 Northern Horizon Capital became the largest residential investor with their acquisition of NREP’s care home portfolio 1.5 Investment highlights 2023 IKEA became the largest logistics investor with their acquisition of their logistics centre in Hedehusene 1.8 Investment highlights 2023 Swiss Life became the largest retail investor with their acquisition of the shopping centre Næstved Storcenter 840

2023 AP Pension became the largest office investor with their acquisition of Codanhus and Kalvebod Bygge 32 2.5 Investment highlights 2023 NREP became the largest hotel investor with their acquisition of the Comfort Hotel Vesterbro 700 Area Volume Change Copenhagen 6.1 -55% Greater Copenhagen 1.6 -77% Aarhus 0.9 -86% Rest of Denmark 8.2 -41% Total 16.8 -59% Area Volume Change Copenhagen 4.9 -29% Greater Copenhagen 1.7 -12% Aarhus 0.3 -45% Rest of Denmark 1.8 -63% Total 8.6 -39% Area Volume Change Copenhagen 0.5 -90% Greater Copenhagen 0.5 -82% Aarhus 0.2 -86% Rest of Denmark 3.7 -61% Total 4.9 -74% Area Volume Change Copenhagen 0.8 -33% Greater Copenhagen - -100% Aarhus - -100% Rest of Denmark 0.5 97% Total 1.2 -21% Outlook 2024 Prime rent Prime yield Transaction volume Outlook 2024 Prime rent Prime yield Transaction volume Outlook 2024 Prime rent Prime yield Transaction volume Outlook 2024 Prime rent Prime yield Transaction volume Outlook 2024 Prime rent Prime yield Transaction volume BN DKK BN DKK BN DKK M DKK M DKK Area Volume Change Copenhagen 0.1 -71% Greater Copenhagen 4.5 72% Aarhus 0.2 -63% Rest of Denmark 4.1 -60% Total 8.9 -35% HOTEL RETAIL OFFICE LOGISTICS RESIDENTIAL ANNUAL REVIEW

Investment highlights

THE YEAR IN REVIEW

2023 was a year where numerous factors made it more challenging for players in the real estate market to make decisions. Was it the right time to invest when there was no evidence that prices had stopped decreasing? Could future expectations justify acquisitions when getting financing and yield levels to match in the current market was difficult? Should tenants choose to move to a new office when the future was and still is uncertain?

These were just some of the dilemmas that defined the market in 2023, which will be explored in the following.

THE SELLERS DEFINED THE MARKET

Across the globe, significant interest rate hikes meant that players in the real estate market had to operate in a new reality in 2023, where real estate financing became more expensive and challenging, and other more liquid assets suddenly became attractive alternatives. Although there were still buyers in the market, general low leverage and strong underlying conditions in the occupier markets meant that sellers were not forced to sell and that it became more attractive to keep the properties rather than sell at prices that were lower than in the good old days. The sellers’ slow adjustment pace thus put a brake on the activity in 2023.

However, prospects of interest rate reductions and continued strong underlying conditions have resulted in an improving optimism in recent months. Therefore, we have entered 2024 with expectations of the market being aligned by mid-year –albeit with lower activity than in recent years.”

Nicholas Thurø, Managing Partner, Capital Markets

6 | RED Danish Investment Atlas 2024

RESIDENTS PUSHED TOWARDS THE RENTAL MARKET

“Every decision is made based on an assessment of pros and cons, and when tenants are to decide between buying and renting a home, the housing burden is one of the most critical parameters. An essential advantage of owner-occupied housing has been that it was cheaper than renting for many years. However, the high prices for owneroccupied housing and the high interest rates have meant that the monthly costs of owning today exceed the monthly costs of renting. Thus, as the market is now, there are not many advantages left to owning, which has resulted in a significant search towards rental properties. Combined with the demographic trends and the low construction activity, this implies that the rental market will be strong in the coming years, and especially in Copenhagen, we expect to see increasing rent levels and a continued high investor appetite.”

Kjeld Pedersen Partner, Capital Markets

THE RETAIL MARKET SURPRISED

“As we entered 2023, it was with prospects of increasing interest rates, high inflation, and low consumer confidence. Thus, not many factors indicated that a year later, we would look back on the year as a positive one for the high streets of Copenhagen. However, that’s what happened. Customers flocked to the high streets, and both well-known and new brands opened stores, resulting in a reduced vacancy. However, some things remained the same. For instance, there is still a direct correlation between the stores’ ability to attract customers and the development in tenant demand. In this context, Amagertorv remains the winner, and Frederiksberggade is the loser.”

Kristian Vinggaard Partner, Retail

THE OFFICE MARKET IS NO LONGER ONE MARKET

“It’s not always easy to know what tenants want and don’t want, but in 2023, office tenants made it clear. They want a physical office located centrally in Copenhagen with easy access to public transport and one that can meet their requirements for shared facilities, sustainability, flexibility, etc. – and as if that wasn’t enough, the office must also be unique to fit the identity of each company. We have, therefore, seen that the market has been divided into leases that can meet all of the tenants’ requirements and those that cannot. Therefore, the supply of older and less well-located offices has increased significantly, whereas there is competition for the most well-located modern offices. In 2024, we are, therefore, looking at a market characterised by an increasing rent spread between primary and secondary office leases.”

Anders Krogh Partner, Office Letting

LOGISTICS INVESTORS CHASED RETURNS

“In recent years, we have seen an insatiable investor demand for core logistics properties. However, in 2023, a different asset type suddenly topped the investors’ wish lists – value-add logistics properties. This shift in preference is due to the fact that, despite the rapid development of logistics tenants’ requirements, a continued large undersupply of logistics areas near the major cities implies that investors have expectations of continued low vacancy rates and increasing rent levels - even for the older and more outdated warehouse properties. At the same time, the yields are at a level where investments can be leveraged despite the worsened financing terms. Therefore, it will be interesting to see whether the investors’ preference shifts back to the core segment if we see further interest rate reductions or if there will continue to be the greatest demand for value-add properties with higher yields.”

Lior Koren, Partner and Head of Capital Markets

| 7

HOTEL RETAIL OFFICE LOGISTICS RESIDENTIAL ANNUAL REVIEW

RED assisted Aage Bangs Fond with the letting of 269 m² of exclusive offices in A.C. Bangs Hus in the city centre of Copenhagen.

8 | RED Danish Investment Atlas 2024

| 9 11 31 53 71 91 111 CONTENT ANNUAL REVIEW The Investment Market 12 Volume & Investors 14 Interview: Are Interest Rate Increases the Golden Opportunity for Pension Funds? 16 Highlight: No Transactions Without Belief in the Future 20 Highlight: Are the Risks Lower, or Are We Simply Behind? 24 Expectations for 2024 26 RESIDENTIAL Volume & Investors 32 Geographical Distribution 34 Top 5 Transactions 2023 38 Interview: Both Pros and Cons in the Danish Residential Market 40 Interview: The Developers’ Business Plans Are Challenged 42 Highlight: Renting Beats Owning – For a Little Longer 44 Highlight: A Capital Gains Tax of 50% Can Be the Solution 46 Expectations for 2024 48 Transactions & Key Figures 50 LOGISTICS Volume & Investors 54 Geographical Distribution 56 Top 5 Transactions 2023 60 Interview: From Core to Value-Add, but What Now? 62 Expectations for 2024 66 Transactions & Key Figures 68 OFFICE Volume & Investors 72 Geographical Distribution 74 Top 5 Transactions 2023 78 Highlight: Is the Physical Office a Thing of the Past? 80 Highlight: Complex Requirements 82 Expectations for 2024 84 Key Figures & Transactions 88 RETAIL Volume & Investors 92 Geographical Distribution 94 Top 5 Transactions 2023 98 Interview: The Winners Will Be Those Who Prioritise the Customers 100 Highlight: The High Streets of Copenhagen in 2023 102 Expectations for 2024 104 Transactions & Key Figures 108 HOTEL The Hotel Market Is Stronger Than Ever 112 Top 3 transactions 2023 116 HOTEL RETAIL OFFICE LOGISTICS RESIDENTIAL ANNUAL REVIEW

10 | RED Danish Investment Atlas 2024

RED assists Realdania By & Byg with the letting of office leases in the iconic multi-tenant property BLOX.

Photo: Realdania By & Byg / Rasmus Hjortshøj

Annual Review | 11 ANNUAL REVIEW

The Investment Market Volume & Investors Interview: Are Interest Rate Increases the Golden Opportunity for Pension Funds? Highlight: No Transactions Without Belief in the Future Highlight: Are the Risks Lower, or Are We Simply Behind? Expectations for 2024 12 14 16 20 24 26 HOTEL RETAIL OFFICE LOGISTICS RESIDENTIAL

ANNUAL REVIEW

THE INVESTMENT MARKET

A New, Different, and Illiquid Market

In 2023, the Danish commercial real estate market faced a new reality. The market’s long-lasting boom came to an end, and investors had to wait for sellers’ price expectations to adjust to the new financing conditions. The combination of non-distressed sellers in the Danish market and that investors saw quicker and more significant price corrections in our neighbouring countries resulted in a significant decrease in the investment activity in 2023.

LOWEST VOLUME SINCE 2014

While the buyers adjusted their business plans to the new high interest rates, the sellers struggled to meet the buyers’ yield adjustments. A significant gap between buyers’ and sellers’ price expectations, therefore, slowed down activity in 2023. Consequently, the volume only reached DKK 43.4 bn, which is the lowest volume on the Danish market since 2014 ( figure 2).

ACTIVITY IMPACTED BY INTEREST RATES

Capital has sought the safest assets in the safest locations for many years. However, in 2023, we saw that the high interest rates impacted the investment activity, resulting in an increase in activity with investment

opportunities that could offer higher returns and positive gearing effects using debt capital.

Within the logistics segment, investors increasingly sought value-add properties, in the residential segment, half of the volume came from investments outside the country’s largest cities, and prime office assets were primarily acquired by Danish equity-financed investors. Finally, the investors demanded the retail assets that could secure the highest returns. A transaction volume driven by different types of properties within the segments, therefore, implied that the volume was widely geographically distributed between Copenhagen,

Greater Copenhagen and the “rest of Denmark” ( figure 3).

INVESTORS WANT RESIDENTIAL AND LOGISTICS PROPERTIES

With a share of 39% of the total volume, residential properties continued to be the investors’ most preferred segment in 2023. While both Danish and foreign investors demanded residential and logistics properties, foreign investors were particularly hesitant to invest in the office segment, which was driven by global trends with increasing vacancy rates on the office market. Nevertheless, Danish investors’ acquisitions of Copenhagen office properties ensured that the office segment reached a total volume which was more or less on par with the logistics segment.

THE INTERNATIONALISATION HAS SLOWED DOWN

For many years, foreign investors have accounted for a significant share of the total transaction volume, and for the first time in 2022, foreign capital dominated the Danish market. However, in 2023, Danish investors reclaimed their position, accounting for almost three-quarters of the total investment volume ( figure 1). Thus, the foreign investors’ appetite for Danish commercial properties decreased in 2023.

43.4 BN DKK VENDORS INVESTORS Asset deals 49% Foreign 22% Share deals 51% Danish 78% Foreign 26% Danish 74% TOTAL VOLUME 2023 12 | RED Danish Investment Atlas 2024 Source: ReData

ANNUAL REVIEW

Figure 1: Origin of the investors & transaction structure 2023

0 20 40 60 80 100 120 140 2023 2022 2021 2020 2019 2018 2017 2016 2015 2014 31% 21% 32% 37% 27% 16% 12% 41% 11% 6% 10% 28% 41% 20% 9% 6% 6% 17% 45% 10% 4% 23% 8% 9% 44% 6% 9% 7% 7% 27% 56% 16% 10% 10% 7% 50% 15% 13% 8% 13% 42% 14% 15% 20% 8% 39% 20% 20% 11% TRANSACTION VOLUME (BN DKK) FOREIGN INVESTORS’ SHARE Residential Logistics Office Retail Hotels Other Foreign investors’ share 0% 10% 20% 30% 40% 50% 60% 70% Source:

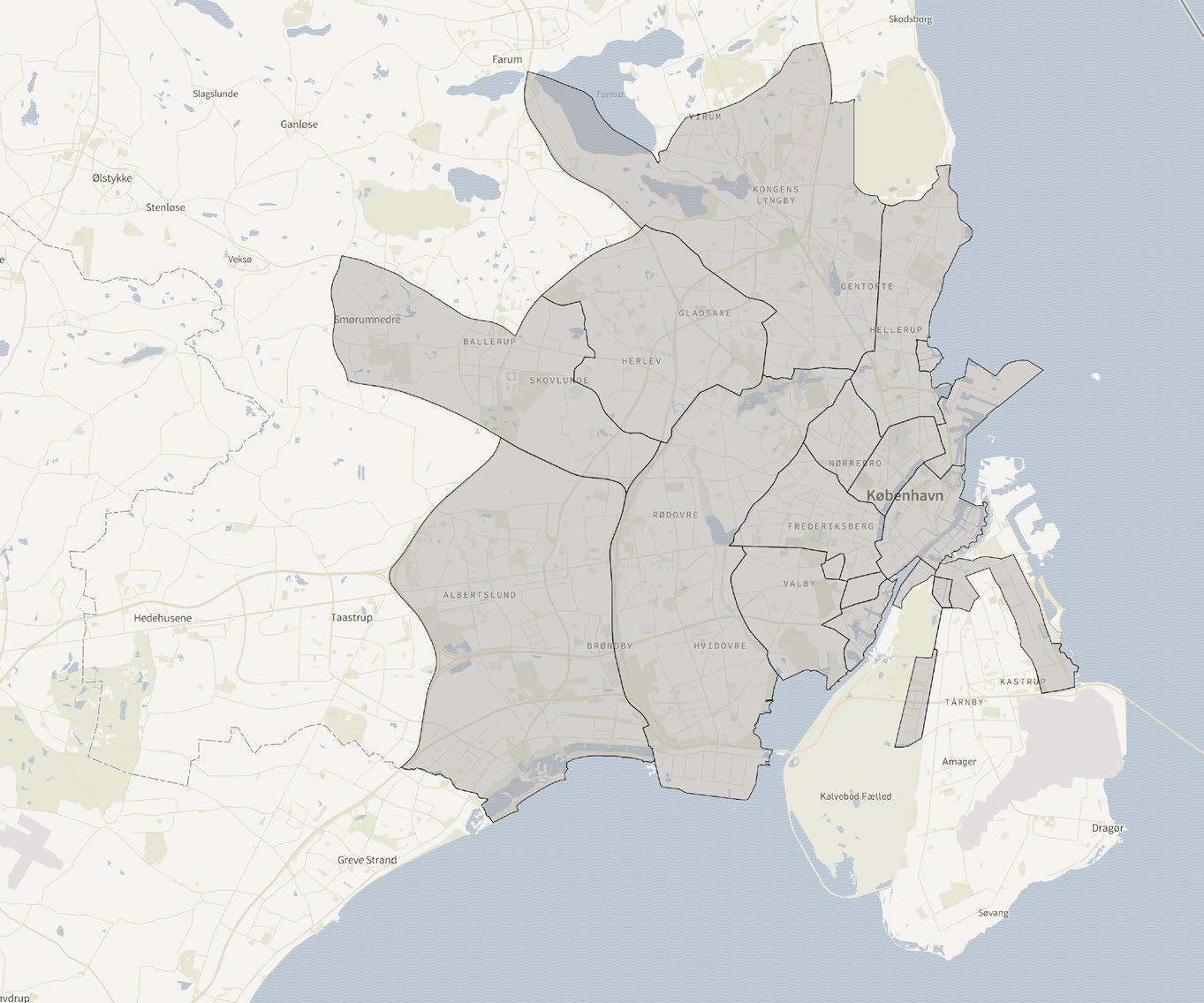

COPENHAGEN

COPENHAGEN

REST OF DENMARK 0 10 20 30 40 50 60 2023 2022 2021 2023 2022 2021 2023 2022 2021 2023 2022 2021 53% 47% 49% 51% 34% 66% 43% 81% 57% 19% 48% 58% 32% 66% 57% 15% 43% 34% 42% 68% 85% 52% BN DKK Annual Review | 13 ANNUAL REVIEW

ReData Danish Foreign

GREATER

AARHUS

Figure 2: Total transaction volume 2014-2023

HOTEL RETAIL OFFICE LOGISTICS RESIDENTIAL

Figure 3: Geographic breakdown of transaction volume 2021-2023

VOLUME & INVESTORS

WELL-KNOWN INVESTORS

OCCUPY THE PODIUM

Before the interest rate hikes and general uncertainty took over the market in the second half of 2022, favourable financing conditions combined with political stability led to the entry of many new investors into the Danish market. However, in 2023, new investors were cautious about investing in Denmark, which is reflected in the fact that nine out of the top ten investors in 2023 (all except Quantum Immobilen) were wellknown investors ( figure 5).

STANDALONE TRANSACTIONS

SECURED THE TOP SPOTS

The residential segment has for many years been the investors’ most preferred property segment, which was previously also reflected in the fact that the largest investors were primarily those who invested in residential properties. However, unlike in the past years, residential investors did not secure the first and second places on the podium of 2023’s largest investors. With the acquisition of a portfolio with two prime office properties (Codanhus and KB32),

AP Pension took the position as the absolute largest investor, and IKEA followed with the user acquisition of their logistics centre located in Hedehusene.

THE HISTORICALLY DOMINANT INVESTORS MAINTAINED THEIR POSITION

Despite the influx of many new investors to the market in recent years, there have been no changes in the top ten investors that have historically invested the most capital in commercial properties in Denmark. Instead, there were some internal rotations among the top ten investors. Thus, Heimstaden, Niam, Koncenton, NREP, and Patrizia maintained their positions as the historically largest investors in Denmark ( figure 6).

THE INVESTORS DEMANDED RISK DIVERSIFICATION

For many years, the Danish market was characterised by an insatiable investor appetite for the safest assets, where portfolios and volumes could not be too large.

However, in 2023, uncertainties left their mark on the activity, which is why it could

be observed that the investors generally demanded smaller volumes and greater risk diversification. Therefore, volume fell proportionally more for larger transactions (> DKK 200 m) than for smaller transactions ( figure 4). For the very large transactions with a volume of > DKK 500 m, the total volume was reduced by 64%, and the number of trans actions decreased significantly (from 30 transactions in 2022 to 14 transactions in 2023). Thus, the year proved that the saying “the bigger, the better” does not apply in uncertain times.

INCREASING OPTIMISM TOWARDS THE YEAR-END

Although the market in 2023 was generally characterised by uncertainty and limited investment activity, we saw a renewed optimism in the market towards the year-end, which was driven by low inflation rates, decreasing interest rates, and a belief in a more stable investment environment.

As a result, the fourth quarter of the year reached a volume that exceeded the total volume for the second and third quarters.

14 | RED Danish Investment Atlas 2024

Price range (M DKK) No. of transactions Volume (M DKK ) 2022 2023 2022 2023 0 - 20 3,263 2,621 14,670 10,309 20 - 50 271 171 8,328 5,523 50 - 100 110 62 7,744 4,289 100 - 200 63 33 8,983 4,718 200 - 300 28 9 7,112 2,127 300 - 500 25 5 9,268 1,763 500 - 1,000 20 9 14,556 6,550 > 1,000 10 5 26,111 8,115 Total 3,790 2,915 96,771 43,394 ANNUAL REVIEW

Figure 4: Breakdown in price ranges 2022 & 2023

Source: ReData

*

Annual Review | 15 ANNUAL REVIEW

Investor Origin Volume (M DKK) No. of transactions 1 AP Pension DK 2,503 2 2 IKEA SE 1,800 1 3 Northern Horizon Capital DK 1,500 1 4 CapMan FI 1,240 1 5 Koncenton DK 1,201 10 6 Quantum Immobilien DE 1,075 1 7 PenSam DK 1,062 2 8 Round Hill Capital GB 1,035 4 9 Swiss Life CH 1,004 2 10 PensionDanmark DK 952 1 Source: ReData

Figure 5: Top 10 investors 2023

Investor Origin Volume (M DKK) No. of transactions 1 Heimstaden SE 45,097 70 2 Niam SE 22,483 84 3 Koncenton DK 20,397 114 4 NREP DK 19,327 65 5 Patrizia DE 14,752 25 6 PFA Ejendomme DK 12,631 57 7 PensionDanmark DK 10,678 37 8 ATP Ejendomme DK 10,567 15 9 Orange Capital Partners NL 10,400 10 10 Jeudan DK 9,974 46 Source: ReData

Figure 6: Top 10 investors 2014-2023

several large transactions

are

included

data, which is

actual volumes

HOTEL RETAIL OFFICE LOGISTICS RESIDENTIAL

After the preparation of data for this publication,

from 2023 have been published. These

not

in the

why the

deviate slightly from the above.

We believe that buyers and sellers will continue to get closer to each other in the new year, which is why we will probably see more transactions.”

Mikkel Lieberkind Head of Projects, AP Ejendomme

86%

16 | RED Danish Investment Atlas 2024

Figure 7: How much should real estate make up of your total assets?

Figure 8: Have the interest rate increases in 2023 meant that your allocation in real estate has changed?

14%

Foto: Muus foto NO YES 0% 2% 4% 6% 8% 10% 12% PenSam Nordea Pension Ejendomme AP Pension Danica Pension Sampension AkademikerPension Industriens Pension 5% 7.5% 8% 8-10% 12%* 10-12% 10% * 9% in Danish properties and 3% in foreign properties

ARE INTEREST RATE INCREASES THE GOLDEN OPPORTUNITY FOR PENSION FUNDS?

The significant interest rate increases from 2022 continued into 2023, leading to diminished or completely disappearing benefits for leveraged investors. The worsened financing conditions made it challenging for geared investors to make profitable business plans, resulting in both increasing yield requirements and a significantly narrowed investor field.

After many years of competing for the assets, this scenario could potentially be a dream scenario for the equityfinanced pension funds, which could now once again become the highest bidders. The question is, therefore, whether the significant interest rate increases have become a golden opportunity for the pension funds?

To shed light on the subject, we have asked a number of the country’s largest pension funds about how their investment strategy has been affected by the new high interest rates, and based on the answers from the pension funds, it can be concluded that the significant interest rate increases did not become the golden opportunity for pension funds, which is due to several different factors.

The pension funds’ allocation to real estate is set as a share of their total asset base – and since six out of seven pension funds state that the increasing interest rates have not led them to change their allocation strategy ( figure 8), real estate must therefore continue to constitute 5-12% of their total asset base ( figure 7). However, to maintain balance in their accounts, pension funds must align the values of their properties against the values of their other assets. This implies that several pension funds have become overexposed to real

(…) We have slowed down the investment pace due to the market situation, and our allocation in absolute terms is affected by the denominator effect, as is the case with many others.”

Søren Møller-Larsson Head of Real Estate, AkademikerPension

estate, as the values of their other assets have fallen proportionally more than the values of their properties.

At the same time, the increased returns for alternative and more liquid investments have also resulted in increasing yield

requirements for real estate among the pension funds, but the sellers in the market have not been willing to adjust their price expectations accordingly.

Although pension funds have been able to execute quickly and without financing contingencies, several factors have thus put a brake on the pension funds’ investment activity. However, the appetite and allocation are still there, so when the price expectations are aligned and the risk-adjusted returns once again become competitive, we expect to see higher activity among Danish pension funds.

To gain a deeper insight into the pension funds’ strategies and considerations, we have conducted a more in-depth interview with Mikkel Lieberkind from AP Ejendomme, who was one of the pension funds that invested in real estate in 2023.

Continued on next page

Annual Review | 17 ANNUAL REVIEW

HOTEL RETAIL LOGISTICS RESIDENTIAL OFFICE

Continued from previous page

AP EJENDOMME Q&A

Which advantages do you have as an institutional investor compared to other investors in the market?

In the current market characterised by significant uncertainty, high interest rates, limited willingness to lend from financial institutions, substantial construction prices, geopolitical uncertainties, climate change, etc., we believe that AP Ejendomme, as an institutional investor, can benefit from several factors. For example, we are not forced to sell our assets in a market with high yield requirements, and the vast majority of our properties are financed with pure equity, which reduces our vulnerability to the interest rate increases we have experienced in recent years. This capital structure also

implies that when attractive investment opportunities arise, we can execute quickly without financing contingencies, which has proven to be reassuring for sellers requiring high transaction security.

How has your investment strategy changed in recent years?

Our primary investment strategy remains “Develop to Core,” with a focus on investments in larger growth cities in Denmark, combined with active portfolio management. Overall, our investment strategy is characterised by a strong ESG agenda, which applies to both new investments and the existing portfolio.

The investment strategy is continuously evaluated and has naturally evolved in line with the dynamics of the real estate market and the changing conditions during the past 1.5 years. An example of our strategy adapting to the market is our recent acquisition of Codanhus and KB32, which fall outside our primary “Develop to Core” strategy. Such adjustments to the strategy make sense for us in a market like the current one, where the costs and risks of a similar development property exceed what we can buy a standing asset for.

MIKKEL LIEBERKIND

Mikkel Lieberkind is Head of Projects at AP Ejendomme. Mikkel has a Master’s degree in Construction Management and Building Informatics from Aalborg University and previously worked as a Project Development Manager at MT Højgaard Projektudvikling.

AP Ejendomme, which is a subsidiary of the pension fund AP Pension, invests in both Danish and international properties across all segments, ranging from office and residential properties to logistics and retail properties. In 2023, AP Ejendomme became the largest investor in the Danish real estate market with their acquisition of two office properties, Codanhus and Kalvebod Brygge 32.

18 | RED Danish Investment Atlas 2024

Which segment(s) do you expect to experience the greatest investor interest in 2024?

We expect the greatest investor interest to be in residential and office properties on prime locations in the country’s largest cities, especially Copenhagen and central Aarhus. These areas are expected to experience population growth, high employment, and stable rent levels. Additionally, we expect that ESG performance will have an increasing importance for the investment interest.

Which factors do you expect to be decisive for the activity on the commercial real estate market in the coming year?

Interest rate fluctuations and interest levels

Since the summer of 2022, we have witnessed significant interest rate increases, and only now are we experiencing stabilisation of the interest rates. The significant interest rate increases have resulted in several investors using leverage, putting acquisitions on hold and having to cancel ongoing transaction processes. Only now are the central banks starting to signal stagnant interest levels, even though the fight against inflation still cannot be declared “won” with certainty. In connection with this, we, like many investors and financial institutions, expect that we will probably see a slight decrease in interest rates in 2024. A decrease in interest rates is expected to result in more investors being able to justify their business cases, which will probably be reflected in the activity.

ESG

We and the majority of the investors and tenants we speak with are already imposing requirements on ESG, sustainability certifications, energy efficiency, and CO2 emissions. In the coming year, we expect these requirements to become even more significant and

that ESG Due Diligence will play a much larger role in new investments. Furthermore, we expect a strong focus on identifying and reducing CO2 emissions from both operations and embedded sources. We also observe that several investors are currently expanding their organisations with specialised ESG expertise, which is also the case at AP Ejendomme.

Bid-Ask Spread

Especially 2022 and 2023 have been characterised by a very large “Bid-Ask Spread”, which we experience in certain cases, has become smaller at the end of 2023. We believe that buyers and sellers will continue to get closer to each other in the new year, which is why we will probably see more transactions.

(…) when attractive investment opportunities arise, we can execute quickly without financing contingencies, which has proven to be reassuring for sellers requiring high transaction security.”

Mikkel Lieberkind Head of Projects, AP Ejendomme

Annual Review | 19 ANNUAL REVIEW

HOTEL RETAIL LOGISTICS RESIDENTIAL OFFICE

NO TRANSACTIONS WITHOUT BELIEF IN THE FUTURE

FUNDAMENTALLY CHANGED

MARKET CONDITIONS

There is no doubt that the new higher interest rates challenged the real estate market again in 2023. However, what do the investors’ business plans actually look like under the new market conditions, and what will it take to make it more attractive for the investors to place their capital in real estate instead of other asset classes again?

Whether we are talking about real estate, bonds, stocks or other asset types, investment decisions will always be based on whether or not the investors expect that they can achieve a given return on their equity during a given period of time. The size of this return depends on the risk-free interest rate and the risks associated with the investment (a risk premium) – the greater the risks, the higher the risk premium.

While the risk-free interest rate is most often defined as the effective interest rate on government bonds, the risk premium depends on both the market risks, the illiquidity risks, the lease agreement risks and the reletting risks. In both the residential, office and logistics segments, the investors were able to generate attractive cash flows and large profits from sales for several years due to significant yield compressions, making it possible to sell the assets at higher prices than they were acquired at. Thus, the investors could achieve high returns on their equity, which was driven by the perfect combination of a low interest rate and low risks.

However, the market’s development in recent years has turned the investment landscape upside down, and the investors are now facing a market where both the risk-free rate and the risks have increased significantly;

The risk-free rate: The significant increases in the interest rates have led to i) an increase in the returns on bonds, ii) an increase in the financing costs associated with real estate investments, and iii) that it has become more challenging to obtain financing. As a result, the investors can no longer derive the same benefits from making leveraged investments in real estate.

Lease agreement risks: Private households and businesses are still doing well, but there is still uncertainty about the future, which could increase the risks of missing rent payments and the possibility of commercial tenants going bankrupt.

Reletting risks: Both the residential, office and logistics segments continue to be characterised by a strong underlying tenant demand. However, it is not expected that the demand (and thus the rent) will increase to the same extent as seen in recent years.

Illiquidity risks: The combination of the above factors has resulted in a decreasing investor demand from Danish as well as foreign investors, and consequently in a lower activity, highlighting the illiquidity associated with investments in commercial real estate.

Market risks : However, Denmark continues to be characterised by political stability and a strong national economy. Therefore,

investors consider Denmark to be a ’safe haven’ and an attractive market.

As a result of the increase in the interest rates and the higher risks, the yield requirements in both the residential, office and logistics segments have increased by approximately 100-125 basis points during 2023, and the prime yields are, therefore, respectively, 3.75%, 4.25% and 5.00% in today’s market.

The development in the market has also resulted in an increase in the investors’ requirements for their return on equity, and in today’s market, the majority of leveraged core investors operate with a return requirement of 9-11% for residential properties and 10-14% for office and logistics properties. To shed light on how the investors’ business plans unfold under the new market conditions, we have calculated the investors’ return on equity under a number of different scenarios below.

While scenario 1 is our benchmark scenario, one parameter is changed at a time in each of the following four scenarios. This is done to highlight the consequences of the changes – even though the investors’ return on equity depends on the combination of several different parameters. Furthermore, the changes are only described for the residential properties in the following texts. However, the return on equity for both residential, office and logistics properties in the various scenarios is shown in the tables on page 23.

All scenarios are based on an assumption of a five-year investment period and that a gearing of 60% can be achieved for residential properties and 50% for office and logistics properties.

20 | RED Danish Investment Atlas 2024

SCENARIO 1

STABILISED MARKET

Scenario 1 is our benchmark scenario for the following scenarios. In this scenario, we have calculated the investors’ return on equity, assuming that the investors expect the market to remain stable, which implies that it is assumed that the investors buy at the current yield levels and the rental income remains unchanged throughout the investment period (i.e., there is no increase in the market rent). In this scenario, the investors’ annual return on their equity will be 3.5%.

The investors’ requirements are thus approximately twice as high as the expected return in this scenario. This significant difference explains the low investment activity that we have witnessed in the past year and which we also expect to see in early 2024. Thus, the question is, what will it take for the risk-adjusted returns to become attractive again and for the investment activity to return?

Continued on next page

SCENARIO 2

HIGHER INITIAL YIELD

One of the primary reasons for the limited investment activity in the market is that the sellers are holding onto the historically low yield levels from 2021/2022. Scenario 2 is, therefore, based on the assumption that the sellers acknowledge that the current risk-adjusted yields are still too low (compared to the interest rate), resulting in upward pressure on yields across all three segments. In this scenario, investors are assumed to buy at yields that are 50 basis points higher than the current levels (i.e., at 4.25%). Although this scenario will require the sellers to adjust their price expectations quite significantly, the investors’ return on equity will only increase by approx. 1.2 percentage points to 4.8%.

LOWER INTEREST RATE

Investors in the market are increasingly expecting that the interest rates will decrease during 2024. However, at the same time, there is also consensus on not expecting that the interest rate will drop to the same low level as we saw a few years ago. Therefore, scenario 3 is based on the assumption that the interest rates will decrease by 50 basis points (i.e., to 3.40%, including the margin), which will increase the return on equity by 0.7 percentage points (i.e., to 4.3%). However, for this scenario, it should be noted that a lower interest rate will also lead to a lower return on alternative investments, and therefore, the investors will most likely also be willing to accept a lower return on their real estate investments.

Annual Review | 21 ANNUAL REVIEW

SCENARIO 3

HOTEL RETAIL LOGISTICS RESIDENTIAL OFFICE

YEARLY NPI RENTAL GROWTH

Scenario 4 is based on the assumption that the investors expect the rent to increase with inflation (i.e., a yearly increase of 2% over the investment period) - an estimation that many investors factor into their business plans across asset types and locations. In this scenario, the return on equity for residential properties increases by 3.9 percentage points to 7.4%. Although the return in this scenario becomes higher than in the previous two scenarios, this expectation alone is still not sufficient to meet the investors’ current return requirements (9-11%).

SCENARIO 5

RENTAL GROWTH HIGHER THAN NPI

In scenario 5, it is assumed that the investors have a slightly more positive outlook and now expect the rent levels to increase at an annual average of 4% over the investment period. This results in an increase in the return on equity by 7.5 percentage points to 11.0%. Thus, this scenario is the only one of the five scenarios that (viewed in isolation) meets the level of the investors’ return requirements in today’s market.

However, this scenario is only assessed to be realistic for modern logistics properties and residential properties located in Copenhagen, whereas we expect more limited growth in the market rent for office properties and for the less attractive properties within the residential and logistics segments. For investors with a long investment horizon, it can also be questioned whether an average rent increase of 4% for logistics properties is realistic, as these properties quickly become technically obsolete, which will be reflected in the rent over time (all other things being equal).

SCENARIO 6

A COMBINATION CAN KICKSTART THE MARKET

Based on the above scenarios, it can be concluded that if the investors do not expect a significant rent increase during their investment period, the investors cannot reach their return requirements if just one of the other scenarios unfolds. In fact, for the investors to reach their return on equity requirements in all segments, it will require a combination of the initial yields increasing, the interest rates dropping, and the investors to expect the rent to increase on par with the inflation (i.e., a combination of scenario 2-4) – and despite this, the return on equity for office and logistics properties is still in the very low end.

Thus, the real estate market still has a long way to go before being an attractive alternative to the other more liquid assets, and it will, therefore, be interesting to see when the investors can reach their return on equity requirements and to what extent the investment activity will then increase.

Finally, it should be noted that all of the above calculations are based on assumptions that the investors buy and sell at the same yield levels. However, there may be conditions for the individual property that result in the investors expecting to be able to sell the property at a lower yield than the property was bought (e.g., improving leasing situation, energy improvements in the property, etc.).

Continued from previous page 22 | RED Danish Investment Atlas 2024

SCENARIO 4

* The calculations do not account for potential capital gains.

Annual Review | 23 ANNUAL REVIEW SCENARIO STABILISED MARKET HIGHER INITIAL YIELD LOWER INTEREST RATE YEARLY NPI RENTAL GROWTH RENTAL GROWTH HIGHER THAN NPI A COMBINATION Net initial yield 3.75% 4.25% 3.75% 3.75% 3.75% 4.25% Interest rate 3.90% 3.90% 3.40% 3.90% 3.90% 3.40% Expected yearly rental growth 0.00% 0.00% 0.00% 2.00% 4.00% 2.00% Return on equity 3.5% 4.8% 4.3% 7.4% 11.0% 9.3% SCENARIO STABILISED MARKET HIGHER INITIAL YIELD LOWER INTEREST RATE YEARLY NPI RENTAL GROWTH RENTAL GROWTH HIGHER THAN NPI A COMBINATION Net initial yield 4.25% 4.75% 4.25% 4.25% 4.25% 4.75% Interest rate 3.90% 3.90% 3.40% 3.90% 3.90% 3.40% Expected yearly rental growth 0.00% 0.00% 0.00% 2.00% 4.00% 2.00% Return on equity 4.6% 5.6% 5.1% 7.7% 10.7% 9.2% SCENARIO STABILISED MARKET HIGHER INITIAL YIELD LOWER INTEREST RATE YEARLY NPI RENTAL GROWTH RENTAL GROWTH HIGHER THAN NPI A COMBINATION Net initial yield 5.00% 5.50% 5.00% 5.00% 5.00% 5.50% Interest rate 3.90% 3.90% 3.40% 3.90% 3.90% 3.40% Expected yearly rental growth 0.00% 0.00% 0.00% 2.00% 4.00% 2.00% Return on equity 6.1% 7.1% 6.6% 9.2% 12.2% 10.7%

RESIDENTIAL OFFICE LOGISTICS

HOTEL RETAIL OFFICE LOGISTICS RESIDENTIAL

RESIDENTIAL AND LOGISTICS:

ARE THE RISKS LOWER, OR ARE WE SIMPLY BEHIND?

Before a series of economic and geopolitical uncertainties slowed down the investment activity, the real estate markets in both Denmark, Sweden, Norway and Finland were characterised by an insatiable investor appetite and a significant yield compression in the core segments. However, the yield curve turned when interest rate increases challenged the historically low yield requirements.

Despite the Nordic countries being comparable in many ways, we have seen significant differences in the rate at which buyers and sellers have adapted to the changed market conditions across the Nordic region. The question now is whether the lower yield levels in Denmark reflect investors demanding a lower risk premium or if we, in reality, are simply lagging behind.

2.40% 2.90% 3.40% 3.90% 4.40% Q4 2023 Q1 2023 Q1 2022 Q1 2021 Denmark Finland Norway Sweden 3.20% 3.70% 4.20% 4.70% 5.20% 5.70% Q4 2023 Q1 2023 Q1 2022 Q1 2021 Denmark Finland Norway Sweden 24 | RED Danish Investment Atlas 2024

Figure 9: Prime yields – Residential properties in the Nordics

Figure 10: Prime yields – Logistics properties in the Nordics

Source: Cushman & Wakefield | RED

THE ADAPTION TO THE MARKET IS TAKING LONGER

In recent years, residential and logistics properties have been at the top of the global investors’ wish lists, and when looking at the yield development across the Nordic region, a trend in the pace of adaptation to the changing market conditions in the individual countries can be observed.

When the market was at its peak and characterised by significant competition and investor appetite, the yield for prime residential properties in Denmark was higher than in both Sweden, Norway and Finland. However, today, we see the opposite situation, where the prime residential yield in Denmark is approximately 35-55 basis points lower than in the rest of the Nordic region ( figure 9). Both during the upswing and the downturn, the market has thus adapted slower to the changed market conditions in Denmark than in the other Nordic markets.

In the logistics segment, we have observed the same trend, as there have also been larger price adjustments in our neighbouring countries than in Denmark. While the yields in Denmark have shifted by 100 basis points from early 2022 to the end of 2023, prime logistics yields in the rest of the Nordic region have moved by 145-185 basis points (i.e., 45-85 basis points more), despite starting from a lower level ( figure 10).

ARE WE COMING FROM A STARTING POINT THAT IS TOO HIGH?

The question now is whether the yield levels for prime residential and logistics properties in Denmark should increase to the same extent as seen in the rest of the Nordic markets or if the risk premium for investing in residential and logistics properties in Denmark should actually be lower than in the other Nordic markets?

FEW DISTRESSED SELLERS IN DENMARK

A significant reason why we have not seen the same price adjustments in Denmark as, for example, in Sweden is that there have been (and still are) few financially distressed sellers on the Danish market. This is because a large share of the property owners in

Denmark are investors with limited use of leverage. However, looking at the Swedish market, the increases in the interest rate have squeezed the owners much harder, as Swedish real estate companies in recent years have financed a large share of their acquisitions with corporate bonds, which had to be refinanced within a short period of time. During the market’s downturn, this has implied that the buyers on the Danish market have had to wait for the sellers to mature and for their price expectations to adjust, whereas the sellers on the Swedish market, to a greater extent, had to accept the prices, that the buyers were willing to pay.

THE SAFE AND LIQUID DANISH RESIDENTIAL MARKET

When looking at the residential market in isolation, the rent levels for prime properties in both Denmark and Sweden have historically been somewhat lower than in Norway and Finland. However, when the market was most attractive, the low rent levels in Sweden were offset by the fact that the yield levels for Swedish residential properties were 50 basis points lower than for Danish properties. This resulted in the market values per square meter being considerably lower in Denmark than in the rest of the Nordic region. Consequently, many investors expected (during the upswing) that we would see further yield compression for prime residential assets in Denmark, bringing yields closer to the levels seen in the other Nordic markets.

Moreover, the rental housing market in Denmark is currently characterised by a significant demand, as the high interest rates combined with the continued high condominium prices have created a high housing burden on the owner-occupied market, pushing residents into the rental market (read more on page 44 “Renting beats owning – for a little longer”). The fact that the residential yields are currently the lowest in Denmark could, therefore, also indicate that the Danish market is a ‘safe haven’ with high liquidity and strong demand.

UNREALISED POTENTIAL IN DANISH LOGISTICS PROPERTIES

Looking into the yield development in the logistics segment, we see many similar trends. Before the interest rate increases, the segment was characterised by a significant yield compression across the Nordic markets. Despite Denmark being a strong logistics hub with efficient access to Continental Europe, the yield levels were higher than in the other Nordic countries. Simultaneously, the rent levels for prime assets were significantly lower in Denmark than in Sweden, Norway, and Finland.

The higher yields in Denmark can partly be attributed to a lack of foreign capital. While it was first around 2020-2021 that foreign investors truly started paying attention to the Danish market, their interest in the logistics market in the other Nordic countries goes back way further. Thus, for a long period, international investors did not have the same focus on Denmark as on the rest of the Nordic region. The Danish market was, therefore, behind – both in terms of market rent and yield requirements.

ARE THE RISKS LOWER IN DENMARK?

During the downturn, the Danish market has proved superior. We have seen few distressed sellers in Denmark, the inflation fell significantly faster and to a lower level than in the rest of the Nordic region. Furthermore, the investors can obtain better financing terms in the Danish market, which also speaks for a lower yield (all else being equal). Finally, the occupier market in both the residential and logistics segments is strong in Denmark. While the Danish rental housing market is (and is expected to continue to be) characterised by significant demand, investors expect to see a continued undersupply of Danish logistics properties and, consequently, a future growth in the market rent.

So, is the Danish market just lagging behind, or are the risks associated with residential and logistics properties actually lower than in our Nordic neighbouring countries? We believe in the latter.

Annual Review | 25 ANNUAL REVIEW

HOTEL RETAIL LOGISTICS RESIDENTIAL OFFICE

EXPECTATIONS FOR 2024

After a challenging 2023 with headwinds, a frozen investment market, and the lowest transaction volume in nine years, we sensed a growing optimism from investors towards the end of the year.

In 2024, we expect to see reduced uncertainty in the market, leading to increased alignment between the buyers’ and the sellers’ price expectations and, consequently, a higher activity.

INCREASED ACTIVITY IN 2024

Following years of high uncertainty in the investment market, impacted by interest rate hikes and high inflation figures, we observed more sellers accepting the buyers’ price adjustments by the end of 2023 and that the investors had an increasing optimism and a belief in future interest rate cuts. Therefore, we expect to see decreasing uncertainty in the market and, as a result, a higher investment activity in 2024.

The increasing optimism and the expectation of increased investment activity among the investors is supported by our Q1 2024 investor survey, which shows that the share of investors who expect to buy more than they expect to sell has increased to 61%, which is equivalent to an increase of approximately 10%-points compared to the previous three surveys ( f igure 11).

Despite the growing investor optimism, we do not expect to witness the same volume as experienced up to the market turnaround. This is because the risk-adjusted return on real estate is still too low in the eyes of many investors, given the returns they expect from more liquid alternatives such as bonds and other types of loans, which will reduce

investors’ appetite and, consequently, their allocation to real estate.

RESIDENTIAL PROPERTIES REMAIN

THE INVESTOR’S FAVOURITE

Recent years’ yield compression in the residential segment implied that the yield had reached a level creating a significant gap between the buyers’ and sellers’ price expectations in the residential segment. This limited the investment activity with all types of residential properties in 2023. However, towards the end of the year, we observed sellers’ price expectations becoming more aligned, and in 2024, we therefore expect to see a higher activity in the investors’ always preferred property segment, the residential segment.

This expectation is further based on the fact that the owner-occupied housing market has maintained a surprisingly high price level, resulting in a housing burden that pushes residents from the owner-occupied market towards the rental market. Therefore, the residential rental market is expected to be in high demand – both for tenants and investors in the Danish market.

Our investor survey from early 2024 shows that investors also have great confidence

in the residential segment, as more than two-thirds of the respondents consider the residential segment as the segment with the best potential to perform well in the coming time ( figure 12).

THE GREEN TRANSITION GAINS MOMENTUM

In addition to a continued appetite for residential properties, we expect to see an increased focus on sustainability in 2024. This expectation is based on the observation that across asset classes, both tenants and owners are increasingly focusing on sustainability. Our investor survey from Q1 2024 further shows that more than four-fifths of respondents have an ESG strategy from which they see several commercial benefits. The majority of investors believe that initiatives implemented through ESG strategies contribute to improving the value of their properties ( figure 13). Furthermore, almost half of the investors expect that a focus on sustainability will i) increase demand from tenants, ii) ensure their organisation’s longterm success, and iii) secure the company against future regulatory requirements.

Continued on next page

Despite the growing investor optimism, we do not expect to witness the same volume as experienced up to the market turnaround. This is because the risk-adjusted return on real estate is still too low in the eyes of many investors, given the returns they expect from more liquid alternatives such as bonds and other types of loans, which will reduce investors’ appetite and, consequently, their allocation to real estate.”

Nicholas Thurø Managing Partner, Capital Markets, RED

26 | RED Danish Investment Atlas 2024

ANNUAL REVIEW

Q1 2024

Q3 2023

Q1 2023

Q3 2022

Increase – more acquisition the disposal

Stable – as much disposal as acquisition

Decrease – more disposal than acquisition

We get more favourable financing conditions

We believe that it improves the occupier demand (i.e., lower vacancy, higher rent levels)

We find it important to secure our organisations’ long-term success (i.e., trust/credibility, customer loyalty, attracting talent, competitive advantage, etc.)

We secure ourselves against future requirements from the authorities

We believe that it improves the value of the properties (i.e., lower yield requirements)

Q3 2022 Q1 2023 Q3 2023 Q1 2024 0% 10% 20% 30% 40% 50% 60% 70% Hotel Retail Office Logistics Industrial Residential 61% 50% 49% 51% 30% 39% 42% 32% 9% 11% 9% 17% 49% 49% 34% 62% 46% Annual Review | 27 ANNUAL REVIEW

Figure 11: Investor Confidence Index - Portfolio size

What is your objective with regard to the size of your portfolio in terms of acquisition/disposal during the coming six months?

Figure 12: Investor Confidence Index - Segment with best potential

Which segment do you consider to have the best potential to perform well during the coming six months?

Figure 13: Investor Confidence Index – Commercial advantages of ESG Strategy

Which commercial advantages do you think are the most important of implementing an ESG strategy?

HOTEL RETAIL LOGISTICS RESIDENTIAL OFFICE

Continued from previous page

EXPECTATIONS OF STABLE YIELD LEVELS

After a long period with an upward pressure on the yields, sellers’ price expectations began to align by the end of 2023. Therefore, we expect yield levels across segments to have found their new level and thus to remain more or less stable in 2024. However, global trends and expectations of increasing risks in the office segment could put upward pressure on yield requirements for office properties – despite fundamental differences between the office market in Denmark and other countries.

The expectation of stable yield requirements is supported by our investor survey, which shows that investors at the beginning of 2024 have become more optimistic about how they expect the value of their portfolio to develop in the next six months ( figure 14).

While 60% of investors expect the value of their portfolio to remain stable, almost a third expect their portfolio value to increase.

INCREASED ECONOMIC STABILITY

After a longer period with macroeconomic fluctuations and worsened financing conditions, there are prospects for a more stable macroeconomic environment in 2024 due to lower inflation rates and expectations of stable, potentially declining interest rates.

When asked about their expectations for their future financing conditions, investors are significantly more optimistic than before ( figure 15). In the previous surveys, more than half of the respondents expected worsened conditions, and this share has now fallen to a quarter. Simultaneously, the same share of investors expects improved

financing conditions, while half of the investors expect their financing conditions to remain unchanged in the coming time.

As also seen in 2023, the development of interest rates will be crucial for investor appetite and activity in 2024. Therefore, Danske Bank’s Chief Economist, Las Olsen, will provide his insights into how interest rates are expected to evolve in 2024 and how it will impact the real estate market.

The Cushman & Wakefield | RED Investor Confidence Index

The index monitors 115 of the most active investors’ expectations for the Danish commercial real estate market during the coming six months. The broad coverage ensures that the findings are representative reflections of the investors’ confidence in the Danish market. By conducting the survey on a biannual basis, we are also able to track changes in the confidence.

31% 8% 26% 17% 15% 13% 8% 60% 43% 48% 40% 43% 48% 37% 28% 9% 49% 26% 55% 40% 37% 50% 64% 28 | RED Danish Investment Atlas 2024

Figure 14: Investor Confidence Index – Portfolio value

How do you see the value of your portfolio developing during the coming six months?

Figure 15: Investor Confidence Index – Financing conditions

Q1 2024 Q1 2024 Q3 2023 Q3 2023 Q1 2023 Q1 2023 Q3 2022 Q3 2022 Increasing Unchanged Declining Improved conditions Unchanged conditions Worsened conditions

What is the future outlook for your financing compared with your current financing? (In terms of the financing of new acquisitions or the refinancing of your existing properties)

DANSKE BANK Q&A

How do you expect the short- and longterm interest rates to develop in 2024?

It is, of course, very uncertain, but we believe that the ECB will gradually normalise the interest rate level because inflation is under control. On the other hand, one does not want to risk inflation flaring up again, and there are still significant wage increases that can push prices up. Our main scenario is that the first interest rate cut of 25bp will come in the second quarter and that two more will follow before the end of the year. Long-term interest rates may decrease slightly as the interest rate cuts are implemented, but, in principle, we do not expect much.

How do you expect the developments in financial markets will affect the real estate market?

The yield requirements for some properties decreased quite sharply during the period with very low interest rates, and now there is an adjustment (red: in yield requirements) in progress to the higher interest rate level. Since we do not expect significant declines, especially in long-term interest rates in 2024, it could look like this adjustment will continue. On the other hand, we also believe that interest rates have peaked for this time, and it may provide a bit more stability in the market in the longer term - for example, in 2025.

Do you expect the ESG profile of companies and properties to affect investors’ financing conditions in the coming year?

In the future, a company’s ESG profile and a property’s energy efficiency will be part of the credit rating, just like the other key elements in the company’s performance. For real estate investors, this means that, in the slightly longer term, companies are expected to regularly report on ESG, and the companies are expected to have a plan for ESG, including a plan for reducing CO 2 emissions property by property. The answer is, therefore, “yes” – in the slightly longer term, there will be differences in financing conditions depending on the ESG profile and the energy efficiency of the property.

In the future, a company’s ESG profile and a property’s energy efficiency will be part of the credit rating, just like the other key elements in the company’s performance.”

Las Olsen Chief Economist, Danske Bank

LAS OLSEN

Las Olsen is Chief Economist at Danske Bank. Las Olsen has been with Danske Bank since 2007 and has a master’s degree in Economics from the University of Copenhagen.

Danske Bank is a Nordic bank headquartered in Denmark. The bank, which is the largest in Denmark, has customers in ten countries and advises both private and business customers as well as institutional customers.

Annual Review | 29 ANNUAL REVIEW

HOTEL RETAIL LOGISTICS RESIDENTIAL OFFICE

RED facilitated the sale of a property with 28 residential units and a grocery store located at Vesterbrogade 162/Platanvej 32 on the border between Vesterbro and Frederiksberg.

30 | RED – Danish Investment Atlas 2023

RESIDENTIAL

32 34 38 40

Volume & Investors

Geographical Distribution

Top 5 Transactions 2023

Interview: Both Pros and Cons in the Danish Residential Market

Interview: The Developers’ Business Plans Are Challenged

Highlight: Renting Beats Owning – For a Little Longer

Highlight: A Capital Gains Tax of 50% Can Be the Solution

Expectations for 2024

Transactions & Key Figures

Residential | 31 RESIDENTIAL

50 HOTEL RETAIL LOGISTICS ANNUAL REVIEW OFFICE

42 44 46 48

A SIGNIFICANTLY LOWER ACTIVITY

Since 2015, the residential segment has been the investors’ most preferred real estate segment, and it remained so in 2023. With a total transaction volume of DKK 16.8 bn, the residential properties accounted for 39% of the total volume ( figure 18). Despite the residential segment maintaining its position as the investors’ most preferred segment, the investment activity decreased by 59% in 2023 compared to the previous year, and we must go back to 2014 to see a lower transaction volume in the segment.

CONTINUED INTEREST IN ALL TYPES

The decline in transaction volume in 2023 should not be seen as an expression of a lack of investor appetite for residential properties but rather that substantial interest rate increases coupled with limited yield adjustments within the segment made it challenging for buyers and sellers to meet.

While investors in the other segments in the search for higher yields can search either for secondary locations or for the more risky asset types within the segments (e.g. for big box in the retail segment), the difference in the risk premium for residential properties is smaller. This means that the volume is

limited by investors not being able to look to alternative residential investments to the same extent but instead having to wait for sellers’ price adjustments.

DANISH INVESTORS DOMINATE AGAIN

Foreign investors dominated the residential segment in 2022, but the situation reversed in 2023, as Danish capital was behind 66% of the total investment volume ( figure 16). Although Danish capital dominated the segment, three out of the top five investors were foreign ( figure 19), and four out of the five largest transactions were carried out by foreign investors.

Source: ReData

”THE BIGGER, THE BETTER” IS OVER

Before increases in the interest rates affected the market, the residential segment was characterised by an insatiable investor appetite, where portfolios and volumes could not be large enough. However, last year, we observed that investors were more cautious with larger investments and instead wanted risk diversification, which is reflected in the fact that both the number of transactions and the total volume fell proportionally more in the transactions with higher volume than in the transactions with lower volume ( figure 17).

16.8 BN DKK RESIDENTIAL VOLUME 2023 VENDORS INVESTORS Asset deals 37% Foreign 8% Share deals 63% Danish 92% Foreign 34% Danish 66% 32 | RED Danish Investment Atlas 2024

Figure 16: Origin of the investors & transaction structure 2023

Price range (M DKK) No. of transactions Volume (M DKK) 2022 2023 2022 2023 0 - 50 1,734 1,144 7,754 4,822 50 - 150 32 32 2,883 2,830 150 - 250 23 12 4,302 2,180 250 - 500 19 3 6,037 1,131 > 500 16 6 19,940 5,838 Total 1,824 1,197 40,915 16,802

Figure 17: Residential – Breakdown in price range 2023

RESIDENTIAL VOLUME

& INVESTORS Source: ReData

0 10 20 30 40 50 60 70 2023 2022 2021 2020 2019 2018 2017 2016 2015 2014 Danish BN DKK Foreign Source: ReData 60% 37.6 40% 51% 35.0 49% 54% 44.2 46% 53% 63.3 47% 57% 40.9 43% 34% 16.8 66% 38% 27.7 62% 41% 28.6 59% 37% 20.3 63% 23% 11.0 77% Residential | 33 RESIDENTIAL

Figure 18: Residential – Transaction volume 2014-2023

Investor Origin Volume (M DKK)* No. of transactions 1 Northern Horizon Capital DK 1,500 1 2 CapMan FI 1,206 1 3 Koncenton DK 1,186 10 4 Quantum Immobilien DE 1,075 1 5 Round Hill Capital GB 1,014 4 Source: ReData

Figure 19: Residential – Top 5 investors 2023

Investor Origin Volume (M DKK)* No. of transactions 1 Heimstaden SE 44,233 73 2 Koncenton DK 19,870 121 3 Niam SE 12,868 59 4 Patrizia DE 11,132 19 5 Orange Capital Partners NL 9,949 10 Source: ReData

HOTEL RETAIL LOGISTICS ANNUAL REVIEW OFFICE

Figure 20 : Residential – Top 5 investors 2014-2023

* The stated volumes are for the residential part only, which is why any other uses in mixed properties are not included in the volume.

COPENHAGEN 6.1 BN DKK 36% COPENHAGEN Danish 30% 70% Foreign Investor distribution Danish Foreign Investor distribution Danish Foreign Investor distribution 10% 70% 20% AARHUS 2.7 BN DKK 16% OTHER ZEALAND 98% 54% 32% 14% 1.6 BN DKK 10% GREATER COPENHAGEN 25% 37% 48% 15% 75% Old housing Danish 30% 70% Foreign Investor distribution Investor distribution Danish Foreign Investor distribution Danish Foreign Investor distribution Danish Foreign Investor distribution Danish Foreign Investor distribution 5.5 BN DKK 33% OTHER JUTLAND AND FUNEN 85% 49% 30% 21% 0.9 BN DKK 5% AARHUS 89% 19% 48% 33% 2.7 BN DKK 16% OTHER ZEALAND 98% 54% 32% 14% 1.6 BN DKK 10% GREATER COPENHAGEN 25% 37% 48% 15% 16.8 BN DKK Danish 34% Foreign 100% 66% 75% Old housing stock 19% 6.1 BN DKK 36% COPENHAGEN Danish 30% 70% Foreign Investor distribution Investor Danish Foreign Investor distribution Danish Foreign Investor distribution 10% 70% 20% AARHUS 2.7 BN DKK 16% OTHER ZEALAND 98% 54% 32% 14% 1.6 BN DKK 10% GREATER COPENHAGEN 25% 37% 48% 15% 16.8 VOLUME Others 33% Danish 66% 75% Old housing stock 19% Danish 30% 70% Foreign Investor distribution Danish Foreign Investor distribution Danish Foreign Investor distribution Danish Foreign Investor distribution Danish Foreign Investor distribution 5.5 BN DKK 33% OTHER JUTLAND AND FUNEN 85% 49% 30% 21% 0.9 BN DKK 5% AARHUS 89% 19% 48% 33% 2.7 BN DKK 16% OTHER ZEALAND 98% 54% 32% 14% 1.6 BN DKK 10% GREATER COPENHAGEN 25% 37% 48% 15% BN DKK Danish 34% Foreign 100% 66% 75% Old housing stock 19% 6.1 BN DKK 36% COPENHAGEN Danish 30% 70% Foreign Investor distribution Danish Foreign Investor distribution Danish Foreign Investor distribution 10% 70% 20% AARHUS 19% 2.7 BN DKK 16% OTHER ZEALAND 98% 54% 32% 14% 1.6 BN DKK 10% GREATER COPENHAGEN 25% 37% 48% 15% 75% Old housing 6.1 BN DKK 36% COPENHAGEN Danish 30% 70% Foreign Investor distribution Investor distribution Danish Foreign Investor distribution Danish Foreign Investor distribution Danish Foreign Investor distribution 10% 70% 20% 5.5 BN DKK 33% OTHER JUTLAND AND FUNEN 49% 30% 21% 0.9 BN DKK 5% AARHUS 89% 19% 48% 33% 2.7 BN DKK 16% OTHER ZEALAND 98% 54% 32% 14% 1.6 BN DKK 10% GREATER COPENHAGEN 25% 37% 48% 15% 16.8 BN DKK RESIDENTIAL VOLUME IN TOTAL Others 33% Market rent 48% Danish 34% Foreign 100% 66% 75% Old housing stock 19% 34 | RED Danish Investment Atlas 2024 Source: ReData MARKET RENT OLD HOUSING STOCK OTHERS RESIDENTIAL

GEOGRAPHICAL DISTRIBUTION

KEY FIGURES FOR ASSET TYPES

MARKET RENT

OLD HOUSING STOCK

*

OTHERS

Residential | 35 RESIDENTIAL

The value is impacted by the sale of a number of larger transactions with properties located outside Aarhus and in other regional growth cities.

The properties are characterised by very different characteristics, which is why the price per m² or the change herein is not shown. RESIDENTIAL

**

AREA NO. OF PROPERTIES VOLUME (M DKK) AVG. VOLUME (M DKK) WEIGHTED PRICE PER M² 2023 Δ 2022-2023 Copenhagen 13 4,246 326.6 45,300 -4% Greater Copenhagen 4 776 194.1 31,700 -6% Other Zealand 15 863 57.6 28,900 7% Aarhus 6 441 73.6 33,800 -14% Other Jutland & Funen 45 1,673 37.2 23,400* 23% Total 83 8,000 96.4 34,600 -7%

AREA NO. OF PROPERTIES VOLUME (M DKK) AVG. VOLUME (M DKK) WEIGHTED PRICE PER M² 2023 Δ 2022-2023 Copenhagen 28 1,187 42.4 26,100 -22% Greater Copenhagen 24 233 9.7 20,600 -18% Other Zealand 93 362 3.9 10,500 15% Aarhus 13 302 23.2 23,500 -25% Other Jutland & Funen 382 1,144 3.0 8,000 -11% Total 540 3,229 6.0 13,200 -3%

AREA NO. OF PROPERTIES VOLUME (M DKK) AVG. VOLUME (M DKK) WEIGHTED PRICE PER M² 2023 Δ 2022-2023 Total 634 5,573 8.8 N/A** N/A** HOTEL RETAIL LOGISTICS ANNUAL REVIEW OFFICE

GEOGRAPHICAL DISTRIBUTION

DECLINING ACTIVITY NATIONWIDE

Despite investors continuing to show significant interest in residential properties, investment activity declined in all geographical areas from 2022 to 2023 ( figure 21). This is mainly because the recent years’ yield compression had resulted in extremely low yield levels for residential properties across the country, making it more challenging to finance residential properties with the new higher interest rates. At the same time, the solid underlying conditions in the rental market also made it attractive for owners to keep their properties and instead get a reasonable cash flow, which caused the sellers to be unwilling to adjust their price expectations sufficiently to meet the buyers.

AARHUS LOSES TO COPENHAGEN

2023 also marked a year where we observed clear differences between the areas. Historically, Aarhus and Copenhagen have followed each other closely, but while the rental market in Copenhagen continued at a high pace in 2023, the completion of many new buildings in Aarhus resulted in a pressure on the rental market. This development is reflected in the fact that the investment activity and the prices per m² fell more in Aarhus than

in Copenhagen. As a result, residential properties in Copenhagen are now traded at an average price that is 34% higher than in Aarhus (see table on p. 35).

The fact that Aarhus and Copenhagen no longer follow the same trends is further reflected in foreign investors’ allocation of capital. While Danish investors were solely dominant in the “rest of Denmark” in 2022, they were dominant in all areas except Copenhagen in 2023. Thus, we once again witnessed a “flight to safety,” with foreign investors allocating their capital to the central areas where the risk is assessed to be the lowest.

OTHER ASSET TYPES ARE DRIVING THE MARKET

For the regions “Other Zealand” and “Other Jutland and Funen,” the increase in prices per m² reflected a completely opposite trend compared to the general market, primarily because the activity was driven by different asset types than previously.

While the volume in previous years was largely dominated by transactions with properties located across “Other Zealand”

and “Other Jutland and Funen”, the activity in 2023 was driven by the sale of several prime properties located in the most attractive cities of the areas (including suburbs of Aarhus, Odense, Rungsted, Birkerød, etc.) as well as the sale of NREP’s care homes.

THE WAITING PERIOD DESTROYS INVESTORS’ BUSINESS PLANS