THE IMPACT OF THE TAX REFORM ACT OF 1986 ON THE INTERNATIONAL COMPETITIVENESS OF SERVICE INDUSTRIES

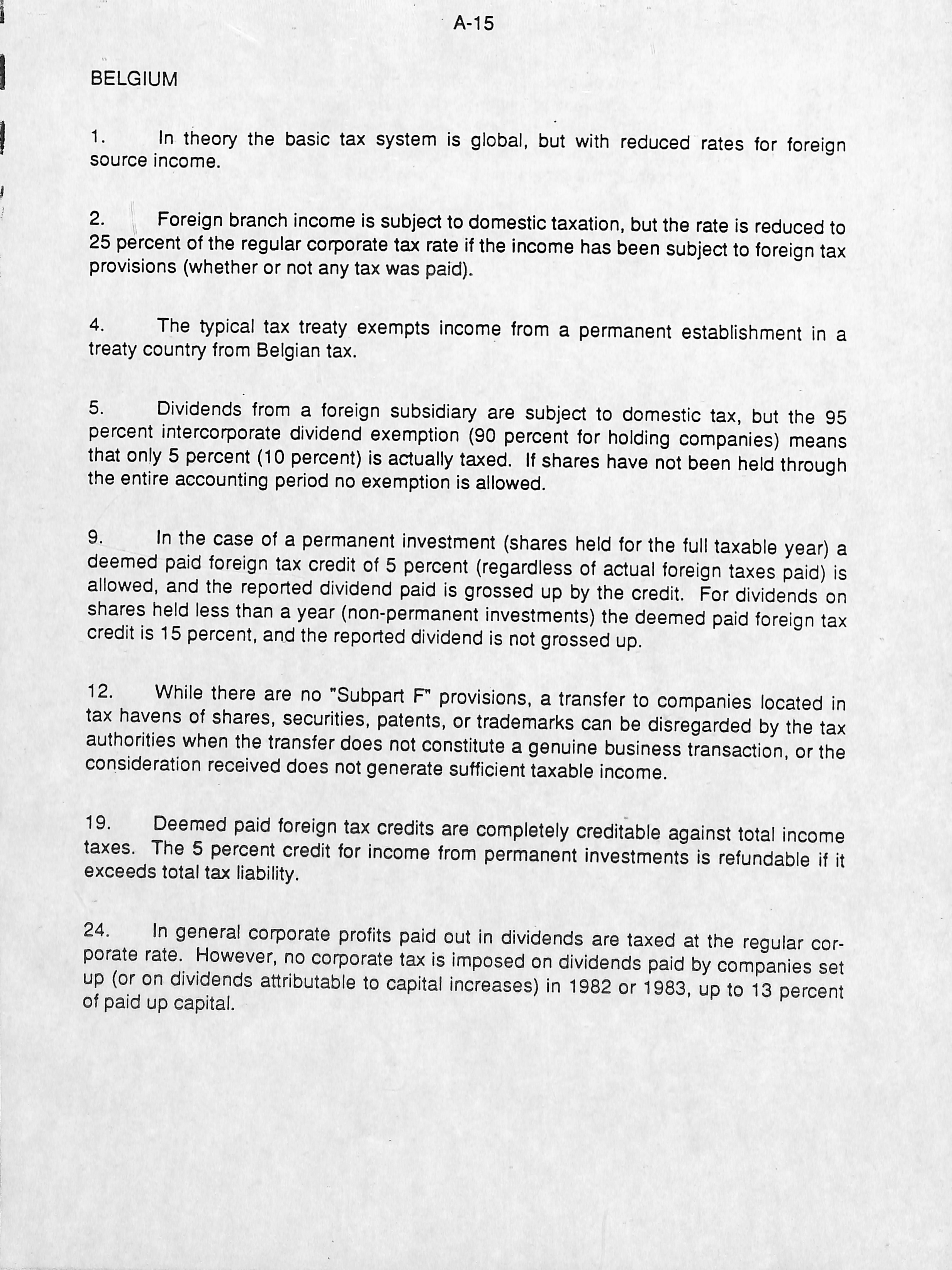

^ , Biblíofeca San Puctto Uico

Thomas Horst

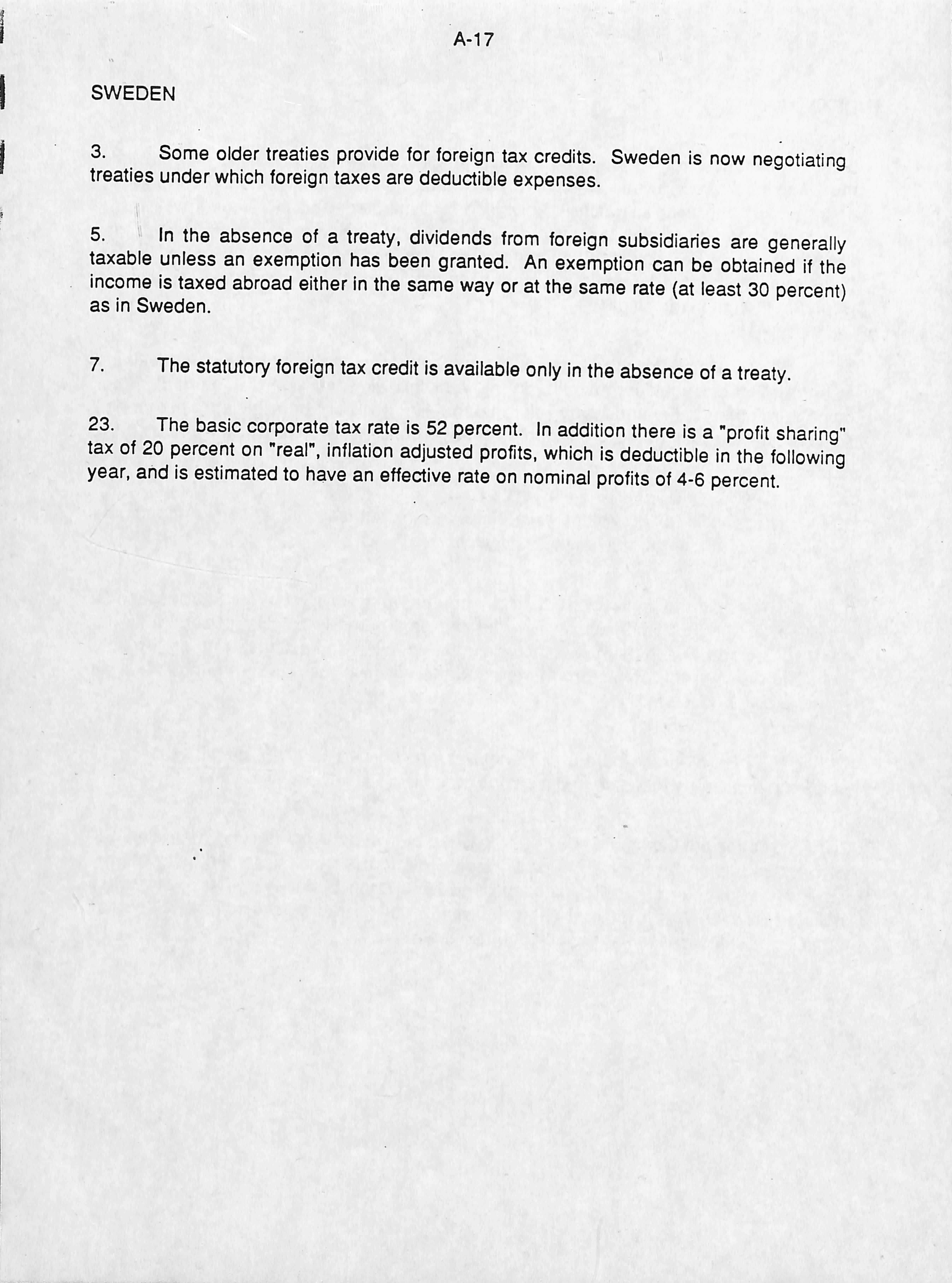

Deloitte Haskins & Sells

William R. Cline

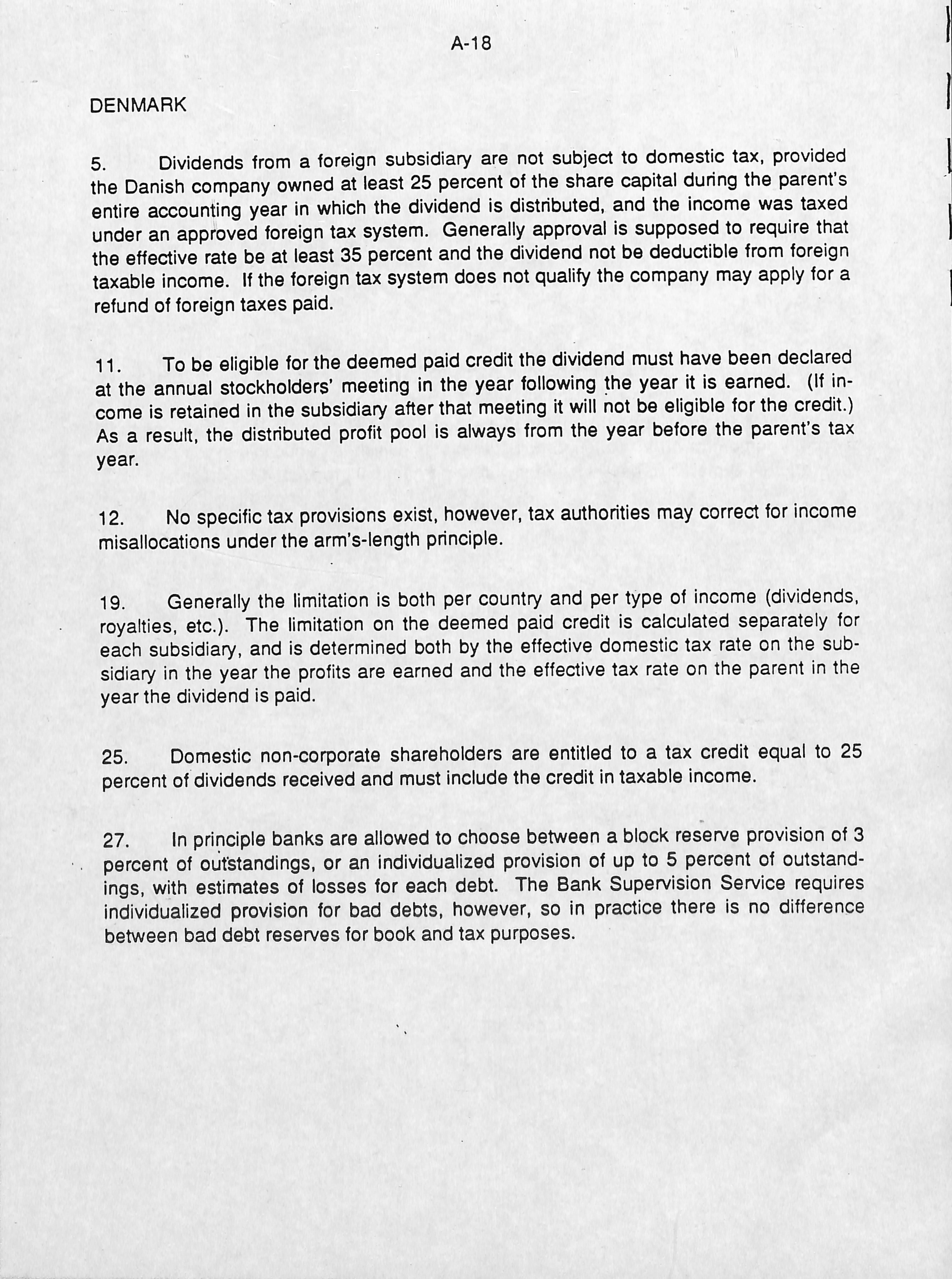

January 1988

This report was preparad for the Coalition of Service Industries, Washington, D.C. by Thomas Horst and William R. Cline.

The Coalition of Service Industries, established in 1982, is the oniy national organization representing the interests of the U.S. service sector. Its members are among the largest service corporations in the United States, and include:

American Express Company

American Intemational Group

ARA Services, Inc.

Arthur Andersen & Company

Bechtel Group, Inc.

Beneficia! Corporation

Chase Manhattan Bank, N.A.

Chubb Corporation

Citicorp/Citibank

Coopers & Lybrand

Interpubiic Group of Cos.

Marsh & McLennan, Inc.

Peat Marwick Main & Co.

Sea-Land Corporation

Additionally, the following companies participated in the study: Akin Gump. Strauss Hauer & Feid, Continental Corporation, Dun & Bradstreet Corporation, The First Boston Corporation, Johnson & Higgins and Cigna Corporation. ^

^^aístradón

About the Authors

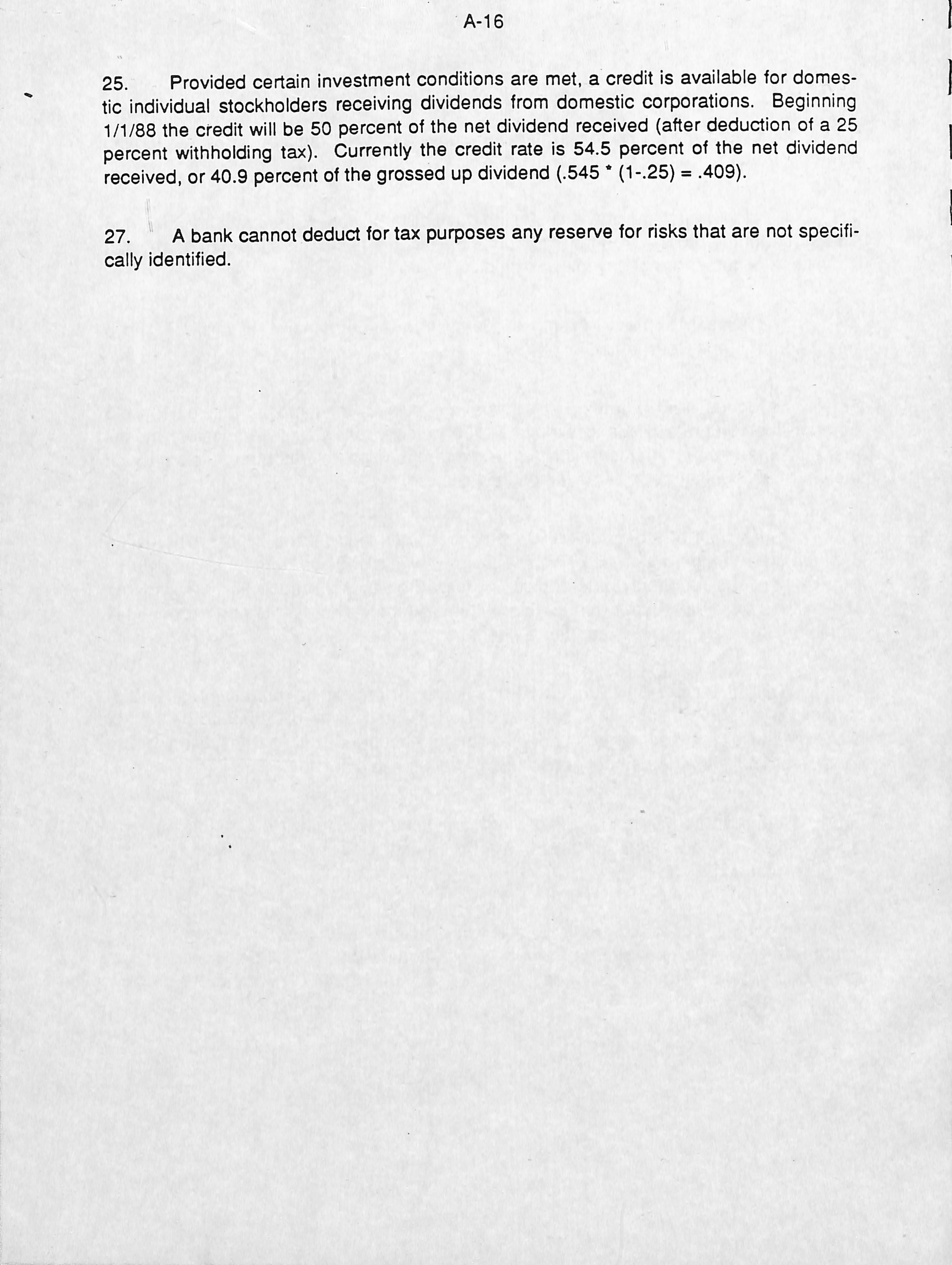

Thomas Horst, a director in the Washington, D.C. office of Deloitte Haskins & Seíls holds a Ph.D. in economics. A former faculty member of Harvard University from 1977 to 1981 he served as Director of the U.S. Treasury Departmenfs intemational tax staff which was responsible for economic analysis of intemational tax issues. Dr. Horst is the author of numerous books and articles on intemational economics and taxation.

William R. Cline is Sénior Fellow at the Institute for Intemational Economics, Washington, D.C. He holds a Ph.D. in economics from Yaie University. He was for mer^ assistant professor at Princeton University, a Ford Foundation visiting professor at the Brazilian Planning Ministry and University of Sao Paulo, Deputy Director for rade and Development Research at the U.S. Treasury, and Sénior Fellow at th'b Brookings Institution. He is the author of numerous books and articles on intemational finance and foreign trade. He participated in this study in a personal capacity, and views expressed herein should not be attributed to the Institute for Intemational Economics.

Part I

Part III

Appendix A

Appendix B

Appendix C

Appendix D

Appendix E

Appendix F

Appendix G

Appendix H

List of Tablea.

Executive Summary.

laxes and U.S. Competitiveness in the Services industries: Overview

Impact of Tax Reform Act on Rate of Return and Comparison to Foreign Tax Systems

The Impact of Tax Changes on U.S. Services Exports and Foreign Affiliate Salea

Footnotes to International Tax Survey

Advertising Agencies

Commercial Banking

Investment

Banking

Insurance

Ocean Shipping

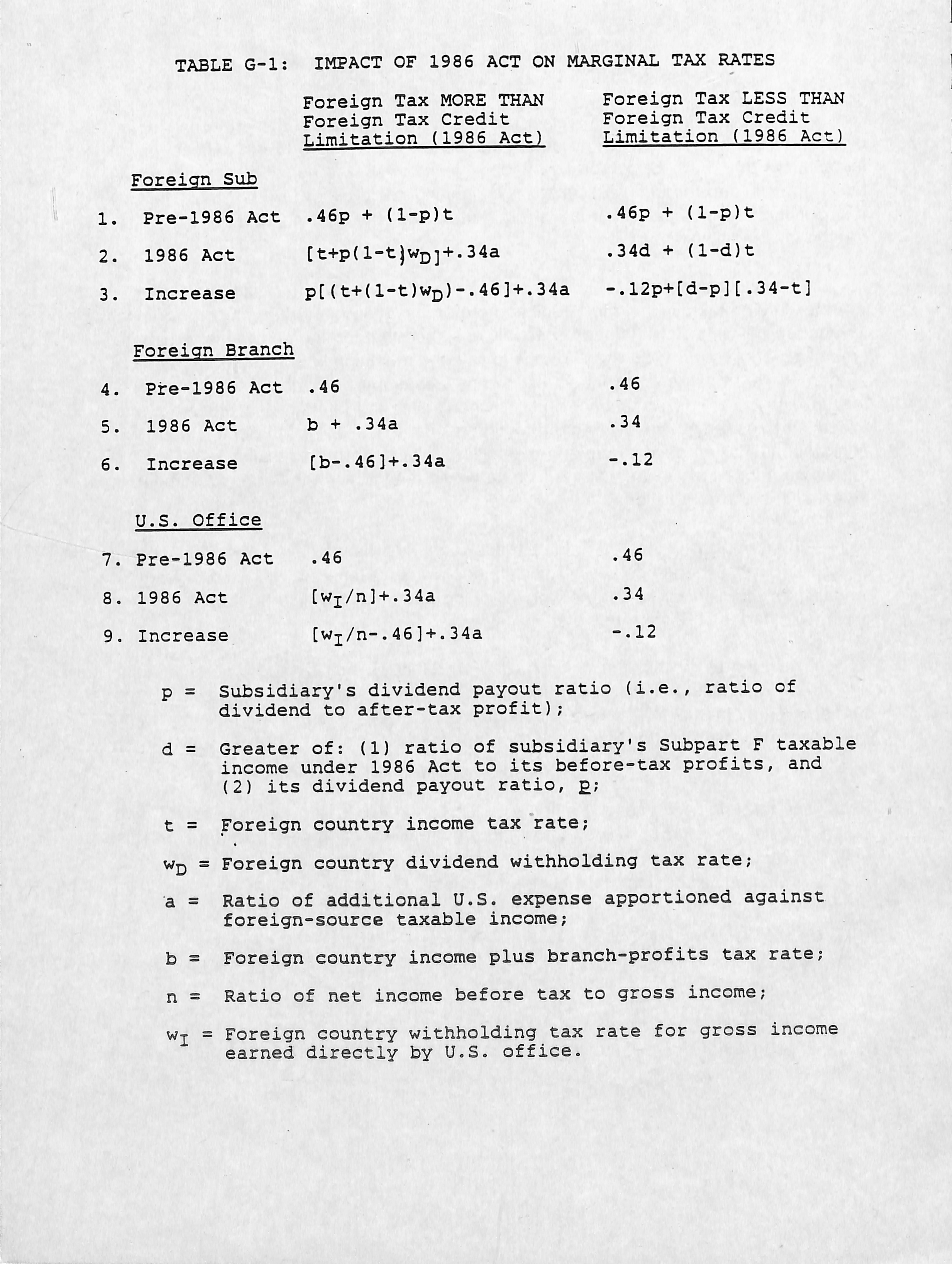

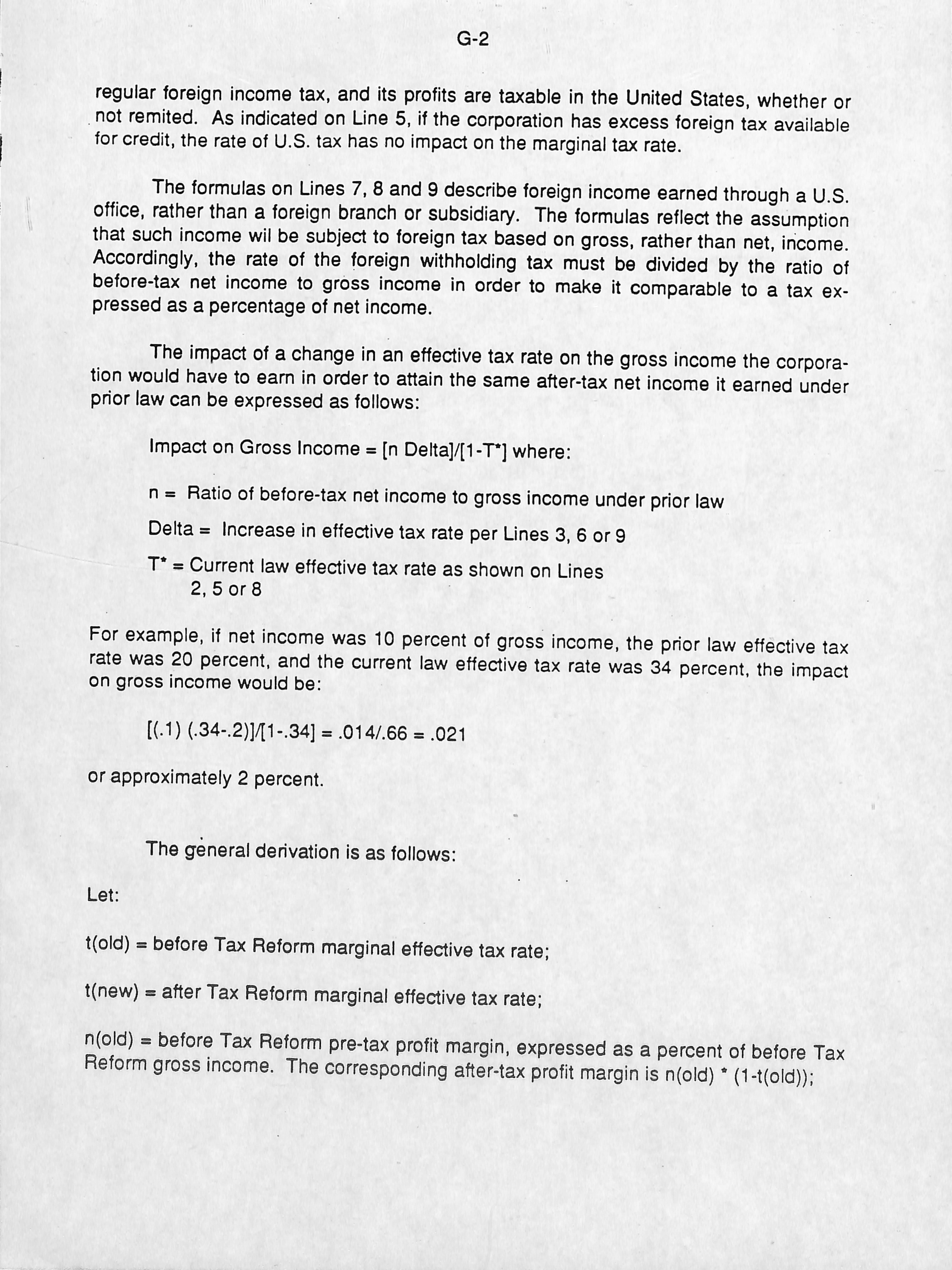

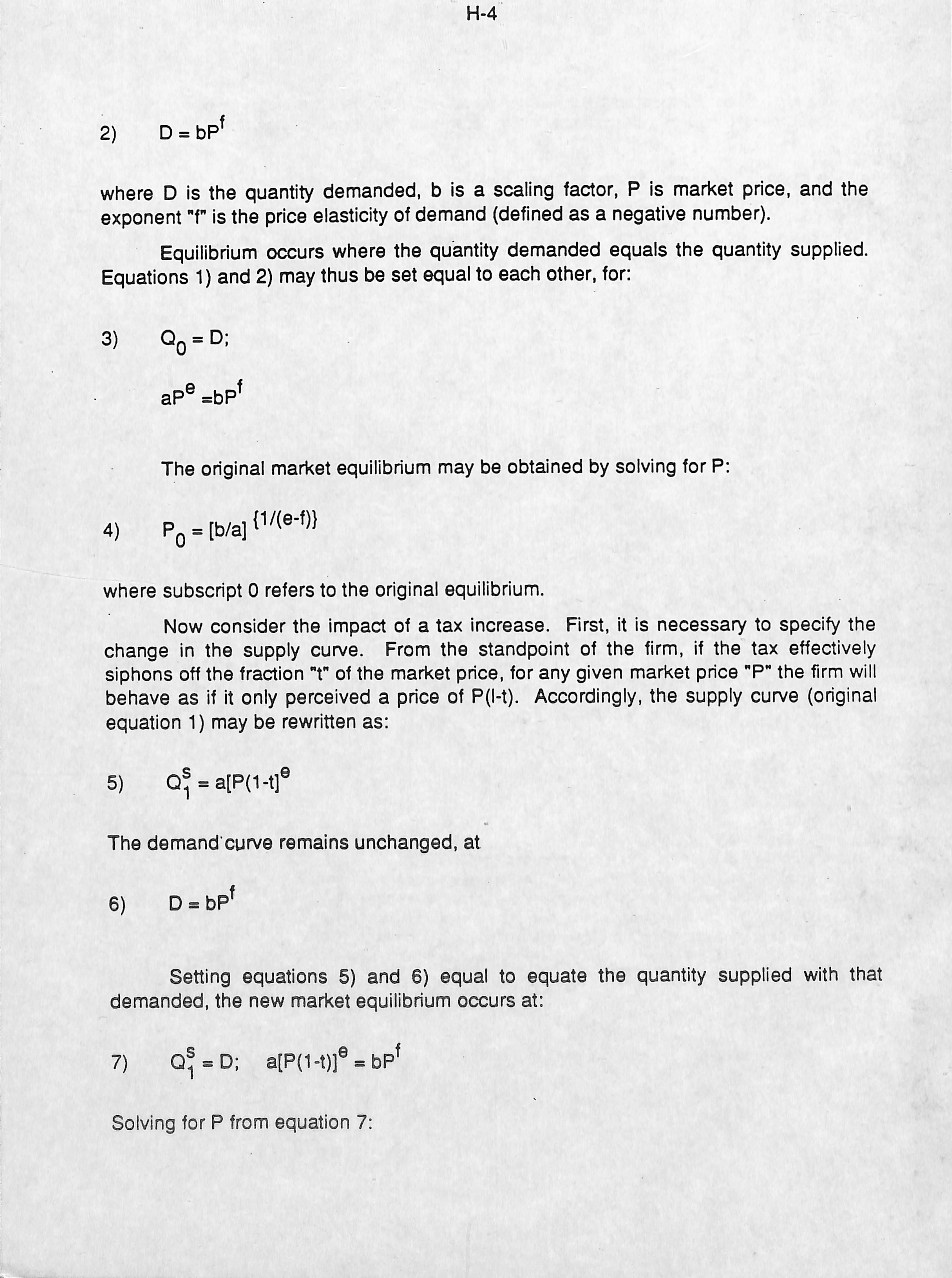

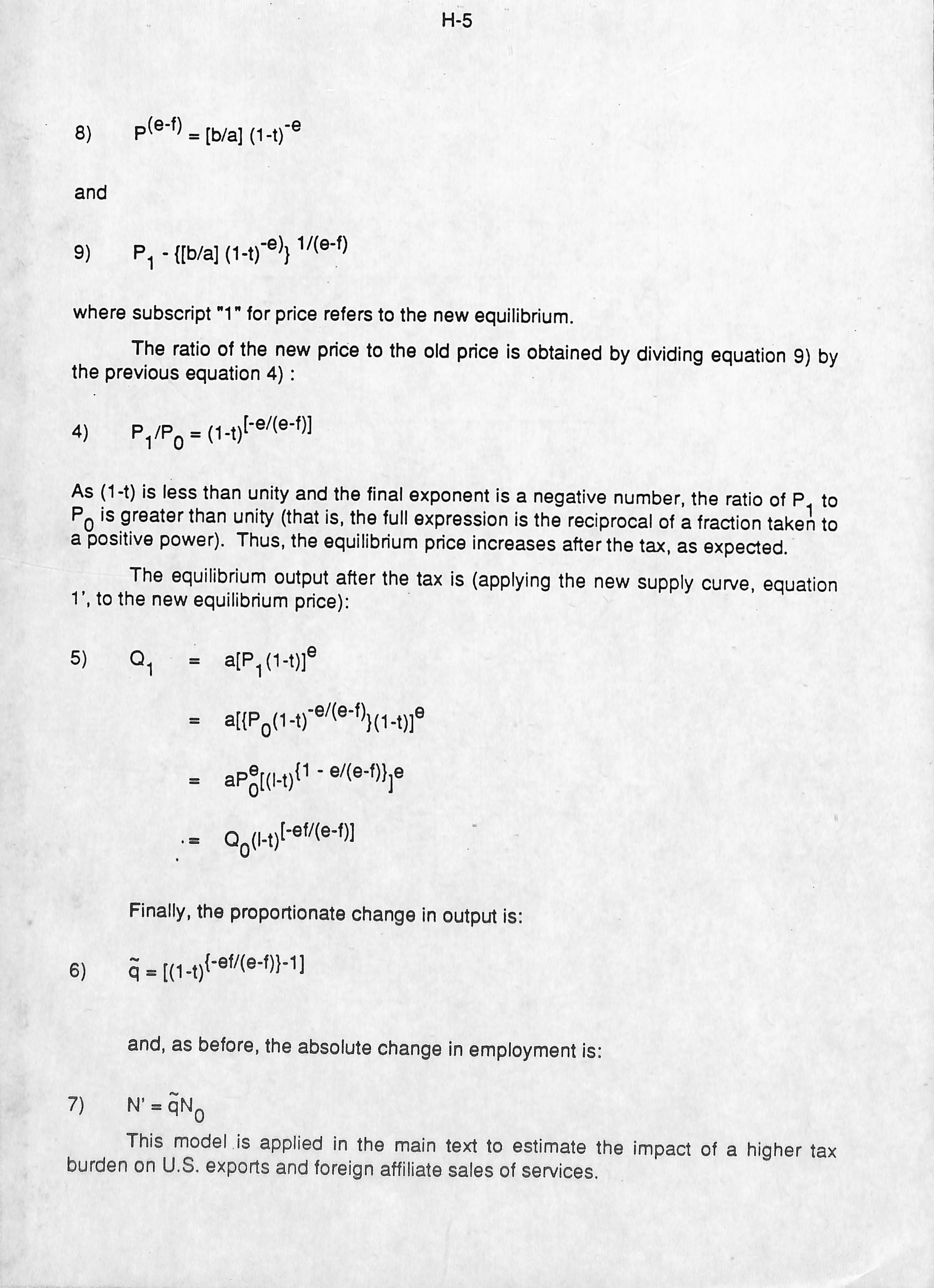

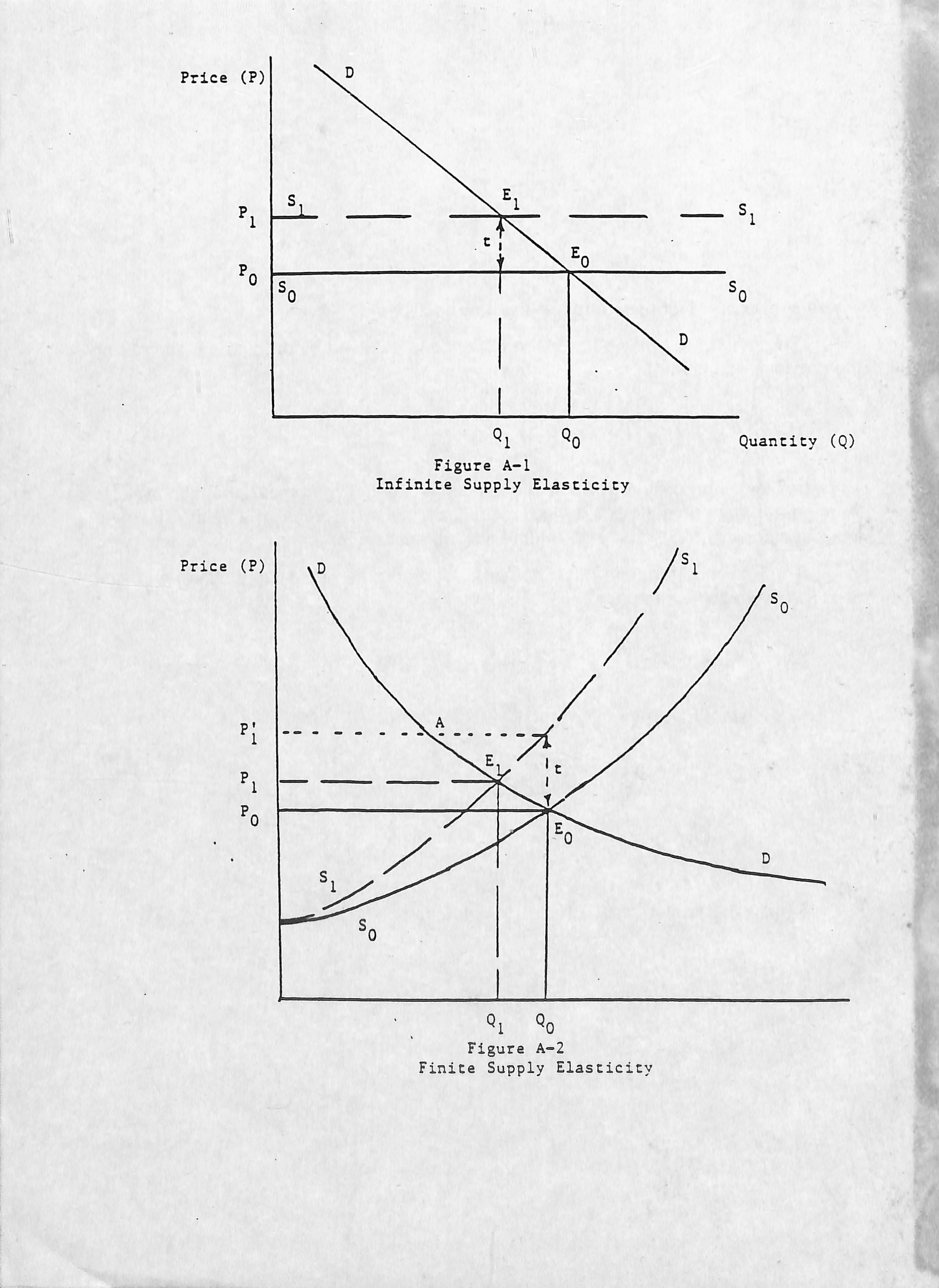

Tax Impact Formulas

A Demand-Supply Model of Services Exports

Table Number Title

Impact of 1986 Act on Ocean Shipping - U.S. Corporation/U.S. Flag

Impact of 1986 Act on Ocean Shipping - Foreign Subsidiary/Foreign Flag

Impact of 1986 Act on Marginal Tax Ratas.

This Repon evaluates the impact of the Tax Reform Act of 1986 en the international competitiveness of U.S.-based service industries. Part I summarizes the resuits of the overall study.

Part II describes U.S. taxation of service companies' foreign income before and after the 1986 Act and compares U.S. taxation with that in eleven other countries Japan, the United Kingdom, West Germany, Switzerland, the Netherlands, France, Belgium, Sweden, Denmark, Cañada and Hong Kong -- that are heme base to the overwhelming majority of U.S. companies'foreign competitors.

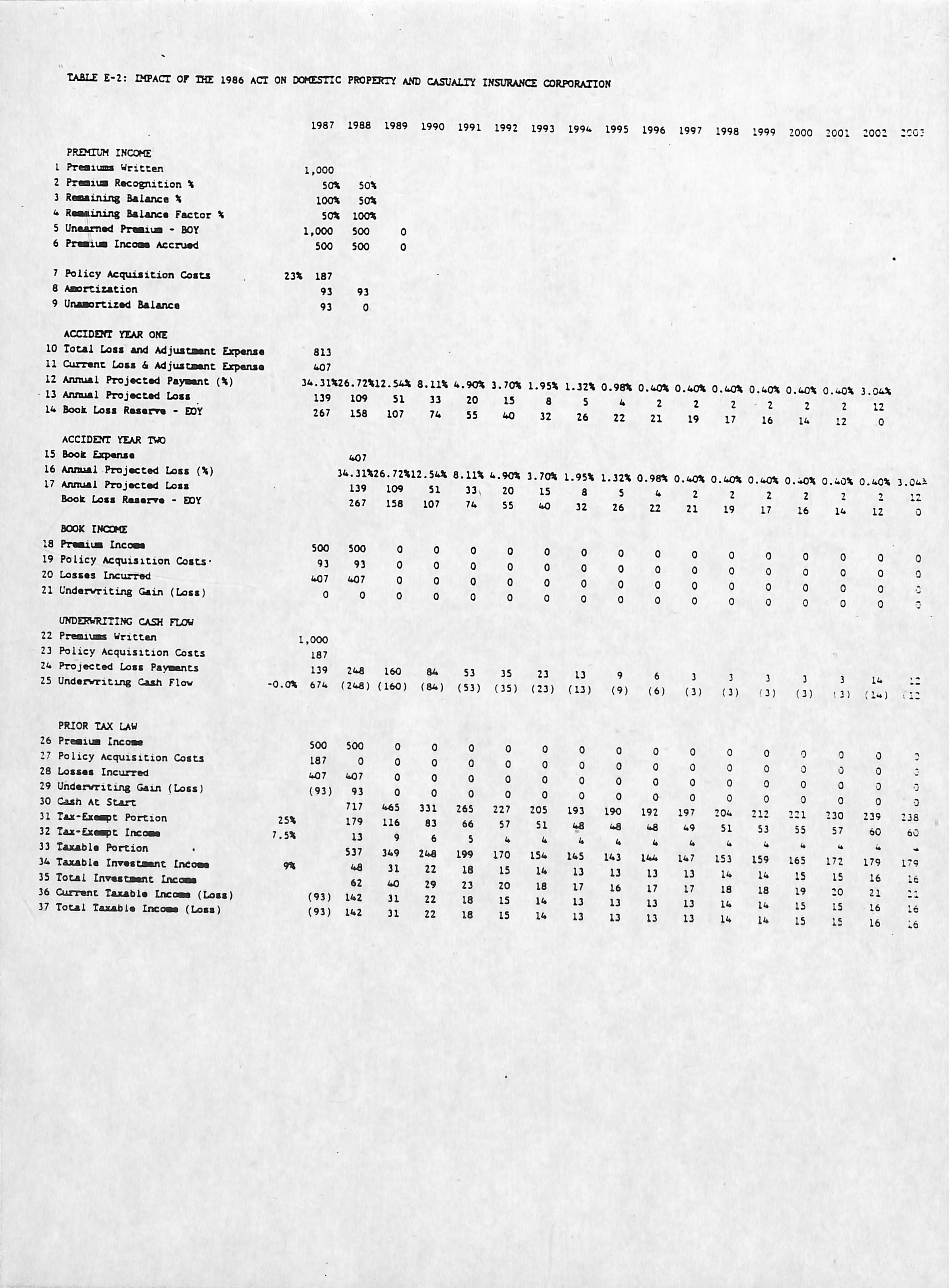

Part II .of the Report aiso quantifies the impact of the 1986 Act on the amount five service industries -- advertising, commercial banking, investment banking, insurance, and ocean shipping -- must charge foreign customers in order to derive the same after-tax profit as those companies would have earned under prior U.S. tax law. These quantitative estimates reflect not oniy the 1986 Act changes in the tax treatment of foreign income ^er but aiso the generally applicable tax rate reduction and base broadening provisions, including the repeal of the bad-debt reserve deduction for large banks, the discounting of loss reserves of property and casualty insurance companies, the deceleration in tax depreciation and the repeal of the investment credit. That quantitative analysis concludes that the 1986 Act had a significant adverse competitive impact on:

Cross-border lending subject to foreign withholding tax of 5 percent or more; Interest and other investment income earned by foreign banking, insurance and other financial service subsidiaries subject to low foreign effective tax rates;

Premiums and other income received by foreign subsidiaries for insurinq

U.S. orthird-country risks;

Srtipping income, whether earned directly by a U.S. corporation or through a foreign subsidiary.

In particular, the calculations indícate that U.S. banks would have had to increase mterest rates and fees for banking services by an average of 3.5% to offset the increased tax burden, and their foreign affiliates by approximately 1%. U.S. producers of shipping services would have had to increase prices by 12% to offset the increased burden; and their foreign flag affiliates, by 4%. International affiliates of U.S. insurance firms would have had to increase prices by 6% to offset the in creased tax burden. The effects are more modest or mixed for advertising invest ment banking, and U.S. resident insurers.

The acíivity and employment effecís from these tax changas may be calculated by applying the pnce changas to "elasticity" measures, which show the sensitivity of foreign demand to price. Each sector is classified as low, intermediate, or high elasticity, and specific elasticity valúes in each class are basad on the émpirical literature for traded goods. This approach yields the estímate that for the five sectors combinad, the tax changes under the 1986 Act may be expected to reduce service exports by a total of $1.7 billion annually (almost 10 percent of their export base), and to reduce eamings of foreign affiliates by $1.9 billion annually.

Apphcation of the labor coefficients to these estimates indicates that the tax changes may be expected to reduce service export employment by a total of approximaíely 15,000 direct jobs. The bulk of this reduction occurs in banking (10,000 jobs) and shipping (6,500 jobs). There are net small, offsetting gains in emolovment in the other sectors.

In general, these categories of service income eamed by U.S.-based companies were competitively disadvantaged not oniy by comparison to pre-1986 U.S. tax law, but aiso by comparison to comparable income eamed by foreign-based service companies. Alíhough the U.S. corporate tax rate has moved from the higher to the lower end of the intemational corporate tax rate spectrum, the base-broadeninq provisions of 1986 Act, particularly the repeal of banks' bad-debt reserve deducíion and the discounting of property and casualty insurance reserves, have generally not een adoptad outside the United States. Even if other countries amúlate the United States in reducing tax ratas and broadening the tax base, U.S.-based companies will continué to be competitively disadvantaged as long as the U.S. treatment of foreign income is more restrictive than that of other countries.

The principal polK^ iroplication of these findings is that in its refinements to the

^ Congress should merge the two tracks of tax and trade policy and consider measures to reverse or offset the negativa effects for U.S. service

ment^^tn

ents to U.S. competitiveness are costiy at a time of acute need for export expan sión and increased foreign earnings to help service the growing U.S. external debt

Moreover emp oymem in service sector exports warrants atteníon in addHton to me more traditional policy focus on manufacturing and agricultural export jobs.

I. Taxes and U.S. Competitiveness in the Services Industries: Overview

It is increasingíy recognized that exports of services are important to the international economic position of the United States. One of the least studied aspects of U S competitiveness IS the Influence of the tax structure. This overview summarizes an empirical analysis of the impact of taxes, and in particular the Tax Reform Act of 1986 on the abihty of U.S. service sector firms to compete internationally. Parí II of this studv

eTe«s" employment

Importance of Trade in Services

The large U.S. external déficit and mushrooming foreign debt place a hiah imhl J affiliates to reduce ihe imbalance and meet payments on the external debt. The service industries have a hITa rim^° United States as a comparativa advantage in important service sectors. Several require human capital, and experience from a large domeslic market, all areas of U.S. strength. The natural ünkage of many service seoTor aotivities to the foreign operations of multinational manufacturing corporations is another basis for sucoess in the sector. poicuions is an

The rJnn confirin U.S. oomparative advantage in the service industries lone e,f """f Assessment has estimated that in 1984 ex p of services (excluding capital income) amounted to $77 billion or one-third the valué of merchandise exports. The trade surplus in services was $14 billion a ^hlrn contrast to the large déficit in merchandise trade in that year. Moreover U S foreicn affihates in service industries earned $92 billion in 1984, which exceeded the'amount earned in the United States by affiliates of foreign firms by $21 billion.

Services trade is an important source of employment as well as exoortc; Tone nt a™, seolTs aftourism bInkL ing (Pan m tabirir^Thirsfir'"^''^"^''"® software, and enginee?-

■ I . . ' '® study estímales that there are 870 000 U S iobs rtírortiu invoived m senrioe sector exports, aimost 60 peroent as high as he numier o?S jobs in the production of manufactured exports.

surh affiliates play a special role in several service sectors Often t mes^'e a:%rn fena'l'rr

scuroing to^e^L' ~

to firms from othGr countriGS. In somG casGS such Iossgs can jGopardizG tha shara cf U.S. firms avan within tha U.S. markat, as soma larQG multinational cliants saakto placa businass giobally with a singla firm and cannot do so if it is not presant in kay foraign markats.

U.S. trada nagotiators hava racognizad tha importanca of tha sarvicas sactors by strassing tha naad to ramova barriars to trada in sarvicas through nagotiations in tha Uruguay Round of multilataral trada nagotiations. Ironically, whila trada policy has accordad a high priority to opportunitias for sarvica axports, U.S. tax policy has procaadad along a saparate track and appears to hava raised naw obstadas to American compatitivaness.

Tha Tax Raform Act of 1986 and Compatitivanass

Tha Tax Raform Act of 1986 raducad tax ratas (from a basic máximum rata of 46 percent to 34 parcent for corporations) whila broadening tha tax basa by limiting daductions and preferances. The Act aiso eliminated or restricted credits and imposed a naw Alternativa Mínimum Tax. Although the reform applied the same principie of reducing ratas whila broadening the base for both corporate and personal income taxes, by dasign tha 1986 Act shiftad tha income tax burden away from individuáis and toward corporations. As a rasult, for corporations in the aggregate, incraasad taxas from a broadar basa excaadad tax raductions from lowar ratas.

Within tha corporata sactor, tha Act had varying affacts among diffarant in dustrias. in tha waka of the Act, analysts widely noted, for example, that capital in tensiva sectors tended to be disadvantagad relativa to less capital intensiva sactors, such as tha sarvicas industrias, by virtua of tha genaral langthaning of dapraciation schadulas and the rapeal of the investment credit. However, this diagnosis was accurata oniy for compañías compating solaly in tha domastic markat. Compañías compating in foraign markats wara confrontad by naw problems in the form of tightaned limitations on the "U.S. foraign tax credit and a significant expansión of the typas of foraign subsidiary income taxabla to U.S. parant corporations whathar or not such incoma was ramittad as a dividand. In addition, a numbar of industry-spacific provisions of tha 1986 Act craatad naw tax liabilitias for thosa spacific industrias that wara mora significant than tha basa-broadaning changas affacting all corporata taxpayars.

Part I! of this raport analyzes in graatar detail the spacific changas enactad by the Tax Raform Act of 1986. In summary, under prior law, cartain typas of foraign incoma earnad through controllad foraign subsidiarias were subjact to immadiata U.S.

taxation, notwithstanding the general provisión that suoh income is taxable in the United States oniy upon repatriation. The 1986 Act significantly expended the range of income subject to current taxation. Included for the first time were:

- dividend and interest earnings of banking, insurance, and other financia! subsidiarias aven though suoh earnings are derivad from the bona fide conduct of an active foreign business;

- securities gains on proprietary accounts;

- underwriting income in connection with the insurance of risks in any third countriesand

- al! shipping income, regardiess of whether reinvested in shipping assets.

The expansión of current taxation to these broad new categories of income will create significantly higher current tax liabilities for firms presently earning suoh income through subsidiarias.

In addition to expanding the scope of foreign subsidiary income subject to current U.S. taxation, the 1986 Act aiso restricted significantly the ability of U.S. corporations to claim a credit for all foreign taxes paid by requiring that the foreign tax credit limit be calculated separately for a number of different income "baskets". Although prior law had aiso required the segregation of certain types of foreign-source income, this segregation was significantly expanded by the 1986 Act. This change will greatly reduce the ability of U.S. firms to combine high and low-tax foreign income, and thus to claim credits for foreign taxes imposed at rates in excess of the U.S. rate. When com binad with the new, lower U.S. tax rates, this revisión will often result in a substantially increased tax burden on U.S. firms doing business abroad.

A similar result is achieved by the third significant change in this area, namely, new rules for the allocation of interest and other expenses against foreign versus domestic income. The effect of the 1986 Act changas will be to require the allocation of additional acense against foreign source income, reducing foreign-source taxable income and thereby reducing further the limit on the foreign tax credit that can be claimed.

Other provisions of the 1986 Act, although not directed explicitly at foreign earn ings, also had adverse effects on the international competitiveness of certain service industries. The reduction of accelerated depreciation, the elimination of the investment tax credit, and the new Alternativa Mínimum Tax were burdensome changas for the capital intensiva containerized shipping industry. The elimination of the deduction for bad debt reserves penalized foreign lending by the U.S. banking industry, and the discounting of loss reserves hurí foreign underwriting by U.S. insurers.

As a result of these provisions, the assessment that service-sector industries generally benefitted from the 1986 Act is reversed for companies engaged in interna tional commerce. Because many of the Tax Reform Act's provisions are industry

spedfic in their application, its impact on the competitiva footing of American businesses must be analyzed on an industry-by-industry basis. This overview summarizes such an evaluation for five specific industries. First, however, we turn to a comparison of U.S. vs. foreign tax practicas in this area.

Comparativa International Tax Structure

In addition to examining how the 1986 Tax Reform Act reallocated tax liabilities among U.S. taxpayers, it is important to compare the relative tax burdens imposed on foreign-based service companies with that imposed on U.S.-based companies before and afterthe 1986 Act.

Parí II of this study provides a detailed analysis comparing U.S. and foreign tax systems. As Table 1 in Part II shows, the United States and about half of its principal trading partners adhere to a "global" tax system. That is, corporations are taxed on their woridwide earnings, and a tax credit for foreign taxes paid is allowed. In contrast, the remaining half of America's principal trading partners tax corporations on a "ter ritorial" basis under which oniy income attributable to domestic activities are subject to the national income tax. Companies based in countries which tax income on a territorial basis thus avoid any home-country tax on by earning income through foreign branches and subsidiarias. Whether this divergence implies a competitiva advantage depends upon the degree to which that foreign income is taxed in the country in which it arises.

The formal similarity of the U.S. and foreign "global" tax systems masks, however, important differences in such features as the degree to which limitations on foreign tax credits are a major concern and in the operation of provisions taxing the unremitted income of foreign subsidiaries. As Table 1 Indicates, many (but by no means all) countries do have provisions for taxing such unremitted income. Oniy the United States, however, goes so far as to tax interest earnings of foreign banking and other financial subsidiaries and third-country insurance underwriting income. Similarly, all countries with global income taxation have a foreign tax credit system. In some cases, such as Japan, the foreign tax credit limit is calculated on an overall basis, as opposed to the United States' basket-type approach. Even in countries in which the foreign tax credit limit is on a per country basis, the foreign rules generally are applied in such a way as to allow our foreign competitors to claim full credit for the foreign taxes they pay. Thus, the binding limits on foreign tax credits enacted in 1986 will generally impose a tax burden on U.S.-based service companies that their foreign competitors do not bear.

Although precise comparisons require a case-by-case analysis, it appears safe to say that foreign countries are generally no more stringent, and usually less stringent, than is the United States in the taxation of foreign source income of domestic corporations.

With respect to general provisions of foreign tax systems, comparisons are difficult to draw. Even with respect to seemingly straightforward features, such as tax rates, considerable compiexity is introduced by provisions in foreign tax codes which reduce corporate tax on earnings distributed to domestic shareholders and/or which permit those shareholders to claim credit for corporate taxes paid with respect to distrib uted profits. However, it does appear that the U.S basic income tax rate, which formerly was among the highest, is now lower than that of most foreign competitors. On the other hand, other countries appear to have narrower tax bases, as illustrated by their typical lack of requirements for loss reserve discounting by insurance companies and their more generous deductions for bad debts. More broadly, because the aggregate effect of the 1986 Act was to increase total U.S. corporate tax even though tax rates declined, it is clearly misleading to use the tax rates alone as the guide to international comparison of tax burdens. A more detailed discussion of these issues is contained in Part I!.

Impact of the 1986 Act: Estimates

The effect of tax changes under the 1986 Act on U.S. competitiveness may be measured by calculating the price increase required for a U.S. firm to maintain the same rate of return on investment as before, when the tax burden increases, or the price reduction the firm can grant with no change in rate of return, in instances of lower tax burden. The net change in taxation depends on the trade-off between the 12-point reduction in the corporate income tax rate and the base-broadening changes, including extensión of Subpart F treatment to interest, insurance (including investment), and shipping income, new restrictions on the foreign tax credit, and others summárized above.

The change in price may be translated into estimated change in sales and employment. As developed in Appendix H, the responsiveness (elasticity) of sales volume to price is imputed to each of the five sectors examined on a basis of the broad range of past statistical estimates for trade and a judgmental classification of the sector as price-sensitive or not. The price change applied to the elasticity yields the estimated change in sales quantiíy. Application of labor coefficients shows the number of U S jobs involved.

The analysis shows a wide variation among sectors for the net impact of the 1986 Act on tax burden. Within each sector, the effects are calculated separately for export activity from a U.S. base and for sales by U.S. subsidiarias and affiliates located abroad (with U.S. employment estimates only for exports).

Although aggregate figures must be viewed with considerable caution because of the substantial variation among the sectors, the overall estimates show that for advertising, banking, insurance, investment banking, and shipping, changes under the 1986 Act may be expected to reduce exports by $1.7 billion annually (9 percent of the export

With respect to banks' fee and other (non-high-withholding tax) interest income, thG changG in thG compGtitivG footing of a U.S. bank dGpands upon thG foraign tax rata it facGS, thG applicability of U.S.tax to such incomG if Garnad through a foraign subsidiar/, and whathar tha bank is in an gxcgss cradit or axoass limitation situation. In ganara!, banks wara advantagad by tha 1986 Act to tha axtant thay earn incoma through branchas(not subsidiarias) in low tax foraign countrias (or in a situation of axoass cradit limitation). On tha othar hand, a subsidiar/ of a U.S. bank oparating in a foraign country with a favorabia tax systam (a.g., Switzarland) and ramitting a smali proportion of its profits would, as a rasult of tha axpandad scopa of U.S. taxabia incoma, find itsalf sevaraiy disadvantagad by tha 1986 Act, both in comparison to tha pra-1986 U.S. situation and in comparison to its foraign compatitors (racaíl that no othar country taxas a foraign banking subsidiary's intarast incoma).

ECONOMIC IMPACT - Tha rastrictions placad by tha 1986 Act on U.S. tax cradits for high foraign withhoiding faxes on crossbordar landing would raise tha prica of this U.S. bank activity raquirad to kaap raturn constant by an astimatad 4.3 parcant (from a typical intarast rata of 8.5 parcant to 8.9 parcant par annum). In contrast, for faa-basad sarvicas tha naw law actual!/ reduces taxas by an amount permitting a prica declina of 1.4 parcant for U.S.-basad activity. Tha weightad averaga prica impact for banking sarvica axports is an incraasa of 3.5 parcant. In viaw of tha high prica sansitivity of damand, this incraasa may ba axpactad to causa a declina of 10.5 parcant in tha voluma of bank sarvica axports, for a loss of $682 million annually (and 9,820 axportralatad jobs).

For banking sarvicas providad by foraign affiliatas of U.S. banks, tha prica changas that would neutraliza tha affacts of tha 1986 Act on rata of raturn ara, again, a 4.3 parcant incraasa for cross-bordar landing and a 0.5 parcant raduction for local currancy landing and faa-basad sarvicas. Tha weightad avaraga prica incraasa of 0.7 parcant translatas into ravenua losses of $137 million (2.4 parcant of tha total). Thasa astimatas imply that tha 1986 Act had a substantially negativa affact on an industry airaady hardpressed by intarnational compatition.

Insuranca

MARKET ENVIRONMENT ~ U.S. firms provida fira, property, casualty, marina, and product liability insuranca to covar not oniy tha oparations of U.S. multinational firms abroad but aiso foraign nationals. üfa insuranca companias ara aiso activa whara antry is parmittad. Sophisticatad financia! and insuranca instrumenta davalopad in tha United Statas can provida a "tachnologicár adga in tha compatition. For national accounts, compatition is primarily with tha national firms in aach respectiva markat. For global accounts of multinational firms, compatition is from a limitad numbar of larga firms, primarily thosa from tha Unitad Kingdom, Garmany, Franca and Switzarland. Japan has aiso bacoma activa, in tha area of late. Raputation of tha firm is important, as wall as prica.

Some 50 large insurance companies domínate U.S. activity abroad. Typically insurance companies operating abroad are torced by foreign regulations to conduct operatíons through branches or subsidiarles located in the country. Measures that place a disadvantage on foreign subsidiarles or affiliates thus tend to result In a ioss of business rather than reallocation of the business to an export base.

In 1984 U.S. insurance firms eamed an estimated $6.5 biiiion in premiums net of claims paid and reinsurance passed to third parties, for insurance provided foreign customers from U.S. offices. In addition, U.S.-owned foreign branches and subsidiarles earned some $12 billion. Approximately 26,000 U.S. jobs were associated with exports of insurance services.

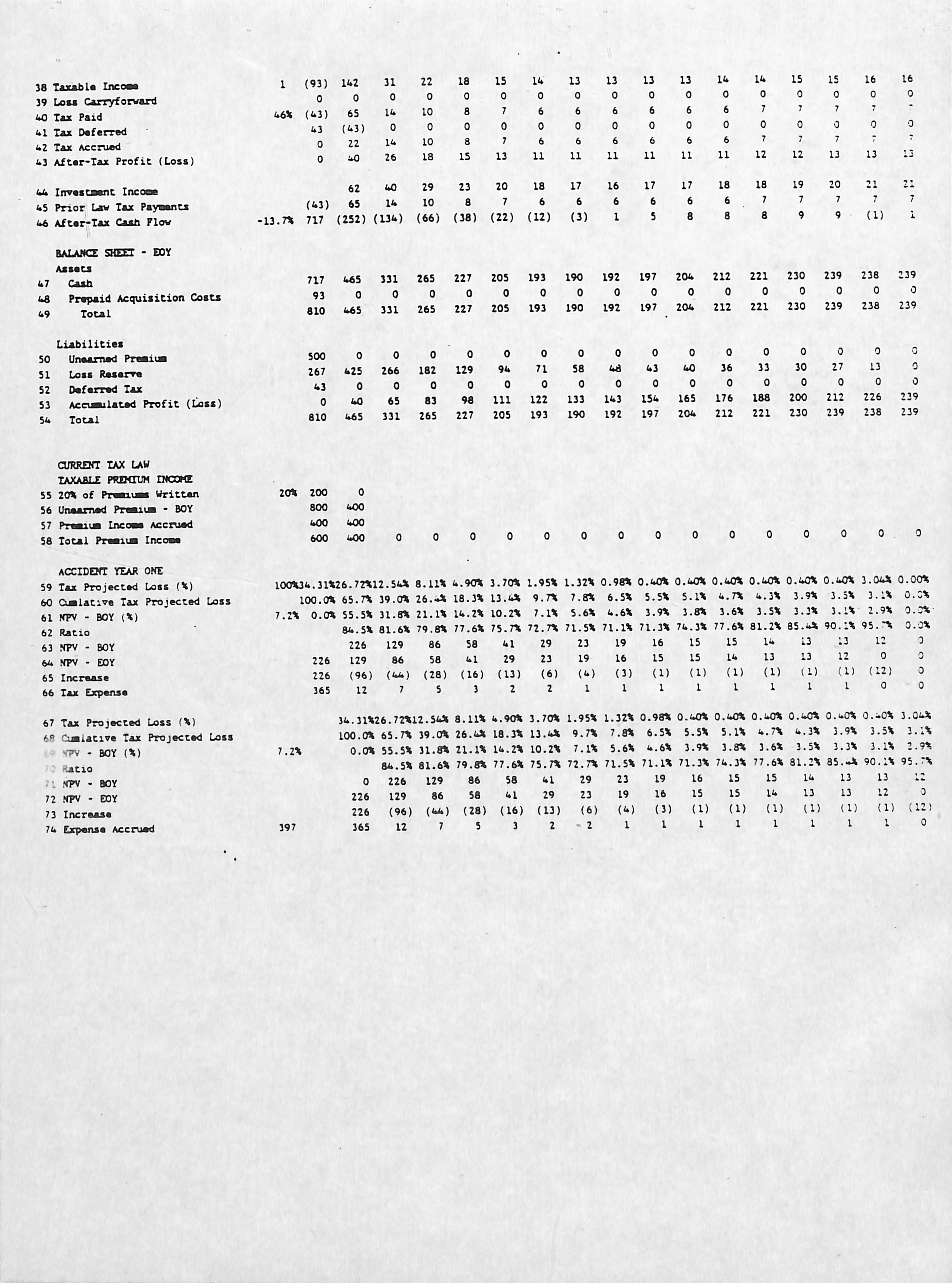

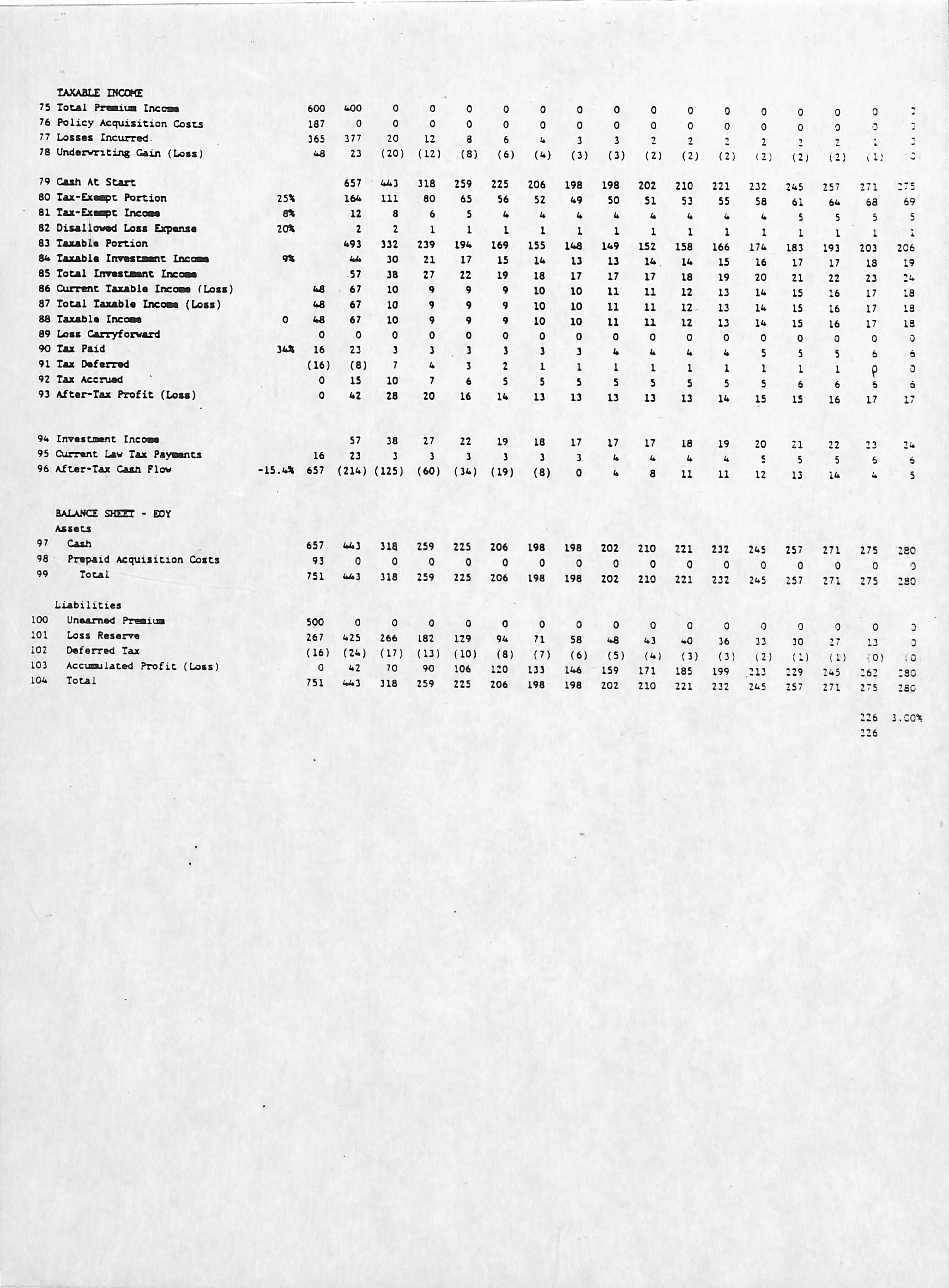

TAX CHANGES - The property and casualty insurance industry was adversely affected by severa! provisions in the 1986 Act. On the purely domestic front, U.S. firms must henceforth discount for the time valué of money the additions to reserves for losses and Ioss adjustment expenses payable in future years. They were disallowed a deduction for a portion of additions to unéarned premium reserves and torced to recapture a portion of existing unearned premium reserves. AIso, 15 percent of the interest from state and municipal obligations and of the deductible portion of dividends received, tax free under prior law. has become fully taxable. These will substantially broaden'the base of insurance company taxable income.

In addition, the 1986 Act extended the reach of Subpart F, which faxes curreníly certain unremitted income of controlled foreign subsidiarles, to two new major sources of foreign insurance income: U.S. third country underwriting income, and investment income generally. As a result of these changes, insurance subsidiarles earning income in foreign countries with low effective tax rafes and remitting oniy small portions of this income to the United States will be significantly disadvantaged by the 1986 Act. Other subsidiarles and branches of the U.S. parent, will be less disadvantaged relative to prior law.

The extensión of Subpart F to large parts of U.S. insurance companies' foreign income places them at a significant disadvantage vis-a-vis insurance companies in foreign countries, none of whom impose such faxes.

ECONOMIC EFFECTS -- The estimates of Part II find that for U.S.-based exports of property and casualty insurance services, the effect of the 1986 Act is to reduce the tax burden by an amount that would permit a reduction in price by 3.0 percent. For foreign subsidiarles and affiliates, the estimated impact of the Act is to raise faxes by an amount requiring an increase of price by 6.0 percent to keep the rafe of return constant. Application of an intermedíate price sensitivity of demand to these changes yields the estimates that the new tax law increased prospectiva insurance service exports by 3.8 percent or $245.7 million, but reduced earnings of foreign affiliates by 5.3 percent or bv $641.1 million. '

The losses in foreign affiliate sales thus far outweigh prospective gains from insurance service exports. As noted, the in si^ nature of the bulk of the foreign affiliate activity means that the losses are unlikely to be recaptured through reallocation of the business to exports.

Investment Banking

MARKET ENVIRONMENT - Investment banking services include the traditional underwriting of securities as they come to market, trading for the firm's own account, commissions on securities transactions, and fee-based advisory work. The principal international competitors include firms from the United Kingdom, Germany, Switzerland, and Japan.

Competition is keen and price sensitivity high on underwriting, where spreads tend to be thin, and sales commissions, where cut-rate brokerages have made inroads. For specialized advisory work (including on mergers and acquisitions) the firm's reputation is a more dominant factor.

The international market is expected to grow more rapidly than the domestic market. Foreign revenue is already substantial, with investment banking service ex ports of $1.75 billion in 1984 and earnings by foreign subsidiaries and affiliates at $7.7 billion. The employment associated with exports may be estimated at some 25,000 jobs.

TAX CHANGES - The investment banking industry was adversely affected by the application of Subpart F rules to securities gains on proprietary accounts and interest and dividends derived in the active conduct of a trade or business, and aiso by the foreign tax credit limitation rules. Although the reduction in the U.S. tax rate appears to have provided some benefit, the newly revised Subpart F rules offset this benefit.

Income earned by providing services through U.S. branches may be more advantageously treated, provided (a big proviso) that foreign withholding taxes can be avoided (i.e. "many foreign countries impose high withholding taxes on advisory services income). income earned through foreign branches and subsidiaries in hightax countries was clearly disadvantaged by the expense allocation and other changes in the U.S. foreign tax credit limit.

Countries where investment banking firms do major business (i.e. Japan, United Kingdom, Ganada, Australia, and Switzerland) have income taxes equal to or substantially higher than the current U.S., rate. The income of a foreign affiliate whose ownership is between 10 percent and 50 percent (often due to regulatory constraints) cannot be included in the financial services basket. Therefore this income will be subject to its own sepárate limitation. In addition, if the investment banking firm or its foreign affiliate receives high withholding tax income, this income will fall into another sepárate basket, increasing the likelihood that the company will end up in a foreign tax credit limitation position.

In general, U.S. investment banks will be helped vis-a-vis their foreign competiíors by the lower U.S. rates, but will be hurt by the more restrictive foreign tax credit iimitation provisions. Their disadvantage vis-a-vis countries with territorial taxation (and henee zero tax rates on foreign source income) will remain in place in lew tax third countries.

ECONOMIC EFFECTS - The net effects of the 1986 act have been to leave the tax borden for both export and foreign affiliate activities of the investment banking industry almost unchanged. As indicated in Section III, the price changes required to offset the net tax effects are relatively low because of the specialized nature of the industry. As a result, estimated changes in exports and foreign affiliate sales are minimal.

MARKET ENVIRONMENT

~ Two features domínate U.S competitiveness in ocean shipping services. First, the United States holds only a. small share of the market; U.S.-flag carriers account for only 15 percent of the "liner" (primarily containerized) cargo in U.S. imports and exports (excluding protected coastal trade), and for bulk cargo the share is much smaller. Even taking into account the fact that a significant portion of bulk cargo is carried by U.S. subsidiarles flying foreign "flags of convenience", the U.S. market share is small. Second, the great bulk of international shipping takes place in a nearly tax-free environment. Subsidiarles operating out of tax-haven bases (such as Liberia) provide an easy vehicle for low-tax operations by firms from other countries, and low-tax competition is also stiff from various East Asian newly industrializing countries (NlCs).

U.S. flag ship operators are able to compete in the face of such unfavorable circumstances largely because the move toward containerization has shifted advantage toward countries with strong capital and technological bases. In the actual construction of ships, however, comparativa advantage lies more with countries possessing rela tively low-wage labor, as the process is labor intensive.

In the past, U.S. policy has combinad tax and subsidy programe to enable the shipping industry to compete more successfuliy in view of national security objectives. These incentives have eroded ovar time, however, especially with the 1986 Act. One past benefit was the Capital Construction Fund provisión of 1970 legislation. Firms could defertaxes on income usad to purchase ships built in the United States, but after U.S. shipyard construction subsidies terminated in 1982 this benefit became of little use as ships were generally purchased from other sources. U.S.-flag carriers have received operating subsidies to offset the higher cost of American crews, but the Reagan Administration has cut back these subsidies as well.

The move toward deregulation under the Shipping Act of 1984 has meant that price and quality competition within the international "liner conference sysíem" has

intensified. All of these factors, combined with a relativa oversuppiy of ships, have meant a squeeze on earnings in the Industry in recent years.

Ocean shipping nonetheless still buiks larga in U.S. export and foreign subsidiary activities. Export earnings (U.S.-flag carriers) in 1984 amounted to $3.6 billion, while revenues of affiliates (fiag of convenience) amounted to $9.3 billion. Soma 18,000 U.S. jobs may be attributed to the formar, export activity.

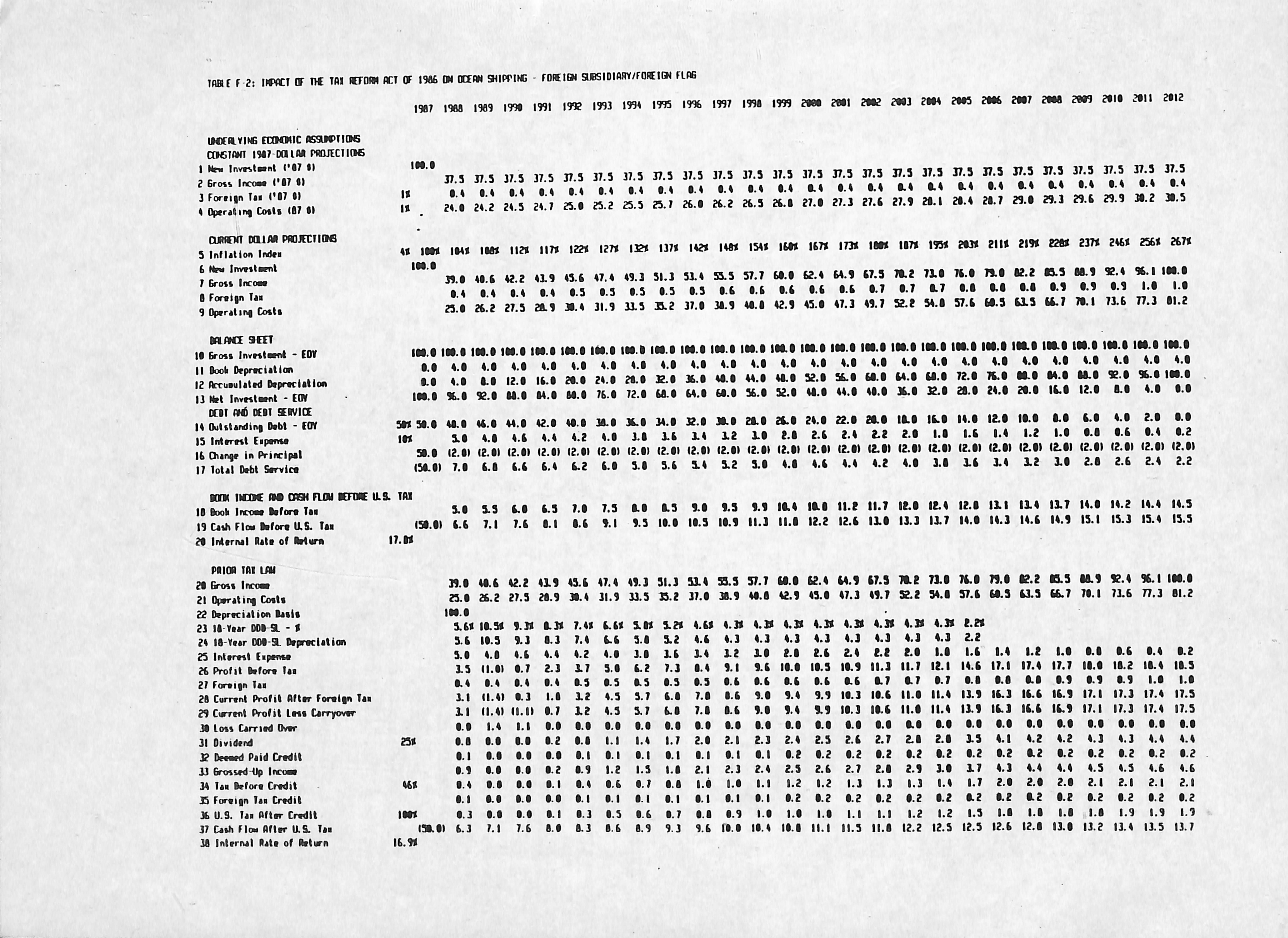

TAX CHANGES -- Both the U.S.-flag and foreign flag operations of U.S. ocean shipping corporations were adversely affected by the 1986 Tax Reform Act. Lengthening of depreciation lives, the repeal of the investment tax credit and enactment of the Alterna tiva Minimum Tax in this capital intensiva industry will substantially increase the ratas that would be charged in order to preserve the after-tax rata of return or, more likely, reduce the after-tax return on shipping investments.

Foreign flag operations, which did not benefit from accelerated depreciation and investment credits under pre-1986 law, are less adversely affected. Still, however, the repeal of the provisión that allov/ed foreign shipping subsidiaries to defer U.S. tax by reinvesting their profits in shipping assets will lead to a substantial increase in the U.S. tax burden. This change will aiso put U.S.-owned shipping affiliates at a disadvantage vis-a-vis foreign-owned ship owners, because other countries uniformiy permit foreign shipping subsidiaries to defer domestic tax by reinvesting their profits.

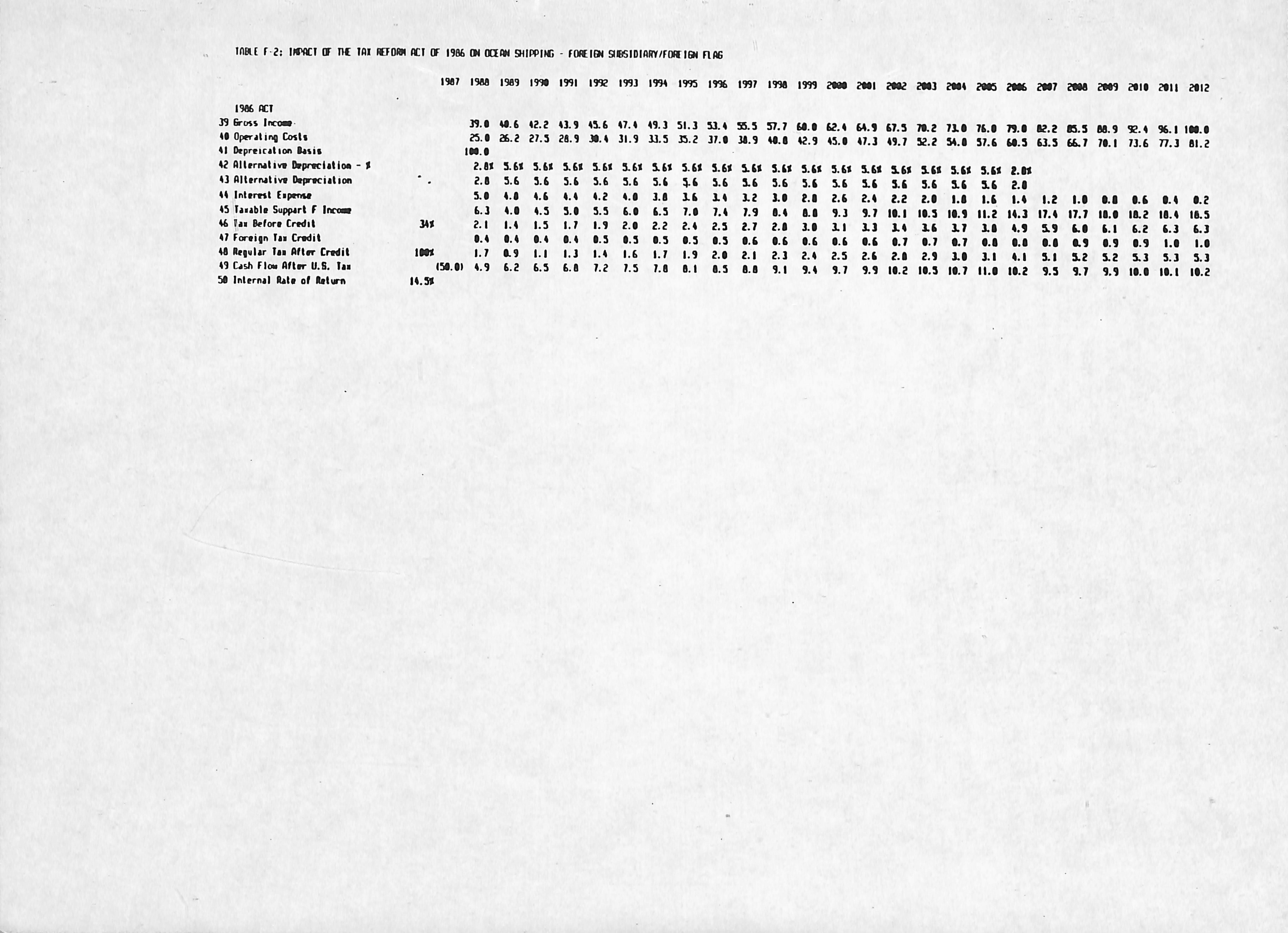

ECONOMIC EFFECTS ~ The heavy impact of repeal of deceleration of ACRS depreciation, the investment tax credit and the Alternative Minimum Tax mean that U.S.-flag ocean shipping bears an additional tax burden from the new law that would require a 12 percent price increase to permit an unchanged rate of return. For foreign flag subsidiaries of U.S. shipping companies, the repeal of the Subpart F exclusión of reinvested shipping profits reinvested in shipping assets means that the tax burden will rise by an amount requiring a 4 percent price increase to maintain the rate of return.

These price increases transíate into large percentage declines of activity because of the relatively high sensitivity of demand in what is a "commodity" type of service with keen competition. Part III estimates the cutback in shipping service exports that may be expected from the new tax law at 36 percent, or $1.3 billion, and the reduction in foreign affiliate revenue at 12 percent, or$1.1 billion. Some 23,000 jobs could be lost as the result of the reduction in shipping service exports (U.S.-flag carriers). Thus, an industry already under severe competitive pressure faces serious new obstacles from the changes of the Tax Reform Act of 1986.

Conclusión

Two principal patterns emerge from the sectoral studies. First, overa!! the 1986 Act has imposed a new obstada to the competitiveness of U.S. service sector exports and sales by foreign affiliates. This burden is untimely in view of the imperativa of reducing the massive U.S. trade déficit and net foreign indebtedness. Second, it is apparent that the adverse effects can be highiy concentrated by sector. Among the sectors examinad, banking and shipping account for the greatest losses. The adverse effects are aiso large in insurance. These results suggest the need for a review of U.S. tax policy that takes account of the impact on U.S. internationa! competitiveness in general and takes particular cara to avoid concentrated damage to the ability of important individual service sectors to compete internationally.

II. Impact of Tax Reform Act on Rate of Return and Comparison to Foreign Tax Systems

Introduction

The Tax Reform Act of 1986 made far-reaching changas in the U.S. tax system. Broadly speaking, the cveraií tax burden was shifted from individuáis to corporations. Although the máximum rata of the regular tax on corporate income was cut from 46 percent to 40 percent for 1987 and 34 percent for later years, the overall corporate tax burden was increased through a series of provisions broadening the measure of gross income, limiting deductions, repealing or restricting tax credits, and enacting a new Alternativa Minimum Tax (AMT). The 1986 Act aiso sharply limitad the general deferral of U.S. tax on retained earnings of U.S.-controlled foreign subsidiarias and imposed several new restrictions on the U.S. foreign tax credit.

This Report evaluates the impact of the 1986 Act on the international competitiveness of U.S.-based service companies. Service companies, like manufacturera, are heterogeneous -- they include providers of personal and business services (e.g., advertising, accounting, law), financial services (e.g., banking, insurance), transportation (e.g., airlines, ocean shipping) and other types of services. Many service companies have developed over the years substantial businesses outside the United States, often initially in response to the overseas expansión of their primary U.S. clients" businesses While U.S.-based service companies often enjoy certain advantages by virtue of their familiarity with the needs and operations of U.S.-based multinational corporations, they must Overeóme the disadvantages of operating in a foreign economic and legal environment, often in competition with established local and third-country rivals. U.S.-based service companies concern for their international competitiveness generally and the impact of U.S. taxation on that competitiveness in particular is every bit as immediate and real as the concern of U.S.-based manufacturers.

To describe the impact of the 1986 Act on the international competitiveness of U.S. service companies, we have examined not oniy the foreign-income provisions of the 1986 Act, but aiso general and industry-specific provisions having significant impact on service companies' international competitiveness. In both areas, we have compared and contrastad U.S. tax treatment with that of Japan, the United Kingdom, West Germany, Switzerland, the Netherlands, Franca, Belgium. Sweden, Denmark, Cañada and Hong Kong, the eleven countries that are heme base for most major competitors of U.S.-based service companies.

Global versus Territorial income Taxation

United States

The United States taxes income earned by U.S. corporations from all sources, including income earned by foreign branches, dividends received from foreign sub sidiarias and in certain instances the unremitted profits of foreign subsidiarias. To prevent the double taxation of income from foreign sources, U.S. corporations can claim a credit dollar-for-dollar against their U.S. tax for foreign income taxes. The U.S. foreign tax credit is limitad, however, to the U.S. tax attributable to foreign-source taxable income or, if a corporation has a domestic loss, to the total U.S. tax liability. The 1986 Act retained the general principies of taxing woridwide income and eliminating international double taxation through a foreign tax credit, but made substantial changas in the practical appiication of those principles.i/

Foreign Countries

At obvious risk of oversimplification, we have summarized the essential features of the eleven foreign countries' tax systems in Table 11-1. (Appendix A contains exten siva footnotes to this table.) Our survey was basad on English-language descriptions of foreign countries tax systems supplemented by materials and information provided by overseas offices of Deloitte Haskins & Sells. Under their statutory law, six of those countries - Japan, the United Kingdom, West Germany, Sweden, Denmark and Cañada -- aiso tax their multinationals' woridwide income and eliminate international double taxation through a foreign tax credit. (West Germany, Ganada, and,to a lesser

1/ In addition to the changas described below, the 1986 Act provided that profit or loss of foreign branches and subsidiarles wiil generaily be translated into U.S. dollars using a profit-and-loss method, ratherthan a net worth method. In a hyper-inflationary economy, the profit-and-loss method incorporales the pureiy inflationary gains and losses reflectad in local currency prices and interest ratas, whereas the net-worth method does not. Although a net worth method may apparently be eiected by taxpayers. the legislativa history of the 1986 Act states that a taxpayer electing the net worth method for one qualified business unit (e.g., a branch in a hyper-inflationary country) might be required to eiect it for all qualified business units (including branches operating in countries with low to modérala inflation ratas). If such a requirement were imposed, U.S. corporations would have to choose between paying the U.S. tax on purely inflationary gains in hyper-inflationary countries or contending in all foreign countries with largely erratic foreign currency translation gains and losses of the sort which usad to arise for financial reporting purposes under Financial Accounting Standards Board Statement No. 8.

extent, Sweden exempts certain types of foreign income from domestic taxation when a tax treaty applies.)

By contrast, Switzerland, the Netherlands, Belgium, Franca, and Hong Kong generally have "territonal" tax systems under which business profits attributable to a domestic branch are subject to domestic tax, but profits attributable to a foreign branch and dividends received from a foreign subsidiary of a domestic corporation are gener ally exempt from domestic tax. Unless a tax treaty applies, countries with territorial tax systems generally allow a deduction from income, but not a credit against tax, for foreign tax withheid from foreign-source income (e.g., interest) earned by a head office or other domestic branch. Thus, territorial tax systems implicitly provide a strong tax incentive to earn foreign income through foreign branches and subsidiarles.

Income Earned Through Foreign Subsidiarles

United States

Prior to the 1986 Act, income earned by foreign subsidiarles of U.S. corporations generally was not taxed until dividends were remitted to U.S. shareholders. However, U.S. shareholders who separately or collectively "controlled" a foreign corporation were taxed to the extent the foreign subsidiary either had tainted ("Subpart F") income or were deemed to have remitted income by investing in tainted U.S. assets (e.g., a loan by a foreign subsidiary to its U.S. parent). Under pre-19B6 tax law, tainted Subpart F income was limited to:

- Certain passive foreign personal holding company income:

- Foreign base company sales income (i.e., sales income from property purchased from, or soid to, a relatad party in another country);

- Foreign base company service income (i.e., income from services performed in a third country for a relatad party);

- income from the insurance of U.S. risks;

- Shipping income, but oniy to the extent such income was not reinvested in shipping assets (as most such income was).

The 1986 Act significantly expended the types of passive income currently taxable to its U.S. shareholders. For example, gains on commodities, securities and foreign currency transactions are generally taxable unless specified trade-or-business tests are met. Securities gains of a regular dealer are excluded from Subpart F income. More significant for U.S.-based service companies, the 1986 Act provided for current taxation of:

- Dividends and interest earned by foreign banking, insurance and other financial service subsidiarias, aven whan such incoma is racaivad from unraiatad parsons and in tha activa conduct of a bona fida businass by I tha foraign subsidiary;

- Sacurity, foraign currancy and commodity gains not quaiifying for tha trada-or-business axcaptions (a.g., sacurity gains on invastmants hald for a daalar's own account);

- Incoma attributabla to tha issuing of any insuranca or annuity contract in connaction with risks in any country (not just tha Unitad Statas) othar than tha country in v\/hich tha insurar was craatad pr organizad: and

- Shipping incoma, aven if reinvasted in shipping assets.

Foreign Countrias

As shown in Tabla 11-1, four of tha tan foraign countrias includad in our survay ~ Switzarland, tha Natharlands, Balgium, and Hong Kong -- hava territorial tax systems under which dividends from wholly-ownad foraign subsidiarias ara ganerally axampt from tax aven when remittad and hava not anactad any provisions comparable to tha U.S. Subpart F rules. Two countrias - Swadan and Danmark - hava global tax sys tems and tax dividends from wholly-ownad foraign subsidiarias, but hava not anactad provisions comparable to tha U.S. Subpart F rules. Tha ramaining five countrias Japan, tha Unitad Kingdom, Wast Garmany, Franca and Cañada ~ hava anactad Subpart F-type provisions, but ganarally do not tax incoma derivad from bona fide banking, insurance, shipping or othar businassas whan racaivad from unraiatad par sons. Thus, tha typas of incoma includad in Subpart F by tha 1986 Act would not be taxabla to a parant corporation in any of tha elevan countrias includad in our survay.

Deamad-Paid Cradit

Unitad Statas

U.S. corporations may claim a foraign tax cradit for incoma taxas paid to foraign govarnmant by tha corporation itsalf (including its foraign branchas) and a daamad-paid cradit for incoma taxas paid by its foraign subsidiarias with raspact to thosa profits that ara aithar paid out as a dividand or ara taxabla as Subpart F incoma. Prior to tha 1986 Act, for daamad-paid cradit purposas, dividends paid aftar tha first sixty days of a yaar or within tha first sixty days of tha following yaar wara traatad as paid first out of that yaaris profits and than out of tha pravious yaars' profits undar a last-in-first-out (LIFO) ordering rula. Through careful yaar-to-yaar timing of foraign incoma tax and dividand payments, U.S. corporations could oftan maximiza tha daamad-paid foreign tax availabla for cradit relativa to dividand incoma and tharaby minimiza any residual U.S. tax.

r .cnL repealed the 60-day rule with the resuit that dividends paid in the first 60 days of a year are deemed to be paid from that year's profits. not the precedino year-s profits. Moreover. a forelgn subsidiary's post-1986 profits and income taxes wil! m cumulative. multi-year pools (sepárate pools are maintained for each oreign tax credit limitation category, as described below). Taken together these w- opportunities and thereby reduce the amount of deemed-paid credit available for those U.S. corporations with foreign subsidiarias «"«"^«ons in their

Foreign Countries

Of the five countries which próvida a deemed-paid foreign tax credit or an equivalent system, Japan and Denmark generally apply an annual vintage-account approach similar to the pre-1987 U.S. system. Subsidiarias of U.K. and West Germán natTTp to any particular ordering rule and can generally desig- nate the source or the year of the profits to be distributed. Profits subject to a high remeted bJp r" distributed. and lightiy taxed profits retained. Dividen^ received by a Canadian corporation from a foreign subsidiary are generally exempt from Canadian tax if the subsidiary is carrying on a business in a country wi h lich Cañada has. or is negotiating. a tax treaty. Other dividends are subject io Canadian tpv h ^

credit^cY ?f

essentially the same tax effect as a deemed-paid Hi!t h + 5 r f ^'"^^Se-account method. Dividends are deemed to be wh rh fi.rth exempt(treaty-country) surplus and second out of taxable surplus which further minimizas any chance that Canadian tax will be imposed. '

deemed-paid foreign tax credit. so absent a tax treatv exemptmg a foreign subsidiary's dividend from Swedish tax the dividend would hp potentially subject to economic double taxation. In addition. benmaXs Seemed-opid credit is limitad to dividends declarad at the shareholders annual meetinq from the LeXVs'íhe u's'deeme2°®'d"°^ dividends. Apart from these two tivrthPrt^l ; credit rules under the 1986 Act appear more restric- tive than those in foreign countries with comparable tax systems.

The foreign tax credit is generally limitad to the U.S tax attributable tn fnrpinn source taxable income, which equals foreign-source gross i coa tes r^a ed e "

Si ,1% olaTT' incide no. en; d rectly allocable ítems (e.g., depreciation of property used by a foreiqn branchl bis aiso a em ^ta share o. general and administratL expensas Sest e^inSS!

Prior to the 1986 Act, U.S. corporations were generally subject to an overa!! ümitation under which the tota! foreign tax credit was limited to the U.S. tax on overa!! foreign-source taxable income. Under an overall limitation, excess foreign tax with respect to a high-foreign tax category of income (e.g., interest income subject to a high foreign withholding tax and against which no deductions are aüowed) couid effectiveiy be offset against the U.S. tax on a second, low-foreign-tax category of foreign-source taxabie income ~ a phenomenon referred to as foreign tax credit "averaging."

The 1986 Act required that the foreign tax credit be calculated separateiy forthe foüowing "baskets" of foreign-source income:

- Interest, dividends, rents, royalties and other specified types of passive income;

- High-withho!ding-tax interest income;

- Financia! services income;

- Shipping income;

- Dividends received from each non-U.S.-controüed foreign subsidiary;

- Ai! other foreign income.

Specia! "iook through" rules generally require U.S. corporations to aüocate Subpart F income and dividends, interest, rents and royalties received from a controüed foreign subsidiary to the appropriate basket based on the nature of the subsidiary's underlying income out of which the dividend was paid or from which the interest, rent or royalty was deducted. The intended and certain effect of these rules is to curtai! foreign tax credit "averaging" by U.S. corporations.

In addition, the 1986 Act tightened the rules for allocating and apportioning interest and other expenses by requiring inter alia that interest and certain other ex penses incurred by affiliated U.S. corporations be apportioned based on the consolidated group's assets, ratherthan the sepárate assets or gross income of the corporation incurring the expense. Prior to the 1986 Act, U.S. corporations could minimize the impact of the interest allocation rules by shifting interest-bearing debt to an affiliate. Under the new Act, by allocating additional U.S. expense against those baskets of foreign income for which the foreign tax available for credit exceeds the limitation, the foreign tax credit is reduced and U.S. tax is increased.

Foreiqn Countries

As noted above, six of the eleven countries surveyed have a global tax/foreign tax credit system. Of those six countries, oniy Japan has an overall foreign tax credit limitatlon under which excess foreign taxes from one source can be offset against domestic (Japanese) tax on income from a low-tax foreign source. Three countries West Germany, Denmark and Cañada - apply a per-country limitation, and one -- the United Kingdom -- applies a per-item-of-income foreign tax credit limitation. Five of the six countries thus appearto limit foreign tax credit "averaging" in a fashion similar to that under the separate-basket approach instituted by the 1986 Act.

The degree of restrictiveness of the foreign provisions is often ameliorated, however, by other provisions in their laws. For example,the United Kingdom applies its foreign tax credit limitation separately with respect to each item of income (e.g., income from a particular sale), thereby apparently denying a U.K. corporation the ábility to "average" foreign taxes with respect to separata items of income from the same country of the same generic type. However, in appiying the foreign tax credit limitation, U.K. corporations.can elect the order in which various items of income and expense are taken into account. By taking high-foreign-tax items of income into account last, a U.K. corporation can avoid allocating any expense against that item of income, with the result that the foreign tax credit limitation equals the rate of U.K. tax applied to the amount of gross foreign income. U.K. corporations can aiso achieve substantial foreign tax credit "averaging" by interposing a foreign holding company between the U.K. parent corporation and its foreign operating companies. Because the U.K. does not have "look through" rules comparable to those enacted by the United States in 1986, the foreign holding company can combine high- and low-tax foreign income and dis tribute blended dividends to its U.K. parent. (With respect to bank lending, the flexibility of U.K. practico has been limitad by the U.K. Finance Act of 1987, which limits U.K. banks' credit for foreign withholding taxes on cross-border loan interest to the U.K. tax on such interest net of the financial cost of funding those loans. As under prior U.K. law, foreign withholding taxes in excess of 15 percent of the gross income are deductible, but not creditable. Where the cost of funding the loan is not readily ascertainable, the cost will be basad on LIBOR or soma other "just and reasonable" measure. Priorlaw treatment of loans outstanding on April 1, 1987 will be continuad for two years. Apart from potential differences in the amount of interest expense allocated against foreign source income, then, the primary differences between the U.S. and U.K. treat ment are: (1) the U.K. limitation is calculated for each cross-border loan separately and (2) U.S. banks, but not U.K. banks, are required to allocate or apportion other expenses and losses, such as G&A or bad loan write-offs, against such income.)

To take a less extreme case, West Germany appears to apply a per-country limitation and applies look through" rules to dividends received from foreign subsidiaries. However, as explained more fully below, West Germany has a spiit-rate tax

syst6rn und6r which rGtainGd Garnings ara taxGd at a 56 parcant rata and distributad aarnings at a 36 parcant rata. For purposas of appiying its foraign tax cradit limitation. foraign-sourca incoma tha Garman tax on which may ba offsat by a foraign tax cradit is daamad to ba distributad last and thus daamad to ba subjact to tha 56 parcant rata to tha extant that any incoma is taxad at that rata.

Datarmining tha axtant to which foraign countrias raquira Intarast and othar expansa to ba allocatad against foraign-sourca taxabie incoma was not simple bacausa foraign countrias' rulas in this araa are not as fully articulated as tha U.S. rulas ara. Most countrias in principia raquira at laast soma intarast expansa to ba allocatad against foraign-sourca incoma: no othar country appaars to apply tha intarast allocation raquiramants to tha consolidatad group takan as a whole, rathar than aach numbar saparataly.

In ordar to gain a battar imprassion of tha trua stringancy of othar countrias foraign-tax cradit limitation rulas, wa askad intarnational tax spacialists in tha ovarseas offices of Daloitta Haskins & Salís whathar tha foraign tax cradit limitation rulas wara a major concern of multinational corporations basad in that country, or whathar multinational corporations can ordinarily claim a full cradit for foraign taxas availabla for cradit. Tha ráspense was surprisingly uniform: tha foraign tax cradit limitation was not a major concern for most foraign-basad multinational corporations, full cradit could ganarally ba claimad for foraign incoma taxas. So whila a superficial analysis would indícate that tha 1986 changas in tha foraign tax cradit limitation rulas brought tha U.S. rulas into lina with thosa in othar countrias, on closar examination tha 1986 Act appaars to hava rastrictad U.S. corporations' usa of foraign tax cradit mora tightiy than foraign compatitors' tax systams do.

Tax Traatias

Tax traatias raprasant bilateral agraamants batwaan two countrias undar which, among othar things, ona traaty partnar eliminates its taxátion of spacifiad types of incoma arising'in that first country and earned by rasidants of tha sacond country (a.g., tha withholding tax on intarast) in axchange for tha othar traaty partnar's raciprocating with raspact to comparable incoma earnad by rasidants of tha first country. Tax traatias aiso ganarally provida for tha elimination of intarnational doubla taxation through aithar tax axamption or a foraign tax cradit by tha country of rasidanca. For countrias othar than tha Unitad Statas, tax traatias oftan provida foraign tax cradits and tax axamptions unavailabla undar domastic statutory law.

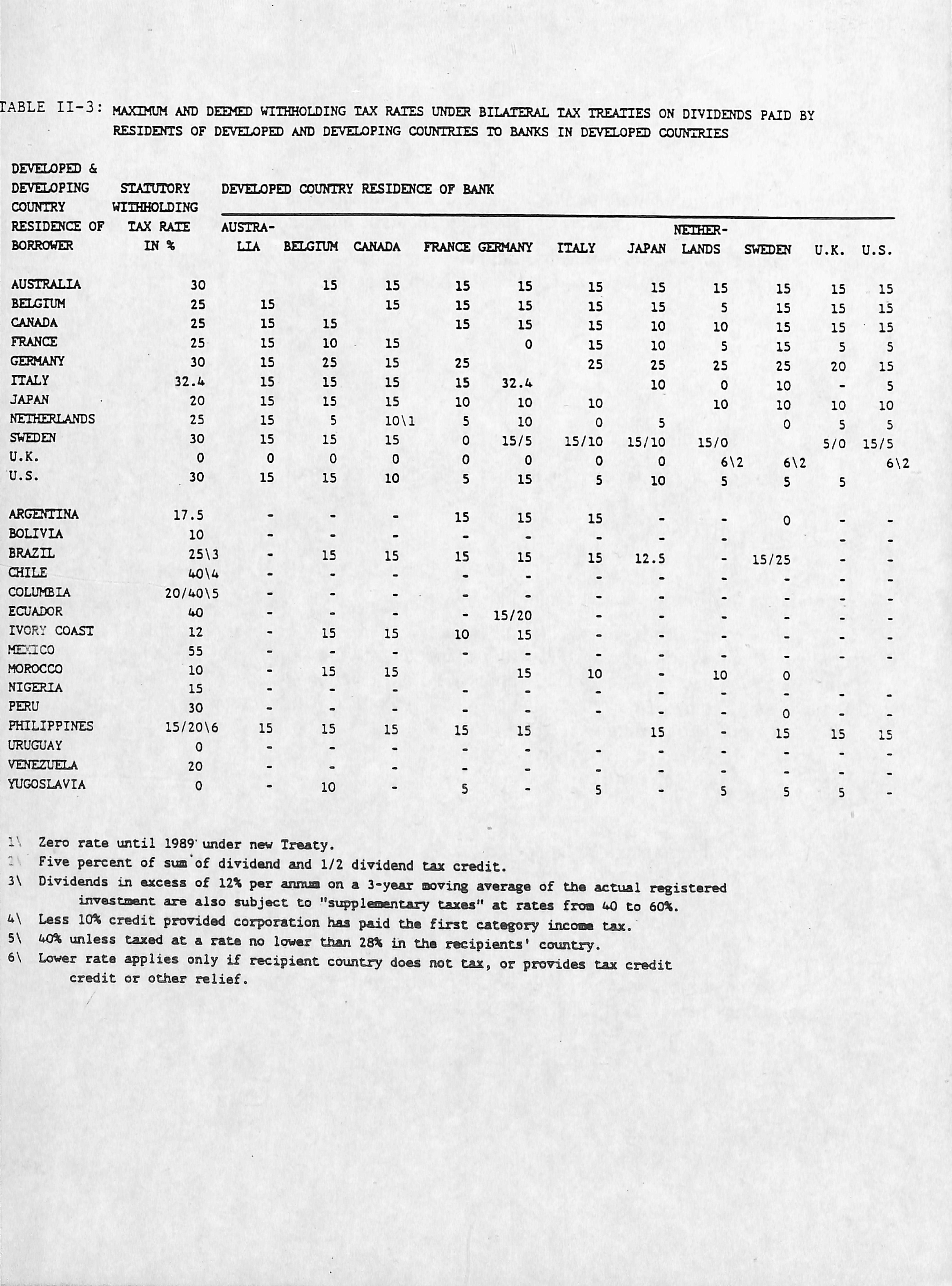

Tablas 11-2 and 11-3 summariza withholding tax ratas on intarast and dividends, raspactivaly, undar various countrias' statutory law and undar its bilateral tax traatias. Whara no bilateral tax traaty applias, or whara tha tax traaty rata axcaads tha statutory rata, incoma would be taxad at tha statutory tax rata. By raading across tha rows of thasa Tablas, ona can compara tha withholding tax ratas applied to dividends and

&

Interest on debts smnired by nortgag., on real «atat. and interest on convertible bonds + incone bonds are subject to 25* withholding tax,

mte^'nl^LrJ"""T" convertible bond, and on incoo» bonds.

Fifteen percant if recexvabl.. collateralized by real estáte located in Italy withholding on re»ittance after withholding of incoae tax. Zaro for loans approved by central banh itnnoiaing May not yet be ratified.

Nine perc^t for loan intarast granted for eore than thre. years by a foreign financial institución in ordar to finance investaents. I^wer rata if recipient financial institución is registered with the Treasury Departaent. Interese on foreign loans exeopt or partially exMpt:

Repaynwnt Period (Including Moratoriua)

MAXIMUM AND DEEMED WIIHHOLDIMG TAX RAIES UNDER BILATERAL TAX TREAIIES ON DIVIDENDS PAIE BY RESIDDÍTS OF DEVQiOPQ) AND DEVELOPING COUNTRIES 10 BANKS XN DEVELOPED COUNIRIES

DEVELOPO & DEVIXOPING STAIÜTORY

COUNTRY WIIHHOLDING

RESIDENCE OF TAX RAE BORRDWER IN

Zero rata until 1989 undar naw Traaty.

Five percent of siá of diridand and 1/2 dividand tax cradic.

Dividands in axcasa o£ 12X par aiutun on a 3-yaar novlng aTaraga of tha actual ragistarad iitrastaant ara alao subjact ta "supplmantary taxas" at ratas froa W) to 60X.

Lasa ioX cradit prorldad eorporation has paid Cha first catagory incoaa tax.

u(A unlasa taxad at a rata no lowar than 28X in tha racipianta' country.

Lowar rata appliaa only if racipiant country doaa not tax, or próvidas tax cradit cradit or othar raliaf.

interest, respectively. received by U.S. corporations to the withholding tax rates applied to comparable income received by otherdeveioped country corporations.

Generaiiy speaking, with respect to dividends and interest having their source in other developed countries, U.S. corporations pay withholding taxes at rates comparable to, or lower than, those for corporations based in other developed countries. With respect to dividends and interest having their source in other developing countries, U.S. investors, unlike their foreign competitors, are often paying withholding tax at the higher statutory tax rate ratherthan a lower treaty rate.

The limited number of U.S. tax treaties with developing countries refleots the U.S. policy opposition to "tax sparing" provisions under which the United States would give a credit for taxes which the developing country might otherwise have imposed, but were spared to attract additional investment. Other developed countries, by contrast, have generaiiy been willing either to exempt income derived from developing countries from home-country tax or to give foreign tax credit for amounts in excess of income taxes actually paid. The result, as noted above, is that U.S. corporations are often subject to the higher statutory withholding tax rates on interest and dividends from developing countries, not the lower tax treaty rates that their foreign competitors often enjoy.

General Tax Provisions

United States

In order to evalúate the impact of the U.S. tax system on companies with foreign operations, it is important to look not oniy at provisions pertaining specifically to foreign income and taxes, but aiso to general provisions that apply to foreign as well as domestic income. Foreign income, like domestic income, benefited significantly from the reduction in the máximum rate of the regular corporate income tax from 46 percent to 34 percent effective July 1, 1987(a blended rate of approximately 40 percent applies to calendar year 1987). This rate reduction considered in isolation will result in a substantial tax saving for U.S.-based service companies, and its effect must be weighed against the base broadening measures described above and below in assessing the impact of the 1986 Act on U.S. companies' international competitiveness.

The Accelerated Cost Recovery System (ACRS) was modified to create addi tional classes of depreciadle property, to reclassify some property to new classes having a longer useful life and to apply a more accelerated depreciation method to short-lived property. Property used predominately outside the United States continúes to be depreciated over a longer life than domestic property, and the use of accelerated depreciation for such property was replaced by straight-line depreciation. The regular investment credit was repealed for property (other than grandfathered "transition property )placed in service after 1985. Moreover,the amount of investment credit

To assure that ai! corporations earning more than de minimis income for financia! reporting purposes wiil pay some tax, Congress aiso enacted in 1986 the Alternativa Minimum Tax (AMT). The AMT generaily equals 20 percent of alternativa minimum taxable income, whioh is calculated by restating regular taxable income (taking account of the new base-broadening rules) to include oertain AMT adjustments and preferences and then adding 50 percent of any remaining differenoe between tentativa AMT income and adjusted book income. For example, AMT taxable" income is adjusted by the amount of the differenoe between regular depreciation and less accelerated "alterna tiva" depreciation. Up to 90 percent of the AMT can generaily be offset by the foreign tax credit, but not by othertax credits (a limitad exception is available for the investment credit claimed with respect to "transition" property or carried ovar from years prior to 1986).

The 1986 Act also repealed or modified oertain deductions and other provisions for specific service industries. Commercial banks have traditionally been allowed a deduction for the net addition to a bad-debt reserve, which is the liability for bad debts which have not been specifically identified as such, but which the bank projects it will suffer basad on its past experience with similar debts and other factors. Under prior law, a formularly deduction basad on a bad-debt reserve equal to 0.6 percent of eligible loans was scheduled to expire at the end of 1987, leaving only an alternativa "actual experience" method. Under that latter method, the bad-debt reserve was computad by multiplying the bank's outstanding loans at the end of the year by a fraction, the numerator of which was the sum of the bank's oharge-offs for actual bad debts for the ourrent and five preceding taxable years, and the denominator of which was the sum of the loans outstanding atthe olese of each of those years.

The 1986 Act repealed the bad-debt reserve deduction for "larga" banks (generaily those with assets in excess of $500 million), with the result that bad-debt losses cannot be deducted until specific loans are determinad to be partially or totally worthless. Moreover, such banks must recapture (i.e., include in taxable income) ratably ovar the four years 1987-90 the accumulated bad-debt reserve outstanding at the end of 1987.

The 1986 Act also made significant changas in the taxation of insurance companies. In the case of life-insurance compañías, the special deduction equal to 20 percent of a life-insurance company's taxable income, which reduced the máximum effective rata of Federal tax from 46 percent to 36.8 percent, was repealed for years after 1986. Thus,the effective rate of tax for life insurance compañías for calendar year 1987 will increase from 36.8 percent to approximately 40 percent before declining to 34 percent for years after 1987. For mutual life insurance companies only, the deduction

for policyholder dividends was reduced by a formulary "differential earnings amount" to achieve an historical 55-45 balance in the tax burden of mutual versus stock Ufe insurance companies and to offset the competitive advantage mutual Ufe insurance compa ñías were allegad to have on account of the deductibiilty of policyholder, but not stockholder, dividends.

The 1986 Act aiso overhauled the taxatlon of property and casualty Insurance companies to provide that:

The deductlon for losses Incurred was reduced by an amount to reflect a time-value of money adjustment for the difference between the time the pollcy Is In effect and the loss Is Initlally accrued and the time It Is expected to be pald;

- The deductlon for losses Incurred was further reduced by 15 percent of tax-exempt Interest plus the deductible portion of dividends recelved from unaffillated corporatlons;

- In Ileu of capitalizing pollcy acquisitlon costs (e.g., agents' commlsslons), property and casualty Insurance companies are currently taxable on 20 percent of the amount which would otherwlse be added to their unearned premium reserve (l.e., premium recelpts whIch would otherwlse be capitallzed and restored to Income ratably over the period the Insurance pollcy was In effect):

Note that these changas generally apply not oniy In determining the taxable meóme of a U.S. corporation (including Its forelgn branches). but aiso In calculating u pail F income and, for deemed-paid forelgn tax credlt purposes, the profits out of which dividends are pald. The Subpart F Income of a forelgn banking subsidlary would generally be calculated without deductlon for any bad-debt reserves, and that of an insurance subsidiary by discounting Its loss reserves and expensing 20 percent of the addition to its unearned premium reserve. Thus. the general base-broadening measures and the Subpart F income measures have greater combinad effect than the sum of the effects ojthe two provislons taken separately.

Forelgn Countrles

1 1 •*

forelgn countrles' máximum corporate Income tax ratas to that ¡n the United States is complicated for those countrles whIch partially or fully Intégrate corporate-level and shareholder-level taxes to relieve the double taxatlon of corporate profits distributed as dividends. in West Germany and Japan, a reduced rate of cor porate tax apphes to distributed profits, so the weighted-average rate of corporate tax decrease as the portion of profits distributed to shareholders Increases. Moreover

^he United KIngdom, France, Belgium, Denmark, and Cañada allow domestic shareholders to claim credit for parí (and. In the case of West Germany, all) corporate-level tax imposed on the profit out of which the dividend was

paid. If that part of the corporate tax is considerad to be the equivalent of a shareholder-level tax for which the corporation is the withholdinQ agent, rather than to be a corporate-level tax, the weighted-average rate of corporate tax rate in all those countries would be further reduced.

With this in mind, Tabie 11-1 indicates that two countries - Sweden and Denmark" had corporate tax rates of 56-58 percent and 50 percent, respectiveiy, higher than even the 46 percent U.S. rate under pre-1986 law.2/ Assuming that 50 percent of before-tax profits are earmarked for corporate-level tax, the weighted average Japanese, Germán and Canadian corporate tax rates appears to be comparable to the prior-Iaw U.S. rate of 46 percent, and the French, Belgian, and Netherlands cor porate rates are 2-3 percentage points less than the oíd 46 percent rate. The United Kingdom rate of 35 percent would be comparable to the 34 percent U.S. rate that carne into effect on July 1, 1987.3/ Switzerland generally applies somewhat lower rates of tax than the new 34 percent U.S. rate, while the rate in Hong Kong is substantially lower than the U.S. rate.

In summary, foreign countries tax corporate income at widely varying weighted average effective tax rates. The 46 percent rate under prior U.S. law was a comparatively high rate, but not as high as the rates in Sweden or Denmark. The 34 percent rate under current U.S. law is certainly below average, but not as low as the rates in Switzerland or Hong Kong.

We also sought to compare the United States rules with respect to banks' baddebt reserves and the discounting of loss reserves of property and casualty insurance companies with comparable provisions in foreign countries. In sum, Japan, West Germany, Switzerland, the Netherlands, France, Sweden, Denmark and Cañada all allow their banks some form of a bad-debt reserve deduction, whereas the United Kingdom, Belgium and Hong Kong do not. None of the eleven foreign countries included in our survey required property and casualty insurance companies to discount losses incurred, but not paid, in the current year. In short, the 1986 elimination of U.S. bad debt reserve and the discounting of property and casualty insurance company provisions will impose U.S. tax burdens that with limited exception have no counterpart in foreign countries' tax systems.

2/ Tabie 1 refiects federal or national income taxes, but generally not income taxes imposed by subfederal or sub-national jurisdictions except in those cases where such taxes are automatically imposed on income earned through foreign branches of domestic corporations (e.g., the Japanese Inhabitants tax). The application of sub-federal or sub-national taxes to foreign source income (e.g., through the inclusión of foreign subsidiaries in a unitary group, the income of which is subject to apportionment in determining a state's taxable income) is an extremely complex question and beyond the scope of this survey.

3/ If corporate taxes for which individual shareholders claim credit are excluded from corporate-level tax, the effective rate of the Japanese, French, U.K., Canadian and particularly the Germán effective tax rates would be reduced further.

Impact on Competitiveness

To assess the impact cf the 1986 Act on the Internationa! competitiveness of U.S. based service industries, one must weigh the tax savings from the 12 percentage point reduction in the corporate income tax rate against the additional U.S. tax resulting from the extensión of Subpart F to interest, insurance and shipping income, the new restrictions on the foreign tax credit limitation, the modifications in the deemed-paid credit rules, and the various base-broadening changes. Necessarily, the impact will vary from industry to industry depending on the rate at which foreign income is taxed in its source country, the incidence of the Subpart F,foreign tax credit limitation rules, and possibly other factors.

Because across-the-board generalizations are diíficult to make, we have sought to assess the impact on a typical investments or activities within a given industry. In performing this analysis, we focused on five service industries -- advertising, commercial banking, investment banking, insurance underwriting, and ocean shipping -- all of which have substantial operations outside the United States and which we believe represent a fair cross section of the service industry. Details of our analyses are set forth in Appendices B-F of this Report and are oniy summarized here.

We have measured the impact of the 1986 Act on international competitiveness by the percentage increase (or decrease) in the amount which U.S.-based companies would have to charge foreign clients for various types of services in orderto achieve the same after-tax profit as they would have achieved under pre-1986 U.S. tax law. As analyzed more fully in Part II of this Report, whether a U.S.-based company could increase its price by that amount without alienating or losing its clients depends, of course, on how competitivo foreign markets for its services are. At one extreme are the highiy specialized services (e.g., merger and acquisition advice) where well-heeled clients may care less about the cost and more about the quality of the service they receive. At the other extreme are the "commodity" services where international com petitiva condjtions may preclude even a 1 percent increase in the charge for the service (e.g., increasing an interest rate charged to a foreign borrower from 10.0 to 10.1 percent per annum). Thus, depending on the context, a 1 percent increase in price may have limited impact on a business or may be sufficient to price a U.S. company out of a hiahiv competitiva market.

Advertising Services

Companies providing personal services ~ that is, services performed by individu áis - have historically been subject to relatively high effective income tax ratas in most countries. At least with respect to their U.S. income, advertising agencies benefitted significantly from the reduction in the corporate rate from 46 percent to 34 percent. Given cultural differences among countries, U.S. advertising agencies can rarely serve foreign clients (including foreign subsidiarias of U.S.-based multinationals) effectively

from the United States or from some low-tax third-country location. Thus, even under prior U.S. law, U.S.-based advertising agencies typically paid foreign taxes equal to or in excess of their foreign tax credit limitation and derived iittie or no benefit from the deferrai of U.S. tax earned through a foreign subsidiary. As a consequence, the reduction of the U.S. rate from 46 percent to 34 percent will result primariiy in foreign tax avaiiable for credit in excess of the U.S. limitation with iittie or no U.S. tax saving.

In the case of a U.S.-based advertising agency serving foreign clients through foreign subsidiaries, we estimate that fees charged to foreign clients would be increased by 1 percent to maintain the same incremental after-tax profit as obtained under pre-1986 law. This result contrasts sharply with an estimated 6 percentage point decrease ín the fee the advertising agency would have to charge if it could serve foreign clients from its U.S. offices without incurring significant foreign taxes in the process. Given the nature of the advertising business however, serving foreign clients from the United States rarely makes good business sense.

Because foreign-based advertising agencies are generally able to claim full domestic credit for foreign taxes paid, the 1986 Act burdened U.S.-based advertising agencies not oniy in comparison to prior U.S. law, but also in comparison with their foreign competitors.

Commercia! Banking

High-Withholdinq Tax Interest

Interest on cross-border loans is often subject to withholding tax at rates of 5 percent to 25 percent (or more). Because withholding taxes are imposed on gross interest - that is, no deduction is allowed for interest and other costs of making the loan "such taxes often exceed the U.S. tax attributable to the r^ income from such loans. Traditionally, U.S. banks and other lenders were able to offset the excess foreign withholding ta)f against the U.S. tax on other, low-tax foreign-source income. Subject to rules "grandfathering" certain outstanding loans, the 1986 Act precludes such foreign tax credit "averaging" in the future by subjecting high-withholding-tax interest to a separata foreign tax credit limitation.

In addition to the separata foreign tax credit limitation for high-withholding-tax interest, crossborder lending also suffered from the requirement that additional interest and other expenses be apportioned against foreign-source income in computing the foreign tax credit limitation and the repeal of the bad-debt-reserve deduction. In the numerical example described at length in Appendix C,the rate of interest charged on a cross-border loan would have to be increased from 8.5 percent per annum to 9.2 percent per annum, an increase of 8 percent.

Foreign banks basad in countries with foreign tax credit systems by statute (e.g., Japan and the United Kingdom) or by treaty often do not appear to face similar restric-

tions on foreign tax credit averaging and thus will enjoy a significant, tax-based competi tiva advantage ovar U.S. banks. Moraovar, as notad abova, tha Unitad Statas has a mora limitad natwork of tax traatias with daveloping countrias than do othar davalopad counthas, so U.S. banks may ba subjact to foraign withholding tax at highar ratas than ara thair foraign compatitors.

Othar Commarciai Banking incoma