The Canadian Mortgage Broker Magazine - Spring 2025

MARKET CONDITIONS

Navigating Canada’s housing outlook p.16 +

BEYOND SUPPLY

Reframing the housing conversation p.8

QUEBEC’S NEW REGULATIONS

Managing and reporting information security incidents p.28

INSIGHTS AND UPDATES

Provincial associations’ conferences p.22, 24, 36

Canada’s Private Lending Space MBRCC’s 2025 Review p.40

Grow from here

At Haventree Bank, we offer smart lending solutions to improve the financial health of Canadian borrowers. We understand the challenges your clients face and are committed to working with you to help Canadians get back on track. Because like you, we see their potential. With flexible terms and empathetic underwriters, we can assist a variety of clients ranging from poor credit to small business owners looking to purchase or refinance their home.

Reach out to our BDM team to learn how a Haventree Bank Mortgage could be the right solution for your Client.

Flexible

Flexible lending when you need it.

Flexible lending when you need it .

cus tom mor tgage solutions your client s require

cus tom mor tgage solutions your client s require

We

We provide a broad range of residential 1s t and 2nd mor tgages tailored to the needs of your self- employed, stated income, and low beacon

client s . Fur thermore, a common sense lending approach allows us to approve and fund deals fas t.

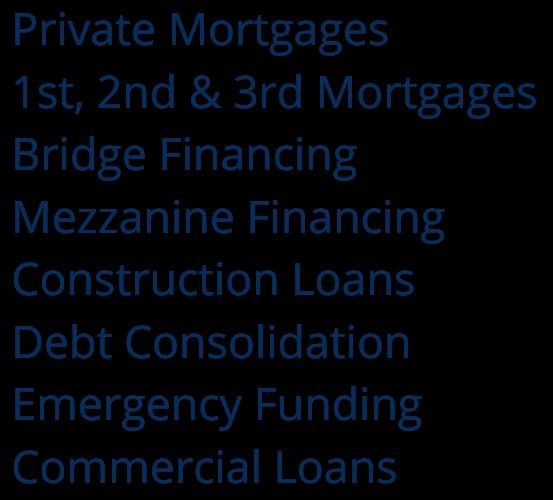

• Re sidential Mor tgages

• LT V Sliding Scale of 6 0% on the balance

• O PEN Terms Standard • B C , Alber ta and Ontario

P r i v a t e L e n d e r – F ilogix, Vel o ci t y a n d L e n des k

P

MBRCC’S 2025 REVIEW

Helpful information for brokers operating in the private lending space BY CARLA GILES 22

EVOLVING MARKET CONDITIONS: NAVIGATING CANADA’S HOUSING OUTLOOK IN 2025

How mortgage brokers can help Canadians manage uncertainty BY CARLA GILES

SUPPORTING BROKER SUCCESS

CMBA Atlantic builds momentum in 2025

BROKERS LOOK FUTURE-FORWARD AT B.C. CONFERENCE

Insights, connections and what’s next for B.C.’s mortgage broker community BY SAMANTHA ASHENHURST

NEW INFORMATION SECURITY INCIDENT FRAMEWORK FOR QUEBEC FINANCIAL INSTITUTIONS

Strict requirements for developing information security incident management policies BY SUNNY HANDA, LOUIS MORISSET, ELINE COLLARD, LINDA MUHUGUSA AND CHLOE BARRETTE

WHEN A GIFT IS NOT A GIFT: RESULTING TRUSTS IN REAL ESTATE

The need for clear legal advice in any gifting of real estate BY SIMON CRAWFORD AND VANESSA KIRALY

CMBA ONTARIO’S 2025 GALA & CONFERENCE

Building a stronger, more connected mortgage community BY MICHELLE CAMPBELL

THE PARTITION ACT

A powerful tool for resolving jointly owned property disputes BY ELLAD GERSH

Advertisers’

Industry Profile: Dustan Woodhouse’s recipe for success BY SAMANTHA ASHENHURST Off the Clock: Marci Deane’s kayaking adventures prove success isn’t just all about work BY SAMANTHA ASHENHURST

RESIDENTIAL COMMERCIAL

CONSTRUCTION DEVELOPMENT LAND

VOLUME 10 ISSUE 2 SPRING 2025

THE CANADIAN MORTGAGE BROKERS ASSOCIATION

EXECUTIVE DIRECTOR Carla Giles

CMBA - ATLANTIC

Mortgage Brokers Association of Atlantic Canada 12 M - 7095 Chebucto Road, Halifax, NS B3L 0A1

CMBA - BC

Mortgage Brokers Association of British Columbia 900-2025 Willingdon Avenue, Burnaby, BC V5C 0J3

CMBA - ONTARIO

Independent Mortgage Brokers Association of Ontario 7 - 40 Winges Road, Woodbridge, ON L4L 6B2

CMBA - QUEBEC L'Association des courtiers hypothecaires du Québec 5855 Taschereau #202, Brossard, QC J4Z 1A5

CANADIAN MORTGAGE BROKER

magazine is produced by the Canadian Mortgage Brokers Association (CMBA National)

Financing plays a central role in unlocking more housing

BY CARLA GILES, MBA, CAE, CEO OF CMBA-BC, MBIBC, EXECUTIVE DIRECTOR, CMBA NATIONAL

In a year marked by growing economic uncertainty, the conversation around housing in Canada remains simple: build more homes. While increasing supply is undeniably critical, focusing on volume alone oversimplifies the challenge. Delivering housing and ensuring it is attainable requires more than units on a map. It demands a broader, systemic approach that addresses not only how much we build, but how we build, who we build for and how Canadians access and sustain homeownership.

Mortgage brokers across the country see firsthand how the system is strained. Clients face not only high prices, but limited housing types, regulatory hurdles, and financing structures that make market entry difficult. While governments at all levels have taken meaningful steps – from zoning reforms to Housing Accelerator Fund investments – Canada’s housing solutions must extend beyond policy cycles. Real progress depends on long-term coordination between industry, government and finance.

A COMPLEX PIPELINE

Canada's housing system faces a capacity challenge. Chronic underbuilding relative to population growth has placed significant pressure on markets – especially in urban centres like Toronto and Vancouver. Yet even as demand climbs, the process of delivering new housing has become increasingly slow and costly.

According to Canada Mortgage and Housing Corporation (CMHC), the average multi-unit project takes seven to eight years from concept to completion – often longer in high-demand cities. This delay is driven by several compounding factors. Skilled labour shortages top the list. BuildForce Canada projects that Canada’s construction industry will face hiring needs of more than 350,000 workers by 2033 due to retirements and new demand. With a potential shortfall of more than 85,000 workers, including in key trades like electricians and HVAC specialists, ongoing labour shortages could continue to delay projects and escalate development costs.

Residential construction costs have also surged – up 36 per cent since 2021, according to RBC’s April 2025 report Canada’s Building

Homes Fast –But For How Long? Combined with elevated financing costs and lengthy municipal approvals, these pressures are jeopardizing the viability of many housing projects.

Yet, there are signs of progress. Canada completed 260,000 housing units in 2024 – the highest in five decades – and 345,000 more were under construction in the first quarter of 2025. But this momentum is not guaranteed. Pre-construction sales in key markets have dropped to multi-decade lows, while shifts in immigration policy may ease demand but create new uncertainties for developers.

Canada’s residential construction sector must also modernize. Productivity gains seen in other industries have largely bypassed homebuilding. Innovative construction methods like modular, panelized and prefabricated systems remain underused. Embracing these technologies could accelerate delivery, reduce costs and improve quality, yet adoption has lagged due to fragmented regulations and limited incentives for adopting new technologies.

Meanwhile, it can take decades for newly built market housing to become more affordable. According to a 2025 CMHC analysis, it can take up to 20 years after completion for new market housing to become attainable for middle-income households.

EXPANDING OPPORTUNITY

Addressing housing challenges also means supporting those trying to enter or remain in the market. Many first-time homebuyers face significant challenges in today’s market – struggling to save for a down payment, qualify under current stress test rules and find affordable homes amid limited supply.

Renewal risk is also growing. About 60 per cent of mortgages are set to renew in 20252026, with many borrowers – especially those who locked in at historically low rates – facing higher payments. Although recent interest rate declines may soften the impact, financial pressure remains significant. Targeted supports such as flexible renewal and improved financial education are critical to maintaining household stability.

A forward-looking housing sector must also reflect how Canadians live. It is not enough to maximize unit counts. We must prioritize livability. Diverse, family friendly and community-oriented housing – connected to services, transit, and opportunity – is essential to building neighbourhoods where people thrive.

FINANCING INNOVATION

Financing plays a central role in unlocking more housing – yet many existing models were not designed for today’s realities. In response to zoning reforms in cities like Vancouver, which now allow four to six stratified units on former single-family lots, some lenders are beginning to adapt. New financing solutions, such as special ized refinancing options, are emerging to help homeowners pursue small-scale redevelopment on their properties.

At the federal level, the Affordable Housing Innovation Fund is encouraging experimentation with new funding models and building techniques. The Apartment Construction Loan Program provides lowcost loans to support rental supply. At the local level, Community Land Trusts (CLTs), such as the Parkdale Neighbourhood Land Trust in Toronto, help preserve affordability by removing land from speculative markets. Vancouver’s Affordable Home Ownership Program similarly helps reduce buyer entry costs through shared equity.

Hour turnaround on commitments – allowing you to present solutions for your clients sooner rather than later.

While none of these options alone can shift the system, they represent important steps. These shifts highlight the importance of aligning financial tools with evolving regulatory frameworks to accelerate innovation and deliver the diverse housing options Canadians need.

BUILDING THE FUTURE

Mortgage brokers are uniquely positioned to bring the housing conversation closer to lived reality. They see the impact of policies on everyday Canadians. As regulated professionals, they help clients navigate complex financial decisions and identify mortgage products and programs that best fit their needs and circumstances.

Canada is making progress, but unlocking our full potential means thinking beyond individual policies or market segments. It requires a long-term vision that aligns land use, training, financing, and innovation to deliver housing that is diverse, sustainable, and inclusive. Mortgage brokers have a vital role in shaping that future – one household at a time.

As we continue to contribute to government consultations and advocate for thoughtful, systemic solutions, we remain committed to ensuring mortgage brokers are part of this national effort.

BRITISH COLUMBIA

Greg Kakuno

Business Development Manager

604-430-1498

gkakuno@capitaldirect.ca

ALBERTA

Donna Hunter

Business Development Manager

403-874-6348

dhunter@capitaldirect.ca

Kyla Hunter

Business Development Manager 403-278-6200 khunter@capitaldirect.ca

ONTARIO

Business Development Manager 905-299-1706

mrendine@capitaldirect.ca

TAKING BETTER BROKER LESSONS

For Dustan Woodhouse, success in mortgage brokering isn’t about rigid formulas – it’s about agility, connection and continual learning.

BY SAMANTHA ASHENHURST

When Canadian Mortgage Broker connected with Dustan Woodhouse to interview him for this article, the Vancouver-based entrepreneur, author and public speaker had just finished broadcasting an episode of his live weekly podcast, Be the Better Broker.

“I launched the podcast in March 2020 without realizing it was a podcast,” says Woodhouse. “It started as 60- to 90-minute Zoom meetings, open to any brokers in Canada who wanted to attend. Word got around and people started asking me for recordings of previous sessions. That was when I realized – ding! – I’ve got a podcast on my hands.” Initially titled This is Brokering, the podcast ran in its original form for more than 425 episodes, wrapping up at the end of 2024. In early 2025, Woodhouse introduced the show under its current title, Be the Better Broker.

“The people who have been in the industry for five to 10 years probably know me best as the author of the Be the Better Broker book series,” he says. “The podcast is a way of updating some of that content, as well as discussing new topics.”

So, every Tuesday at 9 a.m. Pacific, Woodhouse goes live.

“I usually do 20 to 30 minutes,” he says. “Sometimes I have guests, but usually it’s a rant of what’s what that week. A lot of times I touch on the noise and then try and bring people back to the facts.”

In addition to podcasts and books, Woodhouse’s Be the Better Broker brand, established in 2014, encompasses weekly blog posts, as well as a training program, which includes workshops, one-on-one coaching and the annual BTBB Summit. This reach provides ample material for sessions and supports an overall mission of helping mortgage brokers achieve peak performance in their careers.

“I have a regular group of brokers who I have conversations with every week,” says Woodhouse. “So, I have my ear to the ground across the country of what’s happening in different spaces. When I unpack the reasons why brokers having certain

challenges, I realize the challenges themselves are pretty common, which makes for great podcasts and posts.”

While Woodhouse has certainly established himself as a trusted advisor and thought leader in the industry, his path to becoming a mortgage broker was anything but predetermined. In fact, when he first heard the suggestion, he barely knew what the role entailed.

“I had a number of people around me saying, ‘You’d be a great fit for this,’” he says. “I honestly didn’t even really know what a mortgage broker was.”

At that time, Woodhouse was running his own highperformance automotive parts business, which was primarily focused on mail orders to the United States. In this role, he had developed a crucial skill that would transfer nicely to the world of brokering: building long-term relationships with customers –particularly over the phone.

“If you’ve already got that skill of connecting with others via telephone or video call, that’s a huge piece of it,” Woodhouse says. Ultimately, it was the steady encouragement from those around him that led him to the career change.

“I made the pivot in 2008 after six or seven people in my orbit said to me, ‘You should be a broker,’” says Woodhouse. “Finally, I listened to one of them. He knows who he is.”

His professional journey is just one example of how folks from vastly different backgrounds can thrive in the mortgage industry if they’re personable, curious and interested in building lasting connections, Woodhouse says.

“You can come into this business from just about any walk of life,” he explains. “If you’re somebody who asks a lot of questions – questions of clients, questions of lenders, questions, questions, questions – you’ll probably do quite well.”

Of course, that’s not to say it’s all smooth sailing in brokering.

“While this has never been an easy business to find success, it’s certainly more difficult now than ever before,” he says, citing changes in lending criteria and a shifting political landscape as significant factors.

“The only way you’re going to get that next client across the finish line is to stay on top of the changes happening within the industry and within different lenders. The only real way to do that is, frankly, to interact with other brokers and with lender reps in those different types of settings.

That said, one defining feature of mortgage brokering he appreciates is the industry’s robust collaborative spirit. Unlike what is seen in other competitive fields, brokers, he notes, tend to work together and help each other succeed.

“Michael Thorne, who presented at this year’s CMBA-BC Conference, mentioned to me how impressed he was with the comradery in our industry,” says Woodhouse. “He couldn’t believe how collaborative we are with one another. Even when working with different firms, we really work to help each other.”

Key to this support, of course, is building a strong network and staying on top of the latest developments.

“Attending events is crucial in this industry,” says Woodhouse. “Conferences are vital, of course, but just as important are ongoing events throughout the year. The only way you’re going to get that next client across the finish line is to stay on top of the changes happening within the industry and within different lenders. The only real way to do that is, frankly, to interact with other brokers and with lender reps in those different types of settings.”

“It's very difficult to stay on top of all the things, if you never leave your office, right? That’s the reality.”

For those entering the industry, Woodhouse has clear, actionable advice: Consistency in branding and outreach is essential.

“You need to repeat yourself over and over,” he says. “You need to remind everyone in your social circle that you are a mortgage broker. It needs to be in the email signature for every message you send. If you send out an email to your extracurricular sports team or community group, be sure to use your email signature to broadcast what you do.”

“The number one, first and foremost reason people will work with you is they trust you –and they like you.”

But his most unwavering advice? The importance of making outbound calls.

“Pick up the phone and make at least 10 outbound calls every single day, five days a week,” says Woodhouse. “If you want to be successful, that is the guaranteed path. If 10 calls a day isn’t doing it, make 20. If 20 isn’t doing it, make 30. You’ve got eight work hours in the day at least – and, if you don’t have any clients, what else are you doing with your eight hours?”

Grow Your Expertise: Access top industry courses and webinars

Expand Your Network: Connect with brokers and lenders nationwide

Advance Your Career: Gain tools and insights to stay ahead

Shape the Industry: Be a voice for mortgage professionals with CMBA National

Ready to thrive in the mortgage industry? Join us today!

cmbabc.ca cmbaontario.ca cmba-achc.ca/quebec

cmbaatlantic.ca

EVOLVING MARKET CONDITIONS

NAVIGATING CANADA’S HOUSING OUTLOOK IN 2025

How mortgage brokers can help Canadians manage uncertainty

BY CARLA GILES, MBA, CAE, CEO OF CMBA-BC, MBIBC, EXECUTIVE DIRECTOR, CMBA NATIONAL

Canada’s housing market is navigating a period marked by heightened economic uncertainty, shifting financial conditions and evolving consumer preferences. Mortgage brokers and lenders must grasp these dynamics thoroughly to advise their clients effectively. This article explores key market drivers, including economic policy uncertainty, interest rate volatility, housing inventory trends, construction forecasts and new insights from national housing statistics.

ECONOMIC UNCERTAINTY: THE DRIVING FORCE

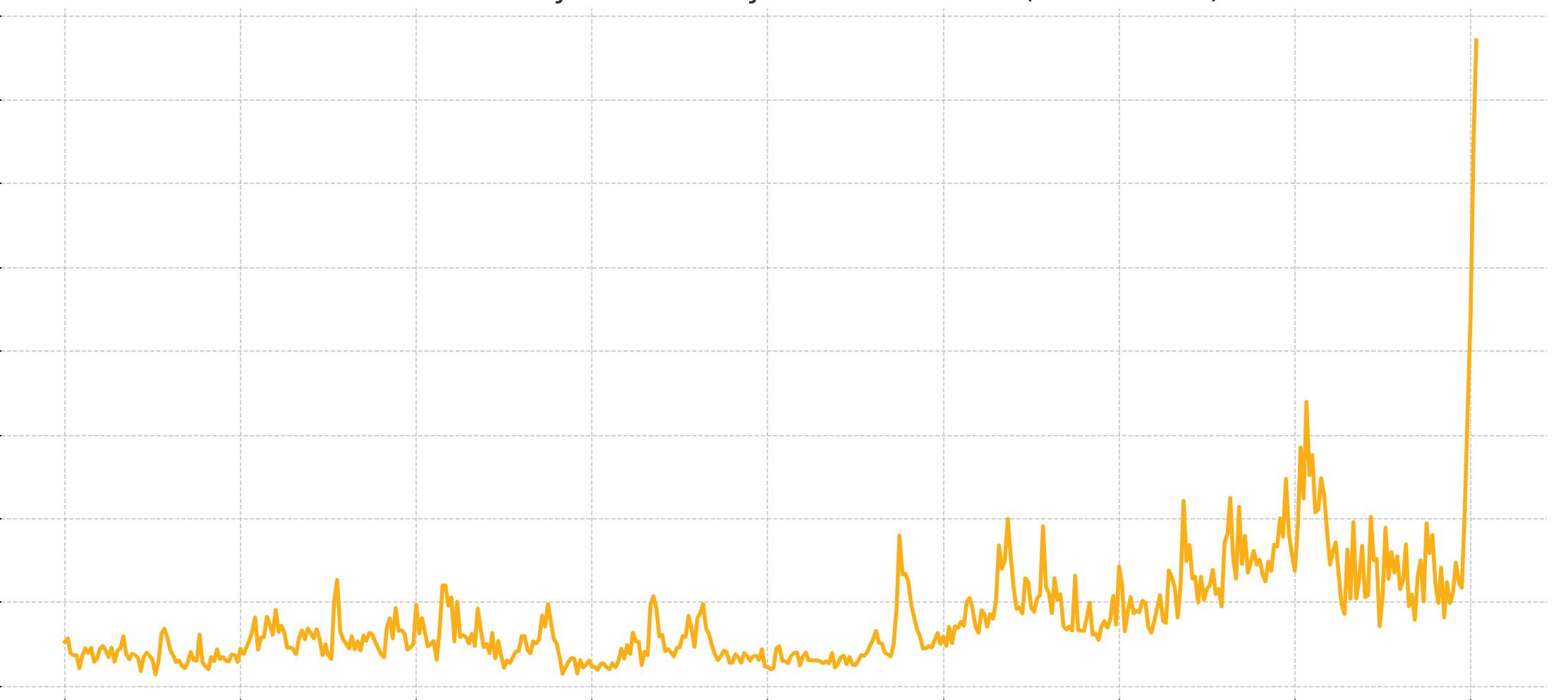

Canada’s housing market slowdown is largely being fueled by significant economic uncertainty. The Economic Policy Uncertainty Index – developed by economists at Northwestern University and Stanford University – has surged to unprecedented levels, exceeding the peaks observed during the 2008 financial crisis and the early pandemic years. Global tariff disputes and unpredictable trade policies, particularly with Canada’s major trading partners, are the main reasons.

Economic Policy Uncertainty Index for Canada (1985–2025)

Economic uncertainty in Canada has surged to levels higher than during the 2008 financial crisis and the early pandemic years. Rising global trade tensions and tariff disputes are key contributors, impacting consumer confidence and housing market activity.

Source: ‘Measuring Economic Policy Uncertainty’ by Scott Baker, Nicholas Bloom and Steven J. Davis at www.PolicyUncertainty.com.

market drivers

The impact is more noticeable for workers in trade-sensitive sectors such as manufacturing, forestry and energy who are increasingly anxious about job stability. In turn, many potential homebuyers are delaying major financial decisions, contributing to the notable pullback in home sales across the country.

HOME SALES AND INVENTORY: A SHIFT TOWARD A BUYER’S MARKET

Recent national statistics from the Canadian Real Estate Association (CREA) confirm that housing activity is losing steam. According to CREA’s March 2025 Housing Market Report:

n National home sales fell by 4.8 per cent month-over-month, marking the fourth consecutive monthly decline.

n Sales were 9.3 per cent lower year-over-year, recording the weakest March performance since 2009.

n The sales-to-new listings ratio dropped to 45.9 per cent, signalling a definitive shift toward buyer’s market conditions. (A ratio between 45 per cent and 65 per cent typically suggests a balanced market.)

The number of properties listed for sale rose 3 per cent in March compared to February and climbed 18.3 per cent compared to the previous year, totaling 165,800 active listings. While still slightly below the long-term average of 174,000, this rise points to growing inventory levels, especially as sales continue to slow.

The Value Is Just The Tip Of The Iceberg

By staying informed and providing client-focused advice, mortgage brokers can help Canadians manage uncertainty and maintain financial resilience through these changing times.

The MLS® Home Price Index (HPI) fell 1 per cent month-over-month – the steepest drop since November 2023 – and declined 2.1 per cent year-over-year. Meanwhile, the national average home price slipped to $678,331, a 3.7 per cent decrease compared to March 2024.

In short, Canada’s housing market is rapidly adjusting: a growing supply of homes, falling sales and softening prices are reshaping conditions in favour of buyers for the first time in years.

Regional insights:

n Ontario and British Columbia are experiencing the largest sales declines and renewed price softness, particularly in urban centres like Toronto and Vancouver.

n Prairie provinces, Quebec and the East Coast continue to see modest price growth, thanks to tighter inventories and more stable local economies.

INTEREST RATE ENVIRONMENT: MANAGING VOLATILITY

Another critical factor shaping the market is interest rate volatility. Bond market fluctuations – driven by global economic uncertainty – have caused government bond yields to hover between 2.5 per cent and 2.8 per cent, impacting fixed mortgage rates, which currently average around 4.4 per cent for five-year terms.

The Bank of Canada has kept its overnight rate steady at 2.75 per cent, within its neutral range. However, the risk of further adjustments remains, depending on how trade tensions and inflation evolve.

DEMOGRAPHIC SHIFTS AND LONG-TERM IMPLICATIONS

Beyond short-term volatility, Canada’s longer-term housing demand is poised to shift due to demographic changes. According to Oxford Economics, federal policies aimed at significantly reducing the number of non-permanent residents could result in Canada’s first population decline since Confederation in 1867. Slower population growth would likely dampen future housing demand and suppress economic expansion, reinforcing a low-interest-rate environment over the longer term.

Mortgage brokers must remain alert to these macro trends, as they will influence market fundamentals and client strategies well into the next decade.

INSIGHTS FROM CMHC: SLOWING NEW CONSTRUCTION

Adding to the shifting landscape is a forecasted slowdown in new housing construction, outlined in the Canada Mortgage and Housing Corporation’s (CMHC) 2025 Housing Market Outlook:

n Housing starts are expected to slow, largely due to a steep decline in condominium apartment construction.

n Investor demand for pre-construction condos is weakening, especially in Ontario, making it harder for developers to finance and launch new projects.

n In British Columbia, a slowdown is anticipated but will be milder and delayed due to relatively strong resale markets.

n Alberta is likely to be more insulated from the slowdown, as its housing market remains more resident-driven and less dependent on investors. Rental apartment construction – which hit record highs in 2024 – is expected to remain strong through 2026, thanks to government incentives and a robust renter population.

However, softening rental conditions could reduce new project starts beginning in 2027. Meanwhile, construction of ground-oriented homes (like townhomes and single-detached houses) may experience a modest rebound at lower price points. Still, developers face challenges competing with the resale market, given high construction costs and squeezed profit margins.

MORTGAGE RENEWAL RISKS: PREPARING CLIENTS FOR HIGHER PAYMENTS

One of the most pressing risks emerging in 2025 is the financial strain facing homeowners renewing mortgages taken out during the period of ultra-low rates. Many borrowers will see higher payments at renewal, although recent interest rate declines suggest the increases will be smaller than previously expected. Mortgage brokers must prepare their clients for these financial shocks by offering proactive advice on budgeting, refinancing options and potential strategies to ease transitions into higher-rate environments.

While mortgage delinquency rates remain relatively low, they could rise if economic conditions worsen or if job losses become more widespread.

GUIDANCE FOR MORTGAGE BROKERS

To successfully navigate the evolving housing market, mortgage brokers should:

n Monitor bond yields and mortgage rate movements to stay ahead of financing trends.

n Proactively educate clients about upcoming mortgage renewal risks and mitigation strategies.

n Tailor advice to reflect regional economic realities and housing market conditions.

n Track demographic shifts and their impact on housing demand and economic growth projections.

By staying informed and providing client-focused advice, mortgage brokers can help Canadians manage uncertainty and maintain financial resilience through these changing times.

Balancing a thriving mortgage career with a passion for adventure, Marci Deane has carved out a life where kayaking provides both escape and connection, proving success isn’t just about work.

OPEN WATER FINDING BALANCE ON

BY SAMANTHA ASHENHURST

Marci Deane’s journey as a mortgage broker began nearly two decades ago, driven by a desire to build a fulfilling career while maintaining the flexibility to prioritize her family. Since 2007, she has served North Vancouver, carving out a reputation as a trusted advisor in the industry, specializing in first-time buyers, renewals and reverse mortgages.

Beyond her professional success, Deane has cultivated a life rich in adventure and personal growth. Specifically, her passion for kayaking – which was sparked, in part, by a chance encounter on a flight to Mexico – has become an integral part of her lifestyle, allowing her to balance the demands of her work with the freedom of the open water.

“About 15 years ago, I was headed to an all-inclusive resort in Mexico,” she tells Canadian Mortgage Broker. “The family next to me on the plane was going to a different Mexican destination on a kayaking trip.”

Despite living 10 minutes from scenic Deep Cove, Deane had never kayaked.

“When they mentioned that, I thought, ‘oh, that’s cool,’” she says. “It really stuck in my mind.”

It was years later when Deane finally tried the sport after attending an event and winning a two-hour kayaking lesson.

“It was a terrible, rainy, horrible West Coast day,’” she recalls, “but I still kind of loved it.”

With her interest piqued, Deane started attending Women on Water (WOW) events at a local club, Deep Cove Kayak. Running from April to October, WOW meets every Thursday and provides a safe, inclusive space for women of any skill level to get together and kayak.

WATER

“You don't need any gear,” says Deane. “You show up, you get in the kayak and go as a group. No experience necessary.”

Deane began attending the weekly events, bringing some friends along to join in on the fun. The communal aspect of WOW quickly grew into a tight-knit group of women, all drawn to the camaraderie and freedom kayaking provides.

“It’s six of us who have been doing it for a few years now,” says Deane. “We still go to WOW, but also all bought annual memberships, so we can go out on our own now, too.”

Indeed, what started as a local hobby has expanded into breath-taking expeditions. Four years ago, Deane and her kayak crew headed to Telegraph Cove and Broughton Archipelago Marine Park off Vancouver Island for a multi-day guided kayaking adventure. In the summers that followed, they made similar trips to Desolation Sound and Quadra Island.

“We’re kind of princesses,” Deane says of the group’s adventures. “We find a lodge to stay. We’re not hardcore enough to camp.”

Last month, Deane and her crew headed down to Loreto, Mexico, where they spent two days kayaking on the Sea of Cortez.

“One of the problems in our business is that it can be hard to fit stuff in unless it’s in your calendar,” she says. “Kayaking is something I book in advance, so I’m always sure to make it.”

Of course, Deane’s experiences on the water aren’t always smooth sailing. A particularly rough day on the Sea of Cortez tested her endurance.

“The second day we were there, we got caught in a huge wind event,” she says. “It was some of the hardest kayaking I’ve ever done. You can't stop when you’re in the rolling sea because, if you do, that’s when you’re going over. You have to just keep your eyes forward.”

For Deane, kayaking has become a gateway to unforgettable moments, deep reflection and a sense of serenity rarely found in daily life.

“On the trip we did to Desolation Sound, there was a beautiful sunset,” she says. “Our guide asked us all to find a spot on the rocks and just be in silence for 20 minutes.”

That rare quiet, away from the hum of the city, offered a profound connection to nature and the present moment. Standing on the rocks, watching the sun sink into the horizon, Deane felt the kind of peace words can’t quite capture.

“It was an interesting full-circle moment,” she says. “I remembered, years earlier, when I met that family on my trip to Mexico. Now I’m doing the same thing they were doing.”

One of the most profound aspects of Deane’s kayaking experiences is the opportunity to disconnect from work.

“When you’re out there on the water, you can’t answer emails or texts because you’re busy paddling!” she says. “You have to not be a mortgage broker for a couple of hours.”

The trip to Loreto provided an even greater sense of separation.

“For the first time, I forwarded my emails and had no cell service for three days,” says Deane. “I had a plan in place – I had my assistant available and I had an autoresponder – but I was largely off the grid. And guess what? Nothing bad happened.”

Deane credits kayaking with keeping her grounded and ensuring she makes time for herself.

“It was an incredible 20 minutes, just being in the silence,” she says. “It was very powerful.”

Through kayaking, Deane has found community, adventure and a space to reset – proof that embracing time away from work can be just as rewarding as professional success.

This interview with Marci Deane continues our series Brokers off the Clock. In every issue, we ask a mortgage broker to tell us what they like to do when they’re not behind a desk. Be it birdwatching, running marathons, stoking your wanderlust through travel to exotic locations or supporting community initiatives, we want to know how you unwind. Would you like to be profiled in a future edition – or suggest a fellow mortgage broker?

Contact info@cmba-achc.ca

Top: Through kayaking, Marci Deane has found community, adventure and a space to reset. Centre from left: Just another Thursday night in Deep Cove at WOW; A moment of quiet reflection in Desolation Sound. Bottom: A full day of kayaking: En route from Powell River to Desolation Sound.

SUPPORTING BROKER SUCCESS

CMBA Atlantic Builds Momentum in 2025

The Canadian Mortgage Brokers Association Atlantic (CMBA Atlantic) is making waves this year with an ambitious calendar of events and a renewed focus on expanding its reach across the four Atlantic provinces. Following a successful Symposium in February and the appointment of a new board of directors and executive team at its April AGM, CMBA Atlantic is turning its attention to growing membership and hosting events in more locations to better serve the regional broker community.

On August 19, 2025, CMBA Atlantic will host its Annual Charity Golf Tournament at the Belvedere Golf Course in Charlottetown, Prince Edward Island – a premier Canadian golf destination. Chosen for its accessibility, the course is a short drive for brokers from New Brunswick, Nova Scotia and Prince Edward Island, and easily reached via airports in Charlottetown and Moncton.

This event offers more than just a great round of golf. With a 1 p.m. shotgun start, brokers and lender partners will enjoy quality time together in a relaxed, off-site setting – perfect for building relationships

and exchanging ideas. It’s also an opportunity for brokers to meet with provincial directors, explore ways to grow their business and connect over shared goals.

Proceeds from the tournament will go toward a cause that reflects the heart of the mortgage profession: helping people find homes. It’s one way CMBA Atlantic is contributing to solutions for the housing crisis – through community, connection and action.

Stay tuned for more details on the tournament and additional events being planned to support broker success in Atlantic Canada.

Ensuring our borrowers see a clear path to success is our unique specialty. We’re one of North America’s leading non-bank commercial mortgage lenders with over $3 billion under administration. We specialize in bespoke lending solutions for commercial real estate financing in amounts from $10M to $100M. We’ll share your vision, and your entrepreneurial mindset, to provide time-sensitive lending and financing solutions. Let’s talk. 800 494 0389 | romspen.com

BROKERS LOOK FUTURE-FORWARD AT B.C. CONFERENCE

Insights, connections and what’s next for B.C.’s mortgage broker community

BY SAMANTHA ASHENHURST

More than 500 mortgage brokers and industry partners gathered at the JW Marriott Parq Vancouver on April 7 and 8 in celebration of the annual Canadian Mortgage Brokers Association – British Columbia Conference & Trade Show.

The event featured thought-provoking sessions and dynamic speakers who encouraged attendees to embrace a ‘future-forward’ mindset, while also prioritizing human connection.

Kicking off the event was a keynote address from digital innovator and thought leader Kate O’Neill. Regarded as a ‘tech humanist,’ O’Neill emphasized the critical balance between digital transformation and human connection, challenging attendees to combine the efficiency of artificial intelligence with the authenticity of genuine human empathy. At its core, her presentation reiterated that technology, as a tool, can help amplify meaningful experiences, but it should not replace human touch.

Building on O’Neill’s message, next to the stage was Michael Thorne, real estate veteran and AI-thought leader. Thorne’s tech-focused presentation offered strategies for how brokers can leverage artificial intelligence to reclaim hours and streamline workflows. Moving beyond the fundamentals, Thorne unpacked how, exactly, one can channel the power of ChatGPT’s intelligence and refine prompting techniques to achieve genuinely smart outcomes.

The afternoon’s sessions embodied the theme of adaptation and resilience, beginning with a keynote presentation by behavioural finance expert Preet Banerjee, who shared valuable insights on improving ‘advice adherence’ and boosting referrals in times of economic uncertainty. Following the keynote, attendees enjoyed a Fireside Chat, where industry leaders exchanged proven strategies for navigating today’s competitive market.

Health and wellness took centre stage the next morning with a standout keynote address from best-selling author and human physiologist, Dr. Greg Wells.

Clockwise from top left: Cluny Coghlan and Lisa West hitch a ride on some dinosaurs; The Lender Panel: Dustan Woodhouse, Kristina Morrison, Imran Khokhar, Dwayne Schmidt and Mark Gawehns; Keynote speaker Kate O’Neil; Ryan W. Smith and Brittany Smith collect stamps for the trade show passport contest; Building connections during an energy break; Keynote speaker Dr. Greg Wells; Attendees enjoying Preet Banerjee’s keynote presentation.

CMBA British Columbia conference

In his session, Dr. Wells explored the science behind peak performance and emphasized the importance of quality sleep as a cornerstone of mental and physical well-being. Specifically, he advocated for ‘defend our last hour’ of each day, using that time to unplug and reset. Sustainable success, Dr. Wells explained, isn’t about working harder, but working smarter – balancing intense performance with meaningful recovery. Practical takeaways included managing technology distractions, protecting sleep quality and recognizing rest as a necessity; not a luxury.

What better way to nurture your brain than with a good book? The day’s agenda continued with the inaugural Broker Book Club, where panelists presented the book that changed their life and shared how it shaped their business and professional development. Up next, business strategist James Kirkwood presented a brand-building workshop with practical insights for how mortgage brokers can stand out, grow their business and secure long-term success.

Amidst the day’s activities, attendees gathered for the MB Awards luncheon. Celebrating excellence and innovation, the awards ceremony was a poignant reminder of the industry’s collective achievements and aspirations for the future. Among this year’s recipients, Troy Resvick received the prestigious Pioneer Award.

The afternoon continued with a much-anticipated market update from keynote presenter Brendon Ogmundson, chief economist of the BC Real Estate Association. Ogmundson covered key topics –including employment rates, housing inventory and tariffs – and their potential impact on Canada. Always insightful and engaging, Ogmundson offered a clear overview of past events shaping B.C.’s current economic climate, along with expectations for the months ahead.

The conference culminated in a lively lender panel. Executives from leading institutions convened to dissect market dynamics and predict future trends, offering attendees unparalleled insights into the pulse of the mortgage industry.

As the CMBA-BC Future Forward Conference wrapped up, attendees left with fresh perspectives, invaluable connections and actionable strategies to navigate an evolving industry. From thoughtprovoking discussions on technology and meaningful engagement to practical insights on market trends and business growth, the event reinforced the importance of adaptability and innovation. More than just a conference, it was a catalyst for progress – a place where professionals could learn, share and propel their businesses forward. With an eye on the future and a commitment to excellence, the mortgage industry continues to evolve. Those who embrace change are poised to lead the way.

MB Individual Partner Recognition recipient; Wayne

MB Community Service Recognition recipient, and Sunny Sarai; Tracey Morrison, accepting the MB Corporate Partner Recognition honour on behalf of Verico Lighthouse Mortgage Corp., with Harriet Cammayo; CMBA acting president Deb White and Troy Resvick, recipient of the MB Pioneer Award for Lifetime Achievement. Below, Taylor Lewis, vice-president of CMBA National.

Top: Kevin Oake attending a session. Above, clockwise from top left: Nolan Smith and Tony Spagnuolo,

Mah,

INFORMATION SECURITY INCIDENT FRAMEWORK FOR QUEBEC FINANCIAL INSTITUTIONS

BY SUNNY HANDA, LOUIS MORISSET, ELINE COLLARD, LINDA MUHUGUSA AND CHLOE BARRETTE

On April 23, 2025, Quebec’s Regulation respecting the management and reporting of information security incidents by certain financial institutions and by credit assessment agents (Regulation) came into force. Issued by the Autorité des marchés financiers (AMF) and approved by the Minister of Finance, this Regulation establishes a new framework for Financial Institutions (hereinafter defined) to manage and report “information security incidents.”

APPLICATION

The AMF regulates Quebec’s financial sector and assists consumers of financial products and services. Its regulatory activities include:

n Insurance

n Deposit institutions (excluding banks, which are federally regulated under the federal Bank Act)

n Securities and derivatives

n Distribution of financial products and services

n Mortgage brokerage

n Credit assessment

Entities wishing to engage in these financial activities in Quebec must obtain authorization from the AMF and be listed in a publicly available online register.

With this in mind, the new Regulation applies to designated credit assessment agents under the Credit Assessment Agents Act and the following financial institutions (these entities are collectively referred to as “Financial Institutions”):

INFORMATION SECURITY INCIDENT

The Regulation defines an “information security incident” as “an attack on the availability, integrity or confidentiality of information systems or the information they contain.”

Notably, such definition of information security incidents is broader than the definition of “confidentiality incidents” under the Act respecting the protection of personal information in the private sector (Quebec Privacy Act), which refers to instances of unauthorized access, use, communication or loss of personal information,

as well as any other breach of the protection of this information. It encompasses not only breaches of personal information but also other incidents affecting information systems. Presumably, it includes unlawful access to confidential or business information, data encryption or malware. Given the breadth of the definition, a case-by-case analysis will be necessary to determine whether notification must be provided to the AMF.

NEW OBLIGATIONS

1.

Developing an Information Security Incident Management Policy

The Regulation mandates that Financial Institutions develop and implement an information security incident management policy (Policy). The Policy must include procedures and mechanisms to detect, assess and respond to information security incidents within the Financial Institution or any third party entrusted with parts of its activities. The Policy must also include procedures for reporting these incidents to the Financial Institution’s officers or managers, as well as to other stakeholders, such as clients, third parties, consumers, the AMF and other regulatory bodies.

Furthermore, the Financial Institution must assign in writing the responsibility for monitoring the management and reporting of information security incidents to one of its officers or, in the case of financial services cooperatives, one of its managers.

Quebec regulatory activities

2. Reporting Information Security Incidents

The Regulation stipulates that notification must be provided to the AMF for the following information security incidents using the form on its website: a. Incidents with Potentially Adverse Impacts

n An information security incident that may have “potentially adverse impacts” must be reported. We note that the Regulation does not define “potentially adverse impact” and provides no indication about the criteria that should be considered to make such a determination.

n Notification Deadline: Within 24 hours of the officer or manager receiving a report.

b. Incidents Reported to Specific Organizations or Individuals

n Any information security incident reported to or subject to a notice to:

• a regulatory body;

• an entity responsible for crime prevention, detection or repression; or

• an entity contractually responsible for compensating injury caused by the incident.

n Notification Deadline: Within 24 hours of the officer or manager receiving a report.

c. Confidentiality Incidents

n Any confidentiality incident involving personal information that poses a risk of serious injury, such that it must be notified under the Quebec Privacy Act

n Notification Deadline: At the same time as notifying the Commission d’accès à l’information (CAI).

Following its initial notification to the AMF, the Financial Institution must provide the AMF with updates on the information security incident at least every three days, and it must continue to do so until it notifies the AMF that the incident is “under control” and operations have returned to normal. The Regulation does not characterize “under control.”

In addition to the notifications, a post-incident report must be submitted to the AMF within 30 days of the notice indicating that the incident is under control and that operations have returned to normal. This report must identify the source of the incident, determine its type, assess the potential for recurrence and describe the actions taken to reduce the likelihood of incidents of similar nature occurring in the future.

3. Maintaining an Information Security Incident Register

A Financial Institution must maintain a current information security incident register and ensure that all recorded information for each incident is kept in a secure and confidential manner to preserve the information’s integrity for at least five years from the date of the corresponding post-incident report. For each information security incident, the Financial Institution must record the date, time, location and nature of the incident, provide a detailed description, indicate any injury caused, identify any third parties involved, outline the actions taken, and indicate whether the residual risk is accepted or not, along with the rationale for this decision. Additionally, the register should list planned actions and record the incident close date. Financial Institutions should consider updating their record-keeping practices to reflect these new requirements.

PENALTIES

Monetary administrative penalties for various contraventions of the Regulation range from C$250 to C$500 for individuals and from C$1,000 to C$2,500 for Financial Institutions.

Contraventions include, for instance, failures to develop an information security incident management policy, appoint an incident management officer, report incidents to the AMF within 24 hours or keep an information security incident register.

BEST PRACTICES

The Regulation imposes strict requirements for developing information security incident management policies, adhering to reporting obligations and maintaining records. To comply with the new obligations that aim to supplement existing laws on personal information protection, Financial Institutions should ensure they have robust policies, procedures and practices in place to handle information security incidents and meet these new regulatory requirements. Financial Institutions should also remain aware of the various other reporting

requirements that may apply to them. For example, some Financial Institutions, such as insurance companies and federally incorporated trust and loan companies, are also federally regulated financial institutions (FRFIs) and are subject to supervision by the Office of the Superintendent of Financial Institutions (OSFI). According to the OSFI instructions, FRFIs must report technology and cybersecurity incidents to OSFI within 24 hours. A list of federally regulated financial institutions is available on the OSFI website.

Other provinces may also have different requirements. In 2021, the British Columbia Financial Services Authority (BCFSA) developed an Information Security Guideline. Although it does not mandate a reporting scheme, financial institutions in British Columbia are expected to promptly notify

BCFSA of any material information security incidents and submit an incident report within 72 hours.

Given the diverse and evolving regulatory landscape, Financial Institutions must stay informed and vigilant about their reporting obligations across various frameworks and be prepared to comply.

This article is republished with the permission of Blake, Cassels & Graydon LLP, a leading Canadian law firm with offices in Toronto, Calgary, Vancouver, Montréal, Ottawa, New York and London. In the Montréal office Sunny Handa is a Partner and Technology Practice Leader, Louis Morisset is a Strategic Counsel; Eline Collard is a Staff Lawyer; Linda Muhugusa is an Associate; and Chloe Barrette is an Associate. More information: blakes.com

When it comes to estate planning, joint tenancy is often seen as a simple way to transfer property after death while bypassing probate fees. But as the case of Jackson v Rosenberg shows, what may seem like a straightforward solution can lead to unexpected legal disputes. When Nigel Jackson added Lori Rosenberg as a joint tenant of his home, he intended to secure her inheritance through the right of survivorship (a hallmark of joint tenancy). However, when a change of heart led Jackson to sever the joint tenancy, the move sparked a legal battle over the true meaning of a “gift” in property law and whether Rosenberg had an interest in the home beyond the right of survivorship. Here’s what unfolded and what it means for future property owners.

BACKGROUND

Nigel Jackson owned a home in Port Hope, Ontario. In 2012, he transferred the title of the home into joint tenancy between himself and Lori Rosenberg, his late partner’s great niece, with the intention of leaving her the property upon his death without probate fees – the idea being, that a joint tenancy results in one tenant becoming the owner of the other’s interest upon death, without it becoming part of the estate. Rosenberg did not pay for the gratuitous transfer, and she never contributed financially to the home’s upkeep or lived there.

Of course, another hallmark of joint tenancy is that both joint tenants have rights of occupation and use of the property immediately … not only upon the death of the other.

In 2020, Jackson got wind that Rosenberg had intentions on dealing with the property prior to his death (potentially trying to sell the home), which caused him great concern. It was his intention that Rosenberg’s rights would vest on his death, not immediately. So, Jackson severed the joint tenancy by transferring his interest in the property to himself as a tenant in common (relying on the fact that tenants in common do not have survivorship rights). The core legal issues focused on in the lower court decision were: a) did the 2012 transfer create a joint tenancy with Rosenberg acquiring the beneficial interest in half the property, and b) whether the 2020 transfer extinguished Rosenberg’s right of survivorship over Jackson’s retained interest.

Why would this be in question? The Resulting Trust.

Lower courts have found (consistent with earlier case law), that when real property is gifted from one person to another, there is a presumption that the person receives that interest subject to a resulting trust in favour of the donor. That’s a fancy way of saying that the gift is presumed to not really

be a gift. That is only a presumption, however. It can be rebutted.

This makes sense. Often gifts of real estate are given by persons who are (or could be considered to be) more vulnerable than those who receive those gifts. And so, courts recognize that there had better be some compelling evidence that it was a gift in order to enforce it as a gift. The recipient must rebut the presumption that the resulting trust was created. So, in this case, the question was, could Rosenberg rebut the presumption of a resulting trust and demonstrate that Jackson’s gift was of an inter vivos beneficial interest in the property?

THE INITIAL RULING

Was the presumption rebutted by Rosenberg? Only partly. The application judge found that the 2012 transfer created a gift to Rosenberg, but only of the right of survivorship, not of a beneficial interest in the property during Jackson’s lifetime. During Jackson’s lifetime, Rosenberg had no beneficial interest in the property and held her share in trust for him. Jackson remained the sole party with control over the property and had the right to encumber or sell it. The application judge also held that Jackson’s 2020 transfer severed the joint tenancy, eliminating Rosenberg’s right of survivorship over Jackson’s share of the property. However, Rosenberg would still inherit any remaining equity in the property from the 50 per cent share held in trust upon Jackson’s death.

THE APPEAL DECISION

Rosenberg appealed the decision, arguing that the application judge erred by finding that the 2012 transfer did not bestow upon her all rights of enjoyment and occupation associated with joint tenancy. In addition, she argued that the gift made to her included a gift of survivorship over Jackson’s retained interest, and that Jackson could not revoke or partially eliminate that gift

This case shows the need for clear legal advice in estate planning and more generally, in any gifting of real estate. A gift may mean different things to the donor and the recipient, and with the operation of resulting trusts, there may be conflicting expectations in the absence of clearly set out intentions.

through the 2020 transfer. Put simply, she argued that once a gift of real estate is made by the granting of a joint tenancy interest …. that gift includes all present and future rights in the property characteristic of a joint tenancy, including the right of survivorship, and there can be no “take backsies” of any of those gifted rights and benefits.

The Ontario Court of Appeal dismissed Rosenberg’s appeal, upholding the lower court’s rulings, with the following key points:

1. Intention of the 2012 Transfer: The court affirmed that Jackson’s intention in 2012 was to gift only the right of survivorship, not full beneficial ownership or any control during his lifetime. The court ruled that a joint tenancy can be created for the sole purpose of survivorship without transferring other rights.

2. Right to Sever: The court agreed that Jackson retained the right to sever the joint tenancy in 2020. Severance is a recognized legal option for joint tenants, allowing them to convert a joint tenancy into a tenancy in common, which ends the right of rights of survivorship. The court emphasized that a joint tenant can unilaterally sever a joint tenancy, even when the joint tenancy was created as a gift.

3. Rosenberg’s Share After Severance: The court accepted that after the severance, Rosenberg continued to hold a 50 per cent share of the property subject to the resulting trust, but her right to inherit Jackson’s share upon his death was extinguished. The court noted that no right of survivorship over Jackson’s share could exist once the joint tenancy had been severed, and that upon Jackson’s death, Rosenberg would receive only the 50 per cent interest she had held in trust, with Jackson’s share passing to his estate.

Both parties agreed that the application judge had made an error by suggesting that Rosenberg’s right of survivorship over her own 50 percent share could persist after the severance, as survivorship rights can only exist in joint tenancies. The court invited both parties to submit arguments on whether any changes should be made to the application judge’s formal judgment to address this point.

KEY TAKEAWAYS

1. Limited Gifts in Joint Tenancies: Joint tenancies can grant survivorship rights without gifting beneficial ownership to the transferee during the transferor’s lifetime. If the transfer is gratuitous, the transferee may only have limited rights unless there is clear evidence of gifting further ownership rights.

2. Survivorship Rights are Contingent on Joint Tenancy: Survivorship rights are inherently tied to the existence of a joint tenancy. A joint tenant can unilaterally sever the joint tenancy at any time, ending survivorship rights, even if the original transfer creating the joint tenancy was a gift.

3. Clear Estate Planning and Legal Advice: This case shows the need for clear legal advice in estate planning and more generally, in any gifting of real estate. A gift may mean different things to the donor and the recipient, and with the operation of resulting trusts, there may be conflicting expectations in the absence of clearly set out intentions.

This article is republished with the permission of Bennett Jones a leading law firm with offices across Canada and in New York. Simon Crawford is a Partner in the Toronto office where Vanessa Kiraly is an Associate. Information: bennettjones.com

Building a stronger, more connected mortgage community

CMBA ONTARIO’S

2025 GALA & CONFERENCE

BY MICHELLE CAMPBELL, VICE PRESIDENT AND CHAIR OF EVENTS CMBA ONTARIO

CMBA Ontario’s annual Gala and Conference on March 26 and 27 brought together the very best of the province’s mortgage community for two days of inspiration, recognition and collaboration. This year’s edition marked a new milestone with record attendance at both the gala and conference, underscoring the growing momentum and unity within the industry.

THE GALA

The gala evening was nothing short of magical. Held to honour the achievements of our industry’s finest, it was also an opportunity to give back to a cause that’s close to our hearts: SickKids Hospital. One of the most powerful moments of the evening came when Jack, a brave young patient from SickKids, took the stage to share his journey. His heartfelt story reminded us of the importance of our collective efforts to make a difference.

CMBA Ontario is proud to be working towards raising $100,000 for SickKids by the end of the year, a goal that reflects the heart and values of our community.

This year’s award recipients exemplify the excellence and integrity that define our profession:

n Brokerage of the Year – A Better Way Mortgage Group

n Outstanding Young Achiever – Justin Theriault

n Lender of the Year – Alta West Capital

n Service Provider of the Year – Newton / Velocity

n Community Service Award – Shane Suepaul

n Ed Karthaus Professional Integrity Award – Bill Nugent

n Hall of Fame Inductee – Elaine Taylor

A special tribute was also made to the late Malcolm Eccles, a visionary who played a pivotal role in founding the Independent Mortgage Broker Association. His legacy continues to shape the values and direction of our industry.

CONFERENCE

Clockwise from top left: Ready for a day of networking and learning at CMBA Ontario’s annual conference were (from left) Bob Pinkney, Yvonne Garvey, Andrew Kennedy and Adrian McInerney; Dario Carpino Jr. (left) and Shawn Stillman have plenty to talk about at CMBA Ontario’s annual conference; Enjoying CMBA Ontario’s annual gala held in March were (from left) Leah Zlatkin, Elaine Taylor and Michelle Campbell; Having fun and networking at CMBA Ontario’s annual conference were (from left) Calvin Fernandes, Nirvina Shamshudin and Pierre Martin; All the fun of the party as (from left) Marianne Grnak, Elena Robinson, Josie Biase, Natasha Alli and Warda Fatima add some glitz and glam to the festivities.

CMBA Ontario event

THE CONFERENCE

The energy continued into the next day with the CMBA Ontario Conference, which featured more than 70 exhibitors, and a thoughtfully curated agenda designed to educate, inspire and empower. From keynotes to debates, every moment was crafted to provide actionable insights and spark meaningful conversations.

Highlights included:

n Douglas Porter, Chief Economist at BMO, who provided an in-depth economic forecast that contextualized the current mortgage landscape.

n A dynamic Lender Panel featuring Andrew Gilmour (CMLS), Devon Ajram (TD), Elena Robinson (First National) and Nick Kyprianou (River Rock), offering a 360-degree view of market trends and brokerlender collaboration.

n A captivating Titan’s Debate that tackled the industry's most pressing issues with spirited discussion and insight.

n A mind-bending performance by a mentalist, adding a touch of entertainment and wonder to the day.

From strategic networking to thought leadership, the conference provided an exceptional platform for attendees to connect with peers, deepen their knowledge and return to their businesses with renewed motivation.

As we reflect on the success of this year’s event, we are filled with pride and gratitude. Thank you to all our generous sponsors – your support made these impactful experiences possible. We’re already looking forward to next year’s event and continuing to build a stronger, more connected mortgage community.

Above: One of the highlights of CMBA Ontario’s annual conference was the presentation by Kevin Hamdan, mentalist and psychological illusionist. Below: Getting together with colleagues at CMBA Ontario’s annual conference were (from left) Angie DiNoto, Armando Diseri and Christine Xu.

A LOOK AT CANADA’S ALTERNATIVE AND PRIVATE LENDING SPACE: MBRCC’S 2025 REVIEW

Helpful information for brokers operating in the private lending space

BY CARLA GILES, MBA, CAE, CEO OF CMBA-BC, MBIBC, EXECUTIVE DIRECTOR, CMBA NATIONAL

As the Canadian mortgage industry continues to evolve, so too does the landscape of alternative and private lending.

In April 2025, the Mortgage Broker Regulators’ Council of Canada (MBRCC) released its Private Mortgage Lending Review Report, a review and analysis of private mortgage lenders across Canada. This document builds on priorities set out in MBRCC’s 2020–2023 Strategic Plan and continued in its 2023-2026 cycle, with the goal of increasing regulatory collaboration, enhancing consumer protection and deepening industry understanding of risks.

MBRCC CATEGORIES OF PRIVATE

WHY THE REPORT WAS COMMISSIONED

MBRCC’s Private Lending Committee was established to respond to increasing concern around the growth and complexity of private mortgage lending in Canada. The Committee’s mandate was to evaluate private lending practices across jurisdictions and develop a clearer picture of the sector’s structure, regulatory gaps and emerging risks. In doing so, the report seeks to support two overarching goals:

n Fostering consumer confidence, particularly for borrowers navigating non-traditional financing channels.

n Monitoring market trends and potential vulnerabilities through regulatory cooperation and information sharing.

1

MORTGAGE FINANCE COMPANIES (MFCs)

For those who submitted a mortgage MFCs are corporate lenders not subject to direct oversight by the Office of the Superintendent of Financial Institutions (OSFI) or provincial prudential regulators. Still, they typically follow OSFI standards and are sometimes referred to as “quasi-regulated” institutions. Many MFCs are licensed as mortgage brokerages and/or mortgage administrators depending on provincial requirements because they perform mortgage origination and mortgage administration activities on behalf of the lenders.

Key characteristics:

n Often funded by institutional investors such as pension funds, securities dealers and banks.

n Many participate in Canada Mortgage and Housing Corporation (CMHC) securitization programs and insure all qualifying loans with mortgage default insurance.

n Primarily originate mortgages via internal brokers and operate in a way similar to monoline lenders.

Before 2008, MFCs were active in higher-risk “alternative” mortgages. During the financial crisis, investor pullback caused a credit squeeze for borrowers needing renewals. The report warns that a similar risk remains today – if housing markets decline, borrowers may again face limited renewal options from MFCs or other private sources.

MFCs are lower risk compared to other private lenders due to their institutional backing, but brokers must still exercise caution and ensure clients understand renewal risks and lending conditions.

2

MORTGAGE INVESTMENT ENTITIES (MIEs)

MIEs raise capital by issuing securities and using those pooled funds to originate mortgages. The most common MIE structure is the Mortgage Investment Corporation (MIC), though Mutual Fund Trusts and Limited Partnerships are also included.

Key characteristics:

n MIEs focus on short-term mortgages (6 -12 months) that prioritize loan-to-value (LTV) over borrower income.

n Many self-identify as “equity lenders,” placing more emphasis on collateral value than debt servicing ability.

n Typically unregulated in terms of lending criteria, but their capitalraising activities are subject to securities regulation.

n Many MIEs are formed by mortgage brokerages, which must be dual-registered with mortgage and securities regulators.

n Some MIEs qualify as reporting issuers and must comply with disclosure and transparency rules under securities legislation.

n The report noted that in the climate of higher interest rates, MIEs were extending loan terms or restructuring to accommodate borrower challenges.

The MBRCC report highlights that MIEs may pose risks to borrowers, including inadequate product suitability assessment and disclosure. Moreover, the report identifies systemic vulnerabilities associated with MIEs – particularly the risk of large-scale investor capital withdrawals during periods of economic uncertainty. Such events could destabilize MIE operations and potentially impact the broader private lending market.

OTHER PRIVATE LENDERS

This category includes individuals and entities lending their own capital – ranging from sophisticated professionals to first-time lenders using retirement funds. These lenders have become a significant source of funding to those who would not otherwise qualify for a mortgage from financial institutions, MFCs or MIEs.

Key characteristics:

n Typically do not qualify borrowers based on income.

n Individual private lenders range from professionals (such as lawyers and real estate licensees) who understand real estate markets and law to unsophisticated individuals often utilizing retirement funds or savings.

n Entities who become private lenders include small to medium-size businesses, holding companies, looking to invest their assets.

n Many operate informally and are often introduced to lending by mortgage brokers.

This group is frequently the source of investor complaints and Errors and Omissions (E&O) insurance claims. The report notes that claims often stem from private lenders unaware of their obligations – such as covering legal fees, paying arrears or dealing with foreclosure. Errors frequently involve a lack of documentation, failure to explain borrower risk or poor due diligence.

4

LENDERS IN A MORTGAGE SYNDICATE

PRIVATE MORTGAGE LENDERS 3

Mortgage syndication involves two or more investors funding a single mortgage. These may include individuals, MFCs, MIEs, or other entities.

Key characteristics:

n Syndicated mortgages are subject to securities regulations in most provinces.

n There are distinctions between “qualified” (primarily residential) and “non-qualified” (typically commercial) syndicated mortgages.

n In Ontario, the Financial Services Regulatory Authority (FSRA) has specific guidelines on supervision of non-qualified syndicated mortgages (NQSMIs) involving permitted clients and legacy investments.

n Where exemptions from prospectus and registration requirements are used, disclosure is still often required and investor eligibility thresholds must be met.

n The investor protection framework varies widely across provinces, with some jurisdictions allowing mortgage brokerages to distribute qualified syndicated mortgages without securities registration.

Brokers participating in syndicated deals must navigate dual compliance frameworks and many brokers are also registered as a Dealer with the securities’ regulatory authorities. Failures in disclosure, inaccurate borrower profiles, or poor coordination among investors can result in serious financial harm and regulatory penalties.

CROSS-CUTTING ISSUES AND REGULATORY GAPS

The MBRCC report highlights that investor protections in the private mortgage lending space are inconsistent and, in some cases, unclear or insufficient. While borrower protection is generally addressed by mortgage regulators, investor-lenders often fall under the jurisdiction of securities regulators – or in some cases, no clear authority. This creates confusion, especially in scenarios involving complex investment structures or cross-jurisdictional transactions. For example:

n A lender who is also an investor in a syndicated mortgage may not receive standard consumer protections unless explicitly covered by securities law.

n Licensing requirements for mortgage lenders vary across provinces, which may create regulatory arbitrage opportunities.

Additionally, the lack of harmonized terminology and definitions across provinces complicates oversight. For instance, Ontario defines private lenders as those who are not financial institutions or National Housing Act–approved lenders, while other jurisdictions use broader or narrower criteria.

WHAT THIS MEANS FOR MORTGAGE BROKERS

The MBRCC report is helpful for brokers active or considering operating in the alternative and private lending space. It underscores that:

n Due diligence and documentation must be strengthened, particularly in transactions involving individual lenders or complex investment structures.

n Brokers must take proactive steps to educate themselves and their clients about regulatory responsibilities and potential risks in private lending.

n Compliance obligations may increase, particularly for brokerages engaged in capital raising, syndicated mortgages, or MIE management.

n Industry associations and brokerages have a role to play in promoting best practices and collaborating with regulators to enhance transparency and professionalism in the private lending space.

For the full MBRCC Private Lending Review Report, visit: mbrcc.ca

Disclaimer: The information included in this article is not intended to be investment or registration advice.

FOR SALE

THE PARTITION ACT

A powerful tool for resolving jointly owned property disputes

BY ELLAD GERSH

In the recently released decision of Ross v. Luypaert, 2025 ONCA 236, the Ontario Court of Appeal reaffirmed that a co-owner of real estate can compel the sale of jointly owned property under the Partition Act. The only exception is where the opposing party can prove that such an application amounts to malicious, vexatious or oppressive conduct – a high threshold that was not met in this case.

THE FACTS

The applicants were litigation guardians for their elderly parents, who were mentally incapable. They brought an application to:

n Sell a duplex in Guelph jointly owned by their parents and their brother; and

n Have the brother vacate a second property solely owned by their mother.

The purpose was to use the proceeds to help fund their parents’ ongoing care. The brother opposed the application, alleging that his siblings had provided inaccurate and misleading information. However, the court found that these claims did not outweigh the applicants’ statutory right to sell the jointly owned property.

Additionally, the court found there was no tenancy agreement entitling the brother to remain in the second property and ordered that he vacate it.

COURT OF APPEAL DECISION

The Ontario Court of Appeal dismissed the appeal and upheld the original decision. The ruling reinforces the principle that, under the Partition Act, co-owners have a presumptive right to sever their interests and compel a sale.

KEY TAKEAWAYS

n Statutory right to partition: Joint owners have a clear right under the Partition Act to apply for the sale of a property.

n High bar to resist: A resisting owner must demonstrate the application is malicious, vexatious, or oppressive to prevent a sale.

n No tenancy, no rights: Occupation of a property without a tenancy agreement may not provide legal grounds to remain.

n Litigation guardianship: The case touches on procedural issues around representation for mentally incapable parties.

n Practical implications: This decision provides clarity for families navigating joint ownership, elder care, and disputes over property rights.

FINAL THOUGHTS

Ross v. Luypaert is a reminder that joint ownership does not lock co-owners together indefinitely. The Partition Act provides a mechanism to untangle property interests, even in difficult family circumstances. The decision also highlights the importance of documentation – particularly around occupancy and tenancy – in intra-family property arrangements.

This article is republished with the permission of Dickinson Wright, a law firm with office across the U.S and in Canada. Ellad Gersh is a Partner in the Toronto office and has a full-service commercial litigation practice, with a special emphasis on property disputes including real estate litigation, construction litigation, commercial tenancy disputes and mortgage fraud. More information: dickinson-wright.com/our-people/ellad-h-gersh

FOR SALE

TopDog is an Appraisal order Platform built by appraisers for brokers, alternative lenders, and TopDog Appraisal Firms.

National Coverage

Connecting Approved Appraisal rms to Alternative Lenders in every major Canadian city.

A Platform Built for Alternative Lending Market

TopDog is the result of 15 years of developing and re ning a platform tailored speci cally for alternative and private lenders.

Track Your Order from Start to Finish

With TopDog you can track the progress of your order at every stage with real-time text and email updates, or from your browser.

Reward Program

Place an order on TopDog and you can earn points that can be redeemed for gift cards, charitable donations, and discounts on future orders.

Find out for yourself how easy the appraisal process can be –visit us at topdogappraisal.com to learn more and get started.