Autumn 2022 n Food security feeding Britain n Entitlement trading update n Green energy initiatives n Farming in a changing climate

There is a continued lack of detail on the subsidy regime for farmers in Scotland post-2025, although it is clear that as well as food production, measures to capture carbon and improve biodiversity will be rewarded. In England the policy framework is much clearer, although we are traversing a period of political upheaval.

The good news though for all of us in the rural sector is that there are numerous – and very significant–reasons to have confidence in the future.

Demand for land and for rural property remains at an exceptionally high level.

Consumer interest in high quality meat and produce shows no sign of abating, and the same is true for leisure and tourism opportunities such as glamping and farm stays.

The planning regime for development of existing rural businesses remains relatively benign and politicians are beginning to take rural crime more seriously.

As ever a balance needs to be struck between the competing pressures on

landowners. Since the war in Ukraine began, there has been greater recognition of the importance of domestic food production and our excellent animal welfare standards.

In this issue we outline opportunities for landowners including renewable energy projects and basic payment entitlement trading, as well as providing much food for thought on the issues of land reform, food security and energy efficiency.

It would be remiss of me not to mention the passing of our dear friend and colleague, Colin Stewart. Colin was a well-respected advisor to the rural fraternity and many of our client base have benefitted from his calm persona and very knowledgeable advice. The loss of Colin has been a great shock to us all at Galbraith, both his expertise and his friendship will be sorely missed.

Ian Hope.

November 2022.

Ian

facing

beauty, stargazing

little-known

rule of

benefit

The reconvening of the Scottish Parliament in 1999 saw the wheels of the Land Reform journey start to gather traction, seeking to modernise and simplify a centuries-old system.

In a world where the population continues to grow, but the land mass stays the same, change is inevitable, but how it is achieved is subject to much necessary debate.

The term ‘Land Reform,’ is defined by the encyclopaedia Britannica as ‘a purposive change in the way in which agricultural land is held or owned, the methods of cultivation that are employed, or the relationship of agriculture to the rest of the

economy.’ Depending on your viewpoint, it is tempting to accuse the Scottish Government of obsessing on the first part of this definition, but is ownership arguably at the crux of the argument? Ownership provides the scope to determine land use, and as land is increasingly in short supply in relation to the needs of a growing population, could it be argued that this level of omnipotence is flawed?

In her ministerial foreword to the ‘land reform in a Net Zero Nation:’ consultation, Mairi McAllan MSP says that she is ‘proud of Scotland’s record of progressive and innovative reform, but the journey is not complete.’ I would suggest that it is misleading to imagine that it will ever be complete, how can it be? As social, economic and environmental change gathers pace around us, and our knowledge of how we interact with the natural world develops, the requirements which we place upon our natural resources will necessarily be subject to constant change. It is probably an over-dramatised analogy, but the fate of the rich and wicked King Tantalus from Greek Mythology is perhaps worth considering. After attempting to serve his own son up at a feast with the Gods, he was punished by Zeus to forever go thirsty and hungry in Hades, despite being stood in a pool of water and almost within reach of a fruit tree. The progression of humanity through history and the related plunder of natural resources does not make happy reading. We are surrounded by incredible Natural Capital Assets, clean air, clean water, and land for food and energy production, but if we are unable to find a way forward for all to benefit, will these fruits remain out of our reach? What are we waiting for? legislation? regulation? policy? Or perhaps just ‘certainty’ from any of these areas would make decision making and progress easier.

The most recent Land Reform Bill, which, it is proposed will come into effect in 2023, further explores how ownership patterns affect land use, and this continues to cause consternation. I mentioned earlier that perhaps part of the contention was the Scottish Government's perceived obsession with land ownership, when really the centre of the debate should be land use, however, as the two are fairly intrinsically linked, perhaps the problem is how to manage one without causing detriment to the other.

As seems to be the way in Scotland, if in doubt, we legislate! When I wrote 18 months ago for Rural Matters Spring Edition 2021, the suggested means of moving forward were being debated, and at the time I was frustrated by a lack of definition or detail. Disputably, some progress has been made as regards definitions, although I would suggest that full clarity is still elusive, but following initial scrutiny and subject to further consultation, it is likely that the new Bill will seek to:

● Introduce compulsory management plans;

● Ensure the public interest is considered on transfers of large-scale landholdings;

● Introduce new requirements to access public funding for land-based activity;

● Introduce a new Land Use Tenancy

Frustratingly, I think that these points illustrate that the focus is still too centred on ownership rather than use. As a society, we increasingly have an environmental conscience and are uncomfortably aware of how the misuse of our planet is catching up with us. A growing realisation that our future health and ability to exist sustainably depends on what we now define as ‘Natural Capital Assets,’ has thrown an even brighter spotlight on those with the ability to manage and influence this. In the past, rural land ownership could have been defined by the cynical rejoinder ‘you can’t eat the view;’ a reflection on the fact that while land ownership conveyed a certain status, the asset in itself generally didn’t pay. However, the recent hype around carbon and the market opportunities that it has created out of formerly marginal rural landscapes has put paid to this, and in the minds of all, the potential economic and environmental impact of how land is used cannot be ignored.

In addition, prior to the war in Ukraine, it had been possible for all of us of a certain generation to stick our heads in the sand over the availability of food and fuel. We were in danger of becoming obsessed with ‘wilding,’ and turning our landscape into parkland, – a ridiculously hedonistic approach to land management that land should simply be available for our enjoyment, rather than to enable our existence. The upshot of this wake-up call for Britain's farmers has been an increased level of respect and appreciation for those who have the knowledge and ability to create food from land. Past experience will hopefully prevent us from creating ‘wheat mountains' and ‘milk lakes’ again, but the importance of managing our resources sustainably is a valuable lesson to have learned.

In light of the above, facts have to be faced, and one of the main problems which land reform faces will be its inability to keep pace. While the heavy wheels of legislation grind along, the speed with which change is required, and the ability to keep pace in real time, both intellectually and financially are incredibly challenging, requiring agility and knowledge from those who hold the future of our resources in their hands. I believe that greater transparency in relation to land ownership and land use needs to be brought about to ensure that our Natural Capital is managed for the best and for the majority; but I think that there is room for a shift in how land reform is either managed or perceived. Wider involvement in land use decisions should be a positive for all involved, but how this is achieved is a question still to be answered. The Land Reform Journey will continue, but an obsession with land ownership may prove to be a ‘spoke in the wheel’ of real and necessary progress. n

Poppy Baggot

Placing a cap on energy bills is not nearly enough to alleviate the energy crisis but instead there needs to be a focus on investing in net zero and improving energy efficiency. However our Prime Minister has expressed support for an increase in fossil fuels and is downbeat on renewables, especially onshore wind and solar. The renewable sector is concerned by these recent changes. Our new Prime Minister must unlock the UK’s full renewable power potential by removing the unfair planning barriers to onshore wind and removing the limit which restricts the quantity of solar and onshore wind projects that the government will support.

The UK has huge renewable energy resources and the majority of our population supports renewable technologies. The different renewable technologies available to us in the UK provide a vast array of options and the technologies are only ever improving and becoming more efficient. Galbraith has a vast amount of experience and knowledge in the renewable sector and how to implement projects with our clients.

The UK is considered one of the best locations for wind power in the world and the best in Europe. Currently the UK has 11,198 wind turbines with a total installed capacity of over 25.5GW (approximately 14 GW of onshore capacity and 11.5GW of offshore capacity).

Wind turbines work through the wind turning the blades of a turbine creating kinetic energy around a rotor, which

in turn spins a generator and converts kinetic energy into electrical energy.

The largest onshore wind farm in the UK is Whitelee Windfarm located just 20 minutes from central Glasgow on Eaglesham Moor. The wind farm consists of 215 turbines which generate up to 539 megawatts of electricity. This is enough energy to power 350,000 homes.

The largest offshore wind farm in the UK is Hornsea 2 which is located approximately 55 miles off the coast of Yorkshire. The wind farm consists of 165 turbines which generate 1.3 gigawatts. This is enough energy to power 1.4 million homes.

Until the 2010s solar power contributed very little to electricity production in the UK. However solar production increased due to Feed-in Tarriff subsidies (now withdrawn) and the falling costs of photovoltaic panels. As of the end of 2021, the installed capacity of solar in the UK was just under 14,000 megawatts and although this only accounts for 6% of the renewable energy share of electricity it continues to increase.

Solar PV systems work when the sun shines onto a solar panel, energy from the sunlight is absorbed by the PV cells in the panel. This energy creates an electrical charge that moves in response to an internal electrical field in the cell, causing electricity to flow.

At the time of writing our new Prime Minister had just announced that in order to limit the 80% rise in domestic bills that was earmarked for October that an annual bill would not rise above £2,500.

The largest solar farm in Scotland is Shotwick Solar Park, commissioned in 2016, which produces 72.2 megawatts a year. Shotwick Solar Park feeds private infrastructure with power including the UK’s largest paper mill. The solar park supplies 70% of the paper mill’s energy requirements.

The United Kingdom has been a pioneer in hydro power and currently the UK has a total installed capacity of over 4,700 megawatts, with the majority of the installed capacity located in the wet and mountainous regions of Wales and Scotland.

Hydropower is generated using flowing water to spin a turbine which in turn powers a generator creating the electricity. Hydroelectric dams require rivers with large volumes of water with a significant drop in elevation – the greater the elevation and the more water that flows through the turbine, the greater the capacity for generation of electricity.

The largest hydroelectric power station is the Dinorwig Power Station, located in Snowdonia which generates 1,728 megawatts. The power station was fully commissioned in 1984.

Similarly to wind, the UK has the largest tidal resource in Europe and currently the UK’s tidal power resource is estimated to be more than 10 gigawatts which represents about 50% of Europe’s tidal energy capacity.

Tidal power is produced by the surge of ocean waters during the rise and fall of tides. There are three different ways to generate tidal energy – tidal streams, barrages and tidal lagoons. Tidal energy works via a turbine (just like a wind turbine) with rotating blades. The turbine is connected to a gearbox that turns a generator creating electricity.

The world’s first tidal lagoon power plant is being built off the south west coast of Wales. The Swansea Bay Tidal Lagoon will comprise 16 hydro turbines and will generate enough electricity for 155,000 homes. The project is due to be completed by 2024 but may start generating power by 2023.

The need for renewable energy is only increasing and the storage of this energy is also of crucial importance, so much so that we are seeing landowners with suitable land being approached for renewable projects for either single renewable technologies or for multiple technologies - termed co-location.

If you have been approached by a renewable developer Galbraith would be pleased to assist in the process, from initial contact through to agreeing the Heads of Terms. n

07917 220 779 philippa.orr@galbraithgroup.com

Galbraith has a vast amount of experience and knowledge in the renewable sector and how to implement projects with our clients.

For new developments, redevelopments or when considering property improvements more generally, ‘green’ energy initiatives are high on the policy agenda and hold great appeal for many of us to help reduce our energy bills.

The Scottish Government aims to generate 50% of Scotland’s overall energy consumption from renewable sources by 2030 (last recorded 23.9% in 2019) and reach net zero by 2045.

The Government’s published strategies including the Energy strategy and Heat in Buildings strategy centre upon heat decarbonisation and emissions reduction, with funding pledged to target the emerging energy technologies sector more broadly, as well as more direct funding to businesses and individuals. This drive is also reflected in planning policy, which is generally favourable towards green energy technologies, where permission is required. However, whilst the use of green energy technologies are beneficial for the environment, not all measures are applicable to every property. Whether you are considering green energy to satisfy a planning requirement, as a means of combating rising fuel and energy prices, or, in the case of business developments, as a positive marketing tool to attract revenue, the available technologies ought to

be reviewed in line with your objectives, as well as the building itself and geographical location. They also require varying levels of investment and on-going maintenance and running costs, which should be considered as part of the overall scheme.

Biomass boilers or wind turbines were the traditional approaches when considering ‘green energy measures’, typically due to the financial attraction of Renewable Heat Incentives or Feed-In Tariff, which increased the pay-back. However, a reduction in energy bills is now the primary incentive given the current drastic increase in energy prices and technology has advanced a long way in the last 10 years. There are now a huge variety of green measures that can assist in providing hot water, heating, and lighting for your property, including but not limited to the following:-

Rainwater harvesting: the process of collecting rainwater in a tank below ground level, utilised for WCs and other ‘grey’ water outlets. Requires infrastructure to separate

mains and harvested water, and therefore better suited to new builds due to the difficulty in implementing tanks below ground retrospectively. It is also better suited for businesses, where it is likely that there will be high usage or demand at peak times.

Air or ground source heat pumps: Ground source heat pumps extract heat from the ground, whilst air source heat pumps extract heat from the air. Ground source heat pumps tend to involve higher installation costs over air source, with the associated ground works required. Heat pumps operate on a lower, continuous heat, and typically work best with a larger heating surface area because they power lower heat levels over a longer period. They are therefore less effective when retro-fitted to a traditional residential building, with smaller radiators, and are best suited to new builds or renovations, with adequate insulation. Without the right building structure, they may result in higher energy bills as a result, both types running on electricity alone.

Solar Photovoltaics: Roof or ground mounted. These require a higher level of initial installation cost but are relatively low maintenance once installed and the average return on investment has been calculated at about ten years for residential properties, though payback periods are reducing as the cost of electricity from the grid increases. The installation cost varies depending on the area available but depending on use, excess energy may be exported to the grid as an additional source of income, particularly worthwhile at a time when export prices are more favourable. Installation is also dependent upon planning permission, and where considering roof-mounted PV panels, the structural integrity of the building and orientation is key. However, both may be retro-fitted to a property, at cost.

Other, lower level methods of energy savings include enhanced lighting control, which reduces lighting output based on natural light levels, through the use of external sensors. With adequate fittings and wiring, this may be retrofitted and provide electricity savings throughout the lighter summer months.

There are also flow restrictors which may be utilised in bathrooms to reduce quantities of water wastage. These measures may also be implemented without the additional planning hurdle.

The installation of draught lobbies may also be of benefit to prevent cold air from directly entering the building, and thereby off-setting any heating measures within the building. These are best suited again to new builds for obvious reasons.

The majority of these items may be installed in conjunction with one another, however not all are suitable for every building. It is also important to note that green measures do not require an “all or nothing” approach, some may be implemented at a later date, when suitable according to planning permission, funding or grants that are made available or for other reasons. In any case, adopting a pragmatic approach will ensure that your project meets your goals in terms of cost-savings or reducing your carbon footprint, and whilst the building and location is important, so are the specific requirements of the residential or commercial occupant. Please contact Galbraith to discuss your specific requirements. n

Nutrient pollution is a major environmental issue for important natural habitats across England. The increased levels of nutrients, particularly nitrogen and phosphate, can speed up the growth of certain plants disrupting natural processes and impacting wildlife as a result, and creating ‘unfavourable conditions’ for sites. The sources of excess nutrients are very site specific but range from sewage treatment works, septic tanks, agricultural and industrial processes. Most internationally important water bodies are designated as protected under the Conservation of Habitats and Species Regulations 2017 (as amended) and are known as ‘Habitat Sites’. When local authorities assess planning applications, they must consider the likely effects on Habitat Sites by utilising the Habitats Regulations Assessment (HRA).

Following the ‘Dutch N Case’ in November 2018 the European Court of Justice decided that projects must not have a significant adverse effect on site conservation objectives. This led to the introduction of nutrient neutrality which is the outcome achieved when a particular land use or development does not result in an increase in phosphate and nitrate levels in the catchment area of vulnerable watercourses above the existing levels.

Natural England has been responsible for preparing a generic methodology for calculating the nutrient burden created by a proposed development. The methodology essentially calculates the existing levels of nitrogen/phosphate from the current use of the proposed development site and then calculates the additional nitrogen/phosphate burden created by the proposed development which includes a 20% precautionary buffer. If the proposed development results in an increase of nitrogen/phosphate then mitigation will be required.

Nutrient neutrality now affects a total of 74 Local Planning Authorities (LPA) ranging from Cumbria to Cornwall. The mitigation that is required can either be on-site or off-site depending on the LPA and site restrictions.

The on-site options for achieving nutrient neutrality can be via creating large scale wetlands, woodlands and fallow habitats. However, in reality, this is limited as often there will not be enough land within the development boundary as the nutrient neutrality measures are onerous and land hungry.

The off-site options are still emerging but are proving to be more popular as it is less onerous in terms of ongoing management. One approach is to purchase nutrient ‘credits’ to offset the increase of nitrogen/phosphate created by the development. There is an opportunity for landowners to take agricultural land out of production to create woodlands, heathlands, saltmarsh, wetland or conservation grassland to generate credits that can be sold to developers to achieve nutrient neutrality within the same local catchment area.

Natural England has advised that the mitigation land is maintained for a minimum of 80 – 125 years, many developers do not want to be involved with the ongoing maintenance of habitats which opens the opportunity for landowners to create an additional income stream.

The Scottish Government has recently released information on a National Test Programme (NTP) to help transform Scotland’s agricultural sector into a more sustainable entity with a focus on cutting greenhouse gas emissions and improving biodiversity whilst enhancing the sector’s food production capacity.

Announced in Spring 2022, the NTP is bolstered by a £51 million package available over three years to modernise and promote regenerative and sustainable farming.

The programme will work through a twin track approach that will support landowners at different stages of their regenerative and sustainability reform.

Track One provides producers with the means of preparing for future rural subsidy schemes which are likely to require farmers to meet set targets in terms of biodiversity gain and greenhouse gas emissions. This first stage, aptly named Preparing for Sustainable Farming, will enable farmers to ascertain their current position, establishing a baseline of information through the use of grant

funded carbon audits and soil sampling.

Farmers will be able to claim £500 to cover the costs of the provision of a carbon audit. This audit will duly be reviewed by a Farm Business Adviser Accreditation Scheme for Scotland (FBAASS) adviser who will then provide a report containing recommendations on how the business can reform its highlighted weaknesses. Following the completion of a carbon audit farmers of Region 1 land will be able to access the next stage of soil sampling. This stage aims to improve nutrient management and planning by implementing widespread, regular testing.

A maximum funding allowance will be calculated during the year the grant claim is made; this will be

done by calculating 20% of the total area of Region 1 land that was claimed on that year’s single application form. A rate of £30 per hectare is then available. An additional, one-off development payment of £250 will also be made available to collate and provide a nutrient management plan during the first claim year. Additionally, suckler beef producers have been provided access to YourHerdStats which falls under the existing ScotEID, which will provide a sleek new means of herd management and information collation.

Track One focuses on an almost stocktake of the current status of the farm in terms of biodiversity, sustainability and greenhouse gas emissions. This is merely the information gathering stage for the next steps in the NTP.

The Government has stated that the purpose of Track Two is to ‘design, test, improve and standardise the tools, support and process necessary to reward landowners for the climate and biodiversity outcomes they deliver’. As we approach the end of 2022 the first step of Track 2 was unveiled in the form of a national survey named ‘Testing Actions for Sustainable Farming’. The questionnaire focused on establishing the farming sectors’ knowledge and understanding of regenerative and sustainable farming. This information gathering exercise was the first act of the cautious development of the new Scottish subsidy support scheme.

At the time of writing the Government has released a

consultation for its proposed new Agricultural Bill. Within this document they outline a provisional, tiered subsidy structure; Tier 1, the Base Payment, is set to follow similar practices we currently see with Greening and Cross Compliance still being required conditions for payment. Tier 2, the Enhanced Payment, is available to producers who are taking extra steps to cut greenhouse emissions and promote biodiversity. This notably includes participation in the National Test Programme. Whilst this consultation is not set in stone, it is not unreasonable to assume the subsidy structure will be very similar to this consultation. It is essential producers begin to consider taking action to ensure that they are identifying areas of

inefficiency in their business but also to ensure that they are taking the correct steps that will allow their participation in this future subsidy structure.

If you are considering engaging in the National Test Programme, Galbraith has a wealth of experience carrying out carbon audits and whole farm reviews. I would urge you to make contact with your local office to discuss the options available to you and your business.

Following 20 months of unprecedented prices for sawlog material, Louise Alexander talks with Jamie Hendry, General Manager, Euroforest Ltd for his view on the current UK timber market and his predictions for 2022-23.

Demand for wood products has led to historically high prices for wood products since January 2021, fuelled by a booming construction industry and millions of lockdown DIYers.

After the record-breaking prices seen for sawlogs during late 2021, there was a slight downward adjustment in the final quarter of the year. Prices for spruce came back from £100115 a tonne to about £90.

Pine and mixed conifer tracked this price fall from £90-95 back to about £85. Prices stabilised at this level in the first quarter of 2022 then showed signs of rallying in Q1 but they declined sharply in June-July after rapid inflation led to a downturn in demand. This coincides with a sharp increase in sawn imports from the EU – caused in part by a lack of demand in mainland Europe resulting from the same economic factors suffered in the UK.

As of mid-July, spruce prices are now at £80 with mixed conifer at £70 delivered. The fall has been exacerbated by the steady stream of sawlogs coming to market as landowners continue to deal with the clean-up from Storm Arwen. Small roundwood (SRW) prices did not achieve the same uplift as sawlogs during 2021, partly due to an increased volume of sawmill ‘co-products’ coming to market as a result of extended mill working hours to meet increased demand for sawn timber. However, there was no downward trend in SRW prices during the mini-slump in sawlog prices in late 2021.

Broadly speaking SRW prices have remained stable at about £45-55/t for the past two years. With rising demand for SRW exports from the UK to the EU, which have already begun, the price will at worst remain stable or should rise by £5/tonne in Q3.

SRW prices remain stable as of late July despite some peaks and troughs in domestic demand. Export of SRW remains strong and is likely to continue at this level for the remainder

The effects of the Russian invasion of Ukraine, whilst boosting demand for UKgrown timber in the short-term to replace imports, have yet to play out fully on the global economy.

of 2022, in part due to the reduction in sawmill production in mainland Europe.

The price differential for FSC wood – deemed by the Forest Stewardship Council to be ethically sourced, and controlled wood, that is, from acceptable sources, has gone from a fairly standard £2-3 per tonne, to a current differential of £10+ for sawlogs, and £3-4 for SRW. This is in part due to an oversupply of controlled wood brought to market in the wake of Storm Arwen from one-off sources such as farm shelter belts.

Lack of FSC pure supplies is an issue in all timber categories, with large volumes of oversized controlled wood, chipwood and fuelwood resulting from wind snap (from trees broken at the stem or stump) currently struggling to find a home. So to maximise returns and ensure product moves to the end user unhindered, those planning to offer timber to the market should make sure it has FSC status.

The effects of the Russian invasion of Ukraine, whilst boosting demand for UK-grown timber in the shortterm to replace imports, have yet to play out fully on the global economy. Huge hikes in energy prices have already led to rapid increases in harvesting and haulage rates and other materials used in construction, such as steel and concrete, all requiring large energy inputs in their manufacture. If this leads to a contraction in the economy or a recession, demand for construction timber will drop, and prices with it.

In summary, the hoped for recovery in timber prices has not arrived, due to a combination of credit issues, rising inflation and the severe hike in utility prices caused primarily by Russia’s invasion of Ukraine and the subsequent Europe-wide energy crisis. However, if you have crops which are poor and heavier to sell as SRW, now may be the time to look at harvesting these. n

Biodiversity faces a global crisis – one which we know businesses need to address. We at Galbraith don’t believe in giving advice we wouldn’t take ourselves – so in June, we went wild.

Over 40 members of the Galbraith team took part in 30 Days Wild. This is a challenge set by the Wildlife Trusts to do something new to connect with nature every day.

Particular highlights included ‘paying more attention to the smaller creatures we share our world with’, ‘trying out new things in the garden, ‘going wild swimming’, ‘exploring new places’, and letting children lead activities – ‘they are always finding bugs and flowers and digging and climbing and making nests or just lying in the grass’.

Most participants joined a messaging group, which buzzed with photos and stories of wild things. For many of us, sharing experiences and knowledge was as valuable as our own activities.

Identifying wildlife was the top activity, aided by knowledge of the team and identification apps. Mindfulness activities – taking time to look, listen, smell, touch, taste, or just be in nature – came a close second. Also popular was taking daily activities outdoors, such as eating, exercising, working, or sleeping out. Participants also took steps to help nature, such as planting wildflowers or putting up bird boxes.

People said the challenge had been good for them, and for nature – increasing health and knowledge, feeling closer to nature and caring more for it. Those of us who had been rather shy of our enthusiasm for identifying bugs or lying in long grass, found ourselves in the in-crowd. It was also great for team-building, bringing together staff from across different business streams.

Now the June challenge is over, will we go back to how we were? Not according to the participants. They’d like to keep the habits of mindfulness, keep learning, keep sharing knowledge, and do more for nature – and take part in a bigger and better 30 Days Wild challenge again next year. We’re planning to do it again, and build on it with thematic challenges and office events. Maybe you’d like to join in with us?

You can hear more about our 30 Days Wild challenge in episode 6 of our podcast, Talking Natural Capital, where I chat with our CEO Martin Cassels about the challenge. n

economy, but as a practical, effective transformation within the entire global economy itself. What a task.

You are probably tired of hearing about the three global crises which make business-as-usual unsustainable. The climate crisis making life on earth increasingly perilous. The biodiversity crisis depleting the quality and diversity of nature to an extent that undermines the ecosystems on which we depend. The resource crisis that means the world’s population risks being unable to enjoy an adequate standard of living.

To address the climate, biodiversity and resource crises, we urgently need to use our resources more wisely and produce more, while simultaneously drastically cutting carbon and increasing biodiversity. This needs to be done, not with handouts from the existing

That’s why it was forestry which turned me from a campaigning environmentalist into a committed industrialist. It was through a chance meeting with a forester that my understanding of a forest changed from a static stand of trees, to a dynamic journey which tackles existential crises at every stage. Let me lead you briefly through that journey.

There is a perception that creating native woodland delivers better for biodiversity than conifer for timber production. I investigated this topic in detail for a report for Confor in 2020, Biodiversity, Forestry and Wood, reading dozens of scientific studies and consulting widely with ecologists and forest managers. I was left in no doubt that, in practice, in the distinctive land use context of the UK, biodiversity in timberproducing forestry has been

woodlands has struggled. The scale and speed of growth, the protection from herbivores and pests, the cycle of thinning and harvesting creating a diverse forest structure, the creation of deadwood through harvesting, and the environmental requirements such as inclusion of native trees and protection of watercourses, contribute to making wood-producing forests biodiversity powerhouses.

Foresters, in my experience, chose their profession from a love of being out in nature. They are thrilled to glimpse slow worm, capercaillie, osprey, crested tits, dormice, or the many other species which live in and around their timber crops – even when they do require special management at harvesting.

Foresters are also delighted when a client shows interest in biodiversity, and the silvicultural tweaks or investments which can be made to enhance it, such as choosing a site which could favour low-impact silviculture or more diverse tree

Galbraith Capital and Carbon leader Eleanor Harris writes about being an environmentalist who became a conifer convert.

species, or interventions like installing nest boxes in a wood too young to have the veteran trees which provide habitat for owls, bats or bluetits.

As for the climate crisis, I know of no other activity that tackles it in so systemic a way as growing timber. Genetic improvements mean UK timber trees suck up climate-changing atmospheric carbon dioxide at spectacular rates. A UK citizen is responsible on average for around 10 tCO2e per year: just half a hectare of timber crop will absorb this amount.

Yet it is when the timber is harvested, while the second fastest-growing crop is capturing carbon, that the magic really begins. Where does UK timber go? Around 42% is used in food production: fencing, pallets and packaging. A further 31% is used in construction, in various forms of sawn and engineered timber products. 20% is used for biomass fuel, and 4% for highquality paper and board. Your forest manager will be able to tell you what the wood you grow is likely to be used for, and how your choices influence the end products.

The wood supplying the food industry is a relatively static amount, although there is significant interest in using it more wisely through higher levels of pallet and packaging refurbishment and recycling. Biomass fuel has been growing, and its role in delivering the lowcarbon economy is complex.

Timber in construction has the biggest potential for growth, and is where new timber-growing capacity in the UK is most likely to be deployed. This has two spectacular carbon benefits. First, it keeps the carbon locked up for the long term, expanding the ‘virtual’ forest far beyond its local footprint. Second, it displaces the need for other materials like brick, block and steel, which have high carbon emissions at production. The home-owner will live in a changed climate as a result of those emissions, not just for the lifetime of the house, but in perpetuity. Trees can recapture carbon – but there is not

enough land in the world to offset the emissions of these materials, and not enough time. Building with wood, a material manufactured by sunlight, takes away the problem: it decarbonises.

Our final challenge is to use resources more wisely. We need to grow and use more timber, but that doesn’t mean we should squander it, because like all resources there is not – and cannot be – enough to go around under business-as-usual. Fortunately, wood is one of the easiest materials to keep in use, and to dispose of without waste and pollution – unlike its major competitor materials plastic and concrete. From the humble pallet upwards, innovations to increase the use and lifespan of timber products is an important area for investment. These often do not involve technical breakthroughs, but achievable, logistical ones: getting the right wood to the right place for the right purpose.

Wood is not a glamorous product, packaged with ecomessaging and purchased unnecessarily by wealthy virtuesignallers. It is a basic necessity of life, bringing food to shelves and roofs over heads – tackling injustices like food- and fuelpoverty. It also supports skilled rural careers: around 30,000 in UK forestry and timber processing.

Ask our forestry team about growing timber: how your investment can create biodiversity habitat, capture carbon, deliver for the lowcarbon economy, support jobs, and provide a healthy financial return. Ask to visit some examples of good-practice forestry, and a local sawmill, because there’s nothing like seeing for yourself.

But be warned: if you are an environmentalist exhausted by existential crises, you might find yourself converted into an industrialist excited for investment and innovation. n

Dr Eleanor Harris 07585 900 870 eleanor.harris@galbraithgroup.com

Timber in construction has the biggest potential for growth, and is where new timber-growing capacity in the UK is most likely to be deployed.

Dr Eleanor Harris

On the 6th September 2022 the Scottish Government announced the latest set of emergency legislative measures, a simultaneous rent freeze and moratorium on evictions until 31st March 2023, as a response to the energy and cost-of-living crisis.

The measures were widely thought to have had immediate effect, despite there having been no consultation or legislation enacting them as such. The statement made by the first minister outlined an “immediate” rent freeze and eviction ban, though subsequent Scottish Government publications on the details of the legislation and the Cost of Living (Protection of Tenants)(Scotland) Bill, published on the 3rd October, make it clear that the measures have not yet come into force but are expected to imminently, and the provisions are intended to be retrospective to the 6th September.

In any case, the vague wording of the announcement was likely deliberate in order to discourage concerned landlords from increasing rents or serving notices to terminate tenancies during the consultation period before the emergency

legislation is enacted. Following a meeting between the Scottish Association of Landlords and the Scottish Government on the 27th September, it was made clear that a rent increase cap of 0% will apply to notices issued from 6th September to 31st March, making any notice issued during this period void in effect.

Rent increase notices issued before the 6th September, not having yet taken effect are likely to be deemed valid, however it is not clear how rent increases issued after the 6th September 2022 but before the legislation comes into force will be treated in the First Tier Tribunal. There have been discussions surrounding the landlord’s ability to demonstrate “extreme financial hardship” to allow rent increases in extreme circumstances, though this again has not been embellished upon as yet.

With regard to eviction orders, it is important to note that the proposed measures only appear to apply to eviction orders by the sheriff court or First Tier Tribunal, and not to the formally issued Notice to Quit. Landlords will therefore still be able to serve notices to terminate tenancies on permitted grounds, however where the tenant does not vacate the property, the landlord will be required to apply to the tribunal for an eviction order. This order may only be granted where it is ‘reasonable to do so’, and could only be enforced where it falls within the following narrow grounds: antisocial behaviour, criminal behaviour, mortgage lender repossession or abandonment or to alleviate financial hardship. This, in effect, will mean that where a tenant refuses to vacate a property after an extended period of non-payment of rent (over multiple periods and the total

arrears equates to 6 months rent), or otherwise, any landlord will be unable to regain possession without a lengthy and expensive legal process, if at all.

The measures are also vague in terms of their application. Though Tenants’ Rights Minister Patrick Harvie announced that the measures give all tenants stability in housing costs, the timeframe for the effective ‘ban’, ending 31st March 2023, conflicts with social housing review rent dates, which are reviewed on the 1st April. Social housing tenancies will therefore be unaffected by these changes.

For private sector landlords the measures coincide with rising material and repair costs and will have a very real effect on the supply of rental housing on the market, as well as the quality. For many landlords, rent reviews were

delayed over the Covid-19 pandemic and have not yet taken place, meaning some rents have remained un-reviewed for 3 years. Whilst the measures do not appear to apply to change of tenancies, landlords may have to put planned improvements to properties on hold or consider alternative, more profitable, short term lets, without security of tenure or rent restrictions.

The changes have been brought in on the back of concerns that rising heating bills will limit tenants’ ability to afford rent, though a national system of rent controls was promised in the ‘New Deal for Tenants’ plan published last year, prior to the cost-of-living crisis, and have also been proposed within the new Housing Bills.

These changes are also introduced as the Covid Reform Act 2022

came into force on the 1st October 2022, making significant changes to the grounds to terminate a tenancy, which were originally brought in as temporary measures during the pandemic.

The Cost of Living Bill has now passed through Stage 3 of Parliament on the 6th October, having been introduced three days prior, and is now set to become law. The provisions are likely to be subject to challenge by various lobbying bodies but it remains a difficult time for the private rented residential sector. More updates will follow on our Galbraith blog. n Ailsa Baird

Asbestos was widely used in all manner of construction from the 1870s to 1999, and was considered a cost-effective building material, suitable for use on exteriors and interiors.

The importation, supply and use of all asbestos has been banned in the UK since 1999, while the Amphibole type of asbestos was banned in 1985.

Many people therefore assume that asbestos is a thing of the past. However, this is simply not the case.

Asbestos is a general name that is given to a number of naturally occurring minerals that have crystallised to form fibres. These asbestos fibres are strong, heat and chemical resistant, and do not dissolve in water.

There are two sub groups of these fibres, Serpentine (white asbestos) and Amphiboles (including blue and brown asbestos). Chrysotile, a member of the Serpentine subgroup, is the most commonly used type of asbestos in the UK.

Asbestos is not always where you might expect. It can be regularly seen on the roofs of agricultural buildings, in light fittings, ceiling panels, insulation, garage roofs and in many types of pipes and fittings. Basically, it can be found in any building constructed before the year 2000.

Twenty years on from the ban of the material, it is largely agreed by the Health and Safety Executive that asbestos is not considered dangerous when it is undamaged.

If damaged, asbestos can release smaller fibres that are easily breathed in or swallowed. This can lead to asbestosis, which can bring about an increased vulnerability to cancer and lung disease.

If you suspect that asbestos is present in your home, shed or an outbuilding, don’t panic.

Active monitoring and regular site visits of existing asbestos material are recommended in order to ensure the asbestos remains intact.

When questioning whether asbestos is present, it is worthwhile getting the material tested by an expert,

which is a cost effective way of determining the management of the material going forward.

The Control of Asbestos Regulations 2012 came into force on the 6th April that year and updated the previous regulations. Much of the content remained the same, although changes included the following points:

- When notifiable non-licensed work with asbestos is carried out, the relevant enforcing agency should be made aware. In this notification, the areas of work should be outlined, medical examinations are to be carried out, and up-to-date health records kept.

Brief written records should be kept of non-licensed work.

From April 2015, workers undertaking notifiable nonlicensed work with asbestos must be under health surveillance from a doctor.

There has also been some updating of language to reflect other UK regulation.

In the majority of cases, work involving asbestos needs to be carried out by a licensed contractor.

When deciding on which contractor to use, it is vitally important to research, and where possible, obtain reviews and recommendations from a reliable source.

Recently, there have been a number of occasions where instructions have not been followed correctly by licensed contractors and subsequently the work completed was not satisfactory, or indeed left incomplete. When this is combined with poor communication from some contractors, it can incur additional time and expenses.

Cost, liability and risk to health all play a part.

Since the regulations set out strict rules on the disposal of asbestos, many businesses are simply not prepared to include this as part of their service. This in turn makes it more difficult in rural areas to obtain the services of such businesses, and therefore makes the process more complicated and more expensive.

In any case, the key advice is not to remove the asbestos in a DIY fashion, but to consult an expert.

3 Get the material tested

3 Create an asbestos management plan

3 Engage with an expert and/or licensed contractor

3 Ensure that the contractor has the appropriate health and safety accreditations

3 Agree a method of work before starting any job

3 Research contractors’ previous work.

8 Never attempt to remove asbestos yourself

8 Don’t ignore the

8 Don’t employ a builder or handyman without the necessary accreditation

8 Don’t leave it to chance – make sure you are aware of the issue and the appropriate action to be taken.

In most cases, engaging with a properly certified contractor will provide reassurance and peace of mind that any asbestos on your property is identified and is being properly managed. If you require any initial guidance, please contact your local Galbraith office.

the

Jake Shaw-Tan and Aaron Edgar give their view of the property market in southwest Scotland, and the wonderful lifestyle on offer in Ayrshire and Dumfries & Galloway.

The property market continues to be very active at the time of writing although the headlines relating to the economic outlook are unfortunately all focused on the cost of living crisis, expected imminently.

We often find that any market slowdown in London and the southeast of England will filter through to Ayrshire six months or a year later. Currently, this is not in evidence, although we remain vigilant to market trends in other parts of the UK and will always advise clients accordingly.

Our most popular properties in Ayrshire are smallholdings and farm cottages with about two to three acres of land. This manageable amount of land offers the opportunity for perhaps a pony paddock, a small orchard or to grow your own fruit and vegetables, but not so large to be off-putting for those making the move to the countryside from the city.

Over the past two years, the dream of a rural idyll has continued to be the main motivation for a wide variety of buyers, from young couples to families and retirees.

Some of these buyers are futureproofing their lives, for example, they are planning for future retirement or are thinking ahead of the need to have an annex at home for family members. In Ayrshire buyers often find that they can often afford a sizable property with a good amount of accommodation, as prices remain relatively low compared with many other parts of the UK.

The pandemic has brought about two changes – the first being that the need to commute to an office five days a week is far less common; the majority of people have established a hybrid working model with the option for a few days working from home. This has widened the appeal of the whole region - traditionally the areas least in demand were those which are furthest from Glasgow, but now there is less of a distinction between the most accessible and least accessible areas.

The second change brought about by the pandemic is that many buyers wish to achieve any longheld dreams as soon as possible.

Ayrshire has beautiful beaches, rolling hills, productive farmland and is easily accessible to Glasgow and the central belt. With so much to offer it is not hard to see why property prices in the region have risen sharply in the past few years.

The region is perhaps best known as the birthplace of Robert Burns, Scotland’s National Bard, and the Burns Museum in Alloway offers a chance to see the cottage where he was born as well as many of his handwritten manuscripts.

Golf courses abound in the region, including championship courses at Royal Troon and Turnberry.

Shaw-TanThere is still a sense of ‘carpe diem’ and people are keen to improve their lifestyle sooner rather than later. A rural property facilitates this lifestyle. Among our buyers are also expats who have been considering returning to Scotland for some time and have brought forward their plans for this reason.

It is worth noting that it’s not necessarily the highest bidder who will secure the property. We often recommend to our clients to consider bidders who do not have a property to sell – and are therefore in a position to proceed without delay. This can prove of great benefit to ensure the sale is concluded promptly and to everyone’s satisfaction.

If you have a property to sell or are looking to buy in Ayrshire, please do get in contact. n

Jake Shaw-Tan 07919 182 474 jake.shaw-tan@galbraithgroup.com

Ayrshire boasts several glorious beaches including those at Ayr, Troon and Turnberry as well as several other hidden gems such as Dunure beach.

With excellent yachting facilities and some of the world’s best water out on the west coast, sailing is also a popular pastime in the county.

Ask locals about the Electric Brae on the A719 coast road - a fascinating optical illusion where a freewheeling vehicle will appear to be drawn uphill by an unknown force!

In Dumfries & Galloway, whilst demand for rural property remains high, with competition between buyers for the most desirable properties, the frenzied post-COVID activity appears to be slowing slightly.

There continues to be an imbalance between supply and demand but it remains to be seen if that will remain, as indicators of the market normalising may develop, with the ripple effect from trends south of the border.

During the past 18 months, so many potential buyers were chasing a relatively limited supply of properties and therefore competition between buyers was boosting the market, increasing the speed of sales and leading to upwards pressure on prices. Typically generating widespread national and international interest with recent examples of buyers travelling from Europe and the US to view.

Today smallholdings remain particularly in demand. The dream of the rural ideal remains a prime factor underpinning the market. Anything from equestrian property, self-sufficiency living, rural retreat or tourism/holiday lets plus of course the ability to earn an income from your home or additional buildings are all of continued appeal. Buyers appreciate also being able to have time to unwind, relax and enjoy their new surroundings.

The natural beauty and attractions of Dumfries & Galloway represent Scotland in miniature, with stunning scenery, picturesque coastal villages and the opportunity to enjoy all kinds of outdoor activities – all without the crowds that flock to other parts of the UK.

Many of our buyers are relocating from England. Even with the recent significant price premiums of the past eighteen months, Dumfries & Galloway still represents good value for money in comparison with most parts of England.

Dumfries & Galloway tends to avoid the rollercoaster of significant peaks and troughs in the market, as seen in London and the south of England over the past 20 years.

Property here is unlikely to suddenly shoot up in value from one year to the next but it is more likely to grow at a steady, more predictable rate over the long term, which most buyers prefer. There remains widespread confidence in Bricks & Mortar as a secure investment. n

Aaron Edgar 07899 877 737 aaron.edgar@galbraithgroup.com

The 7 Stanes mountain bike trails are challenging, world class routes that attract riders from across the UK and beyond. Five of them are in Dumfries & Galloway.

Galloway Forest Park is Britain’s largest forest park, covering 700 square miles, with ancient woodland, lochs and numerous walking and cycling trails, suitable for all ages and ability levels. The park has also been designated by the International Dark Sky Association as the first Dark Sky Park in the UK, offering excellent opportunities for stargazing just with the naked eye. On many nights the Milky Way can be seen and 7,000 stars and planets are visible in the night sky.

Dumfries & Galloway has beautiful coastlines including the Solway coast with its popular beaches at Sandyhills, Mossyard and Sandgreen and perhaps lesser known beaches including Carrick and Powillimount.

Kippford is a sailing hub on the estuary of the River Urr and has a popular marina. It is a charming, traditional waterside village with the wooded slopes of Mark Hill and the Mote of Mark fort behind.

From Kippford the Jubilee footpath leads to the pretty village of Rockcliffe, one of the region’s foremost property hotspots.

The Insider’s Guide to Dumfries & Galloway

2022

Galbraith provides an update on current market prices, giving comments on the issues and drivers of change in the industry. Forward budgeting has always been ever challenging, but with the cost of production rising and the Ukraine crisis causing ongoing uncertainty, it continues to be a concern.

The 2022 harvest in Scotland is now complete with 95% of the total Great Britain harvest being completed by 23rd August. This year’s harvest has been notably faster on average compared to previous years with the 5-year average of 69% being completed by 23rd August (week 7).

Despite the heavy rainfall towards the end of the harvest season, much of the grains remained at a suitable moisture content due to the extended period of hot weather. The hot weather may have fast-tracked the harvest but also brought risks. Combine and machinery fires were occurring across the nation due to the dusty and dry conditions creating a high-risk environment. On average, it has been identified that higher yields have been harvested on heavier soils with a better ability to retain moisture.

The wheat markets are volatile and responding to actions in Ukraine with concerns still on global grain markets. Across the week commencing on the 5th of September UK feed wheat futures (Nov-22) rose £8.75/t, closing at £275.25. The Nov-23 contract closed at £264.75/t, gaining £7.75/t FridayFriday.

Winter wheat finished harvest ahead of its 5-year average of 54% by week 7. This year 98% was complete at the same point in time. Scotland was the last nation in GB to complete harvest with less additional grain drying being

required nationwide. The GB winter wheat yield for week 7 was averaging 8.2 - 8.6t/ha. Milling wheat varieties have yielded 6.512.0t/ha with feed winter wheat experiencing a wide range of yields from 5.0 - 14.0t/ha. Wheat straw from this year’s harvest has been brittle due to the prolonged period of dry weather, therefore making it difficult to bale. Many who already had an abundance of good quality straw already stacked and baled opted to chop and incorporate it back into the soil to avoid nutrient loss. Grain quality was maintained throughout the harvest due to no significant rain holding up the process for the majority of the time with winter wheat grains at week 7 averaging 13.5 - 14.5% moisture.

The GB winter barley harvest was completed by week 5 with the North East of England and Scotland completing in week 4. Yields have varied between 6.0t/ha – 12.5t/ha.

The GB average yield for winter barley in 2022 is 7.2t/ha – 7.4t/ha which is above the previous 5-year average of 6.9t/ha. Quality had been good with hybrids producing lower weights than 2 row varieties. The winter barley crop averaged 13.5 –14.5% moisture content with grain requiring little drying. The winter barley straw has been a more variable quality with reports that it has been brittle and being bleached by the sun.

At week 7, the GB spring barley harvest was 81% complete. This was ahead of the 5-year average rate of

progress of 37% complete, by this point in the season. At this point, 56% of the spring barley harvest was complete by week 7. The lower figure in Scotland was thought to be due to other crops being prioritised. Despite this, the progress in Scotland was still ahead on average. The average for GB spring barley yields was 5.5 - 5.9 t/ha. Yields for malting varieties are between 4.4 –9.0 t/ha, with yields of feed varieties between 4.4 - 10.0t/ha. Moisture content is varied between 11 - 15%, with the GB average at 13 - 14%. The spring barley straw was reported to be higher on earlier drilled crops that were established.

At week 7, the oat harvest was nearing completion at 90%, ahead of the previous 5-year average of 43% by the same time. However, progress slowed towards the end of the season. Yields ranged between 6.0 - 10.0t/ha, with spring oat yields ranging from 5.5 - 9.5 t/ha. The GB average oat yield was 5.1 - 5.9 t/ha at week 7. Moisture content ranged from 12 - 15%, with the average at 13 – 14% by week 7. Winter oat crops had a good straw yield with little green, sappy straw reported. Many farmers have chosen to chop and reincorporate it into the soil.

Winter OSR harvest was completed first in England with Scotland following behind. Yields ranged between 2.1 - 5.0 t/ha. The lowest yields are from crops with poor establishment, water stress and pest/disease infestation. The

average yield remains unchanged from the first report at 3.0- 3.4t/ha.

Oil content is ranging from 43-45%, with a few confirmed reports of 47% oil content with a low amount of seed being dried. The recent cooler temperatures have allowed farmers to harvest during the daytime as the moisture content has increased to an appropriate level. Moisture content on farms has ranged from 6-11%. Early harvested WOSR had many occurrences of seeds with a moisture content below specification (below 5% moisture). (AHDB, 2022).

Andrew Sanderson

07920 292 826 andrew.sanderson@galbraithgroup.com

Dairy farmers have seen prices continue to rise. This is a fact for both inputs and the price milk processors pay farmers for their milk. The UK Average Farmgate Price (excluding bonus) throughout 2022 has increased dramatically month on month, with the July price reaching 45.57 pence per litre (ppl) (AHDB, 2022). The dramatic price increase, of over 10ppl since the start of 2022, has not however led to an increase in production. Milk production for 2022 in Great Britain (GB) is forecasted to be a total of 12.25 billion litres, this is down 1.6% compared to the 2021 calendar year (AHDB, 2022). The soaring costs of production which have been experienced through all of 2022, coupled with the rate of inflation both have contributed to this drop. Additional factors such as the weather and a reduction in the spreading of artificial fertiliser have also contributed.

The increase in milk price has lagged behind both inflation and the cost of production rises. This indicates that farmers are still recovering from previous cost deficits and are not able to benefit by increasing output. Despite the price leaps, uncertainty still looms over the industry. It is unknown how long the price of milk will rise, or indeed what level it will reach.

Jack Marshall

07899 980 246 jack.marshall@galbraithgroup.com

The wheat markets are volatile and responding to actions in Ukraine with concerns still on global grain markets...

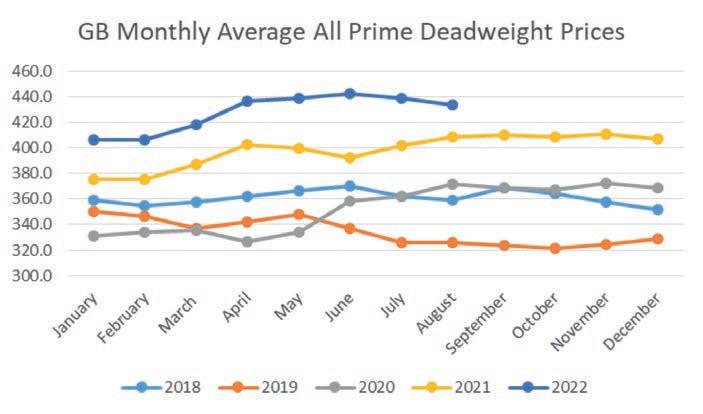

Producers have seen continued record high prices for the entirety of 2022 which has helped to reduce the impact of massively inflated input costs. January 2022 saw an average All Prime price of 406.3p/kg, with this strong position gradually fortifying itself to a high of 442.3p/kg in June. It remains to be seen if these prices are enough to counteract the increasing weight of variable costs.

Cow kill has increased throughout the year as producers understandably look to enjoy the record prices being experienced and as a means of reducing expenditure on inputs such as feed, fuel and fertiliser. The British beef herd is expected to decline due to a culmination of various factors such as increasing input costs, uncertainty over the overall profitability of beef production and doubts over the lack of future subsidy support. Galbraith consultants have experienced a few producers who have made the difficult decision to walk away from their beef herd entirely.

The industry has been supported, in the past year or so, by good levels of consumption which can largely be attributed to the after effects of Covid-19 with consumers enjoying the opening up of the hospitality sector. However, the cost of living crisis has stifled this with increasing food, energy and fuel costs constraining consumer budgets and forcing more cost-efficient lifestyle choices. For instance, consumption levels of beef in both the retail and hospitality sectors have diminished with 36% of consumers expected to reduce the amount they eat out. In the home, AHDB expects chicken and pork, the cheaper proteins, to become the more popular meat choices due to this increased cost of living.

In summary, whilst beef producers enjoy these higher prices which will partly mitigate spiralling input costs, consumers will also have to endure the widespread effects of inflationary increases. Domestic consumption and production of beef are expected to decrease for the remainder of 2022. It is hoped that

when the cost of living crisis ends that beef will be the ‘go-to’ meat that enjoys the resurgence of both the hospitality and retail sectors.

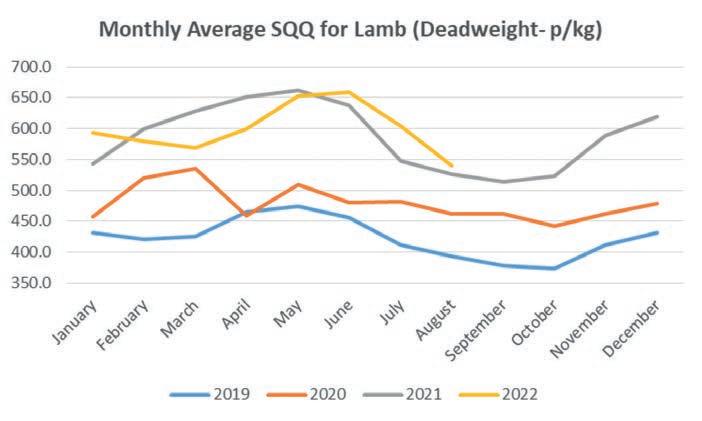

As we enter the final quarter of 2022 we are seeing a downturn in prices being achieved by lamb producers in the year. From a peak of 653.2p/kg in May the second half of the year has seen prices drop to a year-low of 539.3p/kg in August. To this day, it is the most recent data available. It remains to be seen if Christmas will provide a boost to prices, as experienced in the last three years.

AHDB reported that ewe kill for the first half of the year was up by 60,000 head on the previous year, with the total ewe kill numbers for the year reaching 1.27 million. Many farmers have likely been implementing culling policies in response to the high prices being experienced alongside spiralling input costs.

As discussed in the beef section, meat consumption has suffered from the increasing cost of living with retail consumption falling by 17% year-on-year (AHDB 2022).

Lamb is likely to suffer from being a more expensive meat product in comparison to chicken, which is likely to be viewed more favourably by consumers who are constrained by tighter budgets.

Looking forward, uncertainty looms with regard to the structure of subsidy support and how the new management requirements will affect the Scottish flock.

Furthermore, the UK Government is looking to seal a new trade deal with Australia which will open the door to lamb being imported from overseas. n

Calum07917

calum.chalmers@galbraithgroup.com

Galbraith is the market leader in Basic Payment Scheme (BPS) entitlement trading in Scotland. We anticipate a healthy level of demand for entitlements in all three regions. We have seen the start of BPS payments arriving for 2022 in late September. This has provided an excellent return on investment for farmers that had bought entitlements to cover their land earlier in the year.

For any farmers that have recently acquired any new land and do not have entitlement to cover it, now is the time to buy. The 2nd April 2023 is the deadline for transferring entitlements for the next BPS claim in 2023. From the demand that Galbraith experienced for 2022, we are prompting those who may require entitlements to get in touch sooner rather than later.

In addition to those looking to buy, it is also vital for anyone who currently holds entitlements but cannot claim them to look at selling them for the 2023 claim. Excess entitlement can arise for a number of reasons, including but not limited to: the sale of land; land being taken out of agricultural production; or the SGRPID remapping the farm and designating some land as BPS ineligible. If you hold entitlements but have not claimed them in 2022, they must be claimed on or be sold to prevent them being confiscated under the two year usage rules. Selling now would be a wise choice for anyone who has not claimed in 2022 and is unable to claim due to the size of their claimed area being reduced. This year Galbraith forecasts a continuation from last year’s busy trading period, with trading prices being largely similar for entitlement.

Current uncertainty is never good for business, however, there are some plans being laid out for the future. The new Agriculture Bill, currently under consultation until 21st November 2022, gives us a glimpse of what we could expect to see. The Scottish Government has stated in this consultation, that the replacement framework and legislation will be in place for implementation from 2026. This would indicate that the current Agriculture Policy will run until then, meaning there are potentially 3 years of current BPS payments available: 2023, 2024 and 2025.

If a farmer has unclaimed agricultural land, our advice would be to buy entitlements for it. Over the years entitlements have proved a tremendous investment when comparing the purchase price against the subsidy receipts that follow from the investment.

The Galbraith BPS trading team, based in Perth, is more than happy to assist with any enquiries.

Specialist BPS and general subsidy advice is also offered. n

The Ayrshire event brought together approximately 40 farmers to Woodhead Farm to engage with presentations that focused on practical carbon accounting, management, renewable energy and policy that affected the local rural sector.

Galbraith’s Natural Capital & Carbon Leader, Dr Eleanor Harris, held an outdoor presentation in which farmers were taught more about agroforestry and the multiple benefits that woodland can provide.

The benefits described by Eleanor covered private goods such as timber, firewood and chip but also included public benefits such as wellbeing, wind shelter and erosion prevention. Furthermore, Eleanor discussed how trees are carbon sequestering assets which can be planted to meet multiple objectives. Eleanor emphasised the importance of planting the right tree in the right place rather than planting trees that are not suited to site conditions. The presentation contributed to a useful dialogue with farmers who asked

specific questions about natural regeneration, tree diseases and pest management.

Kate Hopper, a land use planner from NFU Scotland, informed farmers about current rural emission levels and how the government was seeking to achieve its net zero target. The NFU acknowledges that the rural sector, particularly livestock and dairy, need to lower emissions, but that it has to be done in a sensible and sustainable way with thought given to the livelihoods of farmers in these industries. Kate warned that if the livestock market was pushed offshore, the UK would have to import the same products from overseas that may have lower welfare standards, or that overseas farms may contribute to global deforestation through unsustainable feed farming practices. It is important for the government to work with farmers by providing investment and incentive opportunities which will bring about better engagement for reducing greenhouse gas emissions.

To assist farmers in finding a practical method for accounting and finding carbon solutions, Robert Ramsay from Agrecalc informed the audience about the benefits of carbon audits. Robert highlighted the critical importance of gathering high quality data as being the most important aspect of achieving a useful carbon audit. The audits will help to secure additional grants and are a way of showing carbon accountability, which customers down the supply chain are now starting to seek. In addition, accounting carbon can be used as a tool to discover energy inefficiencies across the farm which can be rectified with help from Home Energy Scotland and Business Energy Scotland, who were also represented at the seminar by Lisa Johnston and Brogan Devlin respectively. These companies provide free consumer advice to those that are looking for opportunities to install or improve energy efficient heating and lighting. Brogan conveyed the usefulness of Business Energy

Scotland in being able to assist consumers with gaining access to government funding and highlighted the available opportunities for businesses to get cashback for investing in efficient systems. Lastly, Chris Kennedy from CK Energy spoke about the potential rooftop solar opportunities that were currently available and how to generate an income by exporting energy back into the grid.

The seminar was an incredible opportunity for Galbraith and other knowledgeable speakers to engage with farmers about opportunities to reduce carbon emissions. The event highlighted the growing awareness of the farming community to make their rural businesses more resilient

and sustainable through effective action. The team from Galbraith greatly appreciated John taking the time to show us the operation behind Woodhead dairy farm, particularly the practical ideas that have been implemented to improve farm efficiency.

Christine Cuthbertson, who is the Regional Manager for NFU Scotland Ayrshire gave some insight into why events like this have proved crucial.

“Rising farm input costs, especially energy and fertiliser, are certainly focusing the minds of Ayrshire’s farmers to look at farm efficiencies, new technologies and alternative incomes. The event at the Kerr’s dairy farm looked to make an introduction and contacts for our NFUS members to explore the options for their farms. Having been a Climate Change Focus farm 2014 to 2018, John Kerr was happy to share the changes made at Woodhead and how it’s an ongoing learning curve. Ultimately, improving efficiencies on farms can result in the reduction of the business carbon footprint, so it’s a win all round.

We greatly appreciate the support from Galbraith to NFU Scotland as Professional members and the expertise that brings to the table. We must thank Eleanor, Alice, and the team from Galbraith for being an integral part of the day.” n

James

James

The Galloway Glens Scheme is an initiative of Dumfries & Galloway Council’s Environment team, primarily funded by the National Lottery Heritage Fund, with support from a whole range of partners including Drax, the owners of the Galloway Hydro Scheme and the Galloway and Southern Ayrshire UNESCO Biosphere.

Running from 2018 to 2023 in the Ken/Dee valley in Galloway, the scheme aims to ‘connect people to their heritage’ while boosting the local economy and supporting sustainable communities. It will see more than £5million spent on a variety of projects up and down the valley, varying from education and training projects through to building refurbishments, visitor facilities and marketing campaigns.

The scheme has so far spent more than £3.6 million, with 75% of this going to Dumfries & Galloway based businesses. We have adapted well to a number of challenges over recent years, and in our final year of operation we are focussed on completing projects underway and maximising the long-term legacy of the work supported. We have tackled a whole range of

projects, but I am left wondering whether any are more complex than the topic of ‘footpaths’.

Scotland hosts what might be the most ‘access-friendly’ legislation in the world. The Land Reform Act 2003, supported by the Scottish Outdoor Access Code, sets out rights and responsibilities for access-takers and landowners. Other countries cite Scotland in their access discussions as the gold standard and sometimes it can be considered to be a topic that is ‘sorted’ in Scotland. Having now been involved in a few access projects, I see that we are all – even 20 years later - still adjusting to the new legislation.

A footpath is a totemic project to be involved in. Everyone understands the principle behind it but immediately user expectations vary in terms of what constitutes a footpath. Is it a full-blown ‘tarmac’ed surface, fenced either side with benches and litter bins, or is it a line

on a map, actually barely perceptible on the ground?

Councils in Scotland are required to maintain a map of core paths. Here in Dumfries & Galloway, core paths across the region total more than 1,180 miles in length. Some of these routes form the centrepiece of our recreational offering. Others wouldn’t be known or walked by more than a couple of folk a year. Even the phrase ‘core path’ comes in for some criticism – does this overpromise what might actually be encountered on the ground?

Councils have a responsibility to maintain access across the core path network, but in the face of budget cuts, this can result in a minimal ‘responding to loudest complaints’ approach.

If you can ‘roam’ in Scotland, people ask whether there is still any need for footpaths?

I now understand that footpaths, when done well, can actually benefit both the landowner and the access taker. A footpath does more to manage and control access than people might realise. Establishing a footpath means the vast majority of people will follow the route, rather than making their own way across land. If people are able to cross land, it is better that they do it in a managed place. We have found that the presence of a footpath, installed to a reasonable standard, can actually reduce tension between a landowner and access takers.

We installed a suite of three footpaths in January 2020 that were initially intended as a visitor attraction but were immediately put to incredible use by locals through the pandemic restrictions and ‘one hour a day of outdoor time’ requirements. It was startling how well these routes were used and the wider health and wellbeing benefits that resulted. Recent discussions with forestry developers on tweaking proposed access routes from a linear ‘herringbone’ approach to inclusion of a couple of circular routes can yield massive recreational benefits, for a minimal increase in expenditure.

I am so grateful to all landowners that have supported our footpath improvement projects, and endeavour to flag up the positive feedback we receive, illustrating the difference these projects make. Done well, it really can be a benefit to all parties.

As I write (in early October) we are navigating a very turbulent period in UK and global economics. In the midst of a cost of living crisis, with soaring fuel, energy and food costs, the UK Government and Bank of England are seeking to implement measures to curb inflation which is currently at 9.9%.