Galbraith update on Importance of getting a valuation for IHT planning.

2025

Scotland’s burning issue

Reporting on the increasing wildfire risk throughout Scotland and the devastating effect.

Agri Market Update

Galbraith team summarises the current trends in Agri Market commodity prices.

The evolution of Scottish farming

Challenges and policies that have defined farming life in Scotland from the 1960’s to present day.

Welcome to the Summer edition of Rural Matters 2025

Welcome to the latest edition of Rural Matters. What a difference a year makes! The contrast is striking - both in terms of weather conditions and markets. It serves as a reminder that the rural community is constantly challenged by influences often beyond our control.

Yet, we remain as resilient as ever, adapting where necessary. While many might fold, we push forward to survive another day.

In this edition, we highlight the fast-paced and everchanging rural world—from legislation to subsidies—emphasising the need to stay agile, evolve, and adapt.

We also take a nostalgic look at yesteryear, as some of our colleagues share fascinating reflections on their family businesses and how they’ve evolved from the 1960s to the present day. The pace of change is remarkable, but it undoubtedly fosters growth, adaptability, and new opportunities. n

Ian Hope 07968 209 543 ian.hope@galbraithgroup.com Head of our Rural Department

Galbraith is a leading independent property consultancy. Drawing on a century of experience in land and property management the firm is progressive and dynamic employing over 200 people in offices throughout Scotland and the North of England. We provide a full range of property consulting services across the commercial, residential, rural and energy sectors. Galbraith provides a personal service, listening to clients and delivering advice to suit their particular opportunities and circumstances.

Follow us on X: @Galbraith_Group

Like us on Facebook: www.facebook.com/ GalbraithPropertyconsultancy

See us on Instagram: www.instagram.com/GalbraithGroup

Join us on Linkedin: www.linkedin.com /company/galbraith

See us on TikTok: https://www.tiktok.com/ @galbraithgroup

4

The right to roam turns twenty.

6

Natural Environment (Scotland) Bill.

8

Wildfires - Scotland’s burning issue.

10

The importance of and process behind CDM Regulations 2015.

14

Farming subsidy changes 2026... Greening.

12

Plan ahead - The importance of getting a valuation for IHT planning.

16

Full Circle for Flexible Flax.

17

The purpose and benefits of estate and farm reviews.

18

Agri Market Update Summer 2025.

22

28

The evolution of scottish farming & government subsidies - 1960s to present day.

Caerlaverock Estate - Where community, culture and conservation come together.

THE RIGHT TO ROAM TURNS TWENTY

Philippa Orr

07917 220 779

philippa.orr@galbraithgroup.com

2025 marks 20 years of the Scottish Outdoor Access Code or, as more commonly known, the right to roam.

The right to roam was introduced in the Land Reform (Scotland) Act 2003, which came into effect in 2005 and grants the public a general right to access most land and inland waters in Scotland for recreation and other purposes, as long as that right is exercised responsibly.

This applies to everyone in Scotland, whether resident or visitor and the Code allows access to hills, valleys, moors and waters for walking, cycling, horse riding, climbing, sailing and canoeing.

It is a common misconception that open access was only permitted as a result of the Code. In fact, it was happening very widely in Scotland before the legislation was drawn up and that had been the case for generations. Several Scottish estates had an open access policy going back to the 19th century.

The code is, however, a useful tool, formally setting out the rights and responsibilities of members of the public.

Scottish access rights are subject to several important limitations. The right to roam does not apply to the following:

• Land occupied by buildings, fixed machinery, or any place that offers privacy or shelter, such as a tent or caravan (this includes both residential and non-residential buildings).

• Gardens surrounding houses, caravans, or tents and private communal gardens reserved for residents, even if not directly attached to homes.

• School grounds or land used by schools, such as playgrounds.

• Land developed for sports, play, or other specific recreational purposes.

• Land where crops are growing.

Exemptions exist partly to protect the public – for example, areas where machinery may be in operation at certain times of the year, and also to protect the right to privacy of a resident – such as the home-owner’s right to enjoy the garden of a property in a rural area.

Motorised activities, such as off-road driving or motorbiking, are also excluded from public access rights and would require specific landowner permission.

Public access cannot be used for country sports such as hunting, shooting and fishing, which also require agreement in advance from the landowner.

The most important part of the right to roam is that it is based on reasonable access and there are three underlying principles, as follows:

• Respect the interests of other people.

• Care for the environment.

• Take responsibility for your own actions.

Landowners are required to allow the right to roam over their land but they must use and manage their land in a responsible way and cannot unreasonably restrict access.

Should access be required through a field, a walker should avoid damaging the crop by using paths, tracks or unsown ground. If there are animals in the field then people should keep a sensible distance from animals, especially if there are calves or lambs. All gates should be left the way they are found, and it is vitally important that dogs are kept on a lead. Equally, should another route be possible, it would be recommended that this is taken rather than walking through a field with young livestock. Cows are notoriously unpredictable, particularly when they feel threatened.

Many landowners have found that protection of sensitive areas can

“The Code allows access to hills, valleys, moors and waters for walking, cycling, horse riding, climbing, sailing and canoeing.”

be achieved by encouraging access across natural routes and existing informal footpaths – for example, signposts or waymarkers which encourage the majority of walkers to stick to an existing path, or ‘desire line’ between known beauty spots such as a waterfall or historic site.

In the past few years, we have seen a significant increase in the number of people seeking to explore areas of Scotland and take advantage of the many benefits of outdoor activity. Some farmers and landowners have reported an increase in gates being left open, out of control dogs, damaged fences and littering.

As I write, 2025 looks set to be the worst year on record for wildfires, with Scotland particularly hard hit. Some are asking if we should consider modernising the now 20 year-old Code to reflect the scale and type of access being taken by the public.

Ultimately, education is key to responsible access to all types of land. Rural organisations and the Scottish Fire & Rescue Service have campaigned extensively on the risk of wildfire, helping to ensure that there is good awareness of a range of high-risk behaviour, including the use of disposable BBQs in the countryside, a significant hazard. Some supermarkets have now stopped selling them altogether.

It is clear that the process of education and awareness-raising is one which will continue and evolve in the future.

Landowners, farming and countryside organisations and public bodies will no doubt continue to co-operate and share information to balance the demand for reasonable access to our beautiful countryside, with appropriate protection for rural businesses, farmers and landowners. n

Natural Environment (Scotland) Bill

The Natural Environment (Scotland) Bill, introduced to the Scottish Parliament on February 19, 2025, seeks to establish mechanisms intended to curb habitat and biodiversity loss. The Bill comprises five parts covering biodiversity targets, environmental impact assessment (EIA) and habitats regulation modification powers, National Parks, deer management, and general provisions.

James Lighton 07342 093 469

james.lighton@galbraithgroup.com

Part 1: Targets for Improving Biodiversity

The first part of the Bill seeks to amend the Nature Conservation (Scotland) Act 2004. It sets out a framework for Scottish ministers to set achievable environmental targets, to be reviewed not less than once every three years and reported not less than once every ten years. When setting or reviewing targets, ministers must seek and consider scientific advice from independent experts and be satisfied that new or amended targets can be met. Whilst these targets need to be based on appropriate scientific evidence, and ministers have a duty to ensure targets are met, targets can be revoked or diminished under specific conditions, such as the need to set a replacement target due to failure.

Part 2: Power to Modify or Restate EIA Legislation and Habitats Regulations

The Bill seeks to grant Scottish ministers a broad power to modify or amend the relevant Environmental Impact Assessment legislation and habitats regulations. This power is necessary because their previous ability to amend these regulations using powers under the European Communities Act 1972 was lost following the UK's exit from the EU.

This power can only be exercised for specific purposes. These purposes include maintaining or advancing standards related to restoring, enhancing, or managing the natural environment, preserving, protecting, or restoring biodiversity, and environmental assessments. Another purpose is to facilitate progress toward any statutory environmental, climate, or biodiversity target that are in force in Scotland.

Part 3: National Parks

The Bill proposes changes for National Parks by modifying the National Parks (Scotland) Act 2000. The aims of National Parks are updated with added new explicit inclusions, such as restoring and regenerating biodiversity and mitigating and adapting to climate change within the park areas.

Crucially, the duty on Scottish ministers, National Park authorities, local authorities, and other public bodies is strengthened regarding National Park Plans. Instead of merely having a duty to "have regard to" these plans, they now have a duty to facilitate the implementation of them. This requires public bodies to cooperate with and support the execution of the plan, which may involve active steps or removing barriers, provided it is consistent with their other functions. The Bill also allows for regulations to introduce fixed penalty notices for National Park byelaw offences, potentially enhancing enforcement.

Part 4: Deer Management

The fourth part of the Bill seeks to introduce a comprehensive overhaul of deer management under the Deer (Scotland) Act 1996. The aims of deer management are updated to include furthering native deer conservation, promoting sustainable management, ensuring effective control, and safeguarding the public interest.

The Bill introduces two new, explicit grounds for NatureScot intervention: damage by deer and nature restoration. The agency can intervene if deer cause damage to interests like woodland or agriculture, or if they prevent nature restoration efforts which are deemed to contribute towards statutory targets. When these grounds are met, NatureScot may require owners/occupiers to submit deer management plans for approval. It may also seek control agreements. If compliance with an agreement is insufficient, NatureScot must proceed with making a control scheme or explain why this is not possible. The process for making a control scheme involves public consultation and potential objection to Scottish Ministers, with a right of appeal to the Scottish Land Court. It also introduces powers to the agency to recover costs associated with schemes from owners/occupiers. In some positive news for landowners, the Bill proposes to remove the requirements related to licensing to deal in venison.

Conclusion

The Natural Environment (Scotland) Bill proposes wide-ranging legal changes impacting strategic biodiversity targets, environmental regulation powers, National Park management, and deer management. While the Bill's aims are clearly directed at addressing biodiversity loss and climate change, it is essential that input from landowners and managers is taken into account to balance the ambition of nature restoration with financial realities.

In terms of the Bill’s proposals for deer management, many landowners are already acutely aware of the impacts and costs that deer have on operations. Some commentators have argued that a collaborative and joined-up approach, which has yielded proven progress, should be further incentivised, rather than a punitive approach which risks adding additional financial burden. It is also important to acknowledge the potential nexus between the Natural Environment Bill (Scotland) and the Land Reform Bill, which is currently under consultation. Under the Land Reform Bill, certain landowners will be required to have a land management plan, and it needs to be made clear how ministers powers to modify EIA legislation would impact these plans. n

Today, the issue of wildfires burning out of control is not just a potential threat but a reality here in Scotland, just as it has been in the hills above Los Angeles.

Over the past few weeks, wildfires have swept across vast areas of the countryside, devastating habitats, destroying wildlife, releasing colossal quantities of carbon into the atmosphere and putting firefighters in danger.

A massive blaze that started in the Galloway Forest Park in Dumfries & Galloway spread to Merrick Hill, Ben Yellary and Loch Dee, then into neighbouring East Ayrshire, requiring the evacuation of holiday-makers and local residents. The fire was eventually brought under control after four days of sustained effort by the Scottish Fire & Rescue Service, including waterbombing helicopters.

At Stac Pollaidh in the Highlands, eight fire crews described a ‘wall of fire’

WildfiresScotland’s burning issue

A few years ago any comparison between the climate of California and Scotland would certainly have raised eyebrows.

stretching more than three miles at its height and resulting in the closure of the A835. It took two days to bring the blaze under control.

There were also smaller wildfires on Arran, on the Isle of Skye, in West Dunbartonshire and East Dunbartonshire, while a Woodland Trust reserve in North Lanarkshire suffered three wildfires in one week.

A sustained dry spell and higher than average temperatures in March contributed to the spate of fires, but 2025 cannot be seen as an anomaly, rather it is part of a continued trend over the past decade, underlining that periods of fire-supportive weather are becoming more common in the UK, and indeed in Scotland.

Climate change is undoubtedly one of the main reasons for the increasing prevalence of wildfires, coupled with a rise in the number of people enjoying the countryside for a range of leisure pursuits, from hillwalking to mountain

biking, birdwatching, stargazing and wild swimming. The increased visitor access is very welcome but it does also bring an increased risk of fire, due to a minority engaging in high-risk behaviour such as using disposable BBQs or littering.

Land managers are concerned that the Scottish Government’s new muirburn licensing regime will not ease the situation, rather there are fears it may make matters worse.

The regulations, part of the Wildlife Management and Muirburn (Scotland) Bill, are due to come into force on 1 January 2026.

As part of the new licensing system, there will be a revised Muirburn Code. At the time of writing, NatureScot is still consulting on the code and many land managers have expressed concern that the timescale for finalising the code, followed by implementation of the new licensing system, is insufficient and will leave

“A sustained dry spell and higher than average temperatures in March contributed to the spate of fires, but 2025 cannot be seen as an anomaly.”

many land managers unable to obtain a licence in time for the next muirburn season.

Muirburn is the practice of managing upland vegetation through careful, controlled burning of small patches of vegetation, in full compliance with the existing and very detailed Muirburn Code.

By law, burning is only allowed between 1 October and 15 April, extendable to 30 April with the express permission of the landowner.

Gamekeepers and land managers burn off small patches, creating a mosaic of shorter vegetation, which is an important part of the diet of many moorland birds, interspersed with longer vegetation, used for nesting and shelter.

The new regrowth of vegetation is preferred by invertebrates and also sequesters more carbon, as growing plants take more carbon out of the atmosphere than established plants.

The crucial difference between controlled burning and a wildfire is that only the uppermost vegetation is burnt off during a controlled burn, leaving the ground beneath unaffected.

By contrast, wildfires burn for hours or days on end, generating high temperatures and setting fire to the ground itself. Where there is peat in the soil, this can smoulder underground for days on end, providing an exceptional challenge for

fire fighters to fully extinguish. The speed of a wildfire means that birds, reptiles, invertebrates and small mammals will often succumb to the flames. On peatland, a wildfire will also cause vast quantities of carbon to be released, adding to our greenhouse gas emissions and hampering efforts to protect the environment.

Land managers are concerned that the expertise, knowledge and experience of those conserving our rare habitats over generations is not recognised by the Scottish government. In recent years, policymakers have embraced the ideas of vocal campaign groups advocating ‘rewilding’ huge areas of Scotland. This involves allowing vegetation to grow unchecked, whether it is scrub, bracken or Molinia grasses. The impact on Scotland’s biodiversity over the long-term is unclear, but it is well established that bracken and Molinia grass constitute very low-quality habitat, largely devoid of wildlife. Allowing vegetation to reach a considerable height and density across large areas is akin to adding fuel to the fire. During periods of dry weather, wildfires can take hold and spread at incredible speed. Where there are no areas of managed moorland, there are no firebreaks, and we have seen time and time again that unmanaged land provides the ideal conditions for a major conflagration.

Some conservationists advocate ‘rewetting’ as a tool to help prevent future wildfires but experience shows that even bogs can burn, where there is vegetation to fuel the flames. The Flow Country fire of 2019 scorched 5,700 hectares of blanket bog, with the release of 700,000 tonnes of CO2, according to an analysis by the World Wild Fund for Nature. It is estimated by NatureScot that 23% of Scotland’s land area is blanket bog, storing around 1.6 billion tonnes of carbon. It is vital to protect these carbon stores.

Despite the evidence that muirburn is not only a positive factor in conserving upland habitats but a crucial tool to prevent devastating wildfires, the muirburn licensing regime will only

allow muirburn on peatland if “no other method of vegetation control is available”.

Again, this heightens the risk of wildfire. The Scottish government has suggested that the other main method of vegetation control (cutting) could be adopted where a licence for muirburn has not been granted, but vegetation cutting is virtually impossible on steeply sloping land and on rocky areas – anyone with any knowledge of the Scottish uplands will tell you that this rules out a significant proportion of the countryside!

Cutting can in some cases also contribute to the risk of wildfires. Brash left behind after winter mowing is typically left on the hillside. This will dry out and, come the spring, becomes highly flammable - acting as fuel to any wildfire that breaks out.

Land managers and rural organisations have engaged closely with policymakers over the past five years, but many feel that their key concerns have been ignored. The Scottish Fire and Rescue Service acknowledges that muirburn reduces the threat of wildfire, but any neutral voice is discounted.

Well-managed moorland provides the ideal conditions for iconic – and internationally rare – species such as the Black Grouse, Curlew, Golden Plover, Capercaillie and Red Grouse, all of which benefit from open moorland habitats and struggle to survive in areas of dense vegetation or woodland.

In the rush for ‘rewilding’ it seems that the Scottish government is rejecting the landscapes loved by locals and visitors alike – and the species that thrive in them – in favour of untested new approaches to land management.

Urgent attention must be paid to the evidence provided by people who have managed Scotland’s countryside for generations – before even more precious habitat goes up in smoke. n

Alex Davies 01463 224 343 alex.davies@galbraithgroup.com

This article aims to give readers a better understanding of the importance and process behind this important legislation.

In April 2015, the most recent iteration of the Construction (Design & Management) Regulations 2015 (CDM) came into force. These regulations aim to improve health and safety in construction projects by outlining the roles and responsibilities of various stakeholders and managing risks within the project.

CDM is a legal requirement and applicable to all construction projects regardless of size or complexity. It not only governs newbuild projects but also repairs and maintenance, demolitions, renovations, extensions and conversions.

Failure to comply can lead to fines or even imprisonment, as such, it is vital that property owners, managers and contractors alike are aware of their responsibilities and adhere to the practices.

The importance of & process behind CDM Regulations 2015

The words Compliance and Health & Safety are rarely ones that evoke intrigue or excitement, yet they are increasingly important in the modern world.

Roles and Responsibilities

Varying Scales of Projects

Client – The individual or organisation for whom the

• project is carried out and is accountable for the impact that their decisions have. The client is responsible for leading the procurement process, commissioning design and construction works, preparing all necessary documentation and ensuring the Designer & Contractor carry out their duties.

There are two overarching types of projects within the CDM Regulations. These are non-notifiable and notifiable. A project is deemed notifiable if:

• than 20 workers working at the same time at any point, or,

It lasts longer than 30 working days and has more

•

It exceeds 500 person days

Designers – The designer is responsible for ensuring

• that Health & Safety (H&S) is considered during the design phase of a project, identifying, eliminating or minimising any perceived risks.

Contractors – The contractor is responsible for

• ensuring that they and any workforce have the correct skills and qualifications to carry out the works. They are also responsible for managing the workforce on site.

In instances where there are multiple contractors on site there must also be

Principal Designer – The principal designer is

• responsible for planning and monitoring H&S, assisting the client in identifying, obtaining and collating the Pre-Construction Information (PCI) and overseeing all roles throughout construction phase.

Principal Contractor – The principal contractor has

• responsibilities similar to those of the Principal Designer but with more emphasis on the construction phase. These include planning and monitoring H&S during the construction phase, preparing the Construction Phase Plan (CPP) prior to commencement, organising contractors on-site and ensuring welfare facilities are provided.

If a project meets one or both of these criteria then the Health and Safety Executive (HSE) must be notified via service of an ‘F10’ notice as soon as is practicable prior to commencement of works. This duty falls to the Client or can be delegated, often to the Principal Designer in such projects as one is required.

In Practice

As Project Managers and Managing Agents, Galbraith instruct a wide variety of works from minor repairs to large scale agricultural and commercial construction. The key to successful adherence to the CDM Regulations is using them in proportion to the task. This is also key in getting contractors to engage with the process.

Works Involving One Contractor

For the majority of minor repairs and maintenance works that we instruct, typically only involving one contractor, the process is fairly simple and routine requiring the following;

Ensuring the identified contractor has the skills

• and knowledge to undertake the task. This includes having them onboarded as a “competent contractor” within our systems and holding all relevant qualifications and insurances.

“The key to successful adherence to the CDM Regulations is using them in proportion to the task. This is also key in getting contractors to engage with the process.”

Assessing apparent project and site-specific risks

• and completion of relevant Pre-Construction Information (PCI) which is sent to the contractor.

Ensuring the contractor has completed a

• Construction Phase Plan (CPP) prior to commencement of the works and review this document with them. This should outline the process required to complete the task, describe how any risks identified in the PCI will be mitigated against, confirm all tools and apparatus are in good working order and all Personal Protective Equipment (PPE) is present and in good order.

A brief summary of documentation;

Pre-Construction Information (PCI) – Is critical to

• a safe project. It provides H&S information to enable designers and contractors to carry out their work effectively and provides the basis for the CPP. In larger projects, the PCI will be developed over the course of the design phase as new factors to be considered may come to light.

Construction Phase Plan (CPP) – Records how

• H&S is to be approached and managed throughout the project. It outlines the stages of the planned works and the timescales involved and forms the basis of how all stakeholders understand the risks involved in the project.

Health & Safety File – Although not strictly

• required under the regulations for non-notifiable works, it is always best practice to have a H&S file for the project which will hold all of the above documents.

Works involving Two+ Contractors & Notifiable works

These projects by default tend to be larger, much more involved projects with greater detail required in the CDM forms and process. Principal Designer and Principal Contractor roles must be designated and involved throughout.

The F10 form that must be submitted to HSE in the instance of notifiable works comprises much of the detail in the above documents. It is in a prescribed form and is submitted electronically.

How Do Galbraith Help Clients Manage the Risk?

As agents who instruct a wide variety of works requiring CDM on behalf of clients, we understand the importance of the process. To reiterate, the key is to ensure engagement of contractors in the process and confirming each stage is completed correctly in the interests of all stakeholders involved.

James McDonald

07595 278 446

james.mcdonald@galbraithgroup.com

We have a designated group of CDM reps who are leading the field in compliance with the regulations. It is felt that this important piece of legislation is too often overlooked, particularly in some sectors, but the cost of non-compliance can be much greater than many realise. n

PLAN AHEADTHE IMPORTANCE OF GETTING A VALUATION FOR IHT PLANNING

In our previous Rural Matters Winter Edition, we reported on the Inheritance Tax (IHT) changes that were announced in the Autumn Budget 2024.

Edward Fletcher 07990 130 753 edward.fletcher@galbraithgroup.com

These reforms have evolved through subsequent consultation and continue to generate concern among stakeholders in the agricultural sector.

At the time of writing, significant changes to the IHT treatment of agricultural property will take effect on 6th April 2026. Most notably, there will be a cap on the value of agricultural and business assets that can receive 100% IHT relief.

Under the new rules, only the first £1 million of qualifying assets will receive 100% Agricultural Property Relief (APR) and Business Property Relief (BPR). Any amount above this threshold will only be eligible for 50% relief. This means that the excess value will effectively be taxed at 20%— half the standard IHT rate of 40%.

The new rules will also apply to assets transferred into trusts and those passed on through lifetime

gifts. Specifically, if an individual makes a qualifying transfer on or after 30 October 2024, and dies on or after 6 April 2026, the new relief caps will be applied. This aspect of the reform was clarified through a technical consultation which concluded in April 2025, confirming the alignment of the treatment of trusts with that of directly owned assets.

In an effort to recognise the potential financial impact these changes may place on landowners, the government has introduced a mechanism to spread payments. Beneficiaries of estates with qualifying agricultural or business property will be permitted to pay their inheritance tax liabilities in ten annual instalments, interest-free. This aims to reduce the risk of forced asset sales, particularly of productive farmland or key business assets, in order to raise cash for tax payments.

Importantly, the fundamental criteria for qualifying for APR and BPR have not changed. To claim APR for example, the land must still be used for agricultural purposes and meet specific ownership or tenancy duration criteria. Similarly, BPR will continue to apply to businesses that are predominantly trading in nature, rather than investment-led and that meet existing control and activity thresholds in line with the Balfour decision.

Despite government estimates suggesting that fewer than a third of estates currently claiming APR and BPR will be significantly impacted, the proposed changes have sparked a strong response from the rural sector.

The National Farmers’ Union (NFU) has warned that as many as three-quarters of commercial farms could see increased tax exposure, particularly those with diversified holdings or mixed-use properties. Concerns have also been raised in Parliament, with a cross-party group of MPs urging the Treasury to delay implementation until at least 2027, arguing that the proposed timeline does not allow sufficient time for farmers and rural business owners to adapt. However, at the time of writing, the government has maintained its commitment to the April 2026 commencement date. With that deadline approaching, rural landowners are being advised to review their succession and tax plans promptly, assess potential liabilities under the new regime, and consider steps such as restructuring or lifetime transfers— though any such decisions must be carefully weighed against capital gains tax and other potential implications. These discussions should involve a range of professional advisors, specifically accountants, solicitors and surveyors to ensure all appropriate advice is taken into consideration.

Undertaking a valuation is the first step in this process. It will form the basis of all subsequent tax planning and may need to be relied upon if any property transfers are undertaken. Galbraith’s registered valuers are qualified to undertake valuations on a range of rural property types to the RICS Valuation –Global Standards (Red Book), the standard required by HMRC. Once this has been prepared, accountants and solicitors will be in a position to assess the new tax position, advise on any steps that should be undertaken and progress any transfers or restructuring work.

If you are considering your tax planning and require a valuation, please contact your local Galbraith office. n

Does the Planning and Infrastructure Bill Provide New Light For Solar?

The Planning and Infrastructure Bill entered Committee Stage in the House of Commons on 24th April 2025. It aims to make significant alterations in the way land use, infrastructure projects, development and renewable energy sites are planned and approved. The impetus behind this is that the government believes the failure to build sufficient infrastructure is constraining economic growth and undermining energy security.

It is planned to simplify gaining consent of Nationally Significant Infrastructure Projects (NSIPs), taking decisions away from the local authority and handing them to the Planning Inspectorate. These planning decisions are determined against a set of national policy statements specific to the NSIP regime.

A perceived positive to this is solar sites of over 50 megawatts could now be approved faster, reducing administrative burdens – perhaps good news for those with solar potential on their land and for the future of renewable energy deployment.

For landowners generally, the proposed Bill presents both opportunities and challenges. Larger solar farms can offer lucrative leasing arrangements and steady income streams well above that of agricultural productivity of the land. It is likely that landowners in rural areas will see increased interest from developers seeking to maximise project scale and efficiency. In some cases, a proposed scheme may incorporate property of multiple landowners requiring cooperation and joined up thinking to ensure the best deal is achieved for all.

Constraints include that the mechanisms within the Bill may lead to land being repurposed at a faster rate, with a reduction of landowner rights and compensation provided for within the Compulsory Purchase process. It could also raise public concerns about overdevelopment of the natural landscape and loss of natural habitats without proper consultation. To reserve their position landowners need to remain informed about the planning processes and their options when faced with these larger projects.

The Bill’s capability of increasing renewable energy capacity and grid feed in aligns with national goals to reduce carbon emissions and the transition to cleaner energy sources, but it has to be made clear that these developments must be sustainable, environmentally responsible and made with the increasingly fragile rural economy at the heart of decision making.

The ramifications of the proposed Planning and Infrastructure Bill represent a major step toward accelerating renewable energy projects, especially in rural areas. While it offers economic and renewable energy benefits, it also calls for careful management to protect landowner rights, local landscapes, ecosystems, and community interests. Transparent consultation and fair negotiation with landowners will be essential to ensure that the growth of renewable energy aligns with sustainable development and benefits all stakeholders involved. n

Farming subsidy changes 2026... Greening

Recently farmers have had letters from the Scottish government to outline changes to Ecological focus areas (EFA) from 2026. These letters show significant changes to greening requirements, and we have summarised these matters below.

Enhanced Greening Measures

In line with the new support structure, the Enhanced Greening requirements will be updated in 2026. Key updates include:

• Removal of Exemptions: The 75% exemption for temporary grassland on arable land and grassland on claimed land will be removed. This means that more farms will be required to manage EFAs.

Expansion of EFA Options:

Four new EFA options will be introduced:

Green Cover

There has been an introduction of new species that can be included in a cover crop mix including alsike clover, crimson clover, Persian clover, buckwheat, kale, stubble turnip, forage rape and winter beans. Green cover can now be grazed as soon as it is fit to consume.

Nitrogen-Fixing Crops

Calum Smith

01292 268 181 calum.smith@galbraithgroup.com

Low Input Grassland: Areas 1 managed with minimal fertiliser and pesticide use.

Herb and Legume-Rich Pastures: 2 Swards enriched with diverse plant species to enhance biodiversity.

Unharvested Crops: Crops left 3 unharvested to provide habitats for wildlife.

Agroforestry Low-Density Planting: 4 Integration of trees into agricultural land to promote ecological balance.

• The required EFA area will remain at 5% of the arable area in 2026 with plans to increase it to 7% in 2027. A positive change is in relation to the maps as farmers will no longer need to submit EFA maps with their Single Application Form but must retain them for inspection purposes.

Changes to current options: Fallow

Fallow must now either be a diverse mix of temporary grassland, wildflower mix, wild bird seed mix or a soil conditioning crop.

Field Margins

The minimum width of margins has been increased from 1 metre to 3 metres. The same rules apply for classifications of margins, apart from 1 and 2 metre margins are no longer eligible to claim under EFA. Good Agricultural and Environmental Condition (GAEC) rules still apply. Where a new margin comprising a grass sward is to be created, it must be a diverse grass sward containing pollenbearing plants.

Catch Crop

The number of crop types that can be under sown has been expanded to include oilseed rape and maize as well as cereals. You can now use spottreatment to control injurious weeds and invasive weeds with herbicide postharvest.

There are new eligible crops which include alsike clover, berseem clover, red clover, sweet clover and fenugreek. The crop can now be harvested before 1 August. The crop must have a minimum of 3 metres claimed EFA margin around the field. You are now allowed to apply herbicide and fungicides.

The main EFA claimed nitrogen-fixing crop must be less than or equal to 75% of the total area of EFA claimed as nitrogen-fixing crops. You must sow either a single stand or mix of legumes ensuring that the nitrogen-fixing crop species are predominant by weight of seed if other crops are mixed with one or both of the EFA nitrogen-fixing crops. The predominant nitrogen-fixing crop (for each claimed EFA NitrogenFixing Crop area) should be declared as the Land use on your Single Application Form.

EFA Hedges

The definition of a hedge has changed. Previously any gap of up to 20 metres could be claimed. This has been reduced to 5 metres to encourage replanting.

The dates for cutting hedges have also changed. If claiming hedges for EFA, you now cannot trim them between 1 March and 1 December, except for road safety reasons or when establishing a winter crop.

Implications for Farmers

These changes will affect approximately 2,300 additional businesses, particularly larger grass-based livestock units with over 15 hectares of arable land. The introduction of new EFA options provides farmers with more flexibility to meet environmental requirements. However, the removal of exemptions means that more farms will need to engage with greening measures.

Conclusion

On top of conditionality requirements, the new greening measures will result in much greater change and workload for Scottish farmers. Those who grew small areas of barley for home saved feed will be impacted as will those who have forage crop policies.

If you wish to discuss some of these points please contact your local Galbraith office. n

Full Circle for Flexible Flax

East Scotland was once the centre of the world’s linen trade, with flax grown as a commercial crop in Tayside, Fife and parts of Perthshire for hundreds of years.

Callum Woods

07766 250 796 callum.woods@galbraithgroup.com

In Cupar, as many as 30 mills were present along the course of the River Eden. These were initially designed for milling cereals but from around the turn of the 19th Century, flax spinning was the focus of nearly a third of the mills. In 1867, one Cupar mill alone employed over 100 people.

Production ground to a halt in the 1950’s as more profitable crops were favoured and due to the import of cheaper man-made fibres used for clothing. Whilst flax has still been grown in the UK, it has been the shorter stemmed varieties with a focus on seed production, sold as linseed or flaxseed.

Today there are signs that flax is re-emerging as a commercial crop. In light of the demand for low

carbon alternative fabrics, The Edinburgh College of Art recently began trials researching and experimenting with flax varieties for textile production. A number of farmers throughout the region are now starting to grow fibre flax commercially. Whilst the original Scottish varieties have been lost, alternatives have been grown elsewhere and it is these varieties, particularly ones that do well in temperate climates and wet soils, that have been trialled and are now growing in Scotland.

The demand for sustainable textiles could boost the appeal of flax for farming enterprises looking to diversify and create another income stream, whether this is growing flax on one’s own land or letting land out to others. In addition, there are

soil health and environmental benefits as flax is an ideal break crop with low nitrogen needs, generally being used rotationally once every seven years, helping to maintain soil quality, prevent disease and increase the yield of the following crop. Flax may be a good option for those considering regenerative farming or aiming to boost biodiversity, as pollinators are attracted to the flowers.

Flax has an interesting ten-stage cultivation process from the initial sowing, to pulling (as opposed to cutting) to ‘retting’ (allowing the fibres to be broken down), spinning, weaving and sewing. More information on this process and flax in general, can be found at allianceflaxlinenhemp.eu n

THE PURPOSE AND BENEFITS OF ESTATE AND FARM REVIEWS

Estate and farm reviews are an essential tool for agricultural development and sustainability in Scotland. These reviews are conducted to assess and improve farm management practices, focusing on environmental, economic, and social factors.

The purpose of the review is to ensure that farming practices align with best practice and changing agricultural policies while supporting profitability and potential growth.

Estate and farm reviews are typically carried out by advisory services, or independent consultants. They offer landowners and farmers an opportunity to review their operations, identify areas for improvement, and receive expert advice tailored to their unique needs. These reviews often focus on aspects like soil health, crop rotation, livestock management, resource use, building use, and compliance with environmental regulations.

One of the main benefits of estate or farm reviews is the opportunity for farmers to adjust their operations for sustainability. With growing concerns over livestock profitability, climate change, biodiversity loss, and soil degradation, farm reviews provide a framework for implementing best practices. Landowners and farmers can reduce their carbon footprint, enhance biodiversity, and

manage natural resources more effectively, contributing to the overall health of Scotland’s rural landscapes.

Estate or farm reviews also offer significant economic benefits. By identifying inefficiencies or underperforming areas within a farm, these assessments help farmers increase productivity and profitability. Landowners and farmers can gain insight into cost-effective methods of operation, reducing waste, and improving the quality of their products. Additionally, following recommended practices may help secure subsidies and grants, further enhancing financial stability.

In conclusion, estate and farm reviews are vital for ensuring agricultural practices are sustainable, efficient, and resilient. They provide landowners and farmers with the tools and support needed to thrive in a challenging and changing landscape, while also developing a more sustainable agricultural future. n

Calum Smith

01292 268 181 calum.smith@galbraithgroup.com

One of the main benefits of estate or farm reviews is the opportunity for farmers to adjust their operations for sustainability.

Calum Smith

Agri Market Update

Sheep Market update

Supply

As we progress through the second quarter of 2025, the UK lamb market is experiencing a complex interplay of supply, demand, and international trade factors that are shaping pricing and production trends.

A high carryover of 2024 lambs into the 2025 season has contributed to a 2% increase in slaughter numbers compared to the prior year, albeit with suppressed prices for lamb. The high carry over can be attributed to a number of factors including poorer weather, which in turn had a knock-on effect on lambing and grass growth, leading to later sales of lambs.

The outlook for the 2025/26 lamb crop is less optimistic and is predicted to decline 2% on the previous year due to a reduction in the female breeding flock, which has been reducing steadily yearon-year according to analysis from the Agriculture and Horticulture Development Board. DEFRA published data shows that the number of breeding females decreased 5% to 13.1 million from December 2023 to 2024.

Reductions may be linked to rising costs of feed, escalating input costs, labour shortages and a general decline in the breeding hill flock, driven by competing land use priorities that favour biodiversity and climate change initiatives as opposed to food security.

Demand

The timing of religious events, including Ramadan and Easter in 2025, has resulted in a more staggered pattern of demand for lamb compared to the previous year. In 2024, Easter took place on the 31st March and overlapped with Ramadan, which ran from March 10th to April 9th, creating a highly concentrated period of consumer demand. In contrast, in 2025, Easter occurred on April 20th, while Ramadan spanned from February 28th to March 29th, introducing a gap of three weeks between the two events. This separation has contributed to a more gradual and less intensified demand cycle for lamb this spring.

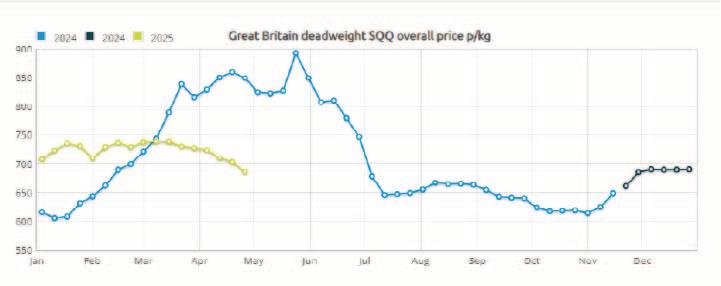

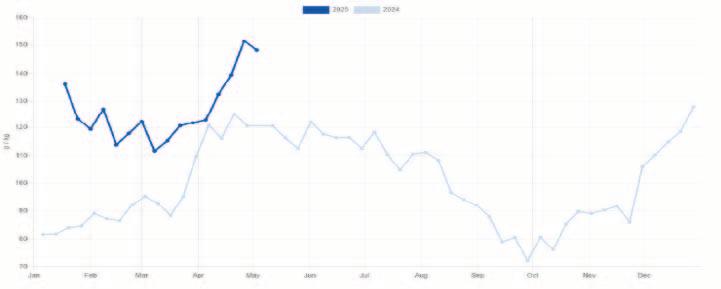

Prices

As we reflect on the previous year, when deadweight prices soared to highs of £8.49/kg in the week ending 27/04/2024, the 2025 period has been somewhat disappointing, with recorded deadweight price at £6.86/kg in the week ending 26/04/2025, showing a steady decrease. Despite this, the recorded price continues to sit above the five-year average. Consumer demand has also tailed off, with data from Kantar showing the year-on-year spend for lamb is down 12.7%.

On the other hand, the weekly average Scottish Ewe and Ram price is up significantly from the previous year by £2.75/kg. Feeding ewes sold for up to £300/head at United Auctions, Stirling in the week ending 02/05/2025.

Global Market

With the introduction of tariffs by President Trump on the 5th April, we now await the potential implications for UK farmers. Australia, which supplies nearly 80% of lamb imported into the United States, alongside New Zealand, now faces a tariff of 10% on exports to the US. These measures are expected to increase costs for consumers, potentially wavering demand for the product. However, current data indicates that

Australian lamb trading at £4.03/kg and New Zealand lamb at £3.70/kg, both remaining at significantly lower than UK lamb at £6.86/kg, Spanish at £7.68/kg and French lamb at £9.29/kg. Therefore, the impact is expected to be minimal. Overall, the market remains in a state of cautious adjustment, with producers needing to stay responsive to both domestic and international developments. n

It has been reported that an unprecedented beef trade continues, with finished prices surpassing £7/kg for the first time. It should be noted that currently the market is still witnessing that the demand for beef is outstripped by supply.

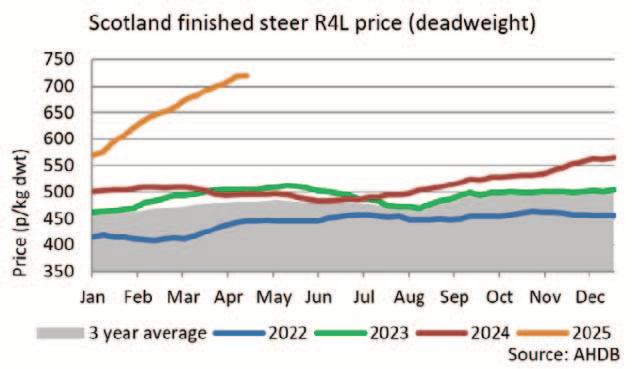

Looking closely at the change in price in regards to deadweight beef prices, it has been recorded that at the start of April 2025 finished deadweight prices were sitting around 705p/kg in comparison to November 2024 where prices averaged at 516p/kg, outlining the demand within the beef market.

Since the beginning of 2025 beef prices have risen by 25% with prices continuing on the upward trend. It has

been noted by the Farm Advisory Service that consumer demand remains high for beef, locked with a shortage of beef cattle which is leading to surges in price as processors work hard to secure supplies. It has been projected that prices are likely to remain stable, and perhaps may start to level out over time as young bulls are being brought forward to help fill in the gap of cattle availability. Albeit it is predominantly consumer demand which will remain the main drive behind the price of beef.

Using a Finished Steer which has been Graded as a R4L, Farm Advisory Service have produced an effective graph highlighting the difference in the beef prices for the same grade of beef over the last 4 years.

Focusing on the cull cow trade it has been acknowledged that it continued to exceed current expectations, it has been assumed that this has been driven by the UK demand for producing beef. It was recorded that in April cull cow prices were sitting at 593p/kg/dwt +14p which was nearly 200p/kg more than the prices which were shown in April 2024. This market is predominantly supported through the summer season linking to BBQ weather and consumer habits creating a higher demand for products.

Quality Meat Scotland has suggested that Scottish Cattle Supplies are likely to tighten further in the second half of 2025. The British Cattle Movement Service has stated that this has been an effect of older cattle having been reduced and culled on a more regular

basis resulting in smaller crops of calves through 2023 and 2024 being fed into the market, reducing the upcoming supply of beef to slaughter towards the end of 2025. Overall in the long term with declined herd numbers throughout recent years which is just starting to reach the reduction in production and slaughter, this is starting to raise concern. If herd numbers continue to decline this will result in a reduced supply which will not be able to support the ever growing demand for these products, whether this be both UK or globally.

Looking at the beef market as a whole, key points to take away are that beef prices have hit a record high, which has been benefitting many producers who are receiving a premium for their products. This has predominantly been

Looking at the beef market as a whole, key points to take away are that beef prices have hit a record high, which has been benefitting many producers who are receiving a premium for their products.

driven by the increase in demand, along with a reduction in the supply available, which has subsequently driven competition helping to increase the overall price growth. Although it should be noted that caution may be required to ensure that the UK Beef market does not reach a stage where there becomes a beef shortage and that they are unable to feed the ever growing demand which is being driven by an increasing population along with consumer habits and seasonality demands. n Olivia Smith

01786 434 600

olivia.smith@galbraithgroup.com

Cereals Market update

The market for cereal crops in the UK has remained relatively subdued following the harvest of 2024 and going into 2025. Despite localised production shortages, prices for feed cereals have remained depressed over the last 12 months primarily driven by a global oversupply of wheat in the year of 2024.

Other factors such as stable global yield forecasts for 2025 and a stronger Great British Pound have contributed to the reduced competitiveness of UK cereals in the global marketplace. The stronger pound has therefore made importing wheat more favorable which is reflected by the future Agriculture and Horticulture Development Board forecasts showing an increase in wheat imports to the UK of 13% in 2025 compared to the previous year.

Despite the downturn of the cereals market, the market for oilseed rape (OSR) has remained relatively strong over the last few months by comparison. This resilience may be due to a weak local UK supply where OSR production fell by 32% to 824,000 tonnes in 2024 – the lowest level of production since 1983. The decline has been caused by a reduction in both area planted and crop yields. This downward trend has continued into 2025 with an estimated fall of a further 17% in planted area.

The reduction of OSR production may be due to several factors including the roll out of the sustainable farming incentive (SFI) in 2022 in England. Under the scheme, many farmers chose to grow approved SFI crops such as wildflower seed mixes to provide a reliable source of income that is not dependent on the yield or performance of the crop. This may therefore explain why crops such as OSR were grown less frequently for the duration of the scheme as they carry a greater risk of failure than other more robust arable crops such as wheat, barley or oats and were therefore replaced by lower risk SFI alternatives.

Additional contributing factors may include the adverse weather and pest pressures experienced by parts of the UK over the last few years, resulting in disappointing OSR yields and poorer margins. These challenges may have discouraged growers, increasing the appeal of subsidising an OSR crop with crops that are eligible for the SFI subsidies, therefore offering a more stable income within the rotation.

In 2025 the cereals market in the UK remains under pressure from global oversupplies and reduced export competitiveness due to the strengthening of the pound which has boosted foreign imports. In contrast, the market for oilseed rape has been more resilient to global factors due to low domestic supplies influenced by poor yields in recent years and subsidised, lower risk alternatives becoming widely available through the sustainable farming incentive scheme. n

John Rodwell

01224 860 710

john.rodwell@galbraithgroup.com

Dairy Market update

The UK dairy sector entered spring 2025 on relatively stable ground, with farmgate milk prices holding steady. In March 2025, the average UK farmgate milk price was recorded at 46.01 pence per litre (ppl), a decrease of 0.08ppl compared to February (Agriculture and Horticulture Development Board). Nevertheless, this remains 18% higher than the same period in 2024, reflecting sustained year-on-year strength. Major processors, including Müller and First Milk, announced they were holding current pricing into May, with First Milk confirming a continued rate of 45.35ppl from 1st May. It’s important to note that this figure represents the standard litre price which is based on milk containing 4.2% butterfat, 3.4% protein, and volumes exceeding one million litres annually. In practice, many producers fall short of these specifications, which can result in lower prices being paid. Favourable spring weather encouraged early grass growth and resulted in increased milk yields. However, unusually dry conditions in March and April, particularly in eastern regions, presented operational challenges for some producers.

According to AHDB the contraction of herd sizes is ongoing. As of January 2025, the GB milking herd had fallen to 1.62 million head, representing the lowest January figure on record and a 0.9% decline from the previous year. The average age of milking cows remains at 4.51 years, continuing the industry trend toward younger herds. Elevated beef prices have continued to encourage producers to cull older cows more aggressively.

Beyond production and price, milk contracts continue to be a point of concern, particularly for buyers interested in acquiring or developing new dairy units. Many milk purchasers remain hesitant to offer contracts in areas not already on established collection routes, due to the currently steady supply of milk. This trend could have significant implications for the future value of dairy units, especially where processing infrastructure may be redundant without a viable milk contract. It raises broader concerns about the economic sustainability of dairy farming in less-connected regions. The push toward regenerative agriculture and sustainable practices is gaining traction, with some milk buyers

offering small incentives for participating. However, this often requires upfront investment, something not all producers can easily afford. The capital intensity of dairy farming and succession challenges remain a significant barrier to long-term planning. As a result, technology and automation are playing an increasingly vital role in maintaining viability. Innovative practices, precision farming tools and labour-saving systems are likely to define the future of efficient and resilient dairy businesses. n

Christina Smith 01292 268 181

christina.smith@galbraithgroup.com

The push toward regenerative agriculture and sustainable practices is gaining traction, with some milk buyers offering small incentives for participating.

Christina Smith

Where community, culture, food production & conservation come together

Rose Nash

01556 505 346

rose.nash@galbraithgroup.com

Caerlaverock Estate is a beautiful and tranquil hidden gem on the shores of the Solway Firth in South West Scotland.

Surrounded by stunning scenery, the Estate features a fairy-tale medieval castle, ancient woodland, a coastal national nature reserve, a wetland reserve, and a 1,000-acre livestock and arable home farm with a herd of Belted Galloway cattle. It also includes several longestablished tenanted farms and a range of properties available as holiday lets or long-term rentals.

Owned by the same family for over 800 years, Caerlaverock has long prioritised community partnerships, environmental stewardship, and cultural heritage. Galbraith supports the Estate with property maintenance, tenancy management, and financial services.

In 2017, Lady Clare Kerr, heir to the title Lady Herries of Terregles, assumed leadership of the Estate. Since then, she has launched The Boathouse Glencaple—an awardwinning restaurant and shop on the village quayside—and introduced new holiday accommodation, including Erriff, a luxury fourbedroom townhouse, and two eco-cabins: The Curve and The Treehouse.

Rose Nash of Galbraith’s rural team in Castle Douglas spoke with Anna Austin, Estate Manager at Caerlaverock, about how the diversified estate successfully balances commercial activity with conservation, community, and sustainability.

How would you say the estate has changed over the past 10 years?

There has always been a strong conservation focus, but over the past decade this has expanded to include climate change adaptation. Wildlife remains a priority, but now

we’re also designing habitats with future risks—like sea level rise, flooding, and drought—in mind.

Our farming has evolved too. We’re concentrating more on soil health for long-term productivity, while also maintaining efficiency.

The rising cost of heating has led tenants to focus more on energy efficiency. Where possible, we’ve added insulation during refurbishments and support tenantled improvements where appropriate.

We’ve shifted from a reactive to a proactive maintenance approach, with an annual programme. While more expensive upfront, it reduces long-term risk and improves predictability.

Creating an in-house Estate Office has brought us closer to suppliers and tenants. This hands-on approach improves management and has helped streamline systems and processes.

The Boathouse and our holiday lets are part of a broader diversification strategy—something we intend to expand on.

What advice would you give other estate owners or managers looking to diversify?

Cost everything out in detail from the beginning. Carefully assess whether your idea is commercially viable. It’s easy to invest in something that ultimately loses money.

Align any new venture with your Estate’s values and strengths. Caerlaverock’s obvious USPs are farming, nature, and heritage. Other estates need to identify and champion what makes them special. A clear understanding of your land’s characteristics is invaluable when planning and helps avoid missteps.

“The vision for the estate is really about the promotion of the whole Caerlaverock area as a sustainable and high quality place to live and visit.”

What’s your vision for the Estate since becoming Estate Manager in 2023?

Clare and I share a vision of promoting Caerlaverock as a sustainable, high-quality place to live and visit. That encompasses everything from future-proof farming and environmental projects to quality tourism and housing, working with partners like NatureScot, Historic Environment Scotland, and the Wildfowl and Wetlands Trust—and bringing the local community along with us.

How do you see the role of estate factor evolving?

Estate factors must now be adaptable, juggling a wide range of responsibilities. Understanding how each business stream contributes to estate-wide goals is crucial—more so than being a deep expert in just one area.

You must stay informed about grants and funding changes, as these create opportunities for diversification.

Factors should also work collaboratively with tenants. Renting from an estate should offer added value. I believe in creating collective benefits that individuals couldn’t achieve alone.

For example, we’re designing a 5,000-acre biodiversity project with tenants and neighbours. The Estate takes on the admin burden, but the benefits—ecological, agricultural, and community— are shared.

How does your hybrid model—retaining a factor and working with Galbraith—benefit the Estate?

Having an in-house presence improves visibility and strengthens relationships, but we can’t employ all the expertise we need internally. Our partnership with Galbraith fills that gap efficiently.

We benefit from Galbraith’s expertise in tenancies, agriculture, land management, and finance. Tools like Re-Leased help with property maintenance and tenancy tracking—accessible and easy to use.

Using Galbraith’s remote finance team is more costeffective than hiring our own, and we gain access to their network of finance and IT specialists. This structure makes our team more robust—holidays are covered, and crises can be managed effectively.

Has TV filming boosted the Estate’s visibility?

Definitely. George Clarke’s Amazing Spaces featured The Treehouse, which raised awareness and increased bookings. More recently, Scotland’s Greatest Escapes and an episode of Netflix’s Love Is Blind were filmed here.

Filming has been minimally disruptive and enjoyable for the team. It’s also a great way to showcase our work.

How has your in-hand farming adapted to subsidy changes?

We’re trying to anticipate where Scottish agricultural policy is heading. Our ethos aligns with the push for conservation, so we’ve pursued projects supported by the Nature Restoration Fund—like creating ponds, wildlife corridors, and meadows on less productive land. These efforts enhance habitat and coastal resilience while maintaining grazing. The corridors offer shelter for livestock and wildlife movement.

We hope these efforts will eventually qualify for future subsidies, but even now, they support ecosystem health, soil quality, and may reduce long-term costs.

Importantly, we’ve achieved all this without significant loss of production, and are now working on a largerscale project for 2026 with tenants and neighbours.

What makes managing an estate in southwest Scotland special?

The Solway coast is a hidden gem. Its scenery, tranquillity, and light make it a magical place.

Organisations like the South of Scotland Destination Alliance are promoting the area for sustainable tourism and nature-based investment.

Being recognised as the Natural Capital Innovation Zone adds momentum to conservation and climate resilience efforts. It’s an exciting time to be here.

How have you used community engagement to benefit both the Estate and local people?

We have long-standing relationships with local organisations, like the Caerlaverock Community Association. The Castle Corner Campsite runs on an honesty-box model, with proceeds supporting local projects.

Our partnerships extend to Historic Environment Scotland (Caerlaverock Castle), the Wildfowl & Wetlands Trust, and NatureScot. The estate’s coastline is grazed by our Belted Galloways as part of a national nature reserve.

We also maintain walking paths linking the Estate’s key heritage and nature sites and promote local suppliers through The Boathouse shop. These collaborations enhance the whole area’s resilience and appeal. Galbraith’s work with Caerlaverock Estate highlights the breadth of rural services we offer. To find out more, contact your local Galbraith office. n

“The addition of The Boathouse restaurant, which can also be hired for weddings and events, and the creation of the holiday lets over the last 10 years has been the culmination of an ongoing strategy of diversification.”

THE EVOLUTION OF SCOTTISH FARMING & GOVERNMENT SUBSIDIES

1960s to Present Day

Scottish agriculture has changed dramatically over the past 60 plus years, shaped by global events, local innovation, and evolving government support. From the post-war production of the 1960s to today’s digitally driven farms, we look to explore some of the key milestones, challenges and policies that have defined farming life in Scotland across each decade.

Martin Rennie

Martin Rennie is an agricultural consultant who works from the Perth office. Martin grew up on a livestock farm in Fife and currently owns small flock of ewes whilst still getting his hands dirty when he can. Working as a consultant for around 13 years has led him to experience a change in the farming sector, even in this short time, from changing subsidies to the continued fluctuation of commodity prices throughout the period.

Beth Dandie

Beth joined Galbraith in 2022 after graduating with a Master’s degree in Land Economy. She grew up involved in her grandfather’s mixed farm, Heatherstacks, in Forfar, where she enjoyed working with livestock. Over the years, the farm has evolved from rearing store cattle and store sheep to a commercial flock of sheep and a bed-and-breakfast pig enterprise.

Senga Barron

Senga is a graduate rural surveyor based in the Perth office, she has a background in agriculture, being brought up on the family farm Findowrie, in Angus. The Barron family originally farmed in both Perthshire and Angus before moving to Findowrie in the 1970’s - the predominant farming systems across these farms at the time was in dairy, potatoes, cereals and berries.

1960s: The Post-War Boom

Following World War II, there was a push for national food security, leading to a boom in farming output and optimism - the war had only outlined the vulnerability of Britain’s food supply. Farms were still largely dependent on traditional practices and a strong labour workforce, with families and seasonal workers forming the backbone of operations.

During this time, the UK joined the Common Agricultural Policy (CAP) framework, laying the foundation for the subsidy systems which would dominate the decades to come. These early subsidies aimed to boost production, ensure stable food supplies and support farmers' incomes.

More locally, Forfar Market was established in 1967 and quickly became a key hub for livestock trading, serving many farms in the surrounding area. During the 1960s and 1970s, large numbers of highquality prime cattle and sheep were sold through the market, reflecting the significant growth in herd and flock sizes during that period.

Following the war, at Findowrie in Angus, my Great-Grandfather had identified that produce was slow to move off the farm and therefore decided to start a milk-round to move produce more quickly. -Senga Heatherstacks Farm made use of rented grazing land throughout the Forfar area. Fat cattle were often walked considerable distancesincluding from Guthrie, near Friockheim into Forfar to be sold at the local fat cattle sale, highlighting both the scale of operations and the central role the market played in the local agricultural economy. -Beth

Prior to moving to Fife the Rennie family were based in West Lothian where the prominent element of the business was dairy. Implementing a new parlour was a key step for the family during this period moving from the Byre to the new parlour. Being in the central belt for both sides of the family made it ideal in terms of the milk round and access to local communities. Farms were small but the number of staff and the sense of community was profound in this decade. -Martin

1970s: The Economic Boom and Growing European Integration

Scotland's entry into the European Economic Community (EEC) in 1973 marked a pivotal moment for agriculture. The Common Agricultural Policy (CAP) introduced by the EEC provided direct subsidies to farmers, leading to increased financial support. By 1979, direct income support to Scottish

livestock producers amounted to approximately £24 million, nearly doubling by 1981 to £47 million. Farmers were paid per livestock animal held, rather than hectares farmed. This had an influential impact on the rapid increase of livestock units across the country. The 1970s saw a continued push for productivity, but also brought new stories of diversification. Many farms, like Heatherstacks in Forfar undertook soft fruit farming and had their berries picked by locals, well before the introduction of tunnels. A berry bus would run from one side of Forfar to the other and then on to Dundee to gather as many willing people as possible to pick the berries. Punnets were tied round picker’s waists either onto their belt or school tie. Each pound punnet was paid at 2.5pence in cash and at the end of the day. Strawberries were picked on the ground where straw would be in between the plants to separate the runners and to increase production. Raspberrys were picked off raspberry canes, with no tunnels on either of the fruit, the natural sun ripened the soft fruits. -Beth

The 1970’s saw a wave of prosperity for the potato industry, strong international demand for high quality Scottish seed-potatoes, disease outbreaks across Europe, favourable weather conditions and crop failures in other countries led to high prices across the north-east of Scotland. This sudden boom saw an increase of farmers jump on the tattie bandwagon and soon supply began to outweigh the demand. By the late 1970’s, and into the early 1980’s, the demand had cooled, nonetheless this wave left its legacy, leaving a more modernised seed potato sector enhancing the global reputation of Scottish seed potatoes. Throughout this period, traditional methods of harvesting were prevalent and the ‘tattie holidays’ allowed local children to assist in the field, practises as such continued into the 80’s until mechanisation reduced the demand for such tasks.

Throughout this period, in the mid 1970’s land values began to steady, with a combination of rising interest rates and inflation this pushed rising values down, allowing many tenant farmers the opportunity to purchase land. Prior to this a surge in values were noted with the average price of land increasing from £501 to £1,557 per acre during the years 1970 to 1973, largely attributed to rising wheat prices. In 1975, the Barron family chose to sell Blackruthven Farm as the opportunity to purchase Findowrie,

arose, which the family had been tenants on, this marking a historic moment for the family.-Senga

For the Rennie Family, being based in West Lothian growing potatoes and moving to soft fruit tunnels were unfortunately not achievable in the area, although there were a few families who tried but shall remain nameless! The main objectives in this period were the expansion of the herd and great grandfather raising his prized ewe lambs. -Martin

1980s: Butter Mountains and Milk Quotas

The 1980s saw a continued emphasis on intensifying agricultural production. In 1985 to 1986, direct financial assistance to Scottish farmers reached approximately £106 million, up from £73 million in 1978 to 1979. The government also invested in agricultural research and development, allocating approximately £50 million annually. However, concerns over environmental impacts and overproduction led to policy reforms aimed at balancing productivity with sustainability.

This decade symbolised both excess and adjustment. “butter mountains” and “milk lakes” became infamous symbols of the CAP’s overproduction problem. Farmers were producing more than markets could handle, leading to waste and distorted prices. In response, milk quotas were introduced in 1984 to curb surplus. Quotas completely upended operations overnight, forcing farms to rethink herd sizes and production strategies.

The year 1985 cannot go unmentioned. It’s countless the farmers of a certain generation who mention this year. For the Rennie family, making silage was a real struggle and a trailed chopper was making plenty black marks. -Martin

1990s – BSE, CAP Reform

One of the most significant events in the 1990’s for the sector was the outbreak of Bovine Spongiform Encephalopathy (BSE), commonly referred to as ‘mad cow disease’. First, identified in the late 1980’s, BSE reached its peak by the 1990’s. With concerns rising over its link to a human variant vCJD caused by consuming contaminated meat. By 1992/1993 there were around 100,000 confirmed cases, prompting the culling of millions of cattle. Measures to control the disease, such as banning animal byproducts in cattle feed were introduced. However, widespread consumer fear led to a dramatic decline in both domestic and international beef demand, and

“The highly contagious nature of the disease led to the government implemented strategy of widespread culling of livestock as attempts were made to prevent further transmission.”

many EU countries, imposed import bans, severely impacting farmers’ income.

In the 1990s, the Common Agricultural Policy (CAP) underwent significant reforms aimed at reducing market distortions and aligning agriculture more with market forces in response to events in the 1980s. The 1992 reforms, often referred to as the ‘Macsharry reforms’ introduced direct income payments to farmers and reduced price supports for key commodities such as cereals and beef. The reforms implemented the set-aside scheme in a bid to reduce overproduction and promote environmental sustainability. These changes marked a shift toward a more market orientated policy. For many, the policy remained controversial and provided financial challenges forcing farmers to think more sustainably regarding their farming practises.

The Rennie’s dairy herd was sold in this decade as the business moved towards a beef/sheep operation only. Changing dynamics and objectives were the incentive for change but often there was a thought to go backwards towards the dairy herd. 1999 saw the family make the move to supposedly sunny

Fife. The move was a big change which brought about challenges but also many positives. Farm size was in general much larger during this period and the ground had the ability to winter cows outside for a longer period of time. Although we soon learnt the Gaelic name for Clatto was a ‘a place of ditch or ditches’ and this proved the case after the weather changes in the 2000’s. -Martin

2000’s – Foot and Mouth

2001 saw a devastating outbreak of foot-and-mouth disease in the UK, one of the most severe crises in agricultural history. The first case of the disease was discovered in Essex in the February of 2001, and whilst swift attempts were made to contain the disease, shortly after, cases were discovered in Cornwall and Scotland. The highly contagious nature of the disease led to the government implemented strategy of widespread culling of livestock as attempts were made to prevent further transmission.

The toll that this outbreak had on the mental health of farmers in the UK was unimaginable. Many will recall the distressing images of mass pyres and carcasses in a desperate attempt to contain the disease,

symbolising not only the scale of the crisis but the emotional toll on rural communities. In addition to the emotional strain the disease had, livestock markets and trading came to a halt, as fears of spreading the disease rose within the country. Furthermore, export markets were severely disrupted as international buyers halted imports from the UK. Thus, leading to financial difficulties for those unable to sell produce, which left many struggling to continue in the aftermath of the disease.

2001 marked a historic moment, the cancellation of the Royal Highland Show, an event renowned across the sector attracting more than 150,000 attendees. The cancellation of the event marked a historic moment, being the first time, the show had been cancelled since World War II, underscoring the unprecedented disruption caused by the epidemic. At Findowrie, we were fortunate that the farm had not fallen susceptible to the devastating impacts of the disease, it was noted as a period of stand-still in the farming sector at the time. Stringent precautions were taken on farm to ensure any vehicle or personnel entering and exiting was sanitised, many of the agricultural shows were cancelled or held with no livestock. -Senga