Increased use of AI and machine learning are driving demand for data centres.

Communications Code complexity

Rules create problems for landowners and risks spreading mobile ‘not-spots’.

Net zero electricity plan could risk lives

Report on plans for a 70-mile electricity modernisation project to meet net zero targets.

Hydro - An asset in high demand

Renewable assets which have outstanding eligibility for the government’s Feed in Tariff.

Welcome to our thirtieth issue of Energy Matters

Our readers, including many clients and partners, tell us we should be proud to produce a magazine of such consistent quality over the years, and indeed we are.

But we must thank them, along with our professional and marketing teams, for their hard work and dedication in maintaining those standards since the first issue in 2012.

We’ve seen a lot of changes – the growth in renewable technologies such as wind, hydro, solar and battery storage; subsidy schemes that have come and gone as well as other schemes that are still operational but are facing challenges for the transition away from that support; such as single wind turbines under the Feed in Tariff (FIT) and biomass heating systems under the Renewable Heat Incentive (RHI). We have also seen the spread of pylons and masts to serve grid electrification and the digital boom.

We covered everything from the farming family who set up a co-op so their wind-power project could let local people participate, to the massive MeyGen tidal project and North Sea decommissioning.

The pages of issue 6 in 2014 EM saw a lively debate between top ministers in the SNP Scottish Government and the Lib-Dem coalition UK administration. Taking our future-watch brief to heart, in 2018 we explored how farming might function in a postdiesel world.

In 2021 we reported on how the bigger blades powering wind energy would soon stand taller than the 683ft high Queensferry Crossing over the River Forth.

In issue 29 we called for a rethink on Shared Rural Network mobile rollout and reported on biosecurity fears for farming land along the new highvoltage overhead cable route along the east coast of Scotland.

See our content page opposite for the engaging stories we carry in this issue.

Rethinking energy

The importance of a safe, reliable energy supply to the UK economy and the health and welfare of its people is increasingly apparent.

For a time, setting a date on net zero greenhouse gas emissions by decarbonising industry, transport and lifestyles looked the best way to tackle what some experts call the existential threat of climate change.

But we didn’t stop consuming oil or gas and so, when Russia invaded Ukraine, world commodity markets soared along with energy prices. While events have strained net zero commitments around the globe, Britain has held out, using law, regulation and subsidy to prioritise green power over fossil fuels.

It’s one thing to encourage innovation in and widespread adoption of renewable energy to bring a better world; quite another to demonise more traditional sources of energy, or pretend they don’t have an important part to play in the UK economy, nor will for many years to come.

The energy transition has been happening for centuries. As the oil historian Daniel Yergin wrote in The Times, Abraham Darby, a metal worker specialising in cast-iron pots, realised in 1709 coal was ‘a more effective means of iron production’ than wood.

Then in 1765, James Watt transformed the steam engine, sparking the Industrial Revolution that heralded Britain’s industrial dominance. It took until the start of the 20th century for coal to overtake wood as the world’s primary energy source. Spurred by the transport revolution, oil took the top spot only in the 1960s.

The Aberdeen-based offshore industry pioneered a visionary outlook in the 1970s by taking up the so-called Houston Effect. This highlighted the Texas oil centre as a model for transferring the knowledge and skills of an entire industry and applying them to generate innovation and wealth in the post-oil era.

In May this year Orsted, the proposed developer of the Hornsea 4 windfarm expansion off the Yorkshire coast, announced it had discontinued the North Sea project, designed to add 2,400 MW of peak capacity – enough to power 2.6 million homes. The Danish company blamed a surge in challenges including higher costs.

Orsted’s move casts doubt over whether the Government’s ‘contracts for difference’ subsidy scheme, designed to promote investment in renewable energy projects, is working effectively or should be reformed. Last year Orsted secured funding for both Hornsea 3 and Hornsea 4 under the CfD system.

I remain confident in the UK’s ability to transition to cleaner, greener energy sources but it’s important to see the process as building on what we have, alongside many other measures we must also take, such as investing in decarbonisation technologies, improving energy efficiency and discouraging waste. History has taught us that the transition to different energy sources isn’t a quick process and the UK must be prepared to manage that transition effectively rather than abandoning any viable energy source before we have a reliable replacement. n

Mike Reid 07909 978 642 mike.reid@galbraithgroup.com

Galbraith is a leading independent property consultancy. Drawing on a century of experience in land and property management the firm is progressive and dynamic employing over 200 people in offices throughout Scotland and the North of England. We provide a full range of property consulting services across the commercial, residential, rural and energy sectors. Galbraith provides a personal service, listening to clients and delivering advice to suit their particular opportunities and circumstances.

Great idea but... we look at how the Communications Code is working out.

6

Exciting wind farm investment comes to market in southwest.

7

Electricity pricingdue for a shake-up?

9

Gridlock - Green project rush puts strain in network infrastructure.

New rules to boost onshore wind south of the Border. 14

AI powerdevelopers on hunt for land for data centres.

Sky-highturbine blades get ever bigger.

16

Hold the phonemast rents down but values rise.

18

Development proposals for sensitive areas must address peatland. 21

20

Hydro - An asset in high demand.

Government rethink on Shared Rural Network.

22

Hydro developments set to stretch local infrastructure.

24 Current sources of Renewable funding.

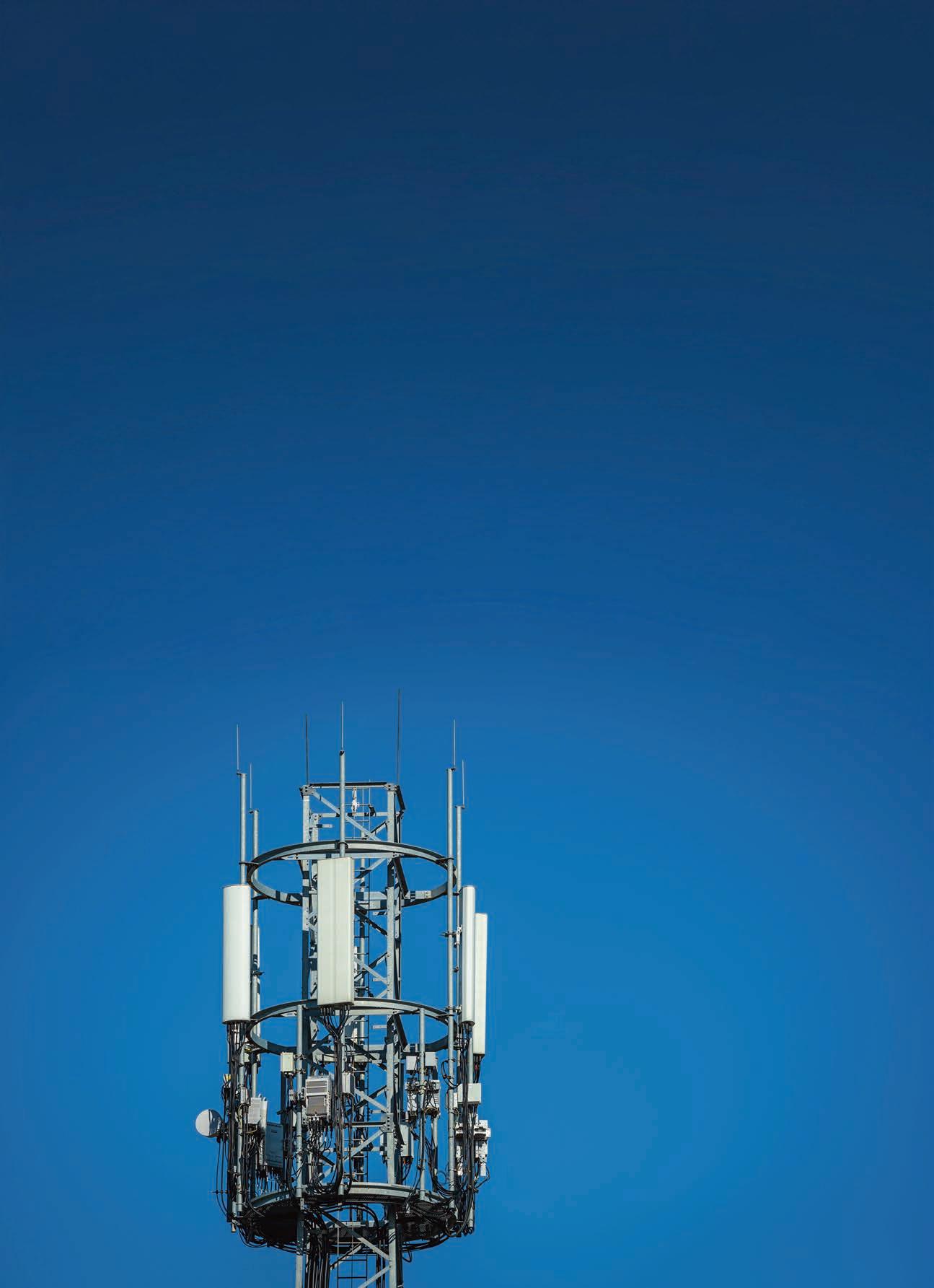

Rules designed to boost digital access risk creating areas of unreliable coverage and disrupting the property market. Low returns are prompting landowners to withdraw property from use by phone network infrastructure providers, potentially widening mobile not-spots in urban areas. Mobile phone networks and their customers rely on sophisticated equipment located on buildings and masts to transmit voice and data around the UK and internationally. For years, rent levels paid to landlords to host this infrastructure was determined by

the market; a rough guide being £20,000 – 30,000 a year in London and £15,000 outside. That changed in 2017 with the introduction of Electronic Communications Code, which aimed to widen public access to digital networks by easing the process by which operators instal, maintain and upgrade their equipment on public and private land. As well as conferring new rights on infrastructure providers, the Code effectively introduced rent controls. Operators now offer up to £5,000 for antennae of rooftops.

FRUSTRATION

Explanations for Britain’s poor mobile phone service include tough planning rules, low investment levels and the forced removal of Huawei equipment from the network. But a more compelling factor is the way the Code limits available property for hosting kit, according to Ian Thornton-Kemsley, a recognised expert on the property aspects of telecommunications who is consultant at the independent property adviser Galbraith.

Communications Code COMPLEXITY

Rules create problems for landowners and risks spreading mobile ‘not-spots’, writes Ian Thornton-Kemsley

Ian Thornton-Kemsley

01224 860710

ian.thornton-kemsley@galbraithgroup.com

Landlords frustrated by the rules say they’re trapped –unable to end leases granted to mobile-phone companies to operate masts, antennae and circuitry on their property, and struggling to agree suitable terms to protect their interests in new agreements. The effect of the legislation is to favour network operators and an emerging class of intermediary investor – called infrastructure providers – at the expense of property owners.

Landlords face multiple problems – unsightly apparatus can reduce building values; equipment owners frequently upgrade equipment without their consent, even when legally required; they often resist landowners in carrying out repair and maintenance, leading to delays, adding costs and interfering with landlords’ obligations to their tenants. Such delays add costs and affect property values, adding to financial pain for landlords.

The problem is highlighted by the fact there are some 90,000 telecom sites in the UK, together worth an estimated £240 billion, of which about 23,000 sites are on rooftops.

NOT-SPOTS GROWING

Problems for landlords are exacerbated by the switch to 5G. The required equipment upgrades are considerably more complex yet frequently, operators fail to address the consequent structural and health and safety challenges. ‘Exclusion zones’, mandated for radiation safety in operating 5G, are much greater, affecting rooftop access and extending over adjoining properties. Landlords complain that some operators seek to conceal the extent of these and place the cost of compliance with the health and safety implications on them.

Landlords face the further challenge of being unable to fulfil a growing list of building energy-efficiency requirements due to the siting of rooftop telecoms equipment, potentially frustrating key regulatory upgrades required to be in place by 2030.

The not-spots that fail phone users in London are starting to appear in other cities and towns in the UK, and for similar reasons.

The recent case of Gravesham BC -v- OTUK where an operator sought to prevent a Council from addressing water ingress into a block of flats has highlighted issues of telecoms apparatus on rooftops.

RELUCTANCE

Gravesham Council had for some three years had been anxious to effect repairs to prevent water leaking into residential flats below telecom equipment, but negotiations with the operator One Tower UK were unsuccessful. In 2021 the council raised an action to obtain vacant possession under the Landlord & Tenant Act. This was unopposed by OTUK and an order for vacant possession obtained. OTUK then sought to frustrate this by applying for a new agreement under the Code. Gravesham sought to prevent this, was unsuccessful and therefore subsequently appealed to the Upper Tribunal. The appeal was upheld in May 2024.

Landlords face multiple problems – unsightly apparatus can reduce building values; equipment owners frequently upgrade equipment without their consent, even when legally required...

In a more recent case, Cornerstone Telecommunications Infrastructure Limited (“CTIL”), another infrastructure operator, was granted consent to instal apparatus on a building in Wimbledon, London, despite an intention to redevelop the building for multi-occupational use which would not have been possible with the equipment in place. In CTIL -v- The Chartered Institute of Personnel and Development the Tribunal ordered a minimum term of five years, effectively preventing development of the building for this period. The building will go on the open market shortly and the outcome of any sale is likely to determine the extent of any compensation claim against the operator in terms of the Code.

In one case, an urban building being developed for accommodation, where cable running from a plant room containing telecom equipment to antennae on top of the structure poses a fire risk and prevents proper roof covering.

The costs, both financial and human, of an operator denying a landlord access for some five years to effect repairs or to develop their property to the detriment of their contractual and business operations and the costs in litigating such cases, illustrate the current imbalance, and explain the reluctance of landowners to host electronic communications apparatus at the levels currently being offered. n

WIND FARM INVESTMENT OPPORTUNITY at Bank and Afton, Ayrshire

An exciting wind farm investment is coming to the market for part of the Enoch Hill Wind Farm southwest of Glasgow.

A parcel of land is being offered for sale at Bank and Afton, with detailed planning permission for the erection of four 4.8MW wind turbines, and will form part of the 16-turbine Enoch Hill Wind Farm.

The 174.46 hectares (431.10 acres) of upland grazing land rises to 477m above sea level around Benty Cowan Hill, bounded to the south by mature woodland. The site is about four miles southwest of New Cumnock and seven miles east of Dalmellington in Ayrshire, with Glasgow 45 miles to the northeast.

Demand for green electricity generated in Scotland is increasing, encouraged by regulatory changes. This is one of the finest wind farm sites in the UK, with full development well underway, and a remarkable opportunity for a suitable investor or investors to participate in the renewable energy transition.

The land is marketed by Galbraith subject to a 32year lease from 1 March 2023 to 28 February 2055 in favour of the major renewable energy developer RWE Renewables UK Onshore Wind Limited.

There is a minimum rent for the 19.2MW installed on Bank and Afton as at January 2025 of just over £160,000 per annum but with potential additional top-up rent payments from a variable income rent of 6% and 8% depending on the average annual turnover price.

Construction of the wind farm began in June 2023, with 3km of road infrastructure leading from the B741, and is expected to be completed in 2025.

Those interested are highly recommended to contact Galbraith for a viewing appointment. n

u “This is one of the finest wind farm sites in the UK, with full development well underway, and a remarkable opportunity for a suitable investor or investors to participate in the renewable energy transition.”

Zonal electricity pricing would shake up energy supply chain

The potential introduction of zonal – or locational –pricing for electricity is one of several potential developments presenting both opportunities and challenges for Scotland's renewable energy sector.

The pricing mechanism would see electricity costs vary by region, reflecting factors such as generation availability and network constraints. This type of electricity market is used in countries including the US, Denmark and Australia.

For Scotland, with its plentiful supply of renewable energy often situated in less densely populated areas, the change could lead to lower electricity prices during periods of high wind or solar generation. This would likely offer a competitive advantage to local consumers and industries, particularly those with very large power requirements, such as data centres.

This could in turn encourage industries and business to relocate to areas where electricity prices are lower, but is probably more likely to just benefit consumers already in these areas as electricity cost alone won't determine a business location.

However, concerns have been raised over the complexities of such a system and its possible disadvantages for projects in areas facing grid limitations. Industry commentators have raised concerns over the potential for zonal pricing to deter investment in renewables, owing to reduced confidence in financial modelling while a new system of pricing is designed and implemented.

Further, owing to the disparity between the locations where generation and consumption are greatest, critics argue it would be unfair for those in central and southern England to pay substantially higher electricity prices than those in northern Scotland.

Given the importance of the renewable energy sector to the UK’s economy and net zero commitments, further proposals and amendments in policy should be expected. Appraising the potential challenges and opportunities will be important many involved in the energy supply chain. n

Mike Reid

07909 978 642 mike.reid@galbraithgroup.com

MOVES TO UNBLOCK GRID CONNECTIONS BOTTLENECK COULD HAVE IMPLICATIONS BIG

The high volume of renewable energy projects seeking to connect to the national grid has placed immense strain on network infrastructure and administrative procedures

This has resulted in two key challenges that the current system has struggled to resolve. First, the average number of days to receive a connection offer has steadily increased, delaying new projects needed to meet net zero targets. Second, the total queue for new projects at the end of 2024 was estimated at generating four times more installed capacity than the UK Government expects the country to need by 2050, with a number of projects effectively ‘stalled’ in the queue and unlikely to progress to construction for a variety of reasons.

Recognising this bottleneck, the National Energy System Operator (NESO) launched an overhaul as part of the GB Connections Reform project. The first phase of these changes sought to introduce a more stringent, graduated approach to new applications known as ‘First Ready, First Connected’ or TM04. This involved NESO evaluating all new connection applications through two new assessment stages – Gate 1 and Gate 2.

‘First Ready, First Connected’ Gate 1 will assess projects on their competency, so that successful applications receive offers for the capacity and technology requested, with an indicative connection date and an indicative connection point. These assessments will be conducted through an annual early application window, in contrast to the current system, where applications can be made at any time.

Gate 2 will determine the queue position for projects within the application window, with a focus on accelerating eligible projects up the queue. Criteria affecting eligibility include secured land rights and submitted planning applications, along with alignment with the UK Government’s strategic priorities. However, NESO determined that the reforms needed to go further than the proposed ‘First Ready, First Connected’ or TM04 process outlined above to tackle the backlog of existing projects in the grid connection queue. This additional process, known as ‘Apply Gate 2 to the existing queue’ or TM04+, expanded the reforms to the existing grid connection queue, ranking projects on their readiness to progress.

Significant delays

These reforms, which were approved by Ofgem on 15 April, resulted in a 56day licence standstill period until 10 June, after which the formal process of assessing all existing offers against the new criteria will take place. Most projects seeking a grid connection will need to apply for a Gate 1 or Gate 2 offer, even if they already have a connection agreement, and developers will learn the outcome of their application by autumn 2025, with pre-2030 connection offers being prioritised.

This could mean projects which looked set to progress in the near future are significantly delayed or become unviable, while others which were low down the queue are suddenly accelerated towards construction.

Developers, landowners and communities should be aware of these changes and seek guidance as required. n

Rachel Russell 07884 657 219

rachel.russell@galbraithgroup.com

Battery projects fade as grid struggles to cope with reforms and upgrade

Interest in battery storage for electricity has seen a period of high activity as developers have sought to secure option agreements over those properties that are near a grid connection point.

Richard Higgins 07717 581 741

richard.higgins@galbraithgroup.com

u “Looking ahead over the next few months, we can see that there will be uncertainty on existing exclusivity and options for battery schemes...”

Battery energy storage system (BESS) are held out as the solution to renewable energy’s intermittency problem – you cannot produce electricity from wind turbines in calm weather or from PV when the sun doesn’t shine. But as technology improves, BESS also serves an increasingly valuable function in grid stability – balancing energy supply and demand.

However, the battery market is currently going through a period of flux, caused to a large extent by the ongoing grid reform process, bringing into sharp focus the viability of a number of BESS schemes.

At this stage we know that across Britain there is a fivefold over-provision of potential BESS schemes in the pipeline to meet the requirements of the grid. There is a risk that a significant number of these projects may fall by the wayside as part of the grid reform process aimed at weeding out projects without clearly defined land rights and planning.

Grid modernisation continues to be hampered by delays in connecting new projects to the network, caused by factors such as outdated infrastructure, ‘zombie’ schemes, a backlog of renewable energy projects and challenges in securing permits and approvals for grid upgrades and expansions.

Uncertainty

To maintain their position in the grid queue and eventually receive a connection offer, developers must now provide demonstrable progress in meeting the requirements of the National Energy System Operator NESO, which oversees the energy electricity and gas network and is charged with accelerating the energy transition.

We have seen a number of BESS developers seeking to repurpose their hard-won grid connection offer for a battery scheme, to service a data centre instead, anticipating an expected rise in demand for such centres to facilitate the growth of AI as reported earlier. Looking ahead over the next few months, we can see that there will be uncertainty on existing exclusivity and options for battery schemes that may fail as a result of the reform process, and uncertainty too in the wider battery market. Insofar as landowners are concerned, we would recommend that they continue to liaise with their agents and ask direct questions of the developer or promoter on the likelihood of the scheme progressing. n

For wind turbines to produce more power, we must either erect towers with bigger rotors and blades to cover wider areas, or make the tip height higher in the sky, where the wind blows more steadily.

Since the early 2000s, we have seen wind turbines grow in both height and blade lengths, with the UK’s largest onshore installation reaching 200m tall. These turbines form part of the Kype Muir Extension Wind Farm in South Lanarkshire.

As the UK transitions away from fossil fuels towards greener alternatives with a view to reaching NetZero greenhouse gas emissions by 2050, wind turbines have proliferated, as they are a clean and sustainable alternative to coal and gas. As they get bigger, turbines also become more efficient and can generate

more electricity as they can capture more wind. For example, a single rotation of the 107-metre blade at Kype Muir can power a home for two days. However, there are concerns that the size of turbines is impacting our environment, local communities and road infrastructure.

We last looked at this in issue 22, since then the growth in wind farms has continued apace.

It can be said that turbines are visually intrusive and scarring to our environment, while also having an impact on wildlife, particularly birds and bats. So if our turbines get bigger, do they become more of an issue? There are mitigations in place to minimise these risks and impacts so that turbines and our environment can go hand in hand.

The burgeoning size of wind turbines helps drive the energy transition. Agreements are needed to ease their transport, reports Philippa Orr

TRANSPORT CHALLENGE

– A NATURAL OBSTACLE TO GROWTH

However, we live in a world of bridges, tunnels, roundabouts and some very twisty and tight country roads. Could it be that our road network, will be what prevents turbines getting even bigger?

There are significant challenges involved in transporting the component parts of a turbine, particularly the blades and the towers, as they are exceptionally long and heavy and quite possibly will often exceed the dimensions and weight limits of standard roads and bridges. Not to mention, more often than not, wind farms are located in remote areas with restricted access to major transport links.

In the UK, we are able to successfully transport turbines at their current size, through widening roads and strengthening bridges. Wind farm developers also use specialised transport companies who have created innovative ways to make it possible to transport turbines safely and efficiently.

If wind turbines keep attaining greater heights, there will need to be even more investment in the UK’s road infrastructure, along with ongoing collaboration between government agencies, industry and transport experts to ensure the UK continues to be able to support the growth of our renewable energy.

OVERSAIL AGREEMENTS NEEDED

Currently, wind developers require overrun and oversail agreements over land along an access route. The route for turbine blades can be substantial depending on where the component parts are manufactured and built. Therefore there can be quite a few agreements required. However it is very important that the right access is granted to the developer and we would highlighted the following points:

What area should be leased and what rights

• should be granted by ancillary rights of access.

The value of the access rights should be

• linked to the benefit of the project facilitated by the rights of access not the value of the land crossed from the overrun or oversail.

The lease should reserve rights for the

• landowner to grant access rights to other developers without requiring consent form the current developer.

It is therefore vitally important that any landowner approached by a developer that they should seek the advice of an agent to ensure that the correct rights are granted and at the best possible return. n

We live in a world of bridges, tunnels, roundabouts and some very twisty and tight country roads. Could it be that our road network, will be what

Offshore wind shakeup puts landowners and developers on notice

Scotland's offshore wind sector is positioned for expansion, buoyed by strong Government support and substantial grid infrastructure upgrades, writes Rachel Russell.

The offshore wind sector stands ready for substantial growth... but will this potential be realised?

Rachel Russell

The planned £58 billion investment in the National Grid announced by NESO, the National Energy System Operator, aims to connect an additional 21GW of offshore wind to the network, alongside other low-carbon generation across Britain. The Government views these upgrades as essential for harnessing Scotland's vast offshore wind resources and delivering clean electricity to meet the UK's growing demand.

While a significant proportion of the upgrades will be focused on undersea cabling, NESO has indicated that additional onshore transmission infrastructure will be essential in realising these targets. This could have major ramifications for landowners and communities located in areas where new offshore connections make landfall and along proposed routes for new transmission infrastructure.

While the UK Government is seeking to reduce capital expenditure on transmission infrastructure through the new capacity limits on onshore wind in Scotland, major reform of the grid network will nonetheless be required to meet growing electricity demand and the potential increase in offshore wind. The offshore wind sector stands ready for substantial growth, underpinned by significant grid investments but with recent concerns over the viability of some projects will this potential be realised? Appraising the challenges and opportunities involved will be crucial for both landowners and project developers.

The offshore wind sector stands ready for substantial growth, underpinned by significant grid investments. Appraising the challenges and opportunities involved will be crucial for both landowners and project developers. n

Rachel Russell 07884 657 219 rachel.russell@galbraithgroup.com

New rules seek to boost onshore wind south of the Border

Onshore wind has been instrumental in the Scotland's renewable energy transition so far – now the sector faces a period of adjustment under the Clean Power 2030 Action Plan (CP30).

This plan sets regional capacity ranges for various renewable technologies, and the proposed limits for onshore wind in Scotland have sparked considerable debate within the sector.

increasing onshore wind in England and Wales, owing to lower wind resources, higher population densities and greater competition between different land uses. It remains to be seen how the public reacts to this policy.

In response, Labour and the National Energy System

CP30 is a response to the foundational shift that has occurred since renewables overtook fossil fuels as the main source of electricity generation in the UK. When the current electricity grid was designed this was primarily powered by a small number of large power stations which were in relatively close proximity to major population centres. By contrast, the majority of wind and solar farms constructed in the past 25 years have been much smaller, numerous and located in more remote locations.

From a Scottish perspective, there is a potential that some projects exceeding the allocated capacity may face delays or even lose their existing grid connection agreements, potentially reshaping the future landscape of onshore wind development in Scotland. While the impact of these reforms on the sector remains to be seen, we could see developers being more selective in their approaches to landowners, resulting in a lower number of projects.

Operator NESO aim to encourage more onshore wind development closer to demand centres in England and Wales...

In response, Labour and the National Energy System Operator NESO aim to encourage more onshore wind development closer to demand centres in England and Wales. By reducing their reliance on renewable energy from Scotland (where generational capacity from onshore wind is high but transmission capacity is low), the UK Government aims to reduce capital expenditure on new transmission infrastructure required to bring electricity from Scotland to the UK’s major population centres in southern and central England. However, questions remain over the viability of significantly

Further, if the total number of consented projects decreases, we could see an acceleration in the timescales associated with project development, and a higher proportion of projects successfully reaching construction.

These factors would require a greater emphasis on site promotion to developers, along with a change in market dynamics that could impact on commercial terms. n

Developers on hunt for Data Centres to power AI Revolution

Increased use of AI and machine learning are driving demand for data centres as technology giants seek access to the electricity grid to power their energy-hungry sites, writes Richard Higgins

Developers are looking to secure locations for global technology companies serving AI and machine learning – the centres are increasingly a critical part of the digitaleconomy infrastructure.

AI is changing how technology is used in work, leisure and almost every aspect of life, as organisations and individuals access systems that enable computers to think like humans. Machine learning, a type of AI, uses algorithms to gather and store information from data, helping processors identify patterns and make decisions.

Hyperscaler demand u Operators and property entrepreneurs are searching for Scottish locations to build campus-style projects on

between 30 and 120 acres to accommodate up to 1.2 million sq ft of data centre space. These sites can require upwards of 100 megawatts per 30 acres of land or more, depending upon intensity of use.

Large amounts of energy are needed to train and run AI models as well as to cool the data centres that house these models. The largest power requirement we have seen is just over 500 MW.

The ‘hyperscalers’ driving AI development such as Google, Amazon, Microsoft and Meta –require guaranteed electricity, via a so-called ‘firm connection’. For continuity, sites must be connected to the grid and the availability of renewable energy sources such as wind can be a benefit to the operators.

Each data centre could employ between 200 and 500 people and there are long-term requirements for education and skills development.

Richard Higgins

In a process of grid reform aimed at modernising Britain’s electricity supply, the window for granting applications for new connections is closing, adding pressure to demand for sites.

The Scottish Government is keen to get behind green datacentres and AI infrastructure, though could do more to catch up, while Scottish Enterprise sees an opportunity to repurpose a number of sites.

There is competition among developers to gain representation by way of option agreements to enable them to negotiate separate occupational arrangements with hyperscalers and other users.

What developers are looking for u

Land values for data centre development are important though not critical drivers. The offers we have seen range from reasonable to very low, albeit based on multiples of

standard agricultural values. Offers may be attractive to some landowners, but this must be balanced with the potential success of planning applications and the availability of quality employment.

Developers look for relatively flat land, capable of achieving planning permission without delay due to environmental or similar considerations, ideally located in the Central Belt of Scotland or in reach of major population centres, to ensure that they can attract the right level of employment.

Each data centre could employ between 200 and 500 people and there are long-term requirements for education and skills development. Employment grades are generally high quality, with salaries approximately 1.2 times the average equivalent.

The total development cost of a data centre is significantly higher than for say a traditional industrial of business

use. The potential for using excess heat generated as a ‘community benefit’ or alternative uses to nearby population centres could aid planning applications.

Future-minded developers will be examining technology trends closely. Currently we understand that under 20% of data is held ‘in the cloud’, that is, in data centres, leaving significant opportunities for large-scale developments, assuming coming generations adopt AI and language learning technologies. n

Richard Higgins

07717 581 741 richard.higgins@galbraithgroup.com

Historically, telecoms mast sites were considered a reasonable investment, generating useful rents together with additional revenues derived from third parties utilising the telecoms operator’s mast infrastructure.

TELEPHONE MASTS RENTS GOING DOWN BUT VALUES GOING UP

Accordingly, masts were traded and acquired by property investors, or retained by landowners to provide an income when disposing of the farm or other landholding upon which the masts were situated.

The introduction of The Electronic Communications Code, a regulation conferring statutory rights on network providers and providers of systems infrastructure, has resulted in the rents and other payments to landlords being significantly reduced with little prospect of future growth. Accordingly, the attractiveness of these assets to the private property investor seeking an appropriate rate of return on capital deployed has diminished.

The Electronic Communications Code was introduced to support the Government’s agenda to improve the digital economy and has resulted in a different ‘market’ arising where operators and infrastructure funds are seeking to acquire and control telecoms mast sites in order to establish control at scale.

Having regard to open market transactions for these assets, it is clear that pricing is not a consequence of the yield to be derived from an individual asset, but of competition in the marketplace

between telecoms operators and infrastructure funds to amass market share.

We have been involved in numerous transactions where telecoms mast sites are being acquired for sums which represent a yield of less than 4% which is less than the return from UK government bonds. Whilst on the surface this appears to make little sense, it reflects the activities of a special purchaser i.e. a particular buyer for whom a particular asset has a special value because of advantages arising from its ownership that would not be available to other buyers in a market. In this case, where other buyers are general property investors.

Accordingly if you have a telephone mast site where you are potentially looking at reduced future revenues, the future may be brighter than you thought and it may be a good time to consider selling. n

Calum Innes 07909 978 643

calum.innes@galbraithgroup.com

u “We have been involved in numerous transactions where telecoms mast sites are being acquired for sums which represent a yield of less than 4% which is less than the return from UK government bonds.”

...the attractiveness of these assets to the private property investor seeking an appropriate rate of return on capital deployed has diminished.

Calum Innes

DEVELOPMENT PROPOSALS FOR SENSITIVE AREAS MUST ADDRESS PEATLAND

More than 20% of Scotland’s landmass is covered by peatlands – forming an important part of our landscape, and cultural and natural heritage.

Peatlands provide several important ecosystem services, not least carbon storage, water filtration and wildlife habitat.

While the majority of peatlands are located in the uplands, away from major population centres, a wide range of development proposals routinely emerge in areas with extensive areas of peat soils. These include wind farms, telecommunication masts, power lines and even space ports.

As the majority of major development proposals relate to renewable energy developments, this creates a tension between protecting valuable habitats and producing green electricity under planning policy.

Under the National Planning Framework 4 (NPF4), planning officials are required to give significant weight to addressing global climate and biodiversity issues when appraising development opportunities.

Under Policy 5, dealing with peatland, development proposals must protect carbon-rich soils by minimising disturbance, or undertaking restoration when this is unavoidable.

Policy 5 outlines a mitigation hierarchy which all development proposals must adhere to:

Avoid – by removing the 1 impact at the outset;

Minimise – by reducing 2 the impact;

Restore – by repairing 3 damaged habitats; and

Offset – by compensating 4 for residual impact that remains, with preference for on-site to off-site measures.

Any development proposal which will take place on peatland, carbon-rich soils or priority peatland must have a site assessment carried out. Combined with the mitigation hierarchy outlined in Policy 5, these site assessments will form the basis for a Peat Management Plan (PMP) for the development proposal.

These requirements are of upmost importance to developers seeking to undertake projects in peatlands and can be a crucial aspect of a planning application. Developers therefore need to consider the potential impact of a proposed development on peatlands at an early stage, and ensure the mitigation hierarchy is adhered to.

u “Any development proposal which will take place on peatland, carbon-rich soils or priority peatland must have a site assessment carried out...”

Where peatlands are present, developers should provide landowners with a suitable PMP for their prior approval that aligns with their wider land management objectives.

Galbraith have extensive experience in appraising PMPs for development proposals and would be pleased to discuss your requirements. n

Edward Fletcher

07990 130 753

edward.fletcher@galbraithgroup.com

Hydro An asset in high demand

The recent sale of Pitnacree Hydro Scheme, a 300kW runof-river hydro scheme in Perthshire demonstrated the continued interest in renewable assets which have outstanding eligibility for the government’s Feed in Tariff. Pitnacree hydro scheme was commissioned in 2015 having been developed under leasehold arrangements with various landowners. The scheme operates at a high level of efficiency with annual output in the order of 1,100,000 kWh and generating revenues approaching £500,000 in the last accounting year.

We are fortunate in having a substantial ‘black book’ of parties who have a potential interest in renewable assets and whilst Pitnacree was quite a small scheme which excluded a portion of the market, there was significant interest from a wide variety of parties who came forward with offers to purchase the assets.

Following a process, a preferred bidder was identified and the sale was completed after appropriate due diligence. n

Calum Innes

07909 978 643

calum.innes@galbraithgroup.com

In Energy Matters 29 we called for a rethink on the Shared Rural Network (SRN) programme to avoid significant impact on remote and protected landscapes where demand for mobile communication is generally low.

Mike Reid 07909 978 642

mike.reid@galbraithgroup.com

u “It is time for Government and mobile operators to work more closely with local communities to ensure an effective, joined up digital rollout to reduce disruption and environmental impact...”

Government rethink on Shared Rural Network mobile rollout

In February the Government announced a review of the SRN rollout in rural areas to cut the £1 billion projected cost of the project and it is understood that officials are planning to cut the number of new mobile masts built under the programme from 260 to around 60.

Although the review has been instigated by a desire to cut costs, we consider the Government should look at the wider impacts of the programme during its review and target any new sites to where they are need most rather than just building sites to achieve a notional geographical coverage.

It is time for Government and mobile operators to work more closely with local communities to ensure an effective, joined up digital rollout to reduce disruption and environmental impact – this will require changes to the current SRN programme.

In Scotland, SRN previously aimed to achieve 74% 4G mobile combined coverage from the mobile network operators, up from 44% at the start of the programme, with coverage from at least one mobile operator increasing to 91%. These targets will also need to be changed as part of any review of the programme.

Improved coverage in rural areas is important for residents and businesses. However, the next phase of the project, Total Not Spots (TNS), looks to locate masts in more remote areas as new masts are put up to fulfil the geographical requirements of the SRN commitment, rather than any other requirement, and the sites identified are often not wanted by local communities and landowners.

There is also significant environmental and other impact caused by new mast sites, whether that is the visual intrusion of the mast structure itself, the power and fibre services required, or access visits for refuelling generators, maintenance or other reasons.

We wait to see the outcome of the Government’s review and how this impacts the overall SRN programme.

Meanwhile, however, the operators are still progressing site development due to the potential penalties if the January 2027 deadline fails to be met.

As the operators should be responsible for paying all the fees incurred for progressing their enquiries, landowners and occupiers are urged to seek professional advice at an early stage of an approach, in order to protect their property rights. n

The Labour Government has made clear its enthusiasm for renewable energy generation and the new National Planning Framework supports its programme from a planning perspective. Making many these projects a reality is set to present major challenges.

Calum Innes

07909 978 643

calum.innes@galbraithgroup.com

Attempts to direct electricity generated offshore and in more remote parts of Scotland, to centres of demand in the south, expose current transmission infrastructure failings.

Disturbance and disruption arising from electricity network reinforcement are apparent, with communities reacting strongly against negative visual impact, loss of amenity and potential effects on property values.

In onshore wind generation, we may be approaching saturation point, but there are plans on the horizon that dwarf the disruption of these developments.

There are some 20 large-scale, pumped storage hydro schemes being promoted in Scotland, representing many hundreds of GW of potential generation – all in remote rural locations.

Even if only a handful of these schemes are developed, the impact is likely to be enormous, as development on this scale has not been experienced for over half a century since the North of Scotland Hydro-Electric Board (NSHEB) launched the post-war boom in hydro infrastructure.

Housing a migrant workforce

In addition to pumped-storage hydro, substantial work is necessary on upgrading the transmission grid and infrastructure to take electricity to where it’s needed.

Due to the remote geography of many line upgrades and the scale of development, we are working for contractors for several worker villages across the Highlands and islands and throughout Scotland.

As each village will need to accommodate between 400 and 500, there will be a lack of housing stock. Potential solutions range from containerised units to wholesale occupation of new residential developments closer to existing towns and cities for up to five years.

A ‘container’ village must have minimal impact on the local rural setting and housing market, and be capable of being decommissioned

following completion of the project.

The shorter-term impact on social infrastructure, provision of food and basic services, recreation and leisure is likely to be significant.

While village design is carefully managed, not all impacts can be mitigated, though the potential for a longer-term legacy for the local population is carefully explored with communities and planning authorities.

Some vacant hotels are being improved and rented to accommodate workers. Investment in refurbishment and upgrading means tired buildings will be handed back to landlords in an improved condition, to boost tourist and worker accommodation in the medium term.

Given the extent of development likely to meet energy demand, we envisage many years of more people living and working in areas which

The logistics of delivering a single project are substantial, with thousands of workers accommodated and plant and materials delivered via inadequate roads. Multiplied by even a small number, the scale is breathtaking. When NSHEB delivered tens of projects in post-war, most remote communities were without electricity and the benefits to those impacted were tangible. Today, this infrastructure is required to balance a grid serving the whole nation, with local benefit limited.

The need for energy storage to balance a grid reliant on intermittent renewable generation is widely understood, and pumped storage hydro has some advantages over battery storage requiring lithium.

That said, delivery of these projects will be reliant on a global supply chain and the question remains whether such can be delivered while leaving a positive legacy.

have seen depopulation.

The Scottish Government announced a national housing emergency in May 2024, presaging an accommodation conundrum to be felt most acutely in the Highlands. The development of freeports at Inverness and Cromarty is expected to create some 10,000 jobs in the next 10 to 15 years.

With Highland Council saying it needs an extra 24,000 homes built in the next 10 years, there is an urgent need to accelerate housebuilding across the area.

Housing demand will hopefully be addressed in the forthcoming Highland Council LDP “Call for Sites” process, together the need for significant investment in order deliver these ambitious targets. The challenge is to ensure a positive long-term legacy. n

CURRENT SOURCES OF RENEWABLE FUNDING

The Domestic and NonDomestic Renewable Heat Incentives have both closed to new applicants as of 31st March 2022. If you are already on the scheme, you will receive payments as usual as long as you continue to meet your ongoing obligations. The Government is still providing financial support to help with the role out of low carbon heat technologies.

Scotland

Home Energy Scotland Grant and Loan – The Home Energy Scotland Grant and Loan is designed to make homes warmer and more comfortable by helping homeowners install a range of energy saving measures, through grants and/or an interest-free loan funded by the Scottish Government.

You can now apply for grant funding. Grants for energy efficiency improvements is up to 75% of the combined cost of the improvements, up to the maximum grant amount of £7,500. A rural uplift (up to £9,000) is also available to provide extra support to rural and island homes which can face increased costs to install home improvements.

In respect of how much a household can borrow, it depends on what improvement or installation is required. These are grouped into two types – Clean Heating Systems and Energy Efficiency Measures.

For Energy Efficiency Measures the maximum grant and optional loan available for each improvement is as follows:

• Solid wall insulation: up to £10,000 (£7,500 grant plus £2,500 optional loan)

• High heat retention storage heaters: up to £5,500 loan (£2,500 grant available for high heat retention storage heaters when installed as part of a package of measures)

• Double glazing, triple glazing, secondary glazing: up to £8,000 (lone only, no grant available). Only available when improving single glazing, not for replacement or improvements of existing double, triple or secondary glazing.

• Insulated doors: up to £4,500 (lone only, no grant available)

• Flat roof or room-in-roof insulation: up to £4,000 (£3,000 grant plus £1,000 optional loan)

• Loft, cavity and underfloor insulation: up to £2,000 (£1,500 grant plus £500 optional loan)

• Warm air units: up to £5,000 (loan only, no grant available).

For Renewable systems the maximum loan/grant amounts are as follows:

• Air/ground/water to water source heat pumps: £15,000 (£7,500 grant plus £7,500 optional loan)

• District heating scheme connection: £7,500 (loan only, no grant available)

• Solar thermal: £5,000 (loan only, no grant available)

• Hybrid solar PV/ water heating systems: £5,000 (loan only, no grant available)

• Wind turbine: £2,500 (loan only, no grant available)

• Hydro turbine: £2,500 (lone only, no grant available)

• Wood fuelled (biomass) boilers (and eligible stoves): £15,000 (£7,500 grant plus £7,500 option loan).

The grant and loan values stated opposite are subject to availability while funds last or until the end of the financial year –whichever is sooner. Funds will be allocated on a first-come, first-served basis. Funding is reserved for householders when they receive a written loan offer, not on application to the scheme.

If you would like to find out if you are eligible and how you apply for the grant and loan funding please follow the link below. Source: https://www.homeenergyscotland.org/home-energy-scotland-grant-loan

ECO4 Grant Funding in Scotland

The ECO4 scheme in Scotland provides grants for homeowners and private tenants to improve energy efficiency and lower heating costs. The scheme is available until March 2026 and is the latest government-funded program designed to lower energy bills and carbon emissions. Eligible Scottish homeowners and private tenants who are deemed to live in fuel poverty can claim a 100% non-repayable grant to improve the energy efficiency of their home.

To qualify for an ECO grant in Scotland, a household must meet the following criteria:

• Live in a property which has a low energy rating (E-G)

• Live in a property with high energy costs, typically those using electric heating or off-grid gas heating like oil and LPG boilers

• A member of the household must be in claim of a means-tested benefit.

The ECO4 scheme covers cavity wall insulation, sold wall insulation, roof insulation, solar panels, air source heat pumps and upgraded heating controls.

The Boiler Upgrade Scheme – The Boiler Upgrade Scheme (BUS) is a UK Government initiative to encourage more people in England and Wales to install low carbon heating systems.

The BUS covers three low carbon heating systems:

• Air Source Heat Pump: £7,500 towards cost and installation

• Biomass Boiler: £5,000 off cost and installation for properties in rural location and properties not connected to the gas grid

• Ground Source Heat Pump: £7,500 towards cost and installation. This also includes water source heat pumps.

The funding available has been increased to £295 million for 2025/2026 and is an installer led scheme which means the installer will apply for the grant on behalf of the home owner. However, we are unsure as to the future of this funding following the recent change in Government.

The Smart Export Guarantee (SEG) is a support mechanism designed to ensure small-scale generators are paid for the renewable electricity they export to the grid. This does not happen automatically, so you must sign up to receive the SEG tariff.

You are eligible to apply if you have one of the following renewable energy generating technologies:

• Solar PV Panels

• A wind turbine

• Hydro

• Anaerobic digestion

• Micro combined heat and power.

Under the scheme all licenced energy companies with 150,000 or more customers must provide at least one SEG tariff.