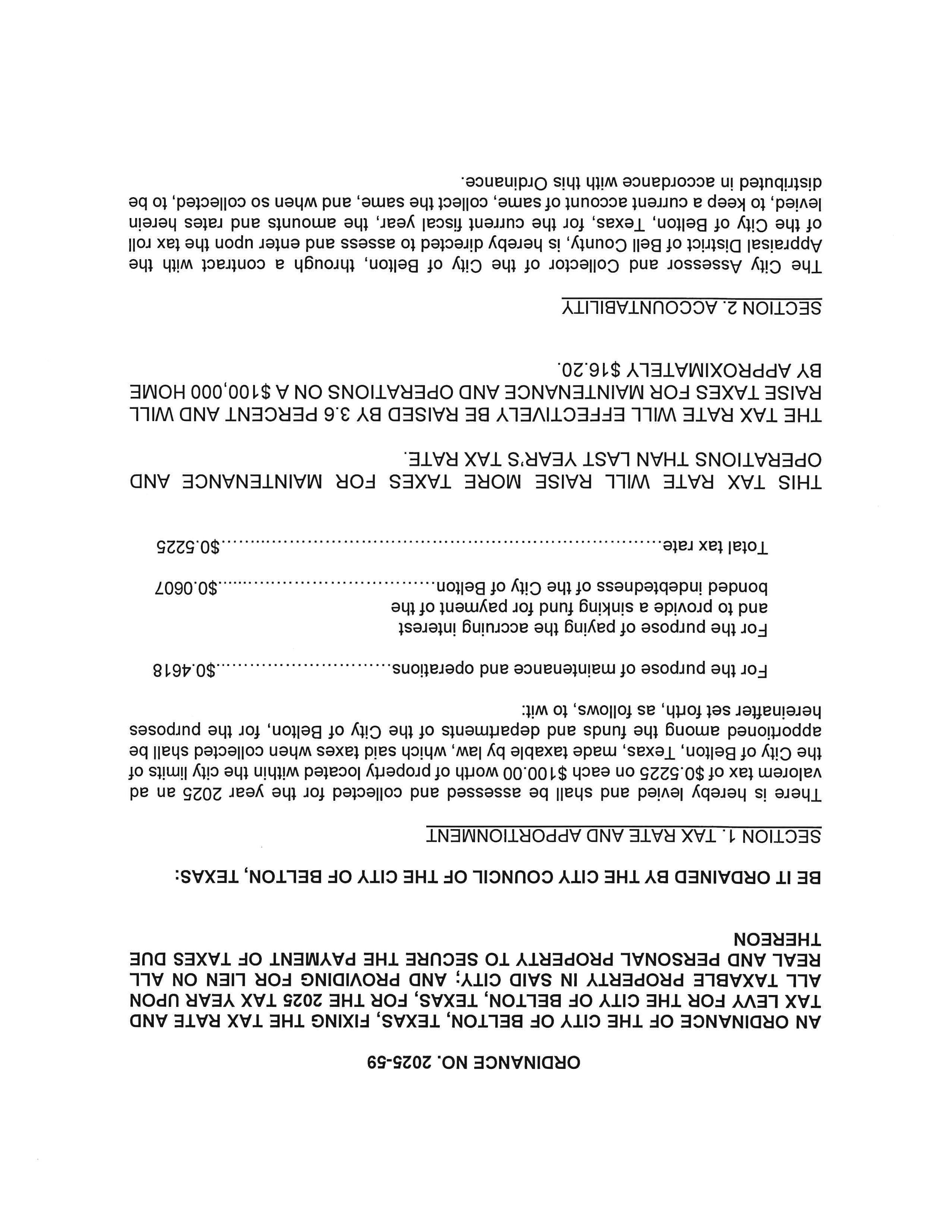

This budget will raise more revenue from property taxes than last year's budget by an amount of $1,217,589, which is a 9.91 percent increase from last year's budget. The property tax revenueto be raised from new property added to the tax roll this year is $443,526.

The membersof the governing body voted on the budget as follows:

For: David K. Leigh, Mayor Dave Covington

John R. Holmes, Sr.,Mayor Pro Tem Daniel Bucher

Craig Pearson Stephanie O’Banion Luke Potts

Against:

Absent:

PropertyTax Rate Comparison

Total debt obligation for City of Belton, Texas secured byproperty taxes: $8,969,426

CITY OF BELTON, TEXAS ANNUAL BUDGET

FISCAL YEAR 2026

OCTOBER 1, 2025 – SEPTEMBER 30, 2026

ADOPTED ON SEPTEMBER 9, 2025

THE MAYOR AND CITY COUNCIL

DavidK.Leigh

JohnR.HolmesSr.

DaveCovington

CraigPearson

DanielBucher

LukePotts

StephanieO’Banion

SamA.Listi

CityManager

Mayor

MayorProTem

Councilmember

Councilmember

Councilmember

Councilmember

Councilmember

This budget will raise more total property taxes than last year’s budget by $1,217,589 or 9.91%, and of that amount $443,526 is tax revenue to be raised from new property added to the tax roll this year.

CITY OF BELTON, TEXAS FY 2026 ANNUAL BUDGET

PREPARED BY

William Michael Rodgers, CPA

Amanda Cox Director of Finance Assistant Director of Finance

Christina Sparks Senior Accountant

Sam A. Listi

Matthew Bates

CITY OFFICIALS

City Manager

Assistant City Manager

John Messer City Attorney

Amy Casey City Clerk

Larry Berg Police Chief

Jonathon Fontenot Fire Chief

Michael Rodgers

Amanda Hairston

Robert Van Til

Megan Odiorne

Chris Brown

Scott Hodde

James Grant

Paul Romer

Cynthia Hernandez

Director of Finance

Director of Library

Director of Planning

Director of Human Resources

Director of Information Technology

Director of Public Works

Director of Parks & Recreation

Director of Communications

Executive Director of Economic Development

Visit us @ www.beltontexas.gov

The Government Finance Officers Association of the United States and Canada (GFOA) presented a Distinguished Budget Presentation Award to the City of Belton, Texas for its annual budget for the fiscal year beginning October 1, 2024. In order to receive this award, a governmental unit must publish a budget document that meets program criteria as a policy document, as a financial plan, as an operations guide and as a communications device.

This award is valid for a period of one year only. We believe our current budget continues to conform to program requirements, and we are submitting it to GFOA to determine its eligibility for another award.

Introduction to the Budget Document

This budget is intended to give the reader a comprehensive overview of funding for the City’s day-to-day operations,scheduledcapitalimprovementexpenditures,andprincipalandinterestpaymentsfortheCity’s outstanding long-term debt. The first three sections, the Budget Overview, Strategic Goals, and Budget Summaries, provide an overview of the City’s strategic planning efforts and how this budget is developed to provide high quality services. Operating expenditures are provided for each department to give the reader aclearidea of howresourcesareallocatedacrosstheCity’svariousprograms. Thefollowingicons have been created to graphically depict the City Council’s six strategic pillars consistently throughout the document and to clearly demonstrate how the budget is founded upon those goals.

Budget Overview and Summary Information

Budget Overview

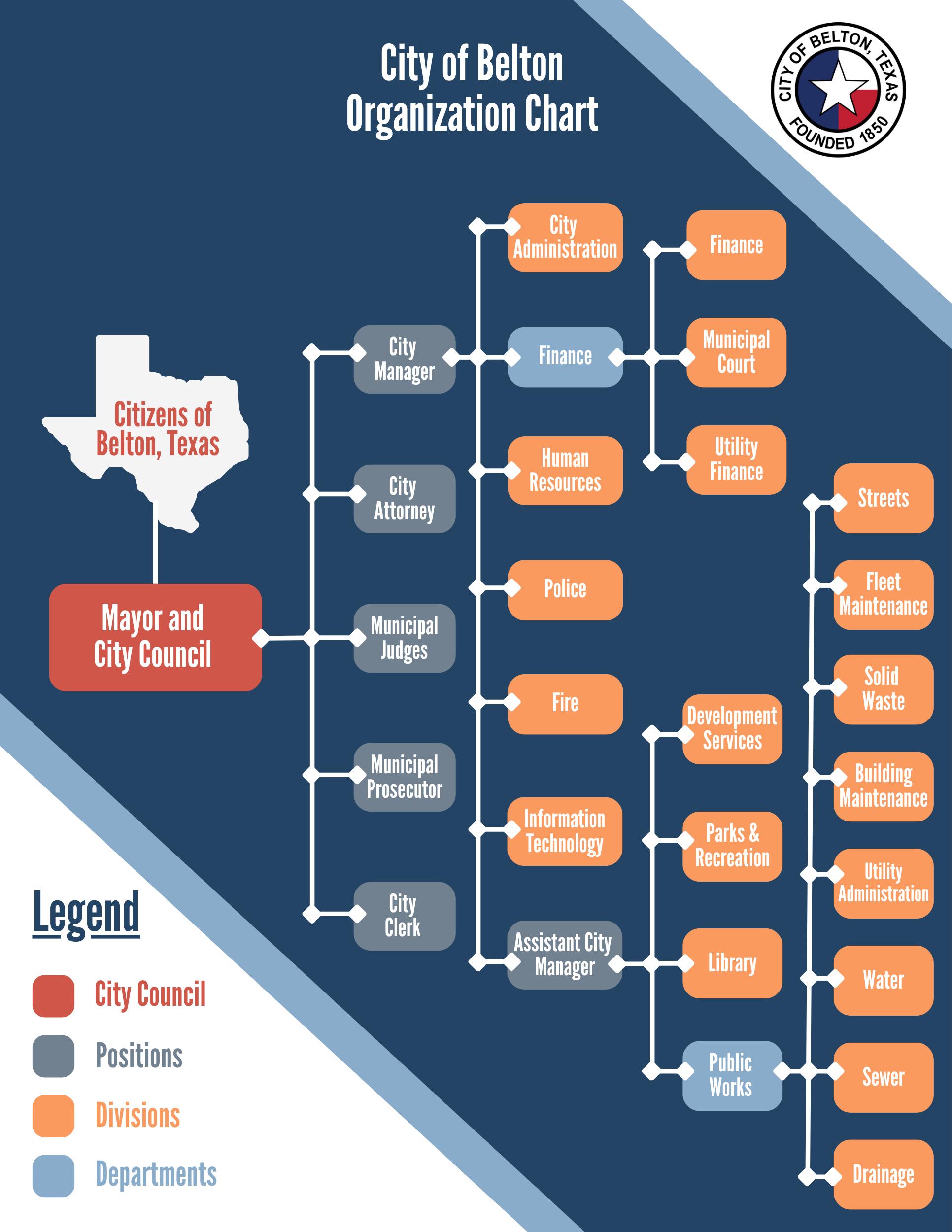

This section includes the City Manager’s Budget Message which addresses major policies and key issues that impacted the development of the Annual Budget. This section also contains information about the budget process, fund structure, organization chart, and employee count history.

Strategic Goals

The City Council has identified six strategic pillars based upon the long-range vision for the City of Belton. Thesestrategicpillarsandassociatedgoalsserveasthefoundationforallbudgetdecisions. Departmental goals and initiatives are linked to these organization-wide, strategic goals and initiatives.

Budget Summaries

Several consolidated schedules of all city funds are presented to give an overall perspective of the upcoming budget as well as historical, estimated and projected fund balances.

Operating Budgets

General Fund Overview

ThissectiondescribesandanalyzestheGeneralFundusingacombinationofnarrative,tables,andgraphs to highlight key aspects of the budget including revenues, expenditures, and fund balance. A brief description is given of the sources, trends and assumptions made for major revenues. Expenditure information is detailed by division, category and account.

General Fund

This section provides strategic, operational, performance, and budgetary information for each of the city’s divisions within the General Fund. Each division’s operating budget includes a description of the division; goals andinitiatives that will be accomplishedduring the fiscalyear with theirrelationship to the overallcity goals; workload and performance measures; significant changes for the upcoming budget year; and a personnel summary. Expenditure budgets for each division are detailed by account.

Debt Service Fund

This section outlines the city’s tax-supported debt. Amortization schedules for all outstanding debt are provided.

Operating Budgets for Other Funds

TheoperatingbudgetsfortheotherfundsofthecityarepresentedinamannersimilartotheGeneralFund. The overview page includes a description of the fund along with a fund balance history. Revenue and expenditure/expense budgets are detailed by account. Additional summaries are presented for the Water & Sewer Fund.

Strategic Plan 2026 - 2030

This section presents the City of Belton Strategic Plan. The strategic plan provides insight into the future needs and goals of the City of Belton and how those needs and goals can be met. As part of the strategic plan, City Council identified six Pillars of Emphasis to guide the strategic planning process. Each pillar is graphically depicted within the budget to show how each pillar is addressed in the budget.

Capital ImprovementsProgram 2026 - 2030

This section presents the city’s plan for development for Fiscal Years 2026 - 2030. Components of this section include:

An overview of the Capital Improvements Program;

A narrative summary of projects;

Afive-yearplandetailingexpectedprojectexpenditures,potentialsourcesoffunding,andpossible future impacts on operating budgets resulting from additional O & M expenditures;

A summary of unobligated fund balances in capital projects funds.

Belton Economic Development Corporation

The operating budget for the Belton Economic Development Corporation is presented in a similar fashion to the General Fund. The overview page includes a description of the fund followed by a fund balance history. Goals, initiatives, and significant changes to the budget along with workload measures and performance measures are highlighted in the mission statement. Revenue and expenditure budgets are detailed by account.

Appendix

Thissectioncontainssupportinginformation,suchasachartofaccounts,aglossary,alistingofacronyms, and ordinances relating to the adoption of this budget and the property tax rate.

CityofBelton

Founded 1850

September 9, 2025

TO THE HONORABLE MAYOR, CITY COUNCIL, AND CITIZENS OF BELTON:

We are pleased to present the FY 2026 Annual Budget for the fiscal year that begins on October1,2025. Thisdocumentrepresentsthecity’sfinancialplanandoperationsguide forthenextfiscalyear. Itidentifiesissuesconfrontingthecommunityandprovidesaplan for serving our constituents. A discussion about the city’s vision and long-term strategic plan is also included. It takes a combined effort by City Council, management, and staff to allocate and deploy the city’s resources to meet the established goals while also maintaining sound financial policies. We will work diligently to administer this budget in a manner that provides exceptional service to the residents of Belton. This message discusses the major issues, initiatives, and assumptions addressed in the budget.

FY 2026 BUDGET OVERVIEW

The FY 2026 Annual Budget includes total resources of $52,873,690 and expenditures of $47,915,770, including transfers and planned use of fund balance. For perspective, the originally adopted budget for FY 2025 contained resources of $50,903,660 and expenditures of $48,666,980.

The budget forFY 2026 is intendedtobe lean without significant changes from FY2025. Consequently,thenumberoffull-time-equivalentpositionsdeclinesbyone. Noutilityrate changes are included. Whileresourcesfrom propertyandsales taxes continue to rise,a fifteen percent jump in health insurance premiums and limited pay increases for employees elevate personnel costs. The appropriation for debt service increases after issuing bonds in 2025 for utility projects, a fire engine, and a facility acquisition. In FY 2026, theCityofBelton will investheavilyin its information technology infrastructurewith data center and software upgrades. Having funded several items during 2025, various transfers for capital projects and equipment willdecrease in FY 2026.

The proposed budget that was presented to City Council in July was based upon a property tax rate of $0.5306 per $100 of taxable value, a slight increase over last year’s adopted rate of $0.5225. Property valuations and property tax rates have been in the spotlight throughout the State of Texas recently. Knowing this, the City Council voted to leavethepropertytaxrateunchangedat$0.5225per$100oftaxablevalue. TheGeneral Fund will use accumulated reserves in FY 2026 to continue providing quality services to constituents.

As the proposed budget was being developed, various departments submitted over $500,000 of supplemental budget requests. These requests included personnel additions, equipment, and facility renovations. Some of these items were funded with moneythatwaspreviouslysetasideforcapitalprojectswhileotherswereeliminatedfrom the proposed budget entirely as a cost-reduction measure. However, many of those needs will need to be addressed in future years.

The budget revolves around several core principles that have been established by the City Council. These philosophies provide guidance for the development of the annual budget.

CoreBudget Principles

CORE PRINCIPLE: STRATEGIC PLAN IMPLEMENTATION

TheStrategicPlanistheCityofBelton’sprimaryplanningdocument. Itoutlinesthevision and goals for the long term. There are six strategic pillars: connectivity, economic/business development, quality of life, infrastructure and public facilities, engagement,andpublicsafety. The StrategicPlan focuseson the City ofBelton’svision of being the “Community of Choice in Central Texas, Providing an Exceptional Quality of Life.”

Each year, the plan is reviewed, revised, and updated as needs and conditions dictate. The revised plan forms the framework upon which the budget is built. Performance of Strategic Plan initiatives is measured regularly during the year. Additionally, each department measuressuccess and progress by tying both accomplishments for the prior year and goals for the upcoming year to the Strategic Plan goals and initiatives.

CORE PRINCIPLE: BALANCED BUDGET

The FY 2026 budget enhances the city’s operating levels to meet the demands that are created by a growing population. Investment in infrastructure remains a priority. A balanced approach of focusing on improving levels of service, while remaining fiscally conservative, served as the basis for this budget. The issues impacting achievement of this goal include:

Assessing staff workload, personnel, and compensation

Recognizing available funding limitations

Seeking supplementalfunding through grants.

In addition to strategic long-range planning, the day-to-day government operations must continue. These tasks include maintaining city streets, repairing utility lines, delivering police and fire services, maintaining park spaces, and providing library and development services. These operational duties must be performed within the constraints of limited resources. The city has adopted financial and budget policies that reinforce the principle that we must live within our means.

Property value growth has slowed from the double-digit increases of the past few years. Salestaxrevenuegrowthhasalsoeased. Yieldsoninvestments,however,remainstrong atapproximatelyfourpercent. ThesegrowingrevenuesinFY2026providetheresources to fund Strategic Plan priorities.

The city also seeks grant opportunities whenever possible to fund major capital projects. Grantfundingallowsthescopeofprojectstoextendbeyondthatwhichmaybeachievable by the city alone. Efficiencies are gained when the work and cost can be shared among

agencies. Examples include Federal Highway Administration grants for sidewalks along East6th Avenue,FederalCommunityProjectFundgrantstoreplaceandrelocatetheEast Central Avenue/Spring Street bridge, and Texas Parks & Wildlife grants to construct Standpipe Park.

The city implemented a capital equipment replacement plan to provide for the replacementof vehiclesandequipmentbaseduponmileage,age, ormaintenancecosts. Money issetaside each yearto ensure sufficient funding exists when theassets need to be replaced in the future.

CORE PRINCIPLE: COMMUNITY INVESTMENT

A strong, thriving community requires continual investment in its people, facilities, and infrastructuretodeliveranexceptionalqualityoflife. AsanimportantgoalintheStrategic Plan, the City of Belton implemented a street maintenance plan with the desire to sustainably fund it. The plan will elevate the quality of streets and create long-term savingsthroughthesystematicuseofpreventivemaintenance. Thecostofmaintenance and other corrective actions each year are analyzed and included in the annual budget. Street maintenance funding tops $1,100,000 in FY 2026.

The City of Belton also implemented a five-year Capital Improvements Program (CIP). By identifying potential capital projects today, funds can be accumulated over time to meet future demand. The CIP includesananalysis of the timing ofexpendituresand the various sources of funding that may be available. The impact upon future operating budgets is also considered.

To be a “quality of life” city, a municipality must provide ample opportunities for residents and visitors to retreat from the rigors of daily life by exploring the outdoors. The City of Beltonaddressed thisby creatingaParks and Recreation StrategicMasterPlantoguide thedevelopmentofparksandrecreationamenitieswithinthecity. Theparksmasterplan will be updated in FY 2026. The result of this update will be a park system that is harmonious with its surroundings and available to all.

GENERAL FUND

The GeneralFund isthechiefoperatingfundof thegovernment. Itisusedtoaccountfor all current financial resources not required by law or administrative action to be reported inotherdesignatedfunds. Theprimarygovernmentalfunctionsoccurring withinthisfund are public safety, parks, library, streets, and general administrative operations.

GENERAL FUNDRESERVE LEVEL

The city has adopted a policy of maintaining a reserve level of at least 30% of budgeted expenditures for the General Fund, Water & Sewer Fund, and the Drainage Fund. This policy ensures that funds will be available in the event of emergencies, financial recessions,andotherunforeseencircumstances. BelowisachartoftheGeneralFund’s

unassignedspendablebalancesforthepasttwoyears,anestimatedbalanceforthefiscal year ending September 30, 2025, and the projected balance for the fiscal year ending September 30, 2026. We expect the GeneralFund to remain in compliance for FY 2026 with an accumulated reserve level of 32% of budgeted expenditures.

$10,000,000

$9,500,000

$9,000,000

$8,500,000

$8,000,000

GENERAL FUNDREVENUES

General Fund revenues total $25,412,250 in FY 2026, increasing $1,030,040 or 4.2% over the adopted budget for the prior year. Revenues are derived from several sources. Foremost among these sources are property and sales taxes.

Property Tax

Thirty-nine percent of General Fund revenues are derived from property taxes. The Bell County Tax Appraisal District reports that the taxable value of property locatedwithin the CityofBeltonhasincreased bynine percent to$2,583,535,000. Current property tax revenue of $9,820,750 is budgeted. The tax rate that will generate that amount is $0.5225 per $100 of taxable valuation, the same rate as the prior year.

The tax rate is comprised of two components - the debt service portion that is dedicatedtothepaymentofprincipal,interest,andfeesongeneralobligationdebt, and the maintenance and operation (M&O) portion which is utilized inthe General Fundforgeneralgovernmentalpurposes. TheratesfordebtserviceandM&Oare $0.0607 and $0.4618, respectively.

Sales Tax

Sales taxes make up 27% of all General Fund revenues. The FY 2026 Annual Budget anticipates sales tax revenue to grow by four percent to $6,810,390. The gain can be attributed to the ongoing expansion of the area economy as more consumers find Belton a great place to shop.

Other Revenues

Refuse collection and contract fees increase by 9% over 2025 due to a rising customer count. Court fines and fees may rise by 11% as more citations are written. Interest income and public safety reimbursements are expected to fall by 10% and 13%, respectively.

GENERAL FUNDEXPENDITURES

General Fund expenditures in the FY 2026 Annual Budget total $25,563,050, increasing $649,160 overthe FY2025adoptedbudget. Encompassing60%ofthebudget,charges withinthepersonnelcategoryriseby$570,350tocoverthecostofrisinghealthinsurance premiums and annual merit increases for employees. Comprising 24% of expenditures, the increase in appropriations for services is primarily due to higher costs for refuse collection and information technology services. The maintenance category includes $1,102,500 for contracted street maintenance.

Transfers from the General Fund occur when additional funding for capital projects is needed, or when the City Council wants to designate funds to be used for a special purpose over a series of years. Transfers for future vehicle and equipment replacement decline in FY 2026.

DEBT SERVICE FUND

This fund is used to accumulate a dedicated portion of property taxes for payment of the city’s general debt. Revenue from property tax collections is expected to be $1,552,560. Expenditure appropriations for FY 2026 total $1,508,740, increasing by three percent aftertheissuanceofbondsduring2025. Paymentsontax-supporteddebtcomprisethree percent of all appropriations included in the FY 2026 Annual Budget.

WATER & SEWER FUND

TheWaterandSewerFundaccountsforallactivitiesrelatedtotheprovisionofwaterand sewer services to the residents of Belton, including administration, operations, maintenance, debt service, billing, and collection. An enterprise fund of the city, it is designed to be financed and operated like a private business. Accordingly, utility fees should be sufficient to cover annual operating and capital costs while providing income for future capital needs.

TotalrevenuesoftheWaterandSewerFundareexpectedto increase bytwopercenton a budget-to-budget basis to $14,745,480. Compared to the FY 2025 estimate however, utility revenue increases by only $190,140, or 1.3%, with no rate increases planned for water and sewer services. Instead, the increase in revenue is derived from higher consumption and a growing customer base.

The FY2026AnnualBudgetanticipatesthatWaterand Sewer Fundexpenseswillfallby $180,480 to $14,374,940. Personnel costs decline by $12,380 with the reclassification ofoneSeniorAccountantposition. Transferstothevariouscapitalprojectfundsdecrease by$226,260aftercash-fundingseveralprojectsduringFY2025. Partiallyoffsettingthese savings, debt service expense grows by $145,860 due to the issuance of bonds for the wastewater treatment plant expansion and other utility projects.

WATER & SEWER FUND RESERVE LEVEL

BelowisachartoftheWater&SewerFund’sunrestrictednetassetbalancesforthepast two years, an estimated balance for the fiscal year ending September 30, 2025, and the projected balance for the fiscal year ending September 30, 2026. Reserve levels may increaseattheendofFY2025due tounanticipatedsavingsfromadelayin the issuance of bonds. Though not included in the FY 2026 Annual Budget, these savings may be

used for future capital projects. With reserves totaling 50.4% of expenses, the Water & Sewer Fund will remain compliant with the fund balance policy at the end of FY 2026.

$8,000,000

$7,000,000

$6,000,000

$5,000,000

$4,000,000

$3,000,000

DRAINAGE FUND

The mission of this fund is to maintain a stormwater management system that efficiently conveys storm water in a safe manner and prevents flooding. The Drainage Fund is consideredautilityofthecity. Resourcesareusedtofunddrainage-relatedexpenditures including the Nolan Creek flood warning system and public education efforts.

The revenue for the Drainage Fund is generated by thecity’s drainage fee. Theadopted drainagefeeremainsunchangedat$5.00permonthforsinglefamilydwellings. Drainage fee revenues are expected to grow by five percent to $682,600 in FY 2026, while budgetedexpenses total $620,910. The Drainage Fund remains compliant with thefund balance policy with a projected reserve balance of 57.0% of budgeted expenses.

HOTEL OCCUPANCY TAX FUND

The Hotel Occupancy Tax Fund records the receipt and distribution of the hotel occupancy tax, which is levied at seven percent of the room rental rates. The City of Belton also receives a small portion of Bell County’s hotel occupancy tax. Authorized by

state statute and approved by City Council, expenditures promote tourism and the hotel industry. ForFY2026,revenueintheHotelOccupancyTaxFundisprojectedtogrowby 14% to $596,540 asnumerous special events draw visitors into thecity. Expenditures in FY 2026 total$523,630.

TIRZ FUND

The TIRZ Fund is used to account for the accumulation of resources from ad valorem taxes collected on the incremental tax values in the Belton Tax Increment Reinvestment ZoneNo.1.Theserevenuesmayonlybeexpendedonprojectswithinthezonethathave been approved by boththe TIRZBoardand the City Council. TheCity of Belton and Bell CountyparticipateintheTIRZ. In2022,theboundaryofthezonewasexpandedby1,168 acres to a totalof 4,384 acres. The TIRZ will expire in 2042.

TIRZFundrevenuecontinuestogrowrapidlyascapturedpropertyvalueswithinthezone swell. Total revenues that are reflected in the FY 2026 Annual Budget increase by thirteen percent from $3,496,920 to $3,959,720. At $2,064,980, expenditures will decrease with less funding transferred for future capital projects.

INFORMATION TECHNOLOGY FUND

The Information Technology Fund is an internal service fund that is used to account for all costs of providing general information technology services to city divisions. These activities are financed through charges to the divisions for services rendered. FY 2026 revenues total $1,538,110 while expenditures equal $1,526,140 to replace data center servers, phones, and several computers.

BUILDING MAINTENANCE FUND

TheBuildingMaintenanceFundisanotherinternalservicefundthataccountsforallcosts ofprovidingbuildingmaintenancethroughouttheorganization. Chargestootherdivisions total $412,270, while expenditures total $485,130. This fund will draw down reserves in FY 2026 by $72,860.

ECONOMIC DEVELOPMENT FUND

The Economic Development Fund was created in 1991 pursuant to the ½ percent economic development sales tax approved by voters in 1990. This additional sales tax can only be used for economic development purposes. Acting through the Belton Economic Development Corporation, Inc., a governmental nonprofit corporation, the purpose of this fund is to promote, assist, and enhance economic development activities within the City of Belton.

RevenuesintheFY2026 AnnualBudgetareessentiallyflat at$3,750,500. Although the corporation’s primary source of income, sales tax revenue, is expected to increase by fourpercentoverFY2025,adecreaseinmiscellaneousincomeoffsetsthegain. Totaling

$1,248,250,expendituresinFY2026include$150,000forentryfeatureswithintheBelton Business Park and $300,000 for infrastructure projects.

CONCLUSION

Conservative management has placed the City of Belton in a soundfinancial position. A growing property tax base provides resources to cover the increasing demand for city services,andsalestaxrevenuecontinuestorise. Nonetheless,thecitywillbechallenged with increasing costs in most areas from personnel to capital projects.

The FY 2026 Annual Budget, while continuing prior year commitments to improve services and facilities, reflects a balanced approach to the multi-faceted needs of a growing community. This budget continues to build on the city’s successes, moving steadily forward, seeking tomeet the dual goal of preserving community character, while prudently planning forfuture growth.

The leadership of the City Council, as well as its time and attention during the development of the FY 2026 budget, is greatly appreciated. Gratitude is also extended to Department Heads and staff members for their work and dedication to serving the community.

Sam A. Listi

Michael Rodgers, CPA City Manager Director of Finance

Created by Resolution No. 030591-1 Three-Year Terms

Name Term Expiration

Brandon Bozon, President

November 30, 2025

Marion Grayson November 30, 2025

John R. Holmes, Sr. November 27, 2027

Tyson McLaughlin November 30, 2026

Stevie Spradley November 30, 2026

Central Texas Housing Consortium Board Two-Year Terms

Name Term Expiration

Marvin Bell January 24, 2026

Malinda Golden January 27, 2027

Ethics Commission

One-Year Terms

Created by Ordinance No. 2005-47

Name Term Expiration

Dr. Jude Austin II

John Glanzman

Amanda Lufburrow

Brooke Morrow

Nicholas Rabroker

Mike Ratliff

May 27, 2026

May 27, 2026

May 27, 2026

May 27, 2026

May 27, 2026

May 27, 2026

Cathy Fox May 27, 2026

Amy Casey, Secy Virtue of position

Historic Preservation Commission

Two-Year Terms

Created by Ordinance No. 2012-18

Name Term Expiration

T.C. Lipe

Ann West

Eric Urben

Barrett Covington

Ashley Potts

September 10, 2026

September 10, 2026

September 10, 2026

September 8, 2027

September 8, 2027

Tina Moore Virtue of position

Building and Standards Commission

(Replacing Housing Board of Adjustments & Appeals)

Two-Year Terms

Created by Ordinance No. 2020-42

Name Term Expiration

Brian Johnson

Eric Haugeberg

November 10, 2026

December 13, 2026

Ralph Masters January 12, 2027

Priscilla Linnemann November 10, 2026

Samantha Crumbaugh

November 10, 2026

Elizabeth Scamardo (Alternate) November 10, 2026

Clinton Bailey (Alternate) November 10, 2026

Library Board of Directors

Three-Year Terms

Created by Ordinance February 28, 1933

Name Term Expiration

Melinda Lanham

Roxanne Sanders

Kerri H. Pridemore

Meg Wagner

August 13, 2028

November 30, 2026

November 26, 2027

November 26, 2027

Ann Locklin November 30, 2028

Chad Green August 13, 2028

Janice Pustka November 30, 2025

Municipal Judge & Associate Judge

Name Term Expiration

Steve Lee, Judge

Jasmine Rios-Harding, Associate Judge

Parks Board

Two-Year Terms

Created by Ordinance No. 51083-3

May 13, 2027

May 13, 2027

Name Term Expiration

Ted Smith

Josh Pearson, Chair

Oscar Bersoza

Diane Ring

Jason Wolfe

Kayla Potts

June 20, 2027

June 20, 2026

June 20, 2026

June 20, 2027

June 20, 2027

January 28, 2027

Jim Deeken January 28, 2027

Planning and Zoning Commission

Two-Year Terms

Created by Ordinance No. 52885-1

Name Term Expiration

Ty Taggart

Quinton Locklin

Brandon Skaggs

Damon Gottschalk

Brett Baggerly

Alton McCallum

Dominica Garza

Justin Ruiz

Lisa Kamprath

May 28, 2026

June 13, 2027

May 28, 2026

May 28, 2026

June 24, 2027

May 28, 2026

June 13, 2027

June 13, 2027

May 28, 2026

Police and Fire Civil Service Commission

Three-Year Terms

Created by Ordinance No. 96-27

Name Term Expiration

Larry Thompson

Jimmy Rowton

September 24, 2026

September 24, 2028

Jerry Samu September 24, 2027

Public Property Finance Corporation Board of Directors

Six-Year Terms

Created by Ordinance No. 51987-1

Name Term Expiration

Vacant August 12, 2029

Stephanie O’Banion

Daniel Bucher

August 12, 2029

August 12, 2029

Tax Increment Reinvestment Zone Board

Two-Year Terms

Created by Ordinance No. 2004-64

Name Term Expiration

David Blackburn, Chair

Barbara Bozon, Vice Chair

Stephanie O'Banion

Craig Pearson

Russell Schneider

Sam Listi, City Manager, Ex Officio

January 13, 2027

January 13, 2027

January 13, 2027

January 13, 2027

January 13, 2027

Virtue of position

David K. Leigh, Councilmember, Ex Officio Virtue of position

Amy Casey, City Clerk, Ex Officio

Virtue of position

Youth Advisory Commisssion

One-Year Terms

Created by Ordinance No. 2007-20

Name Term Expiration

Anahitaa Malhorta (Chair) September 9, 2026

Jada Gage September 9, 2026

Alexandra Bui September 9, 2026

Jasmine Vuong September 9, 2026

Shreya Muni September 9, 2026

Matthew Bates September 9, 2026

London Preston September 9, 2026

Malachi Santana September 9, 2026

Claire Gouveia September 9, 2026

Zoning Board of Adjustments

Two-Year Terms

Created by City Council April 1971

Name Term Expiration

Mat Naegele

June 25, 2026

Amanda Hendrick August 22, 2027

Judy Owens August 26, 2027

Nelson Hutchinson June 25, 2026

Garrett Smith August 22, 2027

Martina Martinez (Alternate) August 26, 2027

Ben Burnett (Alternate) September 12, 2027

THE BUDGET PROCESS

The City Charter establishes the fiscal year, which begins October 1 and ends September 30.Each February, Department Heads receive budget request packets from the Finance Department. These packets contain information about the department, including historical expenditure amounts, current expenditure and budget amounts, and estimated expenditure amounts for the upcoming budget year.

While the departments are preparing their budget requests, the Finance Department calculates personnel costs, debt service requirements, and revenue projections for the new year. This data combined with the department requests form a preliminary or "first draft" budget.

After receiving the first-draft budget from Finance, the City Manager conducts a series of meetings with the individual Department Heads to discuss their budget requests. Held in March, these meetings help the City Manager formulate his priorities and work agenda.

A series of City Council budget workshops are held, usually in May and June. These workshops are open to the public. Information as to date and time can usually be found in the local media coverage. The workshops allow the City Council to receive input on the budget from the City Manager, the various departments, and Finance. It is through these workshops, as well as discussions with city staff, that the Council forms its priorities and work program for the proposed budget.

With guidance from the Council, the City Manager then formulates a proposed budget that is submitted to Council in July. State law and the City Charter require that a public hearing on the proposed budget be held before the Council votes on its adoption. A notice of the public hearing is published in the local newspaper, and the hearing is held during a regular City Council meeting. This hearing provides an opportunity for citizens to express their ideas and opinions about the budget to their elected officials.

After the public hearing, the City Council votes on the adoption of the budget. If the budget is not accepted and formally approved by the City Council before September 28, the budget submitted by the City Manager is deemed to have been finally adopted by the Council until such time as the Council adopts a budget.

After adoption of the budget, the City Manager may approve transfers of any unencumbered budget amount or portion thereof between general classifications of expenditures within a division or department. At the request of the City Manager and within the last three months of the fiscal year, the Council may by resolution transfer any unencumbered appropriation or portion thereof from one division or department to another. The city budget may be amended and appropriations altered in accordance therewith in cases of public necessity after conducting a public hearing called for such purpose.

Budget Calendar - Flow Chart

The following chart summarizes the budget process and the various steps leading to the adoption of the Fiscal Year 2026 Budget. JanFebMarAprMayJunJulAugSepOctNovDec

Strategic Planning:

Review and update Capital Improvement Projects as needed

Revenue projections developed

Budget orientation

Budget Development:

Budget staff prepares and send budget materials to divisions

Divisions prepare draft operating budgets

Budget review sessions with City Manager

City Council budget work sessions

Finance staff compiles Proposed Annual Budget

Proposed Annual Budget filed with City Clerk and published

Finalize and Adopt:

Finance staff finalizes Annual Budget

Public hearing on Annual Budget

City Council adopts annual budget

Public hearing on proposed tax rate if necessary

City Council adopts a tax rate

Annual budget published

Amend budget if necessary (after fiscal year has begun)

CITY OF BELTON Budget & Tax Calendar

FY 2026

2025 Dates Event Requirement/Action

February 1 to February 28

March 3

Budget preparation

Budget requests due

March 4 BEDC Board meeting

March 10 to March 31 Department meetings

April 1

April 22

May 6

BEDC Board meeting

Regular Council meeting

BEDC Board meeting

May 8 TIRZ Board meeting

May 27 Regular Council meeting

June 10 Regular Council meeting

June 24 Regular Council meeting

July 8

Regular Council meeting

July 21 Certified tax roll

August 8 Newspaper notice

August 12 Regular Council meeting

Departments prepare budget requests

Detailed line‐item requests are returned to Finance

BEDC budget kickoff

Departments meet with City Manager and Finance to discuss budget requests

BEDC budget workshop

Workshop to discuss Strategic Plan and long‐term goals for the City of Belton

BEDC approves its FY 2026 budget

TIRZ approves its FY 2026 budget

General Fund and Debt Service Fund

Water and Sewer Fund and Drainage Fund

General Fund and Debt Service Fund update if needed

Hotel Occupancy Fund, TIRZ, Information Technology Fund, Building Maintenance Fund, and BEDC

Discuss 2026 – 2030 Capital Improvements Program

Present the FY 2026 Proposed Annual Budget to City Council (Must be filed with Clerk at least 30 days before budget adoption)

Post proposed budget on City website

Call for public hearing on budget

BCAD delivers certified ad valorem tax values

Publish notice of public hearing on budget (10 – 30 days before hearing)

Budget updates if needed

Present the Strategic Plan

Present fee schedule

Propose an ad valorem tax rate for tax year 2025/fiscal year 2026

Call for public hearing on tax rate, if it exceeds no‐new‐revenue tax rate

Call for public hearing on Strategic Plan

Post proposed tax rates on website

August 26 Regular Council meeting

August 27 Newspaper notice

September 9 Regular Council meeting

Public hearing on budget (at least 15 days after filing with City Clerk)

Public hearing on Strategic Plan

Public hearing on fee schedule

Publish in newspaper and on City website the notice of public hearing on tax rate (if exceeds no‐new‐revenue tax rate, must be at least 5 days before hearing)

Continuous website notice of PH on tax rate (at least 7 days before hearing)

Public hearing on tax rate

Ratify tax revenue increase in budget, if necessary

Adopt fee schedule

Adopt Strategic Plan

Adopt FY 2026 Annual Budget

Adopt ad valorem tax rate (no more than 60 days after receipt of certified tax roll)

*The budget and tax rate must be adopted no later than 78 days before the uniform election date (August 18, 2025) if the City plans to adopt a tax rate that exceeds the greater of the voter‐approval rate or the de minimis rate. If a rate lower than the voter‐approval rate is proposed on August 12, 2025, adoption of the budget and tax rate can occur in September.

The General Fund and the Water & Sewer Fund are considered major funds as each comprises more than 10% of the revenues or expenditures of the total appropriated budget.

Capital project funds are excluded from the annual budget process because appropriations are project based.

Government Functions, Funds, and Divisions

CITY OF BELTON PERSONNEL SUMMARY FISCAL YEAR 2026

Note: Positions are shown as full-time equivalent (FTE)

Budgeted Personnel Positions by Division (Full-time Equivalents)

City Positions (FTE)

Notes: Seasonal employees are hired during the summer as recreation staff. There count is not reflected

Strategic Goals and Strategies

During its strategic planning session, the City Council identified six pillars upon which long-term goals and initiatives should be based. The strategic pillars and goals reflect the vision of the City of Belton. They serve as the foundation for the development of the annual budget. The departmental goals and initiatives demonstratethestepsthatwillbetakenduringtheyeartoaccomplishtheorganization-widestrategicgoals. The complete City of Belton Strategic Plan is included in a separate section of this document,

The six strategic pillars and associated goals are summarized below.

Connectivity

Create mitigation strategies for IH-35/IH-14 widening project

Coordinate transportation projects with FHA,TXDOT, Bell County

Complete local street projects

Enhance the park/trail system

Explore new connectivity solutions

Economic / Business Development

Enhance collaborative partnerships between the City and BEDC

Create a utilities/infrastructure strategy to lead future land development

Established a focused downtown strategy

Explore multi-tenant public and private development

Prepare an update of business recruitment/retention objectives and tourism goals

Enhance community partnerships in employment efforts

Quality of Life

Enhance the quality of life through planning, park development, and recreation programming, preservation and partnerships

Infrastructure / Public Facilities

Address infrastructure and public facility needs through analysis and multi-year funding strategies

Engagement

Communicate proactively with citizens

Enhance community engagement in events and activities

Monitor and improve the development review process

Public Safety

Establish the Belton Public Safety Center

Determine the future Fire Department building facilities plan

Address ongoing emergency preparedness

Total Adopted Budget

Cityof Belton, Texas

Fiscal Year 2026 Annual Budget

All Funds Summary

Revenue Funds

Notes:

Capital project funds are excluded from presentation because they are not part of the annual appropriations process. Appropriations for capital projects are made on a project basis and carry over until the project is completed.

The General Fund and Water & Sewer Fund are consider major funds.

Funds

1,963,000

473,820

Cityof Belton, Texas

Consolidated Statement of Fund Balance

Budget Year 2026

Projected Fund Balance

1 Excludes use of prior years' fund balance

Reason for significant changes in fund balance, if any:

General Fund - The decreases in FY 2025 and FY2026 reflect a planned drawdown of reserves.

Debt Service Fund - The increase in reserves is due to transfers from the General Fund for future debt payments.

Hotel Occupancy Tax Fund -Changes reflect revenue growth and relatively lowlevel of spending.

TIRZ Fund - Changes reflect revenue growth and capital spending.

Water & Sewer Fund - The increase in FY2025 will be used for future capital project funding.

Drainage Fund - The increase in FY2026 will be used in future year capital project funding.

Information Technology Fund - The decrease in FY2025 is due to capital purchases.

Building Maintenance Fund - The decrease in FY2026 is due to a planned drawdown of reserves.

BEDC Fund - FY2025 reflects land acquisitions. FY2026 reflects the low level of spending compared to revenues.

Cityof Belton, Texas Consolidated Schedules of Resources and Expenditures

Fiscal Years 2023 - 2026 All Budgeted Funds1

1 Capital projects funds are excluded from presentation because they are not part of the annual appropriation process. Appropriations for capital projects are made on a project basis and carry over until the project is completed.

Cityof Belton, Texas

Consolidated Schedules of Resources and Expenditures

General Fund

Fiscal Years 2023 - 2026

Cityof Belton, Texas

Consolidated Schedules of Resources and Expenditures

Debt Service Fund

Fiscal Years 2023 - 2026

Cityof Belton, Texas

Consolidated Schedules of Resources and Expenditures

Hotel OccupancyTax Fund

Fiscal Years 2023 - 2026

Cityof Belton, Texas

Consolidated Schedules of Resources and Expenditures

TIRZ Fund

Fiscal Years 2023 - 2026

Cityof Belton, Texas

Consolidated Schedules of Resources and Expenditures

Water & Sewer Fund

Fiscal Years 2023 - 2026

Cityof Belton, Texas

Consolidated Schedules of Resources and Expenditures

Drainage Fund

Fiscal Years 2023 - 2026

Cityof Belton, Texas

Consolidated Schedules of Resources and Expenditures Information TechnologyFund Fiscal Years 2023 - 2026

Cityof Belton, Texas

Consolidated Schedules of Resources and Expenditures

Building Maintenance Fund

Fiscal Years 2023 - 2026

Cityof Belton, Texas

Consolidated Schedules of Resources and Expenditures

BEDC Fund

Fiscal Years 2023 - 2026

Overview

TheGeneralFundisthechiefoperatingfundofthegovernment. Itisusedtoaccountforall currentfinancialresourcesnotrequiredbylaworadministrativeactiontobeaccountedforin designatedfunds. Theprimarygovernmentalfunctionsoccurringwithinthisfundarepolice andfireprotection,parks,library,streets,andgeneraladministrativeoperations. Operations withinthe General Fund arelargely funded fromtaxes. Propertytaxescomprisethirty-nine percentofrevenues,whilesalestaxesgeneratetwenty-sevenpercent.Otherrevenuesinclude franchise taxes, fines, fees, and charges for services such as garbage collection. The organizationalstructureofthisfundcanbebrokenintospecificdivisionsofthegovernment thatarebaseduponthefunctionthateachserves. Relateddivisionsmayformadepartment withconsolidatedmanagement.

Overview

Debt Service Fund is used for payment of the City's long-term debt. Bond obligations have been used to purchase parkland, park improvements, street and sidewalk improvements, bridges, Police Department expansion, and traffic improvement projects. Below are just a few of the projects that have been funded in the past.

Overview

The hotel occupancy tax was established in 1959 and given authority to municipalities in the 1970's. This tax was instituted and restricted to promote tourism and the convention/hotel industry. Belton is thankful to have the Bell County Expo center that brings many visitors to Belton. The City plans many events for FY 26 including Christmas on the Chisholm Trail, 4th of July events, B4 festival and an Octoberfest event .

TheWater& Sewer Fundaccounts forthe City'swaterandsewer operations. Beingan enterprise fund, itis designedtobe financedand operatedinamannerlikeprivatebusinesses. Thecostforprovidingtheseservicestothepublicistoberecoveredprimarilythroughuser charges. Capital improvements are often funded through Capital Project Funds, which are not included in the annual operating budget. MaintenanceofutilityinfrastructureisprovidedbytheWater&SewerFund.

WATER & SEWER RATES

EFFECTIVE NOVEMBER 2025 BILLING

We will not appreciate water until the well runs dry -Benjamin Franklin

The Belton City Council approved a resolution Tuesday, August 13, 2024, that endorsed a four-year water and wastewater rate structure designed to help pay for significant upcoming infrastructure costs, address concerns about high sewer bills during the summer months, protect the most vulnerable water customers from escalating costs, and encourage water conservation. Due to the delay in upcoming infrastructure projects and bond issuances, it is recommended that rates for FY 2026 remain at FY 2025 levels.

New Ways to Pay Your Bill

The City has introduced several new ways to payyourutilitybill.Alongwithbankandcredit card drafts, customers can now receive and payutilitybillsthroughamobileapp(MyCivic Utilities) and text-to-pay. Customers can call 833-234-0898 to pay by telephone. To download the app Search for My Civic Utilities in the App Store or on Google Play or use one oftheQRcodestosignup.

PLANNING FOR FUTURE GROWTH

Delivering Excellence

Capital Improvement Projects are identified through the City of Belton's Strategic Capital Improvement Plan to ensure exceptional service for Belton residents. As the population increases,efficiently managing waterdeliverybecomescritical. Furthermore, expanding and maintaining water and sewer infrastructurewillremainakey focus to sustain service excellence.

Overthenextfiveyears,theCityofBeltonplansto spend more than $19 million on water and sewer projects to expand capacity and distribution. Several projects replace failing or undersized utility lines. Two bond issuances may occur over the five-year time frame. Significant projects include:

$12 MILLION

This project includes the installation of a second North-South water transmission line to increase water volume and capacity to the southernareasofthecommunity.

$4 MILLION

This project will upsize the existing sewer line to handle flows from Shanklin/BISD/Three CreeksthroughMitchellBranch.

This project replaces failing sewer lines underneath E. 6 AvenuefromMaintoComay. th WHEAT ROAD WATER LINE

$2 MILLION

Android AppleIOS

CITY OF BELTON

WATER RATES

BASE RATE STRUCTURE

Water base rates are charged by meter size, which is the industry standard. This recognizesthatlargermetersputagreater demand on the water system. The base rate includes 2,000 gallons for domestic consumption. Almost 90% of water customers have a 5/8-inch meter. For FY 2026,thebaseratefora5/8-inchmeterwill be $18 per month. The base rate for other meter sizes is shown in the following table. Allrateslistedinthefollowingtablesarefor CityofBeltonresidents.Thoseoutsideofthe citylimitswillpay1.25timesthecityrate.

VOLUMETRIC WATER RATE STRUCTURE

Thevolumetricrateischargedforeach1,000gallonsofwater consumed. There are four customer classes: residential, multi-family, commercial, and non-residential sprinkler. Residential and non-residential sprinkler customer classes have a tiered rate structure while multi-family and commercial customer classes will continue being charged flat rates. With the new tiered rate structure, customers who consume less water will pay a lower rate than those who consume more water which promotes conservation. For FY 2026, water rates will remain at FY 2025 rates. A comparison ofthewatervolumetricratesforFY2025andFY2026isshown inthetablesbelow.

RESIDENTIAL CUSTOMER CLASS

MULTI-FAMILY & COMMERCIAL CUSTOMER CLASS

NON-RESIDENTIAL SPRINKLER CUSTOMER CLASS

OUTSIDE CITY LIMITS SERVICES

City services are extended outside of the city limits in certain instances. These water and sewer services are billed at a rate of 125% the inside city limit rates. Customers with these services will have an account number beginning with 38, 39, 46, 49, or 56. The base rate for water begins at $22.50 and the sewer base rate is $22.43, volumetric rates are listed below.

SEWER ONLY CUSTOMERS

SomeresidentswithintheCitylimitsofBelton have water provided by another entity, Dog RidgeWaterSupplyor439WaterSupply,and sewer service provided by the City of Belton. These customers are billed for sewer based ontheirwaterconsumption.Thesecustomers will also be billed based on their winter averageconsumptionforwater.

439 WATER SUPPLY CUSTOMERS

Customersservicedby439WaterSupplyand connected to City of Belton sewer have an accountnumberbeginningwith41.Attheend of each month, water meter reads are provided to the City of Belton by 439 Water Supply. These reads are used to determine the amount of sewer billed. The winter average for water consumption will be used to determine the amount of sewer billed for thesecustomers.

DOG RIDGE WATER SUPPLY CUSTOMERS

Customers serviced by Dog Ridge Water SupplyandconnectedtoCityofBeltonsewer have an account number beginning with 56. On the 25th of each month, the City of Belton reads the waters meters for these accounts. These reads are used to determine the amount of sewer billed. The winter average for water consumption will be used to determine the amount of sewer billed for thesecustomers.

SEWER RATES

Forresidentialcustomers,winter-averagingwillbeinstitutedfor wastewater volumetric charges. Sewer charges will be based upon the average water consumption for the months of December, January, and February as consumption during thesemonthsbetterrepresentstheamountofwastewaterthat returns to the sewer treatment plant. The winter average then becomes the billed sewer volume for which sewer charges are applied throughout the year. New customers who have not establishedawinteraveragewillbechargedbasedupon6,000 gallons of usage until a winter average is determined. Multifamilyandcommercialclasswastewaterrateswillbebasedon water consumption. The non-residential sprinkler class will not paysewer,sincetheselinesareprimarilyforirrigation.

The Drainage Fund is responsible for maintainingtheCity'sdrainagesystemand protecting the water quality through stormwater maintenance. Belton has several bodies of water, and a landscape that has many elevation changes. This can be a potential problem if drainage is not a priority. The City is blessed to have an amazing staff that addresses these issues on a preventative basis to ensure great customerservicetoourcitizens.

StormwaterPollution

The Information Technology Departmentis responsible for the developing, securing andstoringof electronic dataandassistingintheuseofsoftwarethroughouttheentire Cityof Belton. 239 Equipment Maintained

BuildingMaintenanceFund

Overview

The Building Maintenance Departmentprovidescleanlinessandmaintenancetoall Cityfacilities. The Citycurrently haseightmainfacilities,manysmallbuildingsatpublicworksandparks,aswellastraillights. ommunityCenter

Central FireStation

53,827 SquareFeet

STRATEGICPLANNINGINBELTON,TEXAS 2000 -Present

The City Council began an in-depth strategic, long-range planning project in 2000. The objective of this project was to identify long-range problems, challenges, and opportunities for the City of Belton, and to develop and pursue appropriate strategies to address these issues. The development process included Councilmembers, City of Belton staff, and the public. The result was a Strategic Plan to provide the framework of annual budgets and guidance for departmental goals and objectives.Belton’s commitment to Strategic Planning remains a cornerstone of its legacy of conscientious planning for its future.

As a prelude to Belton’s budget process, a review and update of the Strategic Plan occurs each year. This may be a comprehensive review, which should occur at least once every five years, or an in-house update. A comprehensive review occurred in 2025for FY 2026-2030,with a complete plan refreshand changes in the focus of Goals. Beltoncontinuestohaveabrightfuturewiththisongoingcommitmentto strategic planning through the Council’s visionary leadership.

Strategic Plan Session May 30-31, 2025 with Facilitator Hilary Shine, SGR

City of Belton, Texas

Strategic Plan Background, Definitions and Process

FY 2026-2030

Vision and Mission

The Vision and Mission statements serve as a common framework for all citizens of the City of Belton and form the foundation for all activities within the city’s governmental structure. These statements serve as the common values of the community, which gives inspiration and directs the actions of all stakeholders, members of the council, and city staff.

Below are the Vision and Mission statements of the City of Belton, as well as the seven Goal Categories and Outcome Statements. These elements of the current Strategic Plan were discussed, and the City Council agreed that these Statements were appropriate, remain valid, and continue to articulate the direction to be pursued in the next several years.

Vision Statement

Belton is the Community of Choice in Central Texas, providing an Exceptional Quality of Life.

Mission Statement

Enhance Belton’s quality of life through visionary leadership that preserves its character while planning for its future.

Six Pillars of Emphasis

1.Connectivity

2. Economic/Business Development

3.Quality of Life

4.Infrastructure/Public Facilities

5.Engagement (Service Delivery Included)

6.Public Safety

Highlights of Initiatives in each Pillar include:

1.Connectivity

Youth Advisory Commission

Critical and underway street, trail and sidewalk projects – IH-35/IH-14; Loop 121; 6th Avenue; FM 93; TX 317; Central/Spring Street Bridge; Connell Street; Wheat Road Extension

2.Economic/Business Development

Imagine Belton Implementation; Utilities to BEDC properties; Updating Building Codes; Land-scaping/Murals/Sidewalks; Public/Private Facility opportunities; Business and Employee Recruitment/Retention due to IH-35/IH-14 construction

3.Quality of Life

Growth Management/FLUM; Parks Master Plan; Belton’s Historical Cultural Resources; Partnerships

4.Infrastructure/Public Facilities

Water/Wastewater Master Plan; TBWWTP Upgrade; Central Texas Water Alliance; Annual Street Maintenance Program; Water/Sewer CCN Boundary Analysis

5.Engagement

National Citizen Survey Recommendations; Citizen Education Process for Boards/ Volunteers; Continuing Provision of Exceptional Customer Service; Marketing Plan; Enhance Development Review Process

6.Public Safety

Miller Heights Assessment/Phased Occupancy; Fire Station Location Needs Assessment; Mental Health Needs Awareness; Cybersecurity; Community Safety; Emergency Conditions for FD, PD, PW

City of Belton, Texas

Strategic Plan

Recurring Prioritization Process

FY 2026-2030

This Plan is a living document that is driven by flexible long-term goals. Year 1 (FY 2026) Pillars include detailed Action Plans. Years 2-5 Action Plans (FY 2027-2030) are provided with best known information at this time, recognizing these longer term goals are a function of priority and funding.

Goal worksheets for each actionable goal are provided. The Action Plan worksheets include:

Pillar of Emphasis

Goal

Initiative

Coordinator and Assistance

Outcome Description

Performance Indicators

Challenges and Barriers

Partner Agencies

Timelines

Cost and Funding Sources

The City Council is committed to reviewing long-term goals regularly to ensure community focus and direction, carefully looking five years into the future, and beyond. This Strategic Plan reflects actionable Goals and is now linked to a regularly updated Five Year Capital Improvement Plan of Projects, to guide Strategic Plan Implementation.

Strategic Goals and Strategies

During its strategic planning session, the City Council identified six pillars upon which long-term goals and initiatives should be based. The strategic pillars and goals reflect the vision of the City of Belton. They serve as the foundation for the development of the annual budget. The departmental goals and initiatives demonstrate the steps that will be taken during the year to accomplish the organization-wide strategic goals. The complete City of Belton Strategic Plan is included in a separate section of this document,

The six strategic pillars and associated goals are summarized below.

Connectivity

Create mitigation strategies for IH-35/IH-14 widening project

Coordinate transportation projects with FHA, TXDOT, Bell County

Complete local street projects

Enhance the park/trail system

Explore new connectivity solutions

Economic / Business Development

Enhance collaborative partnerships between the City and BEDC

Create a utilities/infrastructure strategy to lead future land development

Established a focused downtown strategy

Explore multi-tenant public and private development

Prepare an update of business recruitment/retention objectives and tourism goals

Enhance community partnerships in employment efforts

Quality of Life

Enhance the quality of life through planning, park development, and recreation programming, preservation and partnerships

Infrastructure / Public Facilities

Address infrastructure and public facility needs through analysis and multi-year funding strategies

Engagement

Communicate proactively with citizens

Enhance community engagement in events and activities

Monitor and improve the development review process

Public Safety

Establish the Belton Public Safety Center

Determine the future Fire Department building facilities plan

Address ongoing emergency preparedness

CITY Y OF F BELTON N STRATEGIC C PLAN N

YEAR R 1 OF F FIVE-YEAR R ACTION N PLAN: : FY Y 2026 6

PILLAR R #1 1 –– CONNECTIVITY Y

1.1 Create Mitigation Strategies for IH-35/IH-14 Widening Project 1.1.1 Maintain dialogue with TxDOTon property access, signage, and local circulation

1.2 Coordinate Transportation Projects with FHA, TxDOT, Bell County 1.2.1 Facilitate Loop 121 project, Phase 2, IH-14 to IH-35: Utilities 2026 Funded

1.2.2 Coordinate 6th Avenuereconstruction by funding Sidewalks/Pipebursting Sewer 2026-2027 Funded

1.2.3 Monitor FM 93 widening, TX 317 to WheatRoad 2026-2028 N/A 1.2.4 Pursue TX 317 (Main Street) Study Recommendations 2026-2027 TBD

1.3 Complete Local Street Projects 1.3.1 Construct E. Central Avenue (Spring Street) Bridge over Nolan Creek 2026-2027 Funded 1.3.2 Secure ROWand Reconstruct Connell Street 2026-2030 Funded 1.3.3 Design Wheat Road Extension 2026-2027 Funded

1.4 Enhance Park/Trail System 1.4.1 Add Regional Trail Linkages 2026

4.1.1 Maintain, update, and implement Water/Wastewater Master Plan

4.1.3 Participate in Central Texas Water Alliance

4.1.4 Maintain Annual Funding for Street Maintenance

4.1.6 Update CIP

5.1.2 Implement robust citizen education process including for citizen boards, volunteerism

5.1.3 Provide exceptional customer service

5. Engagement

6. Public Safety

5.2.1 Implement Marketing Plan, Belton branding, to promote Community events

5.3.1 Address Development Review, Implement State Mandates, Adopt Building Code Updates

6.1.1 Continue phased occupancy of Public Safety Center

6.3.2 Implement Cybersecurity needs

6.3.3 Improve Community Safety

6.3.4 Address public safety emergency conditions affecting FD, PD, PW

City of Belton

Strategic Plan Pillars, Goals & Action Plan FY 2026

Pillar 1: Connectivity

Goal 1.1: Create Mitigation Strategies for IH-35/IH-14 Widening Project

Initiative 1.1.1

Maintain dialogue with TxDOT on property access, signage, and local circulation

Coordinator:

Assisted By: City Manager

Assistant City Manager

Action Plan

Outcome Description:

Performance

Indicators:

Challenges and Barriers:

City Council conveys concerns with proposed Plan to TxDOT and achieves meaningful design revisions.

Pursue comments provided to TxDOT in Summer 2025

Seek entrance and exit ramps that serve Belton interests

Recommend timely updates through TxDOT communication apps during all project phases

Achieve a signage plan that anticipates Belton destinations Engage BEDC to assist in business relocation in Belton

TxDOT funding, timeline, and federal/state design criteria

TxDOT eminent domain authority will allow property acquisition

Belton’s interests and TxDOT’s interests may not coincide Partners:

TxDOT

Local Property Owners

City Council Management Team

City of Belton

Strategic Plan Pillars, Goals & Action Plan FY 2026

Pillar 1: Connectivity

Goal 1.2: Coordinate Transportation Projects with FHA, TxDOT, Bell County

Initiative 1.2.1 1

Facilitate Loop 121 Project, Phase 2, IH-14 to IH-35: Utilities

Coordinator:

Assisted By: Assistant City Manager Director of Public Works

Action Plan

Outcome Description:

Performance

Management Team works to ensure local coordination of Loop 121 Project, Phase 2, is complete to facilitate construction.

Indicators: Finalize city design for relocation of city utilities out of Loop 121 ROW and bid project

Award bid for city utility relocation project Relocate city utilities out of Loop 121 ROW

Challenges and Barriers: Selection of contractor Timeframe for construction

Partners: TxDOT Public Works Department

Selected contractor

City

of Belton

Strategic Plan Pillars, Goals & Action Plan FY 2026

Pillar 1: Connectivity

Goal 1.2: Coordinate Transportation Projects with FHA, TxDOT, Bell County

Initiative 1.2.2 2

Coordinate 6th Ave. reconstruction by funding Sidewalks and Pipebursting Sewer

Coordinator:

Assistant City Manager

Outcome

Description:

Performance

Indicators:

Assisted By:

Director of Public Works Director of Development Services

Action Plan

Management Team coordinates with TxDOT on design for major maintenance project on 6th Avenue, IH-35 to TX 317.

City designs, funds, and pipebursts sewer line, while also relocating small section of water line, prior to street construction City authorizes TxDOT agreement to fund local share of 5’ sidewalk project on both sides

TxDOT finalizes design and reconstructs 6th Avenue to include street pavement, curbs, gutters, and sidewalks

Challenges and Barriers: TxDOT, KTMPO funding allocation

Competition with other area projects – IH-35/IH-14 Rising prices for materials

Partners: TxDOT TIRZ Board

COB Public Works Department KTMPO

$1,500,000

City of Belton

Strategic Plan Pillars, Goals & Action Plan FY 2026

Pillar 1: Connectivity

Goal 1.2: Coordinate Transportation Projects with FHA, TxDOT, Bell County

Initiative 1.2.3 3 Monitor FM 93 widening, TX 317 to Wheat Road

Coordinator:

Assisted By: Assistant City Manager Director of Public Works Director of Development Services

Action Plan

Outcome Description:

Management Team monitors TxDOT progress on FM 93 (2nd Avenue) widening project, recognizing need for ROW acquisition is to be determined. Performance Indicators: Participate in TxDOT project updates on design and funding Monitor KTMPO source for funding in TIP Anticipate TxDOT agreement as project gets closer Challenges and Barriers: Funding limitations for ROW and construction may delay project ROW acquisition may require relocation and delay project Roundabout at 2nd Avenue/FM 93 could impact project Partners: TxDOT

City Management Team

KTMPO

Local Property Owners

City of Belton

Strategic Plan Pillars, Goals & Action Plan FY 2026

Pillar 1: Connectivity

Goal 1.2: Coordinate Transportation Projects with FHA, TxDOT, Bell County

Initiative 1.2.4 Pursue TX 317 (Main Street) Study recommendations

Coordinator:

Assisted By: Assistant City Manager Director of Public Works

Action Plan

Outcome

Description:

Performance

Indicators:

Challenges and Barriers:

Partners:

TX 317 (Main Street) Traffic Study Recommendations pursued by City staff with TxDOT District Officials.

TxDOT/COB coordinate comprehensive signal timing update Process established for signal timing update to occur regularly in future TxDOT prepares designs for roundabouts and coordinates ROW acquisition with City

TxDOT/KTMPO fund reconstruction project

TxDOT roadway requires extensive coordination ROW needed for roundabouts

TX 317 is only north/south city alternative to IH-35, complicating construction

City of Belton

Strategic Plan Pillars, Goals & Action Plan FY 2026

Pillar 1: Connectivity

Goal 1.33: Complete Local Street Projects

Initiative 1.3.1 Construct E. Central Avenue (Spring Street) Bridge over Nolan Creek

Coordinator:

Assisted By: Assistant City Manager Director of Public Works Director of Finance

Action Plan

Outcome Description:

Performance

Indicators:

E.Central Avenue (Spring Street) bridge constructed over Nolan Creek.

Design plans completed by COB and approved by TxDOT (CPF review)

COB bids and awards project

Construction project initiated Challenges and Barriers:

TxDOT coordination process

IH-35/IH-14 project relationship

FEMA Flood Plain

Partners: TxDOT

Federal Government (CPF)

Design Engineer Contractor

$5,000.000 $1,200,000

Community Project Funding (federal grant) TIRZ (local match)

City of Belton

Strategic Plan Pillars, Goals & Action Plan FY 2026

Pillar 1: Connectivity

Goal 1.33: Complete Local Street Projects

Initiative 1.3.2 Secure ROW and Reconstruct Connell Street

Coordinator:

Assisted By: Assistant City Manager Director of Public Works

Action Plan

Outcome Description:

Performance

Indicators:

With Connell Street design complete, staff will secure approximately 32 parcels necessary for project completion.

ROW firm secures rights-of-entry from property owners

Value determinations made and offers submitted to owners

Negotiations for ROW underway and needed before bidding project Challenges and Barriers:

Partners:

Reaching agreement on property values

Some property relocations may be needed

Minor changes in design may lead to redesign and revaluing parcels

Phase 2 Project: 2030 - $4.2M Combination KTMPO, TIRZ, Federal Grant

City of Belton

Strategic Plan Pillars, Goals & Action Plan FY 2026

Pillar 1: Connectivity

Goal 1 3: Complete Local Street Projects

Initiative 1.3.3 Design Wheat RoadExtension

Coordinator:

Assisted By: Assistant City Manager Director of Public Works

Action Plan

Outcome Description: Complete design for new north/south city collector street within secured ROW between Red Rock and Sparta Road.

Performance

Indicators:

Amend the City’s Thoroughfare Plan to change Wheat Road’s classification from an Arterial to a Collector Street. Road street section addresses need for neighborhood circulation and compatibility, sidewalk, trail, possible BRA pipeline COB initiates street design, utility extensions and trunk water line Challenges and Barriers: Neighborhood concerns about road, pipeline, other impacts to area Relationship of BRA pipeline project and timing Shift from arterial (FM 2271 extension) to collector street with adequate pedestrian, trail components

Partners: Brazos River Authority Area Property Owners

Design Engineer Public Works/Parks Departments PD/FD Emergency Services

City of Belton

Strategic Plan Pillars, Goals & Action Plan

FY 2026

Pillar 1: Connectivity

Goal 1.44: Enhance Park/Trail System

Initiative 1.4.1 Add Regional Trail Linkages

Coordinator:

Director of Parks & Recreations

Assisted By:

Assistant City Manager

Director of Development Services

Action Plan

Outcome Description: Complete Parks & Recreation Strategic Master Plan for 2026-2036.

Performance Indicators:

Develop/administer survey that evaluates ways to enhance parks, trail system

Include opportunities for improved and future park facilities, amenities

Add regional trail linkages to area cities – Temple, Salado – along Nolan Creek, rivers, highways, and arterial streets

Challenges and Barriers:

Partners:

Project costs

Right-of-way acquisition

Competition for grants

Management Team

Parks Board

City Council

Texas Parks & Wildlife (TPWD) KTMPO Citizens Area Communities – Temple, Salado

$75,000 General Fund; TIRZ; TPWD; KTMPO

City of Belton

Strategic Plan Pillars, Goals & Action Plan FY 2026

Pillar 1: Connectivity

Goal 1.44: Enhance Park/Trail System

Initiative 1.4.2 Extend City Trails/Sidewalks

Coordinator:

Director of Public Works

Outcome Description:

Performance Indicators:

Assisted By:

Director of Parks & Recreation

Director of Development Services

Action Plan

Team explores extension/provision of hike/bike trails, sidewalks, and shared use paths and reports findings to City Council.

Review subdivision standards for application along collector and arterial streets

Reiterate policy that any city public works project will include hike, bike, and pedestrian facilities

Facilities shall include ADA provisions for full participation Challenges and Barriers: Project costs

Right-of-Way acquisition

Development cost, community (public) cost, or shared cost

Partners: Management Team City Council KTMPO Citizens

Coordinator: Assisted By: Assistant City Manager Director of Public Works

Action Plan

Outcome Description:

Performance Indicators:

Team assertively explores opportunities to expand positive Belton experience with roundabout street designs; micro-transit access; and electric vehicle charging stations and reports findings to City Council.

Roundabouts: Work with TxDOT on 6th Avenue; FM 93; IH-35; IH-14

Micro-Transit Access: Participate fully with HOP on transition from fixed route to micro-transit service

EV Charging Stations: Market availability of City locations Downtown –Penelope/Central and at Library

Enhanced collaboration between City/BEDC achieves successes in business retention and attraction, talent attraction, and increased retail sales.

Performance Indicators: BEDC Board and City Council work together on projects of mutual benefit City Staff completes recommended Imagine Belton rezonings for 5 areas City and BEDC develop materials to highlight development opportunities and enhance implementation

Challenges and Barriers:

Owner concerns about changing standards

Effectively communicating increased flexibility

Market conditions may affect development, redevelopment timing Partners: City Council

BEDC Private Property Owners City Staff

City of Belton

Strategic Plan Pillars, Goals & Action Plan FY 2026

Pillar 2 2: Economic/Business Development

Goal 2 2.2: Create a Utilities/Infrastructure Strategy to lead Future Land Development

Initiative 2.2.1 Provide services to BEDC Land on IH-14/IH-35

Coordinator:

BEDC Executive Director

Outcome Description:

Performance Indicators:

Assisted By:

Assistant City Manager

Director of Public Works

Consultant Engineer

Action Plan

An infrastructure strategy for land acquired by BEDC for future development is determined, services are engineered, and a phased construction plan is outlined.

Utility service concepts are transformed into a preliminary design report with agreement on design alignment

Detailed engineering pursued on IH-14 tract first, then IH-35 tract

A phasing plan for utility construction follows, based on market and funds Challenges and Barriers:

Strategy must evaluate service to tracts or maximizing service to area

of Belton Strategic Plan Pillars, Goals & Action Plan

Pillar 2 2: Economic/Business Development

Goal 2 2.2: Create a Utilities/Infrastructure Strategy to lead Future Land Development

Initiative 2.2.2 Plan for Trunk Water Transmission Line (west)

Coordinator:

Assistant City Manager

Assisted By:

Director of Public Works

Consultant Engineer

Action Plan

Outcome Description: City initiates plans to design north/south 18” water transmission line, located generally along Wheat Road, from Sparta Road to IH-14, shown on Utility Master Plan.

Performance Indicators:

Challenges and Barriers:

Belhouse pipeline presents opportunity for co-location City determines it is timely for preliminary design of pipeline City solicits proposals and selects design team

Design cost may be significant Utility easements may be needed if a stand alone project Area for pipeline currently 439 WSC and DRWSC CCN territory

Partners: BEDC City Council 439 WSC, DRWSC

City of Belton

Coordinator:

Assisted By: Director of Development Services

Building Official Fire Marshal

Action Plan

Outcome Description: City adopts 2024 family of International Codes, including Commercial Building (IBC), Residential (IRC), Fire, Plumbing, Electrical, Mechanical, Gas Performance Indicators: Staff coordinating review of current 2015 Codes Team preparing comparison of 2015 to proposed 2024 Codes Community involvement will provide opportunity for public comment before adoption

Implementation of new Codes will occur following adoption in 2025/26 Challenges and Barriers: Opposition from developers and property owners regarding perceived cost increases

Complexity of multiple codes addressed at one time Inaction or delay in action further prevents the City from compliance with current code best practices

Partners: State Legislature

Insurance Safety Org. (ISO) Fire Department Historic Preservation Commission City’s Governance Subcommittee

City of Belton

Coordinator:

Director of Parks & Recreation: Landscaping

Director of Development Services: Murals

Outcome Description:

Performance Indicators:

Challenges and Barriers:

Assisted By:

Assistant City Manager Director of Finance

Action Plan

Belton welcomes additional public and private landscaping and encourages building murals to enliven Downtown as a destination.

P&R Department identifies opportunities for enhanced public landscaping

COB encourages private landscaping where practical – street trees, hanging baskets, parking lot islands

Murals included in TIRZ budget at annual amount of $50,000 for 5

Limited spots for landscaping in Downtown requiring creativity

Cost for landscaping, irrigation, landscape maintenance

Communicating availability of mural funds to property owners

Partners: City Council City Staff Private Businesses Chamber of Commerce

City of Belton

Coordinator:

Assisted By: Director of Public Works

Assistant City Manager

Action Plan

Outcome Description: City designs and reconstructs sidewalks along Penelope Street, from Water Street to Central Avenue, and designs additional phases along Penelope Street and 1st Avenue for future consideration.

Performance Indicators: City completes design plans for Penelope Street and 1st Avenue sidewalks City rebuilds Phase 1 along the west side of Penelope Street, from Water Street to Central Avenue

Challenges and Barriers:

Collapsed sidewalk due to subsurface conditions Keeping Cochran, Blair and Potts open during construction Penelope Street also needs to be accessible to pedestrians/vehicle traffic

Partners: City Council TIRZ Board Downtown Property Owners Design Firm Selected Contractor

Phase 1 Project: $400,000 (2026)

Phase 2 Project: Amount TBD following design (2026)

Belton

Coordinator:

Assisted By:

Assistant City Manager Director of Public Works

Director of Finance

Action Plan