ANALYSIS: CHINESE ECONOMY to-incomes must go down in EU and the US. Sorry, China, no more easy fuel for your export growth. Now that’s too bad. The Ponzi scheme of investment growth and the export growth are both collapsing. What’s left for China to seek the growth then? Domestic demand aka private consumption? It looks promising but not very convincing. Let’s examine the structural reasons why China’s domestic demand will have its work cut out in refilling the role for economic growth left vacant by collapsing investment and export. First, contrary to what many choose to believe, China’s trade surplus is not caused by Chinese consumers’ high savings rate, but has much to do with their deteriorating disposable incomes which lag far behind GDP growth and inflation. According to the All China Federation of Trade Unions (ACFTU), workers’ wages/GDP ratio has gone down for 22 consecutive years since 1983. It goes without saying that the consumption/GDP ratio is shrinking all the while. Meanwhile, Aggregate Savings Rate has increased by 51% from 36% in 1996 to 51% in 2007. Don’t jump to your conclusion yet that Chinese consumers have been over-tightening their purse strings. The truth is far from conventional perceptions. According to Development Research Center of the State Council’s report, that increase is mainly driven by the government and corporations and not by households. For the past 11 years, Household Savings Rate has only increased from 19% to 22%. Even India’s Household Saving Rate of 24% is higher than China’s right now. All the while, government and corporations’ savings rate has increased from 17% to 22%, which accounts for nearly 80% of the increase

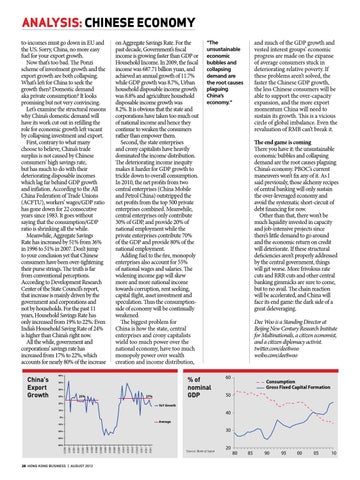

China’s Export Growth

on Aggregate Savings Rate. For the past decade, Government’s fiscal income is growing faster than GDP or Household Income. In 2009, the fiscal income was 687.71 billion yuan, and achieved an annual growth of 11.7% while GDP growth was 8.7%, Urban household disposable income growth was 8.8% and agriculture household disposable income growth was 8.2%. It is obvious that the state and corporations have taken too much out of national income and hence they continue to weaken the consumers rather than empower them. Second, the state enterprises and crony capitalists have heavily dominated the income distribution. The deteriorating income inequity makes it harder for GDP growth to trickle down to overall consumption. In 2010, the net profits from two central enterprises (China Mobile and Petrol China) outstripped the net profits from the top 500 private enterprises combined. Meanwhile, central enterprises only contribute 30% of GDP, and provide 20% of national employment while the private enterprises contribute 70% of the GDP and provide 80% of the national employment. Adding fuel to the fire, monopoly enterprises also account for 55% of national wages and salaries. The widening income gap will skew more and more national income towards corruption, rent seeking, capital flight, asset investment and speculation. Thus the consumptionside of economy will be continually weakened. The biggest problem for China is how the state, central enterprises and crony capitalists wield too much power over the national economy, have too much monopoly power over wealth creation and income distribution,

60%

% of nominal GDP

50% 40%

25%

30%

27%

20%

and much of the GDP growth and vested interest groups’ economic progress are made on the expanse of average consumers stuck in deteriorating relative poverty. If these problems aren’t solved, the faster the Chinese GDP growth, the less Chinese consumers will be able to support the over-capacity expansion, and the more export momentum China will need to sustain its growth. This is a vicious circle of global imbalance. Even the revaluation of RMB can’t break it.

“The unsustainable economic bubbles and collapsing demand are the root causes plaguing China’s economy.”

The end game is coming There you have it: the unsustainable economic bubbles and collapsing demand are the root causes plaguing China’s economy. PBOC’s current maneuvers won’t fix any of it. As I said previously, those alchemy recipes of central banking will only sustain the over-leveraged economy and avoid the systematic short-circuit of debt financing for now. Other than that, there won’t be much liquidity invested in capacity and job-intensive projects since there’s little demand to go around and the economic return on credit will deteriorate. If these structural deficiencies aren’t properly addressed by the central government, things will get worse. More frivolous rate cuts and RRR cuts and other central banking gimmicks are sure to come, but to no avail. The chain reaction will be accelerated, and China will face its end game: the dark side of a great deleveraging. Dee Woo is a Standing Director at Beijing New Century Research Institute for Multinationals, a citizen economist, and a citizen diplomacy activist. twitter.com/dee8woo weibo.com/dee8woo

60

Consumption Gross Fixed Capital Formation

50

YoY Growth

10%

40

0%

Average

-10%

30

-20% -30%

28 HONG KONG BUSINESS | AUGUST 2012

9/2011

6/2011

3/2011

9/2010

12/2010

6/2010

3/2010

9/2009

12/2009

6/2009

3/2009

9/2008

12/2008

6/2008

3/2008

9/2007

12/2007

6/2007

3/2007

12/2006

-40%

Source: Bank of Japan

20

80

85

90

95

00

05

10