The Future of Industrial Mittelstand in Germany In 2030

The Future of Industrial Mittelstand in Germany In 2030

Final Report

Project Management BDI:

Fabian Wehnert, Head of SME and Family Business Department

Study Conducted by: Z_punkt GmbH

Authors Z_punkt:

Christian Grünwald

Daniel Bonin

Holger Glockner

"Although interesting market opportunities are currently emerging, the existential challenges for many companies are growing at the same time. Strategic thinking in advance is tedious and yet a worthwhile investment of time for a promising future."

Dr Hans-Toni Junius, Main shareholder of C.D. Wälzholz GmbH & Co. KG and Chairman of the BDI/BDA SME Committee

What is the current state of the world and the EU in fall 2024?

From a global perspective, I see growing political and economic uncertainties that harbour risks for companies. What is the fundamental situation regarding open markets and free trade? For instance, what is happening in the Indo-Pacific or in the USA? What is happening geopolitically and how are we coping with the direct and indirect effects of increasing crises, conflicts and wars worldwide?

In Europe, I see a new EU Commission and a new EU Parliament coming into office. Which economic policy priorities will not only be named in Brussels, but also implemented over the next few years? Which of these will have a tangible impact in Germany?

Many questions and few answers. The economy has to navigate in the fog. This is a major challenge for entrepreneurs. This ties up energy that we need for the further development of our companies. In any case, it makes entrepreneurial planning for the foreseeable future difficult.

This view of and into the world is painful. What is the situation in Germany?

We are experiencing economic and structural weaknesses in Germany. The economy is sluggish, investments are stagnating and there is a lack of clear prospects. High energy prices, a shortage of labour and skilled workers and infrastructural deficits are the main structural burdens. So far, we have not seen any convincing steps from European and national politicians to noticeably improve this environment.

Interview with Dr Hans-Toni Junius

The climate in cooperation between large, medium-sized and small companies is also deteriorating and there is a noticeable crunch in collaboration. In many sectors and some regions, flexible and innovative value creation networks are in danger of breaking down.

As a result, the very recipe for success for our international competitiveness and prosperity is at stake. The workforce is feeling this and I believe it is one of the reasons why social unrest is on the rise.

The crucial question remains: what does all this mean for entrepreneurial resilience, economic competitiveness, social cohesion and political stability at the federal and state levels?

Germany as a business location is under pressure - or how would you describe it?

It is clear to me that the framework for us Mittelstand companies in our traditional location is shaky.

From a business perspective, the digital and ecological transformation - which we want and need to implement successfully - is changing many of the rules that have applied to date. While interesting market opportunities are emerging for some sectors and regions, existential challenges are growing in other areas.

Time and again, I see companies questioning generational thinking in the face of rampant regulation and rapid and cost-intensive investment and technology cycles. Successfully handing over a company to the next generation always involves major challenges and these are currently greater than ever. Incidentally, this is also because "entrepreneurship" is currently held in low esteem both socially and politically.

Can politics and the industrial Mittelstand still have a future?

Mittelstand companies must constantly reinvent themselves. In practice, I see a high level of motivation among the next generation of entrepreneurs at many Mittelstand companies and well-known family businesses. This is no different to the start-up scene.

For example, we are currently working on the transition from the sixth to the seventh generation in our company. This is challenging for everyone, but it also brings joy and boosts confidence.

Basically, I realise that with entrepreneurial spirit, inventiveness, reliability, patience, discipline, a sense of proportion and a well-founded desire for the future, entrepreneurs are constantly looking for viable paths - or at least further paths - forwards. Politicians are called upon to create suitable conditions for this, including all the necessary freedom. Politicians at federal and state level do not have a problem recognising this, it is mostly the implementation that is lacking.

If you are looking for paths and ways forward, you need reasonable goals. Clearly developed future scenarios can help to derive plausible options for action. This applies to both business and politics. Strategic thinking in advance is tedious but rewarding work towards a promising future. A look into the 2030s can show what we should do today to win tomorrow.

DEFINITION INDUSTRIAL MITTELSTAND

DEFINITION

DEFINITION OF INDUSTRIAL MITTELSTAND

The German industrial Mittelstand sector can be defined in a multidimensional understanding as a complex and multi-layered segment of the economy that is characterised by several distinctive features and dynamics. Here are some key dimensions for a working definition of industrial Mittelstand in Germany, which will be used as a basis in this specific project context:

1. Company size and structure

The industrial Mittelstand sector, characterised by many family businesses, also goes beyond small and medium-sized enterprises (SMEs) in terms of personnel and financial thresholds. It is strongly characterised by a private, family or owner-managed structure. Mittelstand companies tend to be more flexible and agile than large companies, they have flatter hierarchies, less bureaucracy and a special culture.

2. Corporate culture and management style

German Mittelstand companies are known for their strong corporate culture. It is usually characterised by close ties between owners, management and employees, long-term orientation with patience and a sense of proportion, a lively entrepreneurial spirit with a passion for invention and a strong sense of social responsibility that extends beyond the workforce.

3. Economic role and market position

The industrial Mittelstand in Germany traditionally tend to be loyal to their location, often operate in specialised (niche) markets and are characterised by a high level of innovation, quality, reliability and customer proximity. Companies are often key players in flexible value creation networks across sectors and regions and are also involved in international markets and global supply chains.

4. Innovation and technology

Despite relatively low human and financial resources, (family-owned) industrial Mittelstand companies are often highly innovative and technologically advanced, and some are leaders in specific fields ("hidden champions"). They invest sustainably in research and development to continuously develop better or new products and processes in line with customer requirements.

5. Adaptability and resilience

Industrial Mittelstand companies in Germany are often highly adaptable to dynamic market conditions when it comes to products, services and processes. Fair competition at all stages of the value chain and sustainable supplier relationships contribute to its adaptability and resilience. Loyalty to a location, on the other hand, becomes a challenge - sometimes an existential one - when local business conditions erode.

6. Regional and local influence

Industrial Mittelstand companies are typically firmly rooted locally and at the same time integrated into supra-regional economic structures. The companies make a significant contribution to local employment and prosperity - both private and public. They are often important players in their communities, far beyond the economic and social field in the narrower sense.

Overall, the industrial Mittelstand sector represents a dynamic and vital segment of the economy that is of great importance to both local communities and regions as well as the global economy. This multidimensional understanding emphasises the complexity and diversity of the Mittelstand sector, which makes it both unique and indispensable for the economic landscape in Germany.

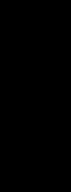

SCENARIOS

SCENARIO OVERVIEW

The Future of Industrial Mittelstand in Germany in 2030

SCENARIO 1: DELAYED MODERNISATION

Partisan politics prevents rapid reform and investment, while extremist forces gain ground. Germany continues to fall behind in the competition between business locations. There is a creeping loss of competitiveness and innovation in the German economy, and powerful companies from abroad are catching up. The intra-European and global location imbalance is leading to the relocation of large companies and Mittelstand companies, and valueadded networks are in some cases disintegrating.

THE PATH TO THE SCENARIO: DRIVERS AND SETTING THE COURSE

2024

⊳ Political blockades in Germany and at the EU level

⊳ Growing conflicts over the distribution of state resources and attention

⊳ Insufficient investment speed and level

⊳ Adherence to the status quo in society and business

SCENARIO WORLD 2030

As in previous years, Germany is facing difficult government formations due to the increasing differentiation of the parliamentary party spectrum and the growing weight of the political fringes. Moreover, there are complicated federal and European negotiation processes. The political culture is characterised by mutual accusations in government coalitions.

The resulting paralysis and lethargy of the political establishment is delaying future public investment in infrastructure, the implementation of e-government or the twin transition to sustainability and digitalisation. This is exacerbated by the lack of budgetary room for manoeuvre, which also means that there is little political will to ease the burden. Tight public finances and overstretched social systems mean that local authorities and the state can only provide a limited range of public services, making the conditions for society and the economy even more difficult.

Stagnation and standstill on many levels

The German economy is stagnating, and the consumer and investment climate is clouded by entrenched expectations of stagnation and lengthy planning and approval procedures. Furthermore, the effects of labour and skills shortages are becoming increasingly visible, not only in the economy but also in public administration. Neither are there any real productivity or service gains from automation. Within Germany, there are growing disparities between urban and rural areas and between structurally weak and structurally strong regions. In addition, the gap between successful and struggling Mittelstand companies is widening, for example when it comes to investment in new technologies. External factors beyond the direct control of Mittelstand companies have played a key role in this development (e.g. political delays, abolition of subsidies).

The lack of planning certainty in the industrial Mittelstand is increasingly becoming an obstacle. Many sectors are experiencing a gradual loss of innovative capacity and technological leadership, partly as a result of delayed investments. In view of the volatile environment, investments are and have been postponed further and further into the future. Moreover, transformation is increasingly seen as a cost driver and an additional bureaucratic burden rather than an opportunity for growth.

The industrial Mittelstand faces growing competition, notably from imports from abroad - e.g. via freight capacity from China - and from factories of foreign companies in lower-cost EU locations. Disparities in location factors within Europe (such as energy costs, bureaucracy, tax and duty burdens, labour availability or pressure from globalised R&D work) lead to loss of orders and (creeping) relocation of large companies and Mittelstand companies. As a result, value networks are increasingly disintegrating. This is accompanied by frequent changes in suppliers and unstable customer relationships.

DELAYED MODERNISATION

(CONTINUED)

Medium-sized industrial companies break new ground

As a strategic approach to the crisis, some Mittelstand companies, particularly in structurally weak regions, are seeking to join forces with local politicians and regional actors in order to strengthen local locations and civil society.

Consequently, they often unintentionally become "political", as they increasingly take on public tasks to attract skilled workers - for example, childcare in company day-care centres or care services for employees' relatives. In doing so, Mittelstand companies are inadvertently filling a vacuum created by the underfunding or overburdening of social systems.

In response to the crisis, some industrial Mittelstand companies are also focusing on occupying new niches by changing their business models. They are trying to exploit their "meta-competencies" and dock onto new value networks (e.g. via service offerings) and new business ecosystems. These can be found in areas such as new space, biotechnology and water-sensitive infrastructure.

Consolidation and acquisitions

The German Mittelstand sector is undergoing increasing consolidation and concentration, which is changing its face to some extent. In addition, foreign investors from Asia (especially China and South Korea), North America and neighbouring European countries are seizing the opportunity to enter the German Mittelstand sector - in some cases involving a major cultural change or relocation.

OVERVIEW: INDUSTRIAL MITTELSTAND SECTOR AND ENVIRONMENT IN 2030 IN THE "DELAYED MODERNISATION" SCENARIO

Location conditions for industrial Mittelstand companies

Labour force and skilled workers and organisation of work

• Germany is falling behind in international location competitiveness, infrastructure gaps are not being closed, and regional and urban-rural disparities are increasing.

• The economy is complaining about declining security of supply for electricity, gas and raw materials, while local protests and political blockades are complicating the energy transition.

• The bureaucracy cost index has risen, mainly due to staff shortages in the administration as a result of longer processing times.

• Germany is facing a massive shortage of skilled labour, while at the same time immigration scepticism is high in the political discourse.

• Attempts to compensate through automation often do not have the desired effect.

• New offers by companies to attract skilled workers are increasing the resources devoted to recruitment and retention.

The industrial Mittelstand in the dual transformation

The industrial Mittelstand in competition and markets

Organisation of value creation networks and supply chains

Social role of the Mittelstand sector

Political framework conditions for Mittelstand companies

Changes in the characteristics of the Mittelstand sector compared to 2024

• The German Mittelstand sector is gradually losing touch with the global innovation dynamic over the course of the ecological transformation. It tends to act in a reactive or adaptive manner, with individual companies at the top continuing to be regarded as hidden champions

• German Mittelstand companies are struggling to keep up with the global pace of innovation in the field of digitalisation, both in the development of technology-based solutions and in the internal redesign of processes and implementation of new technologies. There is a wide gap between "early adopters" and "late adopters."

• Mittelstand companies are trying to break into new business ecosystems and open new value chains in growth areas beyond their core competences, with varying degrees of success.

• The innovative capacity of Mittelstand companies is declining. At the same time, both intra-European and global competitive pressure is increasing.

• In purely statistical terms, direct investments from abroad are increasing because of acquisitions. But often, they are de-facto linked to relocations within the EU; Mittelstand companies sometimes write off investments abroad at an early stage, especially in China, in view of competitive disadvantages (e.g., due to political decisions to strengthen the internal market).

• Company closures and relocations at both large and medium-sized companies are leading in some cases to the dissolution of existing value creation networks, accompanied by frequently changing suppliers and unstable customer relationships.

• The complexity of supply chain design is increasing, and the potential of the circular economy is limited.

• Many Mittelstand companies act as strong civil society players that also take on public infrastructure tasks (e.g. running daycare centres or providing care). On the one hand, this compensates for the overburdening of social systems, but on the other, it also leads to new demands being placed on companies by the public.

• Parties on the political fringes are able to gain ever greater voter shares both nationally and in Europe, while uncertainties regarding long-term stability are increasing.

• The geopolitical situation is characterised by a period of transition to multipolarity, with a large number of smaller conflicts, without any discernible new patterns of order emerging.

• The face of the Mittelstand sector is changing, with mergers and consolidations leading to changes in average size and, in many places, ownership.

• The high level of loyalty to the location is increasingly being called into question by the deterioration in the general conditions, and some are also gradually losing their innovation leadership.

SCENARIO 1:

DELAYED MODERNISATION

SIGNALS OF A LIKELY REALISATION OF THE SCENARIO

SIGNAL 1

SIGNAL 2

• According to OECD data, only 10.05% of all fixed broadband connections in Germany were connected to a fibre optic cable in Q2 of 2023. The proportion was even lower in only two OECD countries - Belgium and Greece. South Korea leads the world with a fibre optic share of around 88.9%. In Europe, Iceland is ahead with 85% - followed by Spain with 84.1%. The existing fibre optic potential in Germany is far from exhausted.

SIGNAL 3

• In 2020, the Scientific Advisory Board of the Federal Ministry for Economic Affairs and Climate Protection (BMWK) considered an investment requirement in public infrastructure totalling 450 billion euros in the coming decade to be plausible.

• In the ifo Institute's latest "Economic Expert Survey" (September to October 2023), 72% of the German experts surveyed stated that conditions in Germany had deteriorated over the last ten years. A sharp deterioration in location conditions was reported by 6.7%, stagnation by 10% and an improvement in conditions by only 12%. This result contrasts with the Europe-wide assessments: Just under 40% rated the attractiveness of their respective countries as a business location as better today than ten years ago.

Over the next ten years, 48% of German experts expect the location to become less attractive. Only 15% assume that the location will become more attractive again and 47% expect location conditions to remain the same.

SIGNAL 4

SIGNAL 5

• According to a study commissioned by Dezernat Zukunft (conducted by Frontier Economics and IW Consult), energy costs in Germany are likely to remain higher than abroad after 2030. The study looks at base-load energy costs that are higher than the pure production costs of volatile renewable energies.

• The Supply Chain Pulse Check survey (September 2023) by Deloitte and BDI shows that Germany is becoming less attractive as a business location and that companies are relocating their value creation activities as a result. According to the survey, high-quality parts of the value chain could be relocated. According to the survey, up to two thirds of component production, almost half of pre-assembly, warehousing & storage and "production in general" could be carried out abroad.

SCENARIO 2:

NATIONAL TRANSFORMATION EFFORTS

In response to the crises of the 2020s, decisive political, entrepreneurial and social responses are paving the way for an economic upturn in Germany, driven by a leading role in the digital and green transformation. For example, infrastructure modernisation is being accelerated and the social value of performance orientation is increasing. The accelerated pace of change offers opportunities but also challenges for the industrial Mittelstand.

THE PATH TO THE SCENARIO: DRIVERS AND SETTING THE COURSE

2024

⊳ Transformative public investment programme through expanded financing scope

⊳ Modernisation of administration, fewer taxes and duties and less bureaucracy

⊳ Reliable political framework supports planning security and thus long-term investments

⊳ National transformation strategies lead to competition and disagreements within the EU

⊳ Increasing social value of performance and entrepreneurship

SCENARIO WORLD 2030

The German economy is growing dynamically and, thanks to a national transformation strategy, is on its way to climate neutrality. The necessary course was set in the mid-2020s and required decisive action in politics, society and business.

The forward-looking public investments (e.g. in energy, transport, industry, education, social housing) are having an impact and strengthening the country's position in international competition. The process of agreeing on an investment plan and financing instruments is not without friction in politics and business, but is ultimately successful. Access to capital (non-bank and bank financing) has improved for the industrial Mittelstand. Mittelstand companies investment is now significantly higher, for example in renewable energy and AI systems to increase labour productivity. The more positive view of the long-term future is also reflected in the robust consumption and investment behaviour of households.

The increased willingness to compromise in society supports political reforms, infrastructure modernisation and investment by Mittelstand and foreign companies (e.g. acceptance of construction projects). The shortage of skilled labour is being significantly alleviated by increased immigration, longer weekly and lifetime working hours and digital transformation. There are various reasons for the increased focus on performance in society, including financial considerations and changing values. Industrial Mittelstand companies are increasing investment in education and training to mitigate skills shortages and prepare the workforce for changing job profiles and skills requirements.

Growing importance of entrepreneurship and flourishing start-up landscape

The greater focus on performance in German society is also reflected in successful company successions and an increase in the number of start-ups. Start-ups are being established on greenfield sites, using new technologies and processes that have become available as a result of technological leaps. Time and again, former start-ups have established themselves as "new" Mittelstand companies, thus increasing competitive pressure. The industrial Mittelstand proactively promotes the flourishing start-up landscape and integrates promising start-ups into value creation networks at an early stage.

Mittelstand companies in the green and digital transformation

The clear regulatory framework and public investments provide planning security for the industrial Mittelstand and business partners at the location. This successfully incentivises investment in climate-neutral processes, resource efficiency and digital technologies. Mittelstand companies not only specialise in individual, separate products or services, but also develop holistic product-service systems and B2B platforms. In this way, Mittelstand companies also successfully open up new export markets in promising emerging and developing countries.

(CONTINUED)

However, not all Mittelstand companies can keep up with the pace of change brought about by technological change and changing regulatory requirements. Despite the economic momentum, some Mittelstand companies that have been left behind are going out of business.

Increased competition within the EU

However, other EU members are also pursuing national transformation strategies. Within the EU, there is intense intra-European competition, protectionist tendencies and intra-European disputes, for example over incentive systems and the organisation of sustainability taxonomies. There is also intra-European competition over taxes and levies and incentives for companies to relocate. European companies and EU countries particularly affected by demographic change are competing for skilled labour from outside Europe and are also poaching skilled labour from each other. Competition between EU Member States and between companies has a positive effect on innovation and productivity growth in Mittelstand companies.

Integrated value chains at the location: between structural change and resilience

National import strategies secure supplies of energy and critical raw materials, sometimes at high prices. Rising commodity prices and competition for them are a consequence of ambitious global climate targets. This is because the negative effects of climate change are increasingly recognised as a global challenge, for example through rising healthcare costs or crop failures in China and India.

German and European industrial policy emphasises the added value of energy-intensive industries in terms of synergies in value networks, resilience and climate protection. The competitiveness of energy-intensive industry is therefore being strengthened by various policy measures as part of the transformation effort. Despite other differences, effective safeguards are being put in place at EU level to counteract the migration of industry to countries with lower ESG standards. This external protection is a common interest that stabilises the EU.

OVERVIEW: INDUSTRIAL SME SECTOR AND ENVIRONMENT IN 2030 IN THE "NATIONAL TRANSFORMATION EFFORTS" SCENARIO

Location conditions for industrial Mittelstand companies

Labour force and skilled workers and organisation of work

The industrial Mittelstand in the dual transformation

The industrial Mittelstand in competition and markets

Organisation of value creation networks and supply chains

Social role of the Mittelstand sector

Political framework conditions for Mittelstand companies

Changes in the characteristics of the Mittelstand sector compared to 2024

• Infrastructure deficits, including by international standards, are gradually being addressed through transformative investments.

• The expansion of renewable energy and related infrastructure (e.g. grids) will be accelerated, making energy supply less dependent on imports of fossil fuels. The supply of critical raw materials is a challenge due to high global demand

• Modern administration: reducing the burden on human resources through digital transformation; rethinking bureaucratic processes, using international best practice as a benchmark

• The shortage of labour and skilled workers is being significantly alleviated by digital transformation, political and entrepreneurial initiatives and an increase in labour force participation.

• Mittelstand companies are proactively developing practical training, improving job quality for older workers and recruiting labour and skills from abroad (high competition, including from large foreign companies).

• Mittelstand companies are on a path to climate neutrality, driven by their own initiative and by strict requirements from companies downstream in the value chain.

• Mittelstand companies are exchanging data and optimising their AI systems across companies thanks to federated learning. Those that do not implement the digital transformation quickly enough are increasingly being squeezed out (e.g. by start-ups)

• The reliability of business partners, supply chains and value chains is increasing worldwide, and global trade is slowly picking up. Improved location conditions are making Germany more attractive for foreign direct investment, while protectionism within Europe is making it more difficult for Mittelstand companies to invest in the EU.

• Mittelstand companies are increasing their innovative capacity with specialised solutions, data-based products and services, and B2B platforms. They are successfully exporting these abroad. Direct investment abroad allows Mittelstand companies to take into account local expertise, market and regulatory requirements.

• Competitive pressure from German start-ups is increasing significantly.

• Mittelstand companies are proactively building cooperation networks with start-ups and integrating them into value creation networks, thereby mitigating and positively harnessing competitive pressures..

• Initiatives and start-ups in the context of the circular economy and the bio-economy will be specifically promoted as part of transformative investment programmes in order to reduce regional disparities and achieve climate targets through decentralised value creation processes.

• Mittelstand companies counteract political polarisation at an early stage.

• Mittelstand companies support the integration of immigrant professionals through training, advice and guidance in everyday life.

• Mittelstand companies and entrepreneurship gain respect in society, which has a positive impact on generational change and strengthens identification with the SME sector.

• The stable political and social environment provides planning certainty, which supports investment in sustainable technologies and processes.

• Intra-European competition and protectionist tendencies weaken the EU internally. However, the EU presents a united front to the outside world, e.g. to protect the single market from competitors such as China (e.g. the carbon border adjustment system).

• Slow international (re-)establishment of effective multilateral forms of cooperation.

• For the emerging start-ups, progressive Mittelstand companies are attractive cooperation and business partners due to their diverse characteristics (e.g. entrepreneurial spirit, inventiveness, quick decisions, flat hierarchies).

NATIONAL TRANSFORMATION EFFORTS

SIGNALS OF A LIKELY REALISATION OF THE SCENARIO

SIGNAL 1

SIGNAL 2

• The first signs of "re-industrialisation" as a result of the energy transition can be observed in Schleswig-Holstein. These include the establishment of a battery factory by Swedish supplier Northvolt in Heide and the construction of a factory for green hydrogen in Neumünster. The locations in the far north of Germany benefit from the very good availability of renewable energy.

• In a working paper published at the beginning of 2024, macroeconomist Tom Krebs analysed the impact of public investment on the growth of the German economy. In his analysis, Krebs postulated that a massive expansion of public climate and social investments in Germany could trigger an economic boom and simultaneously support the transformation to climate neutrality. According to Krebs' calculations, this would require investments totalling 2% of German GDP. Such an investment package could give Germany growth rates of up to 3% over the longer term.

SIGNAL 3

• Management consultants McKinsey advocate a"creative renewal" of Germany. McKinsey argues that the disruptions of epochal change require radically new solutions and breakthrough innovations. It is not the preservation of the status quo, but the creative renewal of society that will enable a growth model that is efficient in the next era and that can meet the demands of a sustainable society. This requires a transformation in all segments of the economy and the further development of critical framework conditions for creative renewal. For example, creative renewal could accelerate average and value-added GDP growth to 2% by 2030. Mittelstand companies need to evolve from product specialists to ecosystem players.

SIGNAL 4

SIGNAL 5

• Michael Hüther (Director of IW Cologne), Clemens Fuest (Ifo President) and Jens Südekum (Professor of International Economics at the University of Düsseldorf) emphasise in a joint guest article that the government and opposition must find ways to solve the financing problems following Federal Constitutional Court’s ruling on compliance with the debt brake. Otherwise, "Germany is jeopardising its future and ultimately also its debt sustainability".

• In its 2023/24 annual report, the SVR discusses measures to "noticeably" increase potential growth and the role of the digital and green transformation for development up to 2070. Investments in education and cross-sectional technologies (e.g., AI) could increase productivity growth. Investments in energy infrastructure and incentives for decarbonisation investments are also necessary. An increase in the volume of labour, immigration, increased administrative efficiency and a reduction in bureaucracy are also important building blocks.

SCENARIO 3:

DEEPER EUROPEAN INTEGRATION FOR RESILIENCE

The US's increasing retreat from Europe is creating momentum for deeper EU integration, with security policy as the new core. This also creates space for common strategies in other areas, such as the data economy, raw materials, energy and the capital market. European cross-border alliances for innovation and value creation are holding their own in a world of high volatility and rapidly shifting alliances.

THE PATH TO THE SCENARIO: DRIVERS AND SETTING THE COURSE

2024

⊳

Security policy as the nucleus for a new deeper EU integration

⊳ European cooperation in key future fields as a strength

⊳ Development leaps in AI and other technologies lead to high pressure to adapt

⊳ "Euro-regional" attachment to home: openness towards cooperation and new locations in other EU countries

SCENARIO

DEEPER EUROPEAN INTEGRATION FOR RESILIENCE

SCENARIO WORLD 2030

In the face of new geostrategic realities, driven by the accelerating withdrawal of the US from Europe and a highly competitive, partly protectionist environment, the European Council is paving the way for deeper EU integration to ensure robust action and competitiveness. Under pressure from the new geostrategic realities, even more Eurosceptic governments are joining in, with the Weimar Triangle of France, Poland and Germany acting as the "engine" of development. The global economy is highly politicised, geostrategy and geoeconomics go hand in hand.

Strengthening resilience is the top priority

The new integration measures aim to strengthen resilience to external shocks and also to improve investment conditions: This is achieved through the implementation of the Capital Markets Union and a coherent fiscal policy. The concept of strategic autonomy, often invoked by the EU Commission, is aimed at strengthening security of supply, for example in chip production or the expansion of renewable energies and networks. In this context, there are always conflicts of interest between environmental and social issues, such as the (re)opening of mines in Europe. The targeted promotion of circularity also serves the European climate goals, the reduction of resource consumption and the strengthening of strategic autonomy.

At the same time, EU regulation aims to create a level playing field in the European single market and to compensate for global distortions of competition. However, questions about the role and depth of intervention by EU institutions and which key sectors should be the focus of EU support are a constant source of controversy. Overall, however, market-based competition within the single market is being strengthened: for example, the tax burden in the EU is becoming more evenly distributed, and bureaucratic barriers to the free movement of goods, services, people and capital are gradually being removed.

New, cross-border value creation networks

An EU-wide strategy for the data economy, critical raw materials, industry, key technology ecosystems and the circular economy facilitates value creation across companies. New value networks are emerging across the EU in border regions and, more recently, in industrial metaverses, with German industrial Mittelstand companies playing a key role. Strong German value networks act as architects of cross-border European ecosystems - a close relationship with one's own country is increasingly being thought of in "euro-regional" terms, i.e. across regional borders.

The alliances translate future EU goals and standards, such as climate protection or responsible industrial AI, into new, competitive solutions. Dynamic developments in key technologies put Mittelstand companies under great pressure to adapt.

DEEPER EUROPEAN INTEGRATION FOR RESILIENCE

(CONTINUED)

However, for innovative Mittelstand companies and technology leaders, there are also a number of new business opportunities in specific contexts that contribute to Europe's resilience, security and sustainability goals. European companies are not only using AI, but also developing powerful AI solutions themselves, often for highly specialised niche applications. At the same time, however, competition within Europe for skilled labour and business relocation is increasing sharply. This is leading to recurring conflicts between some EU member states.

Strong local ties with global networking

German Mittelstand companies are generally very loyal to their established locations and at the same time open to cooperation and new locations in other European countries. As a result, English is being introduced as a second working language in some places, facilitated by real-time AI translations.

European innovation and value creation alliances are closely networked with selected global innovation centressuch as Singapore, India or new growth centres in Africa - and are considered pioneers there (in their niches). They rely on sustainable, reliable relationships with suppliers, customers and, in some cases, competitors in specific contexts to deliver complete solutions for global markets..

OVERVIEW: INDUSTRIAL SME SECTOR AND ENVIRONMENT IN 2030 IN THE "DEEPER EUROPEAN INTEGRATION FOR RESILIENCE" SCENARIO

Location conditions for industrial Mittelstand companies

Labour force and skilled workers and organisation of work

The industrial Mittelstand in the dual transformation

The industrial Mittelstand in competition and markets

Organisation of value creation networks and supply chains

Social role of the Mittelstand sector

Political framework conditions for Mittelstand companies

Changes in the characteristics of the Mittelstand sector compared to 2024

• Investment in (transformation-relevant) infrastructure is being stepped up in all EU countries, including with the help of a newly created European Resilience Fund.

• Renewable energy is being massively expanded across Europe , with the potential of solar power being tapped on a new scale, particularly in southern Europe, while the supply of raw materials has become more complex and costly.

• The cost of red tape has fallen sharply in some areas due to the digitalisation of administration, while in other areas increased European regulation is leading to more requirements and specifications to implement the EU's resilience agenda.

• The list of shortage occupations for the Blue Card is being greatly expanded, while at the same time efforts to recruit skilled labour are being stepped up in almost all European countries, although this is also intensifying the intra-European battle for skilled labour.

• Where there are skills gaps, attempts are being made to fill them through automation and new processes.

• Industrial Mittelstand companies are quite successful in tapping new business potentials and ecosystems along the sustainability transformation, often with the aim of increasing (climate) resilience and climate adaptation.

• Many are catching up in terms of digitalisation, with new potential in AI and industrial metaverses offering new business opportunities.

• The reliability of business partners, supply and value chains is decreasing globally, but increasing in the European context due to reorganisation.

• In many contexts (e.g. sustainable technologies), Mittelstand companies can increase their capacity to innovate, increasing global and intra-European competitive pressures.

• Increased nearshoring and focus on the EU are also changing FDI patterns, with more investment to and from Europe (including EFTA and the UK); gradual shift of FDI by the industrial Mittelstand to China as part of de-risking strategies.

• New value networks in EU border regions and in industrial metaverses, strong German value networks as architects of cross-border European ecosystems, simultaneous cooperation and competition in the EU.

• European mining industry for critical raw materials and rare earths begins to develop, but high dependency on energy supply in Germany, also targeted promotion of circular economy and bioeconomy at EU and national level to strengthen strategic autonomy.

• Nearshoring takes place in selected areas where, for example, energy and labour costs are not the decisive investment criteria due to a high degree of automation.

• Many Mittelstand companies form important hubs in cross-border networks, helping to strengthen the European idea.

• Many Mittelstand companies are highly involved in civil society.

• German policy is strongly oriented towards the European level, with a stable regulatory framework in Germany and the EU and a high level of legal certainty.

• Geopolitical uncertainties increase transaction costs for globally operating Mittelstand companies, "reglobalisation" under the auspices of strengthening regional alliances.

• Little change in characteristics, but stronger European orientation of Mittelstand companies investing in "euro-regional" value networks.

• Industrial metaverses are changing the way sites work together and, to some extent, corporate cultures.

SCENARIO 3:

DEEPER EUROPEAN INTEGRATION FOR RESILIENCE

SIGNALS FOR A POSSIBLE REALISATION OF THE SCENARIO

SIGNAL 1

SIGNAL 2

• Partly in response to the Trump administration's criticism of European defence efforts, the EU member states agreed on Permanent Structured Cooperation (PESCO) in 2017, in which all EU member states, with the exception of Malta, now participate. This cooperation option was created by the Treaty of Lisbon. PESCO serves the goal of a "defence union" and provides for close cooperation in the development and procurement of military instruments. However, it does not involve the creation of a common army.

• In light of the Russian war of aggression against Ukraine, the EU sought to increase energy resilience in the EU with the REPowerEU plan and a series of immediate legislative measures to ensure that energy supply disruptions in Europe are avoided, pressure on energy markets, prices and consumers is reduced and the structural reform of our energy system is pursued.

SIGNAL 3

SIGNAL 4

• In order to prevent the impending de-industrialisation of Europe, a policy paper by the Jacques Delors Centre at the Hertie School argues that the EU and the member states should develop a joint strategy. This should do justice to the economic and climate policy complexity of the situationand also include a partial relocation of energy-intensive industry, as national strategies would fall short if they only focussed on energy price reductions and thus attempted to prevent the relocation of energy-intensive industry altogether. Instead, policymakers should actively shape this relocation and thus help the European economy and decarbonisation.

• As a result of increasing concerns among German companies about their business in China, Tagesschau.de reported that German companies are now changing their strategies to enable rapid nearshoring: Parts of operations should be able to be separated quickly in an emergency, and supply chains should return to Europe. Worst-case scenarios are also being played out.

SIGNAL 5

• The EU Raw Materials Act 2023 identifies both critical and strategic raw materials that are essential for green and digital technologies as well as for the space and defence industries. The law sets indicative targets for domestic capacity along the supply chain of strategic raw materials for 2030: 10% of the EU's annual extraction needs, 40% for processing and 15% for recycling. In addition, the EU should not source more than 65% of its annual demand for a strategic raw material at any relevant stage of processing from a single non-EU country.

SCENARIO 4:

GERMANY IN A WORLD (DIS)ORDER WITH BLOC FORMATION

The systemic conflict between the US and China is escalating into a decoupling of global trade activities. Germany's industrial Mittelstand is facing an existential test. The loss of supplier relationships and sales markets must be compensated in this challenging environment. There will be a long-term loss of prosperity in Germany.

THE PATH TO THE SCENARIO: DRIVERS AND SETTING THE COURSE

2024

⊳ Escalation spiral between China and the USA leads to bloc formation and decoupling of global trade activities

⊳ De-risking strategies of politicians and companies are often not adapted to the situation

⊳ Slow adaptation of supply chains and export strategies

⊳ "Business and innovation with scarcities"

GERMANY IN A WORLD (DIS)ORDER WITH BLOC FORMATION

SCENARIO WORLD 2030

The US and China have failed to manage their competition for influence, status and technology in a responsible way. Instead, trade disputes, mutual containment strategies and the race for international influence continue to escalate. On the way to 2030, the escalation spirals ultimately lead to an abrupt bloc formation along democratic states and authoritarian systems. Non-aligned states try to benefit from this development. The consequences pose existential challenges for the German industrial Mittelstand - and will still be blocking the transformation towards a climate-neutral economy and digitalisation in 2030.

(Dis)order along blocks

The EU and its member states are part of the "democratic bloc", with individual members threatening to leave because of their dependence on China and repeated evasion of sanctions. The transatlantic relationship is robust but strained in some areas: The US, for example, makes import and export conditions dependent on the decisions and defence spending of individual EU members. The non-aligned states are positioned alongside the two blocs. On the one hand, they depend on trade and support (e.g. technology transfer, infrastructure investment) from the blocs. On the other hand, non-aligned states - for example in South America or Africa - sometimes have a good basis for negotiation, for example due to their geographical location, their potential for raw materials or renewable energies. The formation of the bloc is not leaving China and the US unscathed; decoupling is imposing economic costs and increasing internal instability in both countries.

Loss of prosperity and adaptability to a new reality

Global economic exchanges between the two blocs and the non-aligned states have in some cases been abruptly decoupled and are in the process of being reorganised. Trade and investment between the blocs has virtually ground to a halt as a result of trade policy measures. The cessation of direct trade activities between the blocs is leading to increased reshoring and friendshoring activities in Germany and around the world, with government support in particular for critical sectors. On the other hand, there are opportunities for non-aligned countries. Existing and newly established companies use local raw materials, import intermediate products and then export them abroad. Mittelstand companies in export-dependent sectors or with extensive FDI in the "Chinese bloc" face existential challenges. They have to reorganise their business according to the logic of the bloc and the nonaligned states.

The consequences of decoupling for Germany are serious, but manageable in the long term. In 2030, the longterm loss of prosperity due to decoupling will be discussed, while the adaptability of international trade flows in the industrial Mittelstand sector will be emphasised. Trading activities, supply chains and production are increasingly adapting to new realities. Nevertheless, there will be shortages of critical raw materials, inputs and products.

GERMANY IN A WORLD (DIS)ORDER WITH BLOC FORMATION

(CONTINUED)

Mittelstand companies are steadily increasing trade and foreign investment in the EU internal market, with their own bloc and also with non-aligned countries (e.g. raw materials, factories and development of services abroad). Trade policy instruments also reduce competitive pressure in the EU's internal market, for example by eliminating competitors from China.

Security of supply as a challenge and driver of (joint) innovations

Inflationary pressures remain high in Germany despite the adjustment process. The supply of labour and skilled workers, energy, raw materials and inputs is cost-intensive. Companies without a clear service offering and with a weak bargaining position find it difficult to pass on price increases along the value chain. Resource and energy efficiency and savings are therefore essential for the day-to-day business and innovation activities of industrial Mittelstand companies. Decentralised supply concepts, the development of local raw material deposits and the principles of the circular economy are becoming a necessity, but true energy and raw material self-sufficiency is still an illusion. Cross-company, supra-regional value creation networks are joining forces via digital platforms in "B2B sharing networks" to optimise cost structures, investments, capacity utilisation and labour availability.

Consequences of decoupling as a catalyst for regional disparities

Regional disparities and the urban-rural divide in Germany are exacerbated by the economic consequences of decoupling and the resulting reduction in the financial scope of the public sector. Relocations or closures are a particular challenge for regions that have historically depended on medium-sized or large companies. They have ceased to be a source of trade tax and jobs, leaving a lasting gap. Nevertheless, the people in these regions have a strong sense of belonging to their homeland, so there is no significant internal migration.

Technological arms race extends into the Mittelstand sector

A technological arms race between the blocs leads to bloc-specific norms and standards. This creates a high level of complexity for Mittelstand companies that import or export products to non-aligned countries. The arms race also manifests itself in state-sponsored industrial espionage and cyber-attacks from abroad. The risks and costs for Mittelstand companies are reaching record levels. This particularly affects innovation leaders and Mittelstand companies providing "critical" products and services. The military and technological arms race is driving state investment in R&D, thereby favouring technological breakthroughs in key technologies (e.g. AI, materials, health technologies). These technologies can be used for both military and civilian purposes (dual-use). Such technologies are transferred to the economy with a time lag and are taken up by particularly innovative Mittelstand companies. These are often technologies that were at a very low level of maturity at the beginning of the 2020s and can now be used unexpectedly quickly.

OVERVIEW: INDUSTRIAL SME SECTOR AND ENVIRONMENT 2030 IN THE SCENARIO "GERMANY

IN A WORLD (DIS)ORDER WITH BLOC FORMATION"

Location conditions for industrial Mittelstand companies

• The investment backlog is growing, especially in structurally weak regions and those where trade tax revenues have collapsed.

• Energy and raw material supplies can only be secured at higher costs, neutral third countries take advantage of import dependencies, resulting in unpredictable price spikes; the energy transition fails due to disruptions in supply chains (e.g. solar modules).

• High levels of bureaucracy related to data and critical industries; planning and approval procedures are accelerated, and environmental assessments are watered down, for example in order to develop raw material deposits as quickly as possible or to adapt supply chains.

Labour force and skilled workers and organisation of work

The industrial Mittelstand in the dual transformation

The industrial Mittelstand in competition and markets

Organisation of value creation networks and supply chains

Social role of the Mittelstand sector

Political framework conditions for Mittelstand companies

Changes in the characteristics of the Mittelstand sector compared to 2024

• Skills and labour shortages; longer working lives and working weeks (e.g. full-time instead of part-time for financial reasons) cannot offset the negative effects of an ageing population and low levels of immigration.

• Job security as a decisive factor in the competition for labour and skilled workers.

• Mittelstand companies try to pursue climate change projects as far as possible, but uncertain national and international frameworks and supply bottlenecks make this impossible in some cases. As a result, national and global climate targets are being missed.

• High pressure to use automation solutions to minimise costs.

• Supply and value chains have increasingly adapted to the new reality, but production continues to be interrupted by bottlenecks.

• Relocation of direct investment to own block and non-aligned states; at the same time, blocked access to direct investment or even nationalisation in the block of authoritarian systems.

• With the disappearance of markets such as China, many Mittelstand companies face cut-throat competition in the EU single market and other target markets.

• The difficult economic situation is putting long-standing business relationships to the test, and value networks have become more volatile. New value networks are emerging that use platforms to share and optimise resources and systems across companies ("B2B sharing").

• The circular economy and bioeconomy are components of a mission-driven funding and innovation policy. The potential of the circular economy and bioeconomy is being exploited out of economic necessity, but cannot prevent raw material shortages.

• With social systems overstretched and the global situation worsening, the middle class is seen as a stabilising anchor, but this attitude of social entitlement is often overstretched.

• In some cases, historically rooted Mittelstand companies are forced to give up their business, with the loss of not only tax revenues but also social and cultural commitment. This is particularly noticeable in rural areas, where established structures are disappearing.

• German policy focuses on security of supply and mitigating social disparities, while climate and environmental protection targets are watered down for the time being.

• The EU is aligning itself with the democratic bloc, with individual members repeatedly threatening to leave the EU and circumventing sanctions because of their dependence on China.

• Bloc formation around the US and China, which is increasingly facing internal instability. Although nonaligned actors are dependent on the blocs, they also have a good bargaining position (e.g. raw materials, labour, potential market).

• The ability to adapt to dynamic market conditions and to compete fairly will be key success factors in the face of global (dis)order.

• Mittelstand companies need to redesign their export model. In "non-aligned markets", Mittelstand companies are confronted with competing companies (e.g. from China). These companies are now redirecting export capacities that were planned for the EU market to "non-aligned markets".

SCENARIO 4:

GERMANY IN A WORLD (DIS)ORDER WITH BLOC FORMATION

SIGNALS FOR A POSSIBLE REALISATION OF THE SCENARIO

SIGNAL 1

SIGNAL 2

• Against the backdrop of risk reduction ("de-risking") in trade relations with geopolitical rivals in order to reduce economic dependencies and the associated potential for blackmail, international organisations such as the International Monetary Fund (IMF) are already warning of a bloc formation of the global economy along geopolitical lines. A new phase of globalisation could be dawning in which security interests and geopolitical zero-sum thinking dominate economic policy.

SIGNAL 3

• In a study, the Kiel Institute for the World Economy analysed the potential economic impact of a hard decoupling between China and Germany by simulating a scenario "similar to a Cold War 2.0 with fragmentation of the global economy". According to the study, an abrupt decoupling would lead to a short-term loss of 5% of Germany's GNI and a long-term reduction to around 1.5%. The authors see mainly short-term economic effects that would be comparable to the global financial crisis and the COVID-19 pandemic, but describe these costs, although serious, as manageable. German Mittelstand companies in particular would be considered very resilient here.

SIGNAL 4

• In an essay published in 2023, Aaron L. Friedberg, Professor of Politics and International Relations at Princeton University, foresees a world characterised by bloc formations in which a bloc of democratic states has to assert itself against authoritarian blocs.

SIGNAL 5

• In an article, The Economist emphasises the importance of non-aligned states in the current international system. According to the article, 45% of the world's population live in non-aligned states. They also account for 18% of global GDP (1992: 11%), surpassing the EU. Their strategy and attitude towards China and the USA is pragmatic and opportunistic ("mini-materialism"), and some even see increasing global economic decoupling as an opportunity.

• In a speech, Gita Gopinath, Deputy Managing Director of the International Monetary Fund, describes the strong economic integration of non-aligned countries into the global economy and their potential role as a "connector". In a fragmented global economy, they could benefit from redirected trade and investment flows and cushion the negative effects of trade fragmentation.

WHAT ARE WILD CARDS?

In futurology, a wild card is an event with a relatively low probability of occurrence, but a high impact on operational business or government activities if it occurs. Wild cards are serious events and/or developments with exponential acceleration that make business as usual impossible. Because they are perceived in public discourse as unlikely events or developments, wild cards are seen as surprises by much of the business, political and public communities when they occur. They challenge established frameworks and reference systems and change the way we look at the world - and therefore at the future.

Jokers can come from three main areas: Natural disasters, the impact of technological (and social) innovations, or socio-political upheavals. They are used in futurology either to test scenarios for their future robustness or to add surprising scenarios to the scenario space.

In this project, the latter approach has been chosen to outline an extreme scenario. It is important to emphasise that the scenario is not a strategic consideration or option of any of the associations involved in the project. Rather, it is a wild card that, if it were to materialise, would be extremely relevant for the industrial Mittelstand. At the same time, thinking about this scenario can also include thinking about how such an extreme scenario could be avoided.

Wild cards are therefore extreme thought experiments that deliberately leave today's frame of reference in order to depict more extreme developments.

Many wild cards have different variations, i.e. there are different conceivable ways in which the wild card could occur or how it would manifest itself if it did occur (e.g. a wild card that assumes a revolution in a certain country could describe a revolution that takes place either peacefully or violently, just as it could lead to an orderly transition or a spiral of violence).

The extreme scenario described here is therefore not the only possible development path, but only one conceivable development option among several, which is representative of similar developments.

EXTREME SCENARIO:

GERMANY IN A DISINTEGRATING EUROPEAN UNION

As a result of massive tensions between the member states, which lead to an extreme policy of blockade, the states agree to abolish the EU treaties. In the process, the euro is abolished as the common currency and the Bundesbank reintroduces the Deutschmark. Resentments that were thought to have been overcome long ago resurface. All former EU states slip into a massive recession. Businesses and politicians panic and try to reorganise.

THE PATH TO THE SCENARIO: DRIVERS AND SETTING THE COURSE

2024

⊳ Increasing dysfunctionality of the European institutions due to the targeted blockade policy of individual member states

⊳ Reform efforts fail, escalation of political conflicts leads to cancellation of EU treaties; the euro as a common currency is history

⊳ Reorientation of politics and companies under extremely difficult conditions

EXTREME SCENARIO:

IN A DISINTEGRATING EUROPEAN

UNION

SCENARIO WORLD 2030

As a result of the growing influence of Eurosceptic parties in EU member states, there is an increasing number of national unilateral efforts. Rulings by the European Court of Justice (ECJ) to curb such behaviour are being strongly resisted by the nation states concerned. The EU institutions are becoming increasingly dysfunctional, with fierce verbal battles between governments becoming the new normal. The disputes are fuelled by targeted fake news on social media, behind which intelligence services suspect non-EU governments. Some EU states are even beginning to make previously unthinkable military threats against each other. To prevent further escalation in this charged atmosphere, the European Commission proposes the termination of the EU treaties and the orderly dissolution of the European Union and the euro. This proposal is adopted unanimously by the European Council.

Turbulence after the resolution to dissolve the company

Immediately after the vote, however, there is turbulence during the dissolution, making an orderly liquidation impossible. France unilaterally introduces the franc, whereupon the Bundesbank reintroduces the deutschmark virtually overnight. The abrupt reintroduction means that the deutschmark is immediately 30% more expensive than the euro's southern European successor currencies. As with other historical dissolutions of cross-national currency alliances (e.g. Austria-Hungary, Yugoslavia, Soviet Union), this time there is a sharp fall in wages. To prevent goods from becoming much more expensive or cheaper in neighbouring countries, European governments are also introducing a large number of new trade barriers and tariffs. In many places, this is accompanied by a resurgence in public discourse of resentments that were thought to have been overcome, fuelled by national press organs and (social) media.

The German economy slides into a recessionary spiral, with falls of up to 15% of GDP. Tax revenues are collapsing and social security systems are being maintained on a makeshift basis through government bonds. At the geo-economic level, there is a race for bilateral trade agreements, especially in energy supplies. Germany's relative size gives it more bargaining power than other European countries. Supplier networks and complex value chains, some of which have taken decades to develop in Europe and have become increasingly differentiated, allowing a high degree of specialisation at individual locations, are suddenly being lost.

Supply problems and protests

The result is supply difficulties and bottlenecks, productivity losses, declining service quality, reduced competition and rising storage and transport costs. Prices for goods and services rise sharply. Mass redundancies follow, including in small and medium-sized enterprises, leading to a massive loss of confidence in business and entrepreneurship.

EXTREME SCENARIO:

GERMANY IN A DISINTEGRATING EUROPEAN UNION

(CONTINUED)

This leads to raucous protests outside company headquarters and production sites. Companies of all sizes, regions and sectors are facing massive legal uncertainty. To counter this, the German government - like other European countries - is transposing a large part of EU legislation into national law to ensure a stable regulatory framework.

Rapid departure from established locations in Europe

Many (export-oriented) Mittelstand companies are considering relocating outside Europe or even selling their failing companies, as many banks have also been hit by loan defaults. Investors from the US, Canada, China, South Korea and the Gulf States are capitalising on this difficult economic situation to take over medium-sized industrial companies in Germany. In the course of these takeovers, shareholders and management are exchanged, often resulting in the loss of the special corporate culture of German Mittelstand companies.

OVERVIEW: INDUSTRIAL SME SECTOR AND ENVIRONMENT IN 2030 IN THE SCENARIO "GERMANY IN A DISSOLVING EUROPEAN UNION"

Location conditions for industrial Mittelstand companies

Labour force and skilled workers and organisation of work

• Unstable framework conditions and collapsing tax revenues prevent extensive investment in infrastructure, leading to the infrastructure eroding.

• The supply of energy and raw materials is highly volatile and must be renegotiated via bilateral agreements. Trading partners exploit import dependencies, and planning uncertainty becomes a burden on companies.

• Due to legal uncertainties, bureaucratic complexity is increasing, and a large proportion of EU regulations are being transposed into national law.

• Skilled workers from former EU countries lose their residence permits overnight, as it were, and many return to their home countries as a result of mass redundancies.

• Mittelstand companies are trying to save jobs through short-time working and voluntary wage cuts.

• Despite all the redundancies, some sectors (e.g. healthcare and nursing) continue to lack suitable skilled labour.

The industrial Mittelstand in the dual transformation

The industrial Mittelstand in competition and markets

Organisation of value creation networks and supply chains

Social role of the Mittelstand sector

Political framework conditions for Mittelstand companies

Changes in the characteristics of the Mittelstand sector compared to 2024

• Investments in the ecological transformation are being put on the back burner, and demand for sustainable and climate-friendly products in Europe is also collapsing. Mittelstand companies are trying to position themselves more strongly in global markets with the help of non-European partners or investors.

• Industrial metaverses and virtual goods and services are becoming a kind of "lifeline" for many Mittelstand companies, as demand for industrial goods has collapsed in Europe. But not all of them can afford the required investments.

• Almost the entire German economy, including industrial Mittelstand, must reorganise their supply chains and value chains, while the strong Deutschmark makes it difficult to export at competitive prices.

• The imposition of customs duties is fundamentally changing European competition; competition between locations is more difficult and has intensified.

• The dissolution of the eurozone is having a negative impact on foreign direct investment, and the cost of financing foreign investment by the Industrial Mittelstand is rising.

• Value creation networks need to be fundamentally rethought and redesigned, and new dependencies will emerge (e.g. in digital infrastructure).

• The German government is trying to reduce dependence on raw materials through the circular economy and the bioeconomy.

• Many Mittelstand companies are the economic 'beacons of hope' in regions hit hard by the massive recession, but most are being forced to cut back, which is also leading to a sharp reduction in community involvement.

• German politicians are in permanent crisis mode, trying to create systemic stability and reassure the (financial) markets as much as possible.

• The geopolitical situation is changing as a result of the abolition of the EU. Non-European states are trying to play European states off against each other in negotiations for bilateral agreements and to increase their geostrategic influence.

• The face of the Mittelstand sector is changing radically as a result of targeted acquisitions and investors entering the market. Talk of the "end of the Mittelstand sector in Germany as we knew it" is making the rounds.

• The high level of location loyalty is decreasing due to investors entering the market, and the resilience of Mittelstand companies is reaching its limits.

WILD CARD SCENARIO:

IN A DISINTEGRATING EUROPEAN

UNION

SIGNALS FOR A POSSIBLE REALISATION OF THE SCENARIO

SIGNAL 1

SIGNAL 2

• Brexit was the first time a member state left the EU. If the UK recovers quickly from the socioeconomic shockwaves of the exit and the exit is even seen as a success, this could act as an incentive for other countries wishing to leave.

SIGNAL 3

• In many member states, Eurosceptic parties are polling high shares of the electorate. In Germany, for example, the AfD is at 18% in current election polls (as of 4 April 2024), while a majority in France can also imagine electing Marine Le Pen as president for the first time. In the Netherlands, Eurosceptic Geert Wilders was also able to secure a high share of the vote for his party in the November 2023 election. Hungarian Prime Minister Viktor Orban also called for the dissolution of the EU Parliament in its current form

SIGNAL 4

• According to the Task Force of the European External Action Service, which has been analysing Russian disinformation since 2015 and showing which narratives are repeatedly used, disinformation campaigns from the Russian side have increased massively since the beginning of the Russian war of aggression on Ukraine. One narrative is "the threat of collapse", which proKremlin disinformation uses to paint stories about the alleged collapse of individual Western countries or the entire EU.

SIGNAL 5

• A survey conducted by the think tank European Council on Foreign Relations (ECFR) in selected countries around the world revealed that confidence in the long-term stability of the EU is not very high in some countries. When asked "Do you think the European Union will fall apart in the next twenty years?“, 67% of respondents in China, for example, answered in the affirmative. In Saudi Arabia it was 62%, in Turkey 45% and in India still 40%.

• An analysis by the German Council on Foreign Relations (DGAP) suggests that the border closures during the coronavirus pandemic also led to a revival of old resentments between Europeans. Something similar was also observed during the euro crisis. This shows that international friendships in Europe are still fragile.

NOTES ON METHODOLOGY AND PROCESS

METHODOLOGICAL APPROACH

Medium-sized industrial companies in Germany are confronted with a large number of strategic uncertainties in the medium and long term. Strategic foresight offers tools in the form of methods to better deal with strategic uncertainties by systematically and methodically describing and developing future possibilities - always with the aim of generating new perspectives for action and establishing the ability to act in different development contexts.

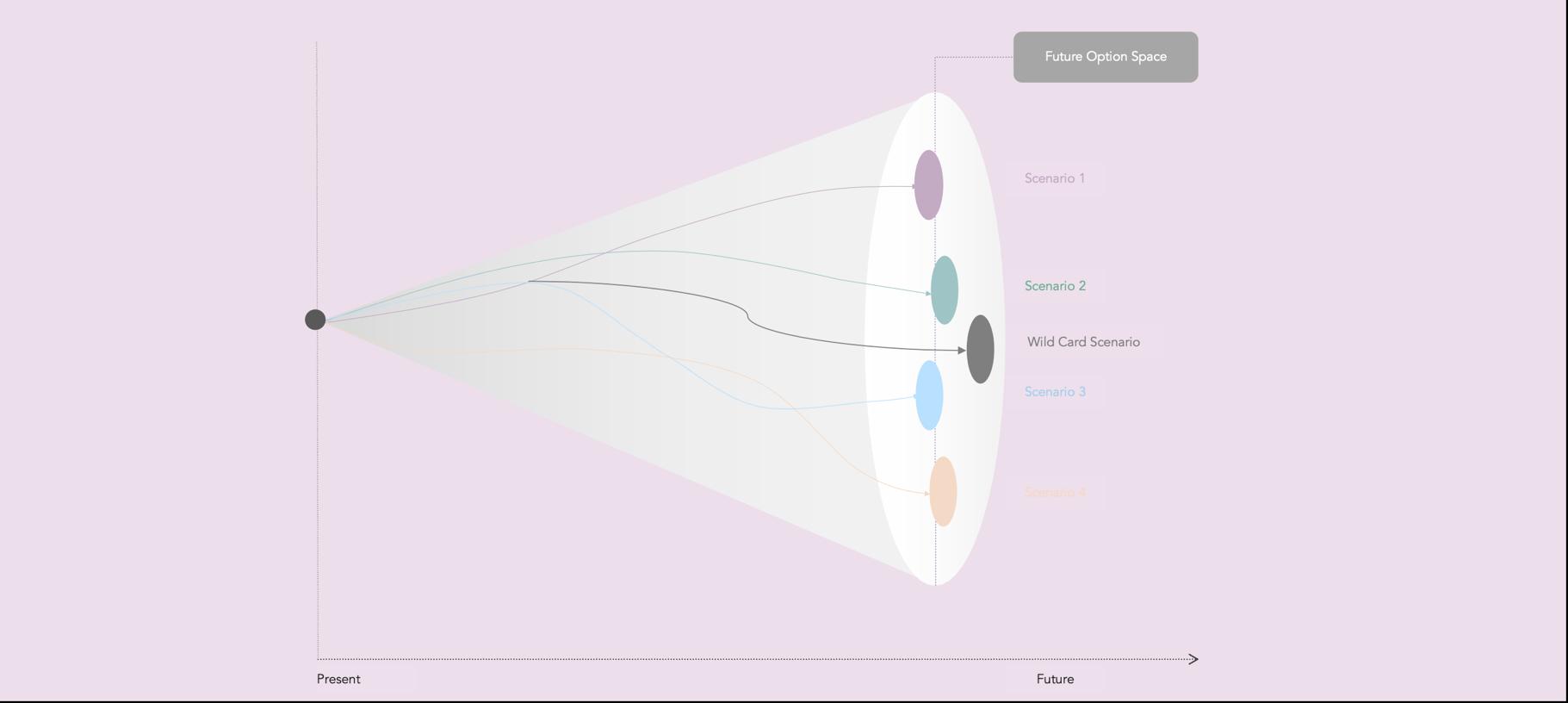

An established foresight method is the explorative scenario technique, on which this project is based.

WHY THINK IN SCENARIOS?

➢ Scenarios make it possible to think in terms of alternative future developments in order to deal with complex uncertainties.

➢ They encourage a deliberate and conscious opening up of future thinking.

➢ Scenarios are used to think through possible, plausible and desirable or undesirable directions of development.

➢ After discussing different scenarios, it is often easier to place individual current events in a medium- to long-term future context.

➢ Scenarios also promote (strategic) awareness of surprising events and developments.

➢ Last but not least, they are a means of strategic planning to make the opportunities and risks of the future tangible today, which also enables the derivation of consistent measures and courses of action for future strategies.

➢ Based on the discussion of the scenarios, new innovation and design potentials can be identified.

➢ The overarching goal of all futures research is to create the ability to act in different contexts.

PROCESS

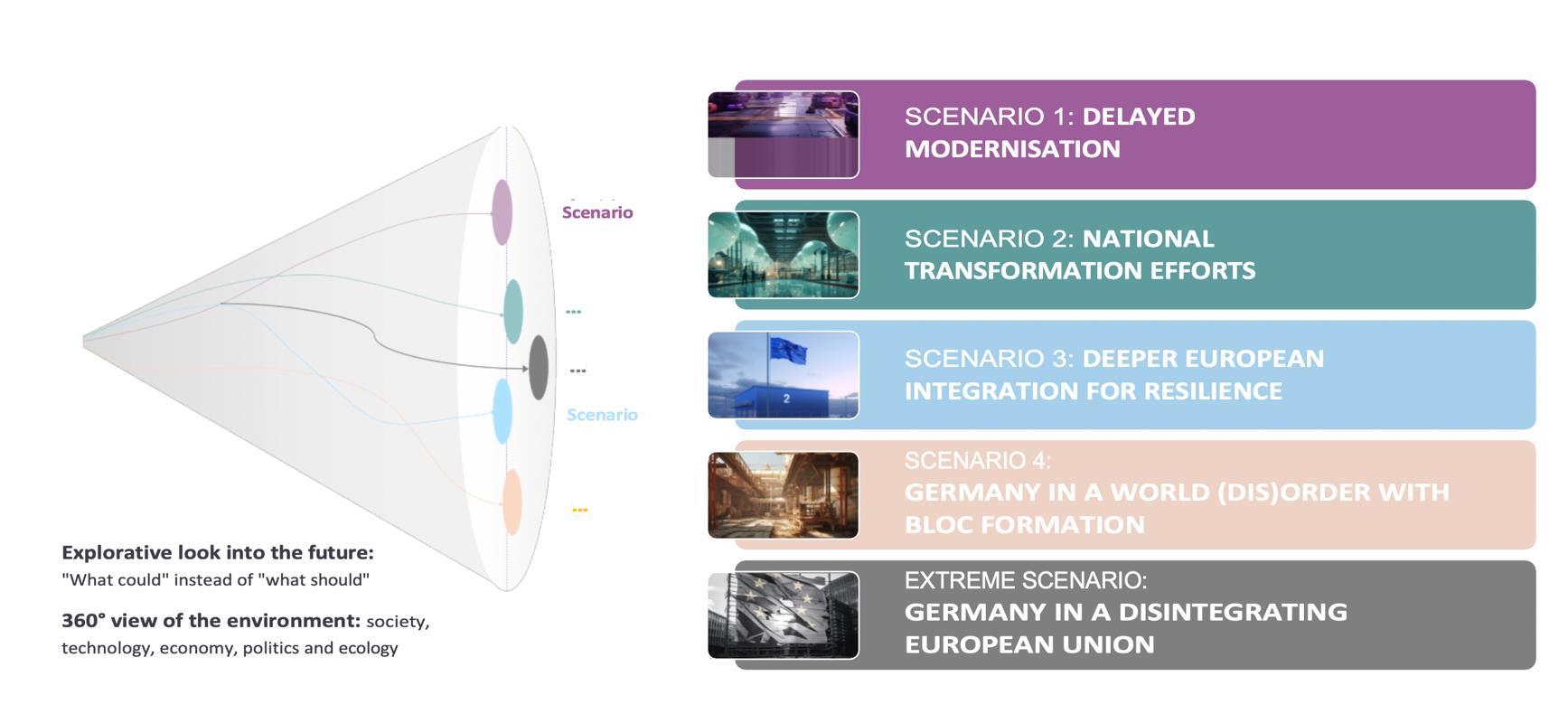

The scenarios in this project were developed through a systematic, multi-stage, participatory process, in which interim results were discussed and validated by the project group.

In the first phase of the project, a total of 32 influencing factors were identified through an environment scan. The aim of the environment scan is to provide a 360° perspective on the focal topic "The future of industrial Mittelstand in Germany".

For this purpose, the STEEP categories are used as a search grid to take into account influences from the areas of society, technology, economy, ecology and politics and to adopt a systemic perspective. Factors were included in the list which, according to a qualitative assessment, are considered to have a significant influence on the future organisation of industrial Mittelstand companies in Germany up to 2030.

A wide range of sources on the future of the industrial Mittelstand in Germany were analysed for the environment scan.

NOTES ON METHODOLOGY AND PROCESS

OVERVIEW OF THE 32 INFLUENCING FACTORS ALONG STEEP SECTORS

SOCIETY

DEMOGRAPHY COMPUTING, KI AND ROBOTICS

MIGRATION

SOCIAL COHESION AND PUBLIC DISCOURSE

DOMINANT ATTITUDES AND VALUE PATTERNS

LEVEL AND SYSTEM OF EDUCATION

QUALITY OF LIFE AND HEALTH

DIGITALISATION AND DIGITAL INFRASTRUCTURES

BIOTECHNOLOGY AND NEW MATERIALS

MANUFACTURING AND PROCESS TECHNOLOGIES

RESEARCH, TECHNOLOGY AND INNOVATION POLICY

ENERGY AND ENVIRONMENTAL TECHNOLOGIES

ECONOMIC DEVELOPMENT IN GERMANY

ELECTRICITY MIX AND ELECTRICITY PRICES

AVAILABILITY AND PRICES OF HYDROGEN AND NATURAL GAS

TAXES AND DUTIES

TRANSPORT INFRASTRUCTURE AND ACCESS TO SOCIAL INFRASTRUCTURE

AVAILABILITY OF LABOUR AND CHANGES IN THE WORLD OF WORK

INTERNATIONAL NETWORKING, TRADE AND VALUE CHAINS

INNOVATION ECOSYSTEMS AND (NEW) AREAS OF VALUE CREATION

CAPITAL MARKET AND FINANCING

RAW MATERIAL AVAILABILITY AND DEPENDENCIES

CIRCULAR ECONOMY AND CIRCULARITY

EFFECTS OF CLIMATE CHANGE

ENVIRONMENTAL AND CLIMATE-RELATED REGULATION

GEOPOLITICS AND GLOBAL ORDER

REGULATION AND BUREAUCRACY

STATE FINANCING

STABILITY OF THE POLITICAL FRAMEWORK

INDUSTRIAL POLICY

EUROPEAN TRANSFORMATION POLICY

PREVAILING PARADIGMS OF SPATIAL AND URBAN PLANNING

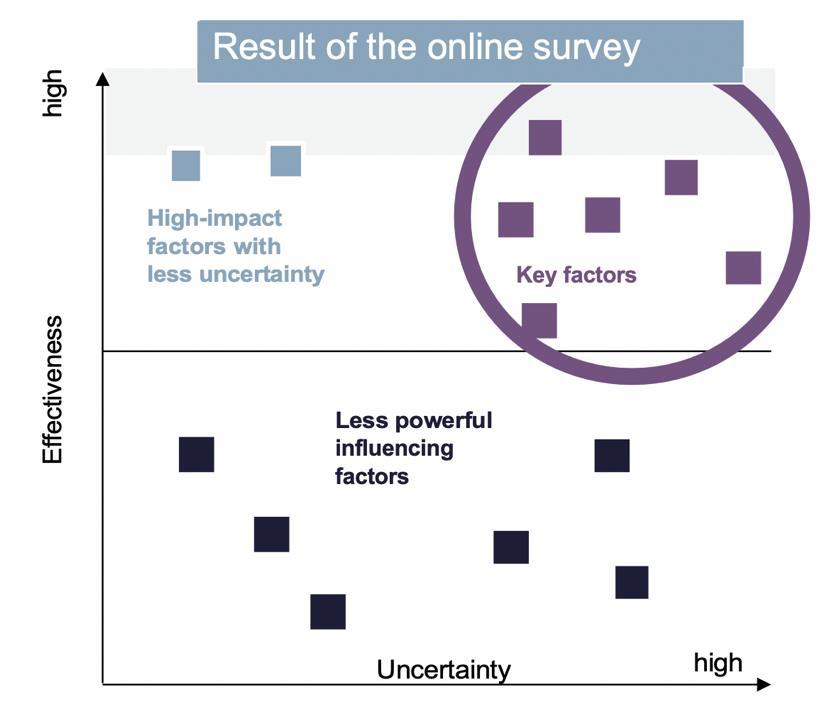

In a second step, the key factors were identified in an online survey using an impact uncertainty analysis based on the qualitative assessments of the project group. The focus on selected key factors is intended to make the complexity of the scenario topic manageable and at the same time to show which factors are most relevant from the project group's point of view and which are subject to the greatest uncertainty.

• Factors with a high impact on the organization of the industrial Mittelstand up to 2030

• Factors with high uncertainty: Various developments are plausible for the factor up to 2030 (various alternative futures can be derived from factors with high uncertainty)

Key factors are those factors that the project group considered to be crucial for the further development of the scenarios. These are, therefore, those of the 32 influencing factors to which the project group attributed the greatest influence and, at the same time, the greatest uncertainty with regard to their further development. Factors with a high degree of uncertainty are of particular interest for scenario planning, as different scenarios can be derived from their unpredictability.

The key factors therefore always provide an important indication of which factors are considered by the project group to be most relevant for future consideration. The results of the assessments were then discussed and validated with the project group in a validation workshop. Individual influencing factors were also combined into aggregated key factors. In total, 14 key factors were identified.

NOTES ON METHODOLOGY AND

SOCIETY TECHNOLOGY ECONOMY ECOLOGY POLITICS

DEMOGRAPHY

MIGRATION

SOCIAL COHESION, PUBLIC DISCOURSE AND VALUE PATTERNS

COMPUTING, AI AND ROBOTICS

DIGITALISATION AND DIGITAL INFRASTRUCTURES

LEVEL AND SYSTEM OF EDUCATION

QUALITY OF LIFE AND HEALTH

BIOTECHNOLOGY AND NEW MATERIALS

MANUFACTURING AND PROCESS TECHNOLOGIES

ECONOMIC DEVELOPMENT IN GERMANY

SECURITY OF SUPPLY AND PRICE LEVEL OF ENERGY SYSTEM (ELECTRICITY, H2 , NATURAL GAS)

TRANSPORT

INFRASTRUCTURE AND ACCESS TO SOCIAL INFRASTRUCTURE

AVAILABILITY OF LABOUR AND CHANGES IN THE WORLD OF WORK

INTERNATIONAL NETWORKING, TRADE AND VALUE CHAINS