(Incorporated in the Republic of South Africa with limited liability under registration number 2022/521382/06)

JSE Alpha Codes:

AGRIA1 ISIN: ZAG000191214

AGRIB1 ISIN: ZAG000202797

LEI: 378900376E9ADF2BD166

(“Agrarius”)

Issue Date: 30 April 2025

Introduction

In terms of paragraph 6.83(a)(ii) of the JSE Limited (“JSE”) Debt & Specialist Securities Listings Requirements (“JSE D&S LR”), issuers of asset-backed securities are required to publish investor reports on a quarterly basis (in accordance with the issuer’s financial year-end or the periodic profit distribution dates of the relevant asset-backed securities) detailing interalia, the performance of the underlying assets, as well as any defaults that may have occurred in respect of such underlying assets.

Agrarius hereby presents its investor report for the three months ended 31 March 2025 (“the Reporting Period”). Agrarius’ previously published investor report was for the 3 months ended 31 December 2024.

The Agrarius Note Programme is a R10 billion, Shari’ah compliant asset-backed note programme in terms of which JSE listed and unlisted asset-backed securities are issued, the proceeds of which are invested in sustainability-focussed projects and transactions in the agriculture sector value chain.

During the Reporting Period, no underlying assets were subject to a demand to repurchase or replace due to a breach of the representations and warranties contained in the underlying transaction documentation.

Investor Summary

South African Economic Environment

The outlook for the South African economy softened somewhat in Q1 2025, with the announcement of an increase in trade tariffs in the United States at the start of Q2 2025 casting significant uncertainty over local and global economic growth. Despite the global turmoil, South Africa’s inflationary environment remains stable, with a decrease in the price of oil and a stabilising rand further giving the South African Reserve Bank some room to decrease interest rates should economic growth falter.

On the political front, the parties making up the South African government appear to have resolved their budget disputes, removing some of the uncertainty that had weighed on local markets and the currency. While slow, improvements in the network industries of electricity and logistics are expected to continue, increasing South Africa’s global competitiveness.

Investments in South Africa: Private Credit Performance

South Africa’s private credit market continued its robust expansion, driven by increased demand for non-bank lending as traditional banks remained constrained byregulatoryand liquidity requirements. Private credit funds played a vital role in bridging the funding gap for mid-sized and growth-stage businesses, particularly small and medium enterprises (SMEs), which face an estimated R590 billion.

General Agricultural Sector Performance

South Africa’s agricultural sector showed signs of recovery and renewed optimism in Q1 2025 following a challenging 2024 marked by drought and animal disease outbreaks. The Agbiz/IDC Agribusiness Confidence Index surged to 70, its highest level since 2021, reflecting improved sentiment across most subsectors, driven by favourable La Niña rainfall, better port efficiencies supporting exports, and progress in animal disease control.

Crop conditions generally improved, with planting proceeding well in most regions, though some areas continued to feel the effects of erratic rains and heat stress from late 2024. Major field crops such as soybeans and sunflowers saw strong deliveries, but maize and wheat production and exports remained below previous years due to lingering drought impacts. Livestock faced ongoing price pressures, but export prospects brightened as biosecurity measures improved Overall, while the recovery was uneven across regions and commodities, the sector was a key driver of economic growth in Q1 2025, buoyed by robust confidence, improved weather, and export momentum

Citrus

Vegetables and Potatoes

South Africa’s citrus industry entered 2025 on a stable and optimistic footing, with export volumes for key varieties such as oranges and grapefruit projected to rise by 5–6% compared to the previous season, reflecting a return to the five-year average and strong fruit quality. Despite these positive production and export forecasts, the industry was hit by a major challenge in April when the United States imposed a sudden 30–31% import tariff on South African citrus, threatening the sector’s competitiveness in a key market andraising concerns aboutpotential job lossesin rural areas. In response, industry leaders called for urgent government intervention and accelerated efforts to diversify export destinations, particularly in Asia and the Middle East. While logistics and port efficiency remain areas of focus, the citrus sector’s outlook for 2025 remains resilient, buoyed by strong global demand and robust export planning, even as it navigates significant new trade barriers.

The vegetable and potato industries showed cautious recovery in early 2025 after a difficult previous year marked by weather shocks and high input costs. Potato production rebounded modestly, with a slight increase in plantings encouraged by strong late-2024 prices, while overall output stabilized despite ongoing weather risks and regional supply dips. Vegetable producers benefited from marginally lower input costs, though high electricity tariffs and logistical challenges persisted. Export opportunities for potatoes improved, with a notable year-on-year increase in shipments, particularly to Namibia.

Grain

Better rainfall boosting crop prospects after a tough 2024. Maize and wheat production rebounded modestly, though maize exports for the 2024/25 season are expected to be lower than last year due to earlier drought impacts and reduced regional demand. Soybean and sunflower deliveries were strong, and overall crop conditions improved, but wheat output remained slightly below the previous year because of smaller plantings and patchy yields. A new risk factor on the horizon is heavy rain hampering harvesting activities in many grain producing areas.

South Africa’s livestock sector showed early signs of recovery after a tough 2024 marked by high input costs, disease outbreaks, and weak consumer demand. Beef, lamb, and pork prices began to stabilize, with analysts expecting modest increases through the year as herd liquidation slowed and feed prices eased, supporting improved profitability. The ostrich industry, which supplies over half of the world’s ostrich meat, leather, and feathers, benefited from the end of a prolonged drought and strong international demand for leather and feathers, leading to higher producer prices and a more lucrative production cycle. However, chick production was hampered by wet and cold conditions, potentially limiting slaughter numbers but helping sustain high prices. While ostrich meat demand remained steady, the sector’s export orientation and rural job creation continued to underpin its importance to the national economy.

Issuer And Main Objective/Purpose Of The Transaction Or Programme

Name of the issuer

Agrarius Sustainability Engineered (RF) Limited

Main objective/purpose of the transaction or programme

Agrarius is a special purpose investment vehicle that issues JSE-listed Shari’ah compliant asset-backed securities in terms of its ZAR10 billion Shari’ah compliant asset-backed note programme, the proceeds of which are invested in sustainability-focussed transactions and projects in the agriculture sector value chain by Agrarius Agri Value Chain RF Proprietary Limited (“Agrarius OpCo”), in terms of a formal master investment agreement entered into with Agrarius.

Table2:AgrariusNoteProgrammeInformation

Agrarius Note Programme Information

Transaction type

ZAR10 billion Shariah compliant, sustainabilityfocussed asset-backed note programme, the investment proceeds of which are invested in projects and transactions in the agriculture sector value chain.

Single issue transaction or programme Note Programme

Revolving or static securitisation/conduit/A BS type

Inception dates

Originator

Revolving/conduit asset-backed structure

AGRIA1 – Inaugural issuance - 28 October 2022

AGRIA1 Tap issuance – 2 February 2024

AGRIB1 – Inaugural issuance - 2 February 2024

Unlisted 1 – 19 February 2024

Unlisted 2 – Inaugural issuance – 9 January 2024

Unlisted 2 Tap issuance – 27 January 2025

Unlisted 3 – 12 February 2025

Unlisted 4 – 12 February 2025

Agrarius OpCo

Back-up or standby servicer

Agrarius OpCo, pursuant to a formal cession agreement and indemnity entered between the Guarantor and Agrarius OpCo, in terms of which the security assets obtained by Agrarius OpCo in its transactions are ceded to the Guarantor for purposes of backing the limitedrecourse guarantee granted by the Guarantor to investors under the note programme.

Maximum programme / issue size (if applicable) ZAR 10 billion, which may be increased in the manner set out in the Note Programme documentation

Reporting Period 1 January 2025 – 31 March 2025

Rating agency (if applicable)

Credit rating of programme (if applicable)

Contact person details

Number of tranches issued under the Agrarius Note Programme and date of issue

JSE Debt Officer: Johan Fourie

Telephone Contact Number: 011 442 2464

Email: info@27four.com

Chief Executive Officer: Werner Opperman

Telephone Contact Number: 011 442 2464

Email: info@27four.com

Agrarius (listed notes):

1. AGRIA1 – 1st tranche issued on 28 October 2022 to the value of ZAR 500 million

2. AGRIA1 – Tap issuance on 2 February 2024 to the value of ZAR 100 million

3. AGRIB1 – 2nd tranche issued on 2 February 2024 to the value of R300 million

Agrarius Crocodile River SPV (Pty) Ltd

Unlisted debentures issued on 19 February 2024 to the value of R100 million.

Agrarius Bergrivier SPV (Pty) Ltd

1. Unlisted debentures issued on 9 January 2024 to the value of R2 million.

2. Tap issuance on 27 January 2025 to the value of R1.25 million.

3. Unlisted debentures issued on 12 February 2025 to the value of R36 million.

4. Unlisted debentures issued on 12 February 2025 to the value of R36 million.

Type of instruments issued

Listed instruments: Shariah compliant, sustainabilitylinked asset-backed Sukuk notes listed on the JSE

Support Services Administrator RealFin Fund Services (Pty) Ltd

Underlying Asset data

–

Type of Underlying Assets

Notes to Table 3:

1. Underlying assets measured at top level. Each counterparty may have multiple assets nested beneath its respective top level.

2. For purposes of clarity, this refers to the reference rate linked to all Underlying Assets

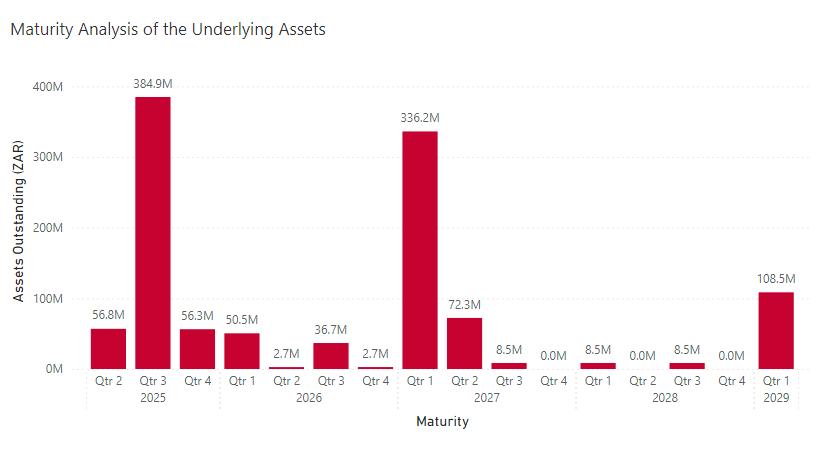

Figure3:MaturityAnalysisoftheUnderlyingAssets

Table4:AssetData–TotalUnderlyingAssets

All Underlying Assets are Unlisted Shariah Compliant Financing Structures with South Africa as Country of Origin.

Notes to Table 4:

1. The counterparties for Assets 3, 4 and 5 are currently in arrears on some of their repayments and revised repayment schedules have been agreed or are about to be agreed on with these counterparties with the newly agreed expected maturity dates captured in Table 4. All assets, with a strong focus on those currently in arrears, are actively managed and the Agrarius team regularly engages with counterparties, both remotely and on location. All assets are securitised, with sufficient collateral to cover the outstanding balances.

Agrarius Notes Data

Table5:MaturityData

Total principal repaid to Reporting Date

Notes outstanding R600,000,000 initial nominal amount plus tap issuance

Maturity date of the notes

initial nominal amount plus tap issuance

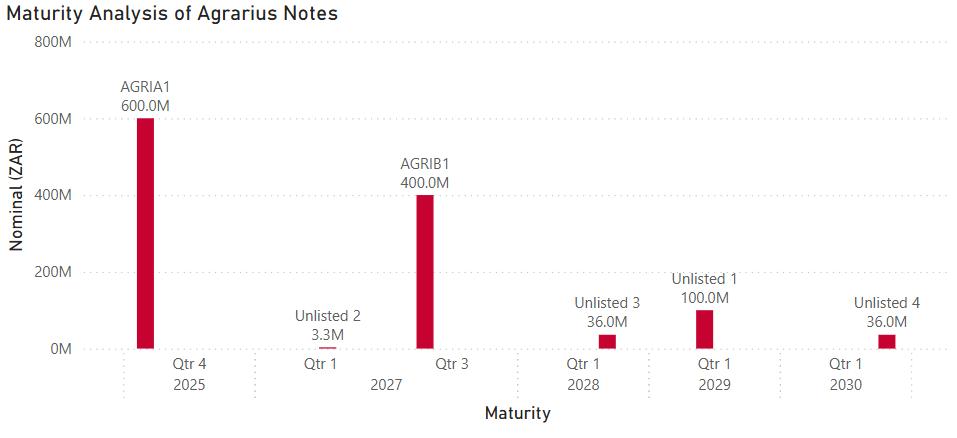

Figure4:MaturityAnalysisofAgrariusNotes

Face value (if applicable)

ZAR 1.00 (one Rand) per Sukuk

Note

ZAR 1.00 (one Rand) per Sukuk

Note

ZAR 1.00 (one Rand) per Debenture

ZAR 1.00 (one Rand) per Debenture

ZAR 1.00 (one Rand) per Debenture

ZAR 1.00 (one Rand) per Debenture

* The instruments issued under the note programme are secured by the Guarantor, in terms of a formal limited recourse guarantee issued in favour of all investors under the Note Programme (“AVC Guarantee”). The AVC Guarantee is issued on the back of a formal cession agreement and an indemnity agreement entered between Agrarius OpCo and the Guarantor (“Agrarius OpCo Cession and Indemnity”).

In terms of the rules of the Note Programme, the holders of the unlisted instruments waive and abandon any rights they have under the AVC Guarantee in favour of the holders of the listed instruments (“Secured Noteholders”), thereby creating a structural subordination. The key term of the AVC Guarantee is that the Guarantor guarantees the payment obligations of Agrarius, being the issuer of the listed instruments. The Secured Noteholders will have limited recourse to the Guarantor and Agrarius OpCo. The ability of Agrarius to pay the amounts due in respect of the secured notes is entirely dependent on the returns generated in respect of the investments which investments are, in turn, dependent upon the performance of the underlying transactions.

Type of note

Secured, Floating Rate Sustainability-linked asset-backed notes, certified as Shariah compliant Sukuk to the value of ZAR600 million, being the Agrarius Sukuk

Secured, Floating Rate Sustainabilitylinked asset-backed notes, certified as Shariah compliant Sukuk to the value of ZAR300 million, being the Agrarius Sukuk

Shariah compliant, floating rate debentures – unlisted instruments to the value of ZAR100 million

Shariah compliant, floating rate debentures – unlisted instruments to the value of ZAR3.25 million

Shariah compliant, floating rate debentures –unlisted instruments to the value of ZAR36 million

Shariah compliant, floating rate debentures –unlisted instruments to the value of ZAR36 million

Long

(if applicable)

amount (if a onceoff issuance)

reporting date

Reference rate (including margin, if applicable)

JIBAR plus 4.75% percent per annum

(Please refer to the explanatory note on the calculation of the Reference Rate on the final page of this report). JIBAR plus 4.25% percent per annum

(Please refer to the explanatory note on the calculation of the Reference Rate on the final page of this report).

plus 5.15% percent per annum

plus 4.75%

plus 3.75%

plus 4.00%

Profit share payment

paid (if applicable)

The Periodic Distribution of R37,516,981.20 for the period 1 October 2024 to 31 March 2025, paid on 31 March 2025.

The Periodic Distribution of R18,511,638.60 for the period 1 October 2024 to 31 March 2025, paid on 31 March 2025.

The Periodic Distribution of R6,619,321.80 for the period 1 October 2024 to 31 March 2025, paid on 31 March 2025.

The Periodic Distribution of R205,308.75 for the period 1 October 2024 to 31 March 2025, paid on 31 March 2025.

The Periodic Distribution of R544,437.50 for the period 1 October 2024 to 31 March 2025, paid on 31 March 2025.

No Periodic Distribution payable during the period 12 February 2025 to 31 March 2025.

March

Explanatory note on the reference

As outlined in the applicable pricing supplement dated 7 November 2022, detailing As outlined in the applicable pricing supplement dated 2 February 2024, As outlined in the salient terms and conditions of the debentures: As outlined in the salient terms and conditions of the debentures: As outlined in the salient terms and conditions of the debentures: As outlined in the salient terms and conditions of the debentures:

the terms of the Sukuk (“APS”):

Rate Determination

Method: The Reference Rate is determined using the Screen Rate Determination method (Reference Rate plus Margin).

Reference Rate: The 3month ZAR-JIBAR, which is determined on the last Calendar Day of each Calendar Month as the benchmark rate for the following Calendar Month. This rate is calculated using a simple rate of return (not compounding).

Margin: A margin of 4.75% is added to the Reference Rate. Whilst the Reference Rate Reset Date is not specifically stated in the APS, it can be interpreted from the wording of the Reference Rate in the APS that the reset occurs on a monthly basis

detailing the terms of the Sukuk (“APS”):

Rate Determination

Method: The Reference Rate is determined using the Screen Rate Determination method (Reference Rate plus Margin).

Reference Rate: For the first periodic distribution period the 9-month ZARJIBAR , which is determined on 30 January 2024 (or such other generally adopted reference rate to be promulgated by regulation under the Financial Sector Regulation Act 9 of 2017, as amended by which it may be succeeded and/or replaced prior to the Maturity Date).

For all subsequent periodic distribution

Reference Rate: For the First Periodic Distribution Period, the 9 month ZARJIBAR as determined on 30 January 2024 (or such other generally adopted reference rate to be promulgated by regulation under the Financial Sector Regulation Act 9 of 2017, as amended by which it may be succeeded and/or replaced prior to the Maturity Date).

For all subsequent Periodic Distribution Periods, the 6-month ZAR- JIBAR (or such other generally adopted reference rate to be promulgated by regulation under the Financial Sector Regulation Act 9 of 2017, as amended by which it may be succeeded and/or

Reference Rate: For the First Periodic Distribution Period, the 9 month ZARJIBAR as determined on 30 January 2024 (or such other generally adopted reference rate to be promulgated by regulation under the Financial Sector Regulation Act 9 of 2017, as amended by which it may be succeeded and/or replaced prior to the Maturity Date).

For all subsequent Periodic Distribution Periods, the 6-month ZAR- JIBAR (or such other generally adopted reference rate to be promulgated by regulation under the Financial Sector Regulation Act 9 of 2017, as amended by which it may be succeeded and/or

Reference Rate:

The 6 month ZARJIBAR or such other generally adopted reference rate to be promulgated by regulation under the Financial Sector Regulation Act 9 of 2017, as amended by which it may be succeeded and/or replaced prior to the Maturity Date.

Margin: A margin of 3.75% is added to the Reference Rate.

Reference Rate:

The 6 month ZARJIBAR or such other generally adopted reference rate to be promulgated by regulation under the Financial Sector Regulation Act 9 of 2017, as amended by which it may be succeeded and/or replaced prior to the Maturity Date.

Margin: A margin of 4.00% is added to the Reference Rate.

In terms of the APS: “3 monthZAR-JIBAR, determinedonthelast CalendarDayofaCalendar Monthforthereference rateapplicabletothe followingCalendarMonth asbenchmarkusinga simplerateofreturn(not compounding) . ”

Rationale for the monthly reset: The Agrarius Sukuk is designed as a floating rate asset-backed note, primarily due to the shortterm nature of the underlying transactions with counterparties in the agriculture sector, with terms typically ranging between 3 to 12 months. Given this characteristic, a floating rate structure aligns perfectly with the dynamic nature of these agricultural transactions, and it ensures that the Sukuk remains in sync with the prevailing market conditions and Reference Rate movements over the relatively short transaction

periods the 6-month ZAR-JIBAR (or such other generally adopted reference rate to be promulgated by regulation under the Financial Sector Regulation Act 9 of 2017, as amended by which it may be succeeded and/or replaced prior to the Maturity Date). This rate is calculated using a simple rate of return (not compounding).

Margin: A margin of 4.25% is added to the Reference Rate.

replaced prior to the Maturity Date).

Margin: A margin of 5.15% is added to the Reference Rate.

replaced prior to the Maturity Date).

Margin:

A margin of 4.75% is added to the Reference Rate.

terms. As a result, it provides a fair and competitive mechanism for both Sukuk holders and the issuer, facilitating a more effective and efficient financing solution for all parties involved in these agricultural transactions, while remaining Shariah compliant.

Disclaimer: This document is strictly for information purposes only and should not be considered as an offer, or solicitation, to deal in any of the investments mentioned herein. Any information and opinions contained in this communication, and any supplemental information provided, is believed to be reliable but no representation or warranty is given as to its correctness, accuracy or completeness. Any representation or opinion is provided for information purposes only. We do not undertake to update, modify or amend the information on a frequent basis or to advise any person if such information subsequently becomes inaccurate. It is not intended to create, and shall not be capable of creating, any obligation or liability on the part of 27four Investment Managers or any of its affiliates, and shall not form part of any contract. All information and opinions provided are of a general nature and are not intended to address the circumstances of any particular individual or entity. We are not acting and do not purport to act in any way as an advisor or in a fiduciary capacity. Any decision to invest must be made by the recipient solely on the basis of its own independent judgement and research and subject to the terms and conditions governing applications to any relevant fund. No one should act upon such information or opinion without appropriate professional advice after a thorough examination of a particular situation. While opinions stated are honestly held, they are not guarantees and should not be relied on. Please note that past performance figures are not audited and should not be taken as a guide to the future. 27four Investment Managers will not be held liable or responsible for any direct or consequential loss or damage suffered by any party as a result of that party acting on or failing to act on the basis of the information provided in this document. This document may not be amended, reproduced, distributed or published without the prior written consent of 27four Investment Managers. 27four Investment Managers is an authorised financial services provider with license number 31045.