YRL REAL ESTATE TALK

SEARCH HOMES CLICK HERE

YOUR LINK TO EVERYTHING HOME YOUR PREFERRED VENDORS

HOME IMPROVEMENT TIPS

BUYER & SELLER DOs & DON’Ts

DIYHOMEIMPROVEMENTFAILURES

HOWTOMAKEANYROOMCOZY

FINDAYRLAGENT

May2023

SEARCH HOMES CLICK HERE

YOUR LINK TO EVERYTHING HOME YOUR PREFERRED VENDORS

BUYER & SELLER DOs & DON’Ts

DIYHOMEIMPROVEMENTFAILURES

HOWTOMAKEANYROOMCOZY

FINDAYRLAGENT

May2023

YRLRealEstateTalkisourownpersonal magazinedigitallyofferedeachmonthtoour buyersandsellersandthosewholovetokeep uponrealestatenewsinourarea.Weoften havesaidinourofficethat“REALTORSshould writebooks“soherewego!

Themagazineisfreeandifyousharewitha friendtheycanalsoreceivethemagazine throughtheiremail.Emailusandrequesttobe addedtoourlist-BTWthismagazinewillkeep youinformedandalwaysprovideusefulreal estateinfobutwepromisethatwewon’tbe repeatingandsendingconstantemails-justone newpublicationeverymonth!

EMAILUSFreeMagazine@YourRealtyLink.comforyour copy!

Our main office is at 2302 E Southport Rd, Indianapolis, IN 46227 (we are right across from Long’s Bakery). We would love to discuss any of your real estate needs! Call or text 317.997.7404 and let’s set a time to meet.

We will put the coffee pot on!

Buying a home can be a financial stretch. With soaring home values and rising interest rates, many potential first time home buyers find saving for a down payment increasingly difficult. For many people, the main source of savings is in the form of a 401k and tapping into this resource for a home purchase is one way to find the down payment necessary to finance a new home; but should you use your 401k to buy a home? Experts are conflicted.A401k is a retirement savings plan offered by employers which takes pre-tax earnings and deposits it into an investment account for use in retirement.The money in a 401k account can be accessed by either taking out a loan against the balance or by a straight withdrawal. A

withdrawal before the age of 59.5 is also subject to a 10% penalty.Taking out a loan from a 401k account may be a viable option for potential home buyers. For one thing, a loan from your 401k should not count against your borrowing power.You also don’t need to qualify because you are borrowing from yourself.The amount you can borrow is limited, for example 50% of the balance, and typically must be repaid within 5 years.The other option is a simple withdrawal; the 10% penalty is incurred, but the value is not usually limited. Saving for a down payment can be challenging. Using your 401k to help may be a great option. Speak with your financial advisor and see if this is the right financial move for you.

The real estate industry is in for a wild ride over the next year, according to the Realtor.com's 2023 Housing Market Predictions Report.This forecast predicts an overall positive outlook with ongoing growth, but it also acknowledges that several regional markets are more volatile than others and may not experience consistent gains.The report notes that there are some headwinds to sustained growth, particularly in regions affected by the pandemic and its economic fallout.Tightening credit conditions, an already low inventory of homes for sale, and historically high lumber costs may all put pressure on affordability and slow the housing market's progress.The good news is that many markets have been resilient and there are signs of optimism as the economy recovers. Realtor.com expects that home prices and sales activity will continue to rise in most markets, albeit at a slower pace.Affordability is projected to remain a challenge for some buyers, however, as potential buyers may have difficulty securing financing.The report also predicts an increase in rental activity over the next year

as renters take advantage of more affordable housing options and the flexibility that comes with not having to commit to a longer-term mortgage agreement.This could spell good news for investors looking to capitalize on these shifting trends. Overall, the 2023 National Housing Forecast predicts a continued rise in housing prices, though certain regional markets may be more volatile than others. It also forecasts an increase in rental activity as renters take advantage of the flexibility that comes with renting.All of this suggests a vibrant and dynamic real estate market going into 2023, so it’s important to stay informed and up-to-date with the latest trends. No matter where you are in your real estate journey, it’s important to stay abreast of the fluctuating market conditions. By doing so, you can ensure that you’re making informed decisions and leveraging the best opportunities available to you. With a comprehensive understanding of the current market conditions and the changing trends, you can make sure that you’re making the most of your investments and positioning yourself for success.

WeekendTV lineups are filled with Do-It-Yourself home improvement programs. One home inspector used to call the results “six-pack projects.” While not all DIYprojects end in disaster, some projects can harm home sales because buyers see these “improvements” as changes they will need to make once they buy the house. If you are planning to sell soon, it’s important to realize that potential buyers may not be as impressed with your handiwork as you are.

1. Garage ConversionHomebuyers love extra square footage, but they don’t want it in the garage. Most buyers will plan to “unconvert” a game room back to space for their cars or storage.

2. New Doors – New doors can add beauty to a room, but if they are not mounted properly, they land on a new buyer’s list of things to fix.

3. Uneven Hardware – If you are trying to update cabinets with new hardware make sure they

are level and line up evenly.

4. Crown Molding –Seems like an easy upgrade but adding elegant crown molding is very difficult and dan end up looking sloppy.

5. Painting to Hide Problems – Cracks, gaps, and surface defects only look worse when covered with fresh paint.

6. Kitchen Cabinets –Old, worn cabinets should be replaced if possible.As with the walls, a fresh coat of paint only accentuates the dated look. Every seller knows they need to freshen their home and add curb appeal to list their home before launching into a frenzied weekend of DIYprojects,

In previous decades, a warm, cozy home required dark colors and heavy materials. One can envision sitting in front of a roaring fire in a dark room filled with pillows and wood paneling. Contemporary homes are brighter, with clean lines and light colors and textures. The challenge is how to create an inviting, cozy space that everyone wants during the cooler months. Fortunately, it’snotnecessarytochoosebetweenthe claustrophobic styles of the past and warm inviting rooms. The first tip is lighting. Soften the lighting and consider swapping cold, metal fixtures for ones using natural materials, such as willow or linen. Next, layer blankets throughout the home. Imagine the luxury of falling into a soft bed with layers of cozy white blanketsandquilts.

Neutral colors gain/add dimension by contrasting subtle hues of the same palate. We change our lifestyle during colder months as well. Lifestyle shifts from our outdoor spaces to interior rooms. Create a warm beverage station to invite guests and family members to relax and unwind. Add pillows to sitting areas to build comfort in living rooms. Finally, add scent to the home. Candlelight not only sets a relaxing mood but fills the space with soothing smells of the season. Cozy, inviting spaces do not have to mean dark colors and heavy materials. Layering is the easiest way to create a softer, warmer room. Combine this with a few seasonal candles and touches, and any room can be cozier this weekend with only a few smallchanges.

We love shopping for “COZY” at HomeGoods - Kirklands - Marshalls - Wayfair

Where do you shop to decorate?

For decades, gas stoves have been the preferred choice for both professional and amateur chefs alike and it’s easy to understand why. Gas stoves allow for quick control of the heat which allows for quick adjustments when cooking. But recently possible bans on gas stoves have dominated national news as unhealthy. Regardless of whether induction stovetops are healthier or not, there are great reasons to make the switch. What is an Induction Range? In simple terms, an induction electric range is powered by an electromagnetic field.This allows the range to have the same degree of temperature as a gas powered stove with a similar level of control.

The first thing to realize in making the switch is that you’ll pay more for an induction stove than a gas range.The increase in cost may be as much as double the price and the installation will require special wiring and circuitry. But this increase in upfront costs will start to pay off very quickly. First, homeowners can take advantage of a federal rebate of up to $480 and an additional $500 to help with the cost of installation. In addition, these new induction ranges will save energy costs over gas.There is evidence to suggest that there are significant health advantages as well. This is the reason for the proposed ban in the first place. Gas stoves emit carbon dioxide which can be hazardous without the proper ventilation or for family members with medical issues. Even without the ban, it’s time to look at some of the great induction ranges on the market and consider making the switch.

Also, you must be sure that your cookware is made for induction heat. You won’t be able to use your old pots and pans unless it shows on the cookware the induction symbol.

We had a great month ofApril representing both buyers and sellers ‘in a pretty tough market’. Listings are low and interest rates have risen BUTour agents are keeping busy AND WINNING BIDS FOR BUYERSAND DOINGAGREAT JOB OF MARKETINGYOUR LISTINGS! Are you Next?

We plan to publish monthly and send to our agent’s email list -YRLTALK will always contain new articles and the last part of the magazine will be helpful info for buyers and sellers and promote our vendors. If you have a friend who would like a free digital copy, let us know. SHARE!

Plants may not be considered furniture, but they are nonetheless an aspect of interior design worth mentioning, as they are important allies for bringing health and quality of life to the indoors.

They purify the air and absorb chemicals that are very common in residential and corporate interiors.The common recommendation is to have a medium-sized plant for every 10m² of space.

Florists have spoken extensively about comfort in interior spaces for the past few years.

Environmental quality indoors is essential in an increasingly dense and populous world, and an uncomfortable, unsafe, or unhealthy interior space can be tremendously harmful to people's physical and mental health, considering that we spend so much of our lives in it.

Comfort ranges from the aesthetics of the space, the aroma of the environment, the breeze that enters through the window, and the temperature felt when entering, to its accessibility and application of technologies or passive strategies to facilitate and improve the quality of life of the inhabitant.

Farmhouse décor has been a trend for the last decade.The look combines functionality with a relaxed, lived-in feel. Pieces look slightly worn, rustic, and inviting.The ease of the farmhouse style is one of the reasons for its lingering appeal as designers look to modernize and update the look. Modern Farmhouse style continues to emphasize a neutral color palette and sustainable materials, such as reclaimed wood and used brick but adds more sophistication to the theme. Capitalizing on the boho trend, the Modern Farmhouse style might include accent pieces in wicker or kilim rugs and pillows, warming the room and merging it with more traditional elements. Contemporary designs such as Industrial and Scandinavian also get an update when mixed with Modern Farmhouse.The bright, light rooms of a Scandinavian Farmhouse look might include a rustic kitchen table or distressed flooring. While cold, Industrial design adds warmth with a sliding barn door entry or rich leather chairs.

The farmhouse style focuses on comfort, practicality, and an informal lifestyle. Today’s family enjoys this kind of living environment because it offers an easy and flexible design. Inexpensive accent pieces are also readily available which makes the style accessible to everyone. Modern Farmhouse is an updated version of the original, incorporating fresh looks and merging textures and palates to suit the contemporary homeowner.

Baby boomers have reached retirement age.This generation is healthier and more active than their predecessors and many want to age in a home of their own. Many of these potential home buyers have fixed incomes and with soaring home prices, they are unable to qualify for a new home when they are ready to downsize. This is where a Family Opportunity Mortgage can help. AFamily Opportunity Mortgage is backed by Fannie Mae and allows you to purchase a home for your elderly parents if they cannot qualify on their own, at the same favorable down payment and interest rates as a primary residence.This is a significant advantage over loan programs for second home or investment properties.The terms of the loan program are simple. The borrower needs a 620+ FICO score, steady

employment, and enough income to qualify for both their current housing and the new loan.Total debt-to-income ratios cannot exceed 45% and that must include all the new costs. Finally, the parents must demonstrate that they do not have the income to qualify for the loan on their own. It’s important to understand that bad credit is not sufficient to use this loan program, it must be a lack of income that disqualifies them. This program can also be used to help an adult child with disabilities. As more people choose to live independently in retirement, the need for housing will continue. By taking advantage of a Family Opportunity Mortgage qualified borrowers can purchase a home for their parents at very favorable owner-occupied rates and terms. Make sure to talk to a licensed mortgage lender to learn more.

LIKE

This magazine is issued monthly and all you need to do is join our email list (or send us a friend’s name and we will send them a free subscription of YRL Real Estate Talk-email us at FreeMagazine@YourRealtyLink.com & ask to be added to our email list. We can also be found on FB at http://www.Facebook.com/YourRealtyLink

AlwaysseeaYourRealtyLinkagentbeforeyouvisit anynewhomecommunityandletussignupwiththe builderasyouragent. Buildershaverepsinthe communitiestoletyou(withorwithoutus)intoview thenewhomesbuttherepresentativeworksforthe builder–whileweworkforyou! Thebuilderpaysus notyouandneedstheREALTORcommunitytohelp markettheirhomes. Youwillabsolutelyappreciate ourexperiencedagentwhileyouaredealingwiththe differentstagesofthebuild,choosingthelotandmodel andchoosingtheupgrades. Ourexperiencematters. Wewillalsomeetwithyouandthebuilderforfinal walk-throughsandhelpdiscussyourfinancing.

Likebuyinganyhome,youneedtohaveagoodideaofthe amountofnewhomeyoucanaffordsoitisalwaysagood ideatogetpreapprovedwhetheryouarethinkingabouta newbuildoranexistinghome. Onceyoufindthenew homecommunitythatyoulike,thebuildermayofferbetter incentivesifyouusetheirfinancing-butthatispartofour jobasyourREALTORtohelpyoudecidewhereto finance.

Youcansearchonmostwebsitesfornewconstruction homesthatarefinanistedandonthelocalMLSasactive andyourYRLagentcanassistinhelpingyoulocatethe homesbybuildersthatarecurrentlyunderconstructionasa spechome.

Thebasepriceisthebuilders‘starting’priceonanyhome andtherewillbeonemeetingwhereyouwilldecidewhat upgradesyouwantinthehome,squarefootageandstyle.

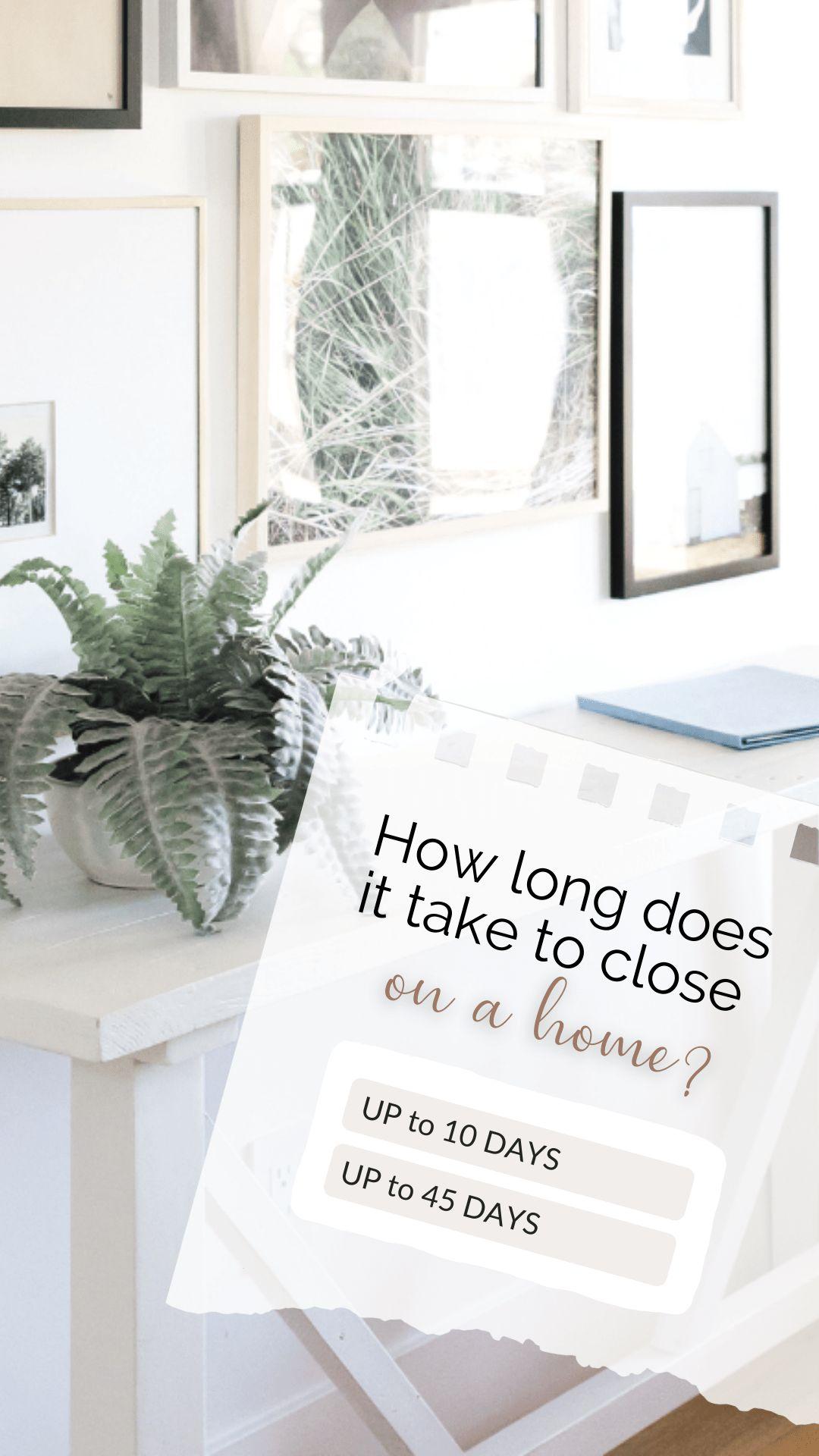

Buying a new home is exciting and confusing. There are a lot of steps to buying a home but using an experienced real estate agent will make the process less overwhelming! These are the most common questions home buyers have, and the answers.

1. How do I get started? –The first step is to speak with a lender and get a pre-approval. This will tell you, and potential sellers, how much you can afford.

2. How long does it take to close on a home? –Typically, it takes about 30-45 days once contracts are signed to complete the lending, appraisal, and inspection processes.

3. What does my agent do? –Abuyer’s agent will negotiate terms and manage the closing process from start to finish.

4. How much do I pay for a buyer’s agent? –Nothing.The seller’s agent gives the buyer’s agent a portion of their commission from the seller.

5. What credit score do I need to qualify? –A 620 FICO score or higher is required for most home loan programs.Talk to a lender for other options for lower scores.

6. How much money do I need for a down payment? - It varies. FHAloans start as low as 3.5% and most lenders offer standard programs for as little as 5% down. YourYRL Agent will have preferred lenders with great programs to offer you under any situation.

7. What other fees will I need to pay? –Closing costs and loan origination fees will add another 2-4% to the costs.YourAgent may also ask the Seller to pay some of these costs for you.

8. What if I change my mind? –Your agent will work with you to build in contingencies for condition, loan terms/approval, and other protections to allow you time to evaluate the home during escrow.

9. When do I get the keys? – Unless you’ve negotiated extra time for the sellers to move, you’ll get the keys at the closing.

10. What’s the best advice for home buyers? –Trust the experts and ask lots of questions. Buying a new home is exciting. Reduce any anxiety by finding a good buyer’s agent who can help guide you through the process.

Any item at the time of settlement will be determined by the PurchaseAgreement although these fees are the normal charges to either the buyer or seller

APPRAISAL- Lender orders the appraisal and buyer pays for the appraisal usually at loan application. Lender should order appraisal immediately and not wait until after inspection is completed. Buyer will receive results of appraisal not the Seller.

“FHAor VA”Amendatory Clause is provided by lender and signed by all parties stating to all parties that the appraisal must equal or be better than the sales price or the buyer is not required to purchase the home. (Seller can always lower the sales price to meet the appraisal price to close or buyer may pay difference.

Home Inspection…Buyer should order the home inspection and will be required to pay at the time of placing the order. Buyer should attend the inspection if at all possible. Buyer’s agent should make sure inspection is performed in the time limits as per purchase agreement and any response also must be made in a timely manner in writing. Utilities must be ON for inspection.

Home Warranty - ordered usually by buyer’s agent and paid at closing by the terms of the purchase agreement.

Homeowners insurance policy - Buyer needs to order early in the homebuying process. Payment may be ahead of closing or paid at closing. Lender will need prior to final loan approval.

Mobile closers, if requested, are provided by the title company and usually do not cost either buyer or seller extra.

Titlework-orderedbytheagentasperthe purchaseagreement. Normallytheowners policyispaidatclosingbytheSellerandthe mortgagepolicyispaidatclosingbythe buyer. Asalways,thepurchaseagreement maybewrittendifferently.

Mortgage payoff (current mortgage of seller) must be ordered by the title company. Payment for payoff may be reflected on settlement statement if there is a cost. Seller will need to complete a form to order the payoff but cannot order on behalf of the title company.

Deed…ordered by the title company from their attorney and paid at closing by the seller.

HOAmonthly fees and transfer fee…title company will need HOAinfo so they can verify fees are current and fees are usually prorated to day of closing. If HOAcharges a transfer fee (fee to change ownership info and bill new owner) is oftentimes split but depends on what the HOAdictates in its By-laws.

Down payment and fees by buyer - if the amount owed at closing by buyer is under $10,000 then a cashier’s or certified check may be provided. If more than $10,000 the funds must be wired. Receive WIRING INSTRUCTIONS from the title company only in a secure manner. Mortgage fraud is not a joke!

1. Thoushaltnotchangejobs, becomeself-employedorquityour job.

2. Thoushaltnotbuyorleaseacar, truckorvan(oryoumaybeliving init)!

3. Thoushaltnotusechargecards excessivelyorletyouraccounts fallbehind.

4. Thoushaltnotspendmoneyyou havesetasideforclosing.

5. Thoushaltnotomitdebtsor liabilitiesfromyourloan application.

6. Thoushaltnotbuyfurniture.

7. Thoushaltnotoriginateany inquiriesintoyourcredit.

8. Thoushaltnotmakelargedeposits withoutfirstcheckingwithyour loanofficer.

9. Thoushaltnotchangebank accounts.

10. Thoushaltnotco-signaloanfor anyone.

Answer: Up to 45 day (usually 30)s

WhatisYRLIndy.tv? Itis‘our’streaming channelonRokuandotherstreaming servicesunderthenameAbagaleTV. BusinessesinIndycanadvertisetheirvideo foraslowas$1perminute! Interested?Send usanemailtoYRLIndyTV@gmail.comand wewillsendyoumoreinfo.

Turn on any popular home network onTV and you’ll find a program on the benefits of staging even though the home may have just been completely rehabbed and everything is new. Rearrange your furniture, pick a soothing color palette, clear out the family photos & your home will sell faster & for more money. Sound too frou-frou to be true? It’s not!The soft and decorative side of staging is backed by hard facts. Ask any experienced REALTOR!

Need a little help in making your home show better? List with aYour Realty Link agent and we will give you valuable tips on the best ways to make your home more sellable!

Did you know:

● Abuyer searching online is attracted to beautifully staged homes.

● Both a buyer and an agent are excited when their first impression is good and they want to see more when they walk through the front door.

● Agents talk to other agents who are also directing their buyers to the best homes on the market. An attractive listing will be shown more often, meaning more market exposure–critical for a quick and profitable house sale.

Staging is non-negotiable in many parts of the country. Staging a listing for sale attracts buyers. Don’t confuse staging with your own personal style of decorating. Staging’s first task is decluttering and depersonalizing. Your YRLagent will give you some handy tips to make your home feel more inviting to buyers.

Like everything in real estate, price range does play a part in how much staging to actually do to prepare for buyers.

If you are still occupying the home while it is being shown clearing out as much as possible makes the home seem larger. It can be difficult with children and pets but important to listen to your agent’s advice.

In higher end properties where the homeowner has vacated, you may find that staging sells the home faster and makes the home feel warmer. Staging an entire home could cost up to $3000 and we can always direct you to those stagers that give that full service, but if you just need suggestions of what to clear out to make your home feel more open by moving some of your furniture around to make your home more cozy…that is free with several of our experienced, accredited agents. Even a new picture over the fireplace and new towels and rug in a bathroom can make a huge difference. Stage and/or declutter before taking any pictures!

Rising interest rates can be a major concern if you’re shopping for a new home.Ahigher rate reduces your buying power and increases the home cost thousands of dollars over the course of the loan. One option to avoid this is to “buy down” your loan rate.This allows you to purchase your home at a more attractive rate.Arate buydown is when you pay an upfront fee in exchange for a lower interest rate.This increases your closing costs and for every 1% of the purchase price you pay in points, your mortgage interest rate is reduced. Buying a lower interest rate may be a good strategy for a home you intend to keep for a long time, thus making up the difference over the life of the loan.There are a couple of options for a rate buydown.

The first is a simple payment of increased closing costs up front in exchange for a lower interest rate.The buydown lasts for as long as you have the loan and is requested by the buyer.The second is a temporary buydown often initiated by a homebuilder or lender to incentivize a purchase. In this case, the buydown is for a set period, two or three years, and then the rate will return to the higher rate if the borrower does not refinance. This strategy is a good one for a starter home or if one believes the interest rates will be lower in a few years. Utilizing a buydown as part of your loan origination can be a smart way to save money and maximize your purchasing power. It’s important to recognize the breakeven point, however, so that you know when you have started gaining money on the plan.

Although yourYRLagent is not a mortgage expert, he or she will have an opinion on whether this is practical or not for you based on the current interest rates. Your agent will also recommend a lender that will be able to show you the different costs using different financing plans when thinking about closing costs and buying the rate down.

Earnestmoneyisadepositonthehome purchase.Itmeans‘sinceritymoney’andapplies towardtheamountdueattheclosingtableonce thedownpaymentandclosingcostsare determinedforthebuyer.Theamountofearnest moneyistypicallyaround1%ofthepurchase priceandispaidimmediatelywhentheofferona homeisaccepted.Theamountofearnestmoney iswrittenintothepurchaseagreementbythe buyer’sagentanddeliveredtothelisting brokerage(orinmanycasesthetitlecompany) typicallywithintwodaysoftheacceptanceofan offer. Oncethelistingbrokerageortitle companyreceivestheearnestmoney,thecheckis depositedinaproperescrowaccountwherethe moneyishelduntiltheclosingoruntilthesale hasbeenterminated.

Thereturnoftheearnestmoneytothebuyermay beinjeopardyshouldthebuyernotcloseonthe homeforavalidreason. WhenaMutualRelease onthesaleisfiled,itmustbesignedbyall partiesbeforethemoneycanbereturnedtoeither thebuyerortheseller.TheStateofIndianadoes haveseverallegalwaysofreleasingtheearnest moneyshouldtherebeaterminationofthe purchaseandthereisnomutualagreementon whogetsthemoney. Therearealsoverystrict rulesforabrokeragetofollowinholdingthe earnestmoney.

Selling a Home is Obviously SellingYour Biggest Investment. It takes more than a sign in the yard or a social media presence...it takes 'experience' in negotiating.

Our Sellers know that we are working for them! We don’t believe in putting a buyer into any home that they cannot afford or wasting marketing time for a Seller by listing a home too high or accepting the first offer without all of the information about the buyer at hand. We will give you an honest opinion based on our knowledge of the real estate industry (and the current market at hand) even if it is not what you want to hear.

Our marketing includes what other brokerages offer such as listing on the BLC and social media sites such asTrulia, Realtor.com, Zillow, Homesnap & more, professional pictures & marketing to other agents directly.YRLhas its own Indianapolis streaming channel and a monthly digital magazine. Our listings are promoted on all of the social media outlets and we use digital technology which allows us to always stay on top of every deal no matter where we are and all we need is an email address for each of our buyers or sellers and you can enjoy being out of town and sign any document right from their cell phone!

We have all the latest technology to sell your home with ease but we also have a brick and mortar location on Southport Rd where we meet our clients if they like knowing where their brokerage operates. We also have a convenience location in Irvington.

Our agents are all members of NAR, IAR and MIBOR and are active in their own communities.

What do I pay when selling my home withYRL?

Commission. Our listing agreement states our selling commission.This fee pays us to market and sell your home and also compensates the buyers’agent at closing.ALLcommissions are negotiable and will be discussed in our listing meeting. Our commission is usually 5%-6% depending on the circumstances of sale. “Buyers” usually do not pay any part of the real estate commission so when we quote you our percentage to sell that is the total commission for us and the buyers agent. We do not charge extra for a transaction fee as many brokerages have this added expense.

Title fees - as the seller you will be charged for what is referred to as the Owner’s Policy by the title company. The title policy covers the search and assures the buyer that he/she is purchasing your home free and clear of any encumbrances.

Deed - there are several types of deeds in Indiana but a Warranty Deed is the most common deed at the closing table. It is less than $100 and is prepared after the attorney for the title company has the title work which provides proper names and legal descriptions.

Pro-rated taxes - In Indiana the property taxes are paid one year in arrears and pro-rated to the date of closing. If you pay your taxes in your escrow account you will receive any left-over balance from your escrow company about three weeks after closing.

Mortgage payoff - your mortgage balance must be paid off at the time you close on your new home unless your lender qualifies you for two mortgages.

Closing costs for buyer, home warranty, inspections, daily possession fees after closing, and other negotiated items may be asked by the agent for the buyer when the purchase agreement is written.

Theseareafewofthetitlecompaniesthatouragents prefer-AstheselleryouwillpayfortheOwner’s PolicyandtheBuyerisusuallyresponsibleforwhat iscalledtheMortgagePolicy. Anyrecorded judgmentwillappearinthetitleworkandmayneed tohavethepaymentnegotiatedtoclose.

TitleAllianceofIndyMetro

48NEmersonAve#200 Greenwood,IN46143 (317)884-9327

indy@TAofindymetro.com

QualityTitleInsurance

750ESouthportRd

Indianapolis,IN46227 (317)780-5700

RoyalTitleServices 365ThompsonRd Indianapolis,IN46227

title@royaltitle.com (317)791-6000

ChicagoTitleInsuranceIndiana North:6925E96thStSte100-Indianapolis (317)570-8607

South:1642WSmithValleyRd-Greenwood (317)888-9797

Yourpurchaseagreementdetermineswho(whichREALTOR/Agent)ordersthetitlework.

GetPreapprovedWithOneofOurFavorite&Most TrustedLendersbeforeyouvisithomessoyouareaware ofwhatyoucanaffordandwhenyoufindtheperfect houseouroffercanincludeyourpreapprovalletter!

JoeRangel

CrownMarkMortgageGroup 8980TechnologyDr. Fishers,IN46038 (317)594-9800

www.CrownMarkMortgage.com

joe@crownmarkgroup.com

JodiBleier,MortgageConsultant

Bailey&WoodsFinancialGroup 616NMadisonAve

Greenwood,IN46142 (317)213-1387

jbleier@bawfg.com

SherrySullivan

FirstCommunityMortgage (317)522-8301

sherry.sullivan@fcmhomeloans.com

JeffCotton TCUMortgage 445SPostRd(butalsotravelstoyou)

Indianapolis,IN46219

Office:(317)572-2628

Cell:(317)557-1608

Email:jcotton@tcunet.com

Youmustorderaninspectionwithinthetimestatedin yourpurchaseagreement. Thebuyerisresponsiblefor ordering.Youwillneedtopayatthetimeofordering. Inspectionstake2-3hours.Itispreferablethatthebuyer attendstheinspection. YourYRLagentwillmakea timelyresponsetotheinspectiontothelistingbroker. YouandyourYRLagentwillreceiveacopyofthe writtenreport.

HousemasterHeartlandHomeInspections (317)209-9100

Heartland.HouseMaster.com

CornerstoneInspectionServices

443N.RangelineRd. Carmel,IN46032 (317)815-9497

PillartoPostHomeInspections

TheJonCarrothersTeam (317)550-4044

USInspect (317)225-4651

WatchDogHomeInspections (317)446-9711

Brenda Dean has been in real estate since 2013 and is one of our top producers. Brenda is married to Jeff who grew up in the Southport area and has four grown children now—’all’Purdue grads. She has 3 grandchildren yet she finds the time to always be available to help other agents in the office when they need assistance of any kind. Brenda’s buyers and sellers will tout her experience and care is never-ending.

Cell: 317.403.2780

Brenda@BrendaDeanTeam.com

Janet has been a REALTOR since 1974 and for most of that time has been an independent. She did work for several large franchises for about 10 years but likes the mentoring and management of owning her own company.

Janet is past president of the Independent Real Estate BrokersAssociation in Indiana and also has an Ohio license since 2001.

I prefer texting: (317) 997-7404

Janet Giles-Schultz (Broker-Owner)

Brenda Dean (Manager)

Janet Giles-Schultz (Broker-Owner)

Brenda Dean (Manager)

Wehandlebothresidentialandcommercialsales. Allofouragents areexperiencedandwillmakesureyourrealestateneedsaremet!

Brenda Dean has been in real estate since 2013 and is one of our top producers. Brenda is married to Jeff who grew up in the Southport area and has four grown children now—’all’Purdue grads. She has 3 grandchildren yet she finds the time to always be available to help other agents in the office when they need assistance of any kind. Brenda’s buyers and sellers will tout her experience and care is never-ending.

Cell: 317.403.2780

Brenda@BrendaDeanTeam.com

Janet has been a REALTOR since 1974 and for most of that time has been an independent. She did work for several large franchises for about 10 years but likes the mentoring and management of owning her own company.

Janet is past president of the Independent Real Estate BrokersAssociation in Indiana and also has an Ohio license since 2001.

I prefer texting: (317) 997-7404

Janet Giles-Schultz (Broker-Owner)

Brenda Dean (Manager)