Member Recognition Banquet & Annual Business Meeting

Friday, May 8, 2026

Brookfield Conference Center

Conveniently attend WICPA conferences from anywhere with an internet connection!

wicpa.org/Livestream wicpa.org/OnDemand

Features Columns

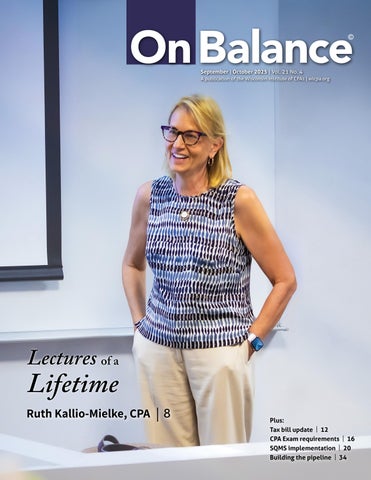

8 Lectures of a lifetime

Ruth Kallio-Mielke, CPA, teaches where she once was a student — and sees a world of opportunities for aspiring accountants.

By Brent Roberts

12 One Big Beautiful Bill enacted

On July 4, President Trump signed into law the One Big Beautiful Bill Act, which includes both individual and business provisions CPAs need to know about.

By James D. Brandenburg, CPA, MST

16 New pathways for CPA licensure

The WICPA is actively working to help current and future accountants level up for a fulfilling and meaningful career.

By Joseph W. Boucher, CPA, JD and Julijana Englander, JD

20 Moving beyond risk assessment in the SQMS implementation journey

Ensure your firm’s new quality management system is both well designed and well executed in time for AICPA’s looming professional standards deadline.

By Heather Lindquist, CPA

26 EMPLOYEE BENEFITS

Supreme Court decision impacts retirement plan sponsors

The court’s impactful ruling is a direct call to review your plan’s oversight process and the quality of your advisory services.

By Joseph Topp,

CPA

28 NONPROFIT ORGANIZATIONS

Navigating challenges facing nonprofits

Grassroots organizations can support and sustain their mission impact and meet the needs of their communities by using best practices.

By Melodi Bunting,

CPA, CMA, CGMA, MBA

The power of networking: Building connections to accelerate your career

The relationships you build today could very well shape your career tomorrow.

By

Victoria Thayer, CPA, MSA

Helping build the CPA pipeline

The WICPA Educational Foundation plays a pivotal role in improving awareness and changing perceptions—and CPA involvement is key to its success.

• Providing strategic governance in accordance with the WICPA strategic plan, mission and vision

• Acquiring new leadership and training skills

To apply, visit wicpa.org/BoardApplication through Nov. 14, 2025.

Questions? Contact tammy@wicpa.org.

Introducing your 2025–2026

WICPA Educational Foundation Board of Directors

The WICPA Educational Foundation Board of Directors provides strategic governance in accordance with the Foundation’s mission to play a pivotal role in supporting programs to improve awareness and perceptions by educating Wisconsin students and educators about the exciting opportunities available in the accounting profession. New members began serving in May 2025.

Jeff Dewane, CPA, CGMA, CMA, MBA, Controller, Vinton Construction Co.

KPMG LLP

DIRECTOR

Gina Skibo, CPA, Partner, Wipfli LLP

SECRETARY/TREASURER

Jon Gaines, CPA, CGMA, MBA, Vice President–Business Services & Finance, Wisconsin Women’s Business Initiative Corp.

Lee Liermann, CPA, Instructor, School of Business and Entrepreneurship, Nicolet College

Teacher & Department Chair, Port Washington High School

Christopher Cholka, CPA, CGMA, Controller, Cousins Subs Principal,

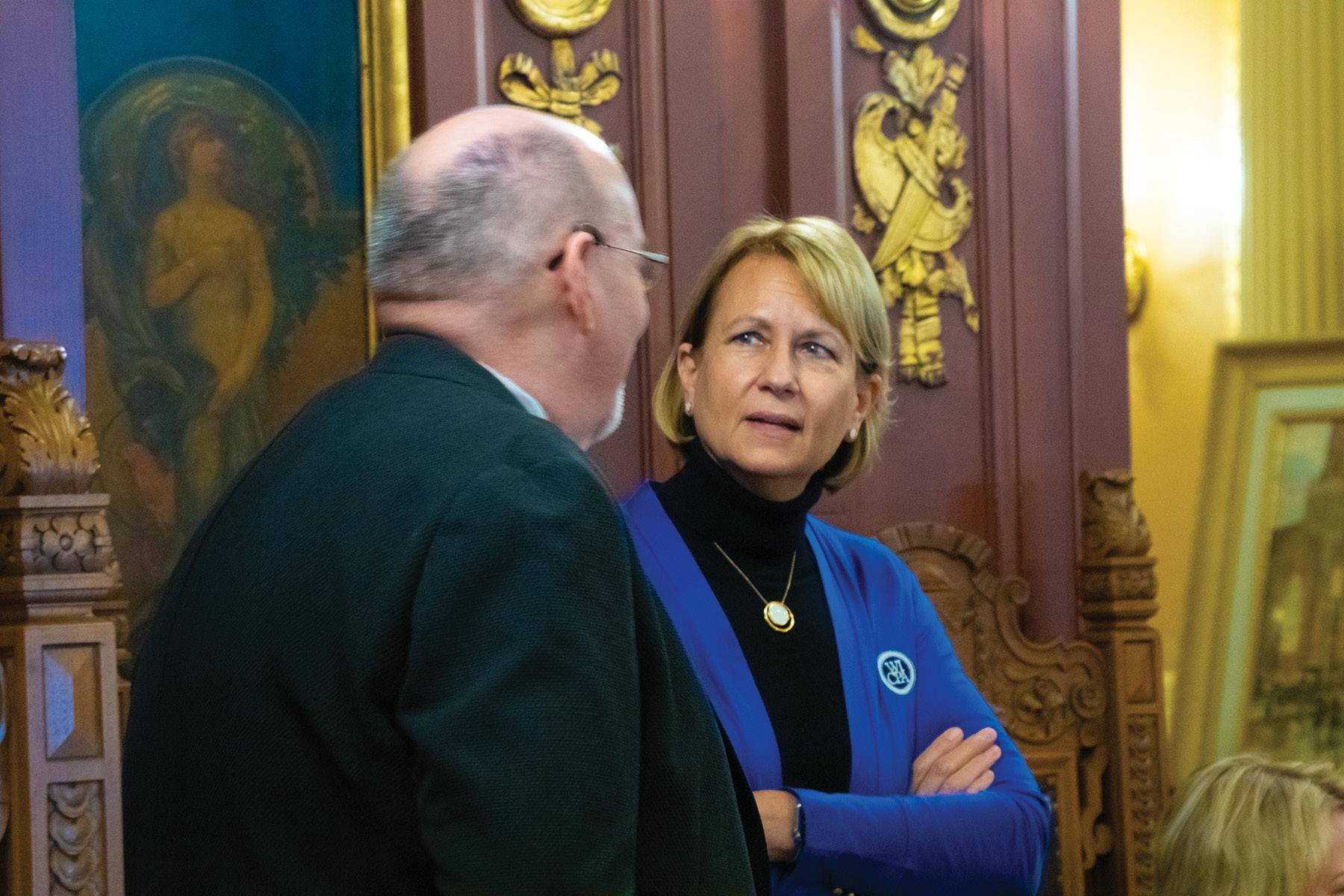

“When people hear from us as accountants, CPAs and constituents, the impact of our advocacy work can be felt across the state.”

Advocating for the Profession in Washington, D.C.

By Stacy A. Stinson, CPA, MBA

When I accepted the nomination to serve as chair of the WICPA board of directors, I concluded my acceptance speech with a focus on four words: intentional, visible, vocal and proud. These words were part of a call to action for us to become ambassadors for the WICPA and support the future of the accounting profession.

As I began my term, I had the opportunity to put those four words into action in Washington during the AICPA Spring Council Meeting that included visits to Capitol Hill by state society members. As a “newbie” to Capitol Hill, the experience was both exhausting (from walking the halls) and energizing, as it allowed me to share the accounting perspective on policy issues. It reminded me that when we show up — prepared, passionate and united — we can make a real impact.

Being intentional

Our bipartisan engagement in Washington was purposeful. Each meeting, conversation and handshake was part of a broader strategy to advocate for the issues that matter to our profession and to those we serve.

We were prepared with specific topics and clear talking points. From federal tax policy to education-related reforms, we ensured our priorities were communicated effectively. Every detail — from the selection of the representatives we met with to the content of our messages — was chosen with intention.

Being visible

The AICPA Spring Council Meeting brings together state society CEOs and state society board leadership from around the country, all of whom are deployed to the halls of Congress to engage with lawmakers from both parties.

The WICPA leadership, along with WICPA CEO Tammy Hofstede, met with legislative and legal staff from the offices of Sens. Tammy Baldwin and Ron Johnson and Reps. Scott Fitzgerald, Glenn Grothman, Gwen Moore, Mark Pocan,

Bryan Steil, Thomas Tiffany, Derrick Van Orden and Tony Wied. We weren’t just visitors — we were representatives of a profession that is vital to the health of our economy and communities in the state of Wisconsin. Our collective presence on Capitol Hill was a powerful reminder that CPAs are not only financial experts but also civic leaders.

Being vocal

We used our voices confidently and constructively to advocate for selected policies that will shape the future of accounting. We shared our insights on the employment outlook; the evolving nature of the profession; and the growing intersection between accounting, technology and education. Perhaps most importantly, we communicated the human impact of what we do: how CPAs help families and businesses of all sizes navigate uncertainty. We also listened to concerns raised by our legislative staff and elected officials regarding changes to the IRS, and we discussed how those changes have impacted or may impact CPAs and our clients,

From left: Allyson Hofstede, CPA; Wendi Unger, CPA; Ryan Hanson, CPA, CGMA; Neil Keller, CPA; Tammy Hofstede; Stacy Stinson, CPA, MBA.

who are their constituents. We continue to offer our support in areas relevant to the profession in the state of Wisconsin.

Here is an overview of the critical issues we advocated for on Capitol Hill:

1. Recognizing accounting as a STEM discipline: The Accounting STEM Pursuit Act (Senate reintroduction) seeks to formally include accounting within STEM education programs. This would open federal grant funding to support K–12 accounting awareness and education and position our field as a dynamic, tech-driven profession. It is a chance to attract diverse, highperforming students into the pipeline.

2. Improving disaster tax relief: The Federal Disaster Tax Relief Act aims to simplify and expand tax relief for victims of natural disasters. Key provisions include removing the 10% AGI threshold for casualty loss deductions and allowing claims without itemization — making relief faster and more accessible when it is needed most.

3. Expanding 529 Plan flexibility: The Freedom to Invest in Tomorrow’s Workforce Act would allow 529 Plan savings to cover professional credentialing costs, including CPA certification. This promotes lifelong learning and helps professionals continue to advance their skills in a changing economy.

4. Protecting the pass-through entity tax deduction: The accounting profession and other service industries are advocating for the preservation of the ability of pass-

through entities (such as partnerships and S corporations) to deduct state and local taxes at the federal level — essential support for the many small businesses that are the backbone of our economy.

Being proud

As we concluded our day, we looked back over our busy schedule and said, “Job well done.” We utilized our time effectively and efficiently to represent the organization. We left our legislators with a deeper understanding of our advocacy positions, the WICPA mission and the value of our CPA membership as a resource for them as they tackle financial issues in government.

Advocacy is something everyone can participate in. You can support the WICPA’s efforts right from your home or office. A letter, an email or even a phone call to your state or federal representative to express your support or concerns can make a difference. You can contact your local school or school board to talk about the importance of accounting education or policy. You can also join a WICPA committee, such as the Wisconsin Taxation, Federal Taxation or Public Policy committees. When people hear from us as accountants, CPAs and constituents, the impact of our advocacy work can be felt across the state.

Let’s be intentional, visible, vocal, and — above all — let’s be proud of who we are and what we do as CPAs.

Stacy A. Stinson, CPA, MBA, is assistant professor of accounting at Concordia University and the 2025–2026 WICPA board of directors chair. Contact her at 262-243-2099 or stacy.stinson@cuw.edu.

Bank-A-Count

Check out our featured member benefit providers

CPACharge

Bank-A-Count Corp. is a leading national printer of business checks located in central Wisconsin with an unwavering focus on low prices and exceptional customer service. We offer a variety of complementary items, including deposit products, pre-inked stamps, and custom print and mailing services.

CPACharge is trusted by accounting industry professionals nationwide and provides a simple and secure online payment solution developed specifically for CPAs, offering an affordable way to accept credit, debit and eCheck payments in the office or online, with no equipment or swipe required.

Waukesha State Bank

Established in 1944, Waukesha State Bank is one of the largest locally owned and independent community banks in Wisconsin, with full-service offices in Brookfield, Delafield, Menomonee Falls, Mukwonago, Muskego, New Berlin, Oconomowoc, Pewaukee, Sussex and Waukesha. For more information, visit www.waukeshabank.com. Member FDIC.

“The

WICPA offers membership categories that provide valuable resources, exclusive events, continuing education and a strong community of peers who understand your journey.”

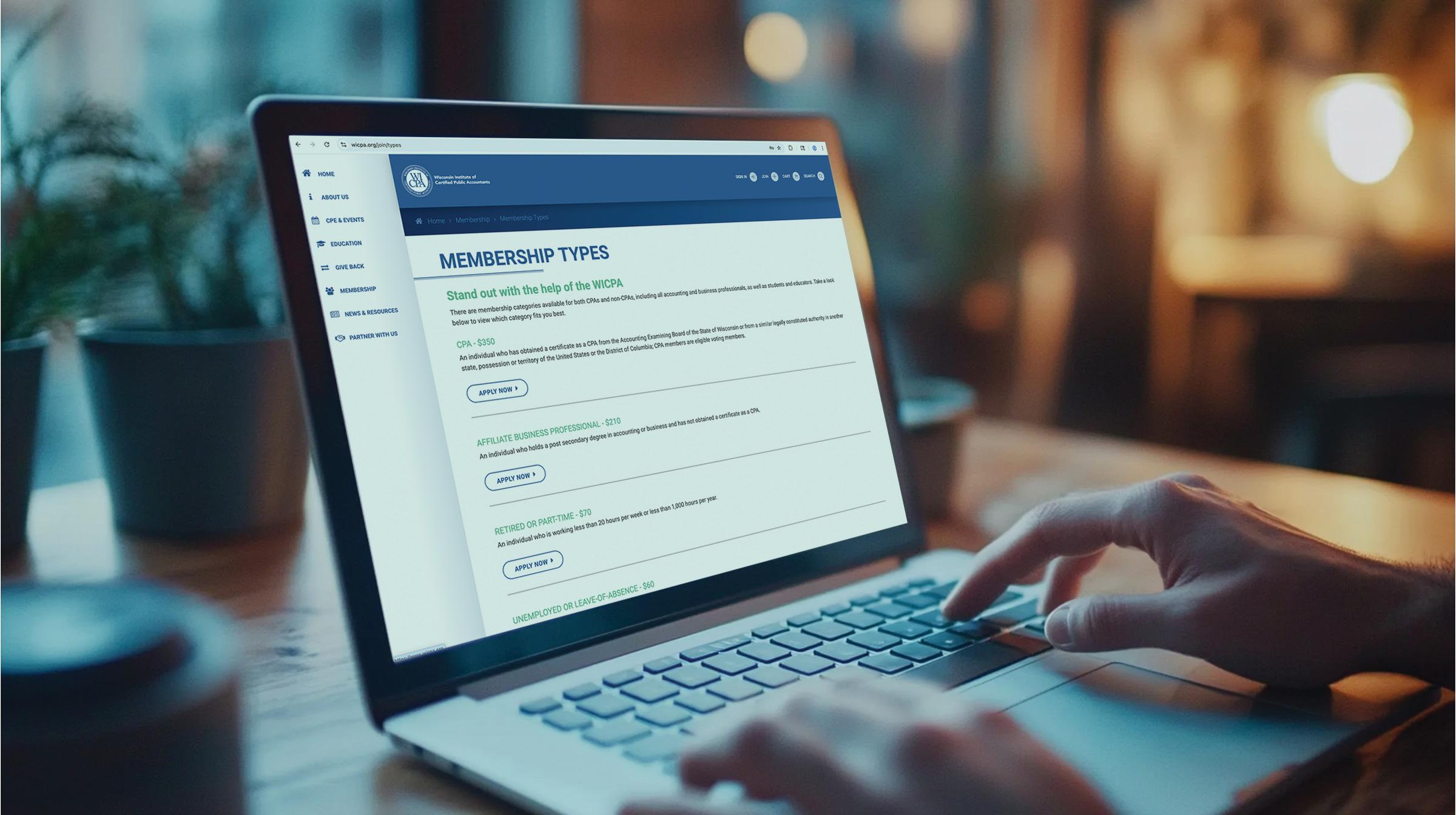

WICPA Membership Categories

Ifrequently receive questions, even from current members and firms, about our membership categories for themselves or their staff. And just as often, they are amazed to hear that we have membership categories from high school student to retiree.

Firms, companies and organizations are also surprised to hear that we have a category for professionals on staff who are not CPAs, as we know they can find just as much value in WICPA membership. Employers find WICPA membership is a valuable benefit for all their accounting and business staff. They bring more value to the company, as they can join committees to expand their expertise and create networks they would not have otherwise, are provided with valuable resources, and receive discounts on CPE to stay updated on current topics and issues in the profession and their positions.

There are membership categories available for both CPAs and non-CPAs, including all accounting and business

professionals, as well as students and educators. Categories are as follows:

CPA — An individual who has obtained a certificate as a CPA from the Accounting Examining Board of the State of Wisconsin or from a similar legally constituted authority in another state, possession or territory of the United States or the District of Columbia (CPA members are eligible voting members.)

Affiliate Business Professional — An individual who holds a post-secondary degree in accounting or business and has not obtained a certificate as a CPA

Retired or Part-time — An individual who is working fewer than 20 hours per week or 1,000 hours per year

Unemployed or Leave-of-absence — An individual who is currently unemployed but is actively seeking work or is on a leave of absence

High School Educator — An individual who is a full-time accounting or business high school educator or guidance counselor; has demonstrated an interest in furthering the study of accounting, finance or commerce; and has not obtained a certificate as a CPA

College Student — An individual who is a student attending college pursuing an associate, undergraduate or graduate degree or coursework to qualify to sit for the CPA Exam and does not currently have a degree

High School Student — An individual who is a student attending high school enrolled in accounting or business courses

Whether you’re a company supporting and engaging your staff, a student exploring accounting, a young professional building your career, a seasoned professional expanding your network or a retired member staying connected to the profession — you belong here. The WICPA offers membership categories that provide valuable resources, exclusive events, continuing education and a strong community of peers who understand your journey.

Tammy J. Hofstede is president & CEO of the WICPA. Contact her at 262-785-0445 ext. 4518 or tammy@wicpa.org.

Visit wicpa.org/CPEcatalog and search “Free to Members” under the Online CPE tab.

The Finance Committee of the WICPA Board has reviewed and approved the WICPA audited financial statements for the fiscal year ended April 30, 2025.

The WICPA Educational Foundation Board has reviewed and approved the audited WICPA Educational Foundation financial statements for the fiscal year ended April 30, 2025. Members may request a copy of the audited financial statements by contacting WICPA president & CEO Tammy Hofstede at 262-785-0445 ext. 4518 or tammy@wicpa.org.

Lectures Lifetime of a

Photography by John Sibilski

Ruth Kallio-Mielke, CPA, teaches where she once was a student — and sees a world of opportunities for aspiring accountants.

By

Brent Roberts

As college students settle into the fall semester, for Ruth Kallio-Mielke, CPA, it’s an opportunity to enjoy a key part of her life that has come full circle. After 40 years in public accounting, she is now an accounting lecturer at the University of Wisconsin–Milwaukee (UWM) Lubar College of Business — a faculty lecturer in the Executive MBA and Master of Professional Accounting programs, presently teaching financial statement analysis, current topics in accounting, cost accounting, accounting for governmental/nonprofit, and consolidations. While Kallio-Mielke’s role now puts her in front of the class, she previously earned her bachelor’s degree in accounting and master’s in taxation from UWM. When she ponders returning to the school as an educator, Kallio-Mielke describes the feeling as “very familiar and very different at the same time. Students are so much more sophisticated, knowledgeable and tech savvy than I was at their stage of life.”

One of the ways that Kallio-Mielke can impart valuable knowledge and insights to her students is by incorporating lessons learned from her decades in the accounting profession. Prior to joining the educator ranks, she most recently served as managing director at Deloitte Tax LLP in the Milwaukee office, retiring in January 2023 after leading the tax practice for seven years. Before spending 20 years at Deloitte, she worked with the tax practices at Arthur Andersen and Ernst & Young. Along with teaching, she currently consults with Continuus Technologies.

“Every role broadened my understanding of business in so many different ways. Students today can ask me any business question. I may not have all the answers, but I will have thoughtful insights on their issues, given my broad background.”

From office to classroom

So, what is it like going back into the classroom after decades in a professional setting?

According to Kallio-Mielke, “It’s so crazy different. I had no idea what I was signing up for. I presumed I was ready for anything after 40 years in public accounting, and I was dead wrong. I loved that they gave me the chance, but I’ve now got

“ The main reason I wanted to teach is that through the WICPA, I’ve been exposed to the statistics about people not going into the accounting profession, and I think people underestimate where you can go with an accounting degree.

my sea legs, and I feel so much better about what I’m doing than what I naïvely stumbled into when I started in January.”

She notes the special feeling it brings when she looks at her students and knows they’re understanding what she’s teaching.

“It’s amazing, and I think they’re amazing, too. That’s one of the things that’s so different from when I was in school. I was a complete wallflower who sat in class, didn’t participate, didn’t talk — I just tried to study as much as I could, and if I couldn’t solve a problem, I would sit there and spin my wheels and think ‘I can do this. I’ll just go through the books, and I’m not going to just show up in my professor’s office and ask questions.’ Students today are totally different and very assertive. They’re unapologetically expecting a high-quality education, which they deserve. But it’s amazing — some of my best students came to me and said they loved my class and were going to sign up for my next class the following semester. That is the highest compliment I think I could ever receive.”

Deciding to make a significant career transition requires much thought and a broader purpose.

“The main reason I wanted to teach is that through the WICPA, I’ve been exposed to the statistics about people not going into the accounting profession, and I think people underestimate where you can go with an accounting degree.

They think you’re a classic bean counter — that you’re sitting at a desk all day long and it’s going to be boring, but it’s far from that. It’s the kind of career in which you can own your success.”

Inspiration all around

Of course, a successful professional who guides the next generation of accountants has also enjoyed the positive influence of others along the way.

Reflecting on her 40-year accounting journey, Kallio-Mielke credits the major influences in her career — and life — with helping her achieve what might not otherwise have been possible. She has special gratitude for her husband, Steve Mielke, whom she met in the accounting program at UWM and who “believed in me more than I believed in myself.” She also expresses appreciation for her children, Sarah Crain and Jack Mielke, “for putting up with a mom who was as committed to her career as she was to being the best mom possible to them.”

While Kallio-Mielke takes great pride in inspiring her students, she has just as much appreciation for her peers, who have inspired and guided her on the path to success.

“I like to call them ‘my board of directors.’ One-on-one over the years, they have taught me so many different things, and I’ve been able to emulate them in different ways. The thing about public accounting is you get exposed to many different leaders. If you work in industry, you may have one or two bosses that you interact with every day, but in public accounting, you have 10 bosses — and everybody is competing for your time, whether it’s your client or your partner. You’re working with so many people that you really get exposed to highperforming leaders who are like mini entrepreneurs running their own businesses.”

Collaboration over competition

Outside the office and classroom, Kallio-Mielke has served in several leadership capacities for the WICPA, including on the board of directors (director and AICPA Council) as well as on numerous committees such as Ethics, Finance, High School Educator, Legislative Review and Wisconsin Taxation.

“Being involved with the WICPA made me realize that I’m not competing against my peers in public accounting. It started on the Wisconsin Taxation Committee, which comprised all these people who are multistate tax professionals, and we would work on Wisconsin state tax issues together. Those are my friends who work in other accounting firms, and I learned so much from them.”

While Kallio-Mielke’s work with the WICPA is extensive, her nonprofit service also extends to other local organizations, including After Breast Cancer Diagnosis,

“

Being involved with the WICPA made me realize that I’m not competing against my peers in public accounting.

Kallio-Mielke volunteered as part of a panel during the 2023 High School Educator Accounting Symposium.

The accounting educator has been involved in many legislative activities throughout her years volunteering with the WICPA.

Photo provided by the WICPA

Photo provided by the WICPA

Friends of L’Arche Milwaukee, Meta House, Milwaukee Habitat for Humanity and St. Matthew’s Lutheran Church Council.

A rewarding career in public accounting, now impacting future accountants as an educator, and serving others in the community all might make one wonder what else Kallio-Mielke could possibly fit into her life. It turns out she’s got plenty of moves.

Dancing dreams

Kallio-Mielke and her husband were awarded third place standing in the Fred Astaire Dance Studios 2024 Top 5 Amateur Couples (Wisconsin) competition, never imagining that ballroom dancing would become an award-winning endeavor.

“My daughter was a dancer, and I spent years taking her to recitals and practices and lessons; helping her do her hair and makeup; and watching her grow into the graceful, beautiful woman she is today. I always loved to watch my daughter dance, and I had this dream of dancing but didn’t think I was ever going to do this. Then my daughter got engaged, and I wanted a nice first dance with her husband and a nice father-daughter dance, so I signed my husband and myself up for lessons. We continued our lessons after the wedding and had more fun!”

While Kallio-Mielke enjoys dancing, she does have other interests outside her new career as an accounting educator. One of them is playing golf. The other is a new family member. “We have a 21-month-old granddaughter, and I’d babysit her every day if they’d let me.”

is the WICPA communications director. Contact him at 262-785-0445, ext. 4515, or brent@wicpa.org.

Kallio-Mieke’s 40-year accounting career came full circle, traversing from a UW-Milwaukee student to eventually becoming an accounting lecturer at the school.

Kallio-Mielke and her husband, Steve, have become award-winning ballroom dancers.

Photo by Lavanya Badrinath

Brent Roberts

By James D. Brandenburg, CPA, MST

On July 3, Congress gave its final approval to H.R.1, the One Big Beautiful Bill Act (OBBBA), capping off months of high-stakes political drama on Capitol Hill. The final week began in the U.S. Senate, where Vice President JD Vance cast the tiebreaking vote on July 1 to approve the tax bill and send it to the House.

The House then faced its own drama. To pass this legislation before the Fourth of July, the chamber had to vote on the Senate’s version without making any changes. Any adjustments would delay passage until after the holiday. The bill narrowly passed through the House early on July 3 by a 218–214 vote. Officially approved by Congress, the legislation moved to the president’s desk, where he signed the bill into law (as P.L. 119-21) on July 4.

Here are some key tax changes in the bill that passed Congress:

Individual

provisions

Individual tax rates: Individual tax rates were made permanent by the bill and will not rise in 2026. This means the

current tax rates are not scheduled to sunset. A future Congress and president could always change the income tax rates, but these tax rates are not set to expire. Taxpayers should plan accordingly. Additionally, the lower rates for capital gains and dividends are unaffected by the tax bill, keeping their tax-favored status.

Increased standard deduction: The standard deduction is increased to $15,750 for single taxpayers and to $31,500 for married-filing-jointly taxpayers. This change is permanent and effective for tax years beginning in 2025 (and thereafter indexed for inflation).

Child tax credit: The expanded child tax credit will increase from $2,000 to $2,200, applicable for the 2025 tax year, and be made permanent. The credit is subject to a phase-out for higher-income taxpayers.

Deduction for seniors: A new deduction will allow qualified individuals aged 65 and older to claim up to $6,000, first effective for the 2025 tax year.

Qualified business income deduction: This deduction for owners of certain pass-through entities (S corporations, partnerships/LLCs and sole proprietorships) was made permanent by the bill and kept at the 20% level (not the 23% proposed earlier by the House).

State and local tax (SALT) deduction: The SALT deduction had been capped at $10,000 since 2018. The Act

increases this to $40,000, beginning with the 2025 year. The higher threshold applies only through 2029, when it will revert to the $10,000 figure. This higher deduction is phased down (at a 30% rate) to $10,000 for taxpayers with incomes over $500,000 and fully reduced to the $10,000 level for incomes over $600,000.

This SALT cap was probably the most contentious issue in the entire bill, hotly debated this year as the bill progressed. Further, the final bill did not contain any adjustment for a pass-through entity SALT workaround, which had been proposed earlier.

Alternative minimum tax (AMT) exemption: The higher AMT exemption amounts are extended permanently and adjusted for inflation, effective for tax years beginning in 2026. The higher SALT deduction of up to $40,000 (noted above) is not allowed for AMT purposes, however, and along with some changes in the exemption phase-out, AMT could be more of an issue for some taxpayers moving forward.

Estate and gift tax exemption: The estate and gift tax exemption maximum will be permanently increased to $15 million, effective for decedents passing away after Dec. 31, 2025. The $15 million threshold is indexed for inflation.

No tax on tips: A new deduction will be allowed for qualified tips for service industry workers. Eligible tip amounts for this deduction are capped at $12,500 for individuals and $25,000 for joint returns. This deduction applies for tax years 2025 through 2028. On Aug. 27, the Treasury Department released a preliminary list of occupations eligible for the new deduction for tip income.1 However, the IRS will still need to provide guidance for impacted employees and employers.

No tax on overtime: The legislation allows for a deduction for overtime pay, applicable to workers whose income does not exceed $150,000 for single filers and $300,000 for joint filers. The deduction applies only to extra overtime income, not to base pay. Thus, if an employee receives time and a half pay for working overtime, it is only the “half” that is allowed for this OT deduction. The IRS will again need to provide guidance for impacted employees and employers. The IRS announced on Aug. 7 that it would not adjust the 2025 payroll forms for the new overtime deduction or tip deduction but will wait until 2026 to make these form changes. Employees and employers are to use any “reasonable method” to determine the amounts to use for these deductions for 2025.

Information on this development can be found on the IRS website: https://www.irs.gov/newsroom/one-big-beautifulbill-act-of-2025-provisions.

Auto loan interest deduction: The legislation allows for a deduction of up to $10,000 for interest paid on auto loans for U.S.-made vehicles. This is available even to taxpayers who do not itemize their deductions. However, there are limitations that reduce this deduction for taxpayers with higher incomes (over $200,000 if married filing jointly). The deduction is

effective for tax years beginning in 2025. Additional new reporting is required on these auto loans.

Trump accounts: The legislation introduces a new Trump account, defined as an individual retirement account — per Section 408(a) — that is not designated as a Roth IRA. It is a savings account for children, and contributions are subject to a $5,000 annual limit for beneficiaries under age 18. Contributions from employers are allowed ($2,500 limit) as well as from tax-exempt organizations. In addition, for children born in 2025–2028, a $1,000 credit from the federal government can be contributed to the account. After age 18, beneficiaries can distribute the funds for qualified use: generally for education, starting a business, buying a house or other eligible purposes. These accounts will then operate similar to an IRA. The IRS will provide guidance on these Trump accounts, including how to establish them, contribute to them, determine the tax treatment on distributions from them and so forth.

Federal scholarship granting organization (SGO) contribution tax credit: The legislation introduces a new tax credit for individual taxpayers who contribute to qualified SGOs. This provision is designed to incentivize private contributions to fund elementary and secondary education scholarships for eligible students. The credit cannot exceed $1,700 annually per taxpayer and must be a cash contribution. The IRS will need to provide guidance on this new credit. Several states already have SGO-type programs in place, and taxpayers will not be able to double up on these SGO contribution credits for federal and state purposes.

Business provisions

Bonus depreciation: The 100% bonus depreciation deduction is restored. This higher threshold will apply for property acquired after Jan. 19, 2025. (Note: A taxpayer may not be entitled to 100% bonus depreciation for property placed in service after Jan.19 if it had a binding contract to acquire that property as of Jan. 19. IRS guidance may be needed in this area.) This change to 100% bonus depreciation is permanent

Research and experimental expenses: Starting with tax years beginning after Dec. 31, 2024, businesses will once again be allowed to fully deduct their research and experimental expenses the same year those costs are incurred. This change will be permanent. This applies to all domestic businesses in every industry but not to foreign research expenses, which will continue to be amortized over 15 years.

Additionally, this bill allows businesses to deduct the unamortized portion of research expenses — capitalized and amortized over five years since 2022 — either entirely in 2025 or spread across 2025 and 2026. Further, retroactive relief is available for small businesses with less than $31 million in revenue. On Aug. 28, the IRS issued Rev Proc 2025-28, dealing with transition guidance for changes made by OBBBA to research expenditures.2

Interest deduction limitation: Since 2023, the deduction for interest expense has been limited to a lower threshold based on earnings before interest and taxes. Starting in 2025, this limitation shifts to a more favorable threshold based on earnings before interest, taxes, depreciation and amortization. This favorable change will be permanent. There is continued relief for small businesses.

Section 179 deduction for qualifying equipment purchases: The Section 179 deduction limit will increase from $1,250,000 to $2,500,000, and the phase-out threshold will be raised to $4,000,000. This provision applies to property placed in service in tax years beginning after Dec. 31, 2024, and is permanent.

Qualified production facility: Traditionally, the structural components of a manufacturing facility have been depreciated over 39 years as nonresidential property using the straight-line basis. However, this new law introduces a provision allowing qualified production property (QPP) to be currently deductible. QPP is defined as a U.S.-based facility engaged in the manufacturing, production or refining of a qualified product that results in a substantial transformation of the property. Further IRS guidance is needed to clarify various aspects of this new deduction, but this might be a significant opportunity for manufacturing, agriculture and refining businesses to explore.

Qualified opportunity zone (QOZ) permanency and enhancement: The new law introduces several changes to the QOZ provisions originally enacted during President Trump’s first term. It enhances the basis step-up for rural investments, adjusts the timing of gain recognition and makes QOZs a permanent part of the tax code.

2 https://www.irs.gov/pub/irs-drop/rp-25-28.pdf

“

This legislation presents many opportunities for individuals and businesses, as well as for CPAs, to meet with their clients and prospects.

Enhancement of employer-provided childcare credit: The employer-provided childcare credit will be enhanced, allowing businesses to claim a tax credit of up to $500,000 — or $600,000 for small businesses with qualified childcare expenses. The credit covers up to 40% of eligible expenses for most businesses — 50% for small businesses — encouraging businesses to support working families.

This article highlights selected individual and business provisions in the OBBBA. There are many other items in this legislation. Here are a few other provisions to note:

• Enhancements to the qualified small business stock exemption under Section 1202

• Repeal (and restriction) of certain energy credits from the Inflation Reduction Act of 2022 (On Aug. 21, the IRS issued FAQs on this.3)

• Certain international tax provisions

• Provisions impacting tax-exempt organizations

This legislation presents many opportunities for individuals and businesses, as well as for CPAs, to meet with their clients and prospects.

Jim Brandenburg, CPA, MST, is a tax director with Sikich LLC in Brookfield. Contact him at 262-754-9400 or jim.brandenburg@sikich.com.

Over the last century, the requirements for becoming a Certified Public Accountant (CPA) in Wisconsin have evolved to meet the changing demands of the profession — and today is no different. The Wisconsin Institute of Certified Public Accountants (WICPA) is championing a change to address this growing issue in the accounting industry within the state of Wisconsin. The WICPA recognizes that the accounting profession has a future that offers continuous value, and the organization is actively working to help current and future accountants level up for a fulfilling and meaningful career.

A numbers problem

“

When you look at the numbers, it doesn’t take an accountant to see that the industry is at a crossroads. A significant number of experienced CPAs, primarily from the baby boomer generation, are nearing retirement; in fact, the U.S. Bureau of Labor and Statistics projects that 75% of current CPAs are approaching the end of their careers.1 This mass exodus is occurring at a time when the number of new accounting graduates is declining — by 20% since 2010.2

Despite a significant number of CPAs leaving the field and fewer new accountants entering it, the demand for accounting professionals is on the rise. Employment of accountants and auditors, projected to grow by 6% between 2023 and 2033 according to the U.S. Bureau of Labor and Statistics, is growing faster than average when compared with other occupations.3 This imbalance has created an important issue that state organizations (including the WICPA) and state legislatures are working to resolve by updating CPA licensure requirements to address this growing shortage in the industry.

The WICPA recognizes that the accounting profession has a future that offers continuous value — and the organization is actively working to help current and future accountants level up for a fulfilling and meaningful career.

Over 20 states across the U.S. have either enacted or proposed changes to their licensing rules, including those near and bordering the Badger State like Illinois, Ohio, Iowa and Minnesota.4 The WICPA aims to join this national trend, actively working with the state legislature to ensure that the future of the accounting profession in Wisconsin remains

competitive. By providing more flexible pathways to licensure, these modifications seek to help aspiring accountants meet the growing demand and enter the industry.

Alternative pathways to licensure

The proposed legislation in Wisconsin seeks to create an alternative to the current 150-credit-hour route. This new framework would offer three distinct pathways to licensure, all designed to maintain the profession’s standards while providing more flexibility to licensure candidates.

Pathway 1: The master’s route — This pathway requires a master’s degree with specific coursework in accounting and business, along with at least one year of qualifying work experience.

Pathway 2: The 150-credit-hour bachelor’s degree — This pathway requires a bachelor’s degree with at least 150 total credit hours of education, including specific coursework in accounting and business, and at least one year of qualifying work experience.

Pathway 3: Bachelor’s degree and experience alternative — This pathway requires a bachelor’s degree with specific coursework in accounting and business and at least two years of qualifying work experience.

The third pathway is seen as an alternative pathway and offers significant benefits for both aspiring accountants and employers of accountants. For accounting firms and other accounting employers, this change opens up a much larger talent pool and offers the option of two years of work experience, which ensures that new licensees not only are academically prepared but also possess the practical skills necessary to succeed in the field.

The future of the profession

The WICPA’s proposed changes are a proactive response to the evolving landscape of the accounting profession. The new framework will produce CPAs who are both well educated and experienced, ready to meet the challenges of a dynamic industry. This initiative is a vital step toward securing the future of accounting in Wisconsin, ensuring that aspiring professionals can find a clear path to a rewarding career and that businesses have the skilled financial experts they need to succeed and to keep the state — and the profession — moving forward.

Julijana Englander, JD, is an attorney with Neider & Boucher S.C. in Madison. Contact her at 608-441-2527 or jenglander@neiderboucher.com.

Joseph W. Boucher, CPA, JD, is a founding shareholder of Neider & Boucher and serves as the firm’s chairman of the board. Contact him at 608-661-4535 or jboucher@neiderboucher.com.

As an accountant, your clients trust you with their most sensitive financial matters. But when legal complexities arise, a strong legal partner is essential. Neider & Boucher specializes in working with accounting professionals to deliver high-value solutions for your clients.

a principal at Baker Tilly in Madison, has magazine’s 2025 list of Best-in-State CPAs. a partner at Johnson Block & Co. in Madison, magazine’s 2025 list of Best-in-State CPAs.

Mark Behrens, CPA, CFO of Johnson Financial Group in Racine, has received the 2025 Lifetime Service Award from the Wisconsin Bankers Association.

Kelly Blau, CPA, has been promoted to principal at SVA Certified Public Accountants in Brookfield.

Benjamin Brossard, CPA, has been promoted to accounting manager for Green Bay Packers Inc.

Erik Bunnell, CPA, a shareholder at KerberRose SC in Wausau, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

David Carbajal, CPA, the founder and president of Squash CPA in Brookfield, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Thomas Carini, CPA, has been promoted to audit senior manager at Deloitte & Touche LLP in Milwaukee.

Christine Dahlhauser, CPA, a managing principal at Baker Tilly in Madison, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Nathan Davis has been promoted to senior accountant at RitzHolman CPAs in Milwaukee.

William Dintenfass has been promoted to senior accountant at RitzHolman CPAs in Milwaukee.

Lynn Gardinier, CPA, CMA, a principal at Baker Tilly US LLP, was selected as the commencement speaker for UW–Whitewater’s spring commencement ceremony, held Saturday, May 17.

Kurt Gresens, CPA, CGMA, a managing partner at Wipfli LLP in Green Bay, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Omunazia Hicks, MBA, has joined Wegner CPAs in Waukesha as a staff accountant. Hicks, who graduated from UW–Whitewater in May, also was selected as the WICPA’s 2025 Student Excellence Award recipient.

Patrick Hoffert, CPA, managing partner at Reilly, Penner & Benton LLP in Milwaukee, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Paige Janquart, CPA, has been promoted to vice president of finance at Capitol Bank in Madison.

Hannah Jensen, CPA, a partner at Wegner CPAs in Madison, has been named to the 2025 class of Forty Under 40 professionals in the Madison area by In Business magazine.

Jason Kadow, CPA, CVA, CGMA, CEO of KMA Accountants & Advisors in Madison, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Robert Keebler, CPA, PFS, MST, AEP, a partner at Keebler & Associates LLP in Green Bay, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Trenton Kleist, CPA, a principal at Baker Tilly in Madison, has been named to the 2025 class of Forty Under 40 professionals in the Madison area by In Business magazine.

Abraham Leis, CPA, managing partner at Hawkins Ash CPAs in La Crosse, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Carl Marzolf, CPA, MSA, the president of Lucida Tax & Accounting Solutions in Waukesha, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Glenn Miller, CPA, CGMA, managing partner at Wegner CPAs in Madison, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Tim Moy, CPA, CGMA, managing partner at MBE CPAs in Baraboo, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Rebecca Muehl, CPA, has been promoted to principal at SVA Certified Public Accountants in Madison.

Eric Neuman, CPA, a partner at Chortek LLP in Waukesha, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs. Joseph Peikert, CPA, CEO of Wolf River Community Bank in Hortonville, has been elected to serve as chair-elect of the Wisconsin Bankers Association board of directors.

Laura Piotrowski, CPA, SHRM-SCP, CEO and president of Cavendish Vernal LLC in Brookfield, has been elected to the board of directors at Waterstone Financial Inc.

Nicole Rotier, CPA, has been promoted to CFO at Spring Bank in Brookfield.

Gina Skibo, CPA, has been named the new industry leader for Wipfli LLP’s manufacturing, retail and distribution practice.

Kory Stoehr, CPA, MST, tax market managing principal for southern California at BDO USA LLP, has been recognized on the Los Angeles Business Journal ’s 2025 “LA500” list of industry leaders and executives in the Los Angeles area.

Haruki Toben has been promoted to senior accountant at RitzHolman CPAs in Milwaukee.

Eric Trost, CPA, has been promoted to president of SVA Certified Public Accountants in Brookfield.

Victoria Thayer, CPA, founder and president at Novii CPA in Madison, has been named to the 2025 class of Forty Under 40 professionals in the Madison area by In Business magazine.

Thomas Carini

Ben Brossard David Carbajal Nathan Davis

William Dintenfass Omunazia Hicks Patrick Hoffert Paige Janquart Kelly Blau

Wendi Unger, CPA, a principal at Baker Tilly in Milwaukee, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Matt Vanderloo, CPA, CGMA, CEO of SVA Certified Public Accountants in Brookfield, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

Nathan Volkomener, CPA, managing shareholder at Vesta in Plymouth, has been named to Forbes magazine’s 2025 list of Best-in-State CPAs.

John Wagner, CPA, controller at Miron Construction Co. Inc. in Neenah, has been named to the 2025 class of 40 Under 40 professionals in northeastern Wisconsin by Insight On Business magazine.

Lauren Wanta, CPA, has advanced to the role of director at CliftonLarsonAllen (CLA) in Green Bay.

Seth Wooll, CPA, has joined the Milwaukee office of Brillect, an accounting and consulting firm and certified women-owned business, as its client solutions director.

FIRM NEWS

Francis LLC, a retirement plan consulting and workplace financial wellness services firm headquartered in Brookfield, has received the 2024 Innovation Award from the Wisconsin Governor’s Council on Financial Literacy and Capability for its excellence in increasing financial literacy, capability and inclusion of Wisconsin residents.

KMA Accountants & Advisors, headquartered in Madison, has announced that it officially became Sorren, a new accounting and advisory firm with more than 1,000 professionals across 20 offices nationwide.

Truity Partners, headquartered in Madison, has announced the firm’s 30th anniversary. Since its founding in 1995, Truity Partners has grown into a recruiting and staffing firm with offices across Wisconsin, Minnesota and Illinois.

Want your new job, promotion or award mentioned in Kudos?

H Email your announcement and photo in JPG format to john@wicpa.org. H

Kory Stoehr Eric Neuman Robert Keebler Joseph Peikert Gina Skibo Haruki Toben Eric Trost Victoria Thayer Wendi Unger

Hannah Jensen John Wagner Seth Wooll

Moving Beyond Risk Assessment in the SQMS Implementation Journey

By Heather Lindquist, CPA

Firms that perform engagements under Statements on Auditing Standards, Statements on Standards for Accounting and Review Services, and Statements on Standards for Attestation Engagements should be spending part of their summer studying up on the AICPA’s new Statements on Quality Management Standards (SQMS). With an effective date requiring that firms’ quality management systems be designed and operational by Dec. 15, there’s little time to waste.

As I outlined in my winter 2024 Insight article, “6 Tips for Implementing the New Quality Management Standards,” the new SQMS lays out a framework that includes two process-oriented components: 1) risk assessment and 2) monitoring and remediation. These two components are integrated with six environmental and operational components (governance and leadership, relevant ethical requirements, acceptance and continuance, engagement performance, resources, and information and communication).

“

Overall, the nuts and bolts of this new framework require firms to set quality objectives, identify and assess quality risks, and design responses for the six environmental and operational components.

In my winter article, I gave an overview on the importance of learning the basics of what’s required under the new SQMS — building a design and implementation team, developing a roadmap for the design process and understanding the new risk-assessment requirements. However, at this stage in the SQMS implementation journey, firms should be moving beyond identifying and assessing risks to responding to quality risks through their policies and procedures, sufficiently documenting the design of their quality management systems, and communicating to and training personnel about the changes. Here, I’ll be addressing all three of these important next steps.

Responding to quality risks

Developing effective responses to quality risks involves leveraging current firm policies and procedures and potentially designing new ones. For example, SQMS No. 1, “A Firm’s System of Quality Management,” requires certain “Specified Responses” be incorporated into a firm’s quality management system, addressing presumed risks within the system. One of the “Specified Responses” requires firms to establish policies and procedures to annually obtain personnel’s confirmation of compliance with independence requirements. (Many firms already have such a process in place and will only need to link this response to related risks within quality management design documentation.)

With an effective date requiring that firms’ quality management systems be designed and operational by Dec. 15, there’s little time to waste.

Conversely, firms will likely need to design new policies and procedures for “Specified Responses” relating to information and communications. Specifically, firms will need to address risk associated with external communication about the firm’s quality management system, including the nature, timing, extent and form of any such communications.

While firms must incorporate “Specified Responses” into their quality management systems, these alone won’t address all quality risks. Firms will need to review current policies and procedures, mapping these out against identified quality risks and designing new responses where necessary.

Further, SQMS No. 1 requires firms to assign ultimate responsibility and accountability for the quality management system to the managing partner (or equivalent) as well as certain other roles. This includes assigning operational responsibility for the quality management system, compliance with independence requirements, and the monitoring and remediation process. Though the same individual may assume

responsibility for all these roles, the standard requires firms specify (and document) which individual or position will fulfill each task.

Developing design documentation

SQMS No. 1 also requires firms to develop documentation supporting both the design and operation of their quality management systems. Firms in the midst of the design and implementation process must determine the best method of documentation to accomplish the following:

• Facilitate understanding of the system’s operation by personnel, including roles and responsibilities

• Ensure consistent implementation and operation of the responses (i.e., policies and procedures)

• Provide sufficient evidence of design, implementation and operation of the responses to support the evaluation of the system

Importantly, design documentation can take many forms and will vary in complexity based on each firm’s circumstances. However, regardless of its form, the design documentation must assign required roles; demonstrate that a risk-assessment and response design process was performed (including the establishment of quality objectives); and, if applicable, address relevant network participation considerations.

For example, one approach could be creating a quality management document supported by a risk-assessment and response document, with each part serving the following purposes:

• Quality management document: This summarizes the firm’s approach to quality management with policies and procedures for all eight components. For the two process-oriented components in the new SQMS (risk assessment and monitoring and remediation), the document would include policies and procedures related to how the firm administers each process. For the six environmental and operational components requiring risk assessment, the policies and procedures summarize the responses to identified quality risks (including the required “Specified Responses”) linking back to the risk-assessment and response document. Additionally, the document would assign the required roles.

• Risk-assessment and response document: This provides evidence of the firm’s risk-assessment process, including the establishment of quality objectives, identification and assessment of risks, and development of appropriate responses. The document demonstrates the linkage between risks and designed responses (policies and procedures that flow into the quality management document). The firm can periodically revisit this document to reexamine conclusions on quality risks and determine the need for new or revised responses depending on changing conditions and circumstances.

Training firm personnel

The existence of a written document means very little without a commitment to educating firm personnel about how to live out its

contents. Though not everyone needs to understand the ins and outs of the firm’s quality management system, having all personnel possess a general understanding of quality management and its role in the firm’s operations is critical to ensuring they adhere to the firm’s newly designed policies and procedures.

To foster this understanding among personnel, begin by spreading awareness. Circulate the quality management document to all personnel, and hold a short meeting to familiarize them with the SQMS basics, including policies and procedures (current and new) and the process that firm leadership went through to identify, assess and respond to quality risks.

Stella Marie Santos, CPA, managing partner at Adelfia LLC, champions this approach, explaining that her firm has always made reading its quality control document a part of the employee onboarding process. Now, with the new SQMS implementation looming, Santos says the firm plans to hold specific training to educate personnel about the upcoming changes and the firm’s new quality management document.

Of course, even after the Dec. 15 implementation deadline, firms should consider how to maintain quality management awareness.

Randall Miller, CPA, partner at Hawkins Ash CPAs, suggests a method his firm uses to keep employees up to date on policies and procedures: requiring employees to confirm receipt of and review the firm’s updated quality management policies and procedures each year alongside their annual confirmation of compliance with independence requirements.

In addition to awareness, providing context of the “why” behind certain policies and procedures is important. For example, firm personnel should consider the criticality of completeness, retention and secure storage of engagement documentation during training as well as prior to locking down engagement files.

For Santos and her team, the plan is to explain the concept of quality risk assessment during training and provide context about the resulting responses and how various business considerations may impact risk, which may then lead to new or amended responses in the future.

Further, asking personnel to identify connections between their roles and quality management concepts, such as whether their continuing professional education plans align with the type of work they perform, can be an effective tool for gauging understanding.

Overall, a successful quality management system hinges on a firm’s ability to comprehensively identify quality risks, develop responses to the risks, and successfully communicate and achieve buy-in from all personnel. Spending sufficient time tackling these challenges will help ensure that your firm’s system isn’t only well designed but also well executed.

Heather Lindquist, CPA, is the Illinois CPA Society’s director of peer review and professional standards.

Reprinted

Elizabeth Ahrens KPMG LLP

Rasem Alawi

Emily A. Anderson Deloitte & Touche LLP

Catherine Aschenbrenner

Ben Bader

Levi M. Ballard Deloitte & Touche LLP

Justin D. Bednarcik Forvis Mazars

Faryn Benedict The Manitowoc Company Inc.

Sara J. Birschbach Menomonee Falls High School

Ryan D. Blair Uline Inc.

Martin G. Boyle

Emily C. Braatz RSM US LLP

Amber Brown CLA

Patrick E. Burke KPMG LLP

Daniel J. Burns Fine Point Consulting LLC

William N. Carl Century Companies

Clayton J. Carlson Wipfli LLP

Sampheus Chhit UW Credit Union

Ethan W. Coons Baker Tilly

Kelvin Cribbs

Juliet A. Deckman

UW–Whitewater College of Business & Economics

WELCOME NEW MEMBERS!

April 1, 2025 – July 31, 2025

Alyssa D. Doering Deloitte & Touche LLP

Andrew B. Donahue KPMG LLP

Brian Donohoe Deloitte & Touche LLP

Matthew Doucette Sr. KPMG LLP

Lauren M. Drews SVA Certified Public Accountants

Patrick G. Durch Bauman Associates Ltd.

Sean Ellefson Kerber, Eck & Braeckel LLP

Aaron Erdmann Hawkins Ash CPAs LLP

Jean M. Evert

Barbara Farrell FOCUS Administrative Services

Emily M. Fitzpatrick Jayme Frisch

Matthew A. Frisone Deloitte & Touche LLP

Jack R. Fritz

Leah Gaffney Baker Tilly

Aaron R. Galvan Baker Tilly

Luis I. Garcia Hernandez NOVII CPA LLC

Ryan A. Glander

UW–Whitewater College of Business & Economics

Karla Gruszynski UW–Whitewater College of Business & Economics

Mitchell Haag Wipfli LLP

Mark Haakenson

UW–La Crosse

Laney Halbach UW–Oshkosh

Connor Handel Deloitte & Touche LLP

Christina Hansen Weaver and Tidwell LLP

Cameron Heiser KPMG LLP

McKenzie T. Henneberry UW–Whitewater Foundation

Barbara J. Hermann

Morgan Hestetune Reilly, Penner & Benton LLP

Nicholas R. Hietala KerberRose S.C.

Katy Hook PwC

Linda R. Huckaby

Andrew Johnson UW–Green Bay

Matthew R. Johnson

Lucida Tax & Accounting Solutions

Daniel P. Jones

Emma Kaczynski KPMG LLP

Tamara J. Kasinski Waukesha State Bank

Max J. Kasper

Samantha Kerkman

Zachary Kestell UW–Oshkosh

Anna Kiskunas KPMG LLP

Konrad Klein

Scott C. Kovtun Nolan Accounting Center

John R. Kuehn

Alexia Kurey

Kathleen Kysely UW–Madison

Benjamin Lamers CLA

Allison S. LaPlante Catalyst Consulting Group LLC

Brittany Larson Western Governors University

Neal Latino

Jaden Lehrmann

Aubree E. Leis Slinger High School

Anna Lien

Johnson Block & Co. Inc.

Kaarin D. Lind

Hawkins Ash CPAs LLP

Wayne G. Link

Timothy Loch Sr. Franciscan Sisters of Christian Charity Sponsored Ministries Inc.

Haofan Lu

John Ludolph

Gracie Mathies

Hawkins Ash CPAs LLP

Nicole M. McDonald

Caleb McFarlane KPMG LLP

Maia L. Messerschmidt UW–Whitewater Foundation

Ally Meyer Motor Specialty Inc.

Maddy L. Mickelson Franklin High School

Elizabeth A. Miller Godfrey & Kahn S.C.

Brian C. Morris Milwaukee County Comptroller’s Office

Timothy P. Muehler CLA

Andrew Muffler Baker Tilly

Thi Van Anh Nguyen

Krysta Nichols Chortek LLP

Eric D. Olmack Deloitte & Touche LLP

Drew A. Paulson BMO Harris Bank

Joshua Pavlik Carthage College

Clara L. Pickett Kaukauna Utilities

Andrew J. Platta AP Income Tax & Accounting LLC

Cheryl Pleinis

Hailey Ploense CLA

Victoria Poje KPMG LLP

Robert Pomerenke Hawkins Ash CPAs LLP

Michelle L. Puls Sorren Inc.

Christopher Pykett Baker Tilly

Allison Rakers KerberRose S.C.

Matthew Redlinger Deloitte & Touche LLP

Dale R. Reichert Herrschners Inc.

Steven M. Reiss

Jaden J. Rice UW–Madison

Addison A. Richardson McFarland High School

Alicia M. Richmond Wegner CPAs

Isabelle R. Rimalovsky Deloitte & Touche LLP

Katherine P. Rogers Cambridge High School

Nathan Rosengarten Catalyst Consulting Group LLC

Korry C. Rowe Reinl Accounting Inc.

Cynthia A. Roy

Brian Salkowski Deloitte & Touche LLP

Benjamin Saltzman

Marcus R. Schmidt Lucida LLC

Laura Schnelle SVA Certified Public Accountants

Tyler Schoemann Kerber, Eck & Braeckel LLP

Lindsey T. Schwellinger Deloitte & Touche LLP

Allison M. Semenak Northwestern Mutual

Ryan Shavlik Baker Tilly

Livia Shi KPMG LLP

Gwen E. Snyder

Kylee M. Sommer Baker Tilly

KellyAnn E. Sotiros Deloitte & Touche LLP

Jamie Spina Batley CPA LLC

Sonia Stafeil UW–Madison

Sierra Steele Black Hills State University

Ethan R. Strasser Hancock & Robinson CPAs

Tanner J. Trombley Deloitte & Touche LLP

Latascha M. Trotter

Cassandra Tyler Brenna Van Rooy Hawkins Ash CPAs LLP

Dana Ver Kuilen Tri City Glass and Door

Dawn Vogel

Madison Metropolitan School District

Calibor L. Welhouse

Amy Weyers Deloitte Tax LLP

Trenton Wild Deloitte & Touche LLP

Samuel Wulfkuhle Deloitte & Touche LLP

Cindy Xiong

Laura Zahn

Northwestern Mutual

Greta Zier Marquette University

Michael A. Zuleger CLA

memorials

Robert Edward Evered, CPA (1946–2025)

Robert (Bob) Edward Evered, CPA, passed away on Wednesday, April 9. He was 78. Evered was born and raised in Superior and graduated from Superior Cathedral High School in 1964. He then joined the Army National Guard, serving for six years. He subsequently worked several jobs before continuing his education at the University of Wisconsin–Superior, where he earned his bachelor’s degree in accounting. Evered was licensed as a CPA in 1984 while working for the Wisconsin Public Service Commission. After leaving there, he joined Superior Water, Light & Power, where he worked as an accountant until his retirement in 2008. Evered was a 40-year member of the WICPA. He is survived by his wife, Kathy; one daughter; three sons; and other extended family and friends.

Louis John Fohr IV, CPA (1941–2025)

Louis John Fohr IV, CPA, age 84, passed away on Tuesday, June 10. Fohr was born and raised in Wauwatosa. After graduating from Milwaukee Lutheran High School, he attended Lakeland College and the University of Wisconsin–Milwaukee. He received his MBA from Marquette University and obtained his CPA license in 1968. Fohr founded his own CPA practice in 1975 and provided business and financial advice to a wide array of clients. Fohr is survived by his wife of 48 years, Susan; a son and daughter; three grandchildren; and two brothers.

Michael John Hablewitz, CPA (1966–2025)

Michael (Mike) John Hablewitz, CPA, age 58, passed away on Sunday, June 8. Hablewitz was born in Neenah and graduated from Neenah High School in 1984. He went on to attend the University of Wisconsin–Oshkosh, where he earned a bachelor’s degree in accounting and management information systems. In 1992, he became licensed as a CPA and joined the WICPA. Hablewitz worked for several employers throughout his career, most recently as a partner at IVI Inc., an industrial ventilation manufacturer in Greenville. He enjoyed volunteering in his community as a member of the Fans of the Foxes booster club and the Fox Valley Memory Care Project. Hablewitz was known to lead wherever possible and socialize often. He is survived by his wife of 35 years, Diane; two daughters and one son; two brothers; and many other relatives and friends.

Keith D. Helm, CPA (1963–2025)

Keith D. Helm, CPA, aged 61, passed away on Sunday, April 6. Helm was born in Milwaukee and raised in West Allis. He graduated from West Allis Central High School in 1981 and the University of Wisconsin–Whitewater in 1985. Helm became a CPA in 1987. He had a robust career that included launching his private practice, Liberty Accounting Services, where he worked for over 30 years. He also developed

partnerships with Green Hotels/Ecovision in Costa Rica and Food Ingredients Inc. in Waukesha, where he served as CFO. Wherever he went, Helm’s top priorities were his faith, family and friends. His favorite pastimes included watching sports, coaching, mentoring, traveling, deer hunting and attending Milwaukee’s German Fest. He is survived by his wife of 37 years, Lori; two sons; four grandchildren; and many other relatives and friends.

Maurice A. Kryshak, CPA (1931–2025)

Maurice A. Kryshak, CPA, aged 94, passed away on Saturday, June 14. Kryshak was born and raised in Stevens Point and graduated from P.J. Jacobs High School in 1948. He served in two branches of military service, beginning with the Army National Guard followed by a four-year enlistment in the Air Force. After his military service, Kryshak continued his education at the University of Wisconsin–Madison, where he received a bachelor’s degree in accounting. He became a CPA in 1962 and enjoyed a lengthy and successful career that included working at an accounting firm in Wausau as well as a national moving company. He ultimately started his accounting business specializing in small businesses and tax preparation. Kryshak’s experiences as an accountant inspired his children to pursue similar professions, with two of them joining his company and eventually taking ownership. He was a lifetime member of both the WICPA and Knights of Columbus as well as a dedicated volunteer with the Cub Scouts and Boy Scouts of his local church parishes. He is preceded in death by his wife of 70 years, Marjorie, and is survived by five children, seven grandchildren, eight greatgrandchildren and one great-great-grandchild.

Scott H. Luber, CPA (1960–2025)

Scott H. Luber, CPA, aged 65, passed away on Wednesday, July 2. He was born and raised in Milwaukee. After graduating from the University of Wisconsin–Milwaukee and earning his CPA license in 1987, Luber worked as an accountant at BDO USA LLP before pursuing a career in advocacy for the disabled. He was the administrative director at Independence First in Milwaukee for 14 years before retiring as an independent consultant. His community leadership involvement included board positions at the Jewish Family Services Inc. in Milwaukee and The Ability Center in Wauwatosa. He is survived by his parents, one brother, several nieces and nephews, and many other relatives and friends.

Gregory Skaar, CPA (1962–2025)

Gregory (Greg) Skaar, CPA, aged 62, passed away on Wednesday, July 9. Born and raised in Viroqua, Skaar went on to graduate from the University of Wisconsin–Milwaukee in 1984, join the WICPA in 1985 and earn his CPA credential in 1988. He started his accounting career at Touche Ross

(now Deloitte USA) and later worked as a controller for 10 years at HB Performance Systems in Mequon. He last served as the CFO for Packaging Solutions Inc. in Milwaukee. Skaar is survived by his wife, Amy; one son; a brother; two nephews; and many lifelong friends.

Mitchell Alan Smith, CPA (1935–2025)

Mitchell (Mitch) Alan Smith, retired CPA, aged 90, passed away on Monday, May 19. Smith was born and raised in Chippewa Falls. After graduating from the University of Wisconsin–Whitewater and passing the CPA Exam in 1967, he joined a growing accounting firm in Lake Geneva. He later started his own firm with several partners and employees, mentoring many young tax professionals during his career. Smith was a 57-year member of the WICPA and also held leadership positions in several community organizations,

including the Knights of Columbus, Jaycees, Friends of the Lake Geneva Public Library, the Library Board and the Lake Geneva Chamber of Commerce, for which he served as president. He was a longtime member of the St. Francis de Sales Parish, where he volunteered for the church’s community meal program and distributed Holy Communion to residents of Lakeland Health Care Center for 25 years. Smith and his beloved wife, Patricia, enjoyed 68 years of marriage before her passing in 2024. He is survived by their two daughters, three grandchildren, five great-grandchildren, a sister and many other relatives and friends.

If you are aware of a member obituary and believe it should be included in Memorials, please send a copy of the obituary or contact John Rasche at john@wicpa.org.

KEEPING COSTS DOWN FOR YOUR CLIENTS

Supreme Court Decision Impacts Retirement Plan Sponsors

By Joseph Topp, CPA

On April 17, the U.S. Supreme Court issued a unanimous and impactful ruling in Cunningham v. Cornell University, reshaping the legal landscape for retirement plan fiduciaries (aka plan sponsors). If you are involved in the oversight of your company’s retirement plan, this decision is not just legal news — it’s a direct call to review your plan’s oversight process and the quality of your advisory services.

Fight over fees

The case originated in 2016, when participants in Cornell University’s multiple 403(b) retirement plans — representing approximately 28,000 employees — alleged that plan fiduciaries breached their duties under ERISA1 by permitting excessive fees through the use of multiple recordkeepers and a large menu of investment options. Lower courts dismissed the case, agreeing with Cornell’s defense that the plaintiffs failed to furnish sufficient facts to support a breach of fiduciary duty.

The persistent plaintiffs successfully appealed, pushing their case up to the Supreme Court, which reached a different conclusion. The justices ruled plaintiffs bringing an ERISA “prohibited transaction” claim (under § 406(a)(1)(C)) do not need to show, at the pleading stage, that fiduciaries violated ERISA’s exemption rules, which permit reasonable compensation for necessary services. Instead, it is the fiduciary’s responsibility

“

If you are involved in the oversight of your company’s retirement plan, this decision is not just legal news — it’s a direct call to review your plan’s oversight process and the quality of your advisory services.

to prove they complied with those exemptions — effectively shifting the burden of proof from the plaintiff to the defendant (plan sponsor).

Plan sponsors’ risk increased

The ruling significantly reduces what plaintiffs need to show in order to survive a motion to dismiss. A plaintiff no longer needs to preemptively refute a plan sponsor’s defense that their actions were “reasonable.” As a result, ERISA class actions — particularly those involving plan fees, investment menus and service providers — will likely increase in volume and reach earlier stages of discovery.

In short: It is now easier to sue plan fiduciaries for alleged excessive fees, and plan sponsors may face higher legal exposure even when their decisions were sound and well intentioned.

Safeguards against meritless claims

Acknowledging the risk of a flood of meritless lawsuits, the Supreme Court offered several ways for lower courts to maintain balance:

• Courts may require plaintiffs early in the case to formally respond to a fiduciary’s affirmative defense that only reasonable fees were paid, helping to flush out weak claims.

• Claims can still be dismissed if plaintiffs fail to allege a plausible injury, such as the presence of genuinely unreasonable fees.

• If a defendant’s exemption defense is obvious, the court may impose sanctions or award attorneys’ fees to the defendant to deter frivolous claims.

While these measures offer some protection, the burden still lies with the plan sponsor to demonstrate that their plan process was prudent.

Plan sponsors’ action plan

This highly anticipated decision should remind all plan sponsors of the duties and responsibilities they accept when deciding to offer their employees a qualified retirement benefit. The key to protection lies primarily in the process you employ to make decisions, not merely the outcome. Now that it’s easier for plaintiffs to bring a complaint, plan sponsors will do well to remember the following:

• Know the rules: Mandate ERISA fiduciary training for anyone in your organization who has a decision-making role in your organization’s qualified retirement benefits.

• Construct a prudent process: Clearly outline responsibility for oversight of your plan within your organization. This process starts with a board resolution delegating authority over your plan. A committee charter and a current investment policy statement serve as vital tools in formalizing your governance process.

• Document all decisions: Once your process is constructed, maintain good records of all meetings and all fiduciary decisions regarding the plan, including the rationale for all decisions made. Quarterly meetings of plan fiduciaries is the industry best practice.

• Properly communicate to participants: For defined contribution plans — ones in which participants are asked to make critically important decisions — be sure to communicate clearly and completely about the plan, its features, its fees and participants’ responsibility to make their own decisions.

• Annually audit your oversight practices: An annual review of plan utilization, the reasonableness of all plan fees using industry benchmarks and a checklist of compliance with the plan’s operational requirements comprise best practice.

• Know your plan costs: You need to understand the individual components of your retirement plan’s costs and should be able to demonstrate proactive activities to benchmark and manage these costs. This exercise needs to be well documented and should occur, at minimum, on an annual basis.

Your process is your protection

The Cunningham v. Cornell decision is a sharp reminder that ERISA’s core fiduciary principles are focused less on outcomes and more on how decisions are made. With the burden of proof clearly laid at the feet of the plan sponsor, industry insiders predict the number of ERISA lawsuits will meaningfully increase, and the subject of these suits — once applied only to the largest of plans — will rapidly move downstream to target smaller plans. Your best defense remains active attention to the oversight process. A quality advisor will push your organization to implement the necessary process and will monitor your ongoing adherence to that process.

Joseph Topp, CPA, is a principal and senior vice president at Francis LLC. Contact him at 262-781-8950 or Joseph.Topp@FrancisWay.com.

Note: This article is not intended as legal advice. Please consult with qualified ERISA counsel.

Navigating the Challenges Facing Nonprofits

By Melodi Bunting,

CPA, CMA, CGMA, MBA

For over 100 years, nonprofits have been recognized as tax-exempt organizations in the U.S.

According to IRS Publication 557, there are 29 specific types of 501(c) organizations. In 2022 the IRS reported 1.48 million — or 75% — of the 1.97 million nonprofits were 501(c)(3) organizations.

The 501(c)(3) organizations are often referred to as charitable organizations, as they are organized for public benefit. These organizations exist for one of the following purposes: charitable, religious, educational, scientific, literary, testing for public safety, and preventing cruelty to children or animals.

Charitable organizations have always faced funding and operational efficiency challenges. Fully 88% of charitable organizations have budgets of less than $500,000. The limited budgets and resources for these grassroots organizations increase these challenges. Fiscal sponsorship or mergers can increase administrative efficiency, reduce costs and increase capacity; however, these options may not be a solution for all organizations.

Grassroots organizations that employ best practices can support and sustain their mission impact and meet the needs of their communities. So, what are these best practices?

Effective board governance and leadership

The board of directors of a nonprofit has three primary fiduciary duties: the duties of care, loyalty and obedience. These duties require board members to act with diligence, prioritize the organization’s best interests and comply with all applicable laws and regulations.

Given these expectations, it is vital to recruit board members who will provide solid financial management and strong oversight. Utilizing a “board matrix” facilitates structuring the board with the diverse skills and capabilities needed. After a candidate who aligns with the matrix needs is identified, the onboarding process is essential in engaging the new board member and setting clear expectations.

“

Grassroots organizations that employ best practices can support and sustain their mission impact and meet the needs of their communities.

Transparency and accountability that build public trust and reputation

Donors, volunteers and other community members want to partner with an organization they can trust. Building this accountability requires transparency and effective communication. A website that includes mission impact stories, financial information, newsletters, board member profiles and ways to get involved is a good start. Being honest about challenges and how the organization is addressing them further demonstrates accountability and strengthens trust.

Financial sustainability

Nonprofits need the resources and strategies for building longterm financial sustainability. It’s not an easy task, but it is a vital one. Creating a strategic plan to achieve and maintain financial sustainability includes both short-term and long-term goals.

It is easy to pursue any available revenue, but a healthy revenue mix includes diverse funding sources and considers the costs of acquiring and administering the various revenue types. Boards that regularly review the revenue mix and the alignment with the strategic plan enhance predictability, mitigate risks and provide growth opportunities.

Having sufficient operating reserves is another key component of financial sustainability. As part of their strategic leadership, boards assess the appropriate level of operating reserves and regularly review it. The funding of the reserves requires intentionality and may warrant inclusion as a line item in the budget.

Another important tool for being prepared for unpredictable circumstances is having a line of credit. The line of credit (in conjunction with the operating reserves) provides the resources necessary to navigate the unexpected.

Effective budgeting and monitoring

When all staff are part of a collaborative budgeting process, decision-making on resource allocation is enhanced. This approach ensures the needs and priorities throughout the organization are understood and fosters shared transparency and accountability for maximizing mission impact.

This participative budget also provides an important communication tool. Comparing the budget to actual results provides feedback on changes in the marketplace and enhances a nonprofit’s agility to respond to unexpected changes.

Agility