THE WorLD IN BrIEF

By Keisha & Isha

What is a mortgage?

A mortgage rate is a type of loan used to purchase a type of real estate. It is where the borrower agrees to pay the lender over time. You will borrow this money from a bank or building society such as Halifax and pay this money back every month for a set number of years. A mortgage can run up to 40 years. However some young buyers are resorting to choosing ultra long mortgages to secure their new houses.

The situation with Ultra long mortgages

The interest rate at the moment is currently 5.25% and this was implemented to help slow down price

rises. As a result, mortgages were made longer to have lower monthly payments as people managed their finances during the cost of living crisis.

This can be seen through Nicola Webb, a 34 year old nurse, who has opted for a 35 year mortgage to pay for her two bedroom flat in Gloucestershire. This is because she says “this is the only way I can just about afford my mortgage as a single homeowner” (BBC News. (2024). Her mortgage is estimated to end when she is 68. However, when her student loan is paid off she hopes to reduce her mortgage from 35 years and use her disposable income to pay it. Recent figures suggest that Nicola’s circumstances are becoming more common.

According to the Bank of England in the past 3 years, 100,000 homeowners have purchased mortgages that they will be paying off into retirement. Even though these long mortgages make repayments more affordable the buyers will be paying more interest overall. However, for some long mortgages are seen as a temporary fix to wait to see if mortgage rates will fall back.

Amidst the public uncertainty, I believe that the Bank of England is likely to cut interest rates in the face of the upcoming election on the 4th July 2024.

By Marwa

Analysis of the latest data from the Office for National Statistics (ONS) confirms “businesses spent £2.9 billion less on air travel in 2023, a decrease of 22%, in comparison with 2019.”. This is despite a growth rate of 1.8% in real GDP, contradicting the aviation industry’s claims that increasing the number of flights will drive economic growth. Instead, airline industries have seen a decline in requests for their business services coupled with a rise in environmental backlash.

New Economics Foundation (NEF) discovered flights for business purposes fell by 29% in 2023, compared to pre-pandemic levels in 2019, with 3.9 million fewer trips made. The collapse in use of business air travel in the last decade, in spite of the huge growth in passenger numbers, can be explained by the widespread adoption of home working and increasing use of platforms such as Teams, Zoom and Google classrooms. Emergence of these platforms has reshaped the

relationship between major companies and business flying, since it has decreased the necessity of travelling to countries for meetings that can be held within the comfort of one’s own home.

Alex Chapman, senior economist at the NEF, states:

“Business use of air travel peaked in 2007 and has fallen further since the pandemic”, expressing concern and evidencing the decline. Moreover, the CEO of IAG (parent company of British Airways and Iberia) said business travel in the previous summer had “plateaued”. This levelling-off period reflects a growing concern for the airline industry and raises questions of the necessity for business flights.

This decline also coincides with increased environmental scrutiny on large corporations. Flying is one of the most carbon-intensive activities, contributing around 4% to global warming, shown in the latest data

figures from the 8th of April 2024. EY (Etihad Airways), owned by the UAE, has taken action to reduce their carbon emissions by 36% by 2025. Encouraging incentives to reduce polluting emissions may include reducing demand for the airline’s business services, which can be viewed as a luxury good.

Greenwashing refers to claims that aim to deceive the public about how environmentally friendly a policy or organisation is. The aviation industry has been involved in many greenwashing allegations, with 2 major airlines being sued in the EU and US, and several facing regulatory reprimands across the globe over their advertising. Resultantly, it has been a major driver towards the decline in demand for business flights, as consumers begin to acknowledge the harmful impacts flying involves.

As the aviation industry continues to evolve, companies and airlines are urged to consider sustainable alternatives to help decrease their total emissions on the atmosphere and minimise their impact on the Earth.

By umandi

On May 14th, President of the United States, Joe Biden, imposed a tariff rate of 100% on electric vehicles (EVs) made in China. Alongside this, he increased tariff rates on other Chinese-made goods including semiconductors, solar cells, and lithium batteries.

Firstly, a tariff is a tax imposed by the government on goods imported to one country from another. Typically, tariffs raise revenue or protect domestic industries from foreign competition. China and the US have been fiercely battling in an ongoing trade war, which, in simple terms, is where countries impose tariffs on each other. Tensions rose in 2018, with former president, Donald Trump, imposing tariffs on Chinese imports following accusations of China’s unfair trading practices. However, there is a perception that America is trying to influence its rise as a global economic power. Currently, the US suffers from floods of cheap Chinese imports.

In China, companies often benefit from low production costs due to low wages, fewer regulations and most importantly, large subsidies from the government, encouraging a larger supply of cheaper products. Whilst

these imports provide US citizens with greater variety and cheaper alternatives, they have a detrimental effect on domestic industries who suffer from a lack of demand. Therefore, the purpose of increased tariff rates is to protect and promote US manufacturing. The recent tariff spikes have affected more than $18 billion of Chinese goods, making the imports more expensive, which consequently boosts demand for relatively cheaper domestic products, encouraging firms to boost production. Moreover, firms become less worried about the threat of foreign competition, encouraging investment which catalyses growth, which can also allow US technology to catch-up with China’s especially in the EV (green technology) industry. Another speculated factor contributing to the tariff increases is political gain related to the upcoming presidential elections. An effect of the tariff increases is increased job security for workers in the manufacturing sector which may lead to less trade union conflict, potentially boosting president Biden’s upcoming re-election campaign. However, the tariff increases are highly controversial. Protectionist

US policies conflict with global efforts to reduce trade barriers, potentially harming the global economy and even US citizens. The German chancellor noted that 50% of Chinese EV exports came from western brands with factories in the country, meaning the tariffs disrupt EV producers globally, not just China. So far, the decrease in average tariffs from 10% to 3% in the last half century has helped increase global trade, which has promoted economies to flourish and global GDP per capita to triple.

In conclusion, the increase in US tariffs on Chinese imports is a strategy to encourage growth within the US economy, but it may spur harmful consequences on the global economy. In the last few decades, the world has observed the rapid growth of China and now, as one of the fastest growing economies, it goes head to head with the US, competing for global dominance. As the trade war continues, it leaves the rest of the world to ponder what it means for us. Will prices increase? Will our own economies suffer? Most importantly, will these tariffs do more harm than good?

By Jasleen

Millions of suffering families have been left in worsening situations as the cost of living continues to affect the UK, especially considering the recent spike in energy costs. There are serious concerns about the cost of living, with the rate of inflation still above the 2% target. There is, however, a ray of hope: a 7% decrease in energy costs is anticipated in July. The price of energy is at its lowest point since February 2022, when Russia invaded Ukraine. Still, expenses are roughly £400 more than they were three years ago and are much higher than prepandemic levels. Customers accrued an estimated £3 billion in debt to suppliers during the period of high prices.

How energy prices will change from July ?

There will be a cap on petrol prices of 5.48p per kWh and an energy price cap of 22.36p per kWh. An average household uses 11,500 kWh of gas and 2,700 kWh of electricity per year. Prepayment metre households will pay somewhat less, with an average bill of £1,522. With an average bill of £1,668, those who pay their bills every three months with cash or cheque would pay more. Though they differ by area, standing charges—fixed daily payments that cover the cost of connecting to a supply—remain constant at 31p for gas and 60p for electricity.

It is noteworthy that Northern Ireland has separate regulations on the energy sector; therefore, the Ofgem price ceiling does not apply there. Nonetheless, comparable patterns of declining energy costs are noted, providing consumers some respite there as well.

“The ugly” regarding the fall in energy price cap

The most recent forecasts from Cornwall Insight state that this is the last fall, and the rises that lie ahead are enormous, if they are correct.

It’s established that from July 1st, it reduces by 7%, meaning that for every £100 paid today, you pay £93. Then, on October 1st, a 12% increase is anticipated, meaning that you will have to pay £104 again.

Although the anticipated drop in energy costs is a good thing, long-term solutions for energy affordability must be worked towards while also addressing the underlying reasons of energy price instability.

The following tactics may be useful: Investing in Renewable Energy - By moving quickly towards renewable energy sources like hydropower, solar power, and wind power, we can lessen our dependence on fossil fuels and eventually achieve more stable energy pricing.

Energy Efficiency Initiatives -

Increasing the scope of initiatives that support energy efficiency can aid in lowering consumption overall. Implementing smart energy management systems, upgrading insulation, and acquiring energyefficient equipment are all practical approaches.

For households that are having difficulty paying for their high living expenses, the anticipated 7% drop in energy prices this July is encouraging news. Many households will see some respite in their monthly budgets because of the Ofgem price cap, which has caused energy costs to drop to their lowest point in two years. However, to guarantee energy affordability and stability going forward, it is imperative that sustainable and long-term solutions be pursued. We can create a more resilient energy landscape that is advantageous to everyone by making investments in energy efficiency, renewable energy, and consumer education.

By Anjalee & Jahnvi

AstraZeneca is a global, science-led, patient-focused pharmaceutical company. They are dedicated to transforming the future of healthcare by unlocking the power of what science can do for people, society and the planet. They are focused on creating genuinely innovative medicines and improving access to them. In this way, they deliver the greatest benefit to patients, healthcare systems and societies globally. Overall, AstraZeneca is recognized for its contributions to the healthcare sector, particularly in the development of innovative medications and vaccines.

AstraZeneca has seen a rise in their share prices by 12%.

AstraZeneca’s plan for growth:

Britain’s biggest pharmaceuticals group will set out its mediumterm growth plans on Tuesday in its biggest investor update since it successfully rebuffed a £69 billion takeover approach from a US rival a decade ago.

On 21st May, AstraZeneca declared its ambitious goal to increase their total revenue from $45.8 billion in 2023 to $80 billion by 2030. They aim to accomplish this by introducing 20 new medications by the end of the decade, in addition to significantly expanding its current portfolio in oncology, biopharmaceuticals, and rare diseases. In order to maintain steady growth after 2030, the company aims to fund innovative platforms and technologies to help revolutionise healthcare. Astraeneca will present its “roadmap” to 2030 at a highly anticipated investor day at the Discovery Centre, its new £1.1 billion global research and development headquarters in Cambridge. This “roadmap” will detail the key pipeline drugs and technologies behind the targets. The

FTSE 100 company has previously vowed to achieve an “industry leading growth rate” between 2025 and 2030.

Internally, the event for investors and analysts is considered the most significant since the company made bold targets during its defence to the takeover tilt by Pfizer in 2014. Shares in the company have rallied to fresh highs in recent trading sessions on the London Stock Exchange in anticipation of the event and amid expectations that it will set out a big 2030 revenue target. The shares closed at £121.10 on Friday, valuing the company at £188 billion.

The release of a series of new blockbuster medicines, particularly building a cutting-edge oncology franchise, led AstraZeneca to reach its sales target set in 2014 as it defended Pfizer’s politically contentious offer. It has recorded five consecutive years of growth and expanded to become the biggest multinational drugs company in China and built a rare diseases division through the $39 billion purchase of the Nasdaq-listed company Alexion in 2021, its largest ever acquisition. Analysts at Jefferies said this month, in a preview of the event to clients, that the focus would be AstraZeneca’s 2030 group revenue aim, with a consensus forecast of a 4% to 5% compound annual growth rate between 2026 and 2030 to $70 billion. It compares to revenue last year of $45.5 billion, excluding Covid drug sales, up 15%. “The key will be the underappreciated pipeline assets underpinning the vision,” Jefferies said. “We argue pipeline optionality remains perhaps best-inclass, but major new drug catalysts are somewhat scarce until 2025.”

Analysts at Bernstein said last month that it expected at least seven phase III late-stage clinical trial readouts by 2027, with cumulative peak sales potential of at least $25 billion, to “drive upside surprise”.

Britain’s largest pharmaceutical group has been expanding into markets such as China, Indonesia and India over the past few years in an effort to widen its supply chain. Enhertu, a breast cancer therapy that slows the spread of the disease, is made by its partner Daiichi Sankyo in Japan. Sir Pascal Soriot, AstraZeneca’s chief executive, said that the Cambridge-based company’s portfolio of cancer treatments, including ADCs, “have shown enormous potential to replace traditional chemotherapy for patients across many settings”. Moreover, AstraZeneca is planning to build a $1.5 billion manufacturing facility in Singapore as it looks to bolster this pipeline of next-generation cancer drugs. The plant will be the FTSE 100 group’s first end-to-end facility for so-called antibody-drug conjugates (ADCs - artificial antibodies that directly target cancer cells which are designed to reduce the toxicity of treatment.) and is scheduled to open in 2029. It has been backed by Singapore’s economic development board, although the company did not provide details on any possible incentives it would receive from the local government.

AstraZeneca announced a £650 million investment in its Uk operations in March, with the bulk of the money being spent at its vaccine manufacturing site in Speke, Liverpool. The decision marked a notable thawing after Soriot, 64, had previously blamed Britain’s uncompetitive tax policies for its decision to invest $360 million in a manufacturing facility in the Republic of Ireland instead of the UK. The Singapore announcement came before an investor day at its Discovery Centre research base in Cambridge, at which the group will present its “road map” for growth to 2030.

AstraZeneca and Sustainability: Sustainability has also become a key component of the company’s operations; they have confirmed that their goal is to “decouple” the company’s carbon emissions from its anticipated revenue growth. By 2030, it hopes to reduce emissions that are produced directly through their operations by 98%, as well as reducing emissions indirectly related to their production by 50%.

AstraZeneca has also proposed a $400 million reforestation plan to help the state erase its “residual emissions” from the environment starting in 2030. The company said it would aim for “sustained growth” beyond 2030 by investing in new technologies that “will shape the future of medicine”, including weight management treatments, where it believes it has the potential to eventually lead.

By Maryam & Aamena

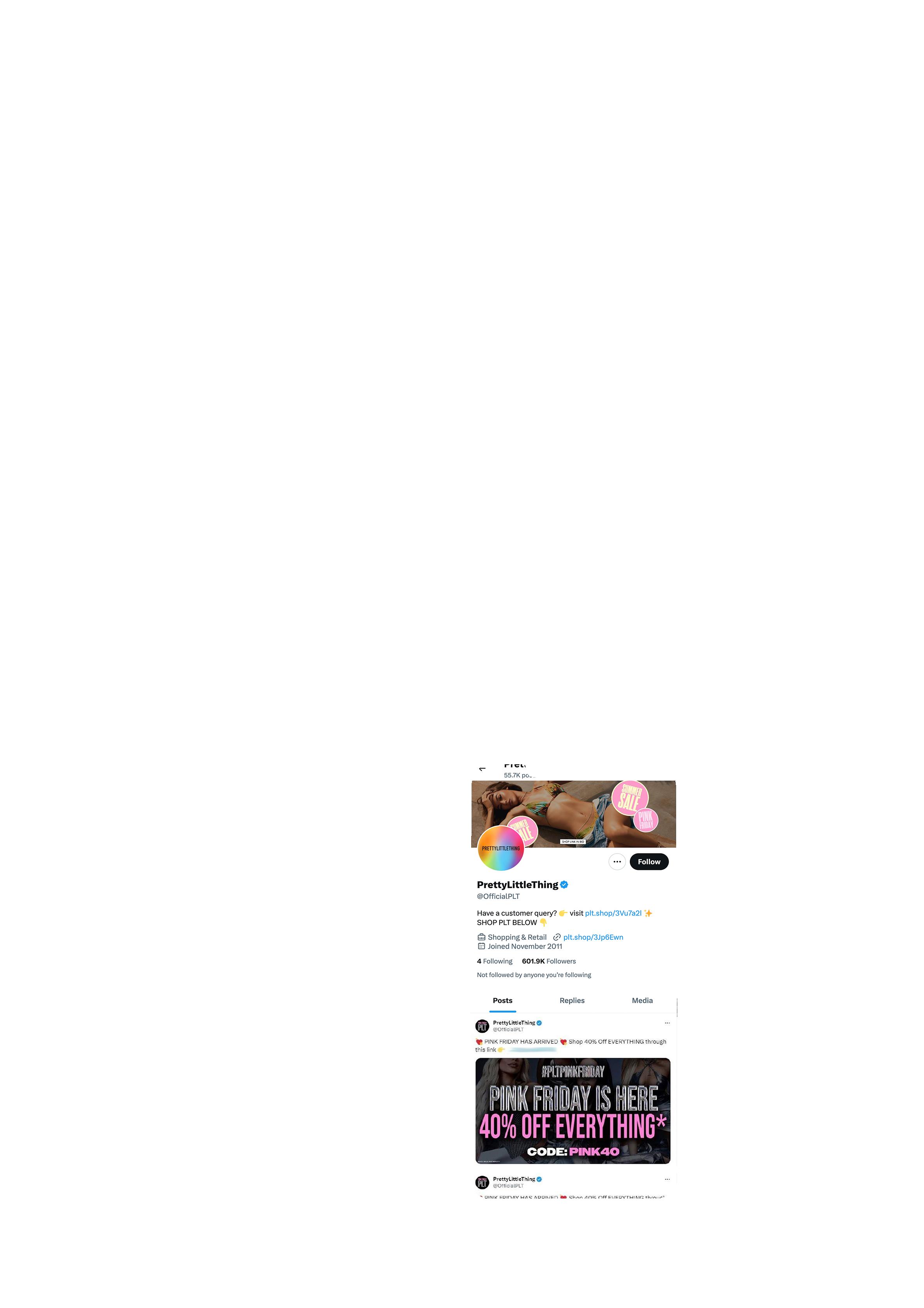

The fast-fashion brand

PrettyLittleThing [PLT] is currently under fire for breaching advertising policies after allegations of “misleading” advertisements were released during the Black Friday campaigns in November last year. The Advertising Standards Authority (ASA) found that the company released deceiving ads, making this the 8th time the retailers have hit headlines for false adverts.

The ASA has reportedly investigated 15 posts on formerly known Twitter, now X, which involved offers for shoppers, including discounts between 30% and 99%. The BBC reported these to have “varying deadlines or no deadlines at all and did not always specify if certain products were excluded from the promotions”. The Authorities have had 3 main problems with their guidelines. Firstly, adverts have ‘misleadingly implied the promotion applied to all products’ even though many have been excluded. Secondly, the ads have breached the code of conduct, where closing dates have

been ‘shortened or extended’. Lastly, ASA stated the advertisement implied further discounts would ‘not be available when the promotion ended’. Despite all allegations, PLT responded by saying their customers were “value oriented and their advertising and marketing was reflective of what their customers wanted and expected” in typical corporate jargon. They additionally mentioned how they “always tried to include significant conditions to promotions in ads, but

sometimes space was limited”. One example of this is by using an asterisk to add on information where possible.

PrettyLittleThing is an extremely popular brand, with its trendy and affordable fashion making their clothes accessible to all. They make use of their social media platforms to engage with customers and frequently collaborate with influencers in order to reach a larger crowd. Because of this, their breach of advertising policies is unlikely to damage their reputation or sales to a large extent; people pay for what they get and are usually happy to do so!

By Zoha & Hiba

Since the water industry was privatised more than 30 years ago, investors have withdrawn a staggering £85.2 billion from 10 water and sewage firms in England and Wales. However, rather than reinvesting this capital, these companies are planning to raise household bills to fund future spending.

Water companies are responsible for the supply, treatment, and distribution of water to residential, commercial, and industrial users. These firms play a crucial role in ensuring public health, supporting economic activities, and maintaining environmental sustainability. Historically, the water sector has been viewed as a safe investment, given the constant demand for water and the regulatory frameworks that often guarantee steady revenue streams. Companies have been under significant pressure due to the recent sewage spills and water leaks, which critics have blamed on the under-investment. Therefore, water and sewage firms want to increase customers’ bills by an average of 33% over the next five years to fund improvements to the service for households. A higher water bill will mean additional costs that can strain household budgets, with many already struggling due to the cost-ofliving crisis. There are several factors that

contribute to the mass withdrawal of capital. The recent shifts in policy, including scrutiny on pricing, service quality, and environmental standards, have created uncertainty, and investors are concerned about the potential changes that could impact their profitability. The increasing frequency and severity of climaterelated events, such as droughts and floods, pose a significant risk to water infrastructure. Companies are also required to heavily invest in infrastructure to increase quality of service and provide safe, drinkable water for their users. This can strain financial resources and deter investors from seeking stable returns. The recent advances in technology, including desalination, wastewater recycling and smart water management systems, require significant investment. While these innovations promise longterm benefits, the upfront costs and associated risks can influence investor confidence.

Withdrawing such a substantial amount of capital can lead to funding shortages, affecting the water companies’ ability to finance essential projects. This can delay infrastructure upgrades, maintenance, and expansion plans, potentially compromising service quality. Recently, Thames Water issued a warning to hundreds of

households in Surrey to not drink tap water due to ‘a possible deterioration in quality’. In Bramley, over 616 homes have been affected by the poor quality of the water. They have been advised not to consume tap water, following the recent water sampling results. Chancellor Jeremy Hunt has been in contact with Thames Water in order to monitor the situation. In a previous interview, he described Thames Water as having a “lousy service” in which Chris Weston, the CEO of Thames Water, responded by saying “it is business as usual for Thames Water.” As a result, Hunt requested for bottled water stations to be installed in Bramley, in order to prioritise the health and safety of the consumers.

Ofwat aims to put in place the 2024 price review (PR24) water regulation. It is a significant regulatory process in England and Wales and will be followed by all firms in the water sector. This is when water companies account for the outcomes that customers pay for and make sure that companies incentivise the interests of customers and the environment. Its focus is to deliver safe and reliable water and wastewater while benefiting the natural world. And its main aim is to make water affordable for customers, financeable for Thames Water as well as investable for equity investors.

By Anjalee & vidhi

Food price rises are returning to “more normal” rates, research suggests, although shoppers are still seeking out cheaper own-brand goods. Grocery price inflation - the rate at which prices increase - has fallen to 2.4%, according to research firm Kantar, the lowest since October 2021. The easing of price rises has raised expectations that the Bank of England will cut interest rates this summer. Fraser McKevitt, head of retail & consumer insight at Kantar, said: “Grocery price inflation is gradually returning to what we would consider more normal levels. It’s now sitting only 0.8 percentage points higher than the 10-year average of 1.6% between 2012 and 2021, which is just before prices began to climb. Typically, an inflation rate of around 3% is when we start to see marked changes in consumers’ behaviour, with shoppers trading down to cheaper items when the rate goes above this line and vice versa when the rate drops,” he added. On average, inflation peaked at 11.1% in late 2022, but increases in prices for food and non-alcoholic drinks were running at a rate of almost 20% last year - the highest since the 1970s. In response, the Bank of England increased interest rates in a bid to slow price rises. The theory is that if you make borrowing more expensive, people have less money to spend, or may choose to save more as saving rates go up. This in turn reduces demand for goods and helps cool inflation. The Bank’s key rate now stands at 5.25% - a 16-year high - but as inflation has fallen there has been intense speculation over when the rate will be cut.

Inflation is the sustained rise in the general price level over a period of time. There are two types of inflation: cost push inflation and demand-pull inflation. Cost push inflation is a rise in the price level due to an increase in the costs of production, while demand pull inflation refers to the rise in the general price level due to excessive increases in aggregate demand. One of the main aims of inflation is to measure the overall effects of price changes for a varied set of goods and services. It allows for a single value representation of the increase in the prices of goods and services in an economy over a period of time.

The prices are falling, meaning that with the same unit of money they can buy a greater number of goods and services, in this case food. This slow rise in investment impacts the cost of living, eventually leading to a rise in economic growth.

What have sales been looking like in the UK?

Ocado Retail was again the fastest growing grocer over the 12 weeks to May 12, with sales up by 12.4% to £613 million fr aom £546 million a year prior – well ahead of the total online market, which saw sales increase by 5.4%. The online-only grocer is a joint venture between Ocado Group PLC and Marks & Spencer Group PLC. Lidl reached a new record-high market share of 8.1%, fuelled in part by its bakery counters, as well as its loyalty scheme. Sales in the 12 weeks to May 12 rose 9.4% to £2.77 billion from £2.53 billion.

Sales at Britain’s biggest grocer Tesco PLC rose 5.6% in the 12 weeks to May 12 to £9.43 billion from £8.93 billion,

taking its market share to 27.6% - an increase of 0.5 percentage points since last year. It was Tesco’s largest annual share gain since January 2022. Its 5.6% growth in sales was matched by J Sainsbury PLC, whose market share nudged up 0.3 percentage points to 15.1%. Here, sales in the 12 weeks to May 12 reached £5.15 billion, up from £4.88 billion.

Asda, meanwhile, holds 13.1% of the grocery market, while Aldi and Morrisons captured 10.0% and 8.6% respectively.

Convenience specialist Co-op’s share of the market is now 5.4%.

Both Waitrose and Iceland held market share steady, with the former remaining flat at 4.6% and the latter at 2.3%.

Shares in Tesco were down 0.2% at 310.00 pence in London on Tuesday. Shares in J Sainsbury eased 0.6% to 283.00p. Shares in Ocado fell 0.9% to 351.10p.

What does this mean for the future?

As food prices fall to 2.4%, expectations have raised that the Bank of England will cut interest rates this summer. Food prices are still rising just at a slower rate. The inflation rate of 2.4% in April 2024 means prices have risen by 2.4% on average in comparison to what they were in April 2023. Prices are still increasing and will continue to do so as long as inflation is in the positive figures. Furthermore, world leading data and insight company, Kantar, have said that despite the easing of food price rises, shoppers were still following money-saving habits. Research states that consumers will continue to practise saving money

and to unwind the habits they have learnt to help them manage the costof-living crisis. Due to the previous cost of living crisis, sales of premium own-brand labels remain popular in 2024. Sales have increased by 9.9% from the preceding year.

Will a fall in food prices mean that interest rates will also be cut?

Recently, the Bank of England has given a strong hint that interest rates could be cut this summer. Usually, as inflation falls, eventually interest rates also fall. This is due to the fact that interest rates are a measure put into place by the Bank of England to help stabilise inflation levels and bring it back down to the target of 2%. The Bank deputy governor Ben Broadbent said in his recent speech that an interest rate cut at some time over the summer was “possible”. His comments were to come ahead of figures on Wednesday that were expected to show a sharp drop in inflation, which measures the rate at which prices are increasing.

Overall, in the wider economy,

inflation continued to slow, however it was not as fast as market analysts predicted. The CPI inflation slowed to 2.4% in April, down from 3.2% the previous month, above expectations of 2.1%. The main driver behind this steep fall was the reduction in the regulatory cap on household energy prices, although food and non-alcoholic drink inflation also contributed to lower CPI inflation. Core inflation, a better measure of underlying inflation as it excludes more volatile items such as food and energy, slowed to 3.9%, down from 4.2% down in March, and above expectations of 3.6%. While service inflation, another indicator thought to be a better measure of domestic price pressures, inched down to 5.9% from 6.0% in March.

To conclude, there is hope that a downward move in the UK’s CPI inflation will encourage members of the Bank of England’s monetary policy committee to vote for a cut in interest rates at its next meeting on the 20th of June. There is also an aim that the UK’s food prices will continue to fall in order to help support the reduction in the cost-ofliving crisis.

By Yumna & Minnah

As summer approaches, many economists are speculating a possibility of an interest rate cut by the Bank of England, from 5.25% to 5%. There are many economic indicators suggesting the potential cut, including slowing inflation and economic growth concerns. A rate cut could provide the necessary stimulation of economic activity. Interest rate cuts are likely to be considered in June and August, depending on how the economy performs and the fall in inflation.

Governor Ben Broadbent said in a speech that a rate cut at “some time” over the summer was “possible.”

Recent communications with the Monetary Policy Committee indicate that they are prepared to act to support the economy, with their main aims being to maintain price stability and support economic growth. However, due to the upcoming elections, the Bank of England may choose to avoid changing the base rate around the time of an election. But, since the March meeting, one more member of the 9-strong committee had voted for a cut, further increasing the possibility of rates being cut in the coming months. Lower interest rates would reduce borrowing costs for consumers, potentially leading to increased spending on goods and services - consumer demand could drive economic growth. Long term economic growth and productivity will be improved through the encouragement of business investment in expansion, innovation, and employing workers.

The current interest rate figure is 5.25% in May 2024. This will possibly change in the summer as the Governor of the Bank, Andrew Bailey, said the Bank expected inflation, which measures the rate prices rise at, would fall “close” to its target level in the next couple of months. Most analysts expect that the first-rate cuts may occur in the second half of 2024, potentially starting in August . However, these cuts are likely to be gradual, with rates anticipated to fall to around 5% (drop by 25 basis points) by the end of 2024 and possibly lower in the next few years as inflation pressures ease to 3%.

By preesha

To conclude, the possibility of a cut in interest rates in the summer is very high as a result of the decrease in inflation over the last few months and economic growth concerns.

The current inflation rate in the UK is 2.3% (in April 2024). This figure is within the UK’s target range (2%, +/-1%). Additionally, there is a general decrease between October 2022 to now, from 9.6% to 3%. Due to the low inflation, it would only make sense to lower the interest rates to help stimulate spending and investment as the cost of goods and services is lower. When inflation is low, the Bank of England would also need to lower interest rates in the summer to stimulate the economy. A cut in interest rates would encourage borrowing, as it would become cheaper for consumers and businesses to do so. This could lead to an increase in spending on goods, services and investments. Moreover, low interest rates would increase consumer spending, since if consumers had cheaper loans and higher disposable incomes, this would increase the marginal propensity to consume and therefore increase consumption.

In addition, fixed mortgage rates fell sharply at the beginning of the year; financial markets forecast that the Bank could cut rates several times in 2024 which will then stimulate the housing market, benefiting both homebuyers and the construction industry. Financial markets will also benefit from lower interest rates as their liquidity will increase and the financing costs for companies will decrease.

Also, Andrew Bailey stated there is a possibility of interest rates falling due to the prediction that inflation would be “close” to its target. In addition, the Bank’s Deputy Governor, Ben Broadbent, mentioned that a rate cut at “some time” over the summer was “possible”. Taking in all these factors, it would lead us to the conclusion that interest rates will most likely be falling in the next few months in the summer, as it will benefit consumers, firms and the economy.

Mastercard and Visa are payment networks which allow the electronic transfer of payments between banks or other financial institutions and companies. They provide branded payment transfers for all types of card payments; credit, debit and even prepaid cards that banks or other financial institutions provide for their customers. Mastercard is widely applied in over 210 countries and locations spanning globally today, and still growing in popularity as the e-world continues to expand, with 4.2billion Visa cards being used worldwide. At the moment, Visa’s growth is currently standing at $497.5 billion, with Mastercard closely behind it with $359.8 billion market capitalisation. There is no considerable difference between the two card companies; however, Mastercard does offer luxury offers on World and World elite levels, which can be deemed to be much more attractive for big investors and big spenders. This high similarity between the two card companies also means that if one bank only lends Visa debit and credit cards and a Mastercard is wanted, another bank would have to be visited that issues Mastercard debit and credit cards. Mastercard and Visa are two of the biggest and most popular card schemes in the UK, accounting for at least 95% of their UK-issued transactions, that do not face effective competition. Over the past couple of years, Visa and Mastercard have increased their schemes and processing by almost

30%, and the popular opinion has spiralled that with the increases in fees, there is ‘little evidence that the quality of service has improved at the same rate’. As a result, the UK regulators have introduced policies to monitor and ensure that these card companies are more transparent and straightforward with their consumers on price hikes, fully justifying the reasons for any fluctuations in prices. A report published by the Payments System Regulator (PSR) has reported the calculation made by Chris Owen (policy adviser at the British Retail Consortium) that these increases in fees have cost UK businesses an astonishing £250 million. Visa and Mastercard both have requirements for their customers to pay costs to access their networks, for authentication, clearing, and settlement of payments. Tina McKenzie from the Federation of Small Businesses has reflected on the burden placed on small businesses as they end up paying as a result of card fees ‘taking out a bite of almost every sale and adding to the financial pressures they face’.

The PSR’s managing director, Chris Hemsley, has reviewed the two card companies and reported that they both have held information about their processing fees in a way that is ‘not easily accessible’ and have made agreements with banks to win contracts as an incentive to try and raise retail prices, which only end up placing a burden on consumers as they pay these higher prices.

In response to this, both Mastercard and Visa have reported back with their consultations and views on the matter. A statement published by Mastercard has disagreed with the policies being introduced and the criticisms they have been receiving, arguing that the UK payments industry has been more competitive than ever before with a broad range of payment options available to British businesses and consumers, therefore, an increase in payment fees is a necessary response in order to maintain their high reputation in the market. Furthermore, the Visa company has sent out a report to account for these condemnations, saying that their levies reflect the ‘immense value that we provide to financial institutions, merchants, and consumers, including extremely high levels of security and near-perfect operational resilience’. They both collectively argue that their prices always reflect constant upgrades in their security checks and services, where they have invested in hightech cyber security and network resilience.

In summary, this new policy will hopefully control the price changes by Visa and Mastercard and result in more thought and reasoning for any increases in fees. This will lessen the burden applied to businesses and consumers and lead to increased spending and investing, as the cost of this wouldn’t be as extortionate.

If the card companies fail to do this, they would risk losing some of their customers to cheaper and more predictable alternatives.

By Luiza & Kitty

Many of us experienced the disastrous effects of COVID-19 throughout 2020/21 across the globe; grief, self-isolation and fear overwhelmed us all. Although the majority have been able to return to their normal lives, copious numbers of families around the world and their economies are still suffering from its effects.

How did COVID-19 affect us during its peak?

Before we delve into the long-term impacts of COVID-19 it is critical to understand how the impacts the pandemic has had on people’s mental health since it began. 23rd March 2020, Boris Johnson announced the compulsory self-isolation rule. Subsequently, children were out of school, students out of university, adults out of work. Socialising and face-to-face interaction came to a halt, affecting both physical and mental wellbeing - approximately 15 million people died across the globe, bringing about immense grief and suffering to families and friends.

How did COVID-19 affect us post peak?

COVID-19 has left a scar on the world. Approximately 10% of people who test positive for the virus experienced long-term health effects, lasting for over 12 weeks post infection (this includes physical, neuropsychological and mental health related symptoms). Alongside this, there are also indirect effects on wellbeing rooting from the unemployment, trauma and stress that many fought against. Despite its focus in the media dying out, its influence can still be seen in current day-to-day life.

Impact on students

COVID-19 had a drastic effect on our young adults. A prime example of this can be seen in the GCSE & A-Level students of 2020 who were left to rely on their predicted grades for their final results, many of which were inaccurate. Those who achieved lower results in their mock exams faced poorer predicted grades, which were not necessarily an exact representation of their

formula sheets and advanced information in order to provide a farrier advantage for all students – but is this really enough? Online school had a substantial impact on students’ understanding and retention of crucial content needed for their exams, which potentially can only be redeemed through relearning the content. Struggling to learn and understand content predominantly by themselves further affected students’ motivation and attitudes towards exams, often making them complacent and careless towards them. In addition, self-isolation had a detrimental effect on their mental health and ability to socialise, feeling alone, depressed, anti-social. Children in nursery and primary school missed out on a vital phase in their development and growth, from learning how to interact with peers and teachers, to learning key concepts about day-to-day society. This hindered growth may have regressive effects for the classes of 2020, especially when entering secondary school.

train, which is crucial to succeeding in their career from the respective apprenticeships. The rise in apprenticeships have contributed greatly to our current economy and towards providing highly skilled workers with this experience, so this was a significant loss.

Lastly, high levels of government spending were necessary in order to compensate for the disastrous COVID-19 effects. For instance, Rishi Sunak introduced the Furlough

potential in the real, final exams. This had impacted their chances of being accepted into their aspired sixth forms, colleges etc. as this ultimately eliminated a chance to redeem themselves in the final exams they had prepared for. This has led to a domino effect, therefore damaging the mental health and self esteem of the students impacted. A-Level students of the class of 2023 suffered with higher grade boundaries as a method to fairly distribute grades post high predicted grades. Although some may argue this was effective, it was at the expense of students’ wellbeing; many either did not meet their universities’ criteria’s and had to resort to back up options. Secondary schools are currently playing catch-up. Students were forced to adapt to online learning, which affected students’ academic growth due to the limited communication with teachers and peers, as well as a lack of motivation. As a result, they have tried to compensate through providing

University students were also victims of the pandemic in similar ways to those in secondary schools. However, they were further deprived of the opportunity of a university life, where the vital connections and friendships formed are essential for a smooth transition into university. The COVID pandemic was a heavy burden on those taking on apprenticeships, where they were not able to experience being in a professional workplace where they

Scheme in March 2020, which lasted roughly 18 months. This was alongside the Eat Out To Help Out Scheme established in July of 2020. These schemes allowed those who were cyclically unemployed to keep

an earning, together with making food more affordable by not cutting into such a large proportion of their disposable income. Unfortunately for the government, as productivity fell to 15.2% in 2020, providing these schemes had an astonishing effect on their borrowing, especially given that tax revenue had fallen due to the extreme rates of unemployment. Overall, this significantly worsened the UK’s National Debt, making it harder to recover from the pandemic and returning to high levels of government spending in order to provide for our society. As a result, future generations may be burdened with higher taxes.

Conclusion

In conclusion, the COVID-19 pandemic caused students to miss out on vital exam content, vital lessons for society, and vital training for their future careers in the economy, which further had detrimental effects on their mental health and ability to socialise. Families heavily suffered from unemployment and loss, additionally creating a burden on the government’s spending and debt due to extremely low productivity in the UK’s economy. Nevertheless, our current economy, education and wellbeing has generally seemed to recover. More so, a positive impact of the pandemic is the source of inspiration for innovation, involving advances in technology, and entrepreneurship it generated, benefiting our current and future economy.

By vida

What is globalisation?

Globalisation refers to the increasing integration and interdependence of national economies in terms of trade, financial flows, ideas, information, and technology.

The OECD (Organisation for Economic Co-operation and Development) defines globalisation as the ‘geographic dispersion of industrial and service activities, for example research and development, sourcing of inputs, production and distribution, and the cross-border networking of companies, for example, through joint ventures and the sharing of assets.’

Globalisation is often associated with transnational corporations (TNC’s) that sell products almost everywhere in the world. For example, Coca-Cola and McDonald’s.

What are the causes of globalisation? With analysis and application!

1. Improvements in communications, technology, and IT – Computers, the internet, e-mail, mobile phones, and satellites have radically changed global communication. e.g. Facebook has over one billion members.

‘This is good because there is’…

• A positive impact on trade and living standards in LEDCs – e.g. mobile banking.

• Better communication allows markets to work better through symmetric information.

• An increase in productivity through technical economies of scale.

• Provisions for outsourcing. (call centres in India - specialisation and division of labour).

‘However...’

• The growth in e-commerce relies on improvements in transport (exporting and importing).

• To what extent will trade take place online rather than face-to-face in future?

• It may still be difficult to manage TNC’s and technology can have technical problems, which could limit trade.

2. Free Market Ideology – it’s a philosophy that emphasises free trade, deregulation, and a reduction in government spending. For example, the collapse of communism in Eastern Europe (1989) and Soviet Union (Russia) (1991).

‘This is good because there is’ …

• Increased global specialisation and division of labour = higher global output

• Increased foreign direct investment which can lead to job creation, tech advancements, and economic development.

• Efficient allocation of resources because capital can flow where it’s most needed or where it can earn the highest return.

• Less government spending (opportunity costs decrease)

• Investment opportunities increase due to firms being able to invest in the most promising markets regardless of location.

‘However...’

• Without capital mobility, the full potential of globalisation cannot be realised. (This also comes with the understanding that capital mobility itself can lead to big economic and social costs. For instance, a sudden withdrawal of capital can cause financial crises in countries.)

4. Growth of Trading Blocs –trading blocs have no barriers to trade between them but have protectionist measures (such as tariffs) on imports from countries outside the bloc. Examples include the EU and NAFTA.

‘This is good because there is’…

• It should mean more exports, imports, and trade due to lower trade barriers.

• It leads to an increase in inequality and exploitation.

• There are many regulatory challenges and without proper regulation and taxation of capital flows, potential issues like tax evasion and regulatory arbitrage can occur.

3. Trade liberalisation – reducing trade barriers. Over the last 50 years WTO members have negotiated large reductions in barriers to international trade (e.g. tariffs and quotas).

‘This is good because there is’…

• An increase in world trade. (19902012: Exports of goods & services rose from 20% to 31% of world output)

• An increase in specialisation and division of labour = higher global output.

‘However...’

• There is an impact on ‘BoP’ –including global imbalances (large trade deficits/large trade surpluses)

• Countries may be less reluctant on reducing trade barriers as they look to protect domestic jobs and growth. (But many did not use protectionist measures after the financial crisis of 2007)

• Trade talks (e.g. Doha) have broken down on several occasions due to disputes between countries in the negotiations.

• Aids globalisation in the long-term if agreements occur between major trading blocs. (It can increase the size of blocs.)

‘However...’

• They may reduce trade between member and non-member countries due to protectionist measures.

• It would create increased interdependence on economic performance in other countries in the trading block. (If the EU goes into recession, it will affect all countries in the EU.) BUT this is almost inevitable due to close relationships between trade cycles.

• Loss of sovereignty and independence. A trading bloc needs to make decisions for the whole area. This may go counter to the wishes of a country.

5. Cheaper transport costs - Air freight and containerisation have become cheaper in real terms since the 1980s. This is partly due to economies of scale due to increased dimensions gained through “containerisation” – e.g. many container ships are 350m long and can take more than 15,000 containers.

‘This is good because there is’…

• Cheaper transport costs which increase world trade.

• Impact on balance of payments.

• Reduced costs of imports which reduces cost-push inflation.

‘However...’

• The cost of transport is very dependent on oil prices, which have risen several times in recent years, and it is heavily taxed for environmental reasons.

• Will transport become more expensive as non-renewable resources become scarce and environmental concern increases or, will renewable energy allow globalisation to continue?

6. The growth of Transnational/ Multinational companies - A TNC/MNC is a firm which produces and operates in more than one country. However, a TNC does not have a centralised management system (no central headquarter in one country that makes all the decisions, while an MNC does have a centralised management system.

‘This is good because there is’…

• Increased specialisation and division of labour = higher global output (TNCs often locate their high-value marketing and R&D operations in developed economies and their low-value manufacturing operations in LEDCs)

• Greater capital mobility which allows outsourcing or offshore to reduce costs and process financial transactions on a global scale.

• Better communication has allowed better efficiency.

• Lower cost of production will attract firms to certain countries globally and will improve profits.

‘However...’

• Can lead to exploitation of workers such as adverse conditions or low wages (Rana Plaza garment factory in Bangladesh collapsed in April 2013, killing more than 1,100 workers, and injuring 2,500 others).

• Eventual backlash if they continue to avoid paying tax, contribute to environmental damage and are accused of exploiting labour.

• But, without transnational companies there would be no interdependence between countries as each firm would just produce inside their own borders.

Benefits of globalisation

• Facilitates deeper division of labour and economies of scale for producers and consumers.

• Competitive markets drive innovation and reduce monopoly profits.

• Higher growth leads to increased per capita incomes and poverty reduction.

• Benefits from the free movement of labour between countries.

• Dynamic efficiency gains from sharing ideas, skills, and technologies globally.

• Access to capital markets helps bridge domestic savings gaps in developing countries.

• Increased global awareness of climate change and income inequality challenges.

• Competitive pressures prompt improved governance and labour protection standards.

Costs of globalisation

• Rising inequality and relative poverty fuel political and social tensions.

• Threats to the Global Commons include irreversible damage to ecosystems and water shortages.

• Interconnected world economies face macroeconomic fragility and volatile capital movements.

• Increasing trade imbalances lead to protectionist tensions and managed exchange rates.

• Shifts in production result in higher structural unemployment in certain countries.

• Dominant global brands may overshadow local producers.

• Some global multinationals engage in exploitative practices, tax avoidance, and neglect environmental issues.

Factors Contributing to Globalisation in the Past 50 Years

• Advances in Information Technology: Internet, mobile phones, and global communication networks.

• Trade Agreements: NAFTA, EU, ASEAN, and other regional trade agreements.

• Global Financial Systems: Integration of financial markets and global capital flows.

• Transportation Advancements: Containerisation, and organisation improvements.

• Economic Policy Shifts: Liberalisation policies in China, India, and former Soviet bloc countries.

2 tins of 400g chick pea tins (drained and rinsed)

2 tablespoons of sunflower oil

3-4 garlic cloves (crushed)

1 large white onion (finely chopped)

1 green chilli (finely chopped) or 1 frozen green chilli cube

2 inches fresh ginger or 3 frozen ginger cubes

1 tin of 400g chopped tomatoes

1 teaspoon of salt (or more dependent on taste)

½ teaspoon of turmeric

1 teaspoon of Kashmiri red chilli powder

1 teaspoon of garam masala

2 teaspoon of ground coriander

1 teaspoon of ground cumin

Fresh coriander (chopped finely)

1. Heat a large pan and pour the sunflower oil. When the oil turns slightly hot, add the onions, and sauté until they turn light golden.

2. Add the ginger and garlic and sauté for a minute or two without burning.

3. Stir in the red chilli powder, turmeric, garam masala, coriander powder and cumin powder. Sauté until the masalas begin to smell good, a minute or two.

4. Add in the chopped tomatoes. Let it simmer/cook until it turns into a thick sauce like consistency.

5. Whilst the tomatoes are cooking add in the green chilli.

6. Add the chick peas in, along with a cup of water. Also, add your salt at this point too.

7. Cover the pan and simmer for 10-15 minutes.

8. Stir in fresh coriander leaves

9. Serve with either rice, naan or roti